Abstract

This article examines the impact of the interaction between institutional investors and large shareholders in value creation process. Our study of Nordic companies from 2001 to 2016 finds a positive relationship between mergers and acquisitions (M&A) initiation and the ownership levels of both large shareholders and institutional investors, while their interaction shows a negative influence. We found no evidence that mergers are driven by value expropriation motives, as the gap between voting and cash flow rights of the largest shareholder has no significant impact on M&A likelihood.

While market reactions suggest potential value expropriation by large shareholders, post-merger performance analysis does not support this hypothesis. Overall, our findings suggest that large shareholders, rather than destroying value, contribute to value creation in Nordic companies, with institutional investors playing a role in safeguarding this process.

Introduction

The influence of concentrated ownership on corporate investment decisions has been extensively discussed in corporate governance literature (Choi, 2018; Kashani & Shiri, 2022). While large shareholders can drive value creation (Wang et al., 2023), their potential to expropriate minority shareholders through mergers and acquisitions (M&As) raises concerns (Crisostomo et al., 2020). This issue becomes more pronounced when their control rights exceed their ownership rights (La Porta et al., 1999; Solomon, 2016).

Large shareholders can use M&As to either create or destroy value in the companies they control. They might potentially expropriate wealth by transferring assets from companies with low ownership rights to those with higher ownership, as seen in previous research (Bae et al., 2002). While existing research examines the roles of both large shareholders and institutional investors, for example, studies on multiple block ownership (Boateng & Huang, 2017; Jiang et al., 2018; Kang et al., 2018), and institutional investors (Dasgupta et al., 2021; Wang et al., 2021), understanding how they interact during M&As remains a significant gap in the literature.

Our study focuses on the impact of institutional investors on the M&A decisions of controlling shareholders in Nordic companies. The Nordic region offers a unique context with significant large shareholder influence and growing presence of institutional investors (Lekvall et al., 2014; Thomsen, 2016). In this study, we investigate whether institutional investors increase the likelihood of value-enhancing M&As in companies controlled by large shareholders. We analyse comprehensive data from Nordic companies over 15 years, including periods before, during and after the 2008 financial crises, to examine the relationship between institutional investors and value-enhancing M&As in companies controlled by large shareholders. The high presence of large shareholders and significant ownership by institutional investors in these companies provides an ideal setting for our study.

Our empirical investigation focuses on three main dimensions: merger likelihood, share performance around announcements and post-merger performance. We investigate whether large shareholders, particularly those with incentives to expropriate value through a high voting-cash flow rights gap, initiate M&As. We also examine if their merger decisions align with the positions of institutional investors and how these decisions relate to the company’s historical performance.

Contrary to concerns about value expropriation, our analysis suggests that controlling shareholders tend to initiate successful M&As, and their interaction with institutional investors does not significantly enhance value. Overall, our findings support the effectiveness of the Nordic corporate governance model, highlighting the role of large shareholders in value creation and suggesting that institutional investors do not necessarily improve M&A outcomes.

Our study contributes to understanding value creation mechanisms in a context with significant large shareholder and institutional investor presence. First, we highlight the importance of studying their interaction dynamics, rather than focusing solely on their individual impacts. Given the challenge of directly observing value destruction due to endogeneity between ownership and performance, our second focus is on the ‘identification’ of the dynamics within M&A setup, when changes in subsequent performance are triggered by deals initiated through interaction between institutional investors and large shareholders.

Third, our study examines multiple dimensions of M&As, including initiation, market reactions and post-merger performance, providing comprehensive insights into the broader implications of large shareholder and institutional investor interactions. Lastly, by focusing on Nordic countries, our study provides insights that can be generalized to settings where ownership concentration is prevalent and institutional investors play a significant role. Our findings contribute to a deeper understanding of shareholder behaviour and governance practices, offering implications for both academic research and practical corporate governance policies.

Literature Review

Our study bridges three strands of literature on corporate governance: the roles of large shareholders in value creation/destruction, institutional investors as minority shareholders and the impact of ownership structure on value creation/destruction through M&As.

Controlling shareholders, due to their high ownership, can either benefit all shareholders by increasing firm value (incentive effect) or prioritize their own interests at the expense of minority shareholders (entrenchment effect). While the former alleviates the principal-agent problem, the latter can lead to value destruction, for example by transferring wealth from one company to another of their choosing (Bae et al., 2002), especially when ownership structures like dual-class shares or pyramid structures are present (Bennedsen & Nielsen, 2010).

In the recent decades, the growing presence of institutional investors has significantly impacted corporate governance. These investors influence firms’ strategic direction through mechanisms like ‘voting with their feet’ (adjusting ownership based on alignment), ‘voice’ (active engagement in governance) and proposing improvements to corporate governance structures (Gillan & Starks, 2003). This engagement reduces information asymmetry, thereby enhancing stock liquidity (Huyghebaert & Van Hulle, 2004), influences executive compensation (Hartzell & Starks, 2003) and promotes better global corporate governance standards (Aggarwal et al., 2011; Guercio & Hawkins, 1999).

While institutional investors can influence corporate governance, their effectiveness varies. Pressure-sensitive investors like banks and insurance companies that may have beneficial business ties with the companies they are vested in are less likely to challenge corporate governance practices than pressure-resistant investors like public pension funds and mutual funds (Bhattacharya & Graham, 2007). Besides, a ‘double agency problem’ arises, as institutional investors themselves are accountable to their beneficiaries, raising questions about their efficiency in generating value through active governance (Allen, 2001).

While institutional investor impact is often studied in companies with dispersed ownership, research on their role in firms with controlling shareholders is scarce. An exception is the study conducted by Hamdani and Yafeh (2013) which found that institutional investors tend to vote only when legally required, with limited opposition to proposals potentially harming minority shareholders. They are more likely to oppose proposals attracting public scrutiny but have limited influence, especially pressure-sensitive investors who align with controlling shareholders.

M&As constitute significant investment decisions for shareholders offering potential benefits like revenue growth via market power and strategic benefits, cost reduction through economies of scale and integration and lower capital costs but also risks like managerial hubris and entrenchment effects by controlling shareholders, leading to either value creation or destruction (Roll, 1986).

Foreign institutional investors are shown to positively influence cross-border M&As, particularly in countries with weaker legal systems, potentially acting as a substitute for local governance (Ferreira et al., 2010). Research suggests that companies with high institutional ownership are more likely to engage in large, cross-border M&A deals with full control over the target (Andriosopoulos & Yang, 2015), but institutional investors with shorter investment horizons are less likely to engage in such deals.

