Abstract

We address developments in collective wage bargaining arrangements in northern Europe in the light of two major political-economic challenges: EU eastern enlargement and the financial and economic crisis which broke in 2008. Through the lens of debates on convergence and divergence, we examine three dimensions of collective wage bargaining: coordination across sectors; articulation between different levels; and regulation of wage floors. We draw on findings from five countries and four sectors. Our analysis undermines the proposition that developments exhibit a common liberalising trajectory. It points to the differential impact of the two major political-economic challenges as between sectors, highlights similar and different policy responses by actors within a sector across countries, reveals differing consequences for governance of collective wage bargaining across sectors and countries, and finds no uniform trend in wage inequality outcomes.

L’examen des accords issus de la négociation collective sur les salaires en Europe du Nord est replacé dans le contexte de deux défis politico-économiques majeurs: l’élargissement de l’UE à l’Est et la crise financière et économique qui a éclaté en 2008. La question de l’existence d’une convergence ou d’une divergence est abordée selon trois dimensions de la négociation collective des salaires: la coordination entre les secteurs, l’articulation entre les différents niveaux et la réglementation des planchers salariaux. Nous nous appuyons sur les résultats obtenus dans cinq pays et quatre secteurs. Notre analyse remet en question l’idée selon laquelle les évolutions présentent une trajectoire commune de libéralisation. Elle souligne la différence d’impact, entre les secteurs, des deux principaux défis politico-économiques évoqués et met en lumière les similarités et les différences dans les réponses politiques apportées par les acteurs d’un secteur dans les différents pays. L’analyse montre également les conséquences différentes pour la gouvernance des négociations collectives salariales entre les secteurs et les pays, et ne relève aucune tendance uniforme dans les résultats en matière d’inégalité salariale.

Wir befassen uns im vorliegenden Artikel mit der Ausgestaltung von Tarifverhandlungen in Nordeuropa vor dem Hintergrund zweier wichtiger politisch-wirtschaftlicher Herausforderungen: der Osterweiterung der EU und der Finanz- und Wirtschaftskrise, die 2008 ihren Anfang nahm. Anhand der Debatten über Konvergenz und Divergenz untersuchen wir drei Dimensionen von Tarifverhandlungen: branchenübergreifende Koordinierung, Verständigung zwischen den unterschiedlichen Ebenen und Mindestlohnregelungen. Zu diesem Zweck haben wir Ergebnisse aus fünf Ländern und vier Sektoren ausgewertet. Unsere Analyse widerlegt die Annahme, dass alle Entwicklungen einem gemeinsamen Liberalisierungstrend folgen. Sie zeichnet die unterschiedlichen Auswirkungen der beiden großen politisch-wirtschaftlichen Herausforderungen in den einzelnen Sektoren nach; und beschreibt vergleichbare und unterschiedliche politische Antworten der Akteure eines Sektors in verschiedenen Ländern mit unterschiedlichen Folgen für die Gestaltung von Tarifverhandlungen in Sektoren und Ländern. Ein einheitlicher Trend bei der Entwicklung von Lohnungleichheiten ist nicht festzustellen.

Introduction

Relatively little attention has been accorded to recent developments in collective wage bargaining (CWB) arrangements in the countries of northern Europe. This contrasts with the extensive analysis of the upheavals to CWB arrangements which featured prominently in the crisis-induced labour market reforms in several southern countries (e.g. Koukiadaki et al., 2016; Schulten and Müller, 2015). Has the assault on multi-employer CWB in favour of more fragmented, decentralised and deregulated arrangements in southern Europe brought pressures on northern countries to move in a similar direction? Or have northern countries sustained their prior trajectory of a controlled decentralisation of CWB within a coordinated framework of multi-employer arrangements, reflecting their differing competitive profile in European and international markets? Or have the consequences of eastern EU enlargement pushed northern economies on to a different trajectory, in response to the pressures on CWB arrangements from flows of labour and services from east to north and of capital in the opposite direction? Are differing responses to these macro pressures evident between northern countries and/or between sectors?

These alternative possibilities invoke debates around convergence and divergence in industrial relations (IR), and in socio-economics more generally. These have been rekindled by the work of Baccaro and Howell (2017) and Thelen (2014). Baccaro and Howell contend that there is a common liberalising trajectory across the advanced economies of western Europe, regardless of variant of capitalism and associated differences in institutions – including those governing IR and CWB. Their core claim is that, persisting institutional differences notwithstanding, outcomes are increasingly similar across countries. Thelen, whilst accepting that pressures for liberalisation are widespread, disputes Baccaro and Howell’s contention about outcomes, identifying important differences in developments in social solidarity, including wage equality, between countries. She contends that institutions still matter in shaping these outcomes.

We address the different possibilities for the development of CWB in northern Europe through the lens of convergence and divergence by examining three distinct dimensions: coordination of CWB across sectors; articulation between different levels of CWB; and the regulation of wage floors. We do so by drawing on the findings of a study of developments in five countries and four sectors (Dølvik et al., 2018). This article’s novel contribution lies in confronting the main theses in the literature on convergence-divergence with a comparison across sectors, as well as countries. The multi-country, multi-sector design enables us to pick up on any ‘converging divergences’ (Katz and Darbishire, 2000). The five countries, Denmark, Germany, Norway, Sweden and the UK, capture different varieties of capitalism. The four sectors, construction, manufacturing, industrial cleaning and temporary agency work, are positioned differently in terms of salience of exports, and cross-border flows of capital, labour and services. The time frame covers the two major political-economic challenges of the past two decades, from prior to the EU’s 2004 and 2007 eastern enlargement, through the onset in late 2008 of the financial and economic crisis and its aftermath, up until 2017. The data come from a programme of interviews with leading employers’ association and trade union officials in, and analysis of a range of documentation from, the sectors and countries concerned.

The next section unpacks the concept of convergence and divergence, clarifying how the terms will be deployed. It then reviews recent controversies around convergence and divergence in IR, including CWB. The third section details the research design and methods. Findings on the three dimensions of CWB for the four sectors are presented in the fourth section. The patterns of convergence and/or divergence which emerge are then discussed in the fifth. The sixth section concludes.

