Abstract

Country risk can significantly impact the flow of investment within a country. The bond market is particularly vulnerable to country risk shocks, as such risks affect government borrowing and lending rates. This article analysed the effect of country risk components on the South African (SA) bond market performance and stability under different market regimes. A sample period of monthly data, spanning January 1995 to December 2018, was selected to reflect South Africa’s shift towards democracy (post 1994). Two-stage Markov switching models (MSMs) were utilized to test the effect of country risk components on bond market return and yield spreads. First, the study showed that both returns and spread undergo a longer bullish trend. Second, the effect of country risks on bond returns was shown to be significant only in the bear regime in which bond returns increase with a change in political and economic risks and decrease with a change in financial risk. Third, the effect of the country risk components on yield spreads was shown to be not significant in any regime. We concluded that the response of bond market performance to country risk shocks is influenced by market cycles, and we provide evidence to support the adaptive market hypothesis (AMH) in the SA bond market.

Introduction

The South African (SA) debt market is the largest in Africa, both by market capitalization and liquidity. It is also one of the most liquid emerging bond markets in the world (Liu, 2013). The bond market occupies a key role in the SA economy by providing a platform through which projects serving a variety of purposes may be financed. Government bonds, which account for over 50 per cent of all debt instruments traded on the bond exchange, are particularly relevant for financing SA infrastructure development, among other functions. Government-issued bonds include, but are not limited to, fixed rate, zero-coupon, inflation-linked, local currency and foreign currency bonds (Johannesburg Stock Exchange [JSE], 2017). Country-specific cost of borrowing is commonly determined by the yield spread on sovereign bonds, defined as the difference in the quoted rates of return on two different investments, usually of differing credit quality or terms to maturity (Rowland & Torres, 2004). Sovereign yield spreads are a key indicator of the composite risk associated with investing in a particular country, with higher spreads generally reflecting lower creditworthiness and a higher risk of default. Consequently, the yield spread is a measure of bond market stability. Because an increase in yield spread (or risk premium) decreases the present value of future cash flows to bond holders, higher spreads could have serious implications for both foreign and domestic investments in the country concerned. For example, Clark and Kassimatis (2009) found that country default risk decreases foreign direct investment when the probability of default increases at an increasing rate.

Within the SA context, the components of country risk 1 have had a significant impact on domestic financial markets (Bloomberg, 2017). Papendorp and Packirisamy (2015) noted that political unrest, protest action, crime and allegations of corruption within the country culminated in South Africa narrowly avoiding a sovereign debt downgrade to junk status in 2016. Other key examples in this case may be drawn from the announcement (and implementation thereof) of a cabinet reshuffle during December 2015 and during March 2017. In this regard, such actions have had direct implications for composite country risk (through the respective sub-risk indices). The resultant impacts upon the country have been noted in a depreciating rand against the dollar, fall in the Financial Times Stock Exchange (FTSE)/JSE Africa Banks Index by approximately 7.7 per cent since 2015 and rising fiscal concerns, with regard to investment-grade credit ratings, all of which cumulated in an expected sovereign downgrade (Bloomberg, 2017; BusinessTech, 2017). Swift market reaction was manifested by an increase in bond yields of the SA bond market. Such rising bond yields were further expected to constitute investment flows into the bond market (The Financial Times, 2017). This was confirmed by Muzindutsi and Nhlapho (2017) and Nhlapho and Muzindutsi (2020), who found that the components of country risk have a negative effect on credit extension and financial markets in South Africa. Additionally, a study by Vengesai and Muzindutsi (2019) revealed that country risk shocks have a negative effect on investment at the firm level, suggesting that changes in rating were found to affect SA firms’ investment decisions.

The effect of country risk on the equity market has been established (Brooks et al., 2004; Diamonte et al., 1996; r17r5Kaminsky & Schmukler, 2001; r29Muzindutsi & Manaliyo, 2016; r39Muzindutsi & Niyimbanira, 2012; r27Nhlapho & Muzindutsi, 2020; r31Sari et al., 2014; Subasi, 2008). The responsiveness of bond markets to changes in country risk is under-researched, especially from an emerging-market point of view. Literature (r11Codogno et al., 2003; r35Erb et al., 1996; Kaminsky & Schmukler, 2001; r43Reisen & Maltzan, 1999; r8Sy, 2002) has shown the effects of changing aggregate country risks on bond markets, but the effect of disaggregated country risks has not been studied in the SA context, thereby raising a question on how country risks affect the SA bond market under changing market cycles or regimes.

