Abstract

Several corporate disclosure and due diligence laws related to the social and environmental impacts of globalized production have been enacted across the world over the last decade. While the emergence, operation and impact of such ‘transnational sustainability laws’ have already been extensively analysed, their legal operability remains poorly understood. This a significant omission because transnational sustainability laws form a novel and increasingly important attempt to conceptualize and govern the new logic of global production networks—global value chains—and their regulatory infrastructure. Against this backdrop, this article deploys a comparison of eleven recent transnational sustainability laws and develops an analytical framework to probe legally-operative conceptualizations of global value chains. By analysing how transnational sustainability laws conceptualize the value chain, the lead firm and adequate value chain governance, we argue, these instruments emerge as proxies for a legally-operative framework that better delineates the emerging law of global value chains. Thus, our analysis contributes to growing literature on the potential and limits of transnational sustainability laws as well as to the development of nascent ‘global value chain law’.

Keywords

1. Introduction

Several states have enacted laws pertaining to the social and environmental impacts of globalized production over the last decade. A range of recent statutes in the European Union, the United States and Australia, for example, require companies to report on the nature and scope of their operations, their global supply chains and the impacts they have on issues such as transnational corruption, trade in conflict minerals and human rights or sustainability more generally. These hard ‘transnational sustainability laws’ have generated active academic and policy discussion in recent years, but their legal operability remains poorly understood. 1 Which companies and sectors are covered, and why? What kind of legal registers are used in regulation: accounting, corporate law, contract law, criminal law or something else? What is the content of obligations? To what extent do the obligations set out in the statutes extend to multiple tiers of subsidiaries and suppliers? This omission of a fine-grained legal conceptualization is understandable because we are dealing with a new form of geographically and organizationally fragmented production—global value chains. 2

Even though global value chains have been at the centre of immense scholarly attention in recent years, law has yet to conceptualize them in a meaningful way. 3 While there is momentum towards developing a ‘law of global value chains’ that spans public international law, private governance, soft law and court-led doctrinal developments of private law, 4 the contribution of transnational sustainability laws is extremely significant because they provide authoritative examples of how national legislators are vying to conceptualize global value chains through local hard laws. As such, a more nuanced view on the legal definitions and mechanisms that sustainability laws utilize can directly help in developing the state-of-the-art of how global value chains can be legally conceptualized. In view of this, we submit that a more comprehensive understanding of transnational sustainability laws’ legal operability is needed for analysing their effectiveness, potential improvements and significance for regulation of global value chain capitalism more generally.

Against this backdrop, this article has two interconnected aims. First, it seeks to deploy a detailed comparison of recent transnational sustainability laws by isolating their most significant legal concepts. Second, it seeks to develop a conceptual framework to better analyse and harness these laws’ developmental potential regardless of e.g. their geographical origin or material focus. Based on the plurality of legal concepts used in current transnational sustainability laws, the analytical framework interrogates how sustainability laws conceptualize 1) global value chains as their regulatory object; 2) lead firms as their regulatory subject; and 3) adequate value chain governance as their regulatory ideal. By analysing how transnational sustainability laws conceptualize the value chain, the lead firm and adequate value chain governance, we argue, these novel national instruments emerge as proxies for a legally-operative framework that helps better delineate the emerging law of global value chains. While the analysis contributes primarily to growing legal scholarship on the potential and limits of transnational sustainability laws as well as the development of a nascent ‘global value chain law’, 5 our analytical framework may also have uses across a range of disciplines, including global value chain theory, political economy and sustainability science, for example by providing enhanced conceptualizations of value chains and their governance grounded in legal research and practice.

The article is structured as follows. Section 2 introduces transnational sustainability laws and frames the technological, organizational and legal developments that have given rise to today’s global value chain capitalism. In particular, the section highlights the foundational role of lead firms and their governance efforts for structuring and governing production organized through global value chains. Section 3 presents a brief overview of previous research on transnational sustainability laws and a comparison of national instruments. The Section then proceeds to deploy an analytical framework to help understand how the sustainability laws relate to one another and how they construct legally-operative conceptualizations of global value chains and their governance by lead firms. This heuristic device, we conclude in Section 4, enables a more nuanced analysis of the legal frameworks that undergird and structure global production and also provides a state-of-the-art of current regulation on value chain governance for future reference and developments.

2. Transnational sustainability laws and global value chains

This section discusses the emergence of transnational sustainability laws as the most recent symptom of fundamental changes in global production. First, the section introduces transnational sustainability laws and their basic operating logic. Using these laws as a narrative device, the section then briefly recounts the historical emergence of global value chains as a result of technological, organizational and legal developments. Finally, the section illustrates the techniques of regulating global value chain governance. Through this historical contextualization we hope to show that any approach to regulating global value chains must focus on conceptualizing global value chains (i.e. the regulatory object), lead firms (i.e. the regulatory subject), and adequate value chain governance (i.e. the ideal that regulation tries to achieve).

A. Introducing transnational sustainability laws

Over the last decade, several statutes focused on regulating the governance of social and environmental impacts of transnational production have been enacted on state, federal and regional levels around the world. Ranging from the Californian 2010 Transparency in Supply Chains Act (‘California Transparency Act’) 6 to the French 2017 loi relative au devoir de vigilance des sociétés mères et des entreprises donneuses d’ordre (law on a duty of care for parent and buyer companies; ‘loi vigilance’) 7 and to the EU Conflict Mineral Regulation (‘EU CMR’) passed in 2017 but coming into force in 2021, 8 these laws—which we call transnational sustainability laws—form the most recent mechanisms used to regulate the governance of social and environmental sustainability of production taking place outside a specific jurisdiction. 9 While the term ‘transnational sustainability law’ has already been used particularly in relation to sustainability focused private ordering by standards and contractual mechanisms, 10 our notion goes beyond this narrow definitional approach. We suggest instead that ‘transnational sustainability law’ could be seen as a hypernym for the regulation of sustainability in transnational production, be it through private ordering, soft law, or, as is the primary focus of this paper, nationally emanating hard laws directly aimed at regulating the transnational production structures of local actors. 11 This is particularly so because, as described in Sections 2.B and 2.C below, all three approaches are intertwined in developing the sustainability of transnational production.

As indicated by the California Transparency Act, the French loi vigilance and EU CMR, recent transnational sustainability laws respond to growing awareness of adverse social, environmental, economic and other effects of global production. In particular, the rise of hard transnational sustainability laws represents national legislators’ efforts to prevent abuse prevalent in global production networks by requiring a measure of responsible value chain governance from companies operating in their jurisdiction. 12 In essence, such hard transnational sustainability laws are driven by the will of some states—often home to large firms at the peak of global value chains—to shine light on the reality of transnational production. 13 While these laws have antecedents, for example, in the US 1977 Foreign Corrupt Practices Act (‘FCPA’) and several unsuccessful attempts at passing similar laws around the turn of the millennium, 14 on the whole they have come to their own only with the most recent wave of regulation.

