Abstract

The presence of high inflation coupled with a persistent and ever-increasing fiscal deficit is the key problem being faced by the developing economies. The fiscal dominance hypothesis suggests that a developing economy is prone to high persistent inflation when government authorities run huge persistent budget deficits and get them financed through money creation. The primary objective of the current study is to test and examine the presence of the fiscal dominance situation over the period 1971–2020. The current study has modelled inflation as a fiscally driven monetary phenomenon by combining monetary and fiscal variables. The study has used the autoregressive distributed lag (ARDL) technique to analyse the long-run and short-run dynamics in a unified framework. The empirical results point to strong and statistically significant long-term relationships between budget deficits and money growth and between money creation and inflation. The study validates the presence of the fiscal dominance hypothesis in the case of a developing economy. The results imply that fiscal dominance handling through a realistic and continuous process of fiscal adjustments on the back of supported monetary policy is necessary for attaining and sustaining price stability in developing countries like Pakistan. In the context of public finance, a broad and wide-ranging tax reforms (increasing the tax base, designing an inflation-proof tax system, and improving tax administration and collection), rationalized government expenditures and privatization of loss-making state enterprises are crucial in establishing the trustworthy fiscal policy.

Introduction

Inflation remains the core indicator of overall macroeconomic stability or the ability of the incumbent government to handle its economy. Fischer (1993) states that if an incumbent government is unable to maintain the optimal level of inflation, it means that the government has lost its control. The conventional wisdom states that optimal inflation should be low or at a moderate level to keep the sustainable economic development. The empirical literature highlights that inflation should be controlled to enhance output of economy by making ‘prices and wages more flexible’, whereas high inflation induces uncertainties in the economic system and hampers overall output of a country. There are mainly two types of uncertainties. The first kind of uncertainty is the policy-induced macroeconomic uncertainty, which would reduce the productivity and growth within the economy, while the second kind of uncertainty would temporarily reduce the rate of investment, as the economic agents would likely pause till the resolution of the uncertain conditions. Besides, high inflation also discourages savings, encourages borrowings and increases the nominal rate of interest, and it has a negative impact on investment and productive activities.

The fiscal and monetary policies are the two tools that governments use to manage various aspects of the economy (Sawhney, 2018). The various studies advocate the monetarist rule, for example, McCallum (1999, 2001, 2003) and Niepelt (2004), and challenge the fiscal theory of price level (FTPL) that was proposed by Leeper (1991), Sims (1994) and Woodford (2001), which elaborates that the public finances must be sustainable for the stable price level in an economy. Previously, a well-known work of Sargent and Wallace (1981) acknowledged that the governments facing persistent deficits have to finance their deficits with money creation that results in high inflation levels. The fiscal view of inflation gains a distinct consideration in the developing countries as it is a generally accepted viewpoint that the developing economies face several issues such as inefficient tax collection, political instability and an inadequate availability of foreign loans (Calvo & Végh, 1999; Cukierman et al., 1992; Drazen & Alesina, 1989), and such factors tend to decrease the relative cost of seigniorage and a high dependency on the inflation tax. Particularly, De Haan and Zelhorst (1990), Metin (1998), and Domaç and Yücel (2005) focused on developing countries and validated that there is a significant linkage between fiscal deficits and inflation in high-inflation economies. Though Catao and Terrones (2005) do not ignore the significance of other factors that play a major role in increasing the level of inflation.

The increase in foreign debt burden of developing economies concerns paves the way towards an extraordinary rise in their debt-to-gross domestic product (GDP) ratio, leading to the trap of debt overhang along with the possibility of fiscal dominance. This possibility is the position of a country where increase in debt-to-GDP ratio restricts the conduct of monetary policy, persuading the central bank to dedicate its attention to decrease the servicing costs of public debt (Ahmed et al., 2021; Blanchard, 2004). Sargent and Wallace (1981) argued that an inflation becomes inevitable in a situation where fiscal policy corrects an exogenous path for the real primary budget deficit, irrespective of the choice of monetary policy. These circumstances lead the public debt to reach a limit, beyond which further government borrowing is impossible, implying that monetary policy will be induced to create sufficient seigniorage revenues to finance the deficit, as may be the case if a central bank’s independence is in doubt.

This arrangement leads to ‘fiscal dominance’, where the central banks are asked/instructed to handle the fiscal pressure. A follow-up perspective on these issues is provided by Woodford’s contributions. Woodford (1998) outlined an example where even an independent central bank will choose to react to fiscal news. Specifically, there are plausible circumstances where the fiscal authority would change its policy when a country’s ‘debt limit’ were reached. A central bank charged to maintain price stability can also concern itself with the conduct of fiscal policy. The central bank might seek to ensure that the fiscal authority is committed to a Ricardian policy, without then feeling any further need to participate in the year-to-year conduct of fiscal policy. Alternatively, a central bank operating in a country where the fiscal policy is non-Ricardian would be aware that unexpected changes in government’s budget would affect the equilibrium price level.

This in turn may induce the central bank to influence fiscal policy decisions on an ongoing basis. Woodford also shows that a policy deemed as achieving price stability in an environment of Ricardian fiscal policy might be disastrous in the case of a non-Ricardian fiscal policy. In these circumstances, a conclusion that fiscal policy is non-Ricardian would concern the central bank with debt management issues since the composition of the public debt matters for the behaviour of equilibrium inflation, as Cochrane (1996) illustrated. Specifically, the longer the duration of the nominal bonds, the more sharply its value will decline with increases in inflation. Thus, inflation is unambiguously less affected by fiscal shocks when the public debt is of longer maturity. In the same vein, higher indexation of government debt affects inflation variability in the case of non-Ricardian fiscal policy.

The present study is an attempt to re-examine the issue under the fiscal dominance framework for Pakistan over the period 1971–2020. The current study has followed the International Monetary Fund (IMF) approach presented in Nachega (2005) and analysed the fiscal dominance situation by combining monetary and fiscal variables in a unified model. The present study has examined the existence of fiscal dominance or otherwise in Pakistan through autoregressive distributed lag (ARDL) approach. The primary objective of the current study is to test and examine the presence/validity of fiscal dominance hypothesis or otherwise in the economy of Pakistan from 1971 to 2020.

To the best of our knowledge, there is no such study available for Pakistan that has tried to analyse fiscal dominance hypothesis by combining monetary and fiscal variables together. Moreover, the study has used the ARDL approach for Pakistan. This approach links the economic theory to multiple time series. The current study has examined the fiscal dominance hypothesis in Pakistan, which is a developing country and has experienced persistent fiscal deficits, a rapid increase in money supply, high levels of inflation and slow output growth over the past five decades. The study has empirically modelled inflation as a fiscally driven monetary phenomenon and pays attention to economic theory, non-stationarity, data congruency of the specification, parameter constancy and exogeneity. Weak exogeneity of the fiscal deficit is not imposed a priori but is established within the empirical model.

The whole study is organized into five sections. Section I provides a brief introduction to inflation and fiscal deficit relationship in the context of the fiscal dominance hypothesis. Section II entails a discussion on the existing body of available literature. Section III illustrates the econometric model, data utilized and the research methodology undertaken for the analysis. Section IV provides the empirical results and discusses the results. Section V concludes the discussion and provides suitable policy implications.

