Abstract

In this study, we investigate Indian anti-dumping (AD) duties imposed on eight products (Harmonized System classification) from Bangladesh over the period 1998–2020. Using the Poisson pseudo-maximum likelihood method, panel regression analysis is applied to examine the relationship between Indian AD duties and goods imported from Bangladesh. Our results provide weakly suggestive significant evidence of trade destruction in the full sample, though statistical significance is enhanced for all product groups other than lead-acid batteries at the product-level investigation. We also provide suggestive evidence for trade diversion from AD duties. Overall, our results show Indian AD duties to be correlated with a decrease in imports from Bangladesh, and an increase in imports of goods from other, unnamed countries. This suggests that India’s protectionist measures may have been ineffective in protecting local producers, as any adverse effects of protectionism on Bangladesh may be offset by import diversion to other foreign suppliers. We also discuss the policy implications of these findings.

Introduction

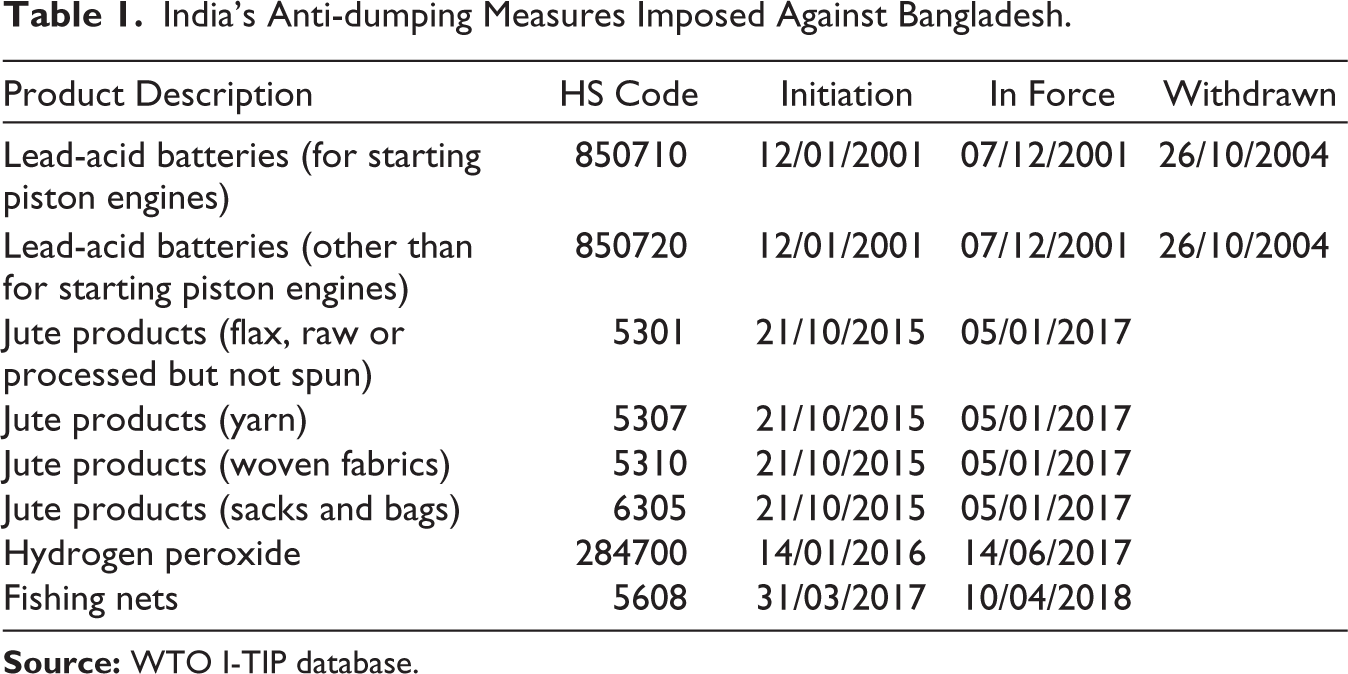

India is the second largest source of Bangladesh’s imports (after China). In 2020, India’s exports to Bangladesh were valued at USD7,913 million, and imports during the same year stood at USD 1,024 million. Historically, the trade balance has always been in favour of India. The huge and persistent trade deficit continues to undermine trade relations between the two countries and has been further complicated by the strain imposed by Indian anti-dumping (AD) measures against Bangladeshi exporters. India initiated its first official AD investigation, of lead-acid battery exports from Bangladesh, on 12 January 2001 and imposed duties equivalent to 131% on 7 December 2001 (Taslim, 2006).

Prior to the Indian case, Bangladesh had contended with two other AD measures: one by the United States in February 1992 against the export of cotton shop towels, and the other by Brazil in October of the same year against exports of jute sacks and bags (Azim, 2021; Bhattacharya & Rahman, 2000; WTO I-TIP database, 2022). Bangladesh, being a least-developed country (LDC), lacked the capacity, expertise and resources to contest the decisions of the United States and Brazil by bringing them to the attention of the Dispute Settlement Body (DSB) of the World Trade Organization (WTO). Moreover, Bangladeshi exporters were hesitant to initiate litigation due to the high legal costs involved and long timeframe of legal battles involving the DSB. By the time India levied AD duties on lead-acid batteries, Bangladesh was already pursuing bilateral negotiations to resolve the trade dispute amicably; however, they did not obtain a fair outcome. Bangladesh then presented India with a formal request for consultations and ultimately brought the dispute to the DSB on 28 January 2004, claiming that Indian AD measures were illegal and in violation of Articles 5.8 and 6.8 of the WTO’s Agreement on Implementation of Article VI of the General Agreement on Tariffs and Trade (GATT; dispute number: DS306). This was the first case of an LDC member enacting their right to dispute perceived trade infractions under the WTO’s dispute settlement mechanism. The dispute was resolved in the consultation stage, with India having to terminate the AD duties on 4 January 2005 with Customs Notification No. 01/2005. Notably, this dispute set a historical precedent for other LDCs in the WTO with respect to the handling of such issues.

