Abstract

This article empirically examines the linkage between foreign direct investment (FDI) and financial development (FD) in 16 selected countries of the MENA region (Algeria, Bahrain, Egypt, Iran, Israel, Jordan, Kuwait, Lebanon, Malta, Mauritania, Morocco, Oman, Qatar, Saudi Arabia, Tunisia, and the United Arab Emirates) over the period 2000–2018. The research investigates the long- and short-run effects of FD on FDI inflows using panel ARDL. This model is based on the dynamic fixed effect (DFE) estimator. The article employs three proxies of FD as developed by the IMF, namely, the overall financial development (OFD), financial markets’ development (FM), and financial institutions’ development proxy (FI). The purpose was to analyze the impact of FD by covering the depth, efficiency, and access to financial markets and their institutions. The findings suggest that even though no significant relationship is established in the short run, the long-run coefficients of the overall FD proxy and FM proxy are positive and statistically significant. The estimates suggest that a 1% increase in the overall FD proxy and FM proxy results in an increase of 172% and 150% of FDI inflows to MENA region countries, respectively.

Keywords

Introduction

Perhaps there is no unanimous consensus among researchers about the absolute importance of financial development (FD) for foreign direct investments (FDI). Still, a well-functioning financial system is considered a prerequisite for achieving maximum gains from foreign investments, which would benefit economic development. Believing in the importance of FDI, academicians and researchers focused their attention on its advantages to economic growth by exploring the different economic attractors, namely the degree of openness, natural resources availability, human capital skills, good infrastructures (Cleeve et al., 2015) but also good institutional quality (North, 1990). Although many factors are emphasized, the importance of FD was, until lately, the least explored.

A sound financial system of a country has been defined by the World Economic Forum, as a set of factors, policies, and institutions that lead to effective financial intermediation and market as well as deep and broad access to capital and financial services (The Financial Development Report 2012, 2012). The report defines the financial system in a multidimensional manner as it approaches the concept in terms of access, depth, and efficiency of both the financial markets and institutions.

Studies on the long-run association between FD and FDI in MENA countries have not yet been well explored. Therefore, it is essential to bridge the gap in the literature related to MENA countries so that necessary support can be provided to policymakers for making decisions on the development of financial systems.

This article contributes to the body of financial economics literature in numerous ways. To the best of our knowledge and having extensively searched the relevant literature, most of the empirical literature approximates FD by the ratio of private credit to GDP and by stock market capitalization. Unlike these traditional proxies, our article uses three proxies of FD as elaborated by the IMF, namely, the overall financial development (OFD), financial markets’ development (FM), and financial institutions’ development proxy (FI). The main goal is to take the financial system in its multidimensional aspect by covering the depth, efficiency, and access to financial markets and their institutions. Also, our article is amongst the first attempts to analyze the long-run relationship between FD and FDI with an ARDL approach on a panel of MENA countries (Algeria, Bahrain, Egypt, Iran, Israel, Jordan, Kuwait, Lebanon, Malta, Mauritania, Morocco, Oman, Qatar, Saudi Arabia, Tunisia, and the United Arab Emirates). Since some countries of the MENA region established stock markets very recently, the sample covers only 16 countries. Also, the choice is motivated by the fact that most countries experienced significant economic growth with approximately the same average GDP growth in the same period. This was coupled with financial liberalization reforms, especially in Morocco, Tunisia, and Egypt. These reforms involved privatization programs, institutional reforms, liberalization of interest rates and capital inflows, and incentive strategies for foreign investors. Given these developments, the average net inflows of FDI between 2000 and 2018 amounted to $57.92 billion 1 .

The next section of this article elaborates on the empirical review of the relationship between FD and FDI in the MENA region countries. This is followed by the research methodology, data description, and pre-estimation tests. Subsequently, the estimation results are discussed, and lastly, the conclusions and recommendations are presented.

Literature Review

FD has recently gained considerable attention among researchers as it plays a vital role in attracting foreign investors. Exploring the empirical literature for the article, we agree on one main idea that a well-developed, well-functioning financial system enhances economic growth, and it has a positive association with FDI. This article deals with two strands of empirical findings; the group of papers that find a positive impact of FD on FDI and another group of papers that establishes the association as being conditioned by a certain threshold level.

