Abstract

Most research on accelerators to date focuses on the startups themselves. There has been limited research on the accelerators and their performance as the unit of analysis. Using the upper echelon theory, this article hypothesises the effects of individual attributes of managing directors on the startup accelerator’s performance and tests these by analysing data from 154 Techstars accelerator cohorts comprising more than 1,500 startups. Two personal attributes of managing directors, education and management tenure, influenced the accelerator performance. The education level of the managing director affects the proportion of the graduating cohort that is acquired, the speed of these acquisitions and the survival prospects of graduates that are not acquired. The tenure of the managing director affects the proportion of the graduating cohort that is acquired. These results suggest that certain attributes of an investor play a role in the future success of startups in their portfolio, extending the upper echelon theory from senior management to outside investors.

Business incubators are designed to help new venture startups survive the challenging early stages of development and increase their chances of success. Startup accelerators (SAs), a type of business incubator that is specifically designed to run in batches or ‘cohorts’, provide a structured environment in which startups working to develop and grow their businesses can receive intensive education and mentoring (Cohen, 2013; Miller & Bound, 2011; Pauwels et al., 2016) and can inculcate the norms and identities of the local startup ecosystem (Roundy, 2016). By providing specialised resources and supporting startups, SAs can help to foster innovation and commercialisation, and thereby drive economic growth. SAs draw upon the resources of stakeholders and the decision-making and organisational expertise of their management. Understanding how these programmes work and how they can be most effectively utilised is important for anyone looking to start or grow a business, as well as for policymakers and others interested in supporting the development of small businesses.

Most accelerator programmes follow a similar incubation process but differ in the individual managing director (MD), who leads it (Cohen et al., 2019; Dempwolf et al., 2014; Tasic et al., 2015; Wright et al., 2018). The choice of MD may significantly contribute to the success of the SA, as the leadership of accelerators can have a significant impact on the performance of the individual startups they incubate. The MD sets the direction and vision for the incubator or accelerator, and their leadership and decision-making can have a major influence on the resources and support provided to startups (Cohen et al., 2018, 2019). Not only are MDs in charge of startup selection (who joins the cohort), but they are also in charge of coaching the founders that comprise the cohort, ensuring the founders can effectively access the SA services and resources (Baum & Silverman, 2004; Busulwa et al., 2020; Polo García-Ochoa et al., 2020; Richards, 2002; Schulz, 2020; Wenzel & Koch, 2018; Yin & Luo, 2018).

MDs have a unique management role. MDs lead the SA, making the key decisions. Therefore, it seems reasonable that the quality of the individual MDs is likely to be a crucial predictor of performance. Cohen et al. (2019) highlight that the backgrounds of accelerator MDs significantly influence programme features and outcomes, suggesting that experienced and well-connected MDs can enhance the performance of accelerators. Banka et al. (2022) further emphasise that SAs provide multidimensional support, and the effectiveness of this support is largely dependent on the capabilities of the SA’s management team. Polo García-Ochoa et al. (2020) argue that the dynamic capabilities of MDs are critical for startup performance within accelerators. Cánovas-Saiz et al. (2020) provide evidence that the location and funding of accelerators, often influenced by the strategic decisions of MDs, are also significant factors in determining accelerator success. Further, Moroz et al. (2024) discuss how structured evaluation of accelerator performance must account for the managerial input in programme design and execution. Lastly, Assenova and Amit (2024) find that MD backgrounds are pivotal in crafting programmes that foster startup growth. Collectively, these studies underscore the importance of MDs in the overall performance of SAs, highlighting how their experience, strategic decisions and network leverage directly impact the success of the startups they support.

This influence is not just limited to the initial stages but persists due to the concept of imprinting (Beckman & Burton, 2008; Stinchcombe, 2013), whereby the initial conditions and decisions continue to shape the programme’s trajectory over time. This unique influence distinguishes the role of MDs from other investor management positions, particularly venture capitalists (VCs), who do not have the same level of involvement in the operational and design aspects of their investments.

MDs are responsible for running the daily operations of the accelerator programmes and typically manage a small team. MDs are actively involved in mentoring startup teams, holding weekly meetings where founders discuss their progress, learnings and challenges, while MDs provide feedback and guidance. This active mentoring is a critical component of the MD’s role, which contrasts with the VC’s role, which focuses more on investment returns and less on day-to-day operational involvement.

MDs are also responsible for setting SA strategy, developing entrance and exit criteria for cohort firms, creating and evolving the suite of services available and facilitating the use of these services by cohort firms (Wise, 2013). The extent to which these startups grow to successful exits depends significantly on the knowledge and learning that flows to them. This knowledge flow is one of the MD’s primary value-creating activities. In some cases, managers possess the relevant knowledge by their prior experience as entrepreneurs dealing with strategic and operational challenges of new venture creation. In other cases, the relevant knowledge is possessed by others, with management acting to broker that knowledge to their cohort startups by drawing upon their professional networks (Osborne, 2004; Papagiannidis et al., 2009; Warren et al., 2009). Finally, entrepreneurs often rely on the MD’s social capital to mitigate the impact of scarce financial capital (Kim, 2021). The ability of accelerator management teams to drive action on behalf of tenant firms through their social capital is a key benefit to tenant firms (Nicholls-Nixon & Valliere, 2020). This ability to leverage social capital and broker knowledge is a distinctive aspect of MD roles, emphasising why they should be viewed as a unique and critical form of management within SAs.

The MD is also responsible for building and maintaining relationships with key stakeholders in the entrepreneurial ecosystem, such as investors and industry experts, which can be crucial for the success of the SA and the companies it supports (Nicholls-Nixon & Valliere, 2020; Theodorakopoulos et al., 2014). Strong leadership and effective management at the top can help to create a supportive and collaborative environment that fosters growth and success for the companies in the programme. Therefore, it is important to study the top management team of a business incubator or SA to understand how their characteristics may affect the performance of the accelerator.

According to the upper echelon theory (UET) (Hambrick & Mason, 1984), the personal characteristics and backgrounds of top managers, such as the MD of a SA, can have a significant impact on the performance of the organisation (Abatecola & Cristofaro, 2018; Aboramadan, 2020; Cohen et al., 2019). This theory suggests that the values, beliefs and experiences of MDs can influence the strategic and operational decisions they make and the choice of services and resources that the SA will provide to entrepreneurs, ultimately shaping its performance (Cohen et al., 2018, 2019). In the case of a SA, the MD’s background could potentially have a significant effect on the performance of the accelerator.

The value of accelerators is largely derived from the support services they provide to tenant firms, and the quality of these services is directly influenced by the expertise and networks of the MDs. As noted by Wise and Valliere (2014), accelerator management adds value through their own relevant personal knowledge and skills developed from direct experience in startups and by leveraging their social capital in professional networks to access additional expertise. This dual capability underscores the importance of examining MD backgrounds.

Additionally, the personal values and beliefs of the MD could influence the performance of the companies it incubates (Park & Gould, 2017; Roundy, 2016). For example, an MD who especially values collaboration and openness may strive to create a supportive culture within the cohort that fosters growth. And it may further act to increase intake screening and resulting cohort performance (Nahata et al., 2014; Nicholls-Nixon & Valliere, 2021). Overall, the personal background of the accelerator MD is therefore likely to have a significant effect on the performance of the accelerator.

Thus, it is important to understand the potential effects of the upper management echelon on the performance of a SA. This article begins with a brief review of the literature on SA performance and the role of the MD on organisational performance. Drawing on the upper echelon theory, it develops hypotheses that connect individual MD attributes to SA performance outcomes. These hypotheses are then quantitatively tested with data from multiple cohorts of a world-leading SA. The final section draws conclusions related to SA performance and highlights implications for theorists and practitioners involved with the successful operations of SAs.

Background Literature

Startup Accelerator Performance

Despite exploratory literature on the performance of earlier forms of incubators (Bergek & Norrman, 2008; Hackett & Dilts, 2007; Mian, 1997; Mian et al., 2016; Voisey et al., 2013), there has been limited explanatory research on the performance of accelerators, primarily because of the newness of the phenomenon and limited data availability (Stayton & Mangematin, 2019). Despite accelerators having quickly proliferated around the world, there remain no large-scale representative public databases covering SA programmes. This undermines researcher efforts to evaluate the impact of these programmes (Hochberg, 2016).

The few studies that have examined the performance of SAs have focused on the accelerated new ventures themselves (Gonzalez-Uribe & Leatherbee, 2018; Stayton & Mangematin, 2019; Yu, 2020), such as their ability to quickly achieve milestones (Yu, 2020; Hallen et al., 2016) and raise capital (Smith & Hannigan, 2015).

