Abstract

The banking industry across the globe has been undergoing severe transformation due to the development in the field of information and communication technology (ICT). This transformation process not only introduced innovative products but also changed the way of service delivery. Mobile banking is the most popular and powerful mode of service delivery, which ensures the delivery of banking services anywhere and anytime. This article attempts to analyse the current status of research on mobile banking in order to identify the themes to be explored by future researchers. With the deft use of different inclusion and exclusion criteria and relevant and appropriate keywords, 79 journal articles published in renowned databases were selected for an in-depth review and thorough analysis. The place of study, target group focus, the theoretical models adopted and the themes considered were the basis for analysis. Most of the studies were found to have been undertaken in developing countries, and the initial adoption is the most explored area of research on mobile banking. Technology acceptance model (TAM) is the most widely used theoretical model for predicting mobile banking adoption. As the continuance intention to use mobile banking is the less explored one, there is a need to shift the research focus from initial adoption to the continuance intention to use mobile banking. Research studies on mobile banking need to be conducted among distinct groups such as the otherwise-abled, migrant workers and marginalized sections of society as they have the potential to make great contributions towards the digital economy and nation building.

Executive Summary

The advancement in the field of information and communication technology (ICT) has made significant changes in the way of doing business for almost all business organizations, and the banking industry is not an exception to this. The hectic competition in the market necessitates the importance of being competitive in order to sustain and survive in this complex business environment. The banking industry, as a major component of the financial system, tries to be more competent not only by way of innovating its products and services but also through cost-effective means of service delivery. One of the important and innovative methods of service delivery is mobile banking, which is becoming more popular as it facilitates the conduct of banking transactions anywhere and anytime. Mobile banking is a recent and most popular system of banking that enables users to conduct banking transactions using mobile devices, particularly mobile phones, with ease and convenience. Despite the benefits and its popularity, both its adoption and continued usage are not up to the mark. Many research studies have been conducted across the globe to explore the various aspects of mobile banking.

This article analyses the current status of research in the field of mobile banking by considering 79 journal articles published in the renowned databases from 2000 to 2019. The PRISMA framework has been employed to systematically extract relevant literature. The application of different inclusion/exclusion criteria helped the authors to select the most suitable articles for analysis, and the selected articles were classified on the basis of nature and place of study. The articles were analysed on the basis of the theoretical models used, target group focussed and the sampling technique adopted. A majority of the studies on mobile banking have been conducted in developing countries, and the technology acceptance model (TAM) is the most widely used theoretical model for predicting the behavioural intention to use mobile banking. Of the seven major themes identified from the literature review, the initial adoption of mobile banking is the most sought-after area. Students are the single most targeted group, as they are more inclined toward technology. It is the need of the hour to shift the research focus towards continuance usage as it is less explored one. There is a great potential to explore both the initial adoption and continued usage of mobile banking among vulnerable sections and other socially and economically disadvantaged groups in society.

Introduction

The unprecedented advancement in technology has made the world shorter and human life better and more comfortable. The banking sector, in any country, plays a key role in the establishment and round the clock functioning of the financial system, which, in turn, lays the strong foundation for the expeditious growth of the economy. Technological advancements have forced the banking business to find alternative ways of doing business that ensure time-saving and cost-effective means, easily and quickly allure customers into their fold. The banking industry across the globe has undergone severe transformation, which has paved the way for the development of innovative methods of service delivery.

Mobile banking is the most recent and most popular innovative system of banking. Mobile banking enables users to conduct banking transactions using a mobile device, popularly a mobile phone, with ease and convenience (Zhou, 2011). Mobile phones have penetrated into our daily lives and the growing number of internet subscribers across the globe expands the scope for delivering banking services anywhere and anytime. Despite the benefits and its popularity, the adoption level of mobile banking is not up to the mark (Chaouali & Souiden, 2019; Cruz et al., 2010) as all mobile phone users in the world are not users of mobile banking (Shaikh & Karjaluoto, 2015). Though people are adopting mobile banking, it may not necessarily result in continued usage in the future. The reasons which are primarily responsible for this range from innovation resistance to risk perception and from complexity to distrust (Cruz et al., 2010).

Mobile banking is going to play a vital role in the digital economy, and its potential towards the creation of a cashless economy or a less cash economy cannot be underestimated. There are different aspects of mobile banking to be studied and analysed, which should not be a mere replication of contemporary studies. Hence, a consolidation of existing literature will definitely help in guiding future researchers to avoid the beaten track and tread upon new and unexplored areas. Literature analysis in this area has been attempted by Shaikh and Karjaluoto (2015) and Tam and Oliveira (2017), with 55 publications during the period 2005–2014, and 64 journal articles published during 2002–2016, respectively. As mobile banking is undergoing several advancements, it is inevitable to look back at the studies before further exploring the research area. This article, therefore, aims to study the current status of research on mobile banking and analyse the extant literature so as to identify the broad themes to be explored in this field of study.

The rest of the article is presented as follows. Section 2 discusses the methodology. Section 3 exhibits the results and interpretation. Section 4 presents the discussion, and Section 5 documents the conclusion and highlights the scope for future research in this field of study.

