Abstract

This article shows that an orientation towards shareholder value and corporate indebtedness at non-financial firms have been negatively associated with union density in the EU over the past 21 years. We argue that the financialisation of non-financial firms makes them prioritise their ‘external (economic) balance’ at the expense of a cooperative ‘internal equilibrium’ model. In other words, corporate financialisation pushes non-financial firms to shift to non-participatory, market-based HR systems that directly undermine the role of trade unions. This study examines this corporate financialisation-induced shift within the EU in the wake of deeper economic integration since 1999 and provides panel data econometric evidence that it has significantly undermined union membership.

Introduction

This article shows that corporate financialisation and an orientation towards shareholder value have contributed to the steady decline of union density in the European Union (EU) since the beginning of the latest phase of EU integration. While a shareholder-value orientation has been a key feature of Anglophone capitalism since the late 1970s, policies implemented across EU Member States as part of European integration over the past 20 years include the ‘harmonised liberalisation’ of stock markets and the protection of shareholders’ rights. Accordingly, some convergence towards the capitalist liberal market economy model has occurred across EU countries since 1999. One of the main implications of the financialisation of non-financial corporations within the EU has been its impact on working conditions and trade unions.

In order to better understand the corporate financialisation-union membership nexus it is worth revisiting the seminal work of Roethlisberger and Dickson (1939), which distinguishes between the two interconnected functions of the firm. On the one hand, there is the economic function or ‘external balance’, which is related to efficiency in terms of production (Organ, 1986: 462); on the other, there is the ‘human’ element that is linked to maintaining an ‘internal equilibrium’ which corresponds to the HR conditions of the work environment (Organ, 1986). Firms’ options and decisions on how to strike a balance between the two depend crucially on their political and economic environment. The more difficult it becomes for a firm to maintain its ‘external (economic) balance’, the more likely it is that it will shift from a cooperative to a disciplinary ‘internal equilibrium’ approach. The prioritisation of short-term profitability as a means of maintaining ‘external balance’ often leads to a change in stance, with workers coming to be treated as ‘resources’ rather than stakeholders (Taskin and Ndayambaje, 2018).

A fast-growing literature within industrial relations, human resource management, and the sociology of work argues that financialisation – in the sense of non-financial actors’ increasing dependence on financial markets, institutions and instruments – has contributed to the decline of workers’ bargaining power and deterioration of their working conditions (for example, see Gouzoulis, 2021, 2022, 2023; Gouzoulis et al., 2023; Hanlon and Harney, 2021). The ‘disconnected capitalism’ thesis, following a comparable distinction made by Roethlisberger and Dickson (1939), argues that financialisation increases the importance of the ‘external balance’ for non-financial corporations (Cushen and Thompson, 2016; Thompson, 2003, 2013). The main premise of the framework provided by the ‘disconnected capitalism’ thesis is that the increasing dependence of non-financial corporations on financial instruments and shareholders compels them to focus primarily on financial performance and meeting obligations to private financial institutions rather than value creation as such. This, in turn, impels them to pass the costs of preserving their ‘external (financial) balance’ onto the weakest stakeholder, namely workers. In this context, a shareholder value orientation is found to be a key negative driver against unionisation across advanced economies either by directly undermining unions or by making them less influential and thus less attractive to workers (Dupuis et al., 2020; Kollmeyer and Peters, 2019; Peters, 2011). This article elaborates on how the financialisation-induced disconnection between firms’ ‘economic’ function and their ‘internal equilibrium’ has undermined union membership in the EU since 1999.

The rest of the article is structured as follows. Section 2 reviews the literature on the drivers of unionisation. Here we highlight that, even though the EU represents a unique instance of financial integration and deregulation, the literature has not yet examined how specific measures related to the shareholder value orientation have affected union density. Section 3 provides an overview of the rise of shareholder value in Europe over the past 20 years and how this is related to the decline of unionisation. Section 4 presents the econometric design, and Section 5 the key findings that show that a shareholder value orientation and non-financial corporation debt are strongly associated with the decline in union density in the EU since 1999. Section 6 concludes and discusses the implications of our findings.

Drivers of union density: key hypotheses and evidence

The steady fall in union membership rates since at least the early 1980s has been a key area of research within industrial relations, the sociology of work and labour economics over the past 25 years. Government ideology and labour market institutions are historically important drivers of union density. A government’s ideological orientation is strongly associated with changes in union membership because labour market regulation and changes in wage-setting institutions implemented by governments affect whether the unions are to play a central role or be marginalised. This in turn affects workers’ motivation to join a union or not (Gumbrell-McCormick and Hyman, 2013; Masters and Delaney, 2005; Rigby and García Calavia, 2018). In labour market regimes characterised by stricter regulation, unions typically hold greater sway in shaping wage determination and negotiating working conditions (Brady, 2007; Korpi, 1983; Sassoon, 1996; Trentini, 2022; Western, 1995, 1997). In such contexts, employees are more likely to join unions and reap the tangible advantages that come with membership. 1

The relevant literature also shows that another crucial factor in the steep decline in unionisation rates has been de-industrialisation. Because of this structural shift a large portion of the workforce has shifted from highly unionised manufacturing/industrial sectors to low union density occupations in services and even (sometimes bogus) self-employment (Blaschke, 2000; Jensen, 2020; Polachek, 2004; Schnabel, 2013). In addition, fiscal adjustment programmes implemented across advanced and developed economies include job cuts in the public sector, which traditionally is a high union density sector (Checchi and Visser, 2005; Schnabel, 2003; Visser, 2002).