Cánovas-Saiz et al. (2020) found that accelerator performance is focused primarily on ROI (e.g., total exits/total funding), and that is secondarily based on the total funding raised post-graduation and growth in the number of employees. Cohen et al. (2019) suggested that accelerator performance is driven by generating time-compressed external feedback, increasing transparency between startups in the same cohort and using structured programming to mitigate the bounded rationality of founders. They also found correlations between SA design elements and the performance of the startups that attend these programmes. Accelerators vary not only in their programmatic features but also in their founding stakeholders’ objectives (Hausberg & Korreck, 2020; Smith & Hannigan, 2015).

The Role of the Managing Director in Organisational Performance

Research findings show that top management characteristics impact organisational performance (Aboramadan, 2020). Park and Gould (2017) demonstrated that the internal dispositions of firm management team members (e.g., personality, emotions) influence important strategic outcomes of that firm. The MD’s role in the survival of new firms is still not well understood, as few studies based on qualitative data have been undertaken (Lukeš et al., 2019), and those that have been performed were limited in scope (Del Sarto et al., 2020; Hochberg et al., 2015). Stayton and Mangematin (2019) suggest three SA mechanisms that can impact performance: helping new ventures to quickly start, helping startups quickly leverage preexisting networks (e.g., alumni, professional service providers, potential early adopters, etc.) and leveraging these networks to allow the SA to fill gaps in the management team. From an investor’s perspective, startups that go public or are acquired boost the performance of the SA portfolio.

Banka et al. (2022) highlight that accelerators provide multidimensional support, care and expertise for startups, acting as intermediaries between startups and corporations. This requires MDs to possess a broad skillset and a deep understanding of both the startup ecosystem and the specific needs of the startups they mentor. This level of engagement and support underscores the distinct and critical nature of the MD’s position in SAs. The intra-cohort dynamics fostered by MDs in SAs are vital to their success, as peer learning and network effects significantly contribute to startup growth and startup performance. A few floundering startups in an accelerator cohort can undermine the value of the entire network, highlighting the importance of MDs in maintaining a cohesive and supportive cohort environment (Cohen et al., 2018).

From an investor’s perspective, startups that go public or are acquired significantly boost the performance of the SA portfolio. Therefore, the ability of the MD to select startups to be accelerated is as important to SA performance as is the MD’s ability to accelerate finding a workable business model for them. Similarly, accelerated startups that fail (shut down before a successful exit) undermine the performance of the SA. Hence, reducing the number of portfolio companies that fail is a way for MDs to improve returns.

The factors that enhance startup success are thus seen as different from those that improve its survival (Dimov & Shepherd, 2005; Radner & Shepp, 1996). Dimov and Shepherd (2005) found in the case of venture capitalists that they generate better exits from their portfolio companies through better selection and offering more valuable assistance to the companies in which they invest. Similarly, MDs who can better assess and assist startups in their cohorts should have more successful exits (e.g., IPO, M&A) and fewer startups that close before generating a return on the accelerator investment. In both investment cases, the executive (VC or MD) decides which startups are selected and what resources and services are provided to enhance the startup. By bringing parallel inferences from VCs and their portfolios to the SA and startup cohort scenarios, it can be argued that SA MD background characteristics play an important role in the startup’s performance. Cohen et al. (2018) found that the overall SA performance is greatly influenced by the original SA founding MDs, which suggests that the same is true at a cohort level where the MD’s background will have a considerable influence on cohort performance.

Nicholls-Nixon and Valliere (2021) have provided a conceptual framework that explains how the entrepreneurial logic used by an incubator (i.e., accelerators for this study) influences the incubation process (selection criteria and service offering). They posited that performance, at the incubator level, can be explained by how well that incubator’s selection criteria screen for companies that match the goals of the incubator and how closely the service offerings available align with the needs of the startups selected in the cohort (the degree of ‘fit’). According to this model, the success of an incubator depends on how well the MD chooses selection criteria and service offerings and how well they fit the needs of venture founders. If the MD can obtain this fit, the accelerator performance will benefit, as the fit may lead to better startups in the portfolio and will ensure those selected will get the resources and services they need at the stage of their development. Nicholls-Nixon and Valliere (2021) have thus provided a micro-foundation for how an MD may influence the strategy and performance outcomes of the accelerator. They showed that strategic orientation (as negotiated by organisational stakeholders) would influence accelerator performance through its impact on selection criteria used to choose startups in the cohort, the choice of services provided to those ventures and the resulting fit for individual incubated ventures.

While the present study appears to be the first specifically examining the effects of individual characteristics of SA managers on organisation performance, earlier research has found such effects in other financial portfolio contexts (Cuthbertson et al., 2016; Golec, 1996). Additionally, in the context of business incubators, Cohen et al. (2019) found that the ‘backgrounds and experience of founding MDs can have a significant impact on the nature and success of the program through multiple channels’.

Theoretical Background

There is an absence of reliable theoretical perspective to investigate upper management effects in incubators and accelerators (Pauwels et al., 2016), and more empirical studies need to be conducted to understand the determinants that influence a startup’s performance (Hausberg & Korreck, 2020; Smith & Hannigan, 2015). This study therefore aims to use the upper echelon theory to investigate the impact of MD background characteristics on startup performance (Assenova & Amit, 2024; Cohen et al., 2019).

Idiosyncrasies (e.g., education, cognitive biases and experiences) reflect the socio-demographic characteristics of executives and their underlying cognitive schemata (Abatecola & Cristofaro, 2018). These idiosyncrasies ‘serve to filter and distort the decision maker’s perception’ (Zhihua, 2010). Cohen et al. (2019) found that ‘The backgrounds and experience of founding MDs can have a significant impact on the nature and success of the program through multiple channels’. It is argued that the idiosyncrasies of SA MDs can influence a startup’s performance in the cohorts.

UET provides a strong and well-accepted theoretical lens to examine the impact that top management characteristics have on organisational performance (Aboramadan, 2020). In the nearly four decades since the Hambrick and Mason’s (1984) work, UET has become widely accepted in a variety of management areas. UET says that each decision-maker brings their own set of ‘givens’ to each strategic decision that they make, and these givens reflect their underlying values (Hambrick & Mason, 1984; Harveston et al., 2000; Madsen & Servais, 1997). They also reflect the decision maker’s cognitive base (O’Grady & Lane, 1997), which is in turn informed by their prior education and life experiences. These also serve to filter and distort the decision-maker’s perception of what is going on in the environment and what strategies to adopt because of such perceptions (Hambrick & Mason, 1984; Sperber & Linder, 2016; Zhihua, 2010).

Early research has highlighted the following idiosyncrasies: age, tenure in the organisation, functional background, education, socioeconomic roots, financial position and group characteristics. Abatecola and Cristofaro (2018) expanded the list to include: career experience, race, gender and individual psychological attributes. Subsequent researchers have continued to build on these attributes (Awa et al., 2011, 2015; Hohl, 2021; Kim, 2021; Li, 2019; Neely et al., 2020; Nishii et al., 2007; Rost & Osterloh, 2010; Shah et al., 2019; Teixeira, 2020; Ting et al., 2015; Yamak et al., 2013; Zhihua, 2010).

This research focuses on individual attributes that increase the knowledge stock of the MD. This follows Hambrick (2007), who found that researchers can dependably use data on senior management’s backgrounds to develop predictors of strategic actions that may influence the organisation’s performance. Previous first-hand experience as a founder leads MDs to gain knowledge to make better strategic decisions on behalf of the SA (March, 1994). MDs can increase their productive capacity through greater education and skills training (Becker, 1975). MDs will be more successful in imparting knowledge to cohort ventures when their authority is accepted by venture founders (Suchman, 1995) and is reinforced by information garnered from the incubation experience itself (Mansoori et al., 2019).

This study specifically focuses on the MD’s founder experience, incubator management tenure and education level and how these attributes influence SA performance. Founder experience is suggested by the need for common shared knowledge to enable communications and legitimacy in the eyes of the incubated founders (Abatecola & Cristofaro, 2018; Yu, 2020). Tenure within the incubator reflects the development of expertise in incubator operations with increasing experience (Nass, 1994; Yu, 2020). Education is suggested by the need for diverse strategic skills in managing portfolio performance (Dimov & De Clercq, 2006; Pegels & Yang, 2000). Of performance measures, acquisitions indicate perceptions of the value of the ventures (Stayton & Mangematin, 2019), and survival indicates the longer-term sustainability of the value created (Schwartz, 2012a, 2012b).

