Abstract

The study investigated the determinants of financial inclusion in selected African countries. Researchers have found an extraordinarily strong positive association between social inclusion and financial inclusion; financial inclusion is the key to eradicating poverty and social exclusion as it presents an opportunity for people to benefit from financial services. A single data set was formed by combining four samples from the Democratic Republic of Congo, Eswatini, Kenya and South Africa. Data were obtained from surveys done by FinScope. FinScope Consumer Survey is a probability survey with an end-user focus (individual or household) on financial services and products. The FinScope Consumer Survey, done by the FinMark Trust, is uniquely aimed at increasing understanding of the informal financial product/service market.

Probit regression models were estimated to find significant factors influencing financial inclusion in selected African countries. The linear probability model was used for the robustness check. The study found that age, education, marital status, bank branch accessibility, location, internet, salary, income, proof of residence, social networks, financial advice, gender and connectivity were significant in influencing financial inclusion. Governments must implement policies that enhance financial inclusion, in particular, ethnic groups, small communities and minorities. These policies will also lead to the reduction of poverty and the attainment of the UN Sustainable Development Goals.

Introduction

Social inclusion involves ensuring that members of society have equal access to the same opportunities (Oxoby 2009; Percy-Smith 2000; Silver 2010). Social inclusion and financial inclusion are two development agendas to improve the socio-economic well-being of all individuals in society. Reduction of barriers to social and financial inclusion will ensure a highly inclusive and developed society. Some barriers to social inclusion include a lack of access to finance to fund their participation in social initiatives, lack of internet access and economic development (Biancone and Radwan 2018). Some of the key indicators of social inclusion in developing countries are gender and equality, violence against women and children or minorities, access to public resources, human resource development opportunities and any form of discrimination (Warschauer 2004; World Bank 2014).

According to Ozili (2023a), there exist specific social inclusion policies that reduce the level of financial inclusion for the older population in low- and medium-income countries. Financial inclusion and social inclusion have been found to influence the economic performance of micro, small and medium enterprises. Ozili (2020) examined the association between social inclusion and financial inclusion. He found that there was a positive and significant correlation between these variables in African, Middle Eastern and Asian countries. These findings imply that policies and laws established in a country to promote social inclusion can support the policies designed to promote financial inclusion and vice versa.

Daniel (2001) defines social inclusion as the removal of institutional barriers and the improvement of access to development opportunities for diverse individuals and groups. It is important to highlight that the participation of individuals in the informal economy or financial systems may not be recognised, registered, regulated or protected under legislation and social protection. Financial inclusion policies are essential tools for the success of micro, small and medium enterprises (Aker et al. 2014) and positively affect specifically the performance of women-owned businesses and enhance social inclusion. Financial inclusion promotes social inclusion through convenient access, availability and usage of formal financial services (Chibba 2009). Bateman, Duvendack and Loubere (2019) argue that institutions that have developed policies supporting social inclusion have achieved higher financial inclusion. Bateman, Duvendack and Loubere (2019) and the World Bank (2014) have found that financial inclusion is the key to eradicating poverty and social exclusion and ensuring that countries meet the United Nations Millennium Development Goals.

According to Chibba (2009), financial exclusion has a considerable influence on social exclusion by preventing individuals or social groups from gaining access to the formal financial system. Chibba argues that institutions that have developed policies supporting social inclusion have achieved higher financial inclusion. Chibba states that financial inclusion implies the provision of all initiatives that make formal financial services accessible and affordable, primarily to low-income people and small and vulnerable communities. Ensuring that both financial inclusion and social inclusion are understood and supported leads to an incremental and complementary approach to meeting the United Nations Millennium Development Goals as financial inclusion promotes social inclusion through convenient access, availability and usage of rules-based formal financial services by the ‘newly banked’, who are generally underprivileged population segments, vulnerable groups such as rural dwellers, women and low-income families who benefit enormously from basic financial services such as savings, borrowings, payment and insurance (World Bank 2014). Finally, Bateman, Duvendack and Loubere (2019) found that financial inclusion is the key to eradicating poverty and social exclusion as it presents an opportunity for people to benefit from financial services. This contributes to the economic and social advancement of the beneficiaries.

Given the strong relationship between financial inclusion and social inclusion, this study sought to find factors influencing financial inclusion in selected African countries. Focus on issues concerning financial inclusion is growing the world over. Financial inclusion is one of the major socio-economic issues that international institutions, policymakers, central banks, financial institutions, researchers and governments must consider (World Bank 2017). This study defines financial inclusion as the delivery of appropriate formal financial services to all segments of society to meet their savings, investment and credit requirements, financial literacy levels and convenience needs responsibly and sustainably. Financial inclusion is useful for equitable growth in all segments of society to reduce disparities. The provision of banking facilities to marginalised sections can enhance the mobilisation of savings in the economy. It is, therefore, proposed that the growth in financial inclusion levels improves the depth of the financial sector.

The absence of accessible and affordable formal bank accounts in a financial system can result in persistent income disparity, poverty and sluggish economic growth (Hussain and Chakraborty 2012). Low levels of financial inclusion in an economy increase the gap between the rich and the poor as the population is characterised by inequitable growth. According to the World Bank (2021), informal financial arrangements are mostly segmented from national markets, which limits the supply of credit. Most loans attract higher rates than moneylenders and pawnbrokers charge, mostly due in large part to the higher costs and risks associated with informal loans and the power imbalance that exists between borrowers and lenders.

This study used data from both the supply and demand sides to determine factors impacting financial inclusion. Data from FinScope Surveys provide, among others, a basis for informed financial inclusion policy formulation. The existence of low levels of financial inclusion in many developing countries reveals the magnitude of the problem that needs to be addressed. The study was informed by the literature that the variables required included social networks, financial advice and the internet, among others, in each questionnaire. Using this criterion, four data sets were selected. The study used 16 proxies, including a new variable, social networks, for the dependent variable of financial inclusion in the four selected African countries: South Africa, Kenya, Eswatini and the Democratic Republic of Congo (DRC). The article analyses data from both the supply side and the demand side. The second section presents literature review; the third section outlines the research methods used; the fourth section reports, analyses and discusses the results and the fifth section presents a conclusion.