Methodology

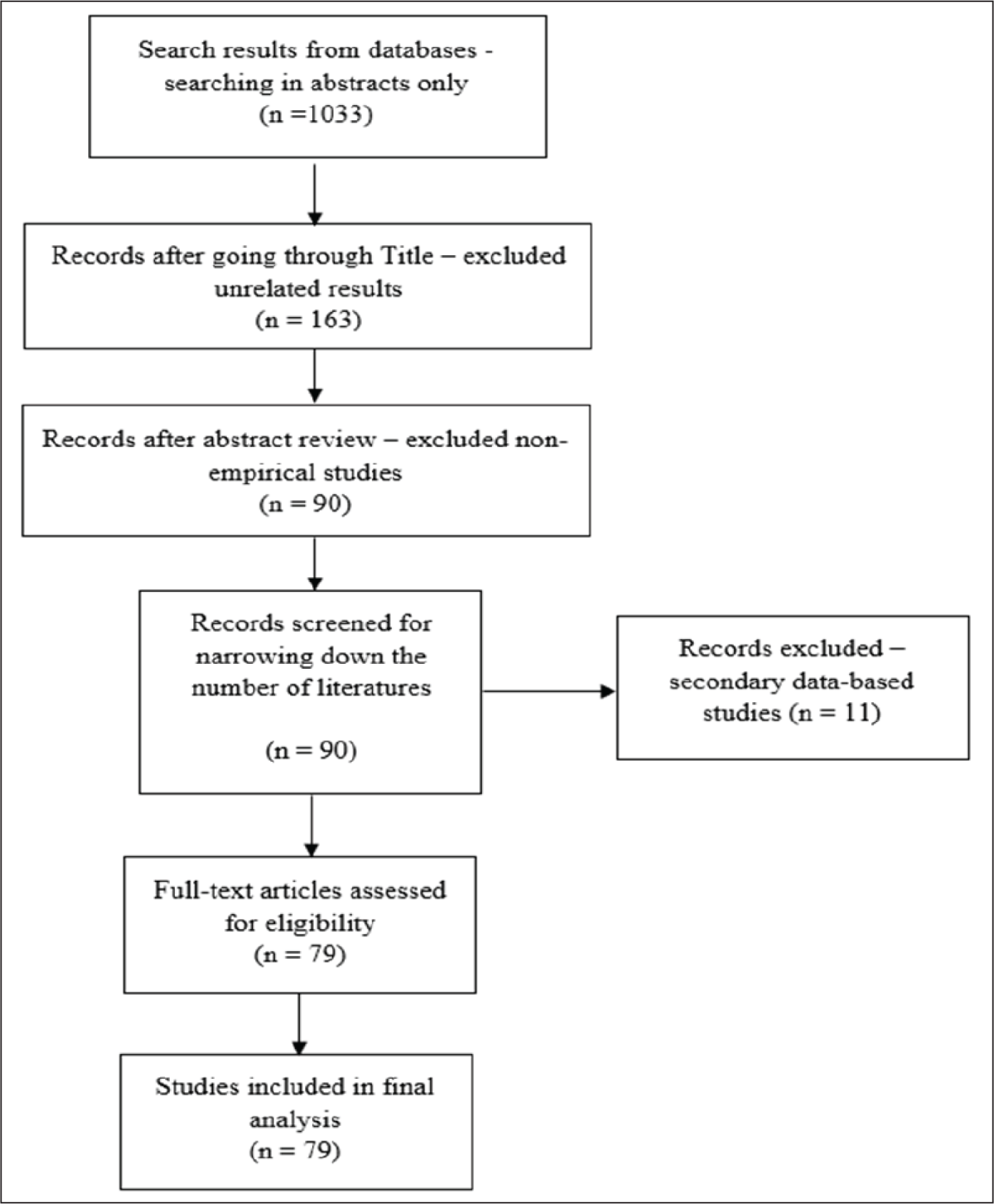

For making a systematic analysis of the literature available on the subject chosen for the present study, the authors have employed ‘Preferred Reporting Items for Systematic Reviews and Meta-Analyses’ popularly known as the PRISMA Statement (Moher et al., 2009). Here, the authors have followed a systematic procedure for selecting literature that is slightly different from the PRISMA framework. The relevant literature was selected from five online databases, namely, Emerald Insight, Science Direct, Wiley Online, Taylor and Francis Online and Sage Journals, the notable databases of the renowned publishers, most of which are Scopus or Web of Science indexed. The necessary and relevant literature from the selected databases was obtained through the careful and deft use of keywords such as mobile banking, m-banking and adoption, with the help of the advanced search option available on the respective websites of each database. The journal articles published in the last two decades, that is, from 2000 to 2019, have been taken for the study, which denotes the exclusion of all book chapters, conference articles and review articles. The search was limited to ‘search in abstract only’ in all the databases, so as to gather the most relevant results. Boolean operators like ‘OR’ and ‘AND’ were also used wherever required to arrive at the relevant results.

On completion of the literature survey, the use of inclusion/exclusion criteria helped in the right choice of the articles. Meticulous scrutiny of the title of the study helped in the selection of only those articles which are empirical in nature. In the second stage of screening, a close and careful study of the abstracts of each selected study made it easy and possible for the exclusion of cross-cultural studies, secondary data-based studies, conceptual articles and exploratory studies without empirical validation. Both quantitative and qualitative studies were given serious consideration. The studies which have concentrated on adoption intention, continuance intention, trust-building and the like have been included. The articles published in the English language only were chosen for the study.

The application of the aforementioned criteria (see Figure 1) has enabled the researchers to make a final selection of 79 journal articles from the chosen five databases. On completion of the selection procedure, began the process of data collection, which was done by making an in-depth study of every article, and the required data was entered into a Microsoft Excel sheet for further analysis. The literature was analysed using descriptive statistics, and further classification was done on different bases, namely, theories used, the methodology adopted, target group considered, dependent variables chosen and the like.

