Abstract

The digital euro might be adopted as early as 2026 – a momentous decision, with profound societal consequences. And yet, little attention has been paid to the European Central Bank (ECB)'s accountability in the process of adoption and beyond. This article attempts to fill this void. It argues that the concept of ‘independent accountability’, still prevalent regarding monetary policy, is an inappropriate standard to hold the ECB accountable for its decisions on the digital euro for at least three reasons. First, while the ECB has the power to issue a digital euro with cash-like features, its mandate is not clear-cut, nor are its decisions merely technical in nature. Second, the digital euro affects areas in which the ECB has no specific expertise or authority, such as privacy, and its adoption requires an unprecedented level of coordination with the EU legislators. And third, it is not only public authorities with which the ECB must engage, but also market actors and citizens to ensure the digital euro's success. What emerges is a new accountability standard, with a broader range of ‘accountability stakeholders’ and a stronger role for ex ante consultations.

Keywords

Introduction

The European Central Bank (ECB)'s independence and accountability have given rise to numerous academic studies 1 and repeated policy discussions. 2 In the then prevailing monetarist spirit, the Maastricht Treaty granted the ECB an unparalleled level of independence, giving it the reputation of ‘the most independent central bank in the world’. 3 This means that the ECB fulfills its monetary policy tasks and makes use of its powers in full autonomy and without instructions from any external body. 4 Accountability was designed to support the ECB's far-reaching independence, rather than as a real counterbalance to it. It was thought that accountability could be limited to the ECB explaining and justifying ex post the actions or decisions taken in the exercise of its tasks. The Treaties gave the European Parliament the role of the ECB's main accountability forum, albeit with limited means to genuinely engage with the ECB on its monetary policy.

Since the global financial crisis, this asymmetry between independence and accountability – the ‘two sides of the same coin’ 5 – has grown further. The ECB has interpreted its monetary mandate much more broadly than anticipated at the time of the drafting of the Maastricht Treaty, taking on new tasks, pursuing new objectives and using additional instruments to attain these objectives. 6 While the 2021 strategy review formalized these developments, 7 the accountability arrangements of the ECB remain largely limited to the old Maastricht paradigm. 8

The aim of this article is not to discuss the appropriateness of these accountability arrangements for monetary policy, to which they are geared. Instead, the article will turn to a new phenomenon – the digital euro – whose implications for the ECB's accountability have not been studied to date. Since October 2021, the ECB has been investigating the introduction of a digital euro as a complement to cash that would allow citizens in the euro area to use public money, i.e., money issued by the central bank, also in digital form. 9 In four progress reports of September 2022, December 2022, April 2023 and July 2023, the ECB has put forward a wide set of foundational design choices for the digital euro, ranging from means to control its use to its distribution and potential privacy features. 10 On 28 June 2023, the Commission published a proposal for a Regulation on the establishment of the digital euro, kicking off the discussion on the necessary legislative amendments for the digital euro's introduction. 11 In parallel, the ECB's Governing Council decided on 18 October 2023 to start the digital euro preparation phase, including the development and testing of the necessary technical and business solutions. 12

Whatever its ultimate design, the decision to introduce a digital euro (or not 13 ) will have profound societal consequences. A digital euro would give citizens access to public money to pay digitally (something that cash does not provide for). Banks and other financial intermediaries would see themselves in new roles distributing the digital euro on behalf of the ECB, while facing competition from the digital euro regarding their own services. More broadly, the digital euro would help strengthen the role of the euro internationally and reduce the EU's dependence on payment infrastructures by non-European providers.

While, as this article will argue, the ECB has the power to issue the digital euro, it cannot act on its own. The ECB must coordinate its decisions to an unprecedented extent with the EU's legislators, assess the feasibility of digital euro design features with relevant market participants and consult with the ultimate users of the digital euro on their expectations and needs. The success of the digital euro, and thus the ability of the ECB to deliver on its mandate, depends on whether the digital euro is taken up by users to make and receive payments. The risk of being rejected by the market is a ‘radically new situation’ 14 and a difficult tightrope exercise to navigate for an independent central bank. After all, the ECB was granted far-reaching independence for monetary policy under the assumption that this would allow the central bank to take decisions that are unpopular at times, but necessary to maintain price stability. Going against the mainstream constitutes a virtue in monetary policy-making. In contrast, public opinion is the key success factor regarding the digital euro, whose failure would inflict huge reputational damage on the ECB.

