Abstract

This research examines whether Chief Finance Officer (CFO) demographics (including age, educational background, gender and tenure) impact firm working capital policies. We argue that the personal characteristics of the CFO impact corporate financial policy, such as working capital management. Using a sample of listed companies in the China Stock market over 2000–2021, we find that CFO age, gender, education, and tenure determine firm working capital management. Further, we identified that findings are more pronounced within firms that do not have state ownership, suggesting that private ownership firms are likely to have aggressive working capital management. In terms of economic significance, our results demonstrated that a one-standard-deviation rise in CFO age is associated with a decrease in working capital of 1.09% to 1.39% for the sample firms. This implies that the effect of CFO age on working capital management is economically significant, implying that it considerably impacts the financial situation.

Keywords

1. Introduction

We examine whether Chief Finance Officer (CFO) demographics (including age, educational background, gender, and tenure) affect firm working capital management (WCM). A CFO is critical for formulating and communicating financial strategies with external stakeholders (Mian, 2001). As financial strategy becomes more critical to overall corporate success, the role of CFO has also gained greater endorsement (Gore et al., 2011). Extant research suggests that WCM affects operating performance and firm value (Burney et al., 2021), especially regarding productivity, cost control, firm performance, and the continuity of corporate business activities (Singh & Kumar, 2014). WCM aims at maximizing profits while simultaneously minimizing the risk of incapability of satisfying the maturing short-term debt. Considering the importance of WCM in a firm’s daily operations and long-term value, we conjecture that CFOs should have strong incentives to plan WCM policies. Moreover, many companies have regarded the CFO as the core of their value creation (Higgins & Gulati, 2006).

Our research extends the findings of Adhikari et al. (2021) and Burney et al. (2021). Burney et al. (2021) evidenced that younger CEOs implement more aggressive WCM policies. The CEO and CFO are the two most critical corporate roles (Arthaud-Day et al., 2006); CEO risk appetite affects leverage and cash holding policies, but CFO risk appetite is relatively more important in explaining debt maturity structure and accrual decisions (Chava, 2010). Although the CEO has a notable degree of influence on corporate decision-making, the CFO could also obviously influence the firm’s decision-making through accounting and financing decisions and their own decision-making experience (Dechow et al., 2010). We suggest that the responsibility of the CFO is more critical in budgeting, forecasting, and safeguarding firm stability. The CFO is responsible for establishing and implementing the company’s financial strategy, which includes WCM. The CFO ensures that the firm has the resources to meet its short-term responsibilities while capitalizing on growth prospects. In addition, the CFO oversees managing the firm capital and ensuring that it is invested wisely to maximize profits and reduce risk. WCM is integral to cash management, and the CFO is responsible for managing the company’s working capital.

Six et al. (2013) studied 319 CEOs and 134 CFOs of 110 German companies and found that CFOs’ impact on the firm accounting and finance policy is more profound than that of the CEO. Since CFOs are the top managers directly involved in corporate financial management policies, using CFOs as the research subject can more directly illustrate the relationship between their leadership attributes and company-level decisions. Menz (2012) indicated that the CFO needs more attention as a back-office financial supervisor or controller and emphasized that a CFO should pay close attention to WCM policies. WCM is strongly related to short-term financing decisions, so for WCM policies, the CFO is more worthy of being studied than the CEO. Following the upper echelons theory, we argue that the personal characteristics of the CFO influence the corporate decision-making process (Adhikari et al., 2021; Bertrand & Schoar, 2003; Huang & Kisgen, 2012; Serfling, 2014; Yim, 2013).

We use a unique setting, Chinese listed companies, to investigate our research questions. Compared to other Anglo-American countries, China is characterized by a lack of traditional corporate governance mechanisms. Also, the Chinese market as an emerging market is quite different from that of a developed market (Chan & Kwok, 2005). The importance of WCM has grown increasingly significant in China in recent years, owing to the country’s fast economic expansion and increased competitiveness of its firms. In China, WCM is especially important for emerging enterprises with small-scale, limited access to finance and heavily depends on internal financing, trade credit, and short-term loans to maintain accounts receivable and inventory turnover (Chittenden et al., 1998; Lin & Wang, 2021). Also, state-owned enterprises (SOEs) in China may have different WCM strategies and goals than privately held corporations. Firms operating in highly competitive industries may be mainly focused on maximizing their liquidity to adapt to changing market conditions.

Based on a sample of 25,815 firm-year observations listed in the Chinese Stock market between 2000 and 2021, we find that CFO demographic attributes, such as CFO age, determine corporate working capital policies. Our findings suggest that firms with older, longer tenure and higher academic qualification of CFOs are more likely to initiate aggressive WCM policy. Also, we find that CFO gender is positively associated with WCM policy indicating that female CFOs are more conservative on holding higher working capital. Our findings are more pronounced within the group of firms that have non-state ownership. Finally, we perform Heckman’s (1979) selection bias and find our reported results are robust. In terms of the economic significance of our findings, a one-standard-deviation increase in CFO age is associated with a 1.09% to 1.39% decrease in working capital to the mean for the sample firms indicating the CFO age effect on WCM policy is economically significant. Overall, our findings suggest that older CFOs in China are more aggressive in maintaining working capital. Furthermore, female CFOs with higher academic qualifications are more inclined to use conservative WCM strategies.

Our research has several contributions. Our study focuses on the specific context of China, where institutional factors and cultural dynamics may shape firm capital management policies differently, compared to other countries. We provide nuanced insights into the interplay between CFO demographics and WCM policies. Further, our research contributes to the growing literature on the importance of CFO demographics in shaping financial policies. We evidence the influence of CFO age, tenure, gender, and education on firm WCM. Policymakers, investors, and professionals can benefit from our findings by recognizing the importance of CFO demographics to design effective regulatory guidelines and investment decisions. Overall, this study adds to our knowledge of the importance of personal characteristics in creating corporate financial policies by bringing additional and significant insights into the influence of CFO demographics on WCM in China.

The rest of the paper is organized as follows. Section 2 discusses the existing research and hypothesis. Section 3 describes the research methodology. Section 4 reports the results and several robustness tests. Finally, Section 5 concludes the paper.

2. Literature Review and Hypothesis

According to the Upper Echelons theory, corporate executives will make different decisions because of having distinct experiences, values, and personalities (Hambrick, 2007). These choices will have an even greater impact on the corporation’s performance and strategic decisions (Carpenter et al., 2004; Hambrick, 2007). Research in management, psychology, and behavioral economics demonstrates notable differences based on demographics (such as work experience, age, and education) in various areas, including decision-making, leadership style, communication skills, conservatism, and risk aversion (Daboub et al., 1995). Neoclassical economic theory argues that managerial demographics will not impact a company’s decision-making (Bertrand & Schoar, 2003). However, agency theory, grounded in neo-classical economics, asserts that the demographics of executives (e.g., CEOs) influence firms’ decision-making processes (Bamber et al., 2010).