Hard transnational sustainability laws have been enacted at an increasing pace starting in 2010, when three separate laws were passed. In addition to the California Transparency Act, Section 1502 of the US federal Dodd-Frank Act, which contains detailed provisions on conflict mineral supply chains, and the UK Bribery Act, which establishes a duty for commercial organizations carrying on a business in Britain to verify that there is no corruption in their supply chain, were enacted in 2010. 15

Similar, thematically narrow transnational sustainability laws have been enacted around the world since 2010. Another UK law, the UK Modern Slavery Act 2015, 16 resembles the earlier California Transparency Act in its focus on human trafficking and exploitation in global value chains, as do the recently passed Australia Modern Slavery Act 2018 17 and New South Wales (‘NSW’) Modern Slavery Act 2018. 18 In a similar vein, the most recent transnational sustainability law, the Dutch Wet zorgplicht kinderarbeid (‘duty of care in relation to child labour’) from May 2019, covers child labour in international production chains. 19 The scope of the most recent regional instrument, the EU CMR, is limited to conflict mineral supply chains. At first sight, the main commonality between these transnational sustainability laws is their limited material scope: They focus on specific issues such as corruption, human trafficking or conflict minerals.

In addition to narrow, thematically-oriented laws, more extensive transnational sustainability laws have started to emerge over the past few years. Perhaps the most significant such law is the 2017 French loi vigilance, which requires large companies to extensively map the impacts of their value chains on fundamental rights, human rights and the environment. Another similar, materially broad proposal for a transnational sustainability law was drafted and extensively debated by the Swiss parliament though its political trajectory is now uncertain. 20 Finally, the most comprehensive regional law, the 2014 EU Non-Financial Reporting Directive (‘EU NFRD’), covers a broad material range spanning from corruption to environmental protection and human rights. 21

Regardless of their varied chronology, heterogenous regional backgrounds and diverging focus areas, transnational sustainability laws share several important commonalities. Most importantly, they purport to make companies identify and mitigate their transnational operations’ adverse social impacts. In doing so, legislators generally assign large firms with duties to evaluate the social, human rights, environmental and other risks of their operations and require public disclosure of adopted risk prevention mechanisms. These laws, many argue, constitute ‘historic’ steps to improve ‘corporate accountability’ and to make ‘globalization work for all’. 22

B. Transnational sustainability laws as symptoms of global value chain capitalism

The recent proliferation of transnational sustainability laws is not a coincidence. Instead, their emergence responds to fundamental changes in the organization of production and the liability deficits it has prompted. Transnational sustainability laws, among other contemporary attempts to regulate and conceptualize the new logic of production, need to be understood against this broad frame as symptoms of global value chain capitalism.

The transformation of production has long historical roots. Over the last two hundred or so years the logic of commerce has gone through major shifts that Baldwin has called ‘unbundlings of globalization’. 23 The first unbundling started in the 19th century when new transport technologies enabled the global distribution of goods. This in turn enabled centralized mass production, the comparative advantage of which was based on locating central phases of production, such as design and manufacturing, under the roof of a centralized production bureaucracy. The centralized mass production model began to erode during the 20th century with the second unbundling of globalization that came by when new communications technologies enabled the increasingly detailed control of production over distances. 24 This resulted in a second fundamental shift in production: companies could now focus on their more value producing ‘core competences’, such as product development, marketing and intellectual property governance, while outsourcing less value-producing aspects of production, such as component development and manufacturing. 25

Law has had a profound, but comparatively unrecognized, role in this shift. 26 The development of trade and investment law through international treaties, for example, has facilitated the global fragmentation of production by removing obstacles to the free movement of goods, services and capital. An even greater role is played by the development of the basic organizational structures of private law—contract and corporation. These two quintessential private law institutions have made possible the limiting of liability for production related contingencies and thus contributed to the organizational fragmentation of value chains.

The result of these technological, economic and legal developments is a globally criss-crossing network where several actors, connected through corporate and contractual relationships, are intertwined to produce products and services. These geographically and organizationally fragmented networks constitute global value chains. Their effective utilization is central to not only the success of individual companies but also for the development of national and global economies. 27

In practice, the efficiency of global value chains hinges on effective control over geographically and organizationally dispersed production, thus emphasising the role of lead firms. 28 A lead firm is the actor most centrally engaged in the governance of a product or service, for example by owning a brand and related intellectual property rights, by designing the product or service, marketing it and making decisions over how different aspects of production are organized: in-house, within the corporate group, or by outsourcing to external suppliers. Lead firms undertake value chain governance for multiple reasons, such as guaranteeing product quality, compliance with target market regulations, value-chain-wide cost management or research and development. 29 Governance may also be implemented in several different ways. At one end of the spectrum the lead firm may view a value chain almost as a single entity, effectively governed as a seamless whole despite contractual and corporate boundaries. 30 Even at the other end of the spectrum a lead firm has at minimum made a choice over whether production is outsourced or not and, in case of the latter, to whom it is outsourced.

Overall, the shifts in global production have been drastic. Already in 2013 it was estimated that about 80% of world trade took place in such value chains organized through corporate and contractual structures. 31 Thus, contemporary forms of economic production are, to a great extent, species of global value chain capitalism. Transnational sustainability laws have emerged as national responses to these fundamental and still-continuing changes.

C. Regulating global value chain governance

Transnational sustainability laws are one of the most recent attempts to regulate global value chain capitalism. They put forward a sustainable governance model that seeks to identify and mitigate adverse environmental, social and human rights impacts inherent in global value chains. In doing so, hard transnational sustainability laws constitute a new type of regulatory intervention that extends a state’s control more directly over production that takes place outside its traditional jurisdiction. Such an approach stands in marked contrast to earlier national models that either focused on production taking place within a jurisdiction or tackled production indirectly by setting standards on imported goods.

The regulatory intervention that transnational sustainability laws purport arises from liability deficits inherent in organizationally and geographically fragmented production. On the one hand, organizational fragmentation has multiplied the number of potential liability subjects, thus raising the question of whether a lead firm should be liable for aspects of production that it has decided to outsource to suppliers or subsidiaries. This may lead to the different treatment of value chain actors already within a jurisdiction, for example on the basis of size, sector or nature of business. 32 On the other hand, fragmentation has become more pronounced in transnational settings where value chain actors are located in different jurisdictions. To a great extent, this is a feature of global value chain capitalism as the comparative advantage of fragmented production may stem not only from specialization and geographical differences but also from regulatory discrepancies in labour, environmental and tax regimes between jurisdictions. 33 As a result of these two features, there are severe gaps—liability deficits—in the legal coverage of global value chains.

