Abstract

The willingness of commercial banks to provide loans is determined by various factors. In this regard, this paper provides empirical evidence on determinants of bank lending in Nigeria. The parsimonious model of this study investigates the impact of growth in loan-to-deposit ratio, growth in inflation, growth in broad money, and growth in bank capital on growth in bank lending using annual data from 1961 to 2016. This study adopts the autoregressive distributed lag (ARDL) bounds testing approach and Granger causality tests to investigate the relationship and direction of causality among the variables, respectively. The Granger causality tests show that growth in broad money Granger-causes growth in bank lending, while there is no causality from other explanatory variables to bank lending in Nigeria. Also, this study shows that growth in bank lending Granger-causes growth in loan-to-deposit ratio and growth in inflation in Nigeria. Thus, this paper argues that commercial banks in Nigeria exhibit stern concern for their liquidity and capital adequacy positions while acting as financial intermediaries. Additionally, this paper argues that the Central Bank of Nigeria (CBN) possesses “paper-based” independence.

Introduction

In every economy, the financial sector is designed to drive economic growth. However, causality results on the finance–growth relationship from different countries remain inconclusive, with unresolved arguments. For instance, the existing studies of Odedokun (1996), Mahran (2012), Marashdeh and Al-Malkawi (2014), Kumar (2014), Fethi and Katircioglu (2015), Deyshappriya (2016), Bist (2018), and Taivan (2018), among others, find evidence to support the finance-led growth view or supply-leading hypothesis. On the other hand, studies such as Hassan et al. (2011), Ndlovu (2013), Pan and Mishra (2018), and Nasir et al. (2018), among others, support the growth-led finance or demand-leading hypothesis. In a dual-causality context, the studies of Calderon and Liu (2003), Ndako (2010), Ogbonna et al. (2013), Adeyeye et al. (2015), Kyophilavong et al. (2016), Taivan (2018), Abosedra and Sita (2018), and Oyebowale and Karley (2018), among others, find evidence to support the bidirectional or feedback hypothesis. Furthermore, the studies of Akbas (2015), Nyasha and Odhiambo (2015), Adeniyi et al. (2015), and Pradhan (2018), among others, find evidence to support that finance does not impact economic growth, or the neutrality hypothesis. Thus, the significance of the financial sector on economic growth remains a topic for continued research.

Historically, studies on the significance of the financial system in enhancing economic growth have specifically focused on the relevance of banking, including the studies of Bagehot (1873) and Schumpeter (1911). These aforementioned seminal studies emphasize the essential role of the banking system in stimulating economic growth through their special function of discovering and funding productive investments. Conversely, the view of Robinson (1952) accentuates that banks perform a passive role in stimulating economic growth. Lucas (1988) argues that the role of the financial system in the process of economic growth is “badly over-stressed.” Nevertheless, the efficiency of the banking system in an economy remains a main determinant of macroeconomic performance and stability (Alexiou et al., 2018; Fu et al., 2018). This assertion is supported by the global economic problems caused by the 2007–2008 financial crisis and other great depressions.

In line with the ongoing discussion, the influence of the banking system in an economy focuses on two main channels: credit allocation (Schumpeter, 1934) and capital accumulation (Hicks, 1969). On credit allocation, the view of Schumpeter (1934) postulates that improved financial intermediation and innovation in an economy drives economic growth, which helps to boost investment and productivity. As regards the capital accumulation role of banking, Hicks (1969) affirms that the financial intermediation function of banks helps to diversify risks and reduces transaction costs in the mobilization of savings. According to Oyebowale and Karley (2018), risk diversification in the financial intermediation process is encouraged for both saving and investing economic units.

Clearly, the credit allocation role of commercial banks from savings-surplus units (SSUs) to savings-deficit units (SDUs) explains the bank lending channel of monetary policy transmission through supply of bank loan. The transmission mechanisms of monetary policy to the real economy is a key topic that has been brought into focus with the attention of scholars in macroeconomics (Ramey, 1993), as the transmission mechanisms serve as tools for monetary authorities to influence activities in the real economy (Apergis et al., 2015). The literature of Mishkin (1996) provides a comprehensive discussion about the channels through which monetary policy transmits into the real economy. The main channels are the traditional interest rate channel (money channel view) and credit channel (credit channel view).

The money channel view focuses on the influence of interest rates on aggregate demand. According to Nilsen (2002), the money channel view posits that when central banks reduce reserves, banks reduce their demand deposits due to higher costs of funds. Consequently, in situations when prices are sticky, the reduction in real balances of banks increases real interest rates to curtail interest-responsive spending and economic activity (Nilsen, 2002). However, the credit channel view emanates due to problems of information asymmetry in the credit markets through the bank lending channel and the balance sheet channel. The bank lending channel focuses on the supply of loans by banks and the notion that there are no other perfect substitute sources of funds (Mishkin, 1996). On the other hand, the balance sheet channel focuses on how the net worth of business firms creates adverse selection and moral hazard issues in lending to firms (Mishkin, 1996).

Literature Review

The Bank Lending Channel

Monetary authorities use the interest rate channel and the bank lending channel as a sub-channel of the credit view to implement monetary policies within an economy. For instance, an expansionary monetary policy through the interest channel reduces interest rate in order to lower the cost of capital; this would further lead to an increase in investment, spending and increase in aggregate demand and output, concurrently. On the other hand, an expansionary monetary policy through the bank lending channel increases bank deposits and reserves, causing an increase in the availability of bank loans to boost investment and consumer spending. Going by the main focus of this research, understanding the bank lending channel is significant in designing and implementing a suitable monetary policy framework (Zulkhibri, 2013).

An earlier proponent of the bank lending channel is the seminal work of Bernanke and Blinder (1988), which builds on the studies of Tobin (1969) and Brunner and Meltzer (1972). The money view focuses on the two-asset world of money and bonds, where bank loans are merged with other debt instruments in a bond market as perfect substitutes. In this regard, the study of Bernanke and Blinder (1988) ignores the perfect substitutability assumption of the money view and develops a three-asset view in recognition of bank loans as a separate asset: money, bonds, and intermediated loans. Another proponent of bank lending is the study of Kashyap and Stein (1994), which affirms that in a three-asset world, monetary policy works through the independent impact of intermediated loans’ supply and the rate of interest in the bond market. The model of Bernanke and Blinder (1988) highlights that three essential conditions must prevail in order to ensure the existence of a distinct bank lending channel of monetary policy transmission: open-market bonds and intermediated loans must not be perfect substitutes; monetary authorities should be able to influence the supply of intermediated loans by altering the quantity of reserves in the banking system; and there must be imperfect price adjustment that prevents the neutrality of any monetary policy shock.

According to Mishkin (1996), the bank lending channel is based on the special role that banks play within the financial system in solving problems of asymmetric information and other imperfections in credit markets. Often, banks serve as financial intermediaries that provide funds to certain borrowers who do not have access to credit markets. Imperfections are reflected in the size of external finance premium, which is the difference between the costs of the externally generated funds of a firm (through issuing equity or debt) and its internally generated funds (retained earnings). Following the special role of banks in channelling funds for productive use, this denotes that banks provide indirect finance while acting as financial intermediaries between SSUs and SDUs. In line with the ongoing discussion, the study of Grodzicki et al. (2000) postulate that the existence of a bank lending channel is based on two essential assumptions: monetary policy decisions affect the liquidity position of banks and changes in the supply of loan from banks affect borrowers due to limited access to other substitute sources of finance. Thus, the bank lending channel of monetary policy has a greater consequence on smaller firms, which are more dependent on bank loans than larger firms that have direct accessibility to other sources of finance in credit markets (Gertler & Gilchrist, 1994).

