Abstract

This study analyses the difference in stock market reactions to dividend announcement during the pandemic. The thirty constituent stocks of Sensex, the index of Bombay Stock Exchange (BSE), is used for analysis. This allows cross-industry comparison of the market reaction. The study examines stock market reactions covering 44 days around the dividend announcement dates. The primary objective of this study is to understand whether the price adjustment linked to the dividend announcement news during the pandemic was different from the earlier years. This empirical study employs the conventional event study methodology using abnormal returns (ARs) to examine the stock market reaction to dividend announcement. The market reaction to dividend announcement was increasingly positive during the pandemic, compared to previous years. The statistical pooled t-tests showed there was a significant relationship between the pandemic and ARs. The findings also indicate that the difference in the market reaction to dividend announcement was more prominent in services stocks than that in manufacturing. Further, the results also verify the weak-form of efficiency of Indian stock exchange.

Keywords

Introduction

COVID-19 and the subsequent lockdowns had an unprecedented impact on economies across the world. Though the economic slowdown was a global phenomenon, the extent of the impact dependent on individual country characteristics and its exposure to the pandemic. The global financial markets crashed in early 2020, even before official forecasts of the economic impact were available. The magnitude of financial market crash and the reactions of investors were different across markets. In this context, this study attempts to compare the investor reaction to dividend announcement on the stock returns during the pandemic, compared to preceding years.

Dividend policy of a company relates to the disbursement of profits to its shareholders. The shareholder theory postulates that the dividend policy is guided by the primary objective of the firm, that is, to maximize shareholder wealth (Friedman, 1970). The companies in growth phase decide to reinvest the profits for future growth prospects, much in line with shareholder expectations. Firms which have crossed the growth inflection point generally pay dividend. In such cases, the shareholder returns are tied to the dividend than on capital gains. Many research studies have tried to understand the dividend policies of companies based on its geography, industry segments and firm characteristics (Bhattacharyya, 2007; Fama & Babiak, 1968; Michel, 1979). Researchers have also studied the investor reaction to dividend announcement using stock price fluctuations (Black & Scholes, 1974; Blume, 1980; Charest, 1978; Fama & French, 2021; Hodrick, 1992). Theories suggest that stock prices should rise when a company is about to announce dividend and decline once the amount is disbursed (Baker et al., 2020). However, this rule is rarely followed due to external factors and investor expectations (Hodrick, 1992).

The empirical evidence supports diverse thoughts on dividend policies, broadly classified as dividend irrelevance and dividend relevance policies. Though these approaches have their pros and cons, none provides complete and satisfactory guidelines across markets and scenarios. The market reaction to changes in share prices is affected not only by the company’s performance and growth potential but also by the nature of the market. Markets tend to be driven by the informational content of events in the external environment and information communicated to the shareholders through various decisions. The dividend decision has a signalling effect, that is, the market perceives the dividend pay-out as the management’s future growth plans. The dynamics between dividend policy and stock returns has been an interesting topic of research among academicians.

According to efficient market hypothesis, the price of financial instruments reflects all the available information to the market (Malkiel, 2003). Hence, we can study the long-term impacts of an event by examining the movement of stock price surrounding the event. This approach, referred in literature as event study methodology, is extensively used in empirical studies on dividend policies impacting stock price movements. COVID-19 pandemic was an unprecedented, non-systemic shock to financial markets. In this article, we adopt the well-established event methodology to identify the impact of dividend announcement information on the daily stock returns of 30 companies listed on the Bombay Stock Exchange (BSE). We compare the market reaction to dividend announcement during the pandemic to that of preceding years. As the index is diversified, analysing the constituents of index allows comparison across industries.

Based on our review, this is the first study examining how the pandemic influenced the Indian stock market reaction to dividend announcement. In addition to providing insights into investor behaviour under uncertainty, the study examines the difference in market responses to non-systemic risks. The study also emphasizes the need to analyse the market reaction by industry. The article is structured into six sections. The following sections cover the theoretical background and literature review, research methodology, results and discussion and conclusion.

Literature Review

Theoretical Background

The theories concerning dividend pay-outs can be broadly classified into two, namely Irrelevance theory of dividend and Relevance theory of dividend, based on whether dividends paid is relevant to the value of the firm. A brief over view of both these approaches are provided below.

