Abstract

The aim of this study is to examine the role of disciplinary tools, that is, capital adequacy requirement and market discipline in maintaining the banks’ performance and financial stability. The study employs a panel dataset of 600 commercial banks from BRICS economies for the period ranging from 2005 to 2020 using the panel regression. The robustness of the results is validated using the system GMM (generalized method of moments). The study reveals that, in a linear model, capital adequacy ratio has a positive influence on performance and stability, and market discipline has a negative influence on performance and stability. In a non-linear model, capital adequacy ratio has a concave relationship. Further, the study discusses the critical determinants of profitability and stability.

1. Introduction

The performance and stability of the banking industry became a matter of paramount significance after the global financial crisis of 2008 owing to its contagious effect on the stability of the entire economy (Hugonnier & Morellec, 2017). Performance and stability are expected to be influenced by various bank-specific, macroeconomic, regulatory, and financial development factors (Goddard et al., 2004). This study attempts to evaluate the determinants of bank performance and stability, specifically in the context of regulatory disciplinary tools as identified in Basel norms in the emerging markets. In 1974, the governors of central banks from 10 countries established “The Committee on Banking Regulations and Supervisory Practices” at the Bank of International Settlement (BIS), Basel, in response to the distress in international markets and the banking industry. 1 The objective of the committee was to improve financial stability by laying down the guidelines for bank supervision. In 1988, the committee issued the Basel capital accord, also known as Basel I. Initially, Basel I entirely focused on credit risk but was subsequently modified to include market risk. It aimed to set a minimum capital requirement for the banking sector, so that they can sustain unexpected losses and withstand any crisis. Under Basel I, the minimum capital requirement was fixed at 8% of risk-weighted assets. The level of regulatory capital provides a cushion against unexpected losses and minimizes the risk of bank failures (Ozili, 2017). The committee issued Basel II guidelines in 2004. It rested on three pillars. The first pillar was the minimum capital adequacy ratio of 8% of risk-weighted assets. The second pillar was a supervisory review, under which banks were required to adopt better risk management techniques to manage all three types of risks (credit, market, and operational risk). The third pillar focused on market discipline. Market discipline implies countervailing actions initiated by stakeholders (mainly uninsured depositors) in terms of increased funding cost in response to excessive engagement of banks in risky activities (Berger, 1991; Martinez Peria & Schmukler, 2001). All these pillars focused on making disclosure requirements of capital adequacy and risk management practices by the commercial banks to the Central Bank of the country more stringent for promoting the safety and soundness of the banks. The global financial crisis of 2008 led to the introduction of Basel III guidelines in 2010. Basel III focused on making the banking system more resilient and increased the minimum capital requirement to cater to capital needs along with the introduction of innovative products and consideration of liquidity risk. All these norms aim to make the financial system resilient to any crisis scenario. But the impact of these on stability and profitability is unresolved. Therefore, this study seeks an answer to the question that does these disciplinary tools have an influence on the performance and stability of the banking system.

This study focuses on BRICS (Brazil, Russia, India, China, and South Africa) economies, as all of them are emerging economies. These economies have experienced a high growth rate in the last few decades. They have witnessed radical changes in their economic activities due to globalization and the liberalization of their financial and commodity markets. Further, these economies have low-cost labor, an abundance of natural resources, and favorable demographics. 2 These nations are members of G20 and account for 26.20% of the gross world product, 32.10% of global GDP PPP, and 41.50% of the global population.

The study makes a significant contribution to banking literature. It explores the impact of capital adequacy requirements and market discipline on bank performance and financial stability in BRICS economies in the presence of other bank-specific, macroeconomic, and financial development factors. The study examines the linear as well as non-linear relationship among the variables under consideration. Further, the study analyzes these relationships using static and dynamic estimation models. To the best of the author’s knowledge, no prior study has been conducted exploring these relationships in the context of emerging economies.

The remainder of the article is structured as follows: “Theoretical background, literature review, and hypotheses development” provides the details of the theoretical background and existing investigations available on the subject. Section 3 discusses the variables, their data sources, and estimation models used to analyze a relationship. Section 4 reports the regression results and provides the analysis of empirical estimation. Finally, Section 5 presents the concluding observations of the study.

2. Theoretical Background, Literature Review, and Hypotheses Development

Banks always have the incentive to engage in excessive risk-taking at the expense of depositors and taxpayers due to implicit and explicit government guarantees and the problem of moral hazard (Haq et al., 2016; Merton, 1977). This behavior became evident during the global turmoil of 2008, which created disturbances in the financial markets all over the world and highlighted the significant role played by disciplinary tools in curbing the disruption caused by the contagion effect.

Academicians, regulators, policymakers, and borrowers focus on the reduction of costs associated with contagion, bankruptcy, and possible disruption in the system in order to maintain the stability and profitability of the banking industry. This provides an impetus for analyzing the impact of regulatory changes on bank performance and financial stability. The two pillars of the Basel norms, that is, market discipline and minimum capital requirement, play a significant role to ameliorate profitability and stability.

2.1 Market Discipline

Market discipline, in the context of banking industry, can be explained as the countervailing actions initiated by the private sector agents (especially depositors or creditors, and stockholders) who face increased costs due to a rise in bank risk (Berger, 1991). Martinez-Peria and Schmukler (2001) highlight that uninsured depositors penalize banks by charging higher rates of interest or by withdrawing their deposits in case banks engage in risky activities. The reduction in the amount of uninsured liabilities along with an increase in bank risk signifies the existence of market discipline (Goldberg & Hudgins, 2002). Therefore, these actions by market participants tend to safeguard their interests and discipline or penalize banks (Hoang et al., 2014). A little intimidation of market discipline forces banks to work conservatively. Market discipline, in a way, mandates the issuance of subordinate debt which in turn induces both direct and indirect discipline in the risk-taking behavior of the banks (Goyal, 2005). The positive correlation between yields and bank risk measures conforms to the existence of direct discipline, which makes banks manage their risk-taking prudently, in anticipation of higher cost of funding (Bliss & Flannery, 2001; Flannery & Sorescu, 1996). Consistent with this argument, Nier and Baumann (2006) suggest that subordinate debt holders demand higher risk premiums from riskier banks leading to an increase in the cost of debt financing; consequently, in order to reduce this cost, banks are encouraged to maintain low levels of risk. The restrictive covenants of uninsured financing disciplines the risk-taking behavior of banks (Chen & Hasan, 2011; Goyal, 2005). Furthermore, information exhibited in market prices assists in the supervisory process and induces indirect discipline in the banks.

The existing literature on the impact of market discipline on bank performance and stability has provided inconclusive evidence. Calem and Rob (1999) reveal that subordinated debt does not have any influence on the portfolio allocation of well-capitalized banks. Godspower-Akpomiemie and Ojah (2021) investigate the impact of market discipline on bank performance taking a sample of 706 banks from 34 countries. Their results indicate the contrasting effect of such actions in developed and emerging markets. Market discipline reduces loan risk in emerging economies and increases loan risk in developed economies due to the presence of higher liquidity and capital cushion. Further, the impact of market discipline on profitability is less in the case of developed economies in comparison to emerging economies. Based on the above literature review, the following hypothesis is formulated:

H1: Market discipline significantly affects bank performance and financial stability.