Transnational sustainability laws try to navigate geographically and organizationally fragmented production by regulating how lead firms govern transnational production. This is natural because lead firms are the drivers behind value chains and responsible for choices related to their structure and governance. Lead firm responsibility for how they organize their production has also been at the core of previous attempts to regulate value chains, and various strands of national legislation already provide several examples of remedies by which lead firms can be held accountable for other actors in their value chains.

In many European states, for example, lead firms are required to undertake due diligence to ensure that other value chain actors, such as suppliers or subcontractors, abide by relevant labour and social security regulations, with repercussions ranging from penalties to joint liability. 34 In some jurisdictions environmental law may enable holding lead firms liable for harm caused by their suppliers or subsidiaries. 35 A further and comparatively wide-spread example is product liability, under which lead firms can generally be held liable for harm caused to users of defective goods whether or not the user acquired the good from the lead firm and irrespective of whether the lead firm itself had manufactured the good or outsourced production. 36 These approaches, however, are primarily focused on the effects of fragmentation in a national context.

Another prominent regulatory strategy has focused on the qualities of products. As an example, national legislators have an interest to ensure that products produced in global value chains fulfil local health, safety, environmental and other requirements when they are brought into a jurisdiction. 37 Again, if a lead firm is located in another jurisdiction, the EU Product Liability Directive places responsibility on the importer of a good. 38 Such regulation clearly has a transnational effect by requiring foreign actors to comply with target market regulations. 39 These approaches do not, however, typically extend for example to dangerous labour conditions or lacklustre environmental protections in the jurisdiction where production takes place. Accordingly, qualities not directly related to a specific imported good have traditionally been left outside the scope of regulatory requirements in importing jurisdictions.

In the current mode of global value chain capitalism, focus on fragmentation in national contexts or indirect transnational regulation by way of qualities of products are increasingly deemed insufficient. While there is an emerging consensus on the need for directly regulating the transnational mode of production in particular from the perspective of sustainability, the liability deficits propelled by the geographical and organizational fragmentation of global value chains have proven challenging to overcome. In part this has to do with political sensitivities, because the direct regulation of production in other jurisdictions raises difficult questions of sovereignty, legitimacy and participation. 40 For this reason, much of the current regulation of transnational production has been left to private actors, such as standardization and certification systems put in place by industry, labour organizations and NGOs, 41 public international law, 42 or some cooperative combination of the two. 43 Even though no extensive hard international regulatory infrastructure has emerged, the mix of various transnational initiatives, including the rise of standards and influential soft law instruments such as the UN Guiding Principles on Business and Human Rights (GPs) 44 and the OECD Guidelines for Multinational Enterprises, 45 has certainly approximated and coordinated international responses to recurrent labour, environmental and human rights violations related to global production. 46 This holds also for many national laws whose intent and regulatory strategies often coincide with enhanced human rights protection by, for instance, requiring human rights due diligence from companies. 47 Such policy diffusion notwithstanding, the recent proliferation of hard transnational sustainability laws suggests that regulatory focus has, in many places, started to shift from private standards and the international level towards national law. 48

3. Transnational sustainability laws: Comparison and a framework for analysis

In this section we deploy an analytical comparison of recent transnational sustainability laws. First, we discuss the reception of such laws in previous scholarship. Next, we present a comparison of the eleven transnational sustainability laws introduced above. We then develop, and explain the logic behind, our proposed three-pronged analytical framework that focuses on how transnational sustainability laws conceptualize the objects of regulation (global value chains), the subjects of regulation (lead firms) and the legal mechanisms and expected results of regulation (the idea of adequate value chain governance). We proceed to apply this framework to provide an overview of the current state-of-the-art of the legal operationalization of transnational sustainability laws.

A. Analysing transnational sustainability laws: a look at current scholarship

The emergence, operation and impact of transnational sustainability laws has already spurred a growing body of scholarship that ranges from supply chain management 49 to politics, 50 business ethics 51 and political economy. 52 Quite naturally, transnational sustainability laws have also generated considerable legal scholarship that touches on international law, EU law and human rights as well as different strands of domestic business law, such as corporate law 53 and accounting. 54 While these laws are closely embedded with the varying legal infrastructures of their home states, their novelty and broadly consistent regulatory techniques have facilitated studies that focus on the commonalities and differences between the national instruments. These studies generally fall into two categories.

First, transnational sustainability laws are often positioned along thematic or regional lines. Thus, different variations of national laws centred on modern slavery 55 or conflict minerals 56 have drawn attention to evaluating the mechanisms and impacts of sector-based sustainability legislation. This type of the scholarship often uses other transnational sustainability laws and international instruments as yardsticks against which domestic initiatives are compared. 57 Similarly, transnational sustainability laws from the same state or region, such as the UK, are frequently discussed side-by-side to analyse the causes for their varying rate of success. 58 Finally, the existing scholarship differentiates transnational sustainability laws also based on their regulatory techniques such as disclosure and transparency or due diligence, often reflecting the development of legislation over time. 59

Second, the proliferation of transnational sustainability laws has also led to cross-cutting studies that examine legal instruments across thematic planes and on multiple geographic scales. In this category, analysis is often deployed from the broader perspective of ‘business & human rights’ and it is usually augmented with discussion on international soft law instruments. 60 Against this backdrop, transnational sustainability laws are usually contrasted with the UN GPs or various OECD instruments, often with a view to develop best practices for future legal instruments, for example by recommending lawmakers to adopt more stringent due diligence obligations instead of focusing on transparency. 61 In both cases, current analysis generally highlights the shortcomings of transnational sustainability laws. Thus, existing studies discuss severe deficiencies in transparency-based regulatory techniques, 62 poor means of enforcement 63 and the limited impact of such laws either on corporate conduct or consumer behaviour. 64

In sum, the proliferation of transnational sustainability laws in the developed economies over the past decade has produced a cross-disciplinary body of scholarship that draws attention to the various ways national lawmakers try to regulate the responsible governance of value chains. The existing analysis highlights the significance of such laws as a legal response to major shifts in the modes and organization of production but, at the same time, underscores the discrepancy between their normative goals and actual effects. As the perceived shortcomings e.g. in their auditing and enforcement regimes illustrate, further analysis of transnational sustainability laws is clearly needed. In this exercise, we submit, more emphasis should be placed on evaluating their legal operability.