Irrelevance Theories of Dividend

The proponents of dividend irrelevance theory suggest that a company’s declaration and payment of dividends should have no impact on the firm’s stock price. They argue that shareholders do not differentiate between dividend and capital appreciation. Hence, according to this theory shareholders are neutral between dividend payments and firm withholding dividends to reinvest in future growth. The two major approaches under this category are residuals theory of dividends (Higgins, 1972) and Modigliani and Miller’s (MM) approach (Miller & Modigliani, 1961). The residual theory states that a firm will find it optimal to pay dividends only if there is a residual retained earning after allocating funds to all future projects with positive NPV. Thus, the dividend policy is treated as a passive process which as no influence on the value of the firm. Similarly, MM approach argued that firm’s value is dependent on its earning power, risk and not on how it distributes earnings. According to the MM model, higher cost of capital will neutralize the dividend effect. However, this model was based on the assumptions of perfect market conditions, absence of taxes, no transaction costs or asymmetric information, and no flotation cost. Though many researchers supported the MM model (Adesola & Okwong, 2009; Chen et al., 2002; Uddin & Chowdhury, 2005), several others argued that the model was based on unrealistic assumptions (Benartzi et al., 1997; DeAngelo & DeAngelo, 2007; Rashid & Rahman, 2008).

Relevance Theories of Dividend

Theoretical approaches stating that the dividend pay-out strategy has a significant role in determining the market value of firm’s stock are commonly referred to as dividend relevance theories. Five major approaches are: Walter approach (Walter, 1963), Gordon (1962) approach, dividend discounting (Farrell Jr, 1985) dividend signalling and agency cost approach (Jensen, 1986).

According to the Walter approach the dividend decision will impact the firm value if the cost of equity is different from the rate of return that the company could earn on retained earnings. Gordon’s approach (also called The-Bird-in-the-Hand theory), the price an investor is willing to pay for a stock depends only on two factors—projected dividends and capital gain. Dividends are paid at regular intervals while capital gain is reported after a longer period of time. Hence, Gordon argued that investors need not be indifferent to earning returns through dividends and capital gains. For example, a risk-averse investor might associate a lower degree of risk with regular dividend payment, rather than the capital gains in the distant future. Hence, dividends are theorized as involving the trade-off between the current income and the future selling price for the investors. Extending Gordon’s approach, the dividend discounting approach hypothesized that the share price is the present value of all future dividend payments. The informational content of dividends hypothesis/dividend signalling asserts that cash dividend strategy reflects management’s assessment of a firm’s future profitability. This ‘dividend signalling’ has motivated a considerable amount of theoretical and empirical research. Empirical models in literature examine dividends as signals (John & Williams, 1985). There is a consensus among researchers that dividend changes convey specific ‘insider’ information about a firm’s future earnings (Bhattacharya, 1979; John & Williams, 1985; Miller & Rock, 1985).

Jensen (1986) Click or tap here to enter text.and Lang and Litzenberger (1989) Click or tap here to enter text.have applied the agency cost theory approach to explain shareholder reaction to dividend pay-out. According to their argument, distributing profits in the form of dividends reduce the free cash flow available for allocation to projects based on the manager’s discretion. Managers would prefer the organization to grow as their compensation is typically linked to growth. Lack of internal funds will force managers to raise capital from the financial market, which would expose their actions to higher scrutiny. Hence, though the shareholders would prefer dividend payment, the management will be hesitant to pay-out dividend. They argued that the magnitude of this conflict of interest between shareholders and managers over the payment policies of dividends could explain the stock price reaction. These findings were further supported by the theoretical work conducted by Easterbrook (1984) Click or tap here to enter text.. According to his reasoning, dividend policies should be designed to minimize total costs, including capital, agency and taxation costs. He argued that exposure to increased scrutiny of the capital markets could reduce the agency cost in the long-run as external stakeholders exercise increased monitoring of managerial decisions.

Recent Literature

Empirical studies to establish the relationship between dividend payment and stock price was pioneered by the work done by Lintner (1956) Click or tap here to enter text.. Lintner examined the determinants of dividend policy and its impact on the market value of the firm based on primary data collected from the management of 28 firms. The results of the study indicated a significant relationship between dividend pay-out and market value. Lintner also concluded that the firms prefer to have a stable dividend pay-out policy and hence focused on maintaining earnings. Gordon (1962) Click or tap here to enter text, introduced the dividend relevance theory and showed dividend pay-outs have a positive impact on share price. He further concluded that dividend pay-outs reduce the risk of stock price volatility.

Recent empirical studies on the impact of dividend announcement on the stock price is inconclusive. Several studies found that dividend payment has a significant positive impact on stock price (Ariff & Finn, 1989; Jose & Stevens, 1989; Kato & Loewenstein, 1995; Lee, 1995; Ogden, 1994), while others found a negative relationship (Rane, 2018; Uddin & Chowdhury, 2005). A few studies have found no relationship between dividend policy and stock price (Allen & Rachim, 1996). A positive relationship is explained using investors’ preference for dividend (The-Bird-in-the-Hand theory) while the negative relationship is explained in literature using the absence of long-term growth (signalling effect) and tax effect. John and William’s (1985) showed a positive relationship between dividend pay-out and stock reaction, showing investor’s preference for dividends. The signalling effect of dividend announcement on stock price was exhaustively studied in the literature. For example, results of the study conducted by Capstaff et al. (2004) Click or tap here to enter text. on the Oslo Stock Exchange (OSE) supported the relevance theory. Several studies conducted across regions have also argued that the dividend policy has a significant impact on the stock price movement (Baker et al., 2002; Dong et al., 2005; Myers & Bacon, 2004; Travlos et al., 2001). Contrasting the above results, some researchers have also argued that dividend policy has no impact on the share price (Adesola & Okwong, 2009; Denis & Osobov, 2008; Ling et al., 2008). According to these researchers, rather than signalling the future performance, dividend policy was a reflection of the company’s past performance.