To expand beyond the UET, linking to broader theories such as network theory and social capital theory provides a richer framework for understanding the interplay between the idiosyncrasies of MDs and startup performance in accelerators. Network theory emphasises the structure and quality of relationships within an ecosystem, suggesting that MDs with extensive networks can facilitate critical linkages between startups and valuable resources such as investors, mentors and industry partners (Burt, 1992; Granovetter, 1973). These network ties not only enhance the legitimacy and resource acquisition of startups but also improve their strategic positioning within competitive markets. Similarly, social capital theory provides insights into how MDs leverage relationships and trust to foster knowledge exchange and collaboration within their cohorts. MDs with strong social capital can create a culture of reciprocity and shared learning among startups, which enhances collective problem-solving and innovation (Coleman, 1988; Nahapiet & Ghoshal, 1998). Combining these perspectives with UET, the background attributes of MDs—such as founder experience, tenure and education—can be viewed not only as predictors of strategic decision-making but also as key drivers of their ability to build and mobilise networks and social capital. This integrated approach underscores how MDs act as nodes and facilitators within the accelerator ecosystem, shaping both individual startup outcomes and the overall success of the accelerator.

The Influence of MD Founder Experience

Direct personal experience with a task leads to learning how to do the task better, more effectively and more efficiently (Amirkhanyan et al., 2018; Herriott et al., 1985; March, 1994). Having been a founder themselves in the past demonstrates that MDs of SAs have firsthand knowledge of the pertinent tasks that the founders they are advising need to complete. This experience shapes their perceptions and cognitions, which allows the MDs to be more skilled in selecting which ventures to admit into a cohort (Wise & Feld, 2017). They will have learned the knowledge and skills that founders need (Wise, 2012) and are better able to share this as a complement to the abilities of their cohort founders (Hallen et al., 2020). In an SA, this manifests as adding increased value to those ventures, which makes them more attractive to potential suitors (Wise & Valliere, 2014).

Experience can be related to both content and process—leading to improvements both in the effectiveness and in the efficiency of task production. Yu (2020) found that incubated ventures at an SA received higher quality feedback, which helped those startups more quickly resolve market and technical uncertainty. Founder experience provides MDs with knowledge and skills associated with accelerating this progress by helping incubated ventures move faster towards key milestones, including gaining customer traction and exit by acquisition (Gregson, 2021). In the SA, this may appear as startups becoming ‘acquisition worthy’ more quickly.

MDs with first-hand founder experience will also have learned methods of entrepreneurial bricolage (Baker & Nelson, 2005) and effectuation (Sarasvathy, 2001), and will therefore be skilled at creatively optimising the use of the scarce resources of startups to become more capital-efficient. Because they have ‘been there, and done that’, MDs with first-hand founder experience have increased legitimacy and credibility with other venture founders (Chatterji et al., 2019; Wise & Valliere, 2014). They are listened to, and their advice is heeded.

An MD’s ability to persuade founders to pivot away from unpromising business models includes the possibility of pivoting away from likely failure but not towards any immediately apparent alternative. The entrepreneurs are encouraged to ‘fail fast’—to quickly learn whether their venture idea is unlikely to succeed—and then abandon it without further resource commitments (Shankar & Clausen, 2020). Therefore, it may be expected that MDs with more founder experience will have cohorts in which any startups who are destined to die, die faster. Among the ventures that have graduated but are destined to ultimately fail, it may be expected these failures occur more quickly.

These various arguments therefore make it possible to hypothesise the following:

H1: An increase in the MD’s founder experience relates positively to the success of the venture cohort being accelerated.

And with respect to the dependent variables described above, it is possible to separately operationalise the ‘success of the venture cohort’ as follows:

The proportion of cohort acquisition after graduation, The speed of cohort acquisition after graduation,

The proportion of cohort survival after graduation, and

The speed of cohort death after graduation.

It is similarly possible to operationalise cohort success according to these four different measures in the additional hypotheses to be developed below.

The Influence of MD Tenure

Repetition of tasks brings increased expertise. Repetition of the MD role leads to learning how to do it better—more effectively and more efficiently. For instance, greater tenure will mean the MD has overseen the teaching of concepts such as bricolage and effectuation multiple times, to multiple cohorts, with multiple sets of founders. They, therefore, learn how to successfully convey this knowledge (Bacon-Gerasymenko & Eggers, 2017; Chatterji et al., 2019; York, 2018). Effectuation and entrepreneurial bricolage refer to the phenomenon of making the best use of limited resources and knowledge available by sharing among concerned stakeholders to explore opportunities and tackle problems from the constrained environment (Baker & Nelson, 2005; Høvig et al., 2018; Mishra & Zachary, 2015). These MDs will have learned to make better intake admission decisions, attract better startups and better leverage the SA support services available across the cohort (Dokko et al., 2009; Hambrick & Mason, 1984; Nass, 1994; Quiñones et al., 1995). These factors combine to increase the overall quality and growth of the startups in the cohort, making them more attractive for acquisition. Therefore, increased MD tenure should lead to increased performance and attractiveness of the ventures being incubated. In an SA, this will result in a greater portion of the cohort being acquired.

Yu (2020) found that SA cohort ventures received higher quality feedback due to the experience of the MDs. This helped those startups to more quickly resolve market and technical uncertainties, which sped up their development and growth. Accelerated ventures thereby decrease the time needed to reach key milestones, such as raising venture capital, gaining customer traction or achieving an exit (Gregson, 2021). These efficiencies are rooted in the process expertise of MDs with more SA management tenure. This results in incubated ventures that learn faster, grow more quickly and thus become attractive to potential suitors sooner.

Youtie et al. (2021) found accelerators also help venture founders to make the shut-down decision by helping them to better evaluate the feasibility and profitability of their opportunities and go-to-market plans. As incubator management experience increases, MDs become more confident and change their risk tolerance (Hambrick et al., 1993; Hellmann & Puri, 2000; Orens & Reheul, 2013), becoming more willing to advocate closing a venture. MDs with more SA tenure are more willing to withdraw support for weak ventures during incubation because they have learned the costs of delaying such decisions and the benefits of focusing on the remaining potential stars. In the SA context, incubated ventures that do not find traction will die quicker if their MD has greater tenure and therefore knows the importance of ‘failing fast’.

Based on these arguments, it is possible to therefore hypothesise the following (with the same four operational aspects as above):

H2: An increase in the MD’s management tenure relates positively to success of the venture cohort being accelerated.

The Influence of MD Education Level

Education level is correlated with formal and explicit knowledge and skills (Ng & Feldman, 2009). Individuals with greater education can better execute relevant tasks (Aboramadan, 2020; Becker, 1975; Becker & Collins, 1964). In particular, they exhibit broader and more complex cognitions (Pegels & Yang, 2000). MDs with higher levels of education are more likely to develop and execute strategic actions that maximise value creation for ventures in the cohort. In the SA context, this appears as a larger portion of the cohort being of high value and being attractive to potential suitors.

Education facilitates performance in most jobs (Hunter, 1986; Kuncel et al., 2004), and its effects are more pronounced in the case of managers with extensive discretion, such as MDs. Thus, higher education levels should result in broader competencies, which may be relevant to the acceleration of incubated ventures’ discovery of scalable business models with economies of scale. MDs with higher education are thus expected to generate more creative solutions when faced with the complexities of new venture creation (Ng & Feldman, 2009). Education level has been found to enhance effective strategic decision-making behaviours of executive managers (Wally & Baum, 1994). Managers with higher levels of education will know more analytical tools and have a greater propensity for using them. In SAs, these tools will help MDs be more efficient and effective in key tasks, including startup selection and post-selection support (Ng & Feldman, 2009). SAs run by highly educated MDs should thus have more well-run startups in their cohort—incubated ventures that are learning faster and hitting milestones faster. These ventures thus become acquisition worthy sooner.

Besides the effects of education on strategic decision-making (Wally & Baum, 1994), increased levels of education are also associated with increased levels of risk tolerance (Grable, 2000). Higher-educated executives are less risk-averse and more open to new ideas, changes and investment opportunities (Barker & Mueller, 2002; Cicchetti & Dubin, 1994; Cohn et al., 1975; Grable, 2000; Riley & Chow, 1992; Schooley & Worden, 1996; Zhong & Xiao, 1995). Highly educated MDs are thus more focused on the ventures in the cohort with the potentially highest payoffs and more willing to allow the other less-promising ventures to fail on their own. This focus manifests as fewer successful graduates (although they are expected to have successes of greater magnitude). In an SA, this takes the form of fewer incubated ventures surviving after graduation, as the weaker ones die out.

Based on these arguments, it is possible to therefore hypothesise the following (with the prediction that this relationship will be positive for acquisitions but negative for survivals and the speed of the resulting deaths):

H3: An increase in the MD’s education level broadly relates to the success of the venture cohort being accelerated.