History of Inflation in Pakistan

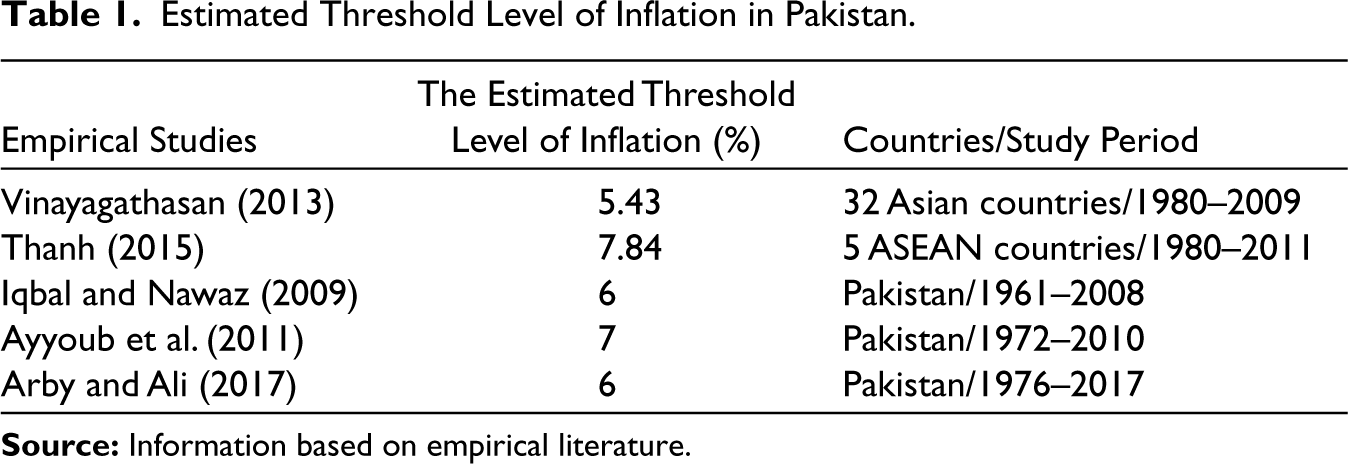

Pakistan remained the high-inflation economy during the past five decades. The threshold level of inflation is estimated to be 6%, implying that the inflation rate beyond this level is hampering the process of economic development by creating the uncertainties in the system for economic agents (Arby & Ali, 2017). Accordingly, it is revealed that the country has experienced high inflation for about 33 years in the past 50-year period. Although the political and institutional structure that links fiscal deficits to money creation and inflation has kept on changing in Pakistan, it is somehow unable to manage the inflation in the desired range. We have experienced two military governments during the sample period of study (first during 1977–1988 and the second during 2002–2008) and seven democratic government set-ups during this period. The period from 1988 to 1999 was the period of extreme political volatility as four general elections were held; however, no political government could complete its allowed tenure of 5 years for which it was mandated through election by the people.

In the 1990s, Pakistan also went through very extensive financial structural and liberalization reforms to transform the financial markets into a competitive, efficient and a market-oriented system (Husain, 2005). Along with this, Pakistan has also taken the IMF relief packages under the IMF Structural Adjustment Programs for 13 times since its membership in the year 1950. Whenever a country is bailed out by the IMF relief package, it has to face and qualify the IMF conditionality. Under the IMF conditionality system, the borrowing government has to assure that the government will adjust its economic policies as per the agreed rules to overcome the distressing economic conditions (Breen, 2013). Unfortunately, the IMF regulatory system also remained unable to ensure inflation in the optimal range. The fiscal deficits have risen from 5% to 9% of GDP that have caused a massive increase in the money supply and a stern depreciation of the Pakistan currency during these years (Qayyum, 2006). After the 2018 election, the situation became even worse, and Pakistan has just touched the highest peak in terms of inflation (i.e., 11%) in its history, and the economy was confronted with increasing debt and liabilities, twin deficits, that is, current account balance and fiscal balance with depleting foreign exchange reserves and rising circular debt (Government of Pakistan, 2018). Given the prevailing alarming and distressing situation, there is an open call for research from the academia. The Table 1 indicates the various studies in empirical literature which estimate threshold level of inflation for the case of Pakistan.

Estimated Threshold Level of Inflation in Pakistan

Estimated Threshold Level of Inflation in Pakistan

In developing countries, high inflation rates are linked to large persistent budget deficits that are largely financed through money creation (Ito et al., 2011). Accordingly, the fiscal deficit has put pressure on central banks for monetary expansion, and consequently, the fiscally driven monetary expansion became dominant due to high inflation, which is known as the ‘fiscal dominance hypothesis’ in the literature (Bildirici & Ersin, 2005; Leeper, 1991; Nachega, 2005; Sims, 1994). The fiscal dominance hypothesis points to the interactions between fiscal and monetary policy, and in such a situation, fiscal policy becomes an appropriate channel for controlling inflation instead of the monetary policy (Gadea et al., 2012; Nachega, 2005). The association between fiscal deficit and inflation has been widely examined in the case of both developed and developing economies and mostly found to be in a significant positive relationship (Adu & Marbuah, 2011; Nguyen, 2015; Solomon & De Wet, 2004).

According to Barro (1979), there exist positive linkages among fiscal deficits and money growth. Fratianni and Spinelli (2001) highlighted the presence of fiscal dominance in the Italian economy since its political unification in 1861. The study emphasized that the nature of the institutional mechanism, which links fiscal deficits to money base creation, has been fluctuating over time. After political unification, the profit-seeking banks crossed the legal ceiling of outstanding currency for lending to the government. The public finances influenced monetary policy during the 1930s and late 1970s when fiscal dominance reached its peak. During the 1990s, fiscal dominance was present but in the opposite direction. For fulfilling the requirements of the Maastricht Treaty and qualifying for entrance into the European Monetary Union (EMU), the policymakers in Italy granted independence to the central bank and considerably controlled the fiscal deficits.

Furthermore, Solomon and De Wet (2004) identified the Tanzanian economy as one of the limited number of countries that has experienced a high inflation rate and high fiscal deficits and traced the causal link between monetization of budget deficit to inflationary effects in the economy during the period 1967–2001. Likewise, Nachega (2005) examined the existence of the fiscal dominance hypothesis in the Democratic Republic of the Congo (DRC) from 1981 to 2003. The study employed a co-integration and vector error correction model for analysis. Empirical results suggest a significantly strong long-run association between fiscal deficits and seigniorage, and between money creation and inflation in the case of DRC. The study by Nguyen (2015) also confirms the validity of the fiscal dominance hypothesis in Asian economies, namely Bangladesh, Cambodia, Indonesia, Malaysia, Pakistan, Philippines, Sri Lanka, Thailand and Vietnam.

A few attempts have also been made to investigate whether inflation is a monetary or fiscal phenomenon in Pakistan as well. Qayyum (2006) empirically verified that growth in money supply has been the main factor in the ever-increasing inflation in Pakistan for the past three decades by using the quantity theory of money and formulated the theory of determination inflation (prices). The study employed correlation matrix and the ARDL approach for analysis of the empirical model. It is noted that Qayyum’s (2006) results are in line with Friedman’s proposition that ‘Inflation is purely a monetary phenomenon everywhere’; however, the study has missed to relate it with the root cause or the factual culprit, that is, the ever-increasing fiscal deficit behind the money supply growth.

In contrast, Mukhtar and Zakaria (2010) bridged this gap and addressed inflation as an outcome of persistent fiscal deficits in the economy and document that inflation cannot be solely controlled or prevented by the sole monetary policy. The said study empirically verified the said argument, however, does not find supportive results for inflation being the fiscally driven phenomenon during the underlying period. However, Shaheen (2018) validates the existence of the fiscal dominance hypothesis in the economy of Pakistan and associated its significance to the democratic/elected government regimes in comparison to the military regimes in Pakistan. Batool and Sieg (2012) relate inflation to the presence of opportunistic political business cycles. The study empirically verified that there is an increase in fiscal deficit that is financed by high borrowing/debt from the central bank and banking sector during the pre-election and election year in Pakistan.

Moreover, literature revealed that there exists a non-linear linkage between inflation and economic performance (Khan & Senhadji, 2000; López-Villavicencio & Mignon, 2011; Seleteng et al., 2013). Non-linear relationships meant that at a certain range, linkages between inflation and economic development would be positive, while it would be negative after a certain level. When inflation level starts inhibiting economic growth, it is known as the ‘threshold level of inflation’ in the literature. More interestingly, it is noted that economies may differ in terms of a threshold level of inflation largely based on some country-specific factors such as financial deepening, trade openness, public expenditures and capital accumulation level (Eggoh & Khan, 2014; Fischer, 1993; Khan & Senhadji, 2000; López-Villavicencio & Mignon, 2011). It is believed that countries that are more financially developed will confront severe economic shocks of inflation (Akinsola & Odhiambo, 2017; Khan & Senhadji, 2001).

Model, Data and Research Methodology

The baseline of our analysis is the following model:

where INF represents the inflation rate in the economy, FD is the fiscal deficit/budget deficit and X elaborates the vector of several conditioning variables that have the potential to influence the inflation rate in any economy. The fiscal dominance hypothesis implies that fiscal deficit influences inflation through its effects on broad money supply and seigniorage in any country. The broad money velocity usually positively influences inflation as it captures the effect of damage of confidence in the national currency, which is the result of high expected inflation or anticipation of currency depreciation. At a specific level of the budget deficit, the high expectation of currency depreciation or high inflation would lead to more flights out of money and lower demand for money.

The functional form of Equation (1) can be transformed as follows:

The INF is the inflation rate in the economy and is measured as a rate of change in the consumer price index. According to the definition put forth by the IMF, inflation is defined as the rate of increase in prices during a certain time period. Inflation is normally considered as a broad measure, like the overall rise in prices or the rise in the cost of living in a particular country. However, it could be narrowly calculated—for certain goods like food, or for services like a haircut. Whatever the context, inflation represents how much more expensive the relevant set of goods and/or services has become over a certain period, most commonly a year. The FD is the overall budgetary deficit of the country expressed as a percentage of GDP. Strong and Yayi (2021) defined budget deficit as a difference between government expenditures and government revenues. The GRM indicates the rate of change of the broad money supply in the economy. The term money supply means the currency and coins issued by the central bank of the country and different types of deposits held by the public at commercial banks and other depository institutions such as microfinance banks, development finance institutions and credit unions. Similarly, The money velocity can be thought of as the rate of turnover in the money supply, that is, the number of times a single unit of particular currency is used for purchasing final goods and services included in GDP. The VEL represents broad money velocity, which is measured as nominal GDP divided by broad money in the country. The SEI denotes an indicator of seigniorage that is measured as a change in broad money in the country divided by the GDP of the economy. Moreover, in the theoretical literature, seigniorage is usually defined as the revenue of the government earned from the creation of money (Klein & Neumann, 1990).

The GRE is representative of the rate of change of the nominal effective exchange rate (NEER) index. The NEER is defined in literature as a measure of the value of a particular currency against a weighted average of group of foreign currencies. An increase in NEER indicates an appreciation of the local currency against the weighted basket of currencies of its trading partners.

Equation (2) works on the assumption of instant adjustment/variation of actual inflation to the level of equilibrium, given its determinants. The instant adjustment/variation is unlikely in the case of transaction costs and uncertain adjustment speed money market where inflation is determined. Here, it is worthy to mention that while the current study focuses on testing and analysing the fiscal dominance hypothesis in the economy of Pakistan, we implicitly undertake that inflation is determined by the money market. A distinction is hence made among the long- and short-run movements/variations in inflation by stipulating a mechanism of error corrections in inflation rate towards its long-run level. According to the quantity theory, it is presumed that the real income escalates in the long run, and the money velocity remains constant. In this assumption, inflation is determined by the change in the money supply. Friedman and Schwartz (2011) reported that this is quite an intense proposition that the velocity remains constant and must not be considered. The level of income and velocity of money grows slowly, and this movement/fluctuation is independent of the variations in inflation and money supply (Laidler, 1997). The quantity theory of money also identifies that the money supply is the primary factor that influences the variations in the price level. According to Bordo and Jonung (1990) and Gordon (1983), the velocity can be determined by several factors, which include the financial structure within the economy, monetization, budgetary deficit, shifts in government spending patterns, etc.

Data

The study has used the annual data series for the period 1971–2020. The data set has been collected from the State Bank of Pakistan (SBP)-published official sources, that is, the SBP Handbook of Statistics on the Economy of Pakistan, 2015, and Annual Report of State Bank of Pakistan, 2020. We have started our analysis from 1971 onwards to get the uniform data set for Pakistan’s economy, formerly known as West Pakistan.

Econometric Methodology

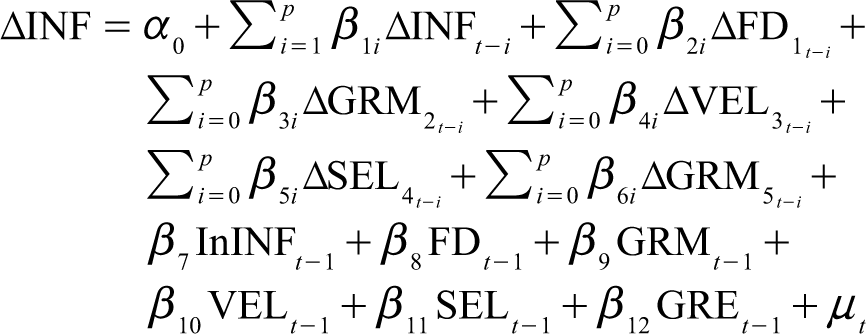

The study has estimated the dynamic long-run and short-run relationship using the ARDL model by Pesaran et al. (2001). The underlying method has a number of advantages over other co-integration methods: (a) other co-integration methods require the variables to be integrated of the same order included in the equation, but the ARDL approach estimates even if the variables are I(1) and I(0) in a same eqaution; (b) it estimates the long-run and short-run impacts among the variables simultaneously even in the case of a small sample size; and (c) it estimates the unbiased and impartial coefficients of variables with true t-values, even if the underlying explanatory variables are endogenous. We have used the ARDL specification as follows:

where Δ is a difference operator. The study used the ARDL bound test of co-integration using F-test for significance. The study has employed several diagnostic tests for checking the irregularities (if any) in the estimations, which include White’s test for heteroscedasticity, Ramsey RESET test for model misspecification and cumulative sum (CUSUM) and cumulative sum of square (CUSUMSQ) tests for testing the stability of coefficients in the underlying model. Further, the study also used the Granger causality test to examine the direction of causality among the variables.