Results and Interpretation

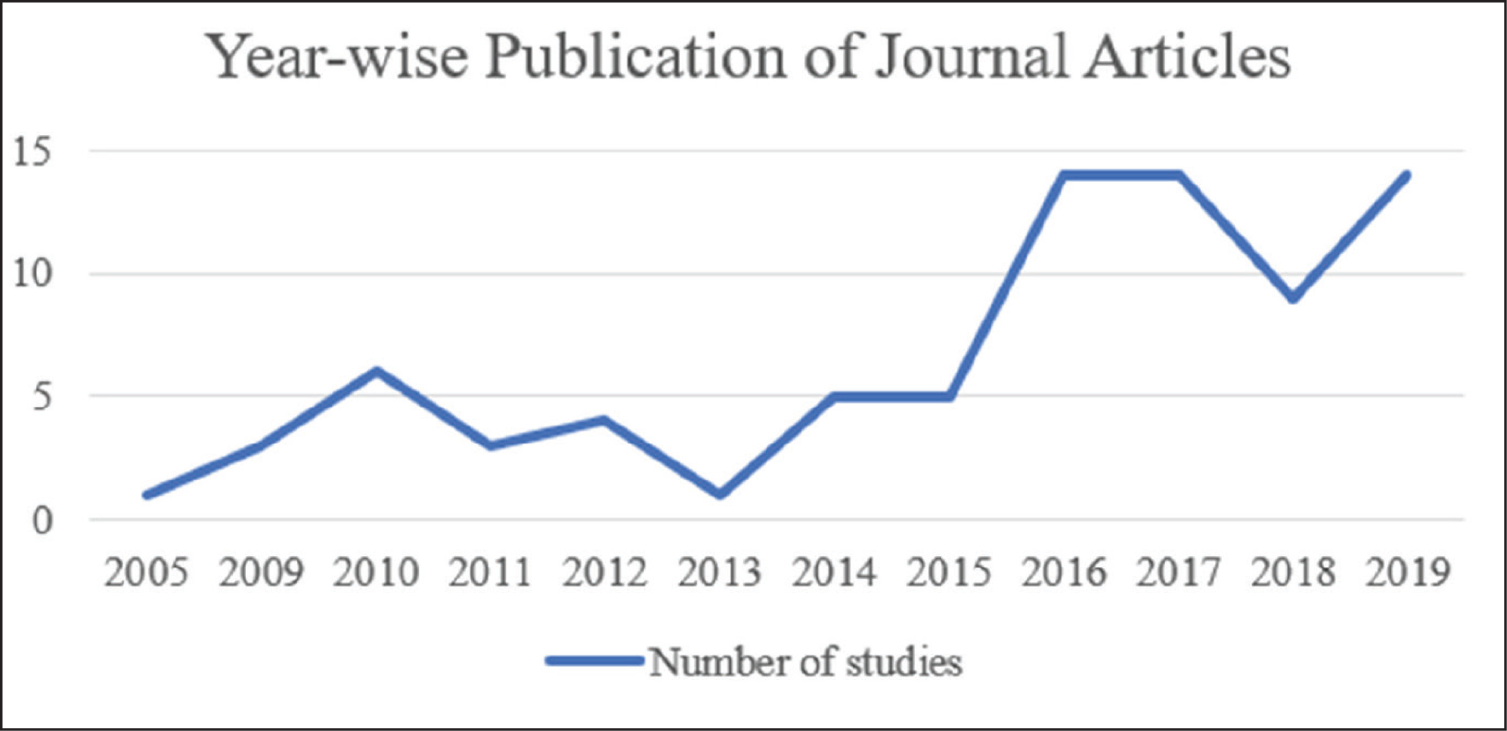

This section presents the results of the analysis of studies on mobile banking undertaken in different parts of the world. A hectic search for the publication of articles pertaining to the subject for the present study showed that though the publication of articles virtually began at the dawn of this millennium quantitatively, it was not encouraging as it moved at a snail’s pace (see Figure 2).

Our inclusion/exclusion criteria resulted in the selection of only one article in 2005 and three in 2009, so the whole of the first decade shows a dismal picture. But the scenario underscores the fact that as many as 75 articles for the present study were the products of the period of 2010–2019. There were six studies in 2010, but that gradually decreased to one in 2013. However, there were 14 studies each in 2016, 2017 and 2019, which is irrefutable proof of the growing popularity of mobile banking, which, in turn, gave impetus to the researchers to explore various aspects related to mobile banking.

