Abstract

This article examined the impact of the unanticipated outbreak of global public health crisis, COVID-19 pandemic, on the equity market performances and on the degree of integration of these markets in BRICS bloc. The empirical analyses lend support to the weakened equity market integration in the BRICS economies amid the pandemic, and the key driving forces include the rate of inflation, the real rate of interest, real exchange rate and composite leading indicator in the long-run, and trade performance and composite leading indicator in the short-run. The implications on the one hand, indicate increased opportunities for international portfolio diversification, and on the other hand, suggest for controlling the macroeconomic uncertainties of inflation, interest rate and exchange rate fluctuations during global health crisis to promote stable economic conditions for ensuring equity market integration in the long-run.

Introduction

International market integration, a multidimensional phenomenon, has been fostered across the globe with the rapid diffusion of information, substantial cross-border deregulation, and cross-country harmonization brought about by globalization and technology revolution (Gallo & Otrando, 2007; Mishra & Mishra, 2015). Recently, the degree of international market integration has been on the rise primarily due to legal relaxation in cross-border capital movements, lower transaction costs, reduced taxes and tariffs on foreign asset trading, and increased opportunity for holding more diversified asset portfolios (Marashdeh & Shrestha, 2010; Mishra & Mishra, 2020; Park, 2014). Specifically, the policy focus is on international financial market integration as it fosters capital flow among nations and contributes to their sustained growth (Hung, 2012; Mishra & Mishra, 2017). One direction of such international financial market integration is equity market integration which is particularly important for several reasons—first, it opens up the opportunities for holding portfolio of foreign financial assets (Gan et al., 2020; Mishra & Mishra, 2020; Vithessonthi & Kumarasinghe, 2016); second, it enlarges the opportunities for risk-sharing (Devereux & Yu, 2020; Marashdeh & Shrestha, 2010); third, it helps in reducing cost of capital and asset price volatility (Tai, 2007); fourth, it is a solution for financial instability and mal-allocation of resources (Trichet, 2005); fifth, it brings into practice innovative and cost-effective financial services (Giannetti et al., 2002); sixth, it improves market discipline and informational efficiency to strengthen capital market segment (Assidenou, 2011; Mishra & Singh, 2015; Reddy, 2003); and seventh, it augments domestic savings and investment, thereby contributing to total factor productivity (TFP) growth and economic growth while ensuring stable consumption pattern in economies (Levine, 2001; Park, 2014).

On the flip side, financial market integration has been observed to transmit financial and economic turbulences across countries, thereby making domestic markets unstable and inefficient (Berg, 1999; Devereux & Yu, 2020; Ferson, 2018; Gan et al., 2020). The occurrences of financial chaos of past decades, particularly global financial recession and Euro-Zone crisis, exemplify how integrated financial markets help in transmitting cross-border contagion and are prone to financial crises carrying increased risks of asset prices, return volatilities, and abrupt reversals in capital flows (Mishra & Mishra, 2020). It has implications for the investors who are always seeking a safe-haven for their investments. Particularly, in the post-global financial recession-era, international investors have been observed to reveal their investment preferences in relatively stable emerging capital markets of BRICS (Brazil, Russia, India, China and South Africa) (Dimitriou et al., 2013; Samar & Walid, 2019). In a study, Swamy and Narayanamurthy (2018) observed a growing level of capital inflows to BRICS countries being driven by their market size, rankings of ease of doing business and sovereign credit ratings. In the recent past, the BRICS economies have been recognized for their role in driving the global economic recovery and contributing to reduced poverty and inequality. Undoubtedly, these economies have aimed to promote economic growth and reduce the loss of foreign capital (Bouoiyour & Selmi, 2018), and have made significant achievements in the global trade flows (Rasoulinezhad & Jabalameli, 2018).

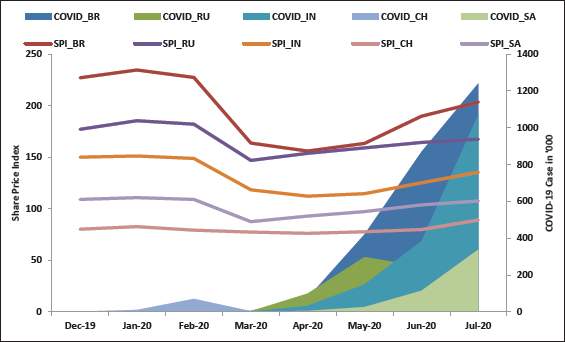

However, the abrupt outbreak of Coronavirus pandemic has upended the international order thereby denting the trade and capital flows and growth prospects across the globe. The equity markets of countries around the world strongly reacted to the within-country outbreak of the pandemic, and also reacted to the global demand-side and supply-side shocks caused by the COVID-19 pandemic in response to the investors’ behavior, particularly from the last week of February to the end of March, 2020. The markets showed a downturn when the Coronavirus made its way through countries across the globe, but revealed the signs of stabilizing trend in April when governments introduced monetary and fiscal interventions to combat the negative impacts of COVID-19. BRICS nations being some of the worst affected territories by the global health pandemic, sent their financial markets into turmoil almost at the same time as other countries on the globe. The total number of COVID-19 infection cases by end of July 2020 in Brazil, Russia, India, China and South Africa were 2,610,102, 834,499, 1,638,870, 87,489, and 482,169, respectively. These increased to 3,862,311 (47.98%), 990,326 (18.67%), 3,621,245 (120.96%), 89,895 (2.75%), and 625,056 (29.63%), respectively, by end of August 2020. This clearly indicates the severity of the Corona pandemic in BRICS nations which has caused multifarious damages in these economies, thereby adversely affecting the quality and quantity of their human resources. From the financial market perspective, the panics and pessimistic sentiments of investors caused severe plunges in market indices (see Appendix 1) and stock market returns in the BRICS bloc (see Figure 1 & 2).