Nonetheless, the inaccessibility of substitute sources of finance by smaller firms hampers their investment (Nilsen, 2002), which concurrently affects the aggregate output within an economy. Evidence of this assertion emerges in the studies of Obamuyi (2010) and Luper (2012). The former study reveals that high interest rates and meticulous lending policies have reduced the aggregate performance of small and medium enterprises (SMEs) in Nigeria. Additionally, the latter study reveals that banking consolidation reforms in Nigeria have reduced the financing of SMEs from 5.78 percent to 0.47 percent, post-consolidation. The bank lending of monetary policy has been the most controversial transmission mechanism of monetary policy.

Notably, the study of Romer and Romer (1989) argues that loans do not perform an essential role, since monetary policy contraction has an effect on interest rates through bank deposits, not through loans. In response to this, Kashyap et al. (1993) postulate that during monetary contractions, firms issue commercial papers as an alternative source of finance to counteract drain of deposits. This further implies that firms are using the alternative source of finance due to reduction in loan supply, not due to reduction in loan demand arising from activity slowdown (Nilsen, 2002). Oliner and Rudebusch (1996) argue, in line with Gertler and Gilchrist (1994), that only large firms issue commercial papers. Thus, small and large firms exhibit distinct behaviors during monetary contractions, which renders the bank lending channel less important.

A later study of Kashyap et al. (1996) responds to the assertion of Oliner and Rudebusch (1996) and argues that differences between small and large firms during monetary contractions do not cut against the bank lending view. In this regard, Kashyap et al. (1996) postulate that contraction by monetary authorities reduces supply of loans to small firms, and that in search of alternative sources of finance, small firms broaden their account payables. Concurrently, the demand for account payables of large firms increases, leading them to raise more external finance through issuing commercial papers to meet the demand. Hence, the financial intermediation function of banks would be moderately and imperfectly taken over by large firms through a surge in commercial papers. Despite the significance of the bank lending channel in the channeling of funds for productive use, the view of Romer and Romer (1989) argues that loans do not play an essential role, as monetary policy contraction initially affects interest rates through deposits rather than loans. Following the credit creation theory of banking, this study argues the assertion of Romer and Romer (1989) by stressing the essential role of loans, as banks do not loan existing money but create new money.

Trend of Bank Lending in Nigeria

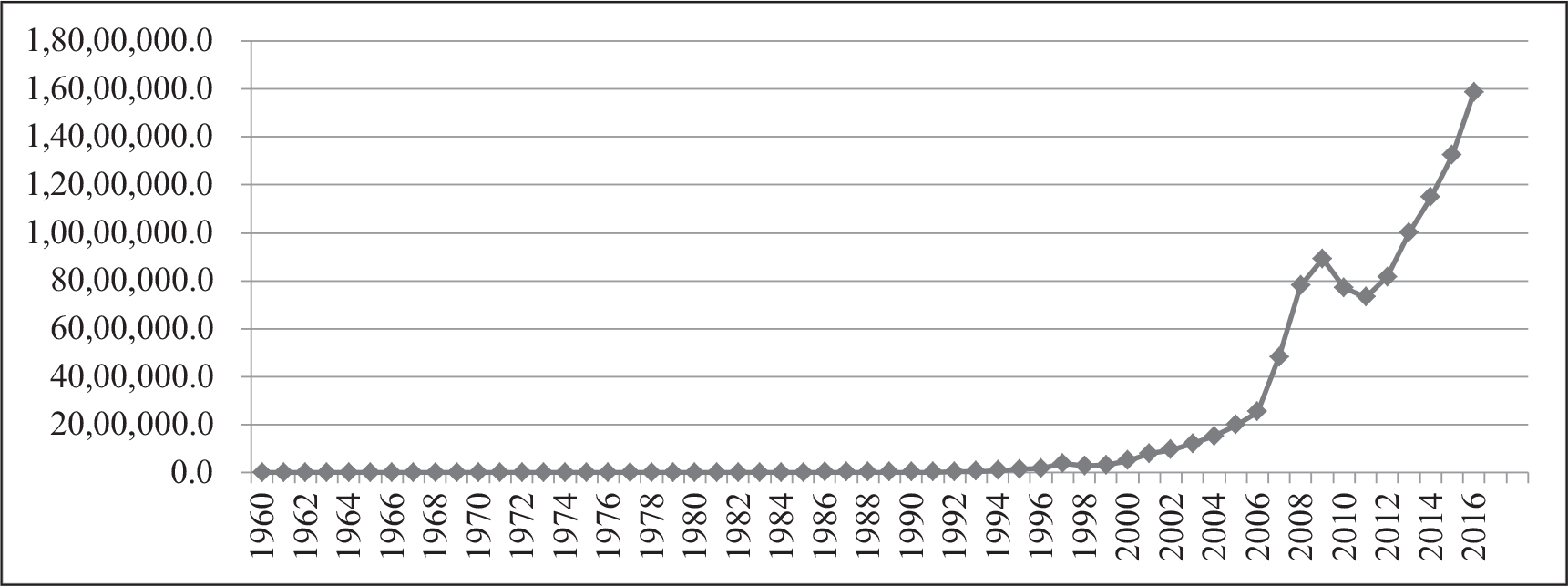

Banking in Nigeria has undergone five different phases: the free banking era (1892–1952), regulation era (1952–1986), deregulation era (1986–2004), consolidation era (2004–2009), and post-consolidation era (from 2009 to date). The most notable phase in the Nigerian banking industry is the consolidation era, which began with an increase in the minimum capital base of banks in Nigeria from N2 billion to N25 billion, to be fulfilled by the end of December 2005. The policy was announced in July 2004 by the Central Bank of Nigeria (CBN) as part of the “13-point Reform Agenda.” Over the years, commercial banks in Nigeria have been involved in the bank lending channel through their special role as financial intermediaries between SSUs and SDUs. The aggregate loans and advances data of commercial banks in Nigeria from 1960 to 2016 are illustrated in Figure 1.

As shown in Figure 1, the trend of bank lending in Nigeria remained stable from 1960 to 2000, with a subsequent significant increase. Despite a momentous regulatory increase in the minimum capital base of banks in 2004, bank lending in Nigeria kept increasing until 2008 when a significant decrease occurred, reflecting the effects of the 2007–2008 financial crisis. Prior to the consolidation era, the minimum capital base of banks was N2 billion. Nonetheless, regulatory policy compelled existing banks in Nigeria to maintain a capital base of N25 billion into the financial crisis. This study argues that without such a proactive capital base requirement, the Nigerian banking industry would have experienced systemic risk during the 2007–2008 financial crisis with a minimum capital requirement of N2 billion. The hit of the financial crisis caused a global credit crunch, and bank lending in Nigeria decreased during 2008–2011. However, bank lending in Nigeria started increasing in 2012, after recovery from the financial crisis, and keeps increasing to date.

Review of Empirical Studies

Several studies have examined the determinants of bank lending in different countries. For instance, the study of Gambacorta & Mistrulli (2004) investigates the influence of bank capital on the lending behavior of Italian banks. The study reveals that bank capital matters in the transmission of various shocks to bank lending. Olokoyo (2011) investigates the determinants of bank lending behavior of commercial banks in Nigeria for the period 1980–2005 using volume of deposits, cash reserve requirements, interest rate, liquidity ratio, investment portfolio, exchange rate, and GDP at market price as explanatory variables of aggregate lending of commercial banks. The study reveals that volume of deposits, GDP at market price, foreign exchange, and investment portfolio have statistically significant impact on aggregate loans and advances of commercial banks in Nigeria. Thus, interest rate, liquidity ratio, and cash reserve ratio do not influence bank lending in Nigeria.

The study of Ogunyomi (2011) examines the influence of broad money supply, minimum rediscount rate, liquidity ratio, exchange rate, and political stability on bank lending in Nigeria for the period 1975–2009. It reveals that only broad money supply shows positive statistical significance in influencing commercial bank lending in Nigeria, whereas the other regressors do not influence bank lending. The study of Olusanya et al. (2012) examines the influence of foreign exchange, interest rate, cash reserve ratio, investment portfolio, GDP at market price, liquidity ratio, and volume of deposits on loans and advances of commercial banks in Nigeria for the period 1975–2010. It reveals that interest rate and investment are not statistically significant on loans and advances, whereas the other regressors in the model are statistically significant.

