Abstract

Corporate social responsibility (CSR) has over the past decades transformed from a philanthropic attribute to something compulsory. It has become the imperative duty of organisations, irrespective of their size, nature of business and age. However, because of poor financial capabilities and lack of support, newly established ventures too often fail to voluntarily participate in social and environmental activities. This is one reason why national governments have initiated various programs and policies to encourage CSR and environmental activities in new ventures. However, previous studies have yet to fully reveal the effects of entrepreneurial finance on CSR and the environmental, financial and innovative performance of newly established ventures. To fill this gap, we used a survey to gather empirical evidence from 255 newly established ventures. The results indicate that entrepreneurial finance directly contributes to financial performance, while indirectly contributing to environmental and innovative performance through CSR. Our research recommends that new ventures efficiently utilise entrepreneurial finance to configure CSR activities that achieve high profitability, and environmental and innovative performance. Moreover, our research encourages governments to make financial loans to ventures engaged in social and environmental activities to help them reach their sustainable development goals.

Keywords

Recent studies in the fields of environmental science and business management describe how environmental and social activities can and should be understood as obligatory rather than voluntary (Carroll, 2008; Khan et al., 2020). Irrespective of their size, age and nature of their business, firms have shown a strong interest in social and environmental initiatives and how they significantly improve reputation and profitability (Ilyas et al., 2020; Min et al., 2017). In other words, a growing number of top managers, owners and corporate executives have been earmarking a considerable amount of resources and time for corporate social responsibility (CSR) and environmental practices (Benlemlih & Cai, 2020). But with this being said, newly established ventures do not always voluntarily participate in social and environmental activities unless they receive adequate support to do so. Smallness, limited resources, poor support and lack of finances hinder new ventures from practicing CSR (Wang & Bansal, 2012). The literature has discussed several programs and policies initiated by governments across the globe to promote CSR and environmental activities among new and established ventures. These include efforts in technological capabilities (Malaquias et al., 2016), entrepreneurial orientation (Zhuang et al., 2020), dynamic capabilities (Gruchmann & Seuring, 2018), leadership strategies (Yamak et al., 2019), intellectual capital (Aras et al., 2011), top management commitment (Ilyas et al., 2020) and institutional pressure (Yin, 2017). Despite extensive debate and literature, what is not yet known is the role of entrepreneurial finance in the environmental, financial and innovative performance of new ventures with a mediating CSR role. More precisely, studies have not yet discussed how entrepreneurial finance directly influences the environmental, financial and innovative performance of newly born ventures. Entrepreneurial finance’s indirect effects also remain unclear, that is, what it achieves through CSR activities. This study aims to fill this gap.

There are several motives for carrying out this research. First, finance can be understood as the ‘grease’ of an economy; it significantly influences sustainability practices (Scholtens, 2006). Studies have examined how financial capital is one of the significant factors of social and environmental practices (Hasan & Habib 2017; Ruggiero & Cupertino, 2018; Scholtens, 2006). In contrast, firms with a lack of financial resources are less likely to participate in social and environmental activities (Khattak, 2020). Surprisingly, entrepreneurial finance in CSR and environmental practices has remained mostly untouched as an issue, specifically when it comes to emerging firms. The majority of strategic, business and environmental management studies have debated the relationship between financial capital and environmental practices in listed firms and corporations (Hasan & Habib, 2017; Lin et al., 2019), with newly founded small businesses otherwise receiving only minor attention—perhaps due to their limited financial and technology resources. Small firms have nevertheless now realised the potential benefits of CSR concerning profit, innovation, reputation and competitive advantages (Gallardo-Vázquez et al., 2019; Khan et al., 2019; Moneva-Abadía et al., 2019) and attempt to efficiently utilise financial resources to achieve their sustainability goals (Khattak, 2020). As society has modernised, business ventures have changed their models to adopt and include environmental and sustainability practices (Garriga & Melé, 2004), with firms opting for social and environmental action as part of their business models (Di Benedetto, 2017; Madsen, 2020). This means that studying CSR and environmental factors in business firms has become an interesting topic. As studies have identified an extraordinary failure ratio among new ventures worldwide (Antretter et al., 2019; Anwar & Ali Shah, 2020), our research tries to mitigate this among newly born enterprises, as a result hopefully empowering top managers/owners of small and medium enterprises (SMEs) with respect to the importance of CSR and environmental initiatives.

