Abstract

The goods and services tax (GST) is a key reform introduced in the indirect tax system of India. This strategic reform aims to improve the revenue performance of the Indian economy through enhanced tax compliance. However, several roadblocks are standing against the effective implementation of GST in India. Thus, the present study aims to identify the prominent barriers faced by business owners while complying with the rules and regulations stated under the GST law. The study employs an interpretive structural modelling approach with the MICMAC technique to examine the association among the GST-related barriers. The smooth and successful GST implementation requires a better taxpayer attitude and tax acceptance, which is essential for voluntary tax compliance. However, the rise in non-compliance indicates that the GST reform has not met the expectations of the tax-paying community. The study’s outcome shows that the lack of skilled manpower and lack of IT infrastructure are root causes and need strong attention from policymakers to take policy action to resolve these barriers in order to improve taxpayers’ compliance levels.

Keywords

Introduction

Indirect taxes play a crucial role in meeting the developmental goals of society through their contribution towards government revenue. Over the past few years, the Indian indirect tax system has undergone several changes, with the most radical reform being the introduction of the goods and services tax (GST). On 1st July 2017, the GST came into existence with the aim of improving the revenue performance of the economy. Indian GST is a comprehensive tax levied on the supply of goods and services, replacing several taxes levied at both the central and state levels. It has subsumed several taxes such as octroi, CST, VAT, entertainment tax, entry tax, and others into a single tax, thereby reducing the cascading effect existing in the previous indirect tax regime. Moreover, the seamless flow of input tax credit throughout the supply chain due to cross-utilization of tax credits between different levels of government will enhance the fairness perception of taxpayers. The complete chain of credit set-off and the transparent mechanism will enhance revenue performance through enhanced tax compliance. Economic unification and following the principle of tax simplification will minimize the compliance burden on businesses. The simplified system reduces compliance costs, thereby improving the cost competitiveness of business concerns. The GST system aims to create a simplified and unified market with harmonization of procedures, rules and rates. Presently, more than 160 countries have opted for different forms of GST. France first adopted the GST in 1954, followed by New Zealand and Canada in 1986 and 1991, respectively. On 1st April 2015, the Malaysian economy implemented GST with the aim of improving business efficiency. Soon after, with a similar objective, the Indian economy witnessed a significant change in the form of the GST. Indian GST is a dual-structured tax where both the central and state governments can concurrently levy GST on the supply of goods and services. Article 366(12A) defines GST as “any tax on the supply of goods or services or both except taxes on the supply of alcoholic liquor for human consumption”. There are certain items that do not come under the purview of GST, such as aviation turbine fuel, petrol, alcohol for human consumption, motor spirit, crude and natural gas. These items are temporarily kept outside the purview of GST and shall be treated in the same manner as before.

International experience shows both positive and negative outcomes of GST implementation. Hakim et al. (2016) revealed that GST adoption had a negative impact on developing economies. The Indian economy, lacking skilled manpower with sufficient tax proficiency and IT sophistication, is facing difficulties in coping with technological advancements regarding compliance with taxation laws (Kumar et al., 2019). To make matters worse, the GST reform is an IT-enabled tax system wherein almost all tax-related obligations, from gaining registration to tax payment, are performed through online mechanisms. For the business community whether manufacturers, traders or service providers, it is challenging to meet the additional requirements in the form of skilled manpower, IT infrastructure and other compliance requirements. A system that changes resource requirements and increases compliance burdens will negatively influence business performance (Jain, 2013). Thus, the assessment of barriers affecting the smooth adoption of GST has become important to improve taxpayers’ perception and GST acceptance levels, subsequently leading to better economic performance.

Theoretical Background

The GST barriers are the downward repercussions standing against the smooth adoption of GST among business concerns (Ghosh, 2022). Tax barriers significantly influence the economic performance of the business and will create an unfavourable attitude towards the GST system, consequently resulting in non-compliance behaviour. These consequences will have an adverse influence on the performance of the businesses (Shinde, 2019). The GST system has brought a radical change in the mechanism by which goods and services are taxed. The GST reform aims to improve transparency and ease of doing business across India (Mehta & Mukherjee, 2021). However, GST barriers will act as a roadblock to these objectives. An efficient tax system would be free from faults and can trigger a better attitude towards the system. Several empirical studies have been conducted on the Indian GST system, covering different dimensions such as GST awareness, GST acceptance, attitudes towards GST, and its impact on the economy. Existing studies used different approaches to explore more about GST. Behavioural models such as TAM, TPB, and SERVQUAL approach have been utilized under different contexts to gain better insight into GST in India (Garg et al., 2018; Shukla & Kumar, 2019). While there are few studies examining GST problems at the business level, no efforts were undertaken to study the priority order of the GST-related problems faced by business owners. Since there has been no standardized approach for measuring GST barriers, the study conducted extensive literature analysis to explore more about the research problem. Existing studies identified different types of barriers faced by business owners in India. The present study focuses on the interaction between barriers that act against effective implementation in India. The study uses the ISM approach to interconnect GST barriers based on their driving and dependence power. The study aims to explore critical GST barriers and contribute more to existing empirical findings.

Literature Review

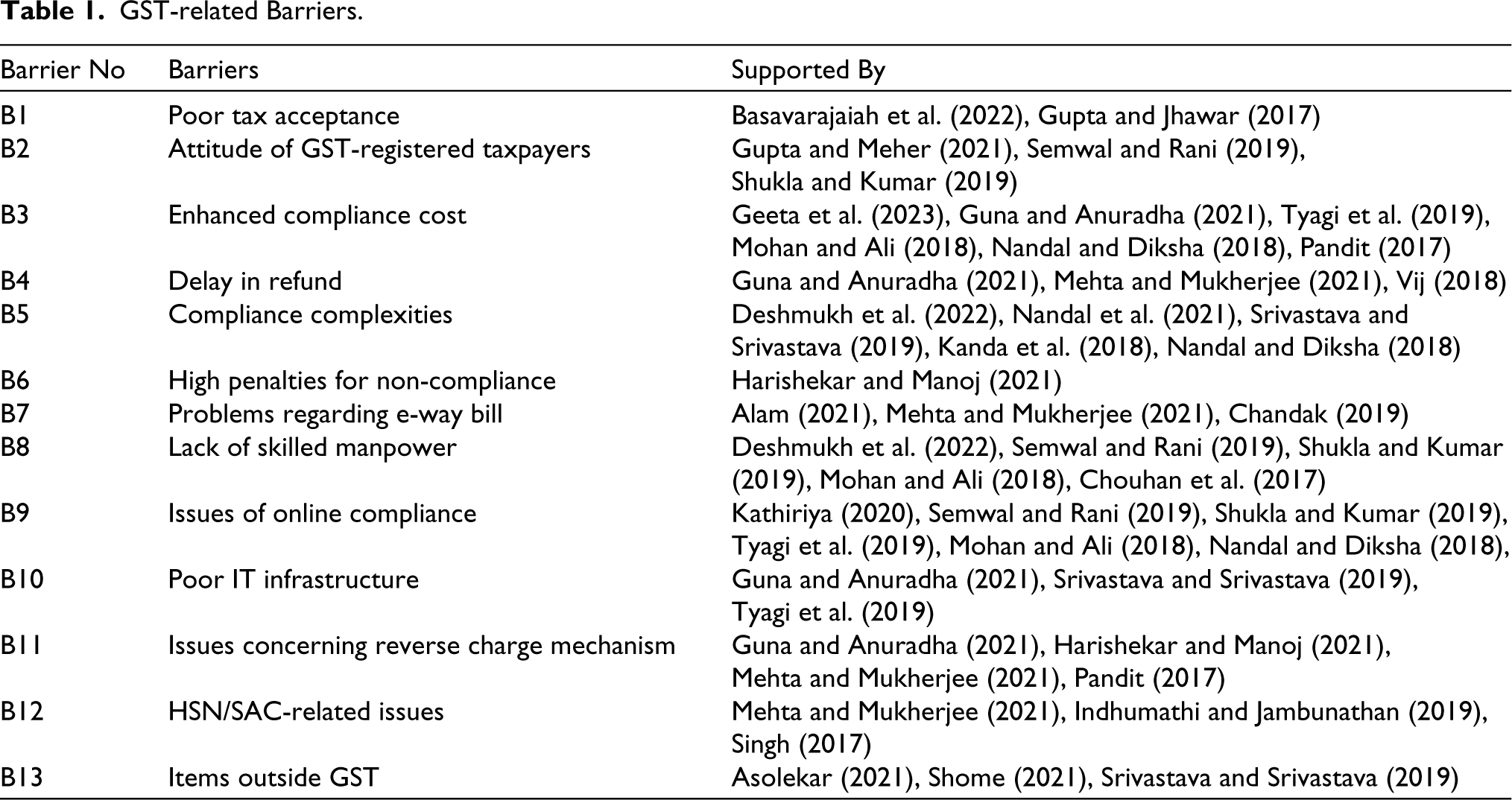

The present section explores the prominent barriers related to the effective adoption of GST in India. Extensive literature analysis identified relevant negative aspects associated with the GST adoption in India. After identifying the relevant GST barriers, a personal discussion session was conducted among 16 GST-registered business owners who had more than 15 years of business experience. The identified factors were shared with business owners who have real-time experience with the rules and conditions stated under the GST law. Based on the selected respondents’ opinions, out of the 17 identified barriers, 13 barriers were finalized. In the next stage, the respondents were requested to indicate the interrelationship between the GST-related barriers. Table 1 reveals the list of 13 GST-related barriers in the context of India.