Similar studies on the Indian stock market have also given mixed results. The study conducted by Pani (2008) investigated the relationship between dividend-retention and stock price behaviour of 500 firms listed in BSE during the period 1996–2006. While controlling the firm’s size and long-term debt-equity ratio, the findings indicated a positive relationship between dividend-retention ratio and stock price. However, the research conducted on specific industries have shown irrelevance of dividend policy on shareholder wealth (Azhagaiah & Priya, 2008).

Researchers have established that the economic policy uncertainty has a significant impact on dividend policy with companies adjusting their dividend pay-outs in response to the crisis (Abreu & Gulamhussen, 2013; Attig et al., 2021). The literature covering the stock market reaction to dividend pay-out during a crisis is limited. In this context, this article attempts to understand the stock market reaction to dividend pay-outs during the pandemic.

Research Methodology

To examine the impact on the pandemic on the market reactions to the event—dividend announcement—this study analyses the daily returns of the constituents of Sensex, the index of the Bombay Stock Exchange (BSE), the largest stock market in India by market capitalization. Consistent with the existing literature, an event window of 45 days surrounding the dividend announcement was considered for analysis. Considering the lack of precedency, we expect the market reactions to dividend announcement during the pandemic to be significantly different, compared to earlier years. Hence, we propose the following null hypotheses.

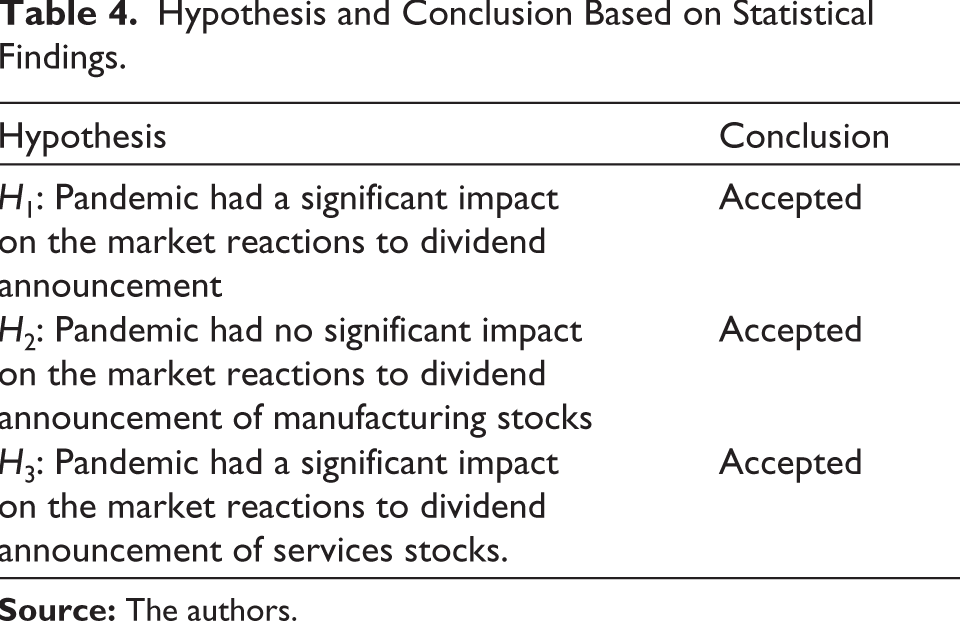

H1: Pandemic had a significant impact on the market reactions to dividend announcement.

We further drill down the analysis to industry segments, namely manufacturing and services. The manufacturing industry was more severely impacted by the pandemic, compared to services companies (Sahoo & Ashwani, 2020). Considering the uncertainty, dividend payment might not have been a significant motivator for investors in the manufacturing industry. Services industries such as finance, information technology and telecom sectors shifted their operations online, thereby remaining largely immune to the pandemic. Bearing this in mind, we expect a difference in the market reaction to dividend announcement between manufacturing and services industry.

H2: Pandemic had no significant impact on the market reactions to dividend announcement of manufacturing stocks.

H3: Pandemic had a significant impact on the market reactions to dividend announcement of services stocks.