This article seeks to identify what this implies for the ECB's accountability. It proceeds as follows. Section 2 revisits the concept of ‘independent accountability’ in monetary policy and discusses why it is inappropriate with regard to the digital euro. Section 3 turns to discussing a key reason for the inappropriateness of the concept of ‘independent accountability’ – the lack of a clear-cut mandate for the adoption of the digital euro. The counterbalancing role of the co-legislators is addressed in section 4. Section 5 explores the ECB's engagement with different stakeholders in the process of preparing for the digital euro's adoption. Section 6 concludes.

Revisiting ECB accountability in the context of the digital euro

Even the fiercest proponents of independent central banks acknowledge the need for the ECB to remain accountable to democratically elected politicians and, ultimately, the citizens of the euro area. The Treaties grant the ECB far-reaching institutional, 15 personal, 16 functional 17 and financial independence, 18 shielding it from instructions by any public or private third party. Limited accountability arrangements were meant to counterbalance this far-reaching independence to some degree. ECB acts are subject to judicial review by the Court of Justice of the European Union (CJEU) 19 and the European Parliament was assigned the role of the ECB's primary accountability forum, albeit without any powers to sanction the ECB in case it failed to deliver on its mandate.

The concept of ‘independent accountability’

In the OLAF case, the CJEU rejected the view that the ECB's independence separated the central bank entirely from other EU institutions and bodies. Instead, the Court held, Article 130 TFEU intends to shield the ECB only from influence that undermines its ability to pursue its objectives effectively. 20 In line with the prevailing view at the time of its establishment that effective monetary policy requires a large degree of insulation from politics, 21 the ECB has interpreted its democratic accountability narrowly to mean that it has to explain ex post the decisions it has made. Under the concept of ‘independent accountability’, the inflation target – defined by the ECB – was thought to be an objective standard by which the ECB's actions could be evaluated. ‘Independent accountability’ assumed that the ECB's tasks are fundamentally technical in nature and clearly and narrowly defined, leaving it with little discretion. In that logic, it is primarily the ECB's clear and narrow Treaty mandate that ensures its democratic legitimacy, justifying that accountability arrangements were kept to a minimum. However, in light of the fundamental changes that monetary policy has undergone since the global financial crisis, the rationale for ‘independent accountability’ has become less clear-cut. 22

According to Article 284(3) TFEU, 23 the European Parliament has two broad instruments to hold the ECB to account. The first instrument relates to the ECB's annual report on the activities of the European System of Central Bank (ESCB) and on the monetary policy of both the previous and current year, addressed to the European Parliament, the Council, the Commission and the European Council. The ECB President presents this report to the Council and to the European Parliament, which may hold a general debate on that basis. According to conventional practice, the ECB Vice-President presents the annual report also to the ECON Committee in a dedicated session. Moreover, in 2016, the ECB started the convention of responding to the European Parliament's resolution on its annual report by giving a ‘feedback statement’. The second instrument is known as ‘monetary dialogue’. The ECB President and the other members of the Executive Board may, at the request of the European Parliament or on their own initiative, be heard by the ECON Committee. Verbatim reports of these hearings are made available to the public. In early 2000, conventional practice added another important line of communication between the ECB and the European Parliament to the obligations enshrined in Article 284(3) TFEU. Members of Parliament (MEPs) now regularly address written questions to the ECB, answered by the ECB in a formal letter signed by its President. 24

According to Article 284(1) TFEU, the President of the Council and a Member of the Commission may participate as observers in meetings of the ECB's Governing Council. The President of the Council may even submit a motion for deliberation to the Governing Council. The European Parliament is not given such observer status. 25

The accountability framework is crucially supported by information that the ECB makes available to the public via different information channels. In addition to the annual report, the ECB publishes eight times a year its Economic Bulletin, containing the economic and monetary analysis that informed the Governing Council's policy decisions, 26 as well as a weekly financial statement of the Eurosystem, providing information on monetary policy, foreign exchange operations and investment activities. 27 The ECB also informs the public through press conferences after monetary policy meetings, the accounts of these meetings, 28 occasional papers, interviews and speeches, published on its website, as well as – more recently – blog posts by ECB staff and Executive Board members 29 and an active use of social media by the ECB and some of its (top) representatives.

Digital euro: Mind the gap!