In addition to the cross-sectoral movement of employees, consumer price inflation is another well-established positive driver of unionisation that operates across sectors. Higher living costs incentivise workers to join unions to help them improve their incomes and protect their purchasing power against inflationary pressures (Bain and Elsheikh, 1976; Checchi and Visser, 2005; Western, 1997).

Union participation is also significantly influenced by external constraints related to the globalisation of trade and production networks (Bluestone and Harrison, 1982; Harrison and Bluestone, 1988). The deregulation (‘liberalisation’) of capital flows that has been escalating since the early 1980s allows employers to easily relocate production to regions with less or unregulated labour markets, where labour costs are comparatively lower in the absence of (strong) unions (Sassoon, 1996; Wallace and Brady, 2001). Segmentation of production can also undermine unionisation as coordination challenges between local unions and foreign employers diminish unions’ effectiveness by blurring responsibility in cases of labour rights violations (Western, 1997). Workers in sectors that are central to a particular value chain have more disruptive power, however, and their unions are therefore often more effective, obtaining better working conditions (Iliopoulos et al., 2023). Econometric studies indeed show that openness to trade, foreign direct investment, and import penetration have reduced labour’s organisational capacity and unionisation rates in both the United States and the United Kingdom (Boulhol et al., 2011; Brady and Wallace, 2000; Slaughter, 2007).

More recently, the literature on the drivers of union membership has enhanced its focus on how financialisation might also negatively impact unionisation. Broadly speaking, financialisation refers to the increasing dependence of the non-financial parts of the economy and society on financial markets, institutions and instruments. 2 The main implication of this process has been that non-financial corporations have become increasingly short-termist, prioritising the maximisation of shareholder value over real, long-term investments (Froud et al., 2000; Lazonick and O’Sullivan, 2000). Common practice among non-financial corporations is to maximise dividend payments to shareholders through share buy-backs financed by corporate loans. The consequent deterioration of firms’ financial standing as a result of increased interest and dividend payments has been linked to reduced investment, downsizing and the adoption of more ‘flexible’ workforce arrangements as ways of improving the appearance of balance sheets through lower labour costs (for example, Appelbaum and Batt, 2014; Appelbaum et al., 2013; Gospel and Pendleton, 2003; Gouzoulis et al., 2023).

The financialisation of corporate governance has been highlighted as one of the main drivers of the decline in commitment-based HR systems and the rise of market-based HR practices (Thompson, 2003, 2013). 3 Market-based HR systems are generally oriented towards managing human resources without the participation or cooperation of the workers themselves. As depicted in some of the most widely used HR management textbooks, the fundamental stance of market-based HR practices is that workers are ‘resources’ rather than stakeholders (Taskin and Ndayambaje, 2018). While market-based HR systems were primarily observed in advanced liberal market economies such as the United States and the United Kingdom, over the past two decades such practices have spread widely within Europe.

Linking the literature on the financialisation of non-financial corporations’ corporate governance with the union density literature, Kollmeyer and Peters (2019) argue that increased financial commitments on the part of non-financial corporations may lead to lay-offs of unionised employees to reduce labour costs and avoid paying union wage premiums. Consequently, in such hostile cost-benefit-dominated environments, workers have an incentive to refrain from joining or to leave a union to mitigate the risk of redundancy, even if that comes with some loss of income. In this respect, financialised non-financial corporations tend to adopt an imposed (rather than cooperative) ‘internal equilibrium’ to maintain or improve their ‘external (financial) balance’. In general, non-financial corporations can become financialised by either increasing their corporate debt ratios (either to fund share buy-backs or invest) or by becoming listed on the stock market and thus focused on maximising shareholder returns. The following two hypotheses are derived from this:

A number of econometric studies have demonstrated that the growth of the so-called FIRE sector 4 (Finance, insurance, and real estate) relative to the real economy, employment in financial intermediation and the FIRE sector, as well as corporate debt, financial openness, and stock market price fluctuations are strongly associated with the decline of unionisation rates and union power in a wide range of advanced economies over the past five decades (Darcillon, 2015; Dupuis et al., 2020; Kollmeyer and Peters, 2019; Meyer, 2019; Mohamed and Darcillon, 2023; Peters, 2011). In a study that is more focused on financialisation in EU countries, Vachon et al. (2016) show that financialisation measured in terms of employment in the FIRE sector has contributed to the reduction in union density in the EU since 1981, given that workers in finance and insurance are rarely unionised.

Union membership and the financialisation of EU corporate governance

A shareholder value orientation and market-based HR practices have been largely associated with advanced liberal market economies such as the United States and the United Kingdom. This is no longer the case, however. Since the beginning of the last phase of European integration, most EU economies have been converging towards an increasingly shareholder value-oriented model of capitalism (Almond et al., 2003). Historically, the EU’s strategy has been to integrate, expand and liberalise the financial and labour markets of its Member States, and to maintain exchange rate stability as a means of improving its international price competitiveness and export performance. While various measures have been implemented since the establishment of the European Coal and Steel Community in the 1950s, it is the January 1999 Exchange Rate Mechanism (ERM II) agreement that marked the start of a deeper integration phase and regulatory harmonisation.

One of the primary goals of EU integration over the years has been to harmonise corporate governance. The 1999 Financial Services Action Plan (FSAP) stated explicitly that the convergence of corporate governance models across Member States is an essential step towards creating – eventually – a unified financial market within the EU (European Commission, 1999). Four years later, the Plan on Modernising Company Law and Enhancing Corporate Governance in the European Union made the direction of the EU’s plan clearer and clarified that this market-oriented convergence of corporate governance models can be achieved primarily by increasing the protection of shareholder rights (European Commission, 2003). While initial plans were based on an understanding that national differences do exist and comparative advantages are important, ultimately EU directives rather aimed to force convergence towards the Anglophone model of capitalism with its shareholder primacy (Höpner and Schäfer, 2010). Full convergence has not been achieved because of the distinct and persistent nature of domestic institutions within EU countries (Clift, 2009), but most of them have become significantly more liberal in terms of financial regulation and corporate governance. Naturally, these processes have empowered shareholders of European non-financial corporations and have made corporate strategies directly aimed at maximising returns to shareholders, such as share buy-backs, more common (Andriosopoulos and Hoque, 2013; Ang, 2023).

