Abstract

Since the last three decades, urbanization has been considered an engine of economic development and attracting foreign investment, particularly for developing countries. We explore the role of urbanization upon inward foreign direct investment (FDI) for a panel of 58 developing economies from Asia, Africa and Latin America. Empirical results reveal a complementary relationship between urbanization and FDI. Moreover, empirical findings suggest that urbanization in developing economies reaps positive benefits from FDI, provides MNCs with a safe investment climate and facilitates FDI inflows. Further, empirical results reflect the role of sociopolitical openness and infrastructure (in particular, energy and transport) in fostering FDI inflows. We suggest fostering appropriate infrastructure and sociopolitical openness will accelerate urban development and create a conducive environment for FDI inflows. Governments and policy practitioners should implement policies to mobilize foreign capital to accelerate urbanization.

Introduction

Since the 1990s, foreign capital cross-border mobility has increased substantially due to reform initiatives in emerging countries. Rapid urbanization emerged as the product of multinational capitalism from the developed to the developing world. Therefore, FDI can be a source of urban development, management and technology for developing countries. In an UN-Habitat (2018) report, the role of foreign direct investment (FDI) is emphasized for sustainable urbanization in Africa. The increasing recognition of locational advantages has led to increasing investments by multinational companies (MNCs), expanding software development and global R&D centres in countries such as India, South Africa and others. The investment opportunities help build infrastructure, R&D facilities and the work environment and help the urbanization process. The urbanization process attracts FDI inflows with endogeneity in the development process. The role of institutions and politics has also been emphasized in Papaioannou (2009)

The rising significance of FDI flows has also emphasized the role of institutions within the host countries. Bhasin and Garg (2020) analysed the impact of the institutional environment on FDI inflows to emerging market economies. Kwok and Tadesse (2006) report that investments from the Global South have weaker demonstration and managerial spillovers on the host country’s firms and institutions than investments from the Global North. Oman (2000) notices that with countries competing for FDI, there is always a risk of overbidding, and, therefore, granting subsidies may surpass the beneficial impacts of FDI inflows in recipient countries. This may lead to market distortions, adverse effects on urbanization and overall welfare losses. Furthermore, it has been emphasized by a recent report (UNCTAD, 2018) that geopolitical risks, taxes, urbanization and infrastructural developments have also been identified as the key factors in reversing the current downward trend in FDI.

The urbanization process has been affected by many factors, with FDI being one of its main driving forces. FDI implies that investors use capital in production and management while they have specific control over the operations. FDI is not only significant for meeting the shortage of funds in developing countries requirements, but also it provides advanced technology and management experience to the host. A number of early scholars argue that the urban system in developing countries, as well as the speed of urbanization and spatial structure, depend on the process of capital accumulation in industrialized countries (Friedmann, 1986; Portes & Johns, 1986).

Many policy makers have also argued that cities are or should be the key drivers of the growth performance of global countries. More importantly, cities rather than countries that bend over backwards to try to attract FDI to improve the welfare of the countries’ people. Many questions have arisen in relevance to the link we are trying to explore in this article. In particular: are urbanization processes successful because they attract significant investment, including FDI, and because they have more reliable institutions? Are cities booming because they are more conducive to international capital flows and have better financial centres than rural districts? Reliable answers to such important policy questions are crucial before one could argue that urbanization is a positive growth factor for countries.

Timberlake and Kentor (1983) document that the higher is the dependence on foreign capital, relative to the country’s economic development level, the greater the population in the city is, with the findings supporting the hypothesis that the more the stock of foreign investment in developing countries, the higher is the level of over-urbanization. In addition, Firman et al. (2007) studied Indonesia’s urbanization process, and the results highlight that FDI is mainly concentrated in the metropolitan area of Jakarta, with the urbanization and economic development processes being driven by domestic investments in the majority of Indonesian regions. Xi (2008) shows that the level of urbanization is driven by FDI flows; the accumulation of the city itself would lead to rapid development of its own after reaching a certain degree. Juan et al. (2011) built up a comprehensive index to measure the level of urbanization and examine whether FDI flows affect the level of urbanization. Their results show that FDI has a positive effect on the level of urbanization in the city with the highest level of urbanization. In contrast, the effect turns negative when the level of urbanization is low.

Moreover, studies exclusively focusing on the link between FDI and urbanization provide solid empirical evidence about their legitimate connection. More specifically, Rong-Lin (2010) uses data from 13 cities in the Jiangsu Province to document the statistical significance of the nexus between FDI and urban development across different Chinese regions, with FDI flows promoting urban development. Further, Xiu-Yu and Hong Quan (2009), through panel data methods, justify the role of FDI flows for urbanization in the Guangdong Province in the long run, albeit the FDI role turns out to be insignificant in the short run. Similar results are provided by Kai-Ming and Cun-Zhang (2010) and Fan (2011). In contrast, Ji-Zeng (2013) provides evidence of the reverse case, where urbanization tends to attract FDI flows.

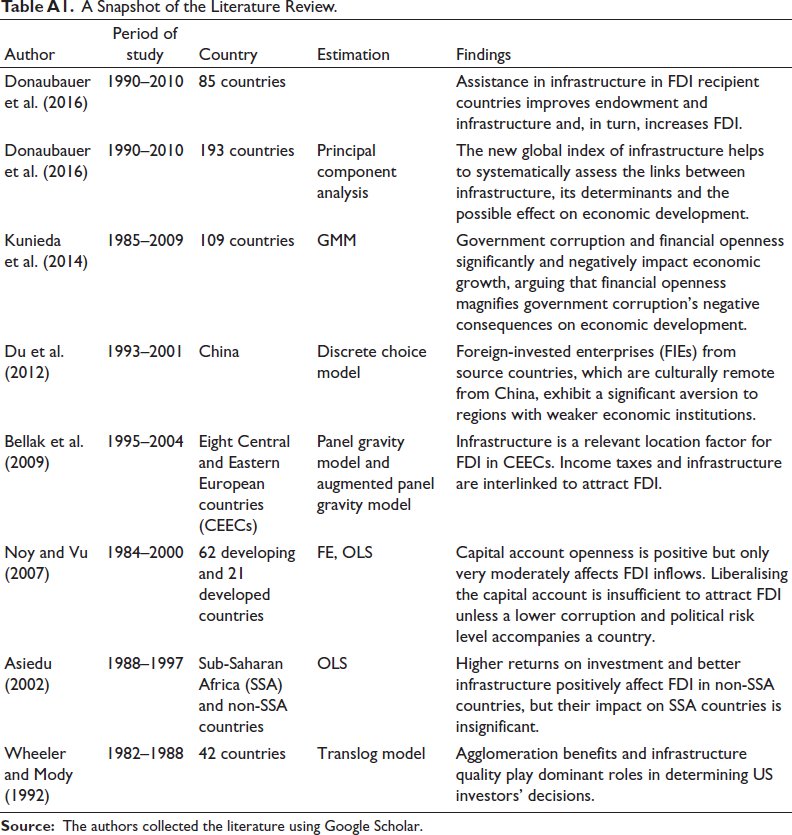

To the best of our knowledge, there is no study analysing the influence of urbanization in the presence of sociopolitical openness and infrastructure on FDI inflows for a panel of countries from Asia, Africa and Latin America. These countries are central to fostering FDI inflows in the coming decades, as emphasized by UNCTAD (2017, 2018). Urban density in these countries’ major cities is driving employment, growth and foreign investment, creating problems in sustainable development (Asian Development Bank, 2014; Cohen, 2006). Therefore, urbanization is our focus variable. In addition, we consider the role of sociopolitical openness and infrastructure in influencing the urbanization-FDI inflows relationship.

