Abstract

This article investigates the impact of economic policy uncertainty (EPU) and fiscal consolidation on government debt share to GDP and GDP in BRICS countries. Using the autoregressive distributed lag (ARDL) model from 2009 to 2022. The article gives insights into the relationship between EPU, fiscal consolidation and government debt share to GDP with the GDP in the BRICS countries, then advance economies which are mostly undertaken in literature. The findings of the article are that EPU has an insignificant impact on government debt share to GDP in the short and long run. However, fiscal consolidation has a significant impact on reducing government debt share to GDP in the long run. In terms of GDP, EPU has a significant negative impact in the long run but not in the short run. Fiscal consolidation has a significant positive impact on GDP in the short run. Fiscal consolidation is recommended as a growth policy that does not reduce government debt share to GDP.

Keywords

I. Introduction

From both theoretical and empirical perspectives, it has been argued that using government debt share to gross domestic product (GDP) to stimulate economic growth in emerging economies is important. Moreover, in recent years, the contraction–expansion fiscal policy, the so-called ‘fiscal consolidation policy’, has emerged through the work of Mellet (2014), Auerbach and Gorodnichenko (2017), Heimberger (2017), Brady and Magazzino (2018) and Jacques (2021), among others. There are mixed results regarding the impact of fiscal consolidation on government debt share to GDP and economic growth. The most used measure of fiscal consolidation is the cyclically adjusted primary balance (CAPB), which has gained interest over the years in the effort to find fiscal consolidation. The CAPB filters out the cyclical movement in government expenditure and tax, which is then attributed to fiscal consolidation over time (Afonso & Leal, 2022; Afonso & Silva Leal, 2019; Agnello et al., 2019). The thinking around fiscal consolidation is that government expenditure cuts and tax increases will result in a fall in government debt share to GDP. This is because forward-looking economic agents will anticipate a reduction in tax and interest rates. This will increase permeant income, crowed in investment, increase economic activities and higher tax collection that can be used to reduce government debt share to GDP (Alesina & Ardagna, 2010; Alesina et al., 2017, 2019). On the other hand, economic policy uncertainty (EPU) refers to a situation in which future economic conditions, trends or outcomes are unknown or difficult to predict Makololo and Seetharam (2020).

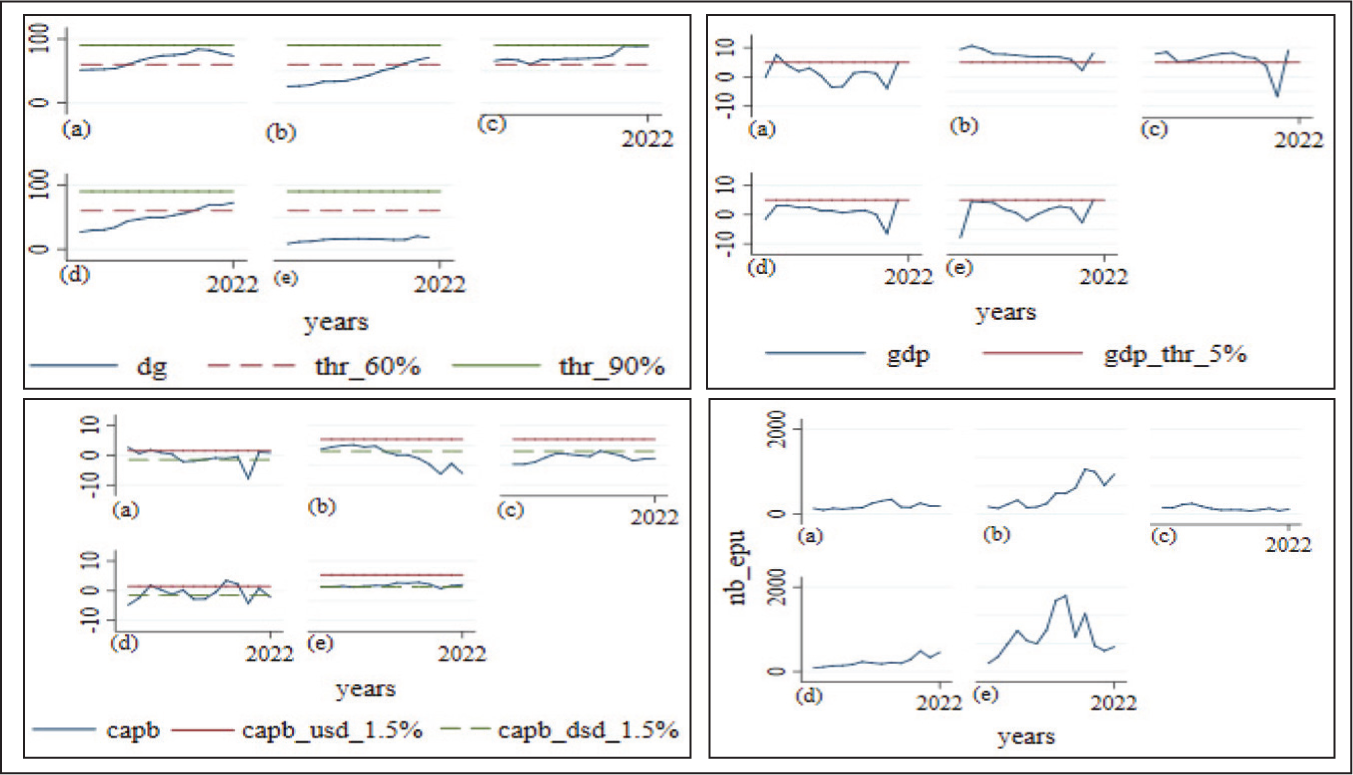

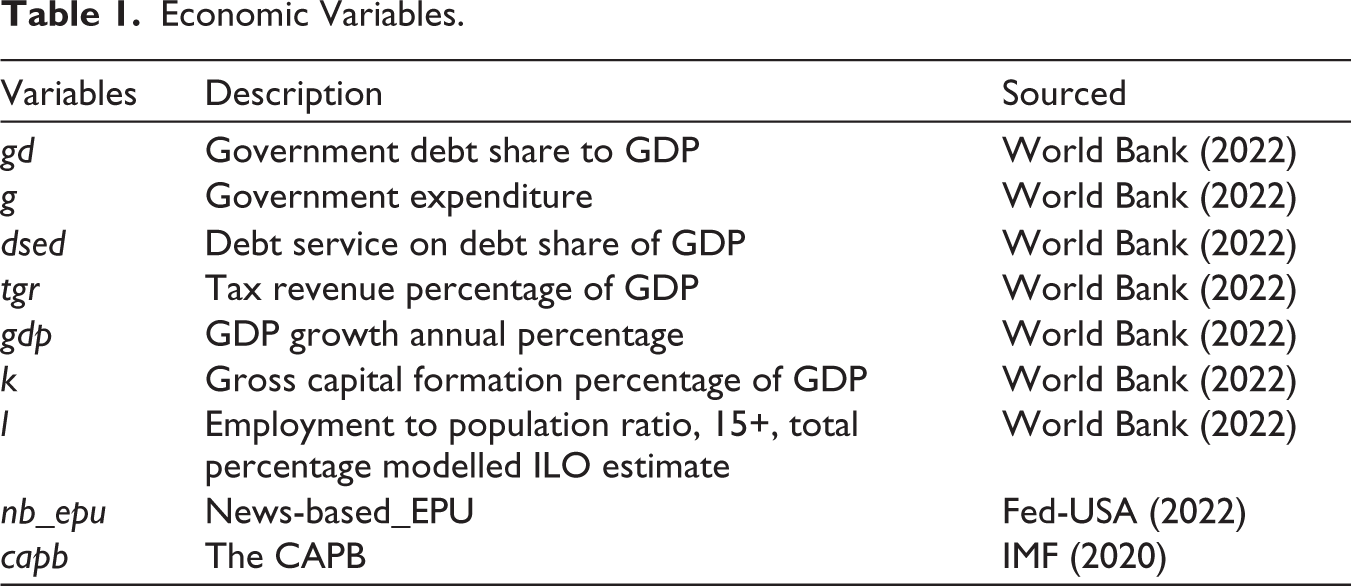

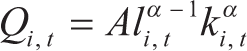

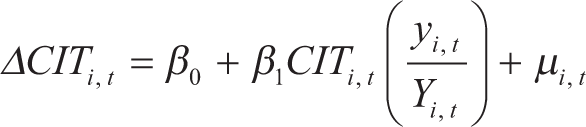

Figure 1 shows the economic data considered in the article. The bottom left graphs (a to e) reflect EPU in BRICS countries. There is a reflection that EPU has been on an upwards trend in recent years. Governments may respond to economic uncertainty by implementing policies to stabilize the economy and reduce uncertainty. In Figure 1, the top left graphs (a to e) reflect the domestic government debt share to GDP in BRICS countries. Across the BRICS countries, the domestic government has been on high. This is because a domestic government hives up beyond the threshold of 60% in four countries in BRICS and approaches the threshold of 90%. This threshold of 60% and 90% is deemed to result in a fall in the GDP (Buthelezi & Nyatanga, 2018). Given the high government debt in BRICS countries, there is a need to investigate the impact of policy intervention through fiscal consolidation. That is what is the impact of fiscal consolidation on government debt? This is critical given that there is less attention in the effort to investigate this question in developing economies such as BRICS countries, and the focus has been more on Organization for Economic Co-operation and Development (OECD) countries. In Figure 1, top right, graphs (a to e) reflect the GDP in BRICS countries. This is an indication that there are only two countries that have been able to achieve an economic growth rate that is above 5% since the establishment of BRICS. Since the start of BRICS, the other three economies have been operating below 5%. This 5% economic growth is variable in the developing economy because it can help fight other macroeconomic challenges such as unemployment, inflation, inequality, and poverty, among others.

The contribution of the study in the text is to investigate the impact of fiscal consolidation on government debt share to GDP in BRICS countries, as there is less attention given to this question in developing economies such as BRICS countries. The study also aims to examine the role of EPU in the context of lower levels of economic growth despite the adoption of fiscal consolidation by fiscal authorities in BRICS economies. BRICS is selected for investigation because fiscal authorities have shown interest in the adoption of fiscal consolidation in the effort to reduce government debt share to GDP; however, there is limited research on the topic. On the other hand, there is no consensus among scholars on the impact of fiscal consolidation impact on government debt share to GDP. Case in point Marattin et al. (2022), David et al. (2022), Afonso and Leal (2022) among others found that fiscal consolidation reduces government debt share to GDP, while Müller (2014), Deskar-Škrbić and Milutinović (2021) and Georgantas et al. (2023) among others outline that fiscal consolidation increases government debt share to GDP; therefore it is self-defeating. As such, it is critical to have a block-based investigation to find out what is the impact of fiscal consolidation. In the effort to find the solution to the problem of high government debt share to GDP, scholars like Agnello et al. (2019) and Nunes (2019) among others have investigated the success of fiscal consolidation (the after-effect of fiscal consolidation) on government debt share to GDP. Quaresma (2021), Olaoye and Olomola (2022) and Marattin et al. (2022) among others have looked the non-linearity of fiscal consolidation on government debt share to GDP. There is a lack of studies that incorporate both fiscal consolidation and uncertainty at once. This article fills this gap in the body of knowledge. Moreover, the study’s findings could provide valuable insights into the effectiveness of fiscal consolidation policies in developing economies and inform policymakers’ decisions to stabilize the economy and reduce uncertainty in BRICS countries. Given this context, the economic questions of the article are as follows: what is the long- and short-run impact of EPU on domestic government debt share to GDP and GDP? What is the long- and short-run impact of fiscal consolidation on domestic government debt share to GDP and GDP?