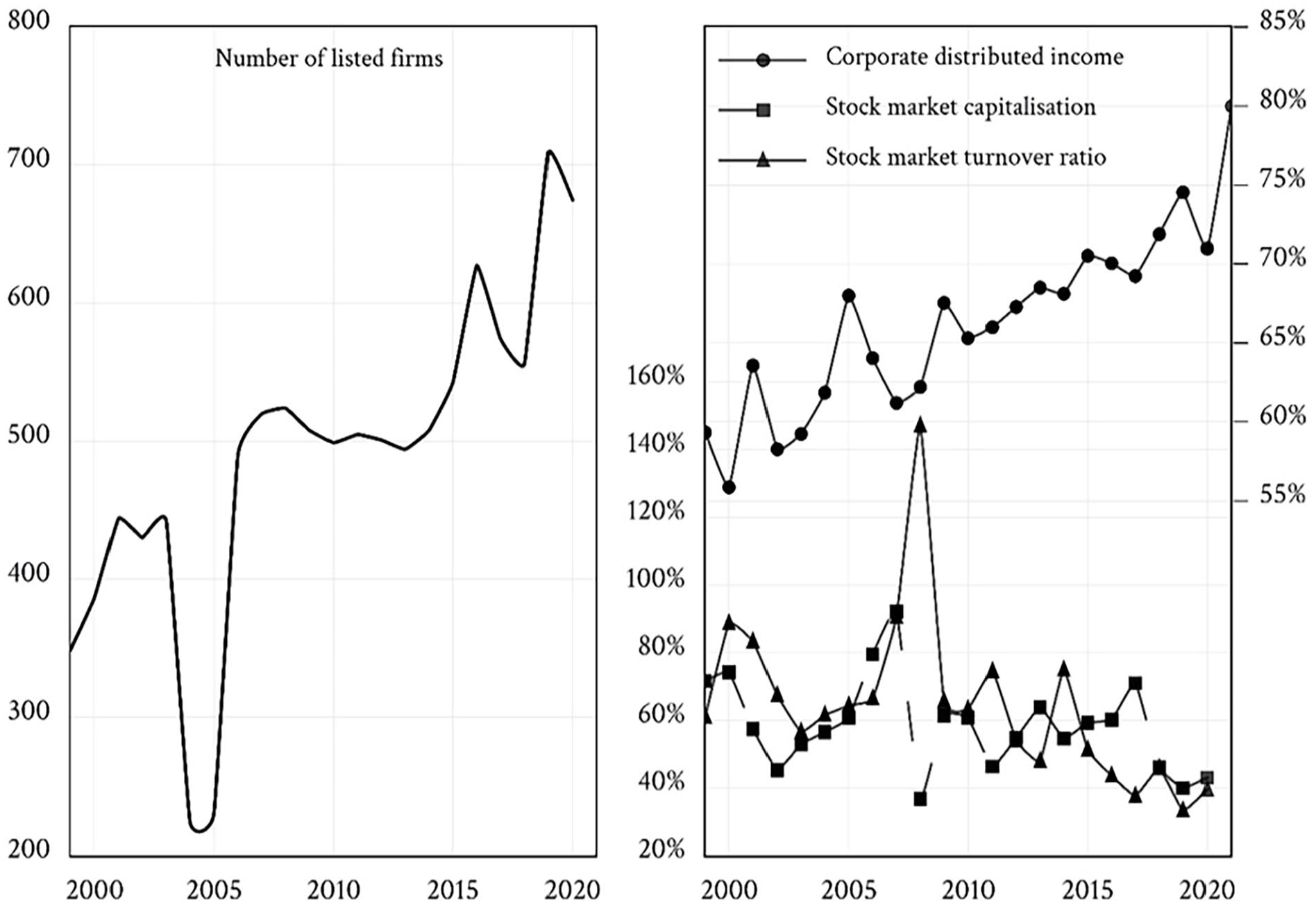

Figure 1 presents different measures of shareholder value orientation for a sample of 15 highly integrated EU countries over the latest phase of deeper EU integration. We use four different indicators for shareholder value orientation. Two of them capture the expansion of shareholder primacy (number of listed firms and corporate distributed income) and two the overall volatility of stock markets (stock market capitalisation and stock turnover ratio). Based on data availability, these include Austria, Belgium, Czechia, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Poland, Portugal, Spain and Sweden, and cover the period from 1999 to 2021. Although Czechia, Denmark, Poland and Sweden have not yet adopted the euro, they are all part of the ERM II agreement. Focusing on the left panel, the average number of domestic firms listed on the stock market rose rapidly from 349 in 1999 to 709 in 2019. This suggests that the growth of financial markets in the context of EU integration made a larger number of firms dependent on shareholders’ preferences. Simultaneously, the right panel demonstrates that this development naturally brought a steady increase in corporate distributed income (right axis), that is, dividends paid to shareholders by corporations. Finally, the bottom of the right panel shows the high volatility of EU stock markets since 1999 as a result of stock market capitalisation and the turnover ratio of stocks traded (left axis). Stock market capitalisation is the total value of the shares of publicly traded corporations, and the stock turnover ratio is the number of stocks traded in a given period over stock market capitalisation. Given the rising number of listed firms during this period, stock market volatility translates into increased uncertainty for non-financial firms, which incentivises them to shift away from commitment-based HR practices and to undermine the role of trade unions, as described earlier.

