Abstract

E-commerce has experienced significant growth and is becoming more relevant to economies. The exchange rate can have notable implications on e-commerce prices, and this relationship is of great interest to consumers and retailers transacting online. Brazil is prominent among other emerging countries in issues relating to e-commerce. This article analyzes the relationships between the exchange rate and e-commerce prices in Brazil. The results reveal that: (a) there is an incomplete exchange rate pass-through to Brazilian e-commerce prices; (b) there is temporal precedence of the exchange rate in relation to these prices; (c) there is the possibility of arbitraging online purchases based on exchange rate variations. This article contributes to understanding the e-commerce price behavior in an emerging country. The evidence can support buyers interested in arbitrage.

Introduction

In the last decades, there has been significant growth in online sales, and e-commerce is becoming more relevant for economies. With increasing access to technology, more consumers can buy online. In 2018, e-commerce grew 24% worldwide, reaching US $ 2.9 trillion in sales. Online sales are growing faster than traditional retailing in practically all countries (Ebit, 2019). The usual motivations for consumers to substitute in-person shopping for online are often conveniences, such as faster processing of purchases, delivery logistics, and others (Litan & Rivlin, 2001). In addition, search engines allow consumers to make price comparisons before deciding to buy on the Internet. Hortaçsu et al. (2009) mention the reduced cost to the consumer of searching for products and their prices in e-commerce. Meanwhile, Gorodnichenko et al. (2018) point out that e-commerce firms also have low costs of monitoring competitors’ prices and adjusting their prices based on them. Hillen and Fedoseeva (2021) discuss related literature that analyzes price rigidity in e-commerce.

Brazil is prominent among other emerging countries when the subject is e-commerce. This country has the most developed e-commerce market in Latin America, with revenues of around US $ 14 billion in 2018. 1 In Brazil, 4.3% of sales were online, and the growth of these sales was 12% in 2018. This year, the country had 58 million online consumers, equivalent to 27% of its population (Ebit, 2019). These numbers illustrate the relevance that e-commerce is acquiring in the country’s retail market. Despite this, Brazil is an inward-oriented economy, and most e-commerce firms compete mainly within the domestic market (Hannigan et al., 2015; Tigre & Dedrick, 2004). Such orientation can be a determining factor for the price level of domestic e-commerce.

The exchange rate can have notable implications on e-commerce prices, and this relationship is of great interest to consumers and retailers transacting online. Despite this, the previous literature on exchange rate pass-through is still incipient when the matter is e-commerce prices, not even including analysis in the context of emerging countries. Gorodnichenko and Talavera (2017) advanced this literature by finding broader results for developed countries.

This article analyzes the exchange rate pass-through to the domestic e-commerce prices in Brazil, considering data from 2012 to 2018. First, we test the hypothesis that there is an incomplete exchange rate pass-through to Brazilian e-commerce prices. Our analysis is based on the FIPE-Buscapé price index, an indicator constructed upon disaggregated prices from the Buscapé price comparison website. This index comprises products sold online in Brazil. The advantage of adopting this aggregated index is that its time series with many observations allows us to use econometric methods that would not apply to data from other studies. In our first analysis, we adopted the bounds-testing approach to cointegration (Pesaran et al., 2001) to estimate the relationship between the exchange rates and e-commerce prices. This approach is based on an Autoregressive Distributed Lag (ARDL) model and allows us to assess the short- and long-run effects. To check the robustness of our result, we also estimated a Vector Error Correction Model (VECM), adopting a more traditional econometric approach (Johansen, 1988).

The literature on exchange rate pass-through to offline prices has assumed that movements in the exchange rates affect the prices in the economies, but it has not been so interested in the effect in the opposite direction (Aron et al., 2014; Goldberg & Knetter, 1997). This assumption also seems to have been made by authors who analyzed the exchange rate pass-through to online prices for developed countries (Gorodnichenko & Talavera, 2017). Despite this, we do not find evidence in the literature about the direction of Granger causality between exchange rates and e-commerce prices. Then, in our second analysis, through a Granger causality test, we evaluated the hypothesis of time precedence of the exchange rate in relation to Brazilian e-commerce prices. Specifically, we adopted the causality testing approach that Toda and Yamamoto (1995) proposed, based on augmented Vector Autoregressive (VAR) models. We also tested long-run causality using VECM. Finally, considering the evidence used to test our two already mentioned hypotheses, we evaluated the hypothesis that there is the possibility of arbitraging purchases in Brazilian e-commerce based on the exchange rate.

Our results suggest that the exchange rate pass-through to prices in Brazilian e-commerce is lower and slower than was documented for developed countries. Furthermore, we confirm that the causality runs from the exchange rate to e-commerce prices. Given the temporal precedence of the exchange rate and the slow speed with which online prices adjust toward their equilibrium level, we conclude that it should be possible for consumers to arbitrage purchases in Brazilian e-commerce.