The rest of the article has the following sections. Section II outlines a literature review. Section III presents the methodology. Section IV discusses the empirical results. Finally, Section V outlines the conclusion of the article.

II. Literature Review

Theoretical Review of Fiscal Consolidation

Theoretically, the Classical school of thought advocates that fiscal consolidation based on tax increases results in less production, as taxes increase the cost of doing business. On the other hand, when fiscal consolidation is based on a government expenditure cut, this will crowd in investments. As such, there is less room for government intervention in the economy (Mankiw, 2019). Given the positive and negative impacts that may come with fiscal consolidation, the net effect depends on the size of fiscal consolidation (Alesina & Ardagna, 2013). The traditional Keynesian model with sticky nominal wages and prices advocates that there are detrimental effects on economic growth that are induced by fiscal consolidation, as it limits the government from spending on economic activities that can boost economic growth. The traditional Keynesian proposed the use of the opposite instrument of fiscal consolidation (Mankiw, 2019). The Ricardian Equivalence theorem counter augers the proposal of the standard Keynesian school, as it argues that economic agents are forward-looking, meaning that an increase in government expenditure financed by debt triggers an expectation of higher taxes in the future. As a result, economic agents in the present time will spend less and save more in anticipation of future tax increases that they will need to pay to settle the debt. In such a situation, increasing government expenditure through debt financing will not trigger economic growth, as demand will remain unchanged (Mankiw, 2019). The new Keynesian point out that fiscal consolidation has a positive effect on economic growth. According to the new Keynesian perspective, fiscal consolidation can have a beneficial impact on economic growth. Advocates of the new Keynesian school argue that if we embrace the concept of Ricardian Equivalence, which takes a forward-looking approach, reducing government expenditure can result in individuals anticipating future tax reductions. This anticipation, in turn, leads to an increase in individuals’ permanent income due to lower taxes. As a result, people are more likely to spend, leading to a boost in economic growth. As such, the economy may have a greater return to reduce government debt share to GDP (Alesina & Ardagna, 2013).

Empirical Literature View

The question of where should South Africa have a fiscal rule was examined by Burger and Jimmy (2006) using the data from the period 1961 to 2004. The fiscal functions and the Markov-switching dynamic regression model provide evidence that there are two regimes of government debt share to GDP with a mean of 27.4% and a value of 67% with transition probabilities of 92.5% and 75%, respectively. The fiscal consolidation policy of government expenditure cuts reduces government debt share to GDP. Swanepoel and Schoeman (2003) used the data from 1972 to 2000 to investigate countercyclical fiscal policy in South Africa analysis. Using the Vector Autoregression (VAR) model their result suggested that fiscal consolidation implementation in a high level of government debt will result in a 0.4% fall in government debt. The discal space and debt sustainability were investigated in 23 advanced economies by Ghosh et al. (2013) in the period 1970–2007. Using the stochastic model, the authors point out ‘fiscal fatigue’ when government debt share to GDP increases. Moreover, the authors noted that fiscal consolidation may be urgently needed to ensure that debt remains on a sustainable path and that shocks, including data revisions, do not derail sustainability. Alesina and Ardagna (2010) used annual data from 1970 to 2005 to investigate the expansionary fiscal consolidations in 15 Europe countries. The fixed effects model was utilized, and it was found that one percentage point higher government spending on GDP leads to a 0.75% lower growth. Based on the neoclassical proposition, fiscal loosening can cause adverse effects on productivity. A Dynamic Stochastic General Equilibrium (DSGE) model was applied in 14 EU countries by Bi et al. (2013) to examine the uncertain fiscal consolidations during the period 1984–2009. It was found that the composition of fiscal consolidation, its duration and the monetary policy stance argue that the conditions that could render fiscal consolidation efforts expansionary are unlikely to apply in the current economic environment. Fiscal consolidation at low debt levels is more surprising than that at sustained increases in debt. An examination of countries under the Organization for Economic Cooperation and Development (OECD) by Ball (2014) from 1995 to 2013 used the VAR model. They found that countries with large losses of potential output are already in a bad growth trajectory due to the inherited weakness that is getting worse by the prolonged austerity. On the other hand, most of the countries have experienced strong hysteresis effects: shortfalls of actual output from pre-recession trends have reduced potential output almost one-for-one during the period in the presence of fiscal consolidation. The counter-cyclical challenges of fiscal policy: a comparative analysis of South Africa and BRICS countries investigation was undertaken by Mellet (2014) from 2008 to 2013. The VAR model reflected the result that highlights the importance of a novel approach such as fiscal consolidation in the effort to create sustained growth.

In the studies cited above from Burger and Jimmy (2006) to Mellet (2014), it is clear from the literature that high levels of government debt can have negative implications for economic growth and sustainability, which may necessitate fiscal consolidation efforts. However, the composition and duration of fiscal consolidation policies, as well as the stance of monetary policy, are crucial factors in determining their effectiveness. There is also evidence that suggests that fiscal consolidation policies can be contractionary in the short run, but expansionary in the long run if implemented sustainably. The specific effects of fiscal consolidation policies on economic growth and government debt levels may vary depending on the country and the specific context in which the policy is implemented. It may be concluded from the above literature that there is a need for a balanced approach to fiscal consolidation policies, taking into account the potential negative impact on economic growth in the short run while ensuring that debt remains on a sustainable path in the long run. The studies highlight the importance of considering the potential hysteresis effects of prolonged austerity measures, as well as the need for a novel approach to creating sustained economic growth. There is a provision of important insights by these studies into the complex relationship between fiscal consolidation policies, government debt levels and economic growth, and suggest that a nuanced and sustainable approach to fiscal consolidation is necessary to achieve long-term economic stability and growth.

The time for austerity and estimation of the average treatment effect of fiscal policy was undertaken by Jordà and Taylor (2016) in the United Kingdom (UK). The Ordinary Least Squares (OLS) estimates suggested that a 1% fiscal consolidation translates into a loss of 3.5% of real GDP over five years when implemented in a slump, rather than just 1.8% in a boom. The panel VAR model was used by Auerbach and Gorodnichenko (2017) in investigating fiscal stimulus and fiscal sustainability in OECD from 2008 Q1 to 2016 Q2. It was found that fiscal consolidation of the government expenditure cut was found to result in a 2.80% fall in government debt share to GDP in the boom period. Between 2011 and 2023 Heimberger (2017) investigated the Euro Area if did fiscal consolidation caused the double-dip recession. The OLS were used and it is noted that there is a between cumulative real GDP growth and fiscal consolidation measures which points to a strong negative association with deep economic crises. Investigation of the sustainability of fiscal policy in a set of 19 European Monetary Union (EMU) countries was undertaken by Brady and Magazzino (2018) using the data over the period 1970 to 2016. The Markov-switching dynamic regression model used provided evidence that there are different regimes of high government debt share to GDP fiscal rules, which can be successful in the event of a build-up in public debt. Moreover, they note that there is a high correlation between EPU and economic growth. The investigation of sustainability of public and external debt burden of Pakistan and India was undertaken by Chandia et al. (2019) from 1971 to 2017. Equation for external debt dynamics includes current account balance-to-exports ratio and exports growth vs. interest rate. Study finds significant role of budget and current account deficits in public and external debt accumulation in Pakistan and India. Concludes debt sustainability is weak but manageable. A panel data analysis for 26 OECD countries from 1980 to 2016 (Bardaka et al., 2021) found that the existence of more persistent austerity affects total factor productivity (TFP). They note that increases in the CAPB (proxy fiscal tightening) in OECD countries are found to decelerate the rate of TFP by 0.46% annually. Gründler and Potrafke (2020) conclude that, when seen from a complete long-run perspective, constitutional fiscal regulations have fostered prosperity both in more recent decades and in the centuries that followed the start of the Industrial Revolution. Additionally, fiscal regulations work well at both the national and subnational levels, increasing per capita GDP over time by an average of 18%. Taxes and other government spending were shown to be responsible for keeping the existing level of debt relative to GDP (Cogan et al., 2020). The models demonstrate that the fiscal consolidation plan raises yearly GDP growth over the long and short terms by approximately 7% and 10%, respectively. Alloza et al. (2020) outline that the public debt-to-GDP reaching 60% beyond this point debt-to-GDP starts to have a detrimental effect on economic growth. However, they were silent on the role of fiscal consolidation. Makololo and Seetharam (2020) investigated how EPU affects BRICS nations. It found that EPU is influenced by how investors or policymakers behave and the results of their choices. The results from Russia, India and South Africa demonstrate the importance of EPU in deciding decisions regarding leveraged financing and the herding effect that a rise in EPU has on these decisions. Chinese and Brazilian businesses have opposite results.

In the studies that are discussed above from Jordà and Taylor (2016) to Makololo and Seetharam (2020), it can be noted that there is no clear consensus on the effectiveness of fiscal consolidation measures. Auerbach and Gorodnichenko (2017) found that fiscal consolidation resulted in a fall in government debt share to GDP, while Jordà and Taylor (2016) found that fiscal consolidation translated into a loss of real GDP, especially when implemented in a slump. However, Bardaka et al. (2021) found that persistent austerity affected TFP negatively, and Alloza et al. (2020) outlined that public debt-to-GDP reaching 60% has a detrimental effect on economic growth. On the other hand, these studies suggest that fiscal consolidation can result in a decrease in government debt share to GDP during a boom period, but may have negative consequences during economic crises. Different regimes of high government debt share to GDP fiscal rules can be successful in the event of a build-up in public debt, and constitutional fiscal regulations can foster prosperity. However, persistent austerity measures can affect TFP and an increase in the CAPB can decelerate the rate of TFP. Moreover, the public debt-to-GDP ratio exceeding 60% can have a detrimental effect on economic growth. Finally, EPU can have a significant impact on investment decisions and economic outcomes.

Glavaški and Beker-Pucar (2020) investigated episodes of fiscal consolidation using the autoregressive distributed lag (ARDL) model from 1950 to 2018. It was found that the cyclically adjusted primary budget balance in GDP increases by 1%, and the real economic growth in western China will grow by 0.26%. This means that fiscal consolidation has a positive impact on economic growth in this region. de Rugy and Salmon (2020) investigated large fiscal consolidations in 26 countries from 1995 to 2018. They found 62 successful consolidations and 73 unsuccessful consolidations. They found that there were 45 expenditure-based fiscal consolidations (EB) episodes, and more than half were successful, while there were 67 tax-based fiscal consolidations (TB) episodes in which less than 4 in 10 were successful. Ardanaz et al. (2020) examined fiscal consolidations if the policy mix matters in Latin America from 1985 to 2018. The probit fixed effect model was used, and it found that 42% explain the importance of fiscal consolidation policy mix matter. There is less applicability of fiscal consolidation during the time of the election of political parties. The definition of a 2% CAB increase in 2 years was used by Kalbhenn and Stracca (2020) to define fiscal consolidation episodes in 26 EU countries from 1997 to 2017. Using the structural VAR, it was found that the fiscal consolidation shock resulted in an increase in government debt in the first year and thereafter started to fall below equilibrium. The fiscal rule investigated by Nakatani (2021) in nine Pacific island states during the period from 1990 to 2018 found that when there is fiscal consolidation or fiscal rule in economies that are experiencing natural disasters and climate change, in the long run, government debt turns to increase. Deskar-Škrbić and Milutinović (2021) used a small short-term, semi-structural macro-econometric model of the Croatian economy from 2014 to 2016. The result indicated that the fiscal consolidation implemented during the excessive deficit procedure is self-defeating as it increases government debt. In 14 EU countries over the period 1970–2019, Quaresma (2021) combines the narrative technique with the standard CAPB method for identifying fiscal consolidations. The fixed effect model reflects that fiscal consolidation coupled with a monetary expansion produces little evidence of non-Keynesian effects or reduction in government debt. The studies from Glavaški and Beker-Pucar (2020) to Quaresma (2021) suggest that the success of fiscal consolidation depends on the specific context and policy mix of each country, as well as the specific econometric techniques used to measure its impact. It is important to consider the trade-offs between short-term and long-term effects on economic growth and government debt when designing and implementing fiscal consolidation policies.