The article contributes to the existing literature in three different aspects. First, it explores the link between urbanization and infrastructure [i.e., transport, information and communication technology (ICT), energy and finance] as the driving forces of FDI inflows for our panel of countries. The selection of countries is based on their dominance in attracting foreign investment globally for the last two decades from these three continents. Second, it explores the role of sociopolitical and capital openness in influencing FDI inflows within these countries. Third, it analyses urbanization’s interactions with FDI in the presence/absence of sociopolitical openness and infrastructure.

The findings document the presence of complementarities between urbanization and FDI inflows. With an increase in urbanization, the marginal effect on FDI tends to improve, 1 indicating positive spillovers from urbanization to FDI inflows. These effects are robust for different model specifications. Furthermore, to attract FDI, most developing economies struggle to build their infrastructure in the transportation, ICT, energy and finance sectors. Therefore, we get evidence that energy and financial infrastructure have a robust and significant effect on FDI inflows across a few sets of developing countries. However, across the developing economies in Asia, Africa and Latin America, the individual infrastructure’s overall impact to attract FDIs is reasonably lower. Political openness has a robust and significant effect on FDI in countries with higher social openness, implying that political and social openness behaves in complementarity, that is, higher political and social openness can generate higher FDI inflows in socially advanced economies.

The rest of the article is organized as follows. ‘Trends in Foreign Direct Investment in Asia, Africa and Latin America’ briefly covers FDI trends for Asia, Africa and Latin America, while ‘A Brief Review of the Related Literature’ briefs the relevant literature. ‘Empirical Model, Estimations and Data’ describes the empirical model, estimation strategies and the data employed in our analysis. The empirical results are analysed in ‘Empirical Findings’. ‘Conclusion and Policy Implications’ concludes while also offering policy recommendations.

Trends in Foreign Direct Investment in Asia, Africa and Latin America

We briefly discuss the primary reasons for selecting these countries in our analysis. Over the last two decades, there has been an unprecedented surge in FDI inflows in developing countries. In particular, capital flows in infrastructure have increased significantly. Following the UN conference on trade and development (UNCTAD, 2018), Asia is the top recipient of FDI worldwide. Following the World Investment Report (2018), the total inflows to developing Asia (excluding West Asia) were $382 billion in 2013, 4% higher than in 2012. China and the ASEAN region started first, with India, South Korea and Japan following later. The total amount of FDI inflows to Africa has increased from $14.6 to $59 billion between 2002 and 2016, while the share of the total FDI inflows has declined from 8.5% to 3.4% for the same period (UNCTAD, 2006, 2017). FDI inflows to the African region are distributed unevenly, with a few Sub-Saharan African (SSA) countries attracting a significant share of total FDI inflows. Most Latin American countries have already reached a minimum level of social capacity with human capital, financial development and a certain level of institutional stability compared to Africa. In early 2000, the criticisms of FDI were common from Latin American economists. Dixon and Haslam (2016) emphasize that reliable investment protection is particularly useful in a combination of deep economic integration (via transaction cost-reducing trade agreements) in the case of Latin American countries. In addition, these countries together account for a significant source of total FDIs within the developing world. 2

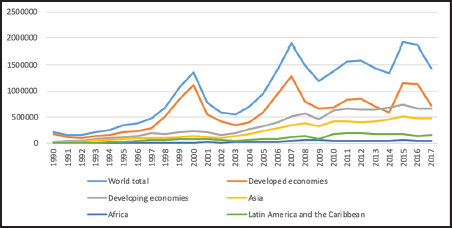

Figure 1 presents the graphical plot of the FDI inflows trend across different groups of countries. It is evident that the trend of FDI inflows has increased gradually for Asia since 2000. Similarly, the trend of FDI inflows for developing economies is shown to have been rising consistently since 1997. In contrast, the trend of FDI inflows to developed economies moved cyclically up and down after 2000. Furthermore, highlights that the shares of FDI inflows are quite lower in African and Latin American countries, vis-à-vis those of the Asian countries, indicating the heterogeneity in receiving FDIs concerning the selected three continents, that is, Asia, Africa and Latin America.

The Trend of FDI Inflows, Global and by a Group of Economies, 1990–2017 (million $).

A Brief Review of the Related Literature

Urbanization and FDI

Song et al. (2002) identify the FDI inflows as a vital economic and institutional factor in the growing urbanization of Chinese cities. It is emphasized by Anderson and Ge (2004) that FDI has been identified as a crucial factor behind Chinese cities, along with economic reforms. Recently, the Chinese government launched a ‘New Urbanisation Program’. FDI inflows and foreign trade play a more significant role in expanding urbanization and economic and market factors, as suggested by Hu and Chen (2015). In China and India, alongside other factors, the agglomeration or cluster approach has helped inward FDI. Covering 11 countries from Asia and Africa, Seto (2011) established FDIs to increase the urban population and overall urbanization. Wu and Zhao (2019) have a recent review of the urbanization-FDI nexus. In the presence of conducive economic and institutional factors, we can assume that complementarity exists between urbanization and FDI inflows.

Sociopolitical and Capital Account Openness and FDI

A growing body of literature suggests that institutional developments are vital for growth and development in the long run (Acemoglu et al., 2001). Openness in sociopolitical aspects and capital account for countries is argued to be a source of comparative advantage for economic growth (Knack & Keefer, 1995), productivity and incomes (Hall & Jones, 1999), and trade and capital flows (Busse & Hefeker, 2007). Gwenhamo and Fedderke (2013) document how institutional qualities, such as property rights, domestic risks and neighbourhood factors, influence the volume of FDI and portfolio investments in South Africa from 1960 to 2006. Alfaro et al. (2008) find that institutional developments are better in developed countries than in the developing world. These are the primary reasons that FDI flows to northern countries have skyrocketed over the past few decades, as discussed in Lane and Milesi-Ferretti (2007). Campisi and Caprioni (2017) and Shah (2017) have emphasized social and political factors in attracting FDIs in the cases of China and India, while Gammoudi and Cherif (2015) also stress the role of the capital account in attracting FDI inflows in the presence of political stability in the cases of the Middle East and North African (MENA) countries. Keeping other factors constant, two aspects of openness, such as sociopolitical and capital account openness, will attract FDI inflows.

Infrastructure and FDI

The factors responsible for FDI inflows could be transportation, energy and information technology, and financial infrastructure. Chowdhury and Mavrotas (2006) emphasize the role of infrastructure, institutions, governance, the legal framework, ICT and tax systems, among others, in Chile, Malaysia and Thailand, when attracting FDIs. Mollick et al. (2006) identify international infrastructure as a significant catalyst for FDI inflows in Mexico’s case. Sinha and Sengupta (2022) find that FDI and information and communication technology (ICT) across the Asia-pacific developing countries are positively related, indicating higher ICT expansion positively influence FDI inflows. Policies towards capable infrastructure, transportation, energy and the ICT sector are expected to impact FDI inflows positively. Donaubauer et al. (2016) establish that infrastructure aid also helps FDI inflows for developing countries. Table A1 in Appendix A summarizes the literature on FDI, urbanization and determinants factors of FDI inflows across different countries.

Empirical Model, Estimations and Data

This section details the empirical model and estimation methods with the data we use for constructing variables.

