Abstract

This article aims to investigate the relationship between green banking adoption practices and performance. A conceptual model has been developed to test the moderating effect of top management commitment in the relationship between green banking adoption practices and performance in a lower-middle-income country context, that is, India. Using a survey instrument, data were collected from 393 employees working in banks in southern India. First, the psychometric properties of the survey instrument were checked using LISREL software for structural equation modelling. Second, the hypothesised relationships were tested using hierarchical regression and double-checked with path analysis. The findings indicate that green banking adoption practices are precursors to environmental, operational and financial performance. The results also provide support for the moderating effect of top management commitment in the relationship between green banking adoption practices and (a) environmental performance, (b) operational performance and (c) financial performance. The green adoption practices encompass a range of initiatives to reduce environmental impact, promote sustainability and address climate change concerns. Top management commitment is at the forefront of driving these practices, which plays a pivotal role in shaping organisational strategies and fostering a culture of sustainability. To the best of our knowledge, the model developed is the first of its kind, particularly in the context of banks in India. Investigating the interaction effect of top management commitment in enhancing performance is a novel idea and significantly contributes to the literature on sustainability. The implications for theory and practice are discussed.

Keywords

Introduction

Recent years have witnessed increasing attention towards green banking worldwide (Arumugam & Chirute, 2018; Aslam & Jawaid, 2022; Belova et al., 2023; Bouteraa et al., 2021; Bukhari et al., 2022). Growing environmental concern has resulted in a radical change in the way banks conduct business (Ahuja, 2015; Bowman, 2010). Furthermore, attention has been directed towards environment-friendly banking practices (Hermawan & Khoirunisa, 2023; Meena, 2013; Shakil et al., 2014). Green banking evolved in the last decade to address banks’ negative influence on the environment (Rehman et al., 2021). Green banking is a type of banking that focuses on environmental protection and sustainable development (SD) while taking into account all social and environmental factors. As a result, the phrase ‘sustainable development’ has expanded worldwide and is now used by international organisations, development planners, researchers, and environmental and SD advocates (Ukaga et al., 2010). Rapid global adoption of green banking signifies a growing trend towards embracing business practices that align with social and environmental standards. Green banking prioritises the preservation of the environment, actively working to prevent ecological degradation and contribute to a more sustainable and liveable planet (Islam et al., 2020). Inadequate industrialisation has degraded the ecosystem and caused natural and industrial disasters (Rehman et al., 2021).

As opposed to the traditional bank, which focuses only on financial transactions and profitability, a green bank goes one step beyond by considering all social, environmental and ecological factors to protect the environment and conserve natural resources. More essentially, the mission of a green bank is to conduct banking activities considering the impact of financial transactions on ecological factors. The terms ‘green bank’, ‘ethical bank’ and ‘sustainable bank’ are interchangeable because the banks focus on maintaining quality, environment and social (QES) standards (Ikram et al., 2019). Banks adopt green banking practices by encouraging customers to use technology by engaging in online banking (online bill payment, conducting operations online), including digital banking (Bose & Gupta, 2017; Bukhari et al., 2020; Rehman et al., 2021; Tu & Dung, 2017). Thus, green banking refers to conducting business in such a way as to reduce external carbon emissions and internal carbon footprint (Masud et al., 2018). Green banking involves environmentally responsible financing; that is, before sanctioning finances, banks must evaluate the environmental risks involved in approving the finances. All banking activities that reduce negative environmental consequences come within the purview of green banking.

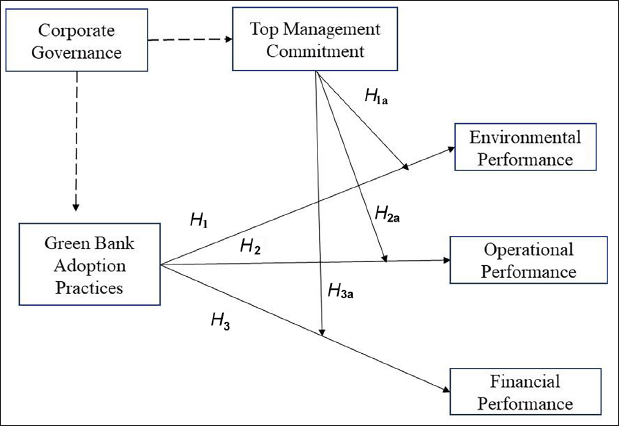

Corporate Governance Mechanism and Green Banking

Growing awareness of environmental protection necessitates organisations to focus on green employee behaviour in manufacturing and service organisations, and the banking industry is not an exception (Cormier et al., 2010; Karaman et al., 2020). Corporate governance mechanism in the banking industry makes it mandatory for banks to adopt green practices and, at the same time, suggests top management the effective implementation of green adoption practices (Islam & Hossain, 2022; Isukul & Chizea, 2017; Nwagbara, 2012). Following agency theory, the governance mechanism is expected to vouch for whether the managers act in the interest of stakeholders, and one of the fruitful ways of achieving this is to show transparency in financial reporting and voluntary disclosure (Brennan & Solomon, 2008; Bushman et al., 2004). With the resurging interest in environmental awareness, the governance mechanism is tilted towards emphasising the disclosure of information pertaining to the green environment in banks (Hsu et al., 2013; Post et al., 2011). Governance mechanisms are reflected in banking when stakeholders are involved in setting green environmental policies and when senior management positions are created for environmental management. Further, corporate governance includes the environmental and public issue committee to settle any disputes arising from violating the environmental regulations in banks. Often, executive compensation is linked to environmental performance and the terms and conditions for financial transactions carried out by the banks when they lend to investors to see that sustainable investments are made.

When the governance mechanism instils a green banking mechanism as the right thing to promote societal welfare, banks are more likely to adopt green banking. Further, top management implements the suggestions of the board of directors to implement green adoption practices. As global warming can be prevented through green banking, corporate governance emphasises green banking adoption. Further, corporate governance in banks is concerned with the health and safety of customers and society; it is essential that they periodically monitor the banks’ operations.