A total of 17 OECD countries from 1980 to 2014 show that austerity, measured with the narrative approach to fiscal consolidations, is associated with a decrease in the proportion of public investment in research and development and gross fixed capital formation (Jacques, 2021). Ghirelli et al. (2021) discover that shocks to financial and EPU have a discernible detrimental impact on private consumption. The negative reactions to investments in capital goods are initially more significant but disappear more quickly. Tran (2021) discovered that the cost of debt financing is positively influenced by EPU and that this effect is larger during the 2008–2009 global financial crisis. Olaoye and Olomola (2022) analysed the public debt structure of Sub-Saharan Africa’s five largest economies, including South Africa. The Markov-switching model was used, and it was found that the first regime of South Africa had 31.43% and 45.71% in the second regime with the expected duration of 13 and 10 years in the respective regimes. Marattin et al. (2022) investigated revenue-expenditure-based fiscal consolidation in 20 regions in Italy using a difference-in-difference model. They provided evidence that there is a pass-through of fiscal consolidation to reduce government debt. The structural models of Afonso et al. (2022) were used in the world economic outlook data based on the International Monetary Fund (IMF) with a sample of 174 countries between 1970 and 2018. There was evidence that fiscal consolidation improves the degree of public financial sustainability in advanced and developing economies. A panel VAR system was used by David et al. (2022) in 21 emerging market and developing economies (EMDEs) from 2000 to 2018. They provided evidence that fiscal consolidation announcements, particularly if made by the government in a country with elevated vulnerability to government debt, have been successful in ameliorating default risk perceptions. In 17 OECD countries from 1970 to 2018, Afonso and Leal (2022) examined fiscal consolidation episodes using a narrative approach and 1.5% CAPB change to identify fiscal consolidation episodes. It was found that countries with debates below 60% of GDP have a more successful result to recede debt than does with higher debt. An investigation of 23 emerging and middle-income countries for the 2009–2018 period by Lahiani et al. (2022) using the GMM model outlines the improvement of government debt and current account when fiscal consolidation is adopted in the medium as well as the long term.

Olaoye and Olomola (2022) analysed the public debt structure of Sub-Saharan Africa’s five largest economies, including South Africa. The Markov-switching model was used, and it was found that the first regime of South Africa had 31.43% and 45.71% in the second regime with the expected duration of 13 and 10 years in the respective regime. However, they were silent on the use of fiscal consolidation to stabilize the debt. The probabilities of transitioning from state 1 to 1 and 2 to 2 are at least 0.92 and 0.93, respectively, in all five countries. Qamruzzaman et al. (2022) examined the association between EPU and government debt share to GDP in the top 13 oil-importing nations during the period 1995–2018 using the causality test for directed association, the panel ARDL for symmetric effects of long-term EPU on government debt. They highlight that there is a negative statistically significant link between EPU and renewable energy consumption. Nguyen and Schinckus (2022) examined the effects of global uncertainty and its associations with each country’s external debt in 69 low- and middle-income economies. Increase in uncertainty decreases government expenditures. Singh and Kumar (2022) investigated the effects of public debt on economic growth in India using the data from 1980 to 2019. The Fully Modified Ordinary Least Squares (FMOLS) found that for a 1% increase in government debt resulted to a 0.690% in economic growth. This result is contrary to the rational of the fiscal consolidation. The investigation from Jacques (2021) to Nguyen and Schinckus (2022) provides evidence that fiscal consolidation can have both positive and negative effects on economic outcomes, depending on the specific circumstances and policy measures taken. While fiscal consolidation can improve public financial sustainability and reduce government debt, it can also lead to a decrease in public investment and consumption, which can have negative impacts on economic growth and social welfare. The studies also highlight the importance of addressing EPU, which can have detrimental effects on private consumption, investment in capital goods and debt financing costs. Reducing policy uncertainty can help improve economic stability and promote sustainable growth. Regarding public debt, the studies suggest that policymakers need to carefully consider the structure and composition of debt, as well as the potential risks and vulnerabilities associated with high levels of debt. Adopting a medium- to long-term perspective and implementing appropriate fiscal measures can help stabilize and reduce public debt.

The panel data investigation of 24 OECD countries from 1990 to 2021 by Georgantas et al. (2023) found 257 cases of fiscal consolidation episodes out of 519 data points. Using the probit model, they noted evidence that fiscal consolidation through government spending in recessions, with tight monetary conditions and when the debt ratio is above 80% are self-defeating as it further increases government debt. Bremer and Bürgisser (2023), a split-sample experiment and a conjoint experiment in four European countries, show that fiscal consolidation at the cost of spending cuts or tax hikes is less popular than commonly assumed. Revenue-based consolidation is especially unpopular, but expenditure-based consolidation is also contested. Buthelezi (2023a) investigated the effects of macroeconomic uncertainty on economic growth in the presence of fiscal consolidation in South Africa from 1994 to 2022 using the time-varying parameter vector autoregression (TVP-VAR). It was found that the shock of macroeconomic uncertainty harms economic growth. Buthelezi (2023b) investigated the impact of government expenditure on economic growth in different states in South Africa. It was found that government expenditure increases economic growth. However, the study was silent on the role of fiscal consolidation on economic growth in South Africa. Nevertheless, this study suggests that there are times in the economy when fiscal consolidation may not be relevant. This back positive effect of an increase in government expenditure on economic growth, while fiscal consolidation advocates for a decrease in government expenditure, invested the time-varying elasticity of CAPB and the effect of fiscal consolidation on domestic government debt share to GDP in South Africa using the data from 1979 to 2022. Using the Markov-switching dynamic regression model it was found that fiscal consolidation increases government debt share to GDP. In the studies from Georgantas et al. (2023) to Buthelezi (2023a) we can note that Georgantas et al. (2023) suggest that policymakers should carefully consider the timing and nature of consolidation measures. Bremer and Bürgisser (2023) highlight the importance of considering public opinion and political feasibility when designing consolidation measures. Buthelezi (2023b) study suggests that government expenditure can increase economic growth, but did not investigate the impact of fiscal consolidation on growth. However, the study does imply that there are situations where fiscal consolidation may not be relevant, and policymakers should consider the potential positive effects of government expenditure on growth. These studies highlight the importance of careful consideration of the economic and political context when designing and implementing fiscal consolidation measures, and suggest that a balanced approach, taking into account the potential positive effects of government expenditure on growth, may be necessary.

III. Methodology

This article uses quantitative analysis to investigate BRICS economies by assessing the influence of EPU and fiscal consolidation on government debt share to GDP and economic growth using panel data from 2009 to 2022. Pesaran et al. (2001) were among the first to introduce the ARDL cointegration approach or bound cointegration technique, which is adopted in this article. This method’s implications have advantages over those of other time-series economics methods. According to Nkoro and Uko (2016) and Pesaran et al. (2001), among others, note that the ARDL cointegration technique does not necessitate a pertest for unit roots, in contrast to previous strategies. Therefore, this method is robust when underlying variables have a single long-run connection in a small sample size and is typically favoured for cointegrated variables having different orders, I(0), I(1), or a combination of both (Das, 2019; Pesaran et al., 2001; Shrestha and Bhatta, 2018). When utilizing the F statistic, the long-term association between the variables was found by the Wald test. According to this method, the long-run association between series is only considered to exist when the F-statistics value is greater than the critical value (Das, 2019). The data used in this article are reflected in Table 1.

Economic Variables.

Theoretical Framework and Model Specification

This article adopts the government budget constraint and Cobb‒Douglas. The government budget constraint framework is used because it is an essential framework that highlights the fundamental relationship between government spending, taxation and borrowing, which is key to fiscal consolidation. On the other hand, the importance of the government budget constraint lies in its ability to help policymakers make informed decisions about fiscal policy and achieve macroeconomic stability. This is key in the first question of this article. The second framework of Cobb‒Douglas is effective in assessing the impact of fiscal consolidation on economic growth, as Cobb‒Douglas’s output can then be extended to include fiscal consolidation variables. In this way, the Cobb‒Douglas production function can be used to analyse the effect of government spending cuts or tax increases on economic growth. Specifically, the function can help to estimate the elasticity of output concerning changes in government spending or taxation (Mankiw 2019). The government budget constraint in the closed economy can be reflected in Equation (1).

where the economic variables are as defined in Table 1, Equation (1) is rearranged to ɡd as the economic variable of interest in this article, as reflected in Equation (2).

The framework is used because it offers flexibility in the inclusion of other economic variables; as such, government budget constraints will be extended with other economic variables, as reflected in Equation (3).

On the other hand, the above Cobb‒Douglas is represented in Equation (4).

where A is a positive constant and α are constants between 0 and 1 (Mankiw, 2019). However, for this article, the above Cobb‒Douglas will be extended with other economic variables, as represented in Equation (5).

Stylized CAPB

The stylized CAPB is derived using the OECD approach, which focuses on the elasticity of government expenditure and tax to find the discretionary action of fiscal consolidation. The OECD approach rationale is that discretional changes are best presented when the present primary deficit would have prevailed if expenditure in the previous year had grown with potential GDP and revenues had grown with actual GDP (Mourre et al., 2013). The OECD approach is reflected in Equation (6).

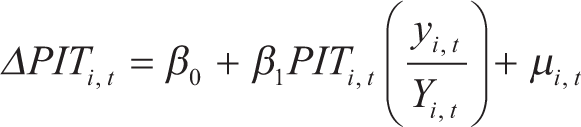

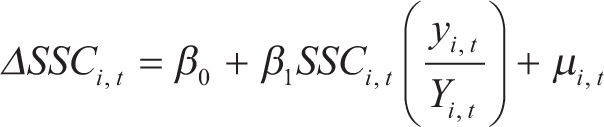

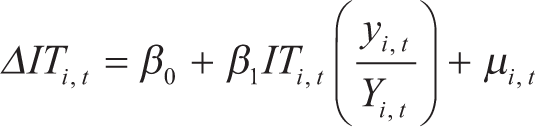

where y is the growth of nominal GDP and Y is the growth of nominal GDP potential, 1 which is estimated based on country-specific production functions. The OECD approach offers a much broader scope of CAPB because it involves a disaggregated approach and the elasticity of εtɡr tax revenue and εɡ government expenditure (Mourre et al., 2013). There are four tax revenue categories shown in Equations (7)–(10).