Also, institutional investors with longer investment horizons, as measured by lower portfolio turnover, tend to experience higher abnormal returns during M&A announcements, indicating their effectiveness in monitoring management and protecting value creation (Gaspar et al., 2005). Furthermore, institutional investors may have conflicting interests in M&A deals, holding equity in both the acquirer and target (Matvos & Ostrovsky, 2008). This cross-ownership, however, can positively influence M&A outcomes by decreasing premiums, transaction costs and negative returns, while increasing post-merger performance (Brooks et al., 2018).

Therefore, extant literature provides mixed evidence on the role of large shareholders and institutional investors in value creation or destruction through M&As. Evidence on the role of institutional investors as minority shareholders in firms with concentrated ownership is scarce. Therefore, in this study, we aim at investigating the following questions:

Do large shareholders expropriate value at the expense of minority shareholders via mergers? (Expropriation effect hypothesis). Do institutional investors contribute to value creation through mergers in companies with large shareholders? (Institutional value enhancement hypothesis).

Materials and Methods

Financial and Ownership Data

Annualized financial data for 2001–2016 were collected from four Nordic stock exchanges (Stockholm, Helsinki, Copenhagen and Oslo). FactSet screening helped identify companies, with special attention given to distinguishing single- and multiple-class shares, often verified manually through annual reports. Shareholder information from FactSet was matched across shares for each investor, and voting and cash flow rights were computed. Missing information was manually gathered from corporate annual reports.

To collect data on the largest owners in terms of voting rights, we utilized sources like FactSet, Thomson Reuters Eikon, SIS Agarservice, company annual reports and the Agarna Och Makten book series. For Swedish companies, we primarily used the SIS Agarservice digital dataset (2001–2012), supplemented with the Agarna Och Makten series (2001–2009) for missing delisted share data. Companies and shares were cross-referenced manually across datasets to ensure accuracy. Thomson Reuters’ spreadsheet link facilitated data aggregation for a large number of companies and years. This approach prioritized data accuracy, accessibility and reliability.

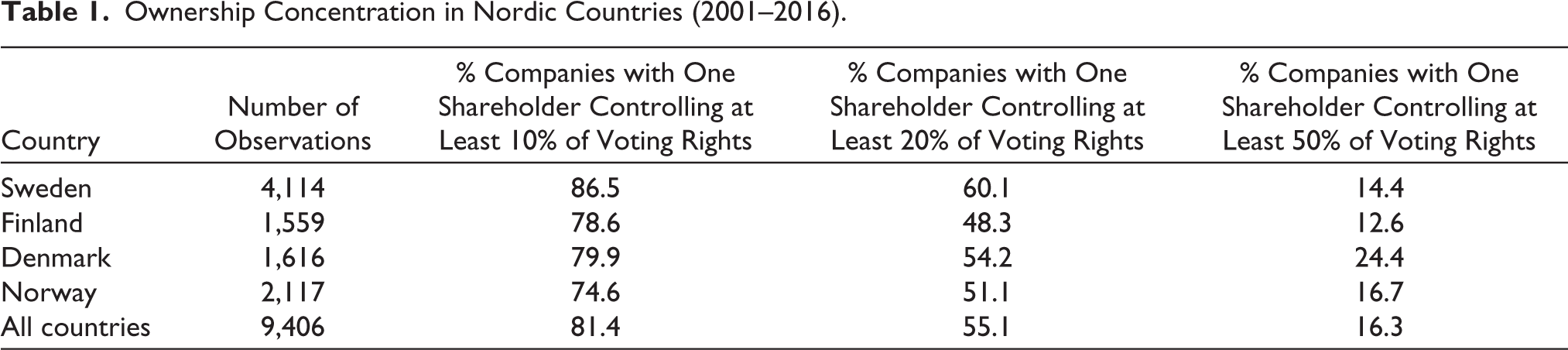

In total, 1,094 companies were included in the sample. Ownership in Nordic companies is rather concentrated as can be seen from Table 1. The highest concentration is observed in Denmark—about one-fourth of the companies—if we count firms with one shareholder controlling more than 50% of the voting rights. Swedish firms too have a high degree of ownership concentration, especially where one shareholder controls more than 10% or 20% voting rights.

Ownership Concentration in Nordic Countries (2001–2016).

M&A Data

M&A data for each company were collected from Thomson Reuters’ M&A deals database (Eikon), including information on announcement date, deal status (rumoured, pending or completed), acquirer/target role, deal type (M&A or investment), pre-deal ownership percentage, percentage shares sought in the deal and deal value in USD. Deals that were rumoured or pending, or classified as investments, were excluded. For each company and year, we selected the M&A transaction with the highest deal value where the acquirer sought more than 50% ownership, resulting in 1,279 M&A observations.

Framework for the Model

As the article investigates the value creation/destruction through the interaction of large shareholders and institutional investors in M&A activities, we leverage existing corporate governance literature and utilize M&A frameworks to analyse their incentives and behaviours. To investigate our research hypotheses, we explore three primary dimensions:

Likelihood of merger occurrence: Examining the motivations and potential conflicts of interest in M&A transactions by companies with large shareholders. Market reaction to merger announcement: Assessing market expectations and reactions to M&A announcements to understand perceived value creation/destruction. Post-merger company performance: Evaluating the long-term impact on company performance and shareholder value.

Standard empirical methods, including regression analyses and event studies, are employed to analyse these dimensions. By integrating theoretical insights with empirical analyses, our estimation model provides a robust framework for examining the dynamics between large shareholders, institutional investors and value creation in the context of M&A activities.

Likelihood of M&A Occurrence

We investigate the role of large shareholders and institutional investors in M&A activity within Nordic companies. We use dummy variables to identify companies controlled by large shareholders (those with over 10% or 20% voting rights), and we analyse the interaction between large shareholder presence and institutional ownership.