The remaining sections of the article contain, in order, the review of empirical literature, the objectives of the study, the rationale of the study and theoretical framework, the research methodology, the empirical results, the discussion of findings, the concluding remarks and the implication of findings and scope for future research.

Review of Literature

Country risk affects the value of investments made in the domestic market by foreign investment activity (Howell, 2017). Country risk is unique across countries, and, as such, is applicable to respective nations in their entirety. Similarly, country risk is usually non-diversifiable, within the bounds of the domestic markets itself (Perry, 2017). An approach to overcome the issue of non-diversifiabilty is through hedging across the different financial markets (within the domestic market itself). This method will lead to investment flows across financial markets, as investors may respond to changes in country risk by shifting their investments in order to hedge their exposures against, or benefit from, fluctuations in country risk fundamentals through gains in speculative positions (Bodie et al., 2010; Eun & Resnick, 2012). In this regard, investors who may have abandoned government bonds as a risky hedge during periods of low interest rates might buy them up as yields rise, making them more attractive (through corresponding decreases in bond price) and a better shield against equity market swings (Hayes, 2017).

By linking the bond market and country risk, Edwards (1986) found evidence that country risk and bond spreads are correlated in emerging markets and indicated that the former has a major impact on the latter. Erb et al. (1996) found correlation effects between the various International Country Risk Guide (ICRG) constituents (political, financial, economic and composite risk indices) of country risk and the expected future values of equity and debt returns. They also indicated that country risk—taken at a disaggregated level—contained substantial predictive power over metrics of stock pricing. In addition, Cantor and Frank (1996) showed that Moody’s and Standard & Poor’s credit ratings have an unbiased influence over sovereign bond yields, while the value of non-investment grade bonds responded instantaneously to rating announcements. Diamonte et al. (1996) explained that the political risk index affected more significantly the share prices in emerging markets than those in the developed markets. Reisen and Maltzan (1999) in an event study reported a statistically significant positive response of expected credit-rating upgrades on yield spreads and negative responses of impending rating downgrades on yield spreads.

On the effect of risk rating on the stability of the emerging markets, Kaminsky and Schmukler (2002) found that bond yield spread is an increasing function of risk-rating downgrades by 2 percentage points and stock returns, a decreasing function of approximately 1 per cent. There is a spillover effect of ratings changes in one country on other emerging markets, especially during crisis periods, and the effects are stronger in non-transparent economies. Block and Vaaler (2004) reported that election periods are associated with rising bond spreads and falling agency sovereign risk rating for developing countries, which eventually evens out on the completion of an election. As a result, both agencies and bondholders demonstrated a negative view of electioneering periods and, consequently, of imposing additional credit costs. According to Brooks et al. (2004), an impending credit-rating downgrade has an inverse relationship with the equity market and foreign exchange rates, while rating upgrades have direct effects. In 12 Latin American countries, Moser (2007) submitted that political news has a significant effect on financial markets, as bond spreads significantly trend upward 40 days before the change of ministers, while Kaminsky and Schmukler (1999) showed that on the announcement day of minister changes, bond spreads are high, flattening out thereafter. As a result, during the Asian crisis, most of the stock price movement was influenced by political risk.