The existing research on the Indian stock market shows that the market is weakly efficient (Hamid et al., 2017). In a weak form of efficiency, any new information, other than the historical values and trends, would alter the market price of a stock. Following the earlier hypothesis, we expect the stocks to have reported positive cumulative abnormal returns (CARs) in the event window surrounding the dividend announcement during the pandemic.

H4: Dividend announcement provided a significantly positive CAR during the pandemic

Again, we expect the CARs to be significantly different from zero and positive only for the services industry stocks.

H5: Dividend announcement of manufacturing stocks had no significant impact on its CAR during the pandemic

H6: Dividend announcement of services stocks had a significant positive impact on its CAR during the pandemic.

Data Collection

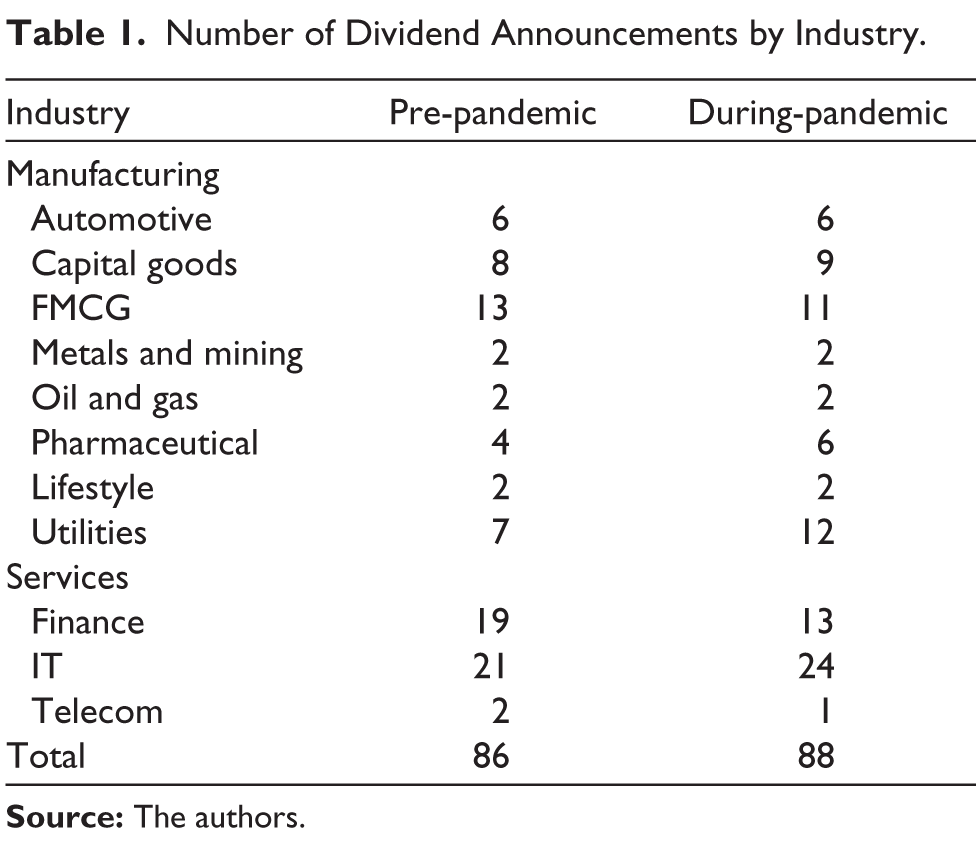

This study covers the impact of dividend announcement on the daily stock returns of the current 30 constituents of Sensex during the period 2018–2021. The period considered for the study covers two years during the pandemic—2020 and 2021, and two years prior to the pandemic—2018 and 2019. We had a total of 174 dividend announcement during the four years. The industry-wise breakup of the dividend announcement is provided in Table 1.

Number of Dividend Announcements by Industry

Event Window

In event studies related to financial markets, a period around the event is identified to track prices or returns of securities. This period is referred to as the event window in literature (Campbell et al., 1997). Following the event study methodology, we considered an event window of 45–30 days prior, event date and 14 days post the event. The event date, that is, date on which the company’s board of directors announces its next dividend payment, is taken as t = 0. The dividend announcement date is also known as the ‘announcement date’ in literature. The 30-day window before the event and the 14-days window after the event will be referred to as ‘pre-event window’ and ‘post-event window’, respectively, in the rest of the article. The post-event window, that is, t = +1 to t = +14 covers the ‘price adjustment period’ during which the market adjusts the stock price based on the new information available. The adjustment of stock price will alter the daily return during the ‘price adjustment period’.

We considered 174 dividend announcements during 2018–2021 with a complete event window, as required by the methodology used in this study.