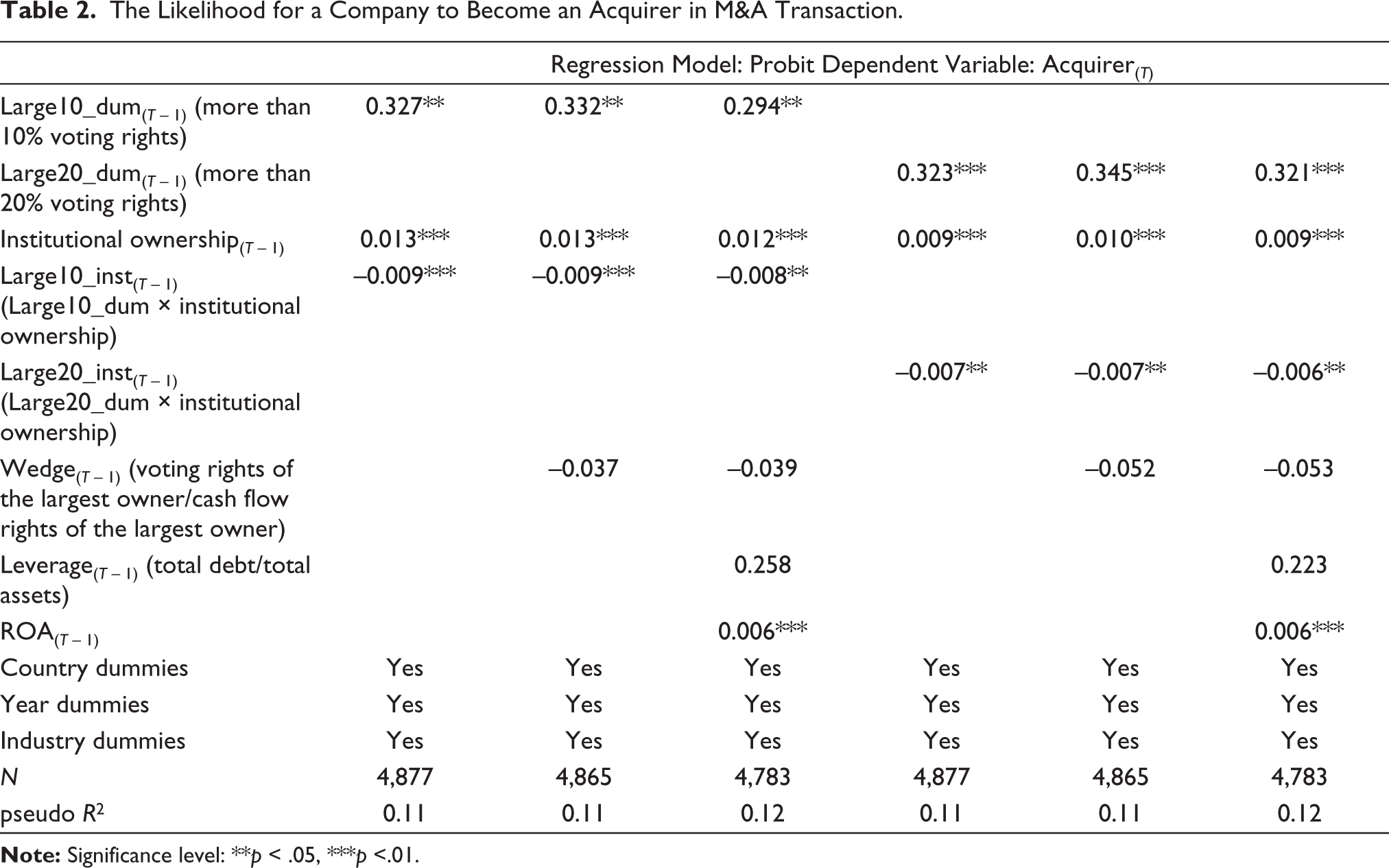

Our analysis employs probit regression models to assess the likelihood of a company initiating an M&A deal. Table 2 reports probit regression results where the dependent variable is a dummy taking the value of 1 if a company was an acquirer in the M&A deal.

The Likelihood for a Company to Become an Acquirer in M&A Transaction.

We incorporate large shareholder dummies to distinguish companies with dominant or controlling shareholders. In countries with dispersed ownership structures, even a 5% ownership stake may confer significant control. However, Nordic companies exhibit much higher ownership concentration, as documented by Lekvall et al. (2014) among other studies. Hence, we use different thresholds for large shareholder ownership (10% and 20%) to ensure the robustness of our findings and examine the impact across varying ownership concentrations. In contrast, we treat institutional ownership as a continuous variable to capture the entire spectrum of changes (including marginal shifts) in institutional ownership. This approach enables us to comprehensively analyse the influence of institutional investors across a range of ownership levels, contributing to a nuanced understanding of their role in corporate decision-making. Finally, our study estimates specifications with levels and interaction of the named variables. While examining the main effects of these variables provides valuable insights, analysing their interactions is crucial for illuminating the main questions under investigation.

This approach allows us to explore not only the individual effects of large shareholders and institutional investors but also their combined influence on M&A activity. By analysing these interactions, we aim to shed light on whether large shareholders and institutional investors share aligned interests when it comes to initiating M&A transactions.

To examine the relationship between financial stability, performance and M&A likelihood, we incorporate leverage, return on assets (ROA), and the wedge between voting and cash flow rights in our regressions. We also include country, time and industry fixed effects. All variables are lagged to mitigate endogeneity concerns.

Our results show that companies with high ownership concentration (Large10_dum and Large20_dum) are more likely to initiate M&A deals. Institutional ownership also positively influences M&A likelihood. However, the interaction term between large shareholder ownership and institutional ownership is negative, suggesting that the impact of large shareholder ownership is diminished with high institutional ownership.

The wedge between voting and cash flow rights does not significantly affect M&A likelihood, indicating that controlling shareholders are not initiating these deals for self-serving purposes. Additionally, high past performance (ROA) is associated with a higher likelihood of M&A activity.

These findings do not support our expropriation hypothesis. While they show that both large shareholders and institutional investors favour M&A activity, they do not indicate whether these mergers ultimately lead to success or failure. We will explore this aspect further in the next section by examining share performance around merger announcements and post-merger operating performance.

M&A Performance

Market Reaction to the M&A Announcement

To investigate share performance during merger announcement days, we compute abnormal returns in the following way:

where ARit is the abnormal return for stock ‘i’ during time ‘t’, Rit is the actual return for stock ‘i’ during time ‘t’ and E(Rit) is the expected return for stock ‘i’ is during time ‘t’.

To compute Equation (1), we estimate the expected return for a particular company or day from the Capital Asset Pricing Model:

where E(Rit) is the expected return for stock ‘i’ during time ‘t’, −RFt is the risk-free rate during time ‘t’ (annual yield to maturity of a 10-year US Treasury Bill), RMt is market return (local benchmark or index identified by FactSet) and βi is the daily price volatility measured by FactSet against a local index (from the latest available date to seven days prior to the M&A deal announcement day).