Convergence and divergence: concepts and recent controversies

In deploying the terms convergence and divergence we build from three points of departure. The first is the distinction between trajectories and end-points. A common trend need not imply arrival at a common end-point. Jacoby’s (2005) longitudinal study of the impact of globalisation on corporate governance arrangements and management’s employment policy and practice in Japanese- and US-owned corporations highlights this distinction. Comparing the 1990s with the 1970s, both sets of corporations had (further) embraced market principles, thereby exhibiting a common trend. Yet their responses to globalising pressures also differed pronouncedly: the US-owned corporations, which already embraced market principles to a greater degree than their Japanese counterparts, had travelled much further in this same direction. The two sets of corporations were further apart in their employment policy and practice than they had been 20 years earlier (evincing movement away from any common end-point).

The second is Hay’s (2000) distinction between four types of convergence: input; policy; output; and process. These are frequently conflated in the literature. Input refers to convergence in the pressures on economies, including labour markets. Policy convergence relates to the policies pursued by public authorities and private actors including employers and trade unions. Output convergence concerns the outcomes of policies. Process convergence manifests itself in the processes which underpin and sustain the evolution of economies. This includes inter alia prevailing modes of governance in IR: the relative emphasis on state-led, associational (between employers’ associations and trade unions) and market-based (entailing employer unilateralism) (Crouch, 2015). Crucially, one type of convergence need not imply others. For example, input convergence does not imply policy convergence, and even where similar policies are adopted in the face of similar input pressures outcomes may still differ. Institutions mediate between input and policy, and between policy and outcome.

Katz and Darbishire’s (2000) insistence that the trajectories associated with different kinds of convergence are at play at sectoral, as well as economy-wide, level constitutes our third departure point. Converging divergences arise when IR arrangements in a given internationalised sector become more similar across advanced economies whilst those between sectors within national boundaries become more different. Furthermore, common cross-border patterns may be more evident in some sectors, such as internationally exposed ones, and less so in others, such as those anchored in domestic markets (Bechter et al., 2012).

For much of the past two decades socio-economic debates over convergence and divergence have been framed by the varieties of capitalism (VoC) literature. Priority was accorded to analysing policy, process and output divergences between different VoCs. This framing has been challenged by critics (e.g. Streeck, 2009) who draw attention to powerful tendencies in contemporary capitalism, towards liberalisation and marketisation, which transcend the different varieties. Focusing on IR and CWB, Baccaro and Howell (2017) identify a common liberalising trajectory across west European countries regardless of variant of VoC, and despite the persistence of distinctively national institutional configurations. This is expressed in the decentralisation, deregulation and de-collectivisation of wage determination arrangements, resulting in enhanced scope for the exercise of employer discretion. Such greater discretion, they argue, can be arrived at by different routes. Employers have found ways to by-pass institutions, or have implemented decentralisation in ways which dilute the impact of higher-level collective agreements at firm level, entailing a shift from associational to market-based governance. Alternatively, they have secured shifts in the functioning of institutions from discretion-limiting to discretion-enhancing, albeit with seeming continuity of associational governance. Amongst northern Europe’s economies, Baccaro and Howell contend that despite continuing institutional differences outcomes in, for example, the flexibility with which employers can deploy labour and in wage inequality in Germany and Sweden are becoming more similar to those in the already liberalised UK.

Viewed through Jacoby’s (2005) lens, Baccaro and Howell’s contention is that this common liberalising trend is a convergent one, towards similar end-points in outcomes. Concerning Hay’s framework, Baccaro and Howell stress the increasing plasticity of institutions reflected in their conversion to pursue different ends to those for which they were originally intended. The implication is that institutions matter less. A common input pressure, liberalisation, tends to be reflected in common policy responses and leads to common outcomes, institutional differences and differences in process notwithstanding. Their (functionalist) emphasis on institutional plasticity also risks losing sight of the extent to which the purpose and outcomes of institutions are contested (Streeck and Thelen, 2005). Baccaro and Howell cannot be read according to our third departure point, since they pay little systematic attention to sectoral differences.

Thelen (2014) distinguishes between institutions underpinning coordination (of CWB) and those promoting social solidarity, including wage equality. She finds that liberalisation, expressed in decentralisation of CWB, is more apparent in Denmark and Sweden than in Germany, whereas social solidarity remains stronger – and wage inequality noticeably less – in the former two than the latter. In terms of Jacoby’s distinction, Thelen identifies different end-points across countries against a widespread liberalising trend. By stressing the role of institutions, and of actors in reframing institutions, the distinct and non-corresponding trajectories of input pressures, policy responses, processes and outcomes (Hay, 2000) are identifiable. Moreover, Thelen shows sensitivity to sectoral differences, including between internationally exposed industrial and more domestically anchored service sectors.

Research design and methods

Our research addressed developments in three dimensions of CWB amongst five northern European countries: coordination of CWB across sectors; articulation between different levels of CWB; and regulation of wage floors. The first two are also focal issues for Baccaro and Howell (2017) and Thelen (2014), placing us well to engage with their respective arguments. Our canvass is extended to regulation of wage floors, and the respective roles of CWB, statutory measures (such as extension and a legal minimum wage) and employer unilateralism. The sectoral element of our research, examining developments in four differing sectors, enables us to tease out cross-cutting sectoral and country trajectories. The research paid attention to employer perspectives towards CWB arrangements, and the rationales for any changes that employers were pressing for, as well as to trade union responses. This allows us to illuminate how employers are actually using the greater discretion which Baccaro and Howell stress.

The time frame for our research, from 2000 until the end of 2017, embraces the two major political-economic challenges faced by the countries of northern Europe over the past two decades: eastern enlargement of the EU/European Economic Area (EEA) to include 10 post-socialist Central and Eastern European (CEE) countries (in 2004 and 2007) and the financial and economic crisis which broke in late 2008 triggering a sharp recession, with longer lasting impacts via austerity policies on economic activity in some countries.

The choice of countries and sectors embodies both the method of difference and of similarity (Djelic and Quack, 2003). The five countries – Germany, Denmark, Norway, Sweden and the UK – span two variants of coordinated market economy (Germany’s social market economy and the more solidaristic Scandinavian ones) and the UK’s liberal market economy. The first four enjoy comparative economic advantage in the strength of their manufacturing in export markets for high valued-added products, whilst the UK’s comparative strength lies in the export of high valued-added services. Germany and the UK are large economies; those of the three Scandinavian countries are smaller. Turning to IR, multi-employer bargaining arrangements predominate in the first four countries whilst the UK is characterised by single-employer arrangements insofar as wages are determined by CWB 1 . Multi-employer arrangements in the three Scandinavian countries are governed by differing cross-sectoral coordination arrangements under which the internationally exposed industrial sector takes a leading role. There is no overt coordination of Germany’s sector-based arrangements, although an informal convoy principle with metalworking in the lead is apparent (Müller et al., 2018).