The study of Ajayi and Atanda (2012) investigates the influence of liquidity ratio, inflation, exchange rate, minimum policy rate, and cash reserve ratio on loans and advances of commercial banks in Nigeria for the period 1980–2008. It reveals that exchange rate and cash reserve ratio are statistically significant on loan and advances of commercial banks, whereas the other regressors are not statistically significant. Also, the study finds no long-run relationship between the independent and dependent variables in the model. Thus, the study argues that monetary policy tools in Nigeria are not credit stimulants in the long run. Jegede (2014) investigates the effect of monetary policy on the lending of commercial banks in Nigeria for the period 1988–2008 using interest rate, exchange rate, money supply, and liquidity ratio as explanatory variables of aggregate loans and advances. The findings of the study reveal that money supply and liquidity ratio show a negative influence on bank lending in Nigeria, whereas interest rate and exchange rate show a positive influence.

In the Ethiopian context, the study of Malede (2014), using ordinary least squares (OLS), reveals that bank size, credit risk, liquidity ratio, and GDP determine commercial bank lending in Ethiopia, whereas deposit, investment, interest rate, and cash reserve ratio are not statistically significant, for the period 2005–2011. The research of Uyagu and Osuagwu (2015) examines the influence of interest rate, liquidity ratio, inflation, cash reserve ratio, and loan-to-deposit ratio on loans and advances of commercial banks in Nigeria for the period 1994–2013. The findings of the study show that interest rate has a negative effect on loans and advances; however, it is not statistically significant. The other regressors are shown to have a negative and statistically significant effect on loans and advances. The study of Pham (2015) investigates determinants of bank credit in 146 different countries for the period 1990–2013 using generalized method of moments (GMM). It reveals that bank credit is enhanced by domestic liquidity and high level of interest rate. Also, the study reveals that credit supply is negatively related to exchange rate, capital requirements ratio, non-performing loans, bank concentration, and the KAOPEN index. Additionally, it provides evidence of country-specific influence of economic growth on bank lending.

In the Nepalese context, the study of Bhattarai (2016) investigates determinants of lending behavior among commercial banks in Nepal for the period 2007–2014 using a model that regresses cash reserve ratio, investment portfolio, deposit-to-capital ratio, bank size, and liquidity on loans and advances. The study reveals that bank lending in Nepal is determined by investment portfolio, bank size, liquidity, and cash reserve ratio. The study of Olaoluwa and Shomade (2017) examines the impact of monetary policies on bank lending behavior in Nigeria for the period 1980–2014 using volume of deposits, foreign exchange, reserve requirement, interest rate, and GDP as regressors on loans and advances. It reveals that exchange rate, interest rate, volume of deposits, and reserve requirements have statistically significant impact on the bank lending behavior of commercial banks in Nigeria. In addition to the ongoing debate, the study of Kim and Sohn (2017), which investigates insured US commercial banks, reveals that bank capital exerts a significant positive effect on bank lending after sufficient liquid assets are retained by large banks.

However, few studies focus on bank capital in Nigeria. For instance, the study of Matousek and Solomon (2018) investigates the bank lending channel in Nigeria for the period 2002–2008 (period of consolidation) using disaggregated data from 23 banks in Nigeria. It reveals that bank size, liquidity, and capitalization were significant determinants of loan supply during this period. Furthermore, the study of Ebire and Ogunyinka (2018) examine determinants of demand and supply of bank loans in Nigeria for the period 2002 Q1–2017 Q1. On the demand side, the study shows that real GDP and lending rate have a negative relationship with bank loans. However, inflation has a positive relationship with bank loans. On the supply side, bank capital has a positive but statistically insignificant relationship with bank loans, inflation has a statistically insignificant relationship with bank loans, borrowing rate has a statistically significant positive relationship with bank loans, and lending rate has a significant negative relationship with bank loans.

Methodology

Data and Model Specification

As seen from the review of empirical studies, various determinants of bank lending have been examined using different models. However, the contribution of this study is based on the argument of Gambacorta and Mistrulli (2004) that bank capital has not been fully considered in the context of the bank lending channel. In this regard, this study extends the studies of Gambacorta and Mistrulli (2004) and Kim and Sohn (2017), which examine bank capital in the context of the bank lending channel. In Nigeria, only a few studies, such as Matousek and Solomon (2018) and Ebire and Ogunyinka (2018), have examined bank capital as a determinant of bank lending, despite the huge attention on bank capital by the CBN since the consolidation era. It is against this backdrop that this study seeks to empirically contribute to the few existing studies on bank capital in Nigeria. Also, following the bank lending channel, as earlier discussed, this study considers broad money as a monetary policy tool, loan-to-deposit as a liquidity measure determined through bank regulation, and inflation measured by consumer price index as a macroeconomic indicator of general price level. Hence, the model for this study takes the form:

Converting Equation (1) into an econometric model, we obtain Equation (2) as:

where

Results and Discussion

Descriptive Statistics

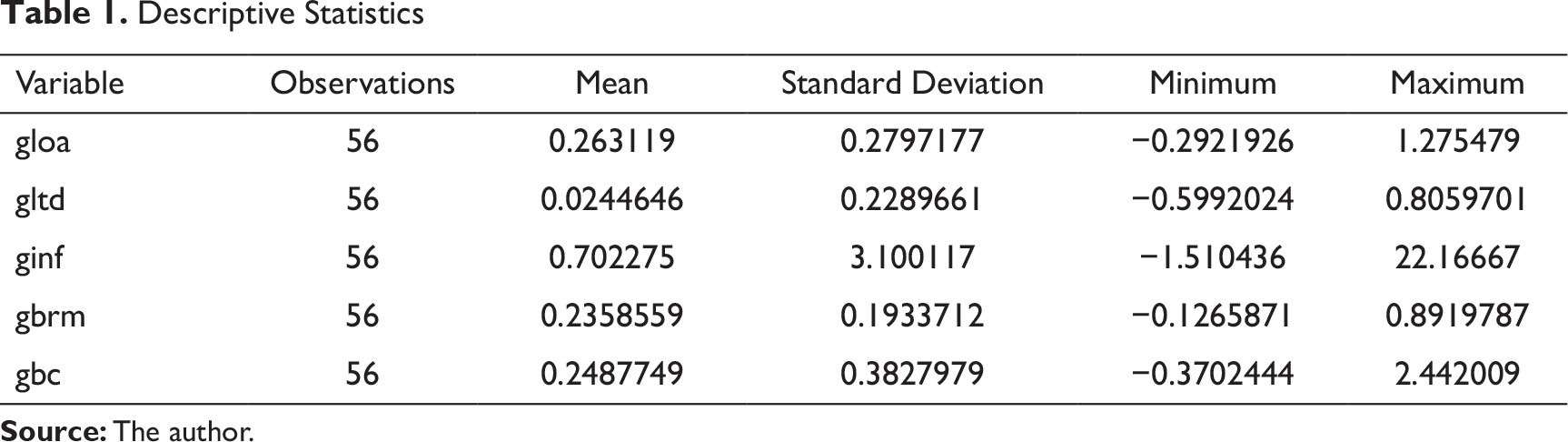

The descriptive statistics for the variables under investigation are shown in Table 1. The statistics show 56 observations for the longitudinal time span 1961–2016. Additionally, the statistics show the mean and standard deviation of the variables over the period under investigation. The mean values illustrate dawdling average growth rates of the variables that are less than 1 percent. Furthermore, the minimum values show that negative growth rates have been recorded for the variables from 1961 to 2016. On the other hand, the maximum values for