Literature Review

Financial inclusion aims to harness savings through financial intermediaries and direct the funds to the productive sector. Jagadeesh (2015) applied the Harrod–Domar growth model using auto-regressive distributed lags when investigating the role of savings in Botswana. The Harrod–Domar model is a classical Keynesian model of economic growth. According to the Harrod–Domar model, the main strategy for economic development is savings mobilisation and generation of investment (Domar 1947; Harrod 1939). The model affirms that savings result in investments that lead to economic growth.

Economic growth needs a stable and conducive macroeconomic environment for sustained economic growth. Research has also pointed to the importance of considering the level of national income when designing policies to boost financial inclusion (Sha’ban, Girardone and Sarkisyan 2020). The ability of the financial system to reduce risks enables the economy to absorb economic shocks (Arner 2007; Easterly et al. 2000). This then leads to a better stable environment that supports growth, according to scholars. It also begs the question: What factors influence individuals to be financially included? Several studies have shown that education influences levels of financial inclusion (Allen et al. 2012; Clamara, Pena and Tuesta 2014; Ghatak 2013). Park and Mercado (2015) found that primary education and lower literacy rates had no significant effect on financial inclusion in developing Asia. Per capita income was found to have an influence on financial inclusion and a correlation between poverty and financial access.

Omar and Inaba (2020) advocate further promoting access to and usage of formal financial services by marginalised segments of the population to maximise society’s overall welfare.

In Nigeria, Adewale (2011) found factors influencing financial inclusion to be eligibility, affordability, cultural capital, financial complacency and religious inclinations. The unbanked population in Nigeria lacked documentation, had lower incomes, lower financial literacy levels and were more likely to be female (King 2011). Physical distance was found to be a hindrance to financial access to individuals in rural areas. Mobile finances positively influence saving habits among poor households in Africa. But this can be reduced using technology, mobile banking and mobile money agents (Ouma, Odongo and Were 2017; Seng and Lay 2018). Kenya, among other African countries, has made progress in the use of mobile phones for financial services (Jack, Suri and Townsend 2010; Johnson and Arnold 2012).

Growth in the use of internet banking, debit and credit cards may reduce the influence of branch use in the country, hence growth in financial inclusion. Distance from financial services providers is losing its importance due to the availability of automated teller machines and internet banking but remains and influential in-service provision in Africa (Brevoort and Wolken 2008, 1). Zins and Weill (2016) found that the more one is educated, being a male, mobile phone usage, greater income, and the older one is positively influenced by financial inclusion. Lenka and Barik (2018) found a positive correlation between the growth of financial inclusion and the expansion of internet services and mobile money. Bapat and Bhattacharyay (2016) found that richer, more educated, as well as married, employed and separated individuals were more likely to be financially included. Sahoo et al. (2017) found that the education level of the household head, land size, level of income and nature of employment were determinants of financial inclusion. There is concurrence among these authors that the better the education, being a male, the higher the income, internet usage, being married and employed are more likely to see one using formal financial services. There remains a void on how social networks influence financial inclusion in the existing studies.

Bending, Giesbert and Steiner (2009) and Demirguc-Kunt and Klapper (2012) found that credit demand, insurance purchases and savings behaviour are influenced by income levels in rural Ghana. Although Karpowicz (2014) focused on enterprises, they found that collateral, cost of services and lack of savings were the major obstacles to financial inclusion in Columbia. Sotomayor et al. (2018) found that some groups in Peru, such as women, young people and individuals living in rural areas, had difficulty accessing the formal financial system. Some studies found that financial education, which is the acquisition of financial knowledge, had an impact on levels of financial inclusion (Allen et al. 2012; Clamara, Pena and Tuesta 2014; Lewis and Lindley 2015).

In Mexico, Martinez, Hidalgo and Tuetsa (2013, 15) found that vulnerable groups were more likely to be financially excluded. The study found that individual vulnerability factors, education, gender, occupation and income level had a positive correlation to an inclination to use the informal financial market, the capability of responding to exogenous shocks, and proclivity to save and community size and location. Soumare et al. (2016) found that financial inclusion in West and Central Africa is driven by gender, marital status, income, employment status, education residence area, household size, age and level of trust in financial institutions. The larger the household, the smaller the probability of bank account ownership in West Africa but was insignificant in Central Africa.

Distance plays a role in accessibility, provision and delivery of banking services, mostly due to the high transaction costs, but ATMs and online banking services have negated these negative impacts in areas with network connectivity and ICT infrastructure. However, the challenge remains concerning loan transactions that tend to require in-person interactions. Age, employment, gender, education and location (urban/rural) are strongly linked to bank access (Clamara, Pena and Tuesta 2014; Johnson and Arnold 2012; Martinez, Hidalgo and Tuetsa 2013; Tuesta et al. 2015). Tuesta et al. (2015) found high correlations between financial inclusion and level of education, income and age. The fact that low financial inclusion levels are still a problem implies that literature gaps still exist. None of the existing studies reviewed have investigated the effect of social networks, the internet and financial advice on financial inclusion levels. Some studies such as Akar and Topcu (2011) found a relationship between consumers’ attitudes and social media marketing. It is on this basis that we included social network variables in our study.

