Abstract

Microcredit is a financial service whose importance is often understated. When lack of access to microcredit is exacerbated by a public health emergency such as the COVID-19 pandemic, its real significance as an essential service in poverty alleviation becomes more apparent. The outbreak and spread of the novel coronavirus (COVID-19) has led to dramatic transformations of every sector of the Nigerian society including microcredit delivery system, where formal and informal actors co-exist often in an uneasy relationship. Unfortunately, strategies for inclusive microcredit delivery before and during the COVID-19 pandemic are lacking in Nigeria, fuelling the further exclusion of informal sector in microcredit governance and policy process in Nigeria. The paper reviews the state of the COVID-19 pandemic in Nigeria and identifies policy gaps in microcredit delivery and governance mechanism. The study also highlights the linkages between COVID-19 and microcredit in poverty alleviation with a view to catalysing increased and inclusive access to microcredit and sustainability policy in Nigeria. It is argued that acknowledging the role of microcredit in informal economy and poverty alleviation is the critical first step towards framing a sustainable microcredit policy in which primary stakeholders are involved.

Introduction

The coronavirus pandemic that broke out in the city of Wuhan, China, on December 2019 and later spread to other parts of the world from early February, 2020 has expectedly worsened the fate of the poor in developing countries like Nigeria. The macroeconomic outlook for Nigeria and indeed the whole world has worsened since the outbreak of the pandemic (World Bank, 2020). The coronavirus pandemic affects the world in a way that has not been seen since World War II (International Monetary Fund [IMF], 2020). The pandemic has led to loss of lives, and death tolls around the world are, in many cases, unacceptably high (WHO, 2020). International trade has been disrupted as countries have shut their borders, and movement of people has been restricted in a bid to mitigate the spread of the virus across borders. International travels have been suspended with all planes grounded and cars parked. Schools have also been closed,as well as factories and workplaces (Wyplosz, 2020). Some employees are working from home, and the level of unemployment has increased tremendously all over the world even for developed economies (IMF, 2020). For a country like Nigeria, the picture is gloomier for obvious reasons.

Even before the pandemic, Nigeria was already battling the impact of poverty and was home to the highest number of poor people in the world (World Economic Forum [WEF], 2019). The pandemic has complicated the poverty situation in Africa and Nigeria, in particular, because of the multifaceted attack of the pandemic on the livelihood on the masses. This was affirmed by the African Union Ministers of Agriculture (African Union, 2020), when they remarked that:

the COVID-19 pandemic poses significant challenges to the already strained health, food and nutrition security and broad socio-economic conditions in Africa. …With the spread of the virus in the continent, containment measures, including social distancing and lockdowns, closing of schools, the prohibition of public gatherings and the closure of non-essential businesses and economic activities, will have far-reaching consequences. (p. 1)

The immediate consequence of the pandemic in Nigeria is worsening the poverty situation especially food shortage and malnutrition. Early in the year, the Government of Nigeria had placed poverty alleviation in the front burner in the 2020 budget proposal (Budget Office of the Federation [FGN], 2020). This was the fifth year in succession that the federal government of Nigeria (FGN) has placed poverty alleviation in the front burner of fiscal discourse and the president has pledged a substantial part of the national budget on poverty alleviation in line with Goals No. 1 and 2 of the Sustainable Development Goals of the United Nations (UN, 2015).

It is estimated that 92.5 million of the country’s population are poor, and half of this number lives in absolute poverty (WEF, 2019). Poverty is particularly severe in the rural areas, where up to 80% of the population there lives below the poverty line and have limited access to social services, infrastructures and credit (IMF, 2019). Women are particularly vulnerable to the scorch of poverty especially in developing countries like Nigeria (Bourguignon & Christian, 2002). The males in rural Nigeria have comparatively higher social status and as a result have more access to formal educational training and credit. Again, the men have higher capacity for higher productivity and can usually combine a number of enterprises, which allows them to have multiple sources of income (Deaton, 2015).

It has been shown that part of the experience in poverty alleviation efforts in Nigeria is that such efforts ‘almost always flounder due to scarcity of and restrictive access to loanable funds’ (Ijere, 1992, p. 32). The role of financial capital as a factor of production to induce economic growth and development and the need to channel credit to rural areas for economic empowerment of the rural populace can hardly be over-stressed. This was affirmed by Soludu (2015) where he remarked that ‘robust economic growth cannot be achieved in Nigeria without putting in place well-focused programme to reduce poverty through empowering the population at the rural areas by increasing their access to factors of production especially microcredit’ (p. 5). According to the Central Bank of Nigeria [CBN] (2006),

the latent capacity of the populace in the rural areas for entrepreneurship would be significantly enhanced through the provision of credit especially microcredit and microfinancial services to enable them engage in economic activities and be more self-reliant, increase employment opportunities, enhance household income and create wealth. (p. 10)

These were the reasons canvassed by the apex regulator for the re-christening and re-tooling of the erstwhile community banks to microfinance banks to enable them deliver more efficiently and effectively the services of providing microcredit and microfinance to the segments of the society who are ordinarily overlooked and under-served by the conventional banks (CBN, 2006).

The COVID-19 pandemic, like other pandemics in the past, do not only produce health shocks, but they also transmit economic shocks (Jackson et al., 2020). For instance, the IMF (2020) projects that every 10% decline in oil prices will, on the average, lower growth in oil-exporting countries by 0.6% and increase overall deficits by 0.8% of gross domestic product. For Nigeria, which is just recovering from a recession in 2016, the coronavirus pandemic effect on oil prices (the main source of revenue to the government) and lockdown on economic activities may completely wipe out the gains the country has recorded since coming out of recession in 2018. This will have impacts on the livelihood of households as well as performance of firms in Nigeria. For instance, as firm productivity dwindled due to lockdowns and closures, it feeds directly into the income and poverty level of households. To smoothen consumption, households will need a greater access to credit and this is where microfinance and microcredit will be crucial (Department for International Development, 2020; Civil Society Organization, 2020). As remarked by Gasper and Mauro (2020), there is still a blind spot in our understanding on the full impact of COVID-19 on household incomes and poverty level and the nature and quantum of support that might be needed to enable vulnerable households stay afloat.