Unit Root Tests

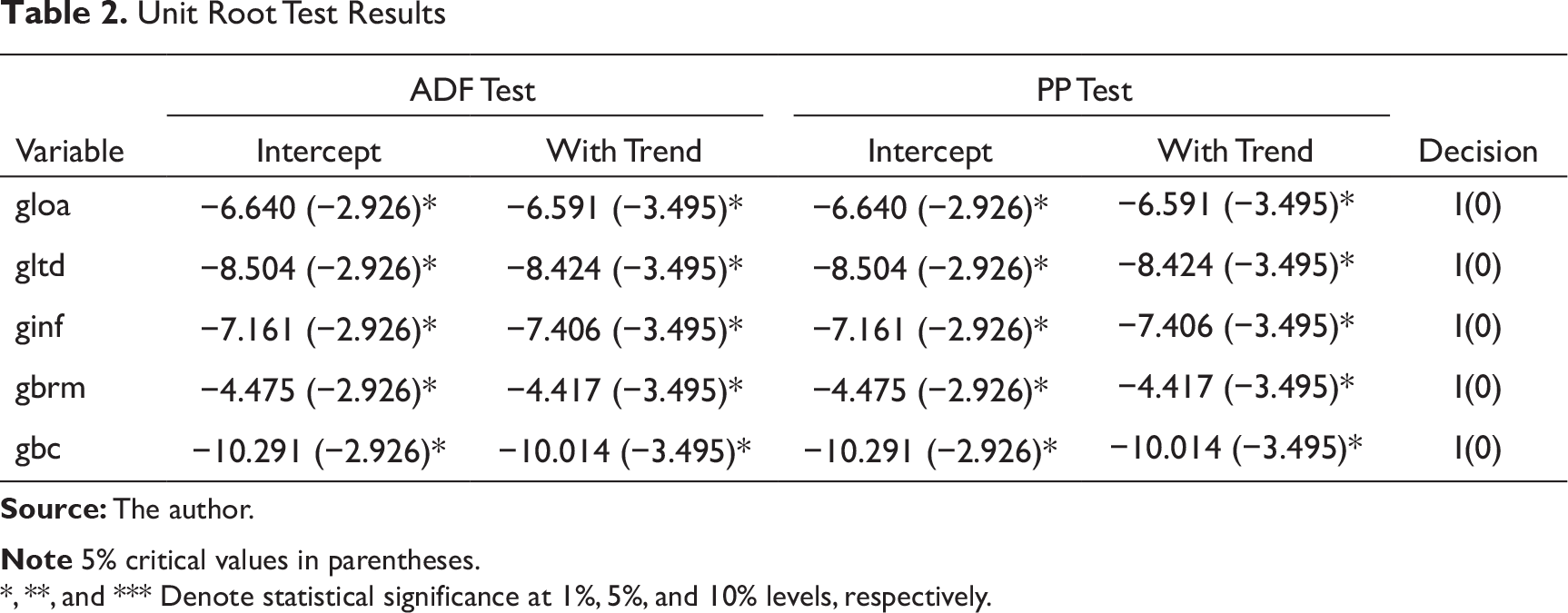

The empirical estimation in this study commences with unit root tests to examine whether the series are stationary or nonstationary, which is essential in order to prevent spurious regression results. This study adopts the augmented Dickey–Fuller (ADF) (Dickey & Fuller, 1979; Said & Dickey, 1984) and Phillips–Perron (PP) unit root tests (Phillips, 1987; Phillips & Perron, 1988). ADF unit root test is a parametric approach that solves serial correlation and heteroskedasticity in an error term, while PP unit root test is a nonparametric approach that corrects serial correlation and heteroskedasticity by directly modifying the test statistics. The unit root test results are shown in Table 2.

Descriptive Statistics

Unit Root Test Results

*, **, and *** Denote statistical significance at 1%, 5%, and 10% levels, respectively.

The Bounds-testing Approach

Drawing on the seminal contribution of Pesaran et al. (2001), this study adopts the bounds-testing approach to examine the existence of long-run relationships between the variables under investigation. This approach is applicable if the regressors are purely I(0) or I(1), or a mix of I(0) and I(1), but not I(2). In this regard, a bounds-testing approach tests the F-statistic based on the critical value bounds of I(0) and I(1). For this study with I(0) variables, the bounds testing approach examines long-run relationship, rather than cointegration which is applicable to I(1) variables. In this regard, the autoregressive distributed lag (ARDL) equation for the model in Equation (2) is specified thus:

where

H0: ∅1 = ∅2 = ∅3 = ∅4 = ∅5 = 0 (null: no long-run relationship)

H1: ∅1 ≠ ∅2 ≠ ∅3 ≠ ∅4 ≠ ∅5 ≠ 0 (alternative: long-run relationship exists)

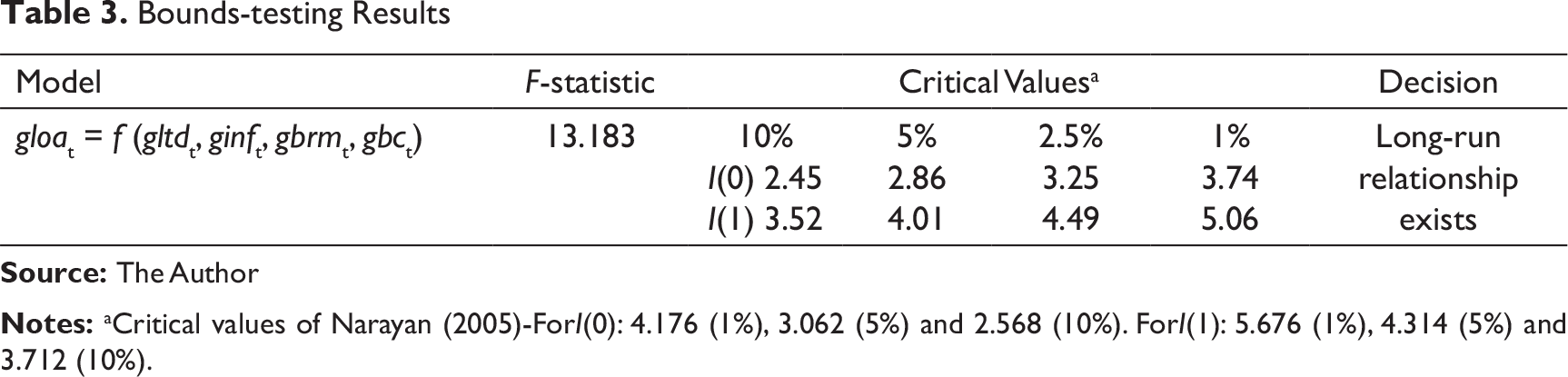

According to the bounds-testing approach of Pesaran et al. (2001), if the F-statistic is less than the critical value for I(0) regressors, then the null hypothesis cannot be rejected, which implies that there is no cointegration or levels relationship. However, if the F-statistic exceeds the critical values for I(1) regressors, then the null hypothesis can be rejected, which implies the existence of cointegration or levels relationship. The bounds-testing procedure results for the model under investigation are shown in Table 3 for the critical value bounds of I(0) and I(1).