In Turkey, Subasi’s (2008) event study methodology revealed declining foreign exchange rates following an impending credit-rating downgrade. Longstaff et al. (2011) submitted that sovereign credit risk is strongly linked to the global economy, as sovereign credit spreads are related more to the US stock and high yield markets than to local factors. In the European Economic and Monetary Union region countries, Maltritz (2012) found budget balance to GDP and trade balance to be the likely drivers of bond yield spreads over the entire period, and debt to GDP to be a likely driver during the pre-crisis period. This suggested that the spread may be sensitive to conditions in the economy. In South Africa, Kapingura and Mathetha-Kosi (2014) indicated evidence of a strong bidirectional causality between economic growth and the bond market. Further, Kapingura and Ikhide (2015) showed that there is a long-term relationship between macroeconomic variables and the bond market of South Africa, and that the key factor in the bond market is liquidity, since illiquidity may result in huge volatility and open market operations. Additionally, Robinson (2015) revealed that bond yield spreads are affected by fiscal policy decision-making and fiscal balance in South Africa, and this suggested that country risk emerging from this policy would affect the bond market. Radier et al. (2016) concluded that the interest rate level, volatility in firm-specific equity and the yield curve are contributory factors in uncovering the factors determining changes in bond yield spread. The effect of these factors is unstable between pre-crisis and post-crisis periods. Moudud-Ul-Huq et al. (2020) indicate that portfolio diversification can be used as a tool for risk control in emerging economies during a financial crisis.

Emerging markets, especially the Brazil, Russia, India, China and South Africa (BRICS) group, have been investigated recently. Walid et al. (2015) evaluated the asymmetric interactions between BRICS stock returns and three country risk components. Using dynamic panel threshold models, which allow for regime changing without the application of the Markov switching model (MSM), revealed that the signs and the significance of the impacts of ratings on BRICS stock returns were not similar in the high and low regimes. Additionally, Balcilar et al. (2017) showed that Brazil, Russia, India, China and South Africa (BRICS) stock returns demonstrated heterogeneous exposures to geopolitical risks, with the highest effect being in Russia. In this context, Nasr et al. (2018) showed through non-linear ARDL that there exists a high heterogeneity in BRICS returns’ interaction with country-based risk components. They concluded that bad news or negative changes in the ratings have a greater effect on stock returns and that there is a similarity in the interaction of the BRICS stock market with rating changes and its interaction with global indicators.

Empirical review reveals that country risks and bond yield factors are correlated, but there exists a dearth of empirical research on which component of country risks affects the SA bond market’s performance and stability. A study by Nhlapho and Muzindutsi (2020) attempted to fill this gap using a non-linear autoregressive distributed lag (NARDL) model to analyse the effect of country risk components on equity and bond markets’ indices, but this study did not address the issue of bond market stability and the recent debate over changing market conditions or regimes advocated by the recent adaptive market hypothesis (AMH).

Objectives of the Study

Consequent to the issues raised in the introduction and empirical literature, we determine the effects of country risk components on the SA bond market’s performance and stability by investigating and comparing the bond returns and yield spread’s responsiveness to changes in political, financial and economic risks under different regimes.

Rationale of the Study/Theoretical Framework

It has been established that aggregate country risk affects the bond markets, but the effects of disaggregated country risks have not been studied in the SA context. This need has become especially relevant given the current period of increasing country risk in South Africa, particularly since such increases to country risk have had broad-based market effects. Interest rates on emerging-market bond/debts vary markedly across countries and over time (Hilscher & Nosbusch, 2010) and could have a significant impact on the flow of investment within the country in question (Clark & Kassimatis, 2009). The consideration of market regime or condition in this study derives from the AMH of Lo (2005), which implies that a risk–return relationship is unlikely to be steady and likely to be dynamic, due to changing market conditions. The new AMH has different implications (Lo, 2005). First, it implies that the market or bond risk premium is unstable, due to factors like changing market size, competitors’ preferences and regulations (Lo, 2005), political conditions and economic conditions, inter alia. Second, it implies that, based on the evolutionary explanation, active market ecology requires the existence of profit opportunities that would evaporate as soon as they are exploited (Lo, 2017). However, new profits would be created continuously as certain participants leave, others enter and regulations and business conditions change. Third, investment strategies under AMH may be profitable under one regime and unprofitable under another regime. There is a need to inform investors and policymakers on the effects of different components of country risk and on bond returns and under different market conditions. This is achieved in this study through the application of the MSM.