Event Study Approach

The event study approach is a well-accepted methodology used by academicians to understand the impact of specific events across business domains (Binder, 1998). In this study we follow the event study approach proposed for financial market analysis (Campbell et al., 1997). According to this approach, we examine the abnormal returns (ARs) reported by the stocks during the event window. ARs are the difference between the actual daily returns and the returns predicted by the market model (Strong, 1992).

Efficient market hypothesis classifies financial markets based on the market reaction to available information (Malkiel, 2003). In a weak form of efficiency, any new information, other than the historical values and trends, would alter the market price of a stock. The stock price changes will depend on how the investors perceive the news to affect the firm’s future cashflows. To understand whether any event had an impact on the stock price, ARs (pre and post-event) and cumulative abnormal returns (CARs) during the event window are calculated. The above hypotheses are tested based on the statistical significance of the abnormal return measures.

The calculation of ARs is as shown in Equation (1).

The first step in the analysis is to develop a market model for predicting the daily returns. The daily returns of a given company i (R it ) was regressed against the market daily return (R mt ). The parameters αi and βi in Equation (1) were estimated by taking the daily returns during 2018–2021. This approach was taken as the dividend announcements were spread throughout the year. The approach also helped in averaging out the daily returns across the years.

Results and Discussion

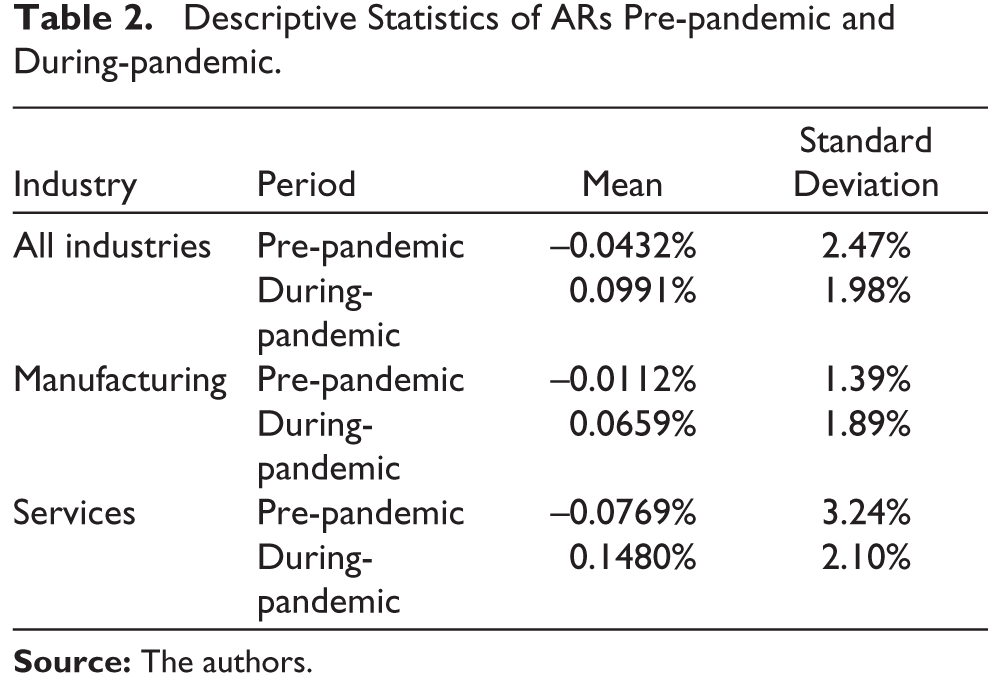

The descriptive statistics of ARs pre and during-pandemic are provided in Table 2.

Descriptive Statistics of ARs Pre-pandemic and During-pandemic

The hypotheses are tested using pooled t-test at 95% confidence level. To do this analysis, the daily returns of pre and post-event windows are assumed to be independent and normally distributed. Correlation analysis between the ARs of pre and post-event windows will also be conducted to test the hypothesis.