Although there have been rapid studies on the effect of COVID-19 pandemic on households’ income and poverty level in advanced and emerging economies, there is still a dearth of similar studies in Nigeria. Unarguably, there may be on-going studies in this direction in Nigeria but currently, there is an empirical gap that provides a justification for this study to examine whether households in Nigeria are accessing credit at this time of pandemic when they needed it more than ever before. To bridge that empirical gap, this study was undertaken.

The study is divided into six sections. Section 2 is a brief review of the linkage between microcredit and poverty alleviation in Nigeria. Section 3 deals with the methodology of the study, while data for the study were presented and discussed in Section 4. In Section 5, we discuss the findings and Section 6 concludes the study with policy recommendation.

Review of Microfinance in Nigeria

Microfinance and Poverty Alleviation

Microfinance connotes provision of financial services to the poor and people at the lower strata of the society who are traditionally not served by the conventional financial institutions especially the commercial banks. Microfinance institutions are defined as institutions whose major business is the provision of microfinance services (CBN, 2006). Microfinance institutions were established to enhance the flow of financial services to the millions of the country’s populations in rural areas and the urban poor who are traditionally overlooked and underserved by conventional banks. In the past, the FGN had initiated a series of publicly funded micro/rural credit programmes targeted at the poor. Some of such notable programmes include: the Rural Banking Programme in 1977, the Sectoral Allocation of Credits with concessionary interest rate in early 1980s and the Agricultural Credit Guarantee Scheme of the CBN. Other institutional arrangements were the establishment of the Nigerian Agricultural and Cooperative Bank Limited (NACB), the National Directorate of Employment, the Nigerian Agricultural Insurance Corporation, the Peoples Bank of Nigeria (PBN), the Community Banks and the Family Economic Advancement Programme (FEAP). All these initiatives and programmes achieved limited success in channelling credit to the rural populace to enhance their means of livelihood.

In 2000, the FGN merged the NACB with the PBN (and FEAP to form the Nigerian Agricultural Cooperative and Rural Development Bank Limited) to enhance the provision of finance to the agricultural sector. The federal government also created the National Poverty Eradication Programme with broad mandate of eradicating poverty through provision of credit and employment opportunities.

The interest in the provision of microcredit has burgeoned in the last three decades in Nigeria. In recent times, multilateral lending agencies, bilateral donor agencies, developing and developed countries and non-governmental organisations all support the development of microfinance services (Chen & Martin, 2009). In consequence, microfinance has grown rapidly during the last two decades from an initial low enthusiasm to occupying the front seat in development discourse on poverty reduction and poverty alleviation.

Rationale for Microfinance in Nigeria

In Nigeria, the formal financial institutions provide services to about 35% of the economically active population, while the remaining 65% are excluded from access to formal financial services (Enhancing Financial Innovation and Access [EFInA], 2018). This 65% of the population are often served by the informal financial sector, through microfinance institutions, moneylenders, friends, relatives and credit associations including age grade and town union associations. The traditional microfinance institutions provide access to credit for the rural and urban low-income earners. They are mainly of the informal groups like rotating credit schemes (CBN, 2002, 2006, 2011, 2020). Other providers of microfinance include savings collections and cooperative societies. The informal financial institutions generally have limited outreach due largely to scarcity of loanable funds.

The CBN (2006) articulated the rationale for the establishment of microfinance institutions in Nigeria. According to the apex body, providing efficient microfinance services for rural dwellers and urban poor is important for a variety of reasons. These mainly include:

Improved access to and efficient provisions of savings, credit and insurance facilities, in particular, can enable the poor to smoothens their consumption, manage their risks better, build assets gradually, develop microenterprises, enhance their income-earning capacity and enjoy an improved quality of life. The improvement of resource allocation, promotion of markets and adoption of better technology to promote economic growth and development especially at the rural areas. Permanent access to institutional microfinance by the poor households so that they can actively participate in and benefit from development opportunities. Providing an effective way to assist and empower the poor women, who make up a significant proportion of the poor and suffer disproportionately from poverty. Contributing to the development of the overall financial system through integration of financial markets.

For more detailed literature on microfinance and rationale of microfinance in Nigeria, see Nwosu et al. (2015).

Microfinance and Rural Development

The quest to develop the rural areas in Nigeria and alleviate poverty at that level has been the avowed commitment of successive governments in Nigeria (Anyanwu, 2004). It is contented that unless the rural areas are developed, the rural dwellers that constitute the major population of the poor will continue to drag back economic development in the country (Soludo, 2006). However, we need an inquest on the characteristics of the rural dwellers for any meaningful policy approach Durrani et al. (2011). The World Bank defines a rural settlement as any settlement of less than 24,000 in population (World Bank, 2003). The World Bank expanded more on the features of rural communities to include those communities that lack in major infrastructural facilities, educational facilities, conservation in behaviour and access to financial services especially credit.

