Abstract

This article investigates the impact of capital requirements and market competition on the stability of financial institutions in the Middle East and North African (MENA) region. We test the hypothesis that capital requirements significantly affect the risk behaviour of both Islamic and conventional banks in the MENA region. We also investigate the moderating effect of market power and concentration on the relationship between capital regulation and bank risk. We find that capital ratio has a strong positive impact on conventional banks’ credit risk, whereas this effect is insignificant in the sample of Islamic banks. Our analysis indicates that, for the conventional banking sector, the increase in the capitalization level is negatively linked to bank credit risk only when banks’ level of market power is high. Regarding the Islamic banks’ behaviour, we find that the relationship between capital and credit risk is weakly moderated by banking competition. This means that Islamic banks are less sensitive to the market’s competitive conditions in the MENA countries, as they still apply their theoretical models, based on prohibition of interest. Our findings inform regulatory authorities concerned with improving the banking sector’s financial stability in the MENA region to strengthen their policies and force banks to better align with regulatory capital requirements during the COVID-19 pandemic.

Introduction

This study investigates the impact of capital regulation and market competition on bank’s risk-taking in the countries that belong to the Middle East and North African (MENA) region. As a result of the financial crisis in 2007–2008, many global initiatives have been developed to limit the likelihood of future banking collapses. Significant efforts have been dedicated to the need for good governance and tighter regulations (Mondher & Lamia, 2016). As a result, many countries’ regulatory authorities have shifted their focus on the development of new rules associated with stricter banking regulations and the establishment of a system of high-quality governance. In this context, capital requirements are considered as an essential element of prudential regulation in the light of the Basel Accords that may enforce banks to decrease their risk-taking level.

The study of the relationship among regulation, bank governance and risk-taking has occupied a particular interest among researchers, focusing on capital requirements and their impact on bank risk and performance (Bitar et al., 2016). The existing empirical literature investigates the effect of regulation mostly in global- or Europe-specific aspect (Altunbas et al., 2007; Demirgüç-Kunt et al., 2013). However, more recent research offers additional insights into banks in other regions and/or countries, including banks in the MENA region (Bitar et al., 2016; Naceur & Omran, 2011). For example, Bitar et al. (2016) examine the impact of various regulatory capital ratios on bank performance, using a sample of 168 banks in 17 MENA countries, and find that capital ratios are positively associated with loan loss reserve ratios, bank efficiency and profitability. Their findings support the recommendations of the Basel Committee to hold higher capital ratios. Likewise, Ghanem (2017) finds that the implementation of Basel II capital requirements has a positive effect on banks; credit risk in Egypt, Jordan, Lebanon, Morocco and Tunisia. Maghyereh and Awartani (2014) investigate the effect of bank regulation on bank distress in the Gulf Cooperation Council (GCC) countries throughout 2000–2009 and find no significant relationship between capital stringency and the likelihood of bank distress, whereas the official supervisory power has a negative impact on bank probability of default. Thus, the results are mixed.

Another strand of empirical literature investigates the impact of market competition on risk-taking behaviour of banks. There are two opposing theories in the literature regarding the impact of competition on bank behaviour (Louati et al., 2015). The first theory shows that a competitive market may increase the risk-taking behaviour of banks in order to maintain their previous level of profit (Allen & Gale, 2004). This risky behaviour can be observed either through the increase in credit risk of the loan portfolio or the fall in the capital buffer level, or simultaneously. Such behaviour can lead to an increased level of non-performing loans (NPLs) and a greater probability of bank default. However, the second theory postulates that restricted competition should encourage banks to protect their high ‘franchise value’ by pursuing safety policies that contribute to the whole banking system’s stability. Therefore, according to the franchise value paradigm, 1 banks limit their risk when they have market power in lending (Louati et al., 2015). As the underlying source of franchise value is assumed to be the bank’s market power, reduced competition among banks has been considered important to promote banking stability. Conversely, an increase in competition erodes their quasi-monopoly rents (Jimenez et al., 2013). This theory has been theoretically and empirically supported in the banking literature.

The role of capital requirements for banking systems’ financial stability during the COVID-19 pandemic has become of significant importance for researchers. Earlier research (Benes & Kumhof, 2015) claims that regulatory capital requirements act as a safeguard of risk and improve banks’ performance and efficiency. In the same context, Karim et al. (2014), Moudud-Ul-Huq (2019a) and Zheng et al. (2017b) find that capital requirements significantly impact lending activities of banks and consider capital as a shock absorber of credit risk. Other similar studies that report a negative relationship between risk and capital also indicate capital as an effective tool for managing risk (see, e.g., Agoraki et al., 2011; Agusman et al., 2014; Chang & Chen, 2016; Deelchand & Padgett, 2010; Guidara et al., 2013; Maji & De, 2015, Nguyen & Nghiem, 2015; Zhang et al., 2008). Thus, the regulatory pressure of implementing Basel III capital requirements and the existing literature supports the notion that capital regulation tends to improve bank efficiency and enhance bank protection against risk. Among the very few studies focusing on the COVID-19 pandemic, Aldasoro et al. (2020) find that banks underperformed significantly relative to other sectors, and credit default swap (CDS) spreads increased the most for those banks that entered the crisis with the highest level of credit risk. During the follow-up stabilization brought about by different policy initiatives, banks with higher profitability and healthier balance sheets have performed better. Moreover, the CDS spreads of the riskiest banks continue to increase even during the stabilization phase. Recently, Li et al. (2021) investigated the effect of the COVID-19 pandemic on bank performance and risk related to the use of non-interest revenue sources. Their findings suggest that non-interest revenue sources are positively related to bank performance but inversely related to risk. These results are consistent with a beneficial portfolio diversification approach during the pandemic for banks expanding beyond traditional lending sources of income. 2

A number of factors make the MENA region a compelling laboratory to investigate this issue. First, the MENA region has faced numerous changes in the past decade, such as opening up their markets to foreign competition, expanding the private sector and increasing bank lending. Thus, there is a need to strengthen banking supervision and regulation by conforming to international Basel standards and capital requirements (Bitar et al., 2016). Second, the adoption of the Basel II requirements in the MENA region has tended to align bank regulations with the level of sophistication of a country’s financial system (Rocha et al., 2011). Third, the empirical research shows that banks in the region undergo a significant transformation as they adjust to the capital adequacy, liquidity and risk management practices outlined in the Basel III framework. 3 For example, Prasad et al. (2016) reports that the MENA countries, in general, and GCC countries, in particular, have made significant progress in implementing the Basel III standards by tightening capital and liquidity requirements, establishing ‘effective early warning systems and regular assessments of systemic risks as integral parts of macro-prudential policies’ (Prasad et al., 2016, p. 22). Therefore, the new Basel III requirements introduced in 2010 are expected to restrict banks’ risk activities and, as a result, will positively affect banks’ performance and stability (Alsharif et al., 2016).

The objective of this article is to empirically examine the relationship between capital regulation, competition and risk-taking behaviour of banks in the MENA region. The question regarding the impact of banking competition on the trade-off between capital requirements and the bank’s risk-taking remains relatively unexplored. Furthermore, this effect is expected to be different between Islamic banks (IBs) and conventional banks (CBs). A study by Hamza and Kachtouli (2014) on CBs and IBs in the MENA region indicates that a conventional market exhibits a high fragmentation or weak concentration, whereas a moderate concentration characterizes the Islamic banking market; however, the analysis indicates that the concentration of Islamic market has been declining since the year 2004. Using a sample of 70 CBs and 47 IBs in the MENA region, Louati et al. (2015) find that capital ratio has a significant impact on the risk behaviour of both types of banks; however, the competitive conditions do not affect the relationship between the risk-weighted assets and IBs’ credit risk, which means that these banks are still applying theoretical models based on the prohibition of interest. We complement these previous studies by investigating the impact of capital regulation and market competition on the bank’s risk-taking using a sample of 162 CBs and 63 IBs in 18 MENA countries, covering a period of 14 years (2006–2019).

Our study differs from previous research on the MENA region in two ways. First, unlike our predecessors (see, e.g., Louati et al. [2015] who examine deposit and loan changes as a proxy for credit risk), we examine both credit risk and insolvency risk of banks in the MENA countries. Second, previous studies that focus on insolvency risk do not differentiate between CBs and IBs. For example, González et al. (2017) empirically examine the relationship between market competition and banks’ risk-taking in the MENA region. The study finds that, in countries where the level of competition is high (e.g., Gulf countries), the increase in competition enhances the probability of default; however, when the level of competition is low (e.g., in non-Gulf countries), the increase in rivalry can be positive in terms of risk-shifting and efficiency. We are the first to examine whether there is a significant differential impact on IBs’ risk behaviour. Using a large sample of banking institutions (both Islamic and conventional) in 18 MENA countries, we find that when markets are less competitive, any increase in the capitalization level will increase the credit supply and, potentially, the level of NPLs, which leads to a higher probability of default. However, banks that operate in highly competitive markets will not be inclined to take more risk in the face of an increased regulatory pressure.

We contribute to the existing empirical literature in several ways. First, most previous studies examine the effect of information asymmetry 4 on the bank’s risk-taking and bank’s operations in general. Since the competitive conditions exert great pressure on the choice of banking portfolio (i.e., the level of risk-taking), we extend the empirical literature on the MENA region (Louati et al., 2015) by highlighting the role of market competition and concentration for the bank’s risk-taking behaviour. We find the relationship between market power measured by the Lerner index and bank credit risk to be strongly positive and significant. Since no prior evidence exists on the trade-off between market competition and bank insolvency risk, we test the hypothesis that in markets with relatively low competition, the powerful banking institutions will be inclined to take more risk to increase their profit. Our analysis does not find convincing evidence in support of this hypothesis.

Second, prior research studies that examine the impact of Basel capital requirements on the risk-taking behaviour of banking institutions (Ghanem, 2017; Maghyereh & Awartani, 2014) finds that capital adequacy ratio has a positive impact on their risk level. However, no evidence exists of whether this effect is significantly different between Islamic and conventional banking institutions. We are the first to report that capital ratio has a strong positive impact on the credit risk of CBs, whereas this effect is insignificant in the sample of IBs. However, market power does shape the IBs’ risk-taking behaviour. Third, our study also adds to the literature on the effectiveness of capital requirements for the bank’s risk-taking in different competitive conditions. Previous research studies provide little evidence of market power’s effect on the relationship between capital adequacy ratio and risk-taking behaviour of banks in the MENA region. For example, Louati et al. (2015) find that this effect is significant only for CBs in markets with a high and medium level of banking competition. Our analysis goes beyond the credit risk to include the insolvency risk as well and indicates a significant difference in the effect of market competition on the relationship between capital requirements and risk level of CBs and IBs.

Finally, our article extends the empirical literature on market competitiveness and risk-taking by focusing on banks’ response to the increased level of concentration in the MENA countries. We find that both IBs and CBs experience a non-linear relationship between market concentration and their risk levels. Our results are in line with the structure–conduct–performance (SCP) hypothesis, which postulates that highly concentrated banks are more competitive, and have more market power that allows them to be more profitable. The policy implications of these findings are that regulators and policymakers in the MENA region should carefully tailor the banking reform initiatives like capital stringency and more intense banking supervision as these policies may have a significantly different effect on CBs and IBs.

The rest of the article is structured as follows. The second section presents the main findings of our analysis of the existing literature and formulates the hypotheses. The third section introduces the data set and the methodology that we use. The fourth section examines the effect of capital regulation and market power on the bank’s risk-taking, while controlling for important bank characteristics and country macroeconomic conditions. The fifth section presents robustness checks and alternative specifications. The sixth section concludes the article.

Review of Literature

We start this section by reviewing the theoretical models related to capital regulation that explain the impact of capital requirements on the bank’s risk-taking behaviour.