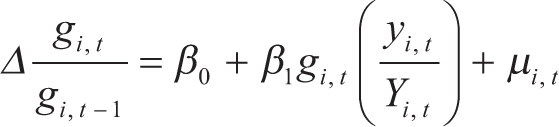

where CIT is corporate income tax, PIT is personal income tax, SSC is social security contributions and IT is indirect taxes. On the government expenditure side ɡ reflect the discretionary action of fiscal authorities is reflected shown in Equation (11).

The CAPB reflects the cyclically adjusted tax revenue and cyclically adjusted government expenditure accounting for elasticity as well as the output gap shown in Equation (12).

Model Specification

A panel of unit root tests is needed to ascertain stationarity on the economic variables used. The tests are required to determine whether the variables are non-stationary before completing the main estimations. This is crucial because it must be ensured that the variables in the regression are either integrated of order zero I(0) or at most integrated of order one I(1) to estimate an ARDL model. This is because the ARDL bounds testing approach does not produce reliable findings when there are integrated variables of order two I(2). The I(2) variables should be removed from the data set as a result (Das, 2019; Pesaran et al., 2001; Shrestha & Bhatta, 2018). The tests conducted are the Im–Pesaran–Shin unit-root test (IPS) and Levin–Lin–Chu unit-root test (LLC) (Dougherty, 2011). Whereas the CIPS unit root test loosens the requirement of cross-sectional independence of the contemporaneous correlation, the IPS test permits heterogeneity (Im et al., 2003). The LLC test is predicated on the notion that the autoregressive parameter is homogeneous. The non-stationarity null hypothesis is used in each of these tests (Levin et al., 2002). This article uses two-panel cointegration tests: Pedroni (1996) and Westerlund (2007) panel cointegration tests. The purpose of these cointegration tests is to determine whether there is a long-term relationship between variables. The Pedroni (1996) test uses three-dimensional approaches and within-four-dimensional methods. It corrects independent idiosyncratic error terms using generalized least square correction. The Westerlund (2007) cointegration test includes a four-panel estimation to test for the absence of cointegration. If the null hypothesis is rejected, cointegration exists in at least one individual unit. Pesaran (2015) introduced the cross-sectional (CD) test, the test performed in the work that controls for the presence of a cross-sectional dependency. Although transnational population impacts raise the possibility of a cross-sectional relationship, panel data estimation assumes that disturbances are cross-sectionally independent. These are all necessary conditions for the ARDL cointegration method to prevent its unwarranted application and presumption. If the conditions are not meet, this leads to inconsistent and unrealistic expectations of the model. The panel ARDL model is shown in Equation (13).

where yit is the dependent variable Xi, t – j is the k * 1 vector that is allowed to be purely I(0) or I(1) cointegrated δij is the coefficient of the lagged dependent variable βʹ ij is the k * 1 coefficient vector φi is the unit-specific fixed effect with p, q is the optimal lag orders i and t = 1, 2, …, T representing country and time, respectively. In a panel error correction representation, Equation (13) has been formulated in Equation (14).

where θi = – (1 – δij) is the group-specific speed of adjustment, λʹ i is the vector of long-run relationships, ec = [yit – λʹ i Xi, t] is the error correction term and ζij , βʹ ij are the short-run coefficients. The estimation of the ARDL equation is represented in Equations (13)–(14). This article utilized pooled mean group (PMG), mean group (MG) and dynamic fixed effects (DFE) models, 2 where PMG is the approach that relies on homogeneous intercepts across units but assumes heterogeneous slopes. The model that assumes variable slopes and intercepts within individual units is the MG. The DFE, a panel data model that implies that individual-specific fixed effects oversee producing the variation in the dependent variable over time, is the last option.

IV. Econometric Results

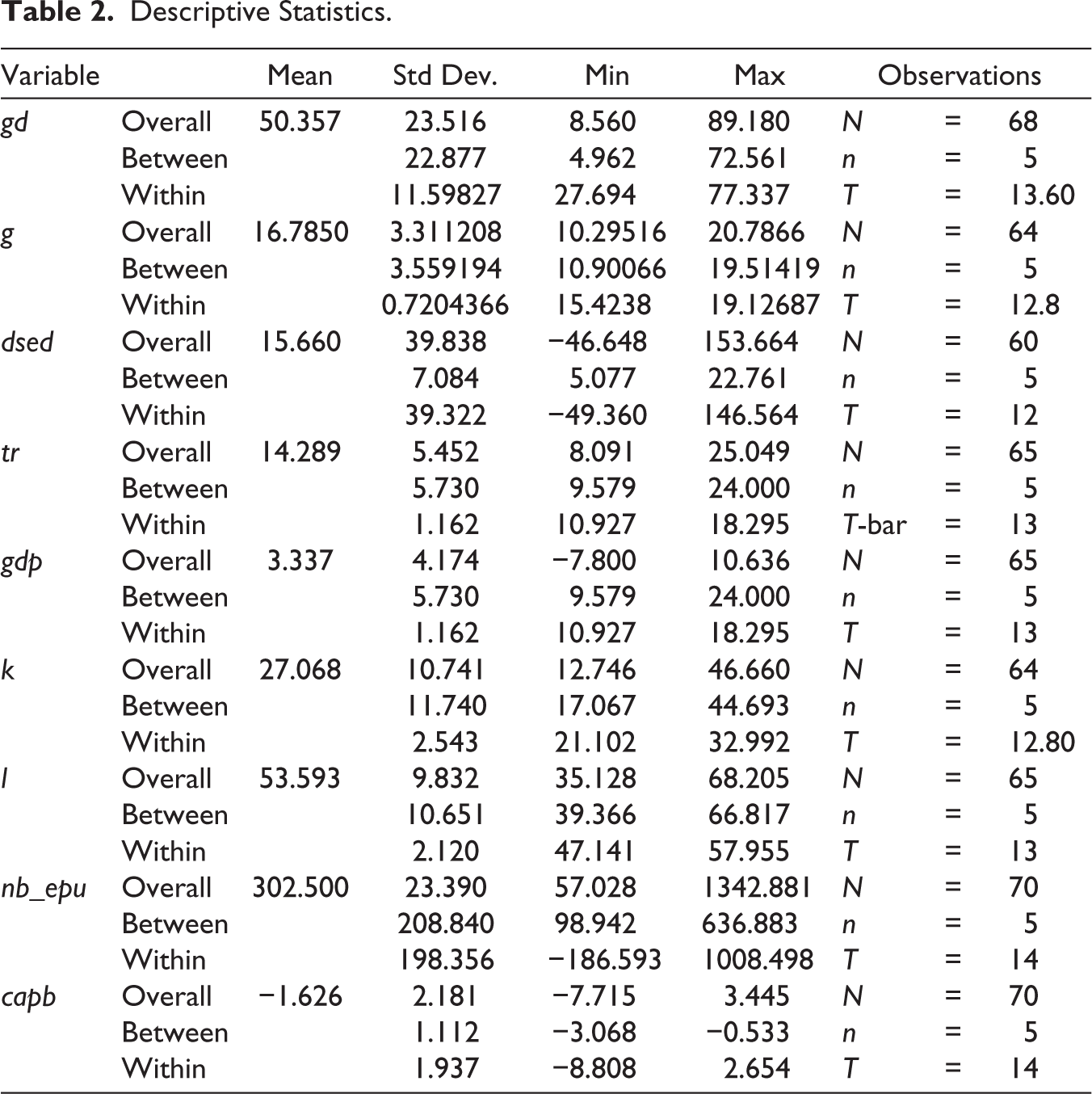

Table 2 shows the descriptive statistics of economic variables in BRICS as a block from 2009 to 2022. The mean for ɡd domestic government debt share to GDP is found to be 50.357%. This mean is below the threshold of 60% (Alloza et al., 2020), which is deemed to be unstable. The ɡ government expenditure is found to have a mean rate of 16.78%. The dsed debt service on debt share of GDP is found to have a mean of 15.660% on average over the period. The government revenue is found to have a mean rate of 14.289%. The debt service is higher than the total government revenue from the BRICS block. The government spends more on debt servicing than it does on tax revenue. This indicates that the government is now running a budget deficit, which is not long-term sustainable. Furthermore, the fact that government revenue is lower than the debt service as a percentage of GDP suggests that the nation may face difficulties in the future in repaying its debt commitments, which could result in a debt crisis. Additionally, the country may not be managing its finances as well as its peer nations in terms of managing debt and revenue if the debt service and revenue are compared to those of the BRICS block countries. This can have an impact on the nation’s credit rating and ability to access international markets. The GDP is found to have a mean of 3.337%. This is low to the 5% that is most advocated to be effective in developing economies and can help developing economies reduce macroeconomic challenges such as unemployment, poverty and equality, among others.

Descriptive Statistics.

Capital and labour are found to have a mean of 27.068% and 53.593%, respectively. This result, as per the Cobb‒Douglas 3 theoretical framework, suggests that BRICS countries are more effective in production with the use of labour. As such, BRICS countries need to focus more on sectors that are labour-absorbing in the effort to stabilize their economies and ensure that all resources, including labour, are used to their full potential. Economic policy uncertainty nb_epu and capb, the cyclically adjusted primary balance, and proxied fiscal consolidation were found to have a mean value of 302.500 and a negative value of 1.6266. This result suggests that there has been fiscal consolidation in BRICS countries. This is because the index value of 1.626 reflects a deviation that is more than 1.5, which can be attributed to fiscal consolidation episodes, as outlined by Mourre et al. (2013) and Afonso et al. (2022), among others.

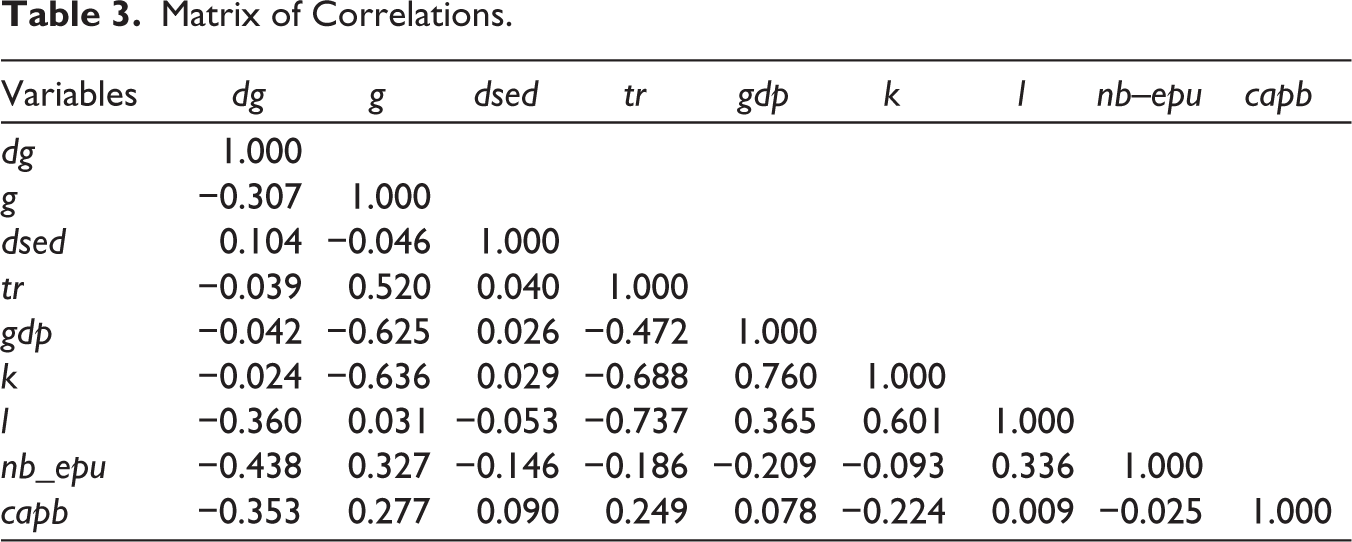

Table 3 shows the correlation matrix among economic variables in this article. Most economics, such as tgr tax revenue percentage of GDP, gdp gross domestic product growth annual percentage, k gross capital formation percentage of GDP, l employment to population ratio, 15+, total percentage modelled ILO estimate nb_epu, which is economic policy uncertainty, and capb the cyclically adjusted primary balance, have a negative relationship with dg domestic government debt share to GDP. This result implies that when these economic variables increase, the level of government debt share to GDP tends to decrease. For example, a higher tax revenue percentage of GDP would mean that the government is collecting more revenue, which could potentially reduce the need to issue debt to finance its activities. Similarly, a higher employment-to-population ratio could lead to more people paying taxes, thereby increasing government revenue and reducing the need for debt. However, it is only dsed the debt services that have a positive relationship with dg domestic government debt share to GDP. This result implies that debt services increase, and the level of government debt share to GDP tends to increase as well. This could be because higher debt services mean that the government is paying more interest on its outstanding debt, which could lead to a higher overall debt burden.