Okonny (2014) observed that the major difference between urban and rural communities including those located within major cities is the level of poverty. He noted that the rural people lack purchasing power enough to maintain a minimum standard of living. The rural people are known as the rural poor. An index of the poverty of this group is the low per capita outputs of agricultural produce like maize, cereals, plantains, melon seeds, fruits, vegetables, palm oil, groundnut oil and host of other Nigerian staple foods. A peasant farmer in the rural area hardly produces enough food to feed two families of about eight people (Adewunmi, 2016). According to Adewunmi (2016), the root cause of poverty in the rural areas can ultimately be linked to the low level of savings and investment in that part of the country.

It is the view of Okafor (1997) that rural development must be part of general economic development, which in itself is an increase in the material and non-material wellbeing of the people over time. The only difference between the two is the emphasis of the first on the rural sector. He argued that though agriculture is the predominant occupation in the rural areas, the rural problem is not limited to agriculture. Rural areas are inhabited by people engaged in agriculture and non-agricultural activities like services, commerce, mining and education. Indeed, a World Bank Survey in 2016 confirmed that approximately 72% of Nigerians live in the rural areas (World Bank, 2017). Since most Nigerians live directly or indirectly on the resources of the rural land, that is, rural areas, the rural economy forms the most important sector of the economy, and national economic development is dependent on them (Anyanwu, 2004). It suffices, therefore, to say that Nigeria’s economic development efforts cannot achieve any appreciable goal until they focus on the rural areas (Chibuike, 1999).

Conceptualisation of the Shockfrom COVID-19

The study adopted the ‘COVID-19 economic impact circular approach’ by Baldwin and di Mauro (2020). This framework abstracts from the very nature of the modern economy. As Pierre-Olivier Gourinchas (cited in Baldwin & di Mauro, 2020) aptly observes: ‘A modern economy is a complex web of interconnected parties: employees, firms, suppliers, consumers, banks and financial intermediaries. Everyone is someone else’s employee, customer, lender, etc.’. If one of this buyer–seller links is ruptured by the disease or containment policies, the outcome will be a cascading chain of disruptions. The framework places analytical spotlight on the transmission channel of the pandemic within the macroeconomy. For instance, the COVID-19 pandemic affects economic agents and disrupts the local and global value chain. This has implication on the livelihoods of households and firms.

As firm productivity declines due to closures and lockdowns occasioned by the pandemic, it trickles down directly into the income and poverty level of households who are both the suppliers of capital, labour and consumers of goods and services produced by firms. As firms shut down due to the pandemic, they will not be able to generate income for households who supply the labour. Moreover, with the shutdown, there will be short supply of goods and services which households need to maintain their standard of living. This will affect both consumption and standard of living and increase the level of poverty for households especially for those who are unable to access credit from formal or informal sources. Poverty level is often measured using economic dimensions based on income and consumption.

Preliminary reports by the IMF (2020) and World Bank (2020) show that COVID-19 will affect household income and consumption and could worsen the poverty level in developing countries. However, access to microfinance could mitigate the impact of the pandemic on household income and consumption. Microfinance is a globally recognised poverty alleviation strategy. It is widely recognised that access to microfinance in developing countries empowers the poor (especially women) while supporting income-generating activities, encouraging the entrepreneurial spirit and reducing vulnerability. For instance, Khandker (2005) in a study using panel data from Bangladesh found that access to microfinance helped to alleviate poverty in rural communities in Bangladesh. Similar studies by Lashley (2004) in the Carribean, Akanji (2006) in Nigeria, Imai et al. (2010) in India, Nawaz (2010) in Bangladesh, Montgomery and Weiss (2011) in Pakistan and Okibo and Makanga (2014) in Kenya all came to the same conclusion that microfinance is a veritable tool to alleviate poverty by empowering the poor and supporting income-generating activities of households especially those in the rural areas.

Similar results were obtained in selected cross-country studies, namely Mwenda and Muuka (2004), World Bank (2007), Westover (2008), Durrani et al (2011), Das and Bhowal (2013) and Banerjee and Jackson (2017). These studies show unequivocally that microfinance had salutary effects on poverty reduction in the selected countries and communities covered by the studies. More recently, studies by Stephen (2020) found that access to microfinance has helped to mitigate the impact of the COVID-19 on the income and income-generating activities of households in low-income countries in Asia. Similar results were obtained by Nathan and Lise (2020) in Paraguay and Bernard (2020) in selected poor and rural communities in Sri Lanka. Unarguably, there is a broad consensus that access to microfinance could mitigate the economic shocks occasioned by the COVID-19 pandemic on households’ income and means of livelihood.

Methodology

Area of Study

The area of study is Ido Local Area in Ibadan, the Oyo State capital. Oyo State is an inland state in South-Western Nigeria. It is bounded in the north by Kwara State, in the east by Osun State, in the south by Ogun Stateand in the west partly by Ogun Stateand partly by the Republic of Benin.

Ibadan as a city was created in 1829 as a war camp for warriors coming from Oyo, Ife and Ijebu of South Western Nigeria. It was a forest site with several ranges of hills, varying in elevation from 160 to 275 m (Mabogunje, 1962). The economy of Ibadan rested largely on agriculture (yam, maize, vegetables, etc.), manufacture (mainly weapons, smithery, cloth and ceramics industries) and trade (palm oil, yam, kola for export, shea butter, salt, horses and weapons from outside).

For administrative convenience, the study was restricted to Ido Local Government Area. The area was purposely chosen because of the presence of rural and urban settlements within the community. Ido is one of the 33 Local Government Areas in Oyo State. Prominent communities in Ido Local Government Area are: Akufo, Apete, Ijokodo, Ologuneru, Oloje, Ido, Alako, Ilaju, Omi-Adio, Bako, Apata, Gbekuba, Morakinyo, Akinware and Idiiya. It has an area of 27 km2 and a population of 156,988 according to the Oyo State Government in 2017. It also has bustling economic activities with the presence of the markets, banks, public institutions, schools and churches. By climatic conditions, Ido LGA enjoys tropical conditions, and rainfall is usually higher from April to July and September to October. Average temperature is 34°C but humidity can be as high as 90% (Mabogunje, 1962). Inhabitants of Ido Local Government Area are predominantly farmers, traders, artisans, factory workers and white-collar workers as a result of its proximity to Ibadan North and Ibadan North-West Local Government Area—the commercial hubs of Ibadan town.

