Abstract

The purpose of the present study is to assess how bank concentration affects female entrepreneurship in 70 developing countries using data for the period 2000–2019. The empirical evidence is based on ordinary least squares fixed effects and the Generalized Method of Moments regression. Three main female entrepreneurship outcome variables are employed, namely women’s entrepreneurial activity rate, women business leaders and the number of jobs created by businesses run by women. Two main moderating variables are employed, namely education and access to credit. The analysis is tailored towards assessing the direct impact of bank concentration on female entrepreneurship outcomes as well as the indirect effect pertaining to how education and credit access, as moderating variables, influence the effect of bank concentration on female entrepreneurship. The results show that bank concentration broadly reduces female entrepreneurship. The negative effect is robust to the inclusion of additional control variables, an alternative estimation technique and a different measurement of bank concentration. Within interactive regressions’ purview, the unconditional effect of bank concentration reduces female entrepreneurship, while education and credit access further complement bank concentration to reduce female entrepreneurship. This evidence of negative synergies is explained, and policy recommendations are provided.

The purpose of the current research is to assess how the concentration of banks impacts the entrepreneurship of women in developing countries. The motivational elements underpinning the purpose of the study are numerous. For instance, women’s empowerment has been the subject of increased scientific focus in the last few decades as a way to improve economic status, mobility, health and women’s participation in decision-making (Afrin et al., 2008; Asongu et al., 2025; Sundström et al., 2017). Furthermore, the sustainable development agenda recognises that women’s empowerment and gender inequality are important factors in increasing women’s opportunities and reducing the gender gap. The authors identified three types of women’s empowerment: political, social and economic. The study concentrates on economic empowerment in the research within the specific remit of women’s entrepreneurship.

Numerous scholars have demonstrated that women are more inclined to favour measures that help other women, such as healthcare and education, when they are given politico-economic power. As maintained by Tchamyou et al. (2023), Kamaluddeen (2019), Asongu et al. (2025) and other sources, women who have access to savings accounts, bank accounts and other financial institutions have greater authority over their earnings and can pay for both personal and productive needs. Additionally, adolescents have greater control over how they choose to spend their time, be it working, playing, earning money or learning (Aker et al., 2016; Asongu & Odhiambo, 2018; Chant, 2016). When it comes to choosing a career, getting married or using contraception, they might have more freedom in their lives (Aker et al., 2016; Asongu & Odhiambo, 2023). They might also be in a better position to choose where and how to work (Field et al., 2016), which could boost their income and productivity and help them escape poverty (Jack et al., 2016).

Even with all of the advantages that women’s empowerment can offer, developing nations continue to lag behind. Women actually participate less in politico-economic activities (Nchofoung et al., 2023). According to Asongu et al. (2025), a majority of studies in the extant literature have ignored any potential relationships between bank concentration and women’s empowerment. Whereas Asongu et al. (2025) have focused on the nexus between bank concentration and female political empowerment, the current investigation is tailored towards assessing the linkage between bank concentration and gender economic inclusion within the specific remit of female entrepreneurship. Moreover, the size of the sample in this study, which includes up to 70 developing nations, enables the study to depart from Asongu et al. (2025) on a multitude of fronts: (a) As previously highlighted, the first distinguishing feature is a focus on economic empowerment within the specific remit of female entrepreneurship contrary to political empowerment. (b) Instead of using information sharing offices (i.e., public credit bureaus and private credit registries) as moderators of the bank concentration channel, the present study uses education and credit availability as moderators.

This study is positioned differently than the existing literature on contemporary entrepreneurship, which has concentrated on the connections among innovation, business constraints, relevant technologies and entrepreneurship for overall sustainability and reduction of income inequality (Bouanza et al., 2024; Régnier, 2023); technological change and the significance of frugal innovations for entrepreneurial development (Khadria & Mishra, 2023); Chinese entrepreneurship and technologies during global challenges (Shi, 2023); development of frugal innovations that are seen as highly innovative from the viewpoint of sustainable entrepreneurship (Rao & Liefner, 2023); and connections between ICT and business opportunities (Fuamba et al., 2023). This article’s other sections are organised as follows: A concise overview of the literature is provided in the second section. In the third section, the data and technique are disclosed. The results are presented and analysed in the fourth section, and the study is concluded in the fifth section.

Theoretical Underpinnings and Literature Review

The investigated linkage between bank concentration and female entrepreneurship can be supported theoretically by four essential theoretical pillars: (a) the financial inclusion theory; (b) the job search theory; (c) the theory of substantive representation of women (SRW); and (d) the creative capital theory (CCT). On the theoretical premise of the financial inclusion theory, it is noteworthy that the theoretical literature on the linkage between financial inclusion and gender empowerment is largely consistent with the importance of providing financial access in order to enable the female gender to realise that maximum of her potentials (Asongu et al., 2025). It is also worthwhile to note that Nchofoung et al. (2024a) have used the theory of financial inclusion beneficiary to establish the relationship between financial inclusion and women’s empowerment. The theory is pertinent to the current study because, according to the theory of financial inclusion, gender access to finance creates opportunities with which to fund and achieve inclusive development outcomes, including gender economic inclusion within the remit of entrepreneurial activities. In what follows, more perspectives of the theory are provided.

First, the fundamental theoretical framework for this inquiry is the financial inclusion beneficiary (Asongu et al., 2025). In this sense, financial services should be seen as a public benefit, and the public goods theory of financial inclusion holds that people’s use of attendant services and access to them should not be restricted. Therefore, the existing financial institutions ought to make use of extant structures to improve financial access to the population (Ozili, 2020). All people, regardless of age, gender or ethnicity, have access to and are free to use the attendant services since they are a public good (Nchofoung et al., 2024a). Credit availability is used as a moderating variable because market power or bank concentration limits access to credit, which is essential in female entrepreneurship (Bennardo et al., 2015; Boateng et al., 2018; Karapetyan & Stacescu, 2014). Another moderator that is used in the present study is education and thus the importance of the ‘job search theory’ in providing a theoretical basis for such an inclusion.

Concerns about students entering the workforce after graduation are largely based on the predicted pay and/or wage that the related work would provide them with a means of subsistence so that they can become capable of maintaining a life, according to the second strand, or ‘job search theory’ (Asongu, 2024; McMahon, 1987). To put it simply, the expected utility depends on comparing the quality of life during one’s time in school to the standard of living after graduating and finding employment. According to the corresponding theory, students’ expectations about their expected salaries may cause them to become self-employed through entrepreneurial endeavours or find employment in private or public organisations that pay what they expect or find appropriate. It is also important to stress that the anticipated advantages align with knowledge from the body of existing research on the topic (Asongu, 2024). Moreover, it seems intuitive that if students are given financial access tools like credit availability, the expected benefits regarding employment and quality of life can increase.

In the light of the above, the second theoretical underpinning is in line with the present study because the purpose of education is to eventually get employed, either in the public sector or in the private sector, especially by means of entrepreneurial activities that are tailored to promote women economically. It follows that educated people can better be informed on how to circumvent constraints associated with limited financial access owing to high banking concentration. It is relevant to note that Asongu (2024) recently employed financial access and education in the interactive regressions in order to fight female unemployment. Hence, beyond the discussed theoretical justification, there is also an empirical justification for the inclusion of the two sets of moderators.

Third, according to relevant research, CCT is based on the idea that a valuable and innovative workforce—comprising citizens involved in economic spheres—plays a key role in a country’s political and economic growth (Lopes et al., 2011; Zogo et al., 2025). When applied to this study’s context, it becomes clear that bank concentration influences access to credit, which is necessary for creative capital relevant for female entrepreneurship as conceived in the present study. Hence, CCT aligns with the theory of SRW in the perspective that capital from financial institutions that is constrained by bank concentration can enable more women to be represented among the population of entrepreneurs (i.e., women being substantively represented among entrepreneurs), in line with attendant literature on SRW (Kodila-Tedika & Asongu, 2018; Zogo et al., 2025).

