Abstract

This study examines the impact of COVID-19 on the migrant workers and remittances flow to Bangladesh, the fastest growing South Asian country. Migrant workers have been playing an important role in propelling the economic activities of the country for a vast majority of the low-income population. Bangladesh is one of the major remittance recipient countries and earned US$21.8 billion in 2020. Over half a million workers from Bangladesh are employed in foreign countries annually, which eases the pressure on the domestic labour market considerably. However, the inflow of these enormous remittances has been encountered by various challenges including the ongoing COVID-19 pandemic, which has brought numerous adverse socio-economic impacts on the migrant workers. Policy recommendations suggest designing and implementing well-coordinated public–private migrant workers’ inclusive policies and creating a supportive environment for the returnee migrant workers to overcome this crisis. Initiating dialogues and negotiation with the employing countries to protect the jobs and workers’ rights can restore the employment and remittances during and after the pandemic, facilitate the expansion of the labour market across borders, and harness the valuable remittances for the overall welfare of the country.

Introduction

Over the centuries, migrating across the border of the home country in search of resources, employment, and higher income and wealth has been a well-documented phenomenon and discussed in the socio-economic as well as history and political analyses. International migration and remittances have created a lot of attention among the observers, researchers, and policymakers as the rapid increase in the total number of migrant workers, especially from the developing countries and the massive inflow of remittances to these countries, has become a salient feature of globalisation from the mid-1980s. More than 272 million people or 3.5% world population lived outside their countries in 2019 (UN, 2020), and among them, 164 million were migrant workers as estimated by the International Labour Organization (ILO). About 33% of these workers come from the Asia and Pacific region. In 2019, the global flow of remittances accounted for US$717 billion compared to a mere US$18 billion in 1980. Remittances to the low and middle-income developing countries (LMIDC) have surpassed the flow of foreign direct investment (FDI), portfolio investment, and official development assistance (ODA) since 2018 and stood out as one of the most important income flows from abroad. The total number of migrant workers from South Asia has increased over the decade from 23.89 million in 1990 to more than 38 million in 2017. South Asia alone contributed US$140 billion or about 20% of the global remittances, which played a significant role in the economic growth and social development of the region. There come numerous challenges with the large flow of remittances to the developing countries. The outbreak of the worldwide COVID-19 pandemic is another unprecedented shock to the remittances flow and the movement of global migrant workers from the early 2020. Since this global health crisis has been adversely affecting both the demand and supply sides of the world economy, the impact on the migrant workers and their dependent families is predicted to be extensive, considering its distressing influence on every economy around the world. The major destination countries for the Asian migrants are Asia (35%), the Middle East (27%), Europe inclusive of the Russian Federation (19%), and North America (18%). The economies of these countries have been greatly affected by the COVID-19 pandemic, and their economic growth has been projected to fall as low as 10% (ADB, 2020). This, in turn, may have a devastating impact on the employment and income prospects of the migrant workers. The World Bank (2020a) had predicted a 20% drop in remittances to LMIDC and above 22% for South Asia in 2020. A further fall of 7.1% in global remittances and 10.9% for South Asia in 2021 has been forecased compared to 8.2% and 12.3% growth, respectively, in 2018. Also, other foreign funding such as FDI is forecasted remain low due to the travel bans, disruption in international trade, as well as fall in wealth level originating from the declining stock prices of some major multinational corporations (World Bank, 2020a). Thus, a substantial decline in these external income flows is likely to increase economic, fiscal, and social pressure for the governments of these countries.