The digital euro has featured in many but not all of these accountability and transparency channels. In its annual reports of 2020, 2021 and 2022, 30 the ECB summarized its investigations into the design of a digital euro as part of its reporting on its task to promote the smooth operation of payment systems. 31 The European Parliament's resolutions on these annual reports generally welcomed and engaged with the ECB's work on the digital euro. The resolution on the 2020 annual report supported, in particular, the ECB's recommendation that the digital euro be accessible outside the euro area to promote the international role of the euro. 32 In the resolution on the 2021 annual report, the European Parliament stressed the need for the ECB ‘to effectively address the expectations and concerns raised during the public consultation on a digital euro’ 33 and requested that the ECB ‘closely align and regularly exchange with Parliament on the progress made during the investigation phase’. 34 The resolution on the ECB's 2022 annual report highlighted the European Parliament's concern regarding the digital euro's potential replacement of cash, the risks it may entail for the banking sector and overall lending to the real economy as well as the involvement of Amazon as a non-European big tech company in testing prototype interfaces for a digital euro. 35 In its feedback statements, the ECB responded to the points and concerns raised by the European Parliament. 36

Moreover, engagement of the ECB with the European Parliament on the digital euro has been strong through ‘monetary dialogue’. While MEPs only occasionally raised questions on the digital euro during the hearings with ECB President Christine Lagarde, 37 former ECB Executive Board Member Fabio Panetta held quarterly hearings with the ECON Committee dedicated entirely to the digital euro project. 38 More recently, these quarterly hearings were preceded by the publication of four ECB progress reports on the digital euro. 39 Regular exchanges also took place between ECB representatives and the Eurogroup. 40

While the interest of MEPs to raise written questions on the digital euro has been limited so far, Mr. Panetta has addressed several public letters on the digital euro to ECON Committee Chair Irene Tinagli. 41 Further publications and speeches by ECB staff and Executive Board members have given insights into the ECB's progress with the investigation phase and the analysis underpinning it. Several blog posts by Executive Board members have highlighted the ECB's work and thinking on the digital euro. 42

It is commendable that the ‘conventional’ accountability arrangements have been used rather extensively by the ECB to explain to the European Parliament, the Eurogroup and the public the views it has on the digital euro's objectives and the steps it has taken in determining its design. However, the novelty of the digital euro and the large societal impact it would undoubtedly have 43 raise the fundamental question of whether these arrangements are appropriate and sufficient regarding the digital euro. For several reasons, the concept of ‘independent accountability’ is not an ideal fit. A first reason is that the digital euro affects issues for which the ECB has no specific expertise or authority. The privacy features of the digital euro, i.e., the extent to which user and transaction data would be transparent to the ECB and/or the intermediaries distributing the digital euro, represents a prime example. The legal framework in which the digital euro would be embedded first has to be created, and the adoption of at least parts of that framework falls within the competence of the EU legislators. This requires a level of coordination between the ECB and the EU legislators that is unprecedented so far.

A second reason relates to the fact that the success of the digital euro crucially depends on its uptake by citizens and merchants as well as the ability (and willingness) of intermediaries to distribute it. Like in the case of banknotes, it is envisaged that the ECB be protected by a monopoly when issuing the digital euro. 44 However, with the digital euro, the ECB would offer a means of payment that competes 45 with other, well-established digital means of payment provided by private intermediaries, such as cards, online platforms or payment apps. 46 This market environment is new territory for the ECB.

The third reason is that the Treaties do not contain an express legal basis for the digital euro. As discussed above, the limitation of the ECB's accountability to explaining ex post why it has taken decisions and with what means it pursues its objectives was based on the assumption that the ECB's monetary mandate was clear and limited to largely technical decisions. This assumption does not hold with regard to the digital euro. The next section will set out why.

A clear and limited mandate for the digital euro?

Both the ECB and the EU legislators, within their respective competences, would be involved in the digital euro's introduction. The ECB would be in charge of issuing the digital euro and establishing an infrastructure or ‘scheme’ for its distribution (B.). The legislators’ task, on the other hand, is to adopt an ‘enabling framework’ that embeds the digital euro in the broader EU legal framework. Regarding certain key design features, the EU legislators have an important counterbalancing role to the ECB's broad powers (C.). Before addressing these spheres of competence in turn, the following subsection (A.) clarifies what the digital euro is.

What is the digital euro?