Research Methodology

Data

This study employed time series data of a monthly frequency, ranging from January 1995 to December 2018, constrained by the availability of data. In this context, the study covered a post-apartheid period characterized by economic and political reform. Country risk rating (CRR) is often expressed as a composite weighted aggregate of corresponding political risk (PR), financial risk (FR) and economic risk (ER) indices 2 (Erb et al., 1996; Harvey, 2004). As a result, the latter are used as proxies for CRR, based on ICRG (Howell, 2017). Each element is assigned a point score of risk rating, set within a fixed range. This predetermined range ultimately indicates the weights assigned to each factor. As per ICRG methodologies, a higher point score, in terms of quantitative risk rating, reflects lesser risk.

We employed secondary yield spreads as a measure of bond yield. Scholtens (1999) showed the superiority of the secondary bond market over the primary bond market. This is further supported by theoretical standpoints, as Scholtens (1999) explained that secondary bond market examination mirrors the shifting sentiments and expectations of bond issuers and bond holders, at an ongoing rate. Arguments for the use of bond yield spread (as a measure of the bond market) were established in the existing literature (Codogno et al., 2003), where changes to this yield spread represent changes in the overall bond market. We measured bond yield spreads as the yield differential of long-term (10 years and over) government bonds, on the SA Treasury Bill (T-Bill), adjusted for inflation. Since the yield spread measures bond market stability, we also examined the effect of risk components on bond market performance proxied by bond index returns. Bond yields data were obtained from Bloomberg, and inflation information was obtained from the South African Reserve Bank (2019).

Estimation Technique

MSM is employed to examine the dynamic relationship between the SA bond market and the three core sub-risk components of country risk ratings. Various economic and financial time series usually go through periods in which the movement of the series varies significantly relative to what was observed in the past (Brooks, 2014). Where the behaviour changes for a period of time and returns to its previous behaviour or shifts to a yet newer behaviour, it is known as a regime shift or switch (Brooks, 2014). Brooks (2014) noted that a regime shift could take place on a regular basis and result in significant variations in financial market return behaviour. In the presence of such ‘regime changes’, a linear model estimated over the entire sample covering the change would be unsuitable. Consequently, we hypothesized that bond returns and yield spread are non-linear and that their supposed relationship with country risk components can be better captured by a regime switching model. This study applied MSM because it permits the estimation of the entire observations on the series and different types of behaviour at different regimes or cycles (Brooks, 2014; Saji, 2017).

The first-order Markov assumed that the probability of being in a particular state depends on the most recent state, such that

where the ith and jth element is the probability of moving from regime i in period t – 1 to regime j in period t. The probabilities are assumed to be constant, such that

Expressing Equation (1) in matrix form:

where P00 is the probability that the bond yield spread or return is at state 0 (low) at time t – 1 and remains there at time t, P01 is the probability that the bond yield spread or return is at state 0 at time t – 1 and moves to state 1 at time t, P10 is the probability that the bond yield spread or return is at state 1 at time t – 1 and moves to state 0 at time t, and P11 is the probability that the bond yield spread or return is at state 1 at time t – 1 and remains there at time t.

Model Specification

The models used in the study are specified in this section. They portray the relationships between country risk components and bond returns, on the one hand, and that between risk components and bond yield spread, on the other hand.

