Abstract

Is Afghanistan a lost frontier? A superficial look might conform to this notion, given the continued state of unrest and instability, rampant hunger, malnutrition, illiteracy and unemployment. In this reflective discourse, however, we highlight a brighter (largely overlooked) aspect: her mineral reserves, estimated at nearly USD 1 trillion, including some of the world’s richest lithium and rare earth elements (REEs), with high market value and critical for global climate combat policymaking (decarbonisation of infrastructure and attaining the net-zero target). By the same token, here, we offer a bird’s-eye view of the Afghan mineral wealth, with special emphasis on lithium and REE, which, if rightly harnessed, could be an engine of economic growth and national development. In its present state of operations, however, that future seems a distant myth as the Afghan mining/mineral sector is undermined by a web of interlocking systemic barriers, including (a) a totalitarian regime, (b) institutional bottlenecks, (c) a lack of social integration (human rights violation and neoliberal outlook) and (d) a lack of foreign investments. To that end, we reflect on the world experience of nations where mineral resources have become engines of economic growth and national development, which may inspire the present Afghan leadership. Rejuvenating the mining/mineral sector may help the leadership simultaneously advance towards multiple targets: (a) stabilising the economy, (b) meeting multiple UN Sustainable Goals, (c) helping mobilising nation- and peace-building efforts and (d) contributing to global climate action. Collectively, these may help redeem the lost reputation in the eyes of the international community and get rid of the economic sanctions. Here, we offer a vision to the present Afghan leadership to rejuvenate the mineral sector: (a) an enabling business environment (increased ease of business and security), (b) a unified water-power supply framework (hydropower development), (c) a participatory ecosystem (an integrated social-ecological-technological framework) and (d) restricting illicit mineral trade (enforcing rule of law and equity). To that end, we call for a data revolution to kickstart the systems’ thinking exercise (facilitating research, exploration and mineral processing).

Keywords

Introduction

Since the Taliban takeover of Kabul in August 2021, Afghanistan has entered a new era of authoritarian regimes, socio-religious upheaval and economic debacle. Afghanistan is already reckoned amongst the poorest nations in the world, scoring the lowest on the Human Development Index (HDI: 0.496) (UNDP, 2019), and its per capita GDP is estimated at $595. Since the new leadership assumed power, the international exchange rate of the Afghani (Afghan national currency) has hit the lowest in two decades (USD 1 = 1 Afghani) (TOI, 2021), while over half of the population is either unemployed or faces risks of livelihood loss and income depreciation in near future (AP, 2022). A third of the Afghan population lives below poverty line (<USD 2/day), while over half is liable to ‘becoming poor’ in near future (Amin, 2017). Moreover, the nation is plagued by hunger and malnutrition (Samim & Zhiquan, 2020). A survey conducted by the UN Food and Agricultural Organization (FAO) indicated that over 53% of the Afghan population is food insecure, while over 11 million are striving for various forms of international food aid (FAO, 2020; USDA, 2019).

Here, we raise a fundamental question—Is Afghanistan a Lost Frontier or the New Gateway—and develop this narrative as a plea to the present Afghan leadership to undertake a systems’ thinking exercise. It points to the Afghan mineral reserves, the production of which, experts believe, could set the nation on a course of unprecedented economic prosperity leading to sustainable human development (TRT World, 2021). Much of this, however, stems from the expeditions of the United States army in 2010, conducted in collaboration with the United States Geological Survey (USGS) and the Afghanistan Geological Survey (AGS), which estimated the economic worth of the Afghan mineral wealth at over USD 1 trillion (CNN, 2010). The USGS report came as an outcome of their continued exploration efforts since 2004, aided by maps prepared by erstwhile Soviet experts in the 1960s and 1970s. However, as the mineral assessment reports came towards the end of the last commodities’ super cycle in 2010, world experts believe that Afghan mineral wealth could be even greater, around USD 3 trillion. Such projections gain momentum with prices of copper and lithium prices soaring in the post-SARS-CoV-2 global economic slowdown (Reuter, 2021).

In view of the above, the aim of this reflective narrative is three-fold to (a) offer an overview of the Afghan mineral wealth, with special emphasis on lithium and rare earth elements (REEs), (b) highlight systemic flaws in the mining/mineral sector administration and (c) suggest means to rejuvenate the mining/mineral sector. It is largely because, despite holding immense potentials, the Afghan mineral sector only contributes to about 7%–10% of the national GDP (Pikulicka-Wilczewska, 2019). To that end, we point to the worldwide growth in demand for lithium and REEs, largely owing to the urgency of decarbonisation of existing energy infrastructure in the wake of climatic anomalies (Greim et al., 2020). Such a need was unambiguously stressed at the Conference of Parties in Parties in Paris (COP-15; Schellnhuber et al., 2016), and more recently at the COP-26 in Glasgow. 1 Considering the outstanding quantities required for the global energy transition, the availability of lithium has become a key agenda in many climate-change dialogues (World Bank, 2017). Lithium-ion batteries (LIBs) are deemed central to energy transition plans and pursuing the net-zero target (Bogdanov et al., 2019; Breyer et al., 2018; Connolly et al., 2016). Moreover, with the continuation of the Russia–Ukraine war and resultant energy poverty, we believe that the Afghan lithium and REE reserves could become an alternate and new energy bank for the world authorities.

We adopted a mixed-method approach—coupling literature review with contextual analyses of the Afghan mining/mineral systems’ operations. An underlining motto was to sound a call to the present Afghan leadership to switch focus from theology to one that welcomes liberalism, democracy, equity, modernity and technological innovation, which in turn may leverage peace and nation-building efforts. To the best of our knowledge, little work has been done in the recent past on this matter, and thus this narrative may even become a foundational document to propel future research and development in the mining/mineral sector.

Methodology

A ‘rapid review’ methodology was utilised, which closely follows the guidelines of the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) methodology, to scan various databases and collate information (Brooks et al., 2020; Naz & Chowdhury, 2021; Lal & Adair, 2014), using search phrases in a phased manner (Chaudhuri et al., 2020a):

Phase I: ‘mining’, ‘min*’, ‘mineral*’, ‘metal*’; ‘precious metal*, ‘gemstone*’ Phase II: ‘lithium’, ‘rare earth*’, ‘REE’, ‘renewable*’; ‘battery *’; electronic *’; ‘EV’; ‘clean*’; ‘green*’ Phase III: ‘water’; ‘power’; ‘hydropower’; ‘dam’; ‘climate*’; ‘transboundary’ Phase IV: ‘governance;’; ‘illegal’; ‘security’; ‘terror*’; ‘foreign invest*’ Phase V: various combination of the above.

The asterisk symbol (‘*’) was used as wildcard to expand the search horizon (Chaudhuri et al., 2021c). Document identification for this part was performed across various search engines, including SCOPUS, PubMed, ScienceDirect, Springer Lin, Blackwell, Social Sciences Citation Index, Web of Science, EconLit, JSTOR and complemented with Google Scholar. Retrieved documents were further screened to remove duplication (Chaudhuri et al., 2021a). After the removal of duplicates, content-based analysis was performed to streamline document search to the main research themes for ‘inclusion’ or ‘exclusion’ based on relevance to the current study.

Bird’s-Eye View of Mineral Deposits

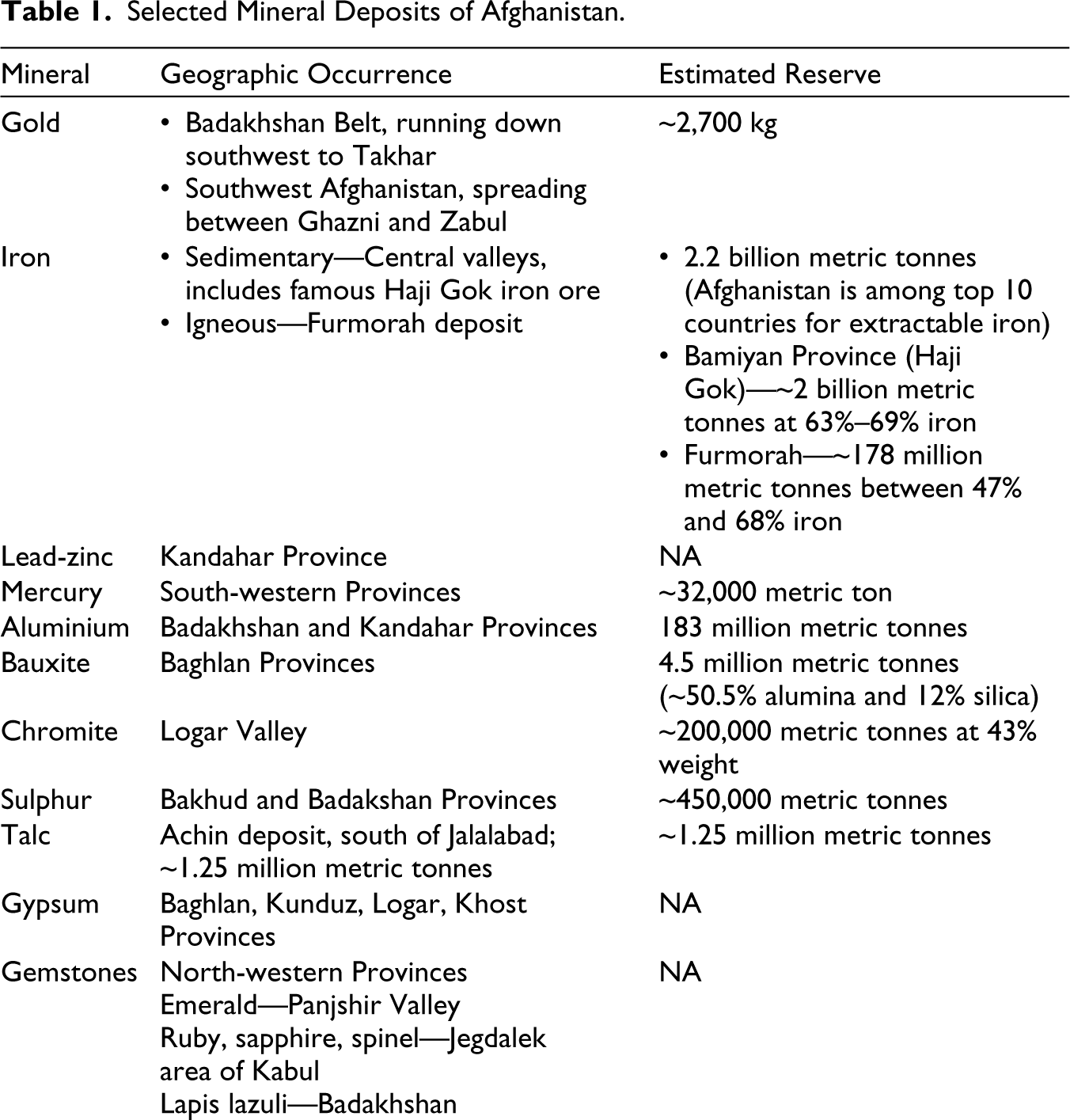

The Afghan mineral trove comprises a wide diversity of ores, ranging from iron to copper, mercury and rich lead-zinc assemblages to precious metals such as gold and various gemstones that have high market value (Table 1). Geologically, the mineral bodies primarily occur along two orogenic belts (Sediqi, 2011; Yigit, 2012):

Crescent extending from Herat in the far central-northwest of the country to Badakhshan region in the northeast corner; it primarily contains iron, gold (mainly in NE), copper, tin, tungsten and gemstones (mainly in NE). Extension of the Tethyan Metallogenic Belt, roughly spanning from Kabul to Kandahar, contains copper, gold, chromite, gemstones and molybdenum.

