Abstract

Corporate governance is enriched by the existence of female directors. Their presence adds value to corporate governance by incorporating different perspectives and experiences. Female directors play an important role in preventing corporate harm, daring to ask critical questions and controlling conflict among various stakeholders. This study aimed to explore the effect of family control (FC) in stimulating leverage and firm value and assess the moderating role of female directors between FC on leverage and firm value. The sample was collected from the Indonesian Stock Exchange of 1,171 data observations-years (2019–2021 period) of companies listed. This research also used a linear regression model to analyse the purpose of hypotheses. The findings of this study indicate that female directors do not moderate the relationship between FC on leverage and firm value. The results prove the opposite of the assumption that the presence of female directors can harmonise and balance the interests of majority and minority shareholders. Finally, this article also contributes to the literature by developing the moderating role of female directors.

Introduction

The issue of board diversity has attracted the attention of researchers, including investors and policymakers over the last two decades because the role of female directors can increase board effectiveness (Martín-Ugedo & Minguez-Vera, 2014; Nielsen & Huse, 2010; Saeed et al., 2016). Although the literature assessing the impact of gender diversity on firm performance has grown significantly, definitive conclusions cannot yet be drawn (Adams & Ferreira, 2009). Female directors play a role in preventing company losses, dare to ask critical questions, and monitor conflicts between different stakeholders (Rhode & Packel, 2014). Other benefits of female directors include deeper market knowledge, the ability to reach broader markets, stimulating creativity and innovation, and improving problem-solving processes (Campbell & Mínguez-Vera, 2008). Overall, female directors are needed to achieve critical mass in decision-making (Shahab et al., 2020), improve corporate governance (Saeed et al., 2016) and have a similar impact on independent directors (Adams & Ferreira, 2009).

However, increased gender diversity can also trigger conflict and slow decision-making. Gender discrimination remains a hurdle because research shows that men are twice as likely as women to commit unethical acts (Betz et al., 1989). Female quotas can potentially be detrimental to well-managed firms, as additional scrutiny can be counterproductive (Adams & Ferreira, 2009). Moreover, females are generally more risk-averse than men in investment decision-making (Barber & Odean, 2001; Estes & Hosseini, 1988; Faccio et al., 2016; López-González et al., 2019). Although gender discrimination and negative stereotypes still exist (Martín-Ugedo & Minguez-Vera, 2014; Marlow & McAdam, 2013), research shows that there are no significant differences in decision-making between gender-diverse boards or when females reach high leadership positions (García-Meca et al., 2022; Wellalage et al., 2020).

Female directors also play a crucial role in the relationship between family control (FC) and firm value. Previous studies have explored how FC can benefit the overall economy and exhibit positive characteristics in governance structures (Keasey et al., 2015; Kim et al., 2017; Gómez-Mejía et al., 2007; Venusita & Agustia, 2021). However, research on FC has been limited due to challenges in obtaining reliable data (Villalonga & Amit, 2006). Family firms have unique management and ownership structures, which adds complexity to the challenges they face. Principals with a high ownership stake often take an active role in organising the firm and serving as board members or leaders for family members (Haider et al., 2021). This involvement aims to maintain control over agents to achieve the company’s goals. Female directors, especially those who are qualified and independent, can help balance the business preferences of family firms. However, directors with family ties may align more closely with family interests (García-Meca et al., 2022). The impact of female directors is more pronounced in countries with weaker shareholder protection and less developed corporate governance mechanisms. In such contexts, their presence can help address some challenges associated with FC. Empirical evidence suggests that female directors tend to approach important company decisions with more caution (Huang & Kisgen, 2013; Levi et al., 2014). This careful decision-making can affect the extent to which FC contributes to increasing firm value.

In 2014, over 95% of businesses in Indonesia were categorised as family-owned enterprises (PricewaterhouseCoopers, 2014). Common characteristics of these family firms, such as strong internal trust and a high level of commitment, significantly influence how managers make decisions and approach investments (Anderson & Reeb, 2003; Poletti-Hughes & Martinez Garcia, 2022; Venusita & Agustia, 2021). These factors often lead to conflicts in decision-making, particularly when balancing family interests with business objectives (Faccio et al., 2001; Fama & Jensen, 1985). In Indonesia, family companies tend to carry higher levels of debt compared to non-family firms, partly because of their close relationships with banks and easier access to debt financing (Mulyani et al., 2016). However, research by Haider et al. (2021) discovered that in the Southeast Asian region, there are not significant differences in how family and non-family businesses handle their debt levels. The inclusion of female directors can bring a more profound understanding of the importance of values in making business decisions. This understanding can help in reinforcing FC without it becoming overly dominant or detrimental to the long-term sustainability of the business, especially when dealing with high leverage. Consequently, family-controlled companies are more inclined to use proportional debt rather than giving up more ownership to outside investors (Gómez-Mejía et al., 2007).

This research makes several important contributions. First, this research contributes to the corporate governance literature, especially in family firms. To the best of our knowledge, this is the first attempt to address the moderating role of female directors between FC on leverage and firm value particularly in Indonesia. Moreover, various studies have analysed the role of the board of directors in family firms, but only a small fraction has examined the relationship between female directors and firm value. A previous study by Poletti-Hughes and Martinez Garcia (2022) discussed internal corporate governance mechanisms, especially female directors in the context of American countries. They found that female directors could moderate reduce the leverage of FC. However, this positive effect was controlled by independent female directors and weakened when family members held key management positions in the firm. They concluded that corporate governance structures in developing countries influence the impact of female directors on firm value. Second, this study contributes to the understanding of how agency theory and trade-off theory can explain the role of female directors in family-controlled firms to enhance firm value and balance the leverage of family firms. Third, this study separates the influence of female directors into the following two categories: dependent and independent. Fourth, the study offers additional insights relevant to emerging markets, such as Indonesia, which are characterised by low investor protection and high ownership concentration.

Theory and Hypotheses Development

Moderating Effect of Female Directors Between FC and Firm Value

The participation of female directors has a pivotal role in enhancing firm value, particularly in the context of FC. Their significant contribution to corporate governance is demonstrated through the unique approach and experience they bring (Sarkar & Selarka, 2021). In addition, their courage in asking critical questions is important in preventing harm at the firm (Rhode & Packel, 2014). The existence of female directors has been shown to balance family business preferences (Poletti-Hughes & Martinez Garcia, 2022). However, they generally enrich boards with different leadership styles, perspectives and expertise that contribute to increased effectiveness, transparency and managerial oversight in decision-making (Nielsen & Huse, 2010; Poletti-Hughes & Martinez Garcia, 2022).

Agency theory is a framework used to understand the relationship between firm owners (principals) and managers (agents) hired to run the firm. This theory can also be used to understand the relationship between FC and firm value by considering how the role of female directors may moderate this relationship. FC in a firm occurs when the family or related individuals have a majority stake or significant influence in the firm’s decision-making (Huang & Kisgen, 2013; Levi et al., 2014). In some cases, FC can have positive or negative effects on firm value. FC can create long-term stability and focus on long-term growth rather than short-term profits. This can benefit the firm in terms of building market trust, reducing agency costs and improving long-term performance (Faccio et al., 2016; López-González et al., 2019). On the other hand, FC can also have a negative impact on firm value. For example, the family’s personal interests may trump the interests of minority shareholders. This could lead to sub-optimal investment decisions or management policies that focus more on family interests than on firm value. Therefore, the role of female directors in the corporate structure may have a moderating effect on the relationship between FC and firm value.

