Abstract

National Highways (NHs) are key facilitators of sustainable growth and development. NHs have a multiplier effect on overall growth, industrialization and urbanization. A key challenge is that the investment that manifests, in terms of savings, deposits and bank credit, is highly endogenous. In such a scenario, a pertinent question arises: Do NHs have an impact or a mirror effect on bank credit? We skirt the problem by investigating the impact of the NH on bank credit. We study this research question by using NHs, examining the growth of banks in the treatment districts (districts within 10 km of an NH) and the control districts (districts beyond 50 km of an NH). We adopted panel regression with fixed effects and long difference estimation to analyse the research problem. The results from the districts that are within 10 km of an NH have a positive association with bank credit and aggregate deposits. This fosters the belief that bank credit and aggregate deposits respond to the development of infrastructural projects such as NHs. In conclusion, the study investigates an empirical association between the construction of NHs during the period between 2014 and 2022 and the local financial sector. Our results are helpful for policymakers and the National Highway Authority of India in evaluating the impact of infrastructural investment on access to banks in the context of an emerging economy. Our results indicate that an NH has a positive impact on the financial sector, but there is still a long road ahead.

Keywords

Introduction

National highways (NHs) are key facilitators of sustainable growth and development. The importance of NHs is rarely questioned. A well-connected NH expands the productive capacity of the country by increasing the mobilization and productivity of available resources. It increases labour mobility. This assertion is straightforward, and there are many ways to justify it. First, a well-developed NH is almost an unpaid factor of production (Pradhan & Bagchi, 2013) and facilitates the circulation of money in the economy. Second, on most occasions, a well-connected NH makes an existing factor of production more efficient and productive. Most importantly, the NH acts as a magnet for the development of microfinance and banking institutions. This concept is known as an ‘agglomeration phenomenon’: infrastructural development attracts resources from other regions.

A well-connected NH and developed banking institutions exert a positive influence on the local economy by significantly raising aggregate demand. In short, the NH has a multiplier effect on the economy. The growth of an NH has a complementary relationship with a rise in public investment. NH construction attracts public investment, in which microfinance and banks act as facilitators. In the absence of NHs and banks, public capital does not percolate in the local economy, leading to a decrease in public investment (Gifford, 2003).

In India, NHs only account for 2% of the total road network. This modest road network carries 40% of the passenger and freight traffic in the country. So, it is important to improve the road network for the economic development of India. The lack of multimodal logistics leads to recurrent and high transportation costs, and the efficiency of operations is reduced unexpectedly (Adhana, 2015). This lacuna can be addressed by the development of banks and financial institutions.

Existing literature review found construction of NH was mostly funded by banks closer to the connecting NH. In short, banks within 10 km of NH aided the extraction practices, such as river sand quarrying, water extraction from underground and ground sources and earth excavation, leading to irreversible damage.

Banks and financial institutions mitigated the risk of road topography. Topography construction in flat plains and rolling terrains affects the drainage systems, leading to floods, overtopping and soil erosion, and in mountains with steep slopes, it entails an increased risk of landslides and debris storage (NHAI Report; No, 2015). To solve the problem, banks closer to the NH and Government of India initiated the Gati Sakti initiative. The programme focuses on improving last-mile connectivity. Therefore, financial institutions aided in NH sustainability.

Banks along with the government conceived sustainable construction through recycled asphalt, solar blinkers and solar energy panels, low-emission concentrates, recycled plastic and fly ash, efficient toll management and roadside platforms (Chakrabarti, 2018; Gifford, 2003). Banks and the Government of India worked on a comprehensive and holistic strategy for road safety audit mechanisms (Nagesha & Gayithri, 2015).

A concessionary develops an NH project in four modes. They are as follows: (a) the ‘Build, Operational and Transfer’ toll mode; (b) the ‘Build, Operate and Transfer’ annuity mode; (c) the Engineering, Procurement and Construction hybrid mode; and (d) the hybrid annuity mode (Nagesha & Gayithri, 2015). Moreover, the Government of India along with banks have taken proactive measures to minimize the negative impacts of NH on the environment.

One of them is to build a resilient ecosystem that is named ‘Green Corridors (GC)’. The Green Corridors will adsorb the dust particles and increase the consumption of oxygen (O2) in the environment (Rathore, 2011). The basic idea is to create plantations across roads and improve the micro-climatic conditions, such as air quality and soil quality. All these initiatives address the three pillars of sustainability: environment, economy and society (Jaiswal et al., 2021). One of the flagship projects to incorporate GC has been the large-scale use of plastic waste in the construction of rural roads, along with the promotion of other local materials for building ecologically sustainable roads. For example, a 40-km stretch along the Mumbai–Nashik national highway was turned into a carbon sink. But with banking interventions, it now serves as a natural reservoir that stores carbon-containing chemical compounds that have been accumulated over an indefinite period of time.

To curb the negative impact of NHs, the National Highway Authority of India (NHAI) has developed innovative strategies, such as solar lighting for the operation of tolls, rescue vans for emergencies and programmes for raising awareness among populations along the NH network. The NHAI, financed by banks, has implemented sound barriers for the stretches that pass through areas of high biodiversity and near wildlife-restricted areas. Furthermore, rehabilitation has been a part of road development strategies. The NHAI has implemented road safety audits to mitigate risks. There are five primary stages: feasibility, detailed design, development construction and safety audits (Chakrabarti, 2018).