Selected Mineral Deposits of Afghanistan.

Afghanistan, reckoned among the global leaders of copper, holds about 30 million metric tonnes (12.3 million of known deposits + 16.9 million of probable reserves) (MoMP, 2019). In 2008, a consortium of Metallurgical Corporation of China (MCC) and Jiangxi Copper took on a 30-year lease for the largest copper project in the country, Mes Aynak (Reuters, 2021). Copper reserves at Mes Ayank are estimated at around 11.08 million metric tonnes, worth over USD 100 billion at London Metal Exchange prices (Reuters, 2021). Estimates of the USGS in 2010 total Afghan copper resources, for all known deposits, at about 57.7 million metric tonnes, valued at about USD 516 billion (Dinic, 2021). Besides copper, the Mes Ayank formations also contain significant riches of cobalt (601.5 metric tonnes), silver (7,670 metric tonnes) and molybdenum (~724,000 metric tonnes). There is a great wealth of gemstone reserves as well, occurring mostly along the north-east parts of the country, the Badakshan, Konar and Nuristan provinces. Emerald is mined in the Panjshir Valley, while ruby, sapphire and spinel are mined in the Jegdalak area of Kabul province, to name a few.

Lithium and REEs

Lithium

Widely touted as the ‘oil of twenty-first century’, globally, lithium is mostly mined in the so-called ‘Lithium Triangle countries’ in South America (Bolivia, Argentina and Chile), followed by the USA, Australia and China. Lithium ores in Afghanistan were first discovered by former Soviet mining experts in the 1980s. However, it was kept secret until 2004, and only came to light when a team of US geologists stumbled upon a collection of old diagrams and data at the Geological Survey of Afghanistan in Kabul. Lithium deposits mainly occur in the Nuristan Province, as veins, within hard rock formations (Montgomery, 2021).

Demands for lithium have skyrocketed in the global manufacturing market over the past few years due to a wide range of applications—ranging from rechargeable batteries for electric and hybrid cars to electric car motors, advanced ceramics, computers, wind turbines, catalysts in cars and oil refineries, monitors, televisions, lighting, lasers, fibre optics, superconductors and glass polishing, to name a few (Bensaid, 2020). It is as Elif Nuroglu, the head of economics at Turkish-German University (TAU), maintained: ‘Lithium, like oil, is rapidly becoming a strategic product. Lithium can be used as a weapon, because in the future it will be used in many fields, from car manufacturing to robots and car machines’ (Khalid, 2021).

In the early months of 2021, lithium prices jumped by about 88% (Mining.com, 2021), which could even triple by the end of the current decade as demand growth for electric vehicles (EVs) outpaces the supply of the metal (Fawthrop, 2021). Analysis from Rystad Energy estimates a ‘serious’ shortage in lithium supply worldwide by 2027 unless short-term investment into new mining capacity accelerates (Fawthrop, 2021). Their estimates indicate that globally, the equivalent of 3.3 million EVs could face delayed production due to the lithium supply shortage, rising to nine million EVs by 2028 and 20 million by the end of the decade. As hunt for renewables increases in the coming years, so does the demand for raw materials to build global clean energy infrastructure development and, thus, Afghanistan’s opportunity to become a supplier state. Under the circumstances, establishing a commercial production chain for lithium will benefit Afghanistan on many accounts. 2 An internal US Department of Defence memo branded Afghanistan as ‘the Saudi Arabia of lithium’, based on Afghanistan’s power to leverage the global lithium trade (Reuters, 2010).

Lithium is the backbone of rechargeable batteries used in EVs (Chen et al., 2019), widespread adoption of which is advocated worldwide as a prime means to combat climate change—decarbonisation of infrastructure and advance towards net-zero emission targets (USTIC, 2020). In regions where solar and wind power sources are uncertain/unstable, lithium is expected to a play critical role in building renewable power infrastructure. LIBs are presently being tested worldwide as a viable option to augment solar power storage in the long run (Jenu et al., 2020), which will further help the global authorities to move to clean power infrastructure and meeting the Paris and Glasgow pledges. With global EV production projected to increase from 3.4 million vehicles in 2020 to 12.7 million by 2024, the sustainable supply of lithium will be a key determinant in global initiatives to move away from fossil fuel, adopt green energy technology and act upon the Paris and Glasgow pledges (Fawthrop, 2020). According to analysis firm GlobalData, lithium demand will grow at a compound annual growth rate of 25.5% over coming years, rising from 47.3 kilotonnes (kt) to 117.4 kt. Two key factors drive the increase in lithium demand: The first is declining cost over time. During the last 5–10 years, tremendous reductions have resulted in the price of LIB packs falling to 300 USD/kWh in 2014 (Greim et al., 2020; Nykvist & Nilsson, 2015) and 176 USD/kWh by the end of 2018. Second, there is the influence of an experience curve. Cost improvements of 16% ± 4% per doubling of historic cumulated capacity lead to about 150 USD/kWh at 1 TWhcap (Schmidt et al., 2017) for battery packs. In terms of time, fast learning might enable 124 USD/kWh by 2020 (Kittner et al., 2017).

Rare Earth Elements

More recent reports of the MoMP (2019) indicated potential occurrence of about 1.4 million metric tonnes of REEs across Afghanistan, of which the Khandeshi deposit in southern Afghanistan is most notable. The Helmand province contains the richest deposits of light rare earth elements (LREEs), including lanthanum, cerium, praseodymium and neodymium. The latter two are in high demand in the international mineral market—going over at a rate of $45,000 per metric tonnes (Montgomery, 2021)—with applications in multiple high-tech manufacturing design. Afghanistan can become a major supplier state for REEs, as the USA, Japan and Europe presently aim to cut back on their dependency on China for REEs (Dinic, 2021; Khalid, 2021). Growing demand for REEs in the modern defence systems’ manufacturing and telecommunication industry may contribute to the inflow of foreign capital, which in turn, may help the present leadership plan and undertake innovative social welfare schemes and create of new job markets.

Nation-Building and Global Action?

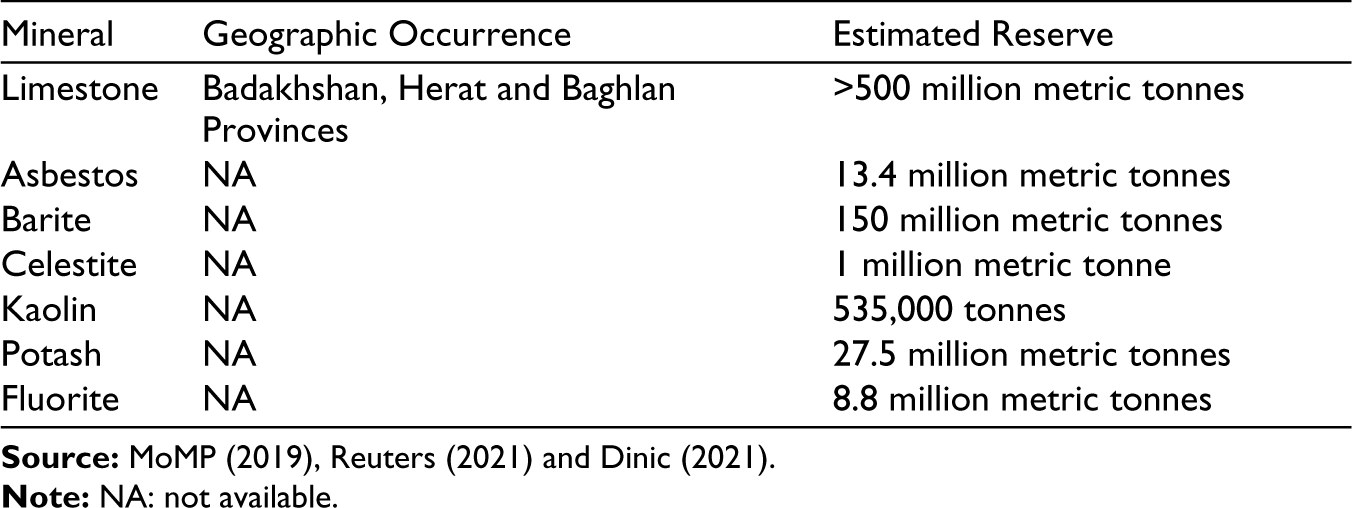

According to a recent estimate of the Observatory of Economic Complexity, an economic watchdog, nearly 50% of all Afghan national exports in 2019 (~USD 2.24 billion) comprised various minerals (Table 2; OED, 2019). It means, harnessing the Afghan mineral power in a strategic fashion may prompt capital formation, invite investments, and create new job markets. In turn, it may trigger innovation and modernization of the economy. In 2017, projected annual revenue from the Afghan mining sector was set at USD 1 billion per annum, with the promise of creating at least 8,500 direct and more than 30,000 indirect jobs (Amin, 2017). Such a billion-dollar prospect hinged on the just two mines: the Mes Aynak copper mine ($350 million) and the Hajigak iron mine ($550 million), with an additional USD 150 million revenue projected from hydrocarbons and gemstones.