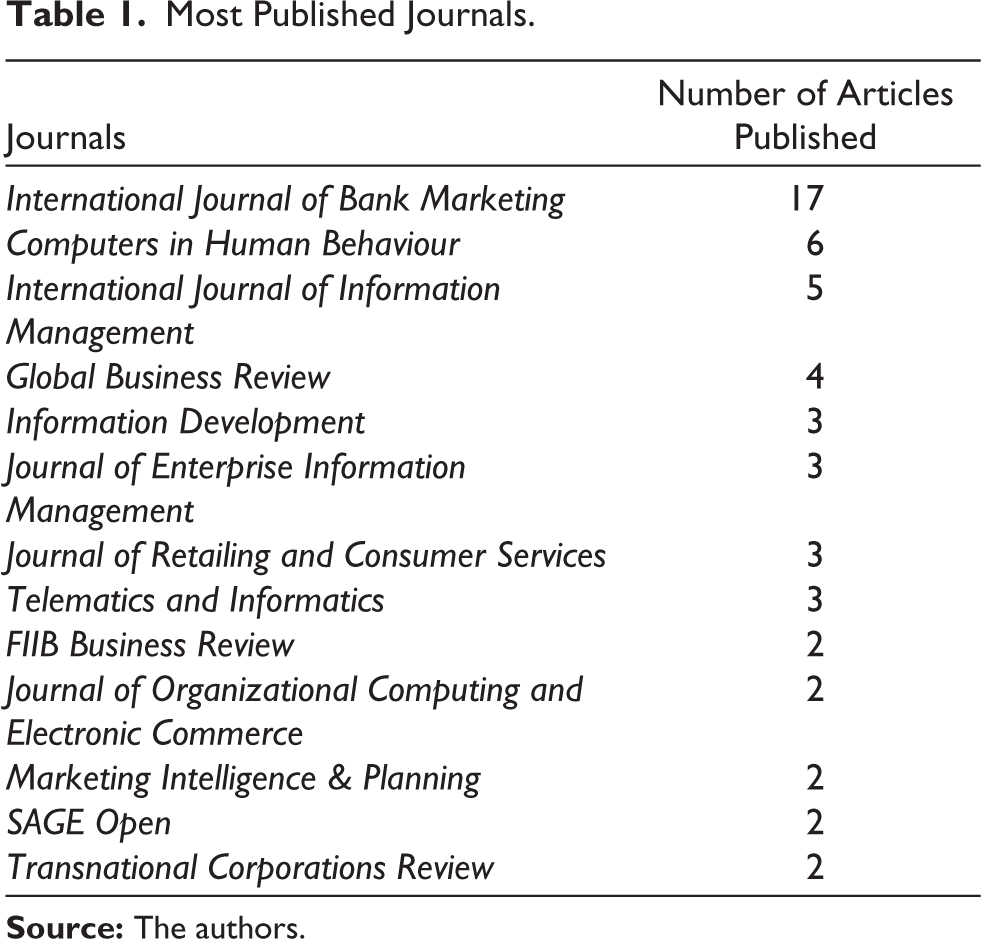

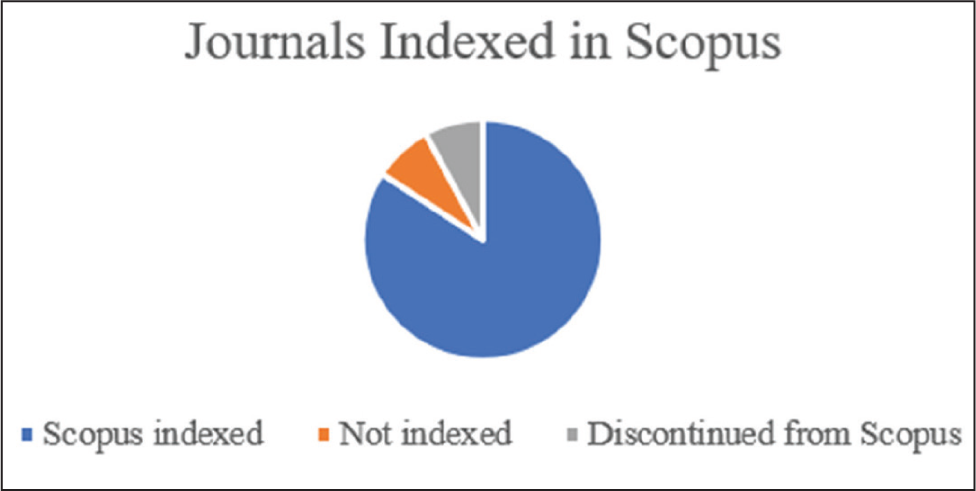

A meticulous mode of extraction enabled the authors to collect a final set of 79 articles published in 38 different journals of international repute. Table 1 furnishes information regarding the journals which have published at least two articles in the relevant research area during the period under review. Thus, it shows a total of 54 articles published in 13 journals. There are another 25 journals which have published one article each. More than four-fifths of selected journals are indexed in Scopus, a largely accepted citation database, which is a clear indication of the quality of the articles chosen for this study (see Figure 3). It is thus crystal clear that mobile banking adoption and usage have grown into one of the most sought-after areas of study.

Most Published Journals

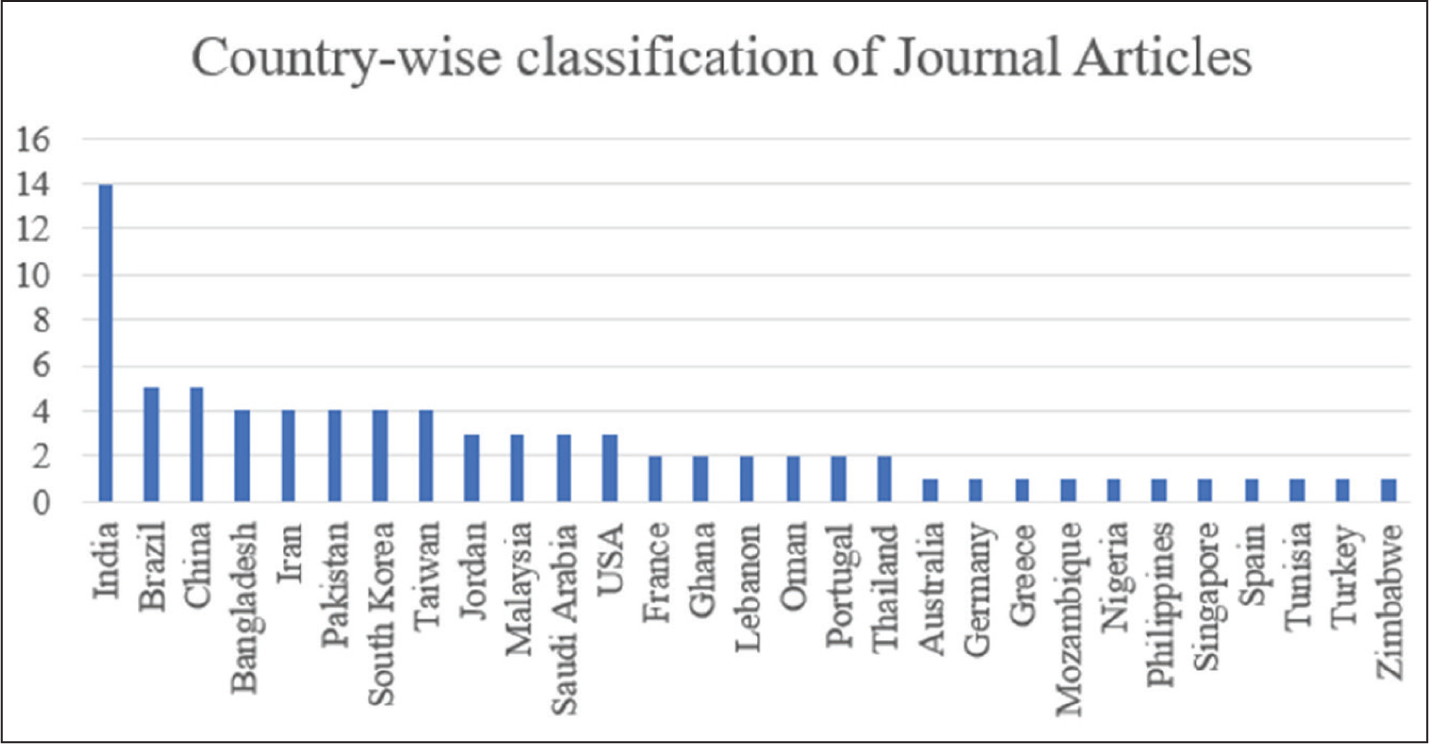

The countries where the studies have been conducted during the period under review are shown in Figure 4. In fact, there are 29 countries spread across all continents. Of these countries, 15 are in Asia, followed by six in Europe, five in Africa and one each from North America, South America and Australia.

Around 70% of the chosen studies are from Asian countries, and India tops the list by providing as many as 14 studies, followed by Brazil and China with a contribution of five studies each. There are four studies each conducted in Bangladesh, Iran, Pakistan, South Korea and Taiwan. At least two studies could be obtained from ten other countries, but only one study was available from each of the 11 other nations at the bottom of the list.

Content Analysis

Nature of Study

Classification of the articles shows that all the 79 articles fall under three categories, namely, quantitative (73), qualitative (1) and mixed (5) studies (see Figure 5). The in-depth study of Tobbin (2012) with a qualitative approach was of immense assistance in exploring the perception of the unbanked population towards the adoption and usage of mobile banking. Qualitative studies followed by empirical validation will help in identifying more determinants of mobile banking adoption (Chiu et al., 2017). However, a host of researchers made deft use of the quantitative data to empirically analyse the adoption behaviour of people.