The downturn in stock markets deepened when governments restricted domestic and international travels, and imposed outright lockdown of affected areas to contain the virus spread. The uncertainties of the pandemic also triggered a swift outflow of capital, causing a nosedive in the capital markets of the BRICS region. The governments across these countries implemented expansionary fiscal and monetary policies to give a timely boost to economies which also affected the movements in stock market indices. All these arguably can have influences on the dynamics of capital market integration in BRICS bloc.

In this backdrop, the current study examined the dynamics of the interconnectedness between the equity markets of BRICS nations amid the unprecedented novel coronavirus pandemic, and also made an effort to identify the significant macroeconomic indicators determining the strength of interconnectedness between these equity markets while controlling for the shocks of the COVID-19 pandemic. The outcomes of the study support the existence of equity market integration in BRICS economies both in the pre-COVID-19 and COVID-19 phases with the indication of the weakened degree of interconnectedness between these markets in the COVID-19 phase. The outcomes also indicate the dented long-run performance of stock markets, and their interdependency has been found to be negatively affected by changes in the rate of inflation, real interest rate, and the shocks of the coronavirus pandemic. This study contributes to the growing COVID-19 literature as follows. First, it examined the effects of the unanticipated outbreak of COVID-19 pandemic on BRICS; second, it complements literature on the conflicting views about the degree and dynamics of equity market integration in the BRICS region; third, this research is the first to study the degree of interconnectedness of BRICS equity markets amid the Corona pandemic; fourth, it is the first to identify the macroeconomic variables which can contribute to the strength of interconnectedness of BRICS equity markets amid the public health crisis. The remaining of the article is organized as follows: the next section reviews the relevant literature followed by the data description and methodology of the study; subsequent section analyses the data and discusses the findings; and lastly the conclusions of the work are presented.

Literature Review

The finance literature reveals the intensification of integration of financial markets primarily due to the espousal of financial liberalization measures by countries in the 1990s to foster the movement of foreign capital for strengthening the process of domestic capital formation in emerging as well as developed economies (Agénor, 2003; Ayuso & Blanco, 2001; Fahami, 2011; Matos et al., 2016; Worthington & Higgs, 2010). Although a plethora of studies are available on financial market integration, only a limited body of knowledge exists on the interconnectedness of the equity markets in BRICS countries. Furthermore, this limited knowledge also indicates conflicting evidence on the degree and dynamics of equity market integration in the BRICS region. We can classify the relevant studies according to three different strands: first, a group of studies found the presence of partial or incomplete integration of equity markets in BRICS economies (Al-Mohamad et al., 2020; Bai, 2008; Prakash et al,. 2017; Sharma et al., 2013; Singh & Sharma, 2012); second, another group of studies demonstrated presence of stronger and increasing integration among the BRICS stock markets (Bai, 2009; Bhar & Nikolova, 2009; Dasgupta, 2014; Joshi, 2013); and third, a few studies found no integration among the BRICS capital markets (Jeyanthi, 2012; Ouattara, 2017; Singh & Kaur, 2016).

In addition to these findings, a group of studies found existence of cointegration or long-run equilibrium relationship between the equity markets of BRICS countries (Chittedi, 2010; Naidu & Subbarayudu, 2014; Nashier, 2015). Another group of studies focusing on the dynamics of financial market integration during the period of financial crises such as Asian crisis, global financial crisis, European debt crisis, and so on, showed an increase in the degree of interconnectedness between stock markets (Jondeau & Rockinger, 2006; Mokni & Mansouri, 2017; Pereira, 2018). In this context, Lehkonen (2015) observes that the global financial crisis had increased the degree of stock market integration in emerging market economies and reduced it in developed economies. Some studies found an increase in the degree of stock market integration in BRICS region during and after the financial crises (Ahmad et al., 2013; Fahami, 2011; Gupta, 2011; Puah et al., 2015; Singh & Kaur, 2016).

Although empirical evidence on stock market integration is available amid financial crises, the literature is almost non-existent about its dynamics amid health crisis such as the ongoing COVID-19 pandemic. Park and García-Herrero (2020) finds Brazil, Russia, India, China and South Africa as the most COVID-19 affected countries after the U.S. as of August 5, 2020. Borio (2020) states that contractions in the global output and employment due to demand-side and supply-side shocks of COVID-19 pandemic is more intense than was observed during the Great Depression. In the financial market perspective, Zhang et al. (2020) observed that the increase in pandemic-induced global financial market risks has been substantial thereby causing significant loss-suffering by investors in a very short time. Park and García-Herrero (2020) observed that the sudden stop in portfolio inflows into the emerging market economies has been unprecedented in response to the Corona pandemic, and also the size of portfolio outflows is several times bigger than seen during the global financial recession of 2007–2008. Consequently, the transnational investors have made a swarm-like exit from the emerging markets in search of a safe-haven. This has increased the interconnectedness of stock markets to a considerable extent (Youssef et al., 2020). This observation has motivated us to examine the degree of interconnectedness between the equity markets in BRICS countries during the ongoing global health crisis. Since the pandemic has created repercussions on the stock market performances primarily through the fundamental and behavioral channels, we have also been motivated to determine the significant macroeconomic factors which exert effects on stock market performances, thereby affecting the degree of equity market integration.