Theoretical Models Related to Capital Regulation

There are two models that explain the impact of capital regulation on a bank’s behaviour (Louati et al., 2015). The first approach to analyse the effect of bank capital requirements is to consider banks mainly as managers of asset portfolios. From this point of view, the main effect of a bank’s capital is to adjust the capital level in accordance with risk and, thus, to encourage banks to select the desired portfolio strategy. The seminal work of Kahane (1977) and Koehn and Santomero (1980) considers a portfolio selection model based on the application of the mean-variance analysis under which a bank uses the asset prices and the equity returns (EVs) as input data, and identifies its optimal portfolio that maximizes the expected utility originating from the period-end capitalization, which, in turn, depends on the degree of a bank’s risk aversion. Both studies examine the capital regulation implications for a bank’s strength and stability, and they evaluate the effect of capital requirements on the probability of default. Binding the capital ratios with the minimum requirements may be considered a barrier limiting the bank assets’ efficient frontier; hence, the bank will react by changing the composition of its portfolio assets per unit of capital. However, the way the optimal portfolio is adjusted depends critically on the coefficient of risk aversion. The authors show that a non-‘risk-averse’ bank will respond to the increase of equity capital requirements by choosing to invest in riskier assets that increase the likelihood of a bank’s failure. Consequently, their model indicates that the impact of regulatory capital requirements on overall stability depends on a bank’s risk aversion.

The second approach to analyse the effect of bank capital requirements is the so-called incentives model. The incentives approach tries to describe the relationship between capital ratio and risk-taking through information asymmetry in the credit markets. Two agency problems may occur related to a bank’s behaviour towards risk (Louati et al., 2015). The first problem is between the bank’s current shareholders (insiders) who maximize their well-being and the new shareholders (outsiders) who have taken new shares to increase the balance sheet’s equity. The primary assumption here is that the bank satisfies the capital requirements by selling stocks to outside investors. Selling loans is another alternative that is a risky approach. Since the minimum capital required is based on the bank’s size, the regulatory standards could be met by reducing its loan portfolio. However, this strategy may also be costly for the bank. For example, if the bank that sells loans is paid to continue monitoring them for the new owners, there will be an additional moral hazard problem (Besanko & Kanatas, 1996). Therefore, satisfying capital requirements may be costly not only for a bank’s insiders but also for the regulators/insurers whose risk exposure may increase as a consequence. Hence, depending on the expectations regarding the regulatory authority behaviour, the bank may decide either to reduce or raise the risk of its portfolio and its market value.

The existing empirical literature fails to provide conclusive evidence in support of either theory. The increase of capital ratio may reduce the risk associated with one type of agency problem but may strengthen that of another type. In this context, Lee and Hsieh (2013) argue that the relationship between capital requirements and a bank’s risk-taking can be explained using the regulatory and moral hazard paradigms. The study refers to the moral hazard hypothesis where capital has a negative impact on the bank’s risk, and the regulatory hypothesis, in which capital and risk are positively associated. From a practical point of view, the optimal level of allocated capital should consider the mandatory control imposed by regulators since the banking sector is one of the most regulated industries in the world (Diamond & Rajan, 2000). Bank regulation is primarily based on the minimum capital requirements set by the Basel Committee to strengthen the stability of the banking system and reduce the bank’s risk. The Basel II guidelines identify three types of major risks to which banks are required to set aside sufficient capital resources (i.e., regulatory capital). These risks are the credit risk, market risk and operational risk (Basel Committee on Banking Supervision, 2011). Thus, the regulatory pressure of implementing Basel II capital requirements and the existing empirical literature both support the notion that capital regulation tends to improve bank efficiency and enhances a bank’s protection against risk. 5 Therefore, the impact of regulatory capital requirements on banks’ risk-taking behaviour in the MENA region is an important issue to explore.

The Impact of Capital Requirements and Competition on a Bank’s Risk Behaviour

According to the banking literature, 6 unregulated banks tend to take excessive risk to maximize the shareholder value at the expense of the depositors. The reason behind this behaviour is that if high-risk loans do not pay off, depositors’ money is protected by deposit insurance (Keeley & Furlong, 1991). In addition, the depositors lose interest in supervising a bank’s investments because their money is guaranteed. As a result, deposit insurance is no longer effective in preventing bank runs (Diamond & Dybvig, 1983). However, this situation creates incentives for managers to take on more risk. A risk-based capital plan must be developed to prevent this moral hazard pattern and support the regulatory theory (Kim & Santomero, 1988). This plan is based on the assumption of a positive relationship between capital and risk, meaning that supervisory authorities encourage banks to increase their capital level proportionally with the amount of risk taken (Altunbas et al., 2007; Iannotta et al., 2007). As a result, banks will be more prudent with their choice of risky activities to avoid costly increases in their capital ratios.

The empirical literature provides strong evidence in support of this notion. For example, Ghosh (2014) explores the relationship between capital and risk in 57 CBs and 46 IBs, during the period from 1996 to 2011. The results show that banks raise their capitalization levels in response to a higher risk rather than the other way round. 7 In the same context, Mastura et al. (2014) argue for a significant and positive relationship between capital adequacy ratio and banking activity. Their analysis is based on a sample of 52 IBs and 186 CBs in 14 countries, during the period from 1999 to 2009. Other studies report opposite results. For example, Berger and Bouwman (2013) examine US banks and find that the capital positively impacts small banks’ probability of survival during crisis periods. Anginer and Demirgüç-Kunt (2014) report a negative association between capital measures and several indicators of a bank’s risk based on a large sample of banks in 65 countries. Examining the UK banks, Alfon et al. (2004) also find a negative relationship between capital and risk-taking from 1998 to 2003. Similar results are reported by Klomp and de Haan (2012) for a sample of banks in 70 developing and emerging countries and Lee and Hsieh (2013) studying banks in 42 Asian countries. Gosh (2014) suggests that the lack of a consensus between these various studies could be due to different risk measures used as dependent variables.

The empirical literature with a main focus on the MENA region also reports mixed results. For example, Maghyereh and Awartani (2014) find no significant relationship between capital stringency and the likelihood of the bank’s distress in the GCC region. However, Ghanem (2017), using bank-level data throughout the period from 1997 to 2013, finds that the implementation of the Basel II capital requirements has a positive effect on banks’ credit growth in Egypt, Jordan, Lebanon, Morocco and Tunisia. A more recent study of Bitar et al. (2016) examines the impact of various regulatory capital ratios on a bank’s performance using a sample of 168 banks in 17 MENA countries. Their findings suggest that the compliance with the Basel II capital requirements improves a bank’s efficiency and enhances a bank’s protection against risk. However, their analysis does not differentiate between Islamic and conventional banking systems that coexist in the MENA region. Since IBs have higher capitalization levels than CBs (see Table 2), we may expect this effect to be different between the two banking institutions. In line with the regulatory hypothesis and the findings of previous empirical studies on the MENA region, we postulate the following hypothesis:

Though there is a growing body of empirical research that reports a positive and significant relationship between capital ratio and a bank’s credit risk (usually measured by NPLs to total loans), only limited evidence exists on the link between capital requirements and insolvency risk. For example, González et al. (2017) empirically examine the relationship between market competition and banks’ insolvency risk in the MENA region. They find that, in countries where the level of competition is high (e.g., Gulf countries), the rise in competition increases the probability of default; however, when the level of competition is low (e.g., non-Gulf countries), the increase in rivalry can be positive in terms of risk-shifting and efficiency.

8

However, no evidence exists of whether this effect is different between Islamic and conventional banking systems. To fill in this gap, we investigate the differential impact of market competition on risk-taking behaviour of IBs. In line with competition–stability theory,

9

we expect a positive association between market competition and bank risk-taking. This is our second hypothesis:

Is There Any Moderating Effect of Market Competition on Islamic Banking Risk-taking Behaviour?

Most of the contemporary theories use the traditional banking system to explain the pattern of IBs. Aggarwal and Yousef (2000) define the Islamic financial model as the prospect of ‘risk and profit sharing’, and conclude that this model is not widely used because of agency and moral hazard problems. The theoretical model of Islamic banking is different from that of conventional banking. Specifically, the CBs’ interest-based contracts are replaced in Islamic banking with earnings-based contracts in which profits and losses are shared between the bank and the borrower. Moreover, IBs are entitled to receive deposits mainly in the form of current accounts, which have no interest, but where the bank is liable to pay capital to holders at their request. Additionally, investment accounts (savings) are defined as accounts that generate a return based on the rate of profit so that the rates may be adjusted depending on the realized profit and even on the loss that would be subsequently shared between the bank and the investment account holders (Iqbal et al., 1998). These banks offer products in accordance with Fiqh Al Muamalet that encourages trading and productive investment (Hamza & Kachtouli, 2014).

Besides the observed differences between the two models, 10 some previous studies confirmed that IBs diverge from their theoretical models by adopting CBs’ strategies. In this context, Siddiqui (2006) argues that IB activities are based on sales instruments rather than on partnership. Bourkis and Nabi (2013) point out that Islamic financial institutions face additional risk because they have limitations in financing, investing and risk management activities. At the same time, their financial modes are more complex. However, Khediri et al. (2015) stipulate that, since both types of banks operate in the same competitive environment and are regulated in the same way in most countries, they are likely to have similar behaviour and thus identical strategies. Chong and Liu (2009) also argue that, in practice, IBs are not different from CBs, and they suggest that the fast growth of Islamic banking in recent years is not due to the principles of Sharia-compliant banks but rather to Islamic resurgence worldwide. Therefore, IBs are subject to some risks that are common with CBs and to other risks that are specific to Islamic financial institutions. The dispute on how IBs’ behaviour deviates from the conventional one is still going on.

The empirical literature that investigates the differential impact of market competition and concertation on the risk behaviour of IBs is very limited. For example, Louati et al. (2015) find that competitive conditions have no significant effect on the relationship between capital adequacy ratio and IBs’ risk behaviour, which means that these types of banks are still applying theoretical models based on the prohibition of interest. In a more general context, González et al. (2017) argue that in markets with a high degree of competition, increasing this level further may have an effect on the margin of interest that does not offset the risk-sifting effect, and they suggest a U-shaped relationship between competition and risk of failure for MENA banks. Since the banking market in the MENA countries is characterized with a moderate level of competition, the relationship between competition and a bank’s risk-taking can be explained by the competition–fragility hypothesis. The supporters of this hypothesis suggest that market competition will lower the interest margin for banks (Allen & Gale, 2004; Hellmann et al., 2000; Keeley, 1990). Therefore, banks’ profits will decrease, leading to an increased probability of default and, consequently, an overall disruption of the banking system’s financial stability. According to Weill (2011), Islamic banking institutions in the MENA region have a lower market power level than conventional ones, so this effect is expected to be different between the two banking systems. Based on this, we develop the following hypotheses:

Theoretical Framework

There are two opposing theories in the literature regarding the impact of competition on bank behaviour (Louati et al., 2015). The first theory shows that a competitive market may increase risk-taking behaviour of banks in order to maintain their previous level of profit (Allen & Gale, 2004). This risky behaviour can be observed either through the increase in credit risk of the loan portfolio or the fall in the capital buffer level, or simultaneously. Such behaviour can lead to an increased level of NPLs and a greater probability of bank default. However, the second theory postulates that restricted competition should encourage banks to protect their high ‘franchise value’ by pursuing safety policies that contribute to the whole banking system’s stability. Therefore, according to the franchise value paradigm, banks limit their risk when they have market power in lending (Louati et al., 2015). As the underlying source of franchise value is assumed to be the bank’s market power, reduced competition among banks has been considered important to promote banking stability. Conversely, an increase in competition erodes their quasi-monopoly rents (Jimenez et al., 2013). This theory has been theoretically and empirically supported in the banking literature. We extend the existing literature in this area by investigating the relationship between capital regulation, competition and risk-taking behaviour of banks in the emerging economies that belong to the MENA region, using a large sample of banks during the period from 2005 to 2019.