We found no other studies that analyze exchange rate pass-through to e-commerce prices in the context of an emerging country, such as Brazil. We also found no studies that tested the temporal precedence of the exchange rate in relation to e-commerce prices. Furthermore, there is no previous evidence of the possibility of arbitrage in Brazilian e-commerce based on exchange rate variations. Therefore, we attempt to cover a gap in the literature. Our article contributes to the understanding of e-commerce price behavior in Brazil. The results can be relevant mainly for consumers and retailers that transact online. The evidence can support buyers interested in arbitrage.

We divide the remainder of this article into six sections. After this introduction, we present the literature review, which leads to our hypotheses. Next, we describe the data used in the analysis and the methods adopted. Finally, we present the results, the discussion, and the final remarks.

Literature Review and Hypotheses

The study of exchange rate pass-through constitutes a recurring research topic in international economics. A vast literature on this issue has emerged, as documented in the surveys provided by Menon (1995) and Goldberg and Knetter (1997). The extent of this pass-through can be related to different aspects, such as market structure, demand, and institutional features that are typically country and sector-specific. Aron et al. (2014) provide an additional survey in the context of Latin America. A salient feature in the context of emerging countries is the more frequent economic and political instabilities, which can give rise to greater exchange rate volatility. This level of variation can have a relevant role in the exchange rate pass-through dynamics.

The literature that analyzes the exchange rate pass-through to offline prices is extensive (Aron et al., 2014; Goldberg & Knetter, 1997; Menon, 1995). Despite this, there are not many studies on the effect of the exchange rate on online prices. Some studies evaluated this relationship with data from specific products or retailers (Boivin et al., 2012; Cavallo et al., 2014). Gorodnichenko and Talavera (2017), who investigated the exchange rate pass-through to e-commerce prices with data from Canada and the United States (US), found broader results. These authors found an incomplete pass-through of approximately 60%–75%, an impact higher than 20%–40% documented for offline markets. They also found that the speed of price adjustment to equilibrium levels is 2–2.5 months. For emerging countries, until then, there were no studies on this issue.

Gorodnichenko and Talavera (2017) argue that the Law of One Price (LOP) justifies a long-run equilibrium relationship between exchange rate and e-commerce prices. In this theory, arbitrage drives prices to equilibrium over time. If the LOP were fully adherent to reality, studies would find a coefficient equal to one for the exchange rate in the estimated econometric models and, therefore, a complete exchange rate pass-through. However, this theory has some simplifying assumptions that are unrealistic, and we must relativize it given the existence of trade frictions, such as some tariff or non-tariff trade barriers. We should not expect a complete exchange rate pass-through, considering the results that the literature has generally found (Goldberg & Knetter, 1997; Gorodnichenko & Talavera, 2017). Therefore, we set out to test the following hypothesis:

H1. There is an incomplete exchange rate pass-through to Brazilian e-commerce prices.

In the literature on exchange rate pass-through to offline prices, typically, the estimated models have prices as the dependent variable (Aron et al., 2014; Goldberg & Knetter, 1997). Regarding the direction of the effect, some studies have sought to test Granger causality between the exchange rate and these conventional prices. Kim (1998) finds Granger causality in the direction of the exchange rate for the US Consumer Price Index (CPI). Nogueira Junior (2007) also finds this direction of causality for several developed economies and emerging markets using consumer and producer price indexes, including evidence for Brazil. However, Granger causality can also occur in the opposite direction when dealing with specific goods or services prices. For example, Usman et al. (2020) found that restaurant and hotel prices precede movements in the exchange rate. Although there is literature oriented to offline prices, we have not found any studies that have tested the temporal precedence of the exchange rate in relation to online prices. Therefore, in this study, we test the following hypothesis:

H2. There is temporal precedence of the exchange rate in relation to Brazilian e-commerce prices.

Anson et al. (2019) expand the literature on e-commerce with a distinct perspective. These authors investigated consumer arbitrage

2

in cross-border e-commerce. They analyzed the effect of exchange rates on parcel dispatches in terms of high-frequency data for developed countries. The evidence indicated that a 1% appreciation of the domestic currency leads to an increase in e‐commerce imports by 0.7%. Boffa (2015) highlights the relevance of waiting for cost when consumers discriminate between international sellers. This author estimates the impact of delivery time on cross-border e-commerce trade. Regarding Brazilian domestic e-commerce, there is no evidence of the possibility of arbitrage purchases based on exchange rate movements. Thus, we attempt to test the following hypothesis:

H3. There is the possibility of arbitraging purchases in Brazilian e-commerce based on the exchange rate.

It should be noted that Anson et al. (2019) measure the percentage of purchases that are arbitraged by consumers. Differently, we seek namely to evaluate whether arbitrage is possible in Brazilian e-commerce. We assume that if there is a long-run relationship between the exchange rate and e-commerce prices, and the movements in the exchange rate temporally precedes those in these prices, the consumers can arbitrage online purchases. We consider arbitrage possible mostly when the prices take several months to adjust to their equilibrium level with the exchange rate.