Matrix of Correlations.

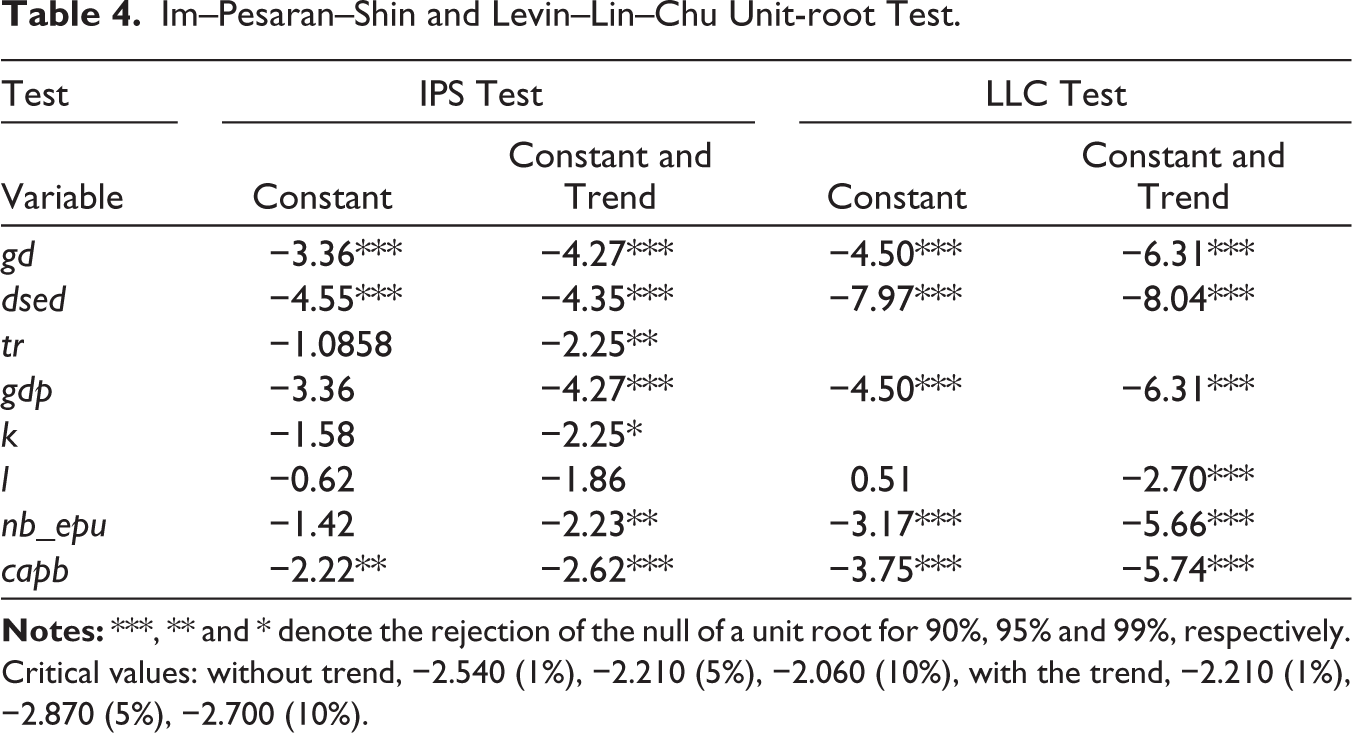

Table 4 shows that the economic variables of interest have both non-stationary and stationary characteristics. 4 All the variables of interest are I(1) according to all units except for k and l, which are integrated into the station when there is a trend in the data. This means that the variables exhibit a trend over time and do not have a fixed mean or variance, making them non-stationary. However, when a trend is removed from the data, k and l become stationary. It is crucial to remember that non-stationarity in the relevant variables might make econometric analysis difficult. The assumptions model can be broken by non-stationarity, which can result in erroneous regression findings.

Im–Pesaran–Shin and Levin–Lin–Chu Unit-root Test.

Critical values: without trend, −2.540 (1%), −2.210 (5%), −2.060 (10%), with the trend, −2.210 (1%), −2.870 (5%), −2.700 (10%).

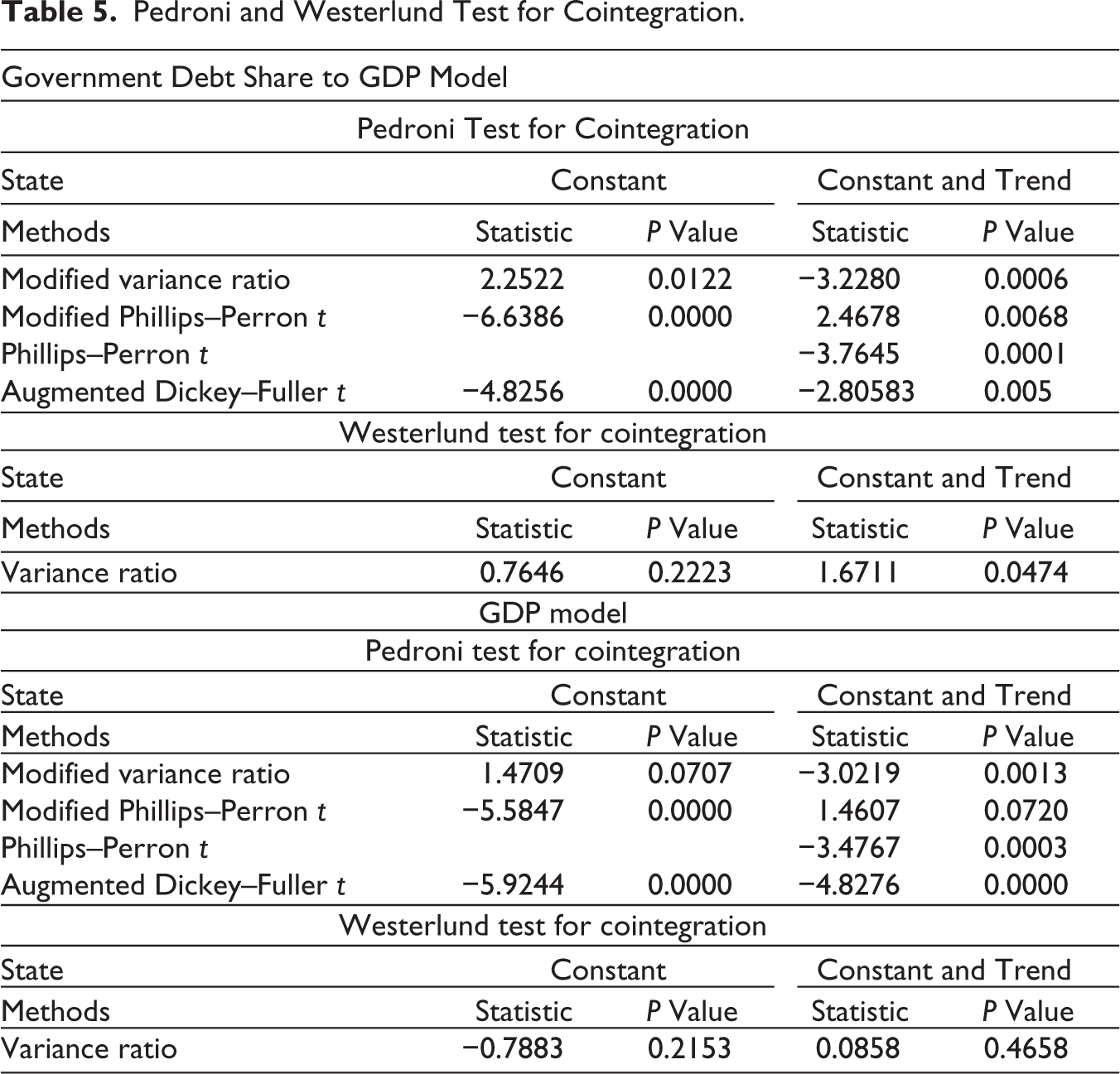

Table 5 shows the Pedroni and Westerlund test for cointegration. To examine the potential long-term connection between economic variables of interest, the paper’s two cointegration experiments are run. Table 5 shows the results of Im et al. (2003) for the Pedroni test, reflecting that it is possible to reject the null hypothesis that there is no cointegration in a varied panel, suggesting the possibility of a long-term relationship between the two variables of interest. The evidence of a potential long-term association is further strengthened by Levin et al. (2002) for the Westerlund test of no cointegration between the variables, which likewise offers strong probabilities of rejecting the null hypothesis in the p values. Cointegration is a statistical concept that plays a crucial role in analysing the relationship between two or more non-stationary time series, particularly in the field of econometrics. When dealing with economic data, many variables exhibit a non-stationary behaviour, meaning they do not follow a consistent trend over time. Cointegration helps address this issue by examining the long-term equilibrium relationship between these variables. In econometric analysis, researchers often aim to explore the long-run dynamics between economic variables. Cointegration provides a powerful tool for identifying and quantifying such relationships. By rejecting the null hypothesis of no cointegration, researchers indicate that there is a statistically significant and economically meaningful long-term relationship between the variables of interest. The results of cointegration tests, such as the popular Pedroni and Westerlund tests, suggest that the two economic variables being studied may exhibit a cointegrating relationship. This implies that there exists a stable equilibrium relationship between these variables, which persists over time. However, it is important to note that the presence of cointegration alone does not provide information about the causality or direction of the relationship. Further analysis and examination of the data are necessary to fully understand the nature and strength of the relationship. Hence the article will also use the ARDL model.

Pedroni and Westerlund Test for Cointegration.