Methodology: Data Source, Sample Frame and Empirical Model

Sample Selection and Data Description

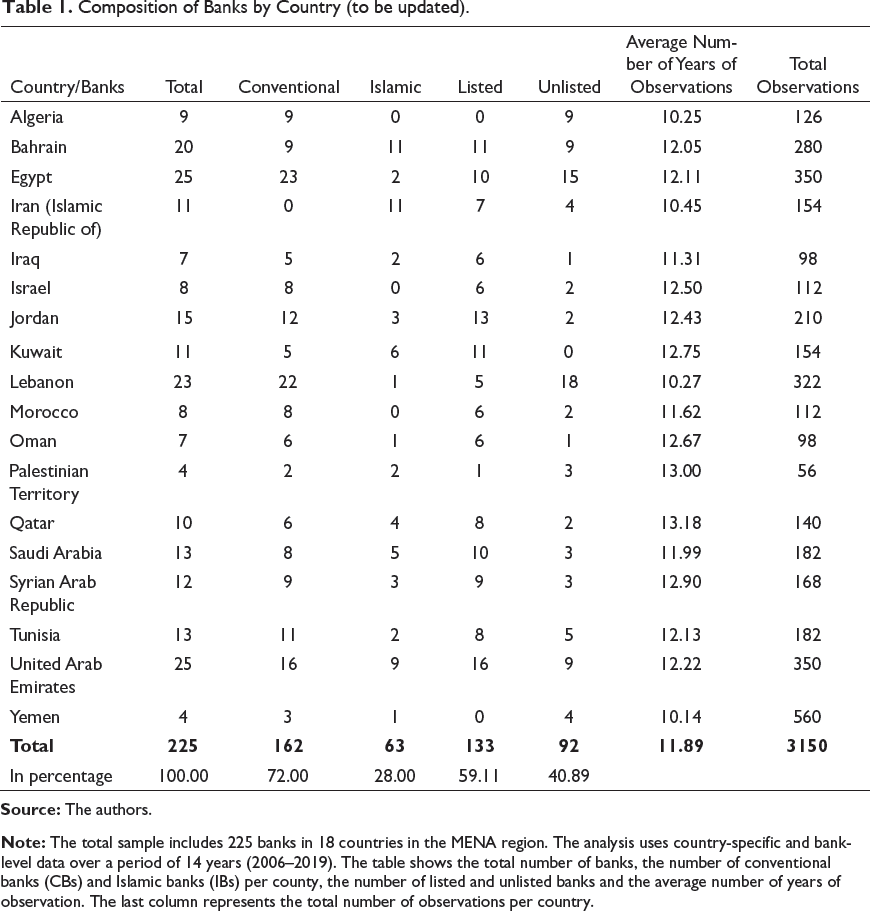

To investigate the capital requirements and market competition effects on the stability of financial institutions in the MENA region, we use a data set, covering 3,150 observations from 225 banks in 18 MENA countries, including the six GCC countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and United Arab Emirates ). The accounting data are collected from the Orbis BankFocus database (Bureau Van Dijk), together with the annual reports of the banks (when possible), included in the sample. All observations with negative equity, operating expenses and zero fixed assets are cancelled to avoid misinterpretations or bias. Moreover, we use other sources of secondary data such as the World Bank’s World Development Indicators (WDI) and Worldwide Governance Indicators (WGI), International Financial Statistics and annual reports of the central banks to collect macroeconomic data. The sample period’s selection to cover the years from 2006 to 2019 is dictated by the data availability for all banks in the sample, and for each year of the observation period. At the same time, the year of 2005 is dropped from the regression analysis because of insufficient data.

Composition of Banks by Country (to be updated).

Empirical Model

Since variables like capital adequacy ratio and market competition are considered to be significant determinants of banks’ financial stability (credit and insolvency risk) and may have a differential effect on IBs’ risk behaviour, we include them as explanatory variables in our analysis. This study uses a dynamic panel data model and employs the bank-level and country-wise characteristics as control variables (see, e.g., Appendix A published as online supplemental material). The basic framework for our analysis is as follows:

where, γ it is a measure of the risk of bank i in year t, CAR it and MarketCompet it are the explanatory variables (respectively, capital adequacy ratio and market competition indicator), X it is the vector of control variables (bank accounting ratios and macroeconomic indicators), β1 to β5 are the regression coefficients and u it is the disturbance term that is assumed to be normally distributed with a mean of 0. The vector of dummy variables (D) includes a GCC dummy variable that is equal to 1 if a bank belongs to one of the six GCC countries, and 0 otherwise, and a crisis time dummy (CRISIS) that takes the value of 1 for the years 2008–2009, and 0 otherwise. In this study, we follow the work of Abedifar et al. (2013) and Beck et al. (2013), and consider 2008–2009 as the crisis period. We also control for year and country fixed effects in each model. Next, we examine the impact of marker competition on the trade-off between capital and risk.

Accordingly, Equation (2) incorporates the interaction term between capital adequacy ratio and the respective levels of market competition (CAR it × MarketCompet it ), together with the capital ratio and the competition index as stand-alone variables, and all the explanatory and control variables of Equation (1). 11

We use fixed-effect/random-effect specifications and perform a Hausman test, where the null hypothesis is that the preferred model is random effects versus the alternative fixed effects. The choice between random- and fixed-effects specification depends on the prob. > χ 2 being more or less than 5%, respectively. The test rejects the random-effects specification at the 1% level. Note that in a panel data framework, Equations (1) and (2) specify dynamic structures and, therefore, endogeneity, autocorrelation and heteroscedasticity problems may exist. To account for such potential issues, we employ dynamic panel data generalized method of moments (GMM) approach developed by Arellano and Bover (1995) as part of our robustness checks (see section ‘Analysis’). Finally, we estimate the level of correlation among capital ratio, market competition indicators and other important variables to identify if there is any multicollinearity problem. No significant correlation between capital ratio variable and market competition measures is observed, as well as between capital ratio/competition indicators and other variables in the model. Therefore, the correlation matrix (see Appendix B published as online supplemental material) suggests that our estimation results do not seem to suffer from multicollinearity problem.

Variables Definition

Unlike our predecessors, we examine both the credit risk and insolvency risk of banks in the MENA region. We measure credit risk using the ratio of loan loss reserves to gross loans (LLRs/GLs). This ratio measures loan quality (Abedifar et al., 2013; Altunbas et al., 2007; Lee & Hsieh, 2013), with higher values indicating poorer loan quality or higher protection against credit default risk. For robustness purposes, we also use NPLs/GLs ratio, following Abdelaziz et al. (2020). 12 This study employs the widely used measure of insolvency risk, namely accounting Z-score, defined as Z = (ROA + CAR)/σ(ROA), where ROA is the return on assets, σ(ROA) is the standard deviation of ROA and CAR is the capital-to-asset ratio. The choice of Z-score is dictated by the fact that this measure is often used in empirical studies to determine the risk and financial stability of a bank (Boyd et al., 2006; Demirgüç-Kunt & Huizinga, 2010; González et al., 2017). We calculate the Z-score variable for each bank in the sample over the estimation period (2006–2019). 13 Higher values of our measure of insolvency risk imply a lower probability of default. Therefore, a positive estimation coefficient on this variable would mean a negative association between capital and risk. We follow the previous research studies (Barry et al., 2011; Haque, 2018; Lepetit et al., 2008) in using portfolio risk (PR) as an alternative measure of insolvency risk. It is measured by the ratio of return on assets (ROA) to the standard deviation of ROA.

The choice of independent variables used in our analysis is primarily guided by previous empirical literature and data availability. These variables include both explanatory variables (capital ratio and competition measures) and a set of control variables (institution, ownership, profitability and efficiency ratios, liquidity, size, macroeconomic variables and dummy variables that capture year or country characteristics). All independent and control variables used in our analysis are described in Appendix A published as online supplemental material.

Following previous research (Anzoategui et al., 2010; Louati et al., 2015), we chose the Lerner index as a direct measure of competition for the reason that it emphasizes the pricing power, which can be seen in the difference between the price and the marginal cost, therefore, capturing the extent to which a firm can raise its prices beyond its marginal costs (Hamza & Kachtouli, 2014). The Lerner index’s value varies between 0 and 1, such as a Lerner index = 0 means a perfectly competitive behaviour, and the firm has no market power. A Lerner index close to 1 shows the competitions’ weakness at the price level, and that the firm exercises a market power due to a higher markup. A Lerner index < 0 implies a price below the marginal cost that could occur due, for example, to a non-optimal banking practice. Details on index definition and the estimation approach are provided in Appendix C published as online supplemental material. We follow the work of Tabak et al. (2012) and Louati et al. (2015), and decompose the Lerner index into three dummy variables, reflecting three levels of competitiveness. The reason is that we want to obtain clear and robust results regarding the role played by the banking competition for the relationship between a bank’s capitalization level and its risk level.

Next, we create an interaction term between capital adequacy ratio and each competitiveness level as proxied by the three dummies (see Equation [3]). The analysis of the Lerner index in the banking industry in the MENA countries shows that Kuwait has the most substantial level of market power (0.573), followed by Saudi Arabia (0.559) and Qatar (0.541). The higher levels of index indicate that banks in these countries are operating in a less competitive environment. Respectively, the countries with the lowest levels of market power are Israel (0.234) and Iran (0.236). These results are in line with Louati et al. (2015), who report that CBs and IBs included in their study of the MENA region operate in markets with a relatively low competitive level than the rest of the regions. 14

The Herfindahl–Hirschman index (HHI) is another well-known measure of competition and concentration of the market conceived by Hirschman (1945) and Herfindahl (1950). It is widely used to estimate the level of competition of a market and its structure. The HHI considers the relative size and the distribution of companies in a market, and aims towards zero when the market consists of a large number of banks of relatively equal size. 15 The more the value of the indicator increases, the more the market is concentrated, and the weaker is the competition between the agents. The market, thus, aims towards a monopoly position and indicates an increase of the power of the market. The decrease of HHI indicates the opposite (marker power and Kachtouli, 2014). Details on index definition and the estimation approach are provided in Appendix C published as online supplemental material. We apply HHI in Equations (1) and (2) as a measure of banking concentration. We create an interaction term between the capital adequacy ratio and the HHI (see Equation [2]) to investigate the impact of banking concentration on the relationship between a bank’s capitalization level and its risk level.

Following Haque (2018), we use two ownership variables to measure internal corporate governance. These include the concentration of ownership as measured by the percentage of shareholding of the largest shareholder and the types of ownership, that is, government shareholding and foreign ownership (see Table 2). In accordance with previous research studies (Iannotta et al., 2007; Shehzad et al., 2010), we expect ownership concentration to have a negative effect on banks’ behaviour, whereas government ownership should exert a positive impact. Likewise, we follow Agoraki et al. (2011) and Lassoued et al. (2016) to predict that foreign ownership will reduce the bank’s risk-taking in the MENA region. Our preliminary tests show that only ownership concentration is statistically significant and negatively associated with the bank’s risk.

Descriptive Statistics of Banks.

We follow Forssbæck (2011), Shehzad et al. (2010) and Zheng et al. (2017a), among others, in using several bank-specific characteristics known to be significant determinants of bank behaviour. These include deposits, loans-to-assets ratio, other earning assets, income diversity, tier 1 ratio, funding fragility, bank size and liquid assets employed in the regression analysis as control variables (see Appendix A published as online supplemental material). While some previous studies (see e.g., Bitar et al., 2016) employ cost-to-income ratio (CIR) as dependent variable in their analysis of bank profitability, others use cost-efficiency as explanatory variable (Bashir & Hassan, 2017). In this study, we use CIR to control for differences in a bank’s efficiency between the two groups of banks (Islamic and conventional). Following the approach taken by Kaufmann et al. (2008), we create an index, institution, which is the mean of six governance variables: voice and accountability; political stability and absence of violence; government effectiveness; regulatory quality; rule of law; and control of corruption (see Appendix A published as online supplemental material). A higher value of the index indicates a better institutional environment in the sample country. In line with previous research studies (Abdelaziz et al., 2020; Louati et al., 2015; Schaeck & Cihák, 2007), we use real GDP per capital, GDP growth rate, inflation and the growth in domestic credit to the private sector as a percentage of GDP to control for macroeconomic differences across the countries in our sample. 16