Data and Behavior of the Variables

As mentioned, we adopted the FIPE-Buscapé price index in the proposed analysis. It monitors 41,000 products sold through e-commerce in Brazil. The Institute of Economic Research Foundation (FIPE) calculates this index based on more than 3 million monthly prices extracted from the Buscapé platform. 3 In the calculation, FIPE also uses weights obtained from an annual survey of approximately 3.6 million e-consumers conducted by Ebit, 4 the principal reference on e-commerce data in Brazil. Ten categories of products that compose the FIPE-Buscapé price index represent around 80% of sales on domestic e-commerce: household appliances, electronics, computers, telephony, photography, cosmetics and personal care, sports and leisure, home and decoration, toys and games, and fashion and accessories. Many mentioned categories include imported finished products or products made from imported inputs. Importation should be one of the main channels through which the exchange rate can affect the e-commerce price level that the FIPE-Buscapé index reflects.

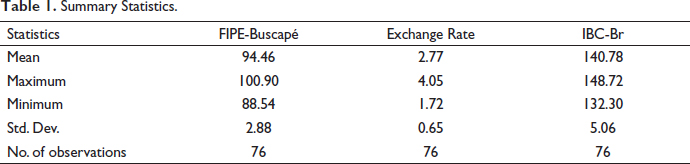

We collected the monthly data of the FIPE-Buscapé index from the FIPE website. 5 The index has a base equal to 100 in December 2010. The methodology of this index is available on the indicated website. We collected monthly data on the nominal exchange rate from the Institute for Applied Economic Research (IPEA) website. 6 Exchange rate data represents the value of the Real (Brazilian currency) per unit of the US Dollar. A positive variation of the exchange rate means depreciation of the Real, and a negative one means appreciation. To check the robustness of our results, we also collected data from Central Bank Economic Activity Index (IBC-Br) on the website of the Brazilian monetary authority. 7 Table 1 exhibits the summary statistics for the FIPE-Buscapé index, nominal exchange rate, and IBC-Br variables. The data refer to the period from January 2012 to April 2018.

Summary Statistics.

Based on the summary statistics, we observe that the exchange rate is more volatile than the prices in Brazilian domestic e-commerce. While the coefficient of variation (standard deviation divided by the mean) of the FIPE-Buscapé index is about 3%, this indicator of the exchange rate is about 23%. These indicators can lead us to believe that, in Brazil, there is an incomplete exchange rate pass-through. We also expect an incomplete exchange rate pass-through in this country because its trade flow (exports and imports) ranks it as one of the most closed countries in the G20 (the twenty largest economies in the world, including both industrialized and developing countries). The high tariffs imposed on Brazil’s international trade inhibit competition by foreign firms and make products sold in the domestic market more attractive to consumers (Spilimbergo & Srinivasan, 2018). This issue is no different when we specifically address e-commerce. Online stores are more oriented to the domestic market in this country (Ebit, 2019).

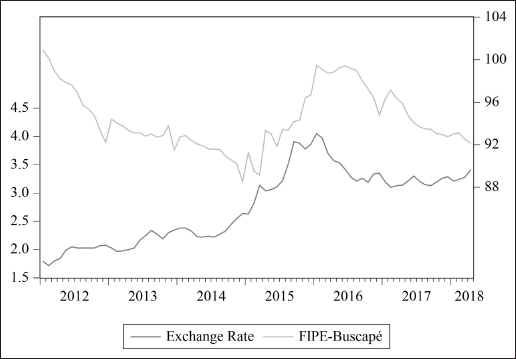

Figure 1 exhibits the evolution of the exchange rate and e-commerce price variables. This figure allows us to observe that in 2015 there was a currency devaluation in Brazil. However, there was no rupture in the relationship between the exchange rate and prices in e-commerce. According to Ebit (2019), as an effect of the depreciation of the Brazilian Real, there was a retraction in cross-border trade, and e-commerce purchases tended to become even more concentrated in the domestic market. The mentioned currency devaluation occurred soon after Brazil entered its deepest and longest economic crisis. During the so-called Brazilian Economic Crisis, there were consecutive drops in economic activity, employment, and income, reducing, in turn, household consumption. Meanwhile, during the period considered in this study (2012–2018), a cultural and technological change also occurred, altering consumer behavior and motivating a growth trend in online sales. The popularization of smartphones, broadband, and 4G access played a relevant role in this behavior (Ebit, 2019).

Exchange Rate and E-commerce Prices.

A preliminary inspection of Figure 1 suggests a co-movement between the exchange rate and online prices. Moreover, exchange rate variations appear to precede those of e-commerce prices. However, to assess the relationships between these variables, we made a careful econometric analysis, as shown in a later section. We analyze the mentioned co-movement using the bounds testing approach to cointegration (ARDL model), besides a robustness check that employs a more conventional error correction model (VECM). The direction of causality between exchange rates and aggregate prices seems well established in the literature since, typically, the models have prices as the dependent variable (Aron et al., 2014; Goldberg & Knetter, 1997). The exceptions for specific goods are rare (e.g., Usman et al., 2020). Therefore, we expected that movements in the exchange rate would precede those in prices. We evaluate this precedence through a Granger causality test using e-commerce prices.