A developed financial system channels foreign investments more efficiently into productive investments, minimizes investment risks, and reduces information asymmetries and related costs, making the countries more attractive to FDI (Hermes & Lensink, 2003). This was considered a crucial precondition for FDI to the LDCs during the period between 1970 to 1995. Levine et al. (2002) suggest that the more a financial system is developed, the better it can effectively absorb capital inflows. The development of financial systems has a varying impact on FDI across countries with different incomes. Furthermore, Agbloyor et al. (2013) expand the association to classify it as a complementary association instead of FD being a simple precondition to increased FDI. Cherkaoui and El Fakiri (2021) analyzed the association in a sample of 135 countries classified by income level over 17 years. Their findings suggest that FD, as represented by the IMF’s composite index, is an essential determinant of FDI entries to high- and upper-middle-income countries, while the impact is inconclusive for low- and lower-middle-income countries. In the African context, Nkoa (2018) investigated the impact of FD on FDI in 52 African countries from 1995 to 2015. The analysis was based on two distinct sample countries: those with financial markets and others without financial markets. The results were interesting; some FD proxies were found to have a positive impact in economies with no financial markets and others were found to be positive on FDI entries to countries endowed with financial markets. Lately, there has been an increasing interest in the association between FD and FDI in the emerging market countries involved in the Road and Belt initiative. Islam et al. (2020) studied the impact on a sample of 79 countries along the Belt and Road through a set of models including pooled ordinary least square (POLS), fixed effects (FE), and two-step generalized method of moments (GMM), which demonstrates evidence of a positive and significant role of FD in triggering FDI. Majeed et al. (2021) investigated the effect of FDI on FD in a sample of 102 Belt and Road Initiative countries from four main regions: Asia, Latin America, Europe, and Africa. The analysis was based on a span of 27 years, using various econometric models. The findings indicate a bidirectional causality in Asia and Europe and a unidirectional relationship in Latin America. The findings also suggest that high-income countries attract less FDI as compared to low- and middle-income countries.

On the other hand, several recent empirical studies have found an inverted U-shaped relationship between FD and FDI, stating that up to a certain threshold level, the sign of the relationship becomes negative or negligible. Omran and Bolbol (2003) give evidence of a significant relationship between FD and FDI in 17 Arab countries over a period of 10 years. Taking into consideration that most of the middle eastern financial systems are bank based, the findings suggest that the impact of FDI on economic growth attained a threshold level of FD equal to 13.8% and 47% for domestic credit and commercial banks assets as a ratio of commercial banks and central bank assets, respectively. The association between FD and FDI is nonlinear and is positive after a threshold level of FD is attained, while it becomes negative beyond a certain threshold level (Dutta & Roy, 2011). The nonlinear association of the variables was also demonstrated in a recent study by Osei and Kim (2020) who investigated how an increase in FD impacts the positive effect of FDI on economic growth. Using a dynamic panel threshold model on a panel of 62 high- and middle-income countries, the authors provide evidence of a negligible growth effect of FDI when FD exceeds a threshold level of 95.6%. This negligible effect was described as the “diminishing returns” effect of FDI on economic growth.

Research Methodology

The main objective of this empirical analysis is to study the short- and long-run effects of FD on FDI flows to 16 MENA region countries, over a period of 19 years (2000–2018). The delimitation is conditioned by data availability. Since the data consists of 16 countries for 19 years, where N =16 is inferior to T =19, the system GMM estimator does not apply to our data. Therefore, since T > N, the panel ARDL approach is the most appropriate for the analysis.

The investigation of the short- and long-run relationship is made through the panel ARDL, which takes into consideration the speed of variables to adjust toward long- and short-term equilibrium situations. One of the main advantages of ARDL model is that it allows the analysis of long-run relationships between variables even though the order of their integration is different, that is, l(1) and l(0) in the case of this article. It also considers simultaneity bias and endogeneity by including lags of both dependent and independent variables. The model is based on three main estimators, namely, dynamic fixed effect (DFE), pooled mean group (PMG) and mean group (MG). The choice of the appropriate estimator is based on the Hausman test p value. The specification of the ARDL (p,q) model is considered (Pesaran & Shin, 1996) as follows:

Y is the log of net inflows FDI in US dollars, X is the vector set of all independent variables in the model including the log of GDP per capita, the gross fixed capital formation as a percentage of GDP, CPI as an annual percentage change, trade openness as a percentage of GDP, gross domestic savings as a percentage of GDP and three proxies of FD for which the value ranges from 0.002 to 0.765 (OFD representing the overall FD, FM representing FM and FI representing financial institutions’ development). ϑ and ∝ are the respective short-run dynamic coefficients of lagged dependent and independent variables, ∅ indicate the long-run dynamic coefficients and ∂ indicates the long-run equilibrium between Yit and Xit. A long-run relationship between FDI and FD exists when ∂ is negative and significant, therefore a Yit and Xit are said to be cointegrated.

The most important variables of our article are FDI and FD. FDI is the dependent variable which is measured in net inflows expressed in US dollars, while the main explanatory variable is the FD proxy. Literature suggests that the development of financial markets and financial institutions are an important subsidy of the process of economic growth (Levine & Zervos, 1996).

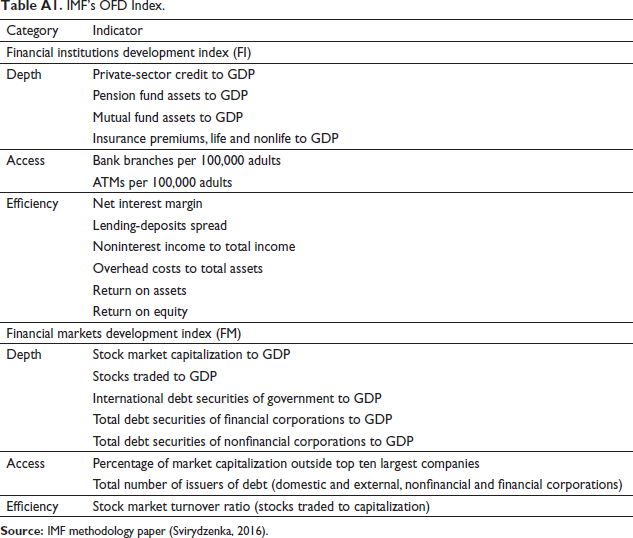

While most of empirical literature approximates the FD through two measures of financial depth (ratio of private credit to GDP and stock market capitalization to GDP), our article uses a proxy which is a composite index constructed through a PCA analysis in a methodology note published by the IMF (Svirydzenka, 2016). The index is composed of two main subindices representing financial markets (FM) and financial institutions’ (FI) development. Each of them is composed of three main subindices which measure how deep, efficient, and accessible financial markets and institutions are. The study employs the overall financial development (OFD) as well as the two main subindices in to show the long-run cointegration of FDI with both financial markets development (FM) and financial institutions development (FI). Therefore, the study runs three models, where Model 1 considers the OFD proxy, Model 2 uses FM along with FDI and control variables, and Model 3 analyzes the long-run relationship with FDI and FI. A decomposition of the FD proxies is given in Table A1.

The article is based on annual data representing economic growth, trade openness, gross fixed capital formation (GFC), gross domestic savings (GDS), inflation, FDI net inflows, and three proxies of FD covering the period 2000 to 2018. The data are all sourced from World Development Indicators (WDI) and UNCTAD online database. The analysis uses gross domestic product per capita (GDP) in constant US dollars to measure economic growth. Inflation (CPI) is measured by the consumer price index reflecting the annual percentage change. The long-run cointegration is expected to be negative. The variable (TO) measuring trade openness is included as it is expected to have a positive long-run cointegration relationship. It is represented by the ratio of exports and imports to the GDP as open economies present opportunities for doing business and therefore tends to be attractive to foreign investors (Cherkaoui & El Fakiri, 2021). The article also uses savings (GDS) which are measured by the gross domestic savings as a percentage of GDP and domestic investment (GFC) as a control variable for which the expected long-run cointegration to FDI is positive. Here, we measure domestic investment as the ratio of gross fixed capital formation to GDP.