Analysis

Descriptive Statistics and Univariate Analysis

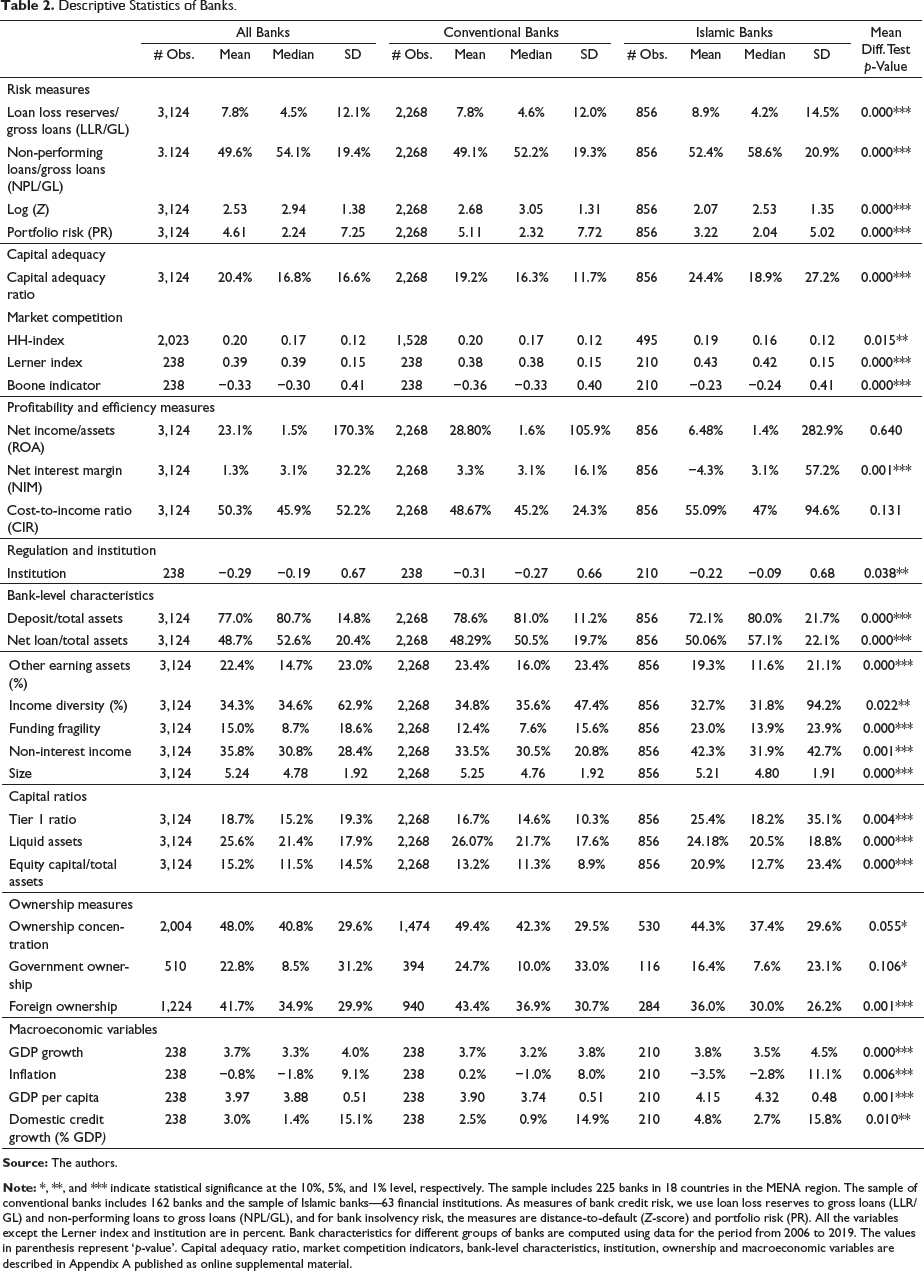

Table 2 presents the summary statistics of the sample and compares different variables used in our analysis across the two banking systems (CBs and IBs). We use two alternative measures for a bank’s credit risk (LLR/GL and NPL/GL); in a similar way, we use Z-score and PR to measure a bank’s insolvency risk. We observe a statistically significant difference between the two sample (CBs and IBs) in all risk measures; the mean difference is significant at the 1% level of significance. The estimated value of profitability ratio (ROA) shows that CBs experience a much better performance over the sample period of 14 years than IBs (28.80% vs. 6.48%). When net interest margin (NIM) is used to measure bank profitability, both types of banks show low performance, with IBs performing much worse than CBs. Our results are in line with Olson and Zoubi (2017), who show that during and after the global financial crisis in 2007–2008, the IBs’ performance has significantly deteriorated. Furthermore, the data in Table 2 indicate that IBs have a higher level of inefficiency measured by the CIR than CBs (55.09% vs. 48.67%); however, the mean difference between the two samples is statistically insignificant.

According to Table 2 data, we observe that capital adequacy ratio’s mean value for CBs and IBs is between 19% and 24%, which is well above the Basel Accords’ minimum capitalization. Previous research studies on Islamic banking indicate that IBs are more durable than their conventional counterparts, which is due to the strong capital ratios that are considerably higher than those of the traditional banks (Abedifar et al., 2013; Louati et al., 2015). However, a study by Bourkis and Nabi (2013) reveals that though the average capitalization ratio of IBs is higher, there is no significant capitalization difference between the two banking systems. Our data analysis shows a statistically significant difference in the capital adequacy ratio between CBs and IBs. Table 2 also provides data for the Lerner index and Boone indicator for each sample of banks. We do find a significant difference in the level of market power as measured by the Lerner index and Boone indicator between the two samples. The overall HHI is 0.20, which is considered ‘moderately concentrated’ for all countries in the sample, with the mean difference strongly significant at the 5% level of significance.

Next, we compare the individual bank’s characteristics across the two samples and find that the bank-specific variables are significantly different between CBs and IBs (the mean difference is strongly significant at the 1% level of significance, except income diversity). Regarding the asset size, CBs and IBs are of almost equal size. Additionally, IBs have a lower deposit to assets ratio but outperform CBs in terms of net loans to total assets (50.06% vs. 48.29%). Data in Table 2 show that income diversity and non-interest income ratios are higher in the sample of IBs; however, funding fragility for IBs much exceeds the same for CBs, which is a sign of greater financial instability of IBs. When we compare the capital ratios between the two groups of banks, we find that the tier 1 and EC/TA ratios for IBs much exceed those for CBs; however, IBs have a slightly lower level of liquid assets (24.18% vs. 26.07%). These results are in line with the previous research findings on banks in the MENA region (Haque, 2018; Mateev & Bachvarov, 2021; Olson & Zoubi, 2017). According to Grassa (2012), Islamic profit–loss sharing products present greater insolvency risk than products offered by CBs, and this type of risk has a more detrimental impact on the bank’s performance during a prolonged crisis. Table 2 confirms this finding; the insolvency risk measured by the probability of default (or Z-score) is significantly different between the two samples of banks, with CBs much less risky than IBs (2.68 vs. 2.07). We also observe that IBs have higher credit risk.

Recent empirical literature emphasizes the importance of the nature of ownership for a bank’s performance and risk-taking. Following Haque and Brown (2017), we use three measures of ownership structure—concentrated ownership as measured by the percentage of shareholding of the largest shareholder, government shareholding and foreign ownership. IBs are typically domestically owned, and the data in Table 2 support this convention; the percentage of foreign ownership in our sample of banks is 41.68, on average. The percentage of ownership concentration is larger for CBs than IBs (49.38% vs. 44.34%). The high percentage of concentrated ownership in both types of banks is in line with the previous studies’ observations for the MENA region (Farazi et al., 2011; Haque & Brown, 2017). Furthermore, around 23% of all banks in the sample are government-owned banks, with IBs having a lower percentage of government ownership. Finally, the institution variable, which is the mean of six governance variables, indicates the quality of institutions in each country in the sample; a higher value of the index indicates better institutions. In line with previous studies on the MENA region, we find that the countries in our sample are characterized with a weak institutional environment (a median value of −0.19 for the total sample). The analysis of the macroeconomic variables shows that, on average, the MENA countries experience a positive economic growth of 3.74% during the overall sample period (2006–2019).