B. Beyond current scholarship: focus on the legal operability of hard transnational sustainability laws

While previous literature is essential in understanding the politics, techniques and limits of current transnational sustainability laws, in our view much of their novelty and significance lies in the legal definitions through which national lawmakers attempt to conceptualize and govern the new logic of global production and its regulatory infrastructure. Thus, rather than replicating the existing approaches, our comparative analysis seeks to isolate and interrogate the most significant legal concepts that arise from such laws. Through this exercise, we aim to unearth broader lessons related to the legal infrastructure of global value chain governance.

The methodology through which we have selected the examined laws and conducted the comparative appraisal follows broadly in the tradition of functional comparison. 65 In Section 2 we suggested that transnational sustainability laws, whether in the form of private ordering, soft law or hard law, are a response to the sustainability deficit of new transnational forms of production. While we believe that this approach may be fruitful also for understanding other forms of sustainability regulation, our comparative focus here is on hard transnational sustainability laws as defined in Section 2. To recap, our focus is on nationally emanating hard laws that aim at directly regulating the governance of transnational production by actors in their jurisdiction. We believe that a comparative analysis of these hard transnational sustainability laws will shine light on the current state of legal conceptualization of the mode of production that they complement, i.e. global value chains.

In practice, we compare nine already-enacted hard transnational sustainability laws, one recently passed bill and one well-developed law proposal using seven legally-relevant variables. The laws, introduced in Section 2.A, were selected because they in diverse ways attempt to directly regulate the sustainability governance of transnational production, which differentiates these regulatory initiatives from approaches focusing either on national contexts or on qualities of end products, such as consumer safety-focused product liability regimes. 66 Another major selection factor was the temporal proximity of laws. By choosing laws enacted in the 2010s, we were able to focus on the state-of-the-art of regulatory initiatives on regional, national and sub-national levels. While further examples of such hard transnational sustainability laws no doubt exist and are in the making, 67 the current batch was also selected on the basis of the availability of material and the authors’ comparative linguistic and legal familiarity with the related languages, cultures and legal systems.

The variables used in the initial comparison of transnational sustainability laws were: type of the legislation, which is used to classify a statute at the most general level (for example, criminal law, ad hoc disclosure); its material scope, which is used to outline the problem or sector a statute is trying to affect (for example, conflict minerals, modern slavery); its personal scope, which is used to determine the actors from which a statute necessitates actions (for example, large companies, importers); its definition of the value chain, which is used to describe how a statute understands both the general (for example, mineral supply chain) and legal structure of the value chain (for example, corporate group, specific tiers of contractual suppliers); the statutory duties assigned, which describes the concrete legal requirements of a statute (for example, disclosure, a risk mitigation plan); statutory repercussions for breach of duty, which is used to illustrate the legal consequences (or the lack of such) for failures to abide by statutory duties (for example, criminal prosecution, injunctive relief); and the wider significance of duty on other forms of liability, which is used to describe the relationship between a statute and broader national systems of liability (for example, tort liability and defences against it).

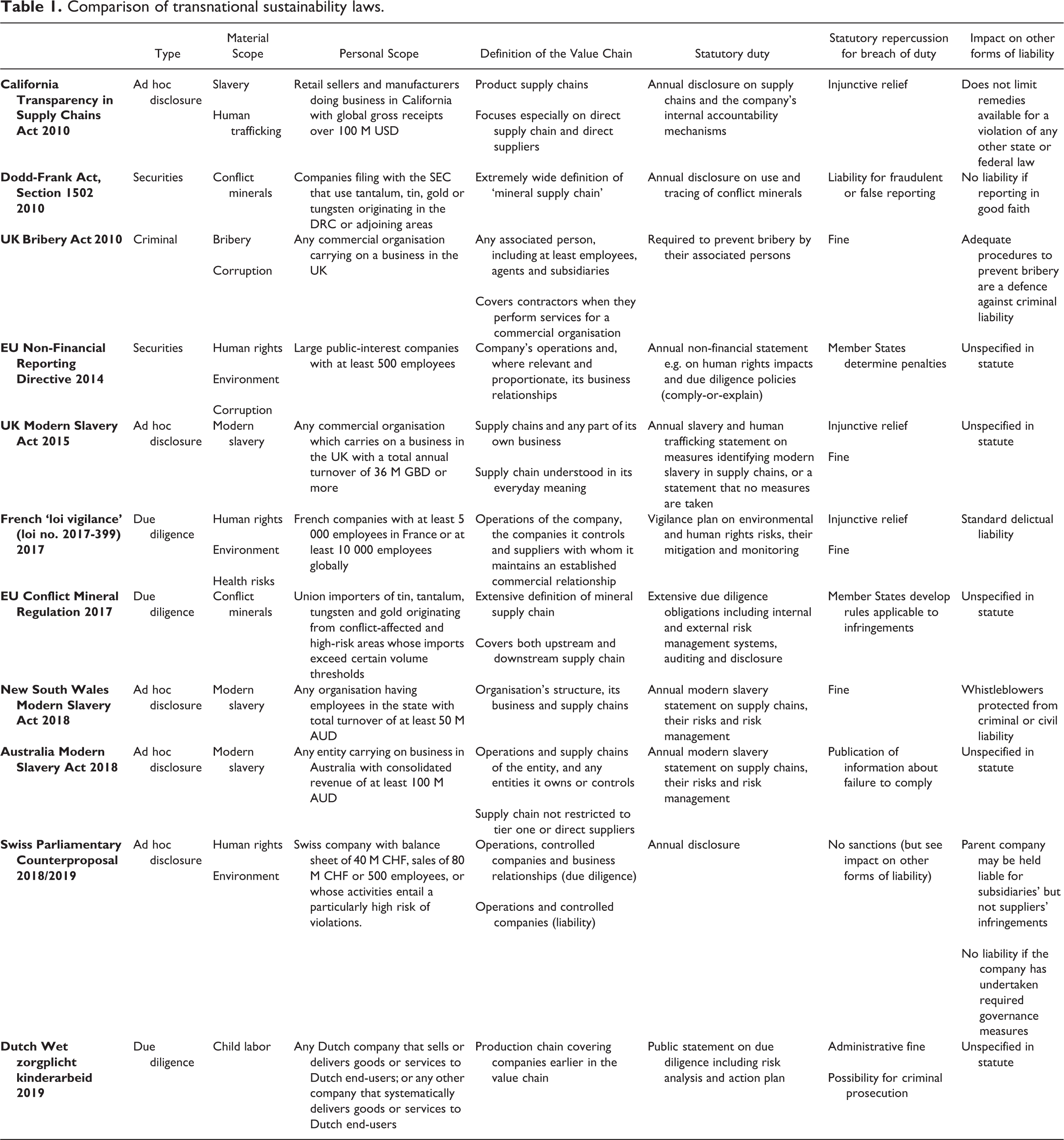

In addition, even though the year of the enactment was not used as its own variable in the comparison, our listing of transnational sustainability laws in chronological order indicates how they have evolved over time and can thus be viewed as an implied temporal variable whose significance should not be underestimated. Ultimately, the comparative appraisal through these seven variables yields a rough description of transnational sustainability laws’ legal underpinnings and mechanisms, thus providing a matrix of their legally-operative conceptualizations of global value chains. The results of this comparative exercise are presented in Table 1 .