Green Bank Adoption Practices

Over the past decade, several green practices have gained traction to handle current environmental concerns and meet the growing demand from customers for ecologically friendly products (De Steur et al., 2020). To maintain a competitive advantage, green management practices should be implemented, including green adoption practices (Linton et al., 2007). The banking industry has developed and executed many strategies to maintain its operations and improve its EP, including using Fintech.

Top Management Commitment

The strong dedication of top management fosters a heightened sense of accountability, leading to proactive measures and decisive actions being taken at the highest level of leadership (Jazairy & Haartman, 2020). Top management functions as leaders and change agents, ensuring the availability of resources for adopting new business ideologies (Yigitbasioglu, 2015). Due to its power to moderate, top management has a significant impact on whether other business divisions embrace green policies and practices (Ahmed, 2012). The branch level will be able to fully embrace green practices only if the bank’s top management shows an acceptable amount of support or enthusiasm for them. The top management’s success depends on implementing the policies practiced in the branch-level management.

Banking Performance

Traditionally, bank performance is judged based on profitability (Zhang & Yang, 2016), and the success of the banking industry has a snowball effect on economic development (Eyuboglu, 2016). In India, after the nationalisation of banks and with the emergence of several private banks, the expanded competitive landscape created challenges for bank managers to perform better to maintain sustained competitive advantage (Al-Surmi et al., 2020). Though the performance of banks is assessed in terms of market value, growth, number of customers, customer satisfaction, efficiency and productivity (Bikker & Bos, 2008), green banking performance includes environmental and social performance (Selvam et al., 2016). One of the recent studies has reported that green banking helps redirect investments towards environment-friendly activities by organisations, which reduces soil degradation, deforestation and biodiversity loss (Hermawan & Khoirunisa, 2023).

This study considers three performance dimensions: environmental, operational and financial (Bag et al., 2020; Gangi et al., 2019; Zhang & Yang, 2016). Environmental performance is seen in a bank’s efforts to reduce air pollution stemming from the toxic, hazardous, and material (Laosirihongthong et al., 2013). Financial performance, measured in terms of market share, rate of return on investment and assets, is a significant indicator of a company’s performance (Richard et al., 2009; Selvam et al., 2016). The third performance component is ‘operational’, which is concerned with efficiently utilising resources, optimising processes, controlling quality and meeting customer needs (Zhu et al., 2013). In this research, a bank’s performance is assessed through three performance dimensions.

Rationale of the Study

Though banks are not directly involved in environmental pollution (Ahuja, 2015), they may indirectly affect the environment through sanctioning projects of companies that may have deleterious effects on the environment (Bukhari et al., 2020). For example, excessive use of paper and electric power and occupation of excessive space may result in sub-optimal utilisation of resources. The rationale for this study stems from the need to reduce environmental pollution through green banking practices such as making environment-friendly investments (Ikram et al., 2019; Lindenberg & Volz, 2016; Rehman et al., 2021; Sarma & Roy, 2021). Literature review reveals that green banking adoption is a precursor to superior environmental performance (Arumugam & Chirute, 2018; Iqbal et al., 2018; Rehman et al., 2021). Some researchers have documented that managers face several challenges in adopting green banking (Qureshi & Hussain, 2020). However, scholars have a consensus that green banking has significant positive outcomes (Aslam & Jawaid, 2022; Sharma & Choubey, 2022). Some organisation-wide benefits of green banking are financial, operational and environmental performance (Akomea-Frimpong et al., 2022; Aslam & Jawaid, 2022).

While green banking adoption practices have potential benefits, a few studies have examined the role of top management commitment in motivating employees to engage in green banking practices. The study is conducted in the context of a lower-middle-income country, India. According to the India Brand Equity Foundation (IBEF) report, India has 34 banks (12 in the public sector and 22 in the private sector), 46 foreign banks, 56 regional rural banks, 1,485 urban cooperative banks and 96,000 rural cooperative banks (IBEF, 2023). The report says that over 80 per cent of the population had bank accounts in 2022, compared to around 17 per cent in 2009. Considering the large number of banks operating and several companies largely depending on the banks as a source of financing, it is essential to focus on green banking practices. There is a dearth of studies investigating the outcomes of green banking practices in the Indian banking sector. The present study addresses this by answering the research questions mentioned in the next section.

Research Gap

Achieving sustainable development is currently a top priority in most developed nations, leading to stricter regulations on the impact of products during their manufacturing, use and end of life, including the requirement to define reverse logistic strategies and systems (Gou et al., 2008; Hong et al., 2008). The problem at hand pertains to understanding the influence of top management commitment on the adoption practices and performance of green banks. Despite increasing emphasis on environmental sustainability, there needs to be more research exploring the role of top management commitment in driving the implementation of green banking practices. The significance of this issue lies in its potential impact on the adoption and effectiveness of sustainable banking practices, ultimately shaping the overall performance of green banks. To bridge this knowledge gap, it is crucial to investigate how top management commitment influences green bank adoption practices (GBAPs) and how it subsequently affects their performance outcomes. This study attempts to answer the following research questions (RQs):

RQ1: How are green banking adoption practices related to environmental, operational and financial performance?

RQ2: How does top management commitment moderate the relationship between green adoption practices and environmental, operational and financial performance?

This study makes five contributions to the advancement of a sustainable environment. First, it highlights the importance of green banking adoption practices in positively influencing environmental performance. Especially in the context of a lower-middle-income country like India, characterised by a vast banking system where over 70,000 banks function, the study suggests implementing green banking practices to protect the environment from pollution. Second, the results from this research provide strong evidence of the positive effect of green banking adoption practices on the operational performance of banks. Third, the positive influence of green banking adoption on financial performance indicates the importance of going green in banks, too. Fourth, this study underscores the importance of top management commitment to strengthening the positive effect of green banking adoption practices on banks’ environmental, operational and financial performance. Fifth, the simple model of showing the moderation effect of top management commitment in the relationship between green banking adoption practices and outcomes adds to the growing literature on sustainable development, especially in the context of India’s banking system. In summary, this study’s outcomes may recommend that policymakers and regulatory bodies encourage green banking practices, leading to a more environmentally conscious financial sector and contributing to broader sustainability goals. This study adds to the literature on corporate governance mechanism in influencing the agents to act in favour of principals and stakeholders interested in promoting a green environment.