Approximate Total Afghan Export of Goods in 2019.

However, a major boost to the national economy can come from commercialising the mining sector around lithium and REE reserves, mainly owing to soaring demand in the international market. As climatic aberrations (extreme weather events, droughts and floods) become more apparent worldwide, they impact Afghan lives and livelihoods as well (Central Statistics Organization, 2016; Islamic Republic of Afghanistan, 2015; NEPA, 2013; Singh et al., 2011). With worldwide growing demand for cleaner technologies, streamlining lithium and REEs production can yield several benefits for Afghanistan and the rest of the world:

Increasing flow of foreign capital/investment in the mining sector that could be strategically routed to various development spheres (food and nutrition, education, healthcare and creation of new livelihood opportunities). This in turn may help Afghanistan make significant progress towards several UN Sustainable Goals (SDGs), possibly leading to the initiation of nationwide mass social welfare programmes. Such economic growth and a sense of social well-being, may foster greater political stability in the nation and may inherently help the new leadership tame down violence and insurgency. Such events might even leverage the peace-building efforts currently ongoing in South Asia (a major driver of economic sanctions currently imposed by the western world). Help Afghanistan become a supplier state for raw materials for building rechargeable batteries (lithium and REEs). Help the world act upon the Paris (COP-15) and Glasgow (COP-26) pledges of moving away from fossil fuels to cleaner/greener infrastructure and production protocols.

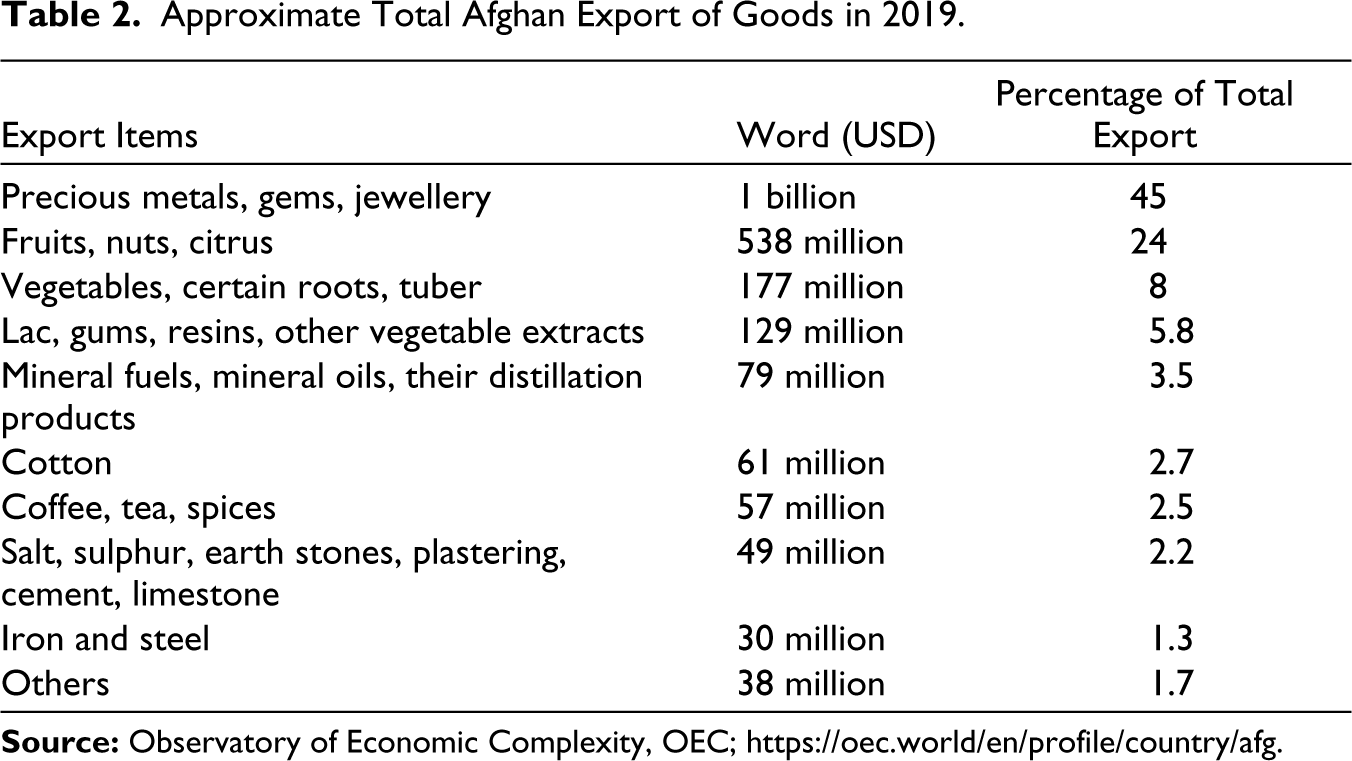

In this regard, the present Afghan leadership may draw inspiration from contemporary world experiences, which suggest that strategic exploration of the mineral treasure alone can prompt widespread economic growth, which in turn may be channelised to finance a variety of social welfare schemes. In Guinea, Zambia, Botswana, Sierra Leone and Namibia, revenues from mineral exports accounted for over 60% of total national revenue (Figure 1). In several of these countries, the annual GDP growth rate multiplied over a short span (1990s–2000s). For these nations, the mineral industry has done more than just kick-starting the economy, as Sediqi (2011) observed: ‘…many of these countries …. see it as the engine of sustainable development. This means no more mining enclaves, but a sector that stimulates linkages to other activities and has strong multiplier effects on the economy, as a large percentage of the income generated in the sector is spent domestically’.

Mining Operations: Systemic Barriers

Since transportation of lithium from Latin America is uneconomical, Afghanistan potentially opens an alternate source (Gilani, 2021). Experts believe that the lithium reserves of Afghanistan may even outshine those of Bolivia (around 21 million metric tonnes) (Patonia, 2021; SIGAR, 2018), which opens the path to prosperity and, for the present Afghan leadership, an in-house means to lift millions out of poverty and unemployment, malnutrition and hunger. Saeed Mirzad, a member of the USGS observed: ‘If Afghanistan reaches peace and stability for a few years and develops its mineral resources, it could become one of the richest countries in the region in a decade’ (Khalid, 2021). However, the first impediments to ‘commercialise’ the Afghan lithium production are the lack of adequate knowledge about the current distribution of ore bodies (horizontal and vertical dimensions), the lack of recent estimates about tonnage and the lack of economic valuation. Moreover, a commercial production chain for lithium takes between 10 and 15 years and is a highly financial and infrastructure-intensive operation, underscoring the need for foreign capital. In the following sections, we highlight the major factors that undermine lithium production and the mining/mineral sector as a whole.

A Totaliterian Regime

What plagues the Afghan mineral (like all other goods and services) sector at root is the continued state of insurgency, terrorism and violence, culminating in violation of human and public property rights, gender discrimination and socio-political-religious persecution. The regime under the new leadership is one of utter intolerance of opposing views/beliefs/practices. On top of that, there is ideological conservatisms—no room for constructive criticism or dialogue, which makes it fundamentally difficult to propose/adopt modern mining methods to streamline production. Such conditions, depict a typical totalitarian outlook that tends to control the flows of capital around the mineral (as all other natural) resources with an iron fist, lacking democratic systems’ approach. Such demeanour shuns the possibilities of foreign and/or private investments in the mining/mineral sector, disincentivising and disengaging all stakeholders, thus curtailing and impeding mineral exploration and production. Added to the above, the worldview of the present Afghan leadership is far from being climate sensitive. By the same token, there is no eagerness (and/or preparedness) to join hands with the international community to combat climate change. In the following sections, we ponder over the main systemic barriers 3 that shroud the Afghan mining/mineral sector, lowering its productivity, despite having rich promises for economic growth and sustainable human development.