The demographics of CFOs are frequently employed as indicators of their managerial cognition and values (Sun et al., 2017). Age is a notable attribute that is an indication of a person’s experience and an internal motivator that influences behavioral decision-making (Dorcas et al., 2021). Older managers are more inclined to use conservative policies when making decisions (Hambrick & Mason, 1984). Adhikari et al. (2021) evidenced that older executives exhibit a greater inclination to invest in working capital. Conversely, Burney et al. (2021) found that younger CEOs are more likely to employ aggressive WCM strategies involving higher trade credit financing and lower inventory levels. The likelihood is that individuals will pursue performance improvement through innovative tactics as they become older since they are more likely to pick risk-averse strategies (Serfling, 2014).

Empirical research suggests a CFO’s age affects firm policy outcomes. Older CFOs have more expertise in boosting firm performance (McClelland et al., 2012). CFOs influence corporate policy choices and accounting judgments, such as accounting practices and earnings management (Chava & Purnanandam, 2010; Dechow et al., 2010).

2.1. CFO Age and Working Capital Management

Adhikari et al. (2021) found executive age affects firm WCM policies. Typically, the longer and older the CFO has been in the industry, the more extensive their job history is, and the more strongly their career worries affect their decision-making. Negotiations with stakeholders in the capital market on a regular basis may help corporate executives establish their reputations for future employment (Pae, 2016). According to upper echelons theory, individual traits, like age, may have an influence on corporate performance and strategy choice (Garcia-Appendini & Montoriol-Garriga, 2013). Younger CFOs are, therefore, more inclined to work to establish their reputations to maintain their current employment and gain possibilities in the future. Alternatively, younger CFOs are more likely to decide against investing in high-risk, creative projects to prevent being labelled as disadvantageous by the labor market (Zwiebel, 1995). Older CFOs have more experience and may adopt a more cautious approach to WCM to reduce financial risk and promote financial stability. As a result, senior CFOs may favor short-term cash preservation above long-term development potential, resulting in lower amounts of working capital. Younger CFOs may be more prepared to take risks and engage in growth prospects, resulting in larger levels of working capital. They may also take a more creative approach to WCM, optimizing cash flows and utilizing innovation to increase efficiency. Therefore, we hypothesize as follows:

H1: CFO age affects firm working capital policy.

2.2. Female CFO and Working Capital Management

Female executives have been found to possess less risky assets overall than male executives and to have less risky investment portfolios (Francis et al., 2013; Schopohl et al., 2021). Furthermore, firms with female CFOs undertake less risk when conducting business operations (Schopohl et al., 2021) and they are also more cautious when it comes to financial reporting (Barua et al., 2010), which lowers the chance of financial reporting errors (Gupta et al., 2020). Additionally, it has been seen that female CEOs attend more board meetings, enable effective board monitoring, and guarantee the efficient use of resources (Adams & Ferreira, 2009; Garcia-Lara et al., 2017). Therefore, female CFOs are more likely to adopt a conservative WCM approach than male CFOs. Considering the scenario above, we hypothesize as follows:

H2: CFO gender diversity affects firm working capital policy.

2.3. CFO Educational Background and Working Capital Management

Higher academic achievement among executives is favorably associated with cognitive skills (Finkelstein & Hambrick, 1996) and more educated executives are better equipped to come up with creative, innovative solutions to issues (Bantel & Jackson, 1989). Education can assist in gaining understanding, thinking more critically, and broadening personal perspectives. Overall, a CFO’s values, skills, and insights vary depending on their level of education. We argue that CFOs with a higher educational background are more likely to understand major contributing factors and techniques that may be utilized to manage working capital efficiently. Considering the scenario above, we hypothesize as follows:

H3: CFO educational background affects firm working capital policy.

2.4. CFO Tenure and Working Capital Management

CFOs with a longer tenure better understand the firm’s financial condition and history and are more likely to take a conservative approach to WCM to keep the company’s financial position stable and lower risk. CFOs with shorter tenure may be more prone to adopt a more aggressive approach to WCM to have a positive influence on the firm’s profitability first since they are eager to positively affect the company’s finances. Therefore, we develop the following hypothesis:

H4: CFO tenure affects firm working capital policy.

3. Research Methodology

3.1. Sample Selection Criteria

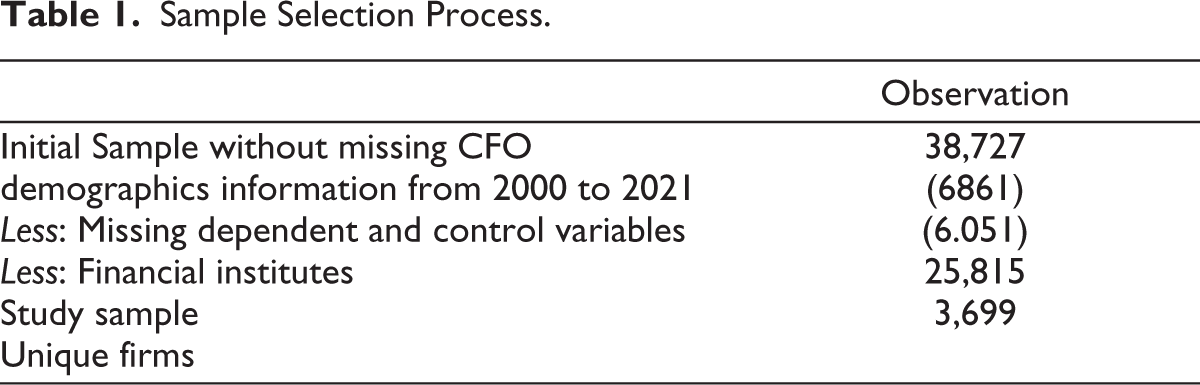

Our initial sample consists of all the listed firms in the China Stock Market & Accounting Database (CSMAR). We start with an initial sample of 38,727 firm-year observations without missing CFO demographics information from 2000 to 2021. Our primary sample consists of non-financial companies listed and traded on the Shanghai and Shenzhen stock exchanges. We exclude firm-year observations with missing values. We also exclude financial companies from this sample because of the working capital policy differences. Our final sample consists of 25,815 firm-year observations of 3,699 unique firms. To minimize the adverse effects of potential outliers, this study winsorised the top and bottom 1% of samples for all continuous variables (Aktas, 2015). Table 1 shows the sample selection process.

Sample Selection Process.

3.2. Research Model

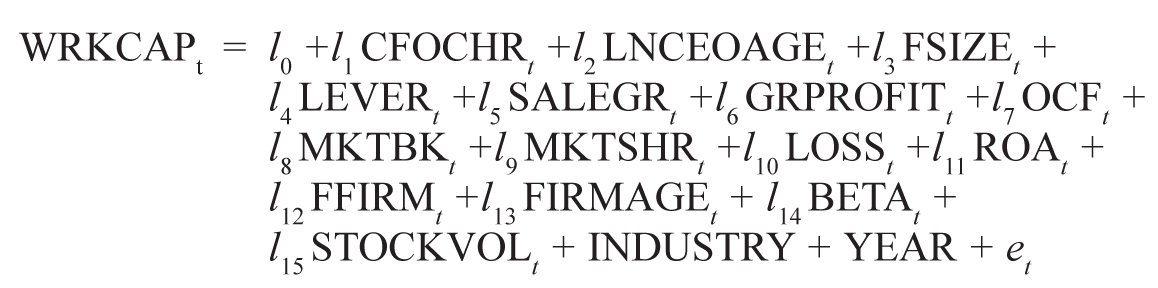

We develop the following ordinary least square (OLS) regression model to address our research question.

We define WRKCAP as the sum of accounts receivable, inventory, and cash or equivalent minus accounts payable and accrued expenses scaled by total assets. A positive WRKCAP means that firms need to obtain additional capital through financing. Conversely, a negative WRKCAP indicates that the corporation uses working capital to finance long-term assets. In other words, the higher value of WRKCAP corresponds to the more conservative WCM policy adopted by the firm and vice versa. To test our hypothesis, we include CFO demographic characteristics (CFOCHR) as an independent variable including CFO age, education (CFOEDUCAT), gender (CFOGENDER), and tenure (CFOTENURE). We use two different proxies for CFO age; LNCFOAGE is a natural logarithm of CFO age, and CFO_ABVAVG is a dummy variable of CFO age assigned a value of 1 when CFO age is above the average and 0 otherwise. CFOEDUCAT refers to the CFO’s educational background (Ph.D., MBA/Masters, Bachelor, etc.), the higher the levels of CFO’s education, the higher the value of the proxy. CFOGENDER is a dummy variable of 1 when the CFO is a female and 0 otherwise. Finally, LNCFOTENURE is the natural logarithm of the length of CFO tenure.

Firm size (FSIZE) is measured as the natural logarithm of the total assets. Large companies with greater negotiating power have more accounts payable, fewer accounts receivable, and less inventory, leading to lower working capital (Yasuda, 2004). Financial leverage (LEVER) is measured by total debt to total assets (Ozkan & Ozkan, 2004). For firms with low financial leverage, the firm’s value will increase with the increase in financial leverage (DeAngelo, 1980). Firms optimize their inventory policies and adjust credit management based on fluctuations in sales growth rates (Deloof, 2003); therefore, we control firm sales growth (SALEGR). Gross Profit Margin (GRPROFIT) is defined as sales minus the cost of goods sold, divided by sales. Studies have shown a positive correlation between gross profit margin and working capital level (Burney et al., 2021). We control firm operating cash flow (OCF), as firms tend to adjust their financing and operating activities depending on the availability of working capital (Long, 1993). A firm with more market dominance in the industry could obtain better trade credit policies and affect the working capital level (Molina, 2009). Therefore, we control market share (MKTSHR) and firm growth (MKTBK). We control firm profitability (LOSS), as firms experiencing negative earnings are likely to develop stricter WCM. Following Ren (2019), return on asset (ROA) is an essential indicator of firm performance and is defined as net income divided by the total asset. Research has shown that family firms avoid risk-taking financial policies and exhibit conservative short-term investment policies by investing more in working capital (Sah et al., 2022). We control the family firms (FFIRM). Following Nguyen et al. (2020), we control the firm age (FIRMAGE). Previous studies have shown that firm risk could also influence a firm’s WCM, so we control the Beta coefficient (BETA) and Stock volatility (STOCKVOL) (Moonis & Shah, 2003; Santos & Winton, 2008). Following Burney et al. (2021), we control CEO age (LNCEOAGE) because the CEO is likely to be engaged actively in WCM. We control for industry and year effects in our OLS regression models.

4. Main Results

This section presents the findings of our research question. We conduct descriptive, univariate, correlation analysis, and multivariate regression.

4.1. Descriptive Statistics

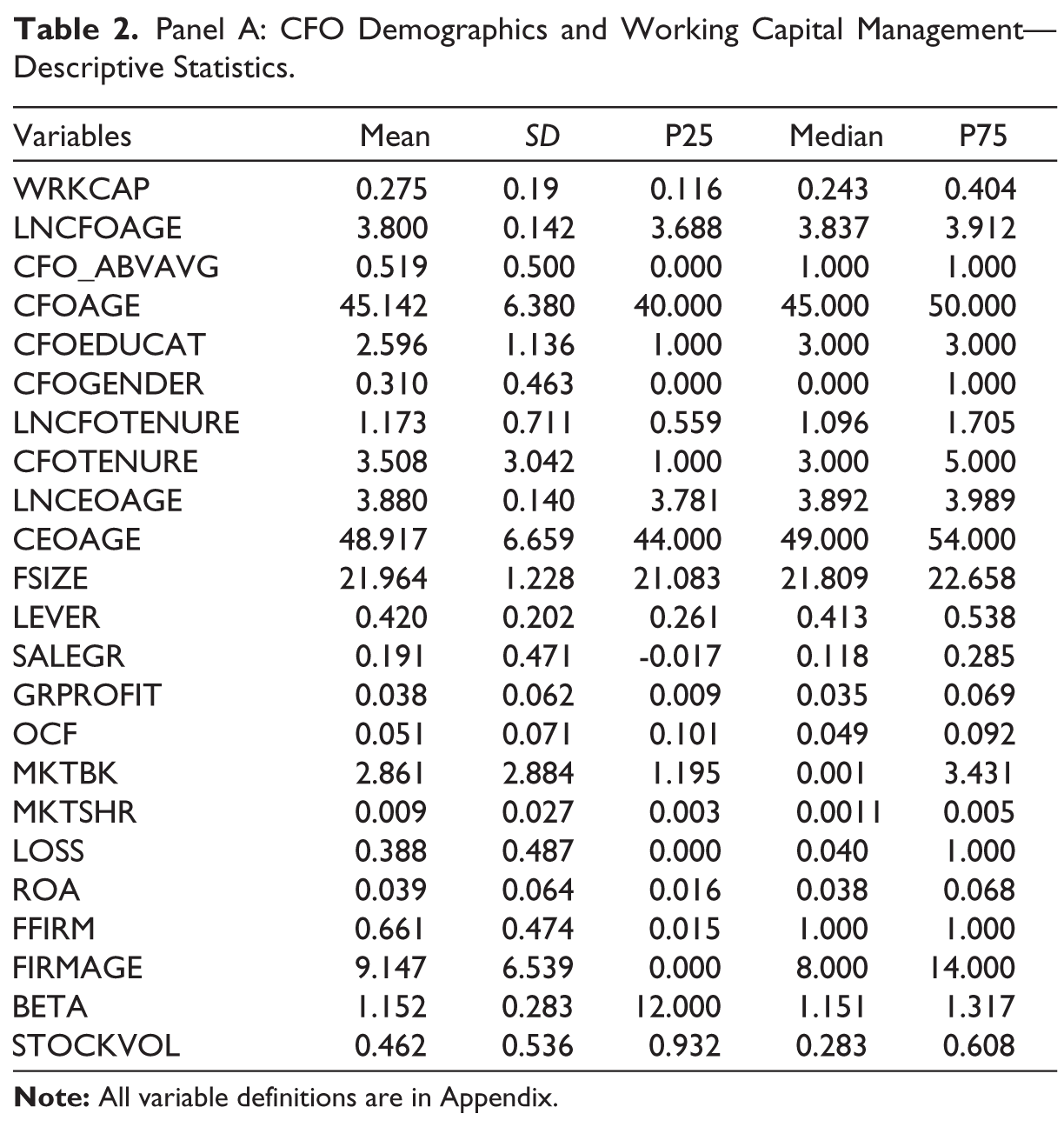

Table 2 reports the descriptive statistics of all the variables included in our regression model. The mean working capital (WRKCAP) of our sample firm is 0.275 indicating that approximately 27.5 per cent of total assets are occupied as working capital. The CFO’s average age is about 45.142 years, and 51.9% of our sample firms’ CFO age is above average. A total of 31% of firm-year observations have female CFOs. The average tenure of a CFO is 3.508 years. Firms have average leverage of 42 per cent of total assets. On average, 38.8 per cent of sample firms has negative profit, and 35.5 per cent of firms are state-owned enterprise. This result is comparable to previous studies such as Ren et al. (2019).

Panel A: CFO Demographics and Working Capital Management––Descriptive Statistics.

4.2. Mean Difference Test

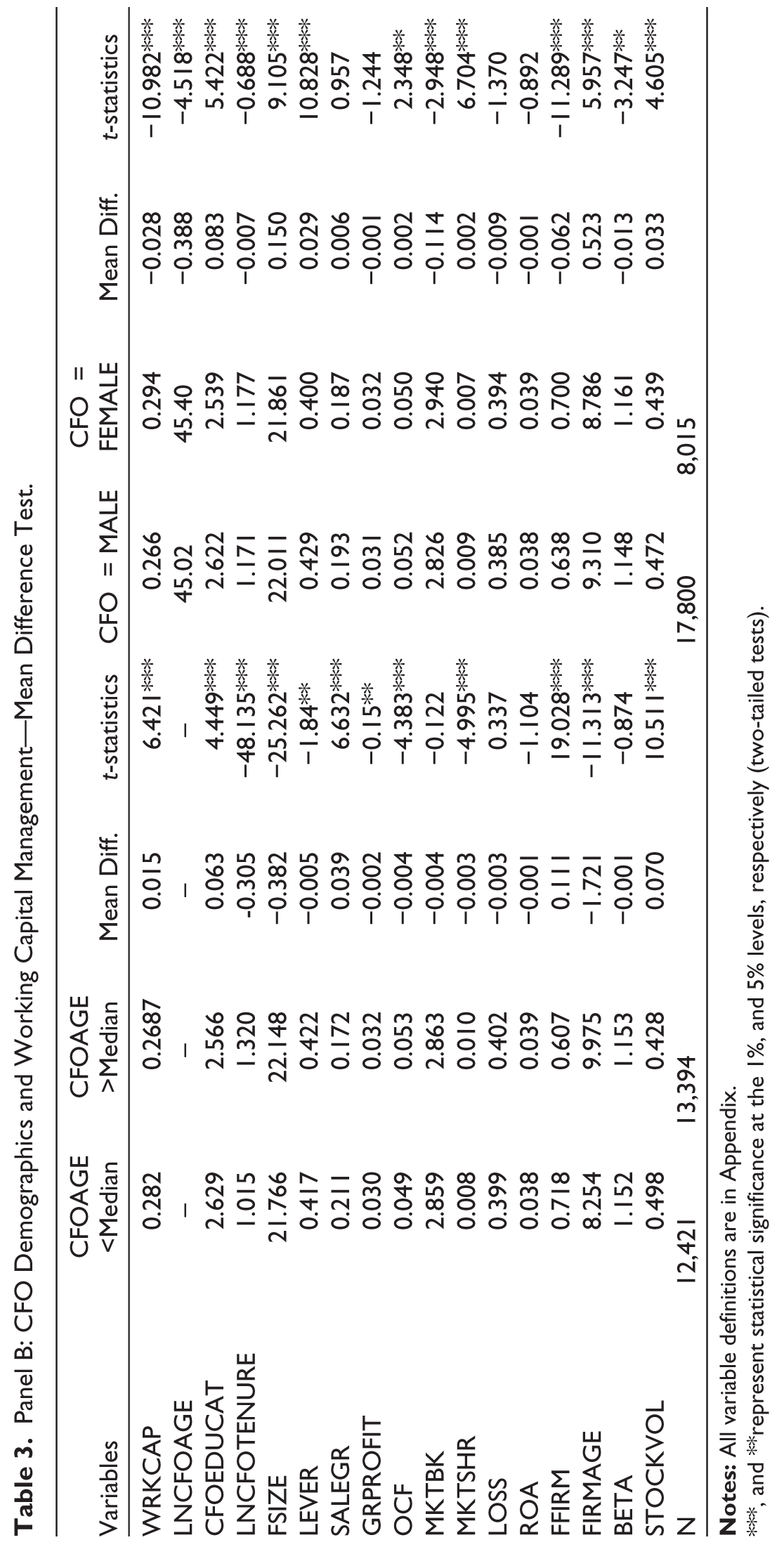

Table 3 reports the mean difference tests of all the variables. We use two different contexts to conduct the mean difference tests. First, the CFO age (CFOAGE) is above and below the median. Second, we compared the mean difference of our variables between CFO gender, such as male vs female. Working capital (WRKCAP) is higher for firms operated by younger CFOs (CFOAGE< = MEDIAN). Also, younger CFOs mainly work in smaller firms (FSIZE) and have lower leverage (LEVER) and higher sales growth (SALEGR). Furthermore, firms with female CFOs hold higher working capital, suggesting CFOs’ age and gender diversity affect a firm’s WCM policies.

Panel B: CFO Demographics and Working Capital Management––Mean Difference Test.

***, and **represent statistical significance at the 1%, and 5% levels, respectively (two-tailed tests).

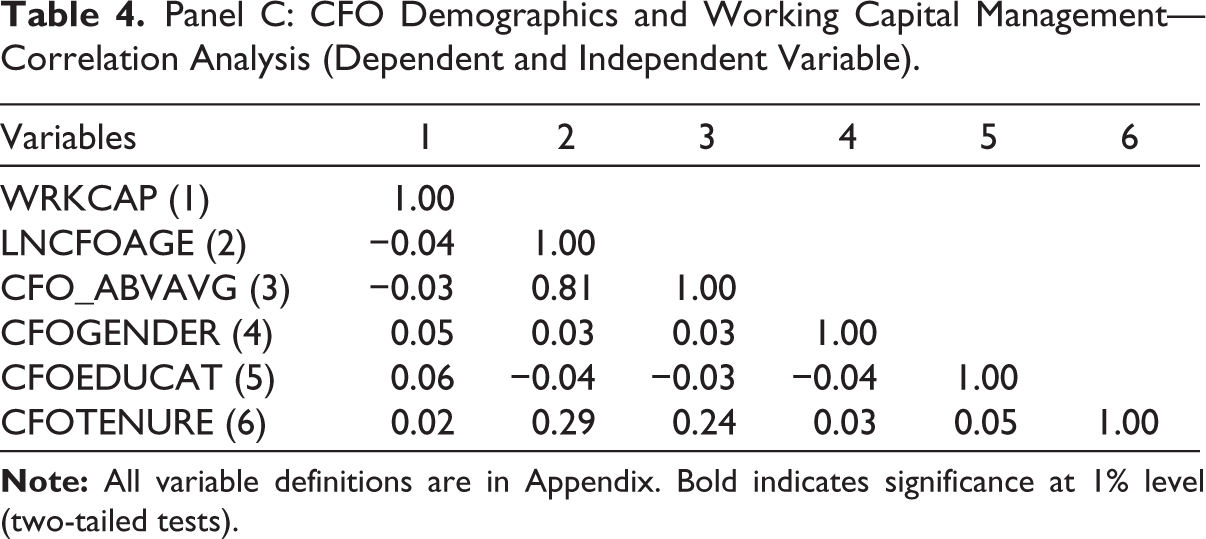

4.3. Correlation Analysis

Table 4 reports the correlation analysis for all the dependent and independent variables used in our regression analysis. We find that firm working capital (WRKCAP) and variables relating to CFO age attributes (LNCFOAGE and CFO_ABVAVG) are negatively correlated, suggesting firm working capital is lower when a CFO age is higher than average. Also, firms choose a higher working capital approach in the presence of a CFO with a higher education degree or female gender. About the other variables (untabulated for the sake of brevity), firm leverage and working capital policy show a negative and statistically significant relationship (correlation = −0.47***, p < .01), indicating that firms maintain higher working capital in a low-leverage capital structure. We find that the firm with a lower market share (MKTSHR) holds more working capital. A firm that has a higher profit margin (GRPROFIT), better profitability (LOSS), holds higher working capital.

Panel C: CFO Demographics and Working Capital Management––Correlation Analysis (Dependent and Independent Variable).

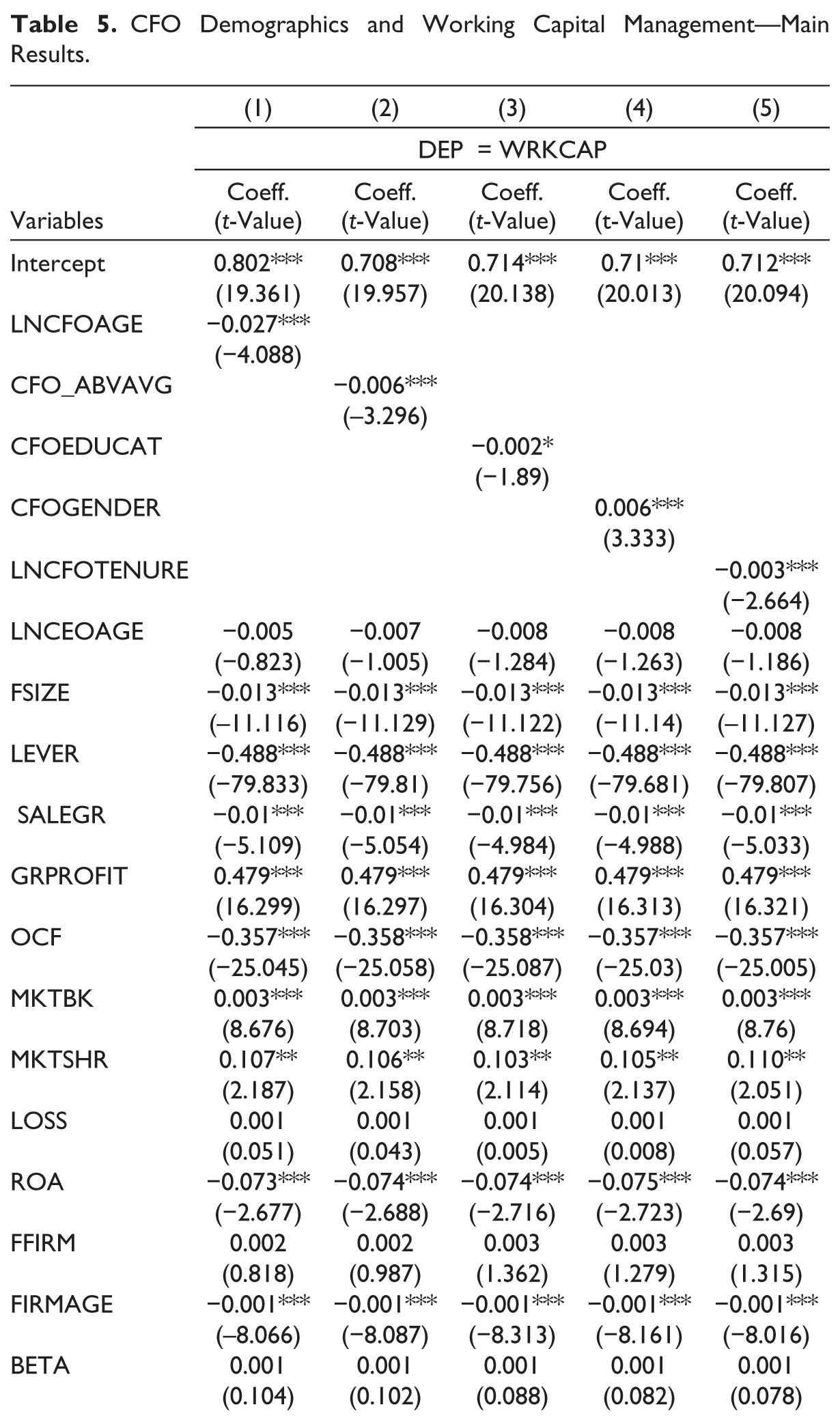

4.4. Regression Analysis

Table 5 reports the results of multivariate regression, which address our main research questions. To test the impact of CFO demographic attributes on WCM, we include CFO age (LNCFOAGE and CFO_ABVAVG), CFOGENDER, CFOEDUCAT, and LNCFOTENURE. In Columns (1) and (2), we include LNCFOAGE and CFO_ABVAVG to examine the impact of CFO age. Both LNCFOAGE and CFO_ABVAVG show a negative association (coefficient =

CFO Demographics and Working Capital Management––Main Results.