Empirical Model and Estimations

We posit an empirical model with FDI inflows of developing countries for the panel as a function of FDI inflows of previous years, urbanization, the interaction between FDI and urbanization, and a set of control variables. The empirical specification can be stated as follows:

where FDI it is net FDI inflows (as a % of GDP) for country i in the year t, and URB it denotes urbanization for country i in the year t. The interactive effect is denoted by the interaction between FDI and urbanization (FDI × URB). It follows that urbanization and FDI act as complements (Hsiao & Shen, 2003; Wu & Zhao, 2019). To consider the complementarity between urbanization and FDI, the model in (1) explicitly considers the interaction between them. Xit represents a matrix of control variables for each country, γi is the vector for time-invariant controls (unobservable country-specific effect), θt represents the vector of time-specific effect and ɛit denotes the error term.

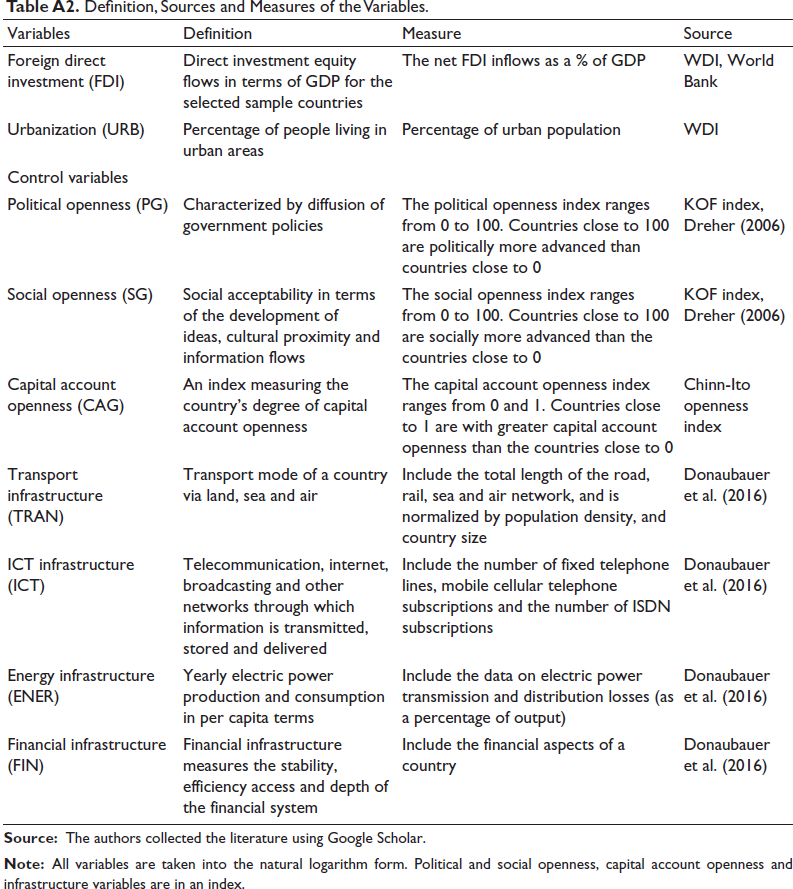

We consider the lagged FDI to check the robustness related to endogeneity. It satisfies the moment condition while generating instruments and the instruments’ validity in the case of GMM estimators. 3 Our benchmark controls include political, social and capital account openness and infrastructure (transportation, ICT, energy and finance). Political openness is characterized by a diffusion of government policies (Keohane & Nye, 2000). We expect that political openness extends to implementing government policies and creating a flexible environment for foreign capital inflows. Social openness can be defined as the spread of ideas, information, images and people (Dreher, 2006; Keohane & Nye, 2000). Increased political and social openness could facilitate FDI-induced growth in host economies. Openness on capital account enables the mobility of capital. Therefore, our panel considers capital account openness a controlling factor for FDI inflows. 4 Following Donaubauer et al. (2016), we incorporate four sub-categories of infrastructure, namely transportation (via air, land and sea), information and communication technology (ICT), energy and finance, into our matrix of control variables in Equation (1). A sound transportation infrastructure attracts FDI inflows into a region and promotes urbanization and economic development.

In Equation (1), we are interested in the sign of the coefficients of β1, and β2. We are interested in examining the marginal impact of FDI at different levels of urbanization. Past year FDI may substantially influence the current year FDI inflows. Therefore, the influence of previous FDI inflows on the current FDI may be induced by the effect of urbanization:

In Equation (2), depending on the sign and magnitude of β1 and β2 and the extent of urbanization will be either >0 or <0. 5 The estimates will determine whether the previous levels of FDI inflows affect the current level of FDI at different stages of urbanization.

We employ the dynamic panel Generalized Method of Moments (GMM) estimators in empirical estimations. The OLS cannot solve the issues of panel data challenges such as endogeneity and reverse causality. The problems of omitted variables cannot be ruled out in the case of panel cross-country regression. However, under the assumption of valid instruments, that is, when the instruments are not correlated to the error terms, the omitted variables will not lead to inconsistent slope estimates in the case of GMM estimators (Wooldridge, 2002). Furthermore, there could be the possibility of reverse causality between FDI and urbanization. The reciprocal causation between urbanization, FDI and economic growth in developing economies is examined (Cheng & Duan, 2010; Li & Liu, 2005; Zhang, 2002). Reverse causality between FDI and urbanization can be justified by the fact that FDI inflows bring in capital, technology, production know-how, modern management, marketing skills and information, competition and so on; as a result, it is expected that FDI will not only contribute to the economic growth through higher capital formation, job creation, technology transfers and knowledge spillovers, but will also affect the urbanization process through (1) facilitating economic structural changes by contributing to the expansion of the secondary and tertiary sectors, (2) absorbing surplus rural labour by creating employment in the secondary and tertiary sectors, and (3) encouraging rural people to migrate to cities by offering higher wages and thus increasing income in urban areas (Chen, 2011; Chubarov & Brooker, 2013). This has been noticed in major parts of Asia, Africa and Latin American cities, where urbanization and foreign investment catalyze the development process. Therefore, the primary advantage of employing GMM estimates will be the immunization to the endogeneity bias that arises from reverse causality.

Both difference and system-GMM estimators address the challenges within panel data, such as the presence of fixed effects, small ‘T’ (fewer time-periods) and large ‘N’ (many countries) panels (i.e., N > T), panels with independent variables that are not strictly exogenous, and the presence of heteroscedasticity and autocorrelation within countries (Roodman, 2009). The system-GMM estimator by Blundell and Bond (1998) includes additional moment conditions to obtain a system of two equations – one in difference and the other in the level. Additional moment conditions result in reduced and greater precision over difference-GMM estimates (Cooray et al., 2017). Therefore, we present system-GMM-based dynamic panel estimators for our benchmark results, further to empirically examine the instruments’ validity. The selected instruments are supposed to be uncorrelated to the error terms. We report the p value on the Sargan test of the over-identifying restriction. The Sargan test is based on the hypothesis that the instruments are uncorrelated with the error terms. Further, the Sargan test is sensitive to the model specification, and an insignificant p value of the test is often treated as the model is correctly specified and the instruments are valid.