In taking the first step, the NHAI focused on providing services and information that are related to the National Highway Network. Therefore, the Suvidha application and prepaid Radio Frequency Identification Device tag, also known as ‘FASTag’, were developed. Both of these measure real-time traffic updates, toll-plaza locations, payment options, emergency services and highway-related notifications. Information is available at petrol pumps connecting to NH. These measures reduce travel time, ensure cashless and secure transactions, produce significant decreases in revenue leakage, increase efficiency and lower the number of complaints. To facilitate the NH, banks were set up.

Hence, our present study tries to focus on two objectives: (a) to estimate the impact of the NH on bank credit or a mirror effect in districts that are closer to NHs, and (b) to understand the effect of financing NHs through bank credit or loans on aggregate bank savings in districts that are closer to NHs.

A key challenge is that the investment that manifests in terms of savings, deposits and bank credit is highly endogenous. This prompted us to formulate our first research question as follows:

We skirt the problem by investigating the impact of the NH on bank credit. We study this research question by using NHs and by examining the growth of banks in the treatment districts (districts within 10 km of an NH) and the control districts (districts beyond 50 km of an NH).

This situation raises a crucial question: Does the construction of NHs influence bank credit, or does it merely mirror the existing financial landscape? To address this question, we delve into the impact of NHs on bank credit. Therefore, our second research question is as follows:

This study highlights the importance of prudent financial management and planning in ensuring sustainable development through NHs. The relationship between banking credit and total deposits in the context of NH development in India is significant and mutually reinforcing. This study emphasizes the significance of fostering this link in order to support long-term economic growth and infrastructure development in the country.

This article draws attention to infrastructural development and bank credits. In the literature review that is discussed in the second section, the relationship between NHs, bank credit risk and deposit stability is a critical area of investigation. The third section contains the research methodology, which uses panel data. The fourth section provides an analysis. The fifth section presents a discussion, and the conclusions are presented at the end.

Literature Review

The present research is derived from endogenous growth theory. Endogenous growth theory emphasizes the proposition that internal forces, such as innovation, human capital and financial development, rather than external ones, such as labour and capital accumulation, drive economic growth (Aghion et al., 1998).

Financial development, which is an important component of endogenous growth theory, is critical for channelling savings (total deposits) into productive investments, such as infrastructure development. Banks play an important part in this process by lending money to fund these initiatives. According to endogenous growth theory, the link between bank loans, total deposits and NH development in India is dynamic and mutually reinforcing. Transportation-infrastructure investments can lead to economic growth, and a well-developed financial sector is essential for facilitating these investments (Aghion et al., 1998).

Indian Perspective on NHs

To develop the transport network, India started working on the construction of NHs. NHs were administered by the National Highway Development Programme (NHDP) in 2001. The project was undertaken to improve the Golden Quadrilateral (GQ) network, the North–South (N–S) and East–West (E–W) corridors, and port connectivity. The idea is to connect districts and states to the NH. NHDP focuses exclusively on infrastructural development.

This effort has, over time, equipped India with one of the largest road networks in the world. The road network includes (a) national highways, (b) state highways, (c) major district roads, (c) rural and village roads. In total, the Indian Government has constructed 79,243 km of NHs, which represents 2% of the entire road infrastructure. This road network carries approximately 40% of road traffic. The state highways and the major district roads (combined) or which account for approximately 13% of all Indian roads are the secondary road system of the country.

Traditionally, investment in NH construction originated from central governments. However, concerted efforts have been made to shift some of that investment to the private sector. During the 1990s, the government budget fell slightly short of what was necessary to improve NHs. Thus, private–public partnerships were initiated to mitigate the problem of NH financing. Over these decades, the NHs were developed to a significant extent. This development led to the creation of an environment that is conducive to investment (Gopalkrishna & Karnam, 2015).

Moreover, the Indian government has taken the following steps to promote investment in NH infrastructure: (a) setting up a robust financial structure for appraising and approving public–private partnerships; (b) developing standardized documents, such as model concession agreements, across infrastructure sectors; and (c) increasing the availability of finance by creating dedicated institutions and providing viability-gap funding. This led to a systematic bias towards NHDP implementation. The implementation of the NHDP was conducted in six phases. The phases are as follows: (a) augmenting the GQ, (b) augmenting the N–S and E–W corridors, (c) creating four lanes on the high-density national highway, (d) upgrading single-lane roads to meet two-lane standards, (e) building 1,000 km of expressways and (f) building ring roads, bypasses, underpasses and flyovers.

It is evident from the literature that the construction of roads led to a rise in employment in districts that are closer to NHs (Asher & Novosad, 2020). The NH has an important role in improving mobility (Banerjee et al., 2020). It has a positive impact: closer proximity to transportation increases sectoral per capita GDP levels. This translates into changes in productivity, labour supply, prices and income. Wang and Zhang, 2020 believed in the spatial spillover effect, which has employment-generating capacity for the regional service industry due to the construction of an NH. The spatial spillover effect accounts for the decrease in time spent on public transport when there is a well-connected NH. Overall, it leads to higher employment levels in districts that are closer to NHs, preferably within 10 km (Van Deusen et al., 2018). Due to the spatial spillover effect, the interquartile range of welfare increased by between 6% and 23%, an impressive gain (Morten & Oliveira, 2018). Therefore, it has been proven that a structural model of infrastructural growth is required from a policy point of view.