Methodology

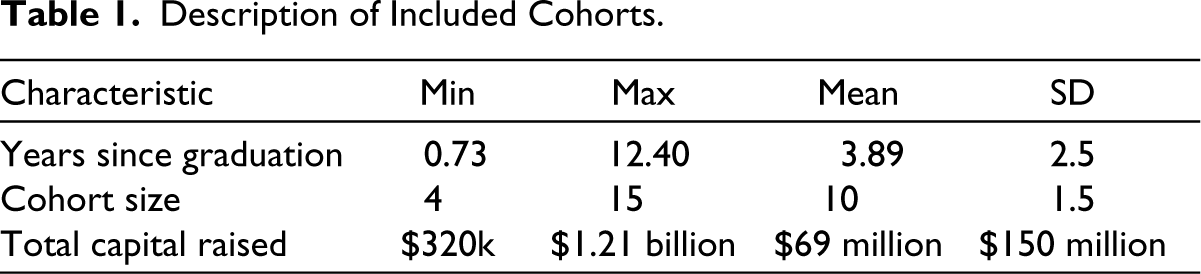

This study is focused on the overall performance of a graduating cohort from an accelerator form of business incubator, rather than individual firm-level performance of the companies in the cohort. The unit of analysis is therefore the performance of a single cohort in the years immediately following graduation. The data sample includes 154 cohorts graduating from Techstars accelerators between 2007 and 2019. These cohorts represent 1,543 new individual ventures that were incubated using the standardised Techstars incubation programme supervised by one of 61 MDs. Each cohort had one MD and started with 10 member companies. Data about which firms were in each cohort were obtained from Techstars. Data regarding the outcomes for each company and the background of MDs were obtained from Crunchbase. In 14 cases, partially missing MD data were supplemented using information from the individual’s LinkedIn profile. Table 1 provides summary information about the cohorts in the sample.

Description of Included Cohorts.

Dependent Variables

Graduating firms face a limited number of potential outcomes: they may be acquired, they may continue to operate independently or they may be discontinued (through either voluntary shut down or involuntary failure). The premise of business acceleration is to increase the likelihood of favourable outcomes and to bring these about more quickly. Accordingly, this study aims to examine both the proportion of a graduating cohort that achieves a favourable outcome and the speed with which this is achieved.

Acquisition

First, the study examined the graduating firms that are acquired post-graduation, separately for one year after graduation, two years and five years. Since not all cohorts are the same size at graduation (due to failures, mergers or divestitures during incubation), the dependent variable was normalised as a fraction of the applicable overall cohort size.

Second, the study examined how quickly the graduating firms are acquired to identify any acceleration effects by testing to see if these eventual acquisitions are accelerated—whether they are brought forward from a later year to an earlier year. Specifically, by calculating the difference in acquisition fractions between years 2 and 1 as one measure of acceleration, and between years 5 and 2 as a separate measure of acceleration, it may be concluded that acquisitions have been accelerated if the eventual acquired fraction has not changed, but the difference between a later year and an earlier year has increased (i.e., the eventual acquisitions have happened earlier).

Survival

Additionally, the study looked at graduating firms that are not acquired and continue to operate independently for one, two and five years after graduation. These were again normalised as a percentage of the graduating class, net of acquisitions.

Finally, the study examined the effects of the speed at which deaths may occur. It tested to see if these eventual deaths are accelerated—whether they are brought forward from a later year to an earlier year. Specifically, it calculated the difference in death fractions between years 2 and 1 as a measure of acceleration and between years 5 and 2 as a separate measure of acceleration. It concluded deaths have been accelerated if the eventual fraction has not changed, but the difference between a later year and an earlier year has increased (i.e., the eventual deaths have happened sooner).

Independent Variables

The study design selected three independent effects with each operationalised as measures within the Crunchbase dataset. Crunchbase offers an extensive database of firms at various stages of development, including early-stage private firms, and is being increasingly used as a resource for similar types of quantitative or empirical research projects (Werth & Boeert, 2013). Marra et al. (2015) provided a wide-ranging description and validation of the data in this database, which included information such as firm size, location, industry sector, lifecycle stage, financing and investor history, and founding team backgrounds.

Founder Experience

Previous research has suggested that the direct start-up experience of accelerator managers may matter more than their connectedness to the ecosystem (Wise & Valliere, 2014), whether as a result of increased personal knowledge, increased sensitivity to the needs of founders or increased credibility with other founders. The design included the direct founder experience of MDs, in years.

Incubator Management Tenure

For each cohort managed by a particular MD, the design included the integer number of prior Techstars cohorts that the MD has managed. This measure excluded prior incubator experience in other roles, such as a mentor, and therefore captures specific experiences and knowledge of the senior management and strategic aspects of the MD role.

Education

General education as a measure of knowledge and intelligence is captured on a five-point rank (5: doctorate; 4: master’s; 3: bachelor’s; 2: some college; 1: high school or less).

Controls

Because Techstars MDs are former successful business leaders and entrepreneurs who have ‘cashed out’ after financial success, little variation in age, socioeconomic roots or financial position can be assumed. The effects of age are reflected in the experience-based independent variables. Race and gender were not measurable in the dataset (which is described below) and thus may limit the generalisability of conclusions that can be drawn.

One difference among cohorts is their specific year of graduation and the effects of the resulting business environment (such as the availability of follow-on investment, the conditions of customers and markets for graduates or the health of potential acquirers). The design therefore included dummy variables for the graduation year to account for these effects.

While most Techstars cohorts have been geographically based (e.g., located in Boston and drawing entrepreneurs from the surrounding area), some cohorts have instead been industry-based (e.g., focused on healthcare or sponsored by a major healthcare corporation and drawing entrepreneurs from all across North America). The design therefore included a binary indicator to control for this difference.

Our analyses attempted to control for the effects of other factors through exclusion—the sample is constrained to only Techstars cohorts, meaning that all cohorts are of similar composition and consist of firms that have undergone very similar incubation processes. All firms accepted into a Techstars accelerator must meet a common set of baseline selection criteria (primarily focused on potential ROI for early investors), and these are assessed through a common intake screening process (online application and interview). In the case of non-geographic (industry-based) cohorts, additional selection criteria were employed to assess the degree of strategic fit with the sponsoring corporation. Once accepted into a Techstars accelerator, firms also receive a common set of services and incubation experiences and are provided with the same $100k seed investment at the same valuation.

Data Analysis

Hierarchical regression was used for data analysis. Four regression models were estimated. The first two models predict the acquisition of graduated firms—once as overall fractions and then as timing differences. The latter two models predict the survival/death of graduated firms—again once as overall fractions and then as timing differences. Each regression was run in a two-stage hierarchy: first with only the control variables and then with the independent variables added.

Results

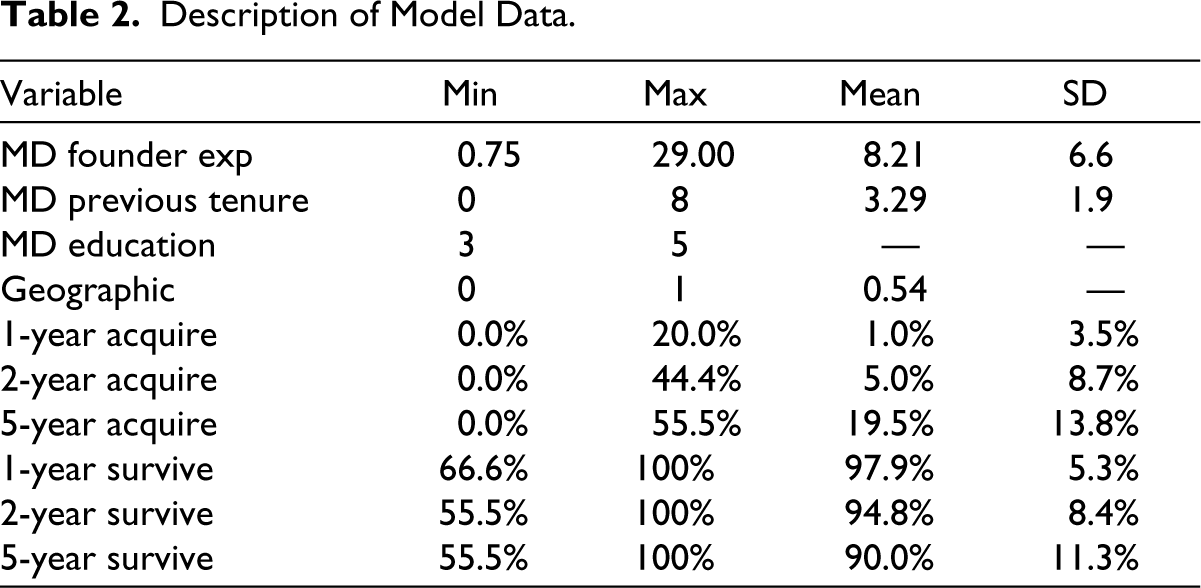

Table 2 provides a summary description of the primary variables in the models. Where a cohort has graduated so recently that it does not yet have five-year (or even two-year) data, measures involving that data are not meaningful, so the datasets have been right-hand censored in models involving those measures. As a result, the sample sizes in different analyses may vary and are reported in tables with the analytic results.