Hypothesis Testing

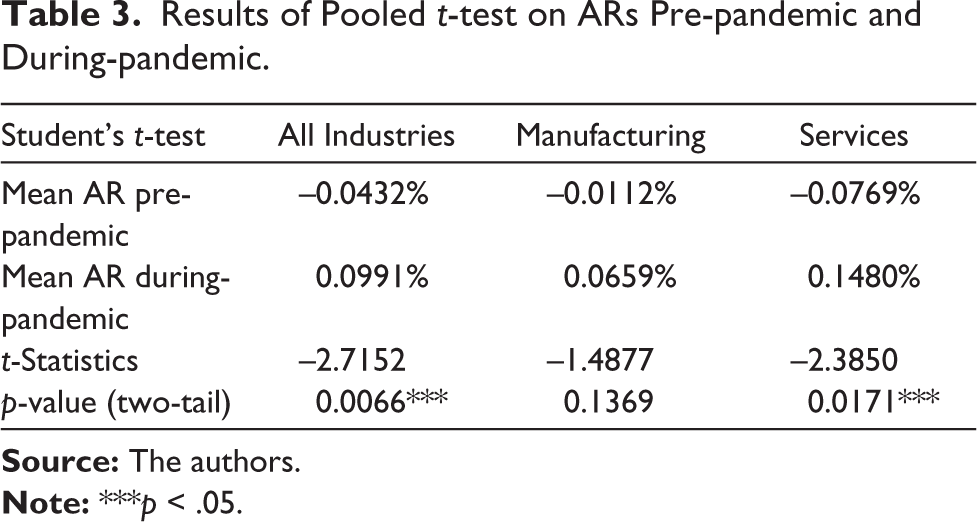

After calculating the ARs, we test the first hypothesis, that is, whether the daily abnormal returns were significantly different during the pandemic as compared to the pre- pandemic period, using pooled t-tests. The null hypothesis of the t-test is that there is no significant difference in the average ARs between the two time periods. The results of the pooled t-test are provided in Table 3.

Results of Pooled t-test on ARs Pre-pandemic and During-pandemic

As the p-value was less than 0.05 when we consider all industries (Table 3), we reject the null hypothesis. We conclude that the daily ARs posted during the pandemic were significantly different from the earlier time period. Further analysis of manufacturing and services industries shows that the difference in ARs between the time periods was significant for services industry. Interestingly, the mean ARs surrounding the dividend announcement during the two time periods indicate that though it was negative pre-pandemic, ARs were positive during the pandemic. This is in line with our expectation that the investors would have been more enthusiastic about the dividend payment in times of uncertainty. Existing literature indicates that during the pandemic, the predictability of the stock price movement across the market was uncertain (Ibikunle & Rzayev, 2020). In such cases, the dividend announcement would provide motivation to the investors thereby increasing the ARs (Miller & Modigliani, 1961). However, the difference was significant only for services industry. The difference in average ARs between the two time periods was not significant for manufacturing stocks. The manufacturing companies were severely hit by the pandemic and its subsequent lock-downs as their supply chains are heavily dependent on processing and transportation. In contrast, the services industry (covering finance, information technology (IT) and telecom) seamlessly shifted its operations online with the aid of technology. This could explain the higher investor enthusiasm towards dividend announcements of services companies during the pandemic. Understanding the trend, the services companies also increased the frequency of dividend payment during the pandemic.

To conclude, the results of the pooled t-test (Table 3) allow us to form conclusions about the first three hypothesis. The hypothesis and our conclusion are shown in Table 4.

Hypothesis and Conclusion Based on Statistical Findings

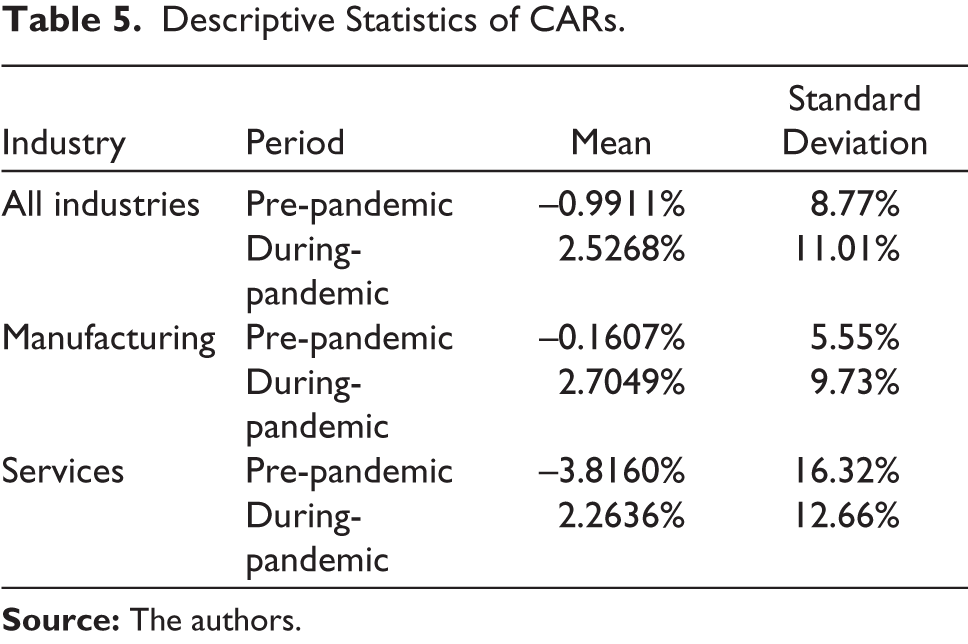

We proceed to examine the CARs obtained by the investors. The descriptive statistics of CARs is provided in Table 5.