Data

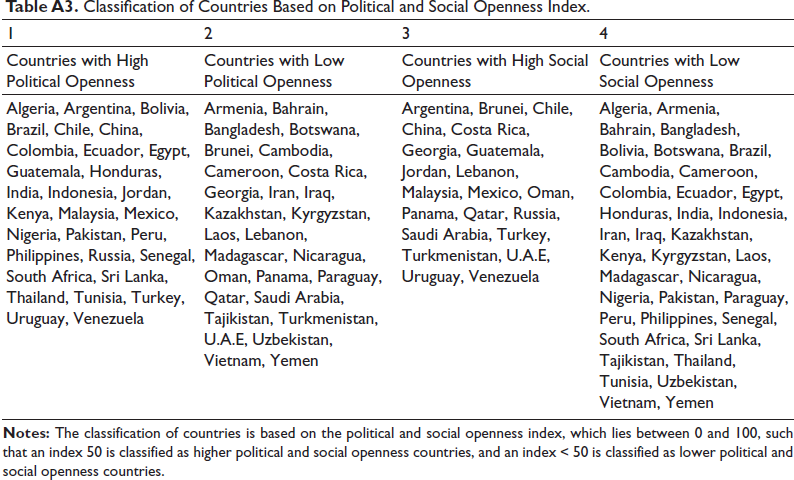

We selected an unbalanced panel of 58 countries from Asia, Africa and Latin America between 1990 and 2013. 6 We classify the 58 developing economies based on their political and social openness index. Moreover, based on the sociopolitical openness index, we classify the full sample into four sub-panels: high and low political openness countries and high and low social openness countries (see Table A3, Appendix). Following the standard literature (Asiedu, 2002; Hsiao & Shen, 2003), we measure the dependent variable as the ratio of net FDI inflows to GDP. Foreign direct investment is calculated as direct investment equity flows to destination countries over a year (in billion $).

For independent variables, urbanization is measured as the percentage of the urban population (Hsiao & Shen, 2003), that is, the total number of people living in urban areas as a percentage of the total population. 7 The data are extracted from the World Development Indicators (WDI), an online database offered by the World Bank. For control variables, political openness is characterized by the diffusion of government policies, which indicates the degree of political cooperation. Social openness is expressed as the spread of ideas, cultural proximity and information flow, as Dreher (2006) considered. Following the literature (Gygli et al., 2019; Mukherjee & Dutta, 2018; Potrflake, 2015), political and social openness indices are obtained from the KOF-index of openness. 8 We expect the index for both political and social openness to positively impact FDI inflows. The data on capital account openness are sourced from the standard Chinn-Ito openness index, a popular index widely used in the literature (Behera, 2015a, 2015b, 2016, 2017; Schindler, 2009). A higher capital account openness allows a country to attract more massive FDI inflows and a positive sign is expected. 9 Table A2 in Appendix A details the measures and the sources of variables under consideration.

Following Donaubauer et al. (2016), we consider four sub-categories for the measure of infrastructure, namely transportation, ICT, energy and financial infrastructure. Transportation infrastructure consists of air, land and sea routes. The ICT infrastructure encompasses telecommunications, the internet, broadcasting and other networks through which information is transmitted, stored and delivered. The energy infrastructure includes electricity production and consumption, while the financial infrastructure includes the country’s financial aspects. 10 The data of these four sub-indices of infrastructure are borrowed from Donaubauer et al. (2016).

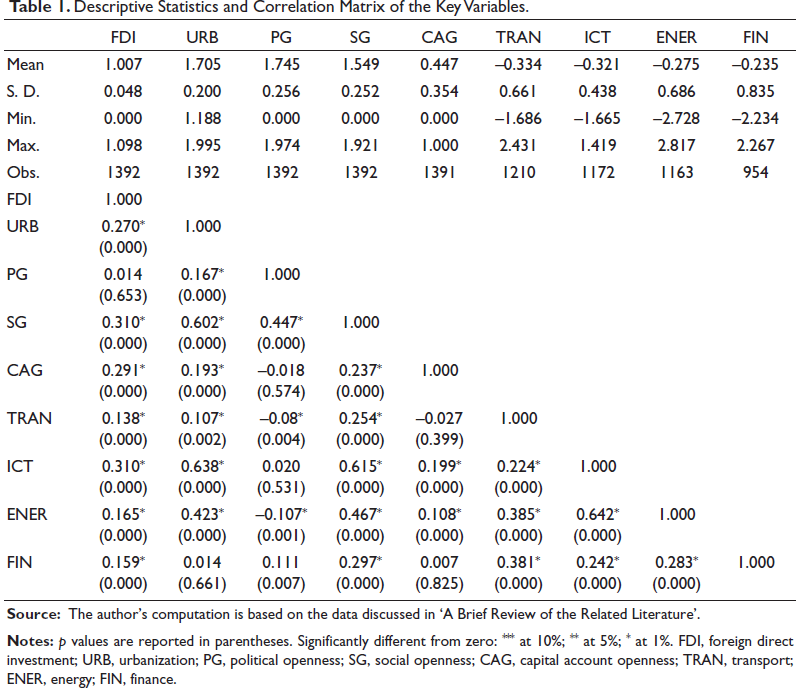

Table 1 reports summary statistics and a correlation matrix of the variables. The results suggest that FDI positively correlates to urbanization, social openness, capital account openness and all four infrastructure sub-indices. The correlation results reflect that higher capital account openness attracts higher FDI inflows. FDI inflows enhance the economic growth of FDI-recipient countries. 11 Although we find a positive correlation between FDI and all sub-indices of infrastructures, infrastructure impacts on FDI inflows are substantially lower.

Descriptive Statistics and Correlation Matrix of the Key Variables.

FDI, foreign direct investment; URB, urbanization; PG, political openness; SG, social openness; CAG, capital account openness; TRAN, transport; ENER, energy; FIN, finance.