Female directors may bring a different perspective to the board, which can include more diverse values, more inclusive thinking and a tendency to consider the firm’s social impact. Previous research shows that the presence of female directors can increase oversight of managerial decisions (Shahab et al., 2020). They tend to pay more attention to issues such as sustainability, corporate social responsibility and fairness, which can moderate decisions that may be influenced by FC (Saeed et al., 2016). In the context of agency theory, the role of female directors can be understood as an internal control mechanism that helps reduce agency conflicts between owners (family) and managers. They can act as agents working to increase firm value by considering not only short-term financial interests, but also long-term impacts on the firm and other stakeholders (Adams & Ferreira, 2009). Thus, in explaining the relationship between FC and firm value, agency theory can be used to describe how the role of female directors as an internal control mechanism can moderate the impact of FC. With a more diverse perspective and focus on long-term performance, female directors can help ensure that company decisions are less influenced by family interests, which can ultimately increase the overall firm value.

García-Meca et al. (2022) have shown that there are differences between the roles of family and non-family female directors, potentially affecting firm value. In contrast, Campbell and Mínguez-Vera (2008) failed to find a significant impact of the presence of female directors on firm value. Furthermore, a series of other studies, such as those conducted by Iriberri and Rey-Biel (2011), Shurchkov (2012), Randøy et al. (2006) and Rose (2007), failed to find a significant relationship between board gender diversity and firm performance. Aspects such as FC and the presence of female directors on the board may serve as moderating factors in this relationship, which may explain the variation in previous research findings.

Moderating Effect of Female Directors Between FC and Leverage

Trade-off theory is a theory that suggests that firms make trade-offs between the benefits and costs of using debt (Olsen & Cox, 2001). In other words, the theory attempts to explain how firms decide on the appropriate level of debt. Firms owned or controlled by families tend to be more cautious in their use of debt (Orser et al., 2006). This is because the families that control the firm tend to take a long-term view of their investments. They tend to avoid the risks associated with excessive debt that could threaten their control. Family-controlled firms may tend to have lower leverage as they focus more on maintaining control than on maximising leverage for the benefit of non-family shareholders.

Previous research shows that the presence of female directors can bring a different perspective. They tend to pay more attention to social, environmental and sustainability aspects. In this context, the role of female directors can moderate the relationship between FC and leverage. Female directors have also been shown to tend to have a more conservative approach to risk. This could mean that in the presence of female directors, family-controlled firms may be more inclined to limit the use of debt (Poletti-Hughes & Martinez Garcia, 2022). The presence of female directors can also increase supervision and accountability in decision-making, including decisions regarding leverage. This can lead to more balanced and measured decision-making, which may reduce the tendency for excessive leverage. Thus, the trade-off theory can explain the relationship between FC and leverage by considering the role of female directors as a moderator. In general, with FC, companies tend to have lower leverage. However, the presence of female directors may reinforce this trend by bringing a more conservative perspective to risk and providing closer oversight on the use of debt.

The moderating effect of female directors in FC on corporate leverage can be understood through various previous studies. According to Mulyani et al. (2016) and Setia-Atmaja et al. (2009), family firms usually maintain a higher level of leverage than non-family firms, an attempt to protect the wealth of minority shareholders and replace independent directors. This contradicts Schmid’s (2013) which found that family firms in Germany are less dependent on debt compared to non-family firms. While it is essential to highlight gender diversity challenges, the argument reduces by focusing on negative findings without considering the research’s context and biases. A more balanced approach would include many study findings, examine underlying issues that generate gender disparities in corporate leadership and identify diversity and inclusion techniques when formulating hypotheses. Overall, the research suggests that the moderating effect of female directors in FC on corporate leverage is complex and influenced by many factors including corporate culture, stage of corporate development and institutional environment.

Research Method

This research applies a quantitative approach, which is rooted in positivist thinking. The research is based on a longitudinal study investigating the relationship between FC, leverage, firm value and the moderating role of female directors in family firms. The initial sample consists of all companies listed on the Indonesia Stock Exchange from 2019 to 2021. The purposive sampling method used to determine the sample in this study is as follows: (a) nonfinancial companies listed on the Indonesia Stock Exchange for the 2019–2021 period, (b) companies with complete data needed in the study. The final sample consists of a panel data set of 1,171 observations of companies listed on the Indonesia Stock Exchange that meet the requirements. Due to the limited data obtained, the author can only identify family and non-family companies using a dummy (binary) and cannot see how much the percentage of their family shares ownership in the company.

This study sets ‘Family Control’ as the main independent variable. This dummy variable is set to one if at least 20% of the company’s shares are controlled by the family and at least one family member serves as a director, CEO or chairman. This approach is adopted from previous studies (Anderson & Reeb, 2003; La Porta et al., 1999; Poletti-Hughes & Martinez, 2022). The moderating variable in this study is the ‘Female Director’. This variable is divided into three components: ‘Female Ratio’ or ‘FD’, which refers to the percentage of female directors (PFD); ‘Female Dependent Ratio’ or ‘FDD’, which refers to the percentage of dependent female directors; and ‘Female Independent Ratio’ or ‘FDDI’, which refers to the percentage of independent female directors. The main sources for these variables are previous studies (D’Amato, 2017; Li & Chen, 2018; Poletti-Hughes & Martinez, 2022; Sarkar & Selarka, 2021). The dependent variables in this study include ‘Leverage’, which is measured as the ratio of total debt to total assets of the company (Cheng, 2014; Fosu et al., 2016; Haron et al., 2013; Mulyani et al., 2016), and ‘Firm Value’, which is measured by two indicators. The first indicator is Tobin’s Q, which is the ratio of market value to book value of total assets (García-Meca et al., 2022; Li & Chen, 2018; Venusita & Agustia, 2021), and the second is return on assets (ROA), which is the ratio of net income (EBIT) to total assets (Gurusamy, 2021; Keasey et al., 2015; Le & Phan, 2017). Finally, this study also includes several control variables, including ‘Firm Size’, which is measured as the natural logarithm of the firm’s total assets (Haron et al., 2013; Pindado & De La Torre, 2011); ‘Sales Growth’, which is calculated as the percentage change in sales turnover (Fosu et al., 2016; Kim et al., 2017; Liew & Devi, 2021); ‘Tangibility’, measured as the ratio of fixed assets to total assets of the firm (Flannery & Rangan, 2006); and ‘Firm Age’, measured as the natural logarithm of firm age (Bjuggren et al., 2018; Liew & Devi, 2021).