The Commission proposal for a regulation on the establishment of the digital euro published in June 2023, together with the first four ECB progress reports, give a good preliminary picture of the basic features and objectives of the digital euro. Complementing tangible cash, the digital euro would provide an alternative, digital access to central bank money to the public. As a liability of the ECB/National Central Banks (NCBs), 47 the digital euro would represent a risk-free and trusted means of payment. Unlike money deposited with commercial banks, digital euro accounts would not be subject to the risk that the issuer (the ECB) or the intermediary administering them (e.g., a commercial bank) fails. 48 Convertibility at par with the money issued by commercial banks 49 and with cash 50 would ensure that one euro is worth one euro – whether in digital euro, coins or in a commercial bank account.

The digital euro is thus a new digital emanation of the existing currency. The Commission proposes that the digital euro – like banknotes and coins 51 – be given legal tender status, entailing its mandatory acceptance, at full face value, with the power to discharge from a payment obligation. 52 In other words, payees must accept payments in digital euro, subject to certain limited exceptions, 53 and no fees must be charged on basic digital euro payments. The obligation to accept the digital euro respects the contractual freedom of parties, as payee and payer may expressly agree on a different means of payment prior to the payment. 54

However, despite its public nature, end users of the digital euro – people, businesses and public authorities – would not maintain a contractual relationship or accounts with the ECB. Their access to the digital euro would be intermediated through payment service providers (PSPs) within the scope of the payment services directive, 55 including banks, e-money institutions and payment institutions. 56 These PSPs would manage the digital euro user accounts, including anti-money laundering (AML)-related checks, and provide users with front-end digital euro payment services. The ECB's role would be confined to the issuance of the digital euro and to providing a back-end infrastructure, including for recording and verifying all settlements of digital euros. The ECB would also manage the supervised intermediaries by setting up a granular ‘rulebook’ for their participation in the digital euro scheme, similar to the rules it has adopted regarding the trans-European automated real-time gross settlement express transfer (TARGET2) system. 57

End users could access and use the digital euro either through the PSPs’ online banking/payment apps or through a digital euro app provided by the ECB. 58 To ensure universal access to basic digital euro payment services, 59 all banks providing payment account services would be legally required to also provide basic digital euro payment services upon request of their clients. 60 For them, the distribution of the digital euro would thus be mandatory.

Both the ECB and the Commission have assigned great importance to the privacy and data protection aspects of the digital euro and have indicated that the processing of user data should be minimized. According to the Commission proposal, users should be able to make and receive digital euro payments both online and offline, 61 with different implications for privacy. 62 The claim is that the level of privacy in digital euro offline payments would be similar to that of payments in cash. The ECB and PSPs would not have access to user data, except related to the funding and defunding, i.e., the depositing and withdrawing of money on a device such as mobile phones. 63 The level of privacy in digital euro online payments, on the other hand, is envisaged to be comparable to that of other online payments. PSPs would have access to a broad range of user information, arguably in order to comply with regulatory requirements, including those related to sanctions screening and AML. 64

Another key feature of the digital euro that has given rise to much discussion is that its use as a store of value would be limited. Early on, the ECB had embraced the fear by commercial banks that the availability of the digital euro would lead to large and rapid outflows of bank deposits into the safety of the digital euro, both structurally and – even more so – in times of crisis. 65 Its mandate, both as the euro area's monetary policy authority and banking supervisor, requires the ECB to take these concerns seriously. Article 16 of the Commission proposal gives the ECB broad powers to develop instruments to limit holdings of digital euros by users, while determining that paying or charging interest on digital euro holdings must not serve as such instrument. 66 In an earlier speech, former ECB Executive Board member Fabio Panetta indicated that the ECB is contemplating holding limits as low as EUR 3,000 to 4,000 per person 67 to mitigate negative effects for the financial system and monetary policy. 68 That limit has been criticized as prohibitively low, especially in the longer term. 69 Whatever their ultimate level, however, holding limits would not affect users’ ability to make and receive payments with a higher value. The ECB proposes that funds could be transferred automatically from and to users’ commercial bank accounts through a discretionary ‘(reverse) waterfall functionality’. 70

ECB powers regarding digital euro issuance and infrastructure

With Article 127 TFEU, the ECB was assigned the primary objective of price stability and given a number of basic tasks to fulfill that objective, including the definition and implementation of monetary policy as well as the promotion of the smooth operation of payment and settlement systems. Articles 17–22 ESCB Statute contain a broad set of instruments that the ECB may deploy to fulfill its tasks. Moreover, according to Article 128 TFEU and Article 16 ESCB Statute, the ECB has the exclusive right to authorize the issuance of euro banknotes. None of these tasks and instruments were drafted with the digital euro in mind, but in the spirit of providing the ECB with a legal foundation that was open and adaptive to the dynamic monetary and economic developments.