This study has several objectives and implications. First, we present the importance of entrepreneurial finance in CSR and SMEs’ performance. In other words, we recognise that entrepreneurial finance either directly or indirectly contributes to the environmental, financial and innovative performance of newly born ventures. Second, this research encourages policymakers, banks and financial institutions to lend to the industrial sector, especially new ventures, in an effort to help establish their CSR practices and performance. As pointed out by the resource-based view (RBV) theory (Barney, 1991), firms with sufficient tangible (technology, land, finance, etc.) and intangible (intellectual capital, information, knowledge, etc.) resources outperform firms who have limited resources. In our research, entrepreneurial finance is understood as a tangible resource that boosts firms’ outcomes and performance.

Theoretical Background

Entrepreneurial Finance

Entrepreneurs have differing growth objectives that can even vary between the different lifecycle stages of their ventures. Some entrepreneurs are motivated by lifestyle factors and may have little need for external finance. Others persistently search for financing for their activities (Fraser et al., 2015). This involves the basic issue of: ‘entrepreneurial finance denotes to the early-stage financing mechanisms, often supplied by the entrepreneurs’ personal network to finance their ventures activities’ (Cumming & Vismara, 2016). There are several sources through which an entrepreneur finances his/her venture activities in terms of growth, expansion, decision making, etc. For instance, Cumming and Johan (2017) state that ‘entrepreneurial finance encompasses venture capital, private equity, private debt, trade credit, IPOs, angel finance, and crowdfunding, among other forms of finance’. In the introductory stage of entrepreneurial finance, it has often been understood as capable of explaining ‘how entrepreneurs get finance to start a new business or expand operational processes of their newly started venture through angels and venture funds’ (Kerr et al., 2014). Recent years have seen entrepreneurs and early stage ventures facing clear difficulties accessing finance, resulting in new funding sources such as crowdfunding, accelerators, government venture capital, mini-bonds and family offers, along with several new entrepreneurial financing instruments such as peer-to-peer business lending and equity-like mezzanine financing as part of an emerging, new era of entrepreneurial finance (Block et al., 2018; Bruton et al., 2015). These new players are not only achieving financial goals, but non-financial ones as well such as social, community-building, strategic, technological and product-oriented goals, changing the entire environment of entrepreneurial finance as a result (Block et al., 2018). These developments have re-shaped existing theories and added new goals to the existing objectives of new ventures (Bellavitis et al., 2017).

Corporate Social Responsibility

Management literature has acknowledged CSR as an imperative corporate duty (Quinn et al., 1987). CSR has received vast attention from worldwide organisations since 1920s, resulting in an increased number of social and environmental management articles (Montiel, 2008). CSR received further attention in the 1950s when organisations realised social responsibility as a key goal accompanying profitability. The definitions of CSR expanded during the 1960s and 1970s. In the 1980s, more empirical research was conducted, resulting in new concepts in the literature including corporate social performance, business ethics theory and stakeholder theory (Carroll, 1999).

Despite the long-debated CSR discussion, the literature has yet to agree on a universal definition of it. Montiel (2008) states that the most often cited definition is Carroll’s (1979) statement that ‘the social responsibility of business encompasses the economic, legal, ethical, and discretionary expectations that society has of organizations at a given point in time’. Aguinis and Glavas (2012) defined CSR as ‘context-specific organizational actions and policies that take into account stakeholders’ expectations and the triple bottom line of economic, social, and environmental performance’. Another definition often cited in the literature is ‘continuing commitment by businesses to behave ethically while improving the quality of life of the workforce, local community, and society at large’ (Col & Patel, 2019; Davis & Weisbeck, 2016; Whait et al., 2018). Carroll (1991) describes the obligation of corporations ‘to avoid damage or reduce harm to stakeholders (the environment, employees, consumers, and others) which is right, just, and fair’. Favouring the most-used definition, we identify CSR activities as those where an enterprise tries to behave ethically, protect the environment, provide social support to workers and support disadvantaged communities.

New Ventures

The literature contains no universal definition of what a new venture is. How long a new venture takes to mature has to date not yet been determined (Chrisman et al., 1998). According to Kazanjian and Drazin (1990), the maturation time of new ventures depends on resources, strategies and the nature of the industry. While they state that a new venture may take up to five years to mature, Anwar, Rehman, et al. (2018) demonstrated in their study on Pakistan that maturity might occur 10 years after the creation of a new venture due to legislation and resources. For our research, we considered ventures as new that have started their operation during the last 10 years.