Assuming et al. (2018) posit that financial inclusion, policies should target key populations like women and young people. Tinta et al. (2022) recommended the improvement of the banking sector, institutions, innovations and income-generating activities to attract women and reduce the gender gap. Jima and Makoni (2022) stressed the possibilities of a trade-off between financial regulation, inclusion and digitalisation versus financial stability for risks to be spread over a greater populace. In a study on countries belonging to OECD, Koceda and Eshun (2023) emphasised the importance of quality literacy policies, trade improvement with restrictions on cross-border capital flows and a more efficient financial system to promote financial inclusion. In coming up with effective policies comprehensive measure of quality financial inclusion that accounts for important dimensions that include diversity, affordability, appropriateness and flexibility of financial products and services should be in place (Chipunza and Fanta 2022).

Assuming et al. (2018) found that while the aggregate level of financial inclusion has improved significantly between 2011 and 2014, there are disparities in the level of development among African countries. According to the Kenya National Bureau of Statistics, formal financial inclusion as measured by the access concept expanded to 83.7% in 2021 from 82.9% in 2019 and 26.7% in the baseline survey in 2006. According to the Gordon Institute of Business Science (2023), South Africa has made gains in providing previously unbanked people access to accounts, the most basic measure of financial inclusion. Lack of financial literacy is holding the country back from achieving greater socio-economic development. The country remains largely a cash society, with low-income consumers wary of fees, although 70% of the population has access to a transactional bank account. Usage is also low with 27% of people withdrawing their money immediately from their accounts.

In Eswatini, although access to financial services for Eswatini improved from 65% in 2014 to 85% in 2018, there is still low usage of banking facilities (UN 2022). The share of adults with access to a bank account or mobile money account stands at an estimated 26% in DRC, compared to a regional average of 43% according to the Digital Banking in Sub-Saharan Africa Report (2022). The financial system in the DRC is relatively small, largely dominated by banks, and highly concentrated (African Development Bank 2022). The African Development Bank among other development partners has been working on the improvement of basic financial services, through increased interoperability of digital financial services. Development partners have also been working on revising the regulatory frameworks of the country and improving access to more than 25 million vulnerable populations that include women, young people and rural populations.

Methodology

The Probit Model

Probit regression, also called a probit model, is applied when modelling binary variables. It is a form of regression where the dependent variable can take only two values, for example, male or female. The model is used when estimating the probability that an observation with specific characteristics will fall into a specific category. In binary regression variable models, the assumption is that the dependent variable is quantitative, whereas the explanatory variables are qualitative or quantitative (Wooldridge 2009). Certain types of regression models have the response variable dichotomous with a 1 or 0 value. The problems associated with such models are inference or estimation. Common models that are used for estimations are the linear probability model (LPM), probit model and logit model. The probit model uses a normal cumulative distribution function.

In this study, a cumulative index was developed using the dichotomous independent variables. For example, the decision of an individual to be financially included or not depends on the value of the index, Ii, determined by the independent variables. For example, the greater the value of index Ii, the larger the probability of being financially included.

The index, Ii, can be expressed as

where x is the explanatory variable.

It is assumed that Ii is normally distributed with the same variance and mean. If this holds, estimations of parameters can be estimated to get information about the unobservable index itself.

In this study, the financial inclusion function was modelled as follows:

FI = ƒ (age, education, religion, education, marital status, bank branch accessibility, location, internet, formal employment (salary), income, proof of residence, financial advice, social networks, gender and phone) + ℮

where ℮ is an error term.

The model was estimated as follows:

where FIA is a financial inclusion indicator for the select African countries under study.

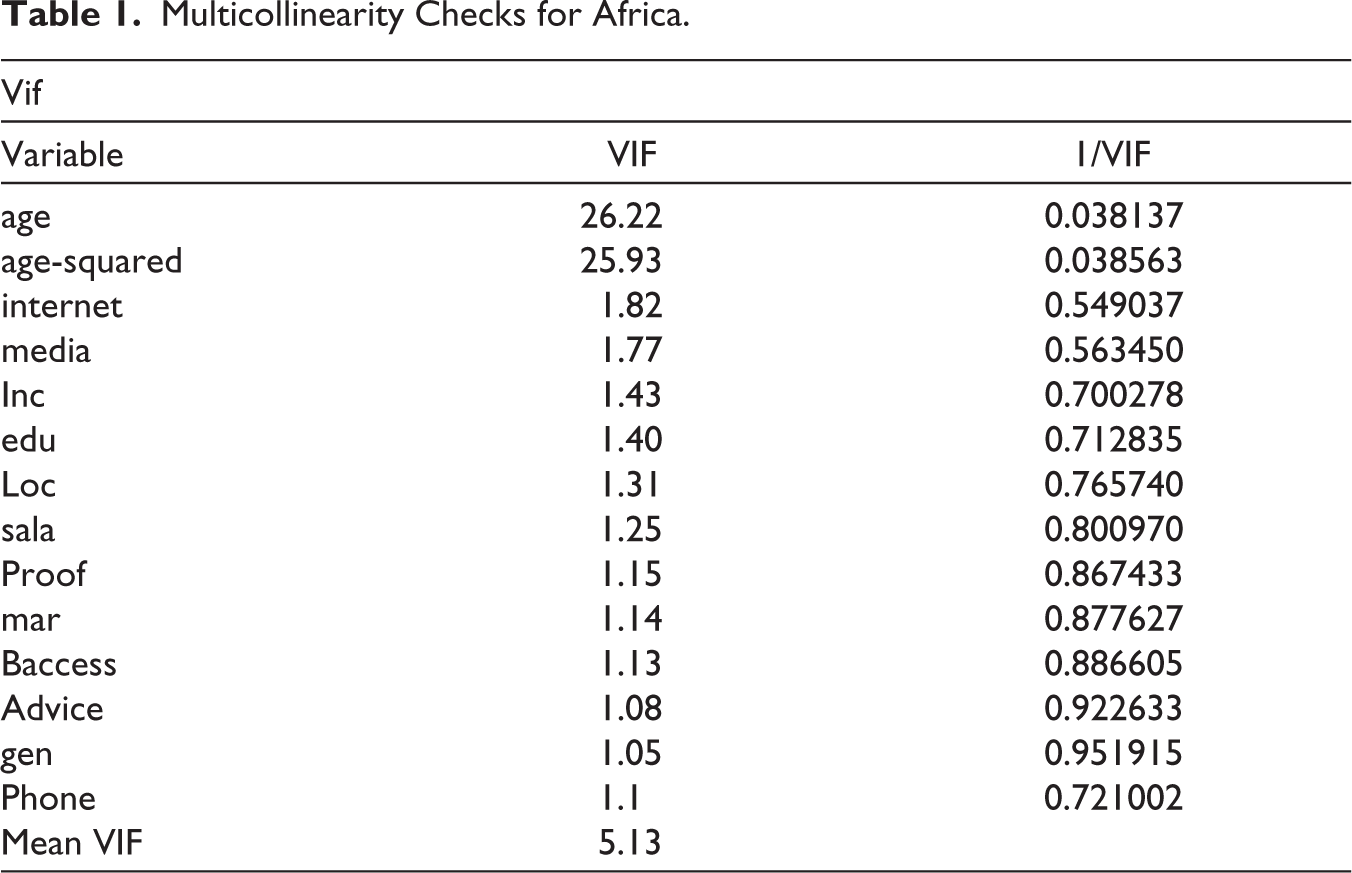

Robust standard errors were used to solve heteroskedastic negative effects. The LPM was also estimated for robustness checks, and probit model results were reported. Multicollinearity checks were done, and all the VIF values were acceptable except for the age variable. These are depicted in Table 1:

Multicollinearity Checks for Africa.

Variables Included in the Model

Below is a brief description of the variables included in the model based on the review of the literature presented. Dummy variables were used to measure the quantitative values of the variables, mostly dichotomous variables.

Proof of residence: When opening an account with a bank, one is asked to provide evidence of identity and confirmation of a physical address using original documents, a challenge in many developing countries. Utility bills, local authority bills, tenancy agreements, current council rent books and mortgage statements are some of the documents that are accepted as proof of residence in many countries.

Salaried: The nature of employment also matters as there is a higher probability of one being financially included when formally employed, unlike a situation where one has no formal employment.

Educational level: As the level of education rises, levels of financial inclusion tend to increase. In this study, there are four categories for the education variable: no official education, primary education, secondary education and tertiary education.

Marital status: Marital status is a basic variable related to access and use of financial services.

Location: Geographical area is one influential factor determining the financial accessibility of people living in remote, rural and marginalised areas.

Gender: Several studies have shown that women have fewer possibilities of accessing formal financial services, so most public policy interventions are focused on promoting financial inclusion among women.

Age: The level of financial inclusion is higher among the economically active people and that of financial exclusion is higher in old age and the minors. For the model, estimated age is taken as a series of dummy variables depending on the age of the respondent ranging from 18 to 85 years.

Age2: This is age squared. For this study, an assumption has been made that the use of financial services increases with age and decreases at some age threshold. The Age2 captures this non-linear effect. Soumare et al. (2016) found the age-squared coefficient negative, revealing a threshold effect for the age variable.

Social networks: Social networks can offer substantial upside in terms of customer engagement, and feedback and are utilised to strengthen relations with external and internal stakeholders. The existing social media theories have explained characteristics influencing user behaviour, ease of use of modern technology, social influence and intermediary functions of these communication platforms.

Financial advice: A financial mentor not only teaches someone financial knowledge but also encourages one to make a positive financial decision to improve quality of life.

Income level: The income of an individual can influence financial inclusion in any economy. It is important to investigate the link between financial inclusion and total income from all sources personally received by an individual in the last 12 months. For the current study, income from all sources personally received in the last 12 months was used.

Physical access: Accessibility to financial services or bank branch may influence the financial inclusion of an individual. Elevated levels of financial inclusion in many developing countries are critical for consumers’ access to formal financial institutions.

Internet access: Does access to the internet influence financial inclusion? The growth in the use of internet banking, debit and credit cards may reduce the influence of branch use in the country, hence growth in financial inclusion.

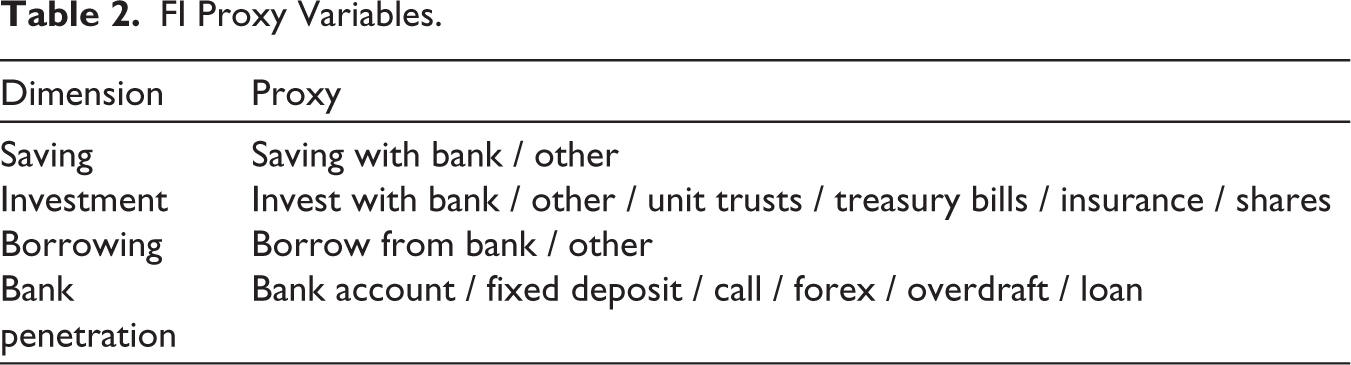

Mobile phone: Mobile phones have brought changes in the way business is done. In Africa, mobile phone connectivity and usage are higher than other forms of connectivity. Financial service delivery has been revolutionised by these technological advancements as shown in several studies. The influence comes with mobile phone users having access to banking services, financial information and other financial services. Table 2 lists the proxy variables used to measure financial inclusion.