The ECB has always held that the concrete design choices and pursued objectives would determine the legal basis for the digital euro. 71 If designed as a functional equivalent of euro banknotes, the digital euro could be issued based on Article 128(1) TFEU and Article 16 ESCB Statute. 72 Banknotes supply citizens with easy, cheap and trusted public money. They also provide an anchor for private monies by enabling users to convert these monies into public money at par value. The medium with which these functions are fulfilled – paper or a digital record – is of secondary relevance.

The monetary anchor function of the digital euro is a stated objective of the authorities. 73 Moreover, although its use as a store of value would be limited (at least initially) due to financial stability concerns, the digital euro would, together with cash, provide euro area citizens with the possibility to pay with and hold public money. Article 128(1) TFEU and Article 16 ESCB Statute thus appear to be an appropriate legal basis for the digital euro's issuance. 74 This implies that it is for the ECB to independently decide whether and when it issues the digital euro. Subject to the requirement that it demonstrates sufficient need for the digital euro's introduction in light of its mandate and the proportionality of the measure, the ECB does not need the approval from the EU legislators or any other body to do so. 75

However, the digital euro not only needs to be issued; it also needs to be distributed and, unlike cash, it needs an elaborate infrastructure for payments in digital euros to be settled. Such a ‘digital euro scheme’ will require a governance structure as well as a set of rules and standards applicable to all participants in the scheme (a ‘rulebook’). 76 While the ECB has given little details on the precise modalities of the distribution, 77 setting up this infrastructure for the digital euro clearly relates to its powers regarding payment and settlement systems. According to Article 127(2), fourth indent, TFEU, the ECB is tasked with ensuring the smooth operation of payment systems, and Article 22 ESCB Statute gives the ECB broad powers to ‘provide facilities’ and ‘make regulations’ to fulfill this task. On this basis, the ECB may oversee payment and settlement systems but also operate its own systems, such as TARGET2.