Results and Discussion

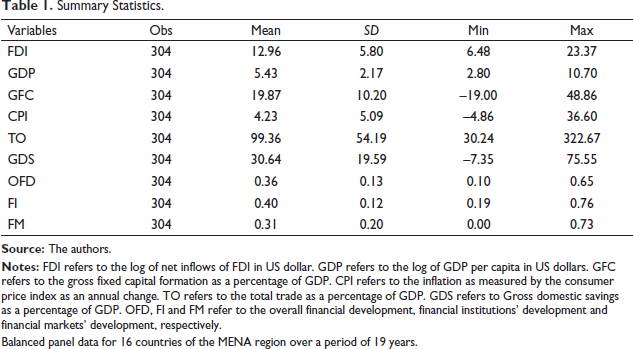

Summary Statistics

Table 1 summarizes the basic statistics of the mean, median, maximum, minimum, and standard deviation of our research variables. While trade openness and gross domestic savings exhibit the highest mean and standard deviation, FD indicators exhibit the lowest dispersion from the mean and standard deviation. The minimum observation amongst variables is represented by GFC, while the maximum observation is exhibited by trade openness.

Summary Statistics.

Balanced panel data for 16 countries of the MENA region over a period of 19 years.

Panel Stationarity Test

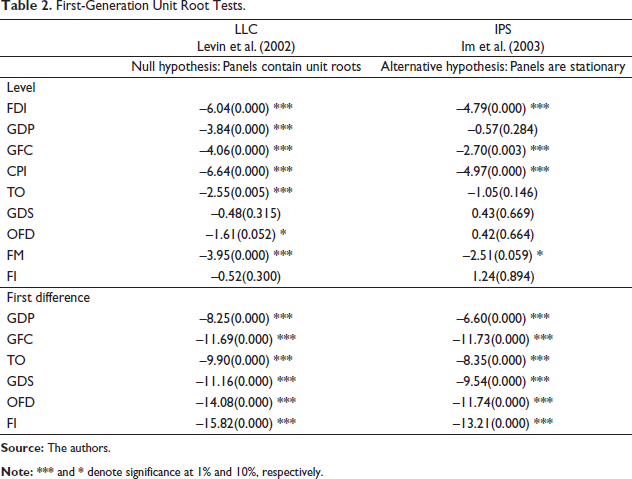

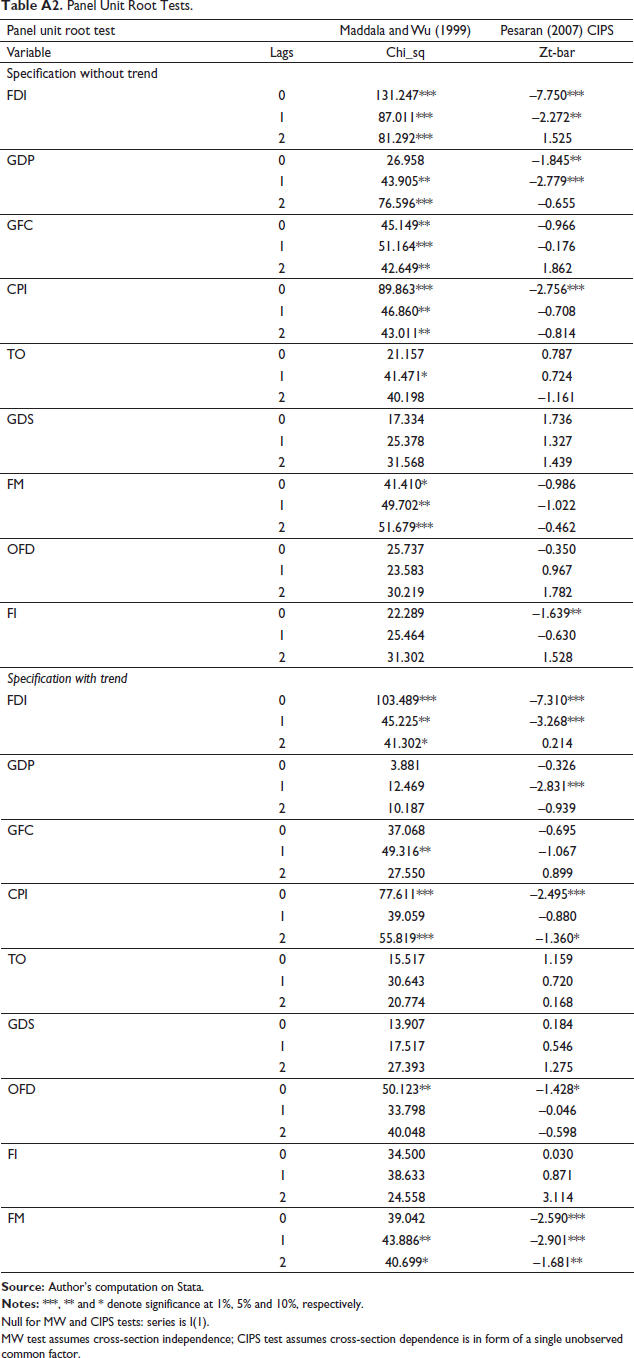

The article uses panel unit root testing models to test the stationarity of the variables and test their order of integration. We first run two first generation unit root tests for strongly balanced panels in particular Levin et al. (2002) and Im et al. (2003). Results of the first-generation unit root tests (Table 2) shows that the variables of different order of integration. FDI, GFC, CPI, and FM are stationary at level, while GDP, TO, GDS, OFD, and FI are stationary at first difference.

First-Generation Unit Root Tests.

Next, we run first- and second-generation unit root tests; Maddala and Wu (1999) and Pesaran (2007) which are applied on both level and first difference with and without trend. The first assumes cross-section independence and the second test assumes cross-section dependence in form of a single unobserved common factor. The results are presented in Table A2.