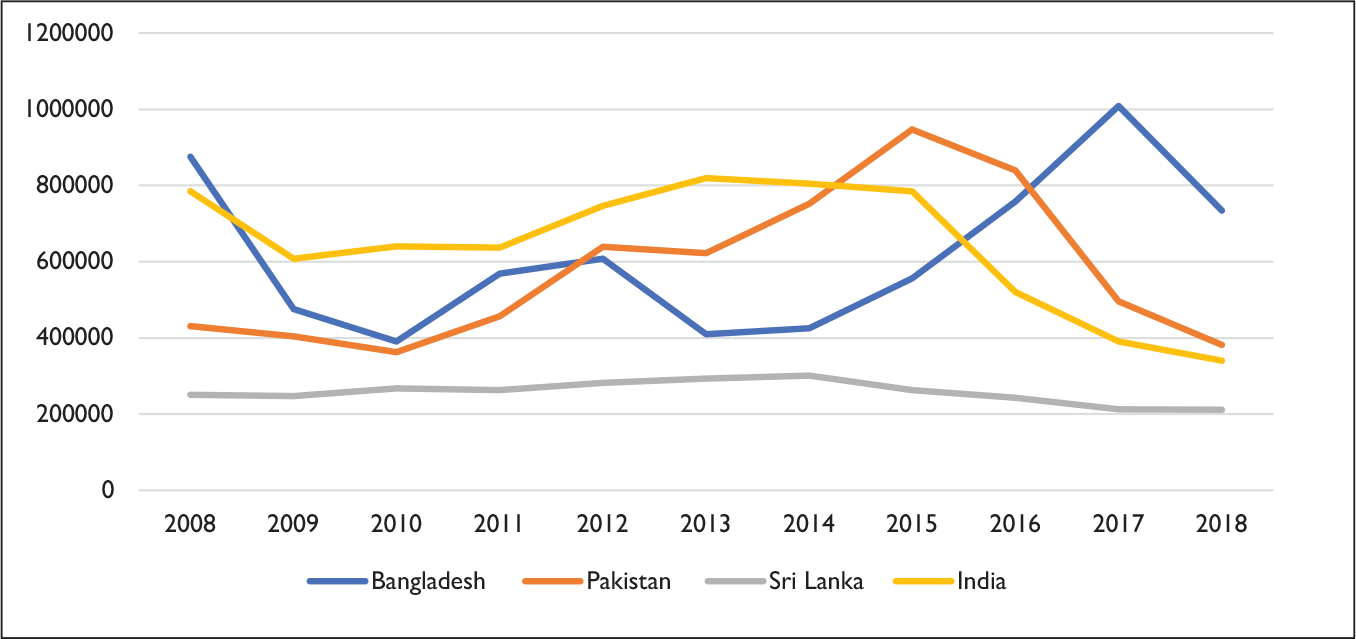

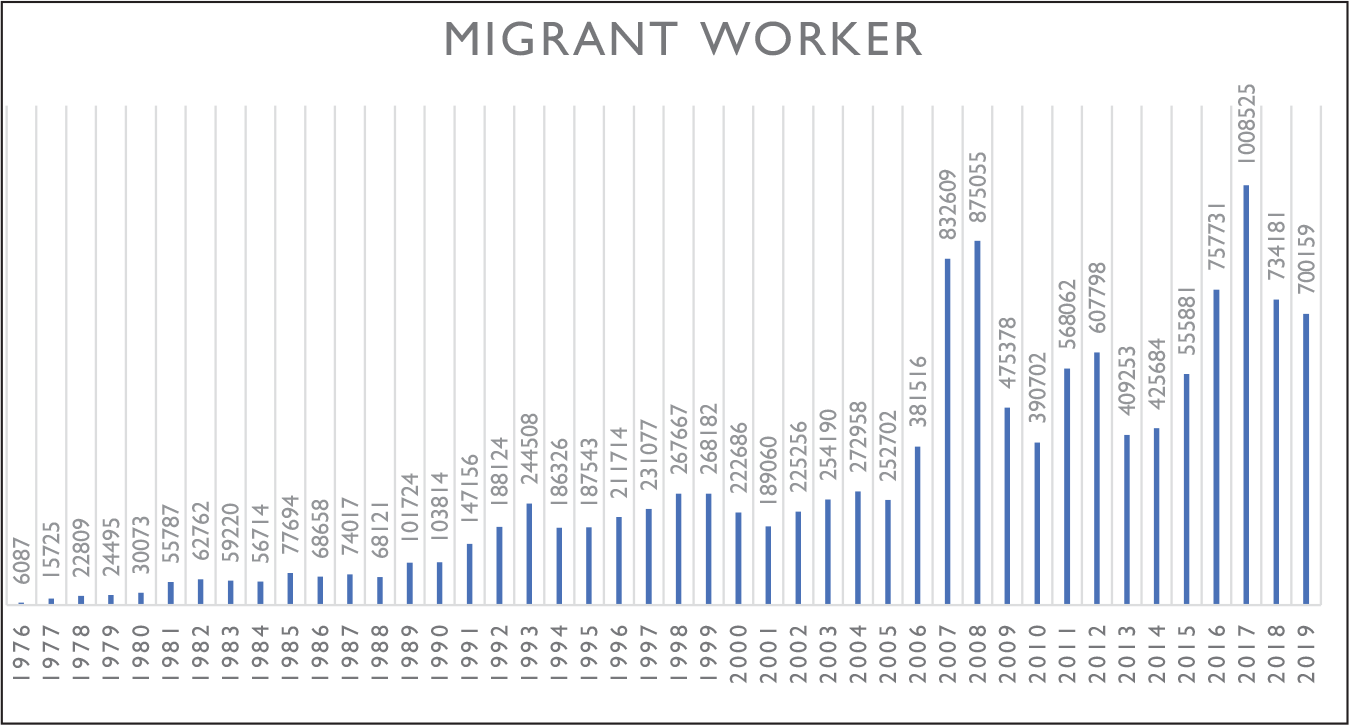

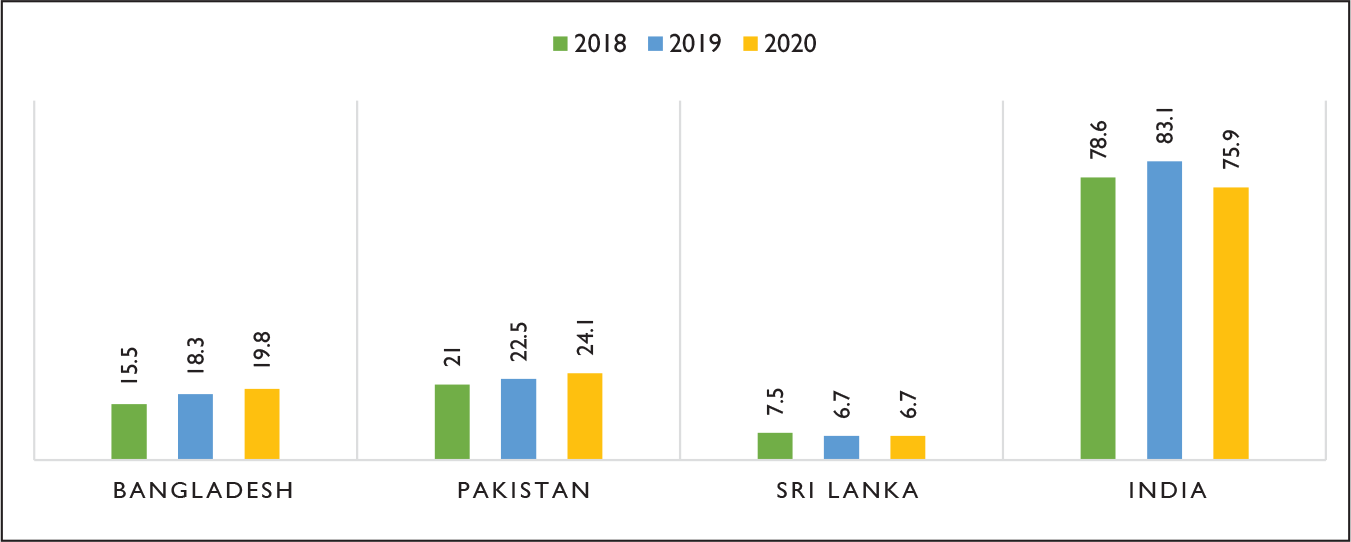

Bangladesh has successfully extended its labour market across the border and has become one of the leading remittance recipient countries in South Asia through the export of its labour services to the Middle East and Southeast Asian countries since the early 1970s (Figure 1). In 2020, Bangladesh received remittances of US$20 billion, which contributes about 13% to the South Asian remittances and ranks as the third largest followed by India (US$75.9 billion) and Pakistan (US$24.1 billion) among the eight South Asian countries (World Bank, 2020a).

Source: Constructed by the authors with data from ILO (2018).

This large flow of foreign exchange earnings not only assists in poverty alleviation and augments the foreign exchange reserve for the country but also supports domestic investment, financial development, educational attainment, women empowerment, and various other social developments of Bangladesh as well as the other developing countries (Acosta et al., 2009; Azizi, 2018; Chowdhury, 2011; Maimbo & Ratha, 2005). Nonetheless, the recruitments of Bangladeshi workers have been disrupted by the worldwide COVID-19 pandemic. Several Bangladeshi migrant workers have reported their loss of employment and wages due to the economic crisis and lockdown in the destination countries. It is also reported that about 200,000 Bangladeshi workers could not join back to work due to global lockdown in spite of possessing all the required documents and work permits (UNDP, 2020).