Discussions

The Effect of Market Power and Capital Adequacy Ratio on the Bank’s Credit Risk

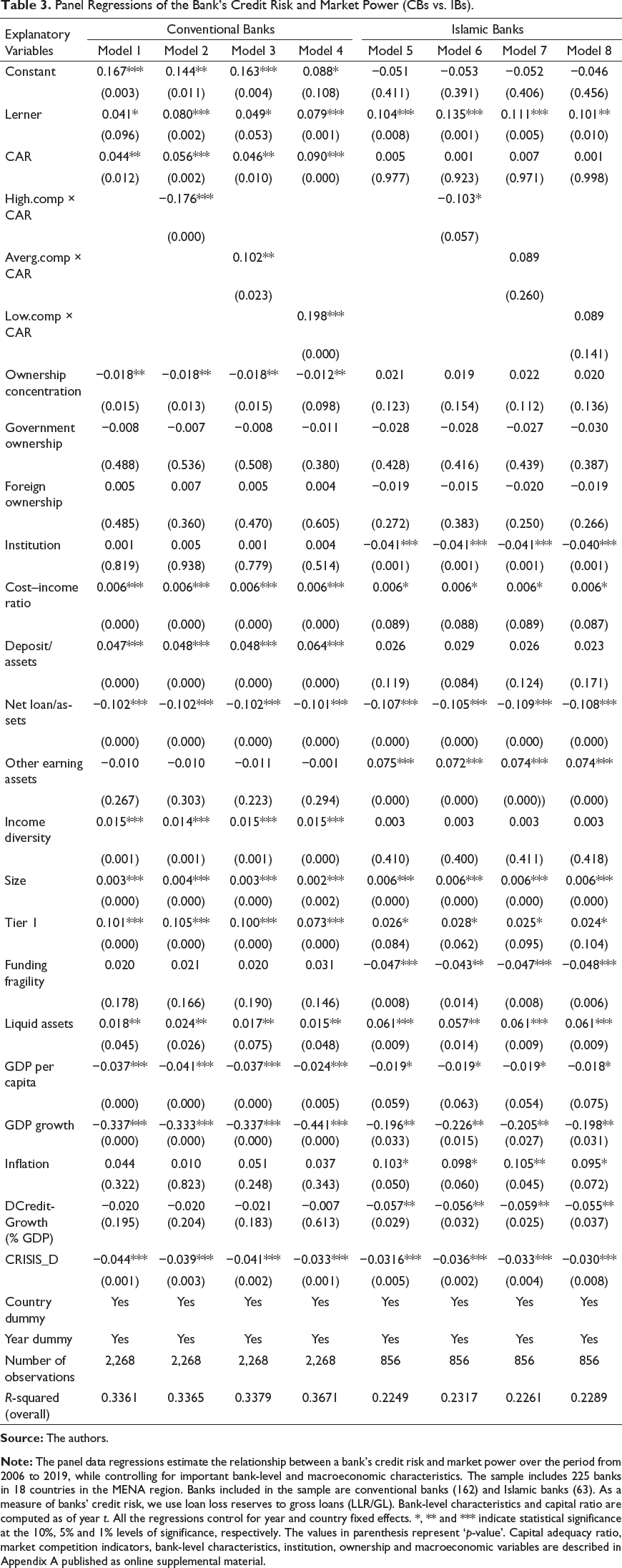

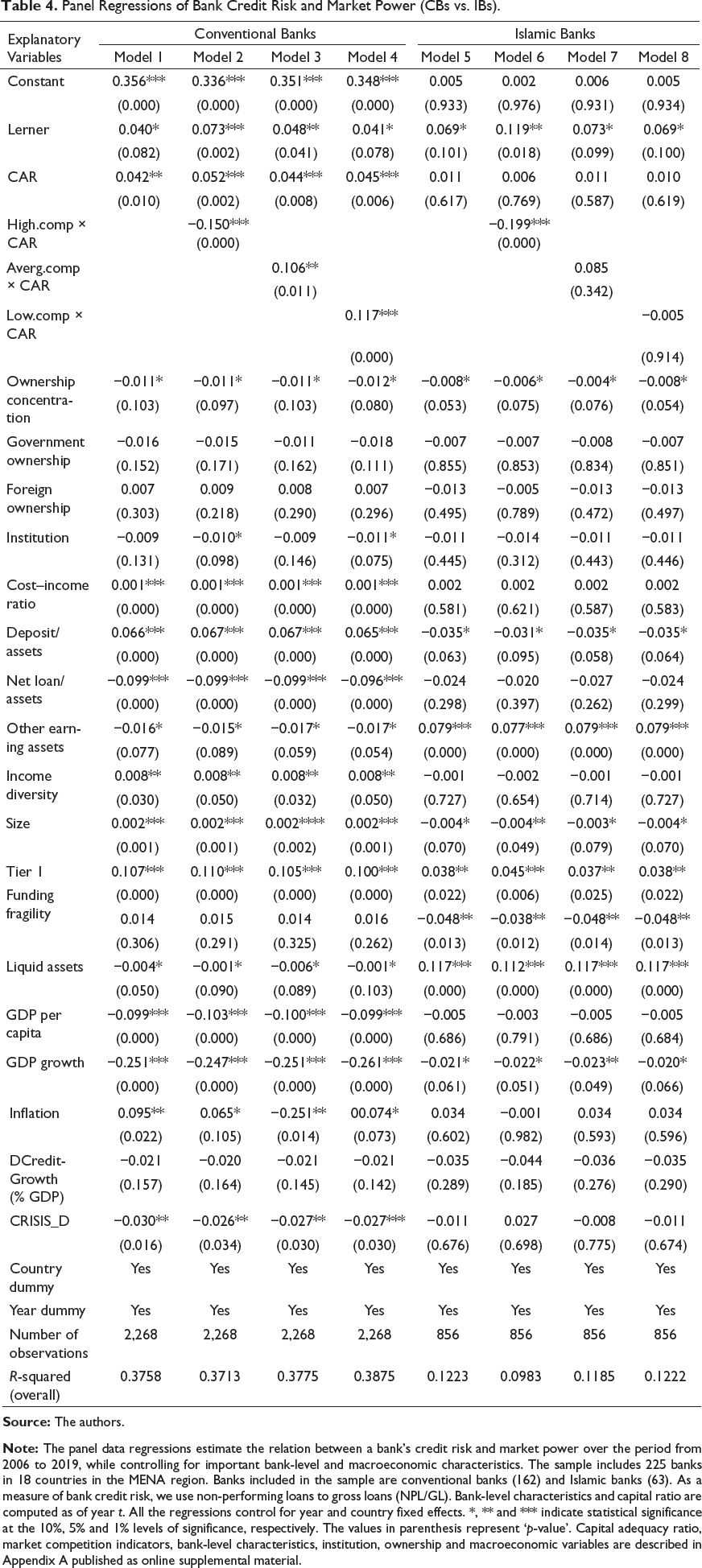

In line with our first hypothesis, we expect capital requirements to positively influence banks’ risk behaviour in the MENA region. We also test the hypothesis that this effect is significantly different between the two banking systems. Therefore, we compare the impact of capital ratio on banks’ risk behaviour between the samples of CBs and IBs. The outputs of the regression analysis for a bank’s credit risk using two alternative measures (LLR/GL and NPL/GL) are presented in Tables 3 and 4, respectively. In each regression, we use the Lerner index as a measure of market power. The outcomes of the analysis are discussed in the following paragraph.

Panel Regressions of the Bank’s Credit Risk and Market Power (CBs vs. IBs).

Following Mateev and Bachvarov (2021), we introduce in each model a composite variable, institution, which measures the overall quality of institutional environment in the sample countries. We find that this variable is strongly significant and negative only in the group of IBs. Therefore, an improvement in the quality of institutional environment in the respective country will have a strong impact on Islamic banking institutions, in limiting their credit risk level. This finding is important for regulators and policymakers in the MENA region because the improved institutional quality and sound prudential regulation will play a significant role for restricting the risk-taking behaviour of IBs only. Therefore, these banks will be more resilient to any potential shocks than their conventional counterparts.

To test the hypothesis that the effect of regulatory capital requirements on a bank’s risk-taking may depend on the level of market competition, in the next three models, we introduce an interaction term between the capital adequacy ratio and the individual level of competition (high, medium and low). To proxy for each level of competition, we use the dummy variables created in the previous section (see Equation [3]). Model 2 shows a significant interaction effect on a bank’s risk level. Specifically, the interaction between competition and capital adequacy ratio exerts a negative association with a bank’s credit risk. This indicates that the increase in capital level is negatively linked to a bank’s credit risk only when banking competition is high. In other words, in highly competitive markets, CBs will not be enforced to increase their credit risk level to meet the increased regulatory capital requirements. For the low and medium level of market competition, the analysis shows that an increase in capital requirements is followed by an increase in the level of loan loss reserves as protection against credit default risk (see Models 3 and 4). This finding has strong policy implications since any increase in the regulatory pressure (i.e., in the minimum capital requirements) will require CBs to keep lower levels of credit risk to cope with the increased competition in the banking market. Regarding the IBs behaviour, we observe that the positive impact of capital requirements on their credit risk level is significant only in highly competitive markets (see model 6). Since this effect is similar across the two samples, we cannot provide further evidence in support of our last Hypothesis (3b) that the moderating effect of market power is significantly different between the two banking systems. In line with Louati et al. (2015) who report that both CBs and IBs operate in markets with relatively low competitive level, we should expect both types of banks to keep higher levels of credit risk.

Our main results continue to hold after controlling for several common bank-level and macroeconomic characteristics. The results presented in Table 3 indicate that a bank characteristics’ impact is not significantly different between CBs and IBs. We observe that most of the ratios (except other earnings assets and funding fragility in the group of CBs) are significant determinants of banks’ credit risk and, therefore, are important drivers of risk behaviour of both CBs and IBs. The negative sign of GDP growth variable tells us that both IBs and CBs are keeping lower levels of loan loss reserves during the periods of significant economic growth as observed in the MENA countries before the outbreak of the COVID-19 pandemic. We observe similar effect of GDP per capita variable in both samples, whereas inflation and growth rate of domestic credit to the private sector variables are insignificant in the group of CBs.

Panel Regressions of Bank Credit Risk and Market Power (CBs vs. IBs).