Theoretical Background and Hypothesis Development

We use institutional theory (DiMaggio & Powell, 1983), resource-based view (Barney, 1991) and agency theory (Eisenhardt, 1989) to provide theoretical underpinnings for the present study. According to institutional theory, three institutional isomorphic pressures—coercive, normative and mimetic—require and expect organisations to comply with the demands to protect the environment. Coercive pressures make it mandatory for organisations to implement environment-friendly practices, and governments and local agencies implement environmental regulations in manufacturing and service firms such as banks (Sarkis et al., 2010; Zhu et al., 2013). Normative pressures suggest organisations follow social norms of increased expectations of preventing environmental degradation (Lai et al., 2011). Mimetic pressures prompt organisations to mimic competitors’ strategies in green production, marketing, packaging and banking (Christmann & Taylor, 2001). These three isomorphic forces motivate banks to adopt green banking practices (Harris, 2006).

Another theory on which the present study is based is RBV, according to which organisations attempt to maintain a sustained competitive advantage by implementing the pro-environmental practices considered as strategic competencies. Companies engaging in pollution prevention, environmental protection and emission reduction and contributing to the sustainability of the environment may enjoy a competitive advantage (Aragon-Correa & Sharma, 2003). Several studies in the past have documented the positive association of pro-environmental behaviours with performance and profitability (Aracil et al., 2021; Aslam & Jawaid, 2022; Watson et al., 2004).

Finally, the corporate governance mechanism applies agency theory to resolve the problem arising from conflicting interests of principals (stakeholders) and agents (top management team, including CEO) (Eisenhardt, 1989; Jensen, 1984). Sometimes, risk-averse agents may not engage in risk-taking, which may benefit principals, thus adversely affecting profitability. Second, when agents have access to more information that principals do not have, it is more likely that agents try to act in self-interest. Agency theory has been widely applied to economics, finance, accounting, political science, marketing, organisational behaviour and banking (Demski & Feltham, 1978; Fama, 1980; Spence & Zeckhauser, 1971; Tan, 2014).

Hypotheses Development

GBAPs and Environmental Performance

Environmental performance is assessed regarding the influence of a company’s operations on the environment (Klassen & Whybark, 1999; Zhang et al., 2022) and is closely linked to corporate performance (Clarkson et al., 2011). In banking, the effect of GBAPs on environmental performance depends on several factors: reducing the use of paper, reducing the consumption of energy and fuel and reducing greenhouse gas emissions (Shaumya & Arulrajah, 2017). There is substantial empirical evidence that green banking results in significant cost reduction, increased environmental performance and increased image (Chen et al., 2022; Rehman et al., 2021; Zhang et al., 2022). Green banking initiatives encourage employees to implement green practices while conducting bank operations (Akter et al., 2018; Zheng et al., 2021), increasing environmental performance. Since environmental performance is reflected in a company’s ability to limit the consumption of harmful and hazardous substances (e.g., air pollutants), the institutional isomorphic forces prompt the banks to safeguard the environment through green banking practices (Ahmad et al., 2018; De Giovanni, 2012; Laosirihongthong et al., 2013; Tang et al., 2012). Thus, based on available empirical evidence, we offer the following hypothesis:

H1: GBAPs positively impacts environmental performance.

GBAPs and Operational Performance

Several studies in the past have documented a positive association of GBAPs with operational performance in manufacturing (Chung & Wee, 2008; Ou et al., 2010; Zhu et al., 2013) and service industries (Harrison & New, 2002; Zhang & Yang, 2016). Operational performance is concerned with the effectiveness of operational processes, which includes reduced delivery of products and services and increased product or service quality (Shin et al., 2000). Efficient supply chain management in manufacturing industries and efficient service delivery in service industries are the parameters of operational performance (Zhu et al., 2013). Operational performance in banking includes the initiatives by banks that prevent organisations from negatively influencing the environment (Rehman et al., 2021). Though banks may not directly impact environmental degradation, indirectly, they may influence it by relaxing the financial conditions and allowing companies to pollute the environment. Recent evidence suggests that green banking practices positively affect banks’ operational performance (Bukhari et al., 2022; Salandri et al., 2022). In a recent study conducted on 360 employees in banks in Pakistan, the researchers found a positive influence of green banking on operational performance (Aslam & Jawaid, 2022). Thus, based on the above arguments, we offer the following hypothesis:

H2: GBAPs positively impacts operational performance.

GBAPs and Financial Performance

A company’s financial performance is judged by financial indicators such as return on investment, assets and market share (Selvam et al., 2016). Organisations are increasingly concerned with profitability, which reflects financial performance and customer satisfaction. Studies exploring the effect of GBAPs on financial performance are scarce (Aslam & Jawaid, 2022), as there is no direct relationship between green practices and financial performance. However, some scholars argue that firms implementing green practices focusing on protecting the environment tend to earn greater profits and financial performance (Akomea-Frimpong et al., 2022; Bag et al., 2020; Ibe-Enwo et al., 2019; Lee et al., 2012). The logos behind the positive association of green practices with financial performance is that customers tend to skew their interest in purchasing products and services of those organisations that care for the environment.

Similarly, concerning banks, it is expected that the customer tends to favour banks that show high environmental concern. Further, when banks restrict their investments to companies that manufacture environment-friendly products, they can expand socially responsible companies’ customer base. Further, the bank’s innovative practices (such as digital banking), internal operational excellence and quick responses to customer requests increase customer satisfaction, boosting financial performance (Ou et al., 2010). Many studies conducted in manufacturing industries provided empirical evidence of a positive association of financial performance with the implementation of green technologies, supply chain management and innovative processes to reduce the consumption of materials energy (Fatoki, 2019; Ou et al., 2010). Paradoxically, some scholars contend that there is a negative relationship between green practices and financial performance (Shrivastava & Tamvada, 2017; Zhang & Yang, 2016), whereas some researchers argue that green practices and financial performance are unrelated (Soto-Acosta et al., 2016). Despite mixed results about the impact of green practices on financial performance, we tilt to the positive side and offer the following hypothesis:

H3: GBAPs positively impacts financial performance.