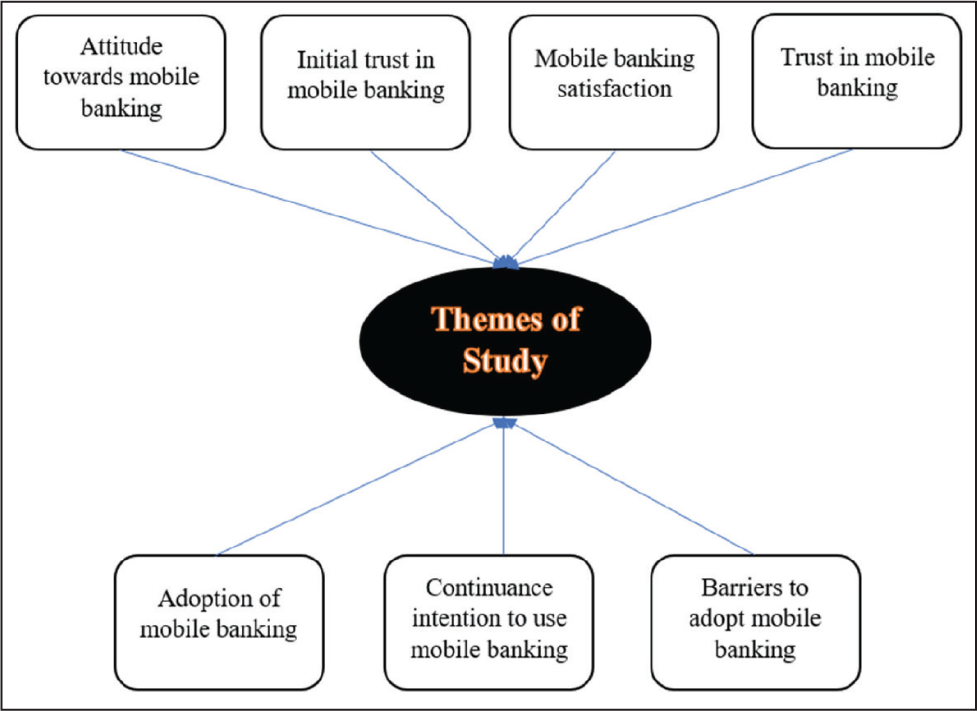

Themes of the Study

The analysis of available literature brings to the fore the varied and various aspects of mobile banking explored by different scholars at different times across the nations. The different themes identified are presented in Figure 6. More than two-thirds of studies have concentrated on adoption of mobile banking, followed by the users’ continued intention to use the same. There were separate studies on barriers to adopting mobile banking (Chaouali & Souiden, 2019; Cruz et al., 2010; Yang, 2009). Trust in a technology is always influential in its adoption, and hence, trust building in mobile banking was also an area of interest by the researchers (Malaquias & Hwang, 2016b). There are various factors affecting the initial trust formation and the same has been studied by Zhou (2011) and discovered that system quality, information quality, structural assurance and trust propensity influence initial trust building. The satisfaction of using mobile banking is also being studied by researchers (Khan et al., 2018; Masrek et al., 2014) to explore the factors that require attention to improve the service quality of the system and thereby satisfy the users. Sohail and Al-Jabri (2014) have differentiated the attitude towards mobile banking between users and non-users.

Mobile Banking Adoption

As mobile banking is something new, it is very important to study whether people have the intention of using it. Adoption involves the installation of a mobile banking app or enabling SMS banking service, etc. The initial adoption of mobile banking is often measured using variables such as behavioural intention to use (BI), actual use and attitude towards the use of mobile banking. There are multiple factors that would affect the decision of the customer to adopt mobile banking. It includes but is not limited to perceived usefulness (PU), perceived ease of use (PEOU), attitude, compatibility, trust, perceived risk, social influence and the like. Adoption of mobile banking is explained using different theoretical models, and notable among them are TAM, UTAUT and UTAUT2. Researchers have compared the validity and suitability of different theories in explaining adoption behaviour (Giovanis et al., 2019). Payne et al. (2018) studied the adoption of AI-enabled mobile banking services. Researchers have also analysed the effect of demographic variables (Chawla & Joshi, 2018) on mobile banking adoption, especially gender (Glavee-Geo et al., 2017; Riquelme & Rios, 2010).

Continuance Intention to Use Mobile Banking

The post-adoption usage is crucial in determining the success of mobile banking, but the analysis shows only a few studies have been conducted with respect to this. Continuance intention to use refers to the intention of users to continue using the system in the post-adoption scenario (Bhattacherjee, 2001). It can happen that the person who has adopted a particular technology in the first phase may stop using it due to several factors. Foroughi et al. (2019) analysed the drivers which influence the continuance intention to use (CI) mobile banking technology and found that users will continue using mobile banking only if they find it useful and are satisfied with their experience.