Between 2000 and 2016, India constructed approximately 1,960,000 km of roads. A literature review found a trickle-down effect in districts closer to New Hampshire. The NH led to expanding grocery shops, well-organized public distribution systems, irrigation and a change in cultivation patterns from subsistence to commercial crops. These commercial crops generated more profits for villagers who were residing closer to New Hampshire’s NH. Overall, financial institutions began developing in parallel to the construction of NHs. It was estimated that bank lending to villages increased by 75% and that bank credit disbursement for villages closer to NHs increased by between 30% and 35%.

Agarwal, 2023, found that the trickle-down effect increased the profitability of bank-credit mechanisms. This was a two-way phenomenon—there are demand- and supply-side perspectives. On the demand side, the profitability of the bank-credit mechanism ensured the expansion of future borrowing possibilities for the villages that are close to NHs. It led to reduced monetary dependency on local moneylenders, who were charging usurious interest rates. The literature review believes districts and villages closer to the NH have a lower loan default ratio, such as in New Hampshire. On the supply side, districts within 10 km of an NH have access to superior loan products. Moreover, there has been an impressive increase in bank borrowing, which has led to a profitable banking business. Furthermore, loan performance, analysed by reference, shows that loan recovery has been significantly higher for districts within 10 km of an NH than overdue loans for districts within 10 km of an NH.

Research Gaps

We study this question by using NH investment in India as a natural experiment on bank-credit mechanisms at the district level. We try to analyse the impact of NH on bank credit at the district level. But there has been a lesser body of work to understand the role of bank credit in NH.

We contribute to this growing literature by using comprehensive data on bank credit that are drawn from Indiastat Districts website. It is evident that businesses require loans. Loans are bank credit. Districts that are connected to an NH need more loans to meet the growing need for economic activity. Financial institutions, including banks, other depositories, securities dealers, insurers and investment companies, are part of the critical infrastructure that a nation requires to engage in minimal economic operations. Financial institutions accept funds from various sources and disburse loans. Moreover, policymakers and the government encourage the financing of infrastructural projects.

Financial institutions face two types of emergencies—a sudden drop in the value of financial assets and an operational failure of the support structure. Either could disrupt the ability of a nation to supply goods and services and, in extreme cases, cause an actual economic contraction (Kumar et al., 2018).

Large-scale road infrastructure could discipline and smoothen the financial system of a nation. However, it is equally true that the theoretical framework of manufacturing and reverse logistics is extremely challenging (Bag & Gupta, 2020). The global infrastructural disruptions include continuity of operations, increased delinquency and defaults on loans due to illness at the borrowers’ businesses and business disruption. Beyond the comprehensive aspect of our study, the availability of financing shapes, directs and promotes real economic activity. It will help us to understand how road infrastructure changes the structure of financial banking.