2.2. Regulation of Capital

The capital adequacy ratio (regulatory capital) is a proxy measure of solvency of the banks. Capital acts as a shock-absorbing buffer and protects the bank in case of adverse market conditions. However, its impact on bank performance and risk remains debatable. Blum (1999) proposes that, in a dynamic and new inter-temporal framework, capital adequacy requirements reduce bank profitability, as banks engage in risky activities today to increase the equity for tomorrow due to increase cost of raising equity in future. As a result, capital adequacy requirement increases bank risk. He further proposes that subordinate liabilities can help in the reduction of bank risk if they maintain their risk at a certain level; however, if banks adjust their risk level in response to changes in interest rates, then subordinated liabilities can raise their riskiness. Risk-based capital regulations restrict investments (Rime, 2001). The inappropriate selection of risk weights in the risk-weighted capital ratio also increases the risk of the banks (Rochet, 1992). Therefore, the allocation of resources becomes lop-sided. It causes a reduction in the quality and benefits of the portfolio (Lin, 1994). On the other hand, Nier and Baumann (2006) report that the bank capital ratio is positively influenced by the uninsured liabilities, which suggests that banks resort to a high capital ratio to save themselves from default risk (Lin et al., 2005). Haq et al. (2014), in their study, examine the impact of disciplinary tools (bank capital, market discipline, and charter value) on bank equity and default risk. The empirical analysis is based on 218 listed banks from Asia-Pacific countries from the period starting from 1996 to 2010. The bank capital is measured by leverage ratio; market discipline is proxied by the ratio of the sum of interbank deposits and subordinated debt to total liabilities (Nier & Baumann, 2006); the charter value is measured by the ratio of the sum of the book value of liabilities and market value of equity to the book value of total assets. The study reports a positive relationship between bank risk and bank capital and reports a negative relationship of bank risk with charter value and market discipline (Berger et al., 2009; Keeley, 1990). Higher charter value reduces banks’ incentive to engage in risk-taking behavior and protects them against potential bankruptcy (Matutes and Vives, 2000). Further, the study concludes that bank capital and market discipline act as complementary tools, while charter value (self-disciplinary tool) is substituted by market discipline in managing bank risk-taking incentives.

Based on the above literature, we propose the following hypothesis:

H2: Capital adequacy requirements significantly affect bank performance and financial stability.

3. Data and Methodology

3.1. Data and Sample

The study uses a panel data set of 600 commercial banks from BRICS economies covering a time frame of 16 years from 2005 to 2020. Our dataset is restricted to the banks having data for subordinate debts and interbank deposits as these are the measure of market discipline. Banks with five-year continuous observation available have been taken into consideration. The data for the empirical analysis is extracted from Moody’s Analytics BankFocus and RBI website [Statistical table relating to Banks in India (STRBI)]. Data for macroeconomic variables and financial development indicators is sourced from the World Bank database.

3.2. Variables

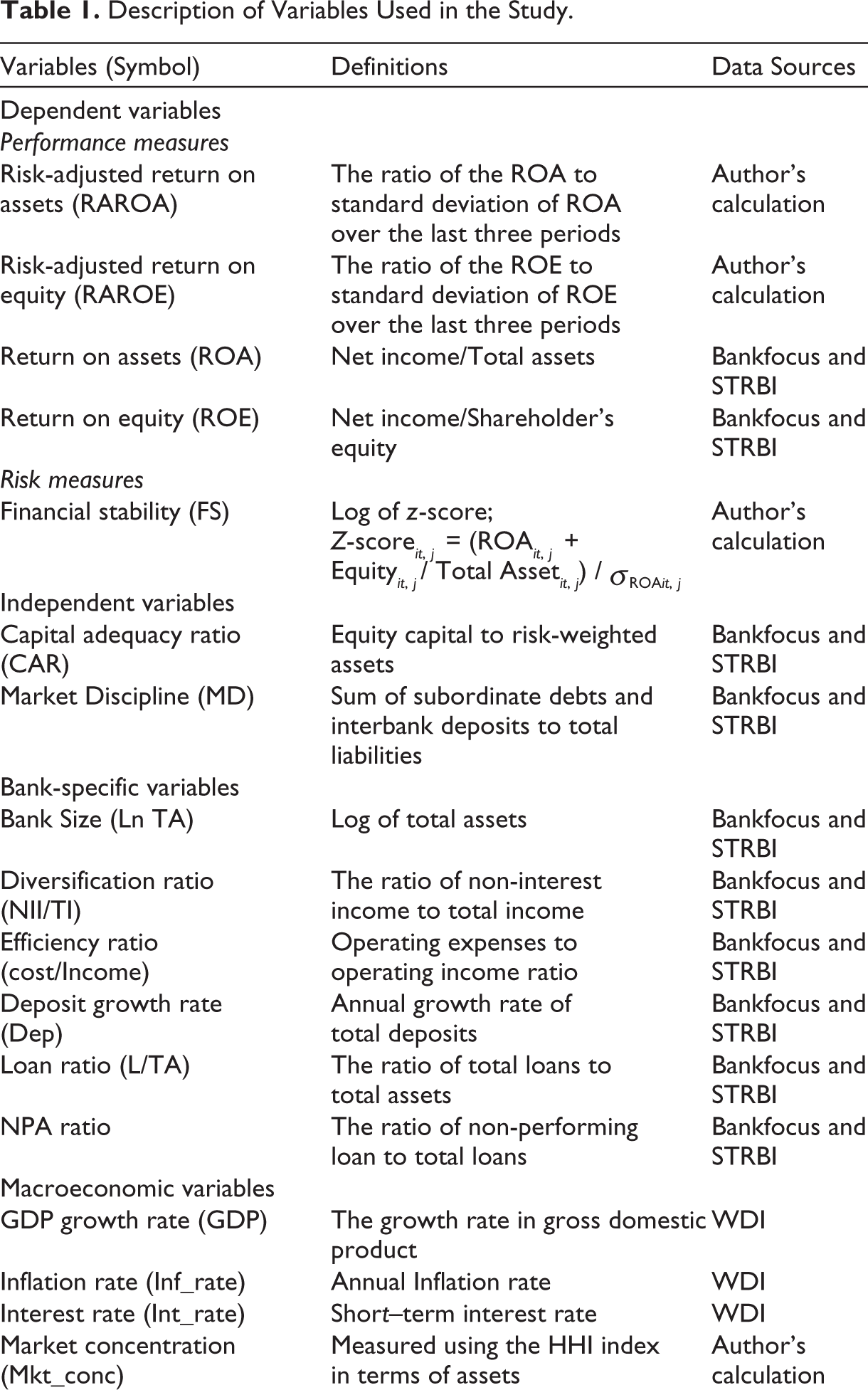

In Table 1, we provide the details of the variable used in the analysis. The performance measures included in the study are risk-adjusted return on assets (RAROA), return on assets (ROA), risk-adjusted return on equity (RAROE), and return on equity (ROE). The log of the Z-score is used for measuring financial stability as suggested by Boyd and Graham (1986). The Z-score is measured as Zit,j = (ROAit, j + Eit, j/ TAit, j)/ σROAit, j where ROA represents the return on assets; E represents equity capital; TA represents total assets; σROAit is the standard deviation of ROA using three-year rolling window; i represents an index of the bank; t represents time variable; j represents country. The log of the Z-score is a widely used measure for financial soundness. Our main explanatory variables include capital adequacy ratio and market discipline. The capital adequacy ratio is measured as the ratio of equity capital to risk-weighted assets. Market discipline is calculated as the ratio of the sum of uninsured deposits (subordinate debts and interbank deposits) to total liabilities (Nier & Baumann, 2006). We control for bank-specific and country-specific variables. Bank-specific variables include bank size, deposit growth rate, diversification ratio, NPA ratio, efficiency ratio, and loan ratio. Bank size is measured by the natural log of total assets and its impact on performance and stability is inconclusive. The diversification ratio is measured as the ratio of non-interest income to total income. Non-interest income is expected to improve bank profitability and stability due to the diversification of risk (Ahamed, 2017). NPA ratio is measured as the ratio of non-performing loans to total loans. The NPA ratio adversely affects performance and stability (Moudud-Ul-Huq, 2020). The efficiency ratio is measured by the ratio of operating expenses to operating income. The loan ratio is measured as the ratio of total loans to total assets.