Top Management Commitment as a Moderator

In every organisation, top management motivates employees to reach organisational goals, meet customer expectations and result in superior performance (Hambrick & Mason, 1984; Wilson & Collier, 2000). Top management teams engage in strategic decision-making with organisation-wide consequences (Parayitam & Dooley, 2007). Scholars of top management team research contend that cognitive conflicts among team members enhance team performance, whereas affective conflicts are dysfunctional (Bantel & Jackson, 1989; Parayitam & Dooley, 2009). With regard to banking organisations, the commitment of the top management team towards green banking plays a vital role in motivating employees (Bukhari et al., 2022). There is substantial empirical evidence in support of positive outcomes of top management commitment (Maidique & Zirger, 1984). Top management’s commitment and initiatives play an important role in shaping the psychological states of employees (Ives & Jarvenpaa, 1991) and prompt them to behave in a way that reflects the top management team’s ideology and intentions.

Top management commitment is a precursor to organisational internal environmental orientation (Banerjee et al., 2003). Institutional isomorphic pressure encourages top management to exhibit environmental responsibility by instilling a sense of legitimacy in these efforts. Institutional pressure develops a widespread belief that environmentally responsible corporate behaviour is ‘desirable, proper, or appropriate’ (Suchman, 1995). Top management commitment has been advocated to regulate the relationship between external stakeholder pressures and green banking adoption. Top management commitment results in a heightened sense of duty and more proactive action from the highest levels of management (Jazairy & Haartman, 2020). This suggests that when top management focuses on green practices, managers and employees at all levels of the organisation are more likely to participate in green activities (Ahmad et al., 2018).

Top management is entrusted with the responsibility of adopting new technologies, systems and practices for the benefit of both organisations and society (Hambrick & Mason, 1984; Yigitbasioglu, 2015; Jazairy & Haartman, 2020). In this process, top management’s commitment to green banking plays a vital role in implementing the practices throughout the banks (Bukhari et al., 2021). Earlier scholars provided empirical evidence in support of the effect of top management commitment on the implementation of green practices (Ahmed, 2012; Chan & Wong, 2006).

While the direct effects of top management commitment to green banking practices are well documented, we argue in this research how the top management commitment moderates the relationship between GBAPs and performance outcomes (Choudhury et al., 2013). As GBAPs positively affect environmental performance, higher levels of commitment from top management ensure the implementation of green practices throughout all the branches of the banks. In a recent study conducted among 212 branch managers from Pakistan, Bukhari et al. (2022) found that top management’s commitment moderated between various institutional pressures and customer pressures in influencing green banking practices. However, previous studies have yet to attempt to investigate the moderating role of top management commitment on the relationship between green banking practices and performance outcomes. Several studies in the past have documented the positive effect of green practices on environmental performance (Zailani et al., 2012), operational performance (Vijayvargy et al., 2017) and financial performance (Aslam & Jawaid, 2022). Top management commitment results in the implementation of green banking practices by employees, resulting in higher levels of operational performance and financial performance.

Further, when customers realise that top management is committed to protecting the environment, it is more likely that they will show loyalty to the banks, thus increasing the profitability of banks. Satisfied customers tend to divert their savings to banks that exhibit a high level of environmental responsibility, which is reflected in their financial performance. At the same time, the companies approaching the banks for finance are likely to follow green practices in their organisations, thus assuring environmental protection. Since none of the previous studies have explored the moderating effect of top management commitment, we offer the following exploratory hypotheses:

H1a–H3a:Top management commitment moderates the relationship between (a) GBAPs and environmental performance (H1a), (b) GBAPs and operational performance (H2a) and (c) GBAPs and financial performance (H3a).

The conceptual model is presented in Figure 1.

Conceptual Model.

Method

Sample

Since this research aims to explore green banking practices, we selected respondents from the banking industry. We prepared a well-structured survey instrument and distributed it among 435 employees working in banks in southern India. The survey instrument was personally distributed to bank managers, who were requested to approach the customers interested in completing the surveys. We wanted voluntary participation so that only interested individuals could complete surveys dispassionately. To avoid social desirability bias, we anonymised the responses and assured the respondents that their privacy would be protected and that information would not be revealed.

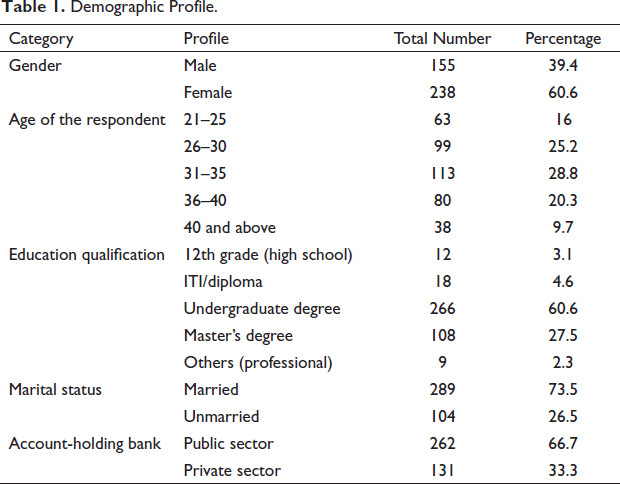

We collected 393 complete surveys (90.3 per cent response rate), more than the required minimum sample size (Krejcie & Morgan, 1970). The demographic profile of the respondents is presented in Table 1.

Demographic Profile.

Measures

All constructs were measured on a Likert-type 5-point scale (anchored as ‘1’ = strongly disagree and ‘5’= strongly agree).

