Abstract

The effectiveness of environmental tax (ET) in addressing environmental and climate-related challenges has been the most debatable issue among policymakers. Whether ET can effectively promote renewable energy remains an open question, especially in Africa, where most nations rely heavily on fossil fuel export revenues. This study, therefore, investigated the impact of ET on renewable energy production (REP) and consumption (REC) in Sub-Saharan Africa (SSA). To this end, the study implemented the dynamic common correlated effects (DCCE) model on panel data of 22 countries from 2000 to 2023. Considering the interconnection between REP and REC, the findings indicate that ET hinders REC but improves REP in the long term. In addition, the moderating effect of corruption is negative for both REC and production, possibly suggesting the driving role of corruption in misallocating tax revenues with detrimental effects on renewable energy producers and end users. Moreover, although there is evidence of Granger causality from ET to REP, the ET does not cause REC, while there is no predictive effect between REC and REP in either direction. Consequently, in order to boost accountability and transparency in the distribution of tax revenue and guarantee that funds adequately support investments in renewable energy, SSA governments and policymakers should concentrate on strengthening governance and anti-corruption measures.

Keywords

Introduction

Renewable energy plays an important role in enhancing access to energy in rural areas, ensuring sustainable development, alleviating poverty, and boosting infrastructure advancements that revolve into the overall economic progress. It has the potential to decrease dependence on fossil fuels, increase energy security, and generate green employment in Africa, alleviating environmental and energy pressures (International Energy Agency [IEA], 2020). A shift towards clean energy will allow Sub-Saharan Africa (SSA) to achieve climate targets and minimise vulnerabilities attributed to its predominantly agriculturally-oriented economies (United Nations Economic Commission for Africa, 2020). The focus on the use and production of renewable energy goes along with the realisation of Sustainable Development Goals (SDGs) 7 (clean energy), SDG 8 (economic growth), and SDG 13 (climate action). The IEA (2022) indicated that clean energy investments were in the range of 1%–4% of gross domestic product (GDP) in leading economies, emphasising their economic prospects. Governments in SSA have embraced environmental taxes (ETs) to promote the use of renewable energy consumption (REC) and its renewable energy production (REP), increase the prices of fossil fuels and energy efficiency.

Africa contributes only about 3% of the total energy-related CO2 emissions, the lowest per capita in the world, though it has approximately 20% of the world’s population (International Monetary Fund [IMF], 2023). The amount of tax revenue collected in African nations based on environmental considerations has grown to 1.62% of GDP in 2017–2022, to 1.62% in 2023 and 1.4% in 2018 (IMF, 2023). The energy taxes raise 75% of ET revenues on the continent in terms of tax resources (Africa Revenue Statistics, 2023), including gasoline and excise duties. Between 2018 and 2022, hydropower generation increased by 25%, whereas the growth of solar and wind power was 13% and 11%, respectively (Pricewaterhouse Coopers [PwC], 2023). Over 24 GW of additional renewable sources have been added since 2013, and it is expected that they will grow to 1.8 EJ in 2022 and reach 27.3 EJ by 2050 (PwC, 2023). Nevertheless, the renewable capacity of SSA was insufficient, amounting to 56 GW in 2022, which is only 1.9% of the world’s investment, relative to Europe (830 GW) and Asia (1,200 GW) (Africa Energy Outlook, 2023). Even though the target is set at 300 GW by 2030, 43% of the SSA population does not have access to electric power, with the problem of income inequality being one of the factors that decreases affordability and access to off-grid systems such as solar home systems. Financing and subsidies are the key to equal access to renewable energy. In SSA, the share of REC in total final energy use rose by 53% in 2000 to 66% by 2023, primarily because of the traditional use of biomass and low rural electrification. REP, however, increased only to 2% of global investment, moving upwards to 56 GW by 2023. In Nigeria and Angola, there are predominant fossil fuels. The current ET regimes are weak and frequently depend on fuel-based taxes over carbon pricing, and are still applied differently among the countries (Nchofoung et al., 2022).

Theoretically, most traditional energy companies are expected to move towards renewable energy sources, particularly in industries that consume more energy. Through this, green innovation has been boosted by the ETs, which challenge them to innovate new technologies (Aydin & Bozatli, 2023). Governments are supporting this transition by imposing taxes on pollutants and providing subsidies to the renewable sector, which encourages the more environmentally friendly energy systems (Bashir et al., 2021). Companies implement clean technologies when the costs of conversion are less than the taxes that are levied. Although ET can enhance renewable investment and long-term gains, the uncertainty of policies can be discouraging to any potential long-term improvement.