We used a linear regression model to this study. The independent variable in this study is time-invariant, so using a panel model with cross-section fixed-effects (FE) is considered inappropriate (Wooldridge, 2008). The author also noticed that with a large sample of companies (N) and a short period (t), FE estimation is inconsistent and can lead to loss of degrees of freedom, so FE can exacerbate multicollinearity problems if solved using least squares dummy variables (Baltagi, 2008). Therefore, the authors used the ordinary least squares model. In such cases, the LM test is always significant at a high level (p < .1%); therefore, the authors will use a panel model with cross-sectional random effects (RE) as in (D’Amato, 2017). The general model is as follows:

As for testing the usual least squares regression model for the interaction model, we use the general model as follows:

Leverage i,t = β0 + β1Family control i,t + (β2Family control i,t × Female directors i,t) + φ Control i,t + ε i,t

Firm Value i,t = β0 + β1Family control i,t + (β2Family control i,t × Female directors i,t) + φ Control i,t + ε i,t

This study also uses robust standard errors in each model to overcome heteroscedasticity and autocorrelation problems so that the estimated model becomes BLUE (best linear unbiased estimator) (Wooldridge, 2010).

Result

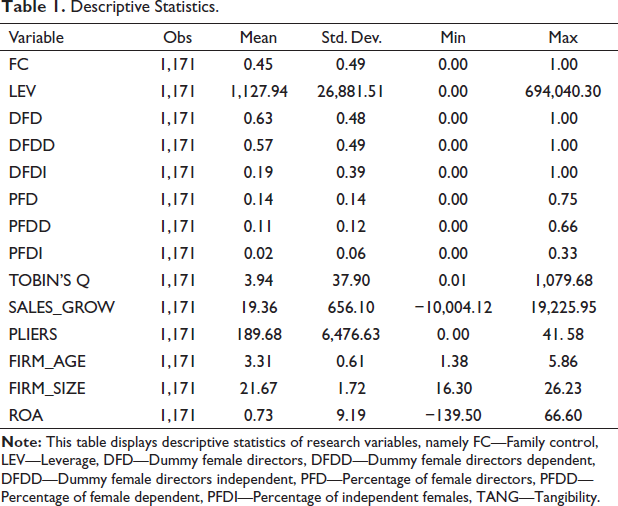

Table 1 illustrates that, out of 1,171 observations, the average family-controlled firm is 0.45. With a standard deviation of 0.49, this data is binary (0 or 1), indicating that approximately 45% of the firms are family-controlled. The mean leverage is 1,127.94, with a very high standard deviation (26,881.51) indicating significant variation in leverage among the observed firms. Leverage ranges from 0.00 to 694,040.30. DFD, DFDD, DFDI (dummy female directors, dependent, independent)––the average firm has 63% female directors (both dependent and independent), with 57% as dependent female directors and 19% as independent female directors. This data is binary, similar to FC. PFD, PFDD, PFDI (percentage of female directors, dependent, independent)––the average company has 14% female directors, with 11.5% as dependent female directors and 2.7% as independent female directors.

Descriptive Statistics.

The average Tobin’s Q is 3.94, with a very high standard deviation (37.90), indicating significant variation in Tobin’s Q among the observed companies. Tobin’s Q values range from 0.013 to 1,079.68. The average sales growth is 19.37, with a very high standard deviation (656.10), indicating significant variation in sales growth among the observed companies. Sales growth ranges from −10,004.12 to 19,225.95. The average tangibility is 189.68, with a very high standard deviation (6,476.63), indicating significant variation in tangibility among the observed companies. Tangibility ranges from 0.00 to 41.58. The average firm age is 3.31 years with a standard deviation of 0.61, indicating that firm age ranges from 1.38 to 5.86 years. The average company size is 21.67 with a standard deviation of 1.72, indicating that the company size ranges from 16.30 to 26.23. The average ROA is 0.73, with a very high standard deviation (9.19), indicating variation in ROA.

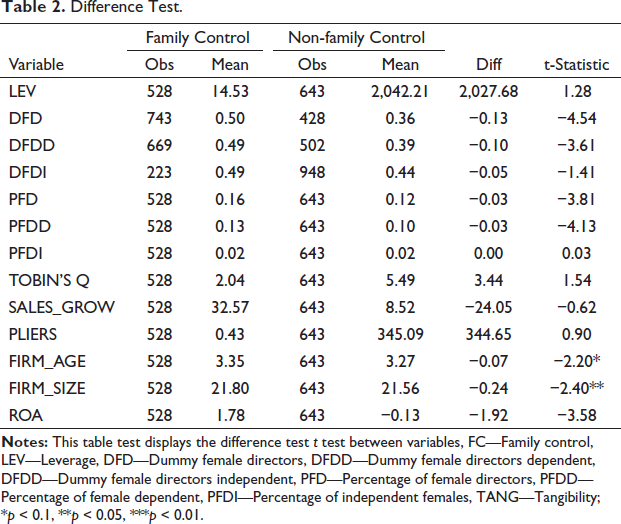

Table 2 reveals that the average leverage of non-controlled firms (2,042.21) is higher than that of controlled firms (14.53). However, the t-statistic value is 1.28, indicating that the difference is insignificant. Regarding the proportion of female directors, both dependent (DFD, DFDD) and independent (DFDI), family-controlled firms show higher numbers than non–family-controlled firms. This difference is significant at the (p < .01) level for DFD and DFDD but insignificant for DFDI. The same situation is also seen in the PFD, dependent and independent (PFDD, PFDI), where family-controlled firms have a higher percentage than non–family-controlled firms. This difference is significant at the (p < .01) level for PFD and PFDD and insignificant for PFDI. The average Tobin’s Q is higher in non–family-controlled firms (5.49) than in family-controlled firms (2.04). However, this difference is not significant.

Difference Test.

Meanwhile, the average sales growth is higher in family-controlled firms (32.57) than in non–family-controlled firms (8.52). Again, this difference is not significant. Average tangibility is much higher in non–family-controlled firms (345.09) than in family-controlled firms (0.43), but this difference is insignificant. The average firm age is slightly higher in family-controlled firms (3.35) than in non–family-controlled firms (3.27). This difference is significant at the (p < .1) level. The average firm size is slightly larger in family-controlled firms (21.80) than in non–family-controlled firms (21.56). This difference is significant at the (p < .05) level. Finally, the average ROA is higher in family-controlled firms (1.78) than in non–family-controlled firms (−0.13). This difference is significant at the (p < .01) level.