Although the CCT has faced criticism in some academic circles, arguing that economic development from a specific working class needs innovation rather than just creativity (Amabile, 2018; Storper & Scott, 2009), considering this study, bank concentration which limits competition in the banking industry can affect women’s access to credit and, by extension, women’s ability to realise their innovative and creative potentials within the framework of entrepreneurship. CCT aligns with the context of this study in view of SRW in entrepreneurial circles.

Literature Review on the Effects of Financial Access on Women Entrepreneurship

Two primary strands can be used to discuss the related literature, especially as it pertains to the positive and negative effects of financial access on women entrepreneurship. This section is developed according to the same sequence that was emphasised.

The first part focuses on how financial education affects the performance of women micro-entrepreneurs’ businesses and its investigation by Tumba et al. (2022). The study employs a survey research design to collect information from 247 female business owners in six states in northeastern Nigeria. The findings indicate that financial education, cash forecasting and bookkeeping, as proxies for financial literacy, have a noteworthy influence on the performance of the business of female entrepreneurs. Furthermore, they show that the two factors that have the biggest and least impact on the variation in the business performance of female micro-entrepreneurs are bookkeeping practices and financial knowledge, respectively. This volatility is least affected by cash forecasting. This implies that financial knowledge is essential to the success of female micro-entrepreneurs.

Principal component analysis (PCA) and cross-sectional data methods are used by Esmaeilpour and Karami (2023) to investigate the effect of financial inclusion through fintech on women’s financial empowerment with a sample of 113 nations. Their findings demonstrate that, in nations with low levels of gender discrimination, there is a positive and significant association between women’s financial empowerment and financial inclusion through fintech. Nonetheless, in nations where there is widespread gender prejudice, this effect is minimal. Gender disparity constitutes a barrier, preventing women from achieving financial independence.

By emphasising the growth of female entrepreneurs, particularly in developing countries, Yingjun et al. (2021) add to the accumulation of existing material. According to their study, the growth of small and medium-sized businesses (SMEs), particularly those run by women in Bangladesh, is significantly influenced by two factors: ease of business creation and access to outside funding. The current credit status must therefore be extended in order to boost female-owned SMEs.

With 144 nations, Hasan et al. (2023) use a cross-sectional approach to assess the effect of digital financial literacy on women’s financial inclusion. Higher digital financial literacy among female entrepreneurs is associated with a higher likelihood of using formal banking channels, according to the study’s probabilistic regression results.

In Ethiopia, Abebe and Kegne (2023) investigate the connection between women’s economic empowerment and financial inclusion. Their results, which were obtained by using instrumental variable and endogenous switching regression techniques, demonstrate that women’s economic empowerment in Ethiopia is positive and statistically significantly impacted by financial inclusion, suggesting that increased access to financial services improves women’s economic outcomes.

The research carried out by Iram et al. (2023) aims to ascertain the degree to which financial awareness mediates the gap between behavioural biases and financial literacy in female entrepreneurs. Utilising AMOS 21, structural equation modelling was used to examine a random sample of 346 Pakistani women business owners. Financial literacy has been proven to have no correlation with mental accounting bias, but it does have a strong direct influence on lowering anchoring and herding prejudices. Financial literacy significantly decreases mental accounting and herding tendency for financially conscientious women, according to the moderation analysis, which also indicated intriguing indirect effects. The association between financial literacy and anchoring bias is, however, not adversely accelerated by financial mindfulness.

The effects of digital financial inclusion on women entrepreneurs are investigated by Yang et al. (2022) utilising a nationwide sample made up of matched data from a nationally representative survey and a digital financial inclusion index. The findings demonstrate how digital financial inclusion strongly encourages women to pursue entrepreneurial endeavours. They discovered that digital financial inclusion can reduce the financial barriers faced by women and help them obtain business information to lessen information gaps.

Gang et al. (2022) examine how the gender distribution of informal economic activity is impacted by new funding choices. They discover compelling empirical evidence maintaining the relevance of financial access in boosting the doing of business in India’s unorganised sector firms by utilising nationwide data on unorganised (informal) enterprises collected by India’s National Sample Survey Office in 2010/2011 and 2015/2016.

As highlighted earlier, the second strand on negative effects is sparse. In this strand, using the mediating variable of perceived entrepreneurial behavioural control, Nguyen (2020) examines the direct and indirect effects of personal and environmental factors on entrepreneurial intention. Using structural equation modelling analysis, the researchers found that students’ perceived environmental factors are significantly correlated with their perceived entrepreneurial behavioural control, serving as a mediator between the environmental factors and entrepreneurial intention. The sample consisted of 635 students from 11 universities in Vietnam. The author claims that without entrepreneurial behavioural control, financial availability alone is not enough to impact entrepreneurial ambition.

As recently shown by a systematic review of female entrepreneurship by Deng et al. (2025), according to Simarasl et al. (2022), there is a strong emphasis that access to resources such as networks, mentorship and funding is essential for female entrepreneurs to overcome challenges and achieve business growth. Furthermore, other studies have concentrated on social cognitive aspects, including confidence, resilience and perceived support from family and friends, as essential elements contributing to women’s entrepreneurial success and decision-making (Shetty et al., 2023). In order to address attendant obstacles, in view of Angulo-Guerrero et al. (2023), feminist empiricists advocate for enhancing women’s skills, education and managerial experience. Rugina and Ahl (2023) is also of the viewpoint that the fluid and energetic characteristics of masculinity and femininity, which influence individual behaviours and result in different life experiences for men and women, should be taken into account. Deng et al. (2023) posit that the family’s role in offering emotional support, practical help and financial aid is essential for female entrepreneurship, while in line with Welsh et al. (2021), in situations where family backing is strong, women are generally better prepared to tackle challenges in entrepreneurship. Furthermore, Dewitt et al. (2023) posit that more egalitarian family arrangements, where responsibilities are shared, create a more supportive atmosphere for women to engage in entrepreneurial pursuits. Nonetheless, these contemporary studies have failed to address the problem statement considered in this study, as stated in the introduction, especially with a robust methodological framework that is tailored to address most dimensions of endogeneity as clarified in the methodology section.

In the light of the above, two main testable hypotheses are examined in the empirical analysis section:

H1: Bank concentration reduces women’s entrepreneurship. H2: Education and credit moderate the negative effect of bank concentration on women’s entrepreneurship.

In the section that follows, the study examines whether the above testable hypotheses withstand empirical scrutiny. H1 is examined using linear additive models, while H2 is assessed within the framework of interactive regressions.

Data and Empirical Strategy

Description of the Data

Imbalanced panel data are used for a sample of 70 developing nations from 2000 to 2019 in this analysis. The accessibility of data informed the selection of the study period and sample size. Accordingly, the extant Global Entrepreneurship Monitor (GEM) data are available for the 70 countries at the time of the study and thus potential bias may not be apparent because the available data at the time of the study is used for the research. The descriptive statistics for each variable utilised in this investigation are shown in Table A1. The nations under investigation are listed in Table A3.

Dependent Variable

The dependent variable is women’s entrepreneurship. It is measured here by three indicators: (a) women’s entrepreneurial activity rate (F/H), which is the share of women-owned businesses or businesses led by women; (b) women business leaders (F%T), which refers to the increasing number and influence of women in leadership positions, particularly in the realm of business; and (c) the number of jobs created by businesses run by women. The data come from the following sources: GEM and Mastercard Index of Women Entrepreneurs (MIWE).

Compared to male entrepreneurs, it is less common to find female entrepreneurs. As recently documented by Minniti et al. (2004), the rate of entrepreneurship is significantly lower among women than among men. Accordingly, the survival of modern market economies depends on entrepreneurship, which creates innovative companies that stimulate competition and maintain economic expansion (De Vita et al., 2014). It is therefore important to know what factors may be at the root of these inequalities.