In the context of the above, the current literature on ET is mostly oriented around the emission-reduction perspective (Li et al., 2021). Nonetheless, there is little literature that examines the influence of ET on the REC, and even fewer research studies consider both REC and REP. Aydin and Bozatli (2023), for instance, dwelled on REC and did not pay attention to the double effect. To understand completely, the role of ET in the energy sector, a thorough analysis of both REC and REP is necessary. Concentrating on consumption does not consider the dynamics of supply and innovation, whereas studying production fails to appreciate the demand responses. Such a dual analysis would help policymakers to achieve a balance between the supply and demand of renewable energy sources, resulting in sustainable energy development. In addition, REC and REP might have different reactions toward ET, and more especially in corruption-stricken areas. Even though ET is designed to discourage fossil fuel consumption, weak enforcement caused by corruption can cause tax evasion and less development of responsiveness among consumers. Corruption further interferes with renewable energy investments as it shifts the funds and restricts the development of infrastructure. Therefore, it is important to include corruption, which acts as a moderating factor, particularly in SSA, where the weakness of institutions is prevalent. Additionally, conducting a panel Granger causality allows the identification of whether ET can predict the variations in REC or REP (Bahar & Silva, 2020). Lastly, the analysis of the long-term relationships will provide additional insights into the efficacy of ET to provide more sustainable policy formulation (Stern, 2020).

Against the above background, this study contributes to the body of literature by assessing the impact of ET on REC and REP among SSA nations. The impact of ET, from the renewable energy generation to end usage, can be examined by looking at these factors. Additionally, the analysis offers a more comprehensive view of the renewable energy process. Conversely, higher demand for renewable energy may stimulate further investments in REP. Furthermore, this study contributes by assessing how governance affects the efficiency of environmental policies through incorporating corruption as a moderating component. In regions with rampant corruption, taxes may not work as intended because corruption diverts resources from their efficient use (Ahmad et al., 2023). In addition, since the renewable energy sector is still in its infancy in SSA, it is also critical to assess the long-run benefits of ET and its effects on the production and consumption of renewable energy. Furthermore, the causal impact assessment provides crucial details on how developing countries might create ET laws that successfully strike a balance between economic growth and environmental sustainability.

The study’s remaining sections are as follows: Section II reviews the theoretical and empirical literature. Section III covers the study’s methodological approach; Section IV presents data presentation, analysis and interpretation. Section V concludes and provides policy recommendations.

Literature Review

Theoretical Framework

ETs result from a growing awareness of environmental issues, including underuse, inefficiency, careless use of natural resources, health risks associated with specific energy sources, environmental degradation, and climate change (OECD, 2016). ETs are policies designed to lower pollutant emissions and have a detrimental effect on greenhouse gas emissions (OECD, 2016). Hsu et al. (2021) saw ET as a tool that policymakers use to reduce energy usage, which varies depending on the economy and industry. Additionally, this tax targets activities considered harmful to the environment, and its purpose is to encourage ecologically friendly activities by providing financial incentives.

Several researchers, such as Hao et al. (2021), discussed the fact that ET is a necessity in global warming reversal, where the carbon emission levels are reduced. Karmaker et al. (2021) also verified the idea that ET will finally drive technological advancement, and this process will ensure that successful businesses accomplish their clean objectives. ET assists in managing total energy consumption and fosters energy efficiency, stimulating policymakers, industries, and residents to facilitate innovation in environment-driven technologies (Bashir et al., 2021).

ET is also an important tool for enhancing the development of renewable energy in Africa, mainly through furthering renewable energy technology use, especially in the transport tax policies. Emerging studies indicate that ET, together with a favourable renewable energy policy, is critical in resolving environmental irritations and encouraging sustainable development in the energy sector in Africa (Nchofoung et al., 2022). Theoretically, a rise in aggregate ET should increase REC in Africa (Abbas et al., 2023), with such taxes deterring the use of fossil fuels and providing funding to make clean energy investments. Furthermore, REP and REC are interconnected in the emerging energy value chain, as higher production enables greater availability for consumption, while rising demand reinforces the need for increased production capacity (Bahar & Silva, 2020). This mutual relationship highlights the relevance of harmonised policies to coordinate ET, production and consumption strategies and achieve the maximum use of renewable energy sources.