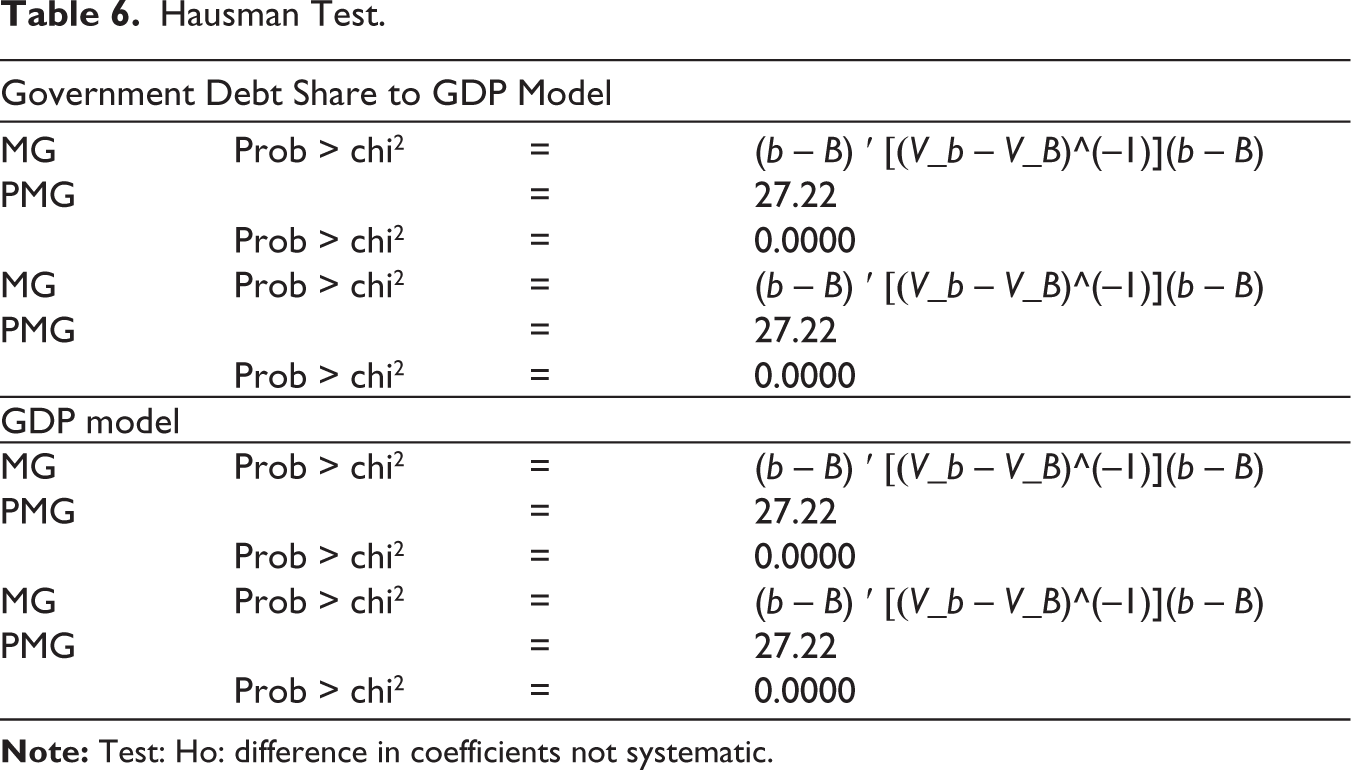

The Hausman test is a statistical test used to compare the efficiency of two or more estimators in econometric analysis. It is commonly used to choose between fixed effects and random effects models in panel data analysis. The test compares the difference between the estimates obtained from the two models to the difference in their variances. If the difference in the estimates is smaller than the difference in their variances, the fixed effects model is considered more efficient than the random effects model. The Hausman test is used in this article to ascertain which model should be used in the analysis of this article. Table 6 reflects the Hausman test result. It is found that for both model estimations of government debt share to GDP and GDP, the pooled mean group is appropriate to the MG and the dynamic fixed effects model; as such, the result that is presented in the article is that of the pooled mean group. The MG combines the advantages of both the fixed effects and random effects models. It allows for heterogeneous coefficients across individual entities (countries in this case) while also accounting for common dynamics and cross-sectional dependencies.

Hausman Test.

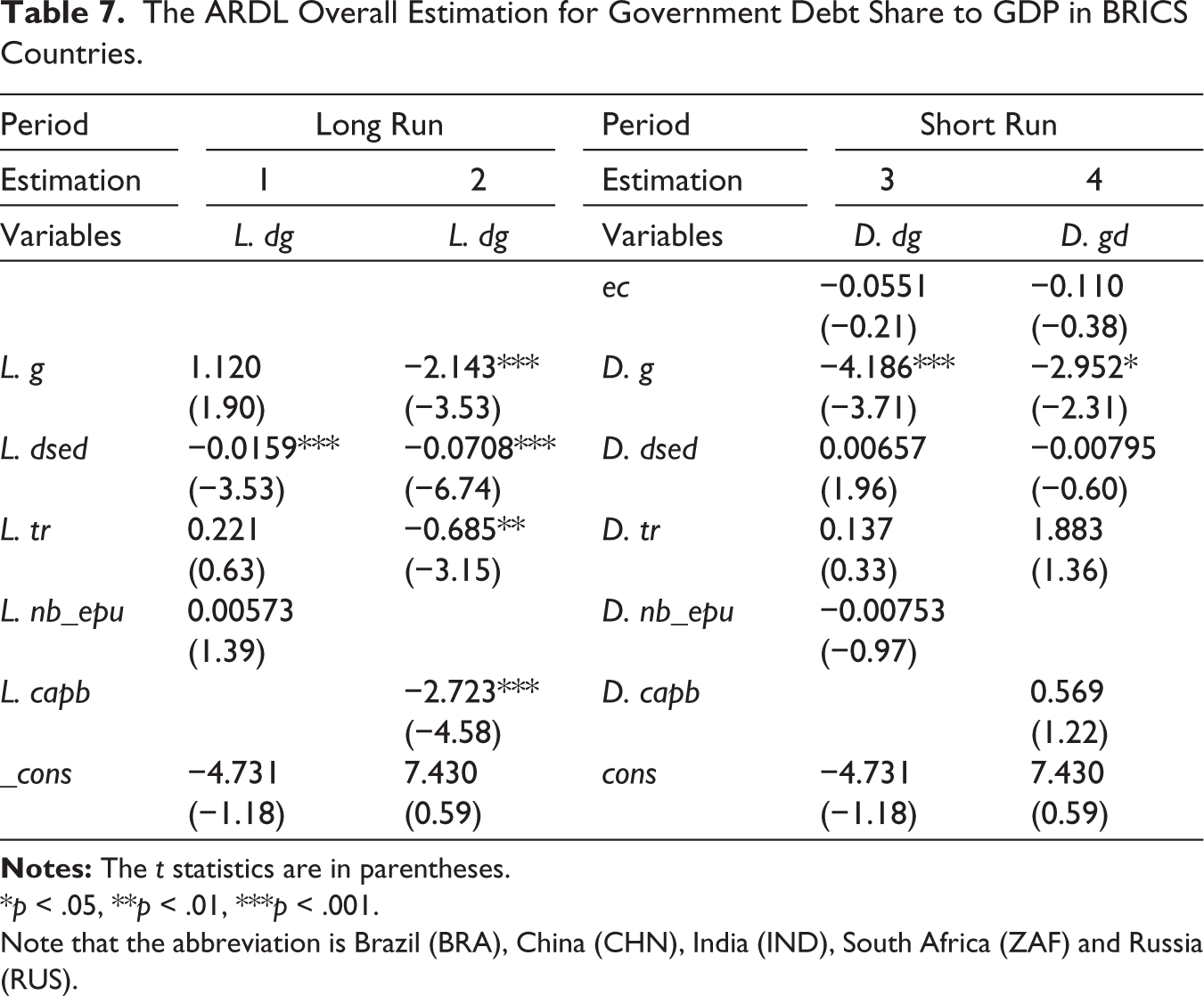

Table 7 shows the ARDL overall estimation for government debt share to GDP in BRICS countries. It is found in estimations 1 and 3 that nb_epu economic policy uncertainty has an insignificant impact on the domestic government debt share to GDP share to GDP. As such, it is not ascertained by how much the impact of EPU has an insignificant impact on the domestic government debt share to GDP share to GDP both in the long and the short run. The results reveal that EPU does not have a substantial impact on the domestic government debt share to GDP share of the GDP in BRICS countries. As a result, the impact of unclear economic policies on government debt share to GDP may not be material in either the short or long term. To preserve fiscal sustainability and stability, BRICS nations must nevertheless exercise caution when managing government debt share to GDP levels. Government debt share to GDP levels may be significantly impacted by other factors, such as changes in interest rates, fiscal policies and external economic shocks, even while EPU may not have a substantial short- or long-term impact on them. Hence, policymakers in BRICS nations must adopt sensible fiscal policies that encourage sustainable economic growth and development while simultaneously aiming to preserve manageable levels of public debt over the long term. This may entail taking steps to encourage economic growth and competitiveness, such as lowering government spending, raising taxes, boosting revenue collection and enacting structural reforms.

The ARDL Overall Estimation for Government Debt Share to GDP in BRICS Countries.

*p < .05, **p < .01, ***p < .001.

Note that the abbreviation is Brazil (BRA), China (CHN), India (IND), South Africa (ZAF) and Russia (RUS).

On the other hand, estimation two reflects a coefficient value of negative 2.723 for the capb cyclically adjusted primary balance, which is statistically significant at the 1% p value. This suggests that for a 1% increase in the fiscal consolidation proxied by capb, there will be a 2.723% fall in the domestic government debt share to the GDP in the BRICS countries that are a block eventually. These results are consistent with that of Marattin et al. (2022), David et al. (2022) and Afonso and Leal (2022) among others found that fiscal consolidation reduces government debt. In the short run, the result in estimation four of capb is found to be statistically insignificant. The results of this study have significant policy ramifications for decision-makers in BRICS nations. The analysis shows that the domestic government debt share to GDP is not significantly affected in the short or long term by economic policy uncertainty, as measured by nb_epu. The domestic government debt share to GDP can indeed be significantly influenced by fiscal consolidation measures, as measured by CAPB. Therefore, it is essential for officials in BRICS countries to prioritize the implementation of responsible fiscal measures that promote long-term economic growth and development. Fiscal consolidation involves measures aimed at reducing budget deficits and stabilizing government debt levels. These measures can include expenditure cuts, revenue enhancements and structural reforms. It is crucial, however, to strike a balance between implementing fiscal consolidation and ensuring that it does not impede economic growth.

To achieve this balance, policymakers should focus on adopting fiscal consolidation measures that are long term in nature and do not hinder economic expansion. This approach entails implementing measures that promote efficiency in government spending, prioritize investments in areas that support growth and development and enhance revenue generation without stifling business activity. Furthermore, officials should consider structural reforms that improve the effectiveness and efficiency of public administration, enhance transparency and accountability, and promote a conducive business environment. Such reforms can help create an environment that encourages private sector investment, stimulates entrepreneurship and fosters economic competitiveness. It is crucial for policymakers to carefully evaluate the potential impact of fiscal consolidation measures on economic growth and employment. By implementing responsible fiscal policies, officials can strike a balance between promoting long-term economic growth and ensuring fiscal stability. This may involve phasing in fiscal consolidation measures gradually, providing support for sectors affected by the reforms, and exploring alternative revenue sources that can contribute to sustainable economic development.