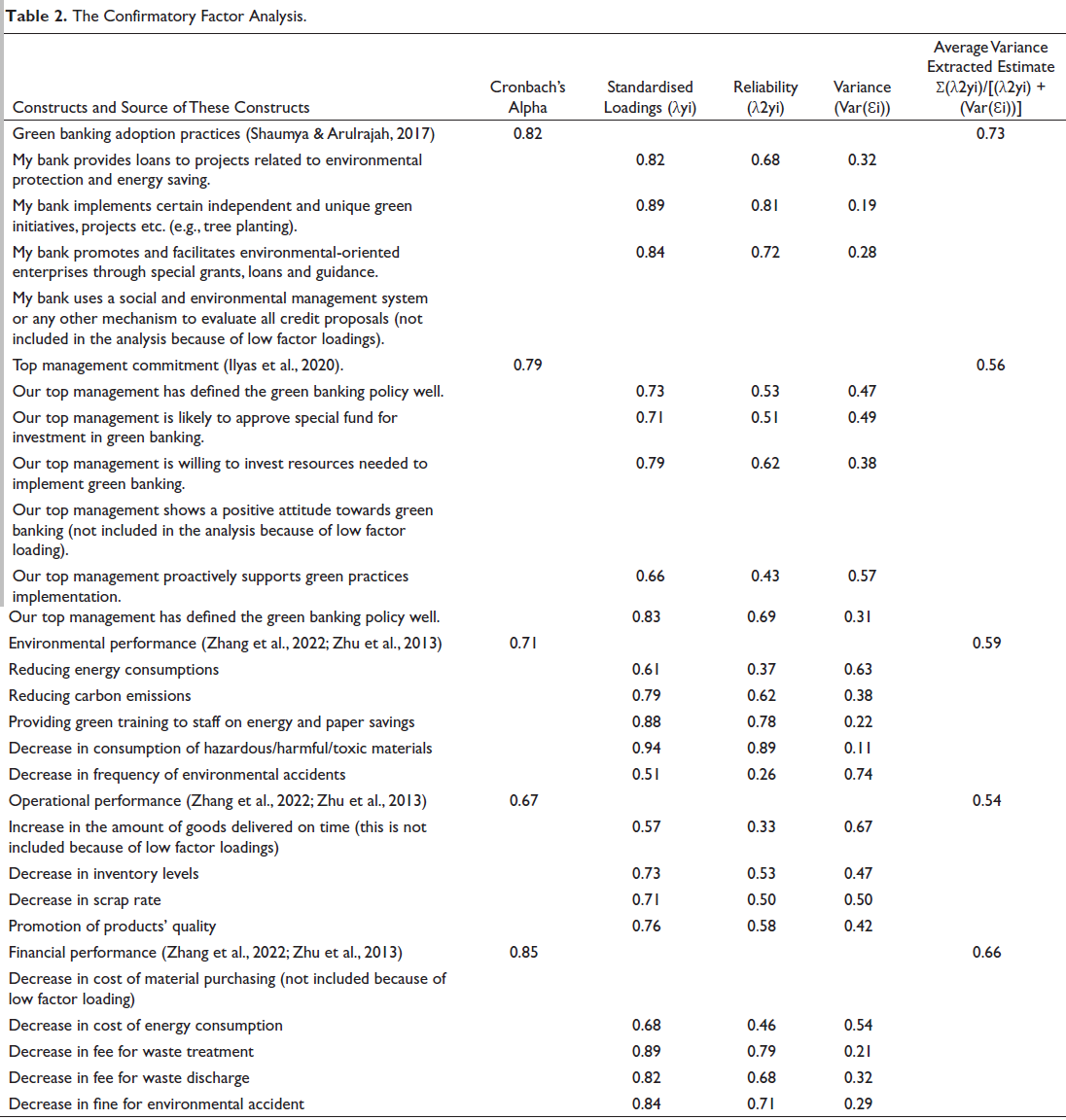

GBAPs were measured with four items (α = 0.82) adapted from Shaumya and Arulrajah (2017). One item was dropped from the analysis because of low factor loadings. Top management commitment was measured with five items (α = 0.71) adapted from Ilyas et al. (2020). Environmental performance (five items; α = 0.71), operational performance (three items: α = 0.67) and financial performance (four items; α = 0.85) were adapted from Zhang et al. (2022) and Zhu et al. (2013). All the indicators of the constructs are captured in Table 2. Comparison of various models is presented in Table 3.

The Confirmatory Factor Analysis.

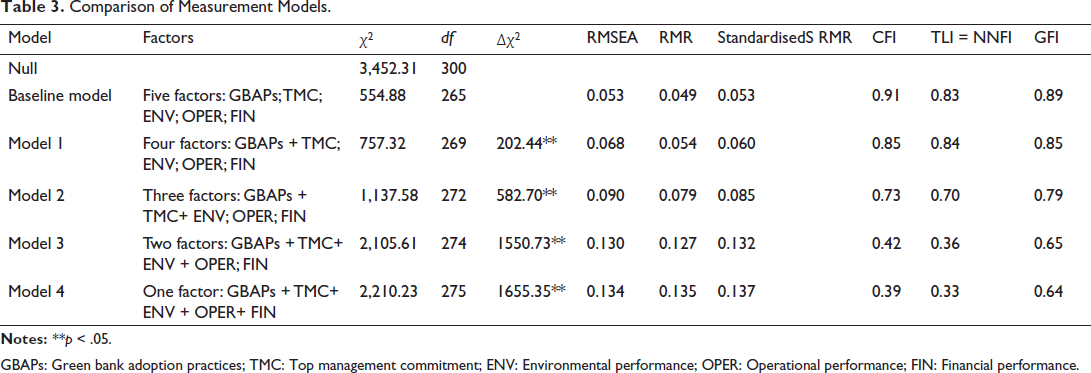

Comparison of Measurement Models.

GBAPs: Green bank adoption practices; TMC: Top management commitment; ENV: Environmental performance; OPER: Operational performance; FIN: Financial performance.

Measurement Model and Confirmatory Factor Analysis

Following the suggestions from Anderson and Gerbing (1986), we first tested the measurement model before testing the structural model. The results of the confirmatory factor analysis (CFA) are mentioned in Table 2.

