Abstract

We examine the association between economic policy uncertainty (EPU) and expected stock returns and how short-selling regulations in China moderate this relationship. Consistent with the overpricing effects literature, we find a negative EPU–return relationship before the introduction of margin trade and short-selling (MTSS) program in 2010. However, after implementation of MTSS, the relationship turned positive for stocks without short-selling constraints, reflecting investors’ demand for higher risk compensation. Using propensity score matching and difference-in-differences, we demonstrate that relaxation of short-selling constraints mitigates overpricing and generates positive uncertainty premium. Our findings highlight the importance of short selling in pricing of uncertainty and implications for policymakers and investors.

1. Introduction

Economic policy uncertainty (EPU), stemming from changes in government policies and regulations, fundamentally shapes investment decisions and resource allocation at both firm and macroeconomic levels (Baker et al., 2016; Pástor & Veronesi, 2012, 2013). 1 Knight (1921) posits that uncertainty increases forecasting difficulty and impedes the ability to quantify future probabilities. Empirical research corroborates that heightened uncertainty amplifies systematic risk, compelling investors to demand additional compensation (Brogaard & Detzel, 2015).

However, the direction and magnitude of the resulting uncertainty premium remain contested even in developed markets. Some studies document a positive relation between the equity risk premium and uncertainty proxied by market return variance (Bali & Zhou, 2016; Rossi & Timmermann, 2015), whereas others report a negative relation (Brandt & Kang, 2004; Brogaard & Detzel, 2015). A further strand of the literature suggests that the risk–return trade-off is state-dependent, varying across economic regimes and market conditions (Bekaert et al., 2022; Drechsler, 2013; Hong et al., 2024). Importantly, Bekaert et al. (1998) highlight that emerging markets, characterized by elevated volatility and time-varying higher-order moments, pose additional challenges for investors in forming return expectations. These dynamics may amplify investor aversion to uncertainty (Izhakian & Benninga, 2011), rendering the sign and magnitude of the uncertainty premium even more ambiguous in emerging markets.

In this theoretical context, China offers a particularly salient setting to examine the asset pricing implications of EPU. Unlike most advanced and emerging economies, China’s capital markets are subject to pervasive government intervention, spanning policy-driven credit allocation, industry-specific directives, and direct administrative controls (Carpenter et al., 2021; Wang et al., 2024). The unique institutional environment generates frequent and often large EPU shocks, magnifying their effects on investor behavior and asset valuations. Furthermore, relative to the developed and other emerging markets, the dominance of retail investors in China’s markets (Allen et al., 2005; Li et al., 2018) increases the likelihood of mispricing uncertainty. Together, these settings underscore the importance of analyzing how EPU is priced in China and highlight the heterogeneity in pricing of uncertainty.

The extant literature on China presents conflicting evidence regarding the relation between EPU and future stock returns. At the market level, Chen et al. (2017) document a negative association for the period 1996–2013, reporting that a one standard deviation increase in EPU corresponds to a 1.2% decline in monthly expected returns. In contrast, Phan et al. (2018) found this relationship statistically insignificant during 1996–2016, suggesting time-varying EPU effects on expected stock returns in China. At the firm level too, the evidence remains inconclusive. While Bali et al. (2017) find a negative macroeconomic uncertainty premium in the United States, Li (2017) documents a positive premium in China, attributing this difference to binding short-selling constraints leading to persistent overpricing of low EPU-β stocks by risk-seeking investors. These contrasting results highlight the importance of the institutional environment, particularly short-selling regulations, in the pricing of EPU.

Two competing ideas dominate the literature on the role of short selling in efficient pricing of stocks. Miller (1977) argues that with short-selling restrictions, stock prices reflect excessive optimism and become systematically overvalued due to the divergence in investors’ views. This “overpricing effect” implies a negative relation between EPU and expected stock returns (Bali et al., 2017; Cheng et al., 2021). Conversely, when short selling is permitted, uncertainty-averse investors demand higher returns for bearing policy-related risks, generating a positive EPU–return relation, characterized as the “uncertainty aversion effect” (Cai et al., 2023).

Despite the critical role of short selling in enhancing information transparency and pricing efficiency, research on its influence on the pricing of EPU in emerging markets like China remains limited. Chen et al. (2017) attribute the negative association between EPU and stock returns to behavioral biases among retail investors, but they do not consider the role of short-selling regulations. Our study advances the existing evidence by leveraging the phased introduction of the margin trading and short selling (MTSS) pilot program launched in March 2010, which offers a unique opportunity for a natural experiment to study how changes in short-selling constraints affect the pricing of EPU.

Prior to the introduction of the MTSS program, short selling was prohibited in China. The MTSS program permitted short selling of eligible stocks over time, providing an ideal setting to examine how regulatory changes affect the EPU–return relationship. Consistent with existing literature, we posit that the period before MTSS introduction would be characterized by the “overpricing effect.” Conversely, after the implementation of MTSS, demand for higher returns by uncertainty-averse investors would give rise to the “uncertainty aversion effect.”

Our sample covers Chinese A-share listed firms from January 2005 to December 2023. We estimate firm-level EPU exposure using uncertainty β (EPUB) and employ Fama–MacBeth cross-sectional regressions and long-short portfolio-level analysis to assess the impact of EPU on stock returns before and after the MTSS program introduction. To address potential endogeneity concerns, we conduct propensity score matching (PSM) and difference-in-differences (DID) analyses to evaluate how variations in short-selling constraints affect uncertainty pricing.

Our results provide robust evidence supporting our theoretical arguments. Consistent with the “overpricing effect,” we observe a negative EPU premium for short-sale-constrained stocks before the MTSS program. However, following its implementation, MTSS-eligible stocks exhibit a positive EPU premium, supporting the “uncertainty aversion effect” arising from the relaxation of short-selling constraints. We investigate the impact on mispricing using the index proposed by Shi et al. (2023) and find a significant decline in mispricing of MTSS-eligible stocks, while it remains unchanged for non-MTSS-eligible stocks. These results align with Chang et al. (2014) and Li et al. (2018), who demonstrate that the MTSS program enhances information efficiency and accelerates price discovery in Chinese markets.

We make three distinct contributions to literature. First, we extend Chen et al.’s (2017) work by demonstrating that uncertainty pricing in China is significantly affected by the presence or absence of short-selling constraints. Second, we provide new insights into the time-varying nature of short selling’s impact on overpricing by employing a mispricing index, which allows us to measure changes in mispricing levels across eight stages of MTSS program expansion over 13 years. Finally, we show that neglecting short-selling regulations can lead to erroneous inferences about the pricing of policy-related uncertainty.

The remainder of the article is organized as follows. Section 2 reviews the relevant literature and develops hypotheses. Section 3 outlines the institutional background. Section 4 describes the data and methodology. Section 5 presents the empirical findings, and Section 6 concludes the article.

2. Literature Review and Hypotheses Development

2.1. Economic Policy Uncertainty and Market Efficiency

EPU plays a critical role in shaping investment decisions, stock returns, and volatility. Baker et al. (2016) construct an aggregate EPU index using newspaper coverage and demonstrate that heightened EPU leads to increased stock price volatility and reduced investment, particularly in policy-sensitive sectors. Subsequent studies corroborate these findings, showing that elevated EPU reduces corporate investment (Gulen & Ion, 2016), curtails corporate risk-taking (Zhang et al., 2021), suppresses credit growth (Bordo et al., 2016), and raises costs of debt (Tran & Phan, 2022). Moreover, EPU is linked to stock price fluctuations in the United States (Pástor & Veronesi, 2012, 2013; Shi & Wang, 2023) and globally (Hong et al., 2024).

Given its significance, accurate measurement of policy uncertainty in China has received considerable attention. Baker et al. (2013, 2016) pioneer this effort by constructing a China EPU index using English-language news reports from the South China Morning Post, a Hong Kong–based newspaper. However, this approach inadvertently introduces cultural and linguistic biases by relying on English-language sources in a predominantly Chinese-language policy environment. To overcome these limitations, Davis et al. (2019) refine the approach by using two widely read Chinese-language newspapers for capturing policy uncertainty discourse more directly. Extending this effort further, Huang and Luk (2020) develop a comprehensive EPU index using data from 10 prominent Chinese-language newspapers to mitigate potential bias by providing broader coverage across different regions and sectors within China. Comparing these indices, Xu et al. (2021) find that Davis et al.’s (2019) EPU index outperforms both Baker et al.’s (2013, 2016) and Huang and Luk’s (2020) indices in forecasting Chinese stock market returns. In our study, we use Davis et al.’s (2019) EPU index as our primary measure of policy uncertainty and Huang and Luk’s (2020) index as an alternative measure for robustness check.

2.2. Short-selling Constraints and the Overpricing Effect

Short selling has significant implications for asset pricing and market efficiency. Miller (1977) argues that restrictions on short selling can lead to overvaluation because pessimistic investors are unable to counter overly optimistic valuations. Short-selling restrictions create conditions that encourage optimists to dominate price formation. While Diamond and Verrecchia (1987) suggest that rational investors adjust their expectations to account for short-selling constraints, empirical evidence overwhelmingly supports Miller’s overvaluation hypothesis. For example, Harrison and Kreps (1978) show that differences in investor opinions, when combined with short-selling constraints, generate a “speculative premium,” pushing stock prices above the most optimistic fundamental valuations. Other empirical studies also support this view, demonstrating that heightened investor disagreement is associated with inflated asset prices and subsequent price reversals (Diether et al., 2002).

International evidence further substantiates these theoretical predictions. For instance, Chang et al. (2007) exploit Hong Kong’s regulatory structure, which restricts short selling to designated stocks, and find that constrained stocks are systematically overvalued relative to unconstrained counterparts. Similarly, Bris et al. (2007), using a global sample of 46 equity markets, show that short-selling bans have a stronger impact on price distortions compared to margin-trading restrictions.

Beyond causing overvaluation, short-selling constraints impede the timely incorporation of information in stock prices. Diamond and Verrecchia (1987) argue that these constraints lead to asymmetric price adjustments, causing negative skewness in stock returns due to delayed assimilation of adverse news. Hong and Stein (2003) contend that short-selling bans could exacerbate return skewness by preventing timely dissemination of negative signals. Empirical evidence corroborates these theoretical insights, with Saffi and Sigurdsson (2011) demonstrating that short-selling constraints weaken price discovery mechanisms across global markets.

2.3. EPU, Short-selling Constraints and Stock Returns: Dual Effects

The interaction between EPU and short-selling constraints generates two competing effects on stock returns. The first is the “overpricing effect,” which is particularly pronounced in markets like China with high a concentration of retail investors (Carpenter et al., 2021) and sensitivity to macro-policy shifts (Tan et al., 2007). Hong and Sraer (2016) theoretically link macroeconomic uncertainty to valuation disagreement, positing that greater uncertainty amplifies differences in investor beliefs. In this setting, stocks with higher sensitivity to aggregate uncertainty become particularly prone to speculative overvaluation. Behavioral finance research provides additional insights into persistence of speculative overpricing when short selling is restricted, as uncertainty amplifies cognitive biases (Hirshleifer, 2001).

The contrasting perspective, “uncertainty aversion effect,” implies that heightened EPU fosters pessimism, leading investors to demand higher returns for elevated uncertainty. Heath and Tversky (1991) link uncertainty aversion to individuals’ perceived competence in evaluating outcomes, while Maenhout (2004) demonstrates that investors facing high uncertainty require a higher equity premium. Anderson et al. (2009) show that securities exhibiting positive correlations with market-wide uncertainty command higher expected returns.

The introduction of short-selling regulations, like China’s MTSS program, affects the balance between these competing effects. When short selling is restricted, the overpricing effect is likely to dominate, leading to a negative relationship between EPU and expected returns (Chen et al., 2017, 2021). Conversely, when short-selling constraints are relaxed, the uncertainty aversion effect prevails as overpricing is reduced through short-selling activities.

Based on these insights, we propose two hypotheses:

H1: Before the introduction of the MTSS program, the Chinese stocks will exhibit a negative association with EPU. H2: After the introduction of the MTSS program, the Chinese stocks will exhibit a positive association with EPU.

3. Institutional Background

3.1. Short Selling in China’s Market

China’s emerging stock market has historically been characterized by weak investor protection, inconsistent law enforcement, and a dominance of retail investors (Allen et al., 2005; Jin & Myers, 2006). 2 Concerned with uninformed trading and market manipulation risks (Pistor, 2005), short selling was prohibited in China. However, in March 2010, the China Securities Regulatory Commission (CSRC) initiated the MTSS program with an aim to improve price discovery, promote market efficiency, and enhance risk management.

The MTSS program began by including 90 constituent stocks from the Shanghai Stock Exchange 50 Index and the Shenzhen Stock Exchange Component Index. To be eligible for short selling, the stocks were required to meet stringent criteria. These included a minimum tradable share count of 200 million, public float exceeding CNY 800 million, and sufficient liquidity. Over the eight major phases between 2010 and 2022, the CSRC expanded the MTSS program (see Table B1 in supplementary material), and by October 2022, there were 2,200 stocks eligible for short selling, representing 44.12% of China’s A-share market.

3.2. Development of Short-selling Activity

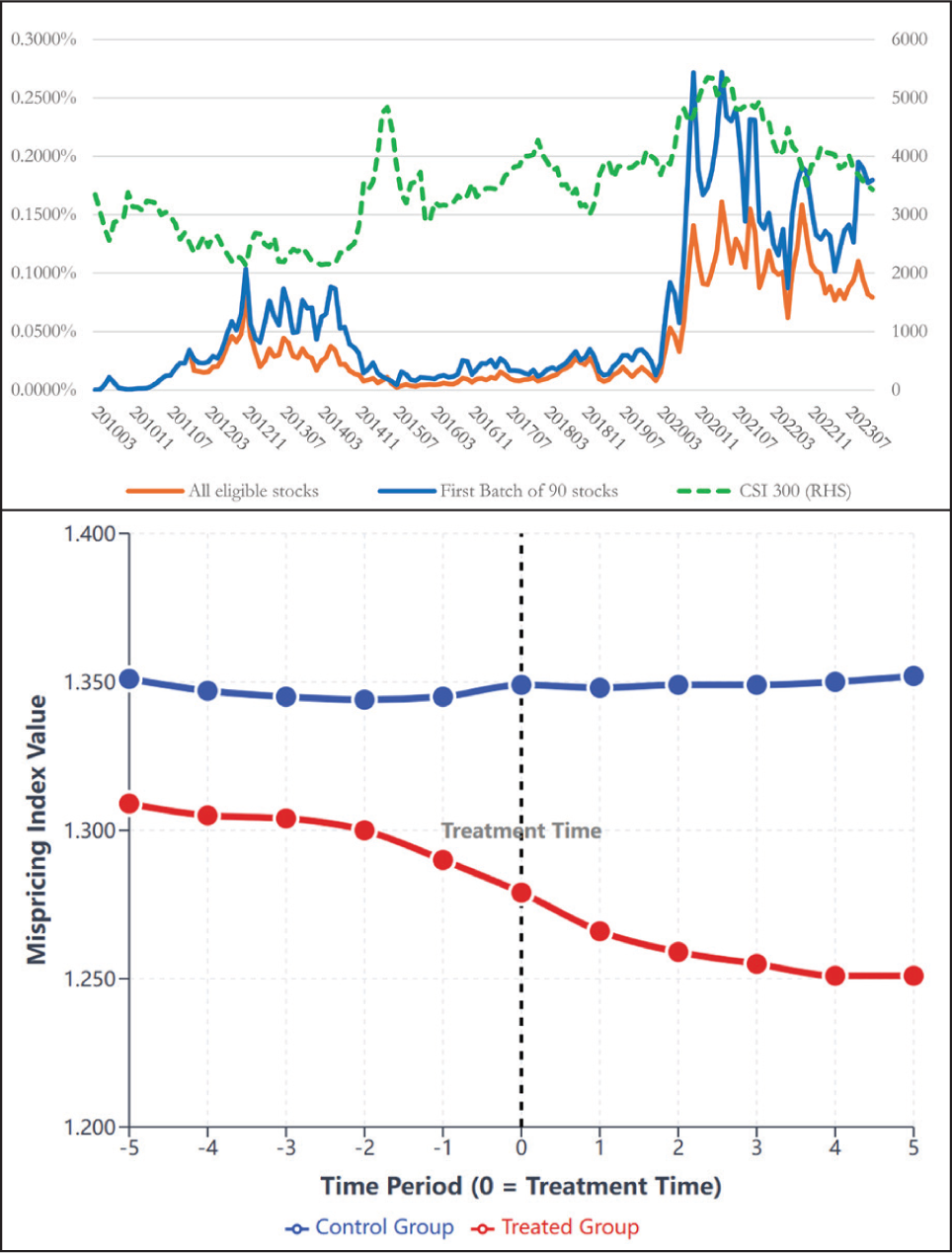

While the introduction of MTSS-regulated stocks represents a structural shift in the Chinese investing landscape, the actual impact on stock prices is dependent on the extent of real short-selling activity. Panel A of Figure 1 plots the CSI 300 index alongside the average short interest of MTSS-eligible stocks from 2010 to 2023, revealing a steady increase in short interest following the implementation of MTSS, with a sharp decline during the 2015 market crash. In response to this crash, regulators prohibited same-day short-covering on August 4, 2015, to discourage short-term arbitrageurs.

A significant development occurred in August 2019 when the MTSS expanded from 950 to 1,600 stocks, marking the largest single increase in the stocks eligible for short selling. Simultaneously, mutual funds were permitted to lend shares to short sellers, giving further boost to short selling. Consequently, average short interest for the initial 90 stocks rose from 0.0275% (2010–2019) to 0.1526% (2020–2023).

Short interest among MTSS-eligible stocks exhibits a marked increase during the first 6 months following program inclusion. Average short interest increased from 0.0041% in the first month to 0.0067% by the sixth month, while the proportion of stocks with short interest grew from 22.26% to approximately 45.57% during this period. 3

3.3. Significance of Low Short-interest Levels

Despite the seemingly low average short interest in our sample (less than 0.30%), we contend that even minimal levels can be significant for three key reasons. First, while short interest in China is lower than global benchmarks, it aligns with the general pattern of low short-interest levels observed internationally. For example, Nasdaq reported median short interest for US mega-cap stocks at merely 0.70% in Q3 2023, 4 while European markets show similar levels (Spain: 0.82%, UK: 0.74%). 5

Second, the predictive power of short selling, rather than its absolute magnitude, carries greater relevance. Kelley and Tetlock (2017) demonstrate that despite median levels of only 0.007%, retail short selling in the United States is able to predict negative returns. Similarly, research in China shows that relaxing short-selling constraints enhances pricing efficiency through rapid information adjustment (Chang et al., 2014; Li et al., 2018). Feng and Chan (2016) report that short sellers significantly adjust positions around earning announcements, suggesting they function as informed, sophisticated traders.

Finally, market participants in China closely monitor short-selling activity as an indicator of investor sentiment. 6 Even at low levels, short interest could constitute a meaningful signal with substantial effects on price discovery and market efficiency.

4. Data and Methodology

4.1. Data Source and Screening

Our sample comprises China A-share listed firms from January 2005 to December 2023. We obtain data from CSMAR and WIND databases. Following Liu et al. (2019), we exclude special treatment stocks and the 30% smallest stocks each month to mitigate the influence of shell stocks. We also exclude stocks with less than 48-month trading records to ensure robustness of EPUB estimation. After screening, our final sample consists of 3,481 unique firms, generating 338,158 stock-month observations.

4.2. Empirical Framework

To investigate the relationship between EPU and expected stock returns, we employ several different approaches.

First, following Bali et al. (2017) and Qian et al. (2025), we estimate uncertainty β (EPUB) using rolling regressions over a 60-month fixed window:

where Reti,t represents the excess return on stock i in month t, βi,tEPU is the uncertainty β for stock i in month t, and MKTt, SMBt, and HMLt are the Fama and French (1993) factors. We calculate excess returns as raw stock returns minus the risk-free rate, proxied by the 1-year CNY fixed deposit rate following Liu et al. (2019). Details of the factor model are provided in Appendix A (Supplementary material).

Second, we examine the cross-sectional relation between uncertainty β and expected returns using Fama and MacBeth (1973) regressions:

Here, Reti,t + 1 represents the 1-month-ahead excess returns for stock i, EPUBi,t denotes uncertainty β, and Control includes a set of firm-specific characteristics observed at time t. Following Qian et al. (2025), we include natural logarithm of market capitalization (SIZE), book-to-market ratio (BM), 11-month momentum returns (MOM), short-term return reversal (REV), asset growth (GROW), leverage ratio (LEV), idiosyncratic volatility (IVOL), and annual share turnover ratio (ASTO) as control variables.

We complement this analysis with portfolio sorts, constructing quintile portfolios based on uncertainty β and estimating α using the Fama and French (1993) three-factor and Carhart (1997) four-factor models. For brevity, we refer to both models as FF3 and FF4, respectively, throughout the article.

Third, to address limitations of cross-sectional analyses and account for the phased implementation of the MTSS program, we employ panel regressions with firm- and time-fixed effects:

where EPUBi,t denotes the uncertainty β for stock i at time t, Control comprises a list of control variables used in Model 2, and FirmFE and TimeFE represent firm- and time-fixed effects.

To capture the effect of short-selling constraints, we extend our baseline model with interaction terms:

where MTSSi,t is a dummy variable indicating MTSS eligibility, and HISIi,t equals 1 if a stock’s short interest exceeds the median short interest of all stocks with outstanding short interest. The interaction terms capture how short-selling constraints affect the uncertainty premium.

5. Empirical Results

5.1. Summary Statistics and Persistence of Uncertainty β

Table B2 (Supplementary material) presents summary statistics, pairwise correlations, and persistence metrics for the uncertainty β (EPUB). Panel A reports descriptive statistics. The mean, median, and interquartile range of EPUB, specifically −0.004 (mean), −0.003 (median), with the 25th and 75th percentiles at −0.034 and 0.028, respectively, suggest an approximately symmetric distribution. The control variables, including SIZE, BM, MOM, REV, GROW, LEV, IVOL, and ASTO, display mean values consistent with the extant literature (e.g., Qian et al., 2025).

Panel B in Table B2 (Supplementary material) shows significant negative correlations between EPUB and SIZE, MOM, GROW, LEV, IVOL, and ASTO (all at the 1% level), implying that high-EPUB stocks are typically smaller, slower-growing and less leveraged and exhibit lower idiosyncratic risk. Conversely, EPUB is positively associated with BM and REV, suggesting that high-EPUB stocks tend to be value-oriented and exhibit short-term momentum.

Panel C evaluates the persistence of EPUB using Fama–MacBeth regressions. Uncertainty β are re-estimated at monthly intervals over forward-looking 5-year windows, both with and without control variables. The results show statistically significant coefficients for horizons up to 4 years (p < .01), supporting the notion that past EPUB serves as a reliable proxy for conditional β and future exposure to policy uncertainty (see Bali et al., 2017).

5.2. Cross-sectional Evidence

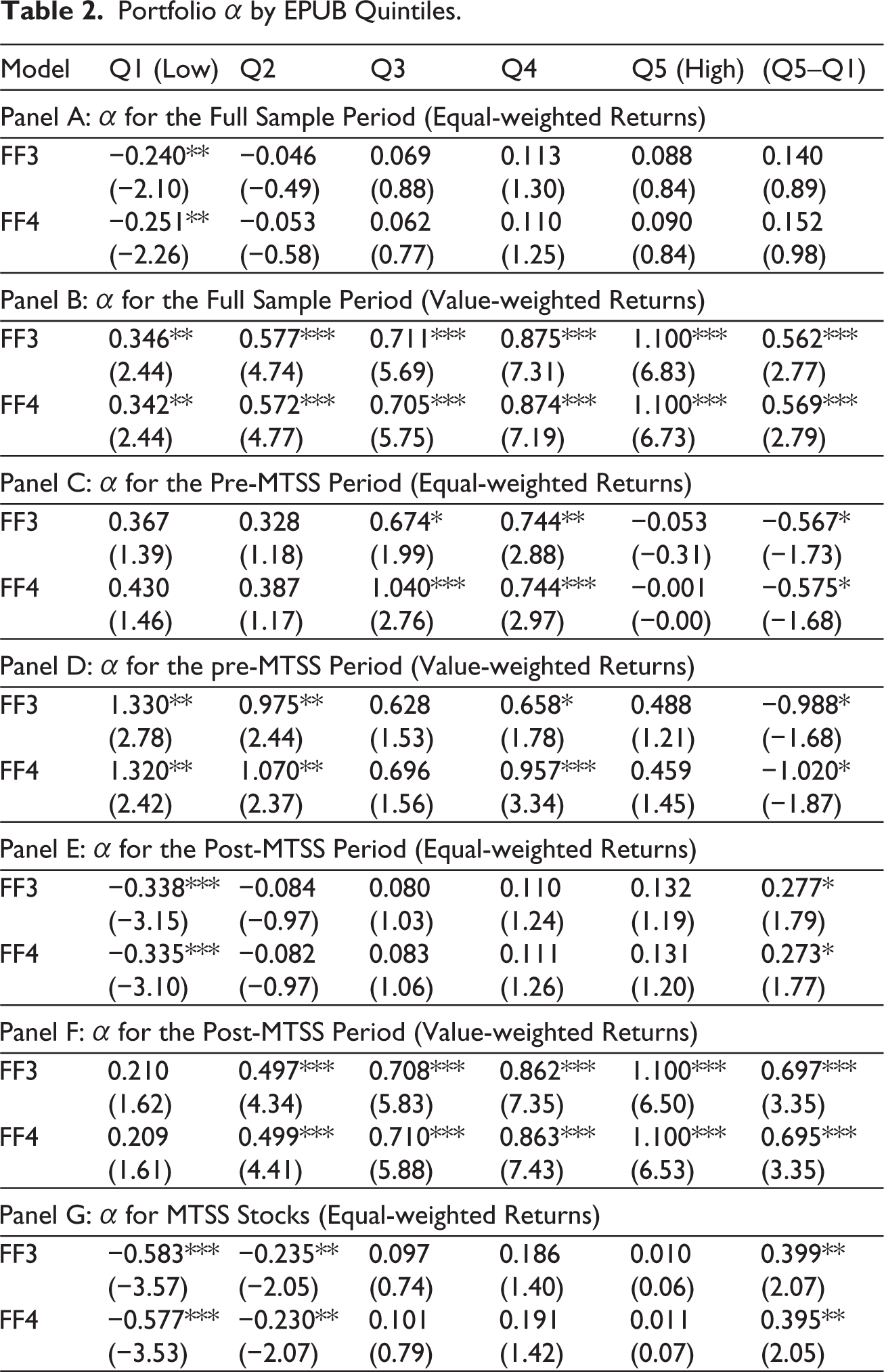

We employ Fama and MacBeth (1973) regressions to examine the relationship between EPUB and expected returns. Table 1 displays the average slope coefficients and Newey–West adjusted t-statistics. Over the full sample (2005–2023), EPUB is significantly and positively associated with future stock returns (slope = 0.016, t-stat = 1.95), indicating a positive uncertainty premium.

Time-series Averages of Slope Coefficients from Fama–Macbeth Cross-sectional Regressions.

This finding contrasts with prior evidence from Chen et al. (2017), which reports a negative association between EPU and returns at the market level. Three factors may account for this discrepancy. First, we exclude shell stocks, which are prone to speculative overpricing, thereby the “uncertainty aversion effect” may dominate (Cai et al., 2023). Second, our analysis is conducted at the firm level, unlike Chen et al.’s (2017) market-level focus. Third, our sample spans a period of gradual relaxation of short-selling constraints.

When we split the sample into pre- and post-MTSS periods, we find contrasting results. In the pre-MTSS era (2005–2010), the EPUB coefficient was negative and marginally significant (slope = −0.011, t-stat = −1.79), supporting the “overpricing effect” hypothesis. In contrast, the post-MTSS period (2010–2023) shows a strong positive relationship (slope = 0.017, t-stat = 2.58), consistent with the “uncertainty aversion effect” as short-selling constraints are eased.

5.3. Portfolio Analysis

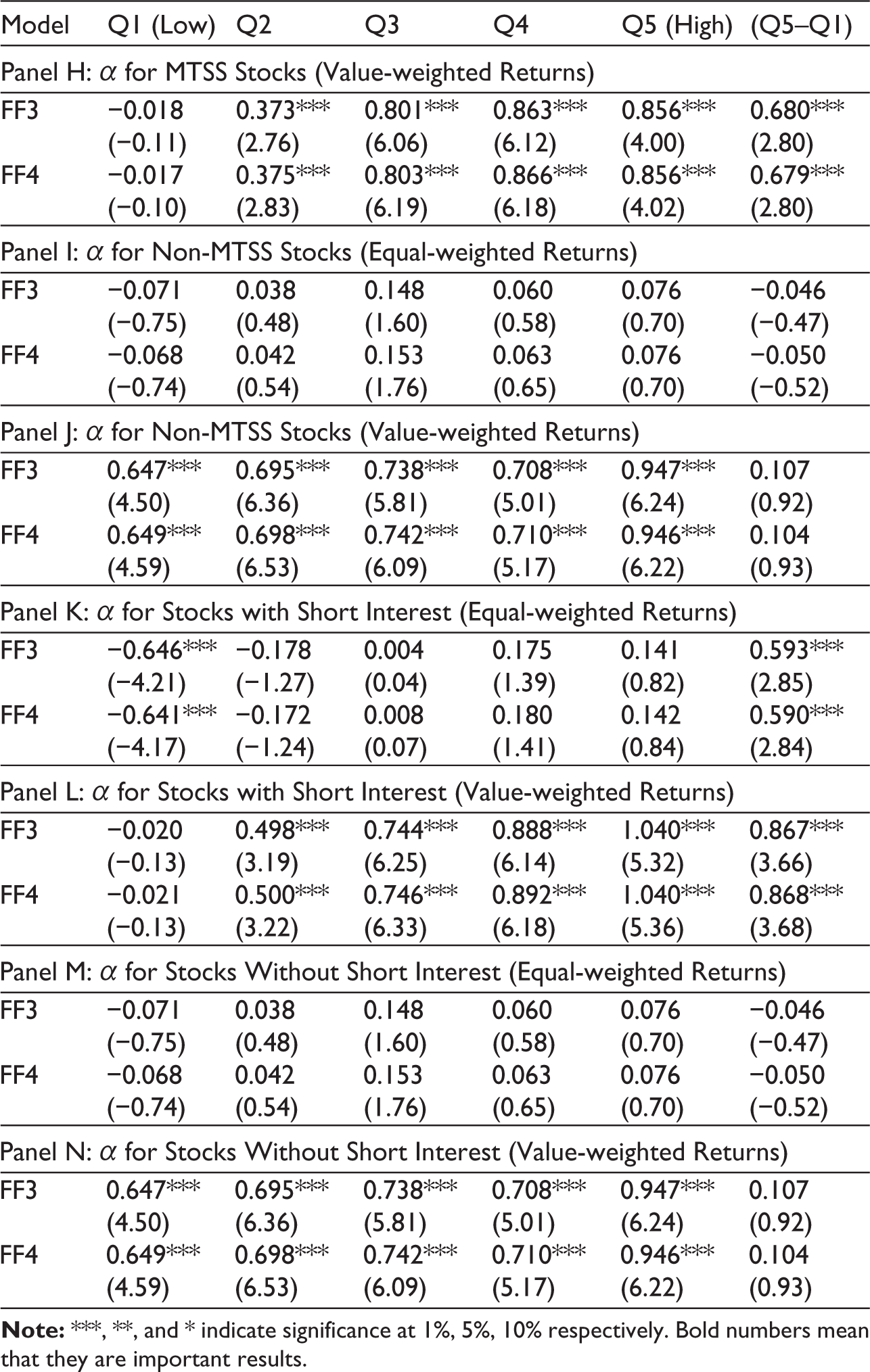

To validate the cross-sectional findings, we implement a portfolio sorting approach. Each month, stocks are sorted into quintiles based on their EPUB values, and subsequent, monthly returns are computed. Panels A–F in Table 2 report the equal- and value-weighted α from the Fama–French three- and four-factor models.

Over the full sample, value-weighted portfolios yield a statistically significant positive α for high-EPUB stocks. The long-short Q5–Q1 portfolio generates an FF3 α of 0.562% (t-stat = 2.73), while the equal-weighted counterpart is positive but insignificant. This asymmetry echoes findings from Phan et al. (2018), who report mixed results for the EPU–return nexus in China.

Disaggregating by regulatory regime, we find strong evidence of regime-dependent pricing. During the pre-MTSS period, equal-weighted long-short portfolios yield a negative and marginally significant α (−0.567%, t-stat = −1.73), in line with the overpricing hypothesis. Conversely, in the post-MTSS period, the long-short value-weighted α rises to 0.695% (t-stat = 3.35) under the FF4 model, affirming that high-uncertainty stocks outperform following the relaxation of short-selling restrictions (Hong et al., 2024).

5.4. Heterogeneity in Short-selling Constraints

The MTSS program’s staggered implementation necessitates a more granular analysis. Post-MTSS, we partition stocks into MTSS-eligible and -ineligible groups. Panels G–N in Table 2 report α for these groups across different portfolio specifications.

Portfolio α by EPUB Quintiles.

Panels G and H show that MTSS-eligible stocks yield significantly positive long-short α (e.g., 0.399%, t-stat = 2.07), whereas Panels I and J reveal no significant return differentials for ineligible stocks. The lack of overpricing among constrained stocks may be explained by the introduction of index futures, which offer an alternative mechanism for shorting of index constituents.

To assess the impact of actual short-selling activity, we reclassify MTSS stocks by short interest. Panels K and L in Table 2 report that stocks with high short interest exhibit a statistically significant EPU premium. In contrast, Panels M and N show that stocks with no short interest show insignificant α. These findings suggest that it is not the mere short-selling eligibility but actual short selling that enables pricing of EPU.

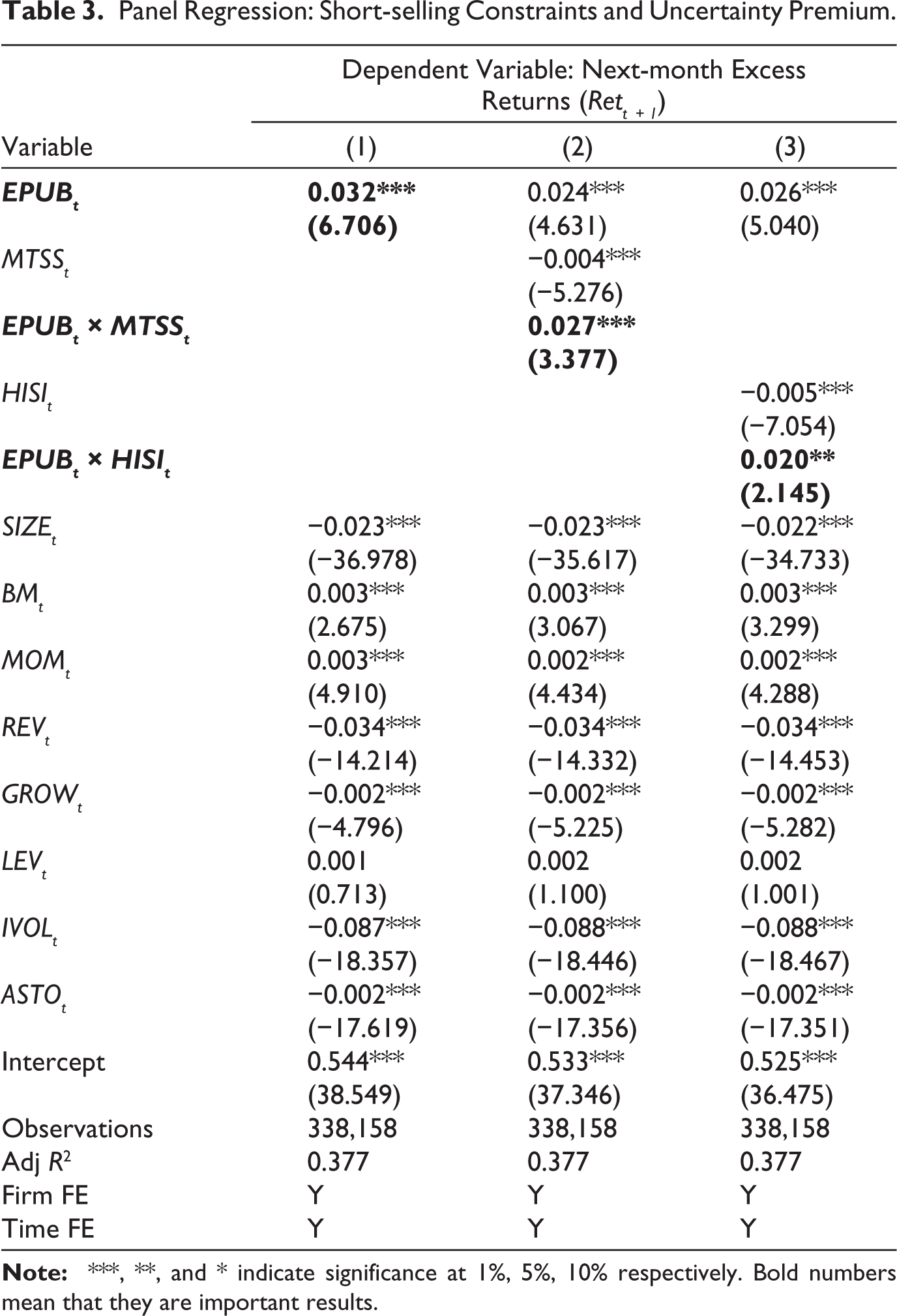

5.5. Panel Regression Analysis

To control for unobservable firm- and time-specific effects, we estimate panel regressions with fixed effects. Table 3 presents the results. In Model 3, EPUB retains a positive and highly significant coefficient (t-stat = 6.706).

Panel Regression: Short-selling Constraints and Uncertainty Premium.

Interaction models further elucidate the key role of short selling. In Model 4, the EPUB × MTSS term is positive and significant (coef. = 0.027, t-stat = 3.377), indicating that MTSS eligibility enhances the positive effect of EPU on returns. Model 5 introduces short interest (HISI) as a proxy for actual short-selling activity, and again, the interaction term is positive and significant (coef. = 0.020, t-stat = 2.145). These findings corroborate the view that short-selling constraints mediate the sign and magnitude of the uncertainty premium (Cai et al., 2024).

5.6. Propensity Score Matching and Difference-in-differences

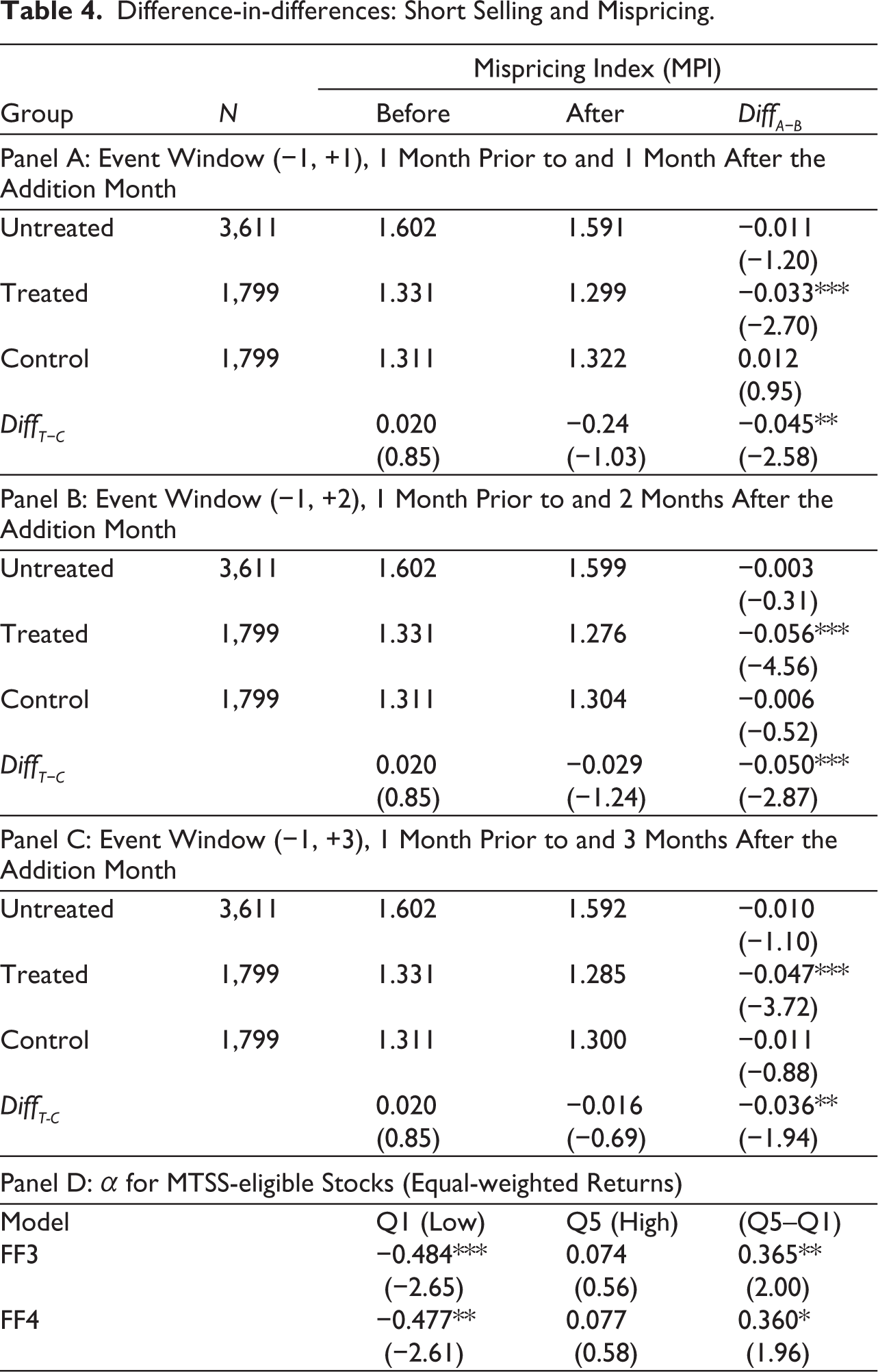

Since selection of stocks in the MTSS program may not be random, we implement PSM to create a control group of non-eligible firms matched on SIZE, ASTO, and EPUB characteristics. Using a 0.25 caliper and nearest-neighbor algorithm, we obtain 1,799 matched pairs. Table B3 (Supplementary material) reports the details of the selection procedure.

Post-matching diagnostics (Panel C in Table B3), supplementary material confirm the balance between treated and control groups. We then conduct a DiD analysis using the mispricing index (MPI) from Shi et al. (2023). Consistent with the expected improvement in pricing efficiency post-MTSS, results in Panels A–C of Table 4 show significant reductions in MPI for MTSS-treated stocks across event windows, with the largest decline observed in the (−1, +1) window (DiffT−C = −0.045, t-stat = −2.58) (Chang et al., 2014; Li et al., 2018).

Difference-in-differences: Short Selling and Mispricing.

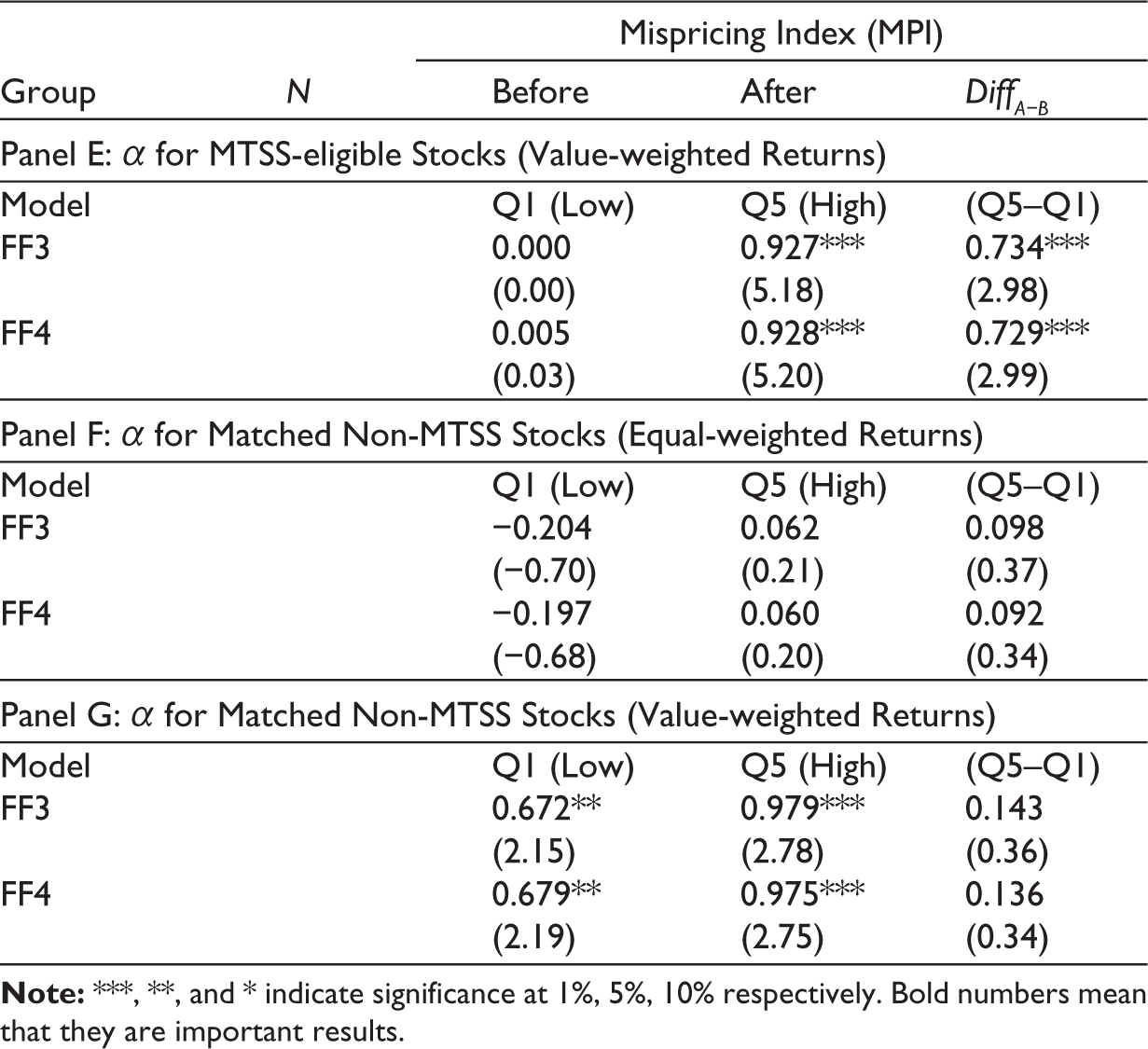

Finally, Panels D–G of Table 4 compare long-short portfolio α across treated and control stocks. MTSS-treated firms show significantly positive FF3 α of 0.365% (t-stat = 2.00) for equal-weighted and 0.734% (t-stat = 2.98) for value-weighted portfolios. Control stocks exhibit lack of significant α, supporting the argument that EPU premium occurs when short-selling constraints are lifted.

The validity of our DID estimation requires that treatment and control groups follow similar pre-treatment trajectories (Angrist & Pischke, 2008). We test this assumption by examining mispricing indices for treatment (MTSS) and control (non-MTSS) stocks over 5 months before MTSS inclusion. 7 Panel B in Figure 1 displays the parallel trend test results. Pre-treatment slopes are −0.0015 for the control group and −0.0043 for the treatment group, with a statistically insignificant difference of −0.0028 (t-statistic = −0.075). The results confirm that the parallel trends hold.

5.7. Mechanism Analyses and Robustness Checks

We undertake several validation analyses and robustness checks to confirm our main findings (Appendix C; supplemenarty material). First, we address potential concerns related to the media censorship and confounding effects from financial crises (Sections C.1.1 and C.1.2). Next, we examine the role of short-selling activity intensity and the persistence of uncertainty shocks in shaping return responses (Section C.2). Finally, we analyze cross-sectional heterogeneity across state ownership, analyst coverage, and regulatory stringency to assess how institutional and informational environments condition the uncertainty–return relation (Section C.3).

We also conduct a set of robustness checks to further validate the uncertainty premium. Specifically, we test sensitivity to alternative specifications, including an alternative China EPU proxy employing commercial sources (Section C.4.1), an alternative proxy for short-selling constraints (Section C.4.2), and an alternative portfolio formation method (Section C.4.3). Across all exercises, the results remain consistent with our baseline findings, confirming the reliability of our main conclusions. Collectively, these tests strengthen the robustness, causal interpretation, and external validity of our results.

6. Conclusions

This study investigates the moderating role of short-selling constraints on the relationship between EPU and expected stock returns in China. Utilizing China’s unique regulatory environment, we explore how economic policy uncertainty is priced under varying short-selling conditions.

Our findings indicate that the impact of EPU on expected stock returns is significantly influenced by the presence or absence of short-selling constraints. Consistent with the “overpricing effect” hypothesis, we observe a negative association between EPU and stock returns before the introduction of the MTSS program in March 2010. Post-MTSS implementation, the relationship reverses, aligning with the “uncertainty aversion effect” hypothesis, implying that when short selling is permitted, investors demand higher risk premiums for bearing heightened uncertainty.

Employing firm-level EPU exposure and proxies for short-selling constraints, including MTSS eligibility and short interest, our analysis provides robust evidence on the role of short-selling constraints in the pricing of uncertainty in Chinese emerging stock markets. These findings underscore the importance of short selling for reducing mispricing and enhancing market efficiency.

From a policy perspective, our results support market-oriented regulatory frameworks that enhance short-selling accessibility for improving allocative efficiency. Specifically, we recommend a phased liberalization approach that gradually expands MTSS eligibility using transparent and predictable criteria. Such measured expansion would allow markets to absorb uncertainty shocks more smoothly while maintaining orderly price formation. This approach is particularly relevant for emerging markets seeking to balance financial stability concerns with the efficiency gains.

While our findings provide valuable insights into the role of short selling in pricing of EPU in China, we acknowledge that the evidence may have limited generalizability. Our analysis focuses on China’s unique institutional settings, which may differ from other emerging markets and developed markets. However, our study creates scope for future research that could refer to our findings to compare and/or generalize the evidence by examining similar dynamics across different markets.

Supplemental Material

Supplemental material for this article is available online.

Footnotes

Author Contribution

Binsheng Qian: Conceptualization, data curation, methodology, software, writing—Original draft preparation, writing—Reviewing and editing.

Sunil Poshakwale: Methodology, investigation, validation, writing—Reviewing and editing.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Declaration of the Use of Generative AI

The authors have not used generative AI or AI-assisted technologies in the writing process before submission.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.