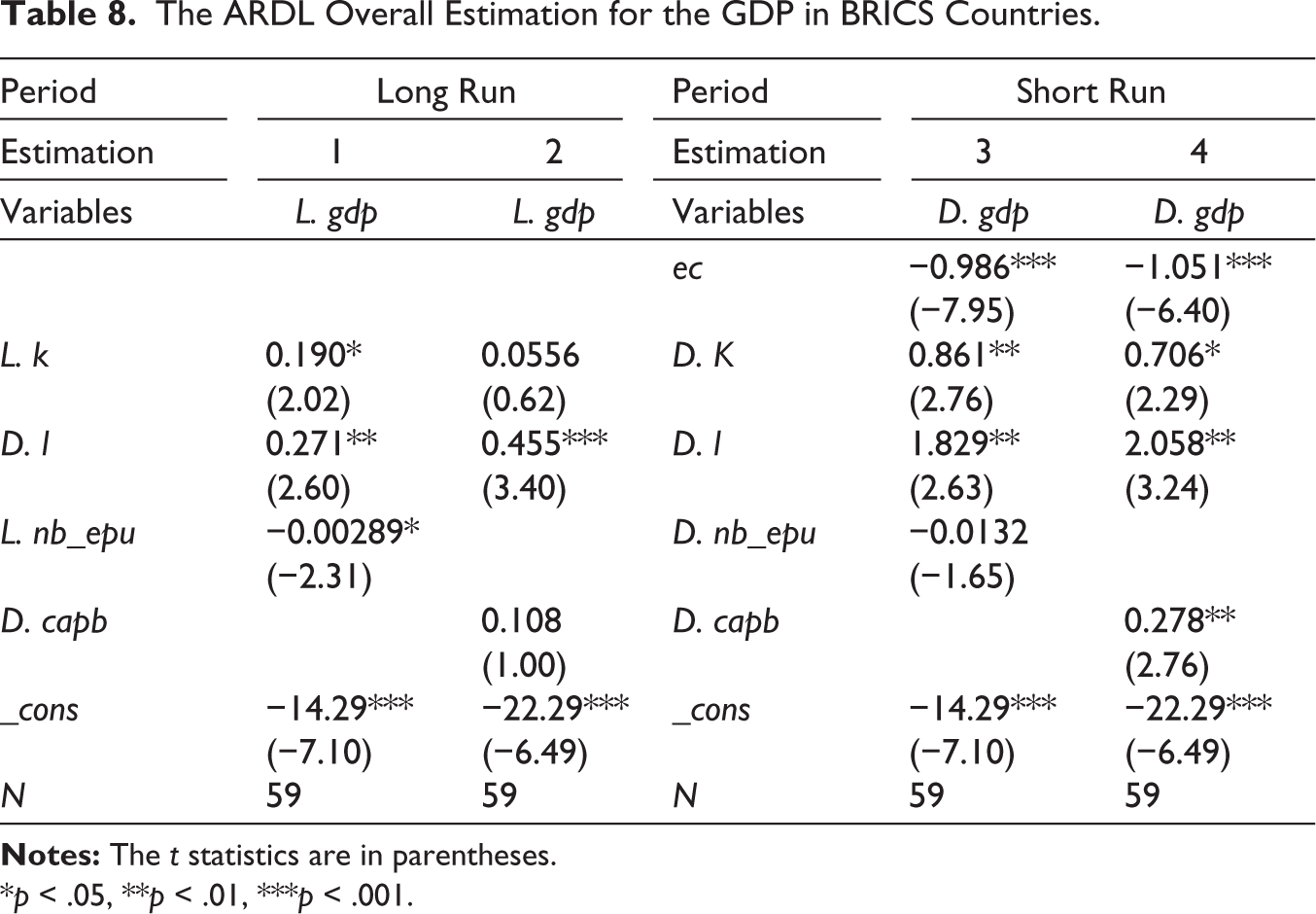

Table 8 shows the ARDL overall estimation for the GDP in BRICS countries. It is found in estimation one that nb_epu economic policy uncertainty has a significant impact at a 5% p value on the GDP with a negative coefficient value of 0.00289. The result reflects that a 1% increase in EPU will result in a fall in the GDP by 0.00289% in the long run. However, in estimation three in the short run, nb_epu economic policy uncertainty is found to be statistically insignificant. There are considerable long-term negative effects of EPU on GDP that have significant economic repercussions. Uncertainty over economic policy may increase the risk for businesses and investors, which may in turn cause them to spend less money on investments and consumer goods, which would limit overall economic growth. Long-term policy uncertainty can have a detrimental impact on the economy, deter businesses from investing, and result in lower employment rates. Wider economic repercussions may result from this, such as decreased tax revenues for the government, increased public debt and diminished economic welfare for the populace. To reduce the uncertainty around economic policy, policymakers may need to take certain steps, such as giving out clear and consistent policy signals, streamlining regulations, and enhancing communication with the public and the business community. Such initiatives may aid in promoting economic stability and growth, which may then have a favourable impact on economic indicators, including employment rates, tax receipts and the level of public debt.

The ARDL Overall Estimation for the GDP in BRICS Countries.

*p < .05, **p < .01, ***p < .001.

Fiscal consolidation is found to be statistically insignificant in estimation two of the long run. However, in the short-run estimation four, the result for capb is found to be significant at a 10% p value with a coefficient of 0.278. This result indicates that a 1% increase in fiscal consolidation results in a 0.278% increase in the GDP holding all other factors constant. The results presented here contradict the findings of Gechert et al. (2019), Bardaka et al. (2021) and Buthelezi (2023b), who concluded that fiscal consolidation has a detrimental effect on economic growth. In contrast, the current findings suggest that fiscal consolidation leads to an increase in GDP growth. These conflicting results highlight the complexity and variability of the relationship between fiscal consolidation and economic growth, which may vary depending on specific factors, methodologies and contexts analyzed in different studies. While there are consistent with that of Gründler and Potrafke (2020) and Cogan et al. (2020) found that fiscal consolidation results in an increase in GDP growth. The significant positive relationship between fiscal consolidation and GDP in the short run suggests that implementing measures to reduce government spending and increase revenues can have a positive impact on economic growth in the short term. This finding may have important implications for policymakers who are considering measures to promote economic growth and fiscal stability. While fiscal consolidation may not be a silver bullet solution for driving economic growth over the long run, it can be a useful tool for promoting short-term economic activity. To avoid the fallacy composition, the article analyses the impact of EPU and fiscal consolidation for each country in BRICS.

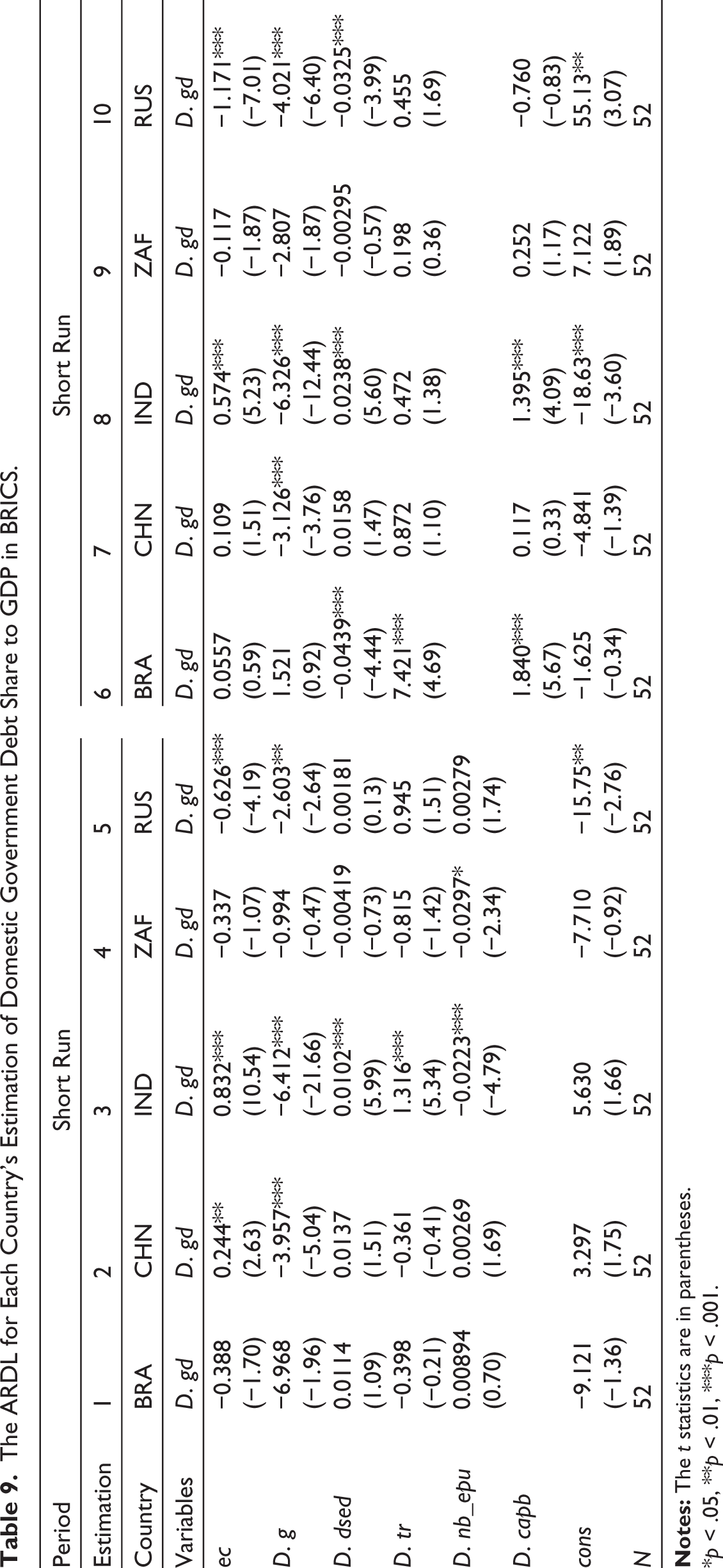

Table 9 shows the ARDL for each country’s estimation of GDP in BRICS. The results in estimations 3 and 4 reflect that in India (IND) and South Africa (ZAF), a 1% increase in nb_epu economic policy uncertainty results in 0.0223% and 0.0297% falls in gd domestic government debt share to GDP, which is statistically significant at 1% and 5% p value in the respective countries. However, in estimations 1, 3 and 5 this result for nb_epu economic policy uncertainty is found to be statistically insignificant. On the other hand, estimations 6 and 8 show that capb cyclically adjusted primary balance, in which fiscal consolidation is statistically significant at the 1% p value. The result suggests that a 1% increase in fiscal consolidation results in a 1.840% and 1.395% increase in the gd domestic government debt share to GDP in the respective country of Brazil (BRA) as well as India (IND). However, in estimations 7, 9 and 10, this result for capb cyclical adjusted primary balance in which fiscal consolidation is found to be statistically insignificant.

The ARDL for Each Country’s Estimation of Domestic Government Debt Share to GDP in BRICS.

*p < .05, **p < .01, ***p < .001.

The result suggests that there is a need to monitor and track government debt share to GDP levels regularly to identify potential risks and vulnerabilities. This can include conducting stress tests and scenario analyses to understand the potential impact of changing economic and financial conditions. Develop and implement a comprehensive debt management strategy that considers both short-term and long-term debt sustainability considerations. This may include a mix of domestic and foreign financing sources, as well as strategies to reduce debt servicing costs and manage currency and interest rate risks. Consider implementing fiscal rules and targets that aim to limit the growth of government debt share to GDP over time. These rules may involve setting limits on deficit spending, debt-to-GDP ratios or other indicators of fiscal sustainability. The results suggest that EPU can have a negative impact on economic growth and government debt share to GDP levels in some of the BRICS countries. Policymakers may need to prioritize measures that reduce policy uncertainty and create a stable business environment for investors and entrepreneurs. There is a need of balancing fiscal consolidation and debt management: The results indicate that fiscal consolidation can have a positive impact on economic growth in some of the BRICS countries, but it can also lead to an increase in government debt share to GDP levels. Policymakers may need to carefully balance the short-term benefits of fiscal consolidation with the long-term risks of increasing government debt share to GDP levels. In this regard, they may want to consider implementing a comprehensive debt management strategy that takes into account both short-term and long-term debt sustainability considerations. Policymakers need to tailoring policies to country-specific conditions because the relationships between different variables and economic growth vary across countries and estimation models. Therefore, policymakers in the BRICS countries need to monitor their respective economic conditions and design tailored policies that are appropriate for their specific contexts. This could involve a mix of fiscal, monetary and structural policies that promote sustainable and inclusive economic growth.