Description of Variables Used in the Study.

BSD, SMD, and Mkt_Conc.

STRBI: Statistical Tables Relating to Banks in India; WDI: World Development Indicators.

Country-specific variables include GDP growth rate, inflation, interest rate, market concentration, and level of financial development. Herfindahl–Hirschman Index (HHI) is used to measure the level of market concentration. HHI is calculated as the sum of squared market share (in terms of total assets). Market concentration influences the competition in the industry, which is expected to have a significant impact on the bank performance (Pant & Pattanayak, 2010).

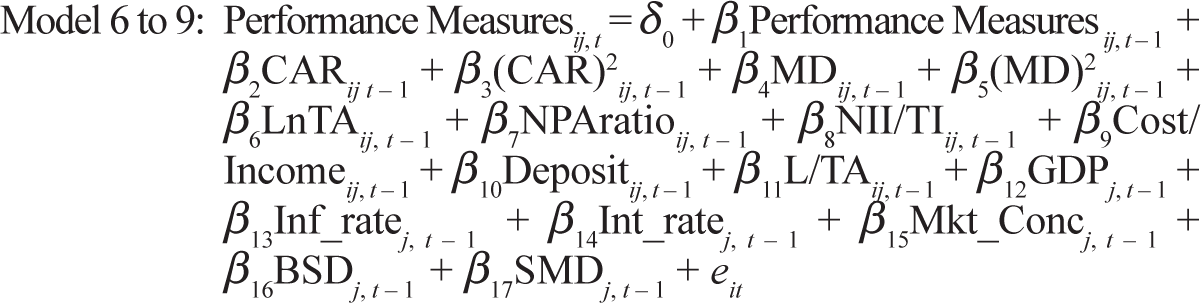

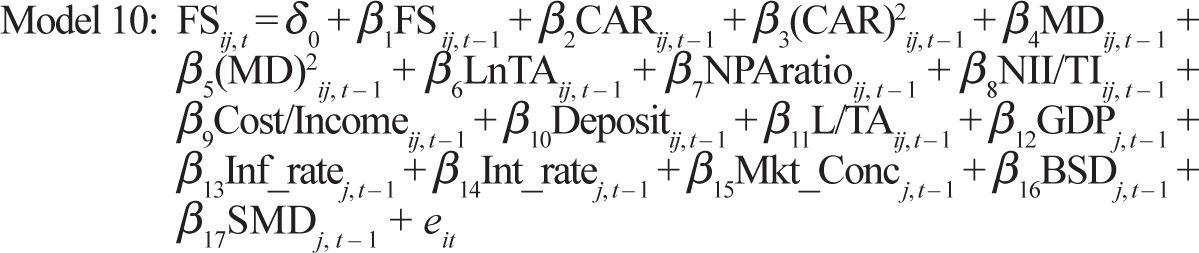

3.3. Model Specification

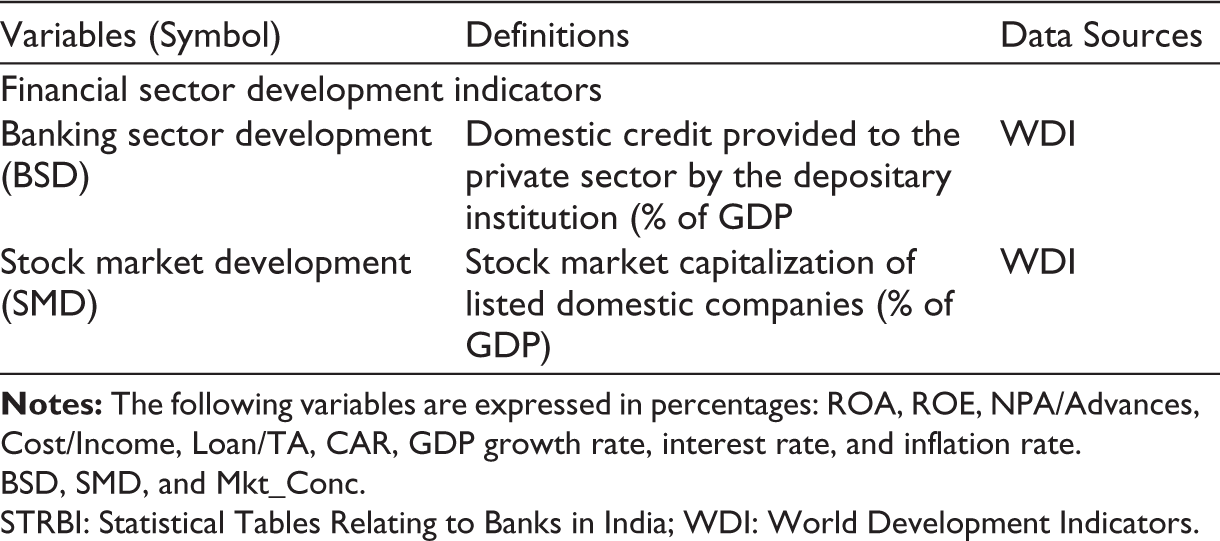

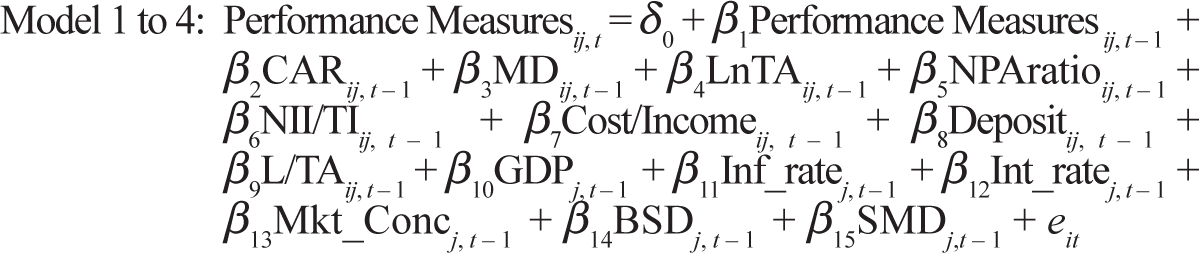

The study employs the following models to test the impact of capital adequacy requirements and market discipline on bank performance and financial stability:

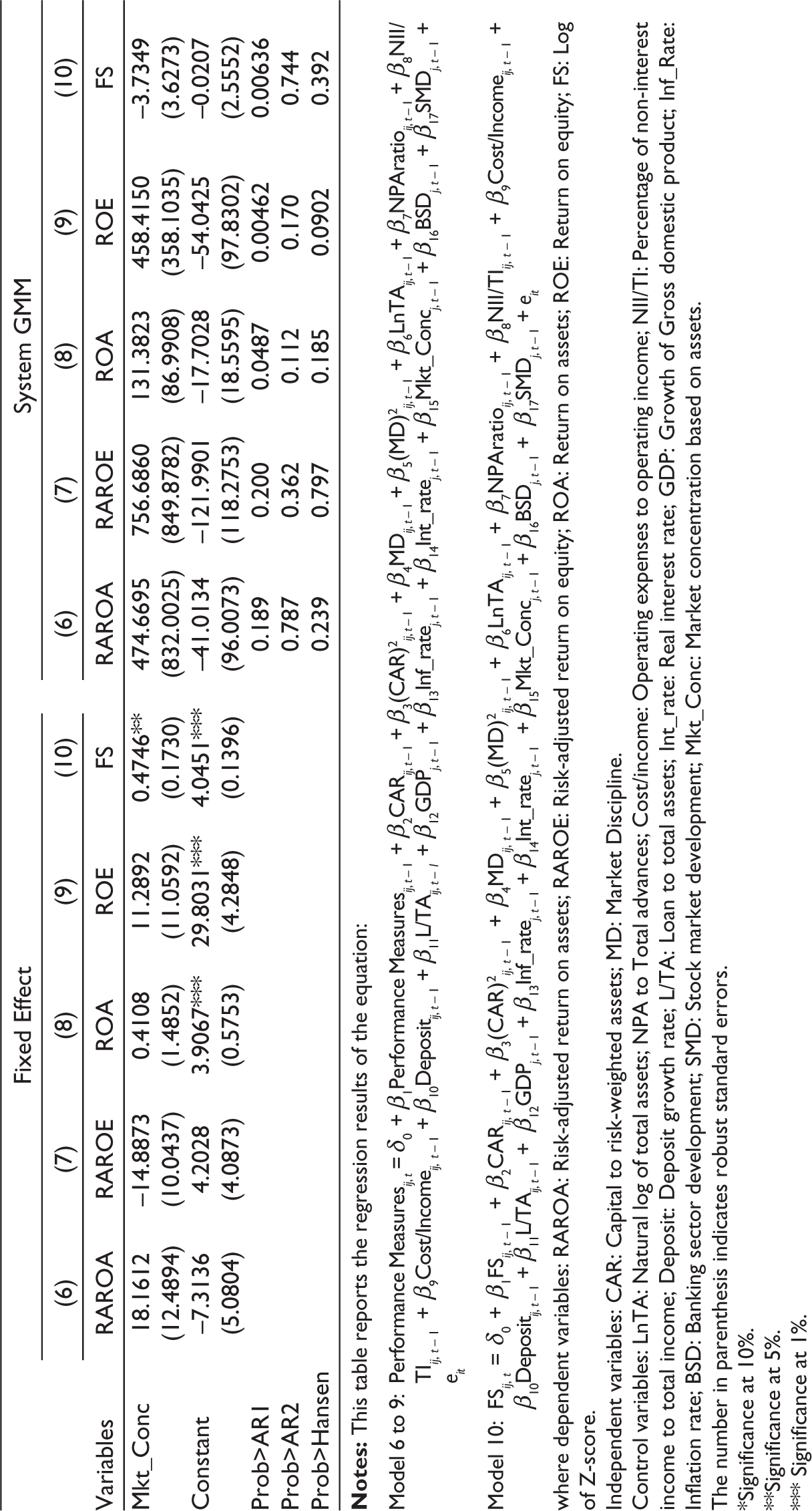

The model uses lagged values of the dependent variable, bank-specific, and macroeconomic variables to indicate the persistence in the dependent and control variables. The effect of control variables on performance and stability is not contemporaneous (Barra & Zotti, 2019). The model is estimated using panel regression (fixed effect model). The robustness of our results is validated by using System GMM. System GMM deals with omitted variables bias, endogeneity, autocorrelation, and heterogeneity [Arellano & Bover (1995) and Blundell & Bond (1998)] and provides consistent results. The diagnostics test, that is, Hanse J-statistics of overidentification, AR (1), and AR (2) are employed to validate our models.