Bounds-testing Results

where λ is the parameter for speed of adjustment, which measures the convergence of the variables towards equilibrium, and

ARDL-ECM Estimates

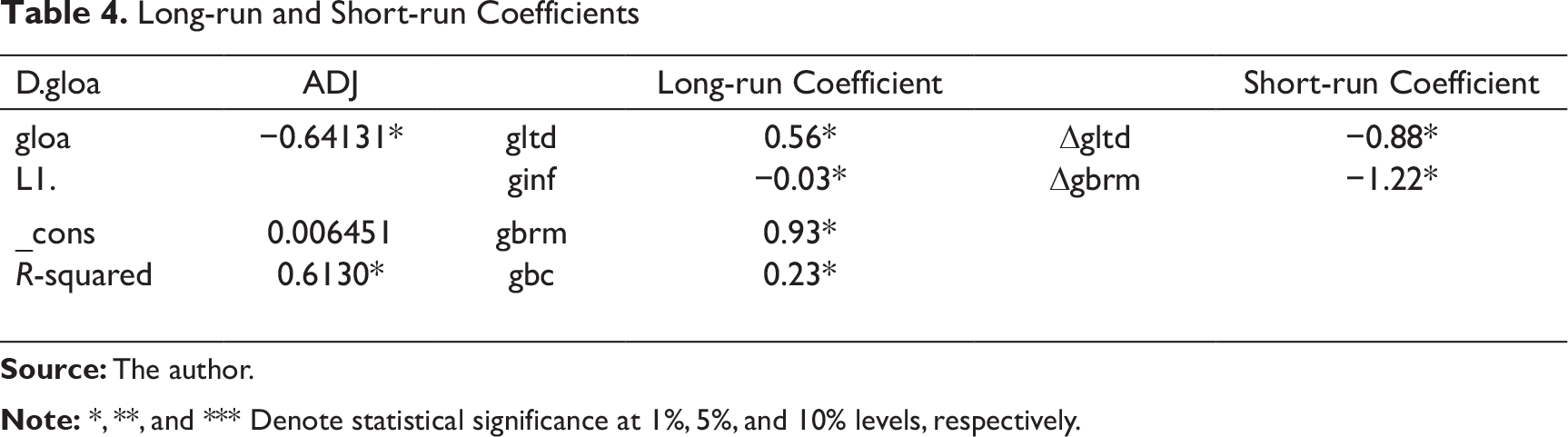

Table 4 shows the long-run and short-run coefficients for the model. For short-run relationship, coefficients for

Regarding long-run relationships, there is a significant positive relationship between

Long-run and Short-run Coefficients

Causality Tests

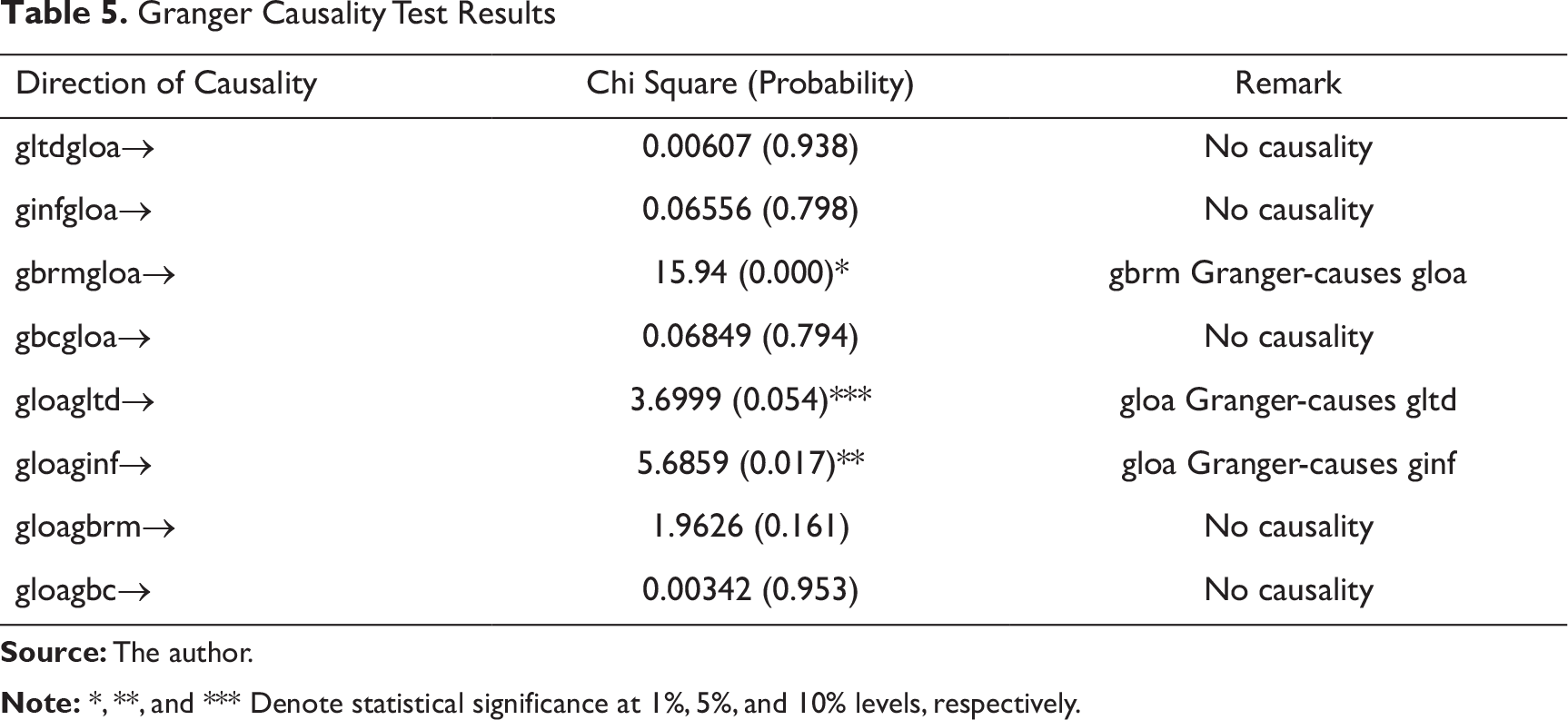

In addition to the ARDL estimates shown in Table 4, this study further conducts Granger causality tests to address the common phrase in statistics that “correlation does not imply causation.” Consequently, testing for causality among determinants of bank lending in Nigeria is another contribution of this study to existing studies such as Olokoyo (2011), Ogunyomi (2011), Olusanya et al. (2012), Ajayi and Atanda (2012), Jegede (2014), Uyagu and Osuagwu (2015), Olaoluwa and Shomade (2017), Matousek and Solomon (2018), and Ebire and Ogunyinka (2018). As the variables in the model of this study are stationary, or I(0), the use of the vector error correction model (VECM) Granger causality framework is not suitable in this case. The framework is appropriate to examine short-run and long-run causality among non-stationary time series, or I(1). Thus, this study adopts the Wald test to examine the direction of causality among the variables under investigation, as shown in Table 5.

The Granger causality test results in Table 5 indicate a unidirectional causality running from

Granger Causality Test Results

Regarding inflation, monetary authorities implement contractionary monetary policy measures to tackle this economic problem by increasing interest rates in order to reduce spending and investment. Subsequently, an increase in interest rates implies higher costs of borrowing, which would concurrently reduce bank lending, as borrowing becomes less attractive to borrowers. Thus, the causality evidence of this study depicts the transmission mechanism from inflation to bank lending. Additionally, this study reveals that growth in bank capital does not Granger-cause growth in bank lending in Nigeria. Consequently, this study argues that commercial banks in Nigeria acquire more capital in adherence to regulatory requirements rather than to boost lending.

A significant regulatory policy in Nigeria occurred in 2004 which marked the commencement of the consolidation banking era. During this period, the minimum capital base of banks in Nigeria was increased to N25 billion from N2 billion, as announced on July 4, 2004, effective from December 31, 2005. In the quest to comply with this new regulatory policy, the 89 banks operating in Nigeria prior to the policy were reduced to 25 through regulatory mergers and acquisitions at the start of 2006 (Sanusi, 2010). However, the number of banks in Nigeria was later reduced to 24 through a market-induced merger and acquisition (Sanusi, 2010). In this regard, the new causality evidence provided in this article opposes the research findings of Matousek and Solomon (2018) and Ebire and Ogunyinka (2018).