Social activities such as protecting the environment, supporting disadvantaged communities and community welfare require financial and non-financial resources. With respect to practicing CSR, it can be noted that financial resources are more valuable than non-financial resources. Consistent with the notion of the RBV theory (Barney, 1991), ventures having unique, rare and immutable resources enjoy higher performance than firms facing resource issues. We therefore argue that newly established ventures build their social reputation and status in the market through entrepreneurial finance.

The RBV theory was initially developed by Barney (1991), emphasising (tangible and intangible) unique, rare and immutable resources as superior performance advantages of one firm over another. Over the last 30 years, the theory has received significant attention from researchers in the field of strategic management and business. Focusing on superior performance in businesses, a number of studies have tested the theory with respect to tangible resources such as financial capital (Anwar, Tajeddini, et al., 2020; Tirumalsety & Gurtoo, 2021; Xiang & Worthington, 2017), technology (Suoniemi et al., 2020; Viete & Erdsiek, 2020), new products (Rajapathirana & Hui, 2018; Ramadani et al., 2019) and unique information and knowledge (An et al., 2021). However, with the passage of time during which innovation became a key organisational success factor among strong competition and globalisation (Anwar, 2018; Clauss, 2017; Clauss et al., 2020), scholars felt the need for RBV when it came to the aspects of innovative performance and its outcomes (Anwar, 2018; Memon et al., 2020). Several studies as a result tested the role of tangible and intangible resources in the innovative performance of firms (Garcia Martinez et al., 2017; Hock-Doepgen et al., 2021; Koo & Lee, 2019).

Recently, organisations have realised CSR activities as key factors of superior performance (Anwar & Clauß, 2021; Bai & Chang, 2015; Khan et al., 2019). Many scholars have tested RBV, acknowledging finance as essential for social and environmental performance as a result (Anwar & Li, 2021; Khattak, 2020; Scholtens, 2006). And the different debates around the topic demonstrate that the RBV theory is not limited to the relationship between organisational resources and financial performance, it involves innovative and environmental performance as well. What makes our research different from other studies is that we focus on the importance of entrepreneurial finance, as it relates to the environmental, innovative and financial performance of newly established ventures, with CSR as a mediator; this has never been tested in previous research. Hence, our research advances our understanding of how entrepreneurial finance contributes to these types of performance, and how CSR plays an intervening role in new ventures.

Literature Review

Entrepreneurial Finance and Enterprise Performance

Finance is considered a ‘liver’ in the success and performance of firms. The RBV theory claims that a firm with adequate resources performs better than other firms with limited resources and capabilities (Barney, 1991). The recent debate on the RBV theory states that firms with sufficient resources are more likely to invest in social activities, resulting in superior environmental and financial performance (Anwar & Li, 2021). Government financial incentives are considered one of the significant predictors of firm performance, innovation growth and reputation (Xiang & Worthington, 2017). In emerging economies such as Pakistan, SMEs have limited financial resources, a major reason why they consider entrepreneurial finance and financial support as fruitful opportunities for competitive advantage and profitability (Anwar & Li, 2021). It is also argued that new ventures in emerging economies enhance their survival through entrepreneurial finance (Anwar, Tajeddini, et al., 2020).

In emerging economies, investment by governments in R&D and novel projects helps configure the innovative performance and profitability of business firms (Wei & Liu, 2015). Many SMEs in emerging economies use government financial incentives for their operational activities, business expansion, new projects and processes (Clement & Hansen, 2003). Many Pakistani SMEs do not like to engage in environmental activities due to a lack of finances. In this case, the government encourages them by providing financial and non-financial incentives (Anwar & Li, 2021; Khattak, 2020).

Firms need sufficient financial resources to produce unique and new products for a market having high levels of competition (Zampetakis et al., 2011). Xiang and Worthington (2017) identified a significant relationship between financial availability and SME innovation. They further stated that SMEs typically face a shortage of financing, hence they are encouraged to invest in innovative projects to respond to challenges. Living in a challenging environment and facing numerous constraints, SMEs use supply chain finance to boost their performance (Ali et al., 2018). Pellegrino and Savona (2017) ascertained how financial constraints cause the failure of innovation in business firms. In a similar vein, García-Quevedo et al. (2018) also revealed that financial constraints lead to innovative projects’ failure in business. One of the possible solutions to overcome and mitigate the extraordinary failure ratio in SMEs is found in the capacity of financial resources (Fatoki, 2011).