Poor Tax Acceptance

Tax acceptance refers to the degree to which taxpayers acknowledge the rules and conditions stated under the tax system. It depicts the willingness of individuals to comply with all stated tax obligations. Effective implementation of the GST requires better acceptance among registered businesses. Tax acceptance is influenced by several factors (Deshmukh et al., 2022; Hung et al., 2006). The study by Hung et al. (2006) identified that resource availability, compliance simplicity, and compatibility strongly influence the attitude of GST-registered taxpayers, which in turn affects their acceptance level. Basavarajaiah et al. (2022) found that only a few individuals are in favour of GST, while most are satisfied with the earlier tax system. Garg et al. (2018) emphasize the need to enhance the level of GST acceptance by cultivating a favourable attitude towards the GST system. Shukla and Kumar (2019) also state the relevance of achieving better tax acceptance in order to enhance the compliance level of the SMEs in India. The study suggests that quality improvement can enhance trust in the system, which can subsequently influence the acceptance level of the businesses. Mellouli et al. (2016) revealed that technical factors, trust, and individual determinants significantly influence the level of e-government acceptance. It was also found that tax acceptance is an essential element for the successful adoption of a tax system. Poor tax acceptance may lead to the abolishment of the tax system (Remali et al., 2020).

GST-related Barriers.

Attitude of GST-registered Taxpayers

The negative attitude of GST-registered taxpayers stands as one of the prime barriers to the successful implementation of GST in India (Shukla & Kumar, 2019). Semwal and Rani (2019) identified a moderate level of taxpayer attitude towards GST implementation. Tomar et al. (2018) describe the negative attitude of the public towards GST adoption in India. The negative attitude is mainly attributed to the ambiguities and complexities existing in the GST system. Garg et al. (2018) recommend a strong need for enhancing taxpayer knowledge to achieve a better and more positive perception and attitude towards GST. Strategic involvement in government efforts, such as enhancing service quality, ensuring the availability of adequate IT infrastructure, and emphasizing the importance of enhanced compliance, can transform less favourable attitudes into positive ones (Hung et al., 2006). Bidin et al. (2019) illustrate the relevance of developing a favourable attitude in order to attain better satisfaction levels among business communities. Ramkumar et al. (2023) emphasize the need to improve the attitude of taxpayers towards GST, highlighting the importance of real-time ramifications related to GST for influencing the attitude and behaviour of the tax-paying community. Similarly, Gupta and Jhawar (2017) emphasizes the need to develop a positive perception among the taxpayers for achieving the revenue objective of the economy.

Enhanced Compliance Cost

Unfavourable attitudes towards GST or poor GST acceptance often stems from a poorly framed tax system. A tax system that leads to increased compliance costs tends to create unfavourable tax attitudes (Arora & Singh, 2022). Pandit (2017) illustrated that a rise in compliance costs can be witnessed during the post-GST period. It is argued that shifts in compliance costs result from the level of compliance complexities, frequent changes in tax laws, and restrictions regarding the availment of tax credits (Vishnuhadevi & Bindu, 2022). The study identified that a significant portion of taxpayers’ compliance costs is attributed to consultation with tax professionals. Additionally, businesses that fully adopt computerized accounting systems were found to incur the highest level of compliance costs. Dhillon and Gautam (2022) and Rametse et al. (2020) identified that GST compliance costs are mainly associated with skill acquisition costs, costs incurred for purchasing software and hardware, and time-related costs. Chen and Taib (2017) revealed that GST compliance cost is mainly related to training costs, record maintenance costs, and employee-related costs. An increase in a cost component may affect compliance with respect to return filing and payment of taxes. Enhanced compliance costs may lead to an increase in corporate tax evasion (Agarwal et al., 2022).

Delay in Refund

Delay in GST refunds can adversely affect the liquidity requirements of businesses. Kumar (2019) discovered a significant negative influence of delayed GST refunds on the working capital needs of businesses. The study emphasizes the importance of eliminating intermediaries that may cause delays in obtaining timely refunds. Promoting self-efficacy among businesses can ensure timely compliance and reduce compliance costs for taxpayers. Vij (2018) found that businesses involved in exports suffer adverse effects from delays in processing GST refunds. The study recommends the automation and acceleration of the GST refund mechanism to enhance operational efficiency. Similarly, Mehta and Mukherjee (2021) also revealed that exporters are worst affected by the issues concerning delay in refunds, which mainly includes blockage of working capital. The study recommends the need to simplify the compliance mechanism related to GST refunds. Siddaraju and Muninarayanappa (2020) and Dhillon and Gautam (2022) emphasize the benefits of timely provision of refunds for improving the operational performance of the taxpayers. Kumar and Singh (2023) highlighted the negative consequences of delayed refund on the operational efficiency of taxpayers. The study opines that delayed refunds mainly arise due to technical errors, legal issues, or frauds, or evading practices.

Compliance Complexities

GST complexities encompass various facets, including rules complexity, computational complexity, structural complexity, and compliance complexity (Saw & Sawyer, 2010). Nandal et al. (2021) revealed that overdependence on external assistance indicates the level of complexity within the tax system. Shwetha (2020) found that compared to other countries that have adopted GST, the Indian GST system involves substantial compliance complexities. The study identified the highest complexity index, attributed to the maximum number of changes in legislation. The main complexities within the Indian GST system pertain to return filing, frequent changes in tax provisions, ambiguous tax rules, challenges in record maintenance, and other computation-related issues. Furthermore, the study results indicated that GST complexities significantly influence the compliance behaviour of SMEs. Kumar et al. (2019) identified that ambiguity in GST provisions is a major barrier standing against smooth GST adoption. Deshmukh et al. (2022) raise the need to reduce complexity and confusion in the tax provisions for better GST implementation in India. Mehta and Mukherjee (2021) and Shinde (2019) stress the need to resolve GST design-related issues for enhancing the economic performance of the nation.

High Penalties for Non-compliance

An adequate level of tax penalties is essential for controlling non-compliance behaviour (Farrar & King, 2023; Triandani & Apollo, 2020). However, both narrow or excessive deterrence efforts may adversely affect revenue performance by distorting taxpayers’ behaviour. Excessive tax-related penalties can negatively influence taxpayers’ perception of tax fairness (Marriott, 2022), leading to unfavourable attitudes among taxpayers. Saranya and Malani (2021) identified issues related to penalties and prosecution as the most frequently faced problems regarding GST legislation in India. Lack of knowledge about tax amendments may result in unintentional non-compliance, leading to penalties or other forms of punishment. Nair and Eapen (2017) revealed that tax enforcement initiatives will not always result in enhanced revenue performance. Slemrod (2019) concluded that an efficient tax system should make a clear assessment before taking any enforcement intervention. Roy et al. (2020) recommend the need to relax GST penalties to reduce the compliance burden of the SMEs in India. The study favours an auto-generated system for levying penalties on taxpayers.

Problems Regarding E-way Bill

Kumar (2019) identified several issues associated with the adoption of the e-way bill system in India. The major issues identified were discrepancies in e-way bill provisions between states, difficulties in accessing the e-way bill portal, and lack of awareness among transporters. Additionally, Chandak (2019) found that delays in generating e-way bills and managing multiple bills are the main challenges faced by business operators. Meanwhile, Chaudhuri and Dafria (2022) highlighted high e-way bill-related penalties and a lack of knowledge about e-way bill-related tax provisions as the major barriers faced by MSMEs. The study recommends simplification of the e-way bill generation mechanism and the enhancement of knowledge-building initiatives to address these challenges. Mehta and Mukherjee (2021) pinpoint the lack of knowledge as the main bottleneck acting against the generation of e-way bills. The complexities in the e-way bill provisions contribute significantly to the negative perception of the taxpayers (Kumar, 2019). Lack of uniformity in the e-way bill rules and technical issues faced while bill generation are the main concerns that the government needs to address to improve better adoption of the system (Alam, 2021).

Lack of Skilled Manpower

The availability of skilled manpower is a prime factor for ensuring the smooth and successful implementation of GST across India (Alm, 2017). Kumar et al. (2019) suggest that the Indian GST system requires an adequate number of both accounting and IT professionals for its smooth adoption. The GST reform led to significant changes in the indirect tax system of India, accommodating several major and minor amendments, skilled human resources are essential for timely and accurate tax compliance (Shinde, 2019). Singh (2019) found that one of the major barriers under the GST system is the lack of skilled manpower capable of complying with all tax-related obligations. Similar findings were obtained by Dhillon and Gautam (2022), with the study revealing that the lack of skilled staff is a major challenge faced by MSMEs in India. The study recommends that business owners need to take essential steps to educate employees about GST laws. A skilled workforce is vital for the smooth and successful implementation of the new system among the users (Mukkerla, 2020). Re-skilling the existing personnel with adequate tax knowledge and imparting a better understanding of GST obligations is essential for enhanced compliance (Alam, 2017).

Issues of Online Compliance

The Indian GST is an IT-enabled tax system, where almost all tax-related obligations are met through electronic mechanisms. Taxpayer obligations such as registration, tax credit availment, return filing, tax payment, and other related tasks are required to be performed online (Haines, 2017; Tyagi et al., 2019). Dhillon and Gautam (2022) opine that Indian MSMEs face difficulties in filing online returns. Taxpayers frequently encounter challenges while accessing the GSTN website. Tyagi et al. (2019) revealed that a lack of digital literacy will influence the taxpayer’s decision to adopt an online tax system. Shukla and Kumar (2019) reveal that SMEs across India encounter issues in obtaining GST registration numbers and filing GST returns. The study identifies lack of technical know-how, system complexities, and lack of trust towards GSTN as factors affecting the proper adoption of GSTN among users. The study strongly recommends simplifying the online compliance mechanism and taking initiatives to enhance users’ knowledge to improve acceptance levels. Common online compliance-related issues faced by Indian MSMEs include GSTN server issues, connectivity issues in remote areas, lack of step-by-step information about online compliance procedures, inflexible return filing, and a poor feedback mechanism (Mohan & Ali, 2018).