It is commonly observed that the sudden outbreak of Corona pandemic has created difficulties for the correct determination of oil prices, exchange rates, inflation rates, trade performances and interest rates. Thus, referring to the extant literature, we believe that the stock market performances might have been influenced by these factors amid the COVID-19 pandemic. Tripathi and Kumar (2016) found inflation, exchange rate, money supply, oil price, and output as significant determinants of the stock return behavior in the pre and post-global recession periods. A similar observation has also been made by Chinzara (2011), Tsaurai (2018) and Demir (2019). Inflation reduces savings by people, shrinks investment opportunities, increases interest payment, and raises firms’ input and capital costs thereby adversely affecting stock returns (Asprem, 1989; Fama, 1981; Geske & Roll, 1983; Mukherjee & Naka, 1995; Naik & Padhi, 2012; Tripathi & Kumar, 2014, 2015a, 2015b). In the finance literature, the interest rate has also been observed to cause an increase in the financial cost and imbalances in investors’ portfolio of financial assets thereby inducing readjustments in risk-return trade-off through right portfolio selection (Asprem, 1989; Chaudhuri & Smiles, 2004; Mukherjee & Naka, 1995). The literature has also documented the impact of exchange rate fluctuations on the stock return behavior due to imbalances in export–import activities during the crises (Jefferis & Okeahalam, 2000; Ma & Kao, 1990; Maysami et al., 2004; Mukherjee & Naka, 1995; Sui & Sun, 2016; Tripathi & Kumar, 2015a). In a very recent study, Mroua and Trabelsi (2020) finds significant effects of changes in the exchange rate on stock market returns in the short and long-run. In another study, Gan et al. (2020) found that the macroeconomic variables are critical in shaping the stock market integration across national borders. Therefore, this study contributes to the literature in providing empirical evidence on strength of equity market integration amid the global spread of Coronavirus pandemic, and also in determining the important macroeconomic factors which drive stock market performances in BRICS economies.

Data and Methodology

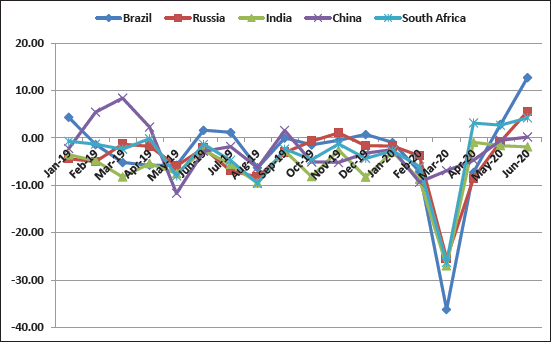

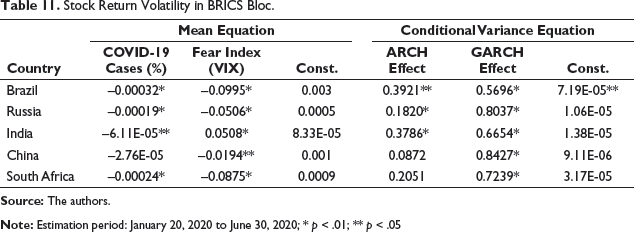

This article investigates the dynamics of the interconnectedness between the equity markets of BRICS countries covering the period of COVID-19. Precisely, it examines whether the equity market integration holds amid the unprecedented novel Coronavirus pandemic in BRICS economies. Furthermore, an effort has been made to identify the significant macroeconomic indicators determining the interconnectedness between the equity markets of BRICS nations while controlling for shocks of the COVID-19 pandemic. Given these objectives, there are two hypotheses of the study: (a) based on the observation of unexpected nosedive of the stock market returns between February to April 2020 and subsequent recovery (see Figure 2), we hypothesize that the outbreak of COVID-19 pandemic does not have a significant impact on the equity market integration in BRICS economies; and (b) assuming that the pandemic can exert an impact on equity markets propagated through the investors’ behavior and leading macroeconomic indicators, we hypothesize that the rate of inflation, the real rate of interest, real exchange rate, trade performance, the OECD composite leading indicator reflecting the economic movements in qualitative terms, and the shocks associated with the outbreak of Coronavirus can have a significant bearing on the stock market interconnectedness in BRICS economies. This hypothesis is based on the observation that the panics and uncertainties of the pandemic caused financial market instabilities (Zhang et al., 2020) being triggered via the investors’ pessimistic sentiments on future market returns (He et al., 2020; Huo & Qiu, 2020; Liu et al., 2020; Mishra & Mishra, 2020; Mishra et al., 2020; Sen & Mallick, 2020; Shanaev et al., 2020; Wagner, 2020). Corroborating these observations, we estimated stock return volatilities in BRICS countries. Also, we employed the event study approach to confirm whether the stock markets in these countries have been adversely influenced by the investors’ behavior triggered by global announcement of deadly spread of the Coronavirus. The results presented in Appendix 1 confirm the influence of weakened investors’ behavior on stock market movements and explains the sudden plunge in BRICS markets.

Based on this observation and given that the macroeconomic activities have large impacts on stock price movements, and investors generally use macroeconomic determinants for investment decisions (Talla, 2013). Therefore, we propose the hypothesis that pandemic has worked to influence the stock market behavior in BRICS through the leading macroeconomic indicators such as interest rate, exchange rate, inflation rate and trade performance.