Independent Variables

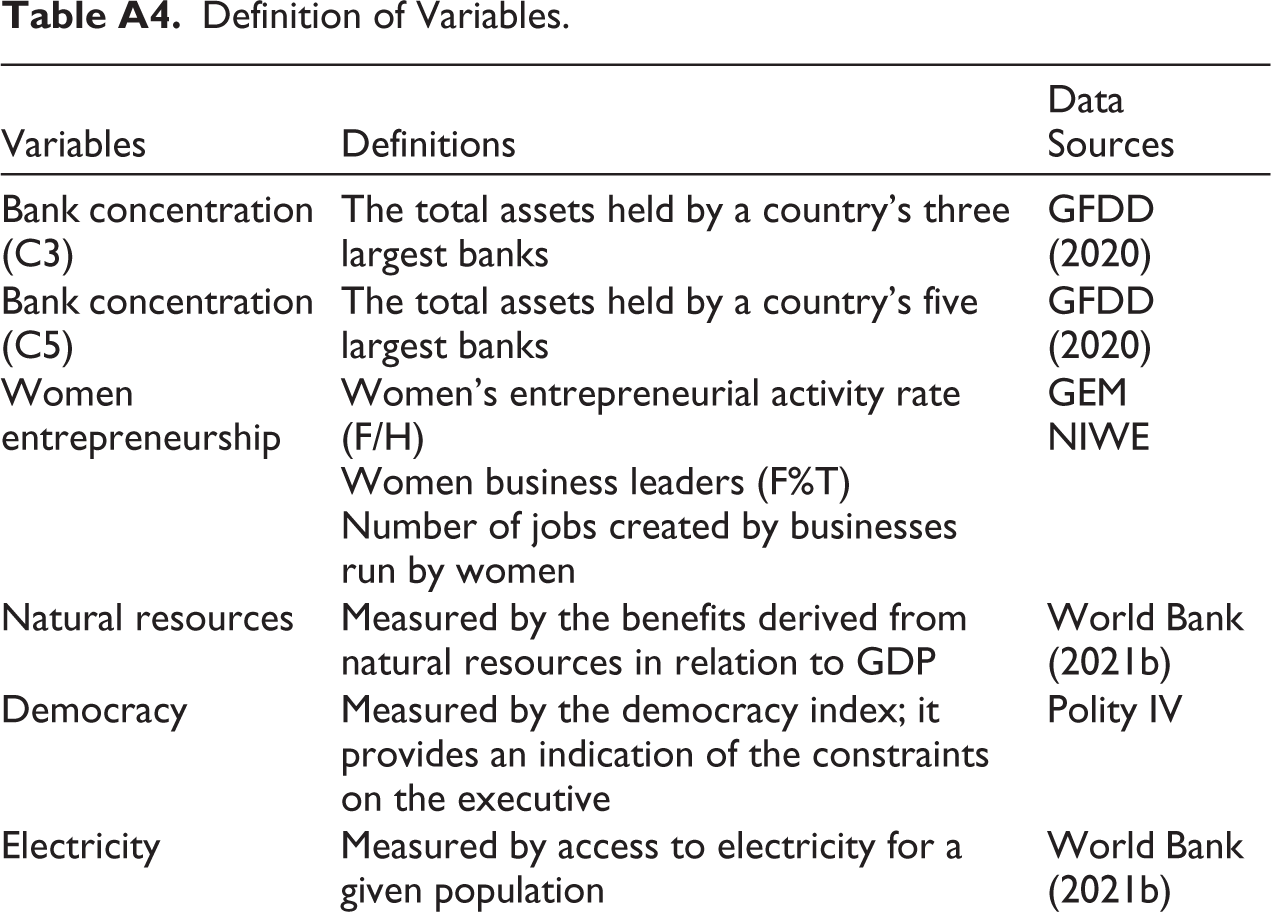

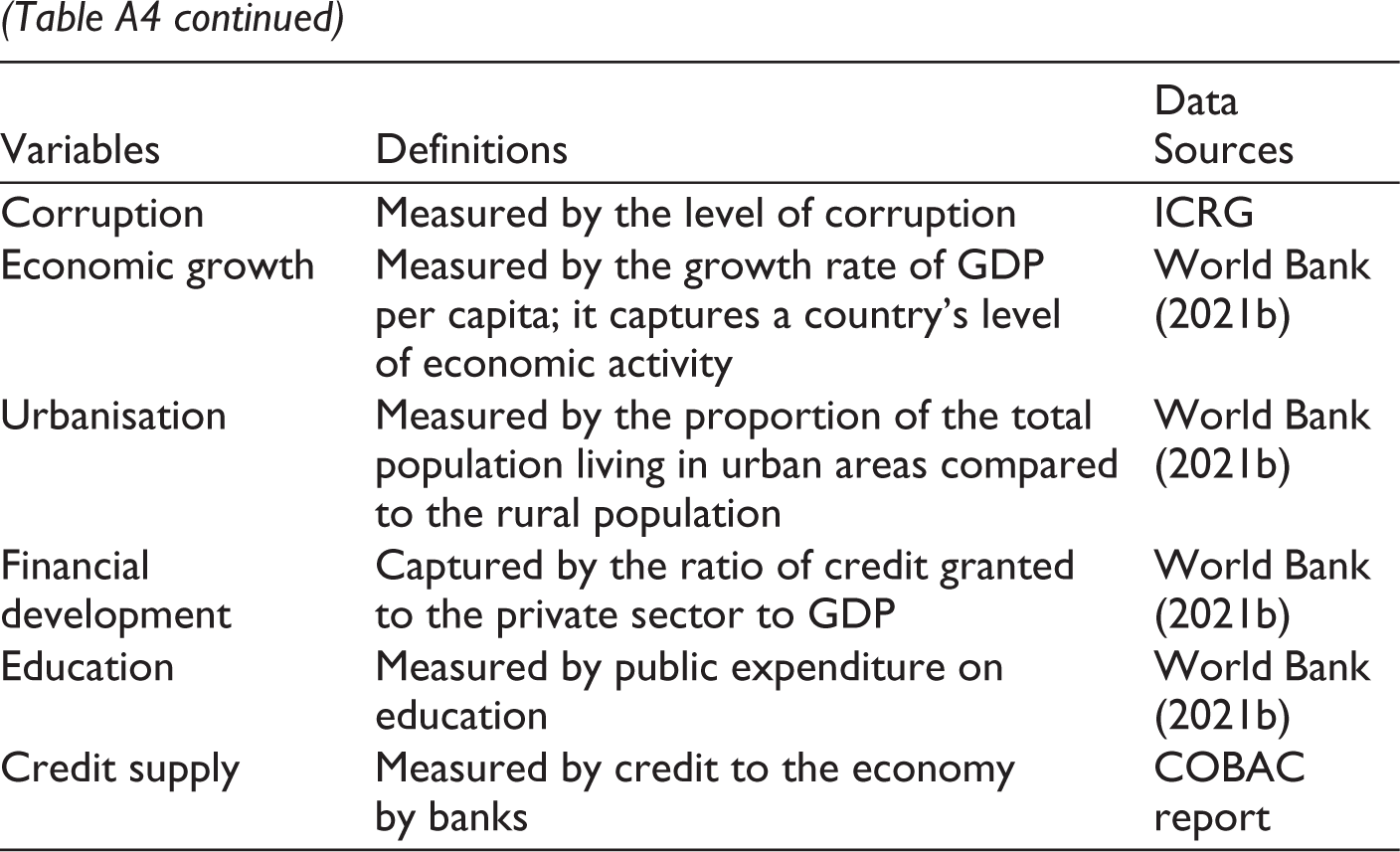

As the main explanatory factor, banking concentration is employed, collected as the total assets owned by a nation’s five biggest banks (C5) and its three biggest banks (C3). The data come from the Global Financial Development Database (GFDD, 2020). As shown in Table A4, two moderators are employed, namely: (a) education, which is measured as the amount of public expenditure in education; and (b) credit supply, which refers to the amount of credit provided by banks in the country.

Consistent with Asongu et al. (2025), banking concentration refers to two distinct realities. A distinction is made between geographical concentration and concentration in terms of activity. Geographical concentration is the agglomeration of banks in a given location. This type of concentration obeys a particular discipline: spatial economics. However, industrial concentration is unanimously defined as a market structure in which the bulk of production is controlled by a small number of banks.