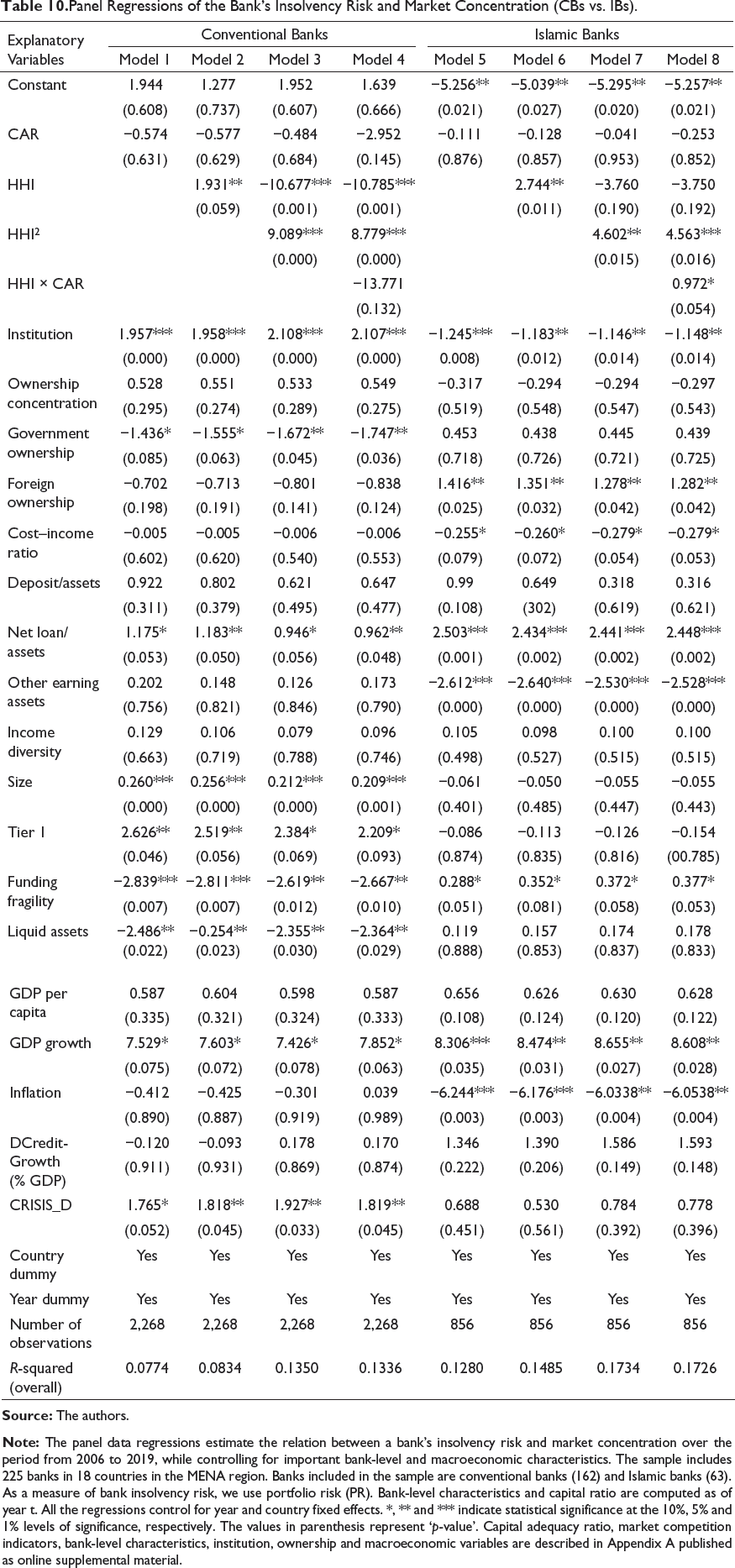

The Effect of Market Power and Capital Adequacy Ratio on Bank Insolvency Risk

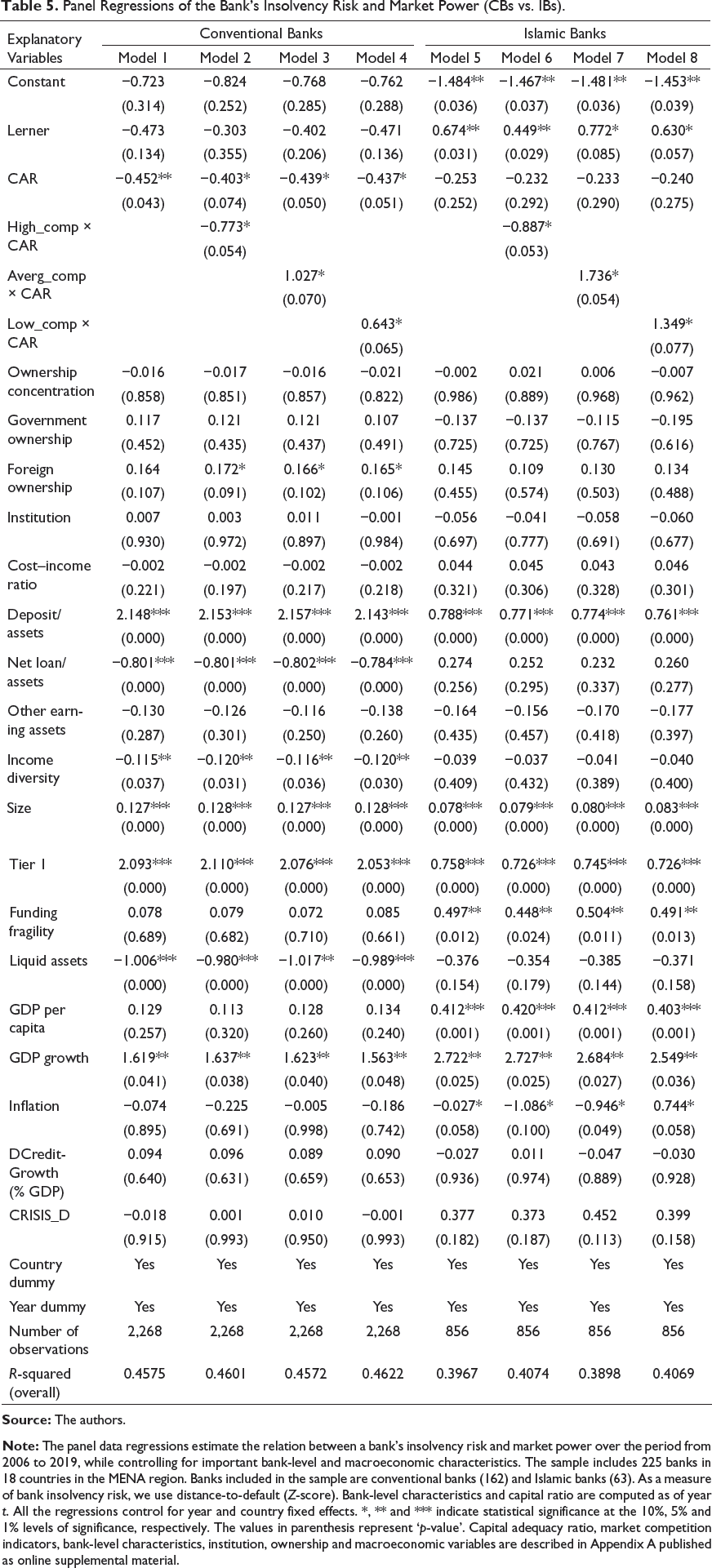

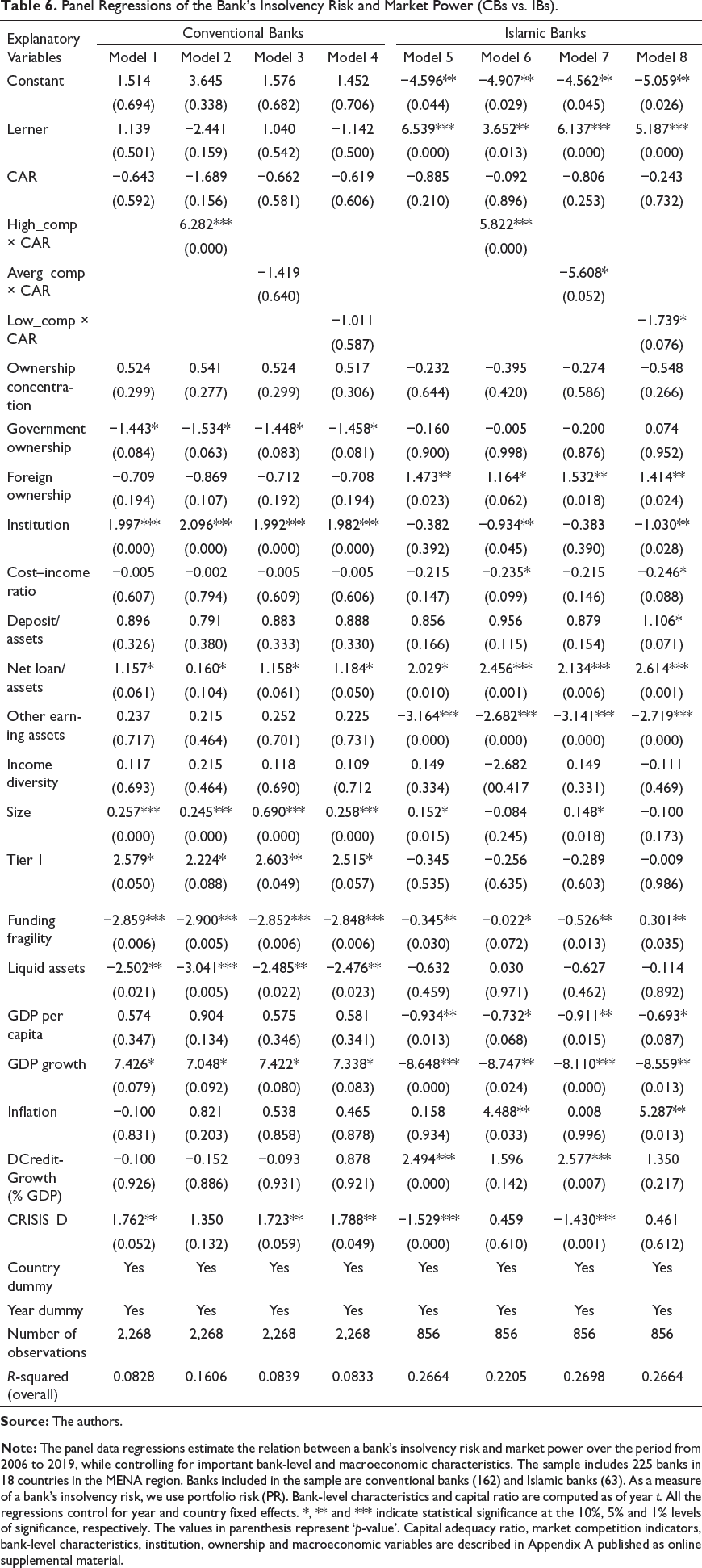

There is no prior evidence regarding the influence of capital regulation and market power on banks’ insolvency risk. We investigate the association between regulatory capital requirements and insolvency risk in different competitive conditions to fill in this gap. We measure the insolvency risk using distance-to-default (or Z-score) as a direct measure of bank stability and portfolio risk (PR) as an alternative risk measure. The outputs of the regression analysis for banks’ insolvency risk are presented in Tables 5 and 6, respectively. The outcomes of the analysis are discussed in the following paragraph.

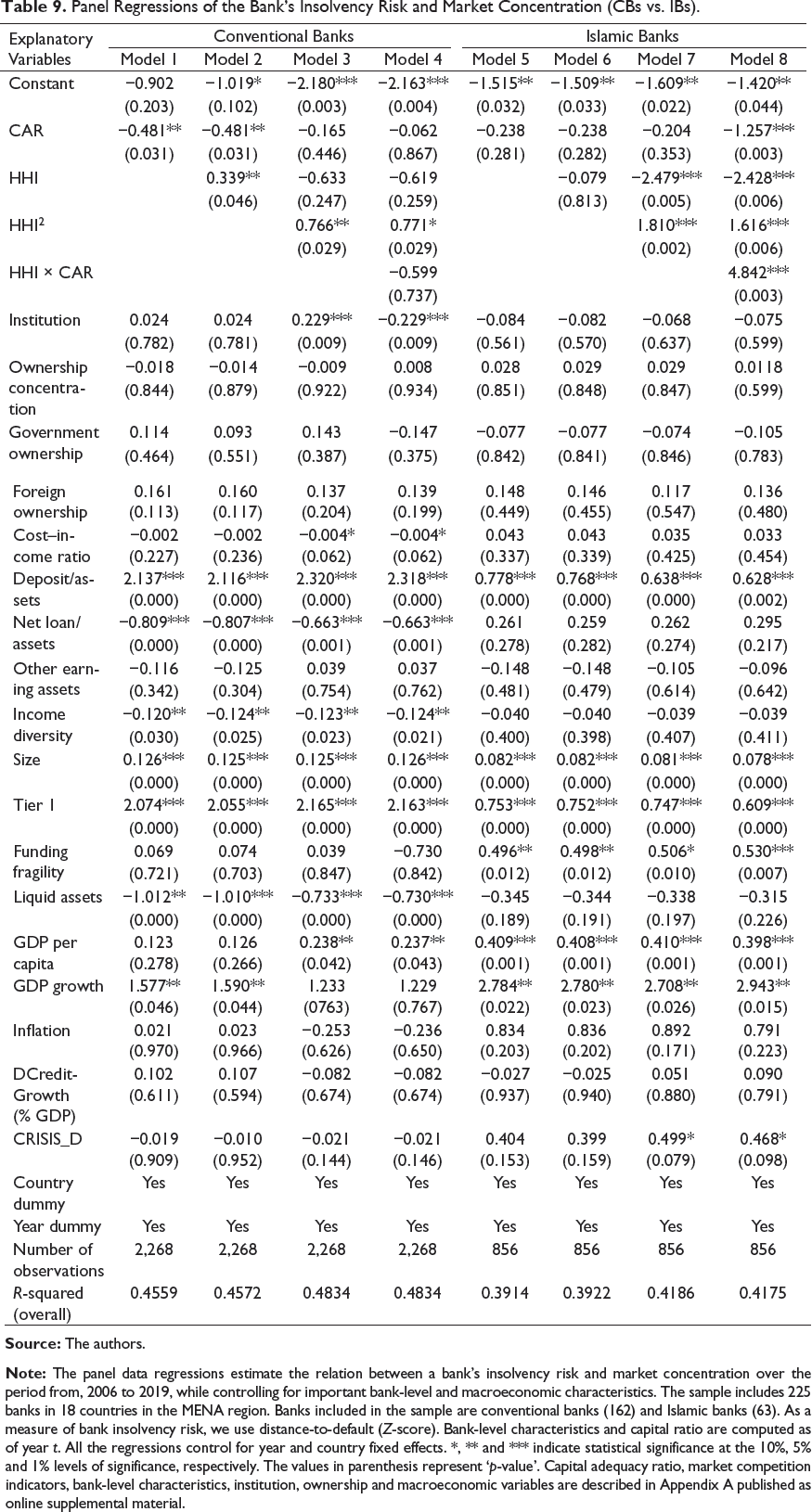

Panel Regressions of the Bank’s Insolvency Risk and Market Power (CBs vs. IBs).

Panel Regressions of the Bank’s Insolvency Risk and Market Power (CBs vs. IBs).

Next, we test the hypothesis that the effect of capital requirements on a bank’s risk-taking may depend on the banking competition level. Therefore, in the next three models, we introduce an interaction term between capital adequacy ratio and competition level (high, medium and low). The coefficients of all interaction terms are only marginally statistically significant. This finding contradicts our last Hypothesis (3a) that market competition has a substantial impact on the relationship between capital ratio and banks’ risk level. Instead, we find that banks’ financial stability in the MENA region can be explained by several bank-specific characteristics such as the level of deposits, net loans to assets, income diversity, tier 1 ratio and liquid assets. The size of the bank also plays a vital role in explaining risk behaviour since larger banks seem to have better financial stability than smaller ones. This finding contradicts the ‘moral hazard’ hypothesis and the ‘too-big-to-fail’ proposition that the larger the bank size, the greater the chance of raising risk and lessening financial stability. From a macroeconomic point of view, both the GDP growth and inflation show a significant impact on risk. While higher GDP growth warrants better banks’ financial stability, higher inflation would discount IB’ financial soundness. This is also confirmed by the strongly positive sign of GDP per capita variable in the group of IBs.

Our results do not change significantly when log (Z) is replaced with PR as a proxy for insolvency risk of a bank (see Table 6). However, we observe a differential impact of capital requirements on the insolvency risk of IBs, which depends on the level of banking competition. For example, the positive association of capital requirements with IBs’ insolvency risk intensifies in highly competitive markets. For the low and medium level of market competition, the analysis shows that an increase in capital requirements in less competitive markets will not enforce IBs to increase their level of insolvency risk (see models 3 and 4). This finding is in line with González et al. (2017), who report a significant and negative impact of market competition on risk-taking when IBs are included in their regressions, and confirms the general notion that IBs are less stable (riskier) than the conventional ones (see also Table 2). This finding has strong implications for bank managers of IBs and CBs since an increase in the minimum capital requirements by regulators may impose on them a significant change in their risky strategies, depending on the level of market competition.

What are the policy implications of these findings? First, since market power does not exert a substantial influence on the positive relationship between capital ratio and bank insolvency risk in either group of banks, we may conclude that the decision to increase or decrease the level of insolvency risk will depend on the expectations regarding the regulatory authority’s behaviour and not so much on the level of banking competition in the MENA countries. Second, since the effect of market competition is more pronounced in the group of IBs, our findings inform regulations and policymakers in the MENA countries to set up capital requirements at levels that would restrain banks with high market power from risky activities in the face of increasing competition.

