Abstract

This article empirically explores the association between accrual earnings management (AEM) and real earnings management (REM) using a sample of 150 non-financial listed firms for the period 2008–2017. The AEM is measured through the original Jones model (1991) and Dechow et al. (1995) model, whereas REM is measured through Roychowdhury’s (2006) model. For empirical analysis, the study estimates simultaneous equations by using ordinary least square (OLS) and the two-stage least square techniques (2SLS). The result of the analysis indicates that there is a negative and significant relationship between AEM and REM, suggesting that Pakistani listed firms employ AEM and REM as a substitute to achieve earnings targets. The results of the study are valuable for auditors and regulators to contemplate, govern and legalize suitable guidelines to enhance the transparency in the financial reporting quality.

Keywords

Introduction

Schipper (1989) argues that earnings manipulation is an intended alteration in the company’s financial reports, in order to attain private paybacks. Earnings management occurs when managers/management alters and smoothen companies’ earnings, using their own discretion for enhancing the firm’s financial outlook, and deceive stakeholders about the firm’s performance (Healy & Wahlen, 1999). The financial reporting will be valuable if the information enclosed in financial reporting can be used as a reference to forecast the state of the company in the future. To achieve the earnings target set by the management, or forecasted by the analyst or by other stakeholders, the managers use their discretion to alter the financial reports—referred to as earnings management. A single attribute that contributed to the decline of the world equity market in the early 2000s was the lack of transparency in the accounting information (Gaio, 2010). Mulford and Comiskey (2002) termed earnings management as vigorous management of a company’s financial reports towards the achievement of predetermined management or analyst targets. However, all these definitions have one thing in common about the occurrence of earnings management, that is, managers alter the earnings by practising their own judgement to gain certain benefits and mask the true financial information which ultimately pollutes the financial reporting quality. Kałdoński et al. (2019) document that managers have two options to manipulate financial data. The first option is to manipulate company financial data through discretionary accruals without affecting cash flows—‘accrual earnings management’ (AEM). The second option is to inflate company earnings by decreasing research and development (R&D) expenses, selling, general and administrative (SG&A) expenses and increasing sales by offering discounts in prices that ultimately affect the cash flows and earnings of the firm—‘real earnings management’ (REM). Due to its direct impact on firm performance and value, REM is regarded as more dangerous compared to AEM (Bedertscher, 2011; Sakaki et al., 2017).

Managers are shifting towards REM due to the fact that it cannot easily be detected by the external auditors (Shayan-Nia et al., 2017). Doukakis (2014) argues that the earnings manipulation techniques depend on scrutiny through auditors. This means that managers also look for the opportunity to employ earnings management techniques to mask the firm’s performance that cannot be detected by external auditors. Shayan-Nia et al. (2017) argue that it is difficult to separate REM from the normal business activities, so managers are more comfortable in manipulating earnings through real activities and without any regulatory consequences from the regulatory authorities and auditors. Most of the authors document that firms employ both techniques to alter reported earnings and achieve earnings targets. Pincus and Rajgopal (2002) examined the association between AEM and REM in oil and gas companies and reported that manager’s substitute both earnings techniques to achieve the desired earnings target. The substitution among AEM and REM has been reported in previous studies (Chi et al., 2012; Zang, 2012; Zhu et al., 2015). According to Zhu et al. (2015), if firms were audited by high-quality audit firms, then both the earnings management behaviour would reduce, as they document a negative relationship between AEM and REM. However, Chi et al. (2011) argue that the cost associated with AEM includes legal actions and high penalties against a firm and that is why managers have shifted to REM.

However, there are some studies that indicate that managers manipulate earnings by employing both AEM and REM techniques simultaneously to achieve earnings targets. Sellami (2016) finds that French firms conduct manipulation of earnings by using both the techniques of earnings manipulation simultaneously. Chen et al. (2012) document that Taiwanese firms employ both techniques jointly as a complement to each other. Das et al. (2017) examine the potential substitutions among Indian firms and report complementary association between REM and AEM in Indian firms.

With respect to earnings management in Pakistan, Shaikh et al. (2019) examine the impact of pyramid ownership structure on REM and indicate that managers manipulate earnings through REM to gain short-term performance and earnings target. Similarly, Tabassum et al. (2015) study the impact of REM on firm performance and indicate that REM practices reduce the firm’s future performance. Shahzad et al. (2017) indicate that family firms in Pakistan are involved in earnings manipulation through REM.

In this context, this article presents a new approach to analyse earnings management strategies. Since accounting and REM are jointly determined, our approach is based on a simultaneous equations model.

Most of the previous studies that examined the complementary and substitution relationship between AEM and REM were conducted in the developed economies, despite the fact that earnings management practices are more prevalent in developing economies as compared to the developed economies (Agarwal & Chatterjee, 2015).

Despite the increasing interest of these two earnings management strategies, prior research has failed to investigate their interaction while measuring REM and AEM as a whole (aggregate). Indeed, the major studies to be investigated in this field measure REM and AEM separately, using only single measure.

We try to fill these gaps in the literature by analysing the relationships between accounting and REM measured jointly. The most important advantage of this method is that it reduces the measurement bias in quantification of AEM and REM. The additional advantage of using this method is that it results in identifying a firm’s decision to adopt either strategies or a single one. This investigation is useful to understand the firm’s behaviour in different contexts.