The Granger causality test results in Table 5 also show that

Impulse Response Functions and Forecast Error Variance Decomposition

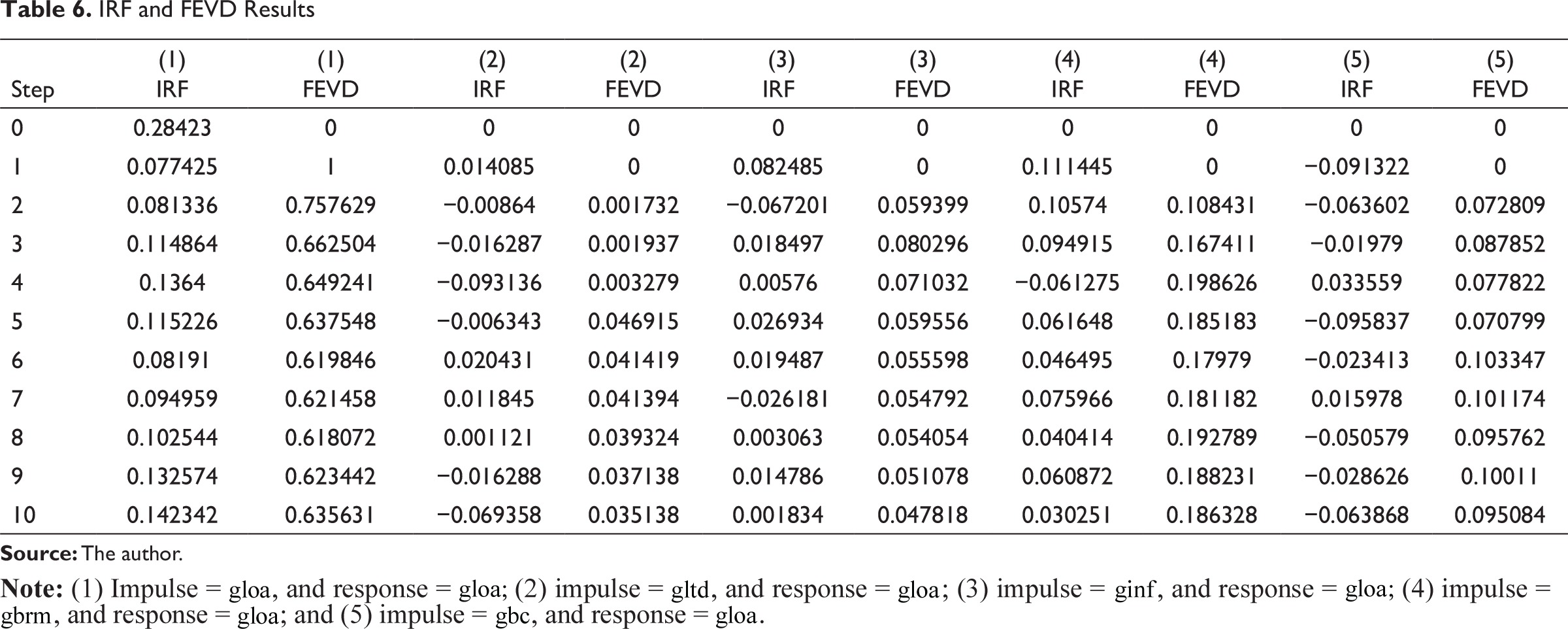

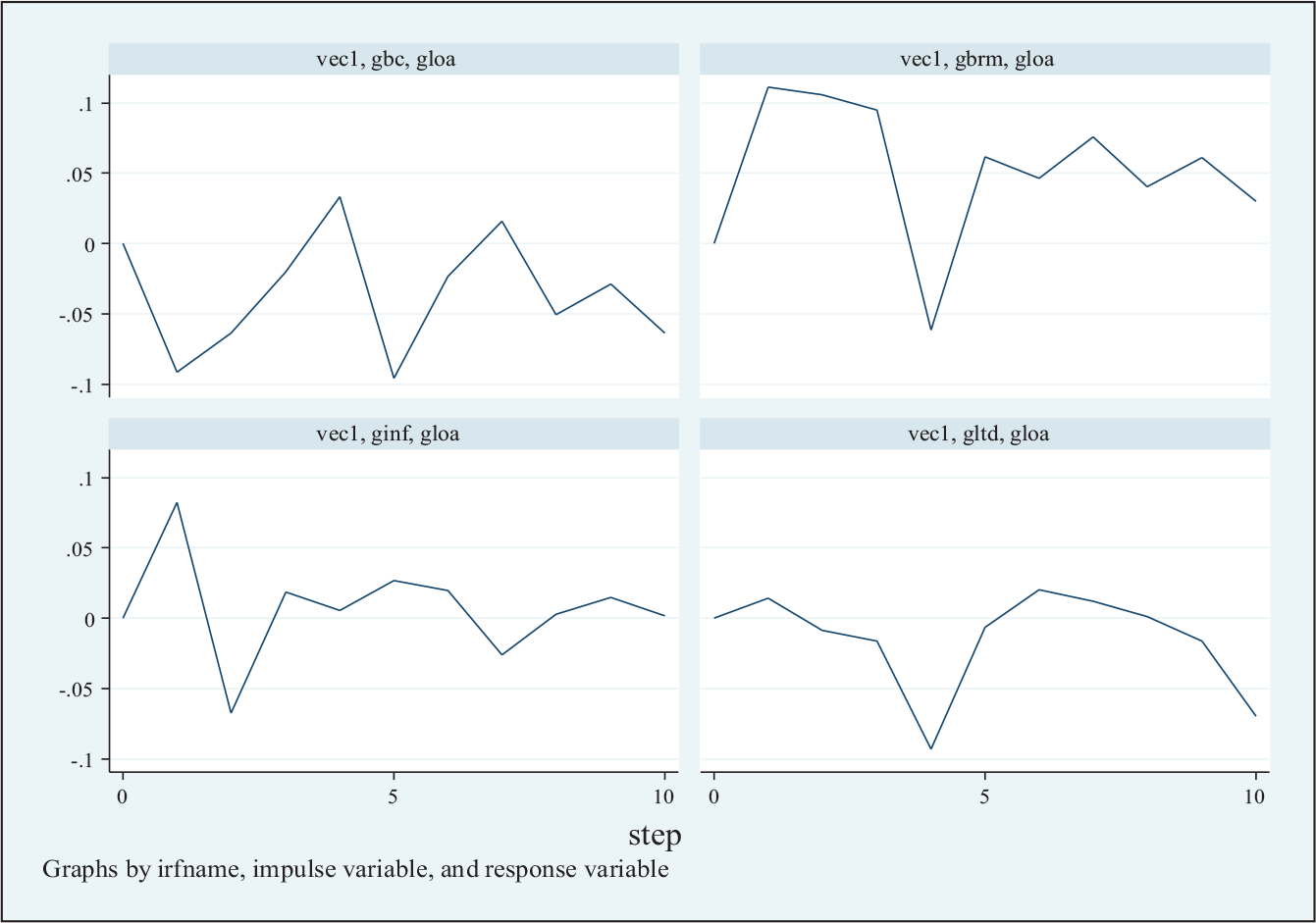

The general limitation of the Granger causality test is that it does not capture the strength of causal relationship among variables beyond the selected time period. Drawing on this assertion, this study applies an innovative accounting approach using impulse response function (IRF) and forecast error variance decomposition (FEVD) to address the limitation of the Granger causality test. IRF shows the effect of orthogonalized shocks on the alteration path of variables, while FEVD shows the proportional contribution in one variable resulting from innovative shocks in other variables.