The goodness-of-fit results reveal that the five-factor model provided a good fit of the data (χ2 = 554.88; df = 265; χ2/df = 2.09; RMSEA = 0.053; RMR = 0.049; standardised RMR = 0.053; CFI = 0.91; NNFI = 0.83; GFI = 0.89). The RMSEA (<0.08) and CFI (>0.90) vouch for the good fit of the data to the five-factor model. The results also show that the factor loadings, composite reliability and Cronbach’s alphas are over the acceptable limits of 0.70 (Bagozzi & Yi, 1988; Byrne, 2016; Hair et al., 2019). These results provide support for the convergent validity of the constructs used in this research.

Analysis

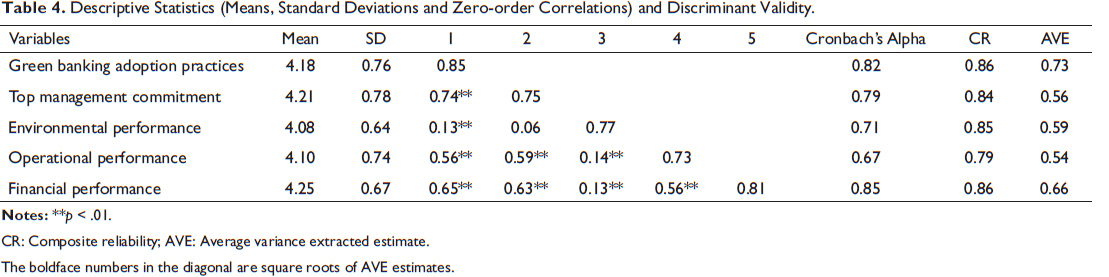

Descriptive Statistics, Zero-order Correlations, Multicollinearity and Discriminant Validity

Table 4 lists the descriptive statistics, Cronbach’s alpha, composite reliability (CR), average variance extracted (AVE) estimations, means, standard deviations and zero-order correlations. The table demonstrates that all the variables’ reliability coefficient (Cronbach’s alpha) exceeded the dependability and is established at the threshold level of 0.7 (Hair et al., 2019). Since the correlations did not exceed 0.75, multicollinearity is not a problem with the data. Further, the variance inflation factor (VIF) values for all the constructs were less than 5, suggesting that the data does not have a multicollinearity problem.

Descriptive Statistics (Means, Standard Deviations and Zero-order Correlations) and Discriminant Validity.

CR: Composite reliability; AVE: Average variance extracted estimate.

The boldface numbers in the diagonal are square roots of AVE estimates.

The AVE estimates for all the constructs were well above the acceptable level of 0.50. The correlations (Table 4) between the variables were less than the square root of AVEs between the variables, thus providing discriminant validity of the constructs (Fornell & Larcker, 1981).

Common Method Bias

As common method bias (CMB) is associated with every survey-based research, it is very important to address CMB. We conducted three tests to verify the presence of CMB. First, the traditional Harman’s single-factor test showed that a single factor did not account for more than 30 per cent of variance (Podsakoff et al., 2003). Second, we compared the five-factor model with the one-factor model and found that the one-factor model was not a good fit of the data to the model (see Table 4 for a comparison of various models). Third, we conducted a latent variable approach by subjecting all the indicators to one construct at a time and noted that the VIF values were less than 3.3, suggesting that CMB is not a problem in this research (Kock, 2015).

Hypothesis Testing

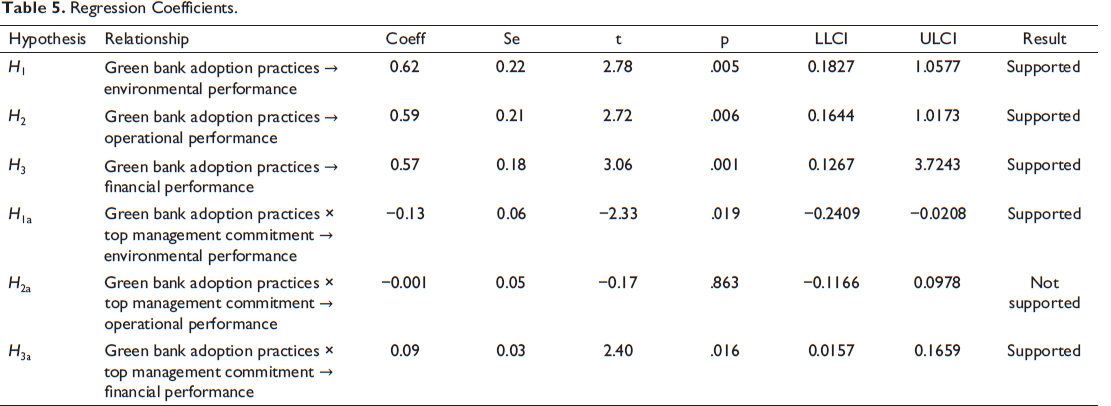

We tested hypotheses by performing hierarchical regression. We also double-checked the results by performing path analysis using Smart PLS (partial least squares). When moderators are involved in the model, hierarchical regression is preferable over structural equation modelling (Pedhazur & Schmelkin, 1991). We present the regression results in Table 5.

Regression Coefficients.

R2 and Adjusted R2, Q2 and Effect Size.

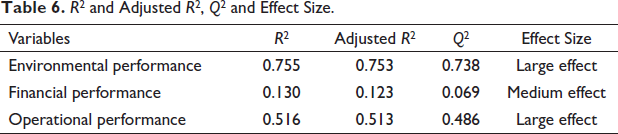

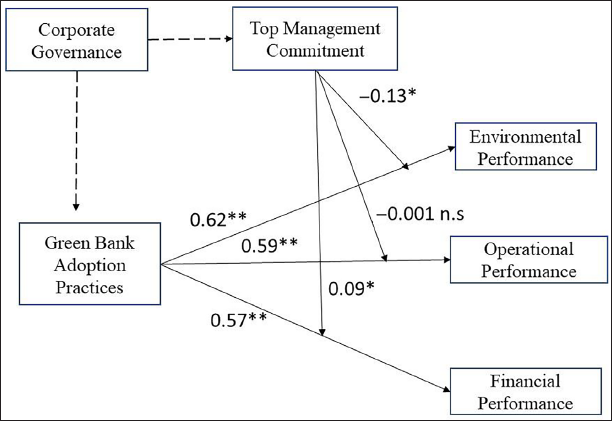

The regression coefficients of green adoption practices on (a) environmental performance were positive and significant (β = 0.62, p < .01), (b) operational performance were positive and significant (β = 0.59, p < .01) and (c) financial performance were positive and significant (β = 0.57, p < .001), thus supporting H1, H2 and H3. R-square, adjusted R-square, Q-square, and effect sizes were mentioned in Table 6.