In light of the earlier discussion, the aim of this article is threefold. First, it quantifies AEM and REM based on the sample of 150 listed Pakistani firms belonging to 14 different sectors. Second, we refine the concept of the potential substitution between AEM and REM at firm level by employing the comprehensive measure (aggregate measure) of both the earnings management strategies instead of employing single measures, in order to reduce the measurement bias. Third, it examines whether Pakistani companies choose a substitute relationship over a complementary relationship between AEM and REM or vice versa. Pakistan provides a particularly interesting context, which is different from American and European ones. Indeed, Pakistan is an emerging country that is known for its lack of transparency, weak investor protection, low voluntary disclosure level and developing capital market (Arshad & Javid, 2014). To our knowledge, our study is the first one to investigate the relationship between these two forms of earnings management by focusing on the Pakistani specificities, which remained unexplored.

There are two main contributions of this article. First, it contributes to the limited literature of earnings management in the Pakistani context. Second, the relationship between the firm’s characteristics and managers’ choice to complement or substitute AEM and REM is a new dimension and not explored in the Pakistani context.

Thus, the aim of this study is to empirically examine that firms in Pakistan employ these two techniques jointly or as a substitute for earnings manipulation. To examine the association between AEM and REM, the study employs the two-stage least square (2SLS) method to eradicate the issue of endogeneity.

Using simultaneous equation system, the study concludes that firms in Pakistan employ AEM and REM as a substitute to achieve the earnings target. The study is useful in assessing the earnings management behaviour in the Pakistani firms and particularly beneficial for auditors and regulators to contemplate, govern and legalize suitable guidelines to enhance the transparency in the financial reporting quality.

The rest of the study is organized as follows. The second section presents the relevant literature and development of the hypothesis. The third section highlights the objective and rationale of the study. The fourth section explains the data and methodology. The fifth section provides an analysis of empirical results, and the final section concludes along with managerial implication of the study.

Literature and Hypothesis Development

Types of Earnings Management

McVay (2006) argues that the immense collection of literature classifies the techniques of managing earnings into two types. (a) Accrual-based earnings management that is referred to changing the estimates and accounting policies (b) Real activities–based earnings management that is referred to as real operating decisions that have direct cash flow consequences.

Accrual-based Earnings Management

International Accounting Standard Board (IASB) due to the globalization of businesses has introduced accrual basis accounting. Cash basis accounting has turned out to be inefficient in measuring a firm’s performance in a continuous process. The cash basis accounting has been banned by International Financial Reporting Standards (IFRS). The firm’s earnings and cash flow difference represent accruals. On an accrual basis, the firm recognizes the credit sale regardless of whether the firm received the cash or not. So, managers apply these discretions (as legally allowed), by recognizing revenues before they are earned or delaying the recognition of expenses which have been incurred, which results in accruals. Kothari et al. (2016) argue that managers alter the financial data by using this discretion to adjust the reported earnings without any cash flow consequences— termed as AEM. Within the limits of regulations, managers use their discretion by bringing future earnings into current periods by Jacking up of revenues and slowing down of expenses. This creates what is called discretionary accruals. Aljifri (2007) argues that managers use their discretions through two approaches—one is related to expenses and revenue recognition timing, which is easy to adopt and difficult to be easily spotted by the external auditors. The second choice is to switch between costing methods (from FIFO to LIFO) or average cost methods. The main advantage of first in first out (FIFO) in the period of increasing sales is that the profit is maximized (reduced sales cost) as compared to LIFO. Managers use both costing methods for earnings manipulation. Thus, the main motive behind using the different costing methods is solely for the purpose to exaggerate the company earnings, the value of assets, and minimize the company expenses and liabilities.

Real Activities-based Earnings Management

When firms take real operating decisions intentionally that affect the firm’s cash flow and earnings is stated as ‘real activities–based earnings management or manipulation’. When managers make operating choices deliberately to deviate from the optimum business operations for the purpose of altering the reported earnings that directly affect the firm’s cash flow is termed as ‘REM’. Through REM, the managers manipulate earnings by offering more sales discounts or offering very favourable credit conditions to the customer to increase sales. In addition, to reduce the overall expenses in the income statement, the managers reduce discretionary expenses like R&D expenses and SG&A expenses opportunistically (Dechow & Skinner, 2000). As reducing R&D expenditure, sales decisions and production volumes are directly under the influence of executives and managers, they can easily control and influence such real activities to manipulate earnings (Badertschter, 2011). According to Zang (2012), the managers prefer the REM as compared to AEM because the latter is easily detected by the auditors. Cohen and Zarowin (2010) argue that in REM, the managers deviate from the normal business activities that have severe economic consequences. Due to its direct impact on the firm’s performance and value, REM is regarded as more dangerous compared to AEM (Bedertscher, 2011; Sakaki et al., 2017). Thus, the main intention behind the REM is that it is purposeful in nature and have serious consequences on the actual cash flow of the firm.