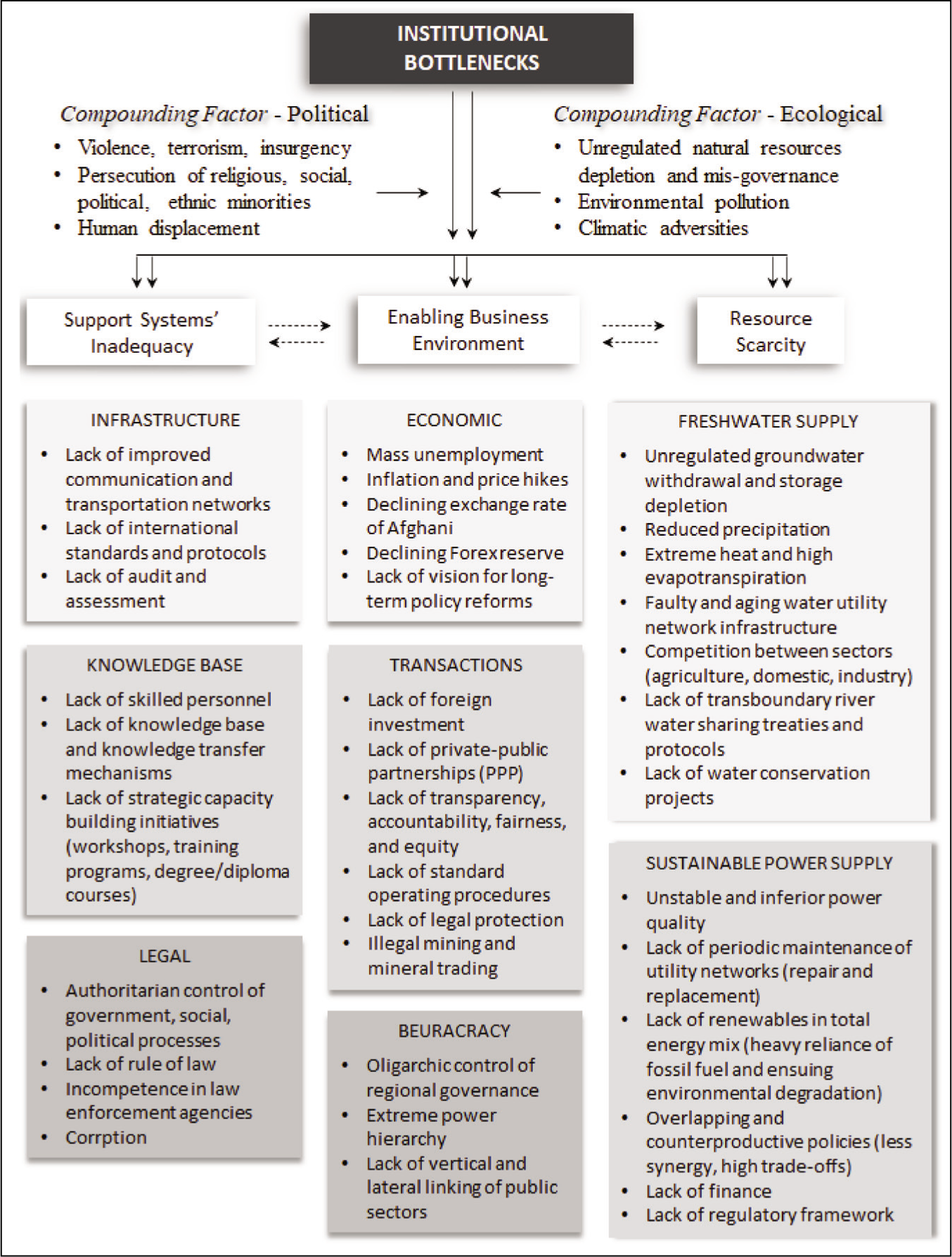

Institutional Bottlenecks (Production Systems’ Incapacities and Failures)

The mining/mineral sector is undermined by a confluence of systemic flaws ranging from support systems’ inadequacy to a lack of an enabling environment, and resource scarcity that collectively affects production (Figure 2). Mining operations are yet in an artisanal form, lacking modern infrastructure and machinery with little or no standard operating protocols (SOPs). What seems alarming is, there appears little willingness (or vision) in the present leadership to organize a functional institutional network (e.g. agencies, resources, collaborations, research modules) around mining operations to facilitate technological innovation and infrastructural modernization. Alongside, there is the appalling lack of a functional legal system and methods of law enforcement (totalitarian control) that undermine the ‘credibility’ of the entire mining/mineral operations sphere. Under these circumstances, commercial production for lithium and REEs is difficult, if not impossible. For example, lithium production (exploration, mining and processing) is a time-intensive proposition. It is believed that commercial production of lithium may take around 10–15 years. Capital required to sustain such long-term operations is difficult, given the present economic crises in Afghanistan and requires a steady flow of foreign investment. In addition, exporting minerals from Afghanistan, a landlocked country with limited modern transport (railways and road networks), and lacking modern power infrastructure, is difficult (Pikulicka-Wilczewska, 2019). Moreover, the transport networks outside urban hubs, are unsafe being mostly controlled by local warlords and militia, fraught with dangers of looting. Last but not least, the bulk of the lithium and REE information dates back to the Soviet era. Without more recent data, there remains uncertainty regarding the exact locations of ore bodies, their dimensions, feasibility of extraction and economic worth, which eventually deters foreign investment.

Simplified Schematic of Institutional Shortcomings That Might Shroud Productivity in the Afghan Mineral Sector. Points of Caution for the New Leadership Are That Socio-Political Instability and Ecological Disasters May Compound Any Solutions Proposed for Mining Operations in Years Ahead.

Illegal Mining and Mineral Trading: The Hurdle to Revenue Generation

A prime hindrance to harnessing revenue generation from the mining sector is rampant illicit mining and mineral trading. In its latest National Human Development Report on mineral extraction in Afghanistan, the UN Development Programme indicated that the nation could have collected over $100 million from minerals in royalties and export duties alone on a yearly basis (Saif, 2020). The report said lucrative large-scale mining sites operate on an industrial scale and openly transport bulk minerals on large trucks along major roads and across the border to Pakistan. On average, the government loses about USD 300 million in revenue from the mining sector due to illegal trade (Pikulicka-Wilczewska, 2019). Most of the gemstones mined in Afghanistan leave the country illicitly, 90%–95% of them ending up in Peshawar, Pakistan, where they are sorted for quality (MoMP, 2019). To describe the graveness of the issues, Byrd and Noorani (2017) termed mineral looting in Afghanistan as ‘industrial scale’. In a report to the United States Institute of Peace (UNIP), the researchers maintained, ‘The rampant extraction and export of minerals likely amounts to well into the hundreds of millions of dollars per year, but government revenues from the country’s mineral resources have been very small, with royalties accruing to the MoMP amounting to only Afs 1.1 billion ($16 million) in 2016’. Such conditions stem from the fallacies in the legal systems’ functioning in the country, and lack of power of the judiciary and law enforcement agencies.

Lack of Social Integration (Building and Mainstreaming Skilled Workforce)

Discrimination and Corruption: Lack of an ‘Inclusive’ Vision

The importance of the vast societal dimension around mineral production is barely considered. By the same token, local expectations, apprehensions and sentiments are seldom taken into account while setting production targets and operational guidelines. This disincentivises the mine workers. Moreover, in an oligarchic setting, mining protocols (whatever there is) have little regard for basic human rights, marked by (a) decrepit working conditions, (b) lack of training, (c) absence of health safety measures, (d) low and arbitrary wage structure, (e) no worker benefits and (f) extended working hours, to name a few.

Moreover, being mostly contract labourers, there is no job security for the mine workers, which disengages them from offering the best. Workers are largely selected and/or offered better wages along religious-ethnic lines, manifesting discriminatory behaviour. Child labour is rampant, with bare minimum recognition for the women. Regarding the latter, there has been little concerted effort for gender mainstreaming and integrating women in the mining workforce. Little or no efforts are made for local skill development. Governmental oversights about mining operations are rare, practically non-existent, and even then, shrouded by corruption—overseeing officials are bribed to evade penalties. All these lead to a lack of credibility in mining/mineral exploration, which, in turn, erodes investors’ confidence.

Neoliberal Outlook: Profiteering Without Accounting

The above is a classic example of neoliberal approach to harnessing natural capital, where the emphasis is on economic returns with little concern for:

Eco-environmental sustainability Socio-cultural identity/rights.

For the first, mining operations are inherently water-intensive processes, which, in the arid to semi-arid landscapes of Afghanistan, threaten native livelihoods (farming, livestock herding). Lithium mining could generate extreme hydric stress and disrupt/damage natural hydrologic cycle, especially in regions where the availability of freshwater is low (Liu and Agusdinata, 2020). Studies have indicated potential risks of evaporative enrichment of salts, impairing land-water quality (Bian et al., 2017), which, in turn, further downscales farming and livestock production (livelihood and income loss). Lithium extraction and resultant hydric stress collectively impact local biodiversity (Guiterrez et al., 2022) and elevate daytime temperature (Liu et al., 2019). The use of primitive and mostly artisanal mining methods further endangers environmental quality. All these multiply the perils of climatic adversities/losses, which in a vicious cycle further aggravate mining conditions. However, in a neoliberal approach, little value is associated with these issues, where the prime focus lies on profit maximisation.

Regarding the latter, mines are often located within natural conservation areas, biodiversity hot spots and protection sites or territories claimed by indigenous communities. Such lands hold a great deal of social, cultural, spiritual, ecological and ethnic value for the native inhabitants (Dunlap and Riquito, 2023), but are frequently overlooked while dealing out the mining permits/contracts. Moreover, under a neoliberal outlook, native communities are rarely consulted with for site selection and/or waste disposal. In addition, little effort is made to relocate and rehabilitate the native population displaced due to mining and/or compensate for the lands they have been dwelling on for generations and considered home. This equates to identity theft. As a consequence, local communities are disincentivised, and, on many occasions, have opposed mining operations.

Foreign Investment

The combined effect of the preceding sections (‘A Totaliterian Regime’ and ‘Lack of Social Integration’) is a hit on foreign investment, which is deemed critical to remodel and rejuvenate the mining/mineral sector. The global benchmarking on the ‘ease of doing business’ by the World Bank in 2019 ranked Afghanistan 173rd out of 190 countries ( Starting a business: 52nd (out of 190 countries) Dealing with construction permits (183/190 countries) Getting electricity (173/190) Registering property (186/190) Getting credit (104/190) Protecting minority investors (140/190) Paying taxes (178/190) Trading across borders (177/190) Enforcing contracts (181/190) Resolving insolvencies (76/190)

While continued political instability, insurgent activities and extreme discriminatory behaviour of the present leadership (just like its predecessors) are frequently cited as prime causes of lack of foreign investment in Afghanistan, others include (a) extreme antipathy for foreign involvement (stemming from a long history of invasion and occupation), (b) stark rejection of international ideas and standards, (c) lack of transparent SOPs to encourage foreign direct investment (FDI) and/or foreign portfolio investment (FPI) and/or foreign institution investment (FII); (d) oligarchic control of business tendering and (e) lack of legal protection for investors (Noorani, 2015). Other issues include (a) currency devaluation, (b) depleting Forex reserves, (c) soaring inflation, (d) stock market instability, (e) low GDP growth (negative most often) and (f) lack of forward-thinking economic policymaking. Collectively, the above portrays the grim reality of the Afghan business sphere and explains foreign investors’ apprehensions about getting involved in Afghan mineral exploration/trading.