Shareholder value orientation in the EU, 1999–2021.

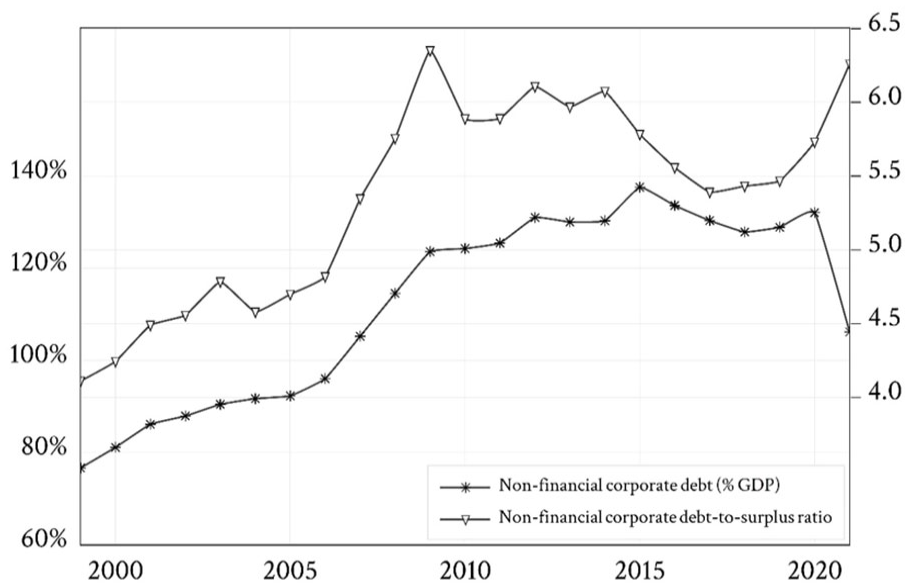

Figure 2 focuses on the rise in the corporate indebtedness of non-financial firms in the EU since 1999. The average debt-to-GDP ratio for non-financial corporations increased from 77 per cent in 1999 to 138 per cent within 16 years, reaching its peak for this period in 2015. Between 2015 and the beginning of the pandemic it remained consistently higher than 130 per cent. In 2021 it fell to 106 per cent because of debt relief measures implemented by governments across the EU during the COVID-19 pandemic. Non-financial corporations’ debt-to-gross-operating-surplus ratio followed a fairly similar trajectory, growing from 4.11 in 1999 to 6.35 in 2009. While its value initially stabilised, it then slightly declined after the onset of the eurozone crisis in 2010, and from 2019 it recovered quickly, reaching 6.26 in 2021. Regardless of whether business debt has been used to buy back shares or to fund real investment projects, it is evident that over the past 23 years, debt owed by non-financial corporations in the EU has soared, outstripping their income or GDP, and has become a major burden for them (Kalemli-Özcan et al., 2022).

Non-financial corporate debt in the EU, 1999–2021.