Methods

ARDL Model

The literature criticized the estimation of exchange rate pass-through using simple linear regression (Aron et al., 2014; Menon, 1995). This method can generate spurious regressions when adopted with non-stationary variables (Granger & Newbold, 1974), and studies state that most macroeconomic variables are non-stationary (Nelson & Plosser, 1982).

For this reason, first, we adopted the bounds-testing approach to cointegration (Pesaran et al., 2001) to analyze the relationship between the exchange rate and e-commerce prices. This approach is based on an ARDL model and allows the estimation of short- and long-run effects. We can apply the ARDL approach utilizing stationary variables, I(0), variables integrated of order one, I(1), or with an unknown mixture of I(0) and I(1) variables. In this approach, the estimators of the long-run coefficients are super-consistent in small sample sizes. Moreover, an adequate specification of the lags in the ARDL model is enough to correct the residual serial correlation and the problem of endogenous variables (Pesaran & Shin, 1999). Nogueira Junior (2007) and Usman et al. (2020) estimated the exchange rate pass-through using the ARDL approach.

In order to assess the exchange rate pass-through to e-commerce prices in Brazil, we considered an ARDL(p, q) model according to Equation (1):

where Pt denotes the e-commerce prices, Et denotes the exchange rate, bo denotes a constant, Ξt denotes a trend, ε t is the error term, and p and q denote the lag structure of the model. The variables are in the logarithmic scale (ln). Our choice to include a trend term considers that it can capture unobservable effects in terms of technological progress or changes in consumer preferences. Consumers have increasingly opted for online shopping in Brazil (Ebit, 2019).

We can represent our ARDL model as a conditional Error Correction Model (ECM), according to Equation (2):

In this ECM representation, the coefficients of the first differenced variables (∆ is the first difference operator) and their lags capture the short-run effects. The sum of these coefficients gives the total of such transitory effects. The ratio –λ2/λ1 provides the long-run exchange rate pass-through, and λ1 gives the speed of adjustment of the deviations from the long-run equilibrium between the variables. In our models, we interpret λ1 in terms of the monthly percentage of adjustment in relation to the total adjustment required to achieve the long-run equilibrium level.

Equation (2) allows us to test the existence of cointegration between the variables through the bounds test (Pesaran et al., 2001). We can define the null hypothesis (H0) and the alternative (H1) of the non-cointegration test as exhibited in Equation (3):

We tested these hypotheses based on an F-statistic, comparing it with two sets of critical values for finite samples reported by Narayan (2005). Since our number of observations is not very large, these values are more appropriate than those asymptotic that Pesaran et al. (2001) provided. If the obtained F-statistic value is lower than the lower bound critical value, we concluded that all variables are I(0). Therefore, cointegration is not possible. In contrast, if this F-statistic value is higher than the upper bound critical value, we concluded that all variables are I(1). Therefore, cointegration is possible. Finally, the test is inconclusive when the F-statistic is between the two mentioned bounds values.

Regarding the expansion of the ARDL model by including additional variables, we have encountered some obstacles. Markups and costs in Brazilian domestic e-commerce are not well established, and the high tariff barriers that exist in Brazil (e.g., import duties for people) hinder the competition from foreign firms. In this country, a considerable portion of the goods sold in e-commerce consists of imported products. However, there were no significant changes in tariffs on imports of consumer goods during the period considered in this study. Hence, tariff variations are not a concern for our models.

Still on potential additional variables, since the gross domestic product (GDP) is not available on a monthly basis in Brazil, one possibility is to take the IBC-Br as a proxy for income, which could affect the dynamics of e-commerce. However, we verified that the IBC-Br has an I(1) time series and that this variable is cointegrated with the exchange rate. We opted not to use the IBC-Br in our ARDL model because this econometric approach requires that the I(1) independent variables are not cointegrated between themselves (Pesaran & Shin, 1999).

Finally, if there is cointegration between the dependent and one independent variable, we can consider that no relevant non-stationary variable is omitted. The cointegration must also not disappear with the inclusion of more variables (Lütkepohl, 2007). Therefore, first, we opted for a parsimonious bivariate ARDL model.

Toda and Yamamoto Granger Causality Test

We can assess the direction of causality between the variables exchange rate and e-commerce prices through a Granger causality test. Specifically, we adopted the Granger causality test that Toda and Yamamoto (1995) proposed, based on augmented VAR models. This testing approach minimizes the risks associated with the potential incorrect identification of the order of integration of the time series. It can be applied considering purely the I(0) and I(1) series and with mixtures of series with these different orders of integration. Usman et al. (2020) adopted this Granger causality test to analyze the causal relationship between exchange rate and both restaurant and hotel prices.

To apply the Toda Yamamoto Granger causality test, first, we determine the lag length k of a VAR model and increase it with the maximal order of integration, dmax, that we suspect might occur in our variables. So, we estimate a (k + dmax)th-order VAR. Considering the exchange rate and e-commerce prices variables, we can express the estimated VAR system according to Equation (4):

Finally, we applied modified Wald (MWALD) tests on the coefficient matrices, ignoring those of the dmax lagged vectors in the model. When we test Granger causality from E to P, the MWALD test involves the γ1 coefficients of E in the first equation of the system. In contrast, when we test Granger causality from P to E, the MWALD test involves the δ1 coefficients of P in the second equation of the system. If we reject the null hypothesis that the coefficients are equal to zero, one variable Granger-cause the other.