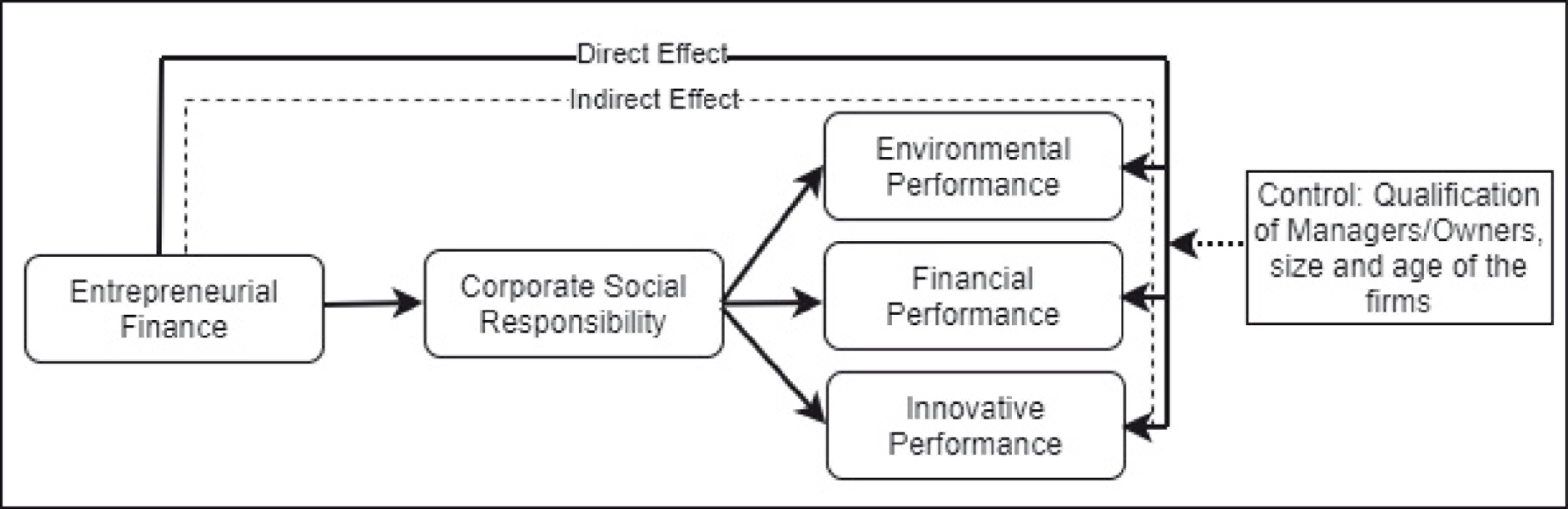

H1: Entrepreneurial finance significantly and positively contributes to the environmental performance of newly established ventures.

H2: Entrepreneurial finance significantly and positively contributes to the financial performance of newly established ventures.

H3: Entrepreneurial finance significantly and positively contributes to the innovative performance of newly established ventures.

The Mediating Role of CSR

Financial capital is considered the most generic type of resource that can be easily converted into other types of resources. It can assist small firms in configuring their processes, resulting in high performance and growth (Wiklund & Shepherd, 2005). In a similar vein, Maranto-Vargas and Rangel (2007) claimed that financial resources are undoubtedly the key to performance; firms need to effectively use finance to improve internal operations (methods and processes) that will lead to superior performance.

Benlemlih and Cai (2020) suggest that firms should utilise their financial resources (e.g., internally or externally acquired) in a way to benefit the maximum number of stakeholders. In turn, it will enhance their value and performance. The availability of financial resources can be a significant predictor of CSR and innovative activities (Donaldson & Preston, 1995). Financial resources provide a buffer against unexpected loss and challenges and also facilitate the necessary response of a firm to changing conditions (Zampetakis et al., 2011). The availability of sufficient financial resources encourages firms to invest in CSR activities that result in high performance (Hong et al., 2011).

Firms observe their financial conditions while investