Abstract

Small producers’ participation in milk collectives such as dairy cooperatives and producer companies is seen as one of the several ways to institutionalize the dairy value chains and leverage their production and marketing strengths. In this context, the study has explored procurement practices of a dairy cooperative vis-à-vis producer company that have recently ventured into direct procurement, processing and retailing of the milk in Indian Punjab and understood their economic impact on the milk producers in Indian Punjab. The findings of the study suggest that both the milk collectives offer higher prices to the producers, resulting in higher profitability than their counterpart non-member milk producers. The findings of the study suggest that the milk collectives need to take additional responsibilities in terms of advancing credit, introducing new production technologies to increase milk productivity and encouraging participation of women milk producers to make such linkages inclusive, effective and sustainable.

Introduction

Agriculture and allied sectors continue to drive livelihoods for about 55% of India’s workforce even though the agrarian economy witnesses a farming crisis of varying degrees across different parts of India (Government of India [GoI], 2019; Kaur & Kaur, 2016; Mishra, 2008). The share of agriculture and allied sectors in gross value added (GVA) has declined to about 17% in 2018–2019 on account of dismal growth in the last decade and so. The livestock sector, which has emerged as one of the most important sub-sectors of agricultural and allied activities, comprises a share of 28% in GVA in agriculture and its allied sectors and 5% in India’s GVA and employs 8.8% of the population (GoI, 2019; Yasmeen et al., 2019). Among all the sub-sectors of the livestock sector, the milk sector alone accounts for a contribution of around 66% in the value of output (GoI, 2020). The agricultural production system in India is quite diverse, mixed and deeply interwoven with livestock rearing and farming, which helps to complement farming income, provide employment, particularly to women, draught power for agricultural operations, fuel for cooking food, manure for maintaining the soil fertility etc. (Kaur & Singla, 2018a; Pawar, 2017; Singh et al., 2007, 2014; Venkatesh & Sangeetha, 2011). The regular flow of income from dairying plays a very crucial role to make whole farm income sustainable and helps to reduce the extent of indebtedness among the farmers (Singh et al., 2008).

After the initiation of the green revolution in India from the mid-1960s onwards, another institutional set-up that transformed the entire rural landscape was the operation flood programme that took place from 1970 to 1996 in three phases with financial support from the World Bank. A peculiar feature of the operation flood programme was development of the dairy sector through the establishment of three-tier producer-driven dairy cooperative societies (DCSs) at village level, milk union at district level and a federation of milk unions at state level across different parts of India, which has helped to increase milk production, augment rural income and provide milk at a reasonable price to the consumers (Birthal et al., 2019; Christie, 2020; Rajendran & Mohanty, 2004). The dairy cooperatives in India have extensive coverage in about 1.94 lakh villages with a membership of 17.22 million milk producers (National Dairy Development Board [NDDB], 2019–2020). Until 1991, the government supported the dairy cooperatives and protected them from internal and external competition. Since 1991, the dairy sector of India was gradually deregulated to induce private investments. However, a major shift of government policy was observed in 2002–2003 with the removal of zonal restrictions for procurement of milk, which allowed private processors to source milk from outside their designated milkshed areas. The government also allowed foreign investors to invest in the dairy sector in the early 2000s. As a result, the number of private milk processing plants rose from 403 in 2002 to 493 in 2006 (Birthal et al., 2017a, 2019; Sharma et al., 2009). Since the post-1991 liberal era, various problems in functioning and performance of traditional cooperatives had also started to appear while competing against multinational giants. Therefore, the Companies Act, 1956, was amended in 2003 to make cooperatives more robust in their structure and functioning, which paved the way for the creation of new generation cooperatives that were referred to as producer companies. Currently, there are around 7,374 registered producer companies in India, out of which, 15 are NDDB Dairy Services (a wholly owned subsidiary of NDDB) supported milk producer companies that have enrolled about 6.2 lakh milk producers (NDDB, 2019–2020; Neti et al., 2019).

India, with milk production of 187.7 million tonnes, is the largest milk producer in the world, accounting for about 22% of the global milk production (NDDB, 2019–2020). Along with that, it is also the world’s largest consumer of milk. Due to rapid urbanization, increase in literacy rate, globalization, upliftment in standard of living, diet consciousness etc., the consumers have shifted their food pattern away from staple food grains to a diversified basket of several nutritious food items such as milk, meat, fruits and vegetables, fibre-rich diets etc. (Birthal & Taneja, 2006; Birthal, 2008; Das et al., 2011). Further, an increase in consumer interest in high protein diets and a rise in awareness and availability through organized retail chains have driven growth of milk and milk products (GoI, 2018). Between 1982 and 2011, the share of food expenditure on milk and milk products has increased from 15.7% to about 20% in urban areas (GoI, Various Reports). Being a smallholders’ enterprise, the rapid increase in demand for milk may also lead to an increase in milk production. But, the further expansion of milk production depends upon the profits that accrue to the milk producers (Ghule et al., 2012). Milk being the most perishable commodity requires immediate disposal after milking the milch animals. However, the milk is largely handled through the unorganized sector in India, which is largely dominated by private milk traders/vendors/milkmen, who buy milk directly from the producers and supply milk either directly to the urban consumers, or to informal institutional buyers (restaurants, tea stalls etc.) or wholesalers and local retailers such as halwai shops/creameries/city-based private dairy shops etc. (Kumar et al., 2011; Singla, 2021). About 60% of the marketable surplus of the milk is largely marketed through the unorganized sector, while the organized sector comprising of dairy cooperatives, producer companies and private dairies handles about 40% of the milk. Under the National Action Plan for Dairy Development, the government has set an ambitious target to increase milk handling through the organized sector to 65% by 2023–2024 (GoI, 2018). Hence, milk collectives such as milk cooperatives and producer companies are viewed as institutional mechanisms that strive to maximize socio-economic relevance in their domain rather than profits alone to improve member’s livelihoods (member centrality). Milk collectives’ share in their business also plays an important role for sectoral economies (patronage centrality) and embeds in local communities for overall regional development (domain centrality) (Shah, 1995, 2016; Singh, 2021a). Thus, the collectives can also help to introduce global competitiveness for small producers (Singh, 2019).

Context and Rationale

Punjab state of India is still considered as agriculturally leading state as it contributes about 21% of rice and 38% of wheat to the central pool and produces about 7% of India’s milk (GoP, 2020–2021; NDDB, 2018–2019). The livestock sector has emerged to play an important role in Punjab’s agrarian economy as it accounts for a share of about 37% of the agricultural GVA of Punjab. During 2018–2019, among all the sub-sectors of agriculture and allied activities, the growth rate of livestock sector was the highest at 5.4% against -0.4% in crop sector during the period of 2012–2013 to 2018–2019 (GoP, 2020–2021). The state ranks first in per capita availability of milk with 1,181 g/day as against 394 g/day at national average (NDDB, n.d.). Milk yield in Punjab is also higher than the national average due to favourable agro-climatic conditions, high availability of animal feed and fodder, reasonably well-developed animal healthcare and breeding facilities and better access to the markets (Birthal et al., 2017b; Vandeplas et al., 2013). The structure of milk production and marketing is also entirely different from that exists at India level. The contribution of landless, marginal and small landholders in milk marketed is only 33% in Punjab as against 69% at India level. This depicts commercialization of dairying in Punjab (Birthal, 2008; Kumar et al., 2011). However, small milk producers in Punjab continue to sell raw milk to neighbouring households or informal traders/buyers comprising milk vendors, small retailers and processors, local dairies, restaurants, tea stalls etc. (Birthal et al., 2017b; Vandeplas et al., 2013). Small milk producers face several problems in production and marketing of milk in Punjab such as low marketable surplus, lack of access to quality inputs such as feed and fodder, low price realization for milk in the informal milk markets, delay in payments, lack of access to extension and veterinary services, lack of credit facilities for technological upgradation etc. (Birthal et al., 2017b; Kashish et al., 2014; Sharma, 2015).

The dairy sector of Punjab has witnessed major structural transformation with the set-up of Punjab State Cooperative Milk Producers’ Federation Limited in 1973 as an apex body of cooperatives, which slowly established a wide network of about 8,018 village-level milk cooperatives with about 4.10 lakh milk producers as its members, associated with 11 district-level milk unions and 10 milk processing plants. These cooperatives procure around 17.66 lakh litres of milk per day against a consolidated milk handling capacity of around 21.85 lakh litres per day (NDDB, 2018–2019a). Since 1961, Nestle India Limited, one of the first private players in the organized dairy industry, has also been active in milk procurement and processing in Punjab. It procured approximately 1.3 million litres of milk per day from approximately 1.10 lakh farmers through a network of 1,916 milk collection centres (Punjabi, 2015; Sekhon & Kathuria, 2019; Vandeplas et al., 2013). The dairy industry in Punjab was also significantly impacted by the reforms. The private sector’s milk processing capacity, which had been practically on par with cooperatives until 2002–2003, grew quickly to overtake cooperatives by 70% in 2012–2013. Even though the private sector had a considerable presence in Punjab before 1991, it grew even quicker after the reforms. While the cooperative sector grew slightly, if at all, between 2002 and 2013, the private sector’s processing capacity nearly doubled (Birthal et al., 2017b). Recently, Punjab’s dairy sector has received a further boost with the operationalization of Baani Milk Producer Company Ltd. as a producer company under the aegis of NDDB Dairy Services (NDS), a wholly owned subsidiary of NDDB. It has enrolled 54,715 milk producers from 1,268 villages in 9 districts of Punjab, with around 27% of them being women and 39% being small milk producers (NDDB, 2019–2020). Thus, Punjab’s dairy sector has undergone tremendous structural transformations in terms of milk production, procurement, processing and retailing of milk with the presence of cooperatives, MNCs, producer companies and other private dairies. It is argued that small and landless milk producers’ participation in new milk collectives will not only provide an alternative assured milk market, and assured and remunerative prices to dispose of their milk, but also help them to gain technical know-how for increasing milk productivity, get access to veterinary services at their doorsteps, avail quality dairy inputs for production, maintain hygiene and quality of milk, get access to credit facilities, etc. In this context, it becomes imperative to explore the performance and inclusiveness of milk collectives, mainly milk cooperatives and producer companies and improve functioning of such collectives to make such linkages effective and sustainable.

Review of Literature

There exist several studies in Indian and global context that had revealed the restructuring in milk markets with the emergence of new forms of markets such as milk collectives/farmer producer organizations, MNCs, food supermarkets, local private players etc. and their linkage building with the small milk producers (Birthal et al., 2017a; Kumar et al., 2011; Reardon & Berdegué, 2002; Vandeplas et al., 2013). In Brazil, Chile and Argentina, the large milk processors introduced private standards of milk quality, which led to the process of concentrating dairy farms. This pushed small milk producers to less-profitable and less-regulated informal markets (Reardon & Berdegué, 2002). On the other hand, cooperatives in Ethiopia were able to introduce technological transformations and commercialization, but were poor in offering better prices (Chagwiza et al., 2016). However, with the emergence of milk producers’ organizations in Czech Republic, the positive economic benefits in terms of negotiating a fair price, securing sales and access to relevant information started to accrue to the milk producers (Boskova et al., 2020). In Zambia, the producers selling milk through modern dairy channels also witnessed a positive impact on their income (Neven et al., 2017). In India, evidence on milk producers participation in dairy cooperatives revealed that monthly income was higher in the case of member producers of dairy cooperatives than non-members in Bihar (Kumar & Sharma, 1999; Kumari & Malhotra, 2016) and Rajasthan (Meena et al., 2009, 2010; Seema et al., 2013; Singh & Sharma, 2006). The women’s dairy cooperatives in Bihar were found to be instrumental in income and employment enhancement among women milk producers (Kumari & Malhotra, 2016). In Indian Punjab, milk producers supplying milk to cooperatives and MNCs were found to more efficient and earned higher profits as compared to the producers, who sold in informal channels (Kaur & Singla, 2018b; Vandeplas et al., 2013). Another study in Indian Punjab also revealed that cooperative supplying milk producers earned significantly higher profits than non-cooperative producers due to the cheaper inputs supplied by the cooperatives that included feed and veterinary services (Gupta & Roy, 2012). These results were also found to be similar to the study by Birthal et al. (2005), which revealed that profitability was double in the case of dairy farmers in contract with Nestle India than the non-contract farmers as costs of production and transaction were reduced drastically. Similarly, Birthal and Joshi (2009) showed that producing and selling milk through formal marketing channels such as contract channel in Punjab was a more efficient form of production as it reduced the marketing and transaction costs of the producers to a significant extent. Yet another study by Birthal et al. (2017a) pointed out that resource-rich large dairy producers in Punjab were able to partner with private dairy processors that included multinationals, while small dairy farmers continued to remain dependent on informal channels for sale of their milk. These studies showed that there exists enough literature on milk producers’ participation in formal channels such as cooperatives and MNCs in the case of India in general and Punjab in particular.

However, the literature in the context of dairy-based producer organizations/companies was relatively scanty in the context of India and did not address the milk producer and producer organization/company interface adequately. One such study by Thakur et al. (2021) revealed that milk producer organizations in Himachal Pradesh provided input services at lower rates, veterinary services, dairy extension and credit facilities to the producers and procured milk from the producers at higher prices than the prevailing prices in the locality. These producer organizations were also engaged in community mobilization through the self-help groups. In Kerala, the milk producers were found to be attached with the producer company due to better price realization, availability of inputs at a reasonable rate and receiving benefits from the government schemes (Jose et al., 2019). A study by Mukherjee et al. (2020) in the Bundelkhand region of Madhya Pradesh, India, observed that joining farmers’ producer companies helped the milk producers to enhance their annual income from milk, higher social participation with progressive dairy farmers, extension agencies and urban contacts significantly. In Haryana, Kumar et al. (2021) found that the producers, who were associated with the milk producer organization received ₹8–10 per litre higher price for milk as compared to the non-members. Besides, the member producers who were shareholders in the company received bonuses, which led to an increase in their income by 25%–30%. Singh (2021b), while attempting to understand impact and performance of producer companies in India, observed that milk producer members of Payaas, a producer company in Rajasthan were either marginal or landless livestock rearers. The producer company was able to make a good impact on the livelihood of the producers in terms of input supplies and ration balancing, which led to an increase in average milk yield, fat and a reduction in the cost of feeding. However, most of these studies did not extensively explore the milk producer’s interface with the producer organizations/companies in terms of the socio-economic profile of the producers, detailed cost-benefit analysis in terms of cost of production, milk yield, price realization for milk for members and non-members, etc. and strengthening the linkages from a policy perspective for overall dairy development. Moreover, we also did not come across any such study, which has examined and compared the functioning of dairy cooperatives with new forms of collectives such as producer companies and their comparative performance and economic impact on milk producers in India.