The existing literature argues for inverse relationship between the interest rate and the stock market returns. Lower interest rates resulting from cheap money policy makes fixed income securities less attractive and raises the value of equity as an alternative to holding bonds, thereby increasing stock market returns (Banerjee & Adhikary, 2009). On the contrary, higher interest rates resulting from the tight money policy tend to reduce the stock market returns. Amid the pandemic, monetary authorities across affected countries were resorted to the implementation of cheap money policy which by lowering interest rates might have discouraged investments on fixed-income assets and induced the investors to make investments on equities for higher yields thereby indicating the existence of an inverse relationship between the interest rate and the stock market returns. So we propose that interest rate and stock market are negatively correlated.

Another important macroeconomic determinant is exchange rate. Exchange rate being international in nature affects global trade and influences firms’ real income and output. Additionally, it affects their expected future cash flows which impacts on the balance sheets that lead to stock price fluctuations (Okechukwu et al., 2019). Dornbusch and Fisher (1980) termed this relationship between exchange rate and stock market return as flow-oriented model according to which a positive relationship holds between them.

On the contrary, another strand of knowledge argues that the presence of extremely high or low exchange rate triggers a negative relationship between exchange rate and stock market in financial markets that are more integrated (Caporale et al., 2014; Cavusoglu et al., 2019; Cenedese et al., 2015; Kasman et al., 2011; Liang et al., 2013; Lou & Luo, 2018; Tsai, 2012). It may be due to market expectations toward international trade restrictions (Gokmenoglu et al., 2021) which affect the capital account transactions having a bearing on exchange rates. Branson et al. (1977) termed this relationship between exchange rate and stock market return as portfolio-balanced model according to which a negative relationship holds between them. During the pandemic, exchange rates of different countries have depreciated owing to the decline in exports and the collapse of oil price due to imposition of sudden international movement restrictions (Nwosa, 2021). This has been argued to create a downward pressure on exchange rate, leading to the exchange rate depreciation which is expected to have negative effects on stock market performances in accordance with the portfolio-balanced model. Hence, we propose that exchange rate and stock market are negatively correlated.

On inflation and stock market relationship, one strand of knowledge, termed as Fisher Effect, argues for positive correlation between them, and holds that stocks provide an efficient hedge against rising inflation rates (Fisher, 1930). Another strand of knowledge, known as Proxy Effect, argues for negative correlation between inflation rate and stock market returns, and holds that rising inflation rate depresses real economic activities, thereby negatively affecting firms’ future cash flows (Fama, 1981). During the pandemic, the real economic activities have been depressed across the affected economies which by negatively affecting future cash flows of the corporate are likely to validate Proxy Effect of Fama (1981) while refuting the Fisher Effect (Fisher, 1930). So, we propose the hypothesis that inflation and stock market are negatively correlated.

Another important macroeconomic indicator is trade performance. Better trade performances at the international level contributes to rising market value of corporate through increased market capitalization of corporate, and thus, stock market return is positively influenced. And the reverse is expected when there is a negative trade performance due to national/international shocks. The unprecedented COVID-19 pandemic revealed an unavoidable decline in trade and output across the globe, and thus, its impact on bilateral trade is significant and adverse, ceteris paribus, on both the exporter’s and importer’s side (Brodzicki, 2020). In this line, we propose that the trade performance and stock market return in BRICS are negatively correlated.

Data

In this study, we have selected Sao Paulo Bovespa Index from Brazil, MOEX Russia Index from Russia, NIFTY 50 Index from India, Shanghai SE Composite Index from China and Johannesburg Stock Exchange All Share Index from South Africa as the representative equity markets based on the availability of weekly and monthly data. We have preferred to use weekly data on these stock price indices to examine the dynamics of the equity market integration in BRICS to overcome the econometric issues related to autocorrelation and noise associated with the daily observations (Al-Mohamad et al., 2020; Wang et al., 2003). The weekly data on these indices were compiled from yahoo finance for the period January 1, 2010 to July 28, 2020. These data were taken in their natural logarithms to avoid the problems of heteroskedasticity, and the log-transformed series have been designated BRA, RUS, IND, CHN and ZAF, respectively, for Brazil, Russia, India, China, and South Africa. The empirical analyses based on the weekly data on stock indices of BRICS countries have been split up into three parts: pre-COVID-19 outbreak phase, COVID-19 phase, and the whole period. Referring to the report by South China Morning Post (Ma, 2020) concerning the tracing of the first COVID-19 case in the Hubei province in China, based on the government data, we have taken November 17, 2019 as the threshold date. Therefore, the pre-COVID-19 period is from January 1, 2010 to November 16, 2019; the COVID-19 phase is from November 17, 2019 to July 28, 2020; and the whole period is from January 1, 2010 to July 28, 2020.

Furthermore, we have used monthly data on real stock market return (SMR), rate of inflation (INF), the real rate of interest (INT), the real exchange rate (EXR), trade performance (EXIM), and the OECD composite leading indicator (CLI) because we have studied the equity market integration in BRICS while controlling for the macroeconomic indicators. The use of monthly data was preferred to offset the problems of non-synchronous infrequent trading in BRICS equity markets (Ibrahim, 2005; Karim & Karim, 2012), and to uphold the data alignment concerning stock market indices and macroeconomic indicators (Gan et al., 2020). The monthly data were compiled from the OECD databank for the period January 2010 to June 2020. Among these monthly datasets, the trade performance proxy is the terms of trade for the BRICS economies, and real exchange rate, trade performance and composite leading indicator are all taken in their natural logarithms while all other variables are in percentage form. We have also created a dummy variable COVID to gauge the likely impact of the pandemic on stock market integration in BRICS economies. We have taken the real stock market return (SMR) as the measure of equity market which is constructed using the formula:

Empirical Methodology

The methodologies employed to carry out the empirical exercises in the study has been divided into two heads—first, the Johansen’s multivariate cointegration approach has been used to investigate the possibility of the existence of equity market integration in BRICS economies based on the argument that the stock markets are integrated when they share a long-run equilibrium relationship among themselves (Al-Mohamad et al., 2020; Bachman et al., 1996; Karim & Karim, 2012; Mishra & Mishra, 2020; Mohd. Yusof & Abd. Majid, 2006); and second, the panel model approach has been employed to determine the macroeconomic factors influencing equity market integration in BRICS economies following Eng and Habibullah (2006), Gan (2014), Lu (2017) and Gan et al. (2020). The entire empirical work has followed the steps as discussed below.