Poor IT Infrastructure

The successful implementation of GST requires robust and easy-to-use IT infrastructure (Deshmukh et al., 2022; Rao & Nagayya, 2017). Many businesses lacking proper hardware and software find it challenging to comply with online compliance requirements (Kumar et al., 2019; Shinde, 2019). The study conducted by Guna and Anuradha (2021) emphasizes the infrastructural challenges faced by MSMEs while fulfilling the GST obligations. Smaller businesses are particularly affected due to the lack of resources for proper and timely compliance. Pandit (2017) highlights the need for robust IT infrastructure for efficient and easy compliance with GST laws. The successful adoption of GST depends on the level of digital adaptation, which is based on the availability of robust technology and IT infrastructure (Tyagi et al., 2019). Lack of system knowledge and IT infrastructure may act against the smooth rollout of an online tax system in India (Mehta & Mukherjee, 2021). However, the better availability of IT resources and a knowledgeable workforce can overcome most of the compliance-related challenges (Desai et al., 2024).

Issues Concerning Reverse Charge Mechanism

The complexities associated with the provisions of the reverse charge mechanism (RCM) have been a serious concern for GST-registered taxpayers (Pandit, 2017). Ghosh (2022) illustrates the downward repercussion of issues concerning RCM, which mainly includes the negative impact on the working capital performance of the businesses. The obligation of registered businesses to assume the responsibilities of unregistered businesses increases the overall compliance burden of the registered taxpayers (Harishekar & Manoj, 2021). Since the implementation of GST in India, there has been an observed increase in tax evasion, with problems associated with RCM contributing to negative compliance behaviour (Vij, 2018). The bottleneck associated with RCM may result in increased working capital costs leading to increased compliance burden (Harishekar & Manoj, 2021). Mehta and Mukherjee (2021) highlighted operational difficulties related to RCM-related tax provisions. Issues such as the inverted duty structure and the availment of input tax credit to set off RCM-related liabilities pose serious concerns for GST-registered dealers.

HSN/SAC-related Issues

Popat and Raval (2023) noted that GST compliance related to the disclosure of HSN or SAC codes has increased the burden on taxpayers. Since many taxpayers rely on tax professionals to meet their tax obligations, tax advisers or practitioners face difficulties in incorporating HSN or SAC code details into relevant documents such as e-way bills, receipt vouchers, credit notes, debit notes, etc. Mehta and Mukherjee (2021) found that a single product falling under the same HSN/SAC code creates ambiguity in determining the applicable tax rate. Disputes regarding product classification may lead to the incorrect application of GST rates, subsequently resulting in tax litigations. Indhumathi and Jambunathan (2019) raise concerns regarding the non-availability of standardized billing modules capable of accommodating HSN- or SAC-related details. The study recommends the need for a user-friendly billing module that can integrate all business and supply-related details. Kothari (2019) revealed that complexities associated with HSN adoption have increased the overall complexity of the GST system.

Items Outside GST

According to Dhillon and Gautam (2022), several items are kept outside the purview of GST, hindering the smooth flow of input tax credit. Excluding specified products from GST creates compliance difficulties for businesses, as different forms of compliances are required for supplies made within and outside the purview of GST (Vij, 2018). The study recommends including petroleum products under the scope of GST to ensure better economic performance. Similarly, Deshmukh et al. (2022) suggest the need to include petroleum products under the scope of GST for achieving better revenue objectives. Shome (2021) states that the exclusion of items under GST may hinder the availment of tax benefits in the form of tax credits. Non-availment of input tax credit may lead to a cascading effect, eventually increasing the cost of production. Haran and Ojha (2021) highlight the relevance of bringing petroleum products within the scope of GST, and the benefits can be availed in the form of price reduction and elimination of cascading effects. Mukherjee and Rao (2015) illustrate the relevance of including electricity, and petroleum products under GST purview to minimize the issues of cascading effect. The study also revealed that the inclusion of these items under GST would not affect the revenue performance of the states.

Research Methodology

Extensive literature analysis was carried out for identifying the relevant barriers that act against the smooth implementation of GST in India. The identified GST barriers were shared with the GST-registered business owners who have real-time experience with the system. A personal discussion was carried out individually among the participants. The relevant barriers were identified by considering the opinion of the selected participants. The present study adopts the ISM technique to examine the association among the barriers identified (Warfield, 1974). The technique helps to identify the relevant association between the selected elements based on firsthand information collected. The ISM technique has been popularly employed by academicians to study interrelationship between factors associated with tax avoidance, tax ethics, fiscal psychology, and tax audit. The technique is mainly based on transitivity and reachability, where the former states that if “A is associated with B, and B is associated with C, then the rule states that A will be associated with C.”

The steps for performing the ISM technique are as follows:

Identification of barriers affecting effective GST implementation in India. Extensive literature analysis was carried out to identify the barriers. Personal discussion among GST-registered business owners was carried out to retain the relevant items. Relevant associations between the barriers were established based on the data gathered from the participants. The structural self-interaction matrix was developed, indicating relevant pairwise associations among the variables. Next, formation of the initial and final reachability matrix. The hierarchy of the relevant GST-related barriers is determined based on level partition. The partitioned reachability matrix is used for developing a conical matrix wherein the GST-related barriers are arranged based on the position level. In the next stage, a digraph is obtained, which is later used to develop the ISM model, wherein the factor nodes are replaced with statements.

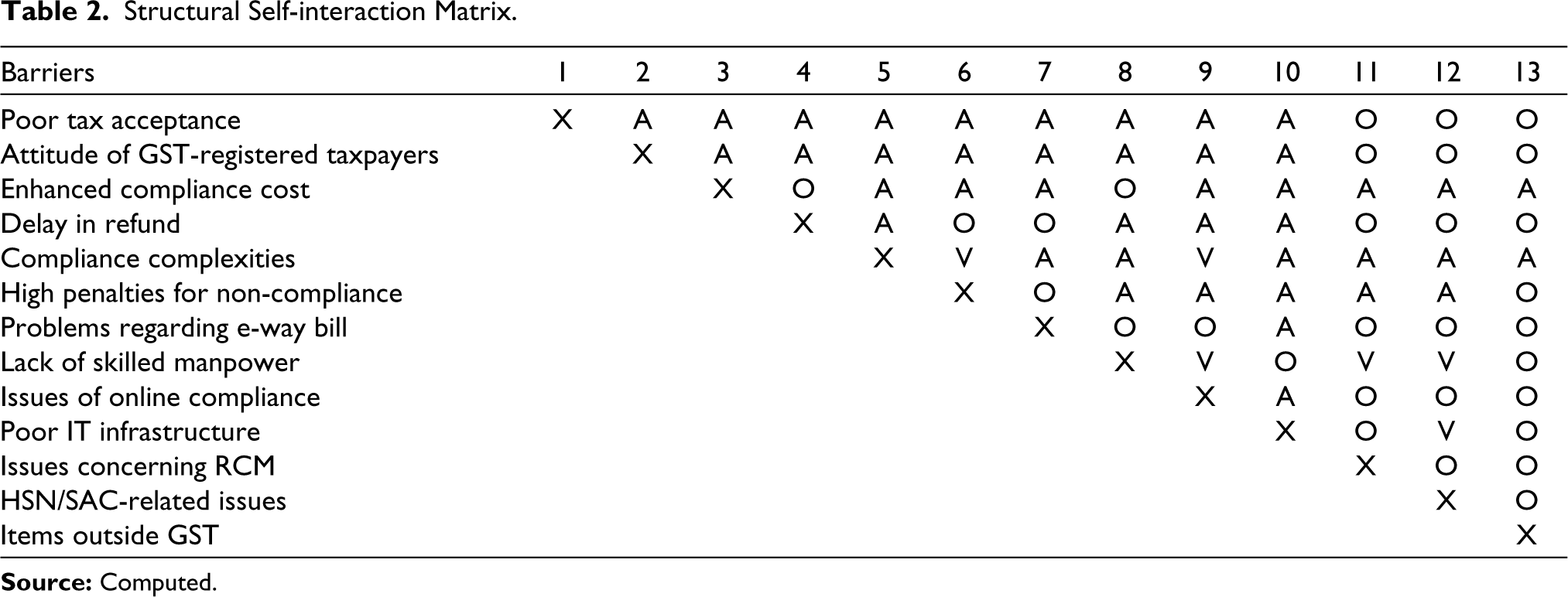

Structural Self-interaction Matrix

Personal discussion sessions were undertaken for establishing the contextual relationship among the barriers standing against effective GST implementation in India. The opinions of 16 individuals from different businesses were used to develop the graphical interconnection among the relevant barriers as shown in Table 2. The study employed led to a contextual relationship to explore more about the GST barriers. For example, a lack of skilled manpower will lead to issues concerning RCM- and HSN/SAC-related issues. Accordingly, the relationship among the other barriers is established. The influence of one barrier on the other was represented using the symbols V, A, X, and O, and i and j denoting the barriers.

V: factor i will influence factor j;

A: factor j will influence factor i;

X: factors i and j influence each other; and

O: factors i and j are unrelated.

Structural Self-interaction Matrix.