Database and Methodology

The study is entirely based on a primary field survey carried out from October 2017 to March 2018 on milk producers supplying milk to two milk collectives, which have recently started milk procurement and processing directly from the milk producers along with their comparison with milk producers selling/supplying milk in informal milk markets. The two milk collectives identified were a dairy cooperative and producer company. First, Kaira Milk Union Ltd., a tier of Gujarat Cooperative Milk Marketing Federation (GCMMF), was identified as a dairy cooperative, while Baani Milk Producer Company Limited (BMPCL) was identified as a producer company, which had entered into milk procurement and processing at the same time in Punjab in 2014. The Gurdaspur was selected for GCMMF and Bathinda for BMPCL, as these two districts of Punjab accounted for the highest milk procurement from the producers for the respective milk collectives. The villages in the selected district were identified and selected based on the highest milk procurement with the help of the data provided by the officials of the milk collectives. A complete list of the milk producers in the selected villages of each district was obtained from the officials of village milk collection centres of both the milk collectives. Thus, 100 milk producers supplying milk to each milk collective were selected using a simple random sampling technique. Another sample of 100 milk producers was also selected for each district, who were in the vicinity of the milk producers associated with milk collectives and did not supply milk to milk collectives but sold milk in informal milk markets. Both types of milk producers were interviewed using the personal interview method through a semi-structured schedule. Since dairying was a joint venture of family members and women in the household were found to be engaged in most of the milk production and supervising activities, the interviewees were mostly women. The data collected from milk producers supplying milk to milk collectives were compared and analysed with the data collected from milk producers selling to informal milk markets using simple statistical techniques such as averages and percentages only. Garrett’s ranking technique was also used to rank the major benefits reported by the milk producers in linking with the collectives using the following formula given by Garrett and Woodworth (1979):

where Rij is the rank given for the ith constraint by the jth respondent. Nj is the number of constraints ranked by the jth respondent.

Then, for each constraint, the scores of each respondent were added, and the total value of scores and mean values of the score were calculated. The constraint having the highest mean value was considered to be the most prevalent constraint.

Procurement and Supply Chain of Milk Cooperative and Producer Company

Gujarat Cooperative Milk Marketing Federation

Before the formation of the GCMMF, the Kaira District Cooperative Milk Producers’ Union Limited (KDCMPUL) was established in 1946 to combat the private Polson Dairy’s exploitative practices. Farmers went on strike, and as a result, it was decided not to sell a drop of milk to the Polson Dairy. After a 15-day strike, the milk commissioner of Bombay (an Englishman) and his deputy visited Anand, assessed the situation and agreed to the farmers’ demands. As a result, the KDCMPUL was formed in Anand and registered on 1 December 1946. GCMMF had 18 district milk unions (DMUs). The Amul model, also known as the Anand pattern, had a three-tiered structure. DCSs at the village level were affiliated with milk unions at the district level, and these unions were further federated into a state-level milk federation (GCMMF).