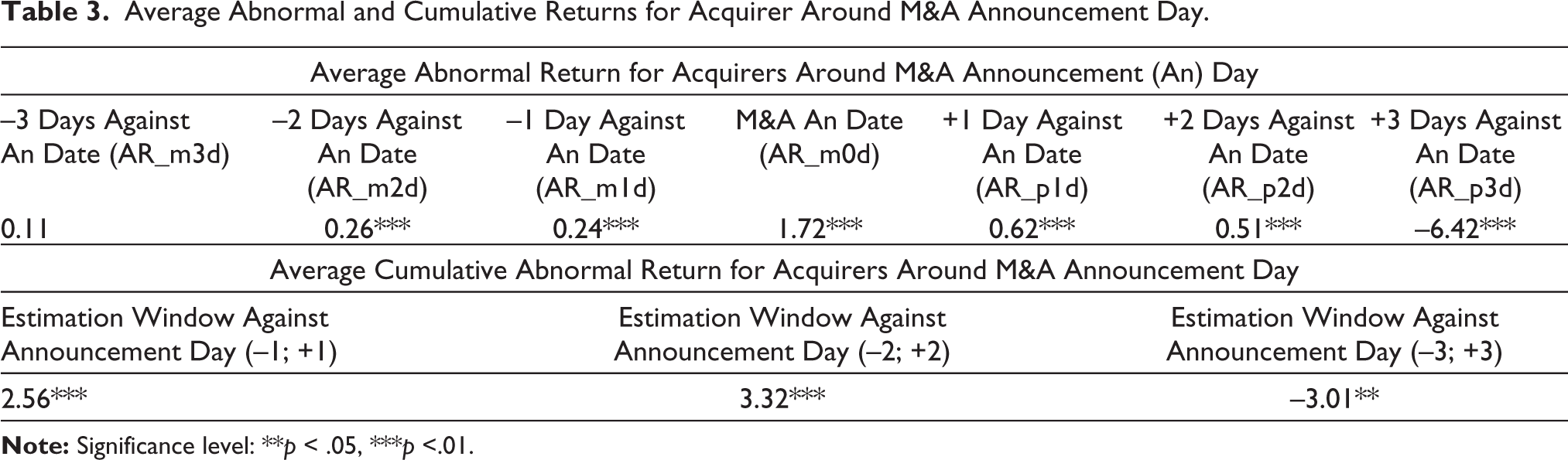

Average abnormal returns for acquirers around M&A announcement day are observed, as seen in Table 3.

Average Abnormal and Cumulative Returns for Acquirer Around M&A Announcement Day.

There is an abnormal return of approximately 2% for acquirers on M&A announcement day. However, there is a drop in acquirers’ abnormal returns three days after the announcement. Table 3 also reports cumulative abnormal returns, that is the sum of abnormal returns during the estimation window. It is highest for acquirers if we regard the closest M&A announcement date window (−1 day or +1 day). Cumulative returns for acquirers are lowest during the (−3 day; +3 day) window primarily because of the drop in their abnormal returns three days after the M&A announcement day. Noteworthy to mention is that the predominantly positive abnormal returns for acquisitions around announcement dates, which we observe, are in line with studies based on non-US data (Ben-Amar & André, 2006; Bigelli & Mengoli, 2004).