The five countries were differently affected by the two major political-economic challenges. The impact of the EU’s eastern enlargement on the flow of efficiency-seeking foreign direct investment (FDI) eastwards was most marked in Germany and least so in the UK, with the three Scandinavian countries in between. Flows of migrant labour from CEE countries have been sizeable for all countries, although more so for Norway, Germany and the UK. Flows of posted workers associated with provision of services have been most prominent in Germany and Norway. Concerning the impact of the crisis, Germany, Norway and Sweden were amongst the least affected in the EU/EEA, whilst Denmark and the UK experienced deep recessions.

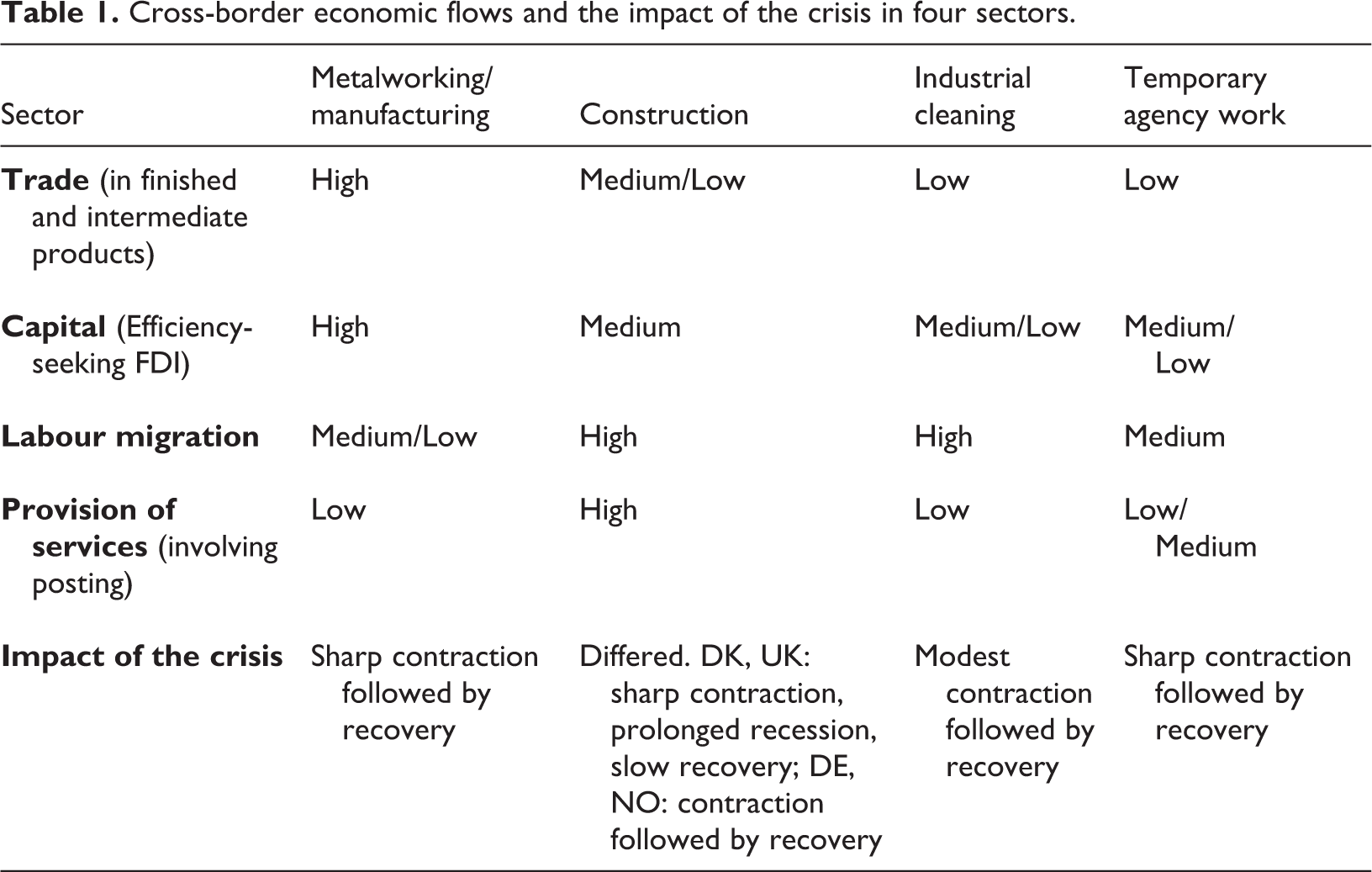

The choice of the four sectors – manufacturing (metalworking in Germany and the UK), construction, industrial cleaning and temporary agency work (TAW) – was informed by their position in respect of four kinds of cross-border economic flow: trade in goods; flows of capital, associated with efficiency-seeking FDI; flows of labour involving migration; and cross-border provision of services which can entail posting. The latter three are more concentrated within Europe’s single market than the first. The first two flows differentiate those sectors where products and production tend to be mobile across borders from those where they tend to be territorially anchored within domestic borders. Table 1 locates the sectors in terms of these four cross-border economic flows, indicating the differences between them. It also indicates the (varied) nature of the impact of the crisis on each sector.

Cross-border economic flows and the impact of the crisis in four sectors.

Concerning IR, manufacturing/metalworking is characterised by strong organisation amongst both employers and trade unions and acts as the pattern setter for CWB in most of the countries. Low pay is not generally a problem: hence (re)regulation of wage floors is not a pressing issue. Construction has been traditionally well-organised, and has tended to set the mark for wage increases amongst sectors oriented towards domestic markets. Pockets of low pay feature in all the countries and have expanded in some. Both sectors have (relatively) high CWB coverage. Industrial cleaning is marked by low rates of organisation, (relatively) low CWB coverage and a high incidence of low pay. In TAW organisation is low, and arrangements for CWB are developing in different ways in each country. Pockets of low pay feature in Norway and the UK. (Re)regulation of wage floors is a salient issue in the latter three sectors.