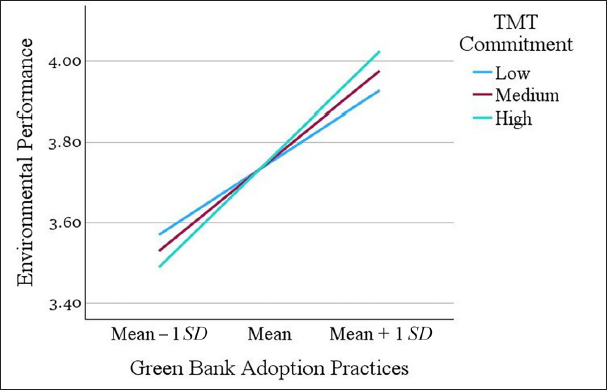

The regression coefficients of the interaction term of green adoption practices and top management commitment on environmental performance were significant (βgreen bank adoption practices × top management commitment = −0.13, p < .05), thus supporting H1b. The negative regression coefficient does not mean a negative interaction. To correctly understand and interpret the moderating effect, it is essential to see the visual presentation of moderation effect (Aiken & West, 1991).

The moderating effect of top management commitment in the relationship between GBAPs and environmental performance is presented in Figure 2.

Top Management Commitment Moderates Between Green Bank Adoption Practices and Environmental Performance.

As can be seen in Figure 2, at lower levels of green banking adoption practices, top management commitment does not play a significant role, whereas as the green banking adoption practices increase from ‘low’ to ‘high’, a higher level of top management commitment results in increasing environmental performance. The intersecting curves render support of top management commitment as a moderator between GBAPs and environmental performance (H1a).

The regression coefficient of the interaction term of GBAPs and management commitment on operational performance was not significant (βgreen bank adoption practices × top management commitment = −0.001, p = .86), thus not supporting H2b.

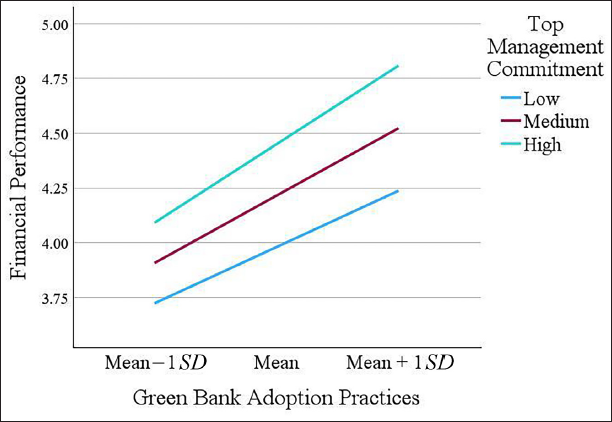

The regression coefficient of the interaction term of GBAPs and management commitment on financial performance was significant (βgreen bank adoption practices × top management commitment = 0.09, p < .05), thus supporting H3b. The visual presentation of moderating effect is shown in Figure 3.

Top Management Commitment Moderates Between Green Bank Adoption Practices and Financial Performance.

As can be observed from Figure 3, the effect of GBAPs on financial performance is higher when top management commitment is higher when compared to lower levels of commitment. Further, with the increase in GBAPs, the rate at which financial performance is increasing when top management commitment is higher as opposed to lower levels of commitment. These curves render support to the moderation hypothesis H3a.

The empirical model is presented in Figure 4.

Discussion

This study aims to investigate the consequences of green banking adoption. A conceptual model was developed and tested based on the theoretical underpinnings of institutional isomorphism and resource-based views. Data collected from 393 bank employees from South India were analysed using hierarchical regression, and all the hypotheses supported and validated the model.

First, the findings indicate that GBAPs are significantly and positively related to environmental performance (H1), consistent with the results reported in the literature (Akter et al., 2018; Chen et al., 2022; Rehman et al., 2021; Zhang et al., 2022; Zheng et al., 2021). As discussed before, green banking indirectly affects the environment, which can be seen when banks scrutinise the offering of credit to companies that conduct businesses in an environment-friendly manner. If the banks find that company activities increase emissions and pollute the environment, then they shy away from sanctioning the funds. At the same time, when employees follow the green practices in the banks, it is more likely that environmental performance is enhanced. Following the institutional isomorphism theory, normative, mimetic and coercive forces prompt the banks to follow green banking, resulting in increased environmental performance. Several studies in the past reported that these isomorphic pressures significantly impact green adoption practices (Laari et al., 2016; Thun & Müller, 2010; Walker et al., 2008), which in turn results in increased environmental performance. Second, this study documented a positive association of GBAPs with the operational performance of banks (H2), which aligns with the findings from earlier studies (Bukhari et al., 2022; Harrison & New, 2002; Salandri et al., 2022; Zhang & Yang, 2016). Unsurprisingly, green practices increase operational performance because of the efficiency of supply chain management and meeting customers’ needs on time without delay.

Further, innovation in practices such as digitalisation also helps improve the banks’ operational performance. Third, the results provide empirical support for the positive effect of GBAPs on financial performance (H3), corroborating the results from previous studies (Akomea-Frimpong et al., 2022; Bag et al., 2020; Ibe-Enwo et al., 2019; Lee et al., 2012). As expected, the traditional performance indicator of any organisation is financial performance, which is seen in terms of rate of return on investment, assets and profitability. Green banking enables the banks to attract environment-friendly companies, resulting in increased financial performance.