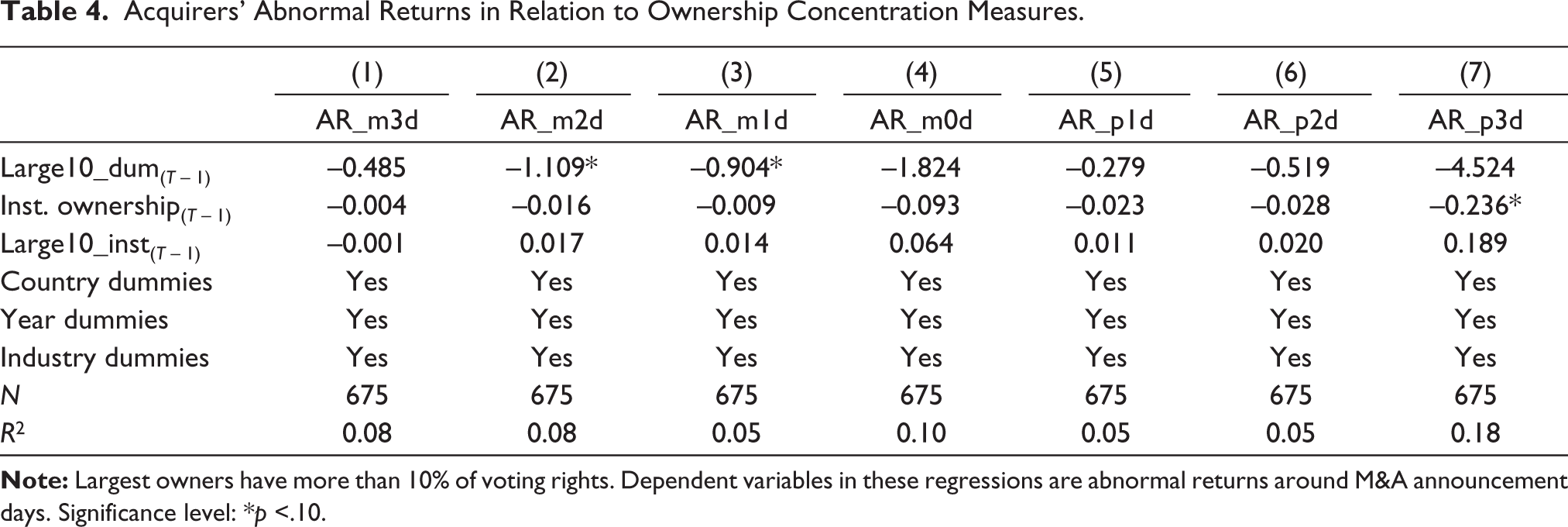

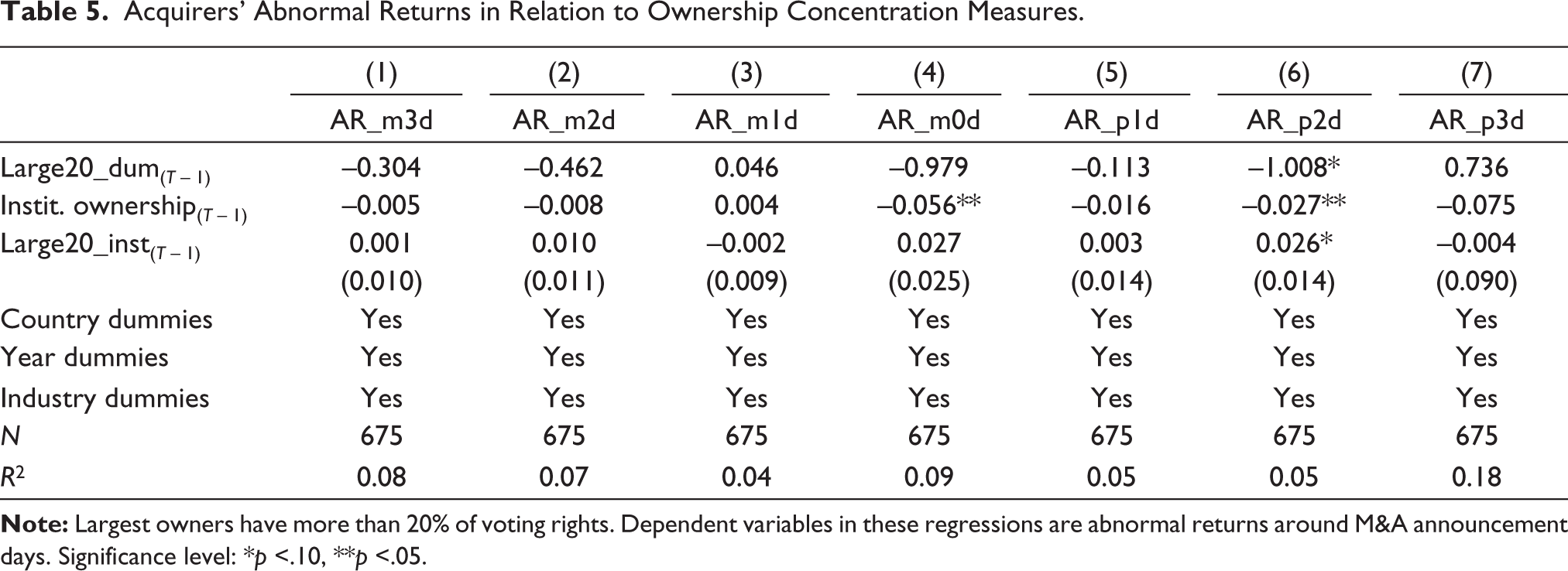

Tables 4 and 5 examine the relationship between abnormal returns of acquirer companies and ownership concentration measures, institutional ownership and their interaction. We control for time, country and industry fixed effects. Due to the complexity of share price movements, we focus primarily on our main variables of interest.

Tables 4 and 5 show negative correlations between abnormal returns and ownership positions of large shareholders (Large10_dum, Large20_dum), specifically 1–2 days prior to the announcement days for Large10_dum variable and 2 days after the announcement days for Large20_dum variable. We also observe instances of a negative correlation between abnormal returns and institutional ownership, observed mostly on the days of or after merger announcements. However, there is a positive correlation between the interaction of institutional ownership and large investor positions (Large20_inst) two days after announcements.

Acquirers’ Abnormal Returns in Relation to Ownership Concentration Measures.

Acquirers’ Abnormal Returns in Relation to Ownership Concentration Measures.