Theories such as the environmental Kuznets curve theory, the Porter hypothesis, the energy efficiency paradox theory, and the double dividend theory, among others, have emerged from the growing body of literature to explain the environmental regulation of air pollution and renewable energy usage. From these theories, the fact that the double dividend theory focuses on both the welfare gain dividend (less pollution) and the economic dividend (reduction in the distortions of the revenue-raising tax system) gives this theory a robust advantage over others. The introduction of ET will reap two advantages, as explained in the double dividend theory. The environmental benefit is the first dividend, meaning that the application of ET will be able to reduce pollutant emissions successfully, and thus positively affect the quality of the environment via possible investments in renewable technologies (Radulescu et al., 2017). According to the economic advantage in the second dividend, the increment in ET proceeds may be employed in funding the cuts in the existing taxes. Based on this theory, ET imposition can perform two roles, such as emission reduction and energy savings, and developing promotion, that is, indirectly boosting energy consumption and efficiency.

In the context of SSA, a double dividend (environmental dividend) may be achieved if the government of SSA rationally spends the ET transactions generating revenue in research and development, renewable energy infrastructures, and alternative green technologies. Also, the high cost of ET compared to renewable energy sources could be a disincentive to the use of fossil fuels, consequently increasing the environmental dividend in SSA, and hence impacting the attainment of SDGs in SSA (Mez, 2020). However, the economic dividend can be achieved in the case it utilises the revenue collected through ET to offset distortionary taxes, which may reverse investment and economic efficiency and, at the same time, further services the environmental aims.

Since SSA depends on fossil fuels to stabilise its economy, it will be difficult to realise the double dividend of the ET, where countries will not be responsive or will not enforce the ET feebly. In addition, corruption, bad governance, and institutional weakness further compromise the ability of ET to contribute economic dividends. Transitions are also restricted by the high initial costs of renewable energy. Therefore, ET can increase energy charges without adequate provisions for clean energy, which causes economic burdens instead of gains. Corruption undermines enforcement, resulting in tax evasion, whereas bribery and inefficiency discourage investments in the private sector.

Empirical Review

Olanrewaju et al. (2019) used random and fixed effects models to study factors influencing the use of renewable energy in Africa. They discovered that ET positively impacts the use of renewable energy. The results of Olanrewaju et al. (2019) are consistent with the conclusions of Bala and Khatoon (2024), who investigated the impact of ET on renewable energy technologies in SSA. They used the autoregressive distributed lag (ARDL) to analyse data from 28 nations covering 2001–2021. These findings are also in line with Peng et al. (2022) in Europe, who employed a Method of moments quantile regression (MMQR) between 1995 and 2020. Wu et al. (2023) had similar conclusions for G7 countries from 1990 to 2020.

However, contrasting findings argued that an inverse impact also exists between ET and REC. For instance, Fang et al. (2022) examined the impacts of an ET on the use of renewable energy in 15 nations along the Belt and Road between 1998 and 2019. Using a panel ARDL model, an ET negatively affect these countries’ use of renewable energy. Akin to this, Bashir et al. (2021) used the fully modified ordinary least squares approach for 29 Organisation for Economic Co-operation and Development (OECD) nations between 1996 and 2018 and came to the same findings. Hájek et al. (2019) examined the effects of ET on European Union (EU) nations (Sweden, Finland, Denmark, Ireland and Slovenia), and concluded that these taxes do not boost the use of renewable energy sources. The research employed the ordinary least squares technique to examine data from 2005 to 2015. Just as Hájek et al. (2019) and Dogan et al. (2023) used ARDL econometric tools in EU countries to analyse annual data from 1995 to 2019. Their study’s findings imply that ET has a detrimental impact on the use of renewable energy.