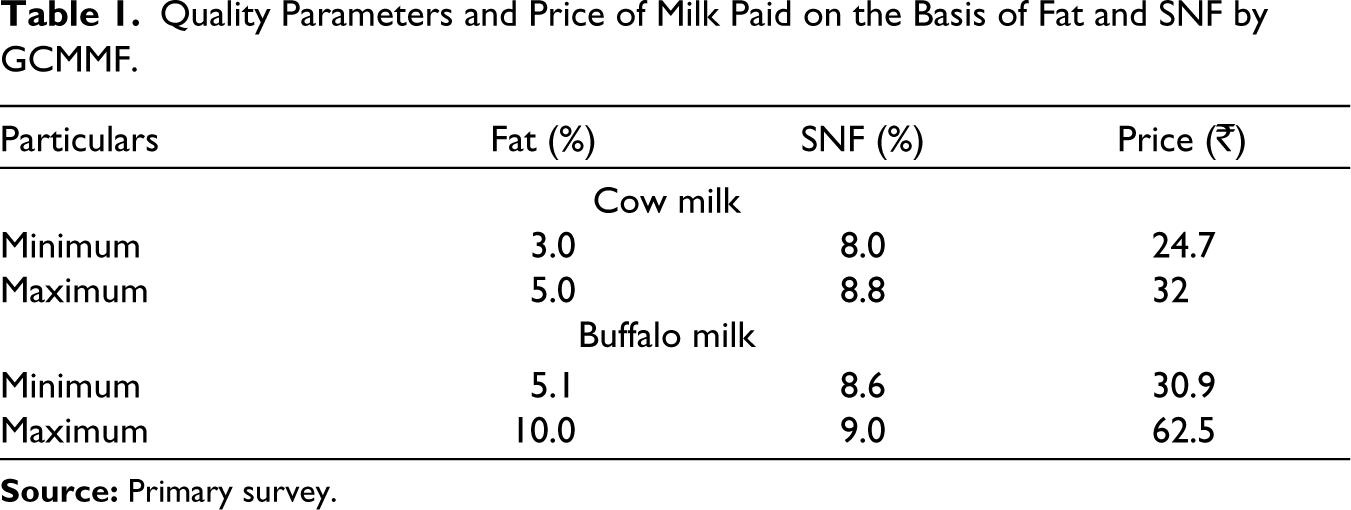

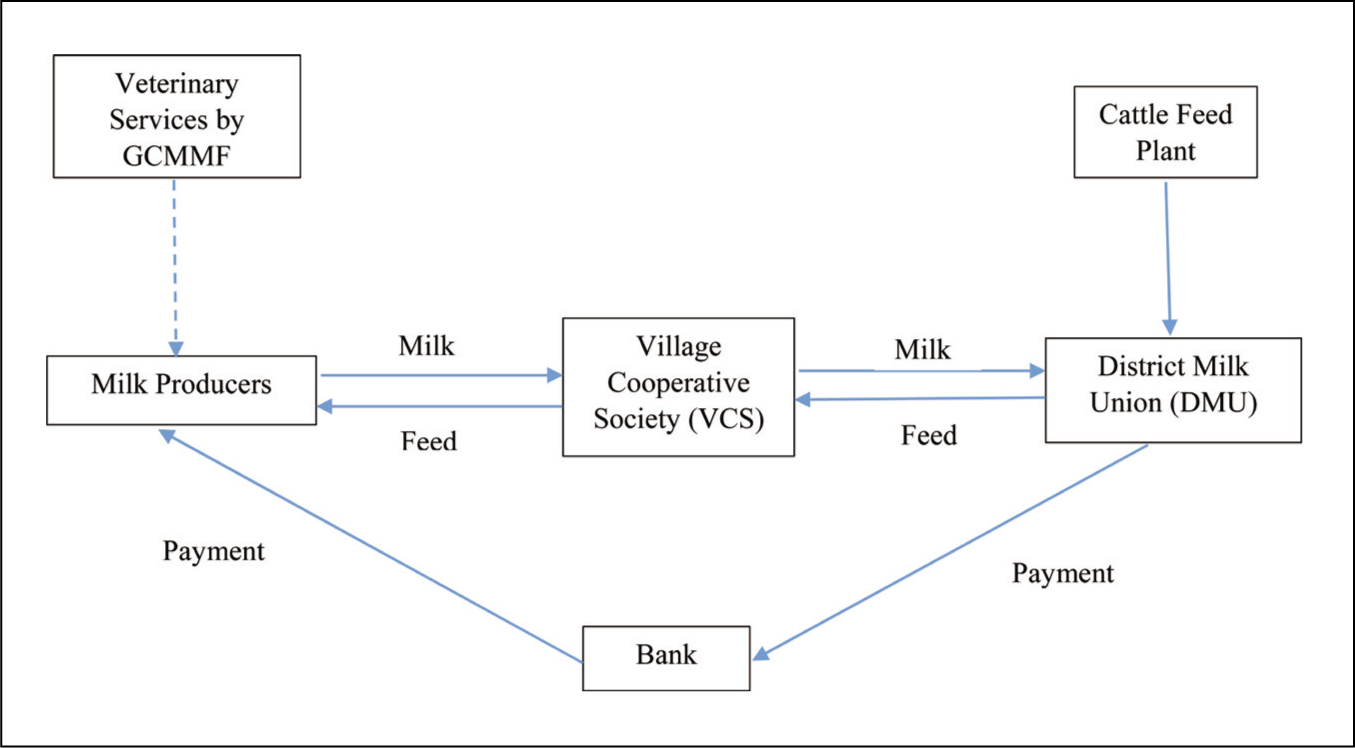

GCMMF started its operations in Punjab in November 2014 with milk processing at a leased plant in Batala of Gurdaspur district. Within two years of its inception, it had expanded its procurement operations to Amritsar and Tarn Taran districts. The milk was processed into packed milk, buttermilk and curd. In October 2016, GCMMF established another plant in Khamano in Fatehgarh Sahib to further expand operations in Punjab. GCMMF had set the quality norms for the procurement of milk. The price of milk to be paid to the milk consumers was determined by fat and soild not fat (SNF) (Table 1). The payment was made after every three days, which was credited into the farmers’ bank saving accounts. GCMMF had tied up with a leading private bank and a public bank to make payments to the farmers. A receipt of payment was made and given to each milk producer. The bank coordinated operations regarding the amount to be paid to milk producers. Unlike informal markets, price of milk paid to the milk producers did not fluctuate seasonally. GCMMF in Punjab worked with about 50,000 farmers with average daily milk procurement of around 3 lakh litre (Table 2). GCMMF had imported a milk analyser, namely, Milkoscreen from Denmark, which was used at each Village Cooperative Society (VCS) to determine content of fat, SNF and adulteration in the milk. The values were immediately displayed on the screen so that the milk producers could view and match the readings with payment slips. Apart from this, the Automatic Milk Collection Unit was also equipped at each VCS to bring transparency in the weighing of milk. Using milk collection software and rate chart for a given day, a printed slip was generated for payment, which had information such as total amount, milk sold, date and time. More than 95% of the bank accounts were opened in the name of women members as GCMMF considered them as the backbone of dairy farming and their participation in animal rearing create women empowerment among its member producers. It also provided veterinary services to milk producers through Amul Research and Development Association (ARDA). The ARDA consisted of a team of veterinarians and para-veterinarians and trained livestock agents, who assisted the milk producers by providing animal health care facilities. After procurement of milk at VCS, it was transported to DMU for processing and production of milk products. The DMU directly made payments to farmers in their bank accounts by taking the record from VCSs. The cattle feed plant provided various types of cattle feed to DMU that distributed it to milk suppliers through VCSs (Figure 1).

Quality Parameters and Price of Milk Paid on the Basis of Fat and SNF by GCMMF

Quality Parameters and Price of Milk Paid on the Basis of Fat and SNF by GCMMF

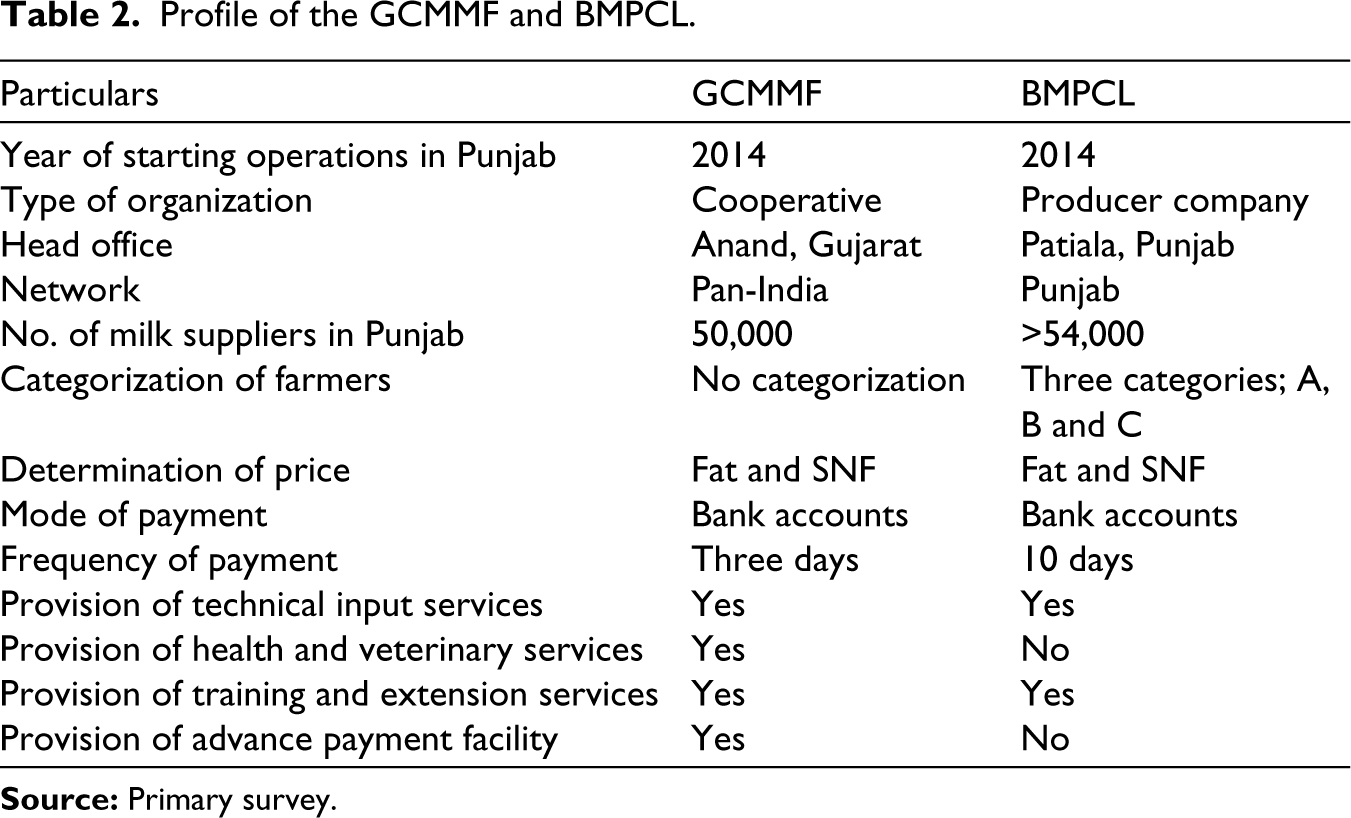

Profile of the GCMMF and BMPCL

Baani Milk Producer Company Limited

BMPCL was incorporated on 11 August 2014 with its head office in Patiala, Punjab, under subsection 2 of section 7 of the Companies Act, 2013 (Table 2). It came into operation with effect from 6 November 2014 as an independent organization to develop the dairy industry for improving the livelihoods of marginal farmers and empowering women milk producers in Punjab. For this purpose, it had registered 54,715 milk producers, of whom about 27% were women and 39% smallholder milk producers. It procured milk from nine districts of Punjab with daily procurement of 2.77 lakh litres of milk from about 1,268 villages through 1,352 milk pooling points (MPPs). For selling milk to BMPCL, a farmer had to become its member by applying through a membership form. The membership fee was ₹200 for males and ₹150 for females. Therefore, only member producers were eligible to sell milk to BMPCL. For membership, a milk producer must have a unique identification card and a bank account so that payment could be directly transferred to their bank accounts. The company also shared the details of the milk pouring to the milk producers through SMS via GPRS enabled Data Processor Milk Collection Unit installed at each village MPP. After the due approval of the members of the board of the company, a 16-digit unique code was issued to member producers, and the date of approval was considered as the beginning date of membership. For continuing membership, it was required for the member producers to supply milk at least for 200 days with a minimum quantity of 500 litres per annum. Besides, the lean-to-flush ratio of milk supplied to the company must be 1:3. The lean months were considered from June to September, while the flush months were from December to March. The remaining four months of April and May and October and November were identified as normal months. Milk was procured twice a day, and it was collected from a particular location in a village. The payment was made after every 10 days in the bank accounts of milk producers.