Cointegration Test

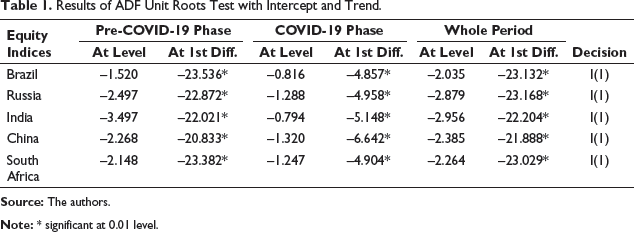

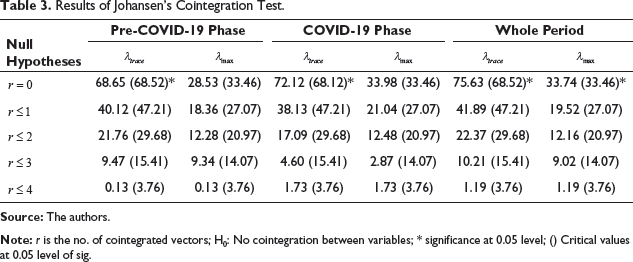

First, we employed the Augmented Dickey-Fuller (ADF) unit root test to check the stationary properties of the weekly time-series under consideration (Dickey & Fuller, 1979). Then we applied the cointegration test to check the existence of long-run interconnectedness between the equity markets in BRICS economies (Johansen, 1988; Johansen & Juselius, 1990) based on the finding that the equity market variables are all integrated of order one in the pre-COVID-19 phase, COVID-19 phase and in the whole period.

Cross-Sectional Dependency Test

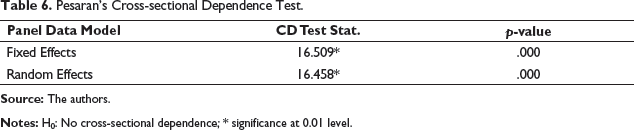

Second, we have tested the cross-sectional dependency among the monthly time-series by using the CD-test as proposed by Pesaran (2004) setting the null hypothesis as “there is cross-sectional independence,” which means the errors in our cross-section units are not correlated. The rejection of the null hypothesis would imply that the BRICS economies are integrated entities. The CD test statistic is given by

Stationarity Test

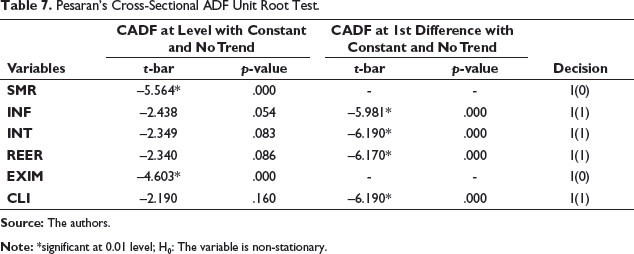

Third, we tested the stationarity of the monthly time-series variables under study for appropriate panel model selection and stability of outcomes. Since first-generation stationarity test methods could lead to significant size distortions in the presence of neglected cross-section dependence (Baltagi & Pesaran, 2007), we employed cross-sectional Augmented Dickey-Fuller (CADF) unit root test as proposed by Pesaran (2007) which accommodates for cross-sectional dependence among the variables of interest using the CADF regression:

Panel Model Approach

Since none of our monthly time-series variables is integrated of order two, the appropriate panel model technique for the study of stock market integration is the Autoregressive Distributive Lag (ARDL) as proposed by Pesaran et al. (1999). The following regression is used for the estimation where

The ARDL panel model can be estimated based on the Mean Group (MG) and Pooled Mean Group (PMG) estimators as follows, and then the Hausman test can be used to choose the best estimator.

In this panel specification, the equity market integration in BRICS requires a stable long-run relationship between the stock market return and other variables of interest. This is indicated by the significantly negative value of

Reliability and validity of PMG estimates will make the results of the panel ARDL approach robust when perceived doubt of the existence of endogeneity issue is eliminated. Since the error term in the panel data model contains both country-specific and time-specific information, the endogeneity problem may arise due to the correlation between the predictors and the error term. But, in the PMG based panel ARDL model, this potential endogeneity issue is resolved as it includes lags of dependent and independent variables (Pesaran et al., 1999; Pesaran & Shin, 1999). When the lag selection is appropriate in a panel ARDL model, the residual correlation is eliminated thereby mitigating the problem of endogeneity (Ali et al., 2016). In other words, the endogeneity problem is prevailed over by estimating ARDL with sufficiently long lags provided the explanatory variables are not cointegrated among themselves and provided the focus is on long-run parameters (Pesaran & Shin, 1999, pp. 372–373, 384–385). Thus, panel ARDL approach can provide unbiased and consistent estimates along with valid t-statistics in spite of the possibility of the presence of endogeneity (Harris & Sollis, 2003; Jalil & Ma, 2008). Menegaki (2019) also stated that PMG estimates are robust to endogeneity and thus, superior to other estimates. Hence, we cross-checked the panel ARDL estimates against the suspected endogeneity by appropriately selecting the lags.