Descriptive Statistics

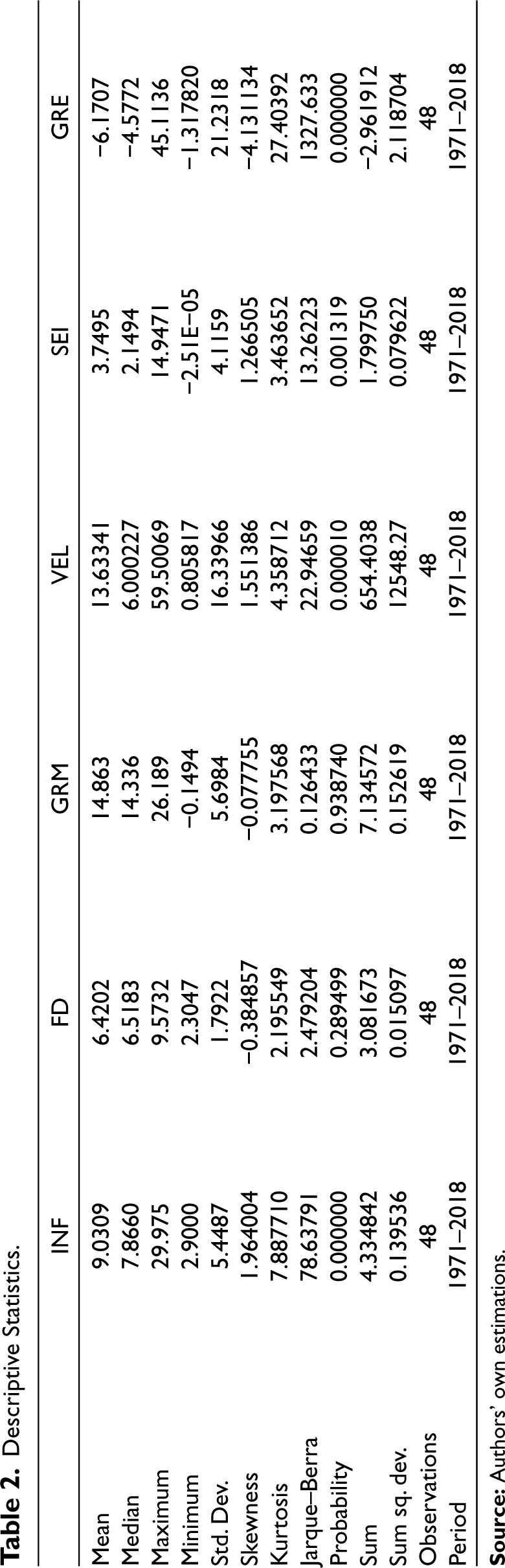

Table 2 summarizes the descriptive statistics of data. The results presented in Table 2 show that average inflation remained at about 9% with a minimum of 2% in the year 2003 and touched the highest value, that is, 29% during the year 1974 and SD was about 5% during the period. The GRM and FD ranged from 0–26% to 2–9%, respectively, from 1971 to 2018. The mean value of all variables is positive except GRE. The variables have a mixed value of skewness, that is, some variables are skewed negatively for some variables, and some variables are positively skewed. Table 2 provides summary statistics for the sample. It is specified that for every variable, the SD value is near to the pseudo-SD.

Descriptive Statistics

Descriptive Statistics

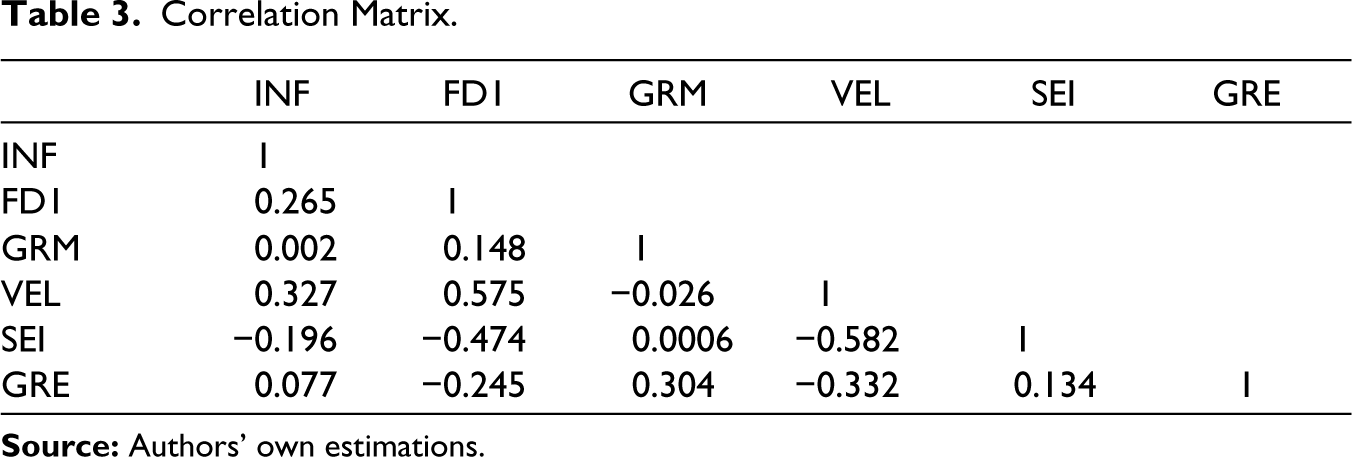

All the series have weak correlation, as all correlation coefficients (r) could not surpass the value of 0.60. Furthermore, these outcomes are verified by the cross-correlation analysis. The results of the correlation matrix are presented in Table 3.

The Unit Root Analysis

The time series analysis works on the assumption that the series employed in the model is stationary. In case the stationarity is ignored, this violation could result in spurious outcomes. Therefore, the very first step is to test the stationarity properties of variables included in the analysis. The augmented Dickey–Fuller (ADF) test was employed to examine the stationarity and non-stationarity properties of the data series. ADF test estimation starts with simple autoregressive AR(1) model:

where μt is a white noise process. If | μt | < 1, the variable is stationary at level, and if | μt | = 1, then the variable is non-stationary at level. In simple words, if the variable is non-stationary, it implies that its mean, SD and covariance are time variant. The empirical results show that all the variables are non-stationary or we say integrated. Furthermore, to check the order of integration, we have taken the first difference of the data series and applied the ADF unit root test again. The results of unit root test results show that series are stationary at the first difference level.

