Abstract

In recent years, the prominence of environmental, social, and governance (ESG) investing has expanded significantly due to growing awareness of sustainability issues, such as climate change and social justice concerns, as well as an increasing understanding of the need for sustainable business approaches. This increasing focus on ESG has led to a growing demand for ESG-related disclosure in the financial market. Therefore, this study investigates the mediating role of financial constraints in the relationship between ESG disclosure and financial performance. The study aims to determine whether firms with strong ESG disclosure experience reduced financial constraints, leading to improved financial outcomes. Analyzing 690 Indian-listed firms from 2011 to 2022, the research provides a comprehensive assessment of sustainability practices in an emerging market. Findings suggest that a company’s ESG disclosure has a positive impact on the financial outcome performance, with financial constraints acting as a partial mediator. Organizations that implement effective ESG disclosure encounter reduced financial constraints, ultimately enhancing their financial stability. Through the application of a mediation effect model, the study clarifies the indirect influence of financial constraints on the relationship between ESG and financial performance. These results highlight the importance of disclosing ESG initiatives in enhancing operational efficiency, mitigating financial risks, and fostering stakeholder trust. The insights contribute to the ongoing discussion on the integrated reporting of ESG and its financial implications.

1. Introduction

Environmental, social, and governance (ESG) factors are becoming more prominent. They influence business strategies and investment decisions. ESG encompasses a broad range of issues, including environmental stewardship, social commitment, corporate governance, and ethical conduct. As global urbanization and economic expansion intensify, emerging environmental and social concerns become increasingly significant. These concerns have received substantial attention from governments, corporations, and academics, emphasizing the necessity for enduring solutions. Thus, sustainable development has become a central focus in academics and policy discussions, highlighting the intersection of economic, environmental and social goals. In support of this, a total of 5,300 institutions have endorsed the UN Principles for Responsible Investment, agreeing to incorporate ESG standards. In 2023, this initiative surpassed its target of managing investments exceeding $121t. In this process, ESG incorporates ESG considerations within sustainable business growth. In India, ESG disclosure gained traction with the 2021 Business Responsibility and Sustainability Reporting framework by SEBI, which mandates standardized reporting for the top 1,000 listed firms. This shift from voluntary to structured disclosure enhances transparency, guides sustainability strategies, and aligns Indian practices with global standards. Unlike previous strategies that focused primarily on financial benefits, ESG emphasizes corporate accountability to stakeholders. It encompasses the concepts of sustainability at the organizational level and is an important criterion for assessing a company’s longevity and responsibility (Bai et al., 2022). Financing is vital for businesses to achieve sustainable growth. Sufficient funds are required for operations, and financial constraints can pose significant challenges and risks to a company’s survival, especially during rapid industry expansion and transition. As the ESG system is emerging, firms can easily acquire capital by implementing ESG practices. Companies can reconsider their commitment to ESG responsibilities and disclosures as an advantage to overcome financial constraints (He et al., 2023). As awareness of ESG issues grows, investors are increasingly considering companies’ ESG disclosures and incorporating these elements into their investment strategies. This trend has led to ESG disclosures, a strategy that seeks to align investment choices with personal values and promote positive social and environmental impact.

Theoretically, firms disclose ESG information to mitigate information asymmetry (Alatawi et al., 2023) and benefit various stakeholders (Martínez-Ferrero et al., 2016), particularly investors, thereby alleviating firm capital constraints. Firms that adopt ethical and sustainable approaches reduce the information asymmetry and conflict of interest among stakeholders (Rossi et al., 2021). Therefore, incorporating an integrated reporting of the firm’s sustainable performance becomes vital (Thawani & Bhatia, 2024). According to the stakeholder theory, businesses disclose financial and sustainability-related information to demonstrate their integrity to stakeholders. Companies that disclose such information can minimize transaction costs and encourage stakeholder participation in driving economic growth (Freeman & Evan, 1990), thus fulfilling the different interests of their stakeholders. According to Elmghaamez et al. (2024), ESG disclosure is crucial for equity holders and key stakeholders to accurately assess a firm’s ESG commitments, which in turn influences its financial outcomes. Investors prefer non-financial information as it helps them make decisions and reduces financing costs. As a result, increased ESG disclosure is connected to reduced capital costs and lower financial constraints. Therefore, these disclosures are important for shareholders’ investment and financing decisions (Chouaibi et al., 2021b). Firms that disclose ESG information may reduce information asymmetry, attract financial assistance from shareholders, alleviate financing restrictions, and enhance company value. Furthermore, firms that incorporate sustainability strategies in their business are also responsible for tax payments. The sustainability disclosure serves as a mirror that reflects the ethical approach of these firms, wherein they are responsible not only in terms of ESG but also for financial responsibilities such as tax payment (Chouaibi et al., 2022a).

Research examining the connection between ESG and corporate financial results has predominantly examined in high income countries (Cornett et al., 2016; Li et al., 2018). However, few studies have been conducted in emerging economies like India, where mandatory ESG disclosure rules are in place. Studies in developed economies indicate that ESG disclosures may indirectly affect business value through risk-taking (Harjoto & Laksmana, 2018), regional diversity and economic slack (Duque-Grisales & Aguilera-Caracuel, 2021), executive power (Li et al., 2018), and market impressions (Bardos et al., 2020). However, these studies have largely overlooked the crucial role that financial constraints play in this context. Notably, increased ESG transparency is inversely related to capital constraints (Cheng et al., 2014), specifically in emerging economies, where financial markets are less established and information asymmetry is more acute. In the Indian context, the lack of comprehensive ESG disclosure requirements and reporting frameworks exacerbates capital constraints, making it more difficult for enterprises to secure financing. As a result, ESG information disclosure may play a crucial role in alleviating these constraints by enhancing transparency and enabling enterprises to secure financial assistance.

Therefore, based on a sample of 690 publicly traded Indian companies from 2011 to 2022, we investigated the connection between ESG disclosure and corporate financial performance, with financial constraints as a mediating factor. The empirical results demonstrate a significant positive relationship between ESG disclosure and financial performance, indicating that companies with robust sustainability reporting are more likely to enhance their financial performance. Prioritizing the integrated reporting of ESG initiatives can help organizations reduce information asymmetry, lower agency costs, increase operational efficiency, mitigate risks, and enhance stakeholder confidence, ultimately leading to improved financial outcomes. These findings highlight the importance of disclosing sustainable business models in mitigating financial constraints and the role of highly sustainable firms in enhancing stakeholder reputation and attracting socially responsible investments.