***, **, and *represent statistical significance at the 1%, 5%, and 10% levels, respectively (two-tailed tests).

Regarding the control variables, our findings show a positive coefficient on firm profitability (GRPROFIT), market share (MKTSHR), and firm value (MKTBK). Our results indicate that higher profitability is likely to have higher working capital, suggesting conservative WCM. We also find a negative coefficient on firm leverage (LEVER), sales growth (SALEGR), and firm age (FIRMAGE), suggesting that highly leveraged, high-sales growth firms and firms with higher longevity are likely to hold lower working capital indicating aggressive working capital policy. The adjusted-R2 is approximately 44 percent. We also consider an alternative measure of working capital, cash conversion efficiency (CCE), following existing research (Filbeck & Krueger, 2005; Seth et al., 2020). CCE is measured as relating net cash flow from operating activities to sales revenue. Our untabulated results are consistent with the main results.

4.5. Additional Analysis

4.5.1. Role of State-ownership

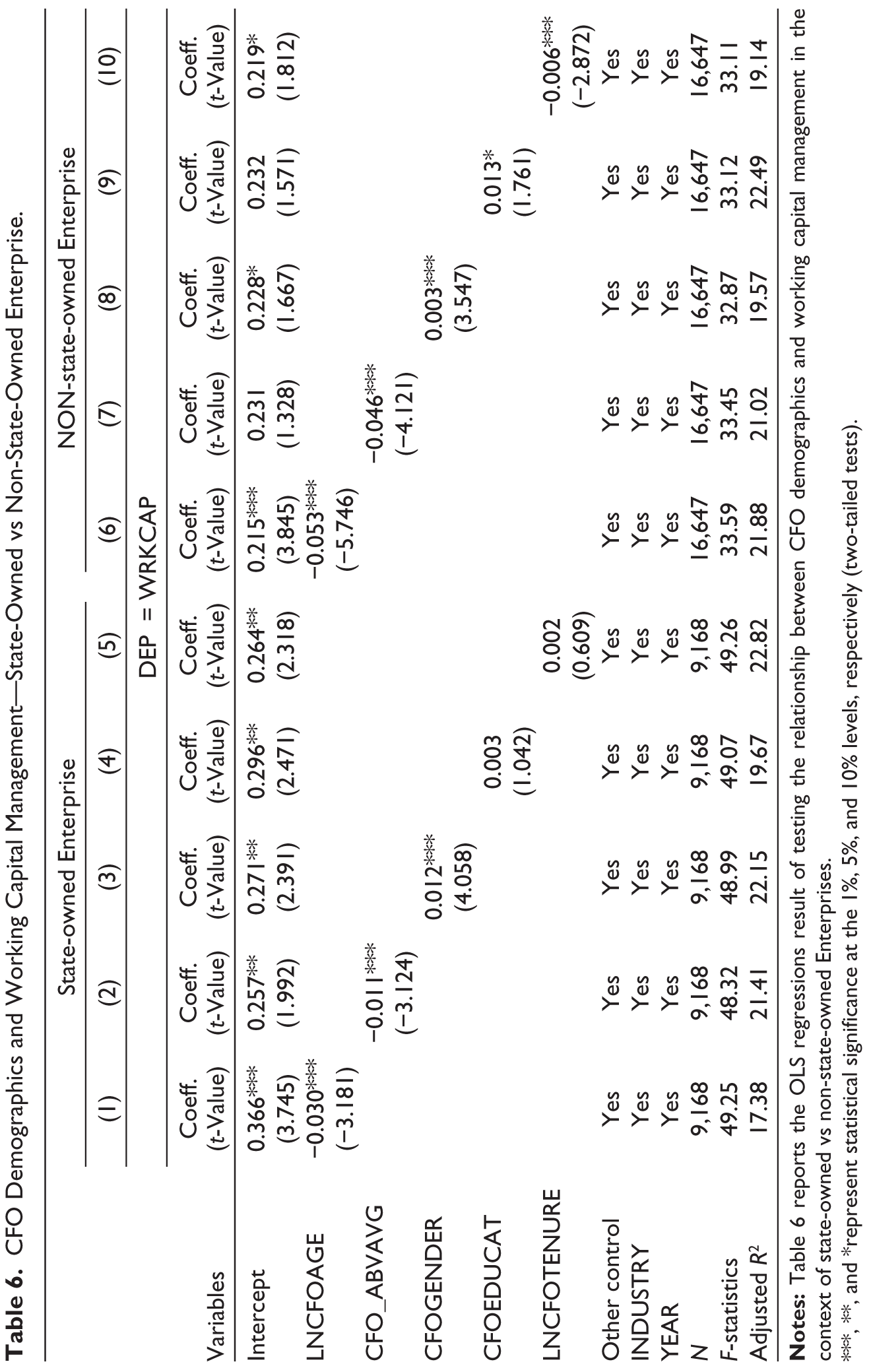

Ownership structure could affect a firm’s working capital structure (Ren et al., 2019). Since 1979, China has begun a string of economic reforms toward a market-based economy, that is, corporatization of formerly owned SOEs. The Chinese government, however, rests on significant shareholder and maintains two key control rights––disposal of assets and mergers and acquisitions and appointment of TMT (such as Chairman, CEOs and CFOs) of these SOEs. Access to finance is another reason for differential reliance on financial information across SOEs and non-SOEs. SOEs typically have better access to finance from state-owned banks (the primary source of capital in China) than non-SOEs because state-owned banks often lend to SOEs for political, employment, and tax reasons other than profitability (Brandt & Li, 2003). On the other hand, access to financial decisions for non-SOEs is mainly based on financial rather than political considerations. Consequently, non-SOEs access to financial decisions depends more on the quality of the financial statement information (Chen et al., 2011).

We decompose the sample into firms with state ownership and non-state ownership. Finally, we rerun equation (1), and the findings are reported in Table 6. Our findings suggest that the association between CFO demographic attributes and firm working capital is predominant in non-SOE firms. Within the firms that have state ownership, the coefficient of CFO demographic attributes (CFOEDUCAT and LNCFOTENURE) shows a statistically insignificant association except for CFOAGE and CFOGENDER. Both LNCFOAGE and CFO_ABVAVG present a negative association (coefficient = −0.030, −0.011; t-statistics = −3.181, −3.124; p < .01, respectively). The estimated coefficient of CFOGENDER is positive (coefficient = 0.012, t-statistics = 4.058) and statistically significant at a 1% level. Our findings suggest that younger or female CFOs in SOEs use conservative working capital policies. Alternatively, the coefficient of CFO demographic attributes (LNCFOAGE, CFO_ABVAVG, CFOEDUCAT, CFOGENDER, and LNCFOTENURE) show an association with WRKCAP in non-SOEs, and the findings are statistically significant. The LNCFOAGE, CFO_ABVAVG, and LNCFOTENURE show consistently negative associations within the group of firms with non-SOEs, and the findings are statistically significant at a 1% level. Our findings suggest that non-SOE firm CFOs are likely to follow an aggressive working capital policy. Our findings are consistent with the broader corporate finance literature, which posits that the Chinese growth miracle is driven by highly productive private firms, which accumulate very high cash flows (Ding et al., 2013).

CFO Demographics and Working Capital Management––State-Owned vs Non-State-Owned Enterprise.

***, **, and *represent statistical significance at the 1%, 5%, and 10% levels, respectively (two-tailed tests).

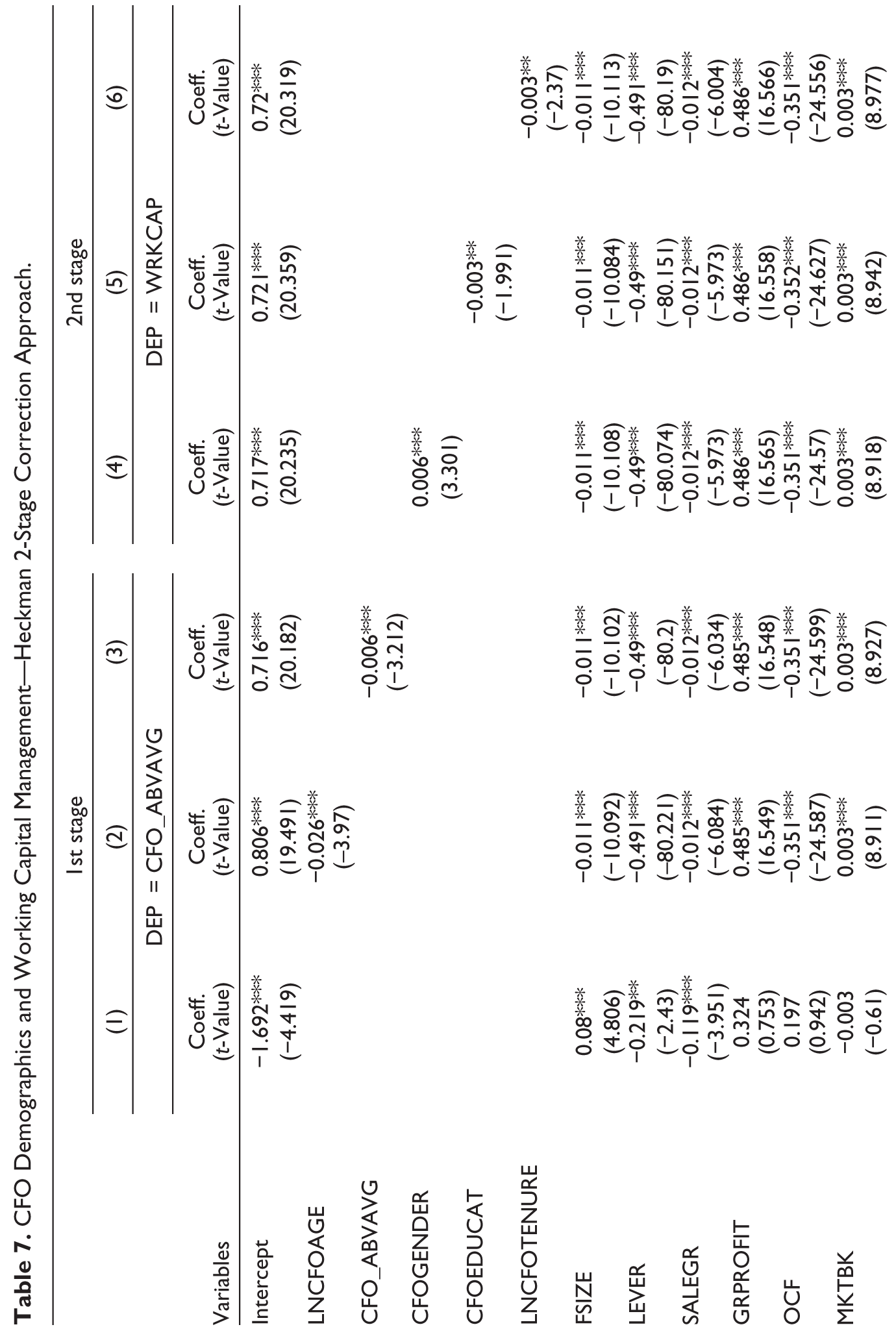

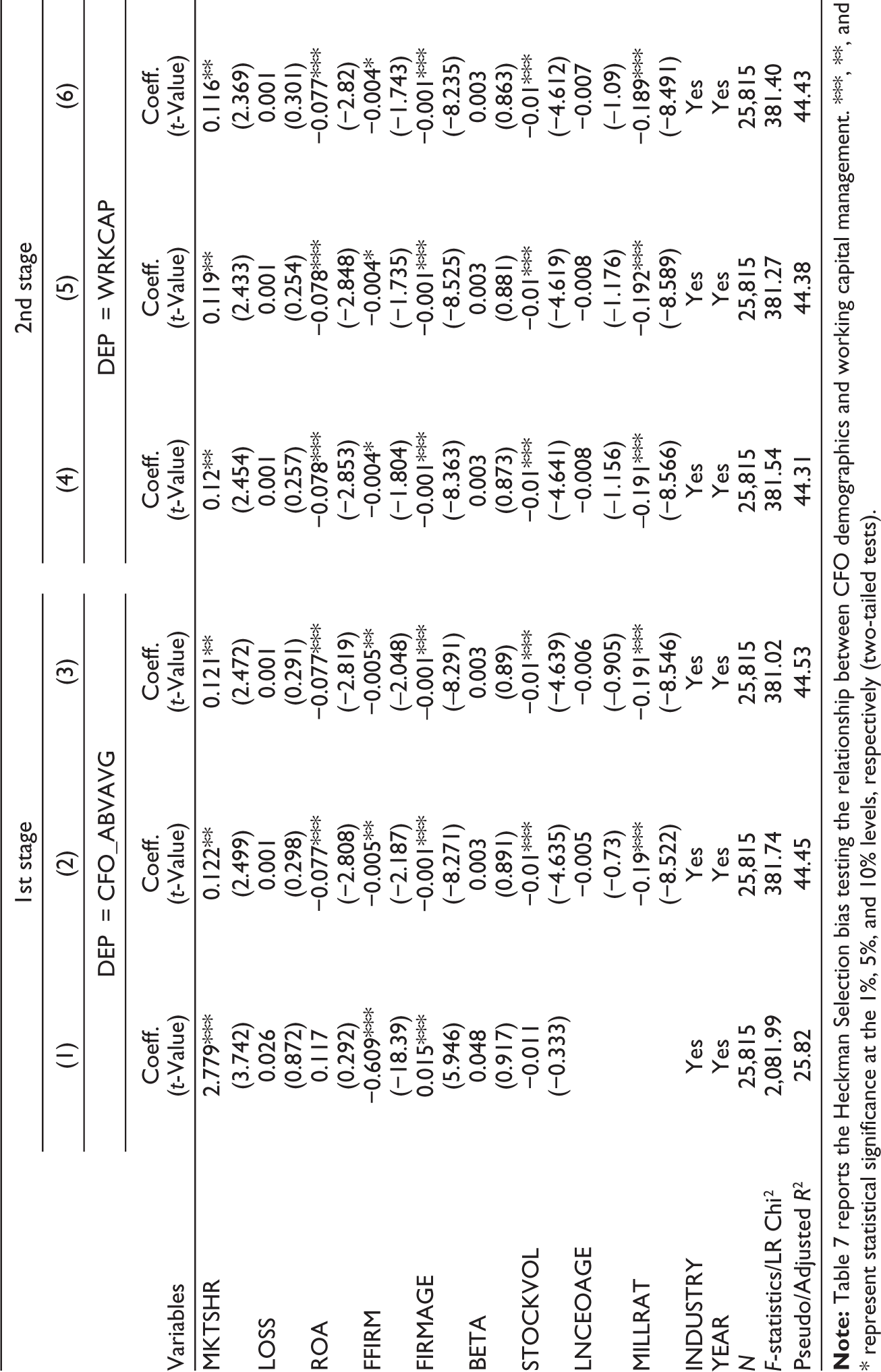

4.5.2. Heckman Two-stage Correction Approach

There is a possibility that self-selection bias might exist in our estimations. To address self-selection bias, it is essential to control for other factors that may influence the relationship between CFO demographics and working capital. We use Heckman’s (1979) two-stage correction approach to alleviate concerns relating to our estimation. The first stage estimates a logit model to control for endogenous selection bias. This stage generates an inverse Mills ratio, which adjusts for the independent variables’ endogeneity. This stage provides the modified estimates of the independent variable coefficients.

Table 7 Column (1) reports the findings of first-stage regression, indicating that CFOs’ (CFO_ABVAVG) age is determined by firm size (FSIZE), leverage (LEVER), sales growth (SALEGR), market share (MKTSHR), family firm (FFIRM), firm age (FIRMAGE), firm’s financial risk (BETA, STOCKVOL), and profitability (ROA). Our findings suggest that larger firm size, lower leverage, less sales growth, market share, non-family firms, and firm age are likely to appoint older CFOs. We incorporate the calculated Inverse-Mills Ratio (MILLRAT) as an independent variable in the second stage regression following Heckman (1979). Columns (2) to (6) report the findings of second-stage regression results. We find that CFO age (LNCFOAGE and CFO_ABVAVG) has a negative association (coefficient = −0.026 & −0.006; t-statistics = −3.97 & −3.212) with the firm working capital policy suggesting the firm chooses a lower level of working capital in the presence of older CFOs. Our findings are statistically significant at 1 per cent levels for both measures. Further, we find that CFO gender (CFOGENDER) is positively associated with the firm’s working capital. However, in the Column (5), we find that CFO education level (CFOEDUCAT) has a negative association with the firm WCM which is statistically significant at 5 per cent level. Consistently, we find a negative association between the CFO tenure (LNCFOTENURE) and firm working capital which is statistically significant at 5 per cent level. Overall, our findings are largely consistent with our primary findings.

CFO Demographics and Working Capital Management––Heckman 2-Stage Correction Approach.

5. Conclusion

Effective working capital enhances profitability and increases firm value. Firms operating with limited resources always ensure efficient and smooth operating functions through better WCM policies. Managers are often perceived as having their own style when making an investment, financing, and other strategic decisions, thereby imprinting their personal marks on the companies they manage (Bertrand & Schoar, 2003). Thus, we argued that the role of the CFO is more noticeable in corporate financial policy and examined the association between CFO demographic attributes and firm WCM. Using a sample of Chinese listed companies over 2000–2021, we find that CFO age, gender, education, and tenure determine firm working capital. Further, we have evidence that the association is more pronounced in firms with no state ownership. Our results suggest older, higher academic qualification, and long-tenured CFOs are likely to conduct aggressive working capital policies. In contrast, we find that female CFOs are more likely to be conservative on WCM policy.

Our findings have a range of ramifications. We show that a CFO’s demographic traits influence a firm’s WCM policies and that the association can be used in the appraisal of CFO performance. These insights can help regulators and policymakers develop laws and regulations to improve corporate financial policies and decision-making. Regulators and policymakers may better adjust their regulations and laws to ensure that firms make sound financial decisions that benefit their stakeholders by analyzing the influence of CFO demographic traits on WCM. Our findings potentially set the stage for future study. We propose that future studies investigate the influence of additional demographic variables on WCM policies, such as CFOs’ nationality, ethnicity, and industry expertise. Future research might investigate the connection between CFO demographics and other financial policies, such as a firm’s risk-taking proclivity and investment efficiency. Additionally, the influence of other contextual factors, such as the financial (for small and mid-sized firms) and economic environment, on the link between CFO demographic traits and WCM practices could be investigated.

Footnotes

Acknowledgements

We would like to thank the participants of the 2022 Auckland Regional Accounting Conference and the 2022 New Zealand Management Accounting Conference for providing helpful feedback on an earlier version of this manuscript. In addition, we wish to thank Tony van Zijl and Solomon Opare for providing insightful comments on an earlier version of this work. Finally, we want to thank Mark Wood for his assistance in obtaining access to the database.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.