Description of Model Data.

Acquisition

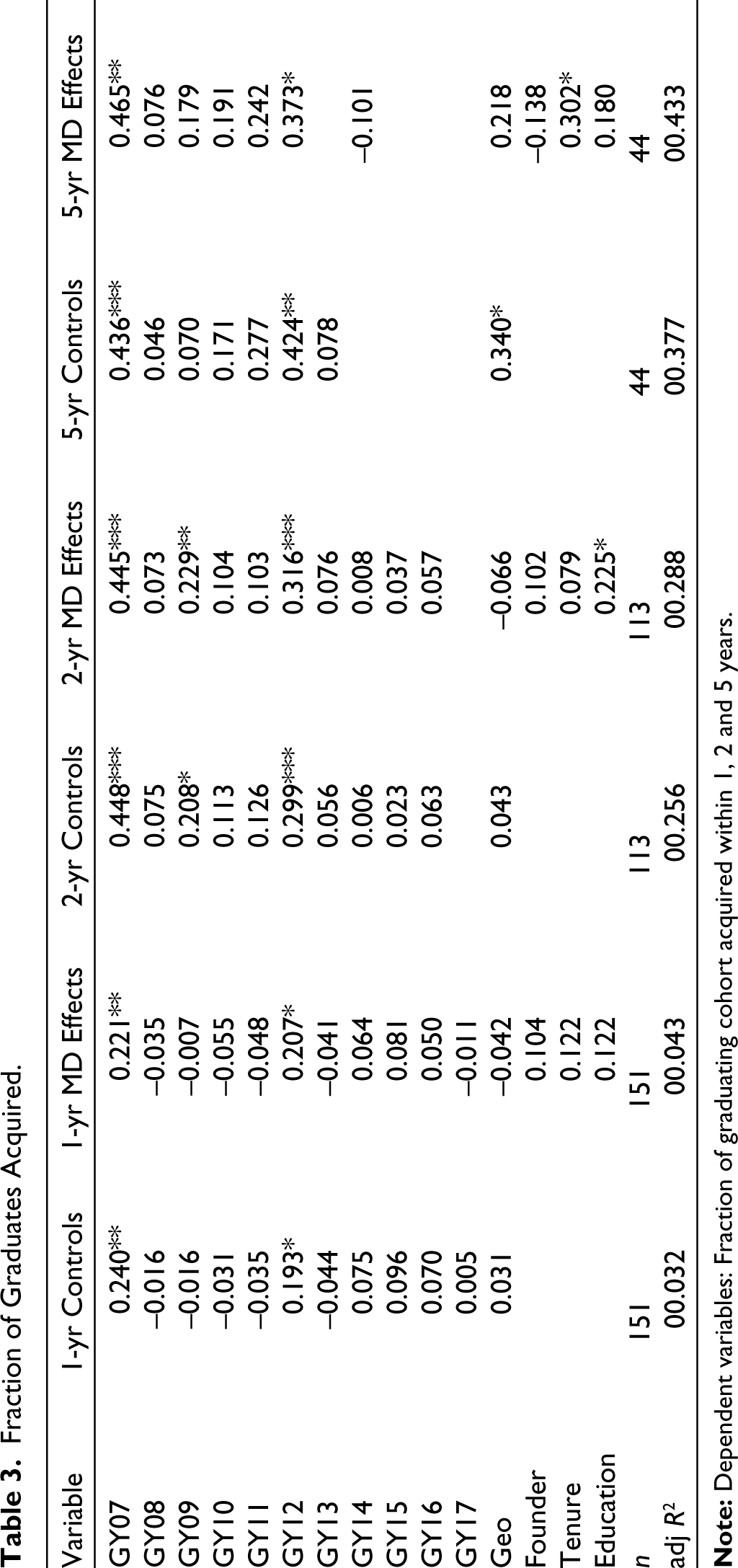

The first regression model investigates attributes of MDs that may be associated with attracting buyers to firms within a graduating cohort. Separate model variants were run to investigate the effects on acquisitions within one, two or five years of graduation. Table 3 shows the results obtained.

Fraction of Graduates Acquired.

The two-year model variant shows a positive and significant coefficient value for the level of MD education (0.225*). The 5-year model variant shows a positive and significant coefficient value for the level of MD tenure (0.302*), as well as a large improvement in R-squared. These results provide some support for hypotheses H2 and H3. Hypothesis H1 is not supported by these results. This table (and the following others) show highly significant results for some years of graduation (2007 and 2012 in particular), which confirms the importance of controlling for business cycle and other environmental effects that are not part of the theorised relationships of this study.

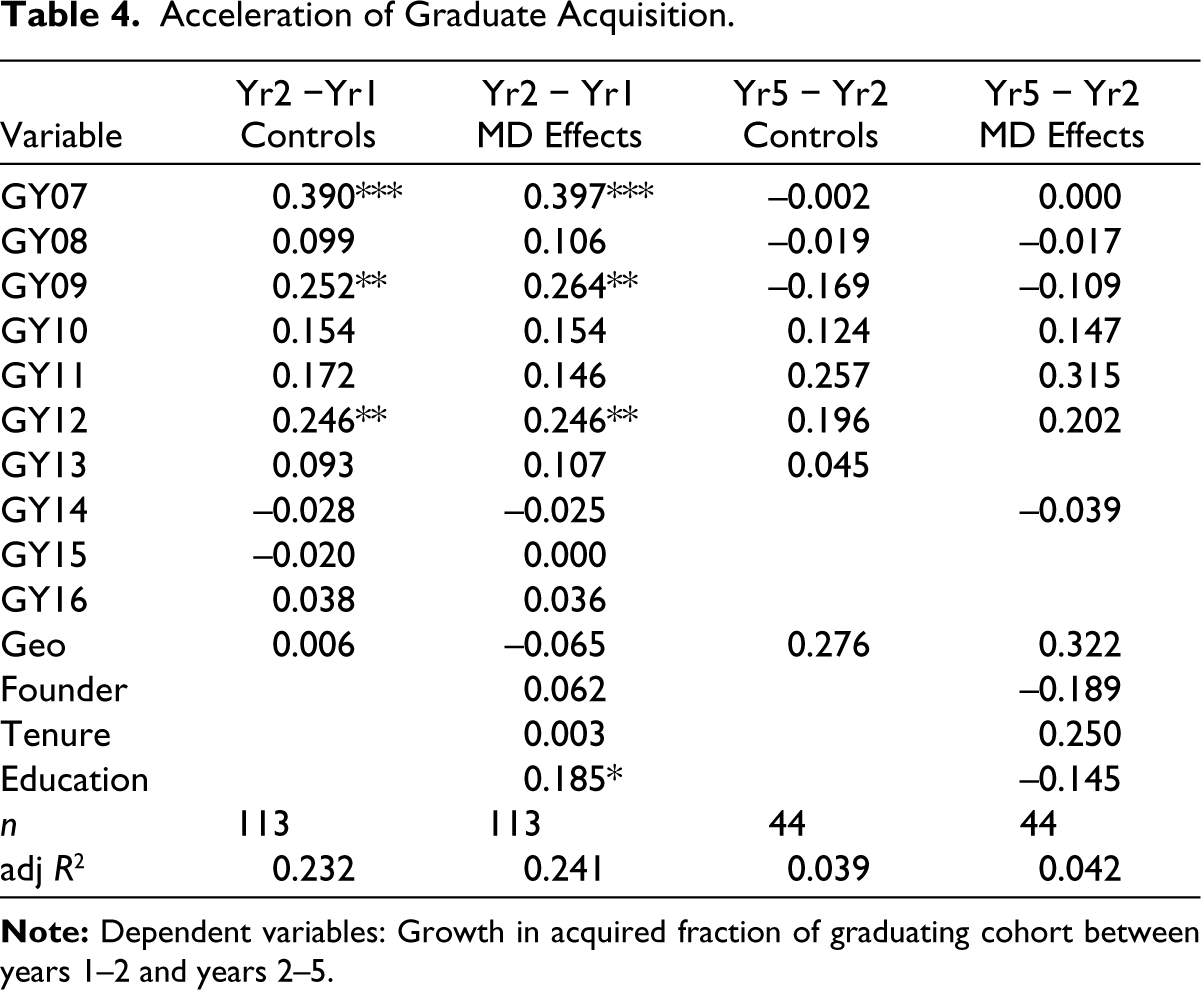

The second model investigates attributes of MDs that may be associated with accelerated acquisitions within a cohort. Separate variants were run to examine the shift of year 2 acquisitions to year 1 and of year 5 acquisitions to year 2. Table 4 shows the results obtained.