Comparison of transnational sustainability laws.

The results suggest that, while novel and heterogenous in their geographical or temporal origin and thematic focus areas, transnational sustainability laws clearly come across as broadly similar regulatory devices that focus on the global value chain and especially its large lead firm from whom lawmakers expect a variety of actions amounting to adequate value chain governance. There is, however, substantial variance in the concrete legal concepts and techniques through which transnational sustainability laws operate. As an example, if a law focuses primarily on the social impacts of clearly-defined actors, such as subsidiaries or bottle-neck suppliers, statutory due diligence and disclosure obligations are often more extensive and specific than in a law that tackles the value chain in its entirety. Such legal variance is significant because it steers certain lead firms to view their value chains differently and, as a consequence, leads to different models of value chain governance. For this reason, the ultimate reach of transnational sustainability laws, as well as their impact on broader notions of ‘global value chain law’, is easily masked by the sheer range of national concepts and experiences.

Against this backdrop, we submit that a more nuanced and cross-cutting analytical framework that emphasizes the contribution of transnational sustainability laws’ individual elements to their overall legal operability is needed to fully harness their inherent developmental potential. Thus, it is suggested that we need to develop a framework for analysis that is able to embed the plurality of legal concepts that undergird the current mix of transnational sustainability laws beyond the basic seven-variable schematic.

68

Based on the historical developments described in Section 2 as well as the initial results of our comparative exercise, we submit that a more analytical evaluation of transnational sustainability laws should group these (or any other) variables based on how they conceptualize: global value chains, encompassing the various legal definitions and doctrines that are used to define the legally relevant extent of transnationally fragmented production structures organized through corporate and contractual means (‘definition of the value chain’ variable); lead firms, encompassing different approaches and arguments towards selecting the regulatory subjects from whom value chain governance is required (‘type of regulation’, ‘material scope’, and ‘personal scope’ variables); and adequate value chain governance, encompassing the core obligational content of transnational sustainability laws and how these are reflected in relation to statutory duties and, crucially, liability (‘type of regulation’, ‘statutory duty’, ‘statutory repercussions’, and ‘impact on liability’ variables).

In the following, we use this three-tiered typology to focus the basic seven-variable comparison between transnational sustainability laws. To this end, the following subsections explain and expand on how transnational sustainability laws utilize the variables presented in our comparison to conceptualize the value chain (Section 3.C), the lead firm (Section 3.D) and adequate value chain governance (Section 3.E), thus exposing how these novel national instruments emerge as proxies for a legally-operative framework that helps better delineate the emerging law of global value chains.

C. Conceptualizing the value chain

The first element in our three-tiered typology is the ‘value chain’. The concept arises naturally from all transnational sustainability laws as their primary regulatory object is the global value chain. Regardless, there is no consensus as to what the ‘value chain’ the national instruments seek to regulate actually entails. This applies to both the general definition and the legal definition of the value chain. The definitional question is not moot or a mere technical issue. Instead, the very definition of the value chain both frames the purpose of regulation and marks more general ‘design philosophies’ of governance. 69

The general definition of the value chain is relatively stable across national instruments. In practice, most transnational sustainability laws understand ‘value chains’ as supply chains consisting of a company’s subsidiaries and suppliers. The NSW Modern Slavery Act, for example, defines value chain as the lead firm’s ‘structure, its business and its supply chains’. 70 The Australia Modern Slavery Act opts for the same statutory language while extending the concept to cover ‘products and services that contribute to the entity’s own products and services’. 71 In the same vein, the EU CMR defines mineral supply chains broadly but precisely as ‘the system of activities, organizations, actors, technology, information, resources and services involved in moving and processing the minerals from the extraction site to their incorporation in the final product’. 72 The Dutch Wet zorgplicht kinderarbeid, in turn, opts for the term ‘production chain’ (productieketen). 73

Broad consistency notwithstanding, the exact terminology used to describe supply chains varies. Thus, the UK Modern Slavery Act only indicates that ‘supply chain’ has ‘its everyday meaning’ without developing the concept further. 74 The UK Bribery Act, for its part, often uses the term ‘contractual chain’ instead of supply chain, 75 while the EU NFRD occasionally opts for terms such as ‘subcontracting chains’ 76 and ‘value chains’. 77 Moreover, even though transnational sustainability laws generally understand value chains as global, some statutes limit their geographical scope. As an example, the Dodd-Frank Act specifically targets the metals and minerals that originate from the DRC or adjoining areas. Regardless of these terminological discrepancies, the general definition of value chain across transnational sustainability laws seems to suggest that the term can, in principle, be inclusive of any actor in any value chain anywhere on the globe.

Crucially, however, any coherence with regard to a general definition of value chain does not carry over to legal definitions of the value chain. Take the case of the Australia Modern Slavery Act, which maintains a dual focus on ‘operations and supply chains of the reporting entity, and any entities the reporting entity owns or controls’. 78 This definition exposes the well-known fault line between equity-based and contract-based value chains. Ideally, transnational sustainability laws ought to cover both the equity-based and contract-based value chain. If the legal definition of the value chain covers only equity-based structures, lead firms may shift liability risks by outsourcing production from the corporate group to contractual counterparties. Regardless, some transnational sustainability laws continue to focus on equity-based value chains. The EU NFRD, for instance, requires companies to report primarily on their own ‘operations’ and extends similar requirements to ‘business relationships’ only ‘where relevant and proportionate’. 79 In addition to definitional differentiation, transnational sustainability laws may also make a distinction between equity- and contractually-organized value chains by distinguishing due diligence obligations from liability. In the Swiss law proposal, for example, the lead firm would be liable only for its controlled subsidiaries’ actions even though the scope of due diligence requirements extends also to contractual value chains. 80

As evidenced by numerous references to both enterprise and contractual structures, most transnational sustainability laws recognize this fundamental challenge. Finding a balance between under and over-inclusive regulation, however, is not an easy task. For one, there are severe challenges in coming up with a technical legal definition of the value chain because it would need to be predefined in a way that guarantees at least minimum levels of clarity and legal certainty. In many ways, the discrepancy between equity-based and contract-based value chain models reflects a legal reality where equity-based value chains have been at the centre of legislative and scholarly attention for several decades, whereas attention is only now shifting towards contractually organized value chains. 81 Against this backdrop, it is significant that some transnational sustainability laws already hint at new models for conceptualizing contractually organized value chains from a legal perspective.