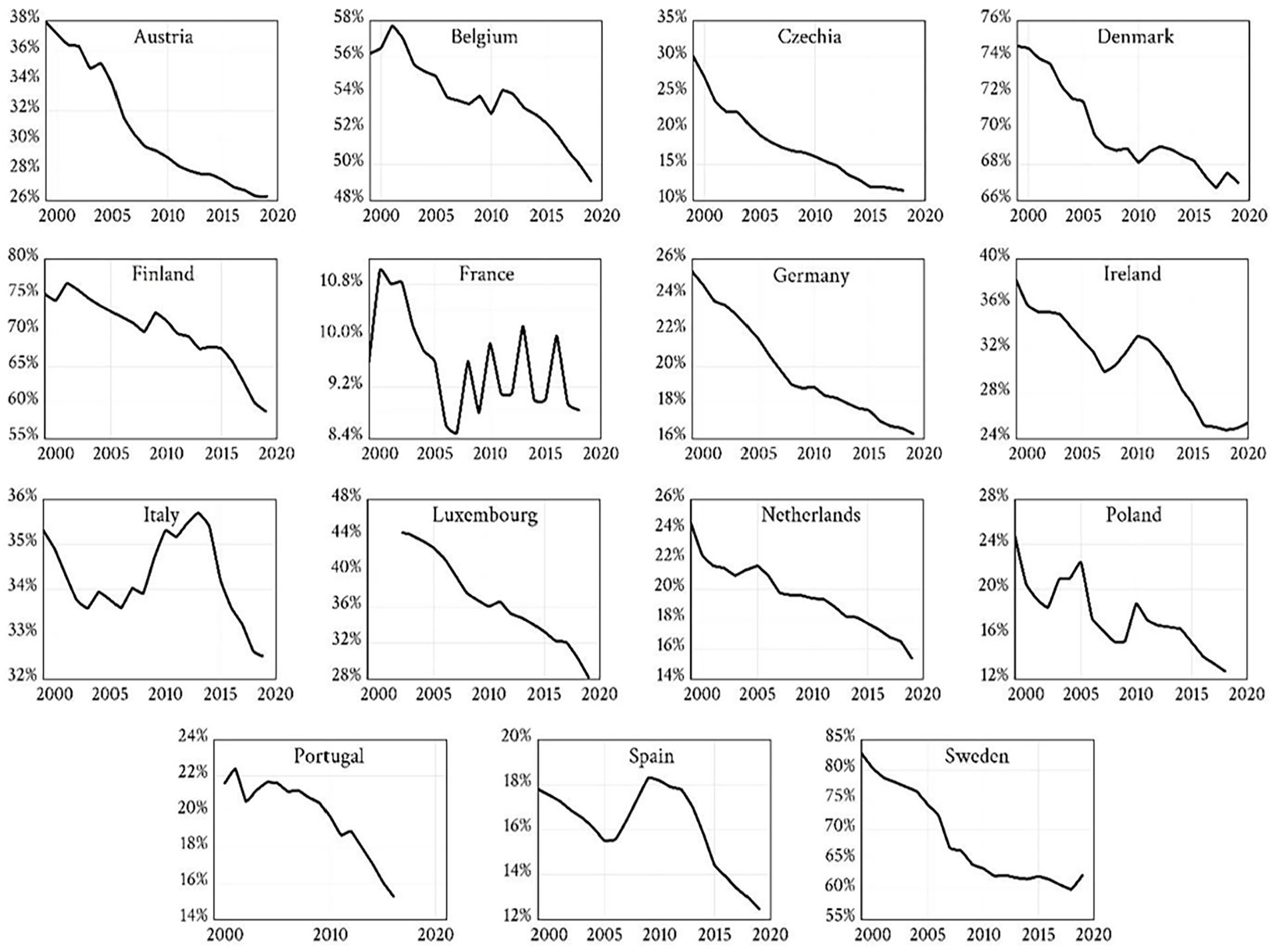

The process of ‘harmonious deregulation’ in financial markets and the increased protection of shareholders’ rights across EU Member States has impacted employment relations. Despite lingering national differences, shareholders’ growing influence in Europe has driven business to converge toward the short-termist corporate governance model typical of Anglophone practices (Cernat, 2009; Drobetz and Momtaz, 2020). Predictably, a significant outcome of intensified corporate short-termism is lobbying for the liberalisation (deregulation) of employment relations and undermining the role of trade unions in workplaces and broader social agreements across Europe (Almond et al., 2003; Culpepper and Regan, 2014). The weakening of unions’ institutional power means that workers have fewer incentives to join or remain members of unions. This sets off a vicious cycle in which unions keep losing influence, exacerbating the divide between firms’ ‘external balance’ and a cooperative ‘internal equilibrium’ approach. As illustrated in Figure 3, union density has declined sharply across EU countries during the period of rising shareholder pressure. The exception is France, where the unionisation rate has remained relatively stable since 2006. It is essential to note, however, that French union density has consistently been lower than in any other EU country since the beginning of the latest phase of EU integration.

Trade union density in the EU, 1999–2020.

Data and methodology

In this section we discuss the panel data econometric approach that this study uses to evaluate the association between the rise of corporate financialisation and the decline of unionisation rates in the EU during the latest phase of European integration. Given the relatively limited time dimension of our sample, individual country analysis using time series analysis would probably yield biased estimates. Thus, our preferred approach is panel data analysis. While there is some variation between the countries of our sample the high level of economic integration over the period under examination favours a panel data-based approach. Based on the discussion in Section 2, our regressions also control for other well-established drivers. Accordingly, our baseline equation is as follows:

where i designates the cross-sectional dimension (country) and t the time unit (year) of our sample. The terms φi, αt, and εit denote country fixed effects (FE), time FE, and the error term, respectively.

Regarding corporate financialisation, we use each of the six measures reported in Figures 1 and 2 to evaluate different dimensions of hypotheses 6 and 7 (see Section 2). Following the mechanisms presented by Kollmeyer and Peters (2019), we expect the two measures of corporate indebtedness, the corporate distributed income ratio and the two stock market volatility indicators to be negatively associated with union density. We proxy corporate indebtedness with the corporate debt-to-income ratio (source: BIS) and the non-financial corporation debt-to-surplus ratio (source: OECD). Regarding the shareholder value orientation, we use corporate distributed income (percentage of property income) from the OECD database to proxy divided payments to shareholders, and the market capitalisation-to-GDP ratio of domestic listed companies and the turnover ratio of domestically traded shares (%) as proxies for stock market volatility (source: World Bank). Similarly, we evaluate the impact of the number of listed companies (source: World Bank). We anticipate that a rising number of listed firms will also be negatively associated with aggregate unionisation rates, as it indicates the spread of the shareholder-value-maximisation ideology across non-financial corporations within EU economies since 1999. Because this variable is given in levels and grows exponentially, we follow standard practice and include its natural logarithm. Compared with Vachon et al. (2016), who centre on employment growth in the low-unionisation FIRE sector, here we explore specific mechanisms related to how shareholder value orientation and non-financial corporations’ debt burden can transform corporate governance and undermine union membership.

Following the main hypotheses (1–5) from the literature presented in Section 2, our regressions also include controls for de-industrialisation, government ideology, labour market regulation, trade globalisation and inflation. De-industrialisation is proxied by the share of industrial employment (% total employment) figure from the World Bank. As for government ideology, we include the Left-Right Index, that is, the weighted seat share of left-wing parties as a percentage of the total parliamentary seat share of all governing parties (left_gov2) (source: Armingeon et al., 2023). The control variable for labour market regulation is BargCent: Centralisation of wage bargaining, a measure of bargaining centralisation from Visser’s (2019) data set. This is a discrete 5-point variable whose range extends from 1 (decentralised) to 5 (cross-industry centralisation). Following standard practice in the literature, we proxy trade globalisation via trade openness (imports plus exports over GDP) from the World Bank. Finally, we also include the rate of consumer price inflation.