Acceleration of Graduate Acquisition.

The year 2/year 1 model variant shows positive and significant coefficient values for MD education (0.185*). This result provides some support for hypothesis H3. Hypotheses H1 and H2 are not supported by this result.

Survival

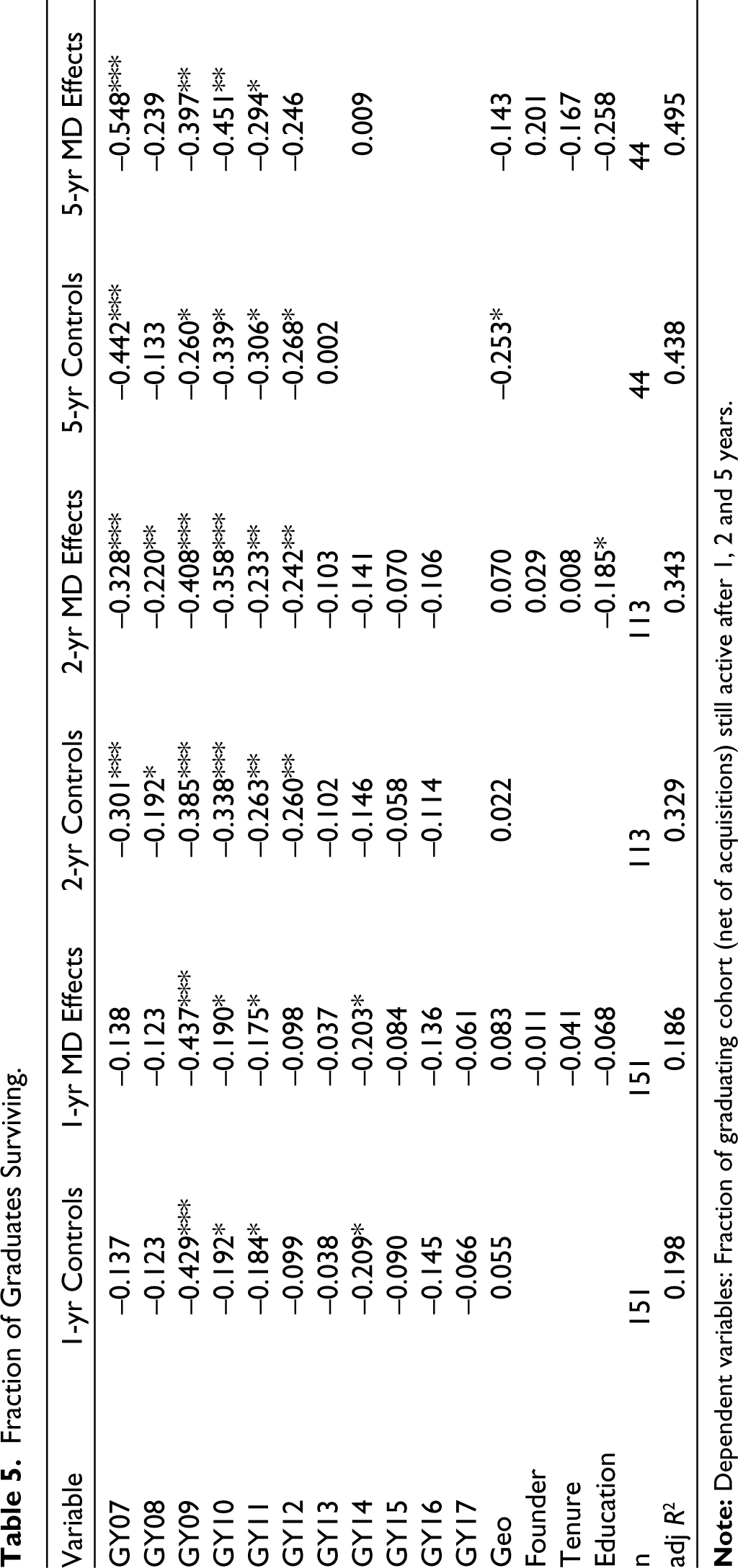

The third model investigates attributes of MDs that may be associated with a cohort’s continuing viability following graduation. Separate model variants were run to investigate effects on survival or death within one, two or five years of graduation. Table 5 shows the results obtained.

Fraction of Graduates Surviving.

The two-year model variant shows a negative and significant coefficient value for the level of MD education (−0.185*), as well as a large improvement in R-squared. This result provides some support for hypothesis H3. Hypotheses H1 and H2 are not supported by these results.

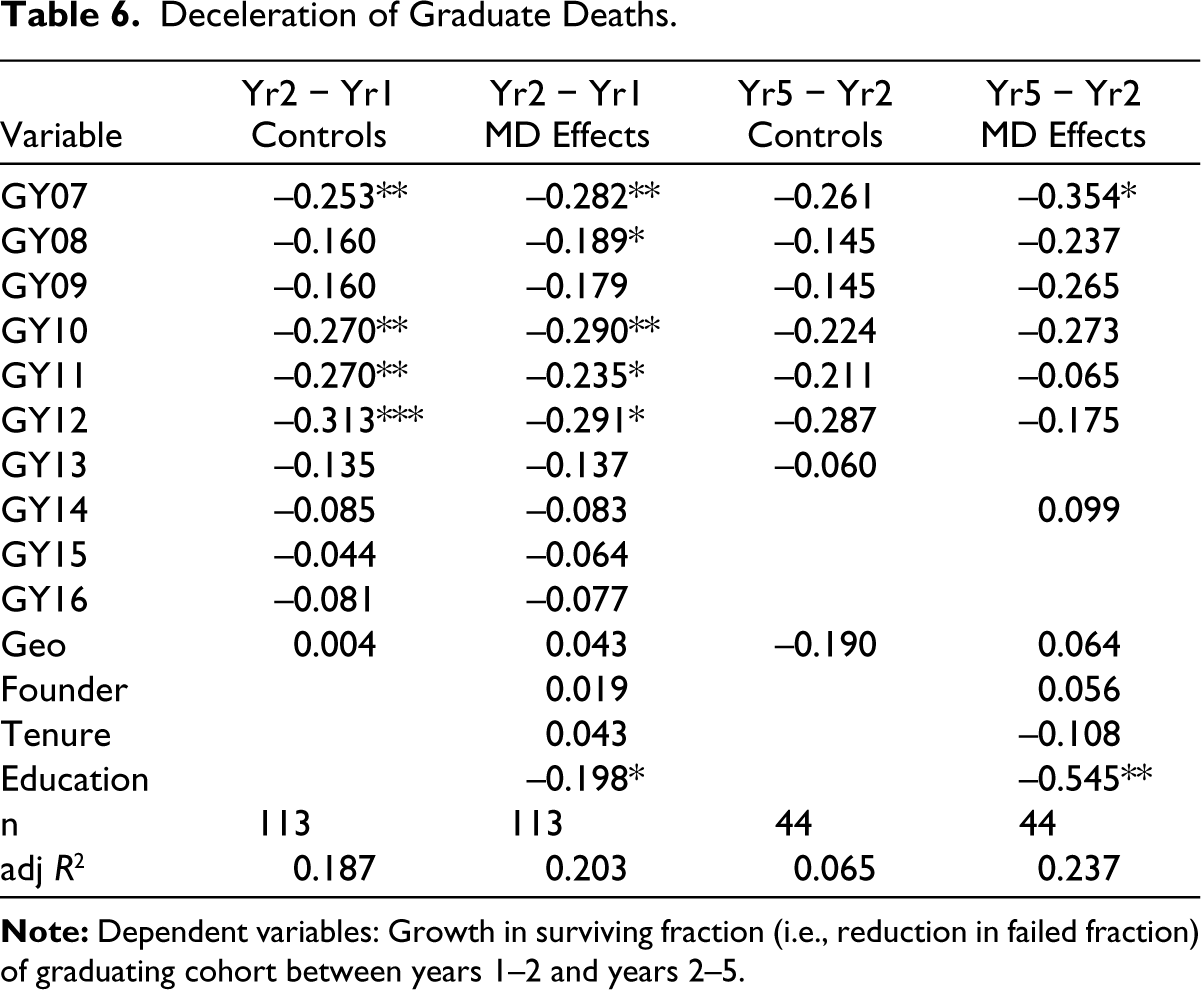

The fourth model investigates attributes of MDs that may be associated with death within a cohort. Separate variants were run to examine the acceleration of year 2 deaths to year 1, and the acceleration of year 5 deaths to year 2. Table 6 shows the results obtained.