Ways to strengthen debt management practices are something that needs to be looked at as the results suggest that there is a need to monitor and track government debt share to GDP levels regularly to identify potential risks and vulnerabilities. Policymakers may want to develop and implement a comprehensive debt management strategy that considers both short-term and long-term debt sustainability considerations. This may include a mix of domestic and foreign financing sources, as well as strategies to reduce debt servicing costs and manage currency and interest rate risks. Strengthening debt management practices is crucial for BRICS countries to ensure sustainable fiscal health. The following measures can be considered to achieve this goals the regular monitoring and tracking as such policymakers should prioritize regular monitoring and tracking of government debt share to GDP levels. This helps identify potential risks and vulnerabilities in a timely manner, allowing for proactive measures to be taken. Developing and implementing a comprehensive debt management strategy is essential. This strategy should encompass both short-term and long-term debt sustainability considerations. It should define clear objectives, guidelines and frameworks for debt management practices. BRICS countries should explore a diversified approach to financing their debt. This includes a mix of domestic and foreign financing sources.

Table 10 shows the ARDL for each country’s estimation of GDP in BRICS. The results in estimations 3 and 4 reflect that in India (IND) and South Africa (ZAF), a 1% increase in nb_epu economic policy uncertainty results in 0.0423% and 0.0187% decrease in gdp gross domestic product, respectively, which are statistically significant at the 5% p value in the respective countries. However, in estimations 1, 3 and 5, this result for nb_epu economic policy uncertainty is found to be statistically insignificant on gdp gross domestic product. On the other hand, in estimation six, it is found that capb is the cyclical adjusted primary balance for which fiscal consolidation is statistically significant at the 5% p value. The result suggests that a 1% increase in fiscal consolidation results in a 0.2400% increase in the gdp gross domestic product in Brazil (BRA). However, in estimations 7, 8, 9 and 10, this result for capb cyclical adjusted primary balance in which fiscal consolidation is found to be statistically insignificant on gdp gross domestic product. For India and South Africa, the results suggest that an increase in EPU leads to a decrease in GDP, which could have negative consequences for economic growth and development. Policymakers in these countries may want to consider measures to reduce uncertainty and provide a stable business environment for investors and entrepreneurs. The result indicated that Brazil’s fiscal consolidation can have a positive impact on GDP. This implies that policymakers in Brazil could prioritize fiscal reforms and reduce public debt to boost economic growth. However, the insignificant results in estimations 7, 8, 9 and 10 suggest that the relationship between fiscal consolidation and GDP may not be straightforward and could depend on other factors.

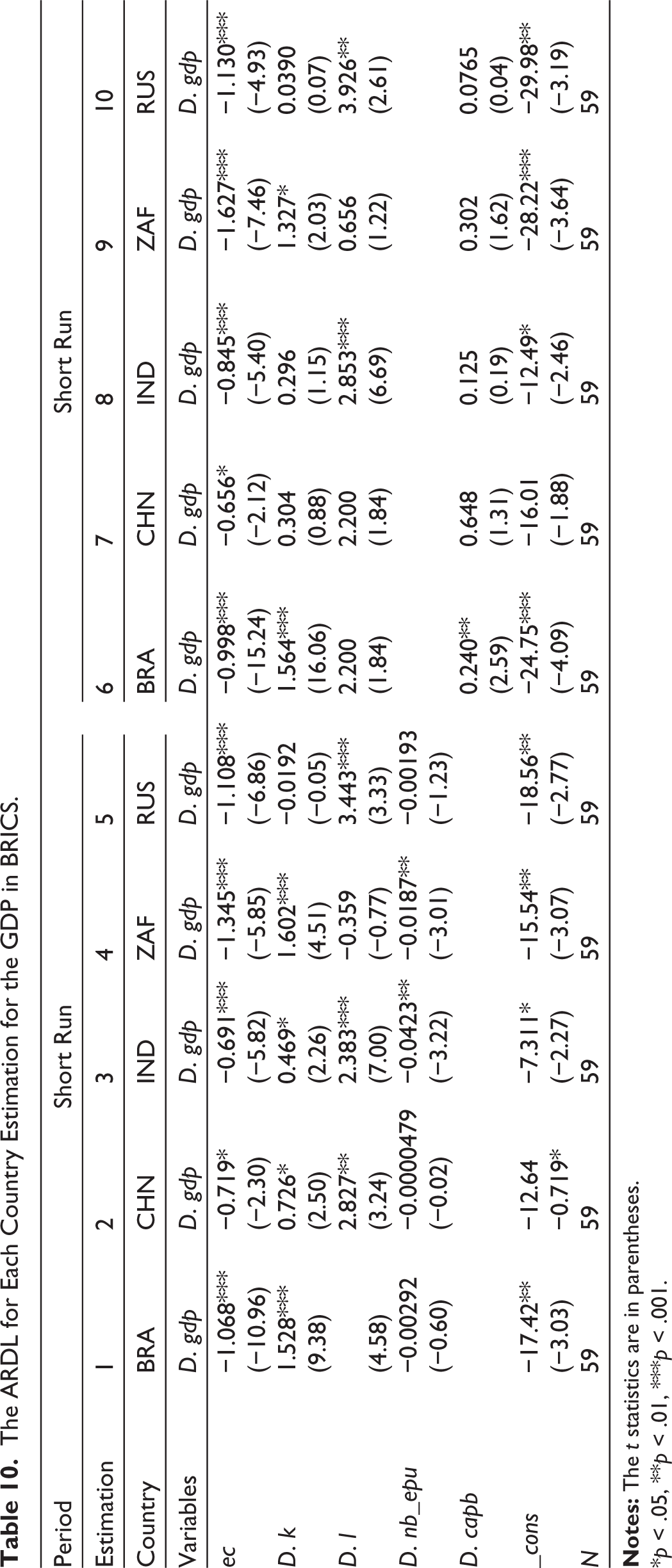

The ARDL for Each Country Estimation for the GDP in BRICS.

*p < .05, **p < .01, ***p < .001.

Tables 9 and 10 show the inconsistencies in the result of cross countries in BRIC. These may be due to the relationship between EPU or fiscal consolidation and GDP may depend on the specific characteristics of each country’s economy, such as the level of development, the size of the government sector, the openness of the economy and the structure of industries. Therefore, the same policies may have different effects in different countries, depending on their economic conditions. Therefore, it may be good for the future to incorporate this aspect in their model. On the other, the measurement of EPU or fiscal consolidation may also vary across countries. For example, different countries may use different indicators to measure EPU, such as stock market volatility, exchange rate volatility or policy announcements. Similarly, fiscal consolidation can be measured in different ways, such as changes in tax rates, government spending cuts or debt reduction targets. Therefore, differences in measurement may lead to differences in the estimated effects of these policies on GDP. The inconsistencies may also arise due to differences in the econometric models used to estimate the relationships. For example, different models may control for different variables, use different estimation techniques or have different functional forms. These differences can affect the estimated coefficients and the statistical significance of the results. It is also possible that due to other factors that are not accounted for in the models, such as external shocks, political instability or structural changes in the economy. These factors can affect the relationship between EPU, fiscal consolidation and GDP, and may lead to inconsistent results across different countries.

V. Conclusion

The article investigated BRICS economies to assess the influence of EPU and fiscal consolidation on government debt share to GDP and economic growth. The article utilized the data from the start of the block in 2009–2022. The ARDL was used in the effort to find the long- and short-run effects of EPU and fiscal consolidation on domestic government debt share to GDP as well as GDP. The key economic questions of this article are as follows: what is the long- and short-run impact of EPU on domestic government debt share to GDP and GDP? What is the long- and short-run impact of fiscal consolidation on domestic government debt share to GDP and GDP? The key result of this article is that the impact of EPU on domestic government debt share to GDP is found to be insignificant in the short and long run in BRICS countries. Fiscal consolidation measures, as measured by CAPB, have a significant impact on the domestic government debt share to GDP share to the GDP in the long run but not in the short run. EPU has a significant negative impact on GDP in the long run but not in the short run, with a 1% increase resulting in a fall of 0.00289%. Long-term policy uncertainty can have a detrimental impact on the economy, leading to decreased investments and lower employment rates.

Some of the broader concept that article provided is understanding the impact of EPU. The article provides evidence that EPU has an insignificant impact on government debt share to GDP in both the short and long run. This finding challenges the notion that EPU directly affects the level of government debt relative to GDP. It adds to the body of knowledge by highlighting the limited influence of EPU on government debt dynamics in BRICS countries. On the other hand, there was a discussion of the importance of fiscal consolidation as the article demonstrates that fiscal consolidation plays a significant role in reducing government debt share to GDP in the long run. This finding underscores the importance of implementing responsible fiscal policies and measures aimed at reducing the level of government debt relative to the size of the economy. It provides valuable insights for policymakers in BRICS countries to prioritize fiscal consolidation as a means to improve long-term debt sustainability. In terms of long-term impact on GDP, the article reveals that EPU has a significant negative impact on GDP in the long run, while its short-term impact is not statistically significant. This finding suggests that prolonged periods of EPU can have detrimental effects on economic growth over time. It highlights the need for policymakers to address EPU to promote sustainable and robust economic growth in the long run. While in the short-term the article finds that fiscal consolidation has a significant positive impact on GDP in the short run. This implies that implementing measures aimed at reducing government debt can provide a temporary boost to economic growth. This finding offers insights into the potential short-term benefits of fiscal consolidation policies, providing policymakers with guidance on managing government debt while stimulating economic activity.

Policymakers in BRICS nations should adopt sensible fiscal policies that encourage sustainable economic growth and development while simultaneously aiming to preserve manageable levels of public debt over the long term. This may entail taking steps to encourage economic growth and competitiveness, such as lowering government spending, raising taxes, boosting revenue collection and enacting structural reforms. BRICS country officials should prioritize enacting responsible fiscal measures that support long-term economic growth and development. Measures for fiscal consolidation that are long term and do not inhibit economic growth should be considered, finding a balance between economic growth and fiscal stability. EPU may not have a substantial impact on government debt share to GDP in the short or long term, but it can have a detrimental impact on GDP, limiting overall economic growth. Hence, policymakers in BRICS nations must ensure that economic policies are clear and provide certainty to businesses and investors to encourage investment and boost economic growth. Fiscal consolidation measures, as measured by CAPB, have a significant impact on the domestic government debt share to GDP in the long run. BRICS nations must exercise caution when managing government debt share to GDP levels to preserve fiscal sustainability and stability. BRICS country officials should prioritize enacting responsible fiscal measures that support long-term economic growth and development. Measures for fiscal consolidation that are long-term and do not inhibit economic growth should be considered.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.