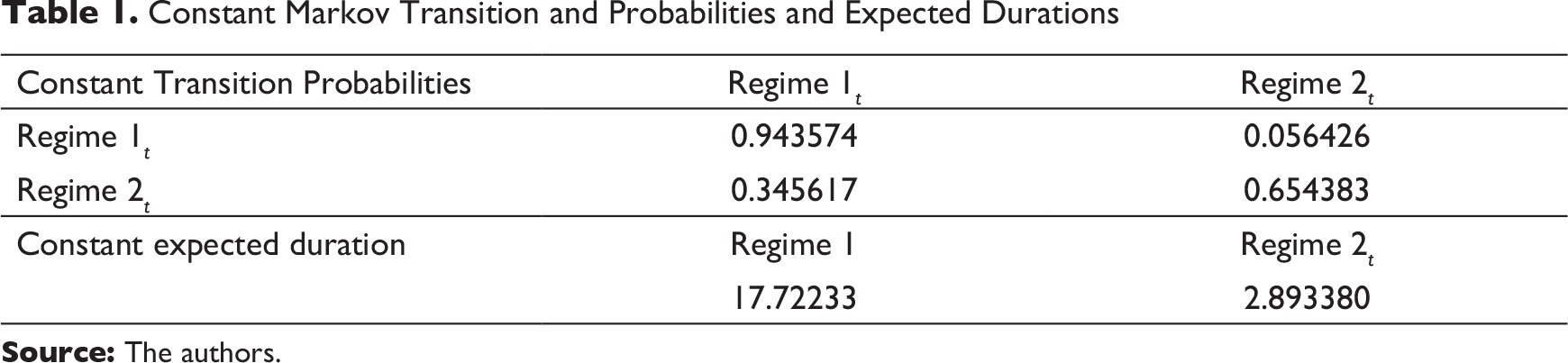

Constant Markov Transition and Probabilities and Expected Durations

Analyses and Results

Bond Index Return and Country Risk Components

Table 1 shows that the probability of bond return to be in a bull regime (0.943574) exceeds that of it being in a bear regime (0.654383), and the probability of return changing from a bull (0.056426) to a bear regime is equally lower relative to that of return changing from a bear to a bull regime (0.196519).