Results and Discussion

Interconnectedness Between the BRICS Equity Markets amid COVID-19

Results of ADF Unit Roots Test with Intercept and Trend.

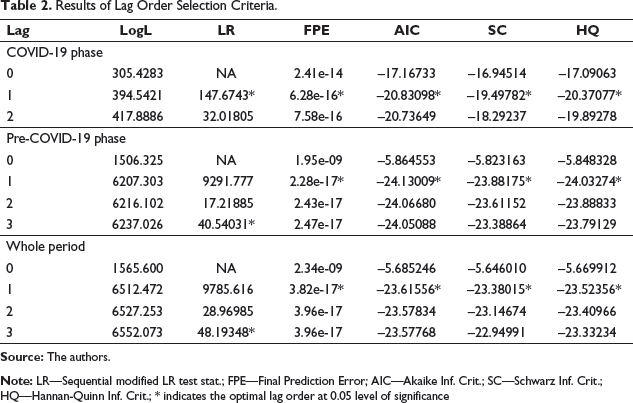

Results of Lag Order Selection Criteria.

Results of Johansen’s Cointegration Test.

Given that the variables are cointegrated and only one cointegrating vector exists, we can specify the equilibrium correction model for the pre-COVID-19 and COVID-19 phases as follows:

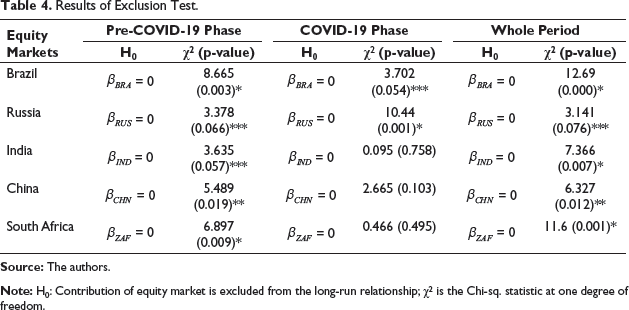

Results of Exclusion Test.

In the pre-COVID-19 phase, the null hypothesis is rejected for the contribution of equity markets of Brazil and South Africa at 0.01 levels of significance; of China at 0.05 levels of significance; and of Russia and India at 0.10 levels of significance. Thus, in the pre-COVID-19 phase the financial integration existed between the equity markets of BRICS countries. However, the results for the COVID-19 phase infers the existence of financial integration among the Brazilian and Russian equity markets, while other equity markets under BRICS contributed nothing to the long-run relationship among the stock markets of BRICS economies. This means the unexpected outbreak of COVID-19 at the global level eroded the equity market integration in BRICS nations thereby providing opportunities for portfolio diversification. Furthermore, we found that the equity market integration upholds among the BRICS economies in the full sample period.

Results of Weak Exogeneity Test.

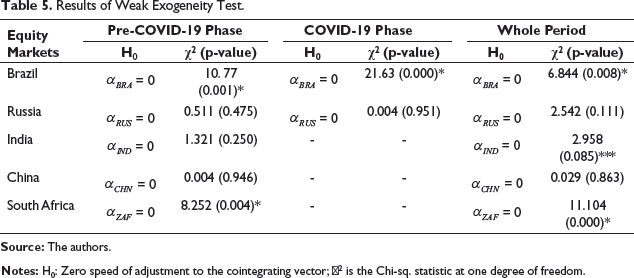

In Table 5, we have not reported the outcomes of the weak exogeneity test for those equity markets of the BRICS region which do not contribute to the cointegrating relationship. In the pre-COVID-19 phase, all the equity markets contribute to the cointegrating relationship, and thus, included in the weak exogeneity test. It is inferred that the null hypothesis is rejected only for Brazilian and South African stock market indices in the pre-COVID-19 phase. It indicates that these two equity market indices are endogenous to the system, that is, they are expected to deviate from the long-run relationship in the short-run and also adjust to the changes in Russian, Indian and Chinese equity market indices that are exogenous to the system. This adjustment will bring back the long-run relationship. Similarly, in the COVID-19 phase, the null hypothesis of weak exogeneity is rejected for the Brazilian stock market indicating its endogenous nature. So, its short-run changes will adjust to changes in the Russian stock market index to reinstate the equilibrium relationship. Thus, in the COVID-19 phase, Russian stock market index is exogenous to the system. Furthermore, in the full sample case, Brazilian, Indian and South African stock market indices are endogenous to the system whereas that of Russian and Chinese are exogenous.