Methods

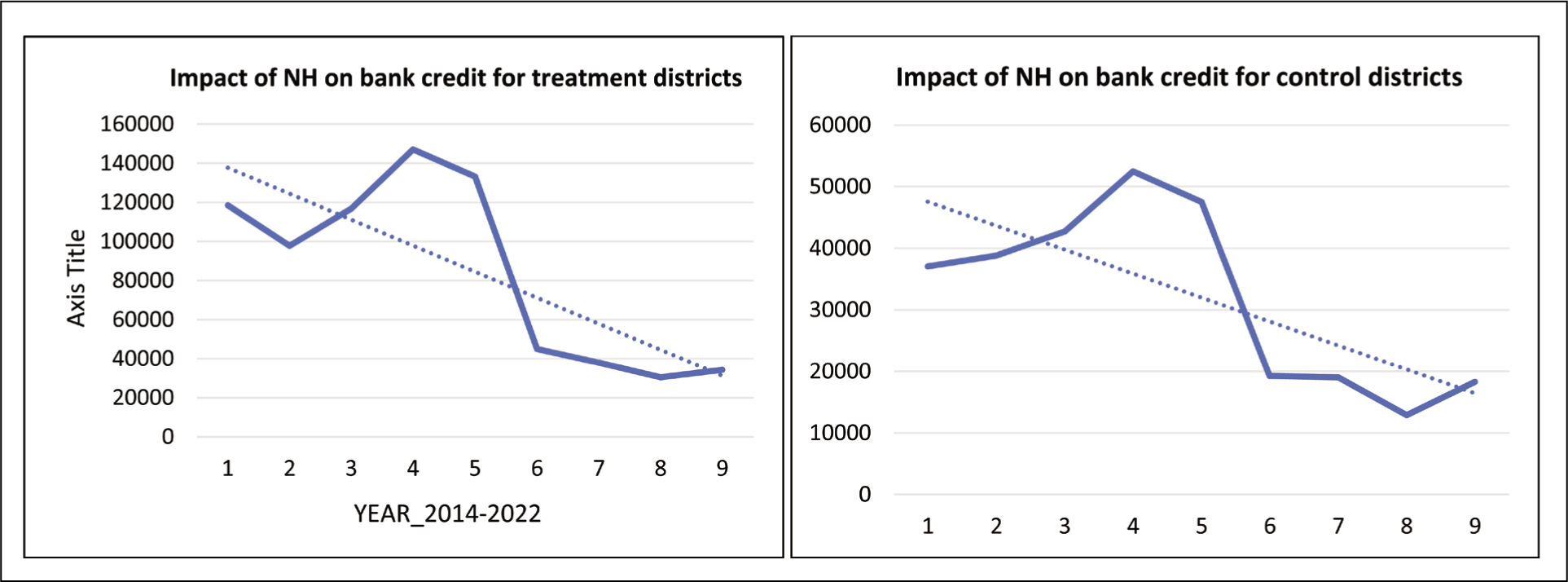

Based on the sample and the methodology that is described in the sections ‘Econometric Methodology’ and ‘Data’, the starting point of the research is the trend-line diagram in Figure 1.

We invested substantial time in cleaning and validating the data and ensuring consistency across years. Our data span the period between 2014 and 2022, and our analysis concentrates on the same period. The empirical specifications use nonparametric statistics to unearth the difference between treatment and control groups. We used two specified range districts that are located between 0 and 10 km from an NH and districts that are located more than 50 km from the NH. Our focus is on the treatment districts. We measure and report effects for the control districts, but the interpretation of these results is difficult because they are intended to be compared to the results from the study.

Data

Our platform combines bank credit and aggregate deposit data from the website (

Econometric Methodology

The econometric model was selected as a tool for quantitative analysis. We adopted a panel regression model with fixed effects. Therefore, the econometric specification is as follows:

Set D contains two categories: ‘0–10 km away from an NH’ and ‘more than 50 km away from an NH’. The coefficient value β measures the average change in the dependent value ΔYd over the period between 2014 and 2022. We consider bank credit as the outcome variable. The variable ‘bank credit’ is expressed as log bank credit.

Results

The results indicate that the relationship between banking credit and total deposits in the context of NH development in India provides dynamic financial variables within the context of infrastructure development. The positive association between the proximity of districts to the NH (within 10 km) and banking credit and total deposits suggests that areas in close proximity to NHs tend to experience higher levels of banking activity, with increased lending and deposit mobilization.

The results in Figure 1 suggest that NH development has a significant impact on the local banking sector. As NHs facilitate improved connectivity and economic development in their vicinity, bank credit increases. The figure shows that bank credit increased during 2022. It fell sharply due to the global COVID-19 pandemic. The figure indicates that bank credit has increased over time.

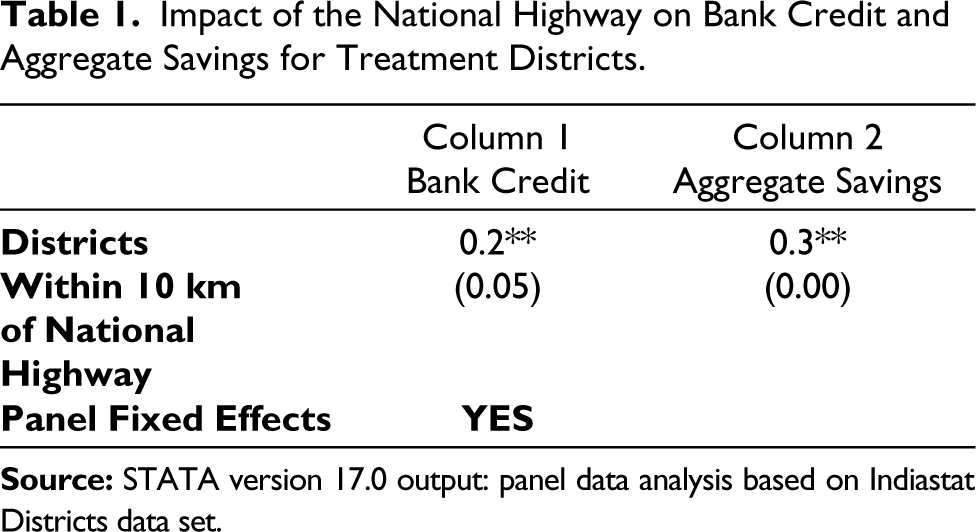

Table 1 indicates that NH development has a substantial impact on the regional banking sector. As NHs boost connectivity and economic development in their immediate vicinity, the availability of banking and deposits increases. Table 1 depicts the regression of two variables, ‘Bank Credit’ and ‘Aggregate Savings’ (0.2** and 0.3**), (which means bank credit and aggregate savings increase by 20% and 30% with the development of the NH) in districts that are located within 10 km of a national highway. The presence of ‘YES’ in the column ‘Panel Fixed Effects’ indicates that fixed effects were used to adjust for time-invariant features that may affect the connection that is being analysed.

Impact of the National Highway on Bank Credit and Aggregate Savings for Treatment Districts.