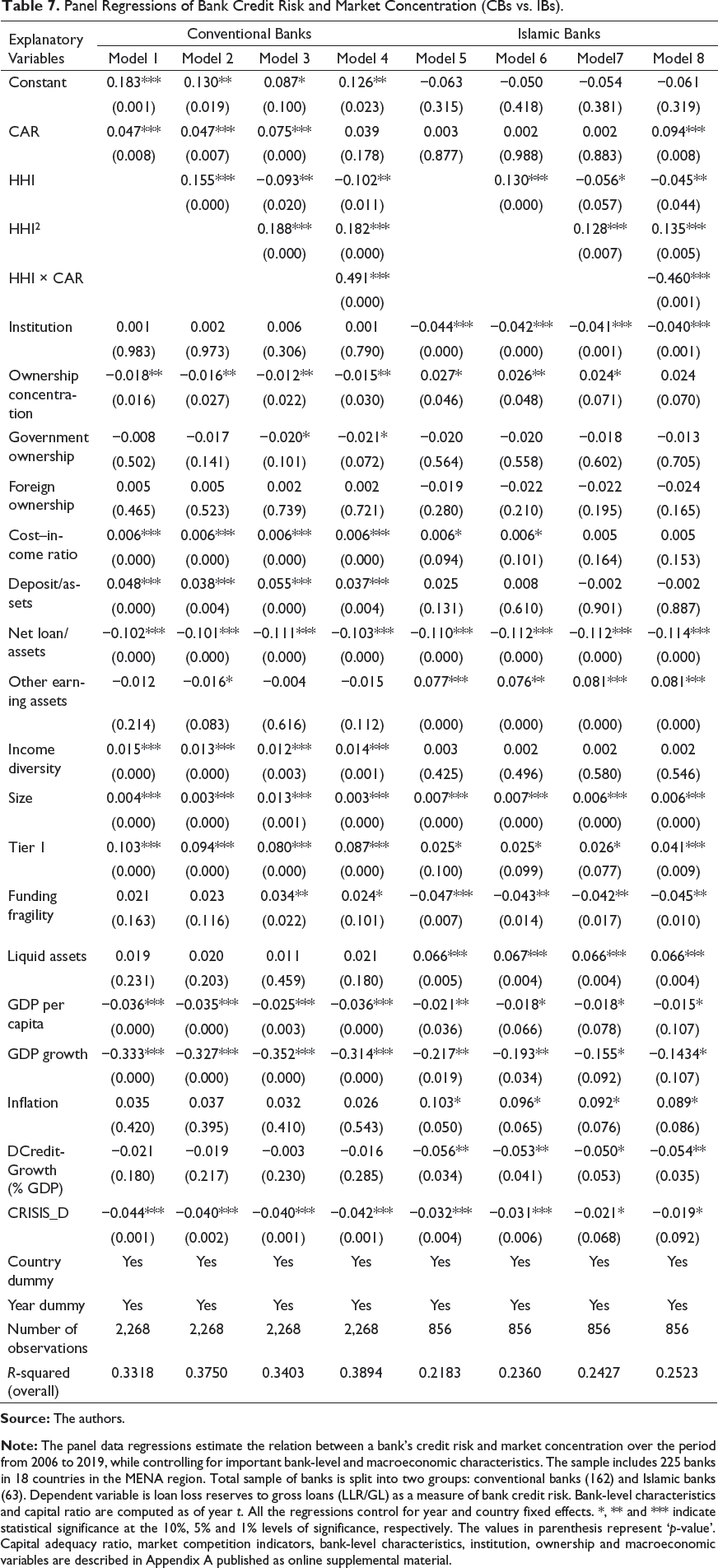

The Differential Impact of Market Concentration on Islamic Bank Credit Risk

Panel Regressions of Bank Credit Risk and Market Concentration (CBs vs. IBs).

Panel Regressions of Bank Credit Risk and Market Concentration (CBs vs. IBs).

In line with our first hypothesis, capital requirements positively relate to a bank’s credit risk (see model 1). The impact of market concentration (measured by the HHI) on the credit risk level of CBs is strongly positive and significant at the 1% level of significance (see model 2). Model 3, which combines the HHI and the squared value of the index, illustrates a classical U-shape relationship in the sample of CBs, where initially a bank’s credit risk decreases but then starts to increase with higher levels of concentration. This finding supports the notion of a non-linear relationship between a bank’s risk and market concentration as reported in some previous studies (Louati et al., 2015; Martinez-Miera & Repullo, 2010). The sign of the relationship is in line with the predictions of the SCP hypothesis, which postulates that a greater degree of concentration phases down the competition, and leads banks to enjoy higher profitability. Finally, model 4 shows that market concentration strongly moderates the relationship between capital requirements and a bank’s credit risk, that is, an increase in the minimum capital requirements will enforce concentrated banks to increase their credit risk level. This strongly supports our third Hypothesis (3a).

The results in Table 7 indicate that the relationship between market concentration and IBs’ credit risk is also significant and positive (see model 6). This finding tells us that banks operating in concentrated markets will increase their interest rates to shift up their profits as predicted by the competition–stability hypothesis. This result is grounded in the fact that banks in most countries in the MENA region operate in highly concentrated markets (which does not always necessitate low competition) as reported by González et al. (2017). Again, a classical U-shape relationship exists between the HHI and the credit risk measure (see model 7). However, the moderating effect of market concentration on IBs’ risk behaviour is significantly negative. This means that, in highly concentrated markets, an increase in regulatory capital requirements (e.g., the minimum required capital level) will not enforce banks to increase their credit risk level. In other words, if a higher concentration is associated with less competition in the market, it will lead to an increased financial stability. The reason is that IBs are known to have higher capital levels than their conventional counterparts (see Table 2). Therefore, regulators and policymakers in the MENA region may influence risk-taking behaviour of IBs through setting up of an appropriate level of capital requirements that will restrain concentrated banks from pursuing risky strategies that lead to increased profits. Such a policy intervention, however, may have an opposite effect on CBs’ risk behaviour.

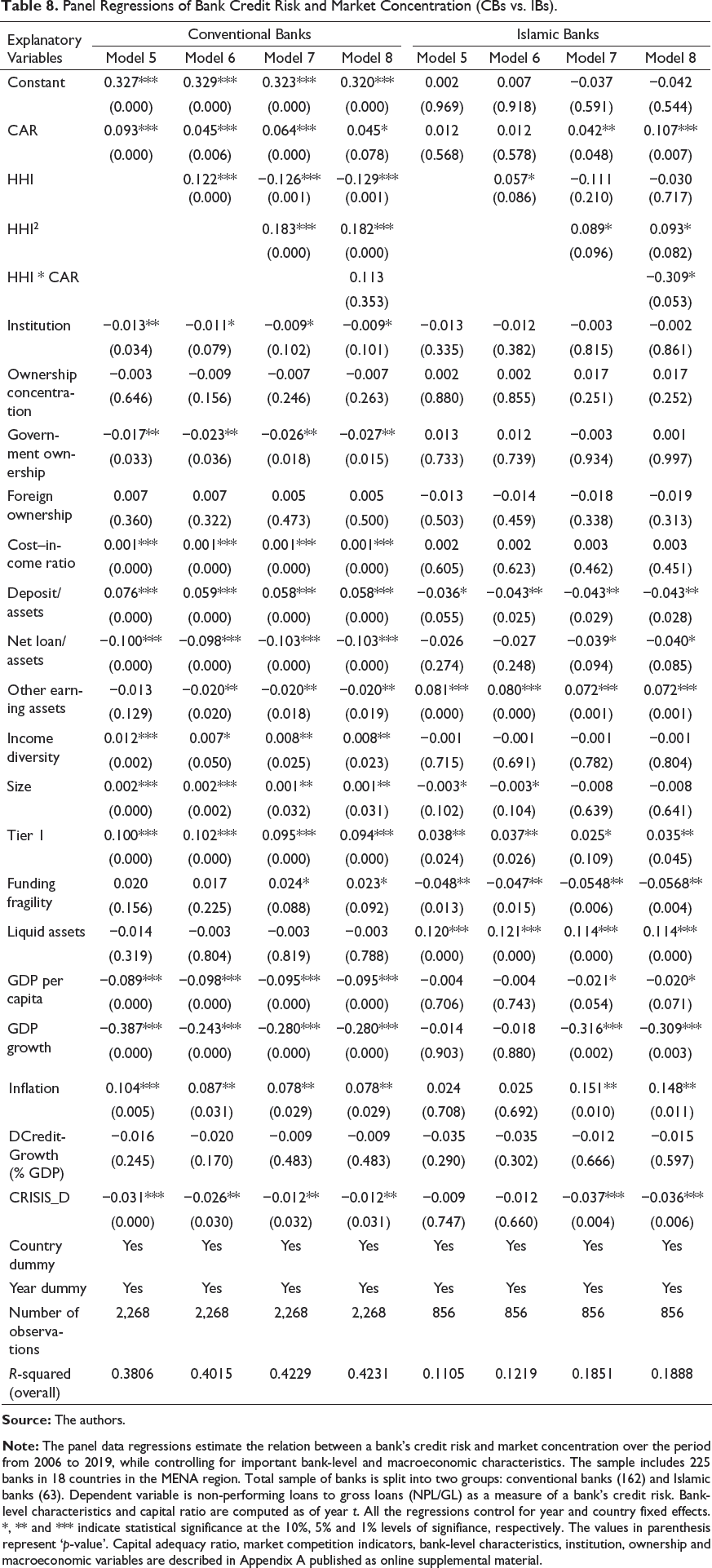

In Table 8, we present the results for CBs and IBs, using the NPLs/GLs ratio, as an alternative measure of bank credit risk. Our results do not change significantly. However, we observe that the positive association between banking concentration (measured by the HHI) and credit risk is only marginally significant in the group of IBs. Therefore, the decisions of IBs’ managers to follow risky strategies in order to increase their profits may not necessarily depend on the level of concentration in the banking industry; instead, they might be related to the expectations regarding the regulatory authority’s behaviour and the decision to increase the minimum capital requirements. In contrast, CBs will increase their credit risk levels in the face of increased concertation. As expected, the increased quality of institutions is associated with lower levels of NPLs (i.e., less credit risk). Similarly, higher levels of governance ownership in CBs help reduce the level of excessive risk-taking.

Panel Regressions of the Bank’s Insolvency Risk and Market Concentration (CBs vs. IBs).

Table 9 reveals opposite results for IBs. Specifically, market concentration measured by the HHI shows a negative (though insignificant) association with the insolvency risk measure (see model 2). This confirms the notion that concentrated banks usually take higher risk. Furthermore, we observe a classical U-shape relationship between Z-score and the HHI (see model 7). The positive sign of the relationship is in line with the expectations of SCP hypothesis as discussed earlier. A second observable difference is that the positive association between capital requirements and a bank’s insolvency risk is augmented with the increase of banking concentration (see model 8). These results provide further support to our last hypothesis (Hypothesis [3b]). Previous studies report a relatively moderate level of concentration in most countries in the MENA region (González et al., 2017). Therefore, we may expect an increase in the level of concentration in these markets to enforce IBs to enhance their risk level in response to an increased regulatory pressure, which will impact their financial stability. However, increased concentration will have the opposite effect on conventional banking institutions. Thus, our findings inform regulators and policymakers in these countries for the need to set the regulatory policies in a manner of preventing concentrated banks from engaging in risky activities.

Panel Regressions of the Bank’s Insolvency Risk and Market Concentration (CBs vs. IBs).