Study Design and Sampling

The survey research design was adopted. Primary data were collected through structured questionnaires. The questionnaire was constructed from the World Bank 2017 Global Findex Questionnaire. The Findex Questionnaire is a standard questionnaire used to elicit information on a wide range of areas related to financial inclusion, access to credit, use of banking services and so on. The questionnaire was complemented by personal interviews. Specifically, questionnaires were administered to selected households within Ido Local Government Area, Ibadan, Oyo State, Nigeria within the period, March–April 2020. Officials of some microfinance institutions, cooperative societies and community leaders were interviewed.

The study adopted the multi-stage sampling technique to select the respondent households for the study because of the large size of the area. The first stage involves the random selection of 14 rural and semi-urban communities that make up the council. The second stage involves the random selection of 29 households per community, making a total of 400 households. The 400 households were administered with a structured questionnaire. Selected rural credit associations and well-known money lenders were interviewed to validate the responses from the questionnaires.

Administering the Questionnaire

The questionnaires were administered directly (face to face) to the respondents with the help of research assistants who are familiar with the area and the local language. The purpose of the study and items in the questionnaire were well explained to the respondents. Those who could write fill in the questionnaire themselves and others who could not write were assisted in doing so. The research assistants were given face masks and hand sanitizers and were assigned to communities that were contiguous to minimise long-distance travel because of the lockdown in Oyo State at the time of the research. All the questionnaires administered were completed and returned same day they were administered. It took the researcher and the research assistants 1 week to complete the administration.

Estimation Method

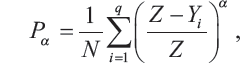

The combinations of statistical and econometric techniques were employed in analysing the data for the study. First, the socio-economic characteristics of the household respondents were descriptively analysed. Second, the technique of Foster et al. (1994) was employed to assess the poverty index, the incidence, depth and severity of poverty among respondent households. The FGT poverty measure is defined as

where α is a non-negative parameter (0, 1 or 2) reflecting social valuation of different degree of poverty. It takes on a value of 0 for poverty incidence, 1 for poverty depth and 2 for severity of poverty. Y is per capita expenditure (N/person/day), q is the number of households with per capita consumption below the United Nations defined US$2.00 per person per day which was equivalent to N720.00 per person per day (US$1 = N360) at the time of the survey. Z is the poverty line (N720.00 per person per day) and N is the number of households in the sample.

Third, we employ the Logit Regression Model to determine the influence of independent variables on the probability of being poor. The dependent variable is the poverty status that is represented with a binary dummy (0 and 1). The independent variables are age (years), age2, gender (female = 1, male = 0), education (years), household system (number), dependency ratio, credit use (yes = 1, no = 0), credit volume (₦) and other jobs (₦).

Data and Discussion

In this section, we analyse descriptively key demographic characteristics of the respondents in the surveys that are relevant to the study. We then present and analyse the incidence, depth and severity of poverty in the area using econometric and inferential statistics.

Socio-Demographic Characteristics of the Respondents

Key Demographics of the Respondents

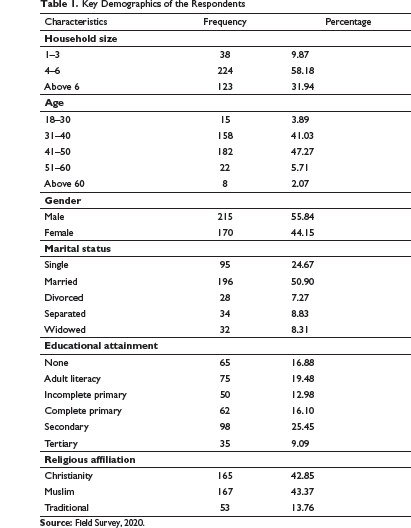

In terms of gender, the result in Table 1 shows that there was a fair spread in gender distribution of the respondents with a slightly higher number of males at approximately 56% of the total respondents. In terms of marital status, the result shows that majority of the respondents are married (50%). Those that are single constitute approximately 25% of the total respondents. Those that are divorced, separated and widowed constitute approximately 7%, 9% and 8%, respectively. In terms of educational attainments, the result in Table 1 is consistent with the level of development of the study area. Majority of the respondents had secondary school education, approximating 25% of the total distribution. There was also ample number of the respondents without any form of education. This group accounts for approximately 17% of the total distribution, while those with tertiary education constituted the least respondents in the distribution approximately 9% of the total respondents.

Finally, Table 1 shows equal distribution in the two major religions in Ibadan, namely, Christianity and Islamic religions, both of which accounted for 43%, respectively. There was also ample number of respondents who still practice the traditional religion (approximately 14%) of the total respondents.

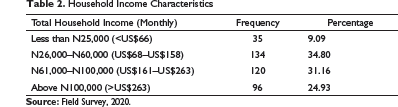

Household Income Characteristics

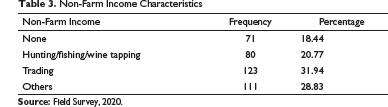

Non-Farm Income Characteristics

Extent of Banking Depth, Use and Credit Availability

This section interrogates the respondents on the extent to which they use banking services.