Descriptive Statistics of CARs

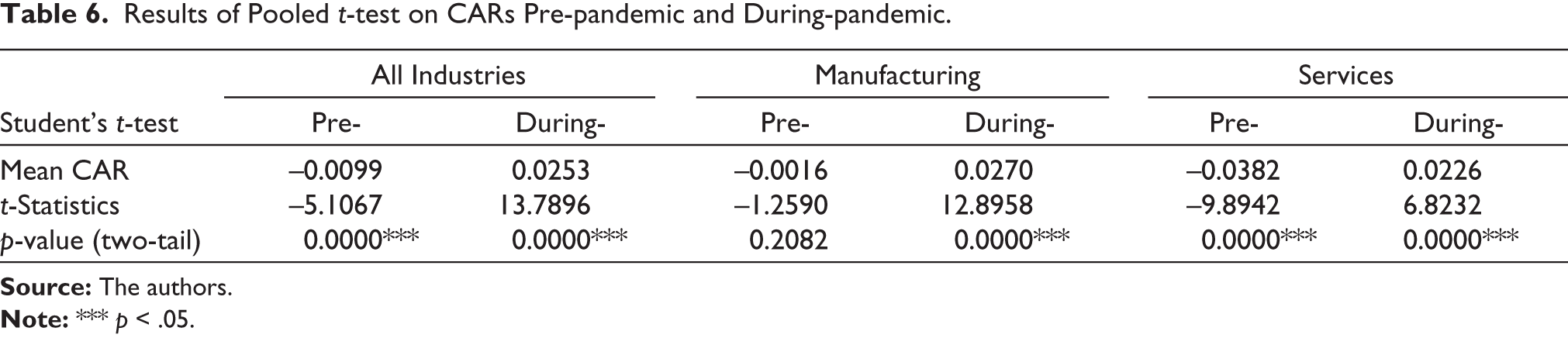

We proceed with the pooled t-test to check whether the CARs were significantly different from zero. The process is repeated for the two time periods, that is, pre-pandemic and during-pandemic periods and industry segments (manufacturing and services). The results as shown in Table 5 indicate the weak form of efficiency of the Indian stock market. Across segments and time periods, except for manufacturing in pre-pandemic period, the dividends caused a non-zero cumulative abnormal return, that is, the market was not able to correct the new information regarding dividend announcement. This led to a non-zero CAR surrounding the dividend announcement. However, unlike the earlier period, the mean CAR around dividend announcement during the pandemic was significantly positive, as is evident from Table 6.

Results of Pooled t-test on CARs Pre-pandemic and During-pandemic

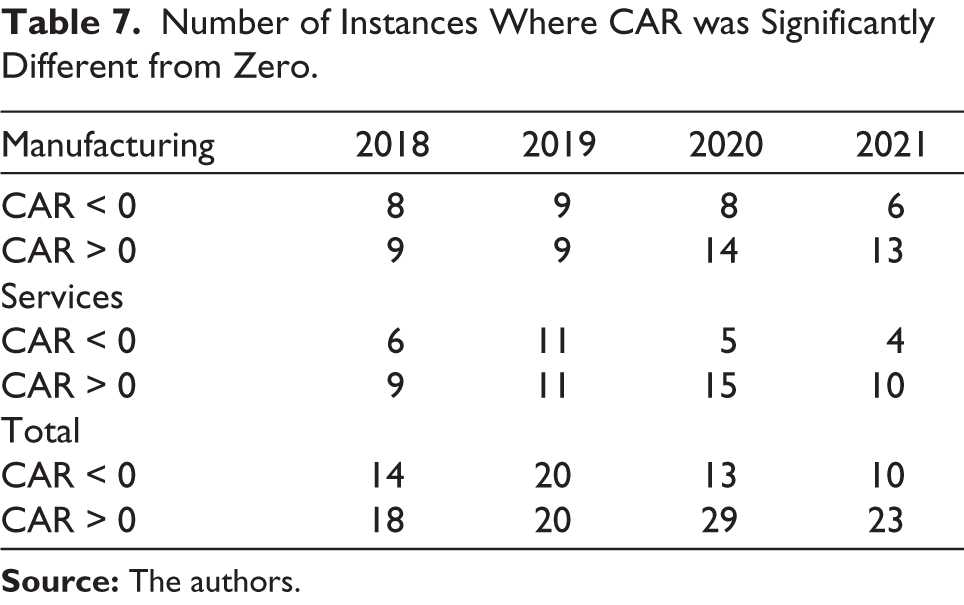

In the next step we considered individual dividend announcement events and checked in how many of these instances the CAR within the event window was significantly different from zero. Table 7 categorizes the events based on whether the mean CAR was greater than zero or less than zero. According to the results, there was a substantial increase in positive CARs during the pandemic, both in manufacturing and in services industries. This result shows that the market reacted positively to dividend announcement during the pandemic years, as compared to previous years.