This study contributes to the expanding body of research by examining the relationship between ESG disclosure and corporate financial performance in several ways. First, unlike previous studies, which have primarily examined the impact of ESG disclosure on company value in developed countries (Cornett et al., 2016), this study focuses on the Indian context, where mandatory ESG disclosure regulations are still emerging. It elucidates how voluntary ESG disclosure influences the financial performance of companies in emerging markets such as India (Siwei & Chalermkiat, 2023). Second, this study employed a mediation model to examine how financial constraints impact corporate financial performance through ESG disclosure. This approach makes a unique contribution to the literature by investigating the indirect link between ESG disclosure and financial outcomes, as previous studies have focused solely on the direct effect (Attarit et al., 2025; Xu & Zhu, 2024). Finally, our research is distinguished by its extensive dataset, encompassing firms listed on both the “Bombay Stock Exchange (BSE)” and the “National Stock Exchange (NSE).” By incorporating companies that voluntarily disclose their ESG ratings, we provide a comprehensive perspective on the disclosure of sustainability practices across various Indian firms. This dataset comprehensively examines the relationship between ESG disclosure scores and financial performance, providing significant insights into how the integration of sustainability concerns into corporate reporting influences financial decision-making.

The arrangement of the article’s subsequent sections is as follows: Section 2 outlines the key hypotheses and delves into the relevant literature. Section 3 presents the research methods, including data collection and a preliminary statistical description of the dataset. Sections 4 and 5 present the model specification and results of the empirical analysis. Section 6 outlines the robustness test. Finally, Section 7 closes the study by summarizing the important findings and implications.

2. Review of Literature and Hypothesis Development

2.1. ESG and Financial Performance

ESG principles expand upon corporate social responsibility (CSR) and socially responsible investment; however, the impact of ESG disclosure on financial performance remains a subject of ongoing debate (Chen & Xie, 2022). With a growing focus on sustainability, stakeholders are increasingly using ESG disclosures to evaluate a firm’s effectiveness (Xu & Zhu, 2024). The stakeholder theory posits that a company’s success hinges on effectively managing relationships with its various stakeholders, including owners, employees, customers, suppliers and communities, emphasizing the importance of considering the interests of all stakeholders for long-term growth (Freeman, 1984). Implementing ESG practices and disclosure can thus enhance firm value.

Recent literature suggests that robust ESG disclosure enhances financial stability and performance. In China, robust ESG policies foster innovation and lead to improved financial outcomes (Xu & Zhu, 2024). Environmental disclosures have a positive impact on financial performance, and social and governance scores moderates this relationship (Chouaibi et al., 2021a). Effective ESG disclosure also reduces risk, enhances operational efficiency, and strengthens a company’s reputation, attracting investors and supporting long-term profitability (Siwei & Chalermkiat, 2023). Additionally, Tang and Loang (2024) find that strong governance significantly contributes to better financial outcomes. Based on this evidence, we present our hypothesis as follows:

H1: Firms’ strong ESG disclosures enhance financial performance by reducing information asymmetry.

2.2. ESG and Financial Constraints

According to stakeholder and resource dependency theories, high ESG disclosure enhances market information symmetry, enabling firms to meet stakeholders’ informational needs, mitigate conflicts of interest and attract external capital, thereby alleviating financing constraints (Hu, 2023). The sustainability theory further posits that while ESG investments may initially increase costs, they ultimately enhance operational efficiency, minimize carbon footprint, retain high-quality employees, and improve overall productivity (Hao & Wu, 2024; Wang et al., 2023). Shareholders and customers increasingly prioritize sustainability, rewarding firms committed to long-term environmental and social goals, which in turn strengthen investor credibility and broaden financing alternatives (Azmi et al., 2021; Hao & Wu, 2024). Multiple studies have shown a strong link between ESG disclosure and fewer financial constraints, showing that effective reporting lowers financing costs, promotes sustainable development, improves access to capital, and attracts green funding through heightened investor confidence (Hao & Wu, 2024; Li et al., 2023). Collectively, these findings suggest that ESG disclosure plays a significant role in mitigating financial frictions and improving firm financial performance. Based on this evidence, we present our second hypothesis as follows:

H2: Firms’ high ESG disclosure scores reduce financial constraints.

2.3. Mediation of Financial Constraints

Financing constraints occur when firms lack sufficient internal capital and face challenges accessing external funds, restricting growth opportunities. The stakeholder theory posits that weak ESG practices and reporting have a negative impact on employees, communities and the society, ultimately affecting both the firm’s and shareholders’ value. In contrast, strong ESG disclosures encourage green innovation, streamline technology and foster positive stakeholder relationships, enhancing both operational efficiency and credibility (Hao & Wu, 2024). Socially responsible firms can increase shareholder equity, maintain investor confidence and mitigate financing constraints (Huang et al., 2023). Empirical evidence suggests that ESG disclosure plays a significant role in mitigating financial constraints, thereby enhancing financial performance. Compelling ESG reporting highlights an entity’s commitment to sustainable practices, reducing financial frictions and enhancing performance outcomes (Shang, 2024). Studies from China further demonstrate that effective ESG disclosure significantly improves financial success, with financial restrictions mediating the link between ESG and corporate financial outcomes. Hence, we state the following hypothesis:

H3: Financial constraints mediate the relationship between ESG disclosure and financial performance.

3. Data and Research Design

3.1. Sample Selection

The research encompassed all Indian corporations listed on the NSE and BSE from 2011 to 2022, utilizing Bloomberg for ESG data, CMIE Prowess IQ for company-specific data, and World Bank sources for macroeconomic indicators. After excluding utilities, insurance, and financial entities due to their unique regulatory environments, the final sample consisted of 690 non-financial companies. All variables were winsorized at the 1% tails on both ends to address outliers (Agnese & Giacomini, 2023). The use of well-established data sources ensures the reliability and authenticity of the data.