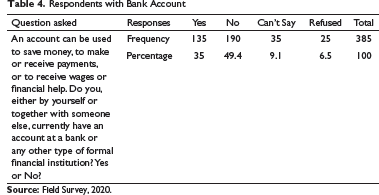

Respondents with Bank Account

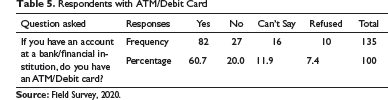

Respondents with ATM/Debit Card

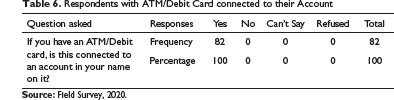

Respondents with ATM/Debit Card connected to their Account

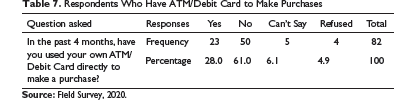

Respondents Who Have ATM/Debit Card to Make Purchases

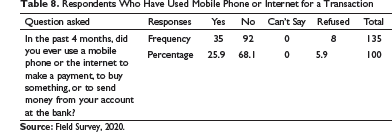

Respondents Who Have Used Mobile Phone or Internet for a Transaction

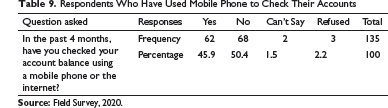

Respondents Who Have Used Mobile Phone to Check Their Accounts

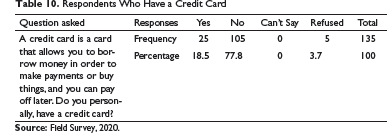

Respondents Who Have a Credit Card

Table 10 shows that majority of the respondents, approximately 78%,do not have a credit card that can allow them to borrow money from the bank to make transactions. This shows that majority of the respondents do not enjoy this credit arrangement from their banks.

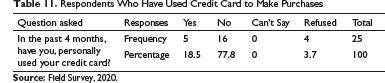

Table 11 shows that for the few of the respondents that have credit card, only about 19% have made use of the card in the past 4 months. This shows reduced credit transactions within the period under review.

Respondents Who Have Used Credit Card to Make Purchases

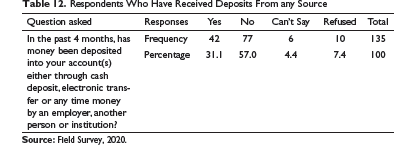

Respondents Who Have Received Deposits From any Source

Unbanked Section—Those With No Bank Account

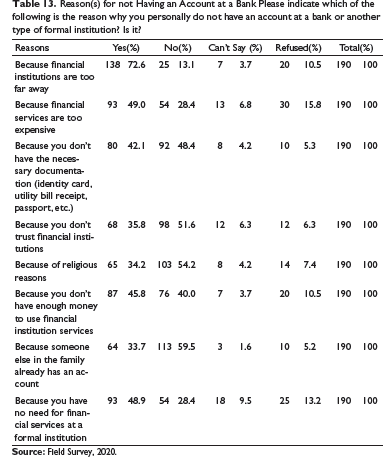

Reason(s) for not Having an Account at a Bank Please indicate which of the following is the reason why you personally do not have an account at a bank or another type of formal institution? Is it?

Savings Section

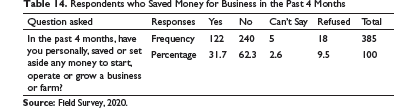

Respondents who Saved Money for Business in the Past 4 Months

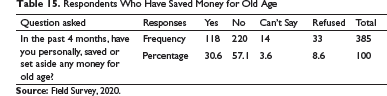

Respondents Who Have Saved Money for Old Age

Table 15 shows that majority of the respondents, approximately 57%, have not saved or set aside any money for old age. This means that majority of the respondents are currently concerned with surviving in this period of the pandemic than thinking for old age.

Borrowing Section

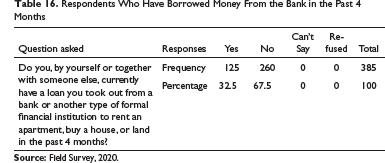

Table 16 shows that majority of the respondents, approximately 68%, have not taken out any loan from a bank or another type of formal financial institution in the past 4 months. This means that majority of the respondents have no financial support from the bank or any other type of financial institution in this period of the pandemic.

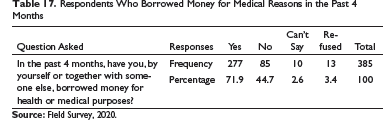

Table 17 shows that majority of the respondents, approximately 72%, have borrowed money for health and medical reasons. This is understandable given the health challenges posed by the coronavirus pandemic and the stress occasioned by loss of jobs, lockdown and restrictions in movement.

Respondents Who Have Borrowed Money From the Bank in the Past 4 Months

Respondents Who Borrowed Money for Medical Reasons in the Past 4 Months

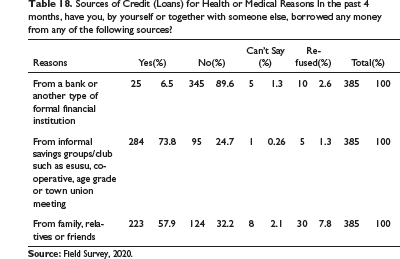

Sources of Credit (Loans) for Health or Medical Reasons In the past 4 months, have you, by yourself or together with someone else, borrowed any money from any of the following sources?

Financial Resilience Section

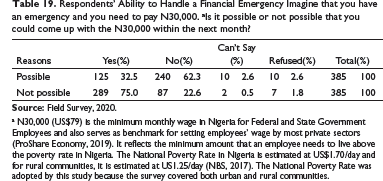

Table 19 shows that majority of the respondents, approximately 62%, stated that it is not possible for them to come up with the sum of N30,000 (US$79 at N380/US$1) over the next 1 month in the event of emergency. This shows that the financial resilience of majority of the respondents is very low at this time of the pandemic.