Overall, our unbalanced time-series cross-sectional data set includes the 15 EU countries mentioned earlier and covers the period 1999–2019, based on data availability. Tables A1 and A2 in the Appendix present descriptive statistics and unit root test results for all variables. Given that all variables are stationary in levels (integrated of order zero), using a first-difference estimator is not necessary in our case. Preliminary analysis using two-way fixed effects (FE), OLS regressions suggests that panel heteroskedasticity, contemporaneous correlation and autocorrelation are present in most cases. The presence of contemporaneous correlations especially is not surprising because the sample includes highly integrated economies, with regard to which changes in one can easily spill over to the rest to some extent. In such cases, the standard approaches are to estimate the equations via either two-way FE with panel-corrected standard errors (PCSE) or feasible generalised least squares (FGLS). FGLS is superior to the FE-PCSE estimator when the sample is asymptotic (in other words, the number of observations increases but not the number of parameters) and the time dimension (T) is larger than the cross-sections dimension (N) of the panel (Beck and Katz, 1995). Given that this is the case with our data set (T = 21; N = 15), our preferred approach is the FGLS, time FE estimator. We use time FE because it is T that increases rather than N.

Results and discussion

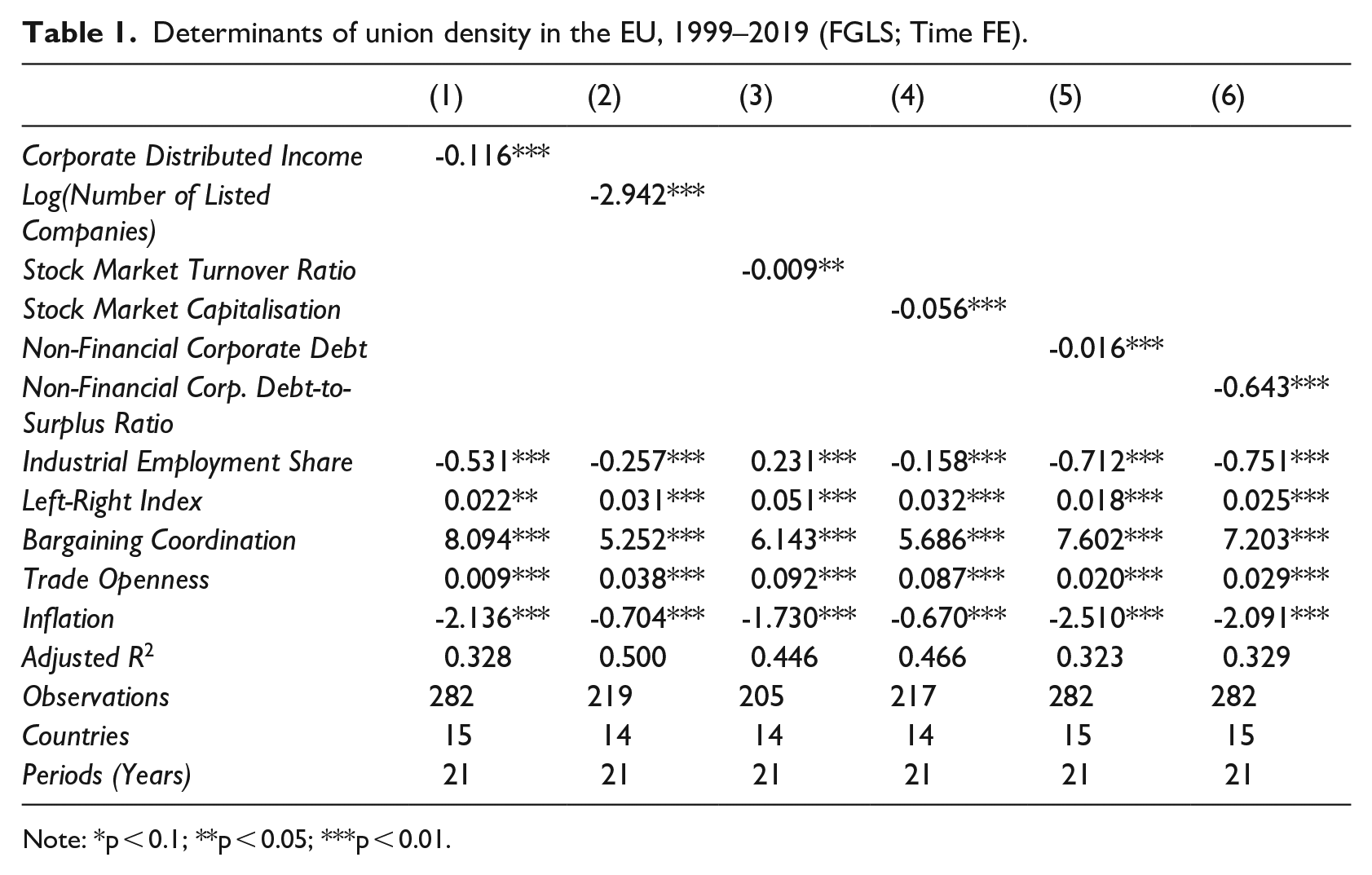

Table 1 reports the findings of our econometric analysis. The coefficients reported show the average change in the dependent variable (union density) in response to a one-unit change in the relevant explanatory variable. Our strategy is to keep our controls in all equations and then use a different measure of corporate financialisation in each of them. Overall, all measures of corporate financialisation, whether related to non-financial corporation debt or shareholder value orientation, are negative and statistically significant in every equation. 5

Determinants of union density in the EU, 1999–2019 (FGLS; Time FE).

Note: *p < 0.1; **p < 0.05; ***p < 0.01.