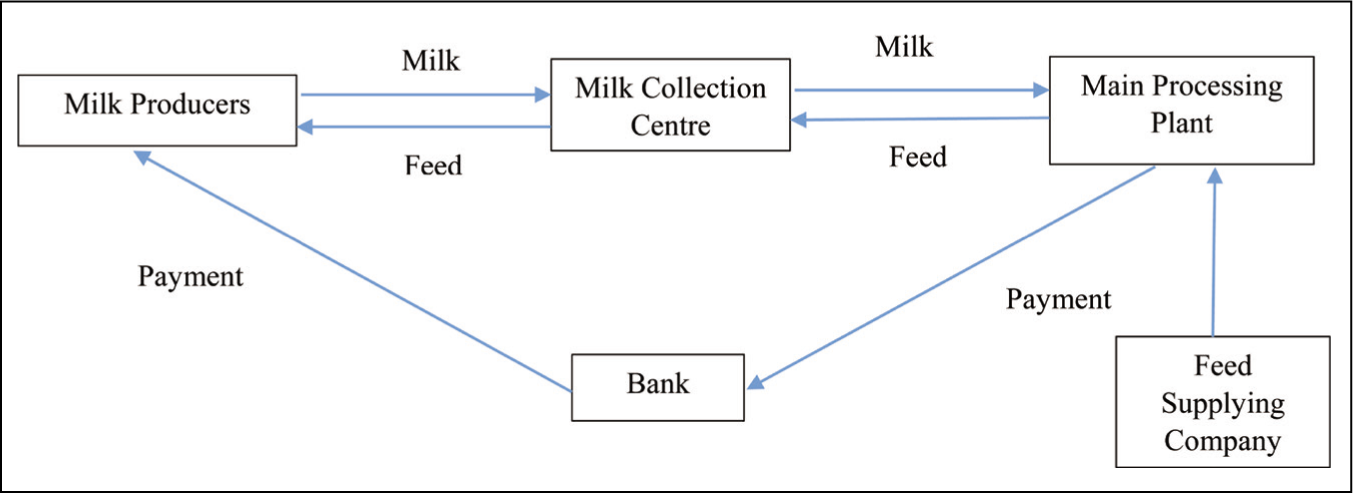

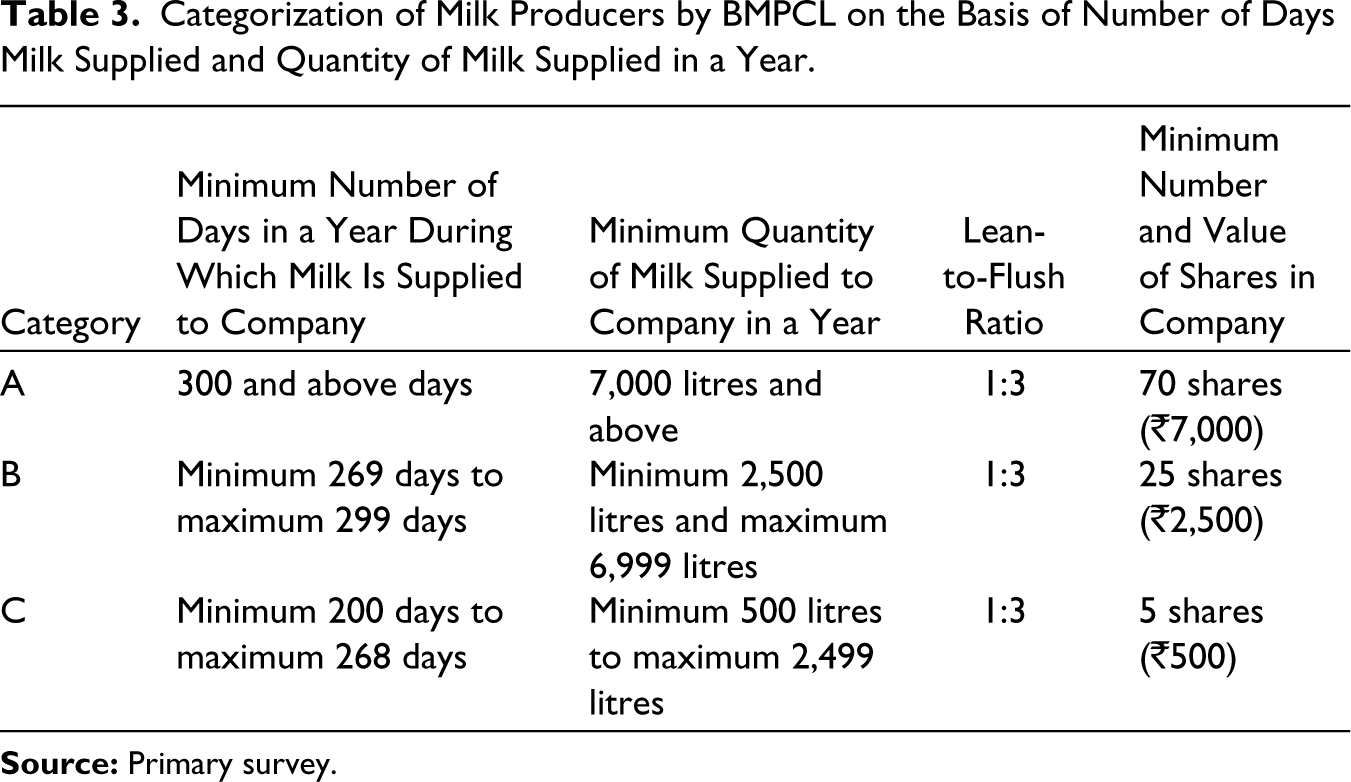

The company had also tied up with a third party namely, Kansal Feed Industries Pvt. Ltd., Khanna for manufacturing and supply of all types of feeds to the milk producers (Figure 2). However, it was not compulsory for the member producers to purchase the inputs from the company. They could also purchase feed and other inputs from the local market. The payment for these inputs was not paid in cash by the milk producers, rather it was deducted while making payments to the milk producers. The company also launched three types of training and extension programmes to aware the member producers regarding better milk production practices through the involvement of NGOs. Each programme was organized once a year in each village. These three types of programmes were related to clean milk production, women awareness and producer awareness. The company did not start to provide any kind of veterinary and credit facilities to the milk producers yet. Figure 2 indicates that milk producers supplied milk to a milk collection centre that transported it to the main processing plant for the production of milk products. This main plant directly made payments to the milk producers in their bank accounts. Further, Kansal Feed Industries Pvt. Ltd. provided cattle feed to the main plant that distributed it to milk suppliers through milk collection centres. The company had identified its member producers in three categories, viz. A, B and C, based on the quantity of milk supplied to the company, the number of days during which milk was supplied to the company and the number of shares in the company. For A category milk producers, it was mandatory for the producers to supply at least 7,000 litres of milk per annum on at least 300 days a year. They had to purchase at least 70 shares of the company. Similarly, for B category milk producers, it was mandatory for the milk producers to supply at least 2,500 litres of milk to a maximum of 6,999 litres of milk per annum on at least 269–299 days a year. Milk producers had to purchase at least 25 shares of the company. For C category milk producers, it was mandatory for the milk producers to supply a minimum of 500 litres of milk to a maximum of 2,499 litres of milk per annum on at least 200–268 days a year. Milk producers had to purchase at least five shares of the company (Table 3).

Categorization of Milk Producers by BMPCL on the Basis of Number of Days Milk Supplied and Quantity of Milk Supplied in a Year

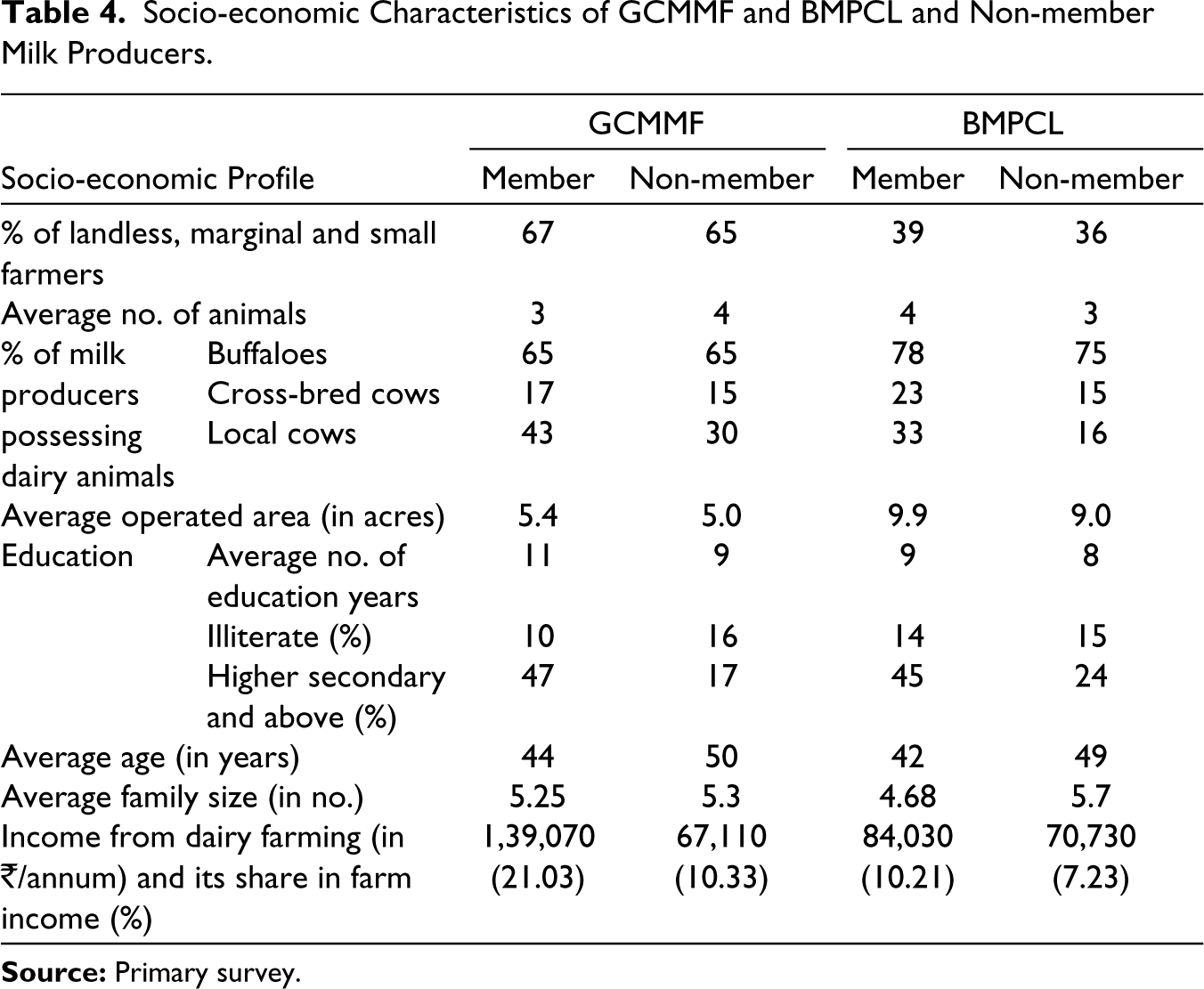

A brief socio-economic background of the milk producers supplying milk to GCMMF and BMPCL and their counterparts (non-member milk producers), who sold milk to local informal/unorganized markets is presented in Table 4. It is evident that proportion of the landless, marginal and small milk producers in milk procurement regions of GCMMF remained very high as compared to that in the case of BMPCL. As a result, the average size of operational land holding among milk producers was also smaller in milk procurement regions of GCMMF as compared to that in the area of operation of BMPCL. The proportion of milk producers, who possessed dairy animals, was turned out to be higher in the case of milk producers of both GCMMF and BMPCL than their counterpart non-member milk producers, though average ownership of dairy animals remained similar across both GCMMF and BMPCL milk producers and their corresponding non-member milk producers. A perusal of Table 4 also shows that heads of the milk producer households of both GCMMF and BMPCL were better educated, younger in age, and had a smaller family size than non-member milk producers. Further, income from dairy farming was found to be much higher among the milk producers, who were members of both GCMMF and BMPCL than their counterpart non-members. As a result, the share of income from dairying was worked out to be 21% in milk producers of GCMMF and 10% in members of BMPCL as against the respective figures of 10% and 7% for non-member milk producers.