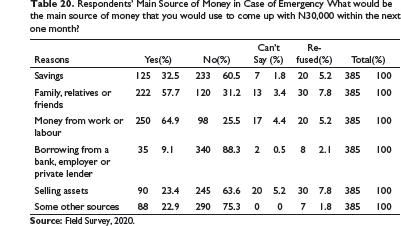

From Table 20, majority of the respondents stated that their main source of income/money in the case of emergency will be from work or labour. The next source of money will be from family, friends and relatives and followed by money from personal savings. Selling assets and some other sources followed in that order. Remarkably, borrowing from a bank, employer or private lenders were the least source of money in the case of emergency. This implies that financial inclusion and microcredit are yet to take root in the informal sector.

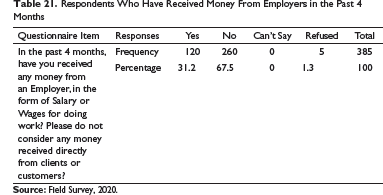

Table 21 shows that majority of the respondents, approximately 68%, have not received any salaries from their employers for the past 4 months, which coincided with the onset of the coronavirus pandemic which have seen offices and shops closed in Nigeria. Only about 30% of the respondents have received salaries from their employers for the period under review.

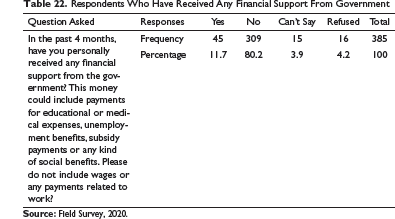

Table 22 shows that an overwhelming majority of the respondents, approximately 80%, have not received any kind of financial support from the government for the past 4 months. In other words, only very few people may have benefitted from the conditional cash grants from government for vulnerable households. The implication is that majority of Nigeria are left to cater for themselves as this critical period of the pandemic.

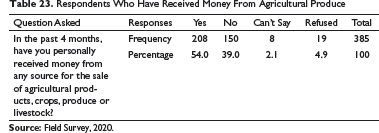

Table 23 shows that majority of the respondents, 54%, has relied on income from the sale of agricultural products, crops, produce or livestock for survival in the past 4 months.

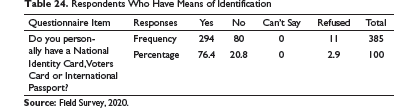

Table 24 shows that majority of the respondents, approximately 76%, have means of identification in the form of national identity card, voters’ card or international passport. Majority have voters’ card as a means of identification. The reason for the preponderance of voters’ card is that it is used to access ‘stomach infrastructure’ 1 from politicians during electioneering campaigns.

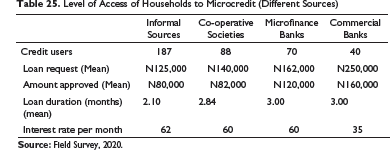

Table 25 summarises the level of access of households to microcredit from different sources. The table shows that a larger percentage of the respondents sampled access microcredit from informal sources like family, friends, local money lenders, esusu arrangements and so on. In terms of loan request, the mean amount usually required are N125,000 from informal sources, N140,000 from co-operatives, N162,000 from Microfinance institutions and N250,000 from commercial banks. However, on the average, N80,000 are usually accessed from the informal sources, N82,000 from co-operative societies, N120,000 from microfinance institutions and N160,000 from commercial banks. Moreover, the average loan duration for loan facilities from informal sources is 2 and 3 months for co-operatives, microfinance institutions and commercial banks, respectively. Again, the interest rate ranges up to 62% per annum from the informal sources like the local money lenders, 60% per annum for co-operative societies and microfinance institutions, respectively, and 35% for commercial banks.

Respondents’ Ability to Handle a Financial Emergency Imagine that you have an emergency and you need to pay N30,000. aIs it possible or not possible that you could come up with the N30,000 within the next month?

a N30,000 (US$79) is the minimum monthly wage in Nigeria for Federal and State Government Employees and also serves as benchmark for setting employees’ wage by most private sectors (ProShare Economy, 2019). It reflects the minimum amount that an employee needs to live above the poverty rate in Nigeria. The National Poverty Rate in Nigeria is estimated at US$1.70/day and for rural communities, it is estimated at US1.25/day (NBS, 2017). The National Poverty Rate was adopted by this study because the survey covered both urban and rural communities.

Respondents’ Main Source of Money in Case of Emergency What would be the main source of money that you would use to come up with N30,000 within the next one month?

Respondents Who Have Received Money From Employers in the Past 4 Months

Respondents Who Have Received Any Financial Support From Government

Respondents Who Have Received Money From Agricultural Produce

Respondents Who Have Means of Identification

Level of Access of Households to Microcredit (Different Sources)

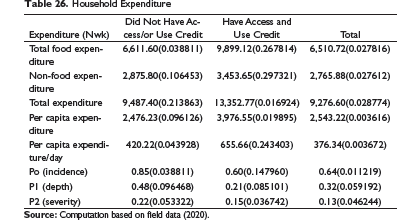

Household Expenditure

Summary of Logit Regression

*Correlation is significant at 0.01, ** at 0.05 and *** at 0.10 level (two-tailed).

Incidence, Depth and Severity of Poverty

To ascertain the incidence, depth and severity of poverty among the households sampled, the study used the expenditure approach. To achieve this, the study aggregated the total expenditure on food and non-food items by the households sampled. The households were divided into two, namely those that access and use microcredit and those that did not use credit. The Foster–Greer–Thorbecke (FGT) technique described previously was employed to assess the poverty index, the incidence, depth and severity of poverty among respondent households. The following estimates were obtained as reported in Table 26.