Panel Cointegration Analysis

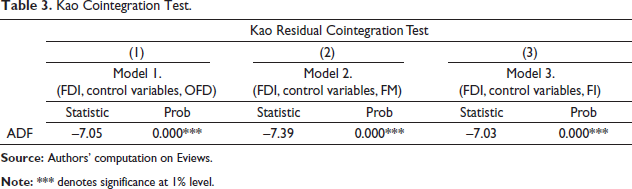

Based on the results of unit root tests, and to test for the existence or otherwise of a long-run relationship among the variables in our sample, this article employs two residual cointegration tests: Kao cointegration test and Pedroni cointegration test. The first residual cointegration test rejects the null hypothesis of no cointegration for the three models as presented in Table 3.

Kao Cointegration Test.

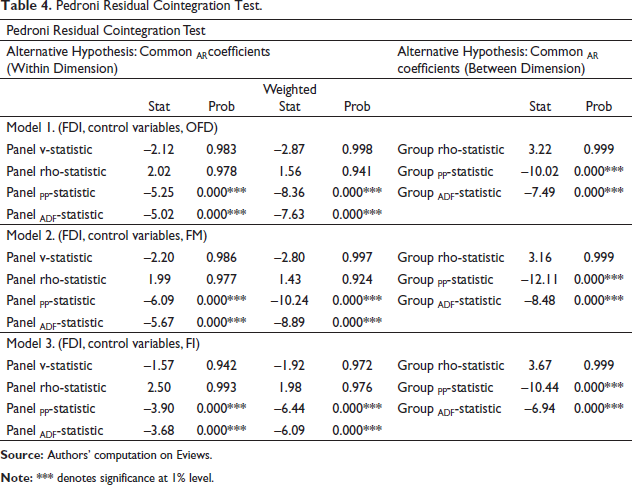

The Pedroni cointegration tests for two types of residuals; the first consists of four subpanel tests (panel-v, panel-rho, panel PP and panel ADF statistics), which pools the residuals along the “within dimension” of the panel; while the second panel consists of three subtests (group-rho, group PP and group ADF statistics) which pool the residuals along the “between” dimension of the panel.

The results reveal that the null hypothesis of no cointegration is rejected, which implies the existence of cointegration. Also, Pedroni (2002) suggests that to conclude the existence of cointegration, panel ADF and group ADF need to be considered as they provide reliable estimates. Results presented in Table 4 suggest the presence of a long-run relationship among the variables.

Pedroni Residual Cointegration Test.

As we find that all the variables are I(0) or I(1), we base our analysis on the Panel ARDL approach.