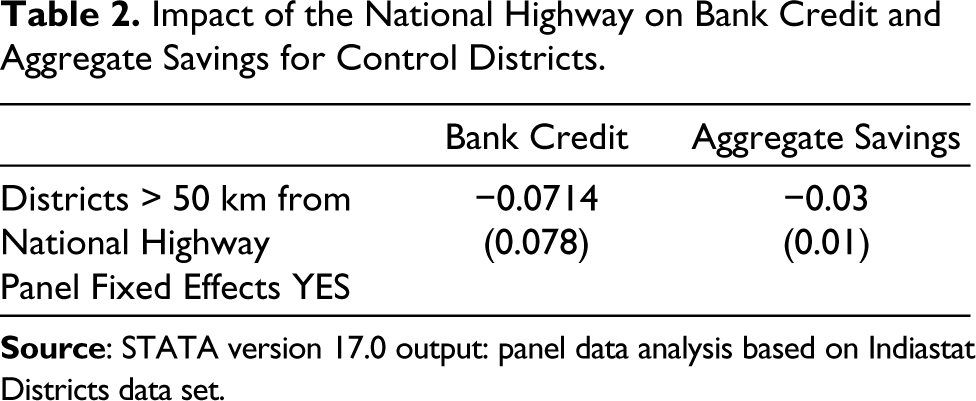

Table 2 shows the effect of distance from a national highway on two variables, ‘Bank Credit’ and ‘Aggregate Savings’, for districts that are located more than 50 km away from the NH. The coefficient value of −0.0714 indicates a negative link between the distance between a district and the NH (when it exceeds 50 km) and bank credit. In other words, as distance from the NH increases, so does ‘Bank Credit’. However, the coefficient is not statistically significant at the conventional level (a p value in excess of .05) The coefficient value of −0.03 indicates that there is also a negative link between the distance between districts and the NH.

Impact of the National Highway on Bank Credit and Aggregate Savings for Control Districts.

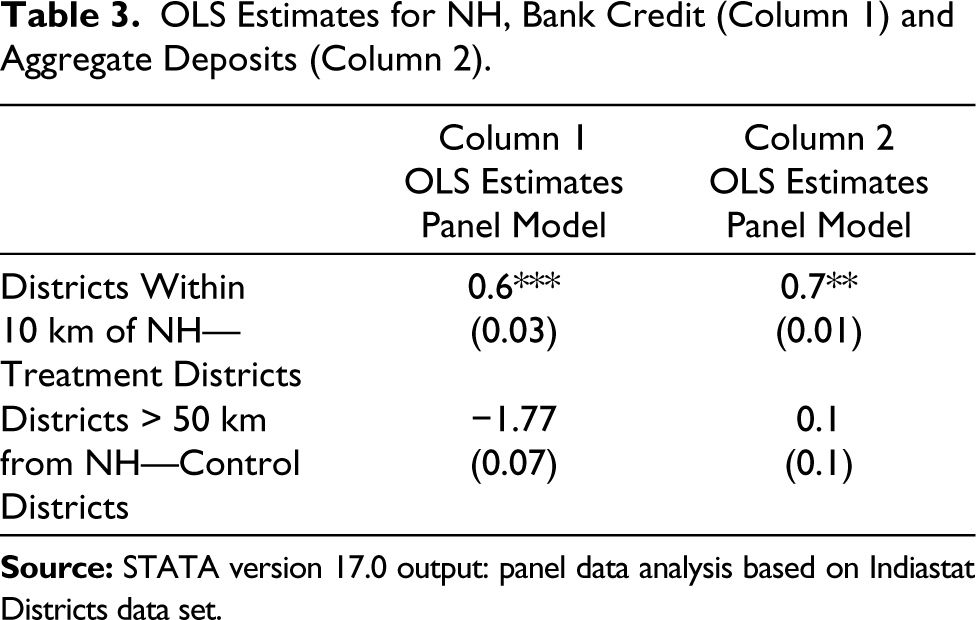

Table 3 depicts the findings from an ordinary least-squares (OLS) regression analysis, with a focus on the impact of proximity to NHs on selected variables. The coefficient value of 0.6*** indicates that treatment districts that are located within 10 km of the NH have a statistically significant positive link with bank credit. This finding means that living near a major highway is related to an increase in bank credit, making this relationship extremely strong. The coefficient value of −1.77, conversely, indicates that districts that are located more than 50 km away from the NH (the control districts) have a negative connection with bank credit. Being further away from an important highway is therefore associated with a decline in bank credit.

OLS Estimates for NH, Bank Credit (Column 1) and Aggregate Deposits (Column 2).

Dynamics of Change in Bank Credit.

Tables 4 (a, b) display the results for the treatment districts in which, there were statistically significant increases in bank credit between 2014 and 2022.

Dynamics of Changes in Aggregate Deposits

Discussion

Bank Credit

The results for districts that are within 10 km of the NH have a positive association with bank credit and aggregate deposits. These results foster the belief that bank credit and aggregate deposits respond to the development of infrastructural projects such as NHs. The implication is that infrastructural development spurs economic growth to a significant extent.

The results reveal a strong association in treatment districts (districts within 10 km of the NH) that manifests in terms of bank credit and aggregate deposits. The lending mechanism of the bank increases economic activity as it increases the marginal propensity of income. Therefore, the credit that the bank extends increases due to well-connected NHs.

Table 1 displays the core results. The dependent variable in column 1 is the change in log bank credit for the treatment and the control districts (districts within 10–50 km of a national highway) over the period between 2014 and 2022. These estimations include district fixed effects, which shed light on the percolation of financial inclusion in the local market.