Table 26 shows that households that had access to microcredit has higher total aggregate expenditure (N13,352.77) that households that did not access and use microcredit (N9.487.40)—a difference of approximately N387 (or 40%). Again, the per capita expenditure (derived by dividing the total expenditure of household by the total size of the household) shows that those who have access to microcredit have higher per capita expenditure, all other things being equal. It should be noted that per capita expenditure is influenced by the total expenditure and the size of the household. In other words, the higher the household size, the lower would be the per capita expenditure and vice versa.

To this end, the per capita expenditure for households that did not access or use microcredit was N2,476.23 per week, while for the households that use microcredit it was N3,976.55 per week. This translates to an average of N420.22 and N655.66 for households without microcredit and households with microcredit, respectively. This again shows that households with microcredit have higher per capita expenditure per week. In terms of incidence of poverty among the respondent households, the data in Table 26 shows that the incidence of poverty was higher on the households without access to microcredit (0.85) than the households with access to microcredit (0.60). There was similar trend for depth and severity of poverty. For instance, for households without access to microcredit has higher depth of poverty (0.48) than households with access to microcredit (0.21), more than doubled. The severity of poverty was also higher for households without access to microcredit (0.22) than for the households with access to microcredit (0.15).

In terms of households that are living below the poverty line, estimated at US$1.70/dayon purchasing power parity (World Bank, 2019), the data in Table 31 shows that the average per capita expenditure for all the households was N420.22 for households without access to microcredit and N655.66 for households with access to microcredit, respectively. The implication is that access to microcredit increases the chances of households not being poor. For the households without access to microcredit, their fate is different and requires urgent government attention with appropriate poverty alleviation strategies and programmes. Unfortunately, the study showed that majority of the households surveyed (approximately 80%) have not received any form of government assistance or palliatives during this period of the coronavirus pandemic.

Impact of Microcredit on Poverty Alleviation

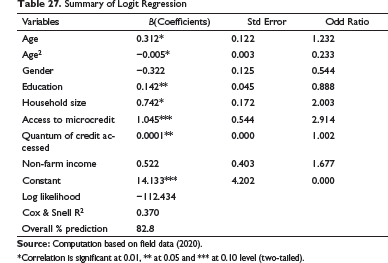

To ascertain the impact of microcredit on poverty alleviation, we estimated the influence of access to microcredit on the probability of being poor or non-poor. Poverty as the dependent variable was proxied by average per capita expenditure of US$1.70/day or NGN614. A household with average per capita expenditure less than US1.70/day is considered poor and household with average per capita expenditure above US$1.70/day is considered non-poor. Microcredit was proxied by the natural logarithms of the quantum of microcredit accessed by a household. Other explanatory variables that could influence the probability of being poor or non-poor were also analysed. Using the logit regression model previously, the following information was obtained as shown in Table 27.

Table 27 is a summary of logit regression on a model that incorporates explanatory variables that could influence the likelihood of a household being classified as poor or non-poor. These explanatory variables include age, age 2 , gender, education, household size, access to microcredit, quantum of microcredit accessed and non-farm income. As remarked above, a household is either poor or non-poor based on a poverty line defined as the average per capita expenditure of US$1.70 or NGN641/day. A household is considered poor if the average per capita expenditure is below US$1.70 or NGN641/day.

The logit model is significant in predicting the likelihood of a respondent household being poor or non-poor based on the expenditure approach. The predictive power at 82.8 is high and reliable. The model shows that microcredit use or access to microcredit increases the likelihood of not being poor and living above the poverty line. The result also showed that the quantum of microcredit accessed has positive and significant influence on the probability of not being poor. In other words, the higher the quantum of microcredit accessed, the lower the probability of being poor.

Moreover, most of the explanatory variables in the model were significant at 1% (p < 0.01). These include age of head of household, square of the age and household size. Others were significant at 5%level (p < 0.05) and 10% level (p < 0.10). These include educational level of head of household. For instance, the model shows that the likelihood of being poor rises initially with increase in household size but decline afterwards, perhaps, as more family members enters the productive age bracket or become more productive in their occupation, all other things being equal. The result also shows that education is a significant variable. The coefficient is positive and significant at 5%level (p < 0.05). It means that the higher the level of education of the head of household, the higher the likelihood of the household not being poor, other things being equal.

The most important observation in the model is that access to and the quantum of microcredit accessed by a household lowers the odd of being poor. This result meets theoretical expectations.

Various policies on poverty alleviation by development partners including the World Bank and IMF emphasised the need for access to credit by households especially those in the rural areas. The expectation is that access to microcredit will enable the populace in the rural areas to enhance their means of livelihood and increase their odds of escaping from the trap of extreme poverty. Unfortunately, the study shows that majority of the households sampled (approximately 68%) lacked access to microcredit and are unable to access microcredit from formal financial institutions.

Discussion of Findings

In discussing the findings of this study, the key question is to what extent has the coronavirus pandemic impacted on access to microcredit and hence poverty alleviation in Nigeria. To put the discussion in context, we compare the findings of the study with the result of the survey on ‘Access to Financial Services in Nigeria 2018 Survey’ conducted by Enhancing Innovation and Access (EFInA, 2018). 3 The 2018 survey by EFInA is the largest, most comprehensive and up-to-date survey on access to financial services in Nigeria.