Although both types of concentration are important, banking concentration in terms of activity is analysed for two principal reasons. The first reason is theoretical and is based on the fact that, to the best of knowledge, the theoretical debate on the effect of the geographical concentration of banks is not sufficiently established (Asongu et al., 2025). However, the effects of bank concentration in terms of activity have been the subject of an unresolved theoretical debate that is constantly being revisited (e.g., Harvard School vs. Chicago School). The second justification for choosing concentration in terms of activity is empirical. Empirical studies generally find contradictory effects from bank concentration (e.g., Asongu et al., 2025; Deidda & Fattouh, 2005). The challenge is therefore to provide new empirical evidence to fuel the debate on the effects of bank concentration in terms of activity.

Control Variables

To substantiate the relationship between banking concentration and women’s entrepreneurship and to avoid variable omission bias, the present study is tailored to account for a selection of current controls that have been demonstrated to be crucial for women’s entrepreneurship (Ghouse et al., 2017; Giménez & Calabrò, 2018; Hechavarria et al., 2019; Pallares-Blanch et al., 2015). Five determinants are introduced: electricity, financial development, natural resources, urbanisation and per capita income. The choice of these determinants is further substantiated in what follows.

Electricity enables women entrepreneurs to use machines and power tools to automate tasks, increasing their efficiency and productivity (World Bank, 2019). This allows them to produce more goods and services in less time, resulting in an increase in their income streams. Other studies, such as that by Llussá (2009), highlighted the role of financial development on women’s entrepreneurship. They showed that financial development affects particular demographic groupings in a distinct way in terms of their propensity to create new businesses. In addition, a developed financial system offers women entrepreneurs better access to credit, loans and other sources of financing to launch and grow their companies (World Bank, 2021). This enables them to overcome one of the main obstacles to female entrepreneurship, which is the lack of capital.

Third, natural resources are introduced, which through rents can have effects on women’s entrepreneurship. According to a World Bank study in 2019, in developing countries, 43% of women entrepreneurs said that lack of access to markets was a major barrier to their growth, partly due to the concentration of men in the extractive sector.

Fourth, another important determinant is urbanisation. According to the World Bank (2021), urban areas offer a greater concentration of potential customers, facilitating market access for female entrepreneurs. They can therefore sell their products and services more easily and to a larger number of people. Fifth, on the premise of per capita income, another strand of the literature looks at the effects of economic growth on women’s entrepreneurship. Indeed, high-growth enterprises, often referred to as ‘gazelles’, are equated to the success of entrepreneurs and celebrated as fundamental to boosting economies, and women’s entrepreneurship is a driver for socio-economic development (Hechavarria et al., 2019).

Empirical Strategy

The objective of this article is to study the effect of bank concentration on women’s entrepreneurship. The study, therefore, builds on the work of Asongu et al. (2025) and begins by specifying a panel model shown in Equation (1), estimated by pooled ordinary least squares fixed effects (OLS-FE):

where WETit represents women entrepreneurs, BCit is bank concentration, Xit is the vector of control variables, μi is the country fixed effect, Vt is the fixed effects time and εit is the error term. It is relevant to note that the choice of variables has been discussed in the previous section. Although this approach is relevant to the study, it is nevertheless the subject of a major criticism often raised in the literature due to its lack of robustness to concerns about reverse causality (Asongu et al., 2024). To overcome this, a dynamic panel model is specified.

Given that the lagged dependent variable in the model places the model within the framework of the dynamic panel model, using OLS-FE to estimate Equation (1) may result in inefficient estimates (see Nickell, 1981). Furthermore, the use of standard estimators such as OLS-FE would lead to biased results, as they do not take into account endogeneity problems that arise from several sources such as reverse causality, measurement error and omitted variables (Tchamyou, 2020).

A common approach in the literature to correct for these problems is the use of the GMM (see, e.g., the work of Wen et al., 2022, and Blundell & Bond, 1998). One benefit of GMM is that it uses internal instruments to treat the endogeneity of all the explanatory factors. In addition, GMM deals with endogeneity arising from reverse causality and produces valid instruments (Tchamyou et al., 2019).

It is relevant to emphasise that the choice of the OLS-FE empirical strategy is to account for the unobserved heterogeneity dimension of endogeneity, while the adopted GMM approach is meant to account for the simultaneity as well as the unobserved heterogeneity dimensions of endogeneity. Furthermore, the methodological approach is tailored to account for the variable omission bias dimension of endogeneity by employing additional control variables as well as the measurement error concern of endogeneity by employing alternative variables of interest.

Empirical Results

Baseline Results

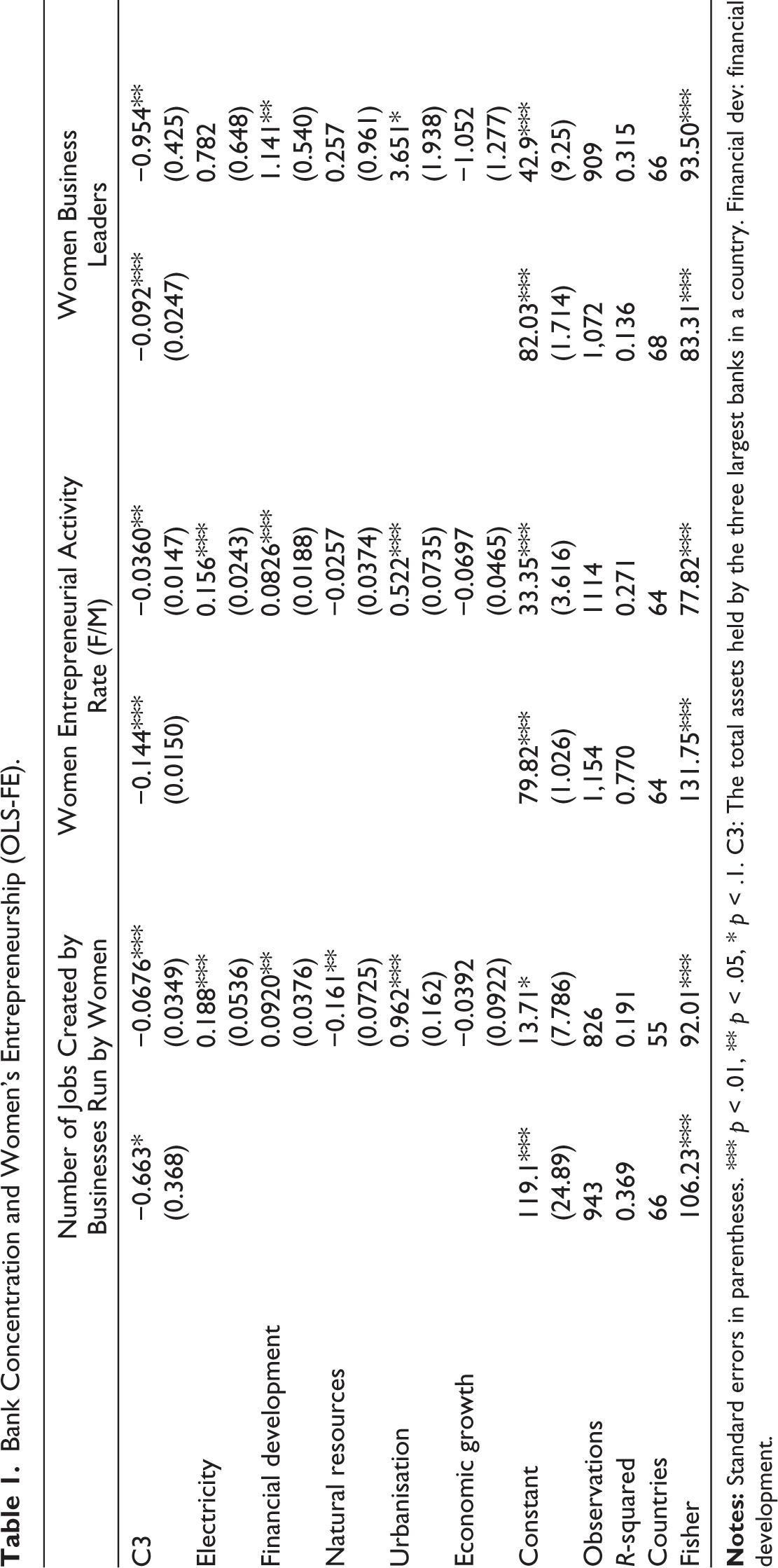

The baseline values calculated using pooled OLS are summarised in Table 1. Table 1 highlights the results of the effect of bank concentration on women’s entrepreneurship without the control variables. Overall, it is found that bank concentration has a negative and significant effect on women’s entrepreneurship.