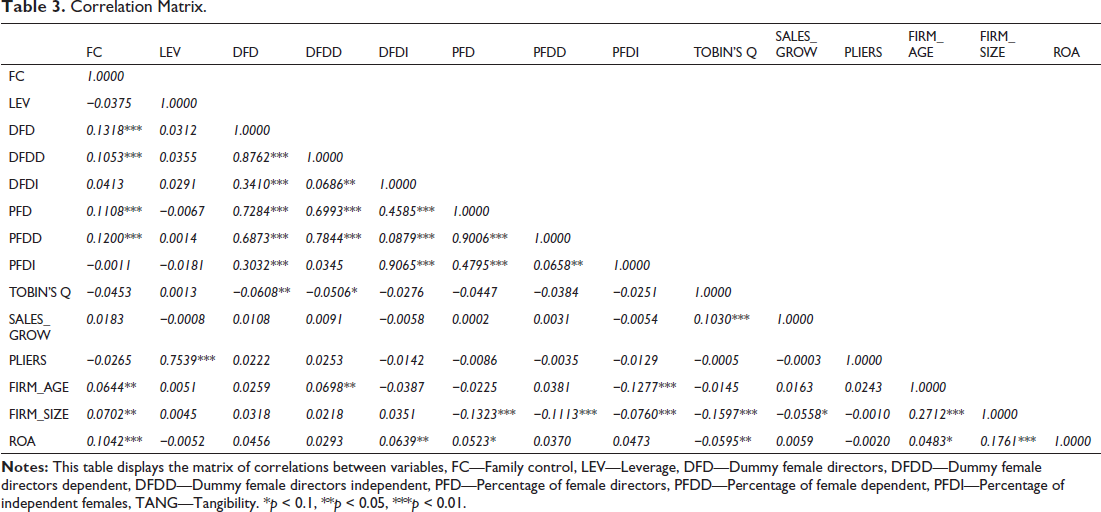

Table 3 illustrates that the correlation coefficients between our main variables are very low. Thus, we conclude that our model’s multicollinearity problem is insignificant. In particular, we find no significant relationship between FC and leverage. However, we find that FC is positively and significantly associated with female directors, referred to as DFD (β = 0.13, p < .01) and DFDD (β = 0.10, p < .01). Furthermore, we also find that FC is positively associated with female directors in the PFD (β = 0.11, p < .01) and DFDD (β = 0.12, p < .01) categories. Different results were shown with independent female directors, who had no significant relationship with FC. These findings suggest that female directors have high involvement in family-controlled firms, especially dependent female directors. Meanwhile, independent female directors show no significant involvement, indicating that they have no significant impact on family-controlled firms.

Correlation Matrix.

Regression Analysis

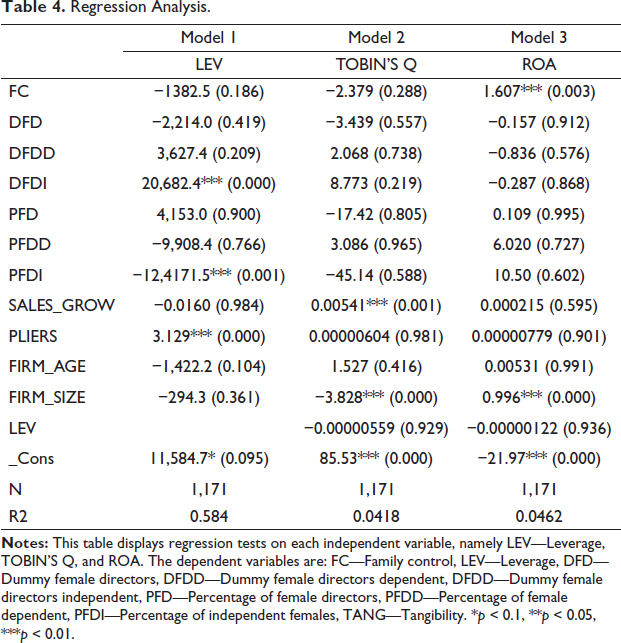

Table 4 displays the results of three different regression analyses, each of which uses a different dependent variable: LEV, Tobin’s Q and ROA. Based on the regression analysis of the first model with leverage as the dependent variable, we find that FC has a negative but insignificant effect on leverage, with a significance level of (β = −1382.50, p > .1). This suggests that FC tends to lower corporate debt, although the effect is insignificant. The only variable with a positive and significant effect is DFDI, with a significance level (β = 20,682.40, p < .01). This finding indicates that the presence of independent female directors tends to increase corporate debt. Meanwhile, the PFDI variable has a negative and significant effect, with a significance level (β = −3.12, p < .01). This indicates that the greater the portion of independent female directors in the company, the lower the level of corporate debt. The control variable tangibility has a positive and significant effect, with a significance level (β = 3.12, p < .01). Other variables, including controls, do not show a significant effect.

Regression Analysis.

Meanwhile, the second regression model analysis with Tobin’s Q as the dependent variable found that FC has a negative but insignificant effect on Tobin’s Q, with a significance level (β = −2.37, p > .1). This indicates that FC tends to reduce firm value. Similarly, the DFD variable found that the presence of female directors has a negative but insignificant effect on Tobin’s Q, with a significance level (β = −3.43, p > .1). This indicates that the presence of female directors tends to reduce firm value. Meanwhile, the DFDD variable found that dependent female directors have a positive but insignificant effect on Tobin’s Q, with a significance level (β = 2.06, p > .1). This indicates that dependent female directors tend to increase firm value. Meanwhile, the DFDI variable found that independent female directors have a positive but insignificant effect on Tobin’s Q, with a significance level (β = 2.06, p > .1). This indicates that the presence of independent female directors tends to increase firm value.

PFD variable found that the presence of female directors has a negative but insignificant effect on Tobin’s Q, with a significance level (β = −17.42, p > .1). This indicates that the greater portion of female directors tends to reduce the company’s value. Meanwhile, the PFDD variable found that dependent female directors have a positive but insignificant effect on Tobin’s Q, with a significance level (β = 3.08, p > .1). This indicates that the greater portion of dependent female directors tends to increase the company’s value. Meanwhile, the PFDI variable found that independent female directors have a negative but insignificant effect on Tobin’s Q, with a significance level (β = −45.14, p > .1). This indicates that the greater portion of independent female directors tends to reduce the company’s value. The sales growth control variable has a positive and significant effect, with a significance level (β = 0.00, p < .01). The firm size variable has a negative and significant effect, with a significance level (β = −3.82, p < .01), while other control variables do not show a significant effect.

Meanwhile, the analysis of the third regression model with ROA as the dependent variable found that FC has a positive but significant effect on ROA, with a significance level (β = 1.60, p < .01). This suggests that FC tends to improve firm value. Similarly, the DFD variable found that the presence of female directors has a negative but insignificant effect on ROA, with a significance level (β = −0.15, p > .1). This indicates that the presence of female directors tends to reduce company performance. Meanwhile, the DFDD variable found that the presence of female directors has a negative but insignificant effect on ROA, with a significance level (β = −0.83, p > .1). This indicates that dependent female directors tend to reduce company performance. Meanwhile, the DFDI variable found that independent female directors have a negative but insignificant effect on ROA, with a significance level (β = −0.28, p > .1). This indicates that the presence of independent female directors tends to reduce firm value.

PFD variable found that the presence of female directors has a positive but insignificant effect on ROA, with a significance level (β = 0.10, p > .1). This indicates that the greater portion of female directors tends to improve company performance. Meanwhile, the PFDD variable found that dependent female directors have a positive but insignificant effect on ROA, with a significance level (β = 6.02, p > .1). This indicates that the greater portion of dependent female directors tends to improve company performance. Meanwhile, the PFDI variable found that independent female directors have a positive but insignificant effect on ROA, with a significance level (β = 10.50, p > .1). This indicates that the greater portion of independent female directors tends to improve firm performance. The control variable firm size has a positive and significant effect, with a significance level (β = 0.99, p < .01), while other control variables do not show a significant effect.