One prominent model relies on established doctrines that have been used to define legally significant relationships between separate commercial actors in the past. The French loi vigilance provides a practical example. When drafting the legislation, the French lawmaker considered the applicability of several contract law doctrines on value chain liability. 82 The final statute defines the relevant value chain to cover, from a legal perspective, a parent company, its subsidiaries, and those contractors and suppliers with which the lead firm has an ‘established commercial relationship’ (relation commercial établie). 83 ‘Established commercial relationship’ is a French doctrine that has traditionally been used to protect suppliers from the termination of supply contracts. The significance of the doctrine under the new law is, however, unclear. Most importantly, its applicability beyond the parties to the contract, that is to second or even further tiers of suppliers, is uncertain. 84 The doctrine may thus only cover first-tier suppliers instead of the contractually organized value chain more broadly.

Despite its uncertainties, the French law is significant in that it attempts to provide a specific legal doctrine to cover also contractual relationships in the value chain. Similar, potentially applicable doctrines can no doubt be found in other legal systems. One prominent example is the debate over whether the Chandler ruling, where an English court found a parent company liable in tort towards its subsidiary’s employees, would be applicable also to contractual buyer–supplier relationships. 85 Among current transnational sustainability laws, however, the French approach is the only one that explicitly proposes using an existing legal doctrine to cover contractual relationships in a value chain.

Instead of direct reference to specific doctrines, many transnational sustainability laws focus on more open-ended approaches to legally relevant definitions of the value chain. The UK Bribery Act, for example, uses the term ‘any associated person’ to define the supply chain. 86 In practice, however, the related guidance makes it clear that a thin contractual relationship, for example, ‘simply acting as a seller of goods’, is not enough to bring a relationship under the statute’s scope. 87 Thus while the statute enacts conditions for the triggering of responsibility, the exact content of these conditions is left unclear. The preparatory materials for the Australia Modern Slavery Act, for their part, make clear that covered ‘supply chains (…) [are] not restricted to “tier one” or direct suppliers’. 88 It is not clear, however, to exactly what extent the supply chain is covered unless, for example, an approach similar to the Chandler ruling is used. Similarly, the explanatory memorandum for the Dutch Wet zorgplicht kinderarbeid states that reporting entities need to extend their analysis to ‘companies earlier in the chain’ (ondernemingen eerder in de keten), but the reach of this exercise is not defined. 89

Transnational sustainability laws can also differentiate between several ‘classes’ of supply chains. Under the California Transparency Act, for example, enhanced disclosure obligations are required from lead firms in relation to their ‘direct supply chain’ and ‘direct suppliers’ as opposed to the rest of the supply chain and other suppliers. 90 This puts a sharper focus on actors closer to the lead firm. Yet another approach might simply make specific actors responsible for all supply chain related problems. The EU CMR, for instance, specifically targets ‘Union importers of minerals or metals’ with extensive due diligence and disclosure obligations that cover the whole conflict mineral supply chain. 91 This approach is in many ways reminiscent of product liability law, being clearly inclusive of the whole value chain.

Overall, transnational sustainability laws do not put forward a settled legal definition of the value chain. The definitions used by individual lawmakers differ in ways that hamper legal conceptualization of fragmented production. This notwithstanding, each law recognizes the organizational complexity of the value chain, acknowledging its legal distinction to equity-based and contract-based production networks. Crucially, many transnational sustainability laws identify the contractually-organized value chain as the primary target of regulation. Likewise, most laws seek to affect the ways the lead firm contractually governs the conduct of other actors in its value chain. Regardless, many transnational sustainability laws continue to make significant legal discrepancies between the equity- and the contract-based value chain, as the examples of the French loi vigilance, the EU NFRD and the Swiss law proposal suggest.

D. Conceptualizing the lead firm

A focal point of transnational sustainability laws is the lead firm which is required to ‘supervise’ the value chain. This duty may be justified for example with the de facto control the lead firm exerts on other value chain actors, ranging from making the decision to outsource production to implementing more advanced means of value chain governance, such as standardization or dedicated governance contracts. 92

While a lead firm is a core concept in all transnational sustainability laws, it can be understood in different ways. One way is to simply see all companies as lead firms. The UK Bribery Act, for example, extends its personal scope to any ‘commercial organisation (…) which carries on a business’. 93 This technique is also the basis for most international soft law initiatives, which favour a broad personal scope. The UN GPs, for instance, apply equally to all companies regardless of size, sector, location, ownership or structure, even if they also allow for modifying corporate responsibilities using the same factors. 94

The vast majority of transnational sustainability laws, however, limit their personal scope. A common technique is to focus on enterprises that are seen as large in light of financial indicators such as turnover, total sales, number of personnel or some combination of these. Sectoral, geographical and other criteria may also be used. The Swiss proposal covers also smaller companies that operate in a ‘high-risk’ sector, 95 while the Dutch Wet zorgplicht kinderarbeid covers companies that sell or deliver goods or services to Dutch end users. 96 The EU CMR focuses specifically on importers located within the EU dealing with conflict minerals. Similarly, the Dodd-Frank Act focuses on companies utilizing minerals potentially sourced from specified conflict areas and which are required to file reports to the US Securities and Exchange Commission (SEC).