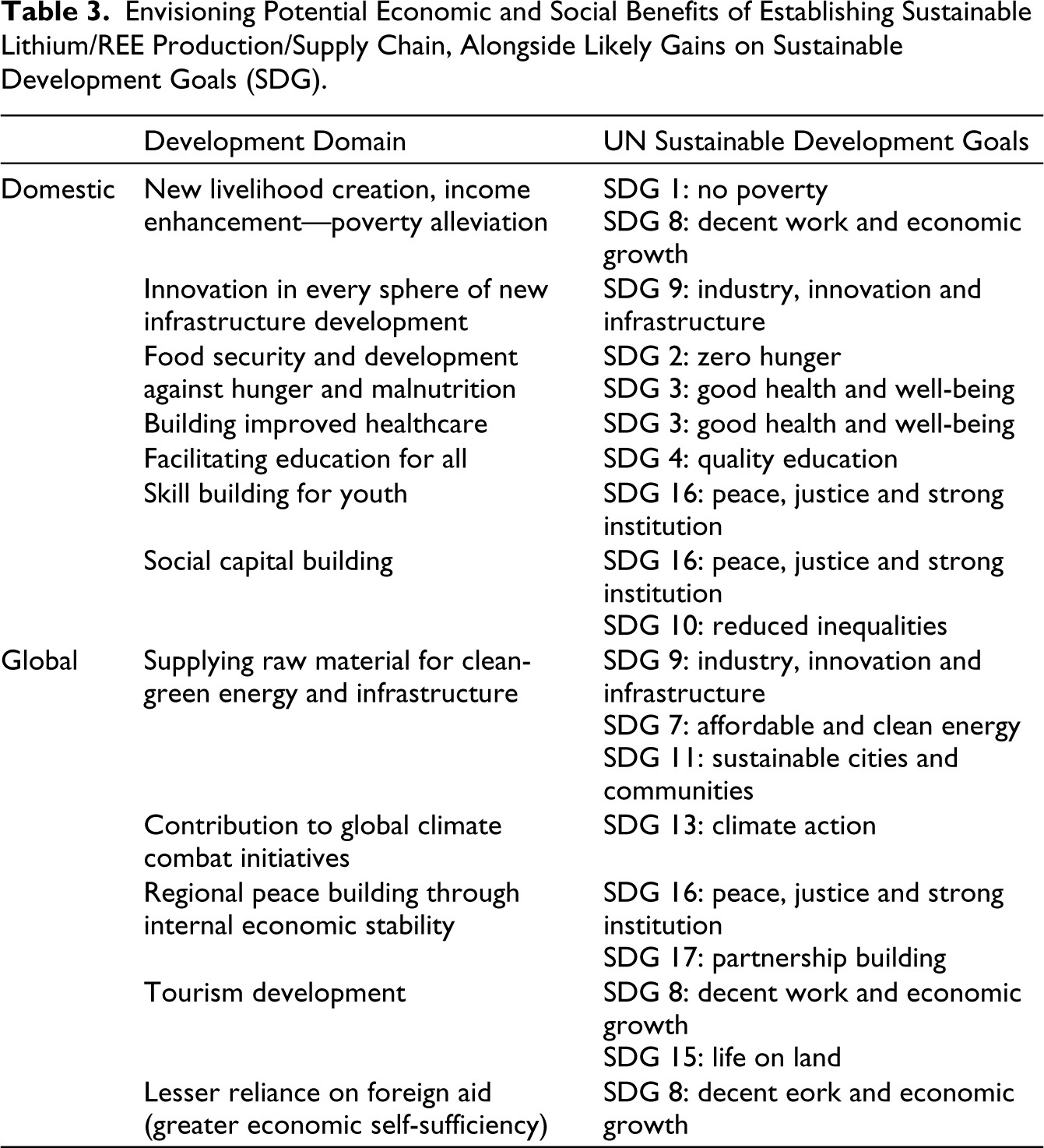

A Systems Thinking Exercise—Transformative Vision

Given the state of violence, inequity, oppression and persecution in the present Afghan regime, a call to restructuring and revamping the mineral sector might sound ambitious. However, conscious deliberation on the matter may also lead, besides many other things, to making major advancements towards multiple UN Sustainable Development Goals (SDGs; Table 3), which could redeem the reputation of the present leadership in the eyes of the world, and thus help get rid of multiple economic sanctions imposed by western nations. In turn, this may brighten the chances of foreign (and private) investments, leading to the creation of new job markets. As added benefit, an increased flow of foreign capital may even transform the age-old image of Afghanistan from a typically foreign aid-dependent economy to one that is more self-reliant and trade-oriented (Gilani, 2021). In the following sections, we invite the present leadership to ponder the core areas of systems’ administration, focusing on which may lift the mineral sector from grips of uncertainty, inconsistency, corruption and production failures.

Envisioning Potential Economic and Social Benefits of Establishing Sustainable Lithium/REE Production/Supply Chain, Alongside Likely Gains on Sustainable Development Goals (SDG).

Youth Development and Women’s Engagement—Change from Within?

We believe that a potential strategy might be for the international community to find ways to mobilise the Afghan youth—helping them organise mass movements to demand more economic (and social–political–religious) freedom, alongside forward-thinking reforms in the mining/mineral sector. As the youth are more likely to be willing to experiment with newer thoughts/ideas, more open-minded to different worldviews, especially those that promise better livelihoods and living standards, their empowerment and involvement could become an engine of change, marking the beginning of a new era in Afghanistan. The youth brigade can even demand increased democratisation and liberalisation of the national economic policies to welcome foreign and private investment that would see a new flow of capital, which, in turn, would create newer livelihood opportunities. However, these issues fall out of the purview of the current work, which requires more contextual research. However, we also expect that the present Afghan leadership will take note of the broad strategies listed in the following sections to chart out the best course of action.

An Enabling Business Environment?

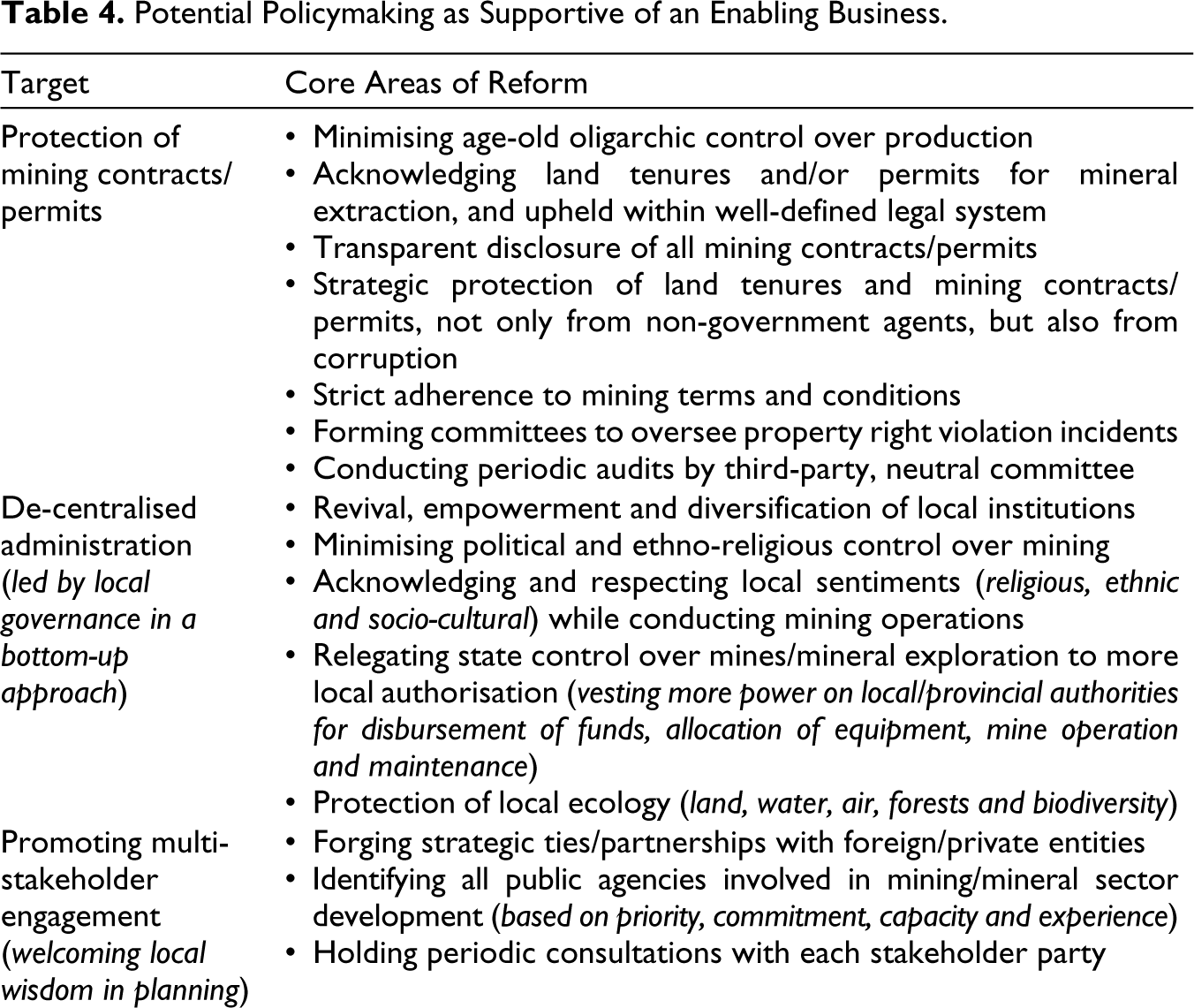

The prime focus to rejuvenate the mining/mineral sector should be identifying means to attract foreign capital. However, decades of war, terrorism, persecution, political instability and foreign occupation have grown a sense of deep apathy for foreigners, which makes the task difficult. While considering structural reforms, the main idea will be to change that attitude towards foreigners while realising the need for external support (finance, infrastructure, technology and training). An implicit motive should be to gain the confidence of foreign investors, portraying Afghanistan as a safe home for start-ups and entrepreneurships.