The overseas employment and remittances are the vital sources of livelihood for a large number of migrant workers and their families. This huge flow of remittances has been creating multiple benefits for the country, such as supporting its foreign exchange reserve, lessening the pressure on its public funding and reducing poverty level. Thus, it is imperative to analyse the effect of COVID-19 on the remittances flow and overseas employment opportunities and take proactive and coordinated measures to minimise the long-run adverse effects on the migrant workers and remittances flow to Bangladesh. Therefore, the objective of this article is to analyse the socio-economic impact of COVID-19 on the migrant workers by presenting the past and present overseas employment opportunities and the remittances inflow to Bangladesh and recommend policy actions that can mitigate the effect of Coronavirus on their current employment status and enhance the future overseas employment prospects. This study can be considered a key contribution to the literature as there are no or very limited comprehensive studies that have been undertaken on this topic. Furthermore, this study briefly compares the current worldwide COVID-19 shocks with those of previous geopolitical, financial, and economic shocks since the Gulf War (GW) in 1990–1991. Thus, the study contributes, in a timely and constructive fashion, to deal with the impact of the pandemic on the migrant workers and their social, economic, health and future employment prospect issues.

The article is organised as follows: the second section presents a brief literature review; the third section illustrates the flow of remittances to Bangladesh economy over the past four decades; the fourth section illustrates the effect of coronavirus pandemic on remittances flow and Bangladeshi migrant workers. The fifth section briefly discusses the previous global shocks on the Bangladeshi migrant workers, remittances flow, and the supports provided by the government during and after the shocks; the sixth section draws the conclusion and policy recommendations for the study.

Literature Review

In the recent theoretical literature, real wage differences, potential higher income prospects, and altruistic and self-interest motives are considered to be the drivers of migration and remittances (Lucas & Stark, 1985; Stark & Bloom, 1985). While the altruistic motive of sending remittances relates to the financial support provided by the migrant workers to their left-behind families in the country of origin, the self-interest motive mainly reflects the concern of increased saving, investment, social prestige, and funds for retirement by a migrant worker. Repaying the past and present debt is also considered to be another noteworthy reason for sending remittances to the home country, since the majority of the migrant workers from the developing countries are from low-income families with lower education and skill; thus, they usually borrow funds to cover the cost of migration to an overseas job.

Various aspects of the effect of migration and remittances are discussed in the empirical literature, including economic growth and development, skill-building, financial development, educational attainment, and the poverty alleviation effects of remittances (Adams & Page, 2005; Chowdhury, 2011; Gupta et al., 2009; Ratha, 2003). Majority of the existing studies find positive, direct and indirect growth and development effect of remittances especially for the developing countries. However, using a large sample of migrant-sending countries, Chami et al. (2003) suggest a negative effect of remittances on economic growth as it reduces the incentive to work by the migrant family members. Chowdhury and Rabbi (2014) also find deterioration of international competitiveness created by the massive flow of remittances to Bangladesh.

The literature on the effects of various geopolitical, socio-economic, and financial shocks on the migrant workers and remittances flow is limited, especially for Bangladesh. All the major shocks over the last three decades, namely Gulf-War (GW), Asian Financial Crisis (AFC), Global Financial Crisis (GFC), and the current global COVID-19 pandemic (GCP) have brought significant socio-economic, financial, and health crises to a region or globally, which impacted the livelihood of migrant workers and remittances flow to the recipient countries. In 1990–1991, the GW crisis resulted in economic loss to Bangladesh due to loss of overseas employment from Kuwait, Iraq, and other Gulf countries; high cost of repatriating Bangladeshi workers from war-affected countries; and higher oil prices (Hossain, 1997). Also, AFC created a loss of employment and deportation of Bangladeshi workers, especially from Malaysia during and after the crisis in 1997–1998 and the remittances started falling from December 1997. However, it is interesting to see that the remittances flow to Bangladesh grew strongly over 37% amid GFC during 2008, which was equivalent to US$9 billion and contributed to 56% of all foreign exchange earnings. The nature of the current GCP is different than the previous shocks mentioned, as it is not only disrupting the demand side of the global economy but also created a supply shock by restricting the movements of resources, especially the labour services. Nonetheless, the literature on the GCP effect of remittances and overseas employment is not clear as it is limited only to the reports and discussion of various international agencies, that is, World Bank (WB), United Nations (UN), Asian Development Bank (ADB), Organisation for Economic Cooperation and Development (OECD, 2020) and Refugee and Migratory Movements Research Unit (RMMRU). Defying the negative forecasts of a massive decline in the remittances flow to South Asia, it is found that remittances flow to Bangladesh and Pakistan have increased in 2020 compared to its previous year suggesting the countercyclical nature of remittances (World Bank, 2020d). Remittance is defined as a private fund flowing from the migrants to their families, which usually increases, especially in the time of distress to provide a cushion against economic hardship. In this way, remittances have often been found to be resilient to adverse shocks, especially in the workers’ country of origin. This possibly explains why remittance flow in many recipient countries remained unaffected during the first half of 2020 when the pandemic first strike. The fall in the flow was mainly noted in Bangladesh from March 2020, which then stabilised and started to increase. This bounce back in remittances flow can be viewed as the increased need of sending money to the families as the recipient countries were fighting hard to survive the pandemic. However, in case the migrants are exhausting their savings to support their families back home, this trend will not be sustainable over time if the pandemic leads to a recession in the host countries (Quayyum & Kpodar, 2020).