The NH upgrade began between 2013 and 2014, and it was approved until 2022. Most of the growth in bank credit and aggregate deposits occurred between 2018 and 2022. Bank credit and aggregate deposits increased over the period between 2014 and 2022 by 80% and 30%, respectively. The results are similar to those of Das et al. (2019), who reported that financial inclusion increased by 80% and 95% during the infrastructural developments of 1999–2004 and 1999–2009, respectively.

Panel regressions with a fixed effect are an empirical approach to predicting the influence or impact of an NH on bank credit. We focus on Table 1, which displays the results for districts that are 10 km away from a NH. The dependent variable, ‘bank credit’, increases for this category. The coefficient suggests that there was a 2% increase during the period between 2014 and 2020. Furthermore, the increase in bank credit is significantly larger, by 20%, in the treatment districts alone. The results exhibit similarity to those of Das et al. (2019), who reported that financial inclusion increased by 23% during the period of infrastructural development. The control districts are associated with a decrease in bank credit, which is due to their distance from the NH.

We constructed Table 1 and Table 2 for comparison. The tables provide a concrete representation of the interactions between bank credit and NH for the treatment and control districts. It is evident from the results that none of the effects that we intend to measure are observed in the control districts.

The stability of the results is encouraging, given the objective of the study. The results showed a positive influence on economic development. Policymakers have persistently found latent growth potential in a well-developed banking system and infrastructure. The significant results are similar to those of Banerjee et al. (2020) and Das et al (2019). Infrastructure has a distributional effect, in terms of increased market access and fixed-factor endowments. The linkage between bank credit and NHs increases the marginal propensity to obtain income. Since roads connect villages and activities, the agglomeration effect intensifies the accumulation of productive capital and aggregate savings, thereby increasing incomes in the long term. Likewise, well-developed roads in the US led to more viable economic models and large-scale urbanization. Therefore, the results represent progress in the academic understanding of the impact of investment on infrastructure and bank credit in the Indian economy.

In short, we found that regions and districts that are closer to a national highway have superior bank-credit facilities. However, these differences are small in magnitude. National highways are constructed in a few districts; therefore, the percolation effect is relatively small at this point in time. However, it is believed that the distributional effect (Marco-Ferreira et al., 2020) will become stronger in the coming years. Bank credit builds a stronger capital market. A stronger capital market creates multiplicative demand in local markets.

The supply of credit is a crucial means of increasing employment levels. It is estimated that employment declines by 15% when a reduction in credit supply occurs. This loss of jobs is concentrated in the transportation and infrastructure industries. During the Great Depression, employment decreased by 7 million. Fluctuations in the supply of credit affect net household income and increase market uncertainty. This phenomenon affects residential and local markets negatively and has a severe influence on the construction sector. Literature reviews have found 13% of all jobs are lost, especially during business cycles and recessions. The starting point of the article is that bank credit increases by 20% due to the construction of NH in districts that are within 10 km of each other. Since the construction of an NH validated the regulation of continuous credit from banks to households, the association between bank credit and NH is persistent and complementary (García, 2020).

The present study adopts a certain approach to linking bank-credit mechanisms to the construction of the NH. A lower amount of bank credit leads to heterogeneous effects, thereby translating to a low level of income and consumption in the local community. This proposition can be validated by one of the results, namely the fall in bank credit in the control districts. Control districts could not witness significant results. Infrastructure usually brings sizeable benefits for the economy in terms of gains from trade as well as localization.

Therefore, NHs improve the credit supply of banks, causing the local economy to acquire the ability to absorb heterogeneous effects. On most occasions, economists believe in the experience of first-order macroeconomic consequences. A lack of transportation infrastructure, especially in districts that are located beyond 50 km of an NH, induces a reduction in the supply of credit and a decrease in demand for loans among consumers.

This significantly affects lower-income individuals or households below the poverty line. Our explanation is consistent with that of Bernanke et al. (1991): infrastructural underdevelopment can cause capacity constraints, leading to an imperfectly elastic market for credit during crises.

Liao (2021) found that bank credit supply leads to friction in the labour market. A decrease in the supply of credit due to a lack of infrastructural facilities increases labour adjustment costs and further decreases investment. These mechanisms have a prolonged impact on the activities of firms and on the local economy. Therefore, the relationship between bank credit and improvements to NHs (infrastructural development) requires adequate attention.

A panel data study on the Brazilian economy reports that the countercyclical expansion of bank credit has a positive effect on economic development. Bank credit can be disbursed more effectively only when the concentration of banks is high. The impact of credit is directly associated with infrastructural development, which may take the form of the construction of the NH. The Brazilian government during the 2008–2009 recession (Capeleti et al., 2022) adopted this strategy. The results bear a resemblance to ours.

Sustainable credit expansion increases economic stability and compensates for shocks during the business cycle. Thus, the NH smoothens long-term economic growth. However, NHs and banks must be close to each other—within a range of 10 km. Close proximity between banks and NHs is a boon for the local economy, providing superior market access for local firms and businesses. This benefit is mainly due to the firms in question receiving bank credit rapidly and increasing their liquidity. The results of this work point to a direct relationship: bank credit increases 90% of business lending. The increase in business lending increases capital mobility. The lack of bank credit facilities does not develop the local market. Improved local markets increase construction and development. Thus, the evidence confirms that bank credit is superior in districts within 10 km of the NH.