An alternative strand of literature has posed mixed findings across countries. Using panel ARDL and non-linear autoregressive distributed lag (NARDL) methodologies, Aydin and Bozatli (2023) examined the effects of an ET on renewable energy using 10 OECD nations from 1994 to 2019. In light of the panel ARDL results, ET eventually promotes REC. Additionally, the non-linear panel ARDL results show that ET has a long-term detrimental impact on REC. Similarly, Degirmenci and Yavuz (2024) in EU nations between 1995 and 2019 used two novel estimators: dynamic common correlated effects (DCCE) and augmented mean group (AMG). The results showed that, while it negatively impacts Spain and Slovenia, ET has a favourable impact on REC in Germany and France. Correspondingly, Li et al. (2022) used the panel quantile regression approach for the Brazil, Russia, India, China, South Africa and Turkey (BRICST) countries from 1991 to 2019. The study’s findings suggest that stricter ET led to higher REC in nations with low levels of renewable energy. However, strict ET has a negative impact on REC in nations where it is becoming more prevalent.

The effect of ET on renewable energy is widely assessed, yet few studies focus on developing economies. The literature on the area primarily analyses either production or consumption individually, ignores the aspect of corruption in SSA, and does not test the causal association between ET and renewable energy (Olanrewaju et al., 2019). This article focuses on the joint dynamics of ET, REC and REP in SSA, with corruption as a moderate variable. It deals with cross-sectional dependence (CSD) and heterogeneity through using a DCCE model. The article discusses the details of ET implications on renewable energy demand and supply, as well as its long-run environmental gains and the effectiveness of corruption in determining the performance of ET. It also uses panel causality analysis to establish predictive relationships between the ET, REC and REP.

Data and Methodology

Data

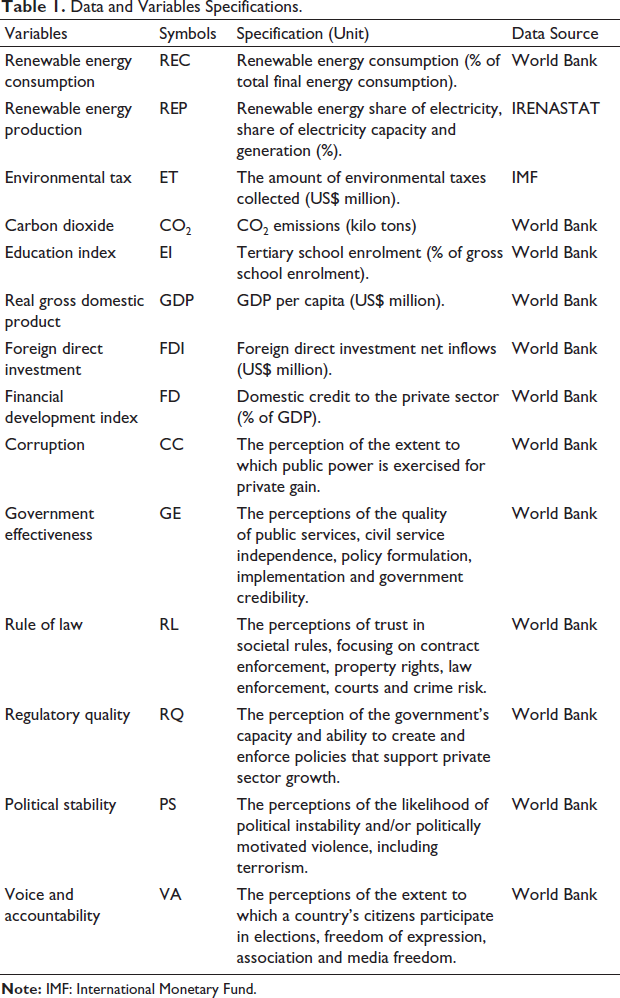

Data and Variables Specifications.

Data and Variables Specifications.

The DCCE Model

The DCCE methodology was developed by Chudik and Pesaran (2015), suitable for panel data to address heterogeneity and CSD issues that are neglected by other traditional dynamic panel approaches.1 This method is essentially based on two estimators: the mean group (MG) model (Pesaran & Smith, 1995), and the pooled mean group (PMG) approach (Pesaran et al., 1996). In effect, the implementation of ETs, the REP and the REC differ across countries. This is the case in SSA, where varying levels of corruption, policy effectiveness and market conditions may lead to different outcomes for renewable energy transitions. Also, by taking into consideration unobserved common characteristics that may affect both ET policies and renewable energy dynamics across regions or countries, the DCCE model effectively manages CSD.