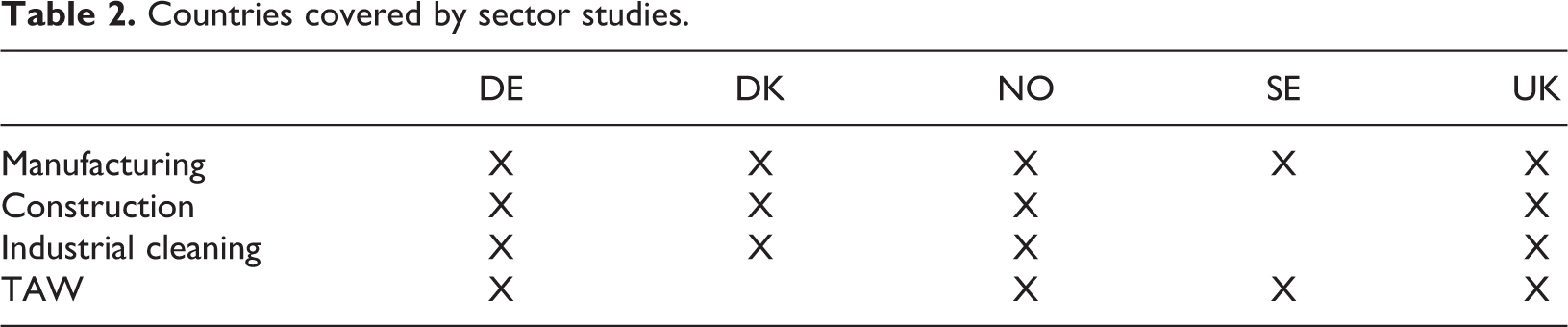

Our data come from a programme of interviews with employers’ association and trade union officials in each of the four sectors across the five countries (and confederal level in Scandinavian countries), together with examination of relevant published and grey documentation for the respective sectors and countries. Typically, respondents were the lead negotiators on both sides. These interviews were undertaken between the summer of 2016 and spring of 2017, and in some instances built on previous conversations from other projects. Respondents were asked about the challenges posed by, respectively, eastern EU enlargement and the crisis for CWB arrangements; their policy preferences on how to respond to these; and their perspectives on any recent changes. Research was not undertaken in all four sectors in every country. Table 2 shows that for each sector there is data for Germany, Norway, the UK and at least one other Scandinavian country. We were not able to obtain outcome data on wage dispersion, which bears on social solidarity (Thelen, 2014), on a consistent basis across countries within each sector. We present, instead, an analysis of developments in wage dispersion at cross-sector level.

Countries covered by sector studies.

Findings

Within each of the four sectors, input pressures tend to be similar across countries. The sectoral accounts which follow therefore focus on policies and processes, with outcomes subsequently assessed at cross-sector level. The sectoral accounts address whichever of the three dimensions of CWB have invoked a substantial challenge within a sector. They draw on fuller expositions of findings from the wider project: respectively, Müller et al. (2018) for manufacturing, Arnholtz et al. (2018) for construction, Trygstad et al. (2018) for industrial cleaning and Alsos and Evans (2018) for TAW.

Manufacturing

Manufacturing (metalworking for Germany and the UK) has a strong export profile across all five countries, and is exposed to intense international competition within and beyond the EEA. Production processes in northern Europe are relatively capital intensive, utilise high-skilled labour and result in high value-added outputs. Northern European countries tend to compete with each other in particular segments of the market. The sector is well-organised, with (relatively) high levels of employer organisation and trade union density in Germany and the Scandinavian countries and, compared to the private sector average, the UK. CWB coverage is high (80–90 per cent) in Sweden and Denmark, less so in Norway and Germany (around 65 per cent) and much lower (25 per cent) in the UK.

Pressure to maintain and improve competitiveness has intensified during and following the crisis, and placed strains on CWB arrangements. In parallel, eastern enlargement has triggered restructuring and relocation of production (or threats to do so) eastwards in pursuit of reduced costs. The associated strain has translated into the spread of concession bargaining, aimed at retaining production and jobs in northern countries, most strikingly in Germany. The main challenges facing employers and trade unions have been: to secure the sector’s continued wage leadership role in relation to other sectors, ensuring that competitiveness considerations remain foremost, involving mechanisms for coordination of CWB across sectors; and enhancing flexibility, which enables companies to respond to particular contingencies, involving articulation between different bargaining levels.

On wage leadership, adjustments have been made to coordination mechanisms in Sweden and Norway aimed at making the wage settlement ‘mark’ negotiated in manufacturing more binding on other sectors. There has been little change to arrangements in either Denmark or Germany. The UK has no mechanisms for coordination across sectors, although manufacturing wage settlements de facto establish a mark for other sectors. In Sweden, initiatives to strengthen cross-sector coordination have focused on the Industrial Agreement, which since 1997 has established the mark for other sectors. Following the 2010 bargaining round, two employers’ federations in the sector threatened to quit the Agreement since it was no longer delivering the requisite wage restraint. This prompted a (2011) deal clarifying and reinforcing the mechanisms for coordination across sectors. In Norway, the previous metalworking agreement was broadened in the early 2000s to embrace most of manufacturing, thereby achieving greater weight in relation to other sectors. Following a turbulent bargaining round in 2012, a public commission was established to evaluate the CWB system. The exercise confirmed the commitment of the parties to coordination based on manufacturing wage leadership, and obliged the employers’ confederation to regularly publish an estimate of the wage mark, based on the Industry Agreement. In Denmark, the shift to a coordinated process under which manufacturing sets the wage mark occurred in the early 1990s, combined with devolution of negotiations over actual wage rates to company level. The Industry Agreement specifies minimum pay scales: negotiated increases in these provide a coordinating indicator for company-level negotiators. In 2010 and 2012, for instance, minimal increases to these scales were widely followed at company level. In Germany, there are coordination mechanisms within sectors but not across them. In practice, metalworking has assumed a wage leadership role given its size and key export role, with other sectors following akin to a convoy. In recent years, any pressure for more formal coordination across sectors has disappeared given minimal wage growth in sectors oriented towards the domestic market.