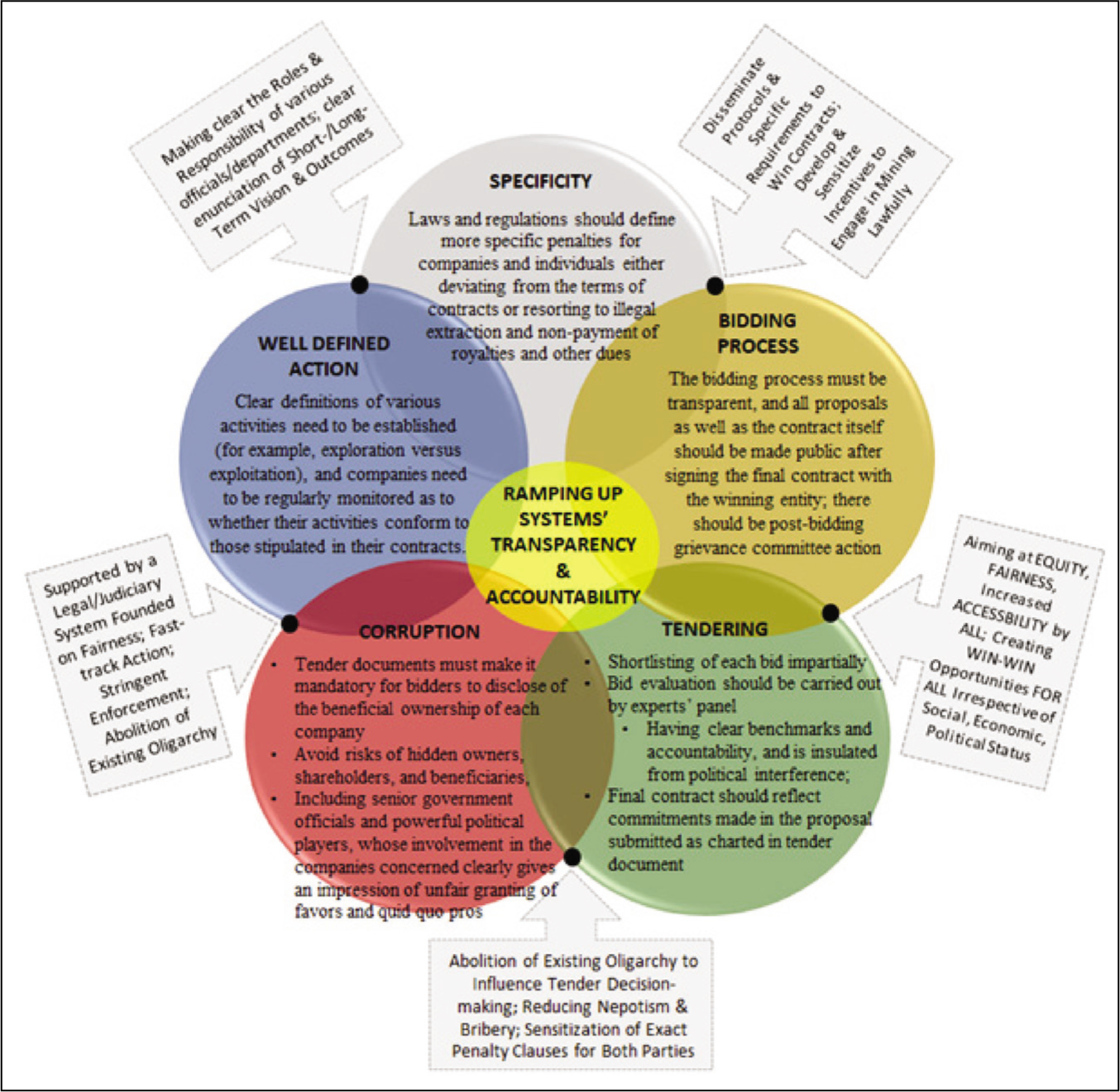

Here, we draw attention to certain key interventions that may kickstart the process (Table 4). The governing idea should be to ensure transparency and accountability in all spheres of mining operations, with clear articulation of SOPs—legally grounded and at par with international standards. At the same time, penalties for not complying with norms should also be mentioned clearly, backed by an impartial system of judiciary and law enforcement to address transgressions. Moreover, paperwork processing for mining permits and/or any financial support (loans, subsidies, tax breaks) should be fast-tracked. However, building transparency and a corruption-free system is a time-consuming process, requiring patience and strategic interventions over the years (Figure 3; Noorani, 2015).

Potential Policymaking as Supportive of an Enabling Business.

Prime Areas of Policy Focus to Increase Transparency and Accountability in the Mining Sector, So as to Develop Corruption-Free Business Environment.

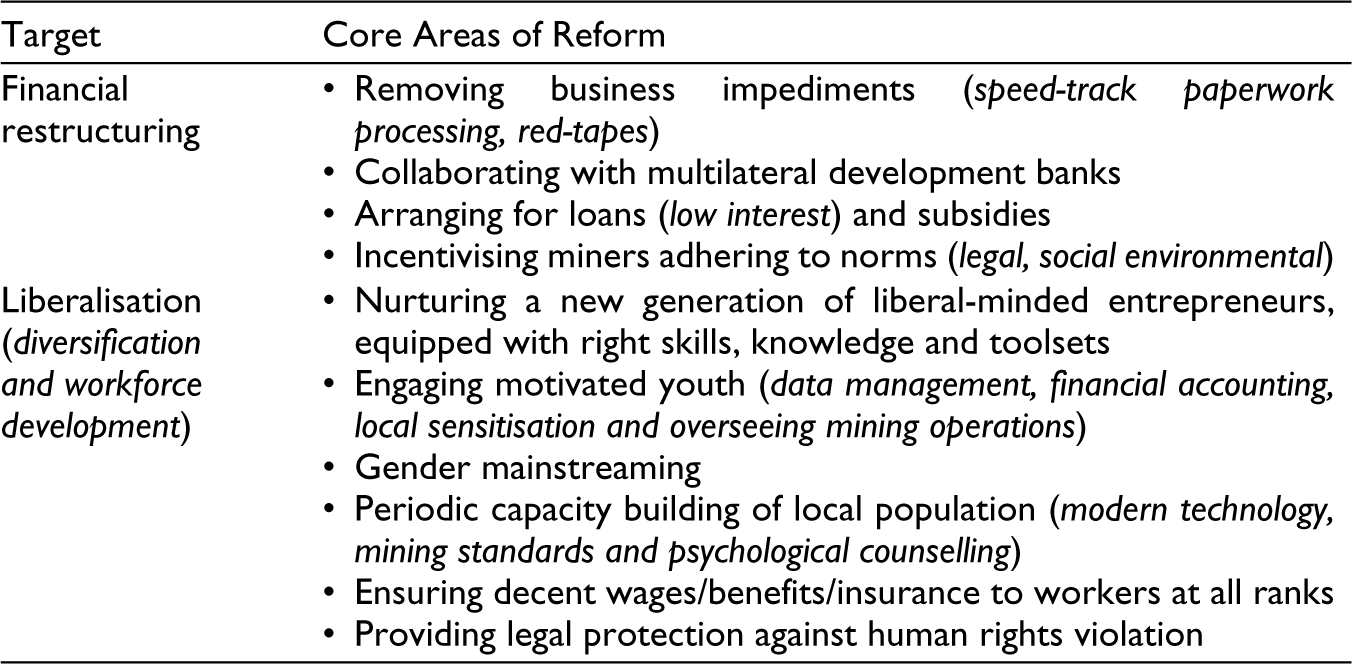

Additional areas of focus could include:

Improved mineral processing and transportation network. Latest technology support system (information generation and dissemination). International environmental standards (conservation and nature protection).

Harnessing Water and Power: A Unified Vision?

Mining operations are water- and power-intensive. The latter is quintessential for sustainable production of lithium and REEs, which should be of sufficient quality (uninterrupted power, minimal voltage fluctuation). However, as Amin (2017a) pointed out, the Afghan energy sector is pitted by myriad technical, financial and institutional constraints, including:

Lack of renewables in the existing energy mix (still heavily reliant on fossil fuel), which means a great deal of logistics—finance, technological upgradation—and, at root, recognising the need and willingness to harness a change. Minimal or no international partnerships and ties. However, with the current worldview of the present Afghan leadership, which detests foreigners and thus any international involvement, this could be a daunting task. Overlaps, contradiction and ambiguities in policies of various public sectors and ministries (lack of multi-sector dialogues). Negligible capacity building at grassroots to train and equip power workers/officials with modern technologies and procedures. Lack of regulatory framework and time-bound power generation targets.

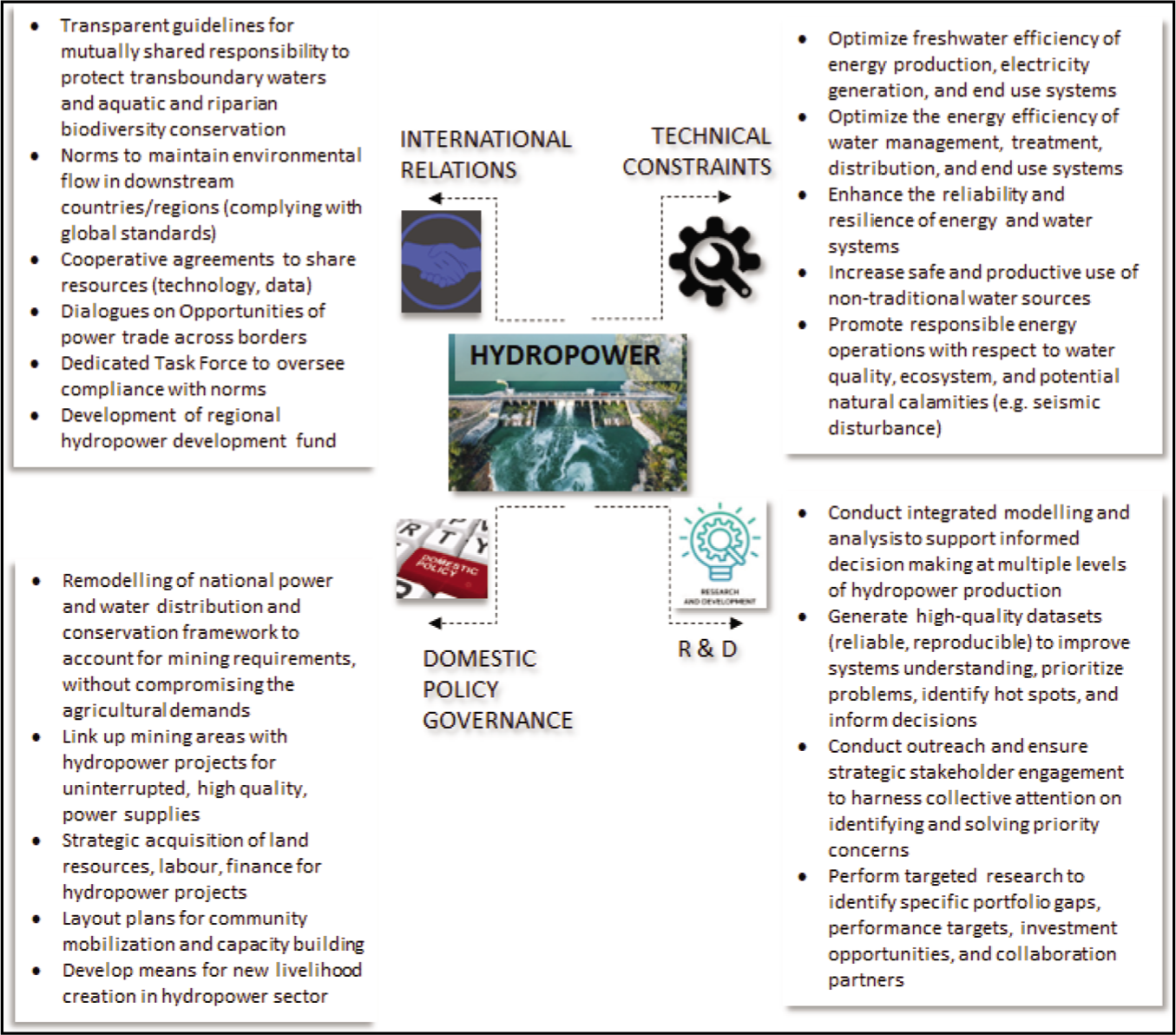

To rejuvenate the mining/mineral sector, we recommend a vision for a unified, harmonised and coordinated development agenda by strategically pulling in all partner institutions while prioritising funds/resources/personnel. Rivers such as Kabul, Helmand, Amu, Panj River, Farah and Murghab River occur in ideal topographic and geomorphologic settings to initiate hydropower utility projects.