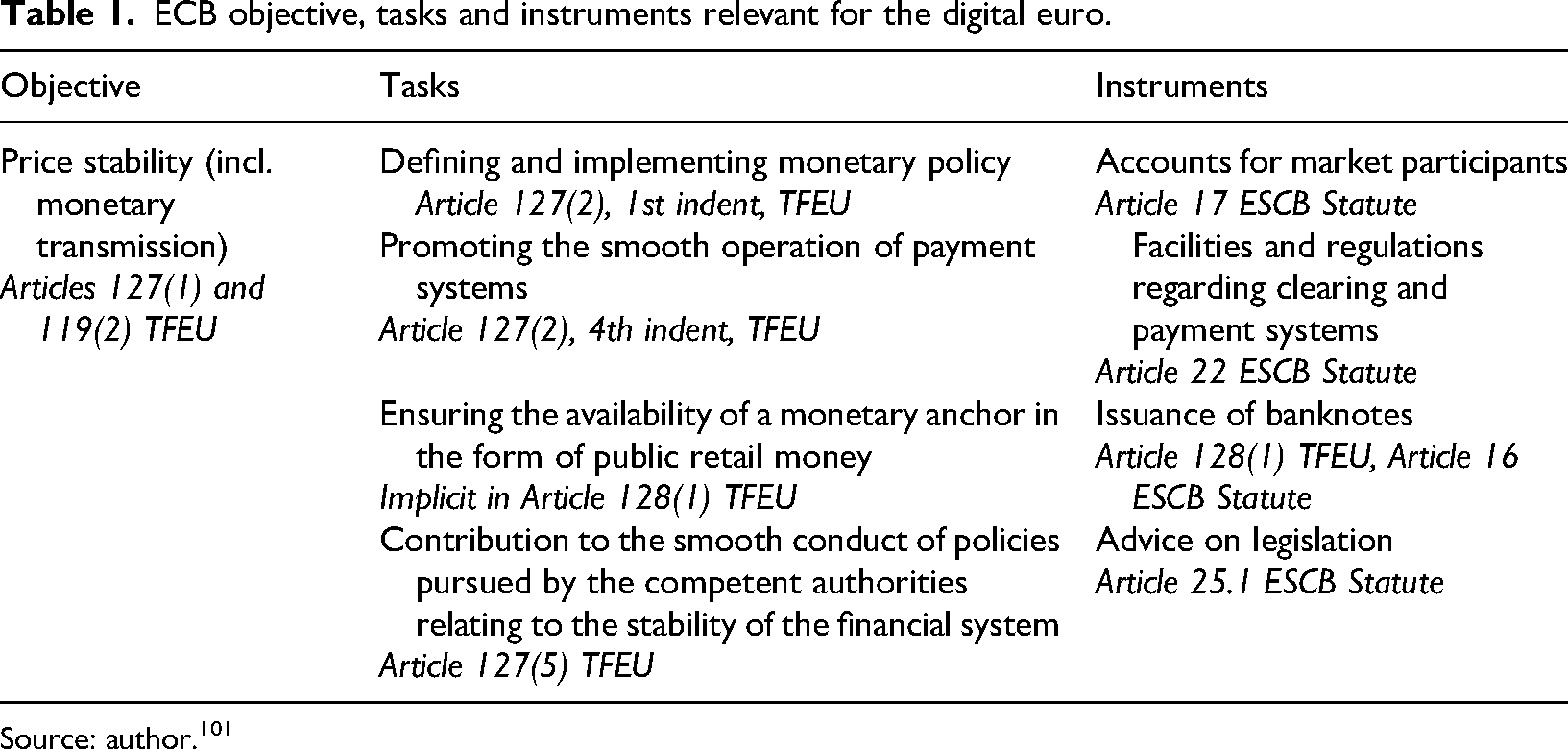

When introducing the digital euro, the ECB would thus rely on a combination of several legal bases: Article 128(1) TFEU could serve as a legal basis for the issuance of the digital euro, while Article 127(2), fourth indent, TFEU as well as Article 22 ESCB Statute provide a legal basis for the establishment of the supporting digital euro infrastructure. Additional legal provisions may need to be invoked, depending on the ultimate design of the distribution mechanism. 78 It would not be the first time for the ECB to rely on several different legal bases when taking a specific measure. 79 The novelty is that the digital euro combines the ECB's basic tasks according to Article 127(2) TFEU with its banknote issuance power according to Article 128(1) TFEU and Article 16 ESCB Statute (see Table 1).

ECB objective, tasks and instruments relevant for the digital euro.

ECB objective, tasks and instruments relevant for the digital euro.

Source: author. 101

A combined application of several legal bases might also be backed by the jurisprudence of the CJEU. If an EU measure pursues several objectives or has several components, the Court adheres to a ‘centre of gravity’ theory, allowing for a cumulation of different legal bases by giving precedent to one legal basis over the merely incidental other legal bases. 80 In exceptional circumstances, the Court permits for a measure to be founded on several legal bases that ‘are inseparably linked without one's being incidental to the other’. 81 Accordingly, if no single centre of gravity can be identified, acts of the Union, including those of the ECB, may be adopted on a dual (or multiple) legal basis, even if this involves a combination of disparate (but not incompatible) procedures. 82

Whether the CJEU would follow this line of reasoning with respect to the digital euro remains to be seen. For the purposes of this article suffice it to conclude that the ECB's mandate regarding the digital euro is not clear-cut but dispersed across a number of tasks and instruments assigned to it by the Treaties. Unlike with monetary policy, where its functional independence requires the ECB to have all the instruments it needs to fulfill its mandate, the ECB depends in its role as issuer of the digital euro on action taken by the EU legislators.

On the basis of Article 133 TFEU, the Commission on 28 June 2023 presented its proposal for a regulation on the establishment of the digital euro. While one may question whether the digital euro needs ‘establishment’ by the EU legislators, the CJEU has acknowledged that there is a regulatory dimension to monetary policy, ‘intended to guarantee the status of the euro as the single currency’. 83 It is a challenging balancing act for the EU legislators to fulfill this regulatory role without unduly interfering with the independence the ECB enjoys when exercising its tasks.

Instead of exploring that balancing act in abstracto, this article briefly illustrates two key areas of legislative concern: privacy and financial stability. Both issues are instrumental for the digital euro's success, but not within the ECB's primary or sole responsibility. They also have a large societal impact, affecting individual rights of citizens and commercial banks.