Empirical Findings

Panel Unit Root Test with Cross-sectional Dependence

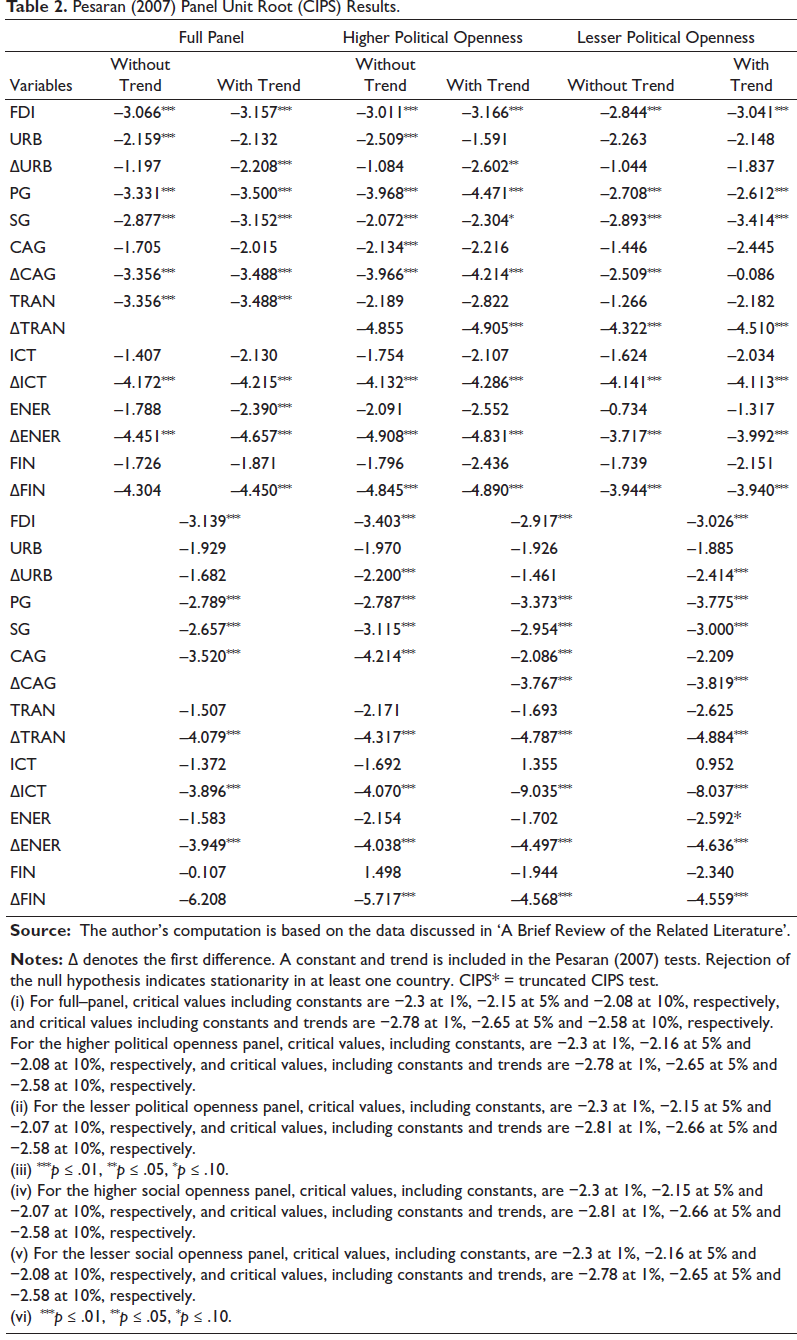

Before estimation, Pesaran’s (2007) second-generation panel unit root test has been used to examine the presence of cross-section dependence and to determine the degree of integration of the variables under consideration. The Pesaran (2007) panel unit root test is based on the average individual cross-sectional ADF statistics (CADF).12 The test statistic is known as a cross-sectional augmented Im, Pesaran and Shin (2003) test (CIPS):

where ti(N, T) denotes the t-statistic based on the OLS estimate for βi in the following equation:

The truncated version of the CIPS test is defined as follows:

where

The truncation points K1 and K2 are selected considering a normal approximation. ti(N, T) Both statistics have the null hypothesis of a unit root. The results reported in Table 2 indicate that most variables have unit roots in the entire panel (levels) and across sub-panels of countries. Therefore, the first differences are recommended to attain the process of stationary of the variables. Consequently, it follows that the variables are characterized as integrated of order one.

Pesaran (2007) Panel Unit Root (CIPS) Results.

(i) For full–panel, critical values including constants are −2.3 at 1%, −2.15 at 5% and −2.08 at 10%, respectively, and critical values including constants and trends are −2.78 at 1%, −2.65 at 5% and −2.58 at 10%, respectively. For the higher political openness panel, critical values, including constants, are −2.3 at 1%, −2.16 at 5% and −2.08 at 10%, respectively, and critical values, including constants and trends are −2.78 at 1%, −2.65 at 5% and −2.58 at 10%, respectively.

(ii) For the lesser political openness panel, critical values, including constants, are −2.3 at 1%, −2.15 at 5% and −2.07 at 10%, respectively, and critical values, including constants and trends are −2.81 at 1%, −2.66 at 5% and −2.58 at 10%, respectively.

(iii) ***p ≤ .01, **p ≤ .05, *p ≤ .10.

(iv) For the higher social openness panel, critical values, including constants, are −2.3 at 1%, −2.15 at 5% and −2.07 at 10%, respectively, and critical values, including constants and trends, are −2.81 at 1%, −2.66 at 5% and −2.58 at 10%, respectively.

(v) For the lesser social openness panel, critical values, including constants, are −2.3 at 1%, −2.16 at 5% and −2.08 at 10%, respectively, and critical values, including constants and trends, are −2.78 at 1%, −2.65 at 5% and −2.58 at 10%, respectively. (vi) ***p ≤ .01, **p ≤ .05, *p ≤ .10.

Robustness Checks: The GMM Estimates to Incorporate Endogeneity Issues

We present the results using the system-GMM estimation to consider the endogeneity between urbanization and FDI inflow. The standard OLS leads to inconsistent slope estimates in the case of cross-country panel data. To address endogeneity and reverse causality, we estimate the empirical model using GMM techniques and lagged values of the dependent variable as instruments and other explanatory variables in explaining FDI and run over-identifying restriction tests to judge the validity of the instruments.

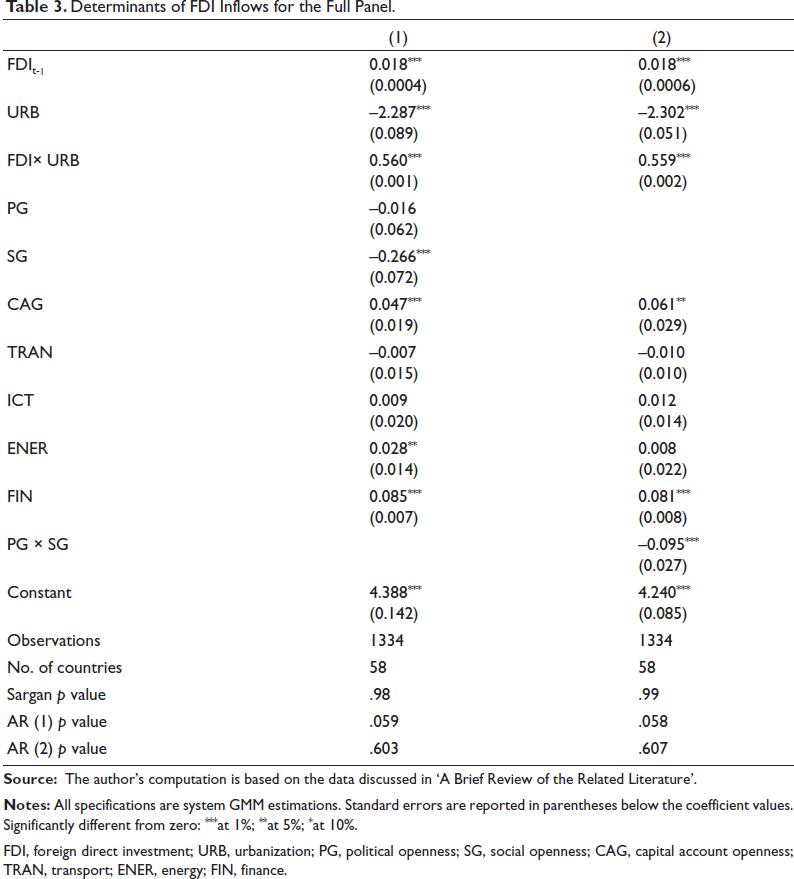

Table 3 presents the findings from the system-GMM estimations. The system-GMM estimation results are in greater precision. However, the estimates might yield bias because too many instruments are generated relative to the difference-GMM estimates. Consequently, we determine our results with the difference-GMM estimators but report only the system-GMM estimates’ results to conserve space. 13 The findings described in columns (1) indicate the absence of the individual role of sociopolitical globalization. However, the interaction effect of sociopolitical globalization is analysed in column (2). The results suggest that urbanization and interaction with FDI, capital account openness, energy, and financial infrastructure significantly affect FDI inflows. The estimated coefficient of social and political globalization interaction is negative and significantly different from zero. As most of the countries in our sample are emerging economies and sociopolitical instability, these two dimensions of openness may interact. Therefore, this reflects that their joint influence on net FDI inflows seems negative. Further, in both specifications, the urbanization coefficients are negative and statistically significant, suggesting a negative impact on FDI inflows to developing economies in Asia, Africa and Latin America. This result is not surprising. A plausible explanation is that FDI inflows to some countries in the panel of 58 developing economies could be low because of political instability, civil war and land dispute problems. Sociopolitical risk factors and the negative consequences of the energy sector (which causes air pollution), the overall impact of urbanization on FDI inflows turns out to be negative and significant. This finding is consistent with those by Asiedu (2002).