FI Proxy Variables.

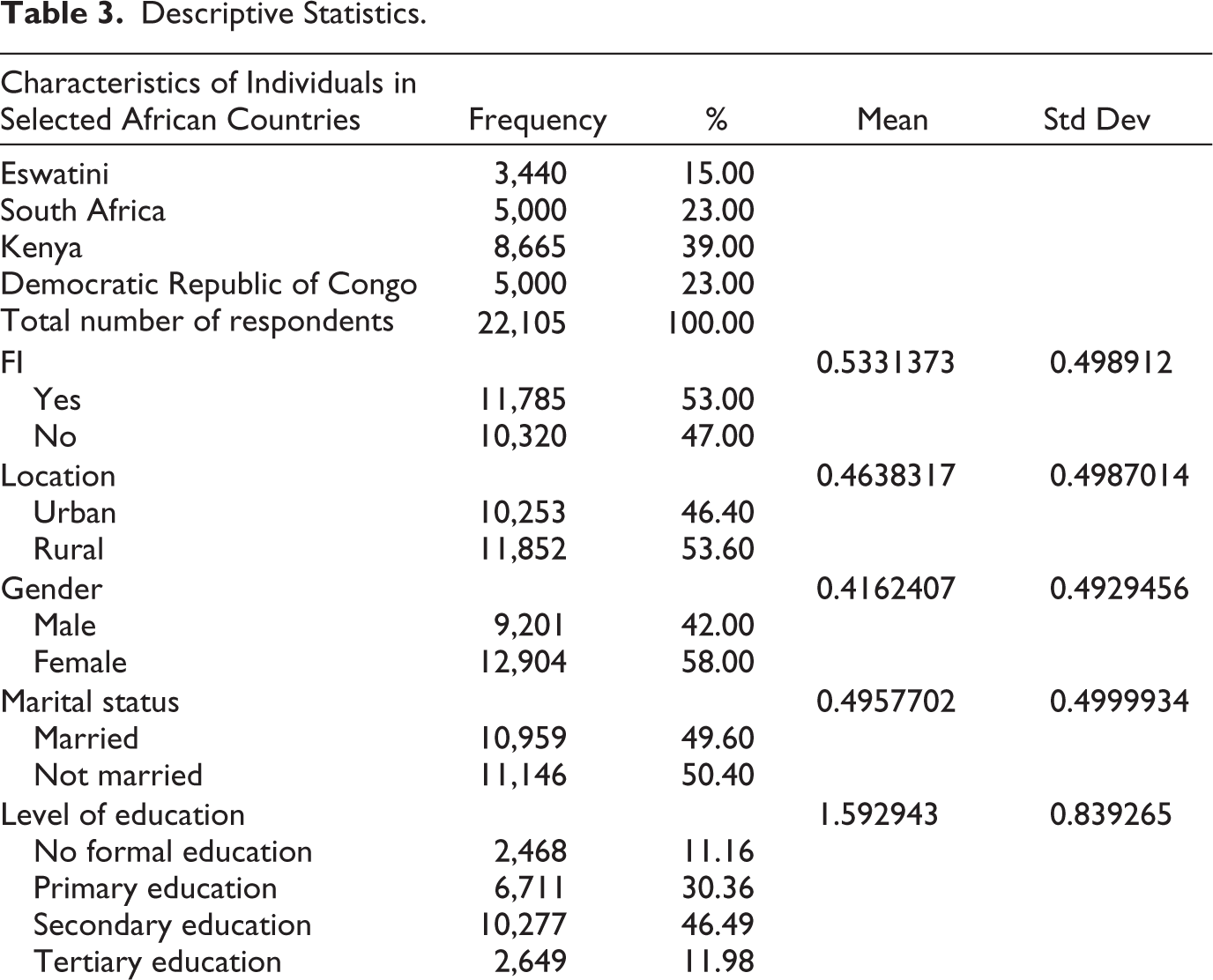

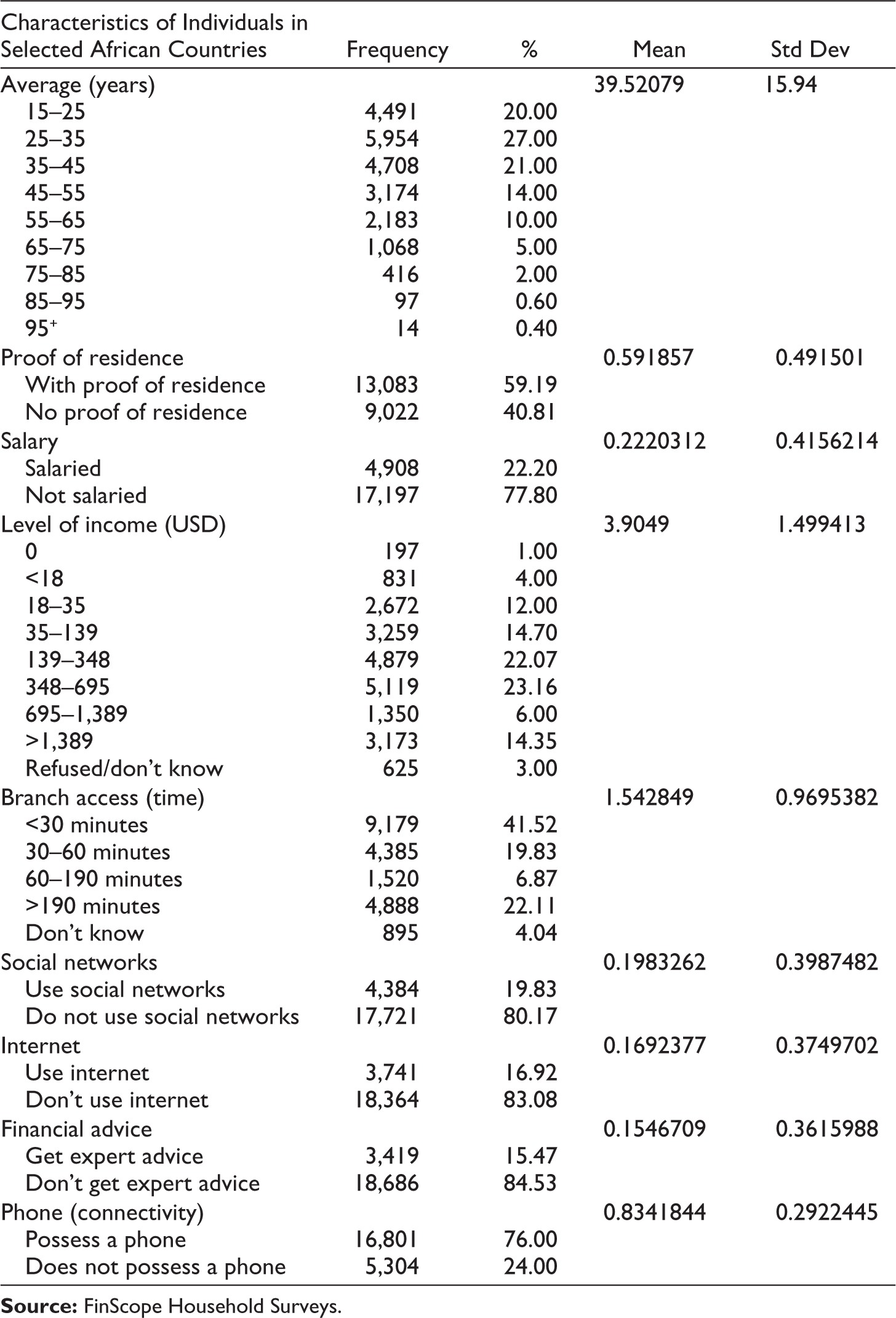

This article used data from FinScope Surveys done in different countries. A sample of four countries was used to answer the research question. FinScope Surveys use a random selection of eligible members in each household by Kish Grid. The surveys used in this study were done in both rural and urban areas of the four countries, namely, South Africa, Eswatini, Kenya and the DRC. The questionnaires were either written in English or the local language or in English but interpreted by the respondents. A purposive sampling technique was used in coming up with the four African countries under study. Initially, there were 21 FinScope country data sets but some questionnaires left out important variables resulting in them being dropped. Variables required included social networks, financial advice, and the internet in each questionnaire, among others. The aggregate sample was 22,105 from DRC (5,000), Eswatini (3,440), South Africa (5,000) and Kenya (8,665). The surveys provided valuable information allowing the analysis of elements of financial inclusion that have not been studied before. Table 3 shows the descriptive statistics.

Descriptive Statistics.