Turning to flexibility for negotiations at company level, Germany formalised widespread scope for negotiating company-level derogations. Sweden, Denmark and Norway have seen limited or no recent change. Under the UK’s single-employer CWB arrangements, the issue does not arise. The temporary, unprecedented, 2009 crisis agreement in Sweden’s manufacturing sector, allowing company agreements which reduced both working time and remuneration, was prompted by the perceived need to respond to the competitive effects of Kurzarbeit schemes available to counterparts in Finland and Germany. Subsequently, the two sides negotiated a revised scheme applicable in the event of future recessionary circumstances, contingent on state funding (confirmed in 2014). In Denmark and Norway existing arrangements, which accord considerably flexibility to company level, have remained unchanged. In Germany, the process of opening up the metalworking agreement to negotiation at company level culminated in the 2004 Pforzheim agreement. This included a general opening clause, which inter alia established the possibility of derogating from the catalogue of issues covered by the sector agreement so long as this can be justified by creating or maintaining employment, or by improving a company’s competitiveness. The agreement also re-regulated the use of derogations, by requiring the approval of the sector-level parties. The possibilities contrast with the three Scandinavian countries where derogation is essentially precluded.

Overall, on coordination across sectors a common policy trajectory is apparent amongst the three Scandinavian countries towards sector-based arrangements which enable manufacturing to exercise wage leadership. The absence of any formal coordination mechanisms sets Germany apart from Scandinavia, whilst the absence of a sector agreement continues to set the UK even further apart. Wide scope for company-level negotiation is long-established in Denmark and Norway; a similar policy trajectory extending its scope can be detected in Sweden (under recessionary conditions) and Germany. None of the countries evidence a change in process trajectory, of the kind which occurred in the UK during the 1980s/1990s as multi-employer CWB unravelled, diminishing associational in favour of market-led governance.

Construction

Despite immobile end-products, the labour-intensive construction sector has seen increased internationalisation through cross-border flows of contractors and labour, particularly after the 2004–2007 enlargement. Due to its size, strong employment multipliers, and quasi-sheltered, highly cyclical nature, the sector holds a special position in national wage-setting regimes. In upswings, shortages of skilled labour, poaching, and ‘leap-frogging’ can unleash wage-price spirals that spill over to export industries. A central element in national coordination efforts has been to curb wage growth in construction, which traditionally set the pace in the sheltered sectors. Conversely, in downturns the sector’s fluid labour market with many small firms, long subcontracting chains, and mobile workforces are prone to underbidding, making wage floor regulation important to maintain a level field. These structural features have underpinned employer interest in collective regulation and institutions that control product and labour market competition, expressed in above average CWB coverage rates. These range from high in Denmark and Germany (respectively over and approaching 70 per cent), less so in Norway (over 40 per cent) and low in the UK (under 20 per cent).

The main driver of change has in all four countries been inflows of labour from CEE countries, involving posting by international subcontractors and direct hiring of migrants by domestic firms. These inflows have brought increased low-cost competition and curbed sectoral wage growth. The effect, reinforced by the (prolonged) impact of the crisis on activity in Denmark and the UK, has been to prevent construction unions from threatening the wage ‘mark’. The principal CWB challenge has been to prevent underbidding by re-regulation of wage floors. The coverage of collective agreements, and their purchase on terms and conditions above minimum rates, has been corroded as migrant workers have been engaged on less favourable conditions. This market-driven strain on sectoral wage floors has been a source of input convergence.

Employer responses have differed. In Germany, having minimalist extension arrangements applicable to posted workers since the 1990s, the sector’s employers and unions cooperated in countering wage dumping by, against the will of manufacturing employers, winning government support for extension of two minimum wage classes. In Norway, construction employers supported, again opposed by manufacturing employers, the unions’ invocation of a dormant provision for extension of minimum terms, which has eventually been raised substantially and flanked by chain liability and other measures. In Denmark, by contrast, the sector’s employers have abided by the strict voluntarist line of the employer confederation, which rejects any state interference in wage floor regulation, and referred to trade union rights to conclude agreements with foreign firms. The latter has proven an uphill battle. Despite high rates of coverage, securing covered posted workers a minimum wage, the unregulated scope for low-wage work has widened. In the UK sector, where multi-employer bargaining still exists, coverage has fallen further. In major parts of the sector the statutory minimum wage is the only wage floor, except where living wage campaigns have made a mark. After a decade with large inflows of CEE labour, often through temp agencies and self-employment, the UK stands out with patchy CWB, a relatively low statutory minimum wage, and much larger scope for employer-led, market-based wage determination than in the other cases.

Overall, Denmark and Norway evidence a divergent policy trajectory whereas there is some similarity in the policy trajectory of Norway and Germany. The UK’s policy trajectory remains distinct. Concerning process, the activation of extension has moved Norway away from Denmark and towards Germany. Market-led wage determination has continued to predominate in the UK, and has shown some growth in Denmark.

Industrial cleaning

Industrial cleaning is a labour-intensive service with low entry costs. International competition is low although competitive pressures are intense within domestic markets. Outsourcing by private and public organisations has driven rapid expansion, whilst the EU’s eastern enlargement triggered inflows of cheaper labour into northern economies. Prior to this the sector already featured substantial areas of disorganisation, with Germany a partial exception. CWB coverage is high in Germany, reflecting use of extension, but modest in Denmark, 40–50 per cent, and Norway, around 55 per cent, and low in the UK, less than 10 per cent.

Inflows of cheaper labour from CEE countries have undermined (or threatened) the regulation of wage floors. Given low establishment costs, migrants from CEE countries have set up self-employed and small businesses as well as being employed by existing companies. Accelerated growth of outsourcing in response to the additional pressures on costs arising during the crisis and its aftermath added further to this dynamic. Organised employers in the three countries with sector-based CWB (not the UK), increasingly feared losing out to non-covered, low-cost competitors. The main challenge to CWB arrangements concerns the regulation of wage floors.

Responses have differed across the four countries. In Germany, the use of extension was long-established but did not cover the entire sector, or the posted workers which proliferated following enlargement. Extension arrangements were augmented in 2007 to establish a sector-wide minimum wage encompassing the entire sector, including posted workers. This remains above the statutory minimum wage introduced in 2015. Further measures to bolster the wage floor have included protection of workers in outsourced activities under public procurement procedures. In Norway, which hitherto had relied on voluntary collective bargaining, sustained joint lobbying by the bargaining parties led to the introduction of extension for the entire sector, including posted workers, in 2011. The wage rates extended were the standard ones in the agreement, whose minimum is closer to the median than in the German case. This was followed, in 2012, by a scheme requiring all providers to obtain approval from the public authorities indicating that they comply with minimum wage rates and regulations governing other conditions. Denmark continues to rely on voluntary collective bargaining to establish minimum wages, even though coverage has declined. Measures have however been taken to bolster enforcement, including a 2004 protocol (subsequently strengthened) requiring cleaning companies to engage subcontractors at a price that reflects the costs of honouring the collective agreement. In the UK, only pockets of the sector are covered by CWB. The wage floor is set by the statutory national minimum wage. A sector-specific development is the sustained campaign, dating from the early 2000s, by trade unions and community organisations aimed at persuading large client organisations to stipulate the payment of a living wage, above the statutory minimum, which has met with some success.