An inappropriate design of the digital euro and the infrastructure supporting it could give rise to significant data protection risks. A public consultation by the ECB revealed a strong preference by stakeholders and citizens for a high level of privacy of payment data. 84 The balancing involved in setting that level is, in principle, for the EU legislators to make. It entails a holistic assessment of the rights and freedoms of digital euro users on the one hand and risks to the integrity of the digital euro ecosystem on the other, as it could be abused for criminal purposes, such as money laundering.

For the digital euro to serve as a functional equivalent to cash, it should have cash-like features also regarding privacy. Following the key principle of data protection ‘by design and default’, the ECB has sought to wire privacy concerns into its own exploratory work on digital euro design and has experimented with privacy-enhancing techniques. 85 Ultimately, it must be ready to technologically implement the privacy standards and requirements set by the legislators.

By enshrining the fundamental privacy choices into EU legislation, it is ensured that future changes to these choices are subject to an open and democratic debate and procedure. However, the devil is in the detail. The technological design to implement these privacy choices is done by the ECB and thus largely removed from public scrutiny. High accountability and transparency standards should apply to the ECB when establishing the digital euro's privacy-related design features and changing them later on. This should include consultations with the European Data Protection Board before any design choices are made. 86

Financial stability is another key concern that requires appropriate delineation of the ECB's and legislators’ spheres of responsibility. As discussed above, 87 the Commission's proposal gives the ECB broad powers to limit the use of the digital euro as a store of value to mitigate detrimental effects on commercial banks, financial stability and real-economy lending. To guide the ECB's choices, the proposal sets some fundamental and broad parameters: when restricting the use of the digital euro as a store of value, the ECB must balance (1) the interest of financial stability (including its effect on monetary policy implementation) against (2) the usability and acceptance of the digital euro, (3) in line with the proportionality principle. 88 Moreover, the ECB must apply holding limits in a non-discriminatory manner and uniformly across the euro area. 89

The ECB has argued that the competence to establish limits on the use of the digital euro as a store of value and to calibrate them over time is intrinsic to its monetary policy tasks. 90 This view neglects that there are other interests at stake here and that the limiting of digital euro holdings by users entails fundamental choices that exceed purely technical decisions. While a stable banking system is a fundamental precondition of the ECB's ability to transmit monetary policy signals 91 and a key supervisory objective within the Single Supervisory Mechanism, the ECB shares the concern for financial stability with other authorities, including the legislators as the EU banking regulator. 92 Moreover, the views in the literature are far from settled on the desirability of holding limits. 93 Higher (or no) holding limits may imply a large shift of commercial bank deposits into digital euro accounts, but might also make the banking sector more stable and public safety nets redundant in the longer term. Lower holding limits, such as those anticipated by the ECB, on the other hand, tend to maintain the status quo and may deter users altogether from opening a digital euro account in addition to bank accounts.

The ECB is well-placed to conduct the complex economic assessments that will ultimately inform the calibration of holding limits. However, strong accountability and transparency mechanisms should guide that process and the choices the ECB makes, both initially and over time. The Commission is right to propose enhanced reporting obligations for the ECB in this regard. According to Article 40(2) of the Commission proposal, the ECB must provide the European Parliament, the Council and the Commission with (1) information on how it plans to implement holding limits in the prevailing financial and monetary environment; and (2) an analysis of how these holding limits are expected to meet the objective of safeguarding financial stability. The novelty of this requirement relates to its timing: the ECB must report on these issues before the planned issuance of the digital euro and before the implementation of any changes to the holding limits. This element of ex ante consultation is an essential complement to the paradigm of ex post explanation of ECB policies under the framework of ‘independent accountability’. 94 It allows the ECB to take into account concerns of the European Parliament, the Council and the Commission in terms of the financial stability implications of its choices in independent, but well-balanced and well-reasoned decisions. Moreover, for PSPs and users it is essential to understand what considerations feed into the ECB's setting of holding limits and to anticipate potential changes to these limits.

ECB stakeholder engagement

ECB engagement has not been limited to exchanges with the European Parliament, Eurogroup and Commission on the digital euro. Outreach to private stakeholders – including banks and other intermediaries, merchants and civil society – has added to the ECB's more conventional accountability channels. That is a welcome and necessary, but also remarkable novelty in light of the broad scope of Article 130 TFEU, which prohibits the ECB from taking or seeking instructions not only from public authorities, but also ‘from any other body’.