Roads play an important role in economic development. An interesting study was found by Asher and Novosad (2020). In China, local GDP decreased substantially with the construction of the NH.

We adopted panel regression with fixed effects in order to analyse the impact of the NH on banks and financial institutions. We found a positive impact on savings behaviour among locals. Our study focuses on district-level analysis. In most cases, the NH and banks lead to structural transformation. The economic concept of propensity to save indicates that a rise in savings and deposits among locals has a recursive and positive impact on individuals. However, in the Western world, there is a contrasting view of the study: in terms of causality, the relationship between infrastructure investment and development is significantly bidirectional.

Baum-Snow et al. (2020) and Brandao-Marques et al. (2020) took the view that infrastructural development and gross capital formation (savings and current deposits) are two sides of the same coin—a synchronized view of our results. The United Nations Millennium Development Goals, 2015, followed individuals who reside in areas with non-existent roads or NHs and lead impoverished lives, a slightly different view from the results that we present (Ogun, 2010).

Baum-Snow et al. (2020) also found that investment in NHs and local transport reduces agricultural activity and promotes manufacturing growth and banking to a slight degree, a similarity of opinion. This finding is mainly due to individuals losing their specialized activities (mostly agriculture), leading to a loss of economic growth. The development of the NH is important because it leads to superior connectivity. Connectivity increases banking behaviour and promotes manufacturing.

Banks receive support from the government through bonds and interest on loans. This increases the willingness of banks to assume risks in investment. We believe that indirect government support (increasing the construction of NHs) increases government spending. This rise in government spending and investment generates superior banking behaviour among the public. The results also confirm that saving deposits are positively related to NHs. Therefore, NHs certainly affect banks and financial institutions.

Banks provide subsidized loans to locals and to local governments. These loans have a multiplier effect on small businesses and self-help groups. Subsidized loans act as an injection of investment and employment for small and medium-sized enterprises. In this case, our results support the idea that NHs stimulate investment.

The Hungarian government engages in economic investment. Economic investments occur due to subsidized loans with interest rates of approximately 2.5% through commercial banks. The amount is a refinance investment at 0% interest from the Hungarian central bank. The subsidized interest rates have a beneficial effect on self-help groups and small and medium-sized enterprises (SMEs; Horvath & Lang, 2021).

The investment loan programme is called the ‘Funding for Growth Scheme’, and it was launched in June 2013 to reduce the burden of external financing on local SHGs and SMEs. Investment, in terms of NHs that are promoted by the government, led commercial banks to retain credit risk exposure. The model was highly successful in Hungary—Hungarian GDP increased by 7% in the same year.

Wu et al. (2022) found a positive relation between NH and saving deposits, which coheres with our results. This positive relationship could be attributable to roads and railways increasing the efficiency of investment, thereby reducing transportation time for goods and individuals.

In conclusion, NHs play a pivotal role in economic activity. This role boils down to a concept called ‘home bias’. The proponents of home bias believe that investors prefer to choose domestic and local stocks. The value of local stock increases with business activity. Business activity (SME/SHG) is encouraged in local markets only when banks have developed and provided locals with subsidized loans. The growth of NHs fosters investment efficiency. Investments operate at optimum efficiency only when NH projects have positive net present values. Therefore, the development of NHs causes firms and individuals to invest in profitable local projects through regularized banking activity and subsidized loans. It is called investment efficiency (Wu et al., 2022). Our results validate the literature. A positive growth of banks and financial institutions with NH will increase government assets in the long run.

Aggregate Deposits

Tables 4a and 4b depict the dynamics of financial inclusion, in terms of bank credit and aggregate deposits, in the treatment and control districts. Panel A displays the dynamic specification of changes in bank credit, and Panel B displays changes in aggregate deposits. The first column shows the changes in bank credit during the 2014–2016 period. The columns to the right suggest increases in time over two corresponding years. The rightmost column covers the entire sample period, 2014–2022.

A strong result emerged from this analysis. The growth in bank credit and aggregate deposits is concentrated in the treatment districts (i.e., districts within 10 km of NHs) and, to some degree, in the control districts (i.e., districts within 50 km of an NH have lower deposits and bank credit). Tables 4a and 4b reveal the dynamic specifications of the treatment and the control districts. We believe that the study has important implications for future scholarship.