Following the settlement of the lead-acid battery case, India abstained from imposing additional AD measures against Bangladesh for about a decade. However, on 21 October 2015, India initiated an AD investigation against jute products exported from Bangladesh. After an investigation period of more than 1 year, India imposed AD duties on four jute goods produced and exported from Bangladesh, ranging from US$19 to $352 per tonne. Apart from lead-acid batteries and jute goods, India imposed AD duties on hydrogen peroxide and fishing nets exported from Bangladesh in June 2017 and April 2018, respectively. The AD duties on hydrogen peroxide ranged from $27.81 to $91.47 per tonne; for fishing nets, the AD duty was $2.69 per kilogram.

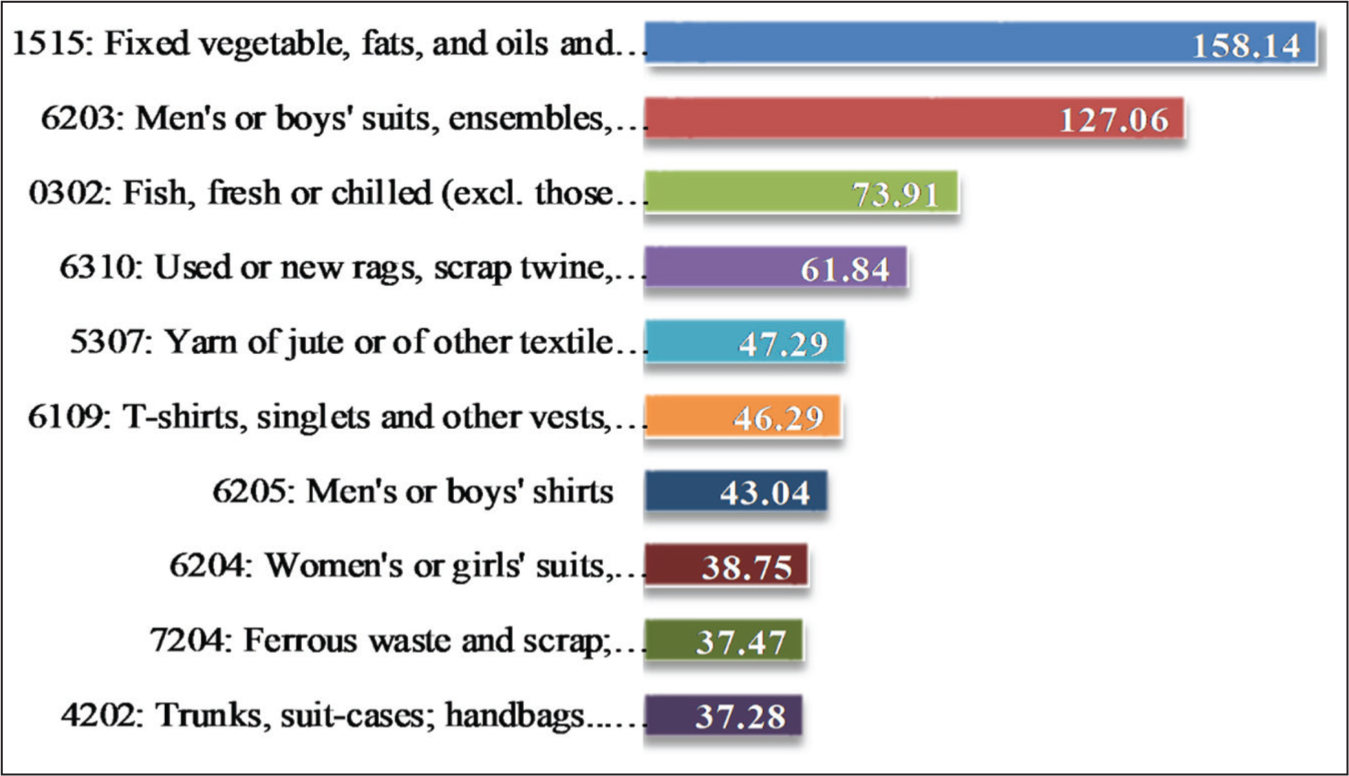

Since 2001, India has enforced AD measures on a total of eight commodities (Harmonized System [HS] classification) from Bangladesh (Table 1). Lead-acid batteries, jute products, hydrogen peroxide and fishing nets are among the Bangladeshi products currently subject to AD duties imposed by India. These are minor rather than major export items for Bangladesh. A thorough analysis of Bangladesh’s export data in the World Integrated Trade Solution dataset reveals that Bangladesh’s exports are dominated by the textile and garment sector, which makes up more than 90% of the total exports from the country (Bhuyan & Oh, 2021). Moreover, the product-wise distribution of Indian imports from Bangladesh for 2020–2021 (July–June), as shown in Figure 1, indicates that other than HS 5307, Bangladeshi products subject to Indian AD are not major export items. Bangladesh sees the implementation of AD measures by India as an attempt to stifle market potential and limit market access for Bangladesh’s minor but promising export commodities. These AD measures have garnered a lot of negative press in Bangladesh; they are widely perceived as glaring evidence of India’s unwavering hostility towards Bangladeshi exporters (Taslim, 2006).

India’s Anti-dumping Measures Imposed Against Bangladesh.