Determinants of FDI Inflows for the Full Panel.

FDI, foreign direct investment; URB, urbanization; PG, political openness; SG, social openness; CAG, capital account openness; TRAN, transport; ENER, energy; FIN, finance.

The coefficients of urbanization and FDI interaction are positive and significantly different from zero. Therefore, urbanization and FDI inflows are complementary concerning their combined effect on net FDI inflows. This suggests that higher urbanization will produce higher net FDI inflows (Table 3). Turning to our control variables, the political and social openness variables are crucial for determining international capital mobility in developing countries. In the full panel of 58 emerging economies, the estimates illustrate that the coefficient of social openness is negative and significantly different from zero, as shown in Table 3, implying that social openness cannot substantially affect FDI inflows relevant to the Global South region. This result is unsurprising when considering the full panel of countries with low and high political and social openness. It could be possible that a few sets of countries pull down the overall positive impact of social openness upon FDIs, which in turn leads to negative spillovers for these FDI inflows. More specifically, the results suggest that a 1 standard deviation decrease in social openness increases FDI inflows by about 0.067 standard deviations across the full panel of sample countries (Table 3); alternatively, a 1 standard deviation reduction in social openness increases FDI inflows up to 6.7% in the full panel of sample countries.

The sub-indices of infrastructure in columns (1) and (2) are statistically significant. The coefficients of the energy and financial infrastructure sub-indices are significant with the expected signs, indicating that energy and finance infrastructure increase FDI inflows in these emerging economies. In the entire sample of 58 developing economies, a 1-standard-deviation increase in energy infrastructure raised the FDI to 2%. Likewise, a 1-standard-deviation increase in financial infrastructure will increase FDI inflows by more than seven percentage points. Therefore, the results suggest that improving the energy and financial infrastructure would increase FDI inflows significantly. Furthermore, our panel includes countries mostly from low-income and middle-income developing economies, where such countries’ energy and financial infrastructure may not be fully developed. Therefore, the influence of the sub-indices of energy and financial infrastructure upon FDI inflows does not reach a very considerable extent. Nor can we establish transportation and ICT infrastructure to be significant enough to attract FDI inflows. From the perspective of ICT infrastructure, it is highly evident that improvement in ICT infrastructure in the region remains unequal and cannot attract uniform FDI inflows across these economies. Our empirical results in this direction demonstrate an insignificant association between ICT infrastructure and FDI inflows. Our findings in this direction are different from a few of the earlier studies (Samir & Mefteh, 2020; Sinha & Sengupta, 2022).

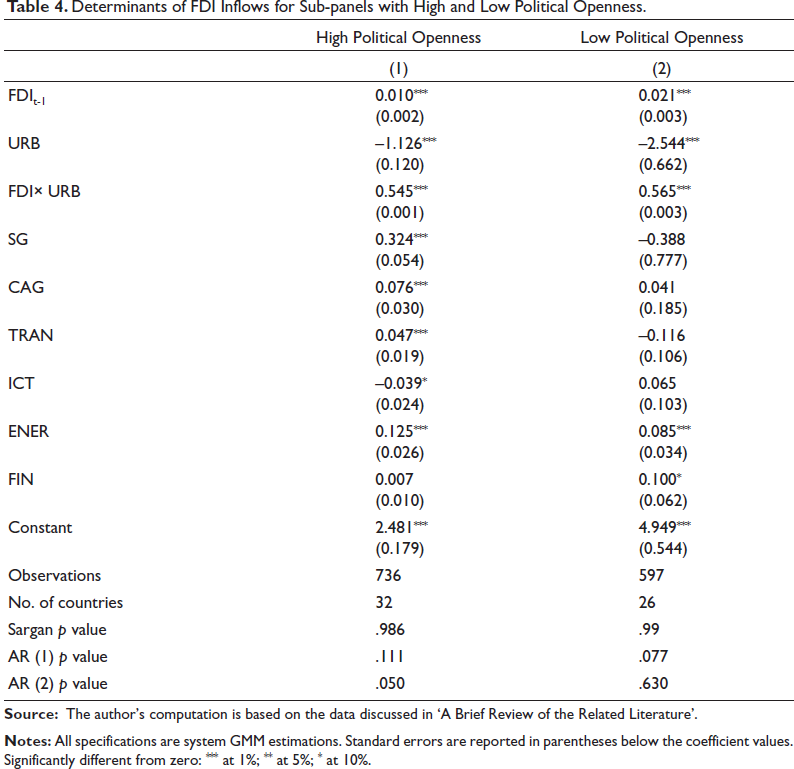

Urbanization and FDI Inflows in the Presence of High or Low Political Openness

To examine the determinants of FDI based on political openness, we classify the full panel of 58 economies into two sub-groups. Our estimation across different sub-groups could provide a rigorous effect of the political openness role on FDI to the developing economies. The first group comprises countries with a political openness index greater than or equal to 50. The second group comprises countries with a political openness index of less than 50 (Appendix A presents a detailed classification of these countries). Moreover, we drop the political openness variable when we run separate regression on high and low-political openness sub-panels to achieve more robust findings and get precise empirical consequences based on the political openness index.

The results of the sub-panels of countries with high and low political openness are reported in Table 4. We find that the interaction coefficients between urbanization and FDI inflows are non-negative across all specifications, suggesting that both factors complement their collective impact on FDI inflows (Table 4). 14 Having noted this, urbanization in isolation negatively affects FDI inflows and the business investment climate. This corroborates with Hsiao and Shen’s (2003) and Chen and Wu’s (2017) research. Developing countries may adopt unsystematic urbanization to attract FDI inflows, which negatively affects the investment climate. Unsystematic urbanization harms environmental degradation and carbon dioxide emissions. Dash et al. (2020) and Behera and Dash (2017) find that unsystematic urbanization has led to severe environmental degradation and air pollution across developing economies. Therefore, unsystematic urbanization does not inevitably lead to FDI inflows.

Determinants of FDI Inflows for Sub-panels with High and Low Political Openness.

Capital account openness appears to significantly affect FDI, implying that the higher openness of capital accounts can generate higher FDIs in developing economies. Furthermore, across different sub-panels, we find that the estimated coefficients of FDI at the first lag are positive and significantly different from zero, suggesting that last year’s FDIs have a robust and significant effect on current FDIs. We also find a negative coefficient of social openness variables in the case of lower political openness countries. This suggests that the estimated coefficient of social openness does not significantly affect FDIs in lower political openness countries (see Table 4). However, the coefficient of social openness is found to be positive and significantly different from zero only in the case of countries with higher political openness. Therefore, we infer that social openness increases FDI only in the case of higher political openness countries.

Furthermore, the empirical results document that social and political openness complement each other, while social openness (acceptability in developing ideas, cultural proximity and information flows) facilitates FDI inflows. Regarding the economic significance of the findings, the estimates are substantially important. For example, a 1-standard-deviation rise in social openness leads to a 7.58% increase in FDI inflows in the case of higher political openness countries. Empirical results exhibit that transport and energy infrastructure significantly affect FDI in the higher political openness countries. Quantitatively, the results suggest that a 1 standard deviation increase in the transportation infrastructure increases FDI inflows by about 2.9% across the countries with higher political openness. Similarly, finance infrastructure significantly raises the FDI inflows across the lesser politically open countries. The plausible reason behind this is the development of robust financial infrastructure, open FDI policies and relaxed macroeconomic norms to attract more foreign capital. Our finding in this direction remains different from a few earlier studies (Nguyen & Lee, 2021; Seyoum & Ramirez, 2019), where these studies claim the significant and moderate roles of government stability and higher political openness in terms of shaping the FDI inflows to the economies.