Overview of Remittances Income and Overseas Employment

Bangladesh Economy and Flow of Remittances

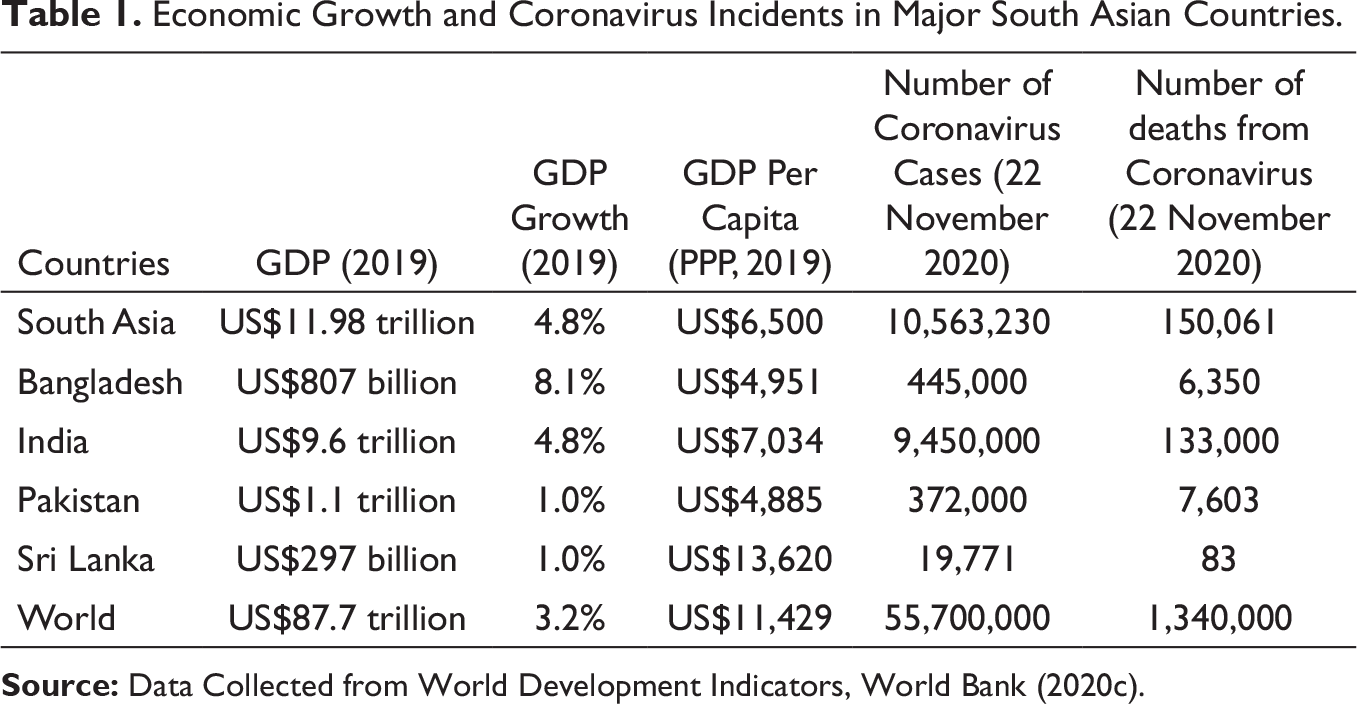

Economic Growth and Coronavirus Incidents in Major South Asian Countries.

Trend in Remittances Flow

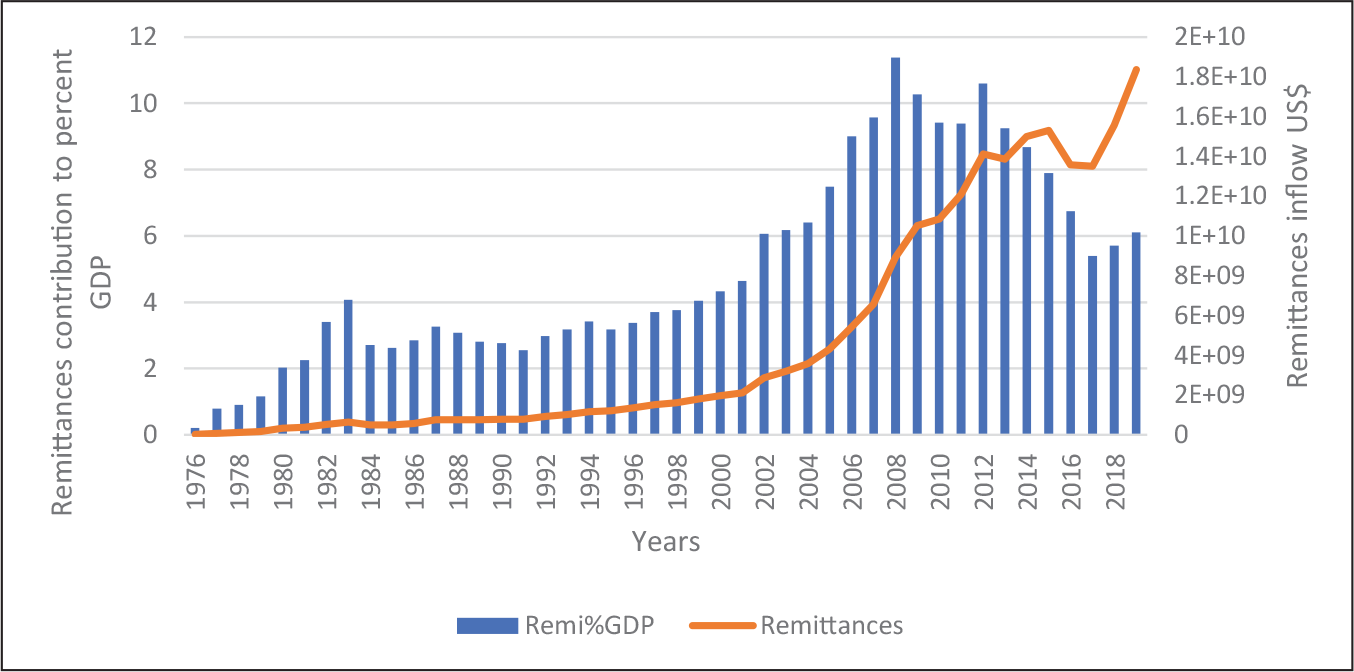

Remittances income increased from US$1.96 billion in 1999–2000 to US$12.1 billion in 2010–2011, which was a dramatic 500% increase over in a period of 10 years (Bangladesh Bank, online). The total value of remittances had increased to over 65% in 2020 since 2011 (Figure 2). In 2020, workers’ remittances became the second largest foreign exchange revenue and constituted 51% of foreign exchange reserve build-up and contributed significantly to the current account surplus. It exceeded 3 times the total foreign aid and 15 times FDI received by the economy. It is believed that the actual size of the remittances coming to the economy through unrecorded formal and informal channels is significantly larger than that of the recorded amount.

Source: Constructed by the authors using BMET (online) data.

Host Countries of Bangladeshi Migrant Workers

Bangladeshi migrant workers are mainly employed by MENA 1

The term MENA refers to 20 member countries of Middle East and North African Countries.