Number of Instances Where CAR was Significantly Different from Zero

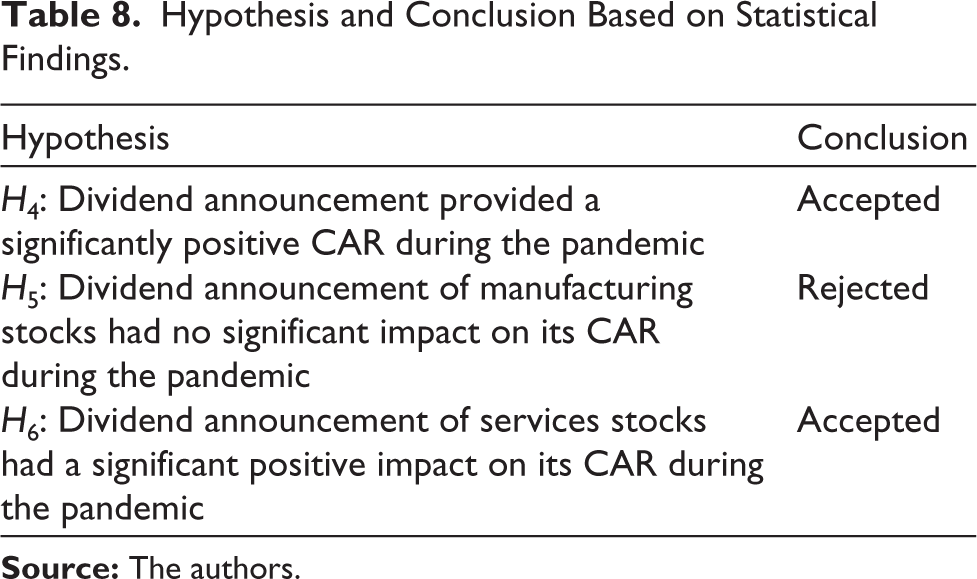

The results of the pooled t-test (Table 6) allow us to form conclusions about the last three hypothesis. The hypothesis and our conclusion are shown in Table 8.

Hypothesis and Conclusion Based on Statistical Findings

Implications of Findings

The findings of our study have significant theoretical and practical implications. As this is one of the foremost studies on the market reactions to dividend announcements during the pandemic, it contributes to the literature on investor reaction during crisis. The article also provides direction to companies on adopting an optimal dividend policy. The theoretical and practical implications of the study are briefly discussed below.

Theoretical Implications

The findings of our study support the preposition that when the future is uncertain, the market responds to dividend announcements. The results indicate the relevance of dividend pay-out during periods of economic policy uncertainty. In such situations, the dividends can be utilized to reassure investors about the firm’s prospects. This is in support of Gordon’s approach to dividend relevance theory according to which payment of dividend is preferred by investors, compared to capital appreciation in the future. The findings are in support of the signalling argument according to which dividend payments indicate a slowdown in future growth prospects. The results show that the market reaction to increases in dividend is more favourable when policy uncertainty is high. This finding indicates that investors place value on the dividend signal, especially in uncertain times. Dividend signalling can be used as a tool to moderate the negative effects of policy uncertainty. This finding is consistent with Gordon’s theory that dividend payment is more important that building precautionary savings during times of uncertainty. Further, the non-zero CAR shows that the market is inefficient during crisis.

Practical Implications

The findings of our study suggest dividend pay-out had a significant positive impact on the stock price. This shows that considering the uncertainty the investors were keen on receiving immediate returns rather than capital appreciation in the future. Also, the significant cumulative abnormal returns during the event window indicate the presence of fresh information. The investors might not have expected the dividend payment and the abnormal returns could be a reaction to this new information. This also shows information asymmetry during the pandemic. Though management’s fear of reducing or omitting dividends seems well-founded, the results indicate that investors prefer dividends to be paid rather than delaying payment until cash flows can be assessed with certainty.

Conclusion and Limitations

The primary objective of this study was to understand whether the price adjustment linked to the dividend announcement news during the pandemic was different from the earlier years. This empirical study employs the conventional event study methodology using abnormal returns (ARs) to examine the stock market reaction to dividend announcement. The market reaction to dividend announcement was increasingly positive during the pandemic, compared to previous years. The statistical pooled t-tests showed there was a significant relationship between the pandemic and ARs. The findings also indicate that the difference in the market reaction to dividend announcement was more prominent in services stocks than that in manufacturing. Further, the results also verify the weak-form of efficiency of Indian stock exchange. This study was limited to the distribution of dividend. Future research can examine the impact of dividend pay-out ratio on the market reaction during the pandemic.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.