Hypothesis Development

Previous research discloses that most of firms shift towards REM (Cohen & Zarowin, 2010; Kuo et al., 2014; Zang, 2012; Zhu et al., 2015). Two main reasons are documented in the literature for the switch from AEM to REM. The first reason is that AEM alone is risky. If there is a gap between the reported earnings and desired benchmark after employing discretionary accruals techniques, then the managers are left with no choice but to switch to REM to manipulate earnings (Cohen & Zarowin, 2010; Roychowdhury, 2006). The second reason is that AEM is under the severe inspection of regulators (auditors) as compared to real decisions about pricing and discretionary expenses (Graham et al., 2005; Shayan-Nia et al., 2017). Cohen et al. (2008) indicate that earnings management behaviour has drastically changed after the induction of Sarbanes-Oxley Act (SOX) in 2002, and the level of REM significantly increased as compared to the level of AEM. Due to strict regulatory constraints on the conduct of discretionary accruals, managers use real activities to manage earnings like reducing sales prices to avoid losses and decreases in earnings (Jackson & Wilcox, 2000) and selling assets and marketable securities to achieve target earnings (Herrmann et al., 2003). Regarding the relationship between the potential substitutions, Zhu et al. (2015) indicate that both techniques are being employed as a substitute by the Chinese firms to achieve the earnings target. However, the conduct of earnings manipulation is reduced when audited by the Big 4 audit firms. They further add that top management easily employ REM techniques to attain the earnings target as the real activities–based decisions are under their discretion. In addition, they argue that firms switch to REM if they have reported higher accruals in the previous years. Barton (2001) examined the earnings management behaviour in the Fortune 500 firms, using a simultaneous equation and found a negative association between AEM and derivatives, which implies that managers substitute earnings management techniques to achieve the desired earnings level. Chi et al. (2011) advocate that managers prefer REM (substitute AEM with REM) if audited by high-quality auditors. While studying Chinese firms, Zhu et al. (2015) found that the choice of the techniques that a firm wants to use purely depends on the cost associated with using it and the firm’s capacity. They further add that the cost associated with AEM includes legal actions against the firm and high penalties. The authors argue that accrual earnings manipulation alone is risky and it is most probable that it draws the regulators’ and auditors’ attention due to which most of the managers shift from AEM to REM. Cheng et al. (2013) argue that firms prefer to report high discretionary accruals to enhance short-term performance compared to REM due to the severe economic consequences of REM.

Zang (2012) argues that both techniques are costly in terms of reputation and firm value, but the managers still manipulate earnings using either technique, especially in a situation where the use of one technique is more constrained as compared to another.

Moreover, Ge and Kim (2014) and Cohen et al. (2008) report that the implementation of SOX, which has enhanced the audit quality and other corporate governance scrutiny, has reduced the level of AEM. They confirmed that managers substitute the earnings management strategies to achieve the desired results.

Enomoto et al. (2015) examine the earnings management strategies across 38 countries from Asia, Continental Europe, and Anglo-American countries. Their research indicates that Asian and Continental European countries employ AEM strategies as compared to Anglo-American countries. Anglo-American countries employ real earnings manipulation to manipulate earnings. Doukakis (2014) argues that the choice of earnings management varies according to auditors’ scrutiny and regulatory environment of the country. According to Shayan-Nia et al. (2017), managers are shifting towards REM, as real earnings manipulation is hard to identify by auditors and subject to less scrutiny. Nnadi et al. (2015) study the impact of the regulatory environment on earnings management strategies in firms across Hong Kong and China. The research indicates that the quality of financial reports is highly influenced by different regulations in China and Hong Kong. The research further indicates that firms in Hong Kong engage more with REM, while Chinese firms prefer accounting discretion rather than REM. Wang (2014) argues that countries that have low legal protection, high corruption and large unofficial economy encourage managers to make abnormal operating decisions for opportunistic reasons.

On the other hand, Achleitner et al. (2014) examine the earnings management behaviour among the family and non-family German firms and conclude that German family firms prefer to report higher discretionary accruals as compared to REM. They report a negative association between AEM and REM. Elleuch Hamza and Kortas (2018) examine the association between AEM measured through discretionary accruals and REM measured through sales manipulation and discretionary expenses in Tunisian firms. The results show that managers prefer to substitute AEM with discretionary expenses but employ sales manipulation and discretionary expenses simultaneously. Khunkaew and Qingxiang (2019) have examined the association between AEM and REM among Thai firms for the period 2014–2017 by employing simultaneous equations and have concluded that Thai firms use AEM and REM as the substitution method to achieve desired earnings targets.

In the support of complementary relationship, Sellami (2016) finds that after the implementation of IFRS in France, most French firms conduct earnings manipulation by using both the techniques of earnings manipulation simultaneously. Chen et al. (2012) document that Taiwanese firms employ both techniques jointly as a complement to each other. They further add that due to weak investors’ protection, low litigation costs and low disclosure requirements, firms use both earnings management techniques for the purpose of manipulation. Matsuura (2008) examines the association between AEM and REM among Japanese firms and reports that there is a complementary relationship between AEM and REM. Hashemi and Rabiee (2011) examine the association between AEM and REM in firms listed on the Tehran Stock Exchange and indicate a complementary relationship between AEM and REM. Das et al. (2017) examine the potential substitutions among Indian firms and report complementary association between REM and AEM in Indian firms.

Most of the previous literature demonstrated evidence that AEM has a significant association with REM, as both the substitution and complementary methods, in a different country, such as China, Hong Kong, Japan, Taiwan, Thailand, Vietnam, India, Germany, Europe and America (Achleitner et al., 2014; Enomoto et al., 2015; Das et al., 2017; Matsuura, 2008; Zhu et al., 2015). In Pakistan, Tabassum et al. (2015) indicate that firms manipulate earnings through sales (REM) to report high earnings that negatively impact the firm’s performance. Shahzad et al. (2017) confirmed that family-owned firms manipulate earnings through REM and avoid AEM for reporting higher earnings. However, there is still a lack of evidence that clearly reflects the relationship between AEM and REM in Pakistan. This is the first study that empirically examines the issue of potential substitution among AEM and REM in Pakistan. Due to the absence of empirical literature in Pakistan, this research suggests a non-directional hypothesis.