Analysis and Interpretation of Results

Main Estimation

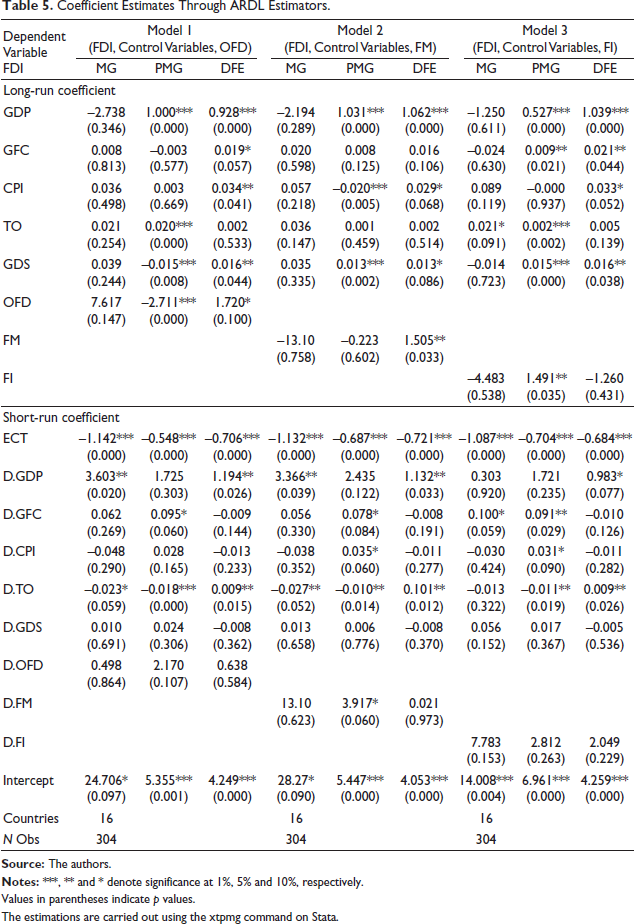

Table 5 reports the coefficient estimates of the long-run relationship using ARDL estimators, specifically MG, PMG, and DFE. The results reveal that the overall FD index has a significant negative impact. The financial markets development index has a negative but insignificant impact on FDI in the long-run according to PMG, while the long-run coefficient of the financial institutions’ development index is positive and significant. The MG estimator yielded to negative and insignificant coefficients for financial institutions development and financial markets indices, while the overall OFD proxy positively impacted the FDI entries. Also, the coefficients estimated by the DFE for both the OFD index and financial markets development index are statistically significant and positive, while the coefficient of financial institutions’ development index is negative and statistically not significant. The short-run coefficients yielded by the three estimators are positive and not statistically significant for the three models, except for the PMG estimation of the FM which is statistically significant at 10 percent level.

Coefficient Estimates Through ARDL Estimators.

Values in parentheses indicate p values.

The estimations are carried out using the xtpmg command on Stata.

Furthermore, to ensure which estimator is adequate, we used the Hausman test. The test rejects the null hypothesis of homogeneity of restrictions in the long run for MG and PMG, suggesting DFE estimator to be the most efficient and appropriate for our article. This finding applies to the three models in this study. Therefore, the following discussion focuses on the DFE estimates of the three models of our study.

Before analyzing the variable coefficients, we should mention that the error correction term is negative and significant for the three models. When there is a deviation from the long-run, the speed of adjustment to the long-run equilibrium is represented by the absolute value of the error correction term. The deviation speed can be achieved for a convergence rate of 70.6% for Model 1, 72.1% for Model 2, and 68.4% for Model 3. It is noted that the speed of adjustment to the long-run equilibrium between FM and FDI is much higher compared to the other two models.

Exploring the different determinants included in the DFE models, first, we find that in the long-run estimation, all control variables are positive. Market size as represented by GDP, domestic savings, and domestic investment are statistically significant. The findings indicate that a one percentage point increase in GDP increases FDI inflows by an average of 100.9 %, and a one percentage point increase in domestic savings and domestic investments increases FDI inflows by an average of 1.5% and 1.8%, respectively. While the impact of inflation is expected to be negative, the three models give evidence of a positive and statistically significant impact on FDI inflows to the selected countries. We explain the unexpected impact of inflation on FDI by a probable threshold effect. Except for the unexpected impact of inflation, the findings correspond with most of the previous research that attempted to analyze the impact of macroeconomic variables on FDI inflows.