Given the importance of trade relations between Bangladesh and India, and the adverse publicity of Indian AD measures in the Bangladeshi media, the main objective of this study is to investigate the relationship between Indian AD measures and goods imported from Bangladesh. While AD measures have been widely studied in the literature, not much attention has been paid to their relationships with minor export items. Their effect on LDCs is also an important issue that has yet to be addressed empirically. Hence, additional research on LDCs and minor export commodities is required to better understand the issue of trade destruction and trade diversion from AD measures. This study attempts to bridge this gap by focusing on Indian AD measures and their relations with minor export items from an LDC like Bangladesh.

We hypothesize that Indian AD measures suppress imports from Bangladesh for three reasons. First, Bangladeshi products subject to Indian AD measures are very minor export items with small markets and limited industrial bases. Under the protectionist push of stronger economies, these minor but promising export sectors in LDCs cannot further expand. Second, protectionist measures are often imposed by larger trading partners to limit market access to exports from LDCs and developing countries. Such measures, in most cases, violate fair trade rules. Third, LDCs, which have been victims of AD measures, are reluctant to file complaints with the WTO due to the relatively high cost of contesting trade issues via the DSB. Ultimately, LDCs, with their small market size and limited trading capacity, are placed on the back foot.

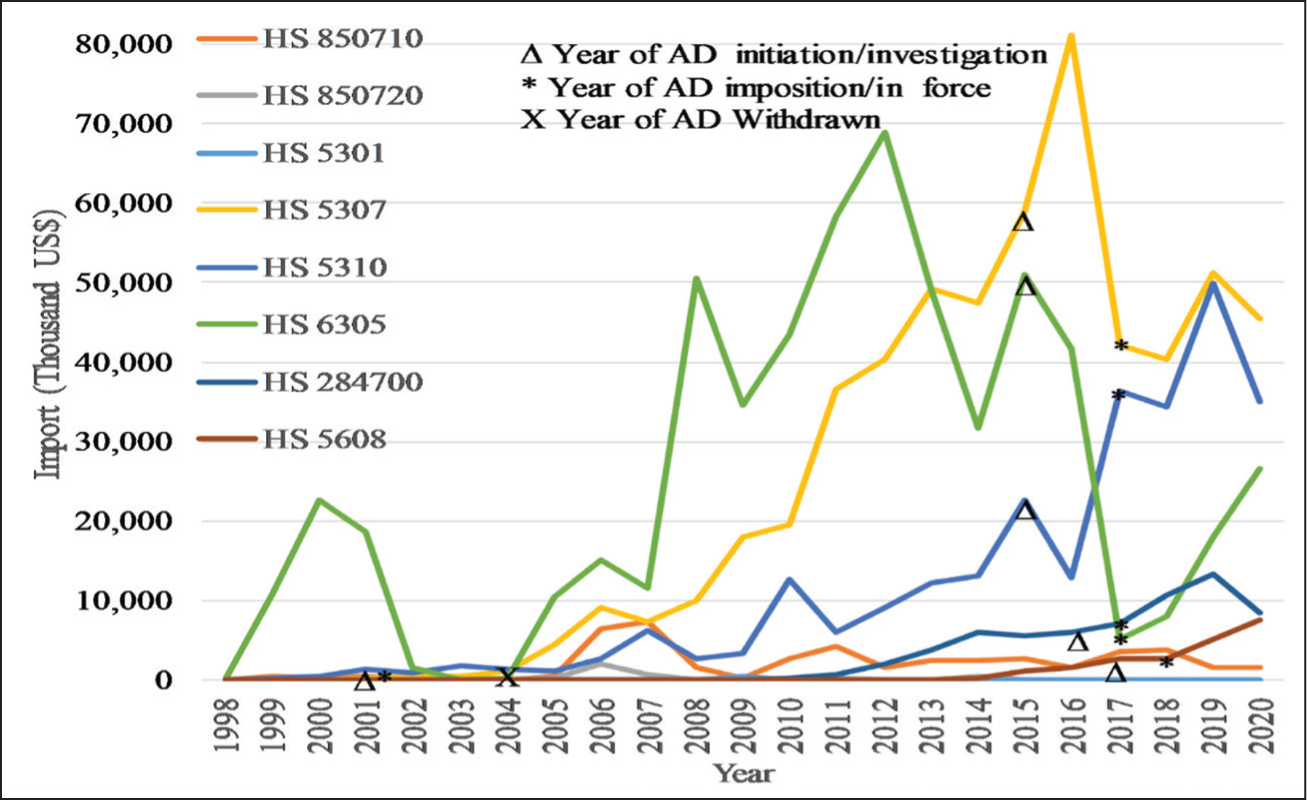

Figure 2 shows the trends in imports subject to India’s AD measures against Bangladesh. When Indian AD duties are in effect, there is a tendency towards a decline in imports from Bangladesh for lead-acid batteries. Imports rose after India eliminated AD duties at the end of 2004. We also observe mixed patterns in India’s imports of jute products from Bangladesh. Apart from HS 5310, all three categories of jute products have experienced a downward trend in imports since India imposed AD duties in 2017. Similarly, imports of hydrogen peroxide from Bangladesh tend to decline sharply when Indian AD duties are in effect. Notably, the import trend of fishing nets is insensitive to AD measures. Overall, analysis of Indian import trends according to AD measures indicates a destructive trade relationship with Bangladesh.

Literature Review

With the proliferation of AD cases, empirical studies have been undertaken to understand the causes and outcomes thereof. The existing literature distinguishes price- and cost-based dumping (Leidy & Hoekman, 1990; Maiti, 2016; Tivig & Walz, 2000). Price dumping is the practice of setting the prices of export items on the foreign market lower than those on the domestic market. In the case of cost dumping, export prices are set lower than the production cost.