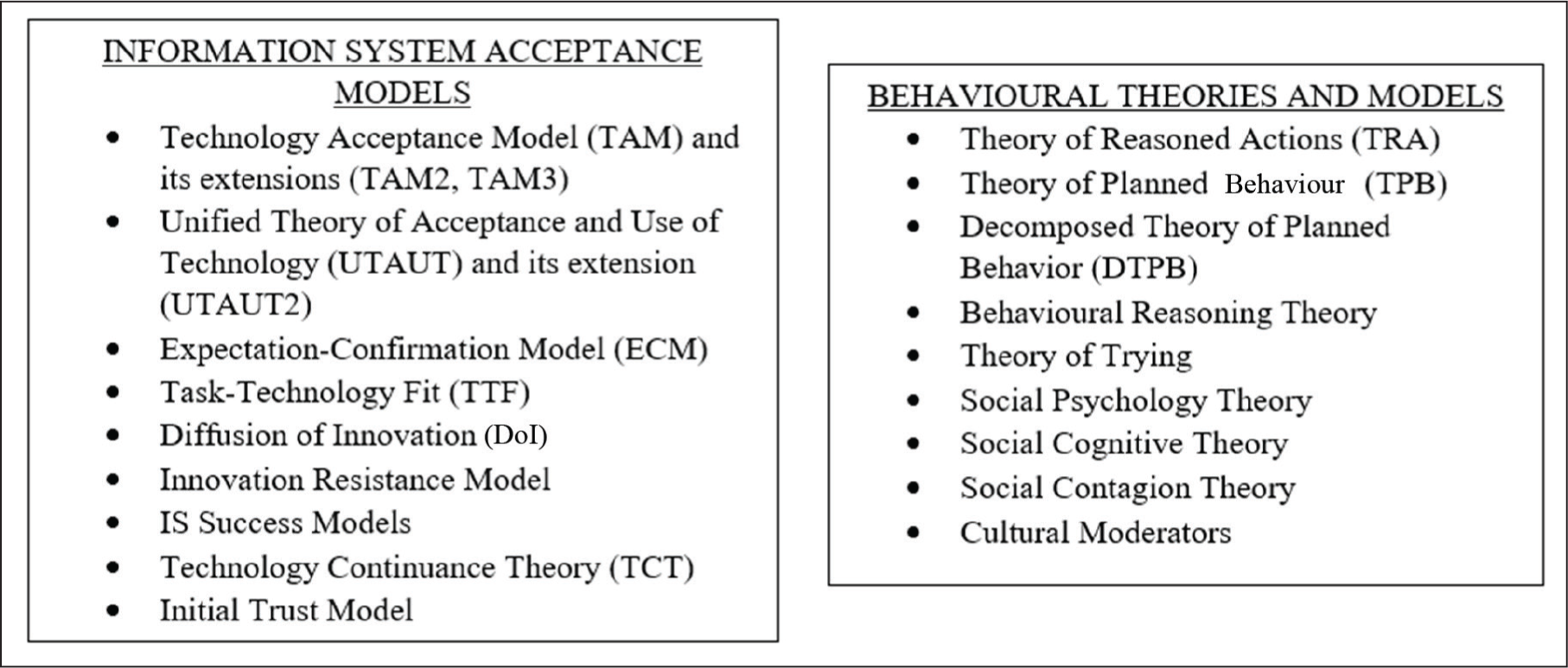

Theoretical Models

The researchers have used different Information System (IS) acceptance models and behavioural theories in their studies related to mobile banking (see Figure 7). Researchers (Chawla & Joshi, 2017; Püschel et al., 2010) have, sometimes, used a combination or mixture of these theories for better prediction of technology acceptance among the target groups under various studies.

A thorough analysis of previous studies makes it crystal clear that TAM (Davis et al., 1989), UTAUT (Venkatesh et al., 2003) and UTAUT2 (Venkatesh et al., 2012) have been put to more use than any other theories and models. TAM is the most widely used model for predicting people’s behavioural intention to adopt mobile banking and the same finding has been put forward by previous study on similar literature (Shaikh & Karjaluoto, 2015). TAM has a strong base of two constructs, namely, PU and PEOU which are assumed to be affecting Attitude towards the technology which, in turn, plays a crucial role in influencing the BI. The simple structure of explaining technology acceptance is the chief reason behind the wide use of this model. As a product of the mixture of various models of the past, UTAUT presents a mirror-like reflection of the constructs used in the previous models. For instance, the relative advantage of DoI (Rogers, 1995) is identical with the PU of TAM and Venkatesh et al. (2003) coined a new construct called Performance Expectancy (PE) by combining such similar constructs. UTAUT2 is a further improved version consisting of three more antecedents of IS acceptance.

Researchers have used these theories simultaneously and, in many cases, TAM is used along with other theories viz., DoI (Deb & Lomo-David, 2014; Koenig-Lewis et al., 2010), TTF (Baabdullah et al., 2019b), TPB (Luarn & Lin, 2005), Social Cognitive Theory and UTAUT (Singh & Srivastava, 2018). Chiu et al. (2017) have combined TRA and TPB. Giovanis et al. (2019) considered four theories for comparison, viz., DTPB, TAM, TPB and UTAUT, and the result showed the superiority of DTPB over other theoretical models in terms of explaining mobile banking adoption.

The systematic analysis of the literature shows that the researchers have used different dependent variables in their studies, of which BI mobile banking tops the list, followed by CI, adoption and actual use behaviour. While the probability of people using the innovative technology is known as BI, the adoption and usage of the system already in vogue is called actual use (Davis et al., 1989), and a flawless assessment of the people who have already shifted to any technology and intend to continue the usage in the future too defines and describes in detail the concept of continuance intention to use (Bhattacherjee, 2001).

Majority of the researchers have adopted TAM and extended the same using additional constructs such as trust (Azad, 2016; Sharma et al., 2017; Siyal et al., 2019a; Zhang et al., 2018), perceived risk (Alalwan et al., 2016; Mohammadi, 2015a, 2015b; Priya et al., 2018), compatibility (Azad, 2016; Mohammadi, 2015a, 2015b; Sharma et al., 2017), social influence (Azad, 2016; Bhardwaj & Aggarwal, 2016; Gu et al., 2009; Kumar et al., 2017), awareness, resistance (Elhajjar & Ouaida, 2019; Siyal et al., 2019b) and perceived self-efficacy (Alalwan et al., 2016; Saji & Paul, 2018) to determine BI. The UTAUT constructs (PE, effort expectancy, social influence and facilitating conditions) as well as the additional constructs embedded in UTAUT2 (habit, hedonic motivation and price value) were also validated as influencing factors of BI mobile banking (Alalwan et al., 2017). Some researchers have used TAM for predicting actual use (Marakarkandy et al., 2017; Riskinanto et al., 2017; Yousafzai & Yani-de-Soriano, 2012), for which BI was the important influencing factor (Alalwan et al., 2016; Prompattanapakdee, 2009).

Besides BI, theories like TCT, ECM, TAM and TTF were used to predict continuance intention (Baabdullah et al., 2019b; Foroughi et al., 2019; Mohammadi, 2015b; Susanto et al., 2016). Apart from this, attitude (Bhardwaj & Aggarwal, 2016; Changchit et al., 2017; Chawla & Joshi, 2018), satisfaction (Khan et al., 2018; Masrek et al., 2014), resistance to adopt (Chaouali & Souiden, 2019; Cruz et al., 2010), customer loyalty (Baabdullah et al., 2019a), initial trust (Zhou, 2012) and trust (Malaquias & Hwang, 2016a; 2016b) were also kept as dependent variables and predicted the same with relevant independent variables.

Target Group

The studies chosen for analysis are found to have focussed on different target groups, and they were selected based on age group, occupation and use of mobile banking. Bank customers were the target groups in most of the studies considered for analysis. Some studies have targeted a few general groups who all tend to be bank customers, like internet users with smart phones (Mehrad & Mohammadi, 2017) and cell phone users (Glavee-Geo et al., 2017). There are studies which exclusively focussed on rural people (Kishore & Sequeira, 2016; Tobbin, 2012) as well as urban people (Gupta et al., 2017). Consumers in general, are also approached to study their intention to adopt mobile banking (Chawla & Joshi, 2017).