Robustness Check: VECM Models

As mentioned, we cannot include the IBC-Br in our ARDL model. However, as a robustness check for the results found using this model, we also can estimate a Vector Error Correction Model (VECM) through Johansen’s (1988) approach, including such variable in the equation. Since the exchange rate, e-commerce prices, and the IBC-Br are nonstationary variables (as the tests below exhibit), they satisfy the I(1) regressors assumption of the VECM approach. Hence, besides a bivariate model, we can estimate an augmented model that considers the effects of income. We estimate two VECM models. The first one, whose system is represented by Equation 5, has only the exchange rate and e-commerce prices variables:

Meanwhile, the second VECM, whose system is represented by Equation 6, is augmented with the IBC-Br variable:

In these systems, the β coefficients of the lagged first difference variables capture the short-run effects, the θ coefficients provide the long-run effects of the variables, and the λ provide the adjustment speed of the variables toward the long-run equilibrium (also interpreted in terms of the monthly percentage of adjustment in relation to total adjustment required to reach the long-term equilibrium level). The α0 term is an intercept fitted into the error correction term. Considering the system represented by Equation (5), we can also apply restriction tests on λ in order to assess the long-run Granger causality between the variables exchange rate and e-commerce prices.

A difference in relation to the error correction representation of the ARDL model is that the VECM has all the variables always lagged and with the same p number of lags. In turn, this can also imply differences in the fit of these models.

Results

Unit Root Tests

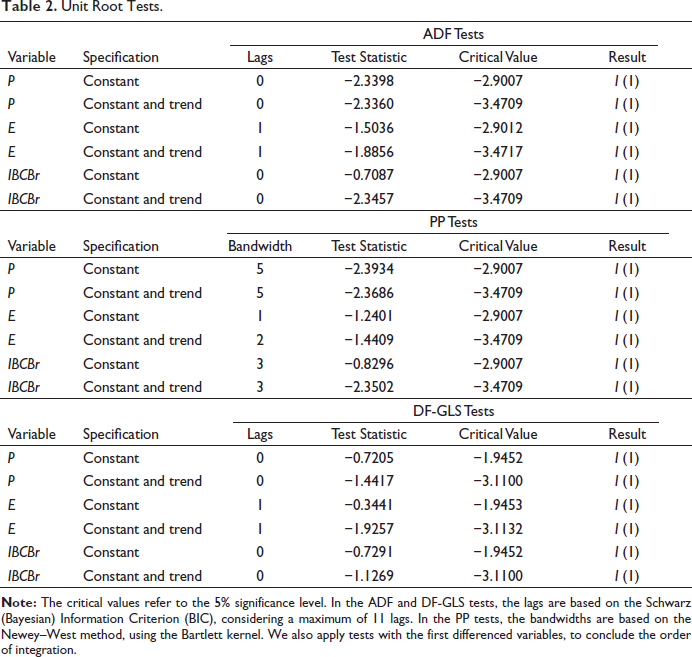

As a preliminary step to the econometric model estimation, we evaluated the order of integration of the exchange rate, e-commerce prices, and IBC-BR variables through the unit root tests: Augmented Dickey–Fuller (ADF), Phillips–Perron (PP), and Elliott–Rothenberg–Stock DF-GLS. The latter-mentioned test is superior to the others in terms of power. Table 2 exhibits the results of these three tests.

Unit Root Tests.

In all unit root tests that the table exhibited, applied to our three variables, the test statistics are lower than the critical values. Therefore, we do not reject the null hypothesis of a unit root in all these time series. By concluding that e-commerce prices, exchange rates, and IBC-Br are I(1) variables, we can estimate both the ARDL model and the VECM.

ARDL Model Results

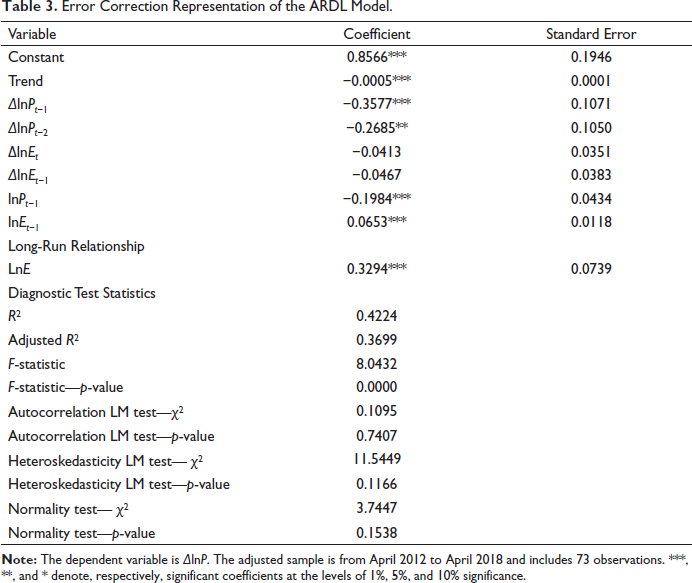

Table 3 exhibits the error correction representation of the ARDL(3,2) model that relates the variables exchange rate and e-commerce prices. This model was automatically selected due to its minimum Schwarz (Bayesian) Information Criterion (BIC), considering 156 evaluated models with a maximum of 12 lags for each variable. Pesaran and Shin (1999) state that BIC leads to slightly superior results in relation to when the ARDL model selection is made based on the Akaike Information Criterion (AIC). We adopted a heteroskedasticity and autocorrelation consistent (HAC) covariance matrix estimator. The results of the estimated model are satisfactory, with most of the coefficients being significant.