Bank Concentration and Women’s Entrepreneurship (OLS-FE).

Column 1 of Table 2 presents the results of bank concentration on the number of jobs created by female-led firms. According to the results, the coefficient related to the number of jobs created by female-led firms is negative and statistically significant at the 1% level, suggesting that bank concentration reduces the number of jobs created by female-led firms. Next, in Column 2, the study analyses the effect of bank concentration on the female entrepreneurial activity rate (F/M). As before, the study finds a negative and statistically significant effect at the 1% level, suggesting that bank concentration reduces the entrepreneurial activity rate of women (F/H). The same result is obtained in Column 3 between bank concentration and the number of women entrepreneurs (F%T). One explanation for these findings is that bank concentration or market power reduces competition, which limits the supply of credit by increasing interest rates (Asongu & Odhiambo, 2019; Bain, 1951; Boateng et al., 2018). Thus, large banks tend to favour lending to large companies and men, leaving women entrepreneurs with limited financing options (Asongu et al., 2020). In addition, women entrepreneurs often pay higher interest rates and additional fees on loans, reducing their profit margins and limiting their capacity to make investments and expand their companies (Leitch et al., 2018).

Estimations with Additional Controls.

Several control variables are introduced into the estimates. The coefficient of female entrepreneurship remains statistically significant and is not affected by the inclusion of these control variables in the regression. Access to electricity has a positive and significant effect on women’s entrepreneurship. Access to electricity increases production through the use of machinery and power tools (Gamette et al., 2024). It is important to note the positive effect of financial development on women’s entrepreneurship. This result can be explained by the fact that financial development makes it possible to offer a range of financial products tailored to the specific needs of women entrepreneurs, such as microcredit, tontines and credit guarantees (IFC, 2017). This better meets their needs and enables them to manage their finances more effectively. Finally, a positive effect of urbanisation on women’s entrepreneurship is noted. This is due to the fact that urbanisation can offer better access to markets, business opportunities, infrastructure and services, as well as foster networks and empower women.

Robustness Checks

Sensitivity analyses are performed along multiple dimensions, including the employment of additional control variables, different subsamples and alternative estimating methodologies, in order to verify the robustness of the primary findings. Overall, it is found that the requirements produce results that are comparable to those in Table 1 in all robustness checks.

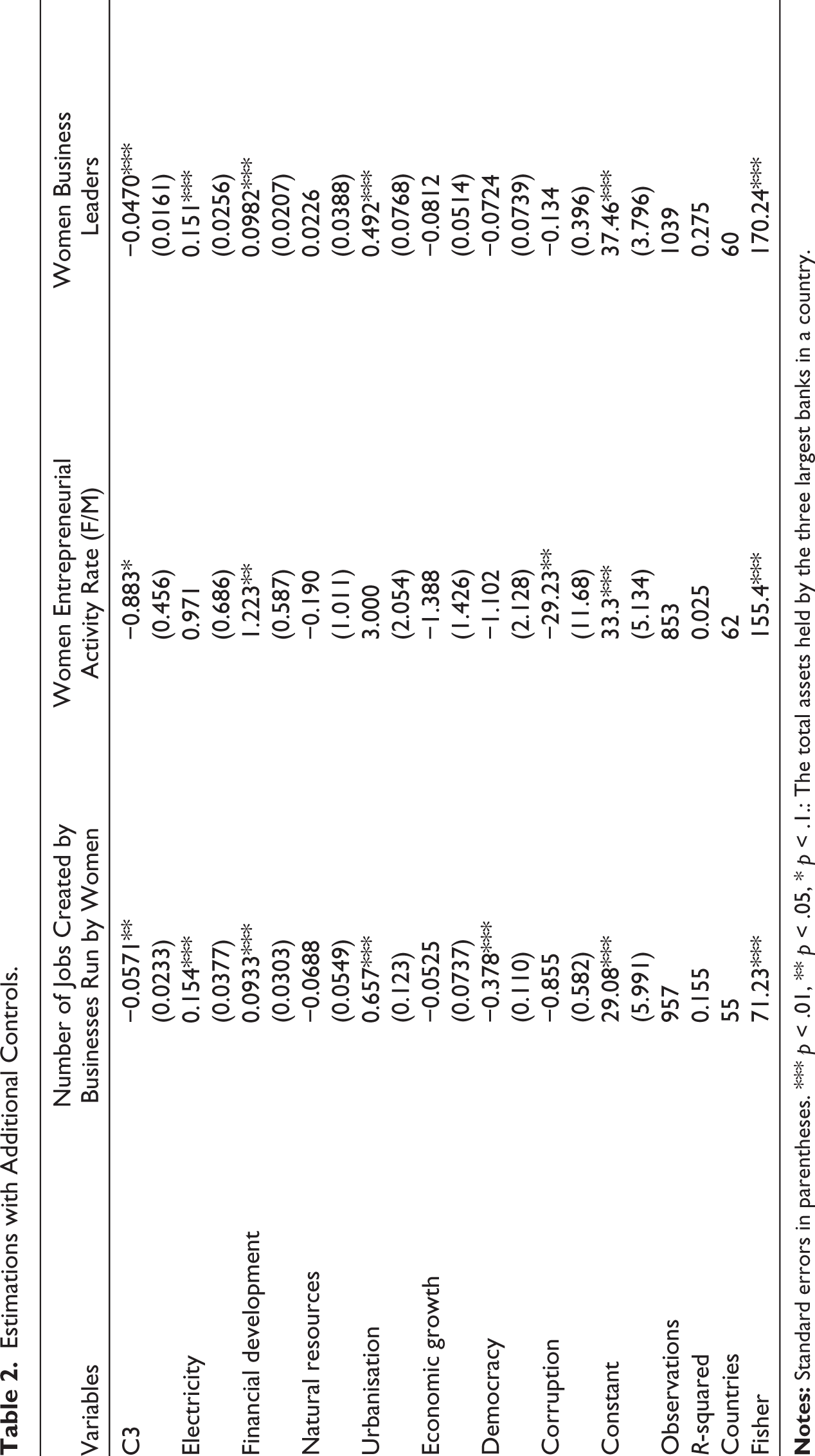

Robustness to Additional Control Variables

Thus far, a statistically significant and adverse relationship between bank concentration and women’s entrepreneurship has been established. It is not possible to completely rule out the idea that this negative link is partly caused by unobserved country factors, though. In order to address this potential issue and guarantee the stability of the calculations, the study accounts for other factors such as democracy and corruption that may have an impact on women entrepreneurs. The results of this exercise are reported in Table 2. By introducing these additional control variables into the model, it is established that bank concentration has a negative and significant effect on women’s entrepreneurship.