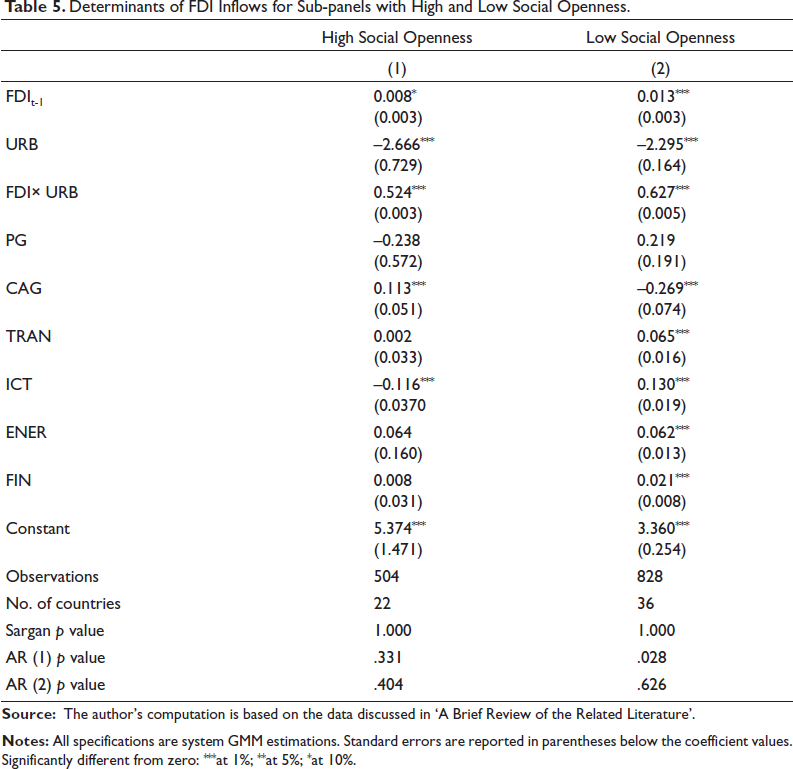

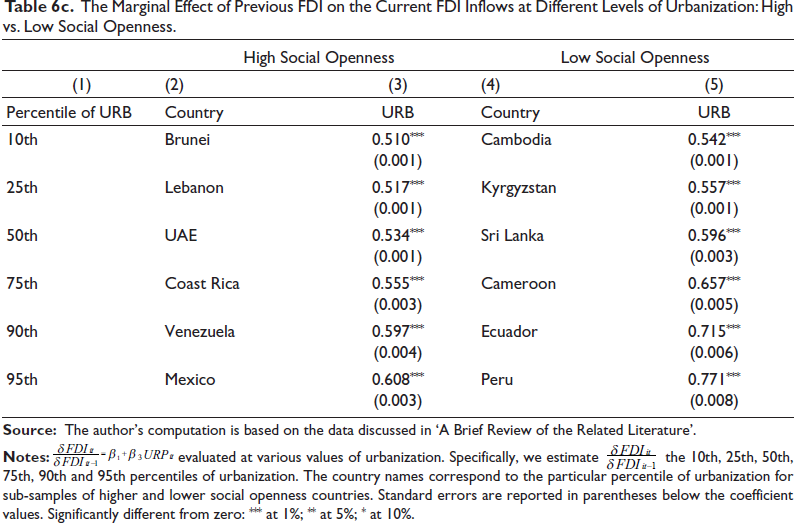

Urbanization and FDI Inflows in the Presence of High or Low Social Openness

To discuss our empirical findings based on social openness, we classify the full panel of 58 economies into two sub-panels: socially advanced and less advanced economies. 15 Using the sub-panels based on the social openness index, we explore whether social openness in emerging economies substantially affects FDI inflows. Further, we divide the full sample based on the social openness index. Therefore, in order to get precise empirical consequences based on the social openness index, we drop the social openness variable in the case of the low and high social openness sub-samples regression. The results reported in Table 5 suggest that the coefficient of the interaction term, FDI×URB, is positive and significantly different from zero in all sub-samples. Hence, FDI and urbanization are complementary concerning their impact on net FDI inflows. Likewise, urbanization does not appear to have a robust and positive effect on FDI inflows. Instead, it seems to decelerate FDI inflows in the higher and lower social openness countries.

Determinants of FDI Inflows for Sub-panels with High and Low Social Openness.

Next, we explore whether infrastructure positively influences FDI inflows across the developing economies in Asia, Africa and Latin America. It seems that different infrastructure components do not have a robust and significant effect on FDI inflows. More specifically, in the higher social openness countries, infrastructure, such as ICT, does not appear to have a positive and significant impact on FDI (Table 5), suggesting that ICT infrastructure is not efficient in attracting FDI inflows to the emerging economies in Asia, Africa and Latin America. Moreover, the inefficiency in ICT infrastructure suggests that developing countries need to rapidly enhance their telecommunication and internet services to attract FDIs. The empirical results illustrate that transportation infrastructure in lower social openness countries significantly positively affects FDI inflows. Quantitatively, the results suggest that a 1 standard deviation increase in the transportation infrastructure increases FDI inflows by about 0.038 standard deviations across the lower social openness countries. Further, energy infrastructure appears to raise the FDI inflows in the lesser social openness countries. Similarly, finance infrastructure seems to have a robust and significant effect on FDI inflows in countries with lesser social openness. Moreover, the findings report that across higher social openness countries, finance infrastructure does not appear to significantly affect FDIs, indicating that developing economies with a flawed financial system cannot boost their FDI inflows. In fact, the results suggest that insignificant ICT networks with deficient financial systems usually discourage MNCs from transplanting their exporting units in developing economies. Therefore, investments in the finance and ICT sectors are necessary for infrastructural improvements to attract FDIs.

Next, we may postulate that capital account openness does not affect FDI inflows. In contrast, other country-specific macroeconomic factors would play the deciding role in FDI inflows to developing countries. The results reported in Table 5 suggest that capital account openness is not substantially promoting FDI in developing economies with lower social openness. A plausible explanation for the subdued response of FDIs to capital account openness is that foreign investors do not perceive reforms as credible because the government’s capital account openness is perceived as highly transitory. Therefore, the economic reforms to open the capital account are ineffective here. The incredible and unreliable reform policies open the capital account that discourages FDIs in the lower social openness countries. Notwithstanding, empirical findings suggest that everything else being equal, capital account openness is significantly effective in promoting FDIs in higher social openness countries, indicating that for these countries, the response of FDIs to capital account openness is well perceived by foreign investors, as they consider the reforms by these groups of countries to be credible.