Exporting firms are motivated to dump in the foreign market for a variety of reasons, including predatory, cyclical, seasonal and discriminatory ones (Kang & Ramizo, 2020; Maiti 2016; Willig 1998; Yandle & Young, 1987; Yarrow 1987). Predatory dumping is an anti-competitive practice that intends to create a monopoly by driving competitors out of the market. Cyclical dumping refers to the temporary sale of goods in the foreign market at a price lower than the average total cost. This happens when a firm has an excessive production capacity and faces a cyclical downturn in domestic demand. Seasonal dumping is done to unload excessive stock of seasonal goods, which have a limited shelf life or may go out of style soon, on the foreign market at a price below fair market value. Discriminatory dumping is persistent or permanent in nature and occurs for goods with inelastic demand on the domestic market and elastic demand on the foreign market. Of these four motives for dumping, legal measures are not warranted for the last three cases unless they violate antitrust laws. Predatory pricing is prohibited and illegal under WTO rules if it harms producers in the export market and thus violates antitrust laws (Kang & Ramizo, 2020; Maiti, 2016).

GATT Article 6 condemns dumping that causes material injury to domestic industries and gives countries the right to levy AD duties in appropriate circumstances. The main objective of AD measures is to ensure fair trade conditions and offset any injury to domestic industry in the importing country. Since AD measures are opaque, unpredictable and protectionist, they can harm the terms of trade, resulting in welfare losses for importing countries (Lee et al., 2013). AD measures not only affect the importing country but also the exporting country and third (unnamed) countries. The study of Staiger and Wolak (1994) is perhaps the earliest and most extensive of the effects of AD measures on domestic production and imports, covering US AD cases from 1980 to 1985. It considered both the direct (duty) and non-direct (investigation) effects of AD measures on imports and revealed evidence of significant negative effects. An investigation effect occurs when a targeted country’s imports are reduced by the mere act of initiating an unfair trade investigation, even if no final AD duties are imposed. Moreover, the study observed that domestic production moves in a positive direction, approximately in line with the magnitude of the lost market share of foreign countries subject to AD measures.

Krupp and Pollard (1996) studied the effects of USAD cases on the chemical sector using product-specific firm-level data over the period 1976–1988 and provided empirical evidence of trade diversion from named to unnamed countries. Prusa (1996, 2001) provided evidence of both trade destruction and trade diversion effects, where US AD measures led to a drop in import volume from the named countries, i.e., a trade destruction effect. Apart from suppressing imports from named countries, there is evidence of a rise in imports from unnamed countries, i.e., trade diversion, due to AD measures. Similarly, Chandra (2017) found evidence of both trade destruction and diversion effects on Chinese exports to major trading partners. Finally, Niels and Kate (2006) provided evidence of trade destruction, but not trade diversion.

Bown and Crowley (2007) studied the effects of trade deflection (an increase in exports of the named countries to other unnamed countries) and trade depression (a decrease in unnamed countries’ exports to named countries) of AD measures. They discovered that US AD measures against Japan deflected trade, by increasing Japanese exports of the same items to non-named third countries. They also found evidence of trade depression, i.e., a decrease in Japanese exports in the third market against which the US imposed AD measures. Carter and Gunning-Trant (2010) found neither investigation nor trade diversion effects in association with US agricultural AD measures, while Wang and Reed (2015) revealed that US AD duties instigated trade deflection of shrimp products to non-named third markets. Aggarwal (2010) showed that only the big firms benefited from protective AD measures of India. The study also revealed that developing countries suffer significant losses from Indian AD measures, while there is no evidence of trade destruction effects for developed countries. Mahajan et al. (2021) found partial evidence that Indian AD measures are highly effective forms of protection against China.

Our literature review shows that the relationship between AD duties and trade flows are not obvious; rather, they are subtle and diversified. We investigate the issue of trade destruction and diversion from AD measures initiated and imposed by India against Bangladesh using balanced panel data from 1998 to 2020. However, this study is different from the existing literature. First, most previous studies considered the relationship between AD measures and major export items, while the relationship between protective measures and minor export items was ignored. India has imposed AD measures on minor export items from Bangladesh. Hence, after reviewing the relevant literature (discussed above), this study focuses on the empirical analysis of the relationship between Indian AD measures and minor export items from Bangladesh. Second, the issue of AD measures and their relationships with imports from LDCs remain to be empirically explored. Through empirical investigation of Indian AD measures against Bangladesh (an LDC), this paper improves our understanding of AD measures and their correlations with the trade flows of LDCs. More importantly, although previous studies included similar variables, few examined Bangladeshi trade data.