The results of coefficients’ estimates in the short-run show that GDP per capita and trade openness are positive and statistically significant while inflation has a insignificant negative impact. These findings are not surprising as they have been previously demonstrated in other research works. Nevertheless, domestic savings and domestic investment as represented by gross fixed capital formation have a negative but statistically insignificant impact on FDI inflows in the short run. These findings suggest that domestic investment and domestic savings in MENA countries do not complement FDI inflows but are rather a substitute. In a research paper by Edwards (1995), the author demonstrated that in Asian and Latin American countries, the relationship between domestic savings and FDI inflows is negative. The paper translates the association by demonstrating that an increase of one percentage point in capital inflows results in a decrease of about 0.5% to 0.63% in domestic savings. Although it was statistically not significant, a one percentage increase in FDI decreased domestic savings by an average of 0.7% and domestic investment by an average of 0.9%.

Table 5 shows that, although FD proxies have a positive but statistically insignificant impacts on FDI inflows in the short run, the long-run coefficients are significant in Model 1 and Model 2. The estimates of the DFE showed that the OFD proxy and FM proxy have a statistically significant and positive impact on FDI, at 10% and 5%, respectively. On the other hand, the proxy of financial institutions’ development is statistically insignificant and has a negative impact on FDI inflow to MENA region countries in the long run. What is interesting in the findings is that the coefficients of FD proxies are quite large as compared to other control variables. This gives strong evidence of how important the proxies are for FDI inflows to MENA countries.

Overall, OFD and FM have a positive and statistically significant impact on long-term FDI at 10% and 5% levels, respectively. The findings suggest that a one percentage point increase in the OFD increases FDI inflows by 172%. The positive impact of OFD indicates that the financial system in MENA countries is modern. A well-developed financial system in these countries strongly attracts FDIs through the different functions of risk diversification, access to financial services, efficient allocation of resources, and faster technological progress. Nonetheless, the analysis of the impact gives an in-depth insight into how the different divisions (financial markets and financial institutions) of the FD impact the inflows of FDI to MENA countries. The findings suggest that, in the long run, financial institutions’ development is less attractive to FDI relative to FM. A one percentage point increase in the FM proxy increases FDI inflows to MENA region by 150%, while the coefficient of financial institutions’ development is statistically insignificant. This finding is of great importance to policymakers since it shows that well-developed financial markets are a crucial determinant of FDI entries; while financial institutions which are bank-based, require more reforms and need to be more efficient at allocating financial services. In the short run, the coefficients of the proxies are statistically insignificant and positive. Therefore, the findings suggest that an increase in the OFD of MENA countries and their financial markets increases the FDI net inflows to the sample countries of the region in the long run and that FDI inflows to the region are insensitive to FD proxies in the short run.

The results of this analysis provide important insights to the policymakers in the selected MENA countries. It is essential to pay attention to attracting FDI through developing the financial markets and pooling their domestic savings to enable efficient risk-sharing. Decision-makers must remove financial, economic, structural, and institutional barriers to the financial system and make the economy more attractive by implementing stable monetary and fiscal policies and liberalization strategies through privatization programs. The continuity in implementing these strategies is key to the success of the economies in the long term.

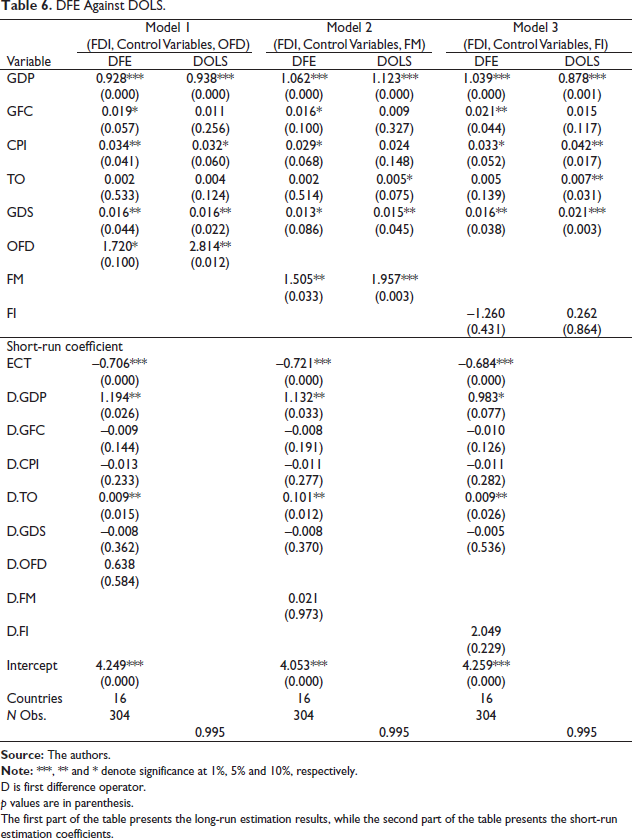

Robustness Check Estimates’ Comparison Between DFE Estimator and Dynamic OLS (DOLS) Model