Analysis, Results and Discussions

Estimated Empirical Results

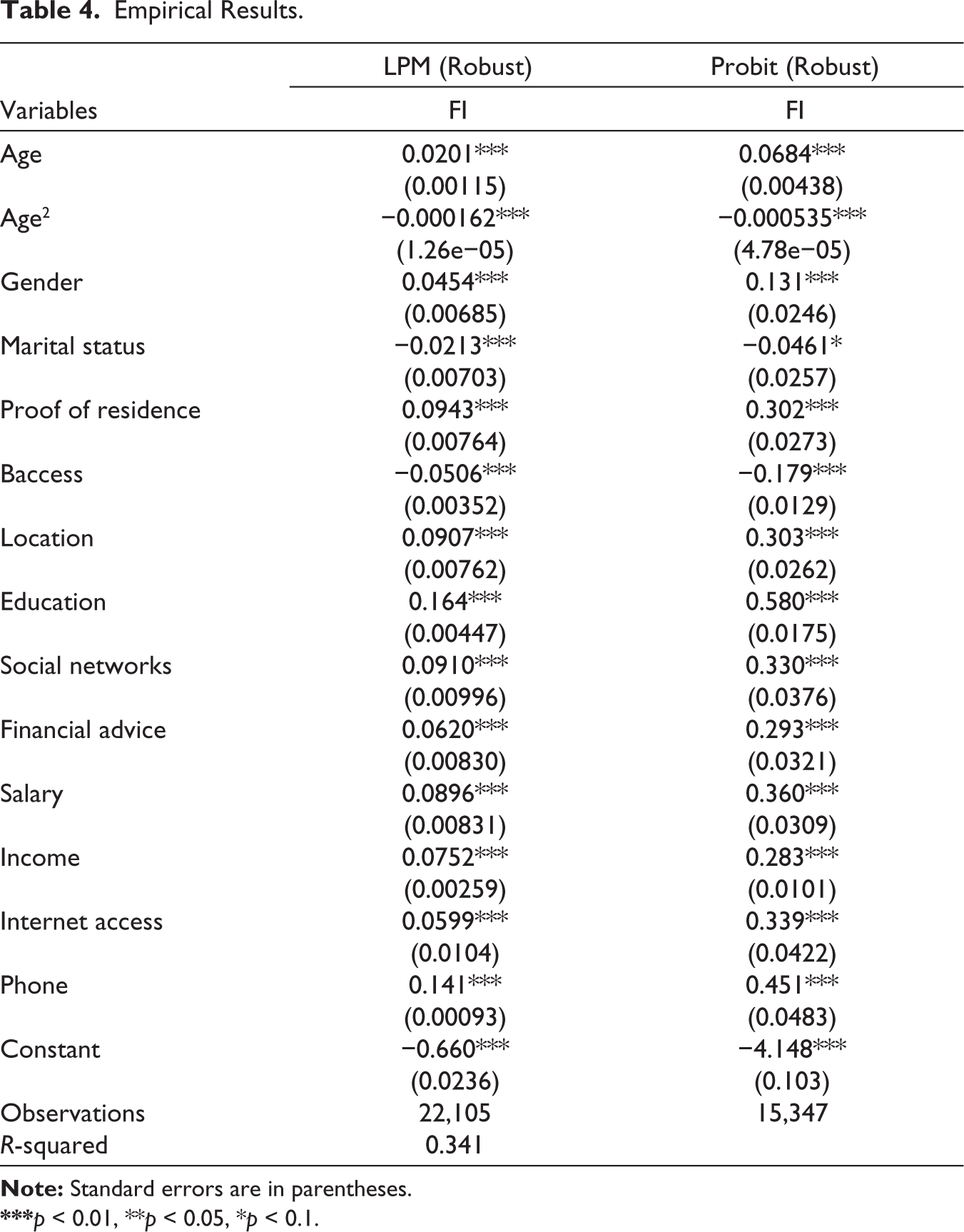

To find factors influencing financial inclusion in selected countries in Africa, probit models were estimated. The LPM was used to check for robustness. Table 4 shows the results of the robustness test.

Empirical Results.

***p < 0.01, **p < 0.05, *p < 0.1.

A high or low R-squared is not necessarily good or bad, as it does not convey the reliability of the model, nor whether you have chosen the right regression (Wooldridge 2002). One can get a low R-squared for a good model, or a high R-squared for a poorly fitted model and vice versa. The low R-squared of 0.341 reported in the LPM in Table 4 was because the study focused on the human decision of whether to use formal financial services or not. This is consistent with Ozili (2023b) who posited that any field that attempts to predict human behaviour typically has R-squared values lower than 50%.

The ‘age’ variable was significant at a 1% significance level and positively related to financial inclusion in selected African countries. This implies that as age increases the probability of one having an account with a formal financial institution is increased. An individual’s age is a crucial factor influencing one’s financial inclusion status. The findings were in line with Soumare et al. (2016) and Deaton (2005). The Age2 captures this non-linear effect. As age2 increases or decreases, financial inclusion levels decrease or increase, respectively.

Results showed that gender was significant at a 1% significance level with a positive correlation. If one is a male, he is more likely to be financially included than a female. The results show that gender is a determinant of financial inclusion in selected African countries. The findings were in line with studies that showed women were less likely to be included than their male counterparts (Allen et al. 2012).

Marital status was significant at a 10% significance level and negatively related to financial inclusion. This implies that if one is married, she or he is less likely to be financially included than an unmarried individual. The findings were in line with Martinez, Hidalgo and Tuetsa (2013) and Soumare et al. (2016), who reported that marriage reduces the probability of being financially included.

Proof of residence was significant at a 1% significance level and positively related to financial inclusion. If one has proof of residence, the more likely the person is financially included. Results show that proof of residence is a crucial factor in the determination of the financial inclusion status of an individual. The findings were in line with the World Bank (2009) report that recommended government authorities ensure people are not hindered by formal financial systems. The creation of a database with information for all citizens will help reduce the risks of opening an account for someone without proof of residence. An identity card must suffice for opening a basic transaction account if a credit bureau system is well established across Africa. This can also be complemented by national database synchronisations where authorised users that include financial institutions can access information.

Baccess (physical access) was significant at a 1% significance level and negatively related to financial inclusion. The more time one takes to get to the nearest bank branch, the less likely she or he to be financially included. The empirical results show that time taken to the next bank branch is an influential factor in financial inclusion. The findings were in line with Brevoort and Wolken (2008) who found the distance from the next branch influenced individual financial decisions.