IRF and FEVD Results

The FEVD results in Table 6 show that in period 1, 100 percent forecast error variance in

Diagnostic and Model Stability Tests

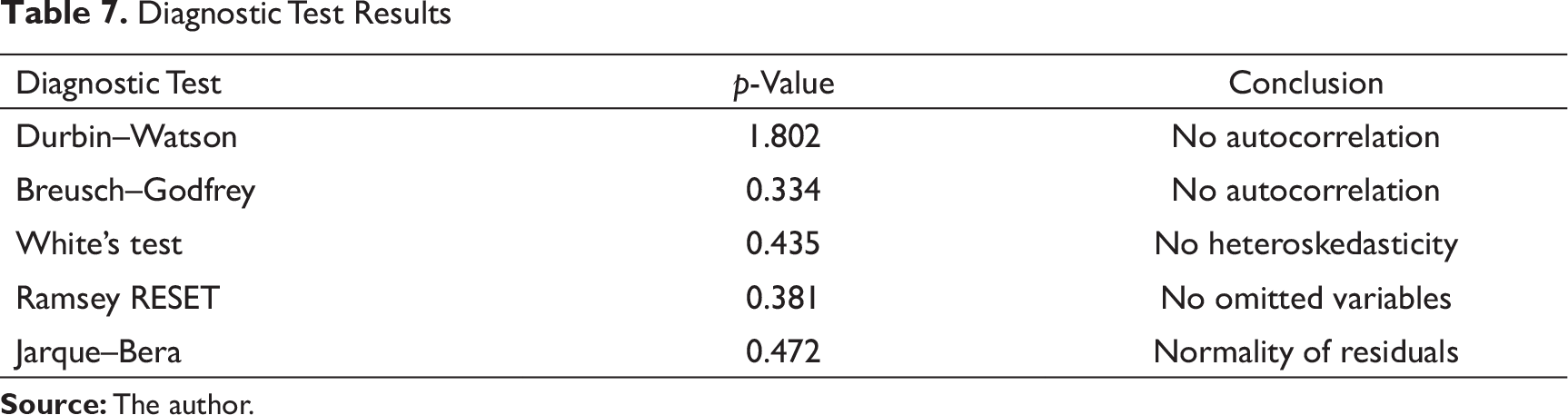

Diagnostic Test Results

Additionally, in this study, Ramsey regression equation specification error test (RESET) is conducted to examine model misspecification for the null hypothesis of “no omitted variables.” The p-value of 0.381, as shown in Table 7, is not statistically significant. Hence, the null hypothesis cannot be rejected, which implies that there are no omitted variables or misspecification in the model. Furthermore, the Jarque–Bera test is conducted to examine the null hypothesis that the residuals are normally distributed. The test shows a p-value of 0.472, which indicates that the null hypothesis cannot be rejected. Thus, the residuals in the model under investigation are normally distributed. Overall, the diagnostic test results denote that the empirical results of this study are robust and reliable for prediction.