Reachability Matrix

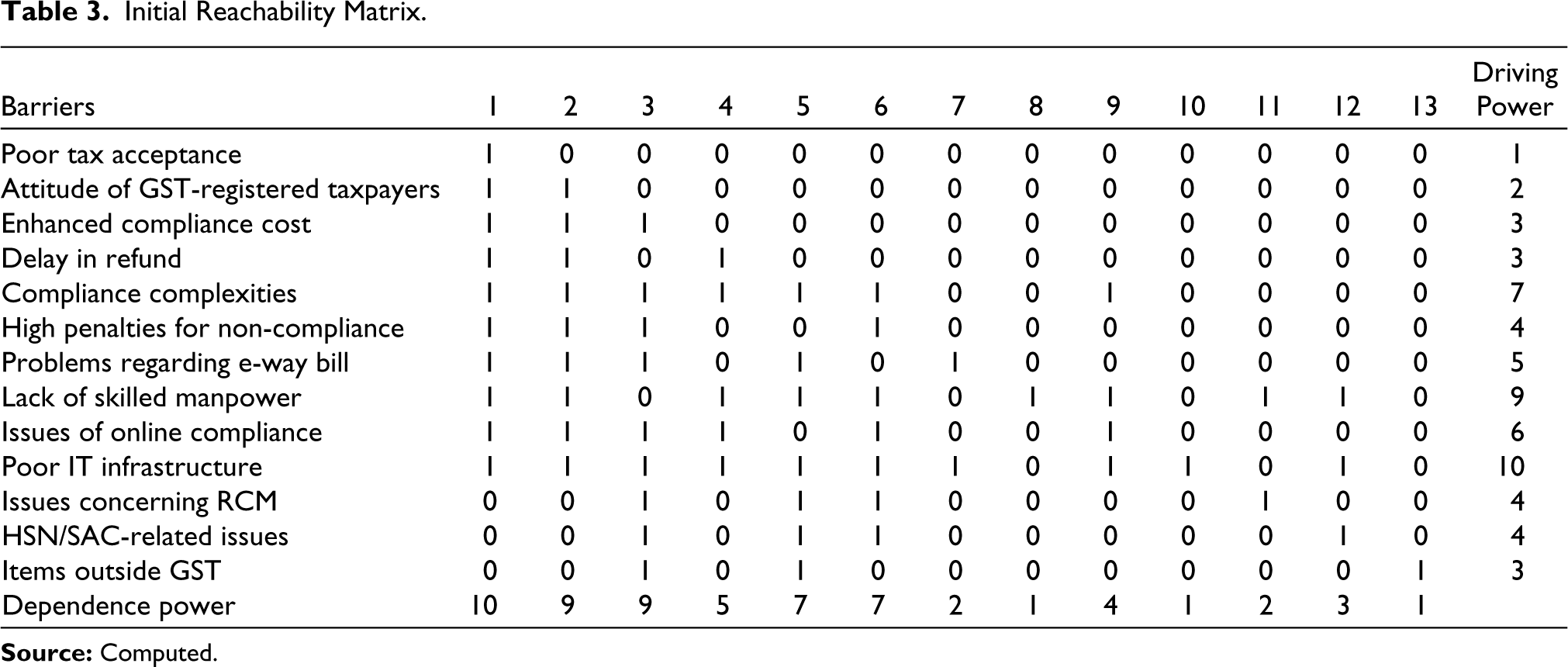

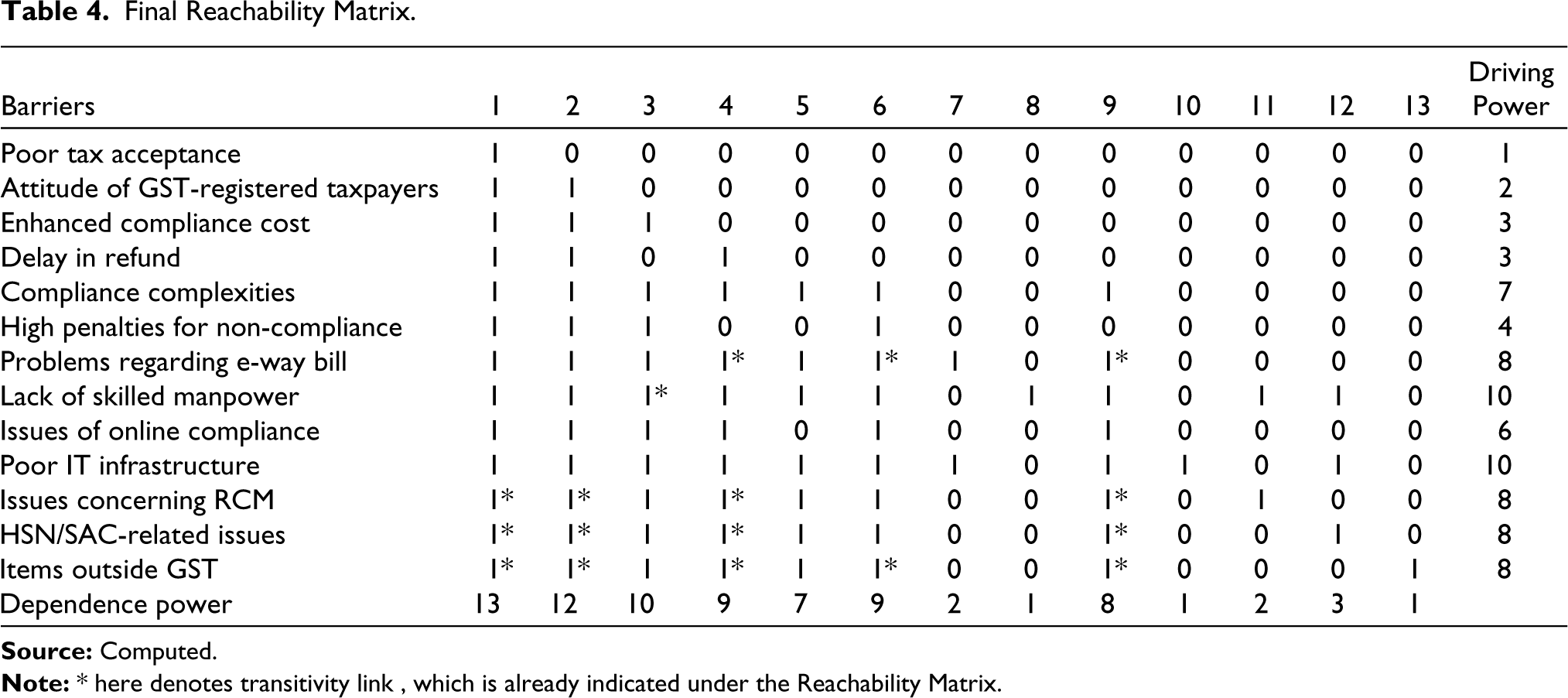

In the next stage, the SSIM is transformed into a reachability matrix. In case the relationship between “i” and “j” is denoted by the symbol “V”, in such a case, (i, j) and (j, i) will be represented by the values “1” and “0”, respectively. In case the relationship between “i” and “j” is denoted by the symbol “A”, in such a case, (i, j) and (j, i) will be represented by the value “0” and “1”, respectively. In case the relationship between “i” and “j” is denoted by the symbol “X”, in such a case, (i, j) and (j, i) will be represented by the value “1”. In case the relationship between “i” and “j” is denoted by the symbol “O”, in such a case (i, j) and (j, i) will be represented by the value “0”. The initial reachability matrix developed based on the stated principle is shown in Table 3. The value “1” indicates that the factor in the row influences the factor in the column. The value “0” indicated that the factor in the row does not influence the factor in the column. Table 4 shows the final reachability matrix. The principle of transitivity is used to develop the final reachability matrix. The transitivity links in the matrix is denoted by “1*”. The table also shows the dependence and driving power of each GST-related barrier. The driving power denotes the sum of barriers which is influenced by a barrier and includes the said barrier, while the dependence power is the sum of barriers which influences the said barrier including the barrier itself.

Initial Reachability Matrix.

Final Reachability Matrix.