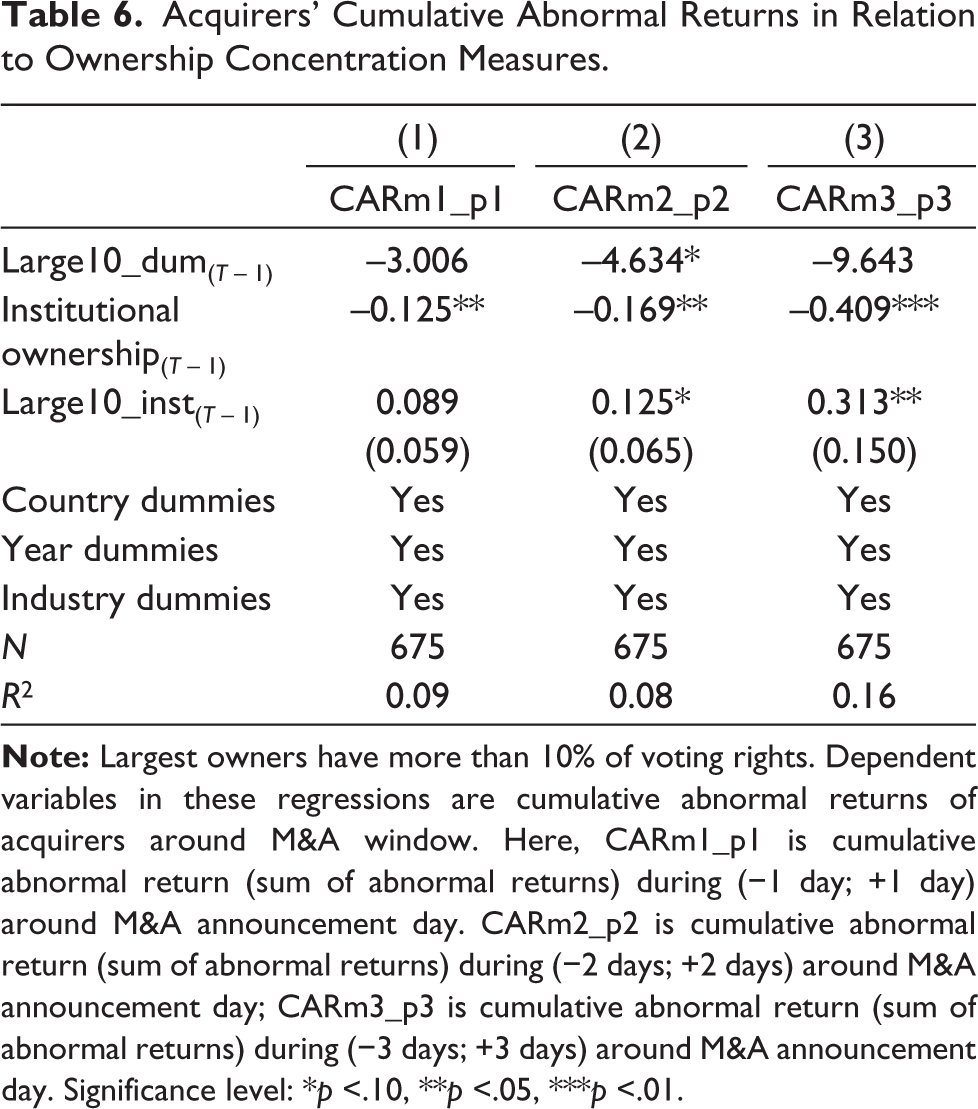

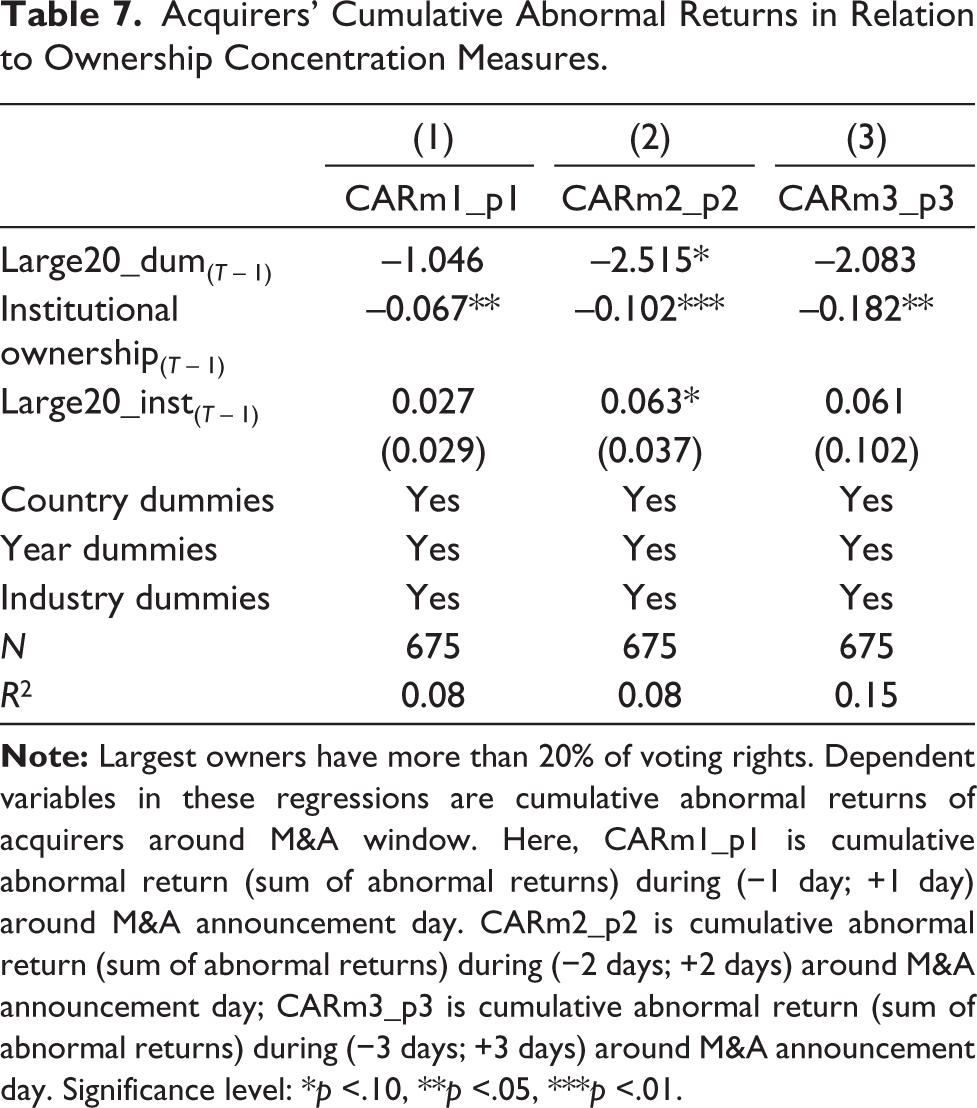

Tables 6 and 7 further reveal that cumulative abnormal returns are negatively correlated with both large investor and institutional ownership around M&A announcement days. However, cumulative returns are higher when large investors and institutional investors interact.

Acquirers’ Cumulative Abnormal Returns in Relation to Ownership Concentration Measures.

Acquirers’ Cumulative Abnormal Returns in Relation to Ownership Concentration Measures.

Thus, in some cases, share performance around merger announcements is negatively correlated with largest shareholder ownership, while the interaction between largest shareholder and institutional investor ownership increases returns. This suggests potential value destruction by large shareholders, potentially mitigated by institutional investors. However, including a wedge variable between cash flow and voting rights does not impact the results, failing to support the value destruction hypothesis. Alternative explanations are explored in the discussion.