Error Correction Representation of the ARDL Model.

The results of the diagnostic test statistics exhibited in Table 3, support the estimated model: the Breusch–Godfrey LM test does not reject the hypothesis of no autocorrelation; the Breusch–Pagan–Godfrey test does not reject the null hypothesis of no heteroskedasticity; the Jarque–Bera test does not reject the null hypothesis that the residuals are normally distributed.

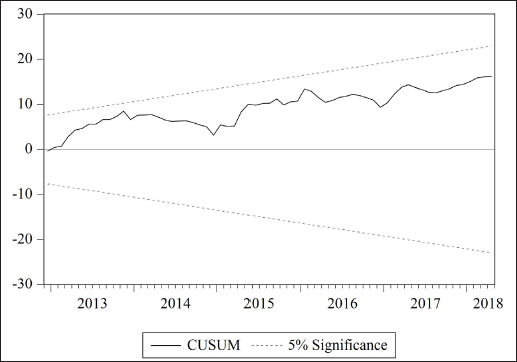

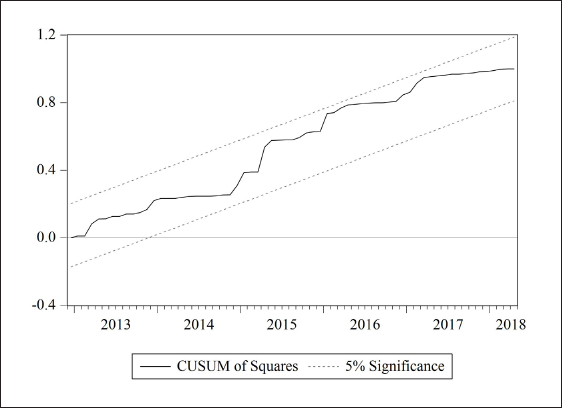

Furthermore, the CUSUM and CUSUMSQ tests (Figures 2 and 3) indicate the stability of the coefficients, despite the sharp rises in the exchange rate and e-commerce prices observed in mid-2015 (Figure 1), at the time of the Brazilian Economic Crisis. Since these rises are nearly synchronized, they do not significantly impact the relationship between these variables.

CUSUM Test.

CUSUMSQ Test.

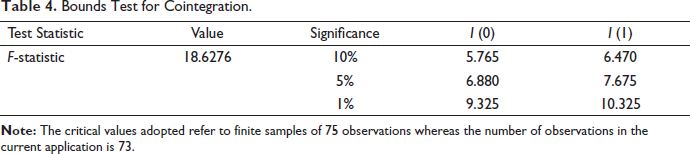

The bounds test (Table 4) suggests the existence of a long-run relationship between the exchange rate and e-commerce price variables. The F-statistic is higher than the upper bound critical value, indicating cointegration.

Bounds Test for Cointegration.

Focusing our analysis again on Table 3, we observe that the trend term is highly significant. It captures unobservable effects in terms of technological progress or changes in consumer preferences. The ∆E coefficients indicate that transitory shocks do not significantly affect e-commerce prices. The long-run coefficient of E suggests that, for each 1% of the permanent increase in the exchange rate, the e-commerce prices will increase by a little more than 0.3% in the long run. In the measure mentioned by Gorodnichenko and Talavera (2017), this pass-through is equivalent to about 30%. Based on this result, we do not reject H1, which states that there is an incomplete exchange rate pass-through to Brazilian e-commerce prices. From a theoretical perspective, we can conclude that the LOP is not valid for Brazilian domestic e-commerce.

The coefficient of Pt−1 suggests that the adjustment of e-commerce prices towards their level of long-run equilibrium with the exchange rate takes about 5 months (about 20% of the total adjustment per month). This time can be long enough for consumers to arbitrate. But for this, there must also be temporal precedence of the exchange rate over e-commerce prices. We assess this precedence further below through Granger causality tests.

Granger Causality Test Results

We estimated the augmented VAR models and applied Granger causality tests as suggested by Toda and Yamamoto (1995). Regarding the information criterion used to select the lag length of the model, this time, we opted for the AIC instead of the BIC. The BIC indicated a lag length that was not enough to eliminate the autocorrelation from the VAR model. The AIC suggested k = 3 optimal lags, and we increased this number with dmax = 1 additional lag. Table 5 exhibits the results of the MWALD tests. They indicate the direction of the Granger causality between the exchange rate and e-commerce price variables.