Essentially, to augment power supply services to feed the mining/mineral sector, we urge the present Afghan leadership to realise the interconnected dimensions of water and power and the need to view both within a unified systems’ framework rather than standalone domains. For Afghanistan, this could mean increased research and innovation to build hydropower facilities (Figure 4). However, to advance towards such targets, the new leadership should think of building a multidimensional ecosystem of actors and agencies (multistakeholder platform) that could meaningfully contribute to the development of hydropower systems on various river reaches. Moreover, it would require extensive data and information from various environmental, economic and social spheres to accurately assess the systems’ requirements and potential outcomes (benefits vs. losses).

Key Domains of Hydropower Development in Afghanistan, as Future Vision for Co-Management of Water and Electricity Within a Unified Framework of Systems’ Governance.

However, the Afghan leadership should also be aware of unwarranted outcomes of hydropower development, such as reduction in environmental flow (threats to aquatic biodiversity, fisheries, irrigation, municipal supplies and recreational uses) coupled with social discontents (displacement of native population) and environmental consequences (deforestation and land degradation). Another critical consideration should be the assessment of future impacts of climatic anomalies on the fluvial systems (reduction of streamflow, surface runoff and, droughts) to build sustainable hydropower plants. To ward off such mishaps, we recommend a full-scale SWOT (strength, weakness, opportunity and threat) analysis around hydropower development. However, the fundamental requirements for this include (a) a multistakeholder ecosystem (actors and agencies from different spheres) and (b) data and models to simulate a range of what-if scenarios.

But thinking in such lines, first and foremost, we expect the Leadership to realize the importance of harnessing bonds with various research and financial organizations, in-house and abroad; collaborate with the experts in various fields; and forge multilateral ties with international authorities for tools and techniques. However, that being said, we also believe that the main barrier to treading such a path is the environment of conservatism and distrust for foreigners in the current regime, just like its predecessor, that may shun the inflow of newer ideas.

Forging a Multidimensional Ecosystem

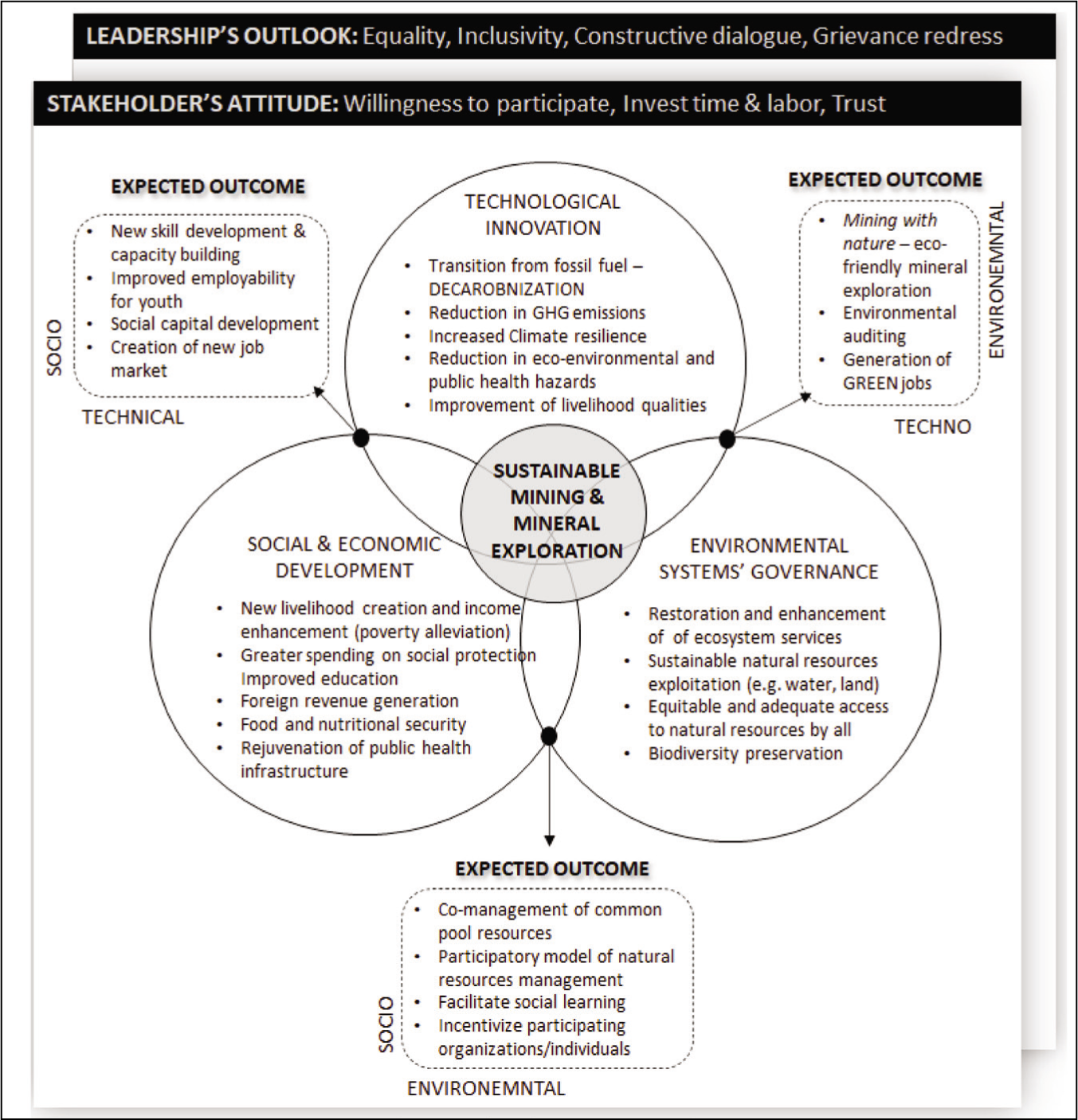

Mining/mineral exploration is multifaceted task that demands involvement of actors from multiple agencies. To that end, we believe that much of the success hinges upon how well the new leadership melds different spheres of development: (a) social and economic, (b) technological innovation and (c) environmental systems’ governance (Figure 5). The idea is to imagine an inclusive system’s governance, founded on an ecosystem of stakeholders, within a sphere of participatory action (Chaudhuri et al., 2020, 2023, 2024, 2021b). Potential stakeholders may include (but are not limited to), the public agencies, development organisations, financial institutions, think tanks, research groups, NGOs, intergovernmental organisations, universities/technical education centres/research organisations, UN offices and any other that could potentially help develop sound mining/mineral exploration protocols.

Envisioning Afghan Mining Sector by Through an Integrative Lens of Socio-Economic, Environmental and Technological Spheres of Development. It Also Depicts Expected Outcomes at the Intersections of Each Sphere (Socio-Technical, Techno-Environmental and Socio-Environmental.

The process should begin with understanding, respecting and strategically aligning the priorities and expectations of various stakeholders to harness synergies in action. However, the leadership should be cognisant of two critical issues: (a) role of local government bodies at each stage of stakeholder engagement and (b) effective interaction mechanisms among the stakeholders (minimise conflict to ensure cooperation and high productivity). A prime game changer could be the mobilisation of the local population. In this regard, certain strategies may prove influential:

Sensitising local population about tangible outcomes (long-term economic benefits). Incorporating local wisdom at each phase of mining planning and development (from site selection to the choice of mining techniques and technology). Empowering local population (with tools and knowledge) to contribute meaningfully to mining planning and development. Building an ambience of mutual trust and interdependency. Developing transparent grievance redress mechanisms.