The ECB's outreach to private stakeholders pursues the main goals of ensuring that the digital euro meets users’ needs and is both technically feasible and state-of-the-art. It implies a different modus operandi for the ECB than under conventional accountability arrangements. Instead of justifying its decisions ex post, the ECB consults its stakeholders ex ante with the aim of learning from their expertise, experience and preferences.

From October 2020 to January 2021, the ECB ran a public consultation on the benefits and possible design features of a digital euro 95 and conducted focus groups in all euro area Member States to gather views from different target audiences on their payment habits. 96 These consultations revealed that privacy, security, usability, low cost and accessibility are the most important expectations of citizens and professionals in the digital euro. The ECB highlighted that these insights ‘provide valuable input to the Eurosystem's ongoing assessments and upcoming decisions on a digital euro’, however, without pre-empting these decisions. 97

ECB engagement with different market representatives has occurred through market contact groups as well as prototyping and market research exercises. 98 The Digital Euro Market Advisory Group was established to advise the ECB on the design and added value of a digital euro from an industry perspective. Its members are market practitioners active in the retail payments market and selected on the basis of a call for expression of interest. In addition, the ECB has consulted the European Retail Payments Board (ERPB) in regular meetings, technical sessions and written procedures. Unlike the Digital Euro Market Advisory Group, the ERPB is a high-level strategic body whose establishment goes back to 2013. Its members include a wide range of representatives from the ECB/NCBs and both the supply side (i.e., PSPs) and demand side (e.g., retailers) of the market.

From July 2022 to February 2023, the ECB conducted a prototyping exercise to establish what paying with a digital euro could look like in different use cases. The exercise entailed five user interfaces each developed by a different provider (front-end prototypes) and their integration into a settlement system designed and developed by the Eurosystem (back-end prototype). 99 In January 2023, the ECB also invited market participants to take part in market research to get an overview of options for the technical design of potential digital euro components and services. 100 Both exercises appear to confirm the technical feasibility of digital euro solutions and innovative user interfaces for digital euro distribution.

Conclusions

At the latest since the adoption of the Commission proposal for a regulation on the establishment of the digital euro on 28 June 2023, the digital euro is on everyone's lips. However, discussions have paid little attention to the ECB's accountability regarding the digital euro – both during the initial investigation and preparation periods and in the future. This article attempted to fill this void. It argued that the concept of ‘independent accountability’ – still prevalent regarding monetary policy and by default applicable in this context as well – is an inappropriate standard to hold the ECB accountable for its decisions on the digital euro.

The argument is supported by several findings. The first is that, while the ECB has the power to issue a digital euro that mimics the basic features of cash, its mandate is not clear-cut. It relies on the application of several legal provisions in a combination that is untested so far. This runs counter to the standard justification that the ECB's accountability can be limited due to its clear mandate that is confined to largely technical decisions.

Related is the second finding: because the digital euro affects areas in which the ECB is not solely responsible, its adoption requires an unprecedented level of coordination with the EU legislators. The delineation of competences between the ECB and the legislators is as challenging as it is important, as it determines whether or not digital euro design choices, and their amendment in the future, are subject to a transparent and democratic process or not. Tackling two areas of particular societal importance – privacy and financial stability –, this article stressed the need for strong accountability and transparency standards regarding ECB decision-making, including ex ante consultations with other EU authorities.

The third finding is that the ECB is not only accountable to public authorities in the conventional sense, but also engages with a broad range of private stakeholders, including banks and other PSPs, merchants and citizens. The ECB seeks their input to understand the added value and feasibility of the digital euro and to feed into its design choices. Only if the digital euro meets users’ needs and is embraced by the market will it be successful and will the ECB be able to deliver on its mandate. This is different from conducting monetary policy, where the ECB is required to remain unsusceptible to any market preferences. As we are reinterpreting the ECB's mandate to include the novelty of the digital euro, we must also rethink the accountability of the ECB for its digital euro-related competences and tasks. That can only happen within the confines of the Treaties, at least for the time being. But there is legal room to explore new channels of accountability, before and after the digital euro's introduction. The ECB's engagement with public and private stakeholders during the investigation phase demonstrates its openness to new forms of collaboration and consultation. To make these a firm component of future ECB accountability arrangements will be key.