3.2. Variable Description

Based on prior literature (An et al., 2025; Shang, 2024; Tang & Loang, 2024), the present study summarizes the variables in Appendix A (Supplementary material). Tobin’s Q is the dependent variable, representing a measure of financial performance. Independent variables include the aggregated ESG score (ESGC) and its components, E, S, and G scores, which reflect sustainability disclosure. Controls include firm size (log of total assets), age (log of years since incorporation), growth (Assetst − Assetst−1/Assetst−1), tangibility (net PPE/total assets), and liquidity (current assets/current liabilities), all from CMIE. Macroeconomic controls include annual inflation (CPI growth) and GDP growth, sourced from the World Bank. These variables provide a comprehensive framework for examining the links between ESG disclosure, financial constraints, and corporate financial performance.

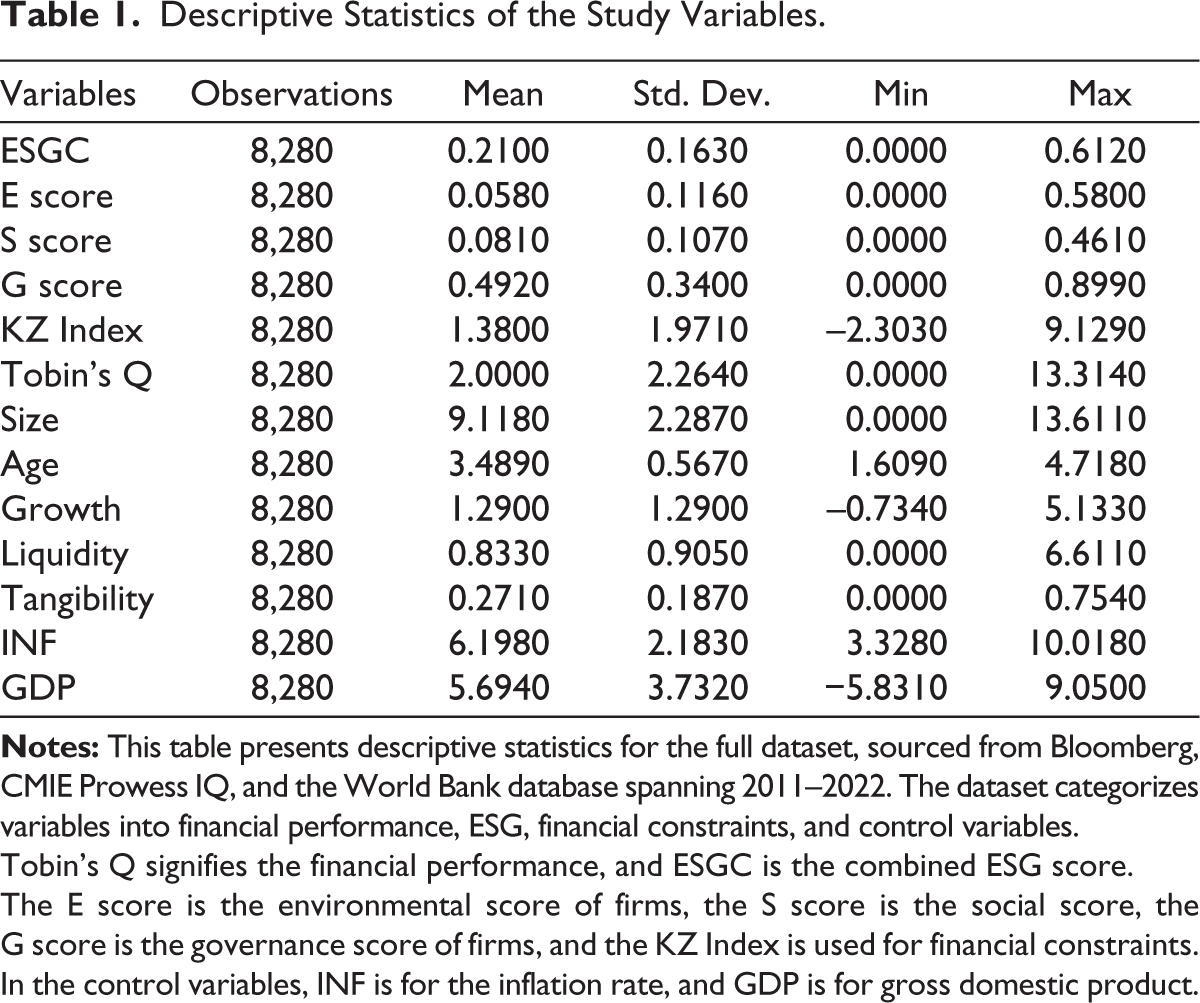

3.3. Descriptive Statistics

Table 1 reports the descriptive statistics. The mean ESGC score (0.2100) indicates moderate disclosure, with governance (0.4920) leading to social (0.0810) and environmental (0.0580) aspects. This hierarchical pattern suggests that governance measures are more advanced than environmental and social measures in the sample. This disparity highlights that governance reporting is institutionally well-established, while environmental and social disclosures remain in a developmental and less-formalized stage. The KZ Index average (1.3800) suggests moderate financial constraints, while Tobin’s Q (2.0000) reflects strong market value. Control variables indicate that firms are generally large (Size = 9.1180) and established (Age = 3.4890), with stable growth (1.2900), moderate liquidity (0.8330), and a moderate level of tangible asset intensity (0.2710). Macroeconomic indicators, including GDP (5.6940) and inflation (6.1980), capture the broader economic conditions during the study period.

Descriptive Statistics of the Study Variables.

Tobin’s Q signifies the financial performance, and ESGC is the combined ESG score.

The E score is the environmental score of firms, the S score is the social score, the G score is the governance score of firms, and the KZ Index is used for financial constraints.

In the control variables, INF is for the inflation rate, and GDP is for gross domestic product.