Adults, in general, have been considered by Baptista and Oliveira (2015), whereas specific studies on young people (Koenig-Lewis et al., 2010; Priya et al., 2018) and old-age people (Chaouali & Souiden, 2019; Motwani, 2016) have also been found. Students are the single-most targeted group, and few studies (Chawla & Joshi, 2018; Zhou et al., 2010) have considered professionals along with students. There were distinguished studies among users (Bankole et al., 2011; Kwateng et al., 2019; Shareef et al., 2018; Susanto et al., 2016), potential users (Bryson et al., 2015) and non-users (Chaouali et al., 2017; Chiu et al., 2017; Cruz et al., 2010; Gupta & Arora, 2017) of mobile banking as well as the mix of both users and non-users (Chawla & Joshi, 2018; Püschel et al., 2010).

Sampling Methods

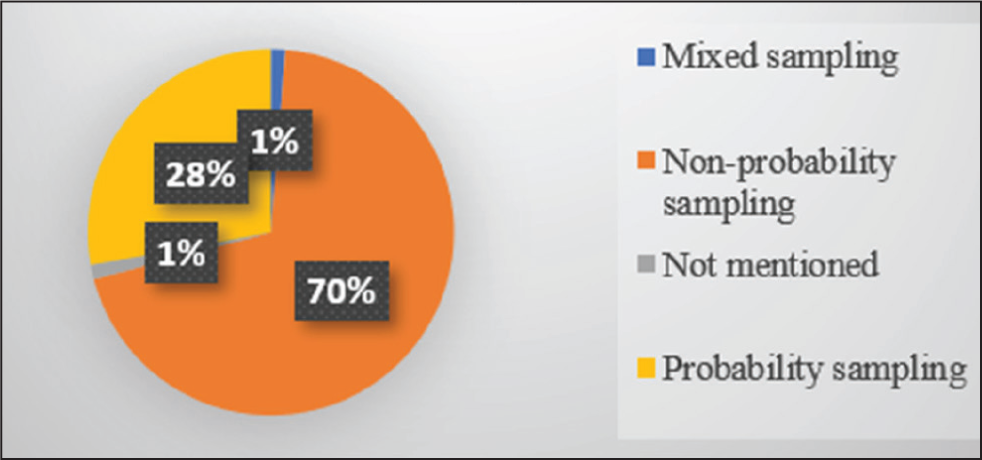

Hence we have chosen only primary data-based studies, where the sampling method plays a significant role. The generalization of findings can be truly done only if the samples are true representations of the population, and for that, theoretically, random sampling techniques should be adopted. However, practically, the researchers would also undertake non-probability sampling methods because of the unavailability of the sampling frame (Giovanis et al., 2019), indefinite population, inaccessibility to the respondents, time and cost and the like. Here, 70% of the studies (see Figure 8) have used non-probability methods of sampling, especially convenient sampling techniques.

Probability sampling techniques such as systematic sampling (Wessels & Drennan, 2010), simple random sampling (Masrek et al., 2014), stratified random sampling (Siyal et al., 2019b), etc., have been used by 28% of the studies considered.

Researchers have used combinations of different sampling techniques. Both snowball sampling and convenient sampling were employed simultaneously (Koenig-Lewis et al., 2010; Veríssimo, 2016). Kishore and Sequeira (2016) adopted a mixed sampling technique consisting of both probability and non-probability techniques. Only one study has not mentioned the sampling methods that they have adopted. According to the authors’ calculation, the average sample size of these 79 studies is estimated at 411, ranging from the lowest of 97 samples (Tobbin, 2012) to the highest of 3,584 (Cruz et al., 2010).

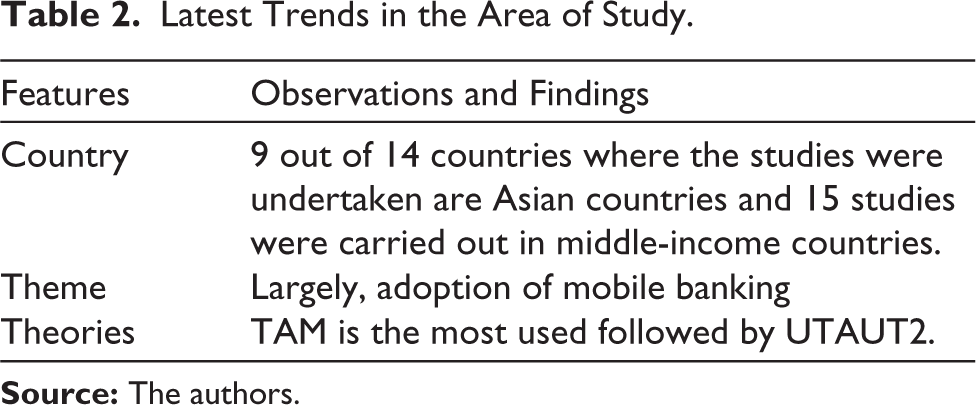

Latest Trends

In order to understand the latest trends in terms of the countries, themes considered and theories followed in the studies on mobile banking, the articles published in the last two years (2018 and 2019) of the last decade were considered, which resulted in the choice of 23 articles. A close watch over the recent articles would certainly be of immense assistance to future scholars in understanding the current status of research in the area of mobile banking, and that would properly guide them in choosing the right road to take (see Table 2).

Latest Trends in the Area of Study

Discussion

The abundant availability and easy reachability make mobile phones a suitable platform for banking, which, in turn, has induced researchers in the recent past to pay much attention to various aspects of mobile banking. It is observed that, though developing countries vie with developed ones in the adoption and usage of mobile banking, the result is not encouraging as they have yet to reach the expected mark. The literature analysis shows that the studies on mobile banking in low-income countries are few and far between, which reveals a research gap in the studies targeting people of low-income countries on their attitude towards the adoption and use of mobile banking.