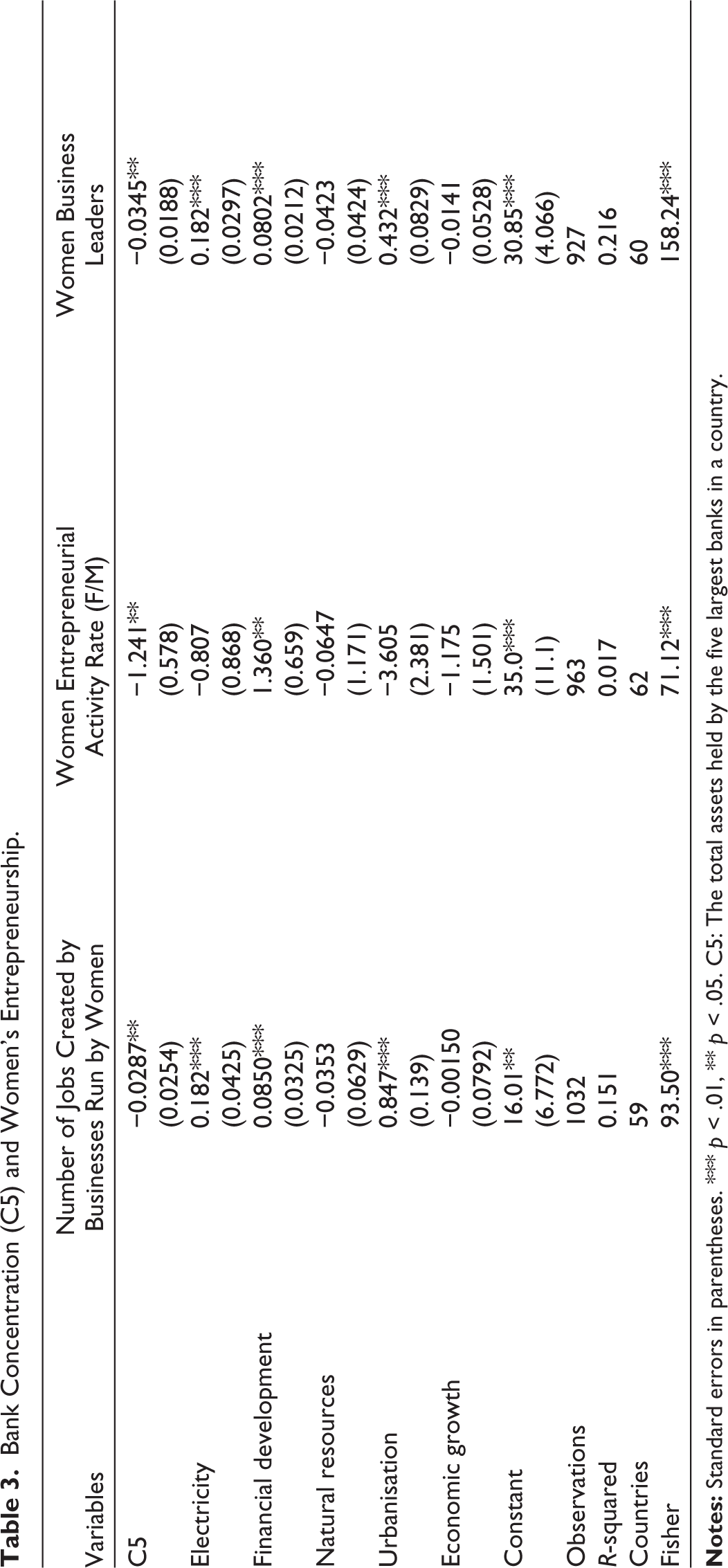

Robustness to the Alternative Measure of Bank Concentration

Different bank concentration metrics to estimate the model are used. The study makes use of the total assets owned by a nation’s five biggest banks (C5). Table 3 shows that bank concentration (C5) has a negative and significant effect on women’s entrepreneurship.

Bank Concentration (C5) and Women’s Entrepreneurship.

Robustness with Alternative Estimation Strategy

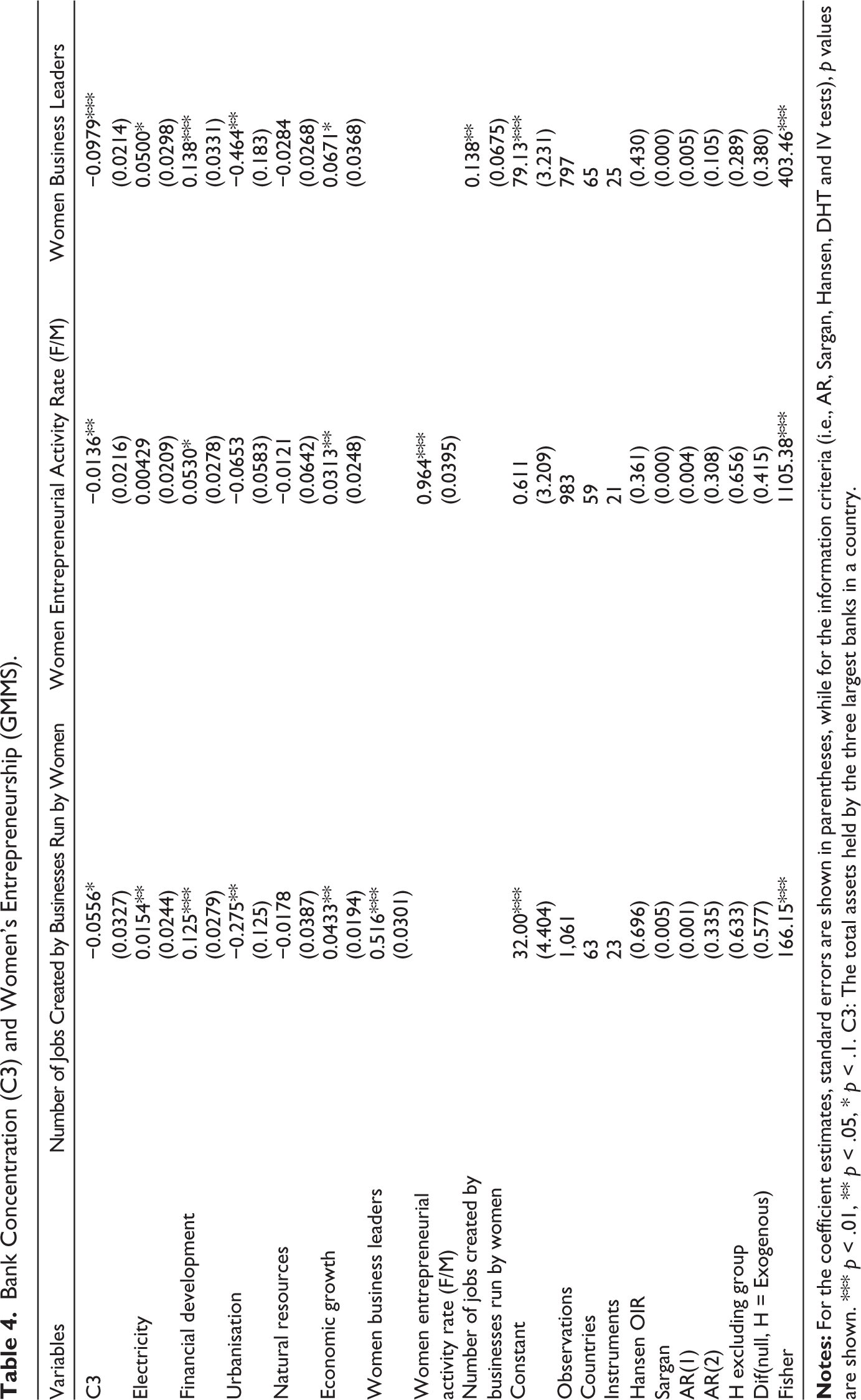

Even while the prior findings support the theory that bank concentration is generally linked to lower levels of female entrepreneurship, it is still worthwhile to investigate the validity of these earlier findings using a different approach. Thus, the study extends the robustness assessments by employing the system GMM proposed by Blundell and Bond (1998), especially as it pertains to the unobserved heterogeneity and simultaneity or reverse causality (Tchamyou et al., 2019). The choice of this method is justified by the fact that it resolves some potential endogeneity problems. Specifically, the GMM system estimator uses an optimal weighting matrix that minimises the asymptotic variance of the estimator. The first differences are needed to eliminate country-specific effects and any endogeneity bias resulting from the correlation of these fixed effects with explanatory variables.

Bank Concentration (C3) and Women’s Entrepreneurship (GMMS).

In line with the GMM results, the coefficients linked to the various measures of women’s entrepreneurship are statistically significant and negative. Consequently, the findings are reliable to the use of alternative estimation strategies.