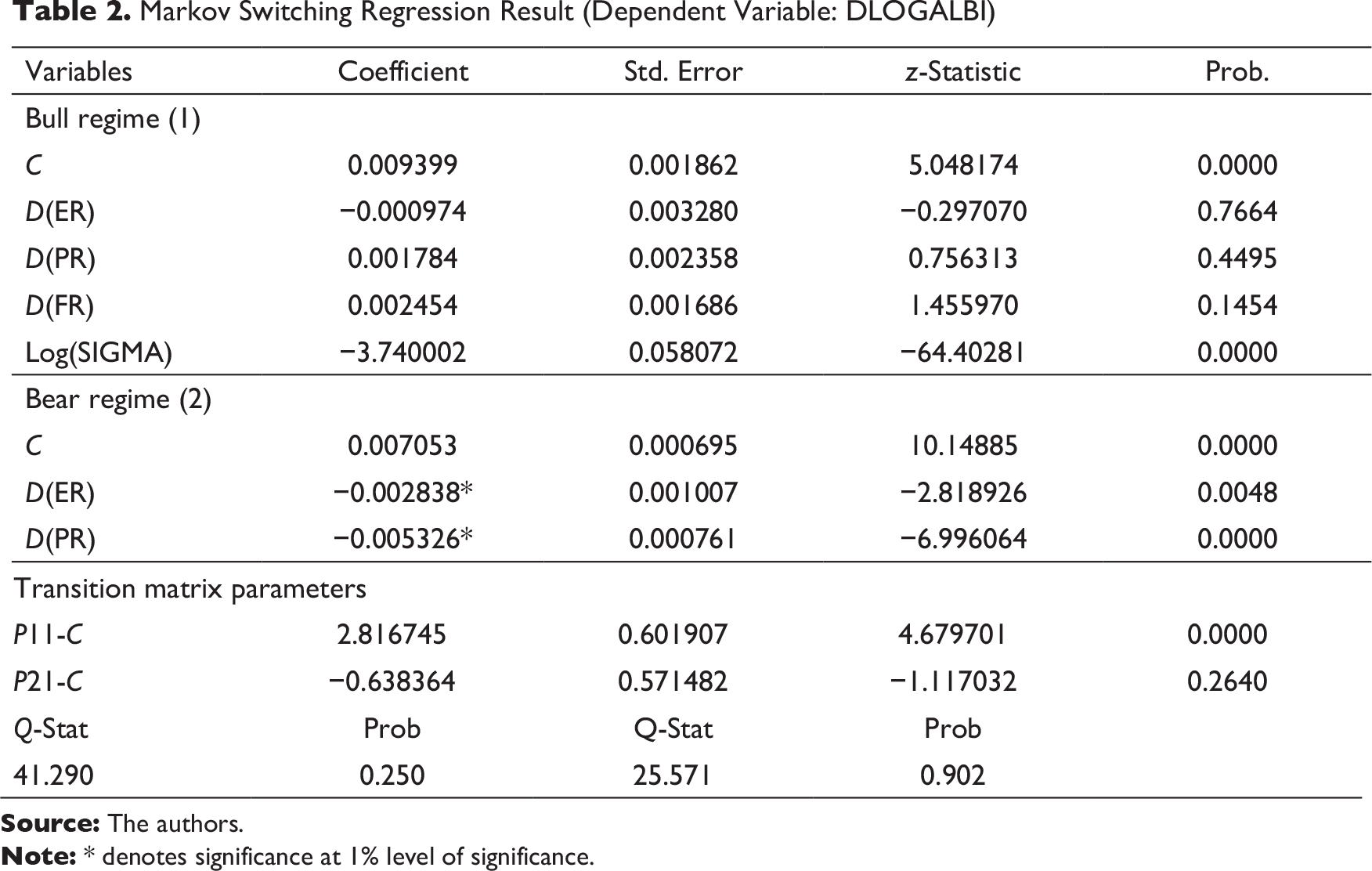

Markov Switching Regression Result (Dependent Variable: DLOGALBI)

Real Yield Spread and Country Risk Components

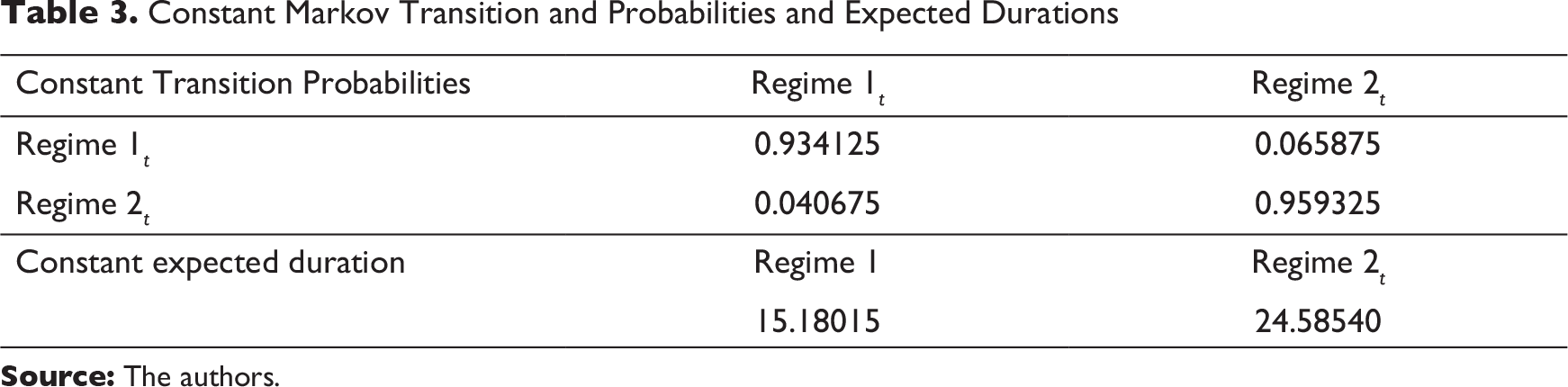

In addition to the above, the study examines whether the real yield spread is affected by the changing regime. Table 3 shows that the bond yield spread has a low probability of being a bear period (0.934125) compared to that of being a bull period (0.959325) and that the prospect of yield spread to transition from a bear regime (0.065875) is higher than otherwise (0.040675).