Robustness Checks and Alternative Specifications

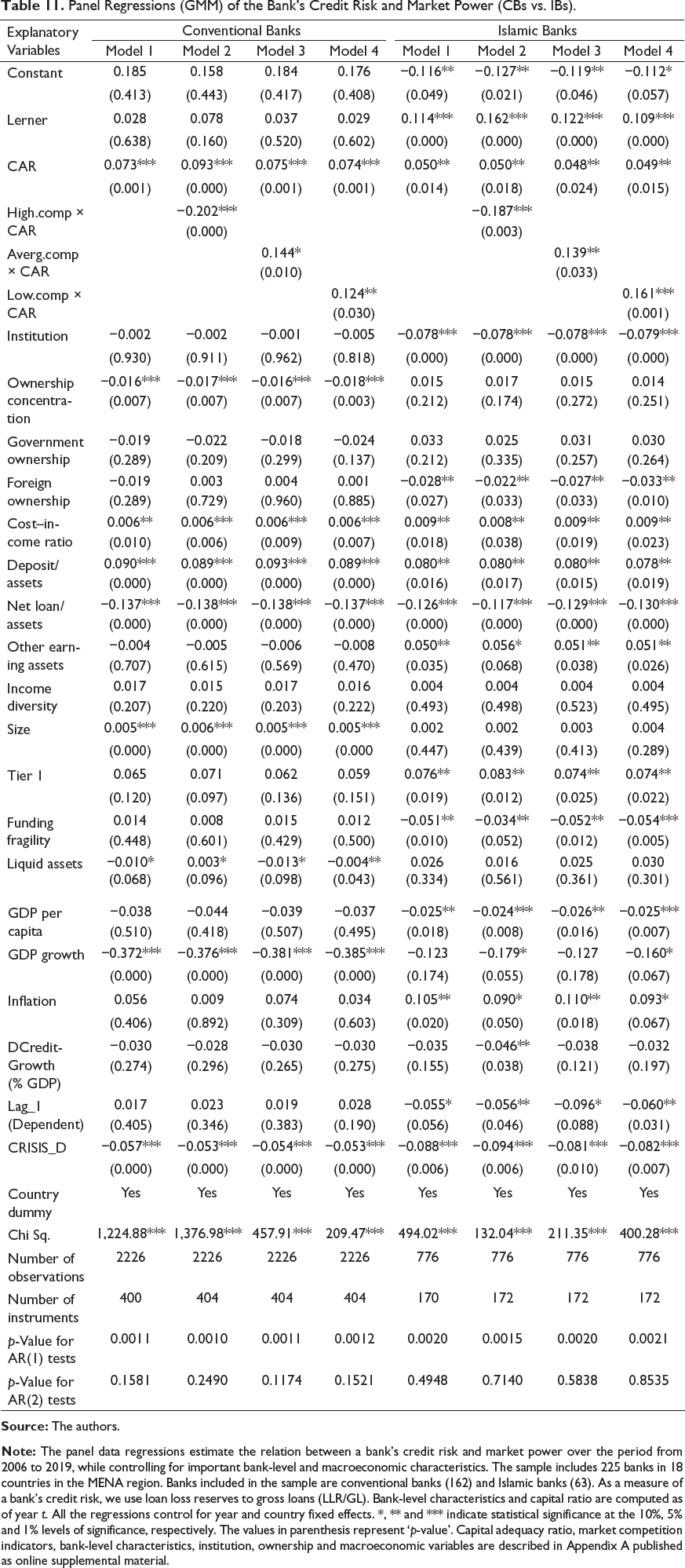

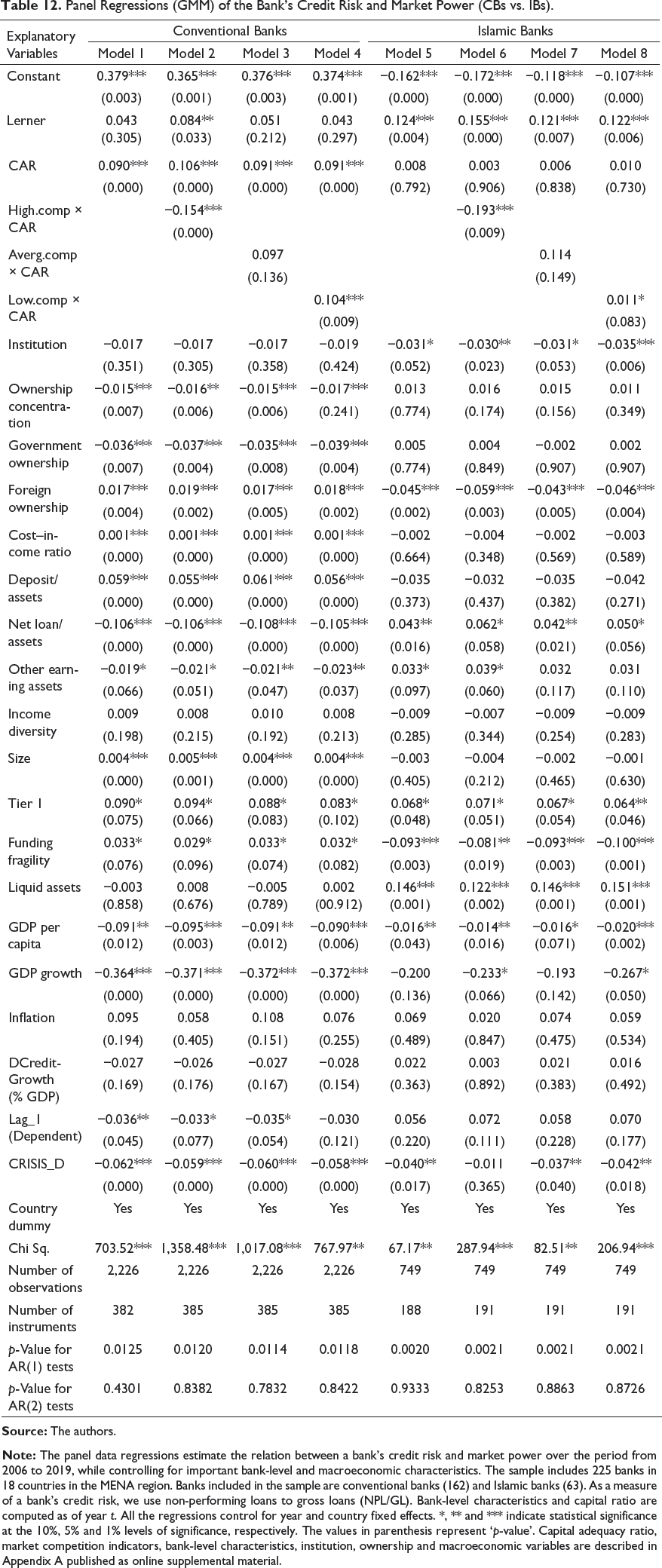

Panel Regressions (GMM) of the Bank’s Credit Risk and Market Power (CBs vs. IBs).

Panel Regressions (GMM) of the Bank’s Credit Risk and Market Power (CBs vs. IBs).

Second, we check the robustness of our results using alternative measures of bank risk and different control variables. For example, we proxy bank insolvency risk with volatility in EV in addition to distance-to-default and PR. The results are similar though the number of observations is limited only to listed banking institutions. We follow Louati et al. (2015) in using changes in deposits and loans to proxy for deposit and credit risk. The estimation results indicate that the relationship between capital requirements and deposit changes is insignificant in both samples, whereas the level of market competition has a strong influence on banks’ risk behaviour only in the sample of IBs (the results are not reported here for the sake of brevity but available on request).

Next, we estimate our model using different control variables. For example, instead of tier 1, we use tangible equity and replace income diversity with non-interest income. Finally, we include an alternative measure of the degree of competition (Boone indicator calculated as the elasticity of profits to marginal costs) as a determinant of bank risk. The regression outputs are insignificant at most instances. As our preliminary regressions indicate that the GCC dummy variable is significant, we split the sample into two sub-samples, including GCC and non-GCC countries, respectively. Our results for the GCC sample are in line with Maghyereh and Awartani (2014), who also find no significant relationship between capital stringency and the likelihood of bank distress in the GCC region. However, market competition is a strong determinant of a bank’s risk behaviour in these countries.

Conclusions

This article investigates the effect of regulatory capital requirements and market competition on banks’ risk-taking behaviour in the MENA region. Most of the previous studies focusing on the MENA region examine the impact of market competition on credit risk only (Louati et al., 2015) or the banking system as a whole (González et al., 2017). The evidence for the differential impact on IBs’ risk behaviour is missing. We are the first to analyse and compare the impact of capital requirements and market competition between different banking systems (Islamic and conventional) in the MENA region.

In line with previous research studies, we observe a positive association between capital requirements and credit risk level, which supports the regulatory hypothesis (Lee & Hsieh, 2013). However, this effect is significant only in the sample of CBs. A possible explanation is that Islamic banking institutions do not need to have an extensive capital base to cushion against losses since risks are absorbed by depositors (or equity holders), and losses are shared between the bank and the borrower. However, the analysis indicates that market power of banks does shape the credit risk behaviour of IBs. This is in line with Louati et al. (2015), who also find that market competition is positively associated with IBs’ credit risk (measured by deposit and loan changes). Since no prior evidence exists for the impact of capital requirements on bank insolvency risk, we test the hypothesis that the capital adequacy ratio is positively associated with the level of insolvency risk. We find strong support to this hypothesis when distance-to-default (or Z-score) is used to measure a bank’s insolvency risk. Thus, we provide evidence that banks tend to increase their risk level in response to the increase in regulatory pressure (e.g., increase in the minimum capital level of 8%).

We also investigate the effect of capital regulation on the bank’s risk-taking in different competitive conditions. Previous research studies failed to provide clear evidence of how market competition moderates the effect of capital requirements on banks’ risk-taking behaviour. We are the first, in this context, to analyse and compare this effect between CBs and IBs. We find a significant interaction effect with market power (measured by the Lerner index) in the sample of CBs. This tells us that in highly competitive markets, banks will be willing to pursue risky strategies when they face the need to raise their capitalization levels. We observed the opposite effect when banks operated in a less competitive market. Regarding the IBs’ behaviour, the evidence shows that market competitiveness has a limited impact on the relationship between capital adequacy ratio and credit risk, which means that IBs are still applying in their operations the theoretical models based on the prohibition of interest. This result is in line with previous research findings on banking systems in the MENA region as reported by Louati et al. (2015). The analysis for insolvency risk indicates a marginal effect of competition on a bank’s decision to increase or decrease the risk of its portfolio, which will depend on the expectations regarding the regulatory authority’s behaviour rather than the level of banking competition.

Finally, our analysis provides strong evidence in support of the hypothesis that there exists a non-linear relationship between a bank’s credit risk and market concentration (measured by the HHI). Our findings are in line with the predictions of the SCP paradigm, which postulates that a greater degree of concentration phases down the competition level and, consequently, increases a bank’s profitability. While this effect is similar across the two types of banking systems (CBs and IBs), insolvency risk analysis indicates a robust differential effect for IBs. Specifically, the results illustrate a classical U-shape relationship in the sample of IBs, which provides further support to the expectations of the SCP hypothesis. What is more, the positive association between capital requirements and bank risk is strongly moderated by market concentration only in the group of IBs. In general, these findings are in line with González et al. (2017), who confirm the importance of the market structure as an explanatory factor for financial stability and indicate that increased concentration should not always be associated with uncompetitive markets.

Managerial Implications

Our results have strong implications for regulators, policymakers and bank managers. First, the positive effect of capital requirements on bank credit risk is moderated by market power only in the group of CBs. With regard to IBs, regulatory capital requirements are less effective in requiring IBs to adjust their risk level according to the Basel Accords methodology. Furthermore, the behaviour of IBs seems to be strongly associated with the level of market competition and, therefore, the interest rates. This result calls into question the efficiency of their business model based on the prohibition of interest. In addition, banks operating in highly competitive markets will be forced to avoid risky strategies in response to an increase in the regulatory pressures (i.e., in the minimum capital requirements). Thus, regulators and policymakers in the MENA region may restrict the risk-taking behaviour of banks through stringent capital requirements; however, the majority of banks operating in the MENA region maintain capital levels above the minimum required one, and hence, they may not be constrained by regulatory pressure.

Second, our analysis shows that market concentration does not moderate the association between capital requirements and bank insolvency risk of conventional banking institutions. So, their decision to go with risky strategies will depend on the regulatory authority’s behaviour and not so much on the level of banking concentration. With regard to IBs, the regulatory capital effect will be more pronounced in concentrated markets. Therefore, regulatory authorities concerned with improving financial stability in the MENA region should proceed differently, when setting up their policies, depending on the level of concentration in the banking market in each country.

Our findings are even more important during the COVID-19 pandemic. On the one side, all concerned authorities and regulators should take appropriate measures to sustain the economy by any means rather than accelerating the economic growth. Therefore, regulators responsible for the stability of the banking sector should require a more disciplined approach in banks’ lending decisions and building a sufficient capital conservation buffer to limit the impact of downside risk from depletion of capital buffers, which can be significant during the pandemic. On the other side, this necessitates a more responsible behaviour on behalf of the bank managers when developing their risky strategies. These recommendations are in line with the recent findings for the impact of the COIVD-19 pandemic on a bank’s performance as reported by Demirgüc-Kunt et al. (2020). Their results show that the impact of prudential measures (which deal with the temporary relaxation of regulatory and supervisory requirements, including capital buffers) appeared to be limited, except in countries that are not part of the Basel Committee, where such policy initiatives have a negative impact on bank returns. Moreover, during the follow-up stabilization brought about by these different policy initiatives, banks with higher profitability and healthier balance sheets are found to have performed better. Therefore, our recommendation to bank managers is to increase their stability by expanding beyond the traditional lending sources of income (e.g., through non-interest revenue sources) as part of a beneficial portfolio diversification strategy to be used during the COVID-19 pandemic.

Supplemental Material

Supplemental material for this article is available online.

Supplemental Material for Capital Regulation and Market Competition in the MENA Region: Policy Implications for Banking Sector Stability During COVID-19 Pandemic by Miroslav Mateev, Syed Moudud-Ul-Huq and Tarek Nasr, in Global Business Review

Footnotes

Limitations/Future Research

The aforementioned policy implications raise a number of issues that need further research. For example, using an extended period of time, a future study shall focus on testing the effect of a bank’s risk-taking and market competition on the capitalization levels of banks in the MENA countries, and more specifically, if during the COVID-19 pandemic, banks raise their capitalization levels in response to an increased financial instability.

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.