3.4. Correlation Matrix

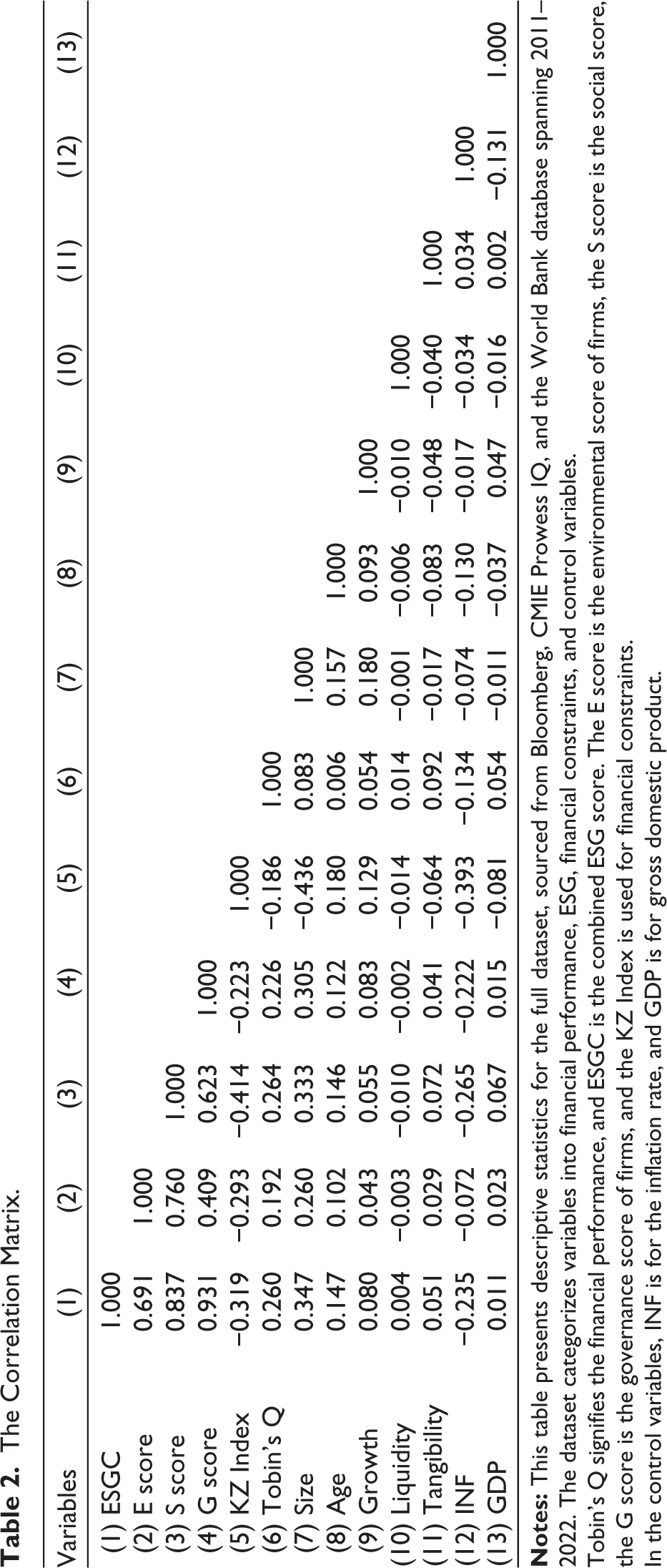

Table 2 presents the correlation matrix. ESG disclosure (ESGC) is positively correlated with Tobin’s Q (0.260) and negatively correlated with the KZ Index (−0.319), suggesting that stronger ESG practices enhance firm value while alleviating financial constraints. Component scores (E, S, G) exhibit similar patterns, with the S score (−0.414) showing the most significant reduction in constraints. The KZ Index is also negatively associated with Tobin’s Q (−0.186), supporting the view that lower constraints lead to improved performance. Among controls, firm size is positively linked to ESGC and Tobin’s Q but negatively to the KZ Index, while firm age shows mixed effects. Growth and tangibility correlate positively with ESGC and Tobin’s Q, while liquidity shows a negligible influence. Additionally, macroeconomic factors such as inflation weaken both ESG disclosure and performance.

The Correlation Matrix.

Tobin’s Q signifies the financial performance, and ESGC is the combined ESG score. The E score is the environmental score of firms, the S score is the social score, the G score is the governance score of firms, and the KZ Index is used for financial constraints.

In the control variables, INF is for the inflation rate, and GDP is for gross domestic product.

4. Model Specifications

To examine our hypothesis, we used Model 1, a panel regression with a fixed-effects estimator, to investigate the relationship between ESG and financial performance. This model explicitly evaluates the influence of the overall ESGC on financial performance, determined by Tobin’s Q. The independent variable of interest is the combined ESGC, and Tobin’s Q is the dependent variable. Control variables, such as company size, age, growth, liquidity, tangibility, annual GDP growth, and annual inflation rate (INF), are used to account for firm-level and macroeconomic factors that may affect financial performance. Furthermore, year (t), firm (i), and industry-fixed effects are incorporated to account for time- and industry-specific fluctuations, resulting in robust estimates. This holistic approach enabled us to capture the multidimensional relationship between ESG disclosure practices and financial performance while mitigating the impact of potential confounding factors. Therefore, we utilize the subsequent regression specification:

Before performing mediation analysis, it is crucial to confirm that the independent variable significantly affects the mediator, as this is a key prerequisite for establishing a mediation effect. Therefore, we estimate Model 2 to examine whether ESG disclosure scores (ESGC) influence financial constraints, measured by the KZ Index. This model employs the same control variables as Model 1 and incorporates year-, firm-, and industry-fixed effects to account for time- and sector-specific variations. Establishing this link enables us to assess the potential mediating role of financial constraints in the relationship between ESG and financial performance. Model 2 specification is as follows:

Following the establishment of direct connections in Models 1 and 2, we proceed with Model 3 to investigate the potential mediating role of financial constraints in the relationship between ESGC and financial performance. This model uses results from previous models to examine whether the KZ Index mediates the relationship between ESG and financial performance. The regression specifications for Model 3 are as follows:

In Model 3, Tobin’s Q is the outcome variable, ESGC is the explanatory variable, and the KZ Index is the mediating variable. To ensure uniformity, the same control variables from Models 1 and 2 are included, along with year-, firm-, and industry-fixed effects. These specifications enable us to assess whether financial constraints amplify or mitigate the impact of ESG disclosure practices on financial performance.