Methodology

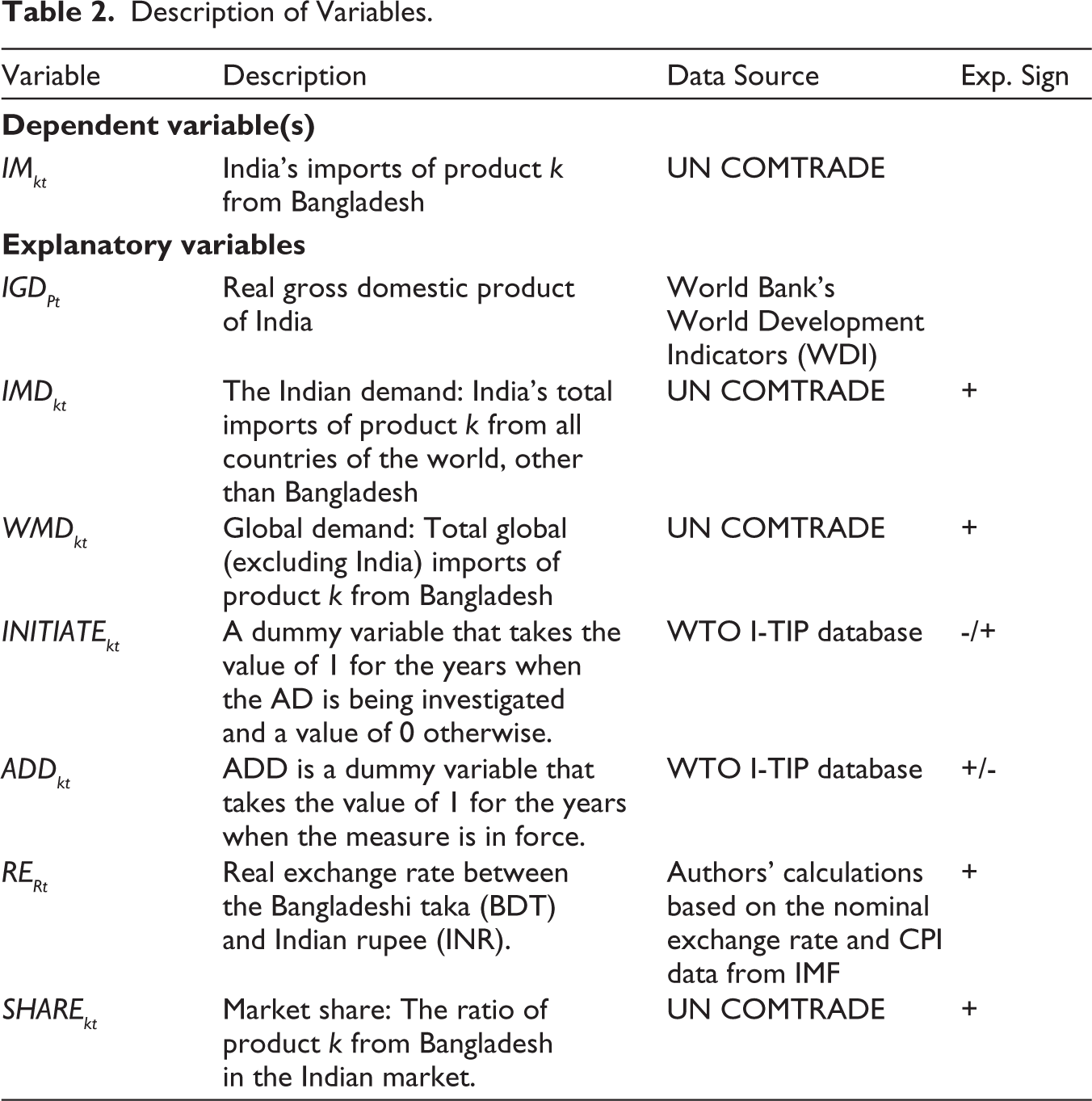

This study empirically investigates the relationship between Indian AD duties and imports from Bangladesh, through panel data regression analyses using Poisson pseudo-maximum likelihood (PPML) estimation techniques. Due to the presence of zero trade values in our sample, we use the PPML estimator. The logarithmic transformation treats values for trade variables as missing in the regressions, resulting in erroneous estimate results. In the existing literature, the issue of zero trade flows is resolved in three ways: by adding a constant value (usually 1) to the trade data before the log transformation (this approach lacks a theoretical foundation); applying the PPML method; or applying Heckman’s (1979) two-stage procedure. In the present study, we utilize the PPML method to deal with zero trade values. As documented by Silva and Tenreyro (2006), the PPML method is effective for dealing with heteroskedasticity issues and zero trade values. Based on Prusa (1996, 2001), Niels and Kate (2006), Bown and Crowley (2007), Shen and Fu (2014) and Cheng et al. (2021), our estimation model takes the following form:

where k is the product classification based on HS codes and t corresponds to the time (i.e., year; from 1998 to 2020). The dependent and explanatory variables, as well as their sources, are summarized in Table 2. The dependent variable IMkt denotes the value of Indian imports of product k from Bangladesh in year t. More specifically, this variable takes the value of imported items k that are being investigated or are already subject to the AD duties imposed by India against Bangladesh. As explanatory variables, we include five continuous variables and two dummies in our model. IGDPt is the real gross domestic product of India in time t. This variable represents the size of the Indian market; the bigger the market, the better for Bangladeshi exports. The Indian demand IMDkt is the total value of all imports of product k in year t, excluding Bangladeshi items. This variable corresponds to India’s global import demand for product k. The variable WDMkt denotes the worldwide demand for product k from Bangladesh, which is equal to the entire import value of product k from Bangladesh, excluding India, in year t.

Description of Variables.

ADDkt is a dummy variable for trade destruction and trade diversion from AD duties. It takes a value of 1 for the years when the AD measures are in force, and a value of 0 otherwise. INITIATEkt is a dummy variable with a value of 1 for the years when AD is being investigated and a value of 0 otherwise. With this variable, we can evaluate whether the AD investigations resulted in harassment. Staiger and Wolak (1989) and Prusa (2001) showed that the initiation and investigation of AD cases have significant effects on imports, regardless of whether any duties are ultimately imposed. It is likely that exporters will face considerable disruption to their trade, as well as significant time and financial costs (in association with their defence), even if the AD case terminates without the imposition of duty measures. This is often called the ‘harassment’ effect. As Prusa (2001) explains, the harassment effect results from temporary duties imposed during an investigation and uncertainty about the outcome.