Findings from the study showed that:

About 35% of adults in the survey have account or banking relationship with a financial institution. The remaining 65% are currently excluded from the financial system. This is approximately 200 basis point decline in the number of adults with account relationship based on the country-wide survey in 2018 by EFInA (2018). In the 2018 survey, the number of adults with no account or banking relationship was 39.7% out of the estimated 99.6 million adults in Nigeria (EFInA, 2018). This means that the financial inclusion strategy launched by the government in 2012 has not yielded much result in bridging the gap of unbanked population especially at the rural areas. About 40% of those who have account relationship with banks are making use of electronic platforms like ATM/Debit cards, phone or the Internet in financial transactions. This represents an increase of 6% from the 36% level in the 2018 survey by EFInA (2018). This shows that the coronavirus pandemic has forced more people to use electronic platforms like ATM/Debit cards, phone or the Internet in financial transactions as a result of the lockdown ordered by various tiers of governments in Nigeria to contain the spread of the virus. Approximately 19% of account holders have credit cards that allow them to borrow money to make payments and pay later. This represents a decline of 12% from the 31% recorded in the 2018 nationwide survey by EFInA (2018). This means that the coronavirus pandemic has worsened the state of credit accessibility from banks and other formal financial institutions in Nigeria. The COVID-19 pandemic has affected households’ income. Only about 20% of households have received any form of income in the past 4 months—the period that coincides with the onset of the coronavirus pandemic. This contrast sharply with the 82% of households that receive income within the same period in the 2018 survey by EFInA (2018). Elsewhere, a study by Stephen (2020) showed that low-income and poor households across Asia have been hard hit by the coronavirus pandemic. According to the study, the economic and financial impacts flowing from lockdowns to curb the spread of COVID-19 have been severe in most Asian countries, with substantial declines in the incomes of people at the base of the economy, many of whom rely on microfinance to manage their household or microenterprise cash flows with average declines in income in Pakistan (85%), Bangladesh (75%) and India (70%). There has been very little financial support from the banks by way of credit to households during the past 4 months. Less than 5% of the households surveyed have received any form of credit facilities from formal financial institutions like the microfinance banks and commercial banks. This represents a decline of 26% from the figure in the 2018 survey. According to the 2018 survey, 31% of the 99.6 million adult populations in Nigeria had access to credit in 2018 (EFInA, 2018). Moreover, 32% of the households that accessed credit did so through informal sources like the co-operative societies and local rotating credit associations. Government support to households by way of palliatives has been very little or non-existent. Only about 12% of the households have received any form of support from the government during this time of the pandemic. Moreover, government palliative consisting mainly of conditional cash grant of N5,000 (approximately US$13) for average household size of 5.2 is grossly inadequate and amount to merely scratching the surface. The level of financial resilience is low among households surveyed. Only about 32% of the households can handle financial emergencies involving sums up to N30,000 (US$78) in a month should the need arises. The lack of insurance coverage for most households in Nigeria has also complicated matters in a health emergency such as the coronavirus pandemic. According to the 2018 survey, approximately 98 million adult Nigerians have no insurance coverage of any kind (EFInA, 2018). Households’ general welfare and wellbeing has deteriorated within this period of the pandemic. However, households who have access to microcredit have fared much better than those with no access to microcredit. This finding corroborates the findings of the study by Nathan and Lise (2020) who found that rural households in Paraguay and Myanmar that had access to microcredit fared better during this coronavirus pandemic than the households that did not have access to microcredit. Moreover, a study by Bernard (2020) in three rural districts in Sri Lanka, namely Gampala, Amara and Affna, found that out of the 500 women sampled, those who receive credit from Microfinance Banks had little problem smoothing household consumption, engaging in trade and generally not badly affected by the coronavirus pandemic than those who did not receive any credit from any financial institution. Overall, in majority of the households surveyed, approximately 83% are living below the poverty line measured by household income of US$1.70 per day. If this figure is weighted to provide for the total adult population and benchmarked to national population estimates, this translates to approximately 96 million people living below the poverty line with 63.3% of this number living in the rural areas.

Conclusion and Recommendations

From the foregoing, we can conclude that the coronavirus pandemic has affected the means of livelihood of majority of the masses, with majority living in extreme poverty. The situation is compounded by lack of access to microcredit from the microfinance banks and other formal financial institutions. The government has not helped matters either. Government palliatives are non-existent in most of the communities surveyed with only about 12% of the households surveyed had received some form of government support within the period under review.

Based on these findings, the study recommends as follows:

Government should rethink its policy on microcredit delivery through the microfinance banks and rural banking scheme of commercial banks. The findings of this study have shown that these formal institutions have not lived up to expectations especially at this period of the coronavirus pandemic. Government may consider bringing in the informal sector groups like co-operative societies and local thrift associations in microcredit framework. These informal groups have co-existed with the formal financial institutions in an uneasy relationship. The time has come for government to formalise this existence and perhaps channel microcredit support through these informal institutions. Government should re-gig the financial inclusion framework. The number of adults with no bank account or any banking relationship with banks is still unacceptably high. In most of the cases, having a bank account is the necessary first step to accessing bank credits. Majority of the respondents who have no bank account blamed it on the absence of banks within their communities. The government may have to reintroduce the rural banking scheme or reinstate the community development ownership model for microfinance banks to encourage more communities to open and operate their own microfinance banks. The government should also ensure the provision of infrastructures, especially electricity and good roads in the rural communities. No bank would want to set up a branch in a community where these key infrastructures are lacking; neither would a community-based microfinance banks survive in that type of business environment. The government should spread its net to cover more people in the distribution of palliatives. The COVID-19 has wreaked havoc on the means of livelihood of the masses especially those in the semi-urban and rural communities. The government should, therefore, increase the quantum and coverage of its palliative measures especially the conditional cash grants to vulnerable families.

Footnotes

Declaration of Conflicting Interests

Funding

The author received no financial support for the research, authorship and/or publication of this article.