Level Partitions

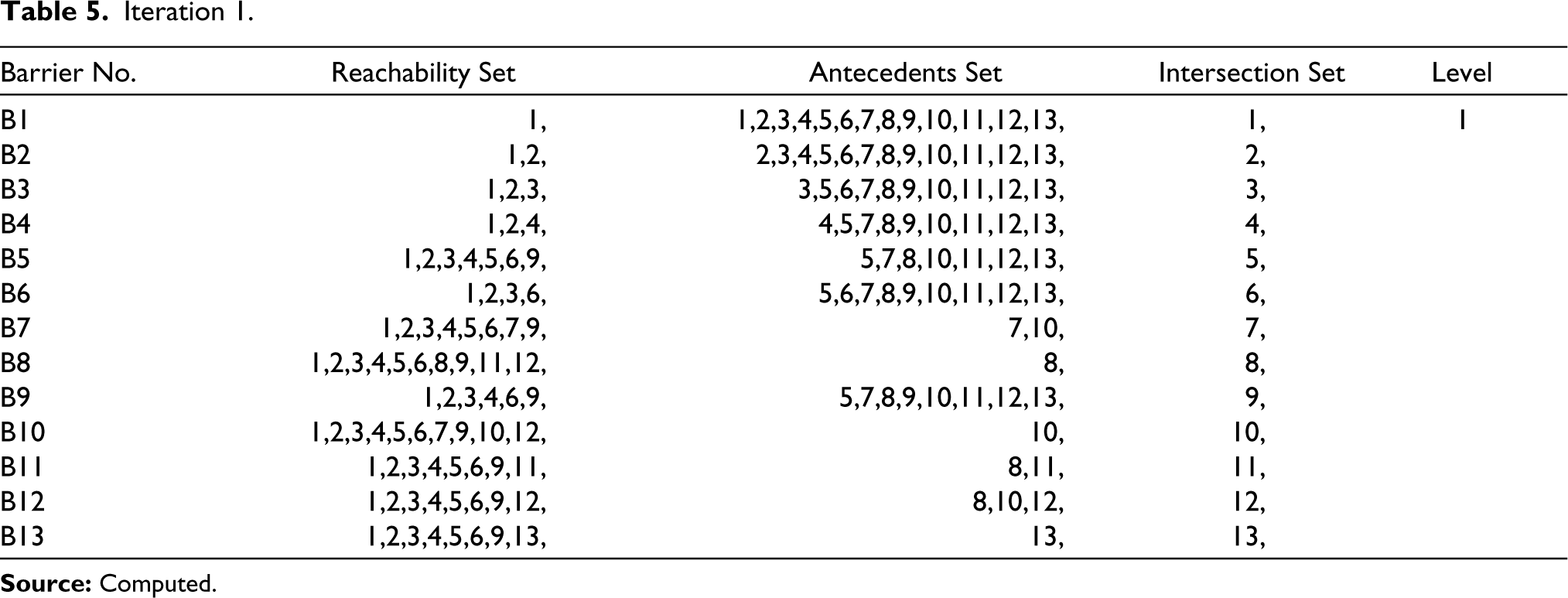

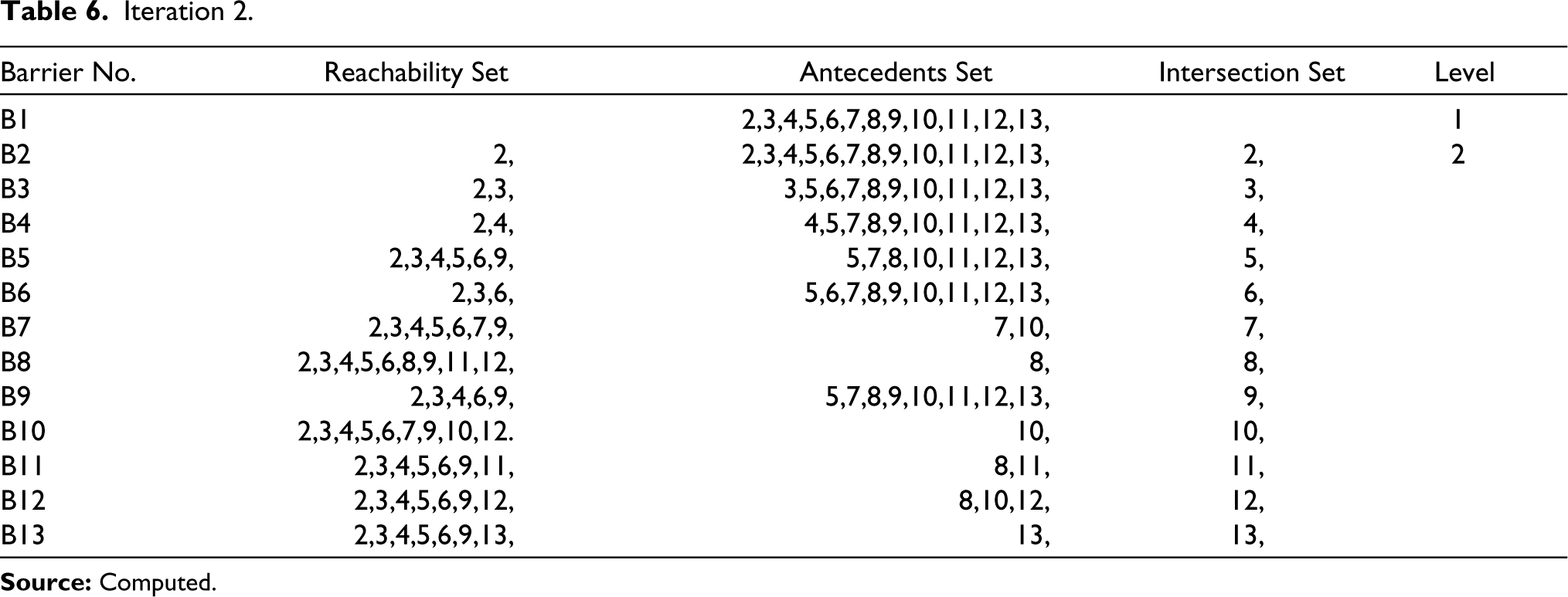

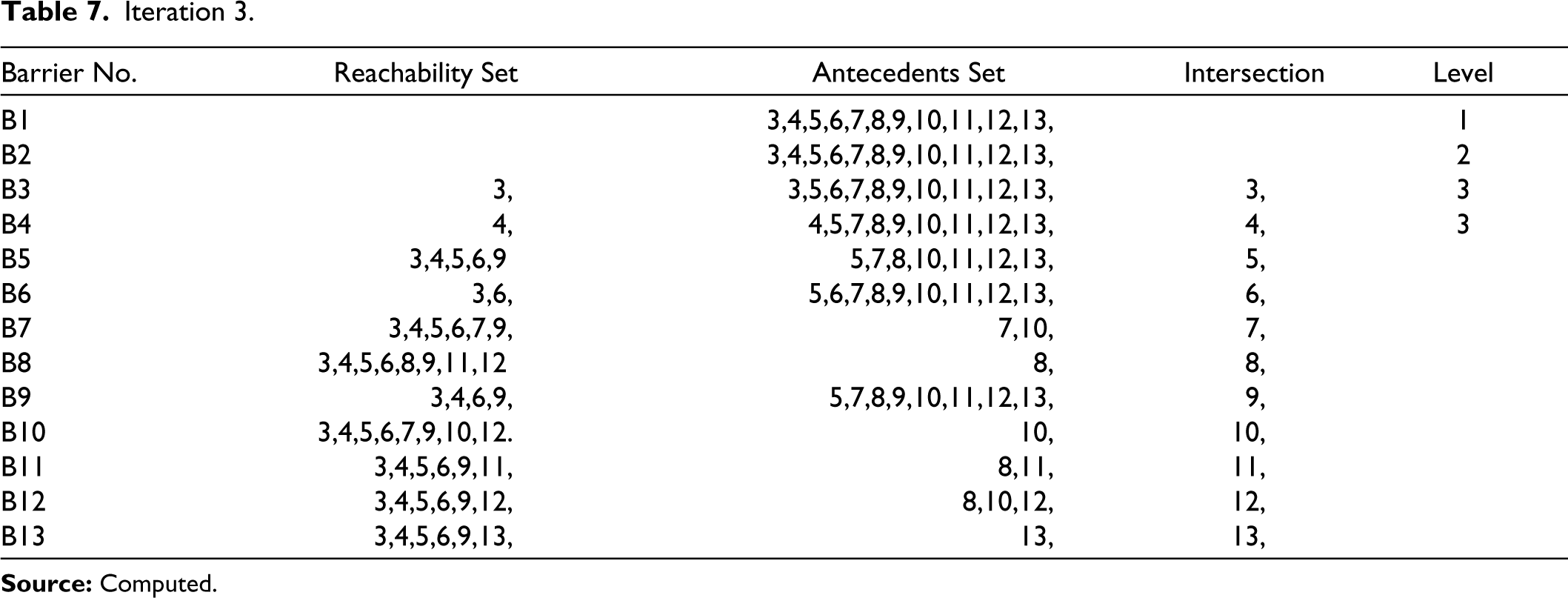

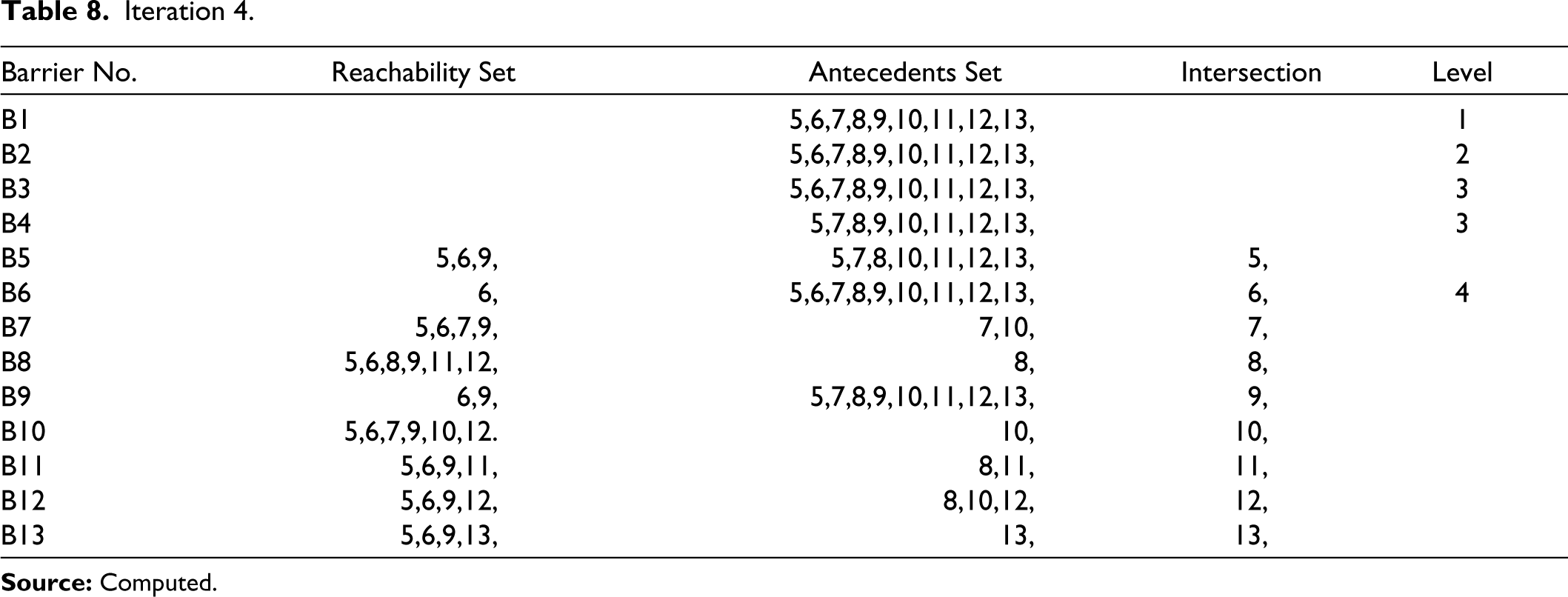

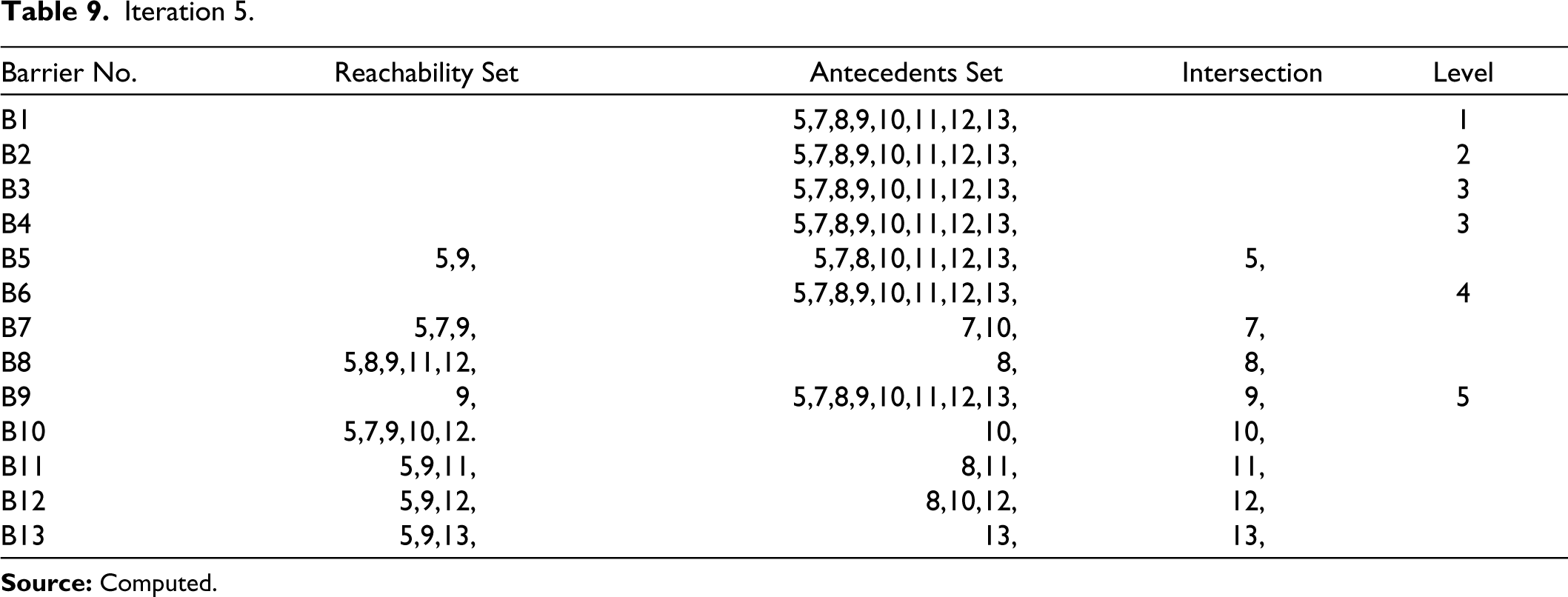

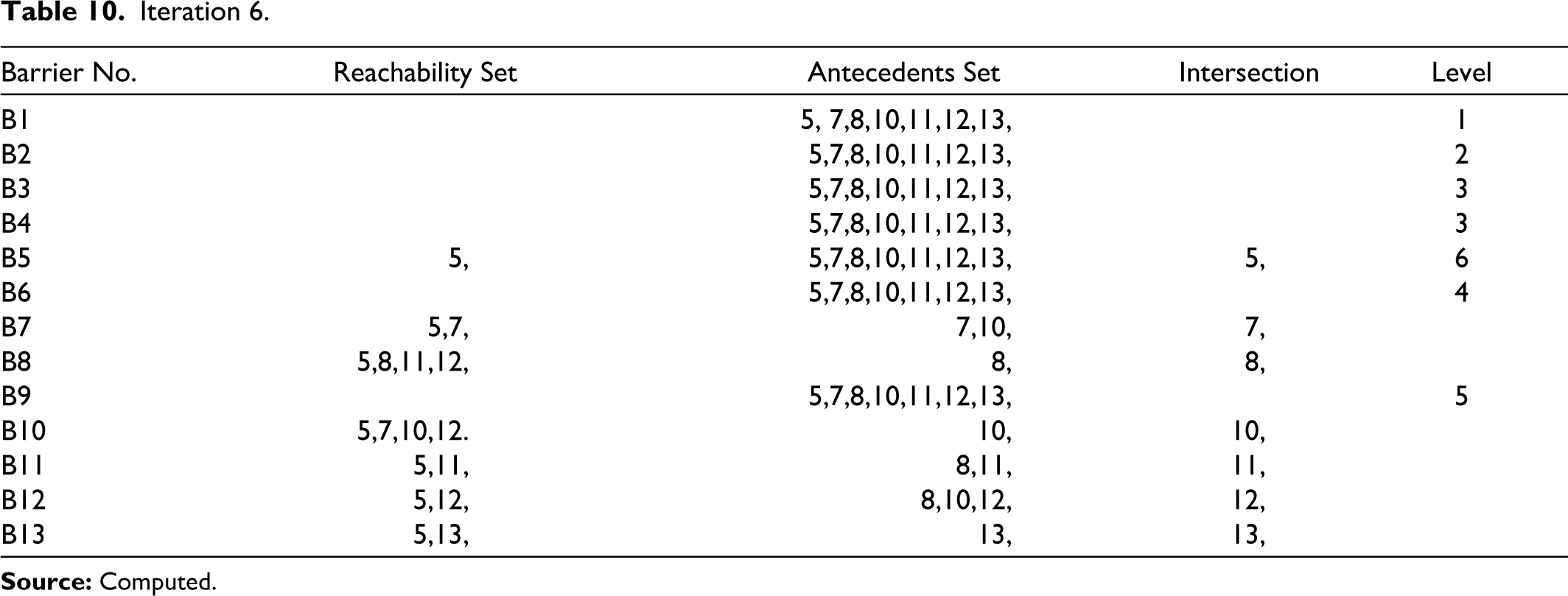

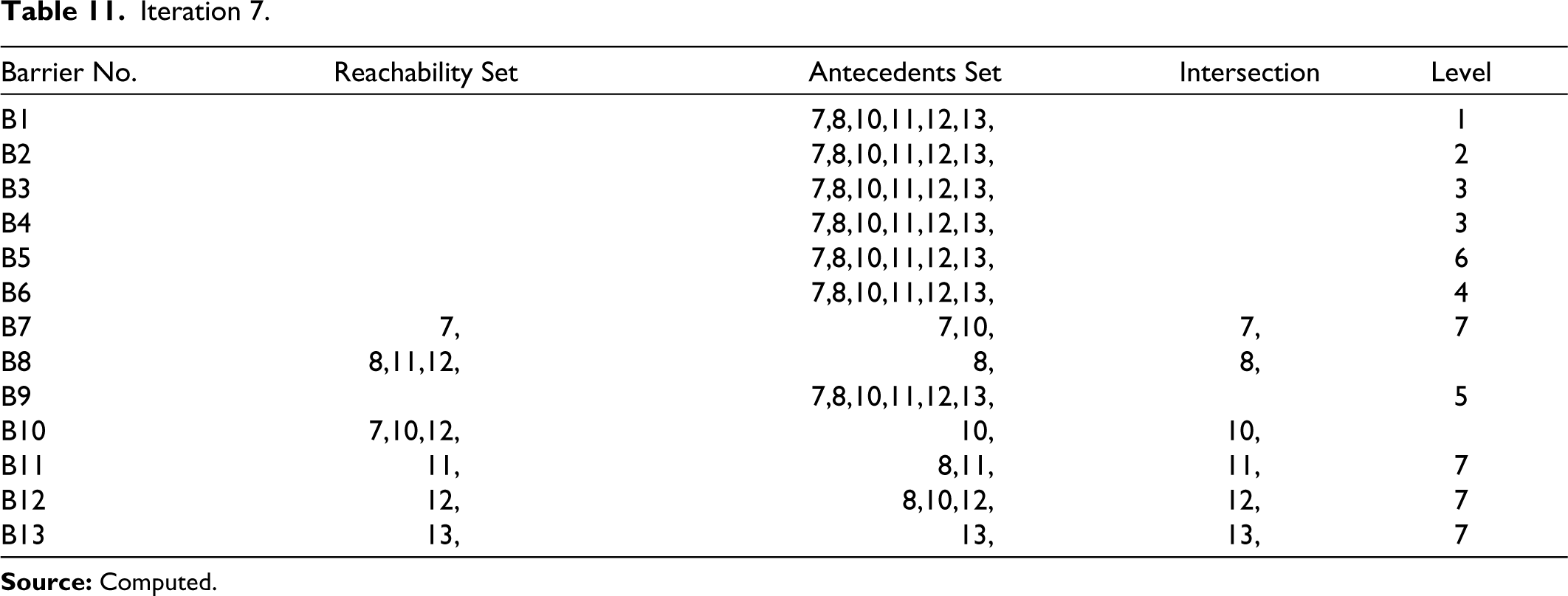

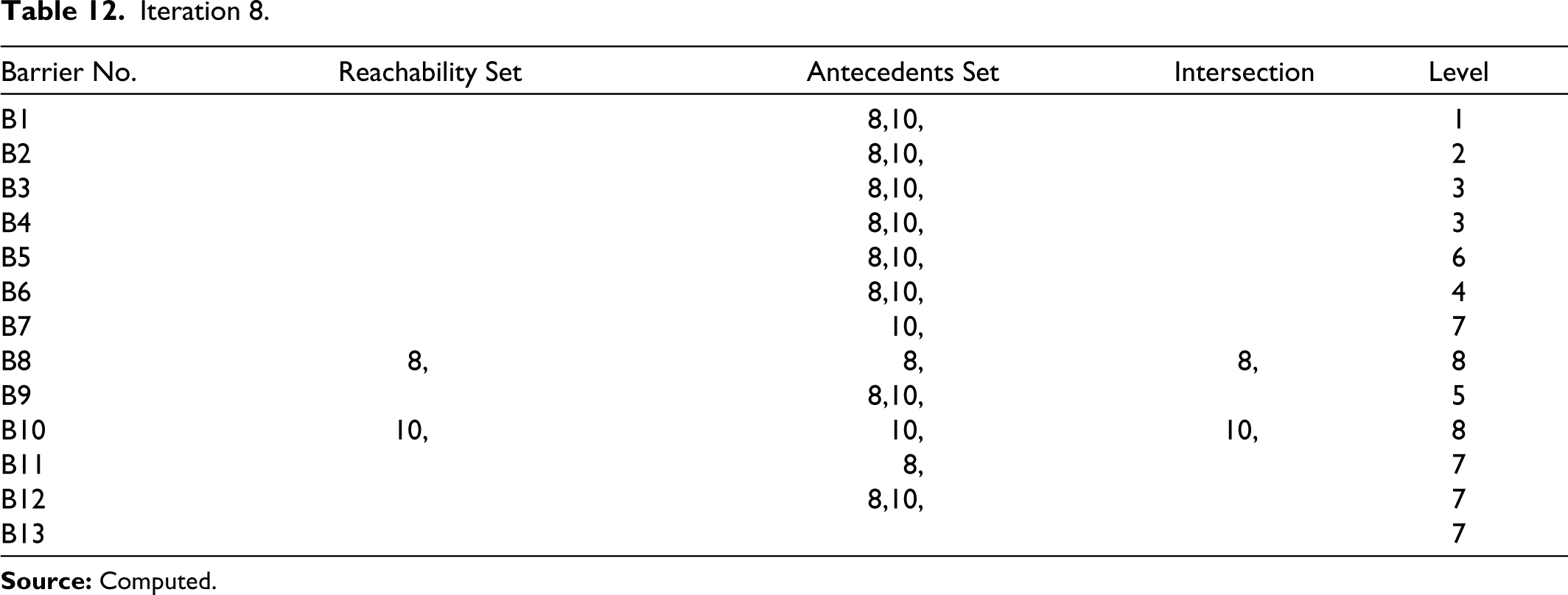

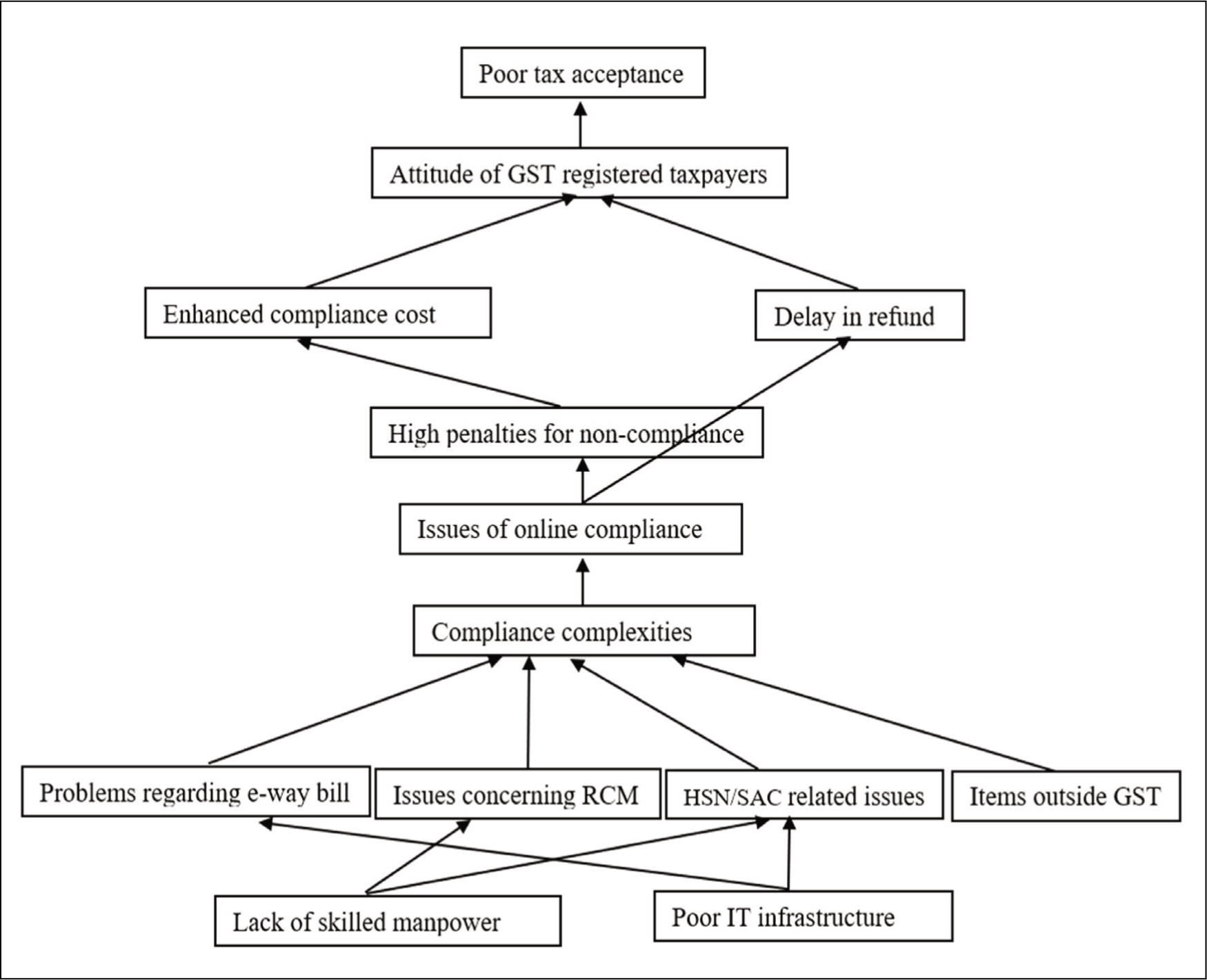

This stage deals with the determination of the levels of the barriers based on the partition of the final reachability matrix. From the final reachability matrix, the reachability and antecedent set is determined for each identified barrier. The common elements in the reachability and antecedent set are shown in the intersection set. The barrier with similar reachability and intersection sets belonged at the highest level in the hierarchy. The highest-level barriers are influenced by several other barriers. In a similar way, the next level below the highest level is determined by removing the topmost level barriers, and the process is continued for developing the hierarchical structural model. The