Equation (1) shows that dividend payments have a negative and statistically significant effect on union density, which strongly indicates that shareholder value maximisation is indeed linked to lower unionisation rates. Similarly, the number of corporations listed on stock markets is found to undermine unionisation in the EU, indicating the effects of the spread of shareholder value orientation across the economy (equation (2)). Furthermore, the stock market trading volume of shares and stock market capitalisation have similar effects in terms of size and statistical significance, which provides additional evidence that the volatility and uncertainty arising from non-financial corporations’ increasing dependence on stock markets is undermining trade union membership (equations (3) and (4)). Finally, equations (5) and (6) show that increases in corporate debt ratios are also associated with reductions in union density. As already mentioned, increased financial payments incentivise managers to undermine unions in order to pass these costs on to workers. Taken together, our results provide robust support in favour of our main argument that indeed union membership has been undermined because of the financialisation of corporate governance in the EU since 1999.

According to the adjusted r-squared values, equation (2) is the model with the best goodness-of-fit between our six equations. Because the financialisation proxy in this equation is the log number of domestic listed firms, it is not surprising that a variable that captures the spread of shareholder value maximisation ideology across non-financial corporations improves the fit of a model of aggregate union density.

Our findings provide evidence that the intensification of corporate financialisation in the EU over the past 21 years has contributed to the decline of union membership as a result of the pressures imposed by rising corporate debt ratios and a heightened shareholder value orientation on corporate governance in non-financial corporations. These results complement the study by Vachon et al. (2016) that focuses on employment shifts between the FIRE sector and the rest of the economy in the EU, and shows that rising employment rates in finance, insurance and real estate have depressed unionisation rates. Our work expands on this by providing evidence regarding specific mechanisms that capture the dependency of non-financial corporations on financial instruments, actors and markets. In contrast to Kollmeyer and Peters (2019), who explore the shareholder value orientation-union density nexus using a wider sample of advanced economies, we focus on a narrower group of countries that have experienced a coordinated shift towards a shareholder value orientation more recently than the Anglophone economies. Overall, our results confirm the historical analysis of Section 2 that the intensification of financial market integration under ERM II, which induced non-financial corporations to become financial performance-oriented and shift towards market-based HR systems, has also significantly undermined union membership in the EU.

Our findings and those of the related studies mentioned above have interesting implications both for dynamic capabilities theory and Roethsliberger and Dickson’s theory of the two functions of the firm. Regarding dynamic capabilities theory, corporate financialisation seems to incentivise corporate managers not only to lay off workers, make work contracts more precarious, and reduce wages, but also to undermine the role of unions and union members at the workplace. Thus, disconnects driven by financialisation are achieved by undermining workers at both the individual and the collective level. Concerning Roethsliberger and Dickson’s theory, the broader literature on corporate financialisation, working conditions and unionisation shows that, in contemporary economies, non-financial corporations’ shift of focus towards maintaining their overall ‘external balance’ at the expense of their ‘internal equilibrium’ is driven mainly by the impact of financialisation on their external financial balance. As trade unions are one of the key safeguards of ‘internal equilibrium’, undermining them is essential as a firm becomes increasingly oriented towards the ‘external balance’.

Conclusions

This article explores the impact of financialisation on unionisation rates during the latest phase of EU integration. We argue that a shareholder value orientation and non-financial corporate indebtedness, two key characteristics of the EU integration process, shape firms’ governance structures by increasing the importance of their ‘economic’ or ‘external balance’ functions relative to their ‘human’ or ‘internal equilibrium’ ones. In other words, financialised non-financial corporations which face rising debt repayment costs and/or pressures to maximise returns to shareholders in the short run, often undermine unions in order to pass the costs on to workers and improve corporate balance sheets. Using available data for 15 EU countries since 1999, we show that rising corporate debt ratios, the increasing number of listed corporations, the growth of dividend payments, stock market capitalisation, and share trading are strongly associated with decreases in unionisation rates. All measures of shareholder value orientation and corporate indebtedness are found to play key roles.

These findings have significant implications that are relevant for the trade union movement and also form a basis for further research on the topic. Political parties aiming to promote a more egalitarian growth agenda with workers’ organisations as key stakeholders should actively advocate for the regulation of shareholder primacy and the imposition of strict rules on downsizing in response to economic conditions. Understanding that labour market regulation is not sufficient is fundamental as the interconnection between financial markets, corporate governance strategies and labour management is stronger than ever. Regarding further research implications, our work could be extended in several directions. Focusing on case studies and/or specific countries is a useful route to obtain a more detailed understanding of the process that we describe here in different contexts.

Footnotes

Appendix

Determinants of union density in the EU, 1999–2019 (two-way FE).

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Corporate Distributed Income | −0.059** | |||||

| Log(Number of Listed Companies) | −0.006 | |||||

| Stock Market Turnover Ratio | −0.001 | |||||

| Stock Market Capitalisation | 0.011* | |||||

| Non-Financial Corporate Debt | −0.029 | |||||

| Non-Financial Corp. Debt-to-Surplus Ratio | 0.119 | |||||

| Industrial Employment Share | −0.311 | −0.218 | −0.204 | −0.227 | −0.466 | −0.298 |

| Left-Right Index | 0.014** | 0.004 | 0.002 | 0.003 | 0.019*** | 0.014* |

| Bargaining Coordination | 0.651 | −0.137 | −0.071 | −0.027 | 0.109 | 0.294 |

| Trade Openness | −0.045* | −0.081 | −0.076*** | −0.077*** | −0.036 | −0.051* |

| Inflation | −0.432* | −0.190 | −0.306** | −0.268* | −0.365 | −0.417 |

| Adjusted R 2 | 0.115 | 0.388 | 0.342 | 0.339 | 0.126 | 0.079 |

| Observations | 282 | 205 | 219 | 217 | 282 | 282 |

| Countries | 15 | 14 | 14 | 14 | 15 | 15 |

| Periods (Years) | 21 | 21 | 21 | 21 | 21 | 21 |

Note: *p < 0.1; **p < 0.05; ***p < 0.01. Beck-Katz Robust Standard Errors (Panel Corrected).