The Objectives of the Study

The objective of this study is to present clear evidence of the association between AEM and REM in Pakistan by investigating 150 listed firms from 14 different sectors for the period 2008–2017. This study empirically examines that firms in Pakistan employ these two techniques jointly or as a substitute for earnings manipulation. To examine the association between AEM and REM, the study employs the 2SLS method to eradicate the issue of endogeneity.

The Rationale of the Study

Most of the previous studies provide evidence that firms employ both earnings management techniques to achieve the desired level of earnings (Das et al., 2017; Enomoto et al., 2015; Zhu et al., 2015). It is obvious that examining one earnings management strategy in isolation cannot explain the overall impact of earnings management, and it can provide misleading results (Zang, 2012). According to Agarwal and Chatterjee (2015), despite the fact that earnings management practices are more prevalent in the developing economies as compared to developed economies, most of the studies examined the complementary and substitution relationships in the developed economies, and less attention has been devoted to the developing economies. Despite the presence of REM in the Pakistani firms (Shahzad et al., 2017; Tabassum et al., 2015), there is no evidence of the association (complementary or substitution) among AEM and REM in Pakistan with low investor protection and weak regulatory environment.

Data and Methodology

Data Source and Sample Frame

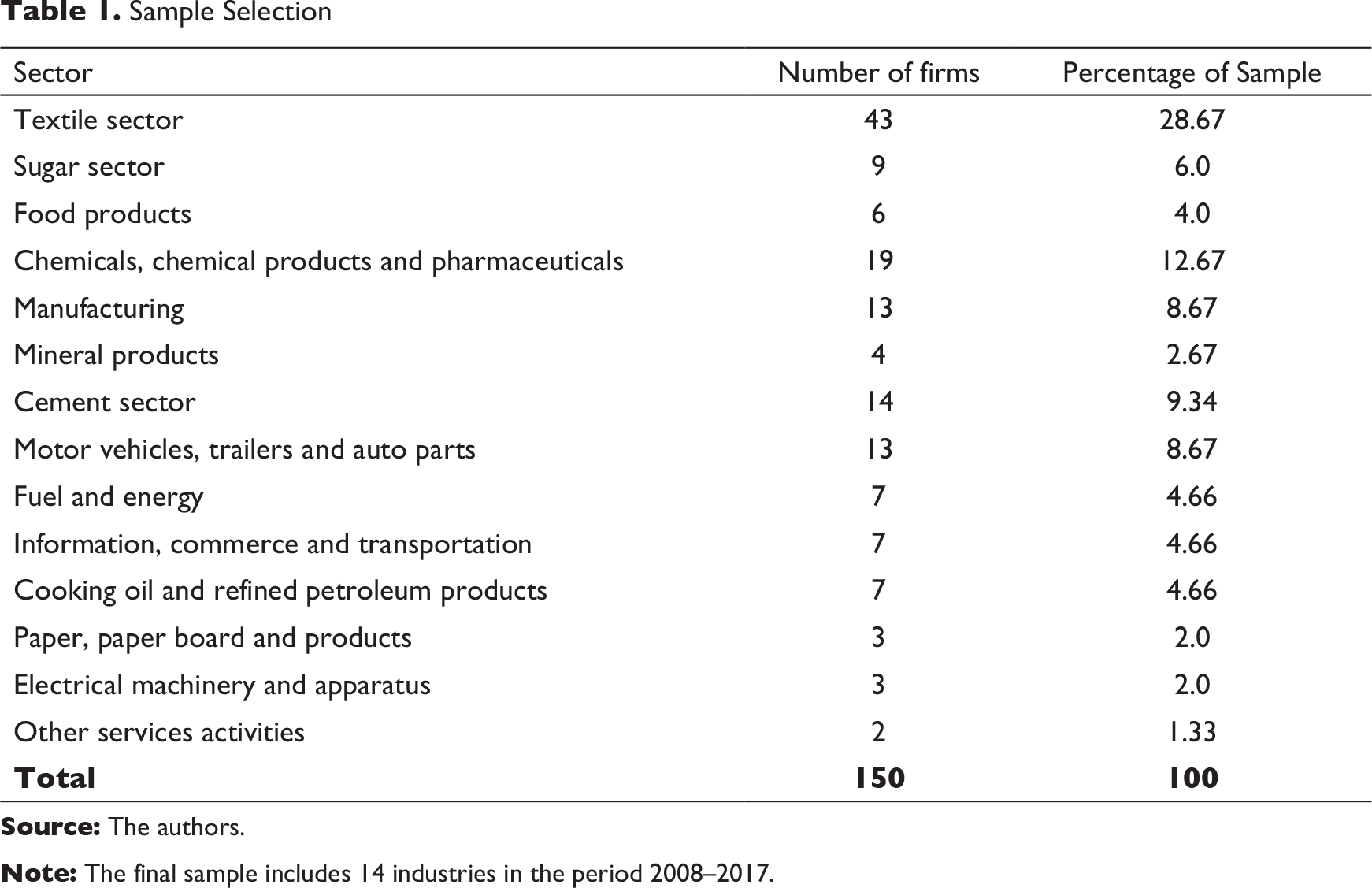

To examine the relationship between AEM and REM in Pakistani firms listed on the Pakistan Stock Exchange (PSX), data are collected from the annual reports available on the company website from 2008 to 2017. The data were collected from 2008 due to the reason that in Pakistan, key changes in accounting standards took place between 2005 and 2006 (Rehman et al., 2014). According to Ma et al. (2015), using data after changes in the accounting standards will bring uniformity in dealing with the accounting variables used in the empirical analysis. The study includes all companies registered on the PSX. Firms from financial sectors are not included in the sample due to their unique and complex characteristics form other sectors (Davidson et al., 2005). According to Türegün (2016), the firms of the financial sector have different earnings manipulation strategies, and that is why the financial sector was excluded from the sample. Consequently, the ultimate sample contains 150 firms. Table 1 reports the sector-wise distribution of the final sample.