The increasing focus on the lead firm reflects the changing logic of global production. Transnational sustainability laws recognize that the lead firm, whether big or small, forms a natural regulatory target because its crucial role in organizing and controlling the value chain results in information superiority. Thus, the lead firm is expected to disseminate information on the impacts of its value chain to consumers, other market actors and the state. The California Transparency Act, for example, requires companies to disclose on their website the specifics of how they evaluate and audit supply chains as well as what actions are taken in relation to direct suppliers and internal management. 97 Most transnational sustainability laws also require reporting to public officials. The Dodd-Frank Act, for instance, requires a disclosure on the reporting company’s conflict mineral supply chains to the SEC, 98 the EU CMR a similar disclosure to EU Member States’ competent authorities, 99 the NSW Modern Slavery Act reporting to the state’s anti-slavery commissioner 100 and the Wet zorgplicht kinderarbeid to the Netherlands Authority for Consumers and Markets. 101 In addition to providing information, transnational sustainability laws often require lead firms to address the misconduct of value chain actors by undertaking specific due diligence measures. The clearest example of this is the EU CMR which assigns EU importers risk management obligations designed to influence and exert pressure on suppliers. 102 Similarly, guidances for the UK Bribery Act and UK Modern Slavery Act discuss contractual techniques that lead firms may use to ensure responsible value chain governance. 103

While lead firms are targeted with extensive duties, most transnational sustainability laws accept that fulfilling due diligence and disclosure obligations can be challenging. The UK Bribery Act guidance, for example, admits that under the practical realities of globally fragmented production a lead firm may only know the identity of first tier suppliers and not those of further tiers. 104 One common strategy used to overcome these problems is auditing and certification. Thus, the California Transparency Act, the Dodd-Frank Act and the EU CMR all require leads firms to open up their value chain structure and shift sustainability risk management to third-parties. The efficacy of auditing and certification, however, remains heavily contested. 105

In sum, current transnational sustainability laws typically conceptualize large lead firms as drivers of responsible value chain governance. Lead firms are required to disclose and disseminate information on their value chains and also to affect the conduct of other value chain actors. Regardless, there is no uniform definition of ‘lead firm’. Instead, comparison suggests that ‘lead firm’, at least for now, is a context-sensitive concept. Thus, for example, in addition to diverse restrictions based on company size, the EU CMR explicitly targets all EU based importers of conflict minerals while the Dodd-Frank Act targets companies that utilize conflict minerals and report to the SEC. The most significant outlier to this context sensitive approach is the UK Bribery Act which applies to all companies regardless of their size, sector or relative position in the value chain. 106 In practice, the development and proliferation of certification, auditing and other governance systems will likely level differences in value chain monitoring capabilities between lead firms of different sizes, sectors and capabilities. 107

E. Conceptualizing adequate value chain governance

While conceptualizations of value chains and lead firms determine the operative extent of transnational sustainability laws, due diligence and disclosure obligations established by such laws outline the core content of adequate value chain governance. As already discussed in Section 3.D, sustainability laws typically require lead firms to report on their global value chains and may also require lead firms to undertake specific due diligence measures. Coinciding with each transnational sustainability law’s material scope, these obligations generally cover, for example, environmental and/or social impacts attributed to lead firms’ value chains. As to their legal basis, obligations may be embedded in existing reporting mechanisms or constituted ad hoc. If immersed in existing reporting mechanisms, their most logical legal setting is often consumer protection, securities legislation or financial reporting. In addition to disclosure and due diligence obligations, transnational sustainability laws may also be connected to criminal law, particularly in the case of anticorruption legislation.

The content of due diligence, disclosure and other obligations varies. Most transnational sustainability laws do, however, assign lead firms with a broadly consistent duty to identify and disclose information about the enterprise’s structure, business and supply chain as well as risks and risk management. The material scope of transnational sustainability laws seems to be reflected in the content of obligations so that a broad material scope is typically accompanied by more relaxed reporting requirements. The EU NFRD, for example, has an exceptionally broad material scope but it also gives great leeway to the lead firm as to actual reported content. 108 By contrast, laws whose material scope is narrower provide more stringent criteria for the content of due diligence and disclosure obligations. The EU CMR, for instance, necessitates EU importers to draft a specific supply chain policy risk management plan. 109 The obligations are also often more complex than statutory language alone suggests. The EU CMR and the Dodd-Frank Act, for example, directly embed the requirements developed in the OECD’s Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas into their own operation. 110

While there seems to be, in general, an inverse correlation between a transnational sustainability law’s material scope and the specificity of disclosure obligations, there are exceptions to the rule. The French loi vigilance, for instance, requires companies to draft an extensive ‘vigilance plan’ which covers a broad range of environmental and human rights risks both in the enterprise context and with respect to supply chains. 111 The UK Modern Slavery Act is diametrically opposite to the French example as its material scope is narrow but, at the same time, its disclosure requirements are close to non-existent: In practice the minimum reporting threshold can be met by merely stating that no due diligence has been undertaken. 112 A third example is the UK Bribery Act which does not establish independent disclosure obligations. Instead, the law simply necessitates lead firms to maintain sufficient bribery prevention policies and procedures embedded throughout their operations, as doing otherwise can result in criminal liability. 113

As discussed above, transnational sustainability laws are distinctively transparency-oriented statutes. Failure to disclose information, however, is not generally sanctioned. Instead, the primary recourse against these failures is often procedural. The California Transparency Act, for example, maintains that the ‘exclusive remedy for a violation (…) shall be an action brought by the Attorney General for injunctive relief’. 114 Similar mechanisms are also included in the French loi vigilance 115 and the UK Modern Slavery Act. 116 Only a few laws establish financial sanctions such as fines, and even if they do, their possibility is often theoretical. Thus, even though the UK Modern Slavery Act contains a rule on financial penalties, in practice the lax disclosure obligations render them moot. The EU CMR and the EU NFRD, for their part, leave the development of possible sanction mechanisms to EU Member States. While there is not yet information available on the EU CMR sanction regimes, the experience with the national implementation of the EU NFRD suggests that EU-level sustainability laws are not usually accompanied with substantial financial penalties. 117

Transnational sustainability laws affiliated with securities regulation, however, enable the use of the latter’s sanction mechanisms. This is the case especially with the Dodd-Frank Act which offers multiple avenues for redress if the reporting company knowingly provides false or misleading information. 118 Violations of the US FCPA, also part of the same securities law framework, have resulted in significant sanctions both on the criminal and civil liability side. 119 Similarly to the FCPA, the UK Bribery Act penalizes companies involved in corruption with a discretionary fine. 120 The NSW Modern Slavery Act also contains a fine in case of false or misleading information. 121 The Dutch Wet zorgplicht kinderarbeid provides for a substantial administrative fine and even a possibility of criminal prosecution in the case of prolonged failure to meet the due diligence requirements. 122

In general, due diligence and disclosure obligations established in transnational sustainability laws require lead firms to pry open their value chain structure. Doing so may, however, increase the general risk of litigation that companies face. The question is fundamentally about the use of disclosed information on value chain structure and governance in civil law suits related to e.g. environmental degradation or hazardous working conditions. 123 The California Transparency Act and the French loi vigilance, for example, explicitly state that the statutes do not limit other legal remedies available. 124 By contrast, the Swiss law proposal incorporates a defence against civil liability if a lead firm has effectively implemented the statute’s risk management obligations. 125 Similarly, the UK Bribery Act establishes a defence from prosecution if the company has ‘in place adequate procedures’ to counter corruption, even if these failed to prevent corruption in practice. 126