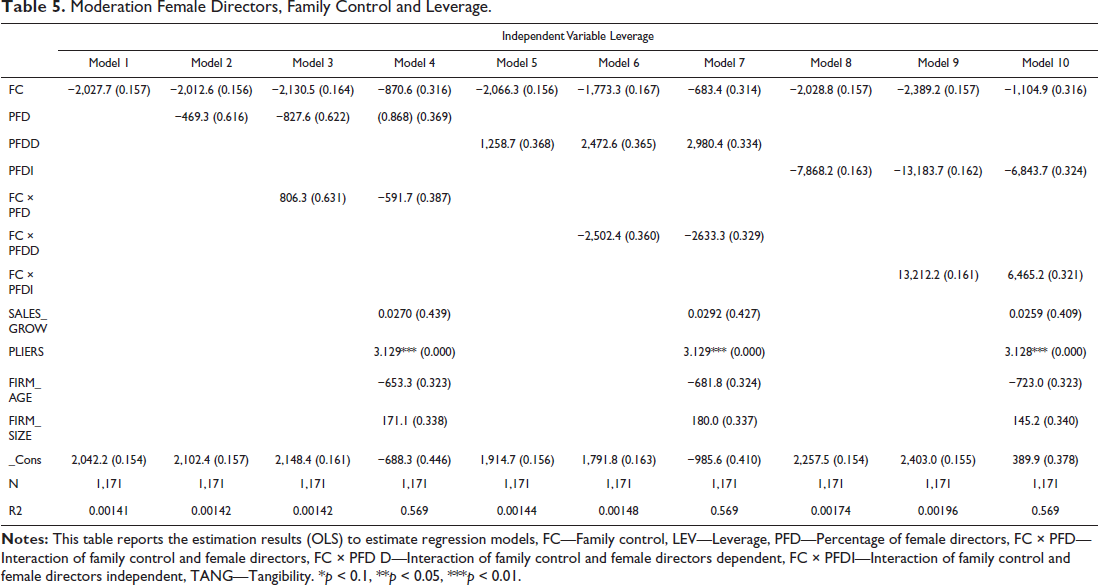

Table 5 details the moderation analysis of female directors on FC and leverage. We present 10 models in Table 5 to make the moderation analysis more conclusive. The moderation analysis of female directors in Table 5 uses the measurement tools of the PFD, percentage of dependent female directors and percentage of independent female directors. Due to data limitations, FC is only measured using a dummy (binary) measure. Based on the table, the FC variable consistently across all models has an insignificant negative effect on leverage with a significance level of (p > .1). This suggests that family-controlled firms prefer to reduce debt rather than increase it.

Moderation Female Directors, Family Control and Leverage.

The female director variable measured using the PFD’s shows that models 2 and 3 in Table 5 have an insignificant negative effect. In contrast, model 4 shows a significant positive effect, with a significance level of (p > .1). This suggests that when the control variables are included in the model, the proportion of female directors on the board tends to favour increasing debt over reducing debt. The percentage of dependent female directors in models 5, 6 and 7 consistently show insignificant positive results on leverage with a significance level of (p > .1). This suggests that the proportion of dependent female directors on the board tends to favour taking on debt rather than reducing debt. Meanwhile, in models 8, 9 and 10, the percentage of independent female directors consistently has an insignificant negative effect on leverage with a significance level of (p > .1). This suggests that the proportion of independent female directors on the board tends to favour reducing debt rather than increasing it.

Analysis of the moderating between FC and the PFD on leverage shows inconsistent results. Model 3 shows a positive but insignificant moderating effect, while model 4 shows a negative and insignificant interaction effect, with a significance level of (p > .1). This suggests that when control variables are included in the model, the interaction between FC and the PFD on leverage tends to reduce debt in family-controlled firms. For the moderation analysis between FC and the percentage of female dependent directors, the results are consistent. Models 6 and 7 show that the moderating has an insignificant negative effect on leverage with a significance level of (p > .1). This suggests that the interaction between FC and the PFD’s dependent on leverage tends to reduce debt in family-controlled firms. The results are consistent in the context of the moderation analysis between FC and the percentage of independent female directors. Models 9 and 10 show that moderation has an insignificant positive effect on leverage with a significance level of (p > .1). This suggests that the interaction between FC and the percentage of independent female directors on Leverage tends to increase debt in family-controlled firms. Finally, control variables, such as sales growth and firm size in models 4, 7 and 10, consistently have an insignificant positive effect on leverage with a significance level (p > .1). Meanwhile, the control variable firm age in the same models consistently has a negative and insignificant effect on leverage with a significance level of (p > .1). The tangibility control variable in models 4, 7 and 10 consistently has a significant positive effect on leverage with a significance level (p < .01).