Post-merger Company Performance

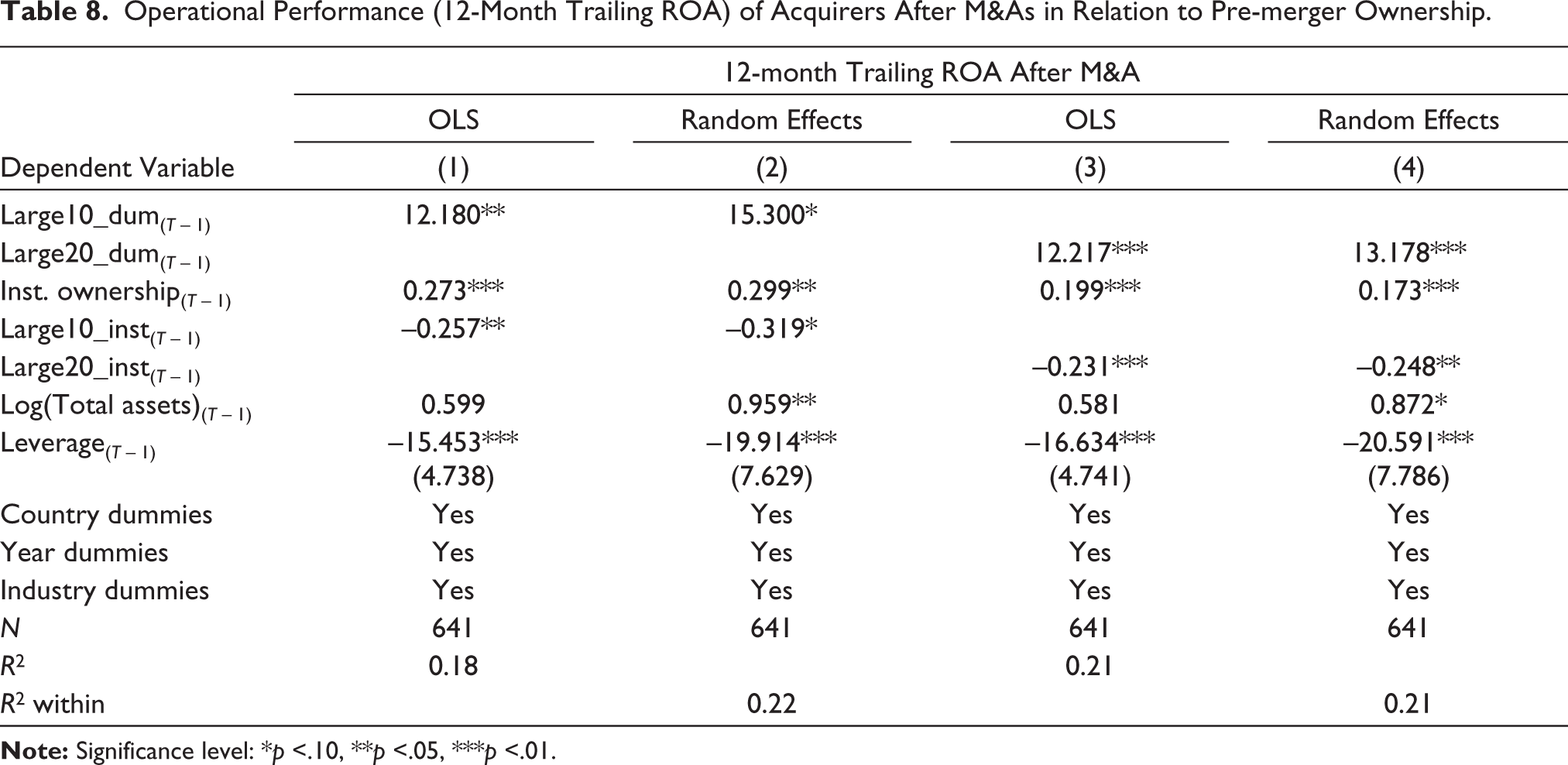

We analyse post-merger performance using 12-month trailing ROA after M&A announcements, regressing it on pre-merger ownership variables, fixed effects for country, time and industry as well as pre-merger indebtedness represented by leverage, and firm size (see Table 8).

Operational Performance (12-Month Trailing ROA) of Acquirers After M&As in Relation to Pre-merger Ownership.

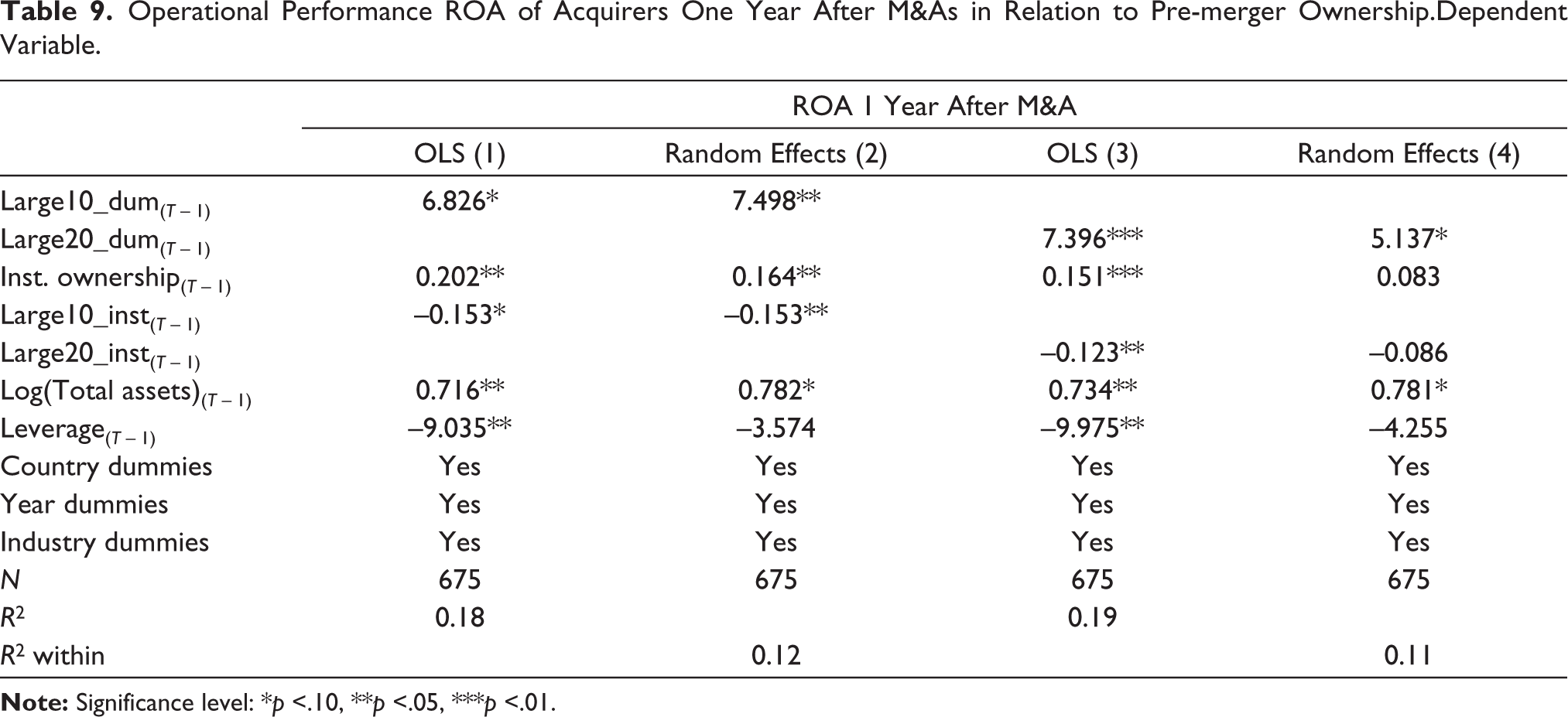

Firms controlled by at least one shareholder who owns more than 10% (or more than 20%) of voting rights perform significantly better after M&As, where these particular companies become acquirers. This is true for all model specifications. Interaction between pre-merger institutional ownership and dominant shareholder dummies decreases the positive effect of large shareholder dummies. If we consider simple annual ROA one year after the M&As instead of trailing 12-month ROA, then our results do not change (see Table 9) except for one specification with the random-effects model (Column 4 in Table 9).