4. Results and Discussion

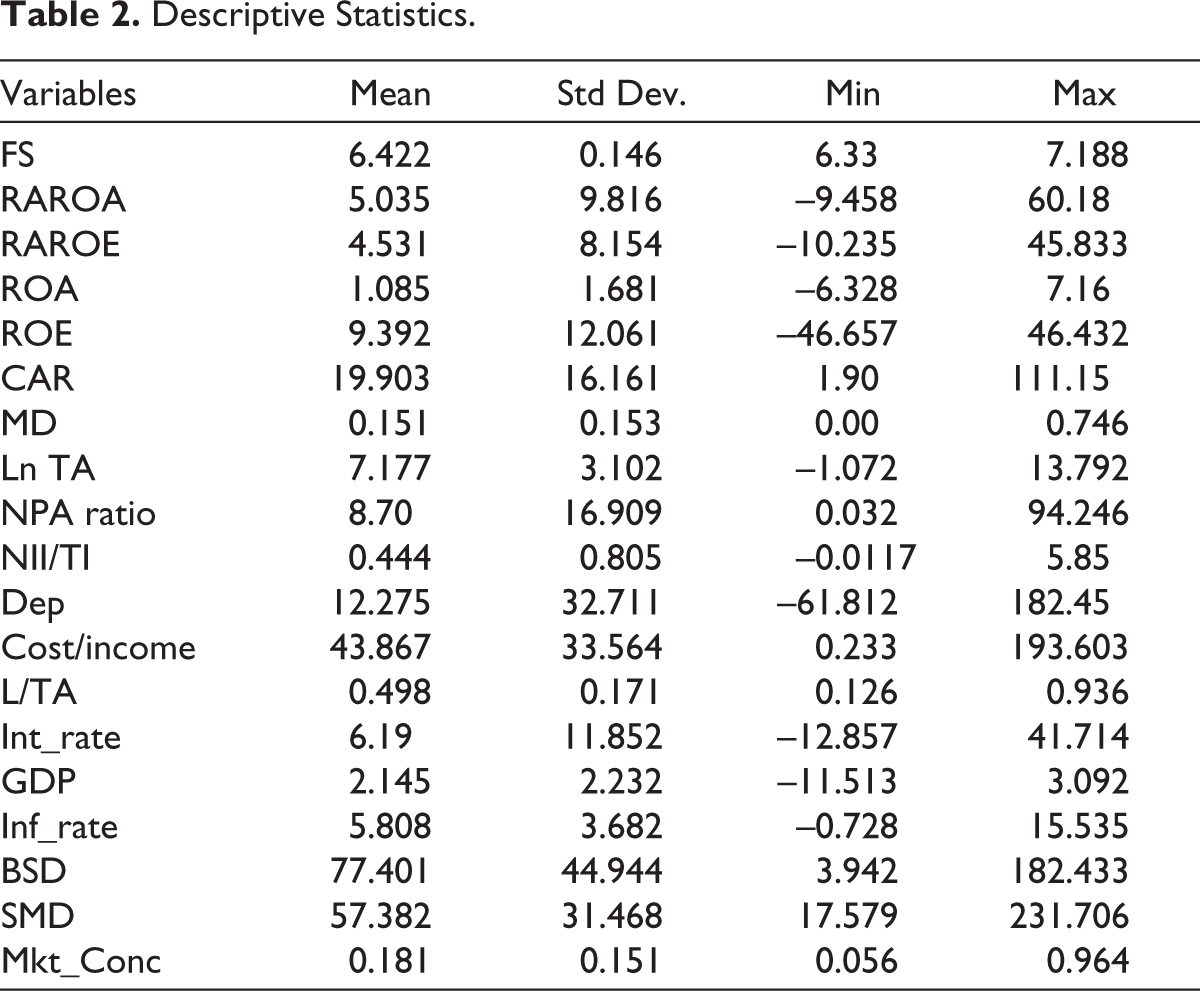

4.1. Descriptive Statistics

Table 2 reports the descriptive statistics of the variables used in the study. The average values of performance measures, that is, RAROA, RAROE, ROA, and ROE are 5.035%, 4.531%, 1.085%, and 9.392%, respectively. The mean value of the Ln Z-score is 6.422. The mean value of the capital adequacy ratio and market discipline is 19.903% and 0.151%, respectively. With respect to control variables, the minimum and maximum value of the NPA ratio ranges from 0.03% to 94.24%. The ratio of non-interest income to total income has a mean value of 44.40%.

Descriptive Statistics.

4.2. Correlation Analysis

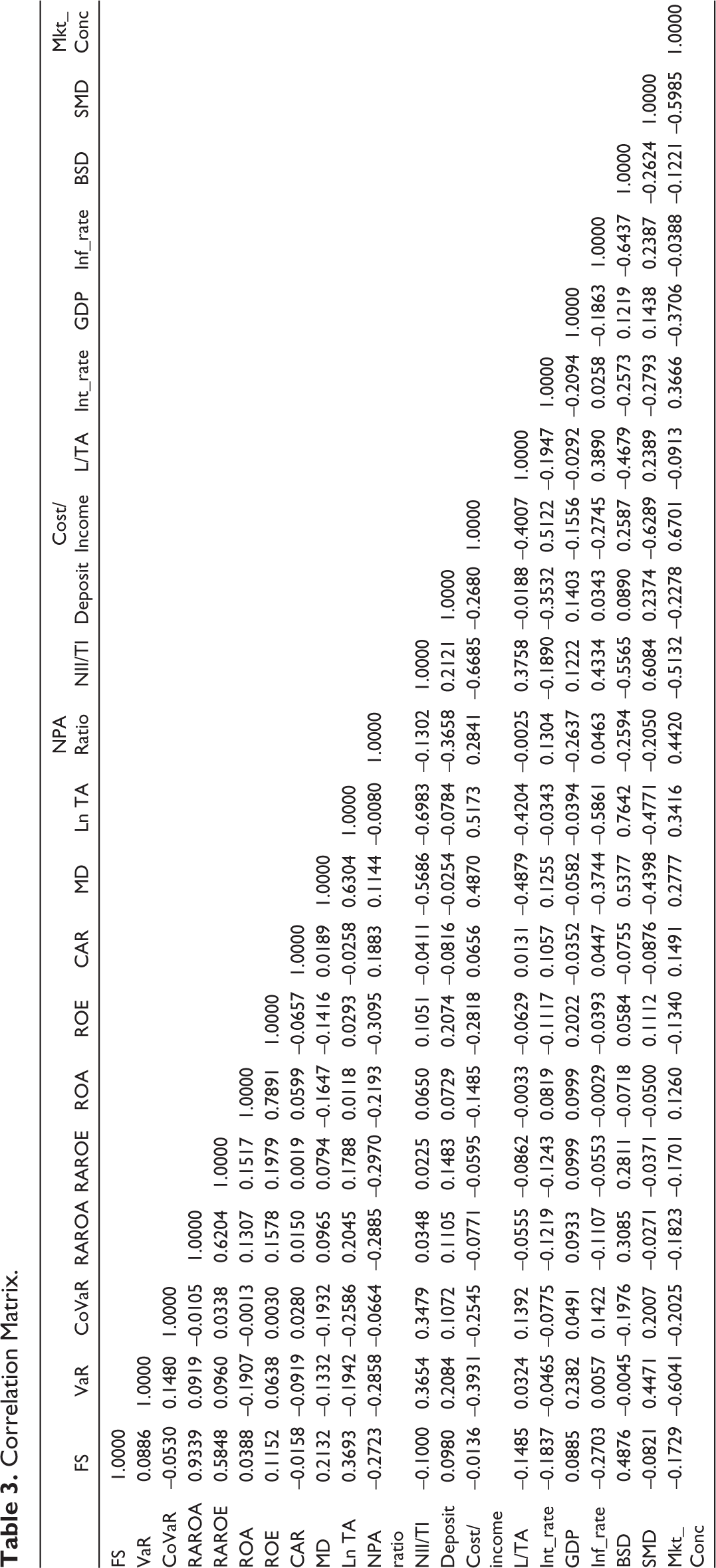

The pairwise correlation coefficients are reported in Table 3. All the correlation coefficients relating to independent variables are less than 0.80 (Hair et al., 1998). Further, the variance inflation factor (VIF) is less than 10 in all estimation models, suggesting that multicollinearity does not exist in our regression model (Neter et al., 1996; Tripathi et al., 2018).

Correlataion Matrix.