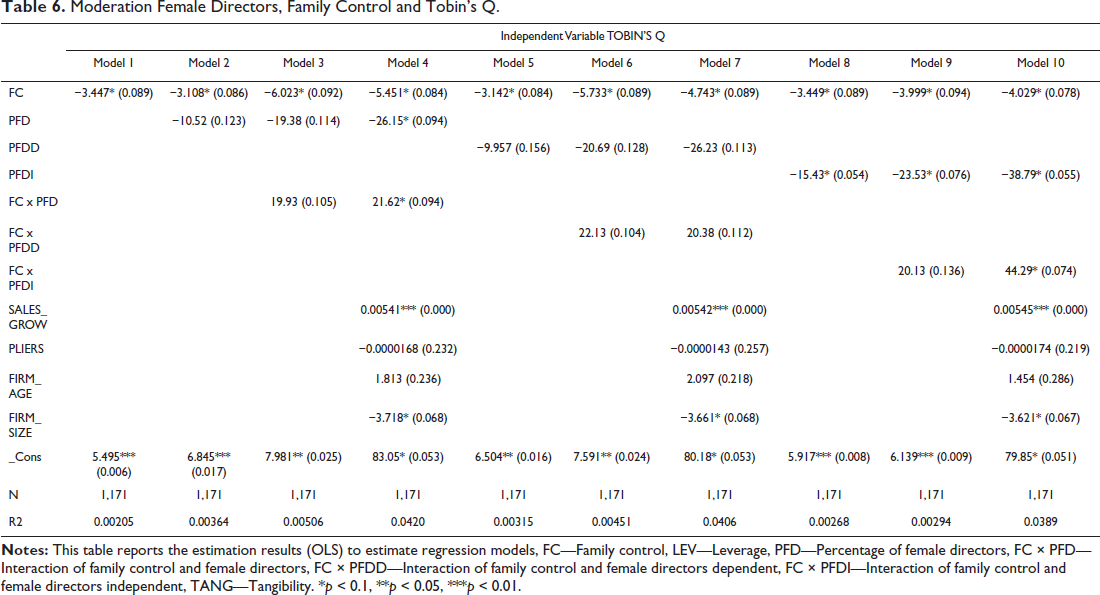

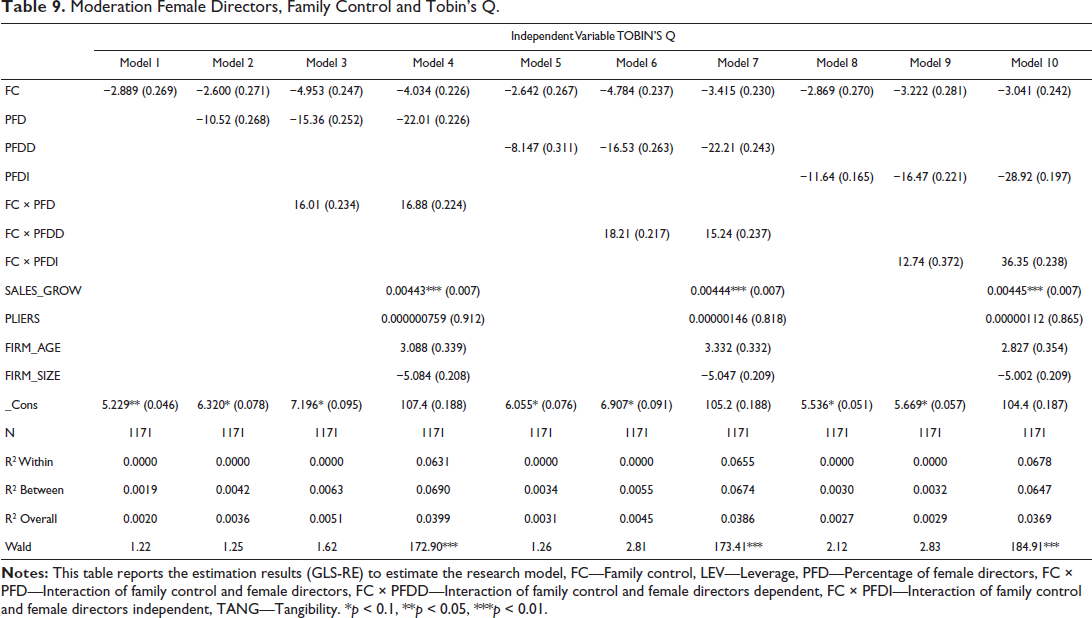

Table 6 details the moderation analysis of female directors on FC and Tobin’s Q. The authors present 10 models in Table 6 to make the moderation analysis more conclusive. The moderation analysis of female directors in Table 8 uses the measurement tools of the PFD, percentage of dependent female directors and percentage of independent female directors. Due to data limitations, FC is only measured using a dummy (binary) measure. Based on the table, the FC variable consistently negatively affects Tobin’s Q with significance (p < .1). This suggests that family-controlled firms tend to lower firm value. The female director variable measured using the PFD consistently has a negative influence on Tobin’s Q, specifically in model 4 shows the PFD has a significant negative effect on Tobin’s Q with significance (β = −26.15 p < .1). This suggests that the proportion of female directors tends to decrease firm value.

Moderation Female Directors, Family Control and Tobin’s Q.

The female director variable measured using the percentage of dependent female directors consistently has an insignificant negative effect on Tobin’s Q with significance (p > .1). This suggests that the proportion of dependent female directors on the board tends to decrease firm value. The female director variable measured using the percentage of independent female directors in models 8, 9 and 10 consistently negatively affects Tobin’s Q with significance (p < .1). This suggests that the proportion of female directors on independent boards tends to decrease firm value. The moderation analysis between FC and the PFD on Tobin’s Q shows consistent results of positive effect on Tobin’s Q. Specifically, model 4 shows that moderation significantly affects Tobin’s Q with a significance level (p > .1). This suggests that the interaction between FC and the PFD on Tobin’s Q tends to increase the value of family-controlled firms. The moderation analysis between FC and the PFD’s dependent on Tobin’s Q shows consistent results. Models 6 and 7 show that moderation has an insignificant positive effect on Tobin’s Q with a significance level of (p > .1). This suggests that the interaction between FC and the PFD dependent on Tobin’s Q tends to increase the value of family-controlled firms. The moderation analysis between FC and the percentage of independent female directors on Tobin’s Q shows a positive effect on Tobin’s Q. Specifically, model 10 shows that moderation significantly positively affects Tobin’s Q with a significance level (p < .1). This suggests that the interaction between FC and the percentage of independent female directors on Tobin’s Q tends to increase the value of family-controlled firms. Finally, control variables, such as sales growth in models 4, 7 and 10, consistently have a significant positive effect on Tobin’s Q with a significance level (p < .01). Meanwhile, the control variable company age in models 4, 7 and 10 consistently has an insignificant positive effect on Tobin’s Q with a significance level (p > .1). Meanwhile, the firm size control variable in the same models consistently negatively affects Tobin’s Q with a significance level (p < .1). The tangibility control variable in models 4, 7 and 10 consistently has an insignificant negative effect on Tobin’s Q with a significance level (p > .1).