Location was significant at a 1% significance level and positively related to financial inclusion. One who lives in an urban area is more likely to have an account with a formal financial institution than one in a rural area. Results show that those in the rural areas are less likely to be financially included as there may not be infrastructure or suppliers of financial services in those areas. The findings were consistent with Kedir (2003) who found those from rural or remote areas less likely to be using formal financial services.

Education was significant at a 1% significance level and positively related to financial inclusion. The more educated one is the more likely she or he is financially included than one less educated. The results show that when one is educated, she or he is likely to be able to appreciate the importance of having a formal account than the one who is less educated. The findings were in line with Lewis et al. (2022) and Messy and Monticone (2012) who found that the higher the education one acquires the greater the probability of using formal financial services.

Social networks were significant at a 1% significance level and positively related to financial inclusion. An individual who uses social networks is more likely to be financially included than one who does not use them. Results showed that a social network user is more likely to be financially included as one may have access to information on financial services’ importance and use. This may also be due to more knowledge and experience in using technology in general which would bode well for mobile banking for instance. Social networks in Africa can lessen financial constraints by promoting households’ access to formal finance. Social networks may be of more impact to the younger generation which is more fascinated and records higher participation on these platforms. No study has investigated the effect of social networks on financial inclusion and the current study contributes to growing literature on the subject.

Financial advice was significant at a 1% significance level and positively related to financial inclusion. If one has access to financial advice she or he is more likely to be financially included than one who does not have. The empirical results show that financial advice is a crucial factor in the delivery of financial services as one will be equipped with the requisite information to make a positive decision. There is a need for governments to ensure the establishment of financial advisory associations or improve access to experts that can foster positive decision-making. The non-governmental sectors can sometimes be more effective than the government to meet grassroots-level needs.

Salary was significant at a 1% significance level and positively related to financial inclusion. One who is formally employed is more likely to be financially included than one who is not. The one formally employed has access to regular income and having a formal account to receive it on a monthly/weekly basis may be a requirement. On the contrary, a study done in Spain showed that unemployment does not seem to be a factor of significance in defining financial exclusion in rural areas (Olit 2011). In Spain, this may be due to informal transactions that may be defined as other income rather than salaries. In Arica, those who earn regular and formal salaries are more likely to be financially included. Those who are employed in the informal sector may not be included as they may earn cash rather than transfers.