Source: Constructed by the author using BMET (online) data.

Skill Composition of Migrant Workers

Among the Bangladeshi migrant workers, only 0.27% of the migrant workers are professionals, 44% skilled, 20% semi-skilled, 28% less-skilled, and the remaining 8% fall in other categories. Bangladeshi workers are predominantly male, about 15% of them were female in 2019, which fell from 19% in 2015 (BMET, online). About 70% of migrant workers are aged between 21 and 30 years and 11% of all workers have no formal education, 31% have primary and lower secondary, and 58% of them received secondary and above education (Asian Foundation, 2013). It is believed that the presence of a large number of female workers from Bangladesh in the Middle East and Asian countries remains undocumented.

Effect of Coronavirus Pandemic on Migrant Workers and Remittances Flow

COVID-19 and the Global Pandemic

The very first cluster of the COVID-19 virus was reported in Wuhan, Hubei province of China in late November 2019 caused by severe acute respiratory syndrome coronavirus II (SARS-CoV-2). This is a new strain of coronavirus that is causing disease in humans and spreading from person-to-person. The World Health Organization (WHO) was notified about the cases of pneumonia in Wuhan on the 31 December 2020. WHO officially declared the outbreak of the virus as an international public health emergency in January 2020 and named this infectious disease as the coronavirus disease on the 12 February 2020. By March 2020, the virus had spread in many Asian and European countries, and some countries started taking measures to prevent the spread of the virus by closing down their borders and locking down various social and economic activities. These measures have had a profound effect on the migrant workers and their socio-economic status since then. Advanced and key host countries started undertaking measures in line with the diverse strategies to contain the virus, which got stricter in March 2020 but were slowly relaxed by the middle of the year 2020. However, the second wave of coronavirus pandemic is hitting several countries of Europe, the Middle East, and North America at present, and this has led to restrictions in cross-country travels including those preventing the migrant workers from travelling back to several of those countries.

Coronavirus Pandemic and Its Effect on South Asian Migrant Workers and Remittances

The economic cost of COVID-19 is expected to reach between US$5.8 trillion to US$8.8 trillion globally, which is almost 6.4–9.7% of global GDP. The negative effect on the jobs was noticeable during the second quarter of 2020 in the USA, UK, as well as in Europe and Central Asia, especially for the migrant workers with declining working hours (World Bank, 2020a). The earlier plausible V-shaped recovery may not hold if the pandemic continues into 2021 until an effective vaccine for coronavirus is out in the market and extensively applied globally to prevent the disease. The World Bank (2020c) has revised its earlier prediction and indicates that the remittance flow to South Asia will decline by around 11% in 2021. Remittances were projected to grow by 8%, that is, to US$20 billion, for Bangladesh and 9% for Pakistan, that is, to US$20 billion, but a 9% fall was expected for both India and Sri Lanka in 2020 (World Bank, 2020c).

The extent of the shocks to migrants’ jobs depends on the sector they were employed in as well as the overall economic condition of the host country. The worldwide coronavirus pandemic is simultaneously hitting the economies of both the host and the source countries of migrant workers, unlike other economic shocks that only have localised effects. The major hosts of the South Asian migrant workers, that is, the Middle Eastern countries, have been severely affected by the worldwide coronavirus pandemic as well as by the suppressed global demand for and price of petroleum (World Bank, 2020a). This, in turn, is causing a decline in the demand for the workers. The hard-hit sectors include the retail and wholesale trade, hospitality and recreation, manufacturing, and foodservice sectors, where the majority of the migrants work. The construction sector is another major employment sector for migrant workers, especially in the Gulf countries. Many construction sites were closed due to potential infection and spread of the virus, while the risk of infection is high among migrants living in densely populated residence. Moreover, travel bans have restricted international mobility and affected workers in the transport sector (World Bank, 2020a).

The migrants and the informal workers are most at risk of losing jobs, as they do not have a regular contract and have poor bargaining power. When prolonged lockdowns drive companies out of business, migrants become vulnerable. The uncertain situation concerning the persisting weak demand for workers in the economies of the major destination countries poses long-term threats to the livelihood of these migrant workers. Since the remittances are crucial in improving the lives and welfare of a large number of poor in the South Asian region, a sudden loss of such an income can plunge such families into a vulnerable situation. The families face the most risk where remittance is the only income source and there is no one else to earn except the migrant worker. Without continuous remittances flow, these households will have to cut down on necessities such as food, clothing, health, and education.

Source: Constructed by the authors using World Bank Data (2020b).

Also, loan repayment remains another challenge when the flow of remittance is restricted (ADB, 2020). A study conducted by ADB (2020) involving microdata from selected economies in the South Asian region suggests that a 10% increase in remittance inflow results in a 3–4% increase in GDP per capita.

The pandemic-related travel restrictions have already impacted the mobility of international migrants including the South Asian Migrant adversely, which is likely to keep the flow of remittances low in 2021 too. Many migrants from the Middle Eastern countries returned to their country of origin such as India, Pakistan, and Bangladesh. Some migrants also had to be evacuated by the government of the respective country of origin. Furthermore, migrant outflows from the region have also been severely impacted. In Pakistan, the number of emigrants was only 179,487 for January–September 2020 compared to 625,203 for the year 2019 (World Bank, 2020a). In Bangladesh, the number of emigrants was only 181,218 for January–May 2020 compared to 302,418 for the same time in the year 2019 (BMET, 2020; World Bank, 2020b). However, it is interesting to note that remittances income increased in both Bangladesh and Pakistan as the pandemic has diverted the flow of remittances from informal to formal channels due to the travel restrictions, risk in carrying the money informally in place, and the incentives that are provided by the governments to channel the flow of remittances through the formal financial system (Figure 4).