Second, the approach uses the MG estimate properties to address the issue of parameter heterogeneity (Roodman, 2022). Besides its ability to study long-term relationships in the presence or not of cointegration, DCCE improve the small sample characteristics of the estimation and is robust to endogenous regression coefficients in both static and dynamic panel data models, regardless of whether the model’s regressors are strictly or weakly exogenous (Chudik & Pesaran, 2019). This suggests that the DCCE model addresses possible endogeneity issues by utilising instrumental factors, guaranteeing the validity of causal inferences about the impact of ET on renewable energy. Moreover, the dynamic nature of the model allows it to consider the lagged effects of ET on renewable energy. Additionally, by using the Jackknife correction function, this strategy can be applied to small data sets regardless of structural breaks or an unequal panel data structure (Chudik et al., 2016).

The major attraction of the DCCE model in this article lies in its ability to study dynamic relationships across heterogeneous yet correlated panels, which are characteristic of SSA countries. Although quite diverse in their governance conditions, corruption rates, and levels of socio-economic and environmental performance, these countries are interdependent through regional blocks, social, geographical, trading and financial connections; raising the issue of heterogeneity and cross-section dependence, which preliminary tests could not reject. The DCCE model addresses these issues by including country-specific fixed effects and cross-sectional averages of dependent and independent variables so as to capture unobserved common factors that are likely to contribute to the observed interdependencies.

REP Model

This study builds on the existing literature and considers CO2 emissions, real GDP, FDI and FD as the determinants of REP. The adoption of clean technology relies on real GDP, whereas REP is characterised by carbon emissions. There is a positive impact of FD on green investments, whereas FDI transfers technology and skills that reduce emissions and facilitate REP. These REP drivers are extended to include ET, following Kamalu and Binti Wan Ibrahim (2024). This is because ET is accepted as a useful policy tool for embracing greener technology and cleaner energy sources, as well as enhancing the achievement of the worldwide goal of full decarbonisation. Since the effectiveness of ET depends on the quality of the institutions, which includes corruption, this study assumes a possible moderation role of corruption in modelling REP. The DCCE with heterogeneous slopes, a heterogeneous factor loading

where

Equation (2) is the cross-sectional-augmented autoregressive distributed lag (CS-ARDL) version of the DCCE model, which includes both the lagged and contemporaneous values of the REP factors, capturing their delayed and immediate effects, respectively. Chudik and Pesaran (2015) showed that the long-run coefficient is calculated as follows:

The long-run coefficient can be derived as:

and the MG long-run coefficient is calculated by averaging across cross-sections:

REC Model

Similarly, this study also builds on the existing literature that considers the determinants of REC, where CO2, as well as the educational index, are extended to be the control variables of REC, following Ameer et al. (2024). CO2 can potentially determine REC, since the effectiveness of environmental policies in reducing CO2 emissions is likely to boost REC. Additionally, the educational index can be applied to reduce CO2 by increasing energy efficiency in the production process. A firm with a higher educational index can significantly reduce environmental costs by adopting environmentally friendly approaches, thereby enhancing REC. These REC drivers are also extended to include ET as the variable of interest because, theoretically, ET is anticipated to support the eco-friendly environment, implying it may encourage REC. However, the success of these taxes is also assumed to be dependent on the governance and institutional quality within a nation. Against this, since corruption is a key governance and institutional quality concern, the study assumes that it can possibly be a determinant of REC. Again, the effectiveness of ET depends on the quality of the institutions, which includes corruption. This study assumes a possible moderation role of corruption in modelling REC, and is specified as follows:

Where

The variations of the individual REC variables and their lags are added to estimate the long-term coefficients. Differences between the explanatory factors are considered while estimating the long-run coefficients in the CS-DL framework as follows:

Where

Causal Analysis

For causal analysis, the study applies the half-panel jackknife (HPJ) test proposed by Juodis et al. (2021). CSD and potential data heterogeneity are taken into consideration when testing for the presence of panel Granger causality across countries. Because of the high level of globalisation, international trade, and financial integration across SSA nations, a shock that affects one country may also have an impact on others if there is CSD throughout the sample (Pesaran, 2006). Second, it also seems sensible to capture the heterogeneity that may be driven by country-specific characteristics. Considering the ET impact on REC and REP, the panel Granger causality test, which controls both heterogeneity and the existence of CSD, can be shown as follows.

where t is the time,

Descriptive Analysis

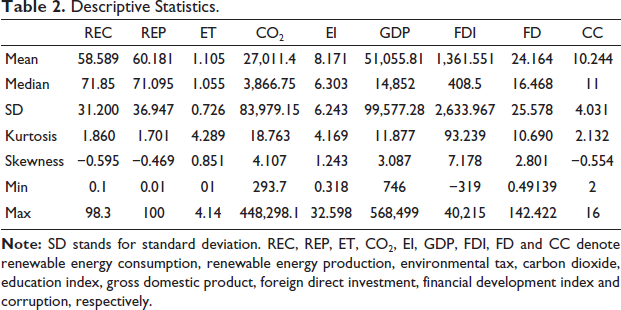

Descriptive Statistics.