Income was significant at a 1% significance level and positively related to financial inclusion. The more income one receives, the greater the probability of one being financially included. Greater income level leads to more disposable income for savings and investment and reduced financial exclusion. Several studies also show a direct relationship between financial inclusion and higher income (Allen et al. 2012; Cano et al. 2013).

Internet access was significant at a 1% significance level and positively related to financial inclusion. One who uses the internet is more likely to be financially included than one with no internet. Accessibility to the internet may imply that one may be accessing financial services online and having access to valuable information leading to one having an account with a formal financial institution. The increase in the use of internet platforms goes in line with changes brought about by COVID-19 restrictions (Kasradze 2020).

Mobile phone accessibility was significant at a 1% significance level and positively related to financial inclusion. One with a mobile phone is more likely to be financially included than an individual without. A phone can enable one to have access to mobile bank financial services and regardless of distance or any form of inconvenience can easily access formal financial services. In a study on Africa, Ouma et al. (2017) found that mobile finances positively influence saving habits among poor households.

Financial inclusion is important for all countries in Africa for poverty alleviation and faster economic growth. According to the World Bank (2022), financial inclusion levels were South Africa −90%, Eswatini −85%, Kenya −83.7% and DRC −26%, where a significant portion of the individuals rely on mobile money accounts. Governments must advocate financial inclusion as the poverty levels are high on the continent. Particularly affected by poverty in Africa are the weakest members of society, their children and women. This may also be attributed to labour markets across most of Africa that are heavily gender-segregated and many women occupy low-paying, insecure occupations besides having less access to land, productive assets, social protection and technology, which are central to production. The determinants of financial inclusion investigated in this study give insight to all stakeholders in crafting, implementing and evaluating policies associated with addressing financial exclusion problems. The results of the study also provide for a combination of participatory approaches and local capacity building to empower vulnerable communities to develop as a reflection of their own needs and values.

Conclusions

The study found that in selected African countries, the following determinants influenced financial inclusion: age, age2, education, education, marital status, bank branch accessibility, location, internet, formal employment (salary), income, proof of residence, financial advice, gender and phone.

Financial institutions must take advantage of consumers’ desire to use or access social media to interact with potential or existing customers. According to Njanike (2021), social media penetration for the four countries is as follows: South Africa, 42.9%; Eswatini, 27.9%; DRC, 4.9%; and Kenya, 19.3%. This will also improve the uptake of formal financial services as consumers are advised through social media. Communication has taken a dynamic shift from print or television to two-way (feedback) chats through different social media platforms. There is a need for financial institutions to come up with innovative methods using technology to reduce barriers and costs in accessing or provision of formal financial services. This may also include simplifying documentation requirements or adding exceptions for certain applicants in addition to financial education and proper regulation of the financial sectors of countries such as DRC. The use of mobile phones can change the cost and access equation, enabling financial services suppliers to serve isolated and poor individuals or communities. According to Njanike (2021), mobile phone penetration of the population for the four countries under study was as follows: Kenya, 117.2%; DRC, 46.9%; Eswatini, 110%; South Africa, 95%. Also, the increase in the use of mobile phones will make it easier for the introduction of mobile financial services such as MPESA in Kenya wherever there is a network. The use of mobile phones is transformational as services are extended to those who would not be reached through traditional branches. In countries such as DRC with a low phone penetration, mobile phone operators have a big role to play by spreading network connections across the country. For the formal financial sector to be able to capture the informal financial system, there is a need to formalise or convert the informal structures. The informal system models existing in many African countries must be understood by the formal sector for formalisation to be possible. For example, in DRC the financial players can use insights on how the unbanked can be attracted into the formal system by opening mobile money accounts and wavering some documents required. The provision of formal education where levels are low cannot be overemphasised in all countries.

What this study confirms is that there is a need to address low financial inclusion, and this should be looked at from the point of view of advocating robust policy formulation and implementation, as well as the evaluation of financial inclusion policies. An important role in policy issues is to help stakeholders understand the options and choices they have. This may include improving formal education standards and financial education and improving access to formal financial institutions by spearheading infrastructure development. This can be done by equipping the population with sufficient information through social networks assuming the technological infrastructures are in place. Whilst many existing studies use only supply data to determine factors impacting financial inclusion, this study analysed data from both the supply and demand sides.

Whilst the data used in the study covered the four selected countries, the FinScope Survey data have additional country data that can be used to extend the scope of this study. This will provide stakeholders with a more robust set of findings that can be used as a foundation for policy formulation in the continent. Information such as distance to the nearest formal financial institution or facility can give direction for financial institution penetration or services provision. Mobile phone usage, internet usage and social media penetration are indicators of the financial services or products that can be offered to improve inclusivity in countries such as DRC. The improved use of technology, social networks and smartphones coupled with higher education levels can improve inclusivity levels in South Africa and Eswatini.

However, the statistics themselves are not adequate for robust financial inclusion strategies, hence the need for research and other appropriate studies. The desire to address these shortcomings is one of the reasons for this study. The existence of low levels of financial inclusion in many reveals the magnitude of the problem that needs to be addressed.

The 2030 Agenda espouses that every person should enjoy the benefits of prosperity and minimum standards of living and well-being. This is captured in the 17 Sustainable Development Goals that advocate for all people globally to be free from poverty and hunger and to live healthy lives. The 2030 Agenda beseeches nations to create inclusive societies and provide access to education, modern energy and information (and technology). The Sustainable Development Goals are broad-based, which allows nations to promote initiatives that will contribute to the attainment of the 17 SDGs. This study contributes to ways in which the countries under study can make a meaningful contribution to the attainment of SDGs by ensuring financial inclusion for its citizens.

Future studies can focus on other factors such as religion on the demand side and corruption on the supply side.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.