Deceleration of Graduate Deaths.

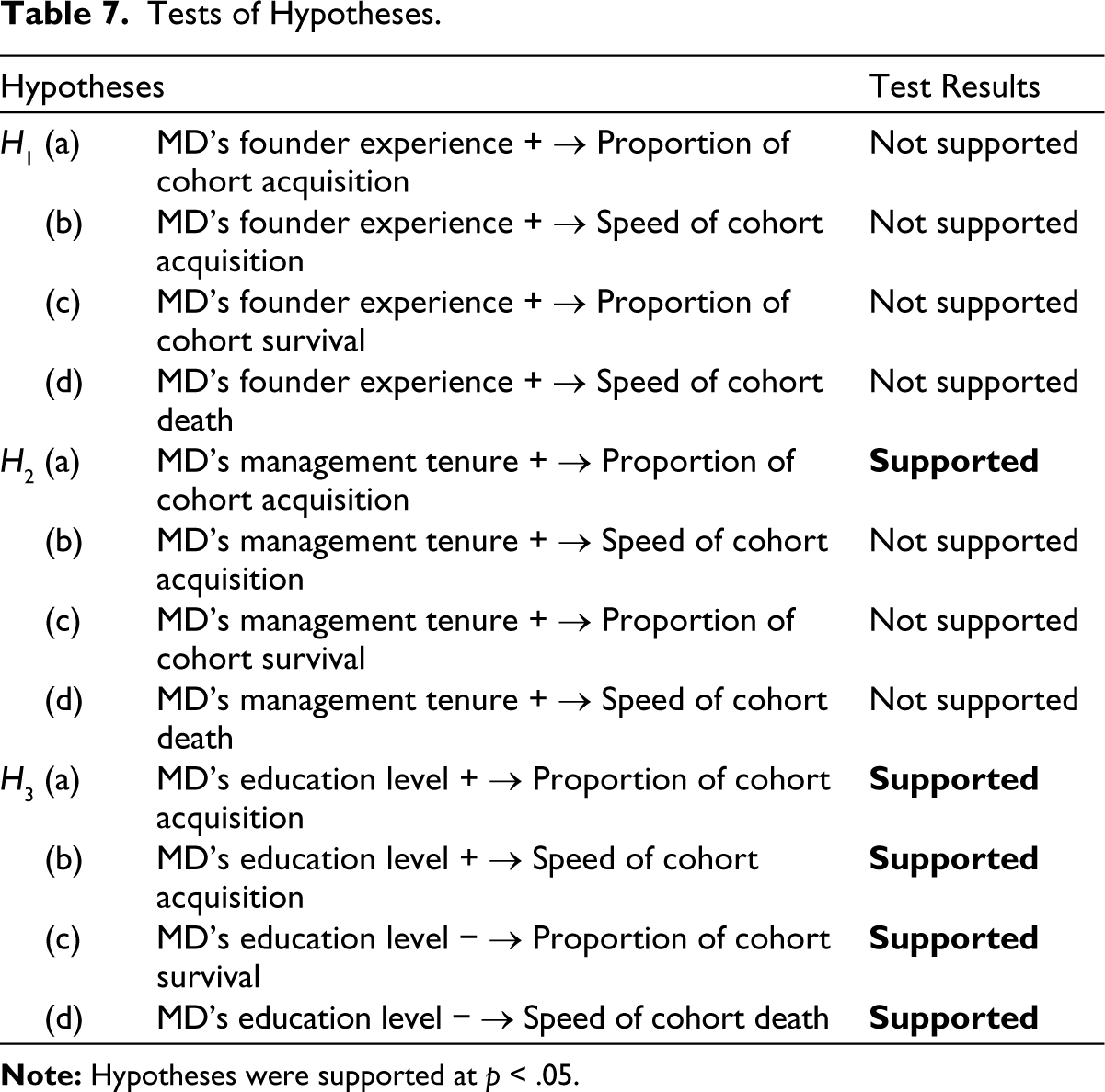

The year 2/year 1 model variant shows a negative and significant coefficient value for MD education (−0.198*). The year 5/year 2 model variant also shows a negative and significant coefficient value for MD education (−0.545**). These results are contrary to the predicted relationship of hypothesis H3. Hypotheses H1 and H2 are not supported by these results. Table 7 summarises the results of these different hypothesis tests.

Tests of Hypotheses.

Overall, these results lack support for the hypothesised effects of prior founder experience of MDs with nothing significant for H1 in Tables 3–6 and provide only weak support for the hypothesised effect of MD management tenure for H2 in Table 3 (affecting only the proportion of a cohort that get acquired). However, they support all of the hypothesised effects of MD education level of H3 in Tables 3–6, both in promoting acquisitions and in reducing and prolonging the survival of non-acquired ventures.

Discussion

The question of whether SAs accelerate new venture development is somewhat controversial, and the drivers of such effects are not well understood. Functional background, company tenure and formal education have been especially prominent in studies of UET in other contexts (Hitt et al., 2001). While some research has investigated the impact of portfolio manager background on investment portfolio performance (Das et al., 2011; Dimov et al., 2007; Franke et al., 2006; Patzelt et al., 2009; Shepherd et al., 2003), the impact of an SA’s MD background characteristics on cohort performance has not previously been investigated to this same extent. This study starts to address this gap by examining the effects of individual MD characteristics.

The Role of Founder Experience

There are arguments to be made, both pro and con, on why the entrepreneurial experience of the MD should have an impact on overall performance. On one side, MDs with much founder experience know first-hand the challenges startups in their cohort face. On the other side, MDs with too much founder experience may get emotionally invested in one or two ventures in their portfolio, and this may undermine their ability to manage all the startups in their cohort (Walske & Zacharakis, 2009).

Professional investors who have been entrepreneurs themselves are generally less risk averse than investors who lack first-hand founder experience (McMullen & Shepherd, 2006; Patzelt et al., 2009; Shane et al., 2003). Yet, no effects on cohort performance were observed here when prior founder experience varied. The results for H1 were not significant in Tables 3–6. This surprising result, if generalisable, would raise important questions and implications for the role of coaching and mentoring within incubators, as it would suggest that incubation outcomes are primarily dependent on process and structures, not on learning and knowledge transfer to new entrepreneurs.

But this result may just be an artefact of the sample. The fact that nearly all the MDs in the sample had significant years of founder experience (the mean value was eight years) may partly explain this result. Since prior startup experience was uniformly present across all MDs studied, there were few variations to compare. This lack of variability prevented isolating or measuring the specific influence of prior startup experience on the outcomes, as it was a constant factor in every instance (Priem et al., 1999). Perhaps there is a minimum desirable threshold level of founder experience that is beneficial, after which the benefits of prior entrepreneurial experience plateau. All sampled MDs may have exceeded this minimum threshold, and thus, the impact is constant across all cohorts.

Another possibility for not observing founder experience effects is that founder years are an incomplete measure of founder knowledge gained. An MD with two years could be, as a founder of a hugely successful venture, more valuable to the cohort than an MD with 20 years as a founder but with only mediocre outcomes. Thus, the number of prior successful exits might be used in future research to distinguish these effects. And, of course, individual MDs can also vary in how much they learn from identical experiences.

The Role of Tenure

Longer tenure in any specific role is associated with more experience and with increased reputation for expertise in that role (Abatecola & Cristofaro, 2018; Abatecola et al., 2013; Yamak et al., 2014). But longer tenure can also result in resistance to change and innovation. In this research, MD tenure had only a small effect on cohort performance. A clear positive effect for H2 was observed for the proportion of the cohort that is acquired in Table 3, but not for the other three outcome measures in Tables 4–6.

While it is possible to argue that tenure within an SA enhances MD expertise and reputation that builds their legitimacy, perhaps the reputation and legitimacy instead accrue to the accelerator itself and not to individual MDs. The average tenure for an MD in this study was only three cohorts (most MDs left their role after 18–24 months). This might not be long enough for prior cohorts to have generated huge exits and therefore not long enough for benefits to repetition and legitimacy to accrue to that specific MD. Due to the extremely early stage of incubated ventures, it may take several years after they graduate from the SA for these results to appear.

The Role of Education

Previous research on portfolio manager characteristics has been inconclusive on the relationship between education and portfolio performance. Zarutskie (2010) found that a higher fraction of investors with an MBA is negatively related to the portion of their portfolios with a positive exit, while Dimov and Shepherd (2005) found no observable effect between the portion of investors with an MBA and the portion of the portfolio that went on to an IPO. But they also found that investment firms led by executives with more education in management have smaller portions of their portfolio going bankrupt. It is reasonable to thus expect that more MD education would be associated with a higher fraction of the cohort that becomes acquired (or accelerated) or that survives long after graduation. Such predictions were confirmed by the results for H3 in Tables 1 and 3. It may be that the educated MD focuses on acquisitions that are timely and then turns their attention to startups remaining in the cohort in later years. However, this sequential or prioritised approach to cohort exits remains a topic for future research.