Toda Yamamoto Granger Causality Tests.

The results indicate that the exchange rate Granger-cause e-commerce prices and that there is no Granger causality in the opposite direction. This evidence means that the movements in the exchange rate precede those in e-commerce prices. Hence, we do not reject H2, which states that there is temporal precedence of the exchange rate in relation to Brazilian e-commerce prices. In our analysis, we find a long-run equilibrium relationship between the variables and that the variations in the exchange rate precede those in online prices. Therefore, we also do not reject H3, which states that there is the possibility of arbitraging purchases in Brazilian e-commerce based on the exchange rate.

Robustness Check Results

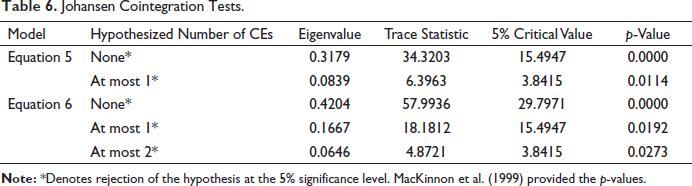

We check the robustness of our results by estimating VECM. The BIC suggested two lags for these models. As a preliminary analysis, we evaluate the cointegration between the variables. Table 6 shows the cointegration tests (Johansen, 1988) applied considering the systems represented by equations 5 and 6. We evaluate the number of cointegrating equations (CEs) based on trace statistics.

Johansen Cointegration Tests.

The results in Table 6 indicate that there are two CEs for the system represented by Equation (5) and three CEs for that represented by Equation (6). Since the variables are cointegrated, we can proceed with the analysis of the exchange rate pass-through to e-commerce prices using VECM.

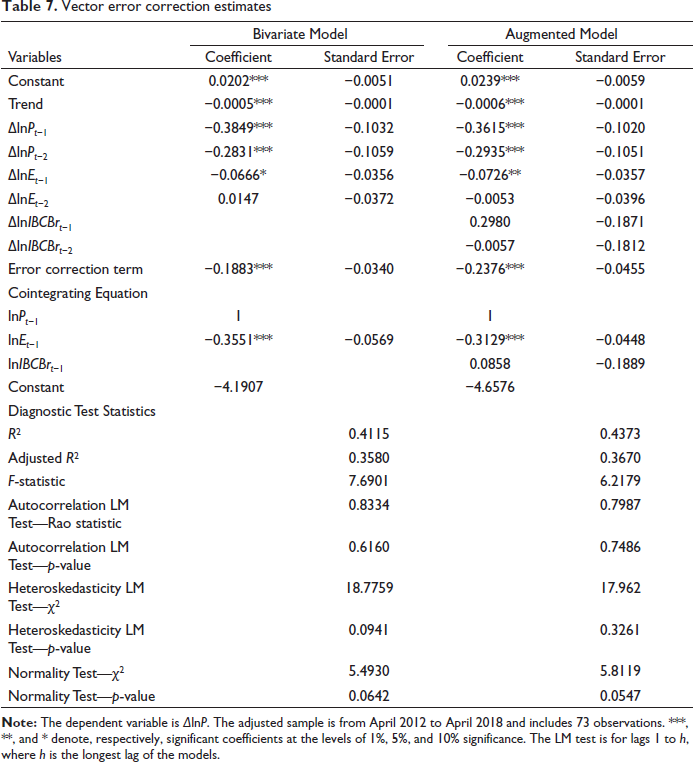

Table 7 exhibits the two estimated VECMs that have e-commerce prices as the dependent variable. The augmented model (Equation 6) differs from the bivariate model (Equation 5) only by having the IBC-Br variable, which captures the income effect. However, note that we do not display all the models that compose the systems since, in this analysis, we are not interested in the effects on variables other than e-commerce prices.

Vector error correction estimates

The results of these models are satisfactory, and the diagnostic test statistics support that they are valid. The VECM estimates are very close to those found using the ARDL approach. The positive long-run effect of the exchange rate on online prices is also a little more than 0.3 (30% of exchange rate pass-through) in these models (one must interpret the coefficient of the cointegrating equation of the VECM with the sign reversed). The speed of adjustment of prices toward their long-run equilibrium level is almost 5 months or a little less. Therefore, our estimates for the exchange rate pass-through to e-commerce prices are robust.

A difference we find in these new estimates is a significant short-run effect of the exchange rate in the model specified according to Equation (6), even though it is not statistically significant at the 5% significance level in the other VECM. We also observe that this transitory effect is small in terms of magnitude (about 7%). In addition, we do not find significant effects of our income proxy, the IBC-Br, either in the short or long run. Observing the R2, we notice that the difference in fit between the ARDL model and the VECM is very subtle.

We can also test for long-run Granger causality for the exchange rate and e-commerce prices by imposing restrictions on the error correction terms, λ, in Equation (5). For this purpose, we apply Wald tests on these terms. Table 8 exhibits the results of these Granger causality tests.

Long-run Granger Causality Tests.