Coronavirus Pandemic and Effect on the Current and Prospective Migration and Remittances Flow to Bangladesh

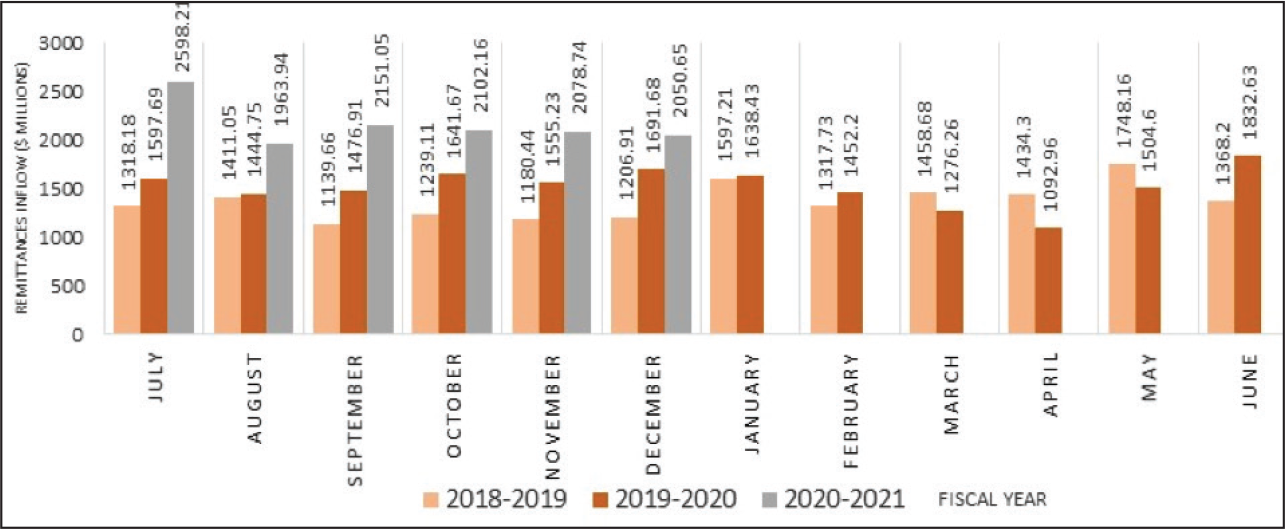

Bangladesh had approximately 10 million migrant workers in various countries who used to send a large amount of foreign exchange income to the country until 2019 before the pandemic started. An earlier World Bank (2020a) projection indicates the total remittances to Bangladesh would fall to US$14 billion in 2020, which is a 20% decline from that of the previous year. Statistics (Figure 5) released for remittances received by Bangladesh show that the year-on-year remittances for March, April, and May fell by 20%, confirming the projection made by the World Bank (Bangladesh Bank, 2020). This drop in income brought a notable stress on the household income of many migrant households as this income assists considerably to reduce the poverty level in the rural areas of the country. Poverty falls faster in the migrant-sending districts, and it is found that for each 0.1% increase in the number of migrants from that district, poverty rate falls by 1.7% (UNDP, 2020).

The country received US$1638 million in remittances in January and US$1452 million in February 2020 (Bangladesh Bank, 2020). After the implementation of extensive lockdowns in the major host counties, remittances started declining from March and the country received 14% less remittance than the same month in 2019. In April, 2020, the remittances amounted to US $1093 million, indicating a 32% fall than that of April 2019, which is the lowest in recent history (Figure 5). Nonetheless, there is always an increase in remittances observed during any festivity season and 2020 was not an exception despite the pandemic. During the month of Ramadan, remittance flow increased to US$1505 million in May, and it reached US$1,833 million in June to support the families during the lockdown and upcoming Eid-ul-Adha festival. However, in July 2020, there was another sudden surge in the amount of remittance income to US$2598 million, mainly because the migrants could sense the uncertainty around their employment due to the pandemic and started repatriating major amounts of their savings abroad (Bangladesh Bank, 2020). The remittances flow to Bangladesh remained solid above US$2 billion monthly for the rest of the year.

Source: Constructed by the Authors using Data from Bangladesh Bank (online).

Though there has been an increase in remittances in June, employment abroad has been low for the past 4 months. The last batch of migrants who could manage to fly out before travel restrictions included only 38,000 workers, of which the normal is 50,000–60,000 monthly. In the past few months, almost 200,000 migrants have not been able to migrate, including 100,000 who had their passports and visas ready for departure. According to the secretary of the Bangladesh Association of International Recruiting Agency (BAIRA, 2020, personal communication), 78,428 people had made all arrangements to travel abroad but have been restricted due to the pandemic. These would-be migrants are becoming impatient due to the elongated period of uncertainty concerning their employment. Also, the agencies have made huge investments, and if the economic condition does not improve shortly, this whole sector would risk a massive breakdown (Hasan, 2020).

The state of the world economy is not expected to get back to normal as soon as the pandemic condition improves. The economic slowdown in the Middle Eastern counties caused by the fall in oil prices and aggravated by the coronavirus pandemic may result in a further loss of future employment. Bangladesh is largely dependent on those countries for absorbing a major portion of its migrant workers. There were around 4 million migrants in KSA alone, 1.5 million are in the Emirates while others such as Qatar, Kuwait, Oman, and Bahrain recruited almost 0.3–0.4 million Bangladeshi migrant workers in 2019. In the face of dampening demand and falling oil prices, these countries will likely cut down jobs that are usually filled by the migrants. TBS (2020) (various issues) reports that about 666,000 Bangladeshi workers were sent back home after the COVID-19 outbreak and about 2 million faced possible deportation. Hasan (2020) refers to an English daily from Saudi Arabia which has stated that almost 1.2 million migrants will lose their jobs due to the pandemic, and the country has informed the Bangladeshi high commission about this gloomy scenario. Also, a UNDP report (2020) indicates that some key host countries are asking Bangladesh to take back their migrants, especially the undocumented ones, as these economies are trying to recover from the pandemic impacts.

Returnee migrant workers were among the first to be pointed out for carrying the virus into the country when Bangladesh reported its first case of COVID-19 on 8 March 2020. The local authorities struggled to keep track of community transmissions from the migrants and whether they were quarantined properly, while panic spread in the community. Amidst this stigmatised attitude of the community, it is unclear how these migrants are accessing health services, especially those suspected of COVID-19 as the infected became the victim of hatred as well as denial of treatment in some instances.

COVID-19 has also claimed the lives of many Bangladeshi migrants. From communications in various Bangladesh High Commissions and media releases, it is found that the virus has claimed the lives of 1,380 Bangladeshi migrants in various countries of the world. There has been 1377 COVID-19 related death of Bangladeshi migrants in 19 countries including the USA, UK, Italy, and the Middle East. Almost 521 migrants had died in Saudi Arabia alone. Moreover, around 70,000 Bangladeshis have been infected by the virus in various counties around the world. The main reason for the Bangladeshi migrants workers being prone to the novel coronavirus is that in the Middle Eastern countries and Malaysia, the majority of these workers stay in congested, unsafe, and unhygienic abode. There is no provision to maintain social distancing and hence this higher rate of contamination. Twenty-three thousand Bangladeshi have been infected by the virus in Singapore alone. However, Singapore also has a negligible record of death of migrants, due to the proper isolation procedure and prompt arrangement of health care facilities. The number of female returnee migrants due to COVID-19 is comparatively lower, but they are in a much dire situation at home. Building Resources Across Communities (BRAC), the largest NGO in Bangladesh, helped some female returnee migrants from Saudi Arabia to open a catering service, but they could not make much business during the lockdown (Hasan, 2020).

The BRAC (2020) migration programme arranged for a survey to get an idea about the well-being of the return migrants during the time of the pandemic. They surveyed 558 migrants during April and May, which focussed on the life and livelihood of these return migrants. Some major findings have surfaced from this survey, which indicates around 87% of the respondents who lost their job and came back due to the pandemic have no source of income at present; 74% of the survey respondents stated that they are suffering from extreme stress, mental trauma, and fear and a sense of uncertainty; 34% said that they have no savings of their own; 91% stated that they have not received any government or non-government assistance after returning.

During times of misery, migrant households engaged in distressed asset sales to get food and meet necessary livelihood demands when remittances were not available. It is usual for migrants to remain highly indebted due to the high initial migration costs, for which they ultimately have to return. When remigration is an uncertain option, the returnees go back to rural areas where the employment opportunities are already low. Their previous accumulated debt and lack of employment opportunities would ultimately put pressure on the rural economies and create pockets of poverty, mainly in the migration-prone districts (Siddiqi et al., 2020). It is feared that in post-pandemic situation, poverty rate may potentially increase alarmingly from the current 20.5% to 44% for the country (Siddiqi et al., 2020).

Global Shocks and Impacts on Migrant Workers and Remittances Flow

Shocks, Incentives, and Supports

Migrant workers are always vulnerable to exploitations, denied proper wages, and repatriations from their destination countries, mainly during times of economic, financial, health, and/or political turmoil; for example, the Gulf Crisis of 1990–1991 resulted in the return of many migrants from that region. Before GW, Kuwait employed 70, 000 Bangladeshi workers and was the third largest source of remittances to Bangladesh. Following the crisis, there has been stricter control on illegal and undocumented migrations in the Gulf states. The vulnerability of the Bangladeshi migrants mainly roots in the fact that the country has an almost equal number of documented and undocumented migrants, and the illegal status of these undocumented ones makes them the first to be shunned in times of crisis (Kibria, 2004). Although there were no specific measures taken to avoid the GW impact on the migrant workers of Bangladesh, an emergency management committee was set up to constantly monitor the economic condition of the country and to take necessary steps to mitigate the adverse effects.

Since then, Bangladesh has tried to diversify its international labour market to the East and Southeast Asian countries. By 1994, Malaysia became one of the significant destinations for Bangladeshi workers. When AFC originated from Thailand in 1997 and spread to the Southeast Asian region with falling currency value and increased public debt, it also brought along the economic crisis to the affected countries. As a result, a large number of Bangladeshi workers lost their jobs and were deported. The total number of Bangladeshi workers in Malaysia declined from 66,631 in 1996 to 2,844 in 1997 and then further to 551 in 1998. Nonetheless, a large outflow of manpower to the Middle East and the non-affected East Asian countries, like Singapore and Hong-Kong, more than compensated for the drop of labour flow to affected Asian nations, and the remittances flow to the country increased by 5% in 1998 compared to its previous year.

To avoid mass deportation, the then prime minister of Bangladesh initiated the legalisation of visa for about 150,000 Bangladeshi migrants who went to Malaysia with a false document, tourist visa or illegally via the Malaysia–Thailand border. Around 8,000 more illegal migrants returned from Malaysia in the face of the crisis and about 5,000 illegal migrants faced deportation from South Korea.

Bangladesh had experienced a huge number of migrant outflows for 2 consecutive years before GFC had started. During GFC, the number of migrants stood at 1.7 million, sending around US$7.9 billion as remittances to Bangladesh in FY 2007–2008. Some major destination countries such as the UAE, Malaysia, and Singapore reconsidered the recruitment of foreign workers in the face of the sluggish economic growth in their own home countries, which led to lower demand for workers. However, during the July–February quarter of FY 2008–2009, remittances flow increased by 27.1% compared to the same period in the previous year.

In the face of the GFC crisis, Bangladesh Bank took steps to improve the effectiveness in transferring remittances, and the government planned a seven-point strategy that involved extending its manpower market as well as looking for new host countries in Europe. However, the stimulus package offered by the government for boosting the economy did not have any provision for the return migrants (Billah, 2009).

COVID-19 pandemic has been hitting the global economy hard since early 2020, and many Bangladeshi workers suffered due to sudden loss of employment, with most of the cases without any compensation to cushion the blow. The pandemic has thrown the Bangladeshi migrant workers into a never-ending uncertainty. Three kinds of situations have been created for migrant workers. First, migrants who were already working abroad but had lost their jobs are now worried about coming back to Bangladesh; second, migrants who have been newly recruited are worried about travelling to the country of destination to safeguard their contracts; and thirdly, migrants who came to Bangladesh for various purposes and got stuck are worried about retaining their contracts, uncertain that their recruiters will be flexible enough to consider their situation (Hasan, 2020).

Before Bangladesh closed its borders in March 2020, almost 400,000 workers returned for various reasons, but mostly due to the impact of COVID-19 in the destination countries. There is uncertainty revolving around their opportunity to remigrate and be reinstated in their overseas employment. The pandemic is also having a detrimental impact on the migrant workers, who are currently stranded in different countries practising strong lockdown measures. These migrants are facing disgrace, prejudices, and discrimination in the host countries, given their limited opportunities of maintaining physical distance and lack of access to healthcare services (UNDP 2020).

The government of Bangladesh (GoB) has taken multiple measures to secure the livelihood of the return migrants. Bangladesh Bank has also announced an opportunity for the deported migrants and their family members to access loans up to US$6,250 without showing any documents relevant to overseas. Loans above the amount can also be accessed upon presenting papers relating to the wage earners scheme. Training will be provided to those who have brought back specific skills from abroad. A one-off benefit of around US$3,750 is being offered to the families of both documented and undocumented migrants. Migrants can draw loans at 9% (male) or 7% (female) interest rates to either start their own business or invest in small and medium enterprises (RMMRU, 2020).