Constant Markov Transition and Probabilities and Expected Durations

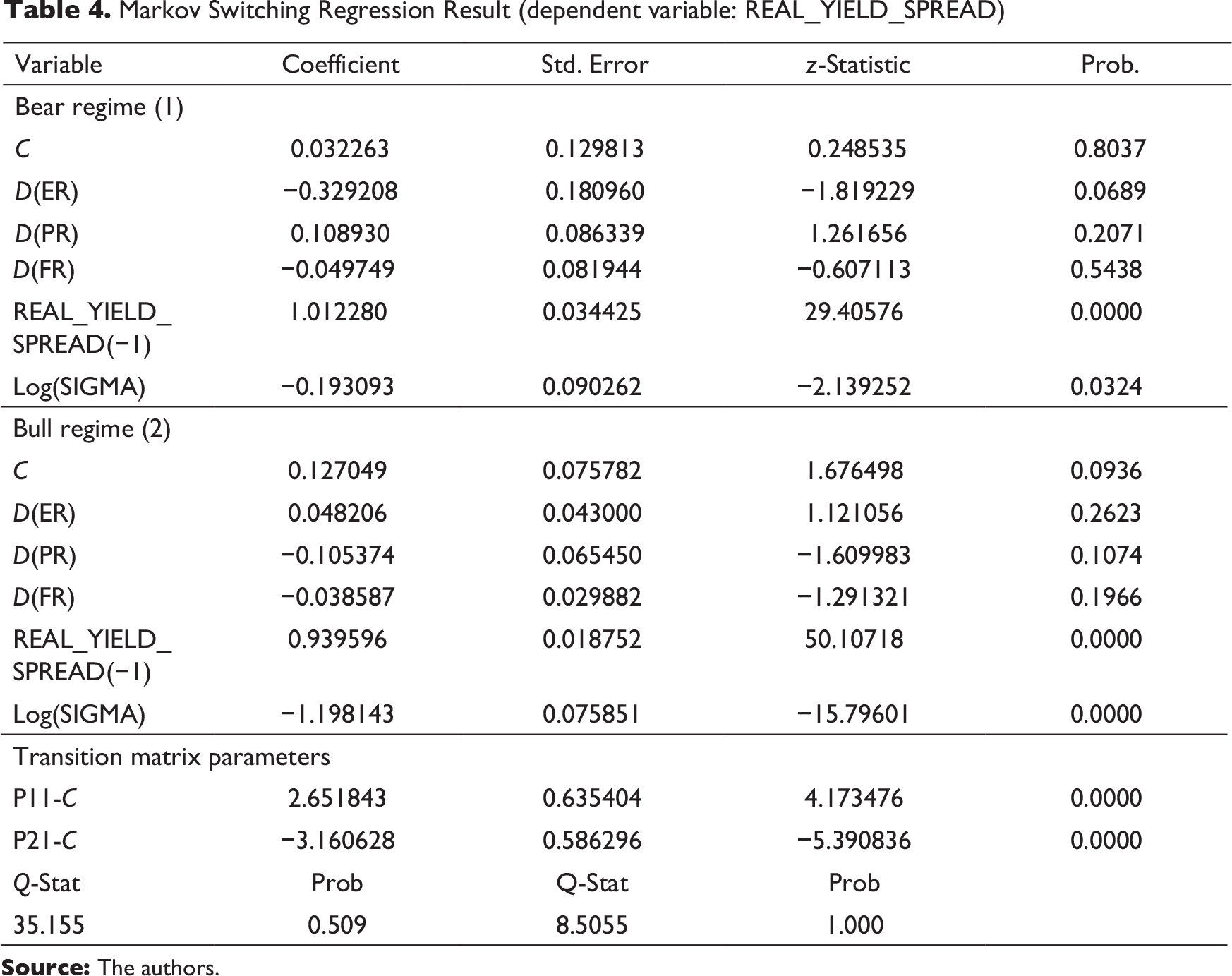

Markov Switching Regression Result (dependent variable: REAL_YIELD_SPREAD)

Residual Diagnostic Tests

The reliability and accuracy of the analytical results depend on the outcome of the residual diagnostic tests. The results were tested for autocorrelations using a correlogram of standardized residuals and that of standardized residuals squared. The results of these tests are presented in the last rows of Tables 2 and 4. The results show that the associated p-values are greater than the 5 per cent level of significance. The rejection of the null hypothesis of autocorrelation in both cases rendered the results reliable.