The overall picture suggests a divergent policy trajectory as between Denmark and Norway, and some commonality in trajectory between Norway and Germany. In terms of process, the invocation of statutory support (in the form of extension) to augment associational governance in Norway represents a shift in trajectory, away from Denmark and towards Germany. The UK’s policy and process trajectories remain different from those of the other three countries.

Temporary agency work (TAW)

The cyclically sensitive agency work industry is characterised by high mobility of labour supplied, the triangular relationship between agency, employee and hiring company, and by the superior position of the latter. These features have impeded collective organisation, especially amongst employees. Although the agencies’ product market is mostly territorially bounded, important client firms competing in international markets exert pressures on agency labour costs. Added to by cross-border movements of agencies and lower-cost labour after eastward enlargement, price competition and pressures on labour costs were further intensified by the financial crisis which hit some key user industries hard. While these structural characteristics have hampered employer and trade union collective action and wage regulation efforts, the implementation of the EU’s 2008 Temporary Agency Workers’ Directive, stipulating equal treatment, gave renewed impetus to regulation in the aftermath of the financial crisis.

The principal challenge for CWB again concerns the regulation of wage floors. Responses differ across countries. In Germany and Sweden, where the organised actors proactively established sectoral collective agreements in the early 2000s (prior to enlargement), subsequent changes have entailed extension of minimum terms in the former and minor adaptations in the latter. The German sector was partly also protected by Germany’s strict transitional arrangements concerning labour migration, which lasted until 2011, and the ban on TAWs for manual labour in construction. The unregulated Norwegian agency industry, by contrast, became a major channel for provision of cheap migrant labour in construction and shipyards. When the social partners were eventually prodded to react by the EU Directive, this resulted in TAW workers becoming partially protected through entitlement to basic terms in user firm collective agreements and extended user industry agreements 2 . This effectively prevented institutionalisation of CWB in the sector itself. In the UK, the Directive prompted tripartite dialogue on statutory regulation, but the central principle of equal treatment has been subverted by widespread (mis)use of the so-called ‘Swedish derogation’ (Alsos and Evans, 2018: 400) thereby allowing low-cost competition to persist.

Although facing similar challenges, different strategic choices, or non-decisions, made by the countries’ employers and unions in the sector’s formative phase have implied that the regulation of wages and conditions has followed very different paths. While the social partners in Sweden and Germany entered the path of collective regulation before the eastward enlargement, though at different minimum wage levels, the laissez-faire approaches of the British and Norwegian actors implied that the sector largely remained without collective wage floors. In sum, TAW displays significant policy divergence between, respectively, Germany and Sweden and the UK, with Norway in between. In terms of process, Sweden stands out with its encompassing, purely associational wage determination and is in sharp contrast with British reliance on employer-driven, market-based wage setting above the statutory minimum wage. Germany and, more recently, Norway are distinguished from these polar cases by the evolving interplay of associational and statutory regulation.