Operational Performance ROA of Acquirers One Year After M&As in Relation to Pre-merger Ownership.Dependent Variable.

These findings suggest that companies controlled by large shareholders perform well post-merger, indicating value creation through M&As. The interaction of large shareholders with high institutional presence lowers post-merger performance, rejecting both our expropriation and institutional value enhancement hypotheses.

Discussion

Our analysis shows a positive relationship between M&A likelihood and ownership by both largest shareholders and institutional investors. This contrasts with Nogueira and Kabbach de Castro (2020), who found a negative relationship in Brazilian firms, attributing it to controlling shareholders’ reluctance to diminish control. They advance the incentive effect argument, suggesting that large shareholders are unwilling to engage in risky ventures such as M&A transactions. However, this argument presupposes that M&As inherently destroy value, as posited by the managerial hubris hypothesis. We also find no support for the entrenchment effect, as there is no relationship between M&A likelihood and the wedge between voting and cash flow rights. Our rationale for this position is that large shareholders may have incentives to expropriate value from minority shareholders through mergers, especially when their voting rights substantially outweigh their cash flow rights. Evidence supporting this would typically manifest as a positive correlation between the wedge and the likelihood of a merger and acquisition, which is not observed in our analysis.

The positive correlation between ownership concentration and M&A likelihood is reduced by the interaction between largest owners and institutional investors. This, combined with our event study and post-merger performance analysis, raises questions about whether institutional investors impact the success or failure of mergers they influence.

Our event study shows that abnormal returns around M&A announcements are negatively associated with ownership concentration and institutional ownership, but positively associated with their interaction. This may suggest value expropriation, but alternative explanations exist. For instance, low liquidity of shares in these companies (Al-Jaifi, 2017; Rubin, 2007) could influence the results, as higher ownership concentration often leads to decreased liquidity (Gaspar et al., 2005), while institutional ownership can mitigate such challenges (Huyghebaert & Van Hulle, 2004).

Post-merger performance analysis reveals that companies with significant ownership by large shareholders exhibit enhanced operating performance after M&As, indicating value creation potential (Boateng et al., 2017). This supports the idea that concentrated ownership provides incentives and power for monitoring management and achieving superior performance after M&As.

Our post-merger performance analysis reveals that the positive impact of ownership concentration diminishes with increasing institutional investor holdings, suggesting that institutional ownership does not necessarily enhance post-merger performance in companies controlled by large shareholders. This, combined with our merger likelihood analysis, leads us to reject our hypotheses: there is no compelling evidence that large shareholders initiate value-destroying M&As, and institutional investors do not enhance value in companies with large shareholders through mergers.

While previous research suggests institutional investors’ positive influence on M&A performance and corporate strategy (Andriosopoulos & Yang, 2015; Brooks et al., 2018; Ma, 2020), our findings demonstrate that this synergy is not consistently observed when large shareholders are involved. Our findings align with Hamdani and Yafeh (2013), who argue that institutional investors play a minor role in companies controlled by large shareholders. Despite legal mechanisms promoting institutional activism, they tend to be active only when legally obligated and rarely exert significant influence, suggesting a generally passive role in corporate governance when large shareholders dominate.

Conclusion

This study examines the intricate relationship between institutional investors and large shareholders within the Nordic corporate governance model, focusing specifically on the context of M&A. Our analysis reveals a strong correlation between controlling shareholders and the initiation of M&A deals. However, the presence of institutional investors, interacting with these dominant shareholders, demonstrably reduces the likelihood of these mergers reaching completion. Notably, the study finds no evidence to support the notion that mergers are initiated solely for the purpose of value expropriation.

A closer examination of abnormal returns surrounding M&A announcements reveals a complex interplay. Initially, the presence of controlling shareholders appears to be associated with negative returns, while interaction with institutional investors correlates with positive returns. However, further nuanced analysis challenges the notion of value expropriation. Moreover, our investigation into post-merger operational performance indicates that M&As initiated by controlling shareholders tend to be successful, with no additional value created by the interaction of institutional investors.

These findings resonate with the core principles of the Nordic Corporate Governance model, which emphasizes the role of large shareholders in safeguarding value creation. Contrary to expectations, the study suggests that institutional investors do not necessarily contribute to the initiation of more beneficial M&A activities in companies dominated by large shareholders.

The policy implications of this research are significant. While protecting minority shareholder rights is crucial, it is equally vital to preserve the effective monitoring role of large shareholders, particularly in concentrated ownership structures like those prevalent in Nordic countries. Enhancing transparency and disclosure across corporate activities is essential for reducing market uncertainties and strengthening investor confidence. However, overly restrictive regulations could potentially hinder the ability of large shareholders to effectively oversee management.

Policymakers must acknowledge the diverse capabilities and motivations among different types of institutional investors. Not all institutional investors possess the same expertise or commitment to influencing corporate governance outcomes positively. Consequently, policies aimed at fostering institutional investor engagement should recognize their autonomy in choosing their actions based on their specific knowledge and objectives. Regulatory responses need careful calibration to avoid unintended consequences that might stifle investment or innovation, particularly within well-functioning governance frameworks like those observed in Nordic companies.

Our findings underscore the importance of tailored policy interventions that prioritize transparency, effective shareholder oversight and strategic engagement with institutional investors. This approach aims to optimize corporate governance practices and foster sustainable value creation for all stakeholders.

Limitations of the Study

The analysis in this article encounters several limitations that warrant careful consideration. One significant concern is the generalization of institutional ownership. It does not differentiate between various types of institutional investors (e.g. pension funds, mutual funds), potentially overlooking their distinct influences on corporate governance and M&A outcomes. Future research could analyse each type separately.

Another critical limitation relates to endogeneity. Despite efforts to mitigate it, the study faces challenges in establishing causal relationships due to potential omitted variable bias and reverse causality. More robust methodologies like instrumental variable approaches could be employed in future studies.

The study focuses on M&A transactions from 2001 to 2016, excluding more recent developments like Sweden’s post-2017 IPO market and the COVID-19 pandemic. Exploring these trends could provide further insights.

Moreover, the study focuses on ownership concentration and institutional investors, neglecting other influential factors like regulatory environments, industry-specific characteristics and managerial motivations. Future research could integrate these variables for a more comprehensive understanding of the complexities involved in M&A transactions and corporate governance in companies.

Addressing these limitations would enhance our understanding of the influence of institutional investors and ownership structures on corporate governance, M&A activities and firm performance in dynamic economic environments.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.