The frequency of publication in this field has begun to grow in gallops, particularly in the last decade of the study period. Though this rapid increase in the frequency of publication is seen as a welcome sign of encouragement, the focus more on the adoption of mobile banking is discouraging and a matter of concern. The majority of the extant studies have focussed on the initial adoption of mobile banking (Susanto et al., 2016). Mere adoption and infrequent usage will not be helpful for the prospects of mobile banking. It is imperative for all the stakeholders, especially the people at the helm of affairs in government, banking sector, financial institutions and corporate, to have a thorough knowledge and perfect understanding of the factors that motivate the adoption and intention to use mobile banking, followed by the CI the same. The successful implementation of mobile banking can be counted only if people are ready to continue using it in the future, for which they should be satisfied with the services provided by the system.

The high probability of becoming future potential consumers with a positive bend of mind towards the adoption of innovative payment methods makes the young, especially students, the most targeted groups. But the older generation should also be taken into consideration, then only technologically advanced products and services like mobile banking may reach their potential. With a view to widening the scope of research in this field, some researchers like Tobbin (2012) have considered the unbanked rural dwellers and whether the inclusion of such excluded sections of society would be helpful in achieving digital financial inclusion.

TAM and UTAUT are the most widely used models simply because they are easy to understand and have the ability to adapt to any technology existing or being introduced. Shaikh and Karjaluoto (2015) also found that TAM is the most widely used model in their literature analysis on mobile banking adoption. Researchers tend to extend TAM with additional constructs (Sharma et al., 2017) or the combination of different theoretical models like DoI and DTPB (Püschel et al., 2010) or their own model (Kim et al., 2009) to explain the adoption intention. In addition to TAM and UTAUT, other models such as ECM, DTPB, TPB, DoI, TTF, UTAUT2, etc. are also found to have been used in other studies.

The factors that trigger the use of mobile banking include, but are certainly not limited to, PEOU, PU, perceived risk, perceived security, social influence, trust, attitude, effort expectancy, PE and compatibility. The constructs embedded in the most used model, TAM, naturally top the list in terms of usage. Many of the researchers who have used these constructs have confirmed their significant influence on adoption of mobile banking (Saji & Paul, 2018; Sharma et al., 2017), attitude towards mobile banking (Changchit et al., 2017) and continuance intention (Mohammadi, 2015b) as well.

Though security concerns and risk perceptions always act as adoption barriers in any e-banking method (Gupta & Arora, 2017; Kim et al., 2010), the same is not included as a basic construct in prominent models like TAM and UTAUT. Hence, the researchers have extended these models with security perception by way of trust, perceived security and perceived risk factors. The qualitative interviews conducted by Zhao et al. (2010) revealed that, generally, people lack trust in the banking system. Therefore, the distrust in the banking system should be studied, and proper measures should be undertaken to improve the security perception. Perceived risk is often considered as a second-order construct consisting of several dimensions such as financial risk, time risk, performance risk, privacy risk, social risk, security risk and psychological risk (Akturan & Tezcan, 2012; Chen, 2013; Giovanis et al., 2019). Tan and Lau (2016) have proposed a model based on UTAUT in which the facilitating condition is replaced by perceived risk. Giovanis et al. (2019) incorporated perceived risk along with four prominent theories and tested the explanatory power of each concerning mobile banking adoption. However, perceived risk was also found to be insignificant in predicting mobile banking adoption (Farah et al., 2018; Glavee-Geo et al., 2017). Though the traditional theories have not paid due importance to perceived risk and trust-related factors, these are incorporated by the researchers for a better prediction of mobile banking.

The studies have focussed more on predicting the behavioural intention (BI) of people to use mobile banking. The aforementioned models also better predicted this dependent variable. Actual use was said to be determined by the BI the system (Davis et al., 1989). But there is a need to develop models for predicting satisfaction, continuance intention and customer loyalty for the growth and expansion of mobile banking technology. ECM (Bhattacherjee, 2001) was used by Susanto et al. (2016) to determine the factors influencing CI mobile banking services. This model is also extended to include security-related factors. An integrated model combining ECM, TAM and Task-Technology Fit (Goodhue & Thompson, 1995) was empirically tested by Yuan et al. (2016) for the same purpose and found significant.

Conclusion and Scope for Future Research

Mobile banking adoption is an extensively but not exclusively explored research area. But the partly attained aim of the adoption of mobile banking attracts researchers all over the world into its fold every day. More diversified studies are required in this field for which qualitative techniques can be employed in the first stage and empirical validation with quantitative analysis can be done in the later stage.

So far, most of the studies have targeted young people and adults in civilized and organized societies. Hence, future researchers have to focus on more distinct groups such as the otherwise-abled, migrant workers and marginalized sections of society to understand their attitude and intention towards mobile banking. The conduct of qualitative studies among the aforementioned socially and economically excluded groups will help to identify the inhibiting factors that prevent them from adopting mobile banking.

There is a need to shift the focus from adoption to continuous usage of mobile banking. Because people may adopt certain technologies and later withdraw themselves from using them. Sustained use is, therefore, a significant aspect that needs to be focussed on by future researchers. As customer retention is as important as customer creation, studies focusing on identifying the barriers to continuance usage of mobile banking may be undertaken in the future. Continuance usage intention of young people is to be explored as they are the future users of this innovative method of banking. The established theoretical models and empirically validated constructs can be attributed to the research on CI mobile banking.

Most of the studies have made an attempt to explore the factors affecting mobile banking adoption based on various IS theoretical models, especially TAM. However, integration of different other theories would certainly help future researchers give an extensive account of the determinants of mobile banking adoption. In order to find out the predictors and inhibitors of adoption of mobile banking, future researchers may adopt and extend existing theories, especially UTAUT, ECM, TTF, UTAUT2, etc., TAM can still be modified by incorporating additional constructs which can be figured out with the help of more qualitative data collection techniques, especially FGDs and in-depth interviews. As trust-building is a key factor in the adoption of mobile banking, the antecedents of trust need to be framed clearly. But it remains an indisputable fact that only a few studies have paid due importance to the study of the impact of trust on mobile banking adoption.The outcome of the studies undertaken in the recent past reveals that most of the studies are unidimensional, sticking around initial adoption and TAM-based conceptual models. Studies focusing on continuance usage intention will help to develop conceptual models based on ECM and Technology Continuance Theory.

Systematic literature reviews and meta-analysis are scarce in this field of study. The application of a meta-analytical approach will help to synthesize and consolidate the effects of different factors that are found to be affecting mobile banking adoption and usage. As mobile banking has become an inevitable one, the higher level of mobile penetration in the society and the efforts to make the financial system more inclusive would certainly result in remarkable changes in both adoption and usage of mobile banking in the years to come.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.