The fourth key finding is the moderating effect of top management commitment in strengthening the relationship between GBAPs and environmental performance (H1a). Fifth, the moderation of top management commitment in strengthening the impact of GBAPs on operational performance (H2a) found support in this research. Sixth, the results also support the interaction of top management commitment with GBAPs in positively influencing financial performance (H3a). Though none of the previous studies have investigated the moderating effect of top management commitment in the relationship between GBAPs and performance (environmental, operational and financial), the direct relationships may support our findings (Aslam & Jawaid, 2022; Bukhari et al., 2022; Vijayvargy et al., 2017; Zailani et al., 2012). Overall, the results supported all the hypothesised relationships and validated the conceptual model in this study.

Theoretical Contributions

This study makes several contributions to the theory and practice of sustainability and corporate governance mechanisms. First, this study highlights the importance of green banking practices in enhancing three performance dimensions: environmental, operational and financial performance. Banks do not directly influence the environment, but banking practices do influence it through stringent and careful procedures before sanctioning finances to the companies. By restricting financing to companies that cause environmental harm and encouraging companies that are environment friendly in their operations, green banking facilitates environmental protection. Further, institutional forces of isomorphism (coercive, normative and mimetic) suggest that operational and financial performance can be increased by following green practices. Second, this study underscores the significance of top management commitment to strengthening the effect of green practices on environmental, financial and operational performance in the banking sector. The findings from this study, thus, have broader implications for the sustainability strategies of companies in the service sector, including banks. Strong top management commitment is needed so green adoption practices are more likely to be effectively integrated into the organisation’s operations. This study recommends that committed leadership from top management needs to overcome potential resistance from employees in adopting green practices. Adopting green practices is essential, and top management plays a vital role. Third, following the institutional theory of isomorphism, this research suggests that managers must upgrade banking technologies geared towards green practices. For example, encouraging customers to prefer digital banking may reduce the negative effect of banking operations on the environment. Recommending the customers to have electronic bank statements instead of paper-based statements will result in less paper usage. Local governments and various branches of banks (whether in rural or urban areas) need to promote green habits by encouraging investments in companies that manufacture ecologically friendly products or provide environmentally friendly services. As some scholars have documented, community pressures play a vital role in green banking adoption influence (Javeed et al., 2020); the findings from this study are compatible with those of other studies in the literature (Bag et al., 2020; Zhang et al., 2022; Zhu et al., 2013). To sum up, following the recommendations of governance mechanisms, the findings from the conceptual model we developed and tested contribute to advancing sustainable banking, especially in the context of banks in developing countries such as India.

Practical Implications

This study has several implications for policymakers, administrators, society and corporate governance interested in protecting the environment and maintaining sustainability. First, the administrators in banks need to follow the guidelines of the board of directors (governance mechanism) and ensure that banks need to divert their investments to companies that do not harm the environment. It is necessary to promote green projects as they have a positive impact on environmental, operational and financial performance. Following the RBV, banks can maintain a sustained competitive advantage by strategising investments to promote a green environment, and with the increase in the number of banks, growing competition prompts them to mimic the strategies of successful banks. As documented in research that green banking practices are precursors to superior performance, top management pays close attention to whether employees are effectively implementing green practices. Second, this study suggests that environmentally conscious customers prefer to show loyalty to banks that exhibit high levels of social, ethical and environmental responsibility. Third, as green banking practices increase various performance dimensions, administrators in other industries can benefit from going green. Green practices, especially in manufacturing units, result in decreased carbon emissions and environmental degradation. Fourth, following the institutional theory of isomorphism, organisations must be constructive in obliging industries that use technology that protects the environment from degradation. Coercive forces require companies to go green, whereas normative forces suggest that companies implement green practices. To sum up, policymakers need to ensure that green banking practices contribute to improving the overall climate, which affects the quality of life of people in society.

Since top management commitment plays a significant role in enhancing performance, organisations in the banking industry should prioritise and foster top management commitment to promote GBAPs. Policymakers can realise that sustainable investment leads to environmental performance in addition to financial performance, so it is suggested to integrate green practices in banks. It is also suggested to incentivise the employees to adopt green banking practices. To sum up, creating a culture of green banking, identifying the areas for improvement and bringing awareness of going green play an indispensable role in adopting green practices efficiently. Local governments and environmental protection agencies (EPA) must implement stringent measures against non-compliance to the emission of gases, higher consumption of energy than needed and excessive use of non-renewable resources. Managers need to implement energy-saving measures, recycle waste material and reduce paper usage by digitalising services. Organisations need to conduct training programmes to exhibit green behaviour and implement green practices.

Limitations and Directions for Future Research

This research has some limitations. First, though our sample is reasonably adequate, our focus on southern India may be an inherent limitation. However, to the extent that the organisational climate in the banking industry is the same throughout the country, we expect that the results will be generalisable across different parts of the country. Second, we focused only on a limited number of variables. Most importantly, we used perceptual measures to assess the performance. Third, the study focused only on the banking industry, which does not directly impact the environment. Green practices are followed in several industries, and concentrating only on the banking industry was narrow in focus.

Despite the limitations, this study offers several avenues for future research. First, future studies may involve more extensive samples to test the hypothesised relationships conceptualised in the model. Second, in addition to subjective measures, it will be interesting to consider objective performance measures (e.g., rate of return on investment). Third, future studies may include customer satisfaction with green banking practices. Fourth, an industry-wise comparison of green practices may help understand differences in implementing them and their consequences. Fifth, comparing green banking practices in Indian banks and foreign banks operating in India may offer additional insights into research on sustainability. Sixth, comparing green practices in various developing versus developed countries will be interesting to study if cultural differences exist. Future studies may also investigate the effect of corporate governance on top management commitment in promoting green environment in banking.

Conclusion

The conceptual model developed and tested in this research underscores the importance of green banking practices, as recommended by corporate governance, in enhancing three performance dimensions: environmental, operational and financial. Further, top management’s commitment to strengthening relationships provides novel insights for practicing managers and policymakers. Further, the results can be generalised across different industries with regard to ‘going green’. This study aligns with the goals of sustainable development as recommended by the United Nations for preventing environmental degradation and climate change through green practices. Considering the increasing importance of sustainability, implementing environment-friendly practices is essential in all industries. Since banks are inextricably interwoven with the fabric of all other industries through financing, adopting green practices plays a vital role in maintaining a healthy ecological system.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.