To draw a conclusion about the long-run coefficients, our analysis is extended to account for the robustness of long-run parameters by re-estimating the coefficients through DOLS. The DOLS model is known for dealing with small sample size and simultaneity bias by taking the lags and leads of the first-differenced regressors (Stock & Watson, 1993). The model’s estimates are efficient and unbiased even in the presence of endogeneity issues and can adjust for possible autocorrelation and residual nonnormality. Therefore, the purpose of the comparison is to draw a conclusion about the efficiency and unbiasedness of our main model’s long-run estimates.

The DOLS estimates are presented in Table 6. For all models, R squared indicates that the regressors explain about 99.5% of the changes in FDI inflows to the MENA sample countries. The results indicate that all variables included in the model were rightly signed and significant as expected, except for the FI. While the proxy has a negative sign in the DFE model, the DOLS model indicates a positive coefficient. Despite the inverse sign, the estimates for the FI are insignificant in both models. Therefore, the findings validate the estimates from the DFE’s long-run estimates.

DFE Against DOLS.

D is first difference operator.

p values are in parenthesis.

The first part of the table presents the long-run estimation results, while the second part of the table presents the short-run estimation coefficients.

Conclusion

This article investigates whether a well-developed financial system leads to increased FDI inflows to selected MENA regions. The study emphasizes the development of financial markets and financial institutions and assesses, empirically, their individual impact on FDIs. For this purpose, we employed three different proxies of FD developed by the IMF. Initially, we split the analysis into three models: the OFD proxy was represented in Model 1, the FM proxy in Model 2, and the FI in Model 3.

Our research article investigates the impact of FD of 16 countries of MENA region on FDI entries over the period 2000–2018. Panel ARDL method, specifically DFE estimator, was used to investigate the long-run cointegration between FD proxies and FDI inflows to the selected countries. Findings suggest that, in the long run, financial institutions’ development is less attractive to FDIs relative to FM. A one percentage point increase in the FM proxy increases FDI inflows to MENA region by 150% while the coefficient of financial institutions’ development was statistically not significant. The OFD has a strong positive and significant impact on FDI entries, meaning that, even though financial institutions are not well developed, MENA countries succeed in their strategy to make FDI more attractive. Findings have important implications for the policymakers since they show that, in the long-run well developed financial markets are a crucial determinant of FDI entries, while financial institutions which are more bank-based, need greater reforms and are more efficient at allocating financial services. Nonetheless, FDI inflows to the region tend to be insensitive to FD proxies in the short run.

The findings of this article have certain limitations. First, the conclusions only apply to the selected countries, they do not reflect the entire MENA region. Second, the article used only some variables (GDP, trade openness, gross fixed capital formation, gross domestic savings, and inflation) amongst various others which were found to be important determinants of FDI, such as human capital development, infrastructure, and institutional quality (Cleeve et al., 2015; Dutta & Roy, 2011; North, 1990). Therefore, the variables of our study could not, solely, represent FDI determinants. Finally, the conclusions of this article do not exclude a possible nonlinear relationship between FDI and financial development. Therefore, further research is required to test whether the relationship between FDI and FD is monotonic and whether the impact of FD on FDI changes beyond a certain threshold level.

Appendix

IMF’s OFD Index.

Panel Unit Root Tests.

Null for MW and CIPS tests: series is I(1).

MW test assumes cross-section independence; CIPS test assumes cross-section dependence is in form of a single unobserved common factor.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflict of interest concerning the research, authorship, and /or publication of this article.

Funding

This work was financially supported by the National Center of Scientific and Technical Research (CNRST) Morocco in the context of the Research Excellence Fellowship Program grant number 21UM52019.