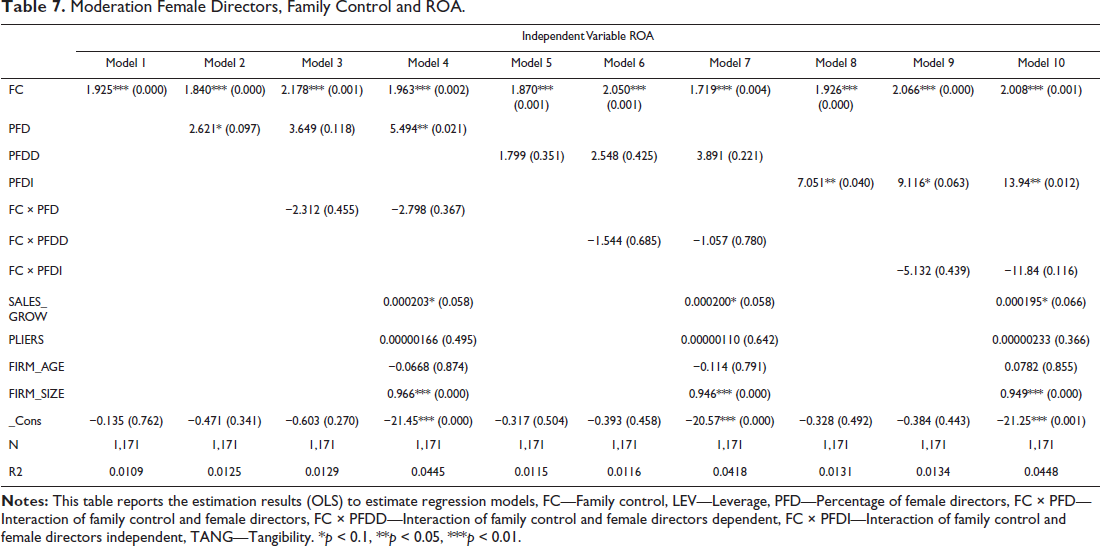

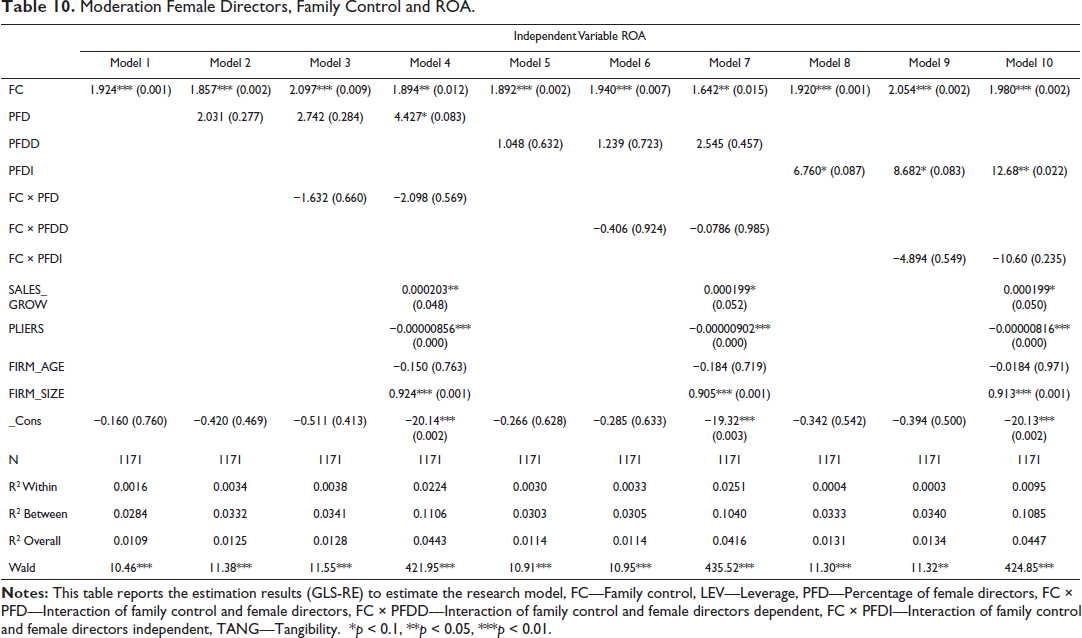

Table 7 details the moderation analysis of female directors on FC and ROA. The authors present 10 models in Table 7 to make the moderation analysis more conclusive. The moderation analysis of female directors in Table 7 uses the measurement tools of the PFD, percentage of dependent female directors and percentage of independent female directors. Due to data limitations, FC is only measured using a dummy (binary) measure. Based on the table, the FC variable consistently from model 1 to model 10 has a significant positive effect on ROA with significance (p < .01). This indicates that family-controlled companies affect good corporate performance. The female director variable measured using the PFD consistently has a positive effect on ROA, specifically in Table 7 model 2 shows the PFD has a significant positive effect on ROA with significance (β = 2.62 p < .1), and in Table 7 model 4 shows the PFD has a significant positive effect on ROA with significance (β = 5.49 p < .01). This indicates that the proportion of female directors on the board can improve firm performance when all control variables are included.

Moderation Female Directors, Family Control and ROA.

The female director variable measured using the percentage of dependent female directors consistently in models 5, 6 and 7 has an insignificant positive effect on ROA with significance (p > .1). This suggests that the proportion of dependent female directors on the board can improve firm performance, albeit insignificantly. The female director variable measured using the percentage of independent female directors consistently has a positive and significant effect on ROA, with significance (p < .5). This suggests that the proportion of female directors on independent boards can improve firm performance when all control variables are included. The moderation analysis between FC and the PFD on ROA shows consistent results. Models 3 and 4 show that moderation has an insignificant negative effect on ROA with a significance level of (p > .1). This suggests that the interaction between FC and the PFD on ROA tends to lower the performance of family-controlled companies. The moderation analysis between FC and the percentage of dependent female directors on ROA shows consistent results. Models 6 and 7 show that the interaction has an insignificant negative effect on ROA with a significance level of (p > .1). This suggests that the interaction between FC and the percentage of dependent female directors on ROA tends to lower the performance of family-controlled firms. The moderation analysis between FC and the percentage of independent female directors on ROA shows consistent results. Models 9 and 10 show that moderation has an insignificant negative effect on ROA with a significance level of (p > .1). This suggests that the interaction between FC and the percentage of independent female directors on ROA tends to lower the performance of family-controlled firms. Finally, control variables, such as sales growth in models 4, 7 and 10, consistently have a significant positive effect on ROA with a significance level (p < .1). The control variable tangibility in models 4, 7 and 10 consistently has an insignificant positive effect on ROA with a significance level (p > .1). Meanwhile, the control variable firm size in the same models consistently has a significant positive effect on ROA with a significance level (p < .01). Meanwhile, the firm age control variable in the model inconsistently has no significant negative effect on ROA with a significance level (p > .1).

Robustness Test

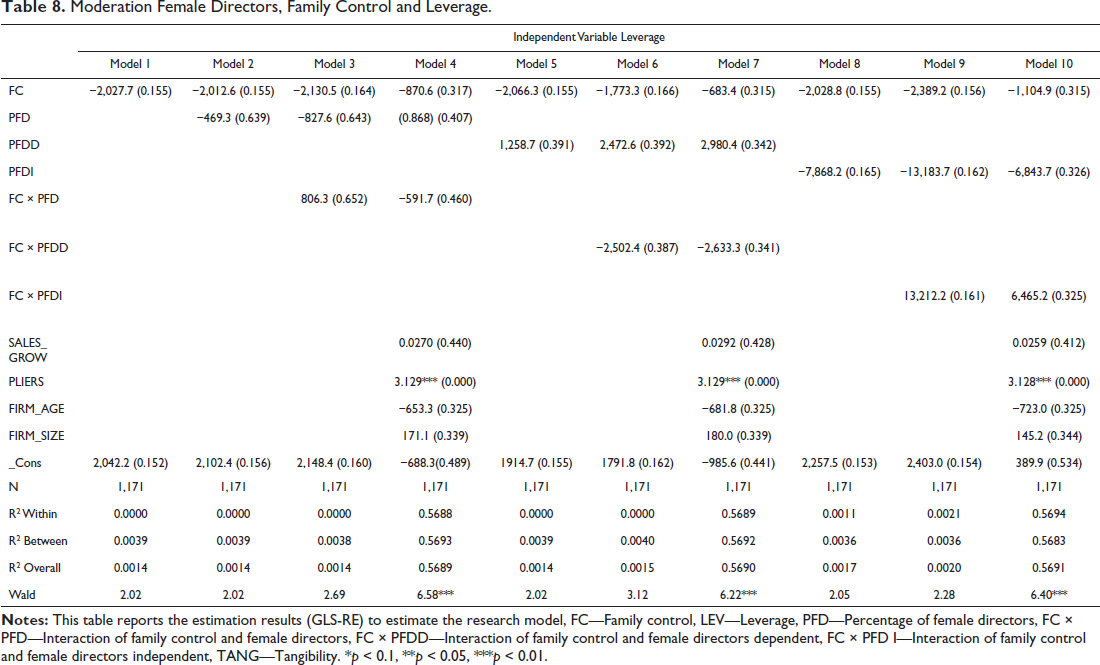

This study tries to test the robustness of the results with different estimation methods. First, the authors test for robustness to first-order autoregressive noise (if any) in an unbalanced panel and cross-sectional correlation and heteroscedasticity across the panel using generalised least square (GLS) RE techniques following research (D’Amato, 2017). Due to unobserved firm heterogeneity, panel FE estimation is recommended (Wooldridge, 2010). However, as discussed earlier, such FE estimation is unsuitable for this study. Therefore, an alternative to FE, namely, GLS RE, is used in this study.

All the models in Table 8 that are of significant concern to the researcher, namely the interaction between FC and the PFD (dependent and independent) on leverage in the study, are generally insignificant at the (p > .1) level. This is similar to Table 5 presented, where the sign and significance of the coefficients are the same. Thus, we can conclude that our results are robust to within-panel unbalanced autoregressive (AR 1) noise and cross-sectional correlation, and between-panel heteroscedasticity.

Moderation Female Directors, Family Control and Leverage.