Discussion of Findings

South Africa has faced mounting economic, financial and political instability in recent years. The impact of this has been felt in the bond market through debt-rating downgrades, which could potentially affect the flow of funds within the country. This study investigated the regime-dependent effects of changes in country risk factors on bond market performance and stability, as measured by the bond returns and yield spread, respectively, using the MSM approach. We found that all the components of country risk exercise significant effects on bond returns during a bear regime. Our finding is consistent with Erb et al. (1996), who investigated the predictive power of country risk on equity and debt returns and found correlation effects between the various constituents of country risk and expected future values of securities’ returns, although they did not take market cycles into consideration. Our findings are in accordance with those of Muzindutsi and Nhlapho (2017), who found that the components of country risk have negative long-term effects on credit extension in South Africa. Additionally, Nhlapho and Muzindutsi (2020) found that political and economic risks affect both equity and bond markets, suggesting that financial markets suffer from the increases in country risk shocks.

Contrary to prior expectation, we found that the relationship of the country risk components with yield spreads is not affected by market cycles. These findings on yield spreads are contrary to the findings of Sari et al. (2014) in Turkey, who showed that the three elements of country risks have a significant long-term impact on bond yield spread and that financial risk has a short-term impact. Additionally, Codogno et al. (2003), in the Eurozone government bond market, showed that yield differential is affected by credit risk. Unlike the aforementioned studies, we reported that yield spread is not significantly influenced by country risk factors, on the one hand, and that the relationship between them is not affected by market cycles, on the other hand. Considering that yield spreads can be considered as a risk premium, the results of the research on yield spreads suggest that SA investors do not require a risk premium for these country risks, which implies that the components of country risks are already priced in the bond yield rates. This finding is therefore in accordance with Mutize and Gossel (2018) who found that African bond markets do not react to sovereign credit risk announcements.

The finding of the significance of political risk as a driver of bond returns is similar to that of Diamonte et al. (1996), despite that the latter was based on share prices in emerging markets and did not take regime sensitivity into consideration. The increase in bond returns that accompanies political risk implies that political risk increases the government’s cost of borrowing. The effect of political risk is detrimental from the government’s point of view. This view is logical when considering the rate at which politics-related crises and instability are publicized and the significance attached to political risk, especially by international investors. Investors are usually sensitive to political crises that may make government bonds unattractive to investors, particularly to international investors. As a result, they would require high yield returns. Similarly, economic risk is often linked with economic crisis, accompanied by a decline in a country’s income. The need for further investment to restore economic performance during such periods may also require payment of high rates by the government to attract investors. Financial risk is often associated with financial crises, which is usually accompanied by a decline in the ability to pay high interests on the bond. This study concludes that bond returns is a decreasing function of financial risk. Financial risk may not be seen as significant to investors, as the government is deemed to exist in perpetuity. In the light of the COVID-19 pandemic, there are indications that the government may not be able to honour its obligations towards bonds, which presents a significant financial risk to investors (Bizcommunity, 2020). Investors should devote specific attention to the SA political and economic environments before entering into a commitment involving government debt securities, while the SA government should cultivate conducive political and economic environments to reduce the cost of borrowing.

Concluding Remarks

This study investigated the regime-dependent effects of changes in country risk factors on bond market performance and stability, as measured by bond returns and yield spread, respectively, using the MSM approach. First, the study showed that both returns and spread undergo longer bullish trends. Second, the effect of country risks on bond returns is only significant in the bear regime, in which bond returns increase with a change in political and economic risks and decrease with a change in financial risk. Third, the effect of the risk components on yield spread is not significant in any regime. As a result, it was concluded that bond market performance is influenced by market cycle, while bond market stability is not. The study is unique, exploring the influence of market conditions or regimes on the relationship between country risks and bond market performance and stability. Subsequently, we provided evidence to support the AMH in the SA bond market. We also narrowed the gap in terms of components of country risks that would affect the SA bond market performance.

Managerial Implication and Future Research

The implication of the findings is that bond market participants and government should afford attention to market conditions, as well as political and economic risks, while making investment decisions and economic policies. Further study is recommended on the influence of changing regimes on the relationship between country risk components and the interactions between bond and other financial markets. Considering the recent downgrade of SA investment market to junk status, there is a need to examine the impact of COVID-19 on bond market performance.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.