Outcomes: development of wage dispersion

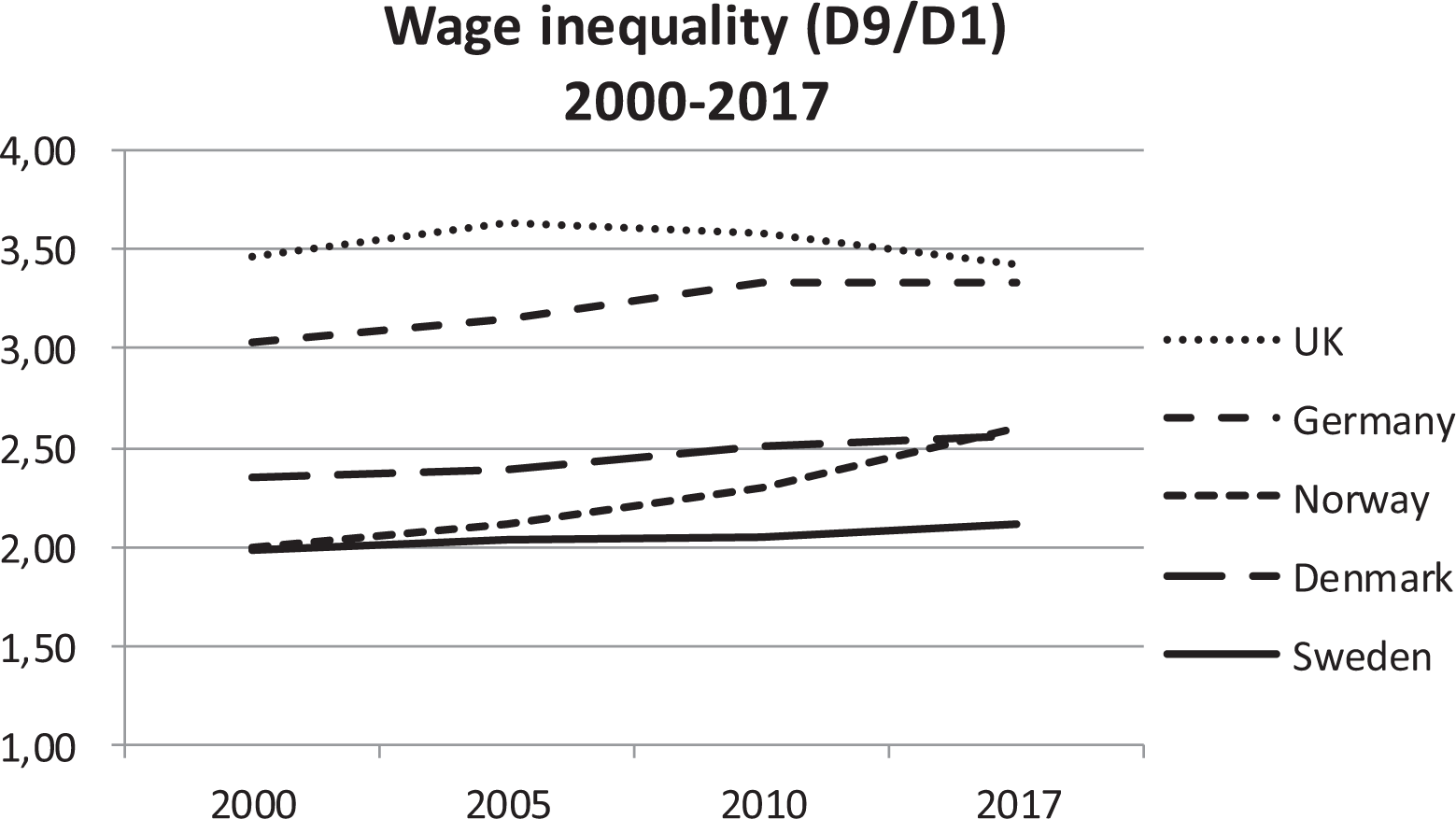

In order to provide some assessment of convergence and divergence in outcomes we examine developments in wage dispersion at cross-sector level. Figure 1 presents developments in overall wage dispersion, as measured by the relative difference between the ninth (D9) and first (D1) deciles of the wage distribution for the period from 2000 to 2017 3 .

Development of wage dispersion 2000–2017: decile 9/decile1.

The development of D9/D1 shows noticeable differences between countries. Already high in the UK in 2000, it remained largely unchanged until registering a small recent decline. At the other end of the spectrum, wage dispersion was lowest in Sweden and has remained remarkably stable. Germany had the second highest overall wage dispersion in 2000, and this has steadily increased. Wage dispersion in 2000 in the other two Scandinavian countries was noticeably lower than in Germany and remained so in 2017, although it increased in both over the period. Whereas these increases were small in Denmark, in Norway it was rather larger. Concerning trend, Sweden and the UK exhibit similarity (little change) but at very different levels of wage dispersion. The other three countries all show an increasing trend, but the rate of increase differs markedly. Shifting the lens to end-points, Germany has converged on the UK and diverged away from Sweden. The other two Scandinavian countries have diverged somewhat from Sweden, and converged on a similar position to each other, but remain some distance from Germany and the UK.

Interpretation of the results differs according to whether convergence-divergence is viewed through the lens of trend or end-point. There is support for Baccaro and Howell’s thesis of a common liberalising trajectory in the cases of Germany and also Norway, much less so for Denmark, and hardly at all for Sweden. Taking their proposition as movement towards a common end-point, as represented by the UK, a similar conclusion emerges. Amongst the Scandinavian countries differences in both trajectory and end-point are apparent, with those in Sweden and Norway contrasting the most sharply with each other. Whether a liberalising trajectory is common is questionable.

Discussion

We compare across sectors and across countries identifying meta patterns which reach across some sectors but are not shared by others and, in similar vein, are common to some countries but do not extend to others. In doing so we underline the insights that flow from differentiating between different types of convergence-divergence (Hay, 2000), from a comparative analytical frame that is across sectors as well as across countries (Katz and Darbishire, 2000), and from distinguishing trajectory and end-point (Jacoby, 2005).

There is an evident contrast between export-oriented manufacturing and the more domestic-oriented construction, cleaning and TAW sectors. In manufacturing, the imperative of competitiveness in international markets has hitherto given rise to cross-class coalitions between employers and trade unions to secure a wage leadership role through bargaining coordination mechanisms across sectors, along with employer pressure for greater scope for negotiation at company level in order to address business contingencies. Until recently the anchored nature of the other three sectors has provided protection for their comparatively less well-organised employers and trade unions from low-wage international competition. The two major political-economic challenges of EU eastern enlargement and the crisis have affected the two sets of sectors very differently, highlighting salient input divergence.

For manufacturing, the opportunities for eastwards relocation of lower value-added elements of production and the impact of the crisis on demand represent further twists to long-running pressure to sustain cost competitiveness in European and international markets. The response of employers and trade unions amongst the Scandinavians has been to recalibrate (Sweden, Norway) or maintain (Denmark) mechanisms of bargaining coordination to (re)secure wage leadership, by establishing an upper mark for wage increases, amounting to policy convergence. Germany remains somewhat apart, having no formal cross-sector coordination mechanism: although maintenance of the convoy principle under which metalworking informally exercises wage leadership has had a similar effect. In parallel, organised decentralisation, under which scope for company-level negotiations is opened up within the framework of the sector agreement, is now the basis for articulation between levels in all four coordinated market economy (CME) countries, albeit with important differences – hence some policy divergence. In Denmark wage negotiations are decentralised with the sector negotiation setting a reference point only, the agreements in Norway and Sweden provide for extensive second-tier negotiation but with minimal scope for derogation. In contrast, possibilities for derogation are extensive in Germany. In the UK, these institutional features – coordination aimed at wage leadership and organised decentralisation – barely featured before the demise of sectoral bargaining in the 1990s. None of the four other countries have sought to emulate the UK by dismantling multi-employer CWB arrangements in favour of disorganised decentralisation and market-based wage determination. Process divergence persists.

Amongst the three territorially anchored sectors, EU eastern enlargement has opened up their domestic markets to low-cost competition through unprecedented flows of low-wage, migrant labour and – in construction – posting of workers on lower wages from CEE countries. Given that labour costs represent a major element of total costs, these inflows of labour threatened the market position and interests of existing employers and trade unions organising their workforces, and hence their organisational basis. The slump (construction) or stagnation (cleaning and TAW) in demand triggered by the crisis intensified these destabilising competitive pressures within domestic markets. As between them, the potential benefits of stronger interest organisation and more widespread CWB coverage in construction compared to the other two sectors have been offset by the compounding effects of posting in addition to labour migration. Despite some input divergence similar policy responses, within if not across countries, are apparent (Hay, 2000).

The main response of employers and trade unions in the CME countries has been to reinforce ‘internal protections’ in domestic labour markets against these destabilising competitive pressures, by measures to re-regulate wage floors – entailing overall policy convergence. This has been done in different ways, at the same time entailing some divergence, through the use of extension mechanisms flanked by other statutory support measures in Germany and Norway, but by joint measures to shore up autonomous CWB in Denmark and in TAW in Sweden. (The latter contrasts with Swedish construction, where employers have opposed union, and government, initiatives to facilitate extension of wage floors to posted workers following the Laval case.) The result is also some divergence in process as associational governance has become underpinned by statutory regulation in two countries. The UK, by contrast, has been marked by the absence of joint initiatives to re-regulate wage floors in these sectors. Reliance has been placed on uprating the national, statutory minimum wage and improving enforcement in order to curb the worst excesses of market-driven wage determination. Policy and process divergence persist.