Correlation Matrix

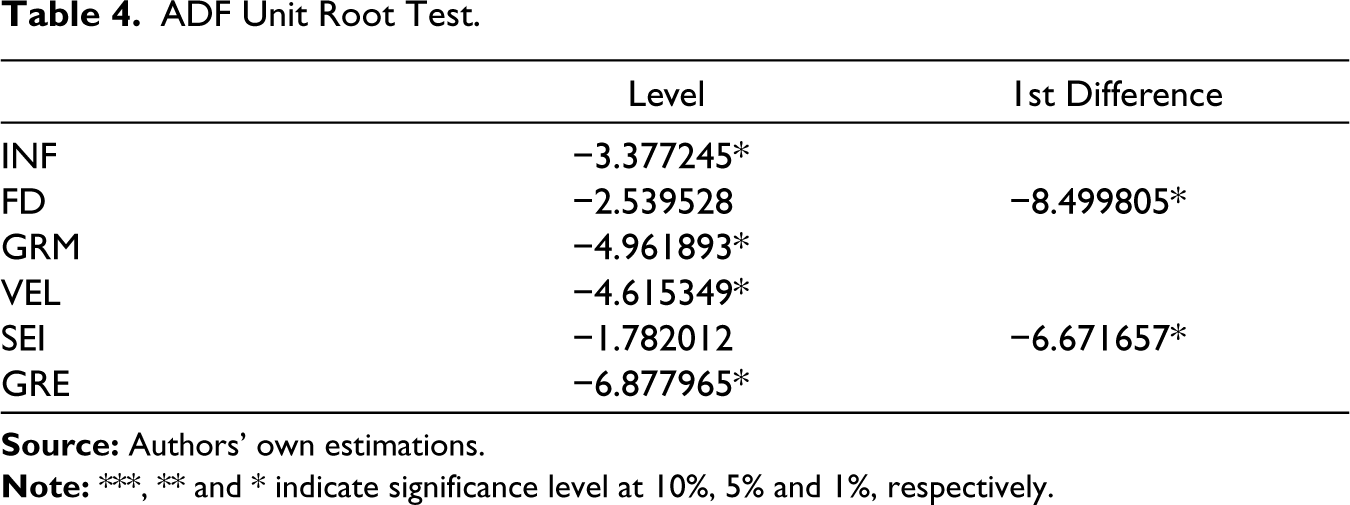

The ADF test results are reported in Table 4. The results indicate that all the series are stationary either at level, that is, I(0) or at level ‘1’ means I(1). Therefore, the study has used the ARDL model here.

ADF Unit Root Test

Autoregressive Distributed Lag Estimated Results

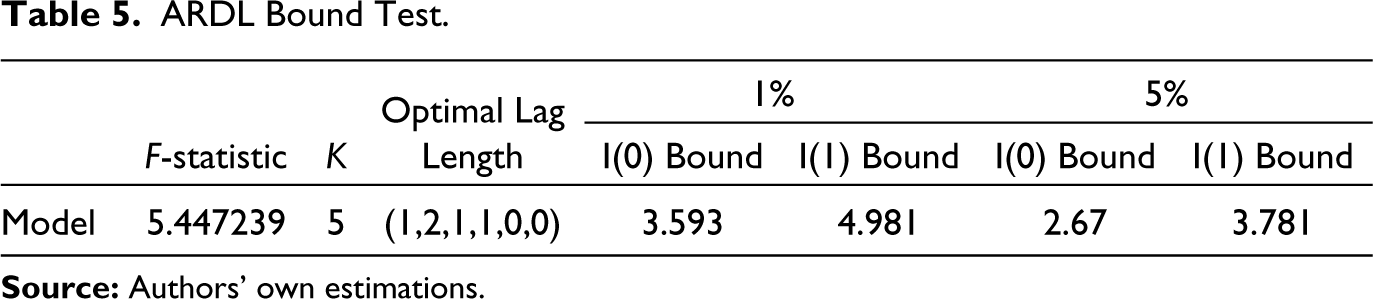

The ARDL bound test method of co-integration is sensitive to lag length; therefore, optimal lag length should be selected carefully. The current study has selected the optimal lag length based on the Akaike information criterion (AIC) mentioned in Table 5. The estimated values and critical values for analysis of the null hypothesis are also presented in Table 5.

ARDL Bound Test

The study estimates two sets of critical values for upper bounds I(1) and lower bounds I(0) for different sample sizes ranging between T = 30–80 (Narayan, 2005). The estimated results show that F-statistic is higher than the upper bound value at a 1% level of significance. It implies that there exists a long-run equilibrium relationship between inflation and its determining fiscal and monetary variables, which include the fiscal deficit, broad money supply, broad money velocity, seigniorage and NEER at a 5% level of significance during the underlying period.

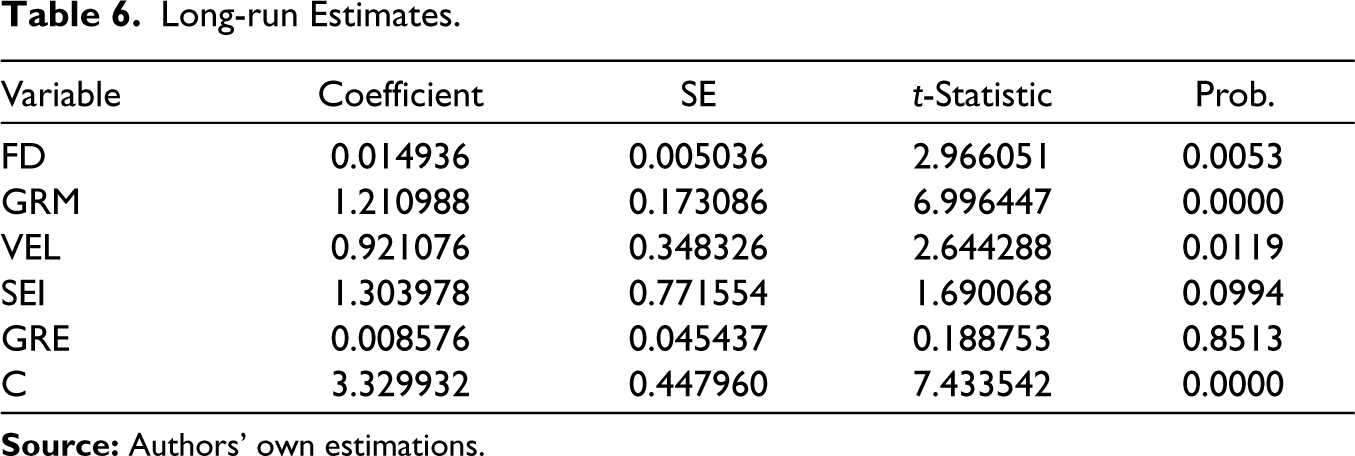

The estimated long-run relationship states that the fiscal deficit has a positive and significant impact on inflation (see Table 6). Similarly, GRM has a strong positive and significant impact on inflation, thus validating Friedman’s proposition that inflation is a monetary phenomenon. The estimated coefficient value of SEI also shows a positive and significant impact on inflation in the economy during the study period. All the variables are found to have a strong and positive relationship with inflation; however, GRE turned out with insignificant results (see Table 6).