different-level partitioning iterations are displayed in Tables 5, 6, 7, 8, 9, 10, 11, and 12. Table 5 shows that the antecedent set of the barrier B1 “poor tax acceptance” contains all the other barriers including the barrier itself. Thus, it can be interpreted that the barrier B1 is influenced by the other 12 barriers and the barrier B1 itself. Meanwhile, the reachability set of B1 only has the barrier B1 itself, indicating that the barrier B1 does not influence any other barrier. The barrier B1 occupies the highest position of level 1 because of the similarity between the reachability and the intersection set. The second iteration is shown in Table 6. In this stage, the barrier B1 is removed, and the barrier B2 “attitude of GST-registered taxpayers” shows the similarity between the reachability and the intersection set; thus, it has been assigned second position in the ISM hierarchy. Similarly, the other barriers are assigned different levels based on the similarity of the reachability and the intersection set. The third level is occupied by the barriers “enhanced compliance cost” and “delay in refund”, the fourth level is occupied by the barrier “high penalties for non-compliance”, the fifth level by “issues of online compliance”, and the sixth level is assigned to the barrier “compliance complexities”. The seventh level contains the highest number of barriers, i.e., “problems regarding e-way bill”, “issues concerning RCM”, “HSN/SAC-related issues”, and “items outside GST”, and the bottom position is assigned to the barriers “lack of skilled manpower” and “poor IT infrastructure”.

Iteration 1.

Iteration 2.

Iteration 3.

Iteration 4.

Iteration 5.

Iteration 6.

Iteration 7.

Iteration 8.

Building the ISM Model

The reachability matrix and the iteration tables are used for constructing the ISM model. The relationship among the items is represented by an arrow depicting whether a barrier influences the other barriers or is driven by the other barriers. The obtained diagram showing the relationship among the barriers is called digraph. Next, the nodes of the digraph containing the codes B1 to B13 will be replaced by statements, thus forming the ISM model as shown in Figure 1.