Variable Definition and Measurement

Earnings Manipulation through Real Activities

where for firm i in period t,

The first model relates to the management offering discount or more favourable credit terms to accolade sales by declining margins for any additional sales. By doing so, the firm earnings in the current period increase as the additional sales are booked. The net effect would be a lower CFO for the current period. Thus, the residual obtained from the model is the abnormal cash flow from operation (ABCFO). Smaller ABCFO indicates more REM (Shayan-Nia et al., 2017). We multiply ABCFO with −1 so that high value represents higher earnings manipulation. The second model pertains simply to reducing discretionary expenses to upsurge the current period earnings. Therefore residuals (deviation from normal) obtained from the model are abnormal discretionary expenses (ABDISEXP). ‘Discretionary expenses of a company i for year t, estimated as the sum of research and development expense, advertising expense and selling, general and administrative expenses’. The expenses are considered as nil if not reported in the annual reports (Shayan-Nia, et al., 2017). Following (Cohen & Zarowin 2010; Shayan-Nia et al., 2017; Mellado & Saona, 2018; Zang, 2012). We multiply ABDISEXP with -1 so that higher value represents higher REM.

We use aggregate REM as a measure of real earnings management to reduce the measuring bias by adding ABCFO and ABDISEX, as both these measures have a similar directional association. Following Badertscher (2011) and Kałdoński et al. (2019), higher ABCFO and ABDISEX indicate higher levels of REM. The aggregate measure is calculated as REM = ABCFO + ABDISEXP (Cohen et al., 2011; Gunny, 2010).

Earning Management Through Accruals

According to Hussain and Ibrahim (2012), accounting standards offer a wide range of flexibility for the firm’s management to use the judgement to maximize the worth of financial reports presented to stakeholders. Degeorge et al. (1999) argue that this discretion of management also creates opportunities for earnings management. Managers usually extend their discretion to the level of exploitation and may shift earnings between periods, which completely undermine the firm’s actual performance. This management discretion about the accounting information is termed as ‘Discretionary Accruals’ in accounting literature. Following Andre et al. (2015) and Lemma et al. (2018), the current research uses discretionary accruals as a measure of AEM. Two popular models are chosen from the literature to estimate the AEM.

where

To avoid the problem of heteroskedasticity, all the variables are divided by lagged total assets. The prediction from the OLS estimation represents the non-discretionary accruals, while the residual is discretionary accruals. Following Chen et al. (2012), the absolute value of residual is used as a measure of earnings management. So, the higher value represents higher earnings manipulation.

where

For the control of heteroscedasticity, all the variables are divided by the lagged total assets to control for heteroscedasticity. The model is estimated in its cross-sectional version for each year and firm. This model has attained extensive support in the accounting literature due to detecting cases of revenue manipulation (Aljifri, 2007). The prediction from the OLS estimation represents the non-discretionary accruals, while the residual is discretionary accrual. The absolute value of residual is used as a measure of earnings management. So, the higher value represents higher earnings manipulation. The absolute value is the best measure of the level to which firms practise accruals to accomplish earnings in the absence of a specific direction (Reynolds & Francis, 2000).

Previous literature documents two possible methods to estimate total accruals. These methods are used by the AEM models. One method follows the balance sheet approach, while the other is a cash flow approach. Kothari et al. (2005) claim that there is embedded error in calculating total accruals through the balance sheet approach, which lessens the power to detect earnings manipulation and produce deceptive conclusions about earnings management. The best way to measure the total accruals is through the cash flow method that produces efficient results. Similarly, Collins and Hribar (2000) argue that the balance sheet approach increases the measurement error in the estimate of total accrual and ultimately in discretionary accruals. Therefore, following previous studies, we use the cash flow method to compute total accruals.

This study employs two most popular discretionary accrual models (Jones model [1991] and modified Jones model [1995]) that are extensively used in the earnings management and are identified as the most common models in the literature that have significant accuracy in capturing the earnings management behaviour (Doukakis, 2014; Jha, 2013). Similarly, Swai (2016) and Doukakis (2014) argue that both these models are considered as the more significant and powerful tests of earnings manipulation through discretionary accruals.

We use an aggregate measure by standardizing these two proxies and taking the average of the two measures for measuring AEM to reduce the measurement bias.

Control Variables

Firm Size

It is measured as the natural log of total assets. Larger firms are mostly concerned about their reputation, and they have a strong internal control system, so the chances of earnings management are very low in large firms (Alzoubi, 2016; Habib et al., 2013). On the other hand, it is also documented in the literature that large-sized firms deploy earnings management techniques to achieve earnings targets and meet analyst’s expectations (Chen et al., 2010).

Firm Growth

A firm’s growth rate is defined as growth in a firm’s total assets over the previous year. A firm’s growth is used as a second control variable. High-growth firms usually have high audit quality. The high-growth firms have a strong internal control system due to which they are less involved in earnings manipulation. Jaggi et al. (2009) indicate that high-growth firms do not manipulate financial reports. However, González and García-Meca (2014) and Sharma and Kuang (2013) document that high-growth firms conduct a higher magnitude of earnings manipulation as compared to low-growth firms. They argue that to maintain steady earnings, high-growth firms engage in earnings manipulations.