RERt is the real exchange rate between the Bangladeshi taka (BDT) and the Indian rupee (INR). This variable is predicted to have a positive sign, implying real depreciation in the value of the BDT against the INR, and enhanced external competitiveness of Bangladesh’s export products on the Indian market. Currency devaluation lowers the cost of export products, resulting in a rise in export volume. Currency appreciation, on the other hand, raises the cost of export commodities and reduces export quantities. SHAREkt is the market share of Bangladesh’s product k in India, which is the ratio of imports from Bangladesh to total Indian imports for product k. During the investigation and implementation of AD measures, market share plays a significant role in decision-making. Lee et al. (2017) found that the larger the volume of Chinese imports to the United States, the less adverse the effects of AD duties; Chinese exports, therefore, continued to rise, despite the imposition of the AD duty.

Empirical Results and Findings

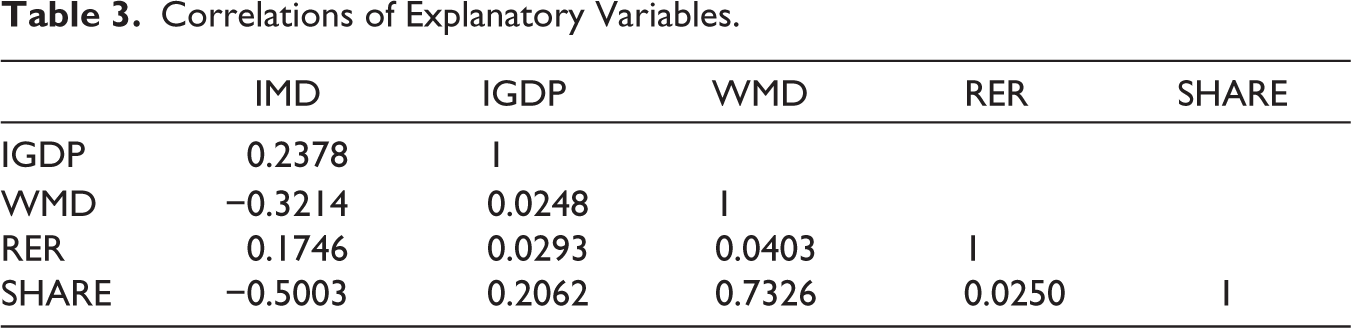

The correlation matrix of the continuous explanatory variables is shown in Table 3. Of all pairs considered, WMD and SHARE have the strongest correlation (0.732). The VIF values for WMD and SHARE are also the highest, at 2.41 and 3.46, respectively. As reported by Marquardt (1980), Hair et al. (2018) and Rogerson (2019), the maximum VIF allowed to avoid multicollinearity is 10. We can reasonably assume that multicollinearity is not serious in our estimation, given that the VIF values are much lower than 10. Nevertheless, the issue of multicollinearity should be considered.

Correlations of Explanatory Variables.