4.3. Regression Analysis and Discussion

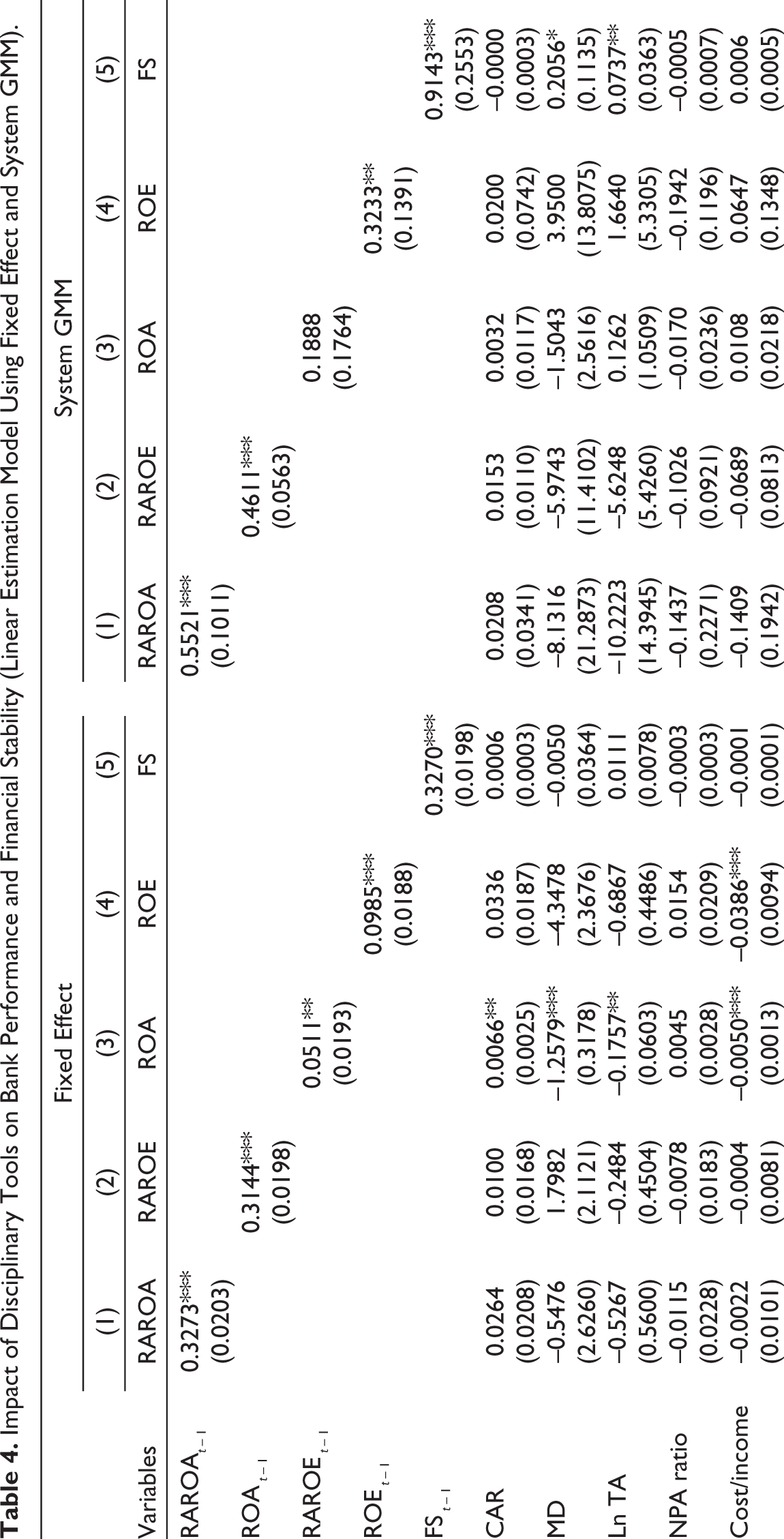

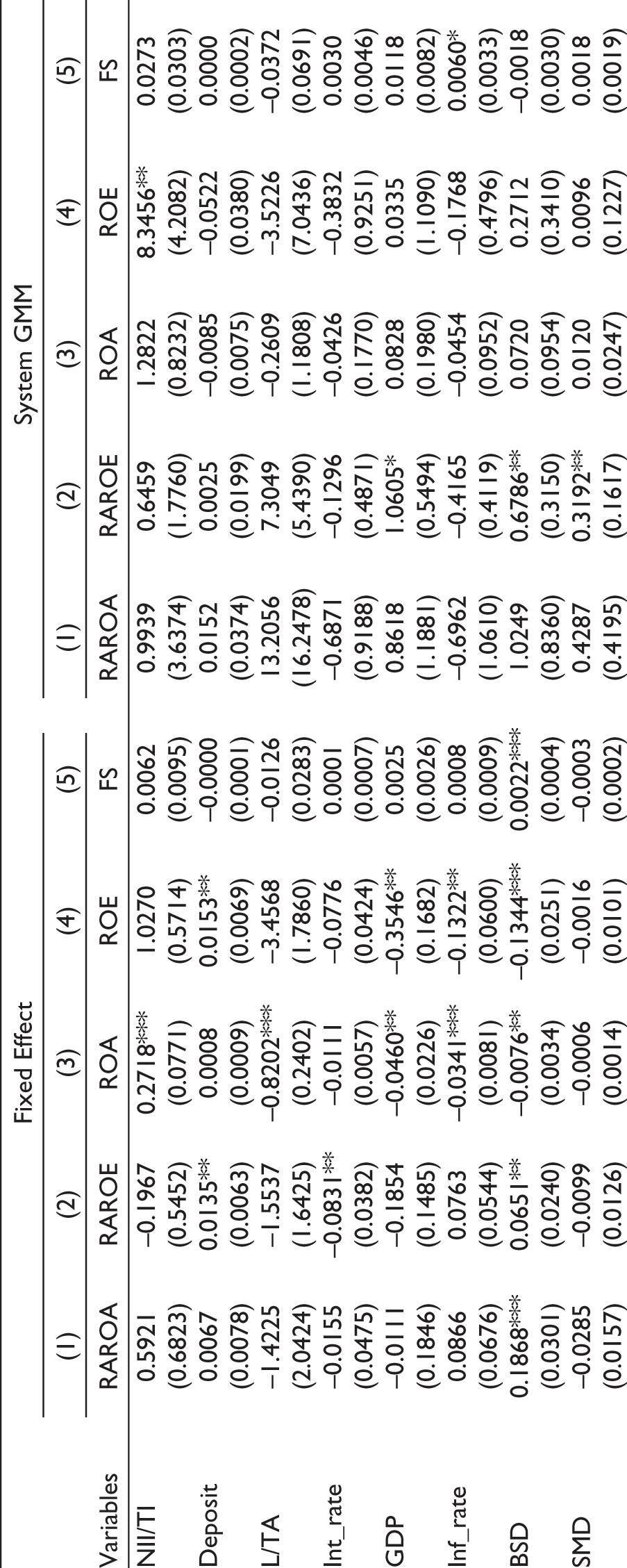

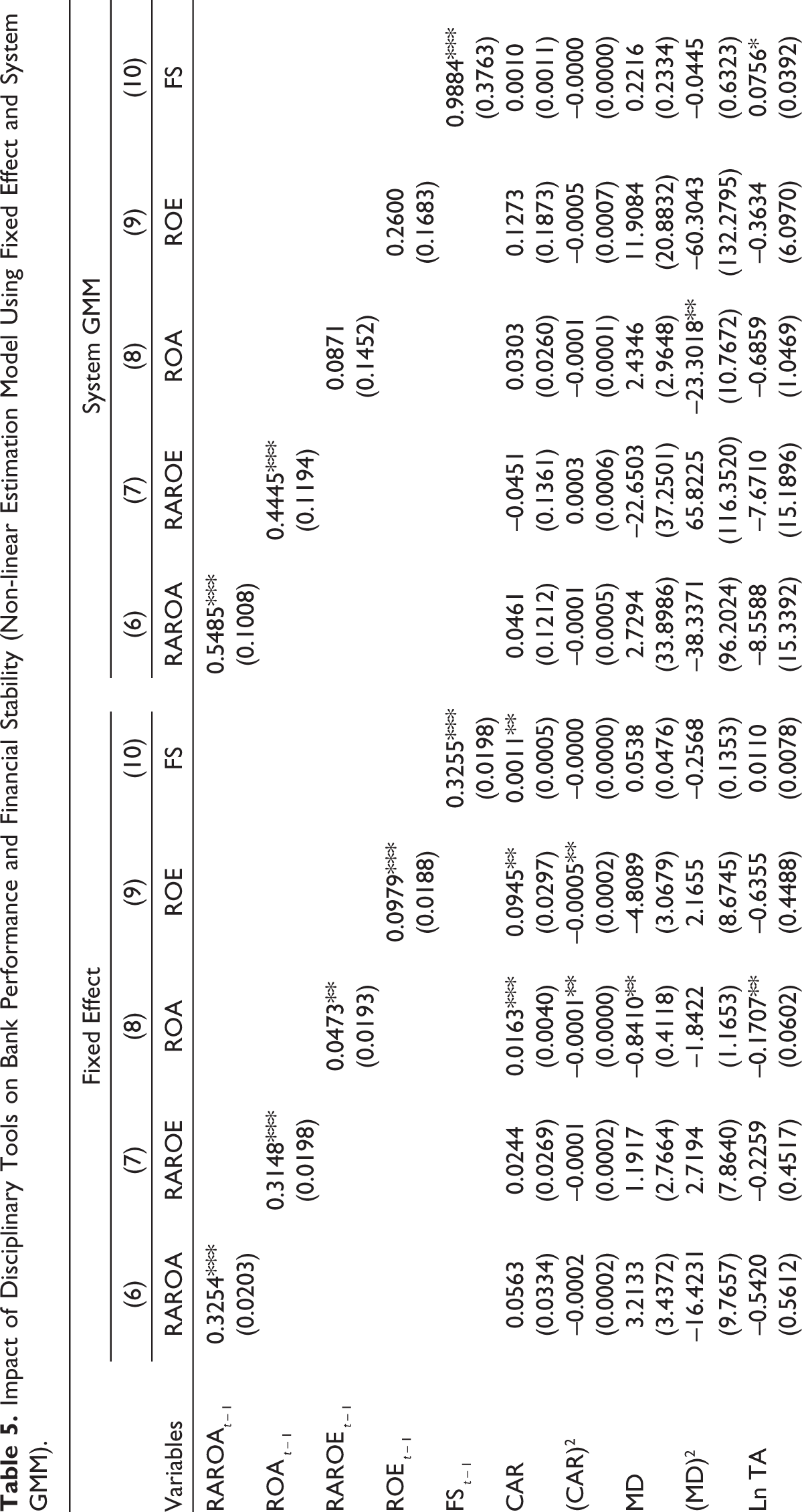

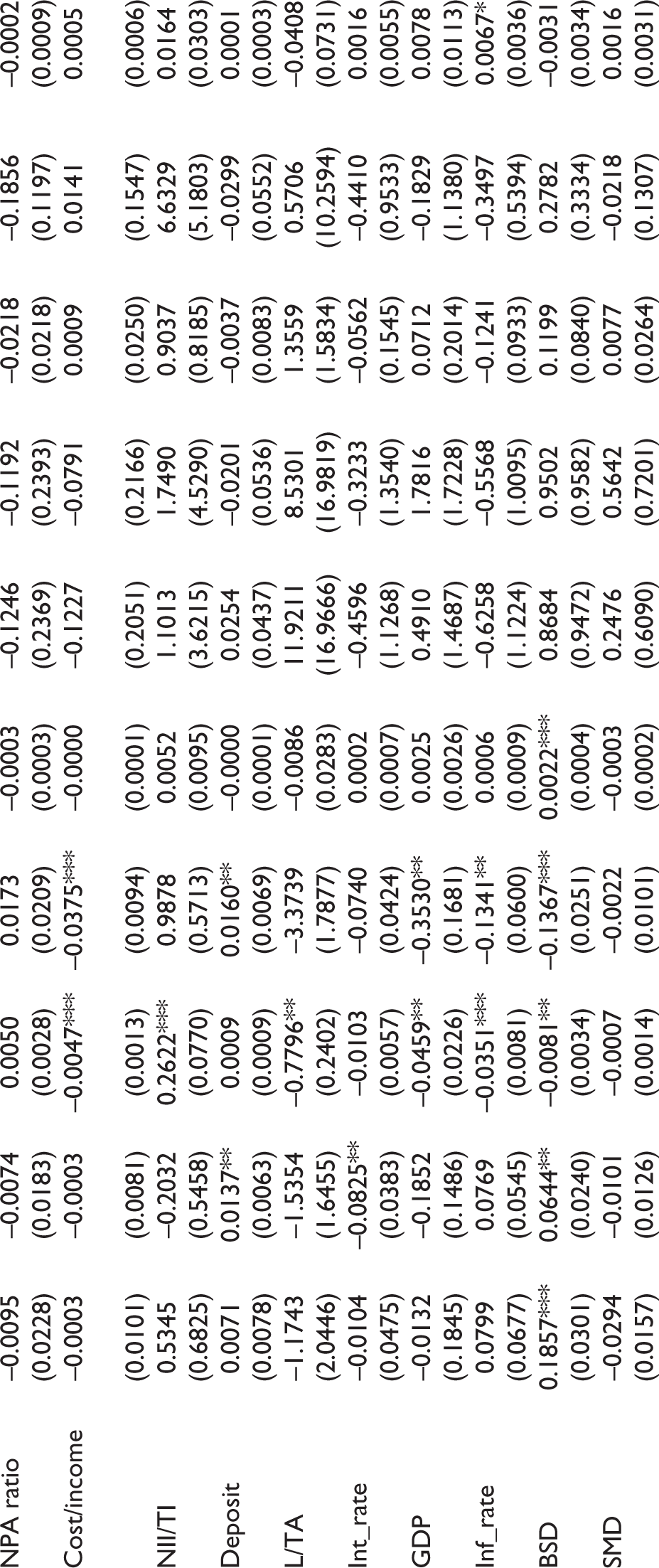

Tables 4 and 5 provide the results of estimation models using the fixed effect model and system GMM. The significant coefficients of lagged dependent variables indicate the presence of persistence and the dynamic nature of performance and stability variables. The relationship is explored in both linear and non-linear models due to the inconclusive evidence provided in the existing literature. To determine the non-linear relationship, the quadratic term of capital adequacy ratio and market discipline has been used. The significance of quadratic terms reveals the existence of a non-linear relationship, that is, U-shape or inverted U-shape (Lind & Mehlum, 2010). In a linear model, the results indicate a positive and significant relationship of capital adequacy ratio with performance and stability. Capital adequacy requirements reduce moral hazard incentives by compelling the shareholders to absorb a large part of losses. When shareholders have large amounts of their own money at stake, they closely monitor the risk-taking behavior of the banks; as a result, banks decrease involvement in risky ventures at the expense of deposit insurance (Rime, 2001). Banks with high capital adequacy ratios and less risk-taking have a lower probability of default. Further, their dependence on government bailout and deposit insurance also reduces, eventually promoting both profitability and stability.

Impact of Disciplinary Tools on Bank Performance and Financial Stability (Linear Estimation Model Using Fixed Effect and System GMM).

Where dependent variables: RAROA: Risk-adjusted return on assets; RAROE: Risk-adjusted return on equity; ROA: Return on assets; ROE: Return on equity; FS: Log of Z-score.

Independent variables: CAR: Capital to risk-weighted assets; MD: Market Discipline.

Control variables: LnTA: Natural log of total assets; NPA to Total advances; Cost/Income: Operating expenses to operating income; NII/TI: Percentage of non-interest income to total income; Deposit: Deposit growth rate; L/TA: Loan to total assets; Int_rate: Real interest rate GDP: Growth of Gross domestic product; Inf_Rate: Inflation rate; BSD: Banking sector development; SMD: Stock market development; Mkt_Conc: Market concentration based on assets.

The number in parenthesis indicates robust standard errors.

*Significance at 10%.