Analysis of Moderators

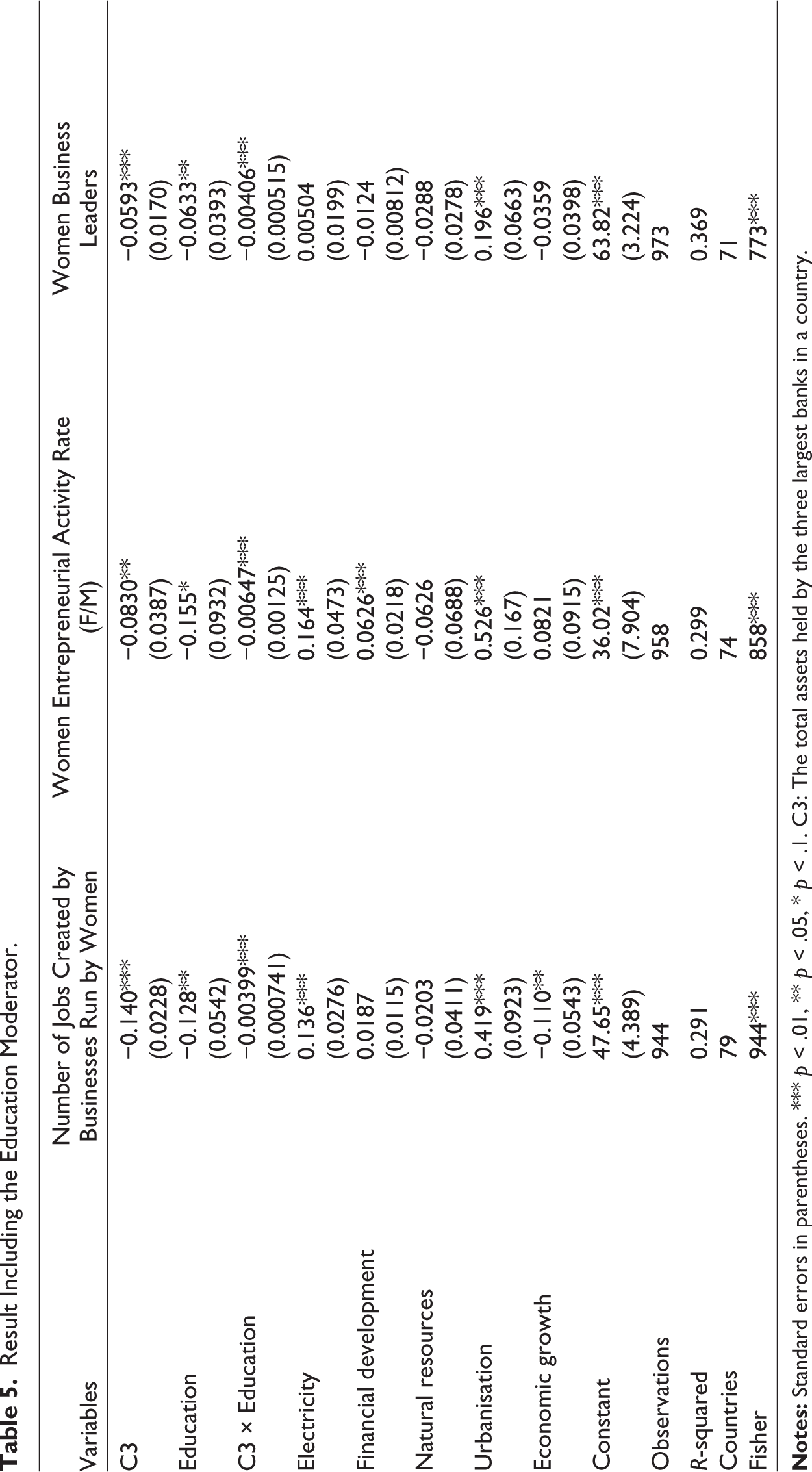

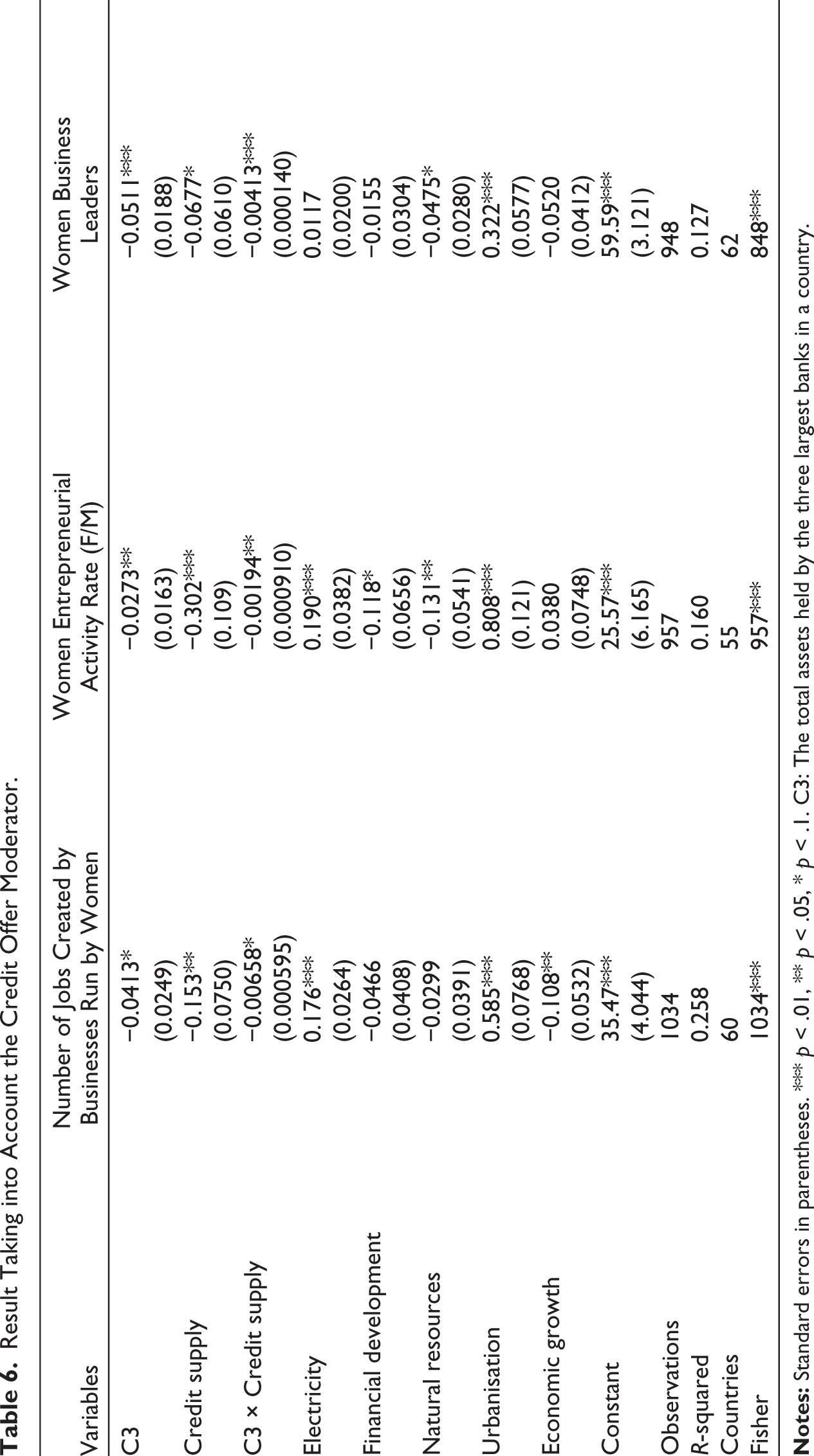

In the second section on the theoretical underpinnings, two moderators were highlighted (education and credit supply) that interact with bank concentration to affect women’s entrepreneurship. The work of Ongo Nkoa and Song (2022) is used to test these channels empirically. Tables 5 and 6 display the outcomes of this activity. The effects of the variables C3 × education and C3 × credit supply are looked at, and it is apparent that they are negatively significant and underline the mediating role. In other words, bank concentration has a negative effect on women’s entrepreneurship (i.e., confirmation of H1), while education and credit supply cannot mitigate the underlying negative effect (i.e., rejection of H2). The facts that the unconditional effects of bank concentration reduce female entrepreneurship and that education and credit access complement bank concentration to further reduce the female entrepreneurship are evidence of negative synergies. It is important to clarify that in this analysis of moderators, bank concentration is the channel or mediator while education and credit are the moderators. The negative interaction effects are traceable to the ineffectiveness of the moderators, especially as they pertain to poor education and limited access to credit owing to information asymmetry that motivate credit rationing.