5. Empirical Results

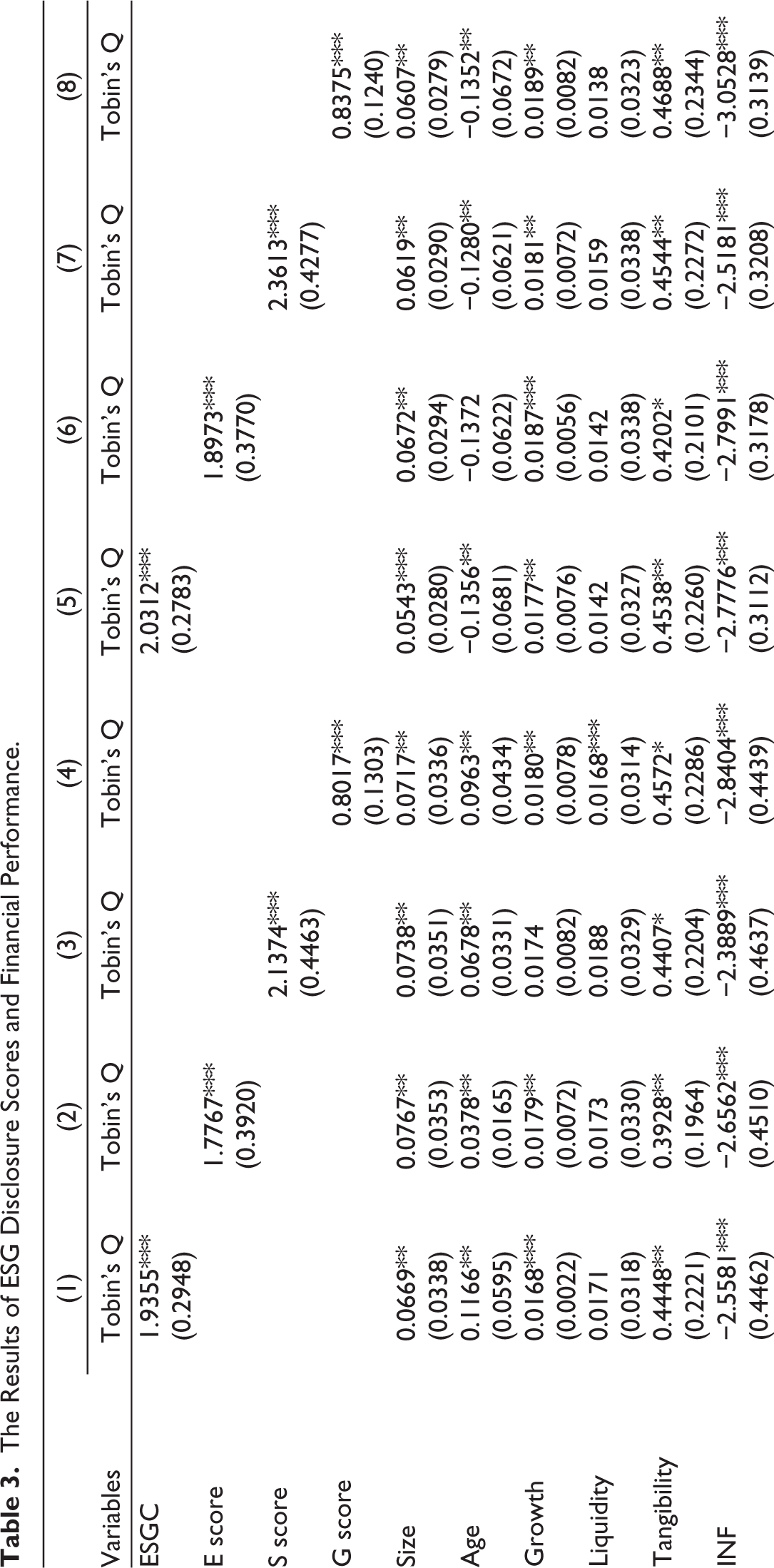

Table 3 presents a comprehensive overview of our findings on the association between ESG ratings and financial performance, utilizing panel regression with fixed effects. Our analysis provides insights into the factors that influence firms’ financial outcomes. The first four columns include year- and firm-fixed effects, suggesting a strong positive association between the composite ESGS and financial performance. Specifically, Column 1 shows a significant positive correlation (1.9355), indicating that entities with higher overall ESG ratings experience substantial financial growth. Columns 2–4 show substantial positive coefficients for the E (1.7767), S (2.1374), and G (0.8017) scores, respectively. The results suggest that enhancing these specific ESG pillars has a positive impact on financial success. The findings indicate that entities that employ effective ESG disclosure policies manage external challenges more effectively and maintain stakeholder confidence, which is critical for long-term performance and wealth creation. Effective environmental management, social responsibility, and strong governance contribute to reducing operational risks, enhancing reputation, and facilitating the secure financing of projects. ESG-focused businesses may be more adaptable to shifting legislation and public expectations, thereby positioning them well for future growth. The positive link indicates that high-performing corporations are more inclined to prioritize ESG and financial goals, resulting in a self-reinforcing cycle. Our results align with the existing research by Xu and Zhu (2024) and An et al. (2025).

The Results of ESG Disclosure Scores and Financial Performance.

The dependent variable is financial performance, proxied by Tobin’s Q. The independent variable is sustainability disclosure, which is proxied by ESG, E score, S score, and G score.

Size, age, growth, liquidity, profitability, tangibility, INF, and GDP are the control variables. All the variables are winsorized at 1% to account for normality issues.

Statistical significance at 1%, 5%, and 10% are indicated as ***, **, and *, respectively.

The standard error values are given in parentheses.

The study reveals significant correlations between financial variables and financial success, each with its own underlying explanations. More prominent companies benefit from economies of scale and increased market power, which improves performance. Age has a positive impact since older entities gain expertise, resources, and stability over time. Growth rate improves financial performance by increasing revenues and expanding market prospects. Tangibility optimizes profits by providing collateral for funding and lowering investment risks. Economic indicators, such as GDP, improve performance by increasing demand and economic activity; however, inflation reduces profitability by affecting input prices and price strategies. Interestingly, liquidity had no significant impact. This may be due to the complex relationship between excessive liquidity, which suggests resource misallocation, and inadequate liquidity, which hinders operations. The results remain significant and unaltered when year- and industry-fixed effects (Columns 5–8) are considered. This adds credibility and validity to our study by considering firm-level and industry-level attributes.

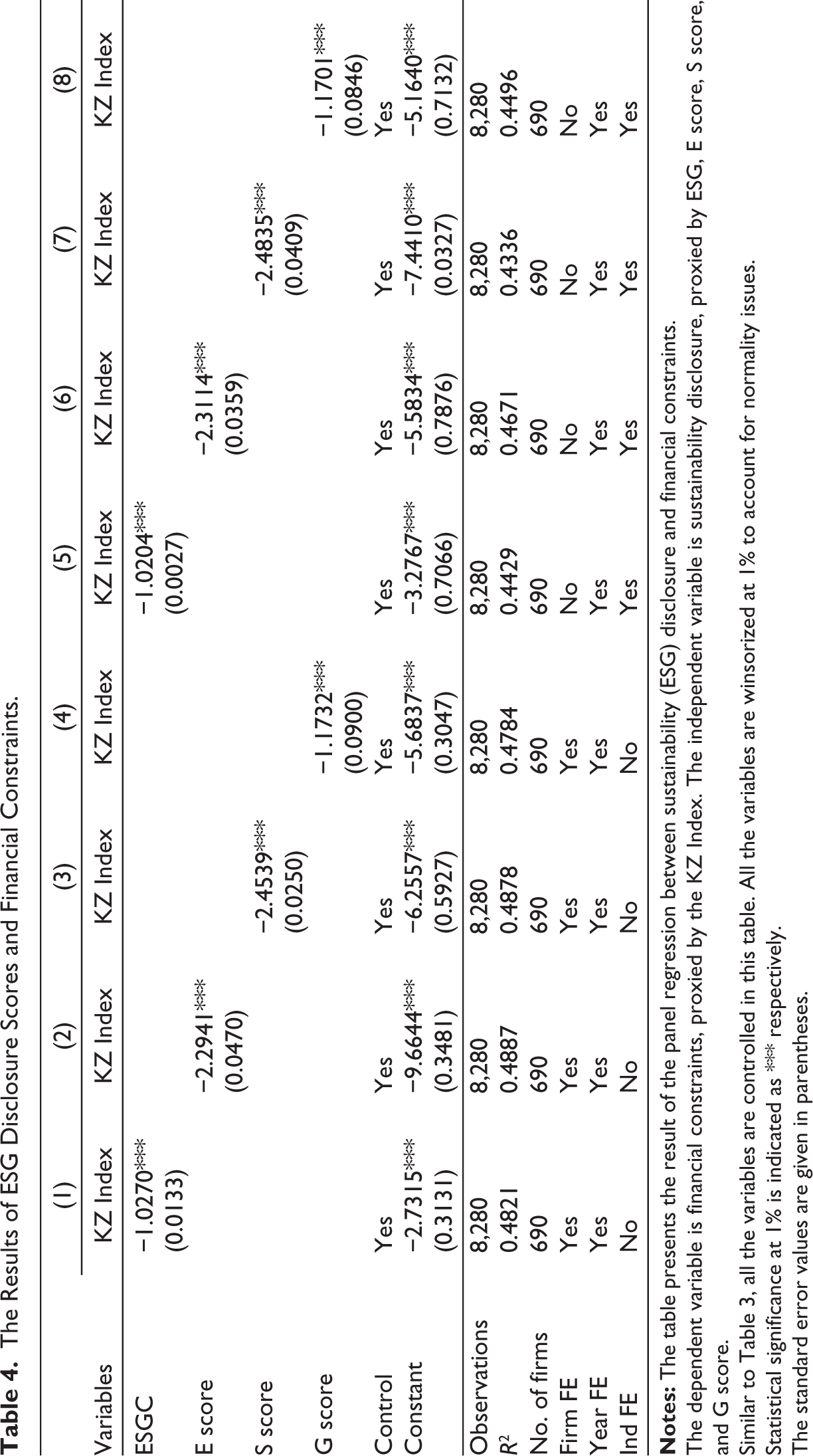

Table 4 presents the results of panel regressions examining the relationship between ESG ratings and financial constraints while controlling for year- and firm-fixed effects. The research reveals a substantial negative correlation for the combined ESGS (−1.0270), suggesting that companies with better ESG scores face fewer financial constraints. Decomposing this impact across individual ESG pillars uncovers significant negative coefficients for the E (−2.2941), S (−2.4539), and G (−1.1732) scores. These findings emphasize the positive impact of strengthening these attributes on financial accessibility. The negative correlation between ESG ratings and financial constraints suggests that more effective ESG disclosure practices are associated with easier access to financial resources. This association suggests that firms prioritizing ESG disclosure may receive higher priority from financial markets due to improved reputation, risk reduction, or matching with shifting shareholder preferences. These findings align with past studies such as Hao and Wu (2024), An et al. (2025), and Li et al. (2023). The findings remained significant and unaffected when tested with year- and industry-fixed effects (Columns 5–8). This provides credibility and validity to our study by considering both firm-specific and industry-specific attributes. Similar to Table 3, all models account for multiple covariates and use robust standard errors to address heteroscedasticity. As a result, the results indicate that firms with superior ESG ratings tend to reduce financial constraints, demonstrating the strategic financial benefits of implementing comprehensive sustainability techniques into business decision-making.

The Results of ESG Disclosure Scores and Financial Constraints.

The dependent variable is financial constraints, proxied by the KZ Index. The independent variable is sustainability disclosure, proxied by ESG, E score, S score, and G score.

Similar to Table 3, all the variables are controlled in this table. All the variables are winsorized at 1% to account for normality issues.

Statistical significance at 1% is indicated as *** respectively.

The standard error values are given in parentheses.

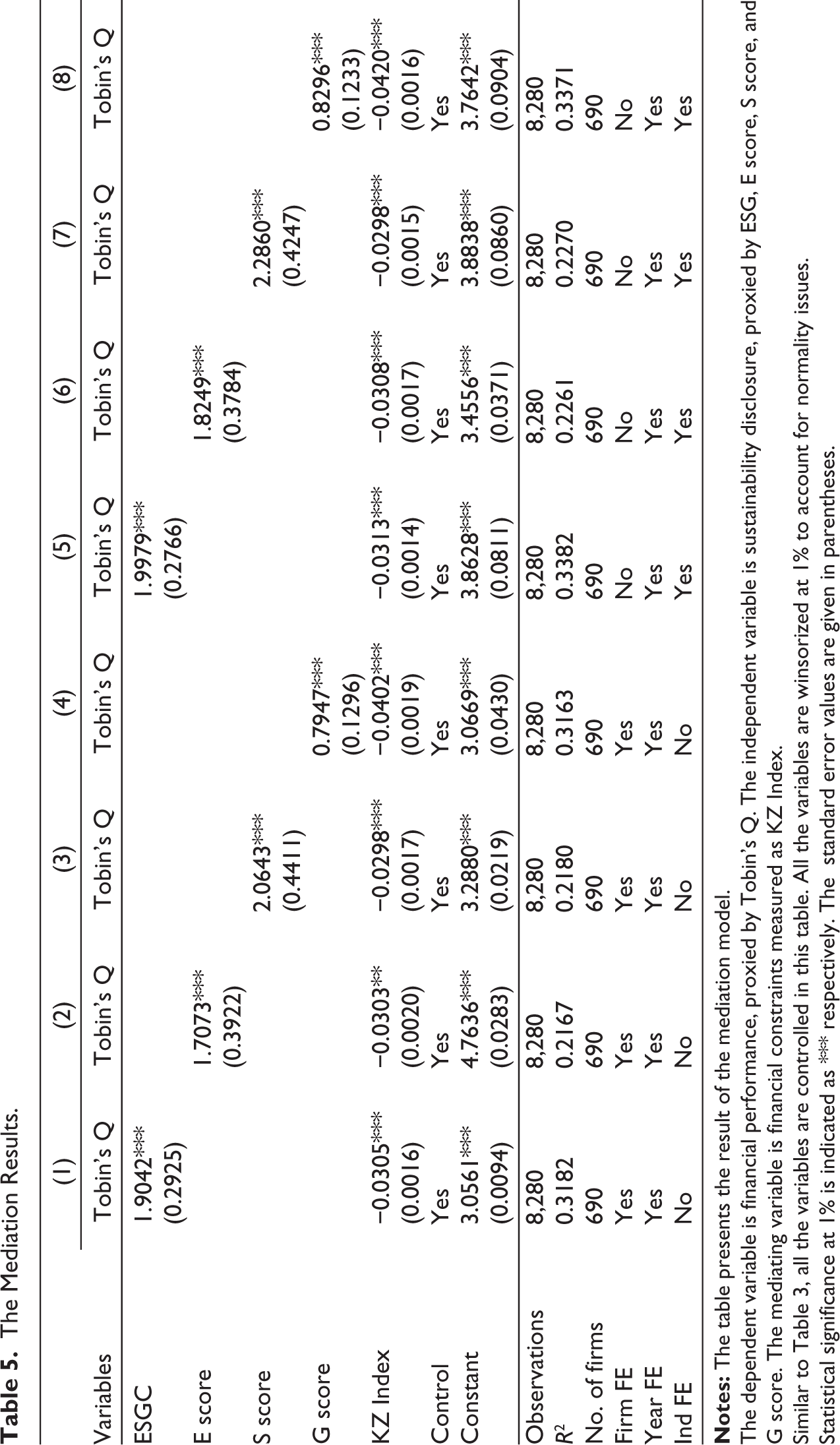

Table 5 summarizes the mediation outcomes, demonstrating how financial constraints mediate the relationship between sustainability parameters and financial performance. Our study suggests a substantial positive direct relationship between the composite ESGS and financial performance, as presented in Table 3 (Columns 1 and 5). This positive connection highlights the significance of the ESG component to business value creation. Further, individual E, S, and G scores also exhibits significant positive direct associations. However, when the mediating variable for financial constraints (KZ Index) is introduced into the model, a noticeable shift in the coefficients is observed (Table 5). The KZ Index consistently shows a substantial negative relationship, indicating that lower financial constraints lead to improved economic performance. This also results in an attenuation of the ESG coefficients compared to their direct impact, as shown in Table 3.

The Mediation Results.

The dependent variable is financial performance, proxied by Tobin’s Q. The independent variable is sustainability disclosure, proxied by ESG, E score, S score, and G score. The mediating variable is financial constraints measured as KZ Index.

Similar to Table 3, all the variables are controlled in this table. All the variables are winsorized at 1% to account for normality issues.

Statistical significance at 1% is indicated as *** respectively. The standard error values are given in parentheses.

The composite ESG coefficient declines from 1.9355 in Table 3 to 1.9042 in Table 5 (Column 1) but remains statistically significant. This attenuation implies that financial constraints partially mediate the relationship between ESG and financial performance. The findings suggest that financial constraints are a partial intermediate element in explaining how ESG disclosure practices lead to better financial outcomes. To quantify the mediation effect, we have incorporated the methodology proposed by Mo (2001). The proportion of mediation is relatively modest. Specifically, the mediation effect for the ESGC is 1.64% of the total effect. Among the individual components, the E score shows a mediation effect of 3.81%, the S score has a mediation effect of 3.19%, and the G score exhibits a mediation effect of 0.94%. Although statistically significant, the effect of ESG on firm outcomes through financial constraints is economically modest, reflecting India’s bank-driven, promoter-dominated financing system, where ESG is not fully integrated into credit decisions (Gidage & Bhide, 2025). While ESG disclosure helps ease financing frictions, its impact depends more on strategic resource allocation than capital access. By contrast, alternative mediators—such as innovation (Zheng & Bu, 2024), reputation (Gidage & Bhide, 2025), and investor confidence (Tang et al., 2024)—provide stronger pathways by enhancing efficiency, trust, and valuations. Thus, although financial constraints remain a plausible mechanism, their role is limited compared to these more direct channels. This suggests that while ESG disclosure has a direct impact on financial performance, it also indirectly contributes to improved financial performance by alleviating economic constraints. This intricate result suggests that ESG disclosure can improve financial outcomes in various ways, including immediate impacts on operational efficiency, risk management, stakeholder relationships, and indirect implications such as increased access to resources and reduced legislative scrutiny. This finding underscores the intricacy and robustness of the ESG–financial performance link, highlighting the need to incorporate both direct and indirect mechanisms when analyzing this relationship. It also supports the idea that adept integrated reporting of ESG practices can give companies a competitive edge and promote sustained financial performance, cost reductions, and risk mitigation. The investigation found that disclosing ESG disclosure improves financial outcomes directly and indirectly by reducing financial constraints and enhancing its positive impact on business value. The study’s findings are consistent with previous studies (An et al., 2025; Shang, 2024); Tang & Loang, 2024).

We further tested robustness by examining industry heterogeneity between manufacturing and non-manufacturing firms. Results show that the indirect effect of ESGC on Tobin’s Q via financial constraints (KZ Index) is positive in both groups, at 0.0121 for non-manufacturing and 0.0203 for manufacturing firms (see Appendix B; supplementary material). The stronger mediation in manufacturing reflects their higher capital intensity, greater dependence on external financing, and stricter regulatory and environmental standards. Consequently, effective ESG practices not only ease financing frictions but also enhance value by mitigating risks, building stakeholder trust, and signaling management quality.

6. Robustness Analysis

To evaluate the robustness of the primary research models, we have employed established alternative measures for financial performance and financial constraints. Specifically, we utilize return on assets (ROA) as an alternative measure for financial performance (Benner & Veloso, 2008; Klingenberg et al., 2013) and the SA Index 1 to assess financial constraints (Cheng et al., 2014; Zhang et al., 2020). The results reaffirm our primary findings regarding the mediating effect of financial constraints on the relationship between ESG and financial performance. Appendix C (Supplementary material) presents the results of the robustness analysis. Columns 1 and 2 illustrate the direct relationship between ROA, SA Index, and ESG, revealing a significant positive relationship among these variables. Column 3 further examines the mediating role of the SA Index in the ESG and ROA relationship. Our analysis reveals that ESG has a significant positive coefficient of 0.0348 when regressed on ROA. Upon including the SA Index in the model, the coefficient increases to 0.0362, indicating partial mediation by the SA Index. Additionally, the results remained consistent when we tested the model using individual ESG scores. Therefore, we conclude that our original model is robust, as validated by this alternative specification, which confirms that financial constraints partially mediate the relationship between ESG and financial performance.

7. Discussion and Conclusion

This study investigates the relationship between ESG disclosure and the financial performance of Indian-listed firms from 2011 to 2022. Employing a panel regression approach with fixed effects, the study explains dynamic interactions while controlling for unobservable heterogeneity across firms and time. The findings demonstrate that superior ESG disclosure enhances corporate profitability, underscoring the strategic importance of integrating sustainable standards into business operations.

Moreover, the study examines the mediating role of financial constraints, which explains this relationship and reveals that financial constraints partially mediate between ESG and financial performance. This suggests that entities with stronger ESG disclosure are better positioned to mitigate financial challenges, such as limited access to capital or higher financing costs. By addressing these constraints, ESG-oriented companies can secure the necessary capital for innovation and growth, thus enhancing their financial performance. The results underscore the multifaceted benefits of ESG initiatives, which directly contribute to financial performance and indirectly enhance it by alleviating financial constraints, providing insights for policymakers, investors, and corporate decision-makers seeking to promote sustainable development.

This study examines the importance of incorporating ESG factors into investment planning for diverse stakeholders. First, to foster sustainable economic growth, regulatory authorities should prioritize enhancing ESG disclosure guidelines, supervision, and disclosure requirements. However, instead of adopting uniform rules, regulators could implement sector-specific disclosure standards, such as stricter climate-related reporting for energy and manufacturing firms, and enhanced governance and labor standards for service-oriented industries. Such targeted regulation reduces compliance ambiguity while minimizing excessive reporting costs for smaller firms. Improved regulations can enhance transparency, enabling stakeholders to make more informed decisions while fostering a culture of responsibility and accountability within firms. Second, companies should proactively integrate ESG principles into strategic decision-making processes. This enables them to enhance operational efficiency, build stakeholder trust, and improve access to capital. Firms operating in resource-intensive sectors, such as energy, construction, or manufacturing, can benefit from incentivized green technology adoption. Meanwhile, financial institutions can prioritize social and governance aspects by implementing stronger risk-screening frameworks. Companies must view ESG adoption as more than a regulatory requirement; it is a strategic advantage that can enhance long-term financial outcomes.

Third, firms with superior ESG scores typically exhibit better financial results, lower risk profiles, and greater long-term growth potential. Investors can enhance portfolio stability, risk management, and investment alignment by prioritizing firms with robust ESG disclosure practices. Nonetheless, investors should remain cautious of greenwashing risks and rely on third-party ESG ratings and independent assurance mechanisms to validate disclosures. Furthermore, ESG-focused investments may facilitate the identification of firms that are better positioned to mitigate financial constraints, drive innovation, and deliver superior returns while contributing to environmental and societal well-being. Finally, businesses and governments should collaborate to develop incentives, such as tax reductions or subsidies, for firms that implement sustainable practices. Such incentives could be designed to reward measurable outcomes, such as tax rebates tied to verified carbon reduction in heavy industries, subsidies for renewable energy adoption in utilities, or procurement advantages for firms with strong labor and governance standards in the services sector. This would encourage more firms to engage in ESG initiatives, amplifying their contribution to achieving broader environmental and societal objectives while enhancing their financial performance.

7.1. Future Research

Subsequent studies in this area could expand on the present research by examining the relationship between ESG and economic performance across a wide range of developing economies, utilizing larger datasets to improve the overall applicability of the results. This study uses Bloomberg ESG scores, which capture disclosure levels rather than actual sustainability performance. Thus, the results reflect the impact of disclosure, not necessarily substantive ESG actions. Future research should integrate measures of real sustainability outcomes alongside disclosure indicators to provide a more comprehensive assessment. Researchers may also investigate how gender diversity and earnings management serve as mediating or moderating variables in the relationship between ESG disclosure and firms’ long-term financial decisions, offering more nuanced insights into the impact of sustainability initiatives on fiscal decision-making. Additionally, future investigations could conduct cross-country comparisons between sustainable and non-sustainable firms, analyzing how diverse regional contexts, regulatory frameworks, and market environments influence the impact of ESG disclosure practices on corporate financial outcomes. This approach would yield a more integrated view of ESG’s implications in the global context and influence on organizational financial strategies.

Supplemental Material

Supplemental material for this article is available online.

Footnotes

Acknowledgements

We would like to express our sincere gratitude to all those who have contributed to the completion of this research article. The first author extends her deepest appreciation to Dr. Gopalkrishna B. V., their research supervisor, for his invaluable guidance, support, and encouragement throughout the entire duration of this work. She also extends her gratitude to Mr. Mithun Samanta, Research Scholar at IIT Kharagpur, for his assistance with data collection and analysis.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Open access APC is paid by my institute (National Institute of Technology Karnataka, Surathkal).

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.