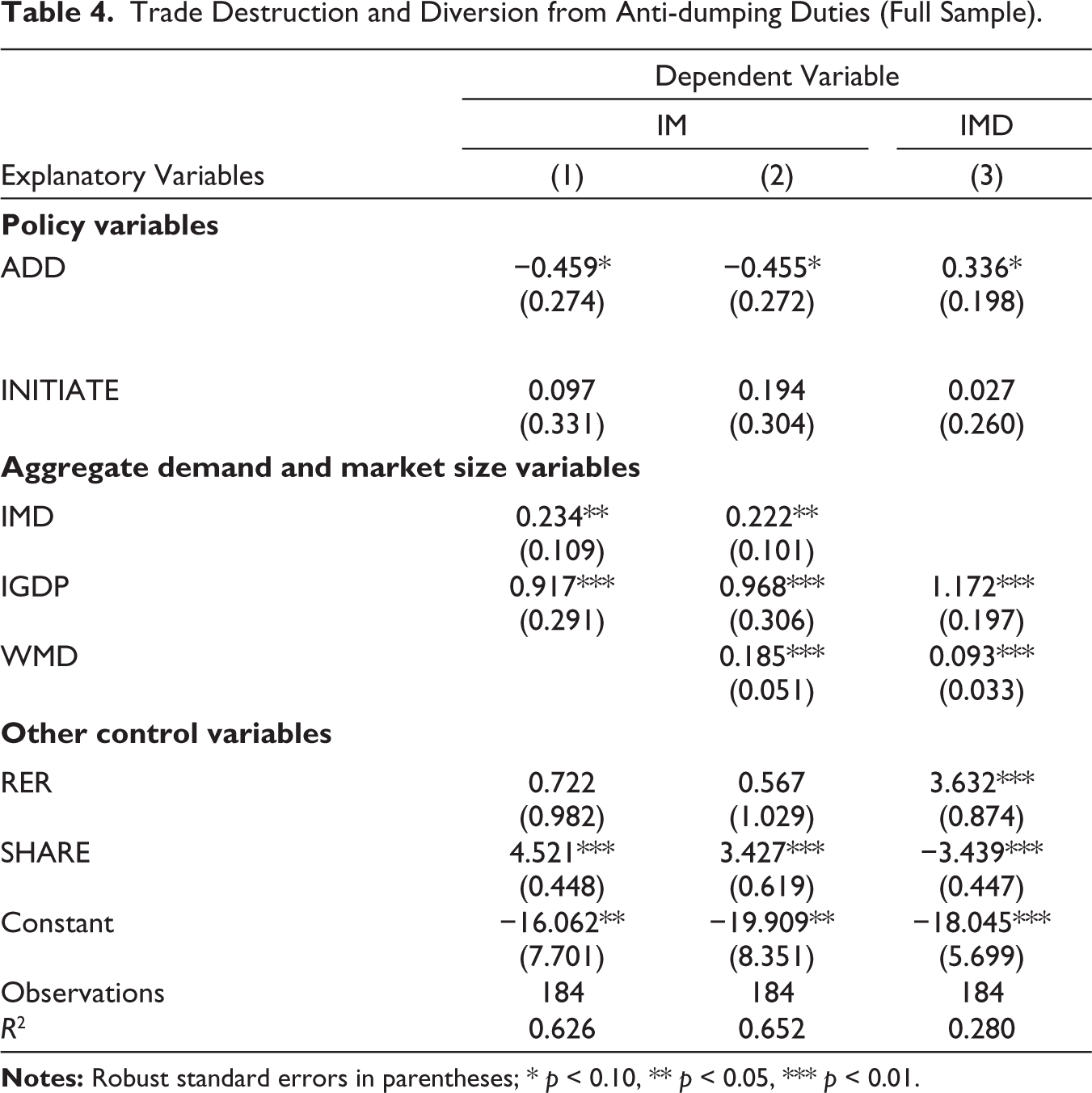

Our estimations are reported in Tables 4 and 5. The first and second columns of Table 4 present the empirical results of the trade destruction, while the third column reports trade diversion. Although our VIF results indicate no abnormalities, we first drop the WMD variable from our estimation, as shown in column 1 of Table 4. We then include the WMD variable, and present our benchmark results of the trade destruction in column 2 of Table 4. We find no inconsistencies in the results, irrespective of the inclusion or exclusion of WMD and SHARE in the same model.

Trade Destruction and Diversion from Anti-dumping Duties (Full Sample).

We hypothesize, based on the simplest theoretical model of Bown and Crowley (2007), that imposition of AD duties would reduce Indian imports from Bangladesh (trade destruction) and increase Indian imports from other unnamed countries (trade diversion). In our simple model to estimate trade destruction, IMD kt has been taken as an explanatory variable, which corresponds to India’s global import demand for product k. The same variable has been taken as a response variable in estimating trade diversion, meaning that any positive correlation between IMD kt and ADD kt would imply the rise of Indian imports of product k from other non-named countries and thus the of trade diversion from Bangladesh.

The coefficients of ADD in the trade destruction models are negative, as expected, although they were weakly significant at the 10% level. These findings suggest that Indian AD duties imposed on Bangladeshi goods restrict imports. Following their imposition, Indian imports from Bangladesh get declined. Hence, there is evidence of trade destruction due to the Indian AD measures against products exported from Bangladesh. As shown in column 3 of Table 4, when taking into consideration trade diversion, the coefficient of the ADD variable is positive and weakly significant at the 10% level. This indicates that some import diversion from Bangladesh (named country) to unnamed countries does indeed occur as a consequence of Indian AD measures. After AD duties were imposed, Indian imports from Bangladesh are diverted to unnamed countries.

None of the coefficients for INITIATE are statistically significant, which suggests no evidence of trade harassment from India’s AD investigation against Bangladesh. The coefficients of aggregate demand and market size variables (IMD, IGDP and WMD) are all positive and statistically significant, in line with our expectations. The real exchange rate (RER) variable is positive but not significant. The other control variable, SHARE, is statistically significant, with a positive sign as expected. This suggests that Bangladeshi goods with a high share of the Indian market are less likely to be negatively affected by AD duties, and more likely to increase exports.