Result Including the Education Moderator.

Result Taking into Account the Credit Offer Moderator.

Discussion of Results

The findings are consistent with the theoretical literature on the detrimental effects of bank concentration on female entrepreneurship that is discussed in the second section (Bennardo et al., 2015; Boateng et al., 2018; Karapetyan & Stacescu, 2014). However, the perspective that financial access does not effectively moderate bank concentration to positively influence female entrepreneurship is not consistent with the theoretical literature on the relevance of financial inclusion in female-inclusive development outcomes (Asongu et al., 2025; Nchofoung et al., 2024a, 2024b). Moreover, in relation to the job search theory, the findings are not consistent with the relevance of education in effectively moderating bank concentration to positively influence female economic participation. Hence, the established negative synergies are not in line with the perspective of research on the importance of literacy for job prospects (Babajide et al., 2021; Dvouletý, 2024; Quagrainie, 2024), especially as it pertains to female employment (Asongu et al., 2023; Kouladoum, 2023).

As maintained by Asongu (2024), the overall findings about how education affects female entrepreneurship do not align with a body of literature on the role that education plays in reducing female unemployment. These include Choi et al. (2019), on the role that literacy plays in the workforce, and Adejumo et al. (2021), on the role that human capital plays in long-term employment opportunities. On the other hand, the position of Achuo et al. (2022) regarding educated people’s inability to find employment due to mismatches in the labour market between employers’ desired skill sets and what graduates offer, ceteris paribus, explains why the expected linkage in relation from education does not withstand empirical scrutiny. According to certain scholars (Shi & Wang, 2022), there is an inherent mismatch between the type of education and management system, particularly in light of the fact that technical education offers more employment chances than general education (Forster et al., 2016; Iqbal et al., 2020).

Conclusion and Implications

The objective of the current research has been to assess how bank concentration affects female entrepreneurship in 70 developing countries using data for the period 2000–2019. The empirical evidence is based on OLS-FE and GMM regression. Three main female entrepreneurship outcome variables are employed, namely women’s entrepreneurial activity rate, women business leaders and the number of jobs created by businesses run by women. Two main moderating variables are employed, namely education and access to credit. It follows that the analysis is tailored towards assessing the direct effect of bank concentration on female entrepreneurship outcomes as well as the indirect effect pertaining to how education and credit access moderating variables influence the effect of bank concentration on female entrepreneurship. The following findings are established. Bank concentration broadly reduces female entrepreneurship. The negative effect is robust to the inclusion of additional control variables, an alternative estimation technique and a different measurement of bank concentration. Within the remit of interactive regressions, the unconditional effect of bank concentration reduces female entrepreneurship, while education and credit access further complement bank concentration to reduce female entrepreneurship. Policy implications are discussed in what follows.

The first policy implication relates to reducing bank concentration or market power in order to enable female entrepreneurs to have more access to credit that is worthwhile for present and future economic operations. Consistent with Chaffai and Coccorese (2023), given that competition in the banking sector is thought to be advantageous for lowering bank concentration or market power and enhancing overall economic performance, it is critical to support lowering the switching costs that banks impose on their clients without keeping them locked in by enforcing large explicit costs or strengthening relationships. In this regard, switching costs could serve as a benchmark for regulators as they carry out their mandate to control bank behaviour and curtail their market dominance, which ensures significant rents. Making information easier to access for consumers who want to switch can lead to lower switching costs (in terms of loan redemption conditions, loan redemption fees, takeover pricing and conditions of competitors, inter alia) or lowering the ‘bureaucratic’ obstacles to moving banks (facilitating, e.g., account number portability). Moreover, there are other crucial elements that contribute to competition, such as promoting new entrants, which calls for the removal of any significant barriers and the vigorous pursuit of deregulation, as well as the endorsement of any measure that boosts bank productivity, the benefits of which could then be distributed to clients in the form of more affordable rates and improved services.

The second policy implication, which relates to quality education, is important, especially financial literacy, which is essential for providing women with the financial knowledge needed to leverage on education in order to improve their entrepreneurial prospects. Such education should be tailored to, inter alia, motivate and encourage females to start saving money as soon as they can. It is also worthwhile within the same remit to introduce them to various tactics, such as budgeting, automating savings and goal-setting for savings. Moreover, financial literacy also entails learning and using techniques for managing and paying off debts, creating budgets and other financial management task.

The third policy implication focuses on addressing potential constraints in credit access related to information asymmetry, especially as it relates to reducing adverse selection and moral hazard that block the provision of loans by financial institutions to the relevant economic activities surrounding female entrepreneurship. The establishment and consolidation of entities that exchange information, such as public credit registries and private credit bureaus, are steps in the suggested direction. While it could take a while for information-sharing offices to be established, in the medium and long terms, these offices contribute to reducing borrowing-related issues such as adverse selection on the part of financial institutions (i.e., before female entrepreneurs are offered credit) and moral hazard on the part of female entrepreneurs (i.e., to avoid credit risk once female entrepreneurs have had access to credit).

There are some limits to this study which can offer opportunities for future research, notably: (a) assessing more channels for boosting female entrepreneurship; (b) putting emphasis on other areas of the United Nations Sustainable Development Goals (SDGs); (c) considering the informal sector in which female entrepreneurs operate and (d) engaging country-specific studies. Accordingly, this work certainly offers an opportunity for future investigations, particularly in view of understanding other channels or mechanisms by which female entrepreneurship can be promoted. This is based on the limitation that female entrepreneurship cannot be exclusively understood within the remit of the present study from the considered mechanisms and policy instruments. Governance, information technology and doing business can be considered as some of these potential future research avenues. Furthermore, considering investigated linkages established in this study as well as the recommended future research directions within the remit of other UN SDGs is worthwhile. Another limitation of this study is that female entrepreneurship as understood in this study is formal, and thus, future studies should complement this study by considering the informal entrepreneurship of women using qualitative studies. Last but not the least, the findings in this study are panel-oriented, and thus, country-specific studies are still worthwhile to robustly motivate policy implications that are country-specific. Furthermore, the limitation of the exclusive quantitative focus of the present study can be addressed in future studies by engaging case examples or qualitative narratives to supplement the quantitative data and enhance contextual relevance. The suggested qualitative research should consider the quality and nature of considered variables instead of incorporating them a uniform moderators.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix A

Definition of Variables.

| Variables | Definitions | Data Sources |

| Bank concentration (C3) | The total assets held by a country’s three largest banks | GFDD (2020) |

| Bank concentration (C5) | The total assets held by a country’s five largest banks | GFDD (2020) |

| Women entrepreneurship | Women’s entrepreneurial activity rate (F/H) Women business leaders (F%T) Number of jobs created by businesses run by women |

GEM NIWE |

| Natural resources | Measured by the benefits derived from natural resources in relation to GDP | World Bank (2021b) |

| Democracy | Measured by the democracy index; it provides an indication of the constraints on the executive | Polity IV |

| Electricity | Measured by access to electricity for a given population | World Bank (2021b) |

| Corruption | Measured by the level of corruption | ICRG |

| Economic growth | Measured by the growth rate of GDP per capita; it captures a country’s level of economic activity | World Bank (2021b) |

| Urbanisation | Measured by the proportion of the total population living in urban areas compared to the rural population | World Bank (2021b) |

| Financial development | Captured by the ratio of credit granted to the private sector to GDP | World Bank (2021b) |

| Education | Measured by public expenditure on education | World Bank (2021b) |

| Credit supply | Measured by credit to the economy by banks | COBAC report |