The government of Bangladesh has already mobilised US$386 million in the budget of 2020–2021 to encourage the migrant workers to send their money through the official channels. Many banks are already providing an extra cash benefit over the existing 2% to the remittance beneficiaries, thus increasing the attractiveness of sending remittances via formal channels. The Probashi Kallyan Bank has decided to allot a US$62.5 million loan on easy terms to the migrants who have lost their jobs due to the pandemic. Moreover, the Wage Earners’ Welfare Board has created a fund to disburse loans through various banks, on easy terms, and at low interest rates, for these return migrants to make productive investments (UNDP, 2020).

As a part of its ongoing efforts, Bangladesh has been trying to reach its development partners, and ADB has already provided a loan of US$500 million on top of the US$150 million of initial financing. The Bangladesh Bank is trying to ensure liquidity in the market while stabilising the foreign exchange rate (Aneja & Islam, 2020).

Conclusion and Policy Recommendations

The majority of the Bangladeshi migrant workers are employed in the tourism, hospitality, and construction sectors in the Middle East and South-East Asian countries. Many have already been laid off due to the dampened economic prospect from the outbreak of the coronavirus in those countries, which was forecasted to lower the overseas employment and remittances flow to the country. However, to the surprise of all predictions, remittances flows to Bangladesh rose dramatically by about 54% in July 2020 from December 2019. An annual 18.5% rise of remittances has been recorded despite a 67% fall in employment in 2020 compared to its previous year (Bangladesh Bank, online; BMET, online). This uplift in the flow of remittances was possible due to GoB’s proactive measures such as providing incentives to direct the remittances to the formal channels as well as by the repatriation of funds by the migrants in fear of future uncertainties and job loss. Since the world is still passing through the pandemic situation and knowing that the effect of any shock on migrant workers has delayed or lag effect on the remittances flow, GoB requires to monitor the situation relating to overseas employment of its manpower resources closely and take proactive and appropriate measures.

Migrant workers are most vulnerable to the disease during the current pandemic situation in the host countries as they have to live in crowded dormitory-styled labour camps, where social distancing cannot be maintained. Many host countries, in the face of the pandemic, have been putting pressure on Bangladesh to repatriate their migrant workers, although Bangladesh has not willing to accept the offer due to the high risk of contagion these returnee migrants may pose for their family and community members. However, as the travel ban lifts, the economy of Bangladesh is likely to be burdened with high number of unemployed migrant workers.

The economy of Bangladesh has also been affected by a prolonged period of lockdown (26 March–30 May 2020) implemented to contain the pandemic; thus, employment opportunities for these return migrants remain low in the country. The lockdown has badly impacted the industrial as well as the service sectors, and almost 4–12 million jobs were permanently lost during this period. Although the country has been gradually reopening its activities starting from early June 2020, economic activities will take longer to regenerate in full form amidst a surge in COVID-19 cases in the major cities of the country. The situation may further jeopardise the current labour market condition of the country while the increase in unemployment continues.

Policy Recommendations

The pandemic policies from the government should be inclusive of the migrant workers’ socio-economic and psychological support while acknowledging their economic contributions. The policymakers and government should further address this important issue of supporting its manpower resources by designing and prescribing coordinated policies and providing a supportive environment for the migrant workers. The current stigmatised and discriminatory attitude towards migrant workers may result in an inability of these migrants to reintegrate into society. The authority should prepare some guidelines to deal with an emergency and allocate a budget for the incidents of current and future similar health and economic crisis. The government should provide public health care support to the returnee workers to change the perspective of the society towards them, especially from highly infected countries such as Italy and other Middle Eastern countries.

Bangladesh has a highly developed NGO sector working in various areas including microfinance and public awareness, simultaneously contributing towards the strengthening of the local government institutions of the country (Baroi & Panday, 2018). As such, GoB can use this network to disseminate awareness not only by addressing the denouncing of these returnees by the community, but also by providing preliminary health care services to the same.

Considering the success of the cash incentive scheme that had been implemented last year, the Ministry of Finance should extend this for the next fiscal year by recommending it for the upcoming budget cycle. Digitalising the remittances procedure on both the senders’ and receivers’ ends will ensure a safe flow of remittances for the households that are in dire need of funds.

Social safety net programmes, as well as social protection coverage, should be extended to cover the return migrants, either in cash or in-kind, to facilitate their well-being and prevent them from falling back into poverty. The government should also design sustainable programmes aiming towards the economic, psychological, as well as social support of the return migrants, based on the assessment of their long-term and short-term vulnerabilities. Diplomatic corps should engage in dialogues and negotiations with the destination countries to stop the forced return for the migrant workers during the pandemic time and request extensions on the visas and work permit of those who cannot arrange for travel back home due to the travel restrictions in place. It would be beneficial for both host and home countries to provide protection and restore the employment of migrant workers during and after the pandemic as they would support labour–market gap in the host countries and send remittances to the home country.

Migrant workers usually gain many advanced skills in the sectors they are employed during their overseas contract. GoB can formulate an online database that will keep a record of these skills of the return migrants and employ them in the relevant sectors when any employment opportunities arise. Private sectors should be encouraged to use these data portals and employ these returnees with a specific skill, wherever possible. Creating domestic employment opportunities for the return migrants, especially in the infrastructure development and other public provisions during and after the pandemic would cushion the employment-related stress for the migrant workers. Allocating public and international support funding can boost up paid vocational training for the returnee migrants, which would increase the employment opportunities for them during and after the pandemic. Bangladesh should adjust its training, education, and human resource policies to take advantage of these job opportunities that have been created by the coronavirus pandemic in the health care and information technology (IT) sectors. Increased training for lab technicians, other supplementary health service-related work, as well as IT and data input-related training can also be introduced in technical and vocational training centres for the future extension of Bangladesh labour market in the overseas countries.

Bangladesh government should work with its development partners to address the fundamental challenges that migrant workers face. At the same time, the support extended to the migrant workers will also depend on the capacity and performance of the institutions entrusted with the duty of implementing them. As such, the capacity of these institutions along with those of the Labour Welfare Wing of Embassy of Bangladesh abroad should be advanced. Provided that these institutions are properly trained and guided as well as monitored, they can play a critical role in negotiating with the destination countries’ authorities to engage the migrant workers abroad when the pandemic subdues. Implementation of well-thought policies in a timely fashion would assist to maintain the overseas labour market and augment the inflow of remittances to enhance the developmental potential for Bangladesh.

Footnotes

Declaration of Conflicting Interests

Funding

The authors received no financial support for the research, authorship and/or publication of this article.