Long-run Estimates

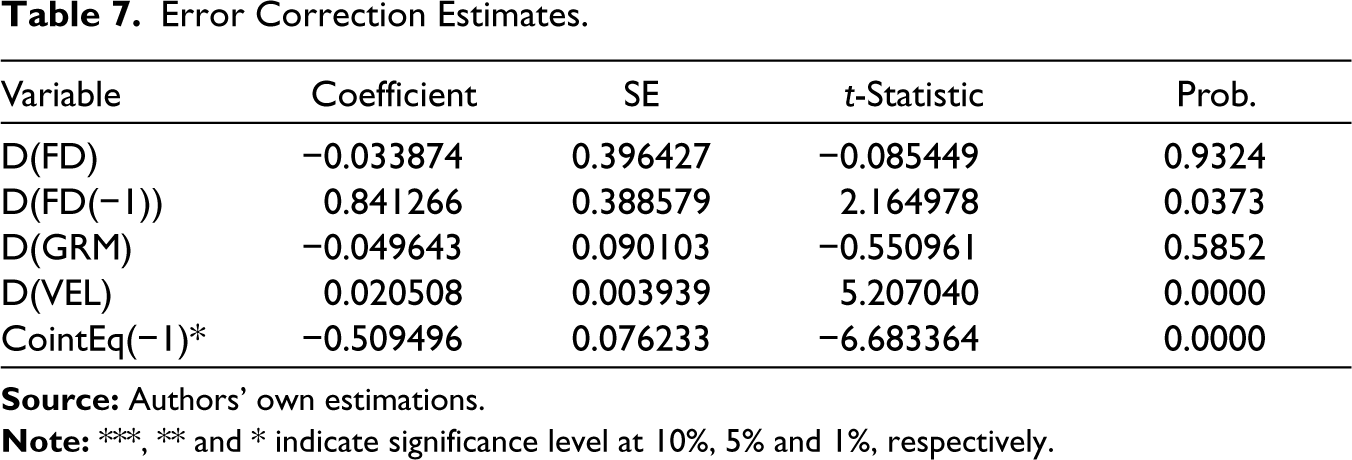

The study also estimates the error correction model to track the short-run adjustment mechanism towards the estimated long-run relationship (Table 7). The estimated coefficient value, that is, error correction term (ECTt−1) lies between ‘0’ and ‘−1’ at a 1% level of significance. Further, the estimated value shows that about 50% of short-run disequilibrium error adjusts towards the long-run relationship in a year. It implies that the adjustments are speedy towards the estimated long-run equilibrium.

Error Correction Estimates

The key outcome of ECM is the ECTt−1 term. The negative and significant estimate of the ECTt−1 coefficient is showing that there exists a short-run relationship as well. This means that whenever there is any shock that brings the linkage out of the long-run equilibrium, the model will adjust back, and the ECTt−1 term is the speed of adjustment from short-run disequilibrium towards the long-run equilibrium. The negative sign implies that disequilibrium will converge towards the long-run equilibrium. The magnitude −0.5094 in the first model implies that it will take approximately 2 years before converging back to the equilibrium path.