Descriptive Statistics.

Estimation of Results and Discussion

The research examines the dynamic relationship between the studied variables using the MG estimator. Tables 3A and 3B display the CS-ARDL results for REP, while Tables 4A and 4B provide the CS-DL results for REC. The causal analysis output is compiled in Tables 5A and 5B.

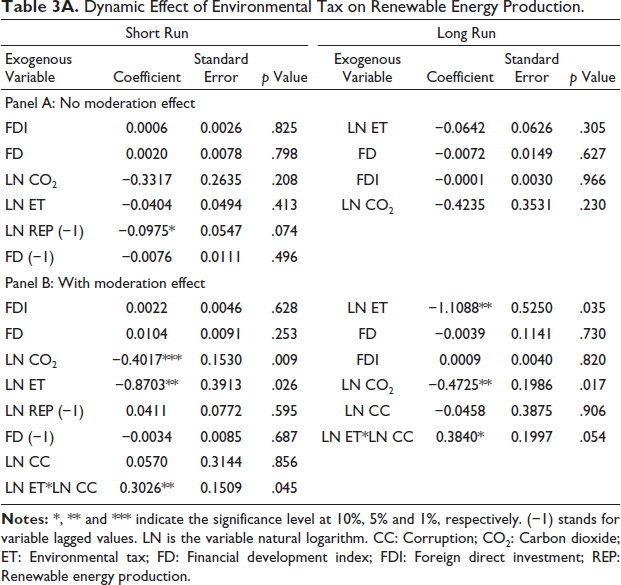

Dynamic Effect of Environmental Tax on Renewable Energy Production.

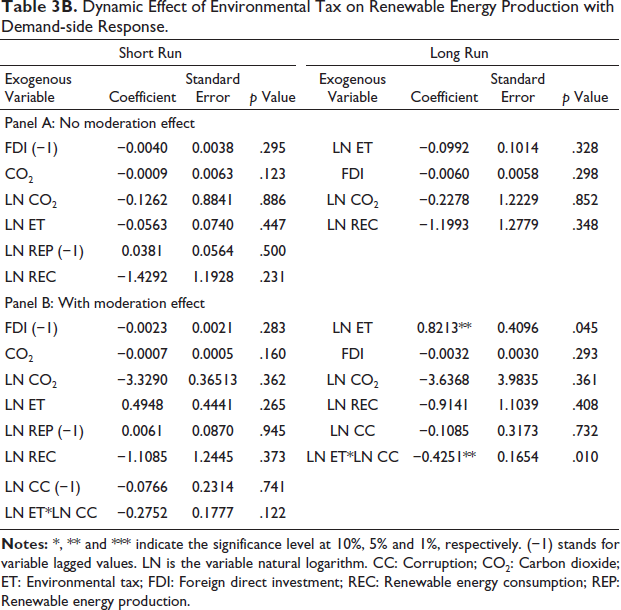

Dynamic Effect of Environmental Tax on Renewable Energy Production with Demand-side Response.

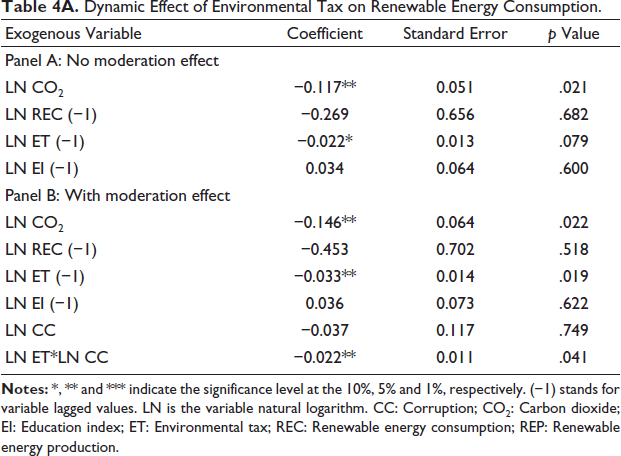

Dynamic Effect of Environmental Tax on Renewable Energy Consumption.