Firm Age

Firm age is measured in years. The main purpose of including a firm’s age in the model is to control the variation that ascends in the reporting quality with the firm’s different life cycles. Wang (2014) documents that mature firms manipulate earnings to attract investment and depict a positive signal to the market.

Leverage

Leverage is measured as the proportion of total debt to total assets. High-levered firms conduct higher magnitude of earnings manipulation to avoid debt covenant violations (Gombola et al., 2016), whereas Esadinia et al. (2014) conclude that earnings manipulation is likely to be less in high-levered firms due to strict audit control, which limits the managers to manipulate earnings.

Audit Quality

BIG 4 represents audit quality and is coded as one if the audit is done by the BIG 4 audit companies, otherwise zero. The BIG 4 auditors are most likely to point out the anomalies and identifying errors in the financial statement (Lisic et al., 2011). The BIG 4 controls the opportunistic behaviour of managers and restricts firms from earnings manipulation (Gaynor et al., 2016).

Profitability

For the profitability, the return on asset (ROA) is included in the model. ROA is measured as net income over total assets. Chen et al. (2007) argue that companies with low profitability have low financial reporting quality as compared to highly profitable companies.

Lagged AEM (AEMt−1)

Sample Selection

The Regression Model

As AEM and REM are two endogenous variables, there is a chance of an endogeneity problem when using OLS in the model of the association between AEM and REM.

To address endogeneity of the earnings management activities, we believe that a simultaneous equations model is the best estimation method where the two endogenous variables are accounting and REM.

According to Elleuch Hamza and Kortas (2018), in the presence of endogeneity, the simultaneous equation model is the superior estimation method and 2SLS is the best econometric technique to yield unbiased estimates. Further, the study employs the Hausman test for endogeneity proposed by Davidson and Mackinnon (1993) to identify the endogenous problem between AEM and REM. The result of the test validates the significance of the endogeneity test, and this study employs the model (SEM) adopted by the previous studies (Das et al., 2017; Elleuch Hamza & Kortas, 2018) to test the relationship between AEM and REM, and testing the model by following 2SLS as follow:

Analysis and Discussion

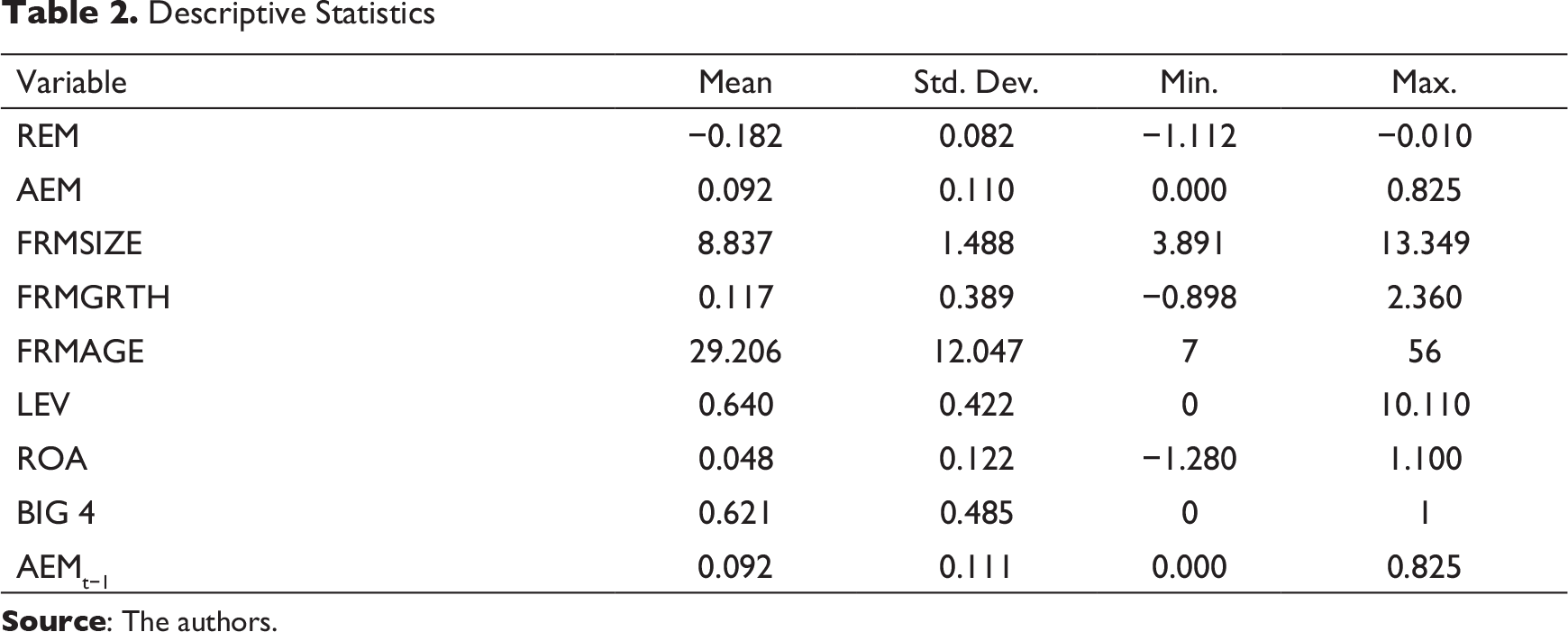

The summary statistics of the variables included in the model are presented in Table 2. The average value of REM is −0.182. This indicates that firms in Pakistan manage to offer discounts or more favourable credit terms to accolade sales and reduce R&D expenses. Murya (2010) argues that most of the time, companies manipulate earnings downward when their manipulated earnings are higher than the forecasted earnings, so they defer these earnings for the forthcoming period. The mean of AEM is 0.092, while the minimum value reaches 0. Similar results are also reported by Kao and Chen (2004), indicating that the mean of discretionary accrual is 0.09. Similarly, Alghamdi (2012) finds a similar value of 0.10 for Jordanian firms. Othman and Zeghal (2006) find that the mean value of discretionary accruals among Canadian and French firms is closer to 0.09. However, in developing countries like Malaysia, Rehman and Ali (2006) find a mean value of discretionary accrual close to 0.07.