Having detected the endogenous and exogenous variables in the pre-COVID-19 and COVID-19 phases, we can depict the long-run relationship in terms of normalized cointegrating equations. This normalization is made around the stock market indices which significantly contribute to the long-run relationship, endogenous to the system and depicts the largest value of chi-square statistics for weak exogeneity test (Al-Mohamad, 2016). Keeping in view these criteria, the normalization is made around the stock market index of Brazil both in the pre-COVID-19 and COVID-19 phases whereas around the stock market index of South Africa in the whole period. Thus the following cointegrating equations have been obtained:

Pre-COVID-19 Phase: BRA = 0.492RUS + 1.499IND – 0.558CHN – 1.553ZAF

COVID-19 Phase: BRA = 2.302RUS

Whole Period: ZFA = –0.610BRA + 0.261RUS + 0.943IND – 0.277CHN

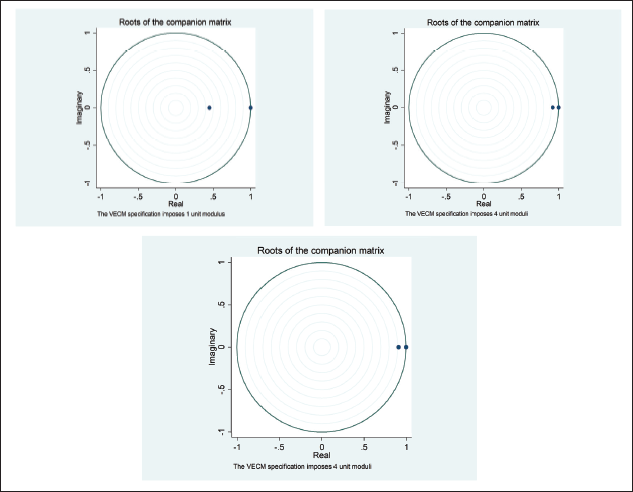

It is important to note that the above mentioned cointegrating relationships are stable as indicated by the strict presence of an eigenvalue that is less than one in each sample case (see Figure 3). The cointegrating equation for the pre-COVID-19 phase suggests that 1% increase in the stock market index of Russia leads to 0.49% increase in the Brazilian stock market index; 1% increase in the stock market index of India leads to 1.49% increase in the Brazilian stock market index; 1% decrease in the stock market index of China leads to 0.56% increase in the Brazilian stock market index; and 1% decrease in the stock market index of South Africa leads to 1.55% increase in the Brazilian stock market index. So, in the pre-COVID phase Russian and Indian equity markets positively contribute to the long-run equilibrium relationship with Brazilian stock market whereas this relation is negative for Chinese and South African stock markets.

However, in the COVID-19 phase such a long-run equilibrium relationship has been impaired due to the non-contribution of Indian, Chinese and South African stock markets. In the COVID-19 phase, only Russian stock market is positively contributing to the cointegrating relationship with that of Brazil. Precisely, 1% increase in the stock market index of Russia leads to 2.30% increase in the Brazilian stock market index. Similarly, it has been observed that Russian and Indian stock markets positively contribute to the long-run relationship with the South African stock market whereas Brazilian and Chinese equity markets exert negative contributions in the full sample case. From the above discussion, it is apparent that the Brazilian stock market is influenced by other BRICS equity markets in both the pre-COVID-19 and COVID-19 phases, but the degree of such integration has been weakened by the non-contribution of all BRICS partners other than Russian market. Such a reduced degree of equity market integration has increased the opportunities for portfolio diversification among the BRICS markets. In other words, the equity markets of BRICS countries can now be counted as destinations for portfolio diversification at the global level. Having determined the degree of financial integration between BRICS stock markets in different sample cases, it is also imperative to know the macroeconomic factors that influence the performance of different stock markets thereby determining the degree of integration among them. This has been taken care of in the next section.

Macroeconomic Determinants of Equity Market Integration in BRICS amid COVID-19

Pesaran’s Cross-sectional Dependence Test.

Pesaran’s Cross-Sectional ADF Unit Root Test.

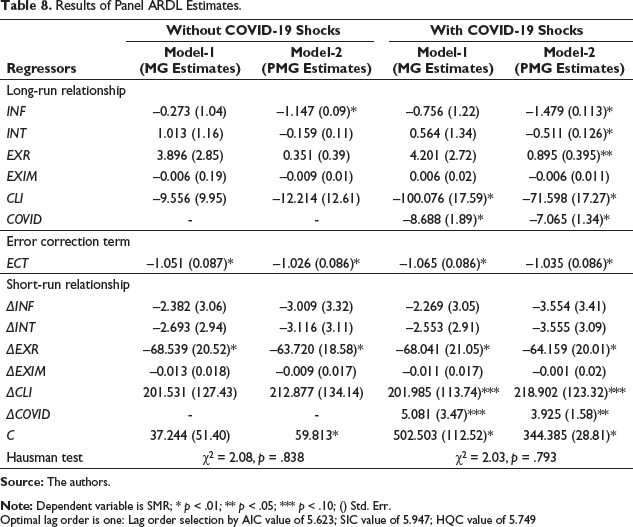

Results of Panel ARDL Estimates.

Optimal lag order is one: Lag order selection by AIC value of 5.623; SIC value of 5.947; HQC value of 5.749

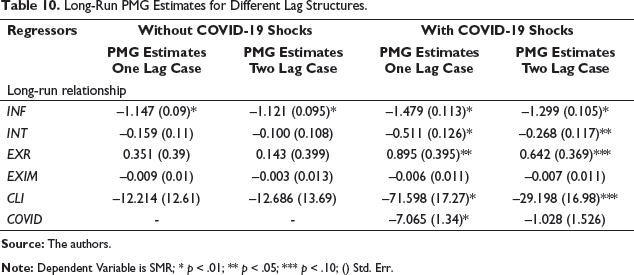

We estimated the panel model with and without the COVID dummy to find out the impact of coronavirus pandemic on the equity market integration. In both these cases, the Hausman test statistic suggests for PMG estimates and thus, we can pool the data of all the regressors by imposing long-run homogeneity. We observed that the standard errors have been reduced indicating that the PMG estimates are consistent and efficient over MG estimates with and without COVID dummy.