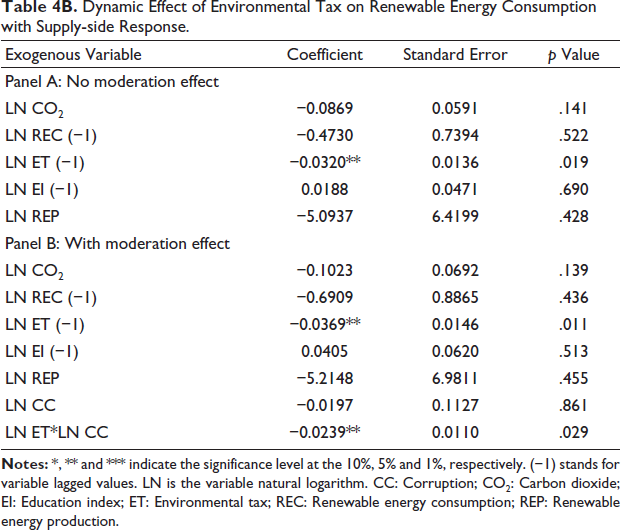

Dynamic Effect of Environmental Tax on Renewable Energy Consumption with Supply-side Response.

Dynamic Impact of ETs on REP

Due to the moderation effect of corruption, Table 3A indicates that ET has a significant negative effect on REP in SSA in both the short and long run at the 5% significance level. The coefficient of ET is negative, which means it hinders REP in SSA. It indicates that the ET revenues might not be spent on renewable energy projects due to corruption, hence the theoretically expected positive effects on REP may fail to materialise. This disputes the double dividend theory and is in line with Zhang (2011) and Böhringer et al. (2017). ET can be a deterrent to the financial aspect, and therefore, there needs to be improved governance and effective utilisation of tax.

The moderating role of corruption between ET and REP turns out to be significant, reporting positive coefficients both in the short and long run, which implies that it enhances REP. In highly corrupt environments, the stakeholders of renewable energy can fast-track REP through informal routes to avoid bureaucracy. Similar findings were found by Hao et al. (2021). The results support the environmental dividend since the interaction factor increases REP. Nevertheless, they are contrary to the economic dividend, given that corruption prevents productivity and effective use of ET revenues. The study also found that CO2 was statistically significant in explaining REP at a 5% significance level, both in the short and the long run. With both negative coefficients, it follows that CO2 emissions may reduce REP both in the short and long run. Similarly, when the effect of REC is accounted for, ET exhibits a positive impact on REP, and this implies that higher ET leads to higher REP in the long run. Further, the existence of corruption essentially depresses REP in the long term, meaning that corruption diminishes the positive influence of ET on REP.

Dynamic Impact of ETs on REC

Table 4A provides evidence that ET significantly affects REC with and without the moderation effect. In both cases, the coefficient of lagged ET is significantly negative, indicating that it hinders REC. The findings are a possible reflection of the lack of preparedness in the SSA’s technological ecosystem. This indicates that in the absence of cheap or advanced renewable technologies, ET might not cause a market shift off fossil fuels, which would cause low growth in REC. These results are consistent with earlier research, including Dogan et al. (2023).

Regarding the moderation effect of corruption, the findings demonstrate that corruption moderates the link between ET and REC amongst SSA nations at a 5% significance level. The negative relationship between corruption and ET implies that in corrupt nations, ET does not stimulate REC. Corruption works against the double dividend theory, restricting the environmental benefits: firms avoid fees, and the economic benefits: revenues are embezzled. This is congruent with He et al. (2019). Also, CO2 was found to be statistically significant in explaining REC in SSA. The inverse association reflects that carbon emissions reduce REC in panels A and B, respectively. Considering the effect of REP (Table 4B, Panel B) and in the presence of corruption (Tables 4A and 4B, Panel B), ET reduces the utilisation of renewable energy, possibly because of improper reinvestment of tax income or cost-prohibitive technology. Additionally, the interaction between ET and corruption triggers the negative effect of ET on REC since corruption undermines the effectiveness of ET due to tax evasion and misappropriation of funds.