The long-run Granger causality tests suggest causality only in the direction from the exchange rate to e-commerce prices. There is no evidence of Granger causality in the opposite direction. This result is in line with those already found and reinforces the temporal precedence of the exchange rate in relation to the prices of products sold on the Internet.

In view of the robustness checks we have conducted, we maintain the non-rejection of H1, H2, and H3. We find an incomplete exchange rate pass-through to Brazilian e-commerce prices (H1) and temporal precedence of the exchange rate in relation to these prices (H2). Given this precedence and that the prices take a long time to adjust from their long-run equilibrium level, we also conclude that consumers can arbitrage purchases in Brazilian e-commerce (H3).

Discussion

Although we use a price index, which has a composition that differs from the set of goods considered in a previous study, we begin the discussion of the exchange rate pass-through found by attempting to make a comparison. In relation to the results that Gorodnichenko and Talavera (2017) found with data from the US and Canada, the exchange rate pass-through to prices in Brazilian domestic e-commerce is lower and slower. In the measure mentioned by Gorodnichenko and Talavera (2017), this pass-through is equivalent to about 30%, which is lower than the 60%–75% found by these authors. The adjustment of prices toward the long-run equilibrium level occurs in about 5 months in Brazil, which is longer than the 2–2.5 months found by these authors. We highlight that in contrast to Brazil and its trade partners, 8 Canada and US are geographically close. Therefore, they have low delivery times and costs. According to Boffa’s (2015) perspective, the waiting cost for cross-border purchases between these developed countries is low. Meanwhile, Ebit (2019) mentions the long delivery time as one of the main reasons that discourage Brazilian consumers from making cross-border purchases. This greater trade friction can imply a lower exchange rate pass-through to Brazil’s online prices.

The results we find are likely to reflect, to a certain extent, the specificities of Brazil’s context. This emerging country has high exchange rate volatility due to frequent domestic political and economic shocks. Aron et al. (2014) mention that studies have shown that exchange rate volatility in emerging countries has implications for exchange rate pass-through. We understand that this volatility can also complicate inventory and price management by e-commerce stores. This issue can explain why we did not find significant short-run effects of the exchange rate in the ARDL model and one of the VECM. Another aspect that can influence these short-run effects is the already mentioned waiting cost. Boffa (2015) states that in countries with high waiting costs (such as Brazil), the exchange rate pass-through should be close to zero in the short run.

Another relevant aspect is that Brazilian e-commerce is a segmented market and the e-commerce stores have their competition more restricted to the domestic market. Brazil has high tariff barriers, high shipping costs due to its extensive territory and borders, and even informational frictions. 9 These factors, to some extent, can make products sold in the domestic market more attractive to consumers and discourage cross-border arbitrage. Boivin et al. (2012) and Goldberg and Knetter (1997) point out the relevance of these features in explaining deviations from the LOP. In view of these mentioned aspects, we can conclude that the characteristics of the Brazilian e-commerce market should motivate a low exchange rate pass-through even in the long run.

Regarding the Granger causality test results, they are in line with what we expected, given that most of the literature on exchange rate pass-through presupposes causality from the exchange rate to the prices (Aron et al., 2014; Goldberg & Knetter, 1997), including when dealing with e-commerce prices (Gorodnichenko & Talavera, 2017). Since the variables are cointegrated, and there is causality only in the direction of the exchange rate to e-commerce prices, it can be possible to predict the path of these prices based on the exchange rate. This predictability can be of benefit to buyers interested in arbitrage.

Final Remarks

This article analyzes the exchange rate pass-through to Brazilian e-commerce prices. The results indicated a lower and slower exchange rate pass-through than found in a previous study for the US and Canada. In addition, they confirm that causality runs from the exchange rate to e-commerce prices. The period found for the long-run equilibrium adjustment between the online prices and the exchange rate is long. It should be enough for consumers to arbitrate the best moment to make their purchases in domestic e-commerce. Consumers can hasten to buy as soon as they observe domestic currency depreciation. The opposite can happen when they notice domestic currency appreciation. There is evidence for arbitrage in cross-border e-commerce (Anson et al., 2019) but not for domestic e-commerce. Thus, our first suggestion for future studies is to test a hypothesis referring to mentioned consumer behavior using domestic sales data.

A limitation of our study refers to the aggregate character of the FIPE-Buscapé price index. Goldberg and Knetter (1997) point out that the price indexes of the countries can consider different baskets of goods. Therefore, the interested agents should view comparisons between the research results cautiously. Furthermore, Gorodnichenko and Talavera (2017) state that there is significant heterogeneity in pass-through and speed of price adjustment across the different goods. However, the index that we have used does not say much about the magnitude of exchange rate pass-through to the prices of specific goods considered in its composition. In view of this limitation, our second suggestion for future studies is to make the analysis in terms of the main categories of goods sold in Brazilian e-commerce when price data at the micro-level becomes available. In addition, we suggest that future studies should also assess the effect of exchange rate volatility on e-commerce prices. Although we mention this issue in the discussion of our results, we have not empirically evaluated it. Finally, studies can relax the assumption of linearity and adopt asymmetric ARDL models (Shin et al., 2014) that relate these referred variables.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.