All models in Table 9 that are of particular interest to the researcher, namely the interaction between FC and the PFD (dependent and independent) on Tobin’s Q, are generally insignificant at the (p > .1) level. This is slightly different from Table 6, where previously models 4 and 10 were significant at the (p < .1) level. However, the other variables are unchanged, where the sign and significance of the coefficients are the same as in the previous Table 6. Thus, we can conclude that our results are robust to within-panel unbalanced autoregressive (AR 1) noise and cross-sectional correlation, and between-panel heteroscedasticity.

Moderation Female Directors, Family Control and Tobin’s Q.

All models in Table 10 that are of significant interest to the researcher, namely the interaction between FC and the PFD (dependent and independent) on ROA in the study, are generally insignificant at the (p > .1) level. This is similar to Table 7 presented, where the sign and significance of the coefficients are the same. Thus, we can conclude that our results are robust to within-panel unbalanced autoregressive (AR 1) noise and cross-sectional correlation, and between-panel heteroscedasticity.

Moderation Female Directors, Family Control and ROA.

Discussion and Implications of the Study

The results of this study contradict those of previous studies because they were carried out in different countries and at different times. In addition, the conflicting results may be due to the different estimation methods used by different researchers, such as the different number of samples/observations and the different control variables used. Therefore, the use of panel data in this study provides a more reliable picture than cross-sectional studies. In addition, this study fully supports the pecking order theory, which describes the financing hierarchy of the firm (Myers & Majluf, 1984). Furthermore, this result also contrasts with other studies which suggest that family firms tend to increase debt. Although some studies suggest that family firms tend to increase debt (Du and Dai, 2005; Poletti-Hughes & Martinez Garcia, 2022; Setia-Atmaja et al., 2009), our results suggest otherwise. Myers and Majluf (1984) found that family firms tend to use retained (internal) earnings more than debt and choose equity as the last financing option. This is consistent with the pecking order theory, where debt is considered a riskier financing option than internal financing. This concept also supports Haider et al.’s (2021) finding that family firms in Southeast Asia adopt similar leverage policies to non-family firms, suggesting that structural decisions on leverage and security issuance do not differ significantly between the two types of firms.

This article has some important implications for academicians and practician. First, the findings of this study revealed that empirical evidence related to agency theory (Jensen & Meckling, 1976; Jensen, 1986) and trade-off theory (Kraus & Litzenberger, 1973; Myers, 1984). Starting with that female director can align and balance the interests of majority and minority shareholders. The findings suggest that in family-controlled firms adding a quota of female directors on the board with the assumption that their presence will automatically improve firm performance and effectiveness is still unclear. The results of this study show inconsistencies. In the context of family firm performance measured using the ROA, these findings indicate that FC positively influences firm value. This aligns with agency theory which states that families can function as effective supervisors and controls in the company. Another study conducted by Anderson and Reeb (2003) supports this finding that showed family firms, whether new or long-established, have higher Tobin’s Q values than non-family firms. They argue that family firms perform better than non-family firms.

Based on trade-off and agency theories, independent female directors should ideally be able to balance majority and minority shareholders. However, the findings of this study show different results. Independent female directors are less effective in family firms, particularly those that do not prioritise gender equality. Thus, their opinions tend to be ignored, and they experience many barriers and difficulties in interacting with other board members, especially men. Regarding agency theory, Carter et al. (2003) state that board member diversity only sometimes results in effective supervision. Instead, diverse board members may be marginalised. This view is in line with that of Campbell and Mínguez-Vera (2008), who assert that the appointment of female board members may negatively impact if motivated by societal pressure to improve gender equality. Although independent women directors have an important role in supervision, their effectiveness is weakened in family-controlled companies. They experience difficulties in exercising oversight in family-controlled companies, as access to opportunities and mentoring networks are fully held by majority shareholders. This behaviour is detrimental to minority shareholders. Fischer et al. (1993) also state that women perform worse than men because they feel disadvantaged due to discrimination and lack of resources, such as education and business experience. However, the ability of an independent board is not necessarily related to gender but is determined by its quality, experience, education level and skills (Campbell & Mínguez-Vera, 2008).

Second, this study contributes to insights on investor protection and ownership concentration are highly relevant to Indonesia and other emerging markets. They can inform stakeholders on how to navigate the unique challenges of these markets, improve corporate governance and foster a more investor-friendly environment. Despite challenges, companies in Indonesia can still thrive. This could be invaluable for Indonesian businesses looking to improve their governance practices, attract investment and ultimately grow sustainably.

Conclusion

This study found that family firms and firms with female directors tend to have lower leverage, which aligns with Pecking Order Theory. In the context of family firms, this study shows the positive influence of FC on firm performance, as measured through the ROA proxy. This finding supports the agency theory that families can be effective supervisors and controls within the firm. However, other findings show differences, particularly when firm value is measured using Tobin’s Q as a proxy. The results show that FC hurts firm values. According to agency theory, this phenomenon may be caused by opportunistic, altruistic and nepotistic behaviour in family firms. This study also found that diversity in the board of directors of family-controlled firms hurts firm performance. This finding is consistent with agency theory which states that family firms tend to face more conflicts when the board of directors becomes more diverse.

According to trade-off theory, balancing gender diversity does not necessarily require an excessive increase in quotas but rather in proportion to the company’s needs. In this context, the presence of women from controlling families on boards can be a source of conflict with other stakeholders and has the potential for opportunistic behaviour (García-Meca et al., 2022). Female directors from the owner’s family often lack independence, which can increase agency conflicts. This may occur due to their tendency to act proactively in maintaining unity and preserving family wealth. In line with trade-off and agency theories, ideally, independent female directors can be a counterbalance between majority and minority shareholders. However, this study found that independent female directors are less effective in family firms, particularly those that do not prioritise gender equality.

There are some limitations in this study. One is that the data we collected comes only from Indonesia, so the possibility of generalising our findings is limited. This study uses secondary data, which exposes all the limitations inherent in secondary data analysis. In addition, this study only family firms in the context of listed companies, where there is more potential to finance investments through equity than debt. On the other hand, the institutional environment in emerging economies is very different from developed economies where the representation of women on boards of directors is still low compared to developed economies. The answer to the question of how and why female directors moderate the relationship between FC and firm performance is still unclear, so further theory development is needed to help us understand the mechanism of the moderating role in the relationship.

This research focuses on female directors of family and non-family origin; however, it also offers promising avenues for future international research. Institutional and cultural contexts may be important when analysing board diversity and its impact. Therefore, further studies should include cross-country analyses. Thus, a comparison of our results with other cultural and regulatory contexts will enrich the debate on board gender diversity in corporate governance and firm performance in both developing and developed countries. Other diversity indicators such as age, nationality and differences in educational and occupational backgrounds need to be considered in further research. This study also opens up opportunities for additional research, such as exploring the role of founders in the firm and how they contribute to firm value. Future studies could also delve deeper into the differences between women and men or between family and non-family male directors. Another suggestion for this study is to continue and develop the research focusing on family firms that still need to be listed. The aim is to explore the effect of gender diversity in family firm management on firm value especially for family firms whose management is not constrained by public interest because the public does not own shares in the company. This is expected to provide a deeper and richer understanding of how board dynamics function in family firms.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.