Overall, transnational sustainability laws use due diligence and disclosure obligations to outline broad standards for adequate value chain governance. In most cases, however, they leave central definitions and the precise content of disclosed information to the discretion of lead firms. In practice, the nature and quality of reporting may vary significantly even within a single disclosure regime. 127 Moreover, the often minimal sanction and enforcement mechanisms embedded into transnational sustainability laws are unlikely to incentivize companies to improve their reporting practices. Against this backdrop, the most effective driver for developing standards of adequate value chain governance is likely to arise from private lawsuits. There are two reasons for this. First, while fragmented and obtuse, disclosure mechanisms nevertheless increase the information available on a lead firm’s value chain practices to aggrieved parties, potentially facilitating litigation. Second, effective statutory mechanisms for limiting liability may motivate companies towards more detailed and comprehensive reporting. A few transnational sustainability laws, such as the UK Bribery Act and the Swiss law proposal, already recognize this incentive and limit a lead firm’s liability in the case of adequate value chain governance, similarly to the well-known development risk defence of product liability law. 128

F. Summary

In sum, the image that transnational sustainability laws sketch of ‘value chains’, ‘lead firms’ and ‘adequate value chain governance’ is neither uniform nor precise. Instead, there is considerable variance as to how a value chain is understood, how the position of lead firms is conceptualized and what kinds of duties of governance the laws establish. These discrepancies notwithstanding, we contend that transnational sustainability laws constitute a significant response to major shifts in the modes and organization of production. In particular, their novelty lies in developing legal definitions through which national legislators attempt to govern global production, conceptualize the legal structure of the value chain and implement responsible value chain governance by regulating lead firms.

While the regulatory techniques used in transnational sustainability laws are fragile and still in their early stages, our comparison reveals that the importance of concepts like ‘value chain’, ‘lead firm’, and ‘adequate governance’ is not going to diminish in the near future. Rather than undermining the attempts that national legislators have taken to regulate the sustainability impacts of globalized production, the different framings of global value chains and the related variance in their legal definitions underline their centrality for future regulatory efforts. It is likely that these concepts will continue to develop from models of business management into legal categories that will shape both the logic of production and its regulatory infrastructure.

4. Conclusion: Towards a state-of-the-art of regulating global value chains

Transnational sustainability laws are a symptom of the geographical, organizational and legal fragmentation of production, which together have turned the regulation of global value chains into a burning issue across political, economic and legal planes. New transnational sustainability laws, requiring responsible value chain governance that extends beyond jurisdictional boundaries, differ markedly from earlier forms of regulation focusing on for example imported goods or value chains within an individual jurisdiction. Collectively, these laws provide a new perspective on regulating transnational production and its primary unit—the global value chain.

In this article, we have deployed a detailed comparison of current hard transnational sustainability laws and developed a conceptual framework for analysing their legal operability. Our comparison shows, in line with previous scholarship questioning the functional logic and effectivity of transnational sustainability laws, that the legal underpinnings of sustainability laws are similarly imperfect, incomplete and varied. Using this comparative realization as well as the historical exposition of the changing logic of production as a springboard, we have further developed an analytical framework which should enable seeing transnational sustainability laws as their own innovative and developing field instead of an eclectic collection of statutes. In our view, this field is characterized by three features: how transnational sustainability laws conceptualize 1) global value chains as their regulatory object; 2) lead firms as their regulatory subject; and 3) adequate value chain governance as their regulatory ideal.

As we hope to have shown in Section 3, focusing on these three features enables the meaningful comparison of transnational sustainability laws despite their many differences, as well as identification of the legal levers through which they operate. In a nutshell, comparing transnational sustainability laws from the perspective of how they develop legally operative conceptualizations of global value chains, lead firms and adequate governance should provide a toolbox of cognitive resources for arriving at a state-of-the-art of how global value chains can be legally understood. We hope that our approach helps to better analyse the current reach of transnational sustainability laws and also to develop new techniques though which global value chain capitalism can be governed. Even though the variance in the framing of global value chains and in their legal definitions across the investigated laws identified in this article can be seen to hinder the development of an overarching model of sustainable value chain governance, it also suggests that there are many avenues and openings available to national legislators to leverage transnational sustainability regulation.

While our analytical approach certainly exposes common traits in the current mix of transnational sustainability laws, it also invites further questions as to the root causes of their diverging legal conceptualizations that our comparative snapshot alone cannot explain. Despite their material similarity, the varied focus areas of transnational sustainability laws may mask deeper discrepancies between, say, instruments focused on the prevention of child labour and those attempting to curb trade in conflict minerals. The development of transnational sustainability laws over time may hint at another potential explanation for the variance in their legal operability. Further research, whether deployed from the perspective of private law, international law, private governance or global value chain theory, is still needed to flesh out the developmental trajectories of each transnational sustainability law. Moreover, a more nuanced exposition to historical developments, political and economic contexts as well as general corporate and contract law traditions of those jurisdictions that have decided to enact transnational sustainability laws will be needed to fully lay out the logic behind their architecture, design and implications.

Another set of questions raised by the variance in the legal operability of transnational sustainability laws relates to their operating logic and effectiveness and, as a consequence, to the future permutations of national sustainability regulation. As evidenced by early empirical scholarship, transnational sustainability laws based only on transparency through disclosure seem inadequate to address the problems of global value chain capitalism that they seek to solve. With this backdrop, new iterations of transnational sustainability laws clearly develop novel and potentially more effective approaches to governing global production. In addition to the proliferation of due diligence obligations, more recent transnational sustainability laws, such as the French loi de vigilance and the Swiss law proposal, contain features such as the legal-doctrinal definition of a value chain and the use of adequate governance as a liability limiting device that would probably have been unimaginable when the California Transparency Act was drafted. Whether they lead to more substantial changes in corporate behaviour than their predecessors is an open question but the proliferation of new regulatory mechanisms will certainly allow more systematic doctrinal and empirical analysis of the impact of transnational sustainability statutes in the future.

While transnational sustainability laws are certainly only one instrument in the broader matrix of sustainability governance, they open a unique view into the dynamics of sustainability regulation and the legal architecture that undergirds global value chain capitalism. Due to their novelty, our understanding of transnational sustainability laws’ legal operability is still under-developed. Our view is that comparative appraisal of current techniques and best practices of how transnational sustainability laws legally operationalize value chain governance, such as the one we have conducted in this article, is a vital tool in gauging their cumulative impact. With this backdrop in mind, we hope that our analysis facilitates further research not only in developing the law of global value chains but also in a range of disciplines related to law, such as political economy and sustainability science.

Footnotes

Funding

Publication of this research was supported by the Academy of Finland (p.n. 324037).