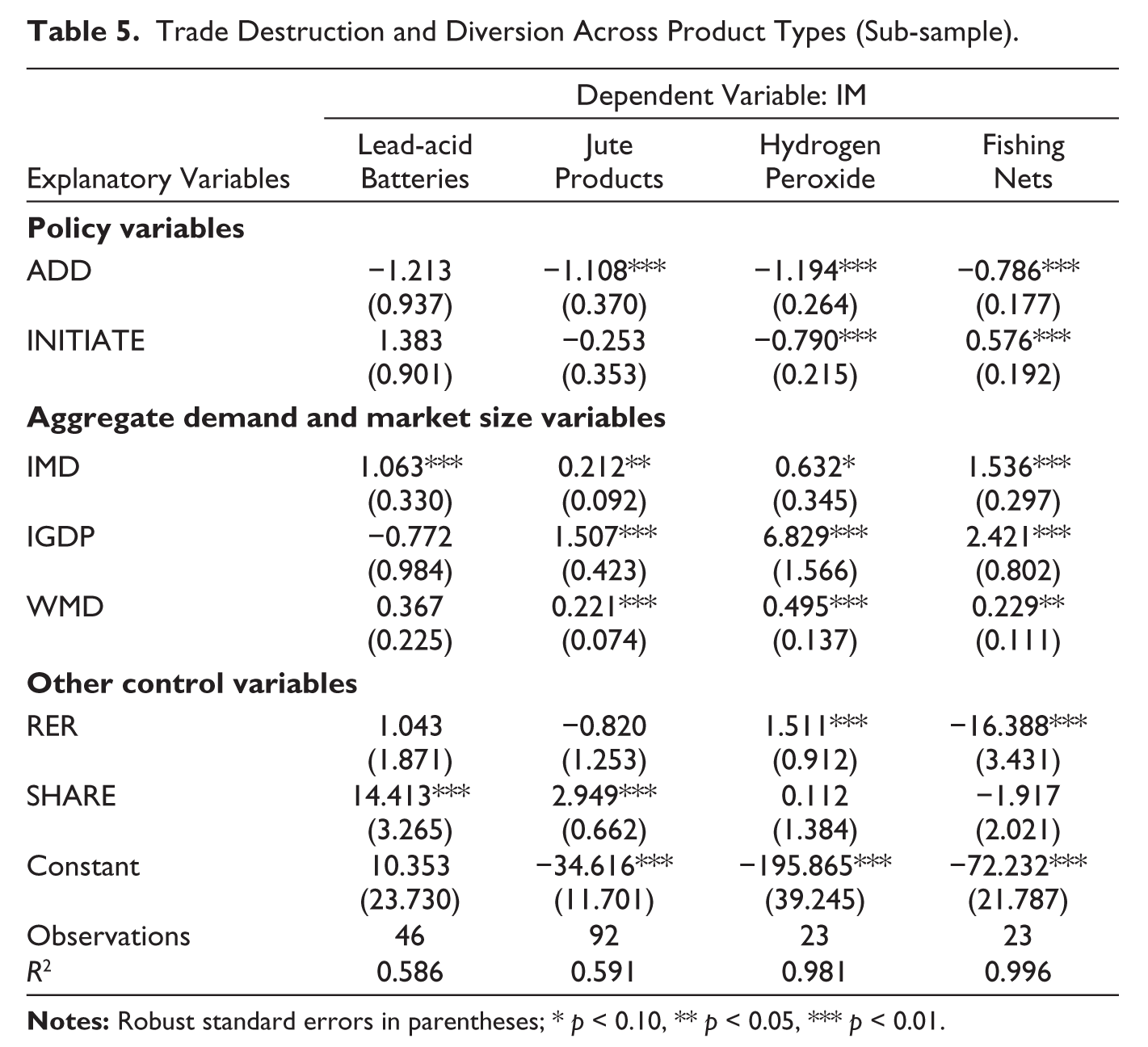

Next, to analyse the relationship between Indian AD measures and imports across product groups, we divide the total sample into four product groups: lead-acid battery, jute products, hydrogen peroxide and fishing nets. As shown in Table 5, there is apparent evidence of trade harassment on imports of hydrogen peroxide, whereas fishing net imports tended to increase after the investigation had begun, in anticipation of possible AD duties. Hydrogen peroxide is a strong oxidizing agent and is widely used in textile bleaching. Countries with textile and garment factories are the major importers of hydrogen peroxide produced in Bangladesh. As Bangladesh is a tough competitor of India in the global textile and garment market, any trade policy issue related to hydrogen peroxide may be very sensitive to influence trade decisions. As such, our results confirm the strong evidence of harassment from the Indian AD investigation, regardless of whether any duties are ultimately imposed. The fishing nets are much cheaper in Bangladesh than in India, although they are relatively new in the Bangladesh export basket and have a low export volume. Immediate growth in fishing net imports from Bangladesh by Indian importers may be due to the expectation of future price increases if AD duties are imposed.

Trade Destruction and Diversion Across Product Types (Sub-sample).

The coefficients of AD duties show a weak but significant negative relationship with imports of all product groups from Bangladesh. In contrast to the results of the full sample, the coefficients are highly significant (at the 1% level) for all product groups other than lead-acid batteries. AD duties are usually imposed at the product level, so companies that produce and export the products in question are more likely to be affected. At the product-level findings, we observe no trade destruction in the case of lead-acid batteries which points to the successful negotiation of Bangladesh with the WTO’s DSB. As mentioned before, the Bangladesh–India trade dispute over lead-acid batteries is the only case to date in which an LDC member has confronted another via the WTO’s DSB resolution mechanism, which resulted in the termination of India’s AD duties. Bangladesh took a bold stance, claiming that India’s imposition of AD duties was not legitimate and in violation of WTO rules. Bangladesh’s experience with the DSB and the findings of this study provide new insight for policymakers and export firms of LDCs and developing countries regarding how to contest trade disputes, both bilaterally and multilaterally, with confidence.

Conclusion

In this study, we investigate the relationship between Indian AD measures and imports from Bangladesh by analysing a balanced panel of annual data from 1998 to 2020. The major empirical findings of this study are briefly summarized in the following.

First, we find evidence of the trade destruction. The imposition of Indian AD duties against Bangladeshi products causes imports to decline. Second, there is significant evidence that India’s imports from Bangladesh are diverted to other unnamed countries after the imposition of AD duties. It seems that the AD duties are not effective in protecting local Indian producers. This suggests that India’s protectionist measures may have been ineffective in protecting local producers, as any adverse effects of protectionism on Bangladesh may be offset by import diversion to other foreign suppliers. Third, the study finds no evidence of trade harassment (investigation) when the sample is examined as a whole; however, we observe different results when the sample was divided into product groups. Due to the fact that AD duties are generally imposed at the product level, they are more likely to affect firms that produce and export the product under investigation. Finally, there is little evidence of the trade destruction in the case of lead-acid batteries; Bangladesh’s success in negotiating with the WTO DSB may have offset any such effect.

The empirical findings of this study have important policy implications not only for Bangladesh but also for other LDCs. Article 11 of the WTO Anti-dumping Agreement mandates that AD duties should be terminated no later than 5 years after first being applied, unless revoked earlier. However, the ‘sunset review’ policy allows for further enhancement of the tenure of the AD duty. Since the imposition of Indian AD duties, Bangladesh has repeatedly tried to contest at the bilateral level; however, India has yet to agree to lift them. Moreover, India is now conducting a sunset review of hydrogen peroxide and jute products imported from Bangladesh. Given the discovery of the trade destruction by this study, indicated by a sharp reduction in Bangladeshi exports to India due to Indian AD duties, it seems reasonable for policymakers in Bangladesh to initiate legal proceedings via the WTO’s DSB. Otherwise, we anticipate that India will continue to impose AD duties for an extended period of time during the sunset reviews.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the research fund of Chungnam National University and the National Research Foundation of Korea (NRF-2021S1A5B8096365).