Descriptive Statistics

Correlation

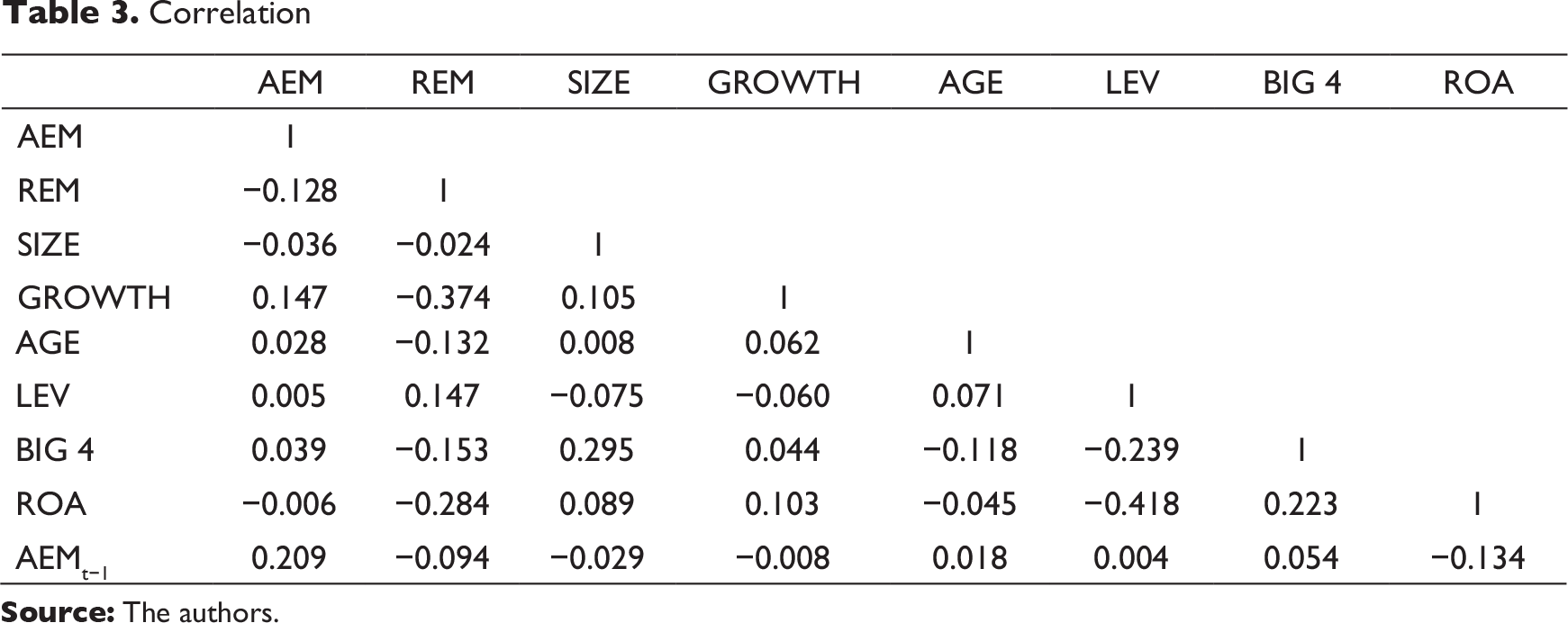

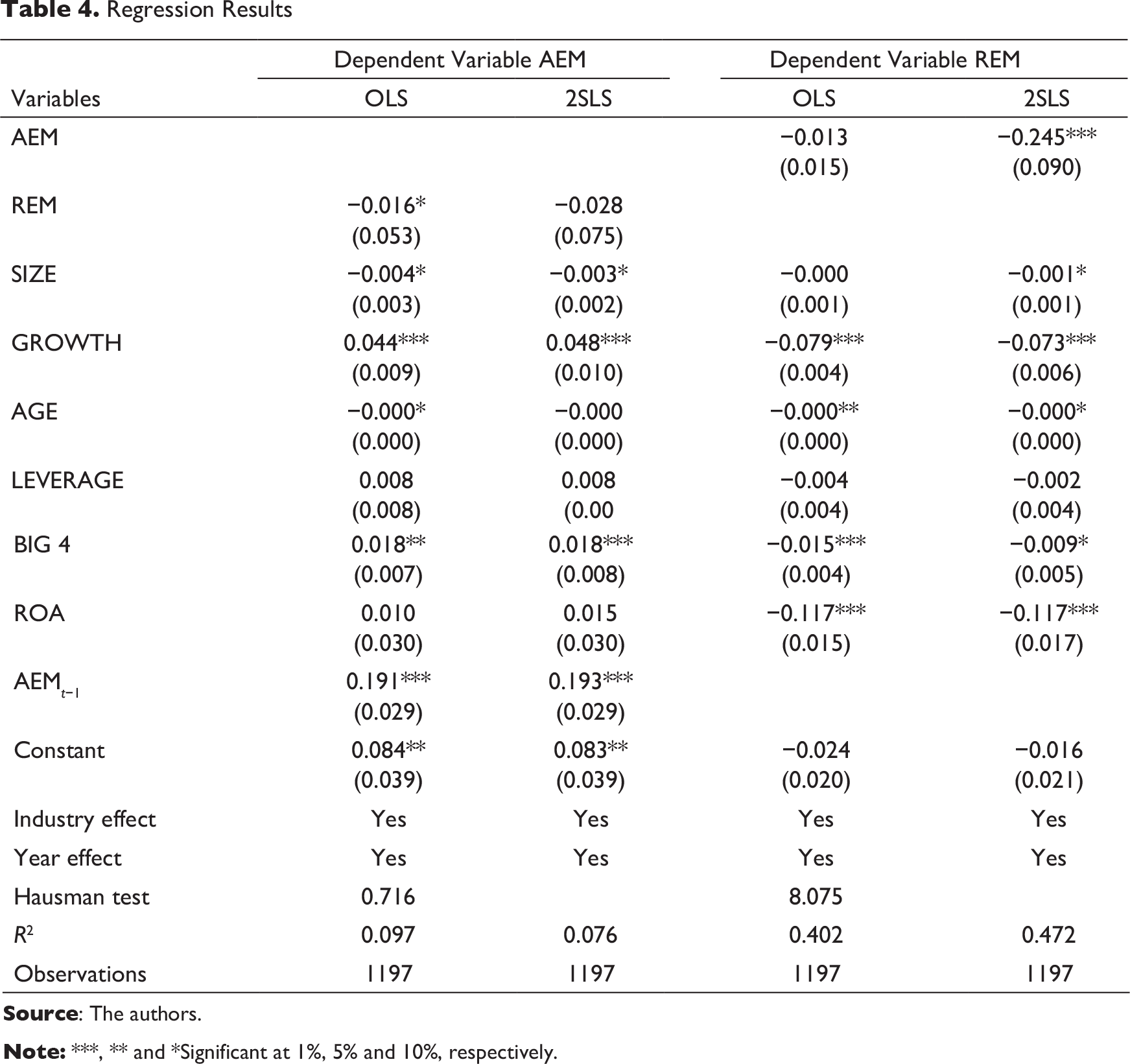

Following the studies of Das et al. (2017) and Elleuch Hamza and Kortas (2018), the study employs the simultaneous equations to examine the relationship between the AEM and REM. To address the issue of endogeneity in the relationship between AEM and REM, we employ the Hausman test. The result of the Hausman test overruled the chance of being exogenous of REM in the AEM model, as the coefficient obtained is 8.07 and statistically significant; however, the exogeneity of REM is recognized in the AEM model, as the value of the Hausman test is very low and statistically insignificant. The result of the Hausman test indicates OLS techniques are a suitable technique in the AEM model, whereas the REM model proffers the use of the 2SLS technique for the empirical analyses. Table 4 reports the resulting AEM and REM of both the techniques used in the study. The result indicates that there is a negative relationship between AEM and REM as the coefficients in the AEM model of −0.016 and −0.028 through the OLS and 2SLS, respectively, while the coefficients in REM are −0.013 and −0.245, respectively.

Regression Results

Regarding the control variables, a firm’s size is negatively significant related to AEM and REM. This indicates that smaller firms in Pakistan tend to manipulate earnings through discretionary accruals as well as through real activities. The possible reason might be that large firms are diligently observed and analysed by outsiders so it is hard for them to manipulate earnings. The firm’s age is significantly negatively associated with both AEM and REM, indicating that mature firms have a lower level of earnings management behaviour in both the AEM and REM approaches. The relationship between firm’s growth and AEM is positive and significant, suggesting that high-growth firms in Pakistan conduct earnings management through discretionary accruals. Firm’s growth exhibits a negative association with REM. Surprisingly, the Big 4 is positive and significantly associated with AEM and negatively significantly related to REM, indicating that the Big 4 auditors fail to control the conduct of discretionary accruals. The result suggests that the Big 4 auditors fail to control earnings management through discretionary accruals as compared to REM.

Conclusion and Managerial Implications

The study aimed to investigate the relationship between AEM and REM in Pakistan, where the legal system is very weak with low disclosure requirement. The study examines 150 non-financial firms from 14 industries listed on the PSE. The AEM is measured through the Jones model (1991) and modified Jones model (1995), whereas REM is measured through Roychowdhury’s (2006) model. The study employs the aggregate measures of AEM and REM to address the issue of measurement bias. The study estimates simultaneous equations and presents the empirical relationship between AEM and REM by employing the two econometric techniques, viz. OLS and 2SLS. The empirical results suggest that managers of Pakistani firms employ AEM and REM as a substitution method to manipulate earnings and achieve earnings targets. The empirical results also indicate that there is a negative significant association between AEM and REM. The results are similar to the findings of Chi et al. (2011) and Zhu et al. (2015).

The findings of the study have significant implications for regulators, auditors and policymakers, as they play a significant part in monitoring the occurrence of earnings manipulation and boost the financial reporting quality. The findings have implications for policymakers and regulators to enhance the disclosure requirement and transparency in financial transactions.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared the following potential conflicts of interest with respect to the research, authorship and/or publication of this article: The author declares that there is no conflict of interest.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: The author declares that he has not received any funding or financial support to write this article.