Furthermore, these initiatives in the territorially anchored sectors have sparked tensions amongst organised employers, and also trade unions, from other sectors, notably those in manufacturing. Pressure from employers’ organisations and trade unions in the construction and cleaning sectors in Germany and Norway on the public authorities for action to invoke and/or broaden the purchase of (pre-existing) extension arrangements have met with resistance from manufacturing employers, with the former eventually prevailing. In Denmark, manufacturing employers vigorously asserted the virtues of autonomous collective bargaining in anticipation of any similar initiative from the bargaining parties in anchored sectors. The German and Norwegian cases highlight the (relative) success of collective action and of coalition building to secure political support by sectoral interest organisations traditionally regarded as being less well-placed to do so than their manufacturing counterparts. The costs of not doing so are indirectly illustrated by the experience of TAW in Norway. Here, employers pursued a strategy of avoiding establishing CWB arrangements for the sector. When, in light of the EU’s TAW Directive and trade union pressure they subsequently reconsidered, the route to doing so was closed off by manufacturing employers which insisted on the primacy of collective agreements concluded with user companies. The contrasting cases and varying outcomes underline two things. In the face of destabilising pressures, and the associated tendency towards disorganisation and market regulation, any revival in collective action and organisation is best regarded as, following Polanyi (2001), a countervailing tendency and not as a pre-determined outcome. Relatedly, any liberalising trajectory (Baccaro and Howell, 2017) is far from linear in nature.

A further implication of our findings is that Katz and Darbishire’s (2000) ‘converging divergences’ proposition – that sectors are becoming more similar across countries whilst within countries sectors are growing apart – needs qualification. The proposition stands up well for manufacturing in the four CMEs, in respect of bargaining coordination and articulation between levels, although it does not extend to the UK. On re-regulation of wage floors, however, the construction and cleaning sectors in our CMEs differ over whether or not extension has been mobilised, while in TAW different regulatory approaches to establishing a wage floor characterise each CME. Again the UK stands apart. The pattern confirms Bechter et al.’s (2012) finding that converging divergences are more apparent in internationalised sectors, such as manufacturing, but less so or not at all in sectors oriented towards domestic markets.

The salience of Jacoby’s (2005) distinction between convergence-divergence of trajectory and of end-point is best illustrated by our analysis of outcomes in terms of wage inequality. Over the period since 2000 wage inequality has changed little in the two polar cases of Sweden and the UK: they exhibit a common, largely flat trajectory. But the respective end-points in 2017 remain starkly different. Bringing Denmark, Norway and Germany into the picture, each exhibits a trend of increased wage inequality, but at differing rates. At the end of the period Germany was further apart from Denmark than it was in 2000, whilst Norway had become closer to the latter.

The findings on wage inequality, although limited to a cross-sector comparison, have the most telling implications for Baccaro and Howell’s (2017) thesis of a common liberalising trajectory. Given their emphasis on the plasticity of institutions, including those governing CWB, the policy and process divergence that we have found between the two sets of sectors, and amongst the countries, could be dismissed as masking functionally equivalent changes shaping the wage outcomes delivered by different governance arrangements. This plasticity proposition does not, however, survive a confrontation with the data on wage inequality. The position of Germany has indeed converged on that of the UK, but there is considerable disparity amongst the three Scandinavian countries ranging from some movement towards the UK in Norway, to Sweden which remains almost as far away from the UK as at the start of the period. Thelen (2014) identified similar differences in developments in social solidarity as between Germany and Sweden.

Conclusion

Our sectoral analysis of developments in CWB arrangements in five northern European countries undermines the proposition that recent developments exhibit a common liberalising trajectory (Baccaro and Howell, 2017). It indicates the very different impact that the two major political-economic challenges since 2000 have had as between sectors, or input divergence. It highlights the differing policy responses to similar input conditions within a given sector across countries, and the differing consequences for the nature of CWB governance – entailing process divergence. Should it be argued that these sectoral, policy and governance divergences are masking underlying similarities in outcome, as Baccaro and Howell claim, then our analysis of outcomes refutes this.

The somewhat surprising result of comparing internationalised manufacturing with the more territorially anchored construction, cleaning and TAW sectors is that it is in the latter, where collective organisation and CWB are supposedly most threatened (construction) or are historically weak (cleaning) or only recently established (TAW) and external pressures most destabilising, that a revival of collective action and coalition building between employers and trade unions is in several instances apparent. The main aim is to re-regulate wage floors, in some countries by also securing support from the state, in order to stem the destabilising effects of low-wage competition introduced into hitherto closed domestic labour markets via the substantial inflows of migrant labour and, in construction, posted labour unleashed by EU eastern enlargement.

The opening of northern European labour markets to internationalised low-wage competition has paradoxically prompted a countervailing tendency among employers and trade unions in these hitherto relatively protected sectors to embark on collective action in an effort to secure domestic re-regulation. The threat of disorganisation, de-collectivisation and resultant employer-driven market regulation in these territorially anchored sectors nonetheless remains strong. The countervailing tendency, moreover, is contested by organised employers in the manufacturing sector, who see competitive advantage deriving from low-wage competition in input sectors that are territorially anchored. How this tension plays out varies across countries.

By distinguishing between different dimensions of wage regulation, our approach echoes that of Thelen (2014) in fruitfully differentiating between the dimensions of bargaining coordination and social solidarity. Regulation of wage floors has been relatively neglected in debates on the recent evolution of CWB (e.g. Brandl and Bechter, 2019; Visser, 2016b) and treated separately in work analysing minimum wage regulation (e.g. Grimshaw, 2013). Integrating the regulation of wage floors within our analysis has enabled us to highlight that territorially anchored sectors are not, as much of the literature holds, merely passive followers of internationally exposed manufacturing but important players in efforts to revive collective action.

Footnotes

Acknowledgements

We are grateful to Kristin Alsos, Jens Arnholtz, Guglielmo Meardi, Torsten Müller and Sissel Trygstad for coordinating the sector studies on which we draw.

Funding

This article derives from a module within the ‘Euro-strain’ project headed by ESOP, University of Oslo, funded by the Research Council of Norway programme ‘Europe in Transition’.