The error correction coefficient in PMG estimates is significantly negative indicating thereby the convergence to long-run equilibrium from any short-run deviation. From the PMG estimates, it is observed that the cointegration of equity market returns in BRICS holds in both the situations—with and without COVID-19. Given that the outbreak of Corona pandemic has had consequences for stock market returns transmitted through changes in investors’ behavior and movements in leading macroeconomic indicators, it is found that only inflation rate is the significant determinant of equity market integration in the long-run when we do not control for COVID-19 outbreak.

Furthermore, it is significantly found that the equity market integration in BRICS is determined by the rate of inflation, real rate of interest, real exchange rate, and composite leading indicator of OECD in the long-run when we control for the outbreak of COVID-19 pandemic. This is to be noted that the impact of COVID-19 pandemic on equity market linkages is significantly negative in the long-run, but positive in the short-run. This may mean that the investors consider the era of market distress to diversify their portfolios in anticipation of making abnormal gains in the short-run while such a possibility does not arise in the long-run. In other words, the unexpected outbreak of Coronavirus has had implications for asset pricing efficiency in the short-run. Moreover, the directions of the impact of the rate of inflation and the real rate of interest are negative on stock market returns in BRICS as expected in the short and long-run, but significant only in the long-run. The impact of the real exchange rate is significantly negative in the short-run but not in the long-run. The trade performance is neither significant in the short-run nor in the long-run despite having the expected negative signs. The composite leading indicator of OECD is significantly positive in the short-run but not in the long-run. This indicator being the proxy for cyclical fluctuations does not indicate the possibility of any unexpected upturns/downturns in the long-run.

Therefore, the equity market integration in BRICS has been influenced negatively by the Corona pandemic when its uncertainties and panics are transmitted to determine the stock market returns through rate of inflation, the real rate of interest, real exchange rate and composite leading indicator in the long-run, and through trade performance and composite leading indicator in the short-run.

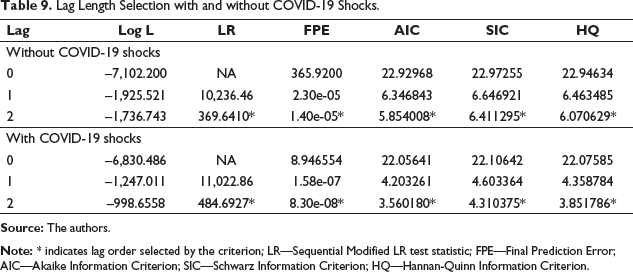

Lag Length Selection with and without COVID-19 Shocks.

Long-Run PMG Estimates for Different Lag Structures.

Concluding Remarks

This study examined the integration of equity markets in BRICS economies with leading macroeconomic indicators and in the presence of sudden outbreak of COVID-19 pandemic. The findings of the study are noteworthy—(a) the cointegration analysis reveals the existence of equity market integration in BRICS economies both in the pre-COVID-19 and COVID-19 phases with the indication of the weakened degree of interconnectedness between these markets in the COVID-19 phase; (b) the panel model estimation suggests for the existence of a long-run relationship between stock market returns and its determinants while controlling for the uncertainties of Corona pandemic; (c) the significantly negative error correction coefficient suggests a rapid return to long-run equilibrium when there is any deviation in the short-run. The policy implication is that the market participants can optimize equity returns from cross-border investments through portfolio adjustments in favor of foreign stocks. Furthermore, the results imply that the policymakers should control the macroeconomic uncertainties such as inflation, interest rate and exchange rate uncertainties during global health crisis to promote stable economic conditions. However, the study has obvious limitations in considering weekly and monthly data. So, the use of high-frequency data such as daily data on stock market returns, rate of inflation, interest rate, exchange rate and the announcement of new COVID-19 cases per day can help in obtaining better empirical insights which we left as the future course of research.

APPENDIX 1

Stock Market Responses to the Pandemic in BRICS Bloc

Stock Return Volatility in BRICS Bloc.

Cumulative Abnormal Stock Returns in BRICS Bloc.

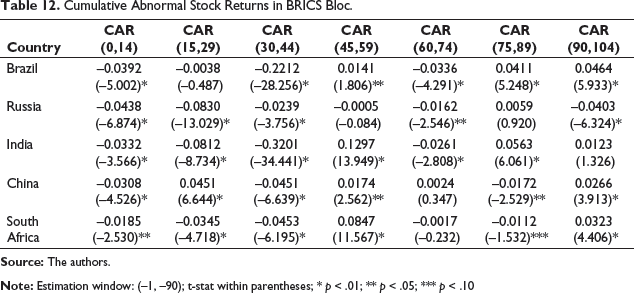

Furthermore, to learn how the rapid spread of coronavirus has affected the sentiments of investors, first we argue that worldwide announcement of deadly spread of COVID-19 infection adversely influenced the investors’ behavior, and then we confirmed it through the event study approach by assuming that the sudden media announcement made by Zhong Nanshan, the high-level expert group leader of NHFC of China, on January 20, 2020 about the possibility of spread of novel coronavirus among people across the globe as the event date in line with other studies (Liu et al. 2020; Mishra & Mishra, 2020). Assuming a 90-trading day estimation period for the event study, we observed that significant negative cumulative stock market returns persisted in the BRICS bloc over a period of 44 trading days or longer from the event date except for China. All these observations led us to hypothesize the propagation of the impacts of the global spread of COVID-19 infection on equity markets through investors’ behavior.

Footnotes

Acknowledgements

We sincerely acknowledge the suggestions of anonymous referees and editors of the journal for their valuable comments which were instrumental in bringing out this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.