Acknowledgements

The authors are grateful to Evelyne Léonard and Laurent Taskin for the invitation to contribute to the Special Issue ‘Human resource management and the worker’ of Transfer. We would also like to thank two anonymous reviewers for their insightful comments that greatly improved our work.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

1

A potential contradiction arises when bargaining coverage extends to both unionised and non-unionised employees, however. In such cases free riding becomes important because most workers enjoy union benefits anyway and thus have little incentive to join or remain in a union (Bryson, 2008; Freeman and Medoff, 1984; Olson, 1965).

2

Early definitions of financialisation centred myopically on the rise of financial profits relative to corporate profits within non-financial corporations (Krippner, 2005). Here, we use a broader definition that captures more accurately the fact that financialisation is closely linked to the dependency of non-financial sectors on finance and insurance institutions and on instruments, which undermines their core functions and ‘internal equilibrium’ (value creation).

3

Commitment-based HR systems typically come with long-term and stable employment relationships, and workers’ associations actively participate in decision-making processes within the corporation.

4

5

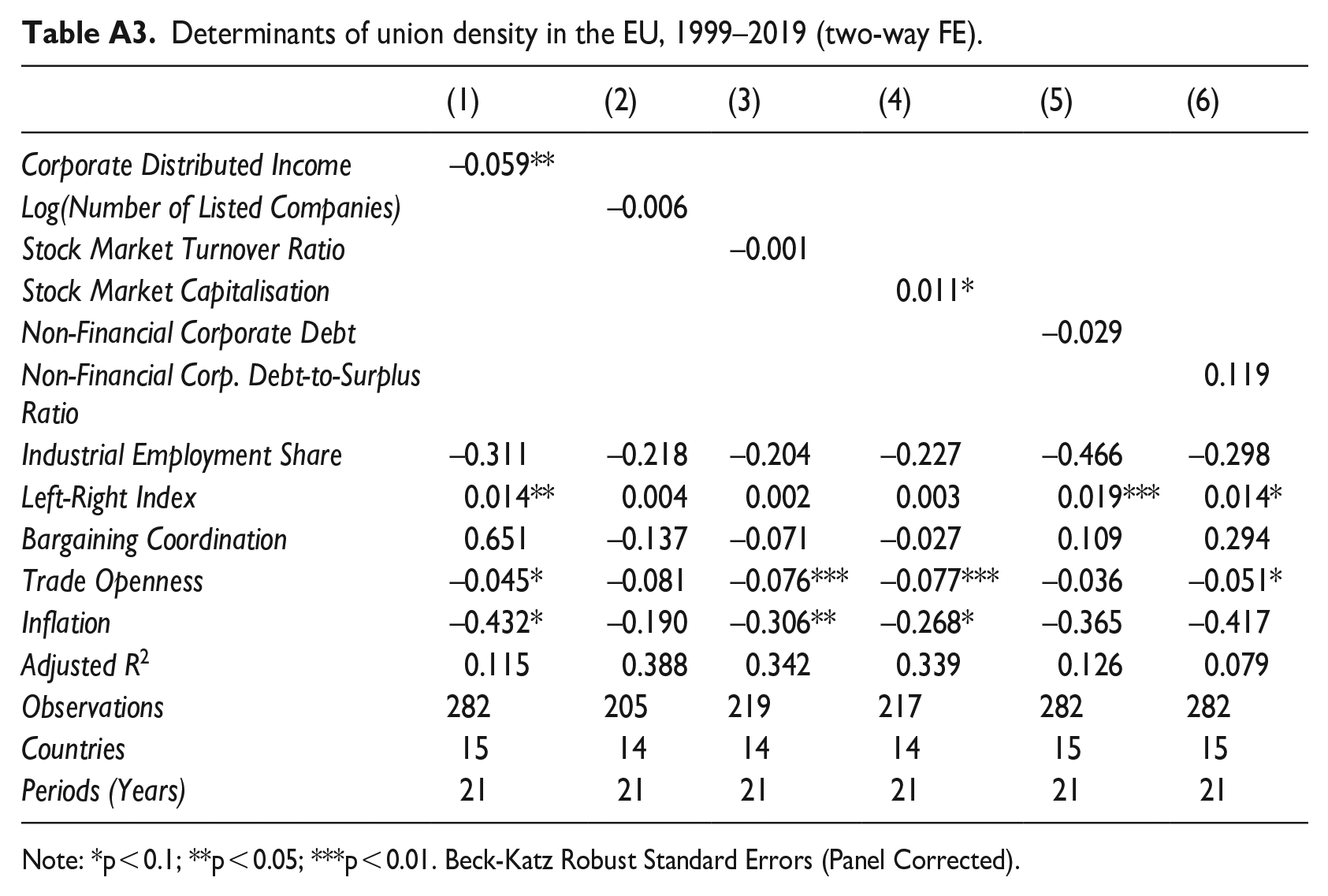

For completeness, in Table A3 of the ![]() we also report estimates of all equations using two-way fixed effects (FE) with panel-corrected standard errors (PCSE). As anticipated (see Section 4), the explanatory power of these models is significantly lower than that of the FGLS-Time FE estimator when comparing r-squared values and the statistical significance of the coefficients. But the majority of variables maintain their respective signs.

we also report estimates of all equations using two-way fixed effects (FE) with panel-corrected standard errors (PCSE). As anticipated (see Section 4), the explanatory power of these models is significantly lower than that of the FGLS-Time FE estimator when comparing r-squared values and the statistical significance of the coefficients. But the majority of variables maintain their respective signs.