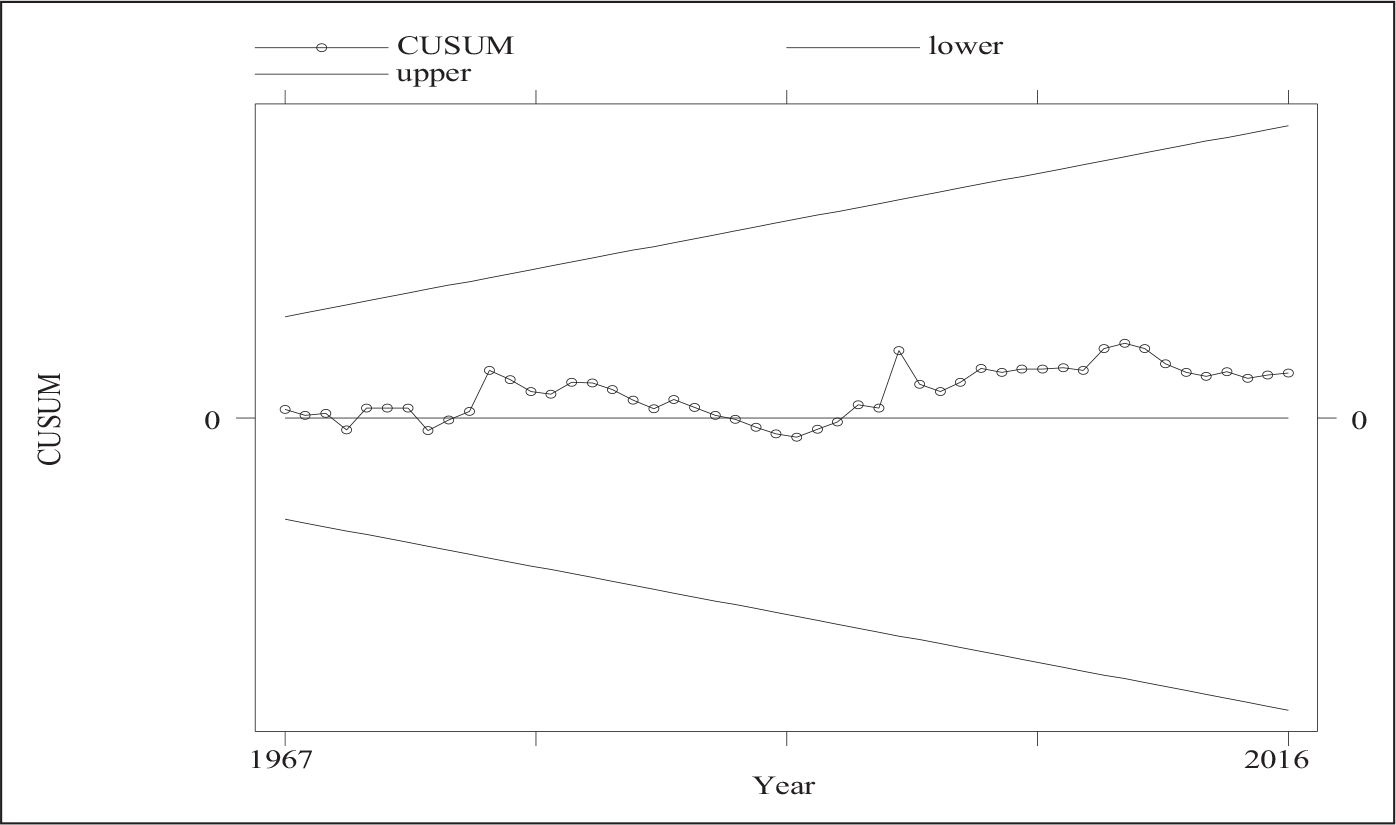

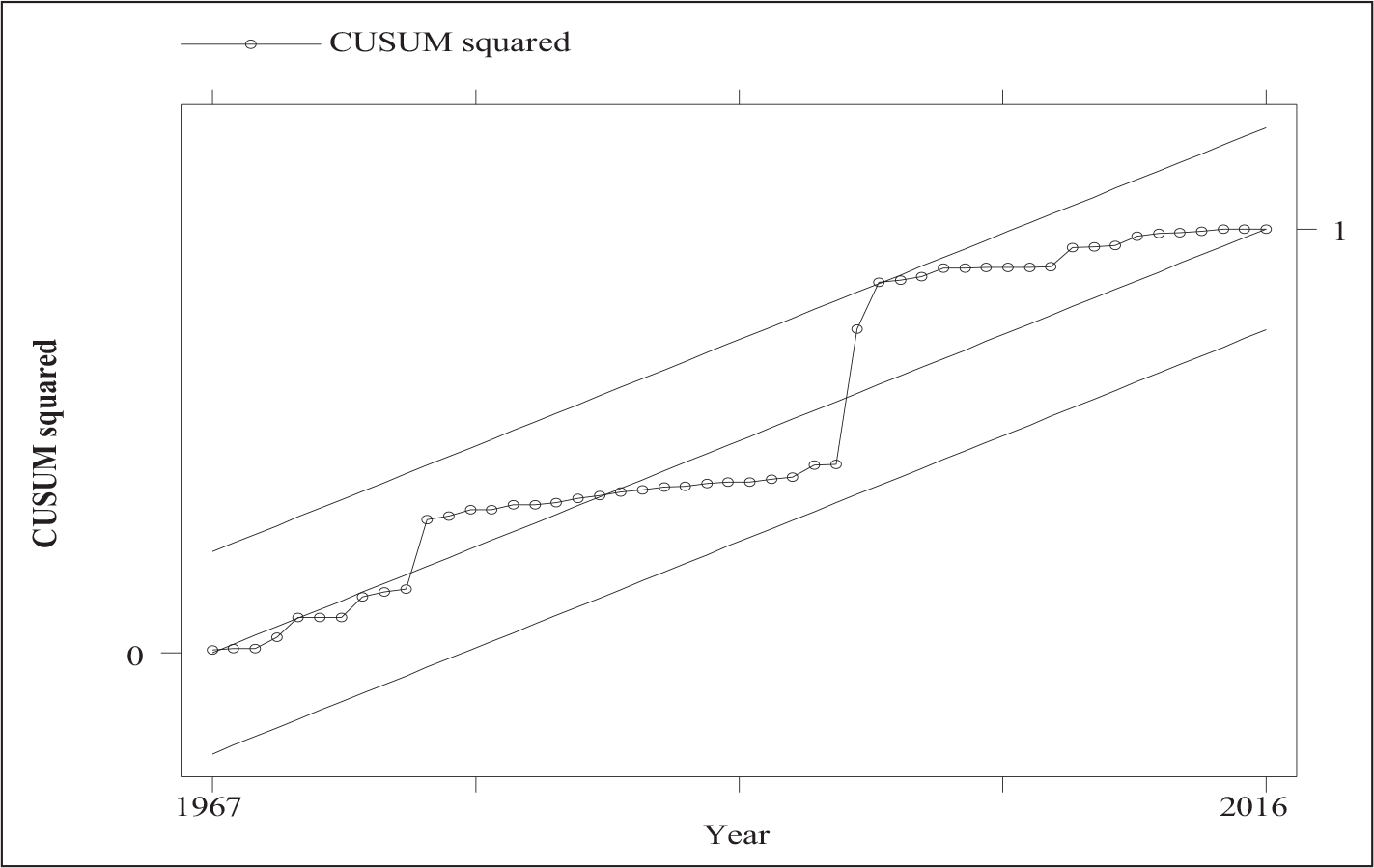

In addition to the diagnostic tests, this study checks the stability of the model under investigation using the cumulative sum of recursive residuals (CUSUM) and cumulative sum of squares of recursive residuals (CUSUMQ) tests developed by Brown et al. (1975), as shown in Figures 3 and 4. The plots of CUSUM and CUSUMQ statistics indicate that the residuals are within the critical boundaries at the 5 percent significance level (represented by the straight lines), thus implying that all coefficients in the ECM are stable over the period under investigation.

Conclusion and Policy Recommendations

This paper makes a twofold contribution to knowledge. First, this study builds on the studies of Gambacorta and Mistrulli (2004) and Kim and Sohn (2017) by providing further empirical evidence regarding bank capital as a determinant of bank lending. Additionally, it makes an empirical contribution to add to the studies of Matousek and Solomon (2018) and Ebire and Ogunyinka (2018) in Nigeria. Second, existing studies on determinants of the bank lending channel in Nigeria, such as Olokoyo (2011), Ogunyomi (2011), Olusanya et al. (2012), Ajayi and Atanda (2012), Jegede (2014), Uyagu and Osuagwu (2015), Olaoluwa and Shomade (2017), Matousek and Solomon (2018), and Ebire and Ogunyinka (2018), focus on the relationship without providing causality evidence. Against this backdrop, this study provides Granger causality evidence of the relationship between the regressors and bank lending in Nigeria.

By and large, the empirical findings of this study reveal that growth in loan-to-deposit ratio, growth in inflation, and growth in broad money are determinants of bank lending in Nigeria. However, growth in bank capital is not a determinant of bank lending in Nigeria despite its 9.51 percent contribution to bank lending. As such, this paper argues that commercial banks in Nigeria show stern concern for their liquidity and capital adequacy positions while acting as financial intermediaries. Particularly, during the consolidation era which led to a series of mergers and acquisitions among banks in Nigeria. To date, Nigerian banks still struggle to maintain a buffer beyond the regulatory capital requirements in order to prevent distortion in banking activities.

On September 21, 2018, the license of Skye Bank was revoked, as the bank required urgent recapitalization based on the outcome of the CBN’s examinations and forensic audit. Thus, the CBN, in consultation with the Nigeria Deposit Insurance Corporation (NDIC), established a bridge bank, Polaris Bank, to take over the activities of Skye Bank effective from September 24, 2018. The first intervention in this strategy was the injection of N786 billion into Polaris Bank by the Asset Management Company of Nigeria (AMCON). Thus, this study recommends the adoption of the moral suasion instrument by the CBN in order to encourage bank lending. According to Breton and Wintrobe (1978), moral suasion serves as an instrument of direct communication between central banks and commercial banks. Hence, it can be used to reveal some constraints facing the central bank, perspectives that the central bank holds about the economy, suitability of monetary policy, and causes of economic problems to commercial banks (Breton & Wintrobe, 1978). Consequently, the adoption of moral suasion will help the CBN communicate such constraints to commercial banks in order to persuade banks to increase lending reasonably without exposure to liquidity risk and erosion of capital.

However, the instrument independence of CBN has been deterred by existing conflicts between monetary and fiscal policies in Nigeria (Ogbole et al., 2011). In this regard, this study recommends the segregation of monetary and fiscal policy measures in Nigeria, which is determined by the degree of central bank independence. In 2007, the CBN Act was passed into law in Nigeria by the National Assembly and assented by the president. The provisions of CBN Act 2007 focus on strengthening the previous CBN amendment, Decree No. 37 of 1998, and the Banks and Other Financial Institutions Act (BOFIA) amendment, Decree No. 38 of 1998. However, this study argues that the provisions of CBN Act 2007 are conflicting. For instance, section 1(3) of CBN Act 2007 states that the CBN shall enjoy operational autonomy. Thus, the CBN should possess the authority to run its own operations without extreme involvement of the government, such as appointing staff and setting budgets (CBN, 2012). Consequently, CBN (2012) further accentuates that operational independence should help facilitate goal and instrument independence. In the same Act, sections 8, 10, and 11 state that the appointment of the Governor, the Deputy Governor, and Non-executive Directors shall be decided by the President subject to the Senate’s confirmation. Also, the removal of the governor is subject to confirmation by the Senate. Additionally, the composition of the Monetary Policy Committee (MPC), as stated in section 12 of CBN Act 2007, includes the governor, four deputy governors, two members of the Board of Directors of the bank, three external members appointed by the president, and two external members appointed by the governor.

Following the highlighted provisions of CBN Act 2007, this study argues that the operational independence of the CBN as claimed in section 1(3) is in jeopardy. This argument is based on the fact that the President and the Senate are involved in the appointment of key positions in the CBN. In this regard, this study further argues that the CBN possesses “paper-based” independence rather than practical independence. Hence, this has adverse effects on the facilitation of goal and instrument independence, which has stimulated the existing conflict between fiscal and monetary policy measures in Nigeria. In line with these assertions and arguments, this study recommends a revision of CBN Act 2007 to reduce or prevent the involvement of the government in the appointment of the CBN’s key positions. By so doing, the CBN can enjoy operational independence, which will further facilitate goal and instrument independence. As fiscal and monetary policies interact within an economy, achieving goal independence by the CBN might be somewhat difficult. However, the CBN should enjoy instrument independence along with operational independence in order to ensure the appropriate use of monetary policy tools to achieve policy goals.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflict of interest with respect to the research, authorship, and/or publication of this article.

Funding Source

The author received no financial support for the research, authorship, and/or publication of this article.