This study also found evidence in Tables 2 and 4 that an MD’s education does delay or prolong the deaths of graduated ventures that do not achieve eventual success (within the five-year post-graduate window of this study). It could be argued that the MD’s education level strengthens the resilience mindset among entrepreneurs, and that helps entrepreneurs to keep trying or that experience with that MD has inculcated in the entrepreneurs a culture of perseverance. In either case, the entrepreneurs continue in their efforts even past the point where they should give up on this venture, and so the venture deaths get delayed.

Research Implications

For researchers and theorists, these results highlight the importance of individual-level factors in understanding the operations and performance of accelerators (and potentially other forms of business incubator as well), as an important supplement to the institutional-level factors that have been the primary concern of research to date. The results demonstrate that the characteristics of a single individual in a role of strategic influence can have material influence on the performance of an entire SA cohort and therefore on the ability of an SA to meet the performance objectives of its stakeholders. This individual-level influence suggests that accelerator performance is potentially a level-crossing phenomenon that is strongly influenced by individual-level idiosyncrasies—of MDs, of founder entrepreneurs and potentially of the coherence among these (such as homophily among actors). Future research is needed to explore how homophily between the MD’s and founders’ characteristics impact each other, sometimes referred to as the homophily hypothesis: ‘The alignment of values, perspectives, and cognitive styles between the entrepreneurs and investors can foster a sense of mutual understanding and increase the likelihood of funding being provided’ (Brahmana & Kontesa, 2023, p. 657). Future research is also needed to better understand how MD characteristics and background interact with the strategic and operational details of the incubation process. Since it has been suggested that MD effects may persist beyond the tenure of the specific MD (especially in the case of founding MDs) (Cohen et al., 2019), longitudinal studies may be needed to understand potential path dependencies and lag effects in eventually understanding the influence of specific MDs upon accelerator performance.

These results extend the applicability of UET to a novel context that features significant strategic uncertainties with limited resources and under conditions of bounded rationality (Cyert & March, 1992; March, 1994). According to UET, managers in such situations have to rely on their past experiences and personal perceptions and interpretations (Hambrick, 2007). The case of SAs is further complicated by the indirect connection between upper management cognitions and actions, the strategic choices of the SA itself and the ultimate performance of the individual startup ventures in the cohort. One theoretical implication is that the connection that Hambrick and Mason (1984) envisioned between senior management characteristics and organisational performance can be mediated by entities or individuals external to the organisation. In the case of SAs, this may operate through the influence of MDs on cohort entrepreneurs, the resulting performance of each accelerated venture and the resulting collective performance of the entire cohort. Since SA performance depends on the performance of individual incubated ventures, the upper echelon influence of the MDs may similarly operate through the thoughts and actions of individual founders. This is a dimension of UET that warrants further exploration.

The findings of this study, while rooted in the framework of UET, also hold significant implications when viewed through the lenses of network theory and social capital theory. The idiosyncrasies of MDs not only shape strategic decisions but also serve as pivotal elements in cultivating and leveraging relational networks and trust-based exchanges. From the perspective of network theory, the ability of MDs to act as central nodes in the accelerator’s ecosystem enhances the flow of information, resources and legitimacy across the network, thereby increasing startup access to critical external stakeholders. Similarly, social capital theory highlights how MDs contribute to building a cohesive culture of reciprocity and shared learning within cohorts. By fostering trust and enabling knowledge sharing, MDs amplify collective capabilities, resulting in stronger innovation and resilience among startups. These broader theoretical insights extend the implications of the findings, suggesting that the effectiveness of MDs in accelerators hinges not only on their attributes but also on their capacity to actively shape the social and relational dynamics that underpin ecosystem success. This integration of theories underscores the multifaceted role of leadership in startup ecosystems and provides a richer understanding of how individual-level attributes and broader relational mechanisms converge to drive performance.

Practical Implications

For incubator practitioners, these results highlight the critical importance of the MD’s role, as their individual characteristics can have an impact on the overall performance of cohorts and thereby the SA itself. This is a significant issue for stakeholders of an accelerator, as they must therefore understand how the background of any specific MD put in charge is likely to influence the outcomes that the accelerator can achieve. There should be a careful match between the desired accelerator objectives and the characteristic attributes of the selected MD.

Viewed holistically, these results suggest that the choice of individual for the role of MD is critically important to everyone associated with an SA. Founders should be aware of how the background of a specific MD may influence their incubation and acceleration experience and the results their new venture achieve. MDs and prospective MDs should be aware of the likely effects of their own backgrounds and how this may be best leveraged (or mitigated) to the benefit of the SA mission. SA stakeholders should be aware of how this choice may greatly affect the ability of an SA to meet their expectations and objectives. And external ecosystem partners and policymakers should be aware of how the effects of this SA choice are multiplied in the broader context through the subsequent impact of successful new ventures.

Conclusion

While much research has investigated the impact of investment manager backgrounds on portfolio performance (Dimov et al., 2007; Franke et al., 2006; Patzelt et al., 2009; Shepherd et al., 2003), the analogous impact of an SA MD’s background on startup cohort performance has not received nearly as much attention. This research has explored which attributes of MDs are associated with better performance. It has identified MD attributes that have an impact on the overall success of the cohort and extended understanding of which attributes lead to better performance when applied to running an SA.

The study examined the experience and education of MDs to see which upper echelon attributes matter. It found that MDs with more experience or education tend to have more startups in the cohort being acquired with faster exits while simultaneously helping the remaining startups in the cohort survive.

This study found that the MD’s background and education level impact the cohort’s overall performance. However, it found no support that an MD’s prior experiences as an entrepreneur lead to better cohort performance.

Unlike prior works, this research contributes to the recent trend to examine the outcomes of the SA, not simply the outcomes of startups themselves. This research also extends the conversation on the importance of fit between the services offered by the SA and the needs of the startups in the cohort. The primary theoretical contribution is to extend UET to include accelerator MDs. Finally, the contribution to practice may help founders and other SA stakeholders understand on what basis to choose an MD with whom to work. This research finds that the prior experience and education level of MDs have a material impact on the success of startups under their care.

Moreover, hands-on knowledge from founding experience, education level and venture management tenure of MDs perhaps enhances the absorptive capacity of the cohorts through the day-to-day interaction with the MD and the knowledge transfer that takes place. Absorptive capacity is found to be one of the key perquisites for knowledge transfer to take place in organisational settings (Priestley & Samaddar, 2007). Future studies can be conducted on this front.

Limitations of the Study

This study, while offering valuable insights into acceleration success factors, is not without its limitations. First, the sample size is relatively small, with participants predominantly from a single geographic region. This limits the generalisability of the findings to broader populations that may have different national cultures and institutions or follow very different models of incubation. Future studies should aim to include larger and more diverse samples to enhance the applicability of the results.

Second, the cross-sectional design of the study restricts the ability to make causal inferences. The data collected provides a snapshot in time, which may not accurately reflect the dynamic nature of entrepreneurial processes. Longitudinal studies are recommended to better understand the evolution and impact of the identified factors over time.

Third, self-reported data was used, which is subject to biases such as social desirability and recall bias. Entrepreneurs may tend to overstate their successes and underreport their challenges. Utilising multiple data sources, such as financial records or third-party evaluations, could mitigate these biases and provide a more objective assessment.

Suggestions for Future Research

Building on the limitations identified, future research should consider directions to deepen and broaden the understanding of accelerator success. Future research might incorporate objective data sources, such as financial performance metrics, customer feedback and market analyses. This approach would provide a more accurate picture of the entrepreneurial outcomes of an SA. Next, investigating the role of external factors, such as economic conditions, industry trends and policy changes, would also provide a broader context for understanding the entrepreneurial success of an SA. This research focused only on startups from one SA. Conducting a broader study to determine whether these findings apply universally or are merely specific to Techstars’ acceleration model would be a good next step in this research area. Another future research project might examine factors such as investor network size, industry goodwill and MD reputation, which were not covered in this study but may be relevant according to theories such as network theory, social capital theory and signalling theory. Investigating the similarities between the attributes of MDs and venture founders, with a focus on the potential interplay between these individuals rather than solely on their individual characteristics, would be another avenue for future research. By pursuing these research directions, future studies can build on the current findings and contribute to a more comprehensive and applicable body of knowledge. This approach will enhance not only the validity and reliability of this research but also its practical relevance for aspiring and current entrepreneurs.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.