The results show that aggregate deposits have increased by 30% over the period of infrastructural development, in terms of the construction of NHs. The results are similar to those of Das et al. (2019), who found that financial inclusion grew by 23% during the period of infrastructural development. Aggregate deposits and bank credit had a direct and significant relationship with the NH over the period between 2014 and 2022. This proposition is supported by an economic theory that predicts the relationship between bank credit and aggregate deposits. It is known as the Böhm-Bawerk (Kim, 2020). The study shows that there is a causal association between the supply of credit, aggregate deposits and long-term investment. The homogeneity of money in the economy fosters a belief among depositors that they will receive their funds from the bank. The increases in bank credit and aggregate deposits are allocated to production or investment. This proposition is justified and complimented by our results. Böhm-Bawerk believed that credit-market supply is a mirror image of saving-investment decisions in the economy. This ultimately leads to the growth of the economy in the long run. We found that, due to the construction of NHs, aggregate deposits and bank credit increased significantly. To be precise, the development of the banking system depends on aggregate deposits and the effective circulation of bank credit. This phenomenon influences the investment decisions (through capital accumulation) of the government in the long run. A well-developed financial system has four functions: (a) innovation in the factor of production, (b) effective employment of existing resources, (c) the generation of capital resources and (d) investment in the factor of production (Kim, 2020). Past studies have shown that NH has led to an increase in the debt-asset ratios of firms and the credit-saving ratios of local banks. Investments in NH have raised aggregate savings by 10%, boosting the local economy.

A pertinent question arises: Is NH development an outcome or an effect of financial development? Important questions emerge if financial development must precede investment (in terms of NHs) in the local economy. It is evident from the present results that infrastructural construction impacts the real growth of the economy. Bank credit and aggregate deposits increased in the treatment districts, with a slight rise during the initial years and rapid expansion during the subsequent period. However, we believe that, due to COVID-19, the dynamics of the 2014–2020 and 2014–2022 periods remained constant.

Conclusion

In conclusion, we investigated the empirical association between the construction of NHs during the period between 2014 and 2022 and the local financial sector. We analysed the local financial sector in terms of bank credit and aggregate deposits. NHs create a powerful tool for measuring financial inclusion and percolation in the local market. These results cannot be quantified or related to developed economies because their infrastructural investment began in time immemorial. Our results are helpful for policymakers and the NHAI in evaluating the impact of infrastructural investment on access to banks in the context of the emerging economy. Our results indicate that the NH has a positive impact on the financial sector, but there is still a long road ahead.

Our method is largely based on endogenous growth theory developed by Aghion et al. (1998). The theory proceeds from the premise that savings should be generated through productive investments and are interconnected elements for long-term economic growth. Productive investments lead to infrastructural development, which may take the form of NHs. In a way, NHs create a trickle-down effect.

Drawing on endogenous growth theory, we collected bank credit and aggregate-deposit data from Indian state districts. Bank credit and aggregate savings are typically characterized by multiple inputs and multiple outputs that are associated with transport network centrality (Das & Kumbhakar, 2012), such as different forms of deposits, loans, the number of accounts, the group of customers the bank caters to and the close proximity of the branches to NH. These differentials between the developments of NH to the growth of banks are mostly ignored in empirical studies. Our study tries to delve into relationship between banking credit and total deposits in the context of NH development in India. However, the heterogeneity of different districts or contextual differences were not taken into account while performing the study. These omissions make the practical value of variables like banking credit and aggregate savings slightly questionable because the contextual settings of the districts or the heterogeneity of the districts are beyond the scope of this research work. Moreover, with the increase in the NH development of districts or heterogeneity associated with districts will be studied in future. The government has proposed to study the contextual settings of the districts in the five-year and ten-year plans of NH development (Chakrabarti, 2018; Kumar, 2017).

The second possible reason is that the infrastructure gap is one of the impediments to India realizing its growth and poverty reduction potential. Research has shown that the effect of NH or GQ is stronger for treatment or nodal districts (districts within 10 km of NH). It is evident that NHs has helped to spread economic activity in terms of banks and markets in treatment districts. Therefore, we cannot nullify the linear and positive impact of NHs. Especially in moderate-density districts and districts closer to the NH, this has a significant impact on aggregate savings and banking credit. The data for this research work were collected based on microeconomic knowledge and GIS. The NHs were mapped with the districts closer to it based on GIS software systems. Thus, there exists heterogeneity in terms of diversity and economic growth of the area. Moreover, heterogeneity or contextual differences are due to investment decisions, which are often governed by political parties. Decision-maker’s preferential treatment of a particular district makes it difficult to analyse the heterogeneity (Gühnemann et al., 2012). But the study acknowledges that the strategic policy goals and investment options must homogenously select district across the districts.

We adopted the panel regression model with fixed effects and performed difference in difference. The results confirm the existence of a positive association between the proximity of districts to NHs and bank credit and aggregate deposits. However, the results of this study found districts within 50 km of NHs have lower or negligible levels of bank credit and aggregate deposits. Thus, study assumed linear impact of NHs on banking credit and aggregate savings. In addition, the results of this study found that districts within 50 km of NHs have lower levels of bank credit and aggregate deposits.

In conclusion, the NH leads to a home-bias and the trickle-down phenomenon. The development of NH leads to a rise in investor preferences for domestic and local markets. However, the research is not without limitations. One of those limitations were due to the COVID-19 pandemic; some of the NHs could not be completed in time, which led to losses for the Central Government of India and delays in the manifestation of the trickle-down effect and home-bias phenomenon.

Footnotes

Acknowledgements

The views expressed herein solely belong to the authors and do not necessarily represent those of any affiliated institution. The first and second authors are grateful to the authorities of IIM Bangalore for providing office space and access to the Indiastat districts dataset.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The study was sponsored and funded by the National Highway Authority of India, Government of India. The first and second authors worked as post-doctoral fellows at IIM Bangalore and contributed to the research individually or out of their own interest.