Socio-economic Characteristics of GCMMF and BMPCL and Non-member Milk Producers

Socio-economic Characteristics of GCMMF and BMPCL and Non-member Milk Producers

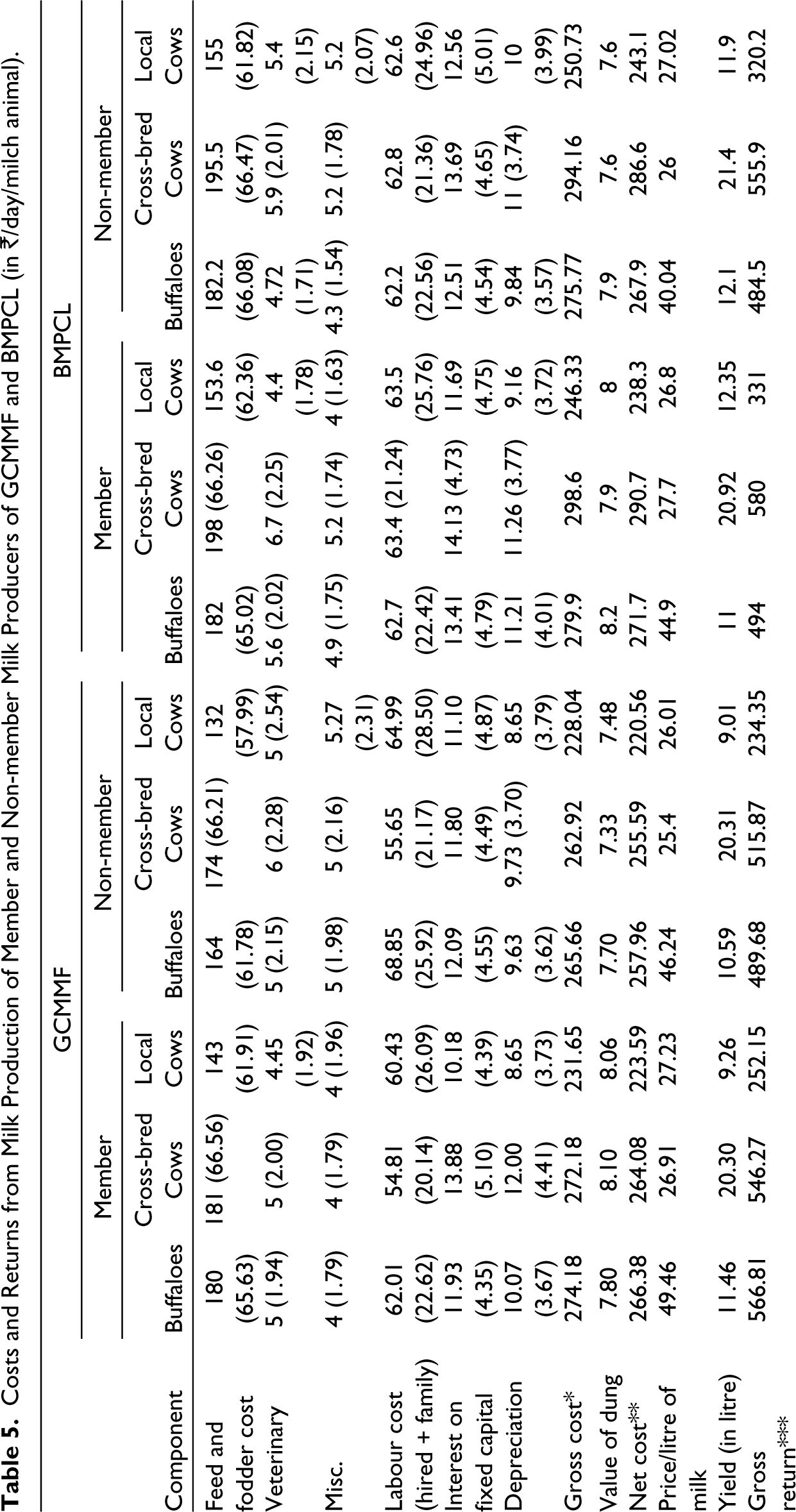

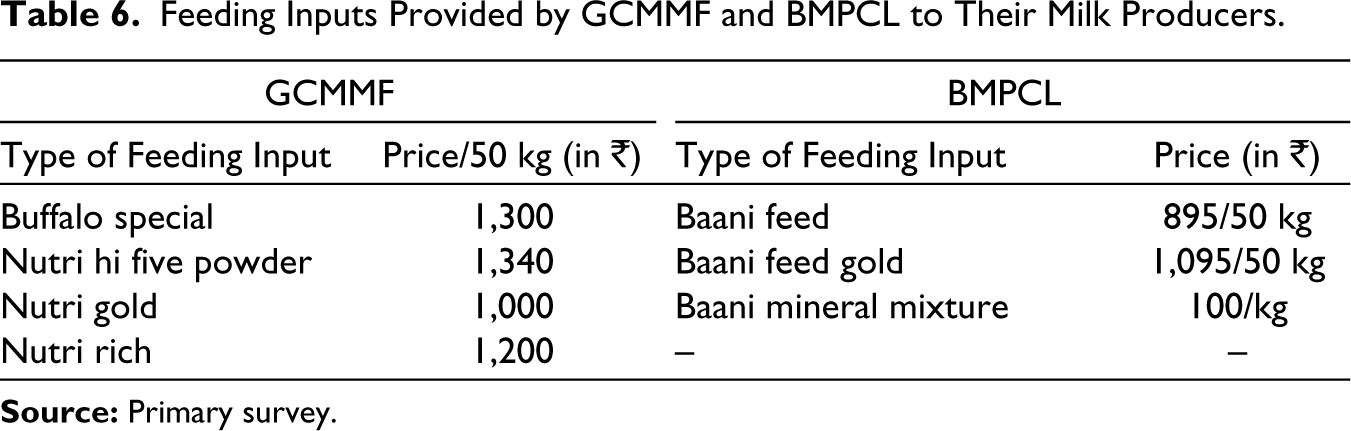

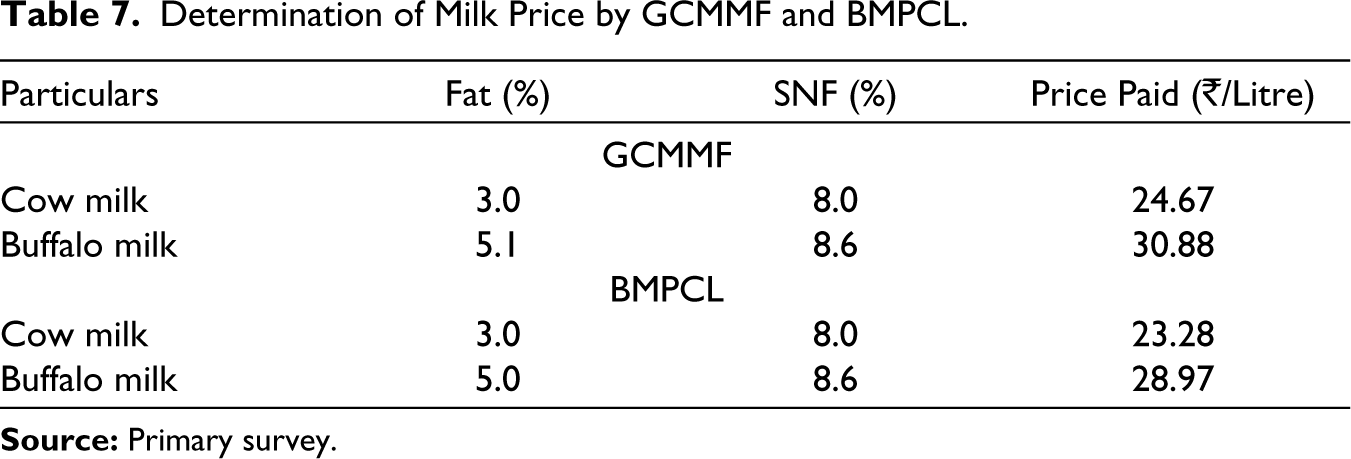

To determine whether the participation in milk collectives was beneficial for the milk producers or not as compared to their counterpart informal market supplying non-member producers, a species-wise comparison of gross and net returns from milk production was also carried out (Table 5). The gross cost was found to be slightly higher in member milk producers of both the collectives, GCMMF and BMPCL (except local cows of member milk producers in case of BMPCL) than their non-member milk producers. However, the net returns were also more among member milk producers of both GCMMF and BMPCL mainly due to more prices offered by the milk collectives as compared to informal milk markets. Milk yield was found to be similar across both members of milk collectives and non-members. In fact, milk yield of buffaloes and cross-bred cows was slightly higher among non-member milk producers than that among milk producers of BMPCL. Thus, although the collectives claimed to provide quality feed for improvement in milk production to the member producers, but milk yield was found to be similar across both the member and non-member producers for different species. Therefore, the net returns were more among member milk producers due to higher price offered by milk collectives (except the price of milk of local cow of member producers of BMPCL). While comparing the returns from milk production among milk producers supplying milk to GCMMF and BMPCL and their counterpart non-members, significant differences were observed in net returns from buffalo milk. Due to higher price offered by GCMMF, net returns were more among GCMMF milk producers than non-members. However, a significant difference was observed in net returns from local cows. Despite being offered a higher price for local cow milk by the GCMMF, the net returns were more among member farmers of BMPCL due to difference in milk yield. Hence, price was a significant component in buffalo milk production in case of GCMMF milk producers, whereas yield was significant among local cows of BMPCL, and thereby, net returns were also higher for them. The variation in feeding cost was mainly due to the difference in the price of feeding inputs as the member milk producers of GCMMF and BMPCL had used different types of feeding inputs provided by the milk collectives (Table 6). However, it was not compulsory for the member producers to purchase the feeding inputs from the milk collectives. The price of milk under both the milk collectives was determined based on fat and SNF in the milk. For cow milk with a fat of 3% and SNF of 8%, GCMMF paid a price of ₹24.67 per litre, while BMPCL paid ₹23.28 per litre. Similarly, for buffalo milk, the price paid was ₹30.88 per litre for a fat of 5.1% and SNF of 8.6% by GCMMF and ₹28.97 per litre by BMPCL for a fat of 5% and SNF of 8.6% (Table 7).