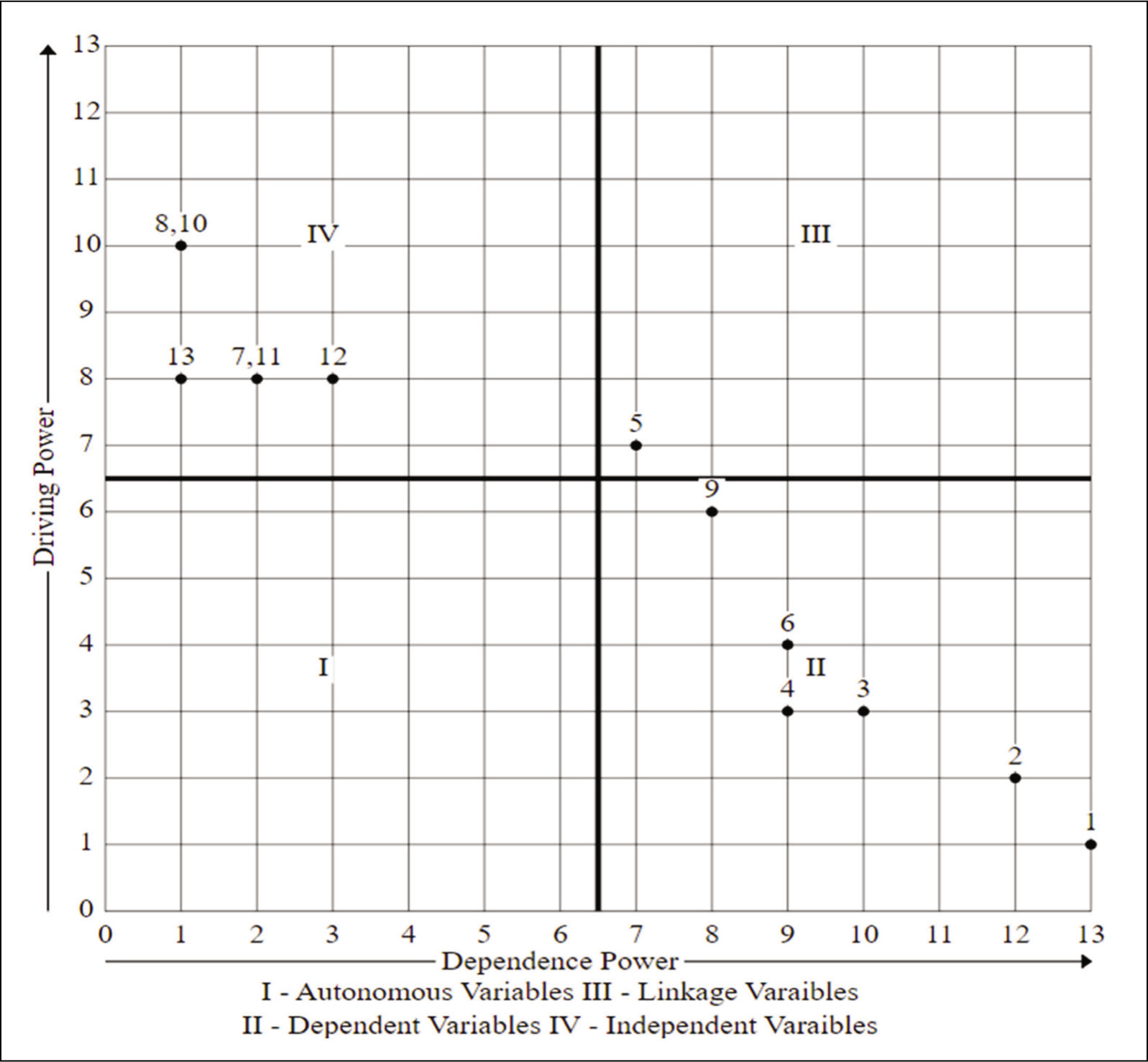

MICMAC Analysis

The MICMAC analysis makes use of the dependence and driving power to categorize the GST-related barriers into four groups. The categories include dependent category, autonomous category, independent category, and linkage category. The x-axis of the MICMAC diagram denotes the dependence power and the y-axis denotes the driving power of the barriers. The first category consists of autonomous variables. The elements belonging to this category have low dependence and driving power.

Figure 2 reveals that there is no element coming under the autonomous category, thereby ensuring that no element is disconnected from the other elements. The second category consists of dependent variables. The element belonging to this category has low driving power and high dependence power. These barriers are strongly influenced by the other barriers, and, thus, need less attention than the other barriers. The barriers “Poor tax acceptance”, “Attitude of GST-registered taxpayers”, “Enhanced compliance cost”, “Delay in refund”, “High penalties for non-compliance”, and “Issues of online compliance” belong to the second cluster of the MICMAC diagram. The third category consists of linkage variables. The element belonging to this category has high driving and high dependence power. These elements connect the dependent and independent variables and, thus, need to be properly managed to reduce the negative consequence of the barriers. The barrier “Compliance complexities” belongs to the third cluster of the MICMAC diagram. The fourth category contains independent variables. The element belonging to this category has high driving and low dependence power. These elements or barriers are the root cause of the ineffective implementation of GST in India. The barriers under the category are “Problems regarding e-way bill”, “Lack of skilled manpower”, “Poor IT infrastructure”, “Issues concerning RCM”, “HSN/SAC-related issues”, and “Items outside GST”.

MICMAC Diagram.

Discussion

The present study delves into the barriers hindering the effective implementation of GST in India. GST-related barriers are crucial for the policymakers, since the policy action to resolve the core GST barriers can lead to better GST adoption. The paper identified the prominent GST-related problems faced by the GST-registered business owners and further explored the interrelationship between the relevant barriers. The findings of the study can guide policymakers and government organizations to prioritize the efforts and resources to eliminate the most severe problems faced by the business community while complying with the GST law. The ISM approach revealed that “Lack of skilled manpower” and “Poor IT infrastructure” are placed at the lowest hierarchical level, which influences the other level barriers. The study findings corroborate the results obtained by Desai et al. (2024), Dhillon and Gautam (2022) and Shinde (2019) illustrating “Lack of skilled manpower” and “Poor IT infrastructure” as the major barriers acting against GST adoption. The study found that the issues due to the compliance complexities need immediate attention (Deshmukh et al., 2022), and the barriers “problems regarding e-way bill”, “issues concerning RCM”, “HSN/SAC-related issues”, and “items outside GST” are the root cause for increasing compliance complexity regarding GST. Mehta and Mukherjee (2021) state that non-availability of skilled manpower and lack of IT resources may cause procedural complexities leading to tax inefficiency. Procedural complexities are mainly attributed to complexities relating to various compliance obligations specified under the GST Act and related to the generation of e-way bills, disclosure of HSN/SAC code, issues pertaining to RCM, and complexities arising due to keeping certain products outside the purview of GST. Earlier studies also highlighted the influence of these barriers on taxpayer’s perception regarding complexities (Kothari, 2019; Mehta & Mukherjee, 2021; Shome, 2021). Saad (2014) provides empirical evidence that procedural complexities may increase the chance of non-compliance behaviour. However, proper strategic intervention in the form of tax simplification or imparting tax knowledge can reduce computational and procedural complexities to a larger extent (Hamid et al., 2022). The barrier of “poor tax acceptance” is placed at the highest hierarchical level, followed by “attitude of GST-registered taxpayers” at the second level, and ‘enhanced compliance cost’ and ‘delay in refund’ at the third level below it. The influence of taxpayer’s attitude on tax acceptance has been previously identified by Garg et al. (2018) and Hung et al. (2006). Fu et al. (2006) clearly state that developing a positive attitude can influence the acceptance level of the system. It is relevant to develop a positive tax attitude, since there is a positive association between tax attitude and tax acceptance. Attitudinal change is possible through the provision of enhanced service quality, imparting tax education and tax simplifications (Garg et al., 2018). The influence of enhanced compliance costs and delay in tax refunds on taxpayer’s attitude is already confirmed by Savitri (2016) and Bobek et al. (2007). Enhanced compliance costs and delays in tax refunds will have negative repercussions on the financial position of the business. This reduction in the economic resources of the taxpayers will create an unfavourable attitude towards GST. The top-level barriers are influenced by the other barriers placed at the bottom levels of the hierarchy. Better GST implementation depends on the initiatives taken by decision-makers to control the bottom-level barriers, which will subsequently reduce the effect of the other level barriers. Policy intervention in its right form can create a better tax perspective and consequently enhance taxpayers’ willingness to comply with tax obligations (Garg et al., 2018; Shukla & Kumar, 2019).

Conclusion

The present study delved into the pertinent factors impeding the seamless implementation of GST in India. The study performed extensive literature analysis and collected expert opinions to determine the relevant barriers and specify the inter-connection between the selected barriers. It was revealed that the barriers “Lack of skilled manpower” and “Poor IT infrastructure” occupy the bottom position in the hierarchy. These bottom-level barriers emerged as the most severe factors contributing to the ineffective adoption of GST among taxpayers, significantly influencing other barriers positioned at higher levels. The barrier “Lack of skilled manpower” leads to “Issues concerning RCM” and “HSN/SAC-related issues”, and the barrier “Poor IT infrastructure” leads to “Problems regarding e-way bill” and “HSN/SAC-related issues”. It is also revealed that the barriers placed at the seventh level, that is, “Problems regarding e-way bill”, “Issues concerning RCM”, “HSN/SAC-related issues”, and “Items outside GST”, exerted influence on taxpayers’ compliance complexities. The GST system brought significant changes in the tax mechanism of the Indian indirect tax system. In addition to the novelty of the compliance mechanism, the system accommodating several minor and major amendments has raised the compliance complexities faced by the taxpayers. The compliance related to generation of e-way bills, disclosure of HSN/SAC codes, RCM-related issues, and multiple compliance because of the items kept outside the purview of GST affect the overall complexities regarding GST. Furthermore, businesses, especially smaller concerns lacking skilled manpower and IT infrastructure, struggle to ensure timely and accurate compliance with GST-related tax obligations. The bottom-level GST barriers will ultimately lead to unfavourable attitudes and, thus, result in poor tax acceptance among the GST-registered taxpayers. These insights underscore the importance of addressing bottom-level barriers to enhance GST implementation effectiveness in India.

The study findings underscore the importance of skilled manpower and sophisticated IT infrastructure for effective GST implementation. Organizing knowledge enhancement programmes and providing robust IT resources can alleviate the compliance burden on taxpayers and foster a positive perception towards the Indian GST system. Additionally, simplifying tax processes related to e-way bills, RCM, HSN/SAC codes, and expanding the scope of GST levy can further mitigate compliance complexities of the taxpayers. With proactive policy action and tax simplification measures, the GST system has the potential to significantly enhance economic performance by increasing compliance levels of the GST-registered taxpayers. The study’s findings provide insights for the government to take corrective action and strategically improve the GST system by focusing on the identified GST barriers.

Limitations and Future Research

The ISM model developed under the study is based on the real-time problems faced by selected GST-registered business owners, thus, the validity of the study results is based on the opinion of a few selected participants. An empirical study based on a larger sample size could provide more robust study outcomes. Extensive literature analysis led to the identification of 13 relevant GST barriers, based on which the ISM model was formed. The scope of the present study can be widened by including other relevant barriers affecting GST adoption among the taxpayers. Moreover, there is scope to include the opinions of other relevant stakeholders such as tax professionals, tax officials, and consumers to gain a better understanding of GST. The present study only specifies the interrelationship between the variables, and the level of intensity of the association or influence cannot be determined using the ISM approach. Thus, further studies can be conducted using more advanced statistical techniques such as regression, factor analysis, and SEM to validate the hypothetical model. Moreover, comparing the outcomes of the present study with results obtained from other analytical techniques such as fuzzy analytic network process or analytic hierarchy process could offer additional perspectives and validate the robustness of the findings. The comparative analysis could further enrich our understanding of GST implementation challenges and potential solutions. Further, the study was not based on well-established theories or models, so future researchers could use behavioural or management models such as TPB, TAM, or IS success model to gain more robust results pertaining to the topic of GST. A theory-driven approach can become a roadmap to find out potential barriers that need to be addressed.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.