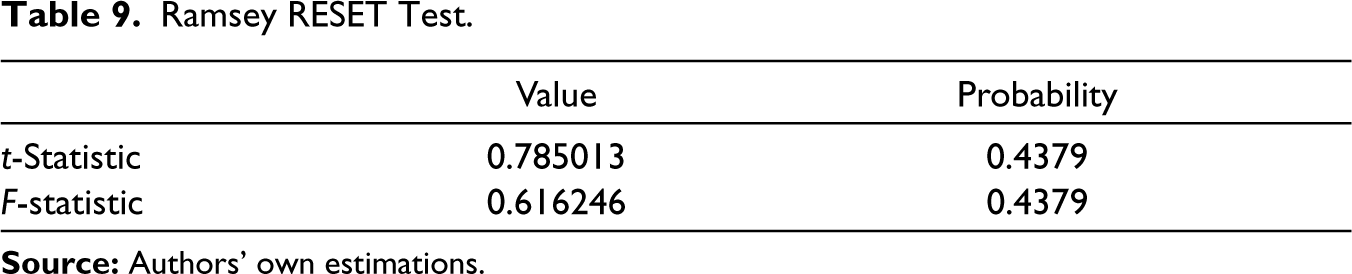

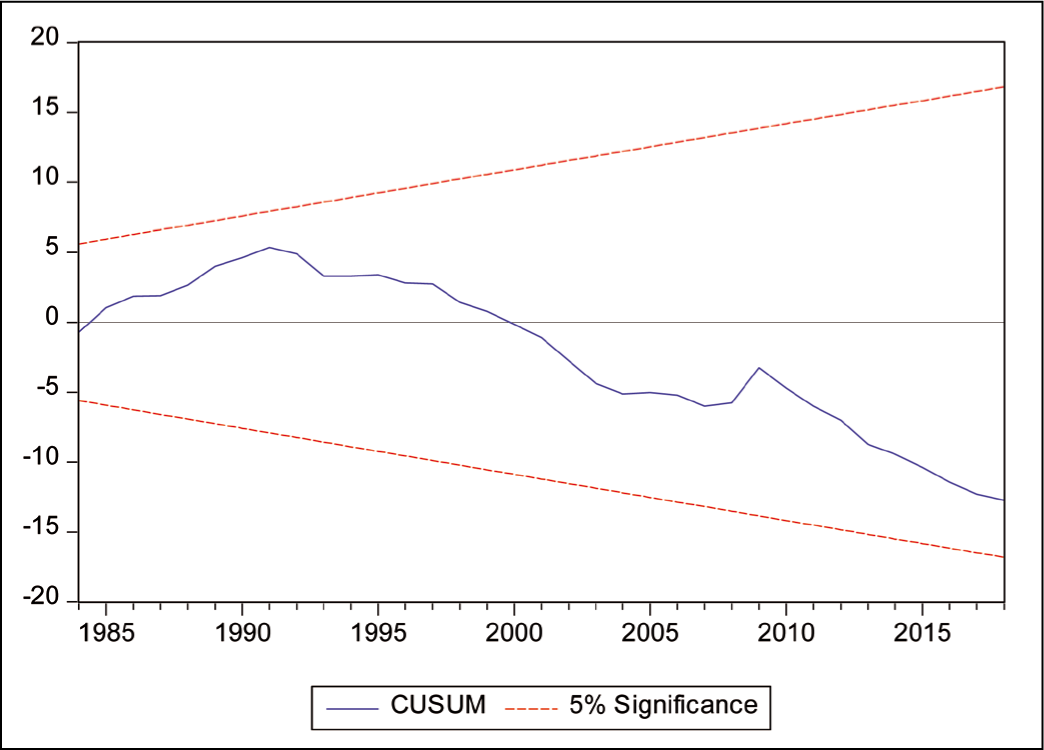

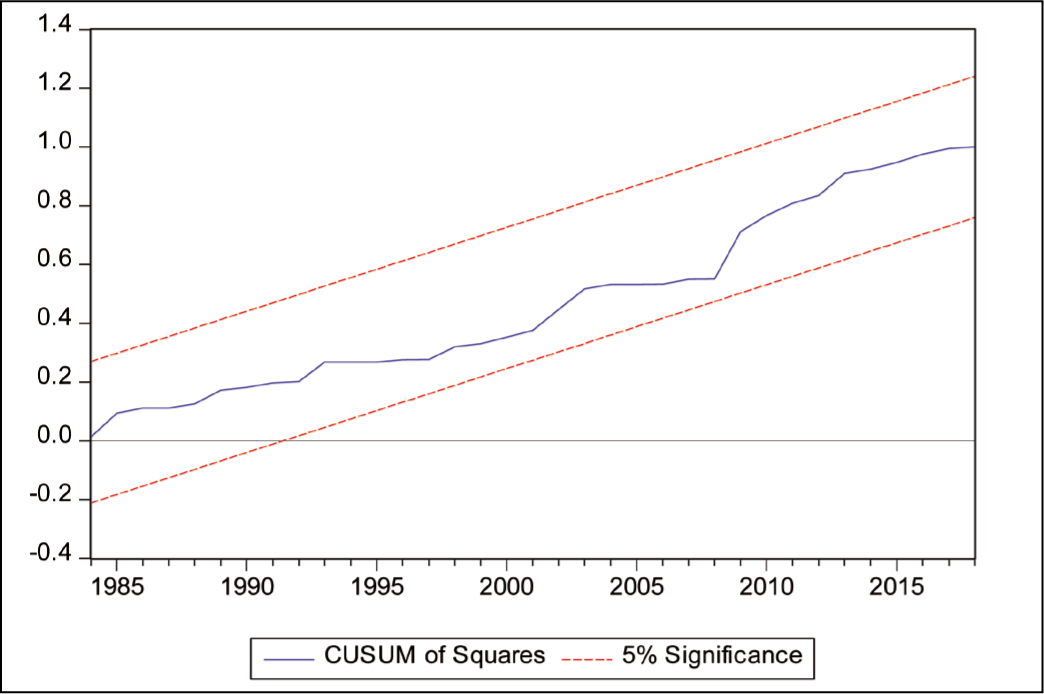

Estimated results reported in Tables 8 and 9 indicate that there is no evidence of heteroscedasticity and model misspecification in the estimated ARDL bound test model. The values of the CUSUM and CUSUMSQ, indicated in Figure 1 and Figure 2 respectively, also lie within the limit of a 5% level of significance, which indicates that coefficients of the estimated model are stable during the whole study period.

White Heteroscedasticity Test

Ramsey RESET Test

Granger Causality Analysis

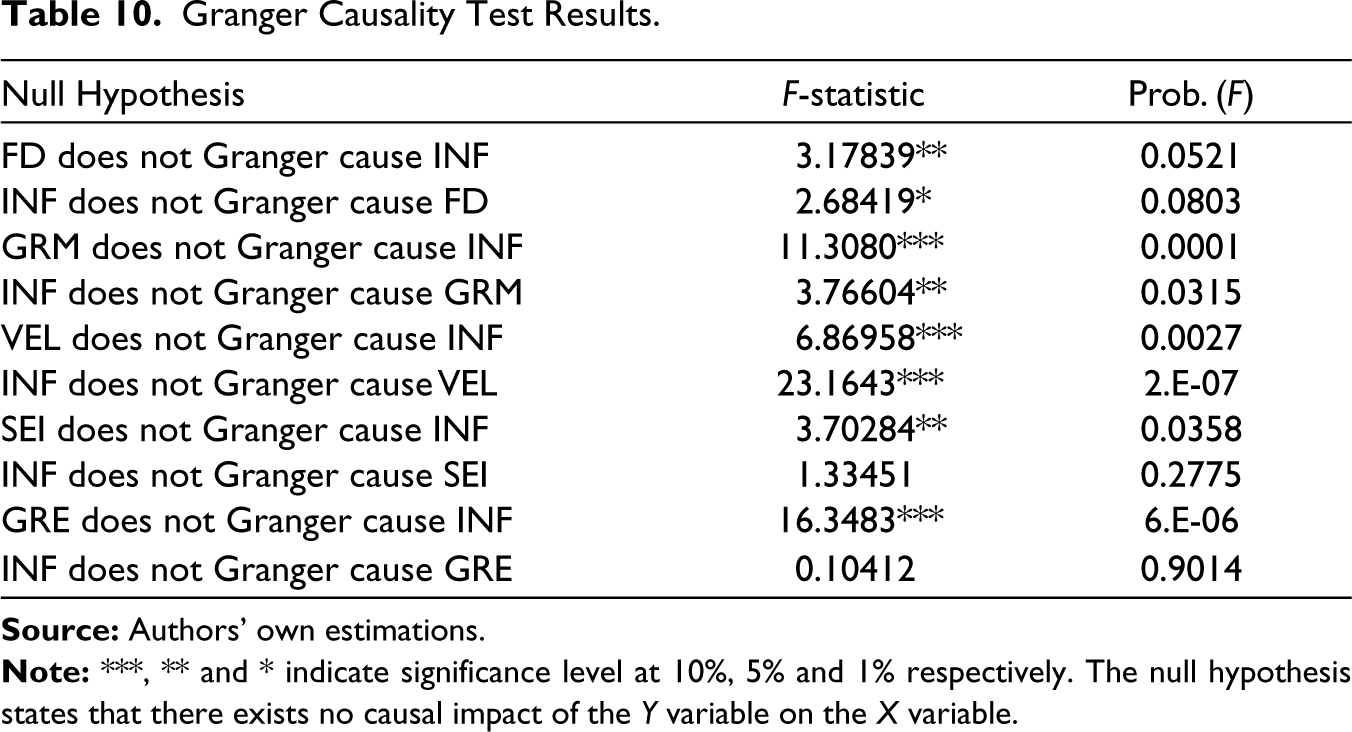

Moreover, the study also employed the Granger causality test to investigate the bidirectional causality between inflation and its determining variables. The estimated results shown in Table 10 state that there exists a bidirectional causality between fiscal deficit and inflation. It implies that fiscal deficit does cause inflation, and inflation also causes fiscal deficit to rise. It further confirms the fiscal dominance situation during the underlying period. Likewise, empirical results suggest that there exists bidirectional causality between inflation and the broad money velocity in the case of Pakistan. The estimated results found uni-directional causality between inflation and change in the broad money supply of Pakistan. Furthermore, the study finds support in favour of inflation and seigniorage through a uni-directional causality running from seigniorage towards inflation in the case of Pakistan.

The current study also found uni-directional causality from a NEER towards inflation in the case of Pakistan. It may be true because of the higher nominal exchange rate, the imported inflation would rise, and therefore, the general price level rises. Generally, our results are consistent with theoretical and empirical literature (Javid et al., 2011; Qayyum, 2006). The empirical results of the current study revealed that the monetary policy in Pakistan is presently functioning in an environment of persistent budget deficits and increasing public debt.