**Significance at 5%.

***Significance at 1%.

Impact of Disciplinary Tools on Bank Performance and Financial Stability (Non-linear Estimation Model Using Fixed Effect and System GMM).

where dependent variables: RAROA: Risk-adjusted return on assets; RAROE: Risk-adjusted return on equity; ROA: Return on assets; ROE: Return on equity; FS: Log of Z-score.

Independent variables: CAR: Capital to risk-weighted assets; MD: Market Discipline.

Control variables: LnTA: Natural log of total assets; NPA to Total advances; Cost/income: Operating expenses to operating income; NII/TI: Percentage of non-interest income to total income; Deposit: Deposit growth rate; L/TA: Loan to total assets; Int_rate: Real interest rate; GDP: Growth of Gross domestic product; Inf_Rate: Inflation rate; BSD: Banking sector development; SMD: Stock market development; Mkt_Conc: Market concentration based on assets.

The number in parenthesis indicates robust standard errors.

*Significance at 10%.

**Significance at 5%.

*** Significance at 1%.

Market discipline has a significant negative relationship with profitability indicating that the increased cost of debt financing reduces the net interest margin of the banks (i.e., the difference between the interest charged on loans and interest paid by the banks on deposits), consequently, has an adverse impact on profitability and stability. The performance of the banking industry suffers in the presence of market discipline as uninsured depositors punish banks by charging higher interest rates or by withdrawing their deposits (Nguyen & Le, 2023). When a bank increases its reliance on uninsured liabilities, initially, its level of risk increases. But eventually, market discipline plays its role and leads to a reduction in bank risk. This finding contrasts with Hoang et al. (2014) who conducted an analysis of banking industries of developed economies as this relationship depends on numerous external factors such as regulatory environment, market competition, transparency in financial reporting, and disclosure of risk exposure. Further, accommodative monetary policies and unbalanced government protection in emerging economies weaken the effect of market discipline (Cubillas et al., 2012). Financial markets of emerging economies are less developed in comparison to that of developed economies leading to poor risk assessment and monitoring, and ineffective implementation of regulatory requirements due to limited resources. This restricts the effect of market discipline and increases the risk-taking activities of the banks, thereby affecting the profitability (Godspower-Akpomiemie & Ojah, 2021).

In the non-linear model, the capital adequacy ratio has an inverted U-shaped relationship with performance and stability. The capital buffer maintained by banks to comply with standards of regulatory capital protects banks from unforeseeable circumstances and adverse market conditions. However, holding capital beyond the threshold point adversely affects profitability and stability as banks fail to invest in valuable but risky opportunities. Our results are aligned with the findings of Ozili (2017) conducted on a sample of African banks. A higher capital ratio reduces the cost of funds, and therefore improves profitability and stability (Amidu, 2014; Pasiouras & Kosmidou, 2007). But, in order to maintain a high capital ratio, banks act over-cautiously by investing in low-risk and low-return activities and avoid investment in high-risk-high-profit potential activities. Consequently, beyond the optimal ratio, this adversely affects profitability indicating diminishing returns to capital (Berger & Bouwman, 2013). This optimal level of capital ratio varies according to the business model, regulatory environment, and risk profile of the financial institutions.

From the above findings, it can be concluded that in the context of emerging economies, capital adequacy requirement and market discipline do not complement each other in improving the profitability or financial stability of the banks. In respect of the control variables, bank size measured by the natural logarithm of total assets has a negative and significant impact on profitability and a positive impact on stability. Similar findings are reported by Boyd and Runkle (1993) and Kosmidou et al. (2008). Large banks suffer from diseconomies of scale and scope, as they face stagnation in growth rate. However, large banks have better opportunities to diversify their risk, which helps in enhancing stability. The cost-to-income ratio has a significant negative impact on profitability and stability, as an increase in operating cost adversely affects bank performance. An increase in non-performing assets also has a negative and significant impact on profitability and stability (Arora, 2014; Rizvi et al., 2018). The NII ratio (ratio of non-interest income to total income) improves bank performance and stability. The diversification of income sources to non-interest income-generating activities helps in risk reduction and mitigation, as revenue from unrelated activities reduces income volatility (Ahamed, 2017). Our results are aligned with the findings of Elsas et al. (2010), Sanya and Wolfe (2011), and Ahamed (2017). Market concentration has a positive influence on profitability and stability. This implies that the presence of a few banks in the industry is easily monitored by the regulators and prevents their engagement in high-risk activities. The concentrated banking industry boosts profitability and supports the paradigm of structure-conduct performance (Beck et al., 2006). The high profits accumulated by the financial institutions in concentrated banking sectors reduce the systemic risk and improve the charter value (Fungáčová & Weill, 2013).

5. Conclusion

The study analyzes the impact of capital adequacy requirement and market discipline on bank performance and stability for a sample of 600 banks operating in BRICS economies. The findings indicate that capital adequacy ratio has a positive impact on performance and stability of banks in BRICS, indicating that capital cushion protects banks from unforeseeable circumstances and helps in preserving profitability. The high capital ratio acts as a buffer for the banks to absorb the losses incurred at the time of financial distress. Adequately capitalized banks convey favorable information to the market, thereby improving business prospects and performance, and reducing credit and bankruptcy costs (Singhal et al., 2022). Market discipline (captured by the percentage of uninsured liabilities) has a negative impact on bank performance and stability in the linear model. The increased cost of funding due to the presence of market discipline causes a detrimental effect on profitability and stability.

In the non-linear model, capital adequacy ratio shows a concave relationship with performance and stability. This implies that maintaining excessive capital adequacy ratio or holding a capital adequacy ratio beyond the optimal level adversely affects banks as they operate over-cautiously and ignore all the high-risk-high return opportunities available in the market (Goddard et al., 2004). The non-linear relationship is more prevalent in emerging economies due to greater economic uncertainties and limited access to sources of funding making it difficult for banks to maintain high capital ratio. Further, banks in emerging economies prefer growth opportunities over profitability; therefore, they maintain a low capital adequacy ratio or capital at a threshold level to invest in valuable opportunities. In a dynamic framework, an increase in capital requirement increases the insolvency risk and reduces the bank profits, if banks have an expectation of low profits in the future (Blum, 1999).

Our study emphasizes the crucial role played by capital and market discipline in maintaining the profitability and financial stability of the banking industry. The findings provide practical implications for regulators, policymakers, investors, creditors, and management of the banking industry. Due to the existence of a non-linear relationship between capital adequacy ratio and profitability in BRICS economies, policymakers should focus on identifying the optimal level of capital ratio in accordance with their economic environment. Regulators should carefully design policies in the context of capital adequacy requirement considering the potential trade-off between capital ratio and profitability. Further, policies and regulatory frameworks should be adaptive in emerging economies as they should evolve in consonance with economic growth and development (Gupta & Kashiramka, 2020). To ensure greater market discipline, policymakers should make stringent disclosure requirements so that investors have access to accurate and timely information. The effect of market discipline is tempered by undersupplied information, lack of implementation of governance mechanisms, and problems in the assessment of fundamental values and risk. Regulators should focus on a gradual implementation of capital regulation and market discipline keeping in view the existence of system-wide disturbances in emerging economies.

Although our study attempts to make some relevant contribution to the literature on emerging markets, it can be extended further to other emerging economies to draw similarities (or dissimilarities) with our findings. Alternate measures of market discipline can be used to extend the analysis. The possibility of the existence of a bi-directional relationship between market discipline and bank risk can be explored in emerging economies.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.