Restraining Illegal Mining and Trading

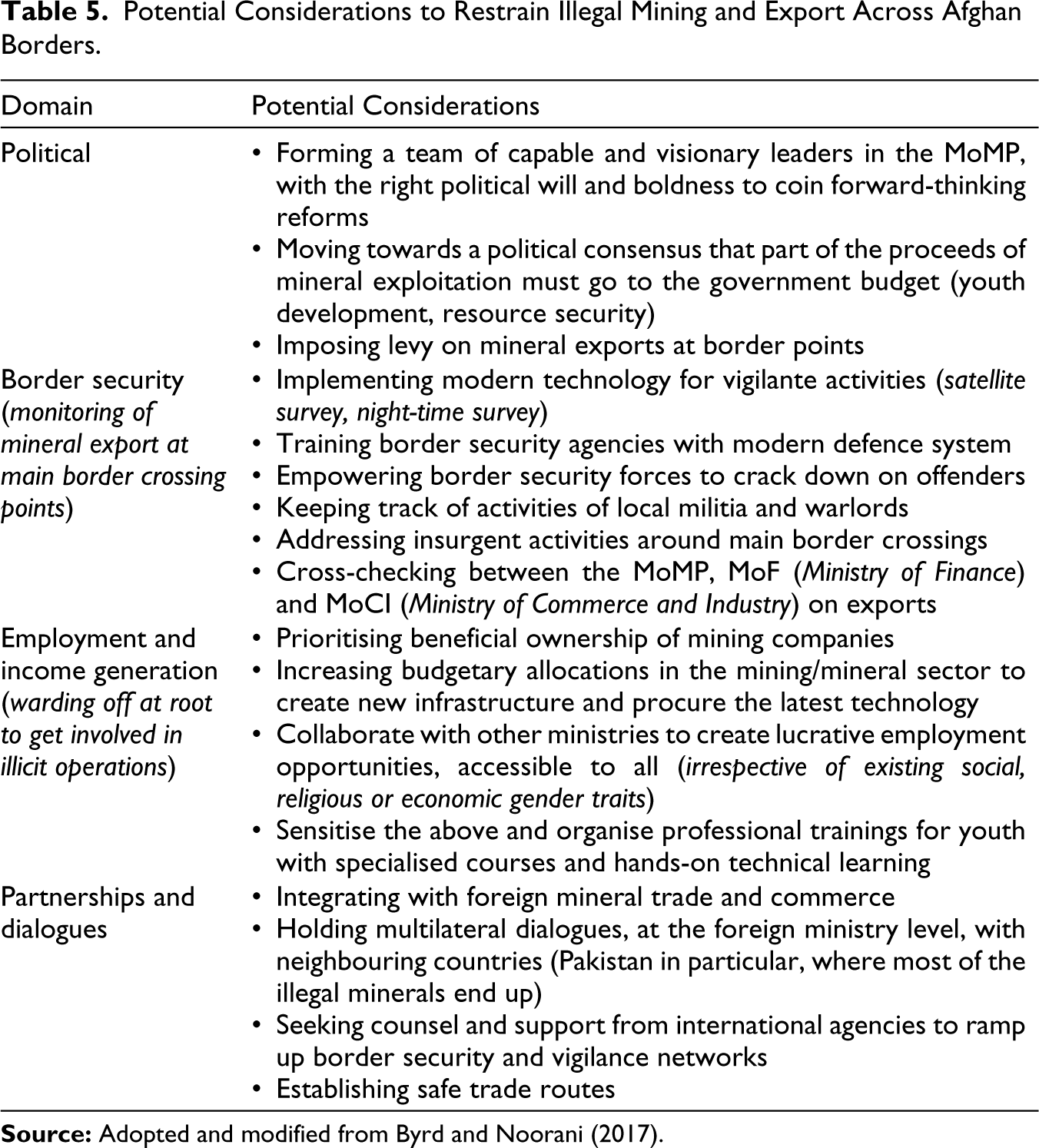

Leashing down illegal mineral trade should be a priority for the new leadership to create an enabling business environment and earn the confidence of foreign investors. Although there is no one-size-fits-all solution to restrict (downscale?) illegal operations in the mining sector, their report to the UNIP has put forth certain recommendations that could be worth considering for future (Table 5). The leadership should realise earning from that illegal mineral trade feeds insurgency, violence and conflict, especially in the northern and eastern provinces where local factions relentlessly compete for territorial control, which gives rise to social and economic instability and chaos, affecting every sphere of Afghan lives and livelihoods. Besides the opium trade, the revenue from mineral help the regional warlords establish supremacy, run parallel governance in provinces and extort taxes (forced extortion) from the mine owners, which disincentivizes them to adopt newer technology to increase production. In particular, the new leadership should develop targeted socio-economic interventions for the youth, who fall prey to temptations of ‘quick’ money. Rampant unemployment, poverty, hunger/malnutrition and a lack of marketable skills have attracted the youth, especially in rural areas, to give up traditional farming and livestock rearing and get involved in illegal mineral trading business. Here, we expect the present Afghan leadership to show some sense of responsibility and commitment to the youth - create a network of jobs in the mining sector with appropriate remuneration packages, besides ensuring long-term job security, and opportunities of skill development and career advancements.

Potential Considerations to Restrain Illegal Mining and Export Across Afghan Borders.

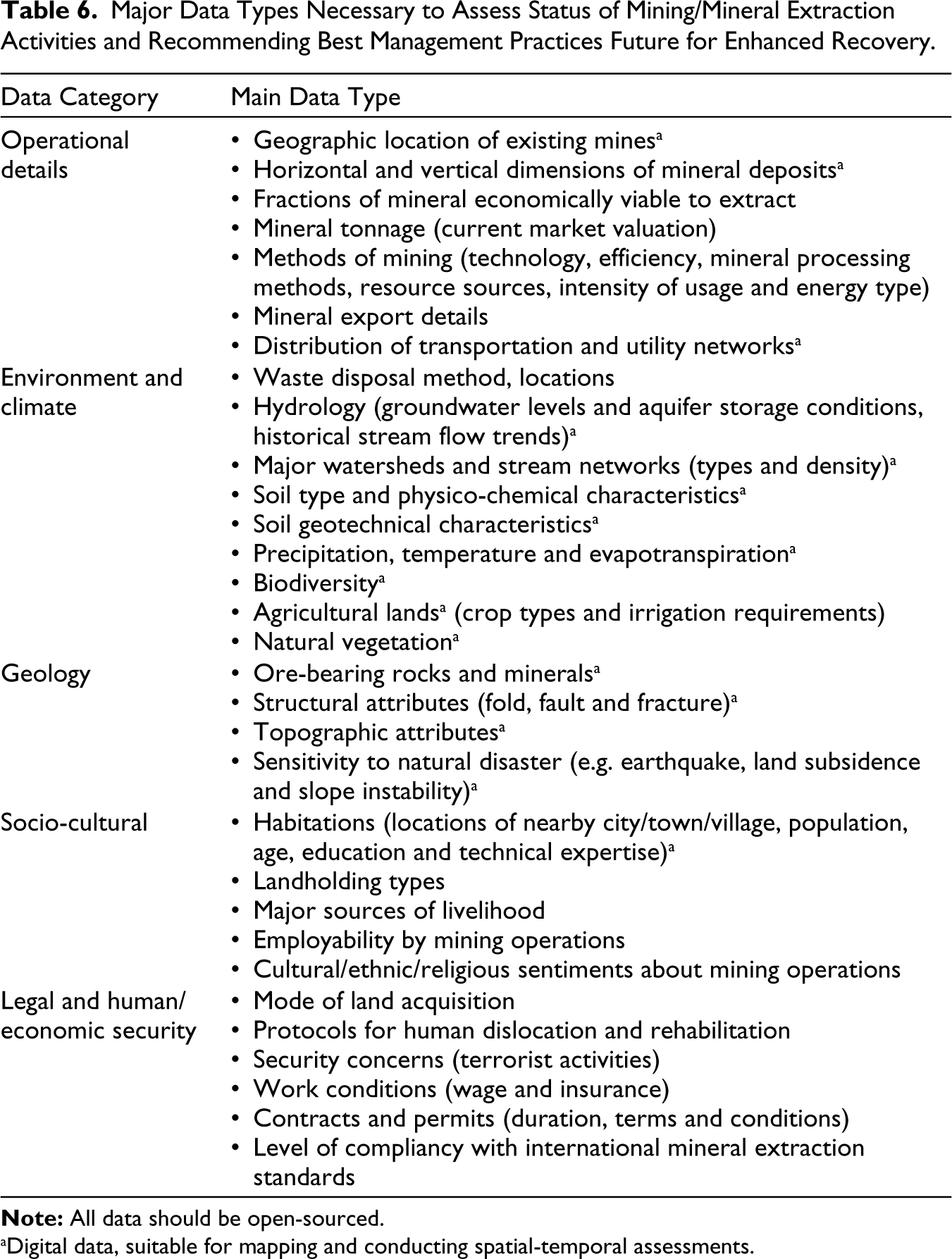

Call for a Data Revolution?

While conducting the study, we identified an appalling lack of information, which we think would require planned efforts. For example, we found a complete lack of data about the mineral deposits (e.g., latitude/longitude, horizontal and vertical distribution); they either do not exist or are only within government archives (not open-sourced), which require security clearances. Our apprehension is that very little, if any, of the mineral data yet exist in digital format (hard copy only), which makes it difficult to perform detailed research to facilitate exploration. To support targeted and informed policymaking, we urge the new leadership to acknowledge the need and make efforts to collect the spatio-temporal information from all possible sectors associated with mining and make it available for the global research community to access, investigate and provide sound recommendations (Table 6). In the process, there should also be conscious efforts to internationalise that data for the global research community to access, analyse and interpret mining/mineral information to offer sound recommendations.

Major Data Types Necessary to Assess Status of Mining/Mineral Extraction Activities and Recommending Best Management Practices Future for Enhanced Recovery.

aDigital data, suitable for mapping and conducting spatial-temporal assessments.

Concluding Remarks

Through this narrative, the Afghan leadership is offered a fresh glimpse of the existing mineral wealth, especially focusing on the lithium and REEs reserves, which could potentially transform the cash-strapped economy while presenting a means to advance towards the global decarbonisation and net-zero agenda. However, to get to that point, the new leadership will have to overcome a range of structural and institutional challenges in the mining sector. Here, emphasis is laid on means to increase foreign investment, create an enabling business environment, restrict illegal mining operations, develop unified water-power supply framework and, to complement all of the above, a ‘data revolution’ that would facilitate research and development.

Given the present state of terrorism, oppression and socio-religious persecutions under the new leadership, it might appear a little ambitious to sound a call for rejuvenating the mineral sector. However, this narrative is presented out of a profound optimism that sooner than later the present Afghan leadership will realise, acknowledge and appreciate the urgency of putting economic opportunities before all others and adopt a more humane, open-minded and reformative approach towards the mining/mineral sector that has all the potential to jumpstart the economy. To that end, this narrative might serve as a foundational document to begin a full-scale systems thinking, which in days ahead might herald a new era of strategic skill and youth development and women’s empowerment; trigger economic boom; alleviate political tensions and terrorism; and collectively, set Afghanistan in paths of holistic social wellbeing.

Footnotes

Acknowledgements

The authors thankfully acknowledge the support of the Centre for Environment, Sustainability and Human Development (CESH), O.P. Jindal Global University, Sonipat, Haryana, India, to help conducting the research.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.