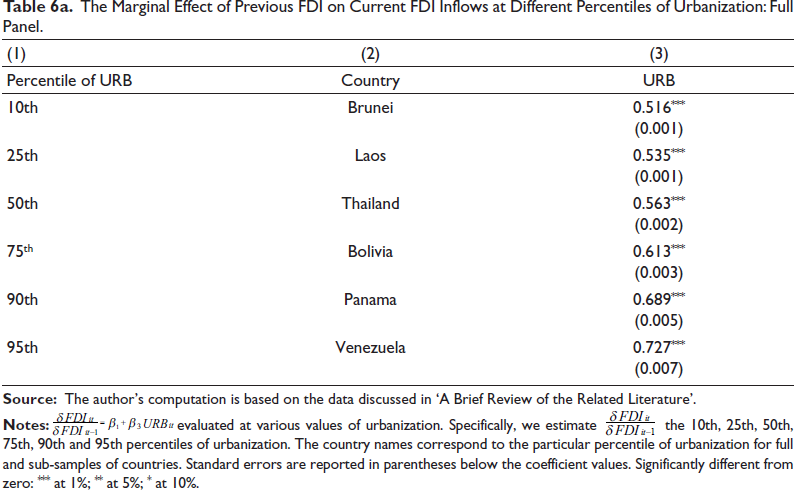

Finally, we explore whether the previous level of FDI inflows affects the current level of FDIs at different stages of urbanization. To get the marginal effect of FDI at a different level of urbanization, we further estimate the equation’s specified empirical model (2). Moreover, the marginal effects reflect that the impact of urbanization on FDI inflows could be either positive or negative. We report these results in Table 6a. Different percentiles of urbanization can determine the effect on net FDI inflows. Following Asiedu et al. (2009) and Cooray et al. (2017), we estimate the marginal impact at the tenth, twenty-fifth, fiftieth, seventy-fifth, ninetieth and ninety-fifth percentiles of urbanization. To give a detailed perspective of the effects estimated, we provide country names corresponding to urbanization’s particular percentiles.

The Marginal Effect of Previous FDI on Current FDI Inflows at Different Percentiles of Urbanization: Full Panel.

We find that is non-negative and significant at any percentile of urbanization, as shown in Table 6a. In sum, this suggests that the previous year’s FDI and urbanization are key determinants of current FDI inflows into emerging economies. The magnitude of marginal impact varies over the different percentiles of urbanization. In terms of economic significance, the relevance of urbanization for FDI inflows is substantial. For instance, at the ninety-fifth percentile of urbanization, a 1-standard-deviation rise in FDI t-3 for Venezuela leads to a 0.004 percentage point increase in FDI inflows. However, the impact is less for Venezuela, as it substantially increases FDI inflows to other emerging economies. For instance, in the case of Panama, a 1-standard deviation rise in FDI t-1 leads to a 0.014 percentage point increase in FDI inflows, suggesting that past FDIs could provide certain indications for the current mobility of FDI. As MNCs wish to explore new emerging markets, they expect to transplant their exporting units or subsidiary firms in the host country. Therefore, the empirical inference could provide a particular indication to the MNCs while exploring new emerging markets.

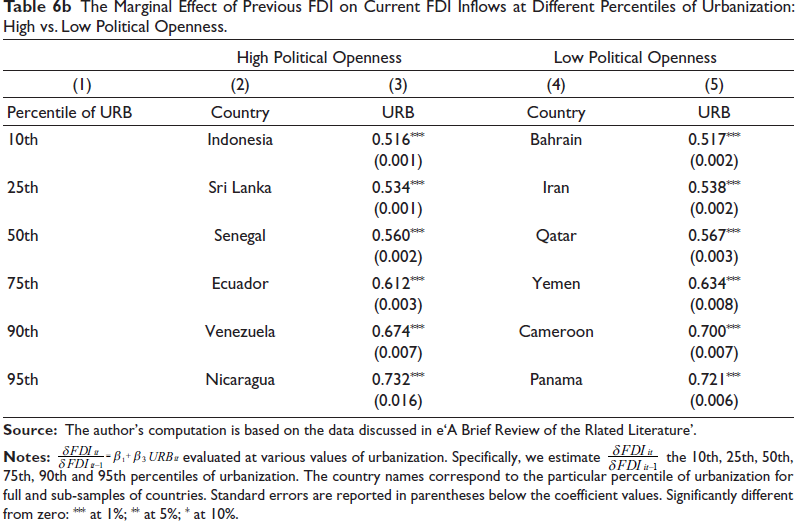

In Table 6b, we closely examine the marginal effect over the sub-panels of high and low political openness at different percentiles of urbanization. The coefficients are positive and significant. As the percentiles of urbanization increase, the magnitude of the marginal effect increases, suggesting that urbanization and FDI inflows behave in a complementarity fashion. Therefore, higher urbanization leads to higher FDI inflows to emerging economies. These empirical results indicate that to boost FDI inflows, developing economies must systematically enhance urbanization and their investment climate. From the sub-panels of higher and lower social openness countries, we find that the marginal effect coefficients are positive at the different percentiles of urbanization (Table 6c), suggesting that the marginal impact of FDI t-1 and urbanization play a crucial role for the MNCs to decide whether to invest in developing economies. We conclude that urbanization in developing economies helps reap benefits from FDI inflows, provides MNCs with a safe investment climate and increases FDI inflows.

The Marginal Effect of Previous FDI on Current FDI Inflows at Different Percentiles of Urbanization: High vs. Low Political Openness.

The Marginal Effect of Previous FDI on the Current FDI Inflows at Different Levels of Urbanization: High vs. Low Social Openness.

Conclusion and Policy Implications

This article explored the role of FDI inflows in the urbanization process. The results established that complementarities exist between urbanization and FDI inflows, implying that greater urbanization levels facilitate FDI inflows. The findings survived certain model specifications.

The results imply the presence of a positive environment for urbanization and foreign investments. With the growth of the urban sector, people can interact and participate in economic activities. Governments and policy practitioners need to invest more resources in improving the sociopolitical environment in cities and utilize aid in infrastructure (particularly in the ICT and finance sectors) to promote further urban development and accelerate FDI inflows simultaneously in these countries. The urbanization process should also allow more foreign capital participation (FDI) in urban infrastructure construction and real estate activities. To this end, policymakers should establish a sustainable funding mechanism while promoting reforms of financial institutions.

Moreover, they need to encourage social capital to participate in urban utilities investment operations. To attract more foreign capital to participate in urban public infrastructure while minimizing or even deleting any institutional obstacles, such as land circulation and social security, that prevent the full exploitation of FDI benefits to elevate the quality of urbanization. Such activities are expected to optimize and improve urban infrastructure and service functions, which will enhance the city’s capacity to attract further FDI inflows, attract non-agricultural production factors to urban agglomeration and consistently improve FDI inflows. Finally, it is substantially and equally important for policymakers to encourage a planned urbanization process that enables resources to be managed in a sustainable way, which requires an efficient coordination process between national and municipal governments to redesign and develop FDI-friendly infrastructures by increasing green urban areas, which contribute to carbon sequestration. In that sense, policymakers should perfect the needed infrastructure construction, strengthen the cultivation of cultural identity and transfer the competitive advantage of industry agglomeration into urban competitiveness to better attract foreign investments.

A potential limitation of the article is that the empirical findings are not supported by the presence of panel causality tests. Given certain size constraints, the authors plan to remedy this in an upcoming article. Further, the authors plan to explore the direct link between international capital flows and urbanization through nonlinear panel methods that could provide more explicit results in the case that urbanization gets important after a certain threshold point.

Appendix

A Snapshot of the Literature Review.

Definition, Sources and Measures of the Variables.

Classification of Countries Based on Political and Social Openness Index.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of this journal for their suggestions to improve the quality of the manuscript. Usual disclaimer applies.

Conflict of Interest

The authors declared no potential conflicts of interest concerning this article’s research, authorship and/or publication.

Funding

The authors received no financial support for this project, authorship and/or publication.