Granger Causality Test Results

Discussion

The empirical results show that budget deficits and money growth are the long-run economic determinants of inflation. Besides, empirical results also show that there exists a direct linkage between the inflation rate and money supply and between inflation rate and velocity of money. The study suggested on the basis of empirical results that the inflation remained due to the fiscal, monetary or short fiscally driven monetary phenomenon in the case of Pakistan. The positive linkage between Pakistan’s budget deficit and the level of inflation highlighted through the empirical results of the current study is in line with the proposition of FTPL, which suggests inflation to be a fiscal phenomenon (Leeper, 1991; Sims, 1994). The empirical finding of the current study that the fiscal deficit affects inflation positively in Pakistan has also been observed previously by Shabbir et al. (1994) who find positive significant results.

The outcome of one-to-one linkages among the money supply and the inflation rate is consistent and in line with the previous literature such as McCandless and Weber (1995), Rolnick and Weber (1994), and Lucas (1983). Furthermore, the results of the current study also verify the monetarist’s hypothesis that money supply is the primary and core factor that adds towards the increasing inflation in the economy of Pakistan.

The linkage between inflation rate and money velocity is referred to as GDP growth is directly linked to the inflation as money velocity is measured as the ratio between nominal GDP growth and money supply. Moreover, the role of financial sector reforms is traced and witnessed in the impact of money velocity.

Like many other developing countries, in Pakistan, monetary policy remains under the pressure of fiscal deficit and fiscal policy shocks that might play a key part in the determination of prices (Sims, 1994; Woodford, 1994). According to Qayyum (2006), the central bank in Pakistan, which is widely known as the State Bank of Pakistan, has the obvious authority of safeguarding the stability of price level and promoting economic growth. For the purpose of containing inflation rate within the desired level set by the government, the State Bank of Pakistan used money supply as an ultimate instrument. However, statistics related to money supply growth showed that actual money supply growth exceeded its target levels till the year 2005, mainly because of soft and easy monetary policy for supporting the growth process. Consequently, the expansionary monetary policy resulted in rapid inflation reaching double digits in 2005. In fact, the financial system is a closed mechanism in which funds flow from one agent, entity or institution to another. If surplus liquidity is infused beyond the level of nominal economic growth, a monetary overhang would be created, and inflation is unavoidable. Unless the excess money liquidity is absorbed, or its future growth is brought down, inflationary difficulties would ultimately persist and propagate. Javid et al. (2011) state that there was a widespread perception that there is no central bank in the country, and there is no monetary policy; however, in later years, the State Bank of Pakistan has squeezed the money supply as per the inflation targets and tried to improve its image.

The years from 2008 to 2013 were extremely difficult years for the economy of Pakistan. The foremost factor is the transformation of power from martial law regime to democratic regime. The democratic government took power in Pakistan at the time when Pakistan was facing severe terrorism activities, and power shortages created difficulties in production activities with industry performance declining. Inflation touched its second highest peak (i.e., 20%) in 2009, and interestingly, fiscal deficit also remained high around 6–7% of GDP during these years. Moreover, in 2010, the excessive monsoon rains caused major flooding and food supply shortages, deteriorating the economy of Pakistan. Similarly, the board money supply and seigniorage remained high on account of high fiscal deficit during 2002–2017 and 2011–2017, respectively, as there was no other option available to the government, and the US government also stopped providing coalition support fund to combat terrorism in Pakistan.

In 2018, the new elected government of Imran Khan took charge. Again, economy is at its worst stage as it is exhibiting a GDP growth of about 3.29% (Government of Pakistan, 2018). The main problem is the accelerating consumption patterns that increase inflation, besides burdening external and fiscal deficits. Since the macroeconomic conditions remain the same till date, the current Government in Pakistan clearly has an opportunity to introduce reforms in fiscal as well as monetary policies.

It is a conventionally known fact that controlling and regulating inflation are the primary goals of monetary policy authorities. The phenomenon of fiscal dominance highlights the interactions between fiscal and monetary policy. In a fiscal-dominant regime, monetary policy authorities accommodate government liabilities to finance budget balance (deficit). In such a situation, monetary authorities of the country put a lot of effort to raise upcoming seigniorage revenues for the financing of principal loans and interest payments of loans. Hence, central banks do compromise on their primary objective of controlling inflation in such economies.

The primary objective of the current study is to test and examine the presence/validity of the fiscal dominance hypothesis or otherwise in the economy of Pakistan. To estimate the long-run relationship among the variables, the study used the ARDL model using the time series data set for the period 1971–2020. Estimated results show that there exists a long-run relationship among the variables. It implies that there exists a long-run equilibrium relationship among inflation, fiscal deficit, broad money supply, broad money velocity, seigniorage and NEER. Furthermore, the estimated coefficient value of ECTt−1 and its significance confirm the disequilibrium adjustment towards the long-run equilibrium. The empirical results show that budget deficits and money growth are the long-run economic determinants of inflation. So inflation has remained the fiscal, monetary or fiscally driven monetary phenomenon in the case of Pakistan.

It is revealed that the government borrowings from the central bank to finance the budget deficit in Pakistan would not allow the central bank to control inflation in the future as well. A rise in the money supply as a result of a persistent budgetary deficit would lead to a real depreciation of Pakistani rupee, which will ultimately result in a further rise in inflation rate. In this scenario, fiscal policy becomes the actual culprit behind the inflation, as well as an appropriate channel for controlling inflation instead of the monetary policy in Pakistan. It also implies and it is matter of fact in Pakistan that monetary authorities are unable to enjoy the monetary independence as they keep focused on economic growth targets and defend the increase in inflation as the cost of high economic growth during the said years. The current study recommends that the government should carefully structure the fiscal expenditures and financing arrangements as it is directly linked with the monetary expansion and creates inflationary pressures in the economy.

From a policy perspective, restraining and controlling the fiscal deficit are the primary measures in attaining and retaining price stability in the long run in the case of Pakistan. Chandia et al. (2019) suggest the need for coordination between fiscal policy and monetary policy so that the primary budget balance could be reduced in Pakistan, which creates inflationary pressure in economy. Moreover, it is also worthy to mention and seek guidance from the recommendations suggested by the study of Chandia et al. (2022). The work of Chandia et al. (2022) has recommended the need for extensive fiscal policy reforms for the control of budget deficits. There is a need to establish and implement a strict, sound and regular fiscal adjustment programme, with the coordinated efforts of all stakeholders such as the Ministry of Finance, Federal Board of Revenue (FBR) and the State Bank of Pakistan. Although a number of steps have already been taken by the current government such as zero budgetary borrowing, increase in energy tariffs, imposition of regulatory duties, withdrawal of some tax relaxations in the previous budget, a widespread tax reform ranging from expansion of the tax base and designing an inflation-proof tax system to the improvements in tax administration, collection and streamlining of government expenditures are essential in instituting the credibility and reliability of the fiscal policy in Pakistan. Fiscal integrity and trustworthiness should also be maintained through enhancing the independence of the central bank as proposed in recent amendments in SBP Act, with a vibrant mandate of maintaining the stability of price level as the key purpose of monetary policy.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.