Costs and Returns from Milk Production of Member and Non-member Milk Producers of GCMMF and BMPCL (in ₹/day/milch animal)

Costs and Returns from Milk Production of Member and Non-member Milk Producers of GCMMF and BMPCL (in ₹/day/milch animal)

*Gross cost includes all the expenditure on milk production.

**Net cost is gross cost value of dung.

***Gross return is the value of milk production, i.e. price of milk × milk yield.

****Net return is gross return - net cost.

^Dairy gross receipt = Gross return + value of dung.

^^Input–output ratio = Gross return/Gross cost.

Feeding Inputs Provided by GCMMF and BMPCL to Their Milk Producers

Determination of Milk Price by GCMMF and BMPCL

Garret Ranking of Benefits to Milk Producers in Milk Collectives

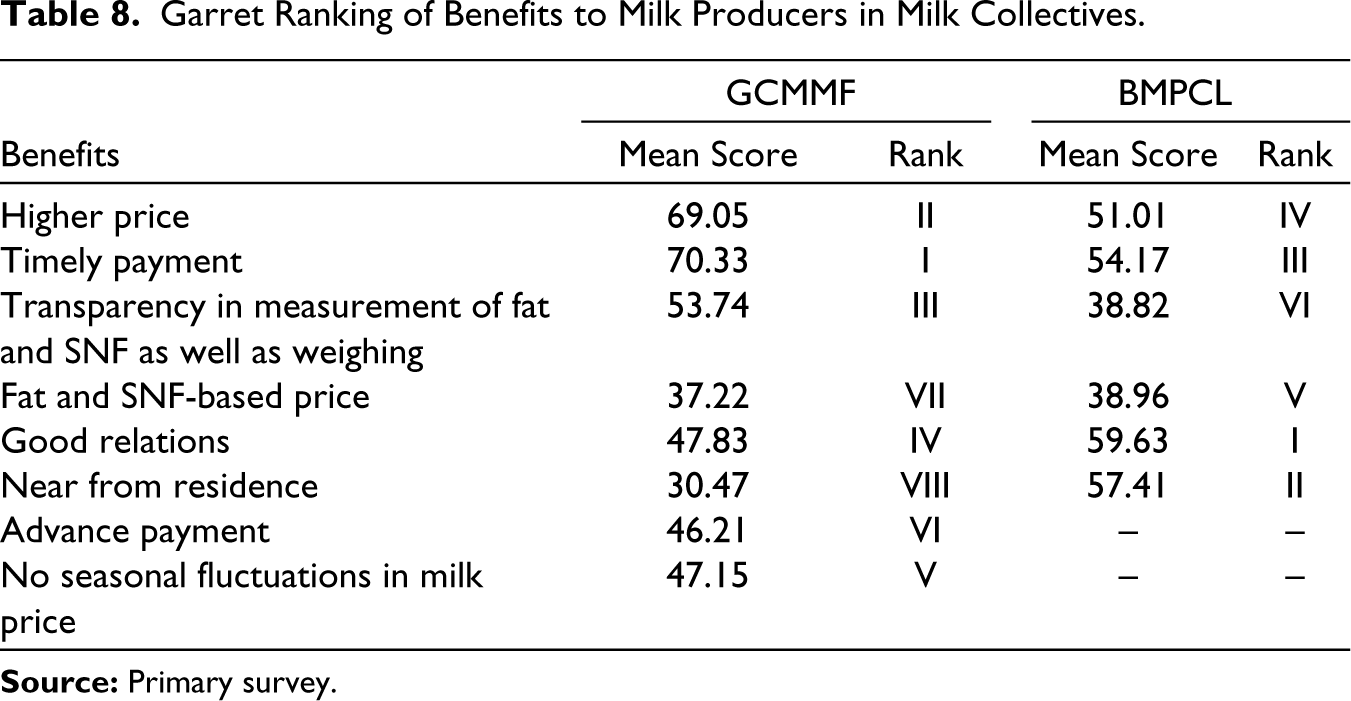

The perceptions of the milk producers regarding major benefits and constraints were also ranked while linking with the milk collectives. Timely payment was turned out to be ranked topmost for selling milk to GCMMF. Milk producers argued that sometimes, it took long time to get the payment for the milk in informal markets whereas, dairy cooperative transferred payment into their bank accounts after every three days. Moreover, price paid by the dairy cooperative was also higher as compared to the informal markets. This was also ranked second by the milk producers of the dairy cooperative for linking and supplying milk to it. Another notable benefit under the dairy cooperative was found to be the facility of advance payment, which helped the milk producers to buy inputs and clear off the pending dues in the local markets. On the other hand, good relations with the milk buying agency were found to the topmost reason followed by lesser distance from milk collection centre for linking with BMPCL. Transparency in the measurement of fat and SNF, along with proper weighing, fat and SNF-based milk pricing, was another major benefit under both the milk collectives (Table 8).

Conclusions

Small producers’ participation in milk collectives such as dairy cooperatives and producer companies has been identified as an institutional mechanism to mobilize and integrate small and marginal producers in modern dairy value chains in order to collectively leverage their production and marketing strengths (GoI, 2018). In this context, the study has examined the performance and functioning of two milk collectives and their impact on milk producers in Indian Punjab. The findings of the study revealed that both the collectives had created their own supply chains to procure, process and retail milk directly from the milk producers. Also, the collectives had brought quality consciousness among the milk producers as both had procured milk based on fat and SNF in the milk and paid the price directly into their bank accounts. Realizing the role of women in milk production, the dairy cooperative opened saving accounts of the milk producers in the bank in the name of their women member in their household. The quality-based milk pricing led to fetching of higher price and consequently, higher profitability for the milk producers supplying milk to the collectives as compared to their counterpart non-members.

Further, the findings of the study also revealed that the dairy cooperative was more inclusive than the producer company in terms of participation of the producers. In this context, it becomes imperative to ensure the participation of marginal and landless producers, who are excluded from other networks such as institutional credit and produce markets as they require such producer organizations more than any other kind of landowner or producer (Singh, 2021b). The milk producers in both the collectives were relatively younger and better educated as compared to their counterpart non-member producers. It was also argued that younger, educated and more informed producers have more probability of participation in such collectives, which could lead to improvement in their income, consumption expenditure and investments in productive assets, which in turn could reduce their farm indebtedness (Singh & Vatta, 2019). Further, the collectives claimed to provide quality feed to the milk producers to increase their milk production, but there was no improvement in the productivity of milch animals as milk productivity was similar across member and non-member producers. Therefore, it seemed that the collectives were more interested to promote the sale of third-party firms than the milk producers’ welfare. Therefore, there was a need for the collectives to take greater responsibilities in terms of advancing credit, introducing new technologies to improve milk production and productivity and encouraging participation of women milk producers to make such linkages inclusive, effective and sustainable.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.