It is worth noting that corruption, FDI, FD and EI are insignificantly influential contributors to renewable energy outcomes in SSA, with underlying structural and institutional limitations. The outside funds tend to circumvent local governments, restricting the effect of corruption. FDI does not target renewables but rather the traditional sector. The financial markets are poorly developed, with costly interest rates and low volumes of green financing. The education index is not important at all, as the infrastructural works are poor, and there is no policy on environmental education.

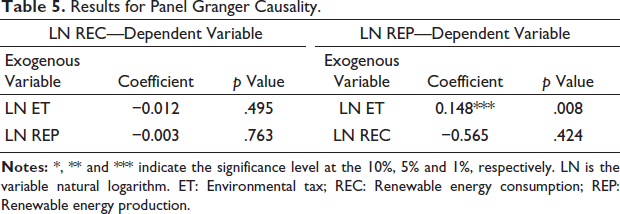

Causal Impact of ETs on REC and Production

The results of Granger causality between ET and both REC and REP are shown in Table 5 shows the results between REC and REP, as well as REP and REC, using the Jackknife estimator.

Results for Panel Granger Causality.

Robustness Checks

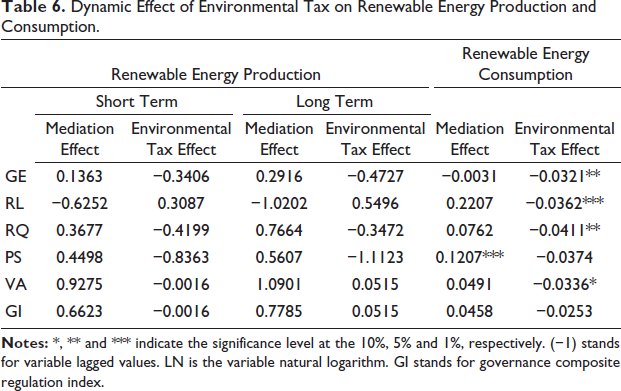

Dynamic Effect of Environmental Tax on Renewable Energy Production and Consumption.

Although ET and other sustainability measures have the potential to encourage the use of renewable energy in SSA, political, economic and infrastructure obstacles currently limit their efficacy. Many nations lack the financial resources, legal frameworks and infrastructure required to properly direct environmental revenue towards renewable energy initiatives. Therefore, these regulations might unintentionally hinder the sector’s growth and innovation, especially in countries where the energy industry is still in its infancy. As a result, the current study examines the dynamic impact of ET on REP and consumption in SSA, demonstrating the role of institutional quality in ensuring the realisation of the environmental double dividend. To this end, the common correlated effect model is employed to account for both country heterogeneity and interdependence across SSA nations.

Considering the interconnection between renewable energy supply and demand, the findings reveal that, in the presence of corruption, ET impedes the consumption but improves the production of renewable energy in the long run. These findings violate the environmental dividend of the double dividend theory, as the environmental improvement is not being effectively realised in terms of shifting consumer energy choices toward renewables.

In addition, the moderating effect of corruption appears to be negative for both the consumption and production of renewable energy. This follows that, by twisting policy decisions in favour of private gains, corruption reduces clean energy supply while triggering negative effects on demand. This demonstrates that policy distortions perpetuated by corruption impede the flow of resources toward renewables, which hinders technological innovation, infrastructure development, and undermines the economic dividend.

Finally, the panel Granger causality test indicates no evidence of Granger causality between ET and REC, as well as between REC and REP, in either direction. However, ET is found to Granger-cause REP in SSA. Therefore, the SSA government are recommended to refine their ET policies through the use of tax incentives or subsidies so that they are more geared toward promoting REC. Furthermore, anti-corruption initiatives are essential to enhancing the efficacy of ET. While minimising the negative effect on REC, strengthening institutional frameworks, increasing transparency, and guaranteeing accountability in renewable energy projects can assist optimise the positive impact of ET on REP.

Footnotes

Acknowledgment

During the preparation of this work, the authors used Scopus AI to screen the relevant literature and ChatGpt 5 for improving language clarity, checking grammar and coding assistance. After using this tool, the authors reviewed and edited the content as needed and take full responsibility for the final version of the manuscript.

Declaration of Conflicting Interests

The authors received no financial support for the research, authorship and/or publication of this article.

Funding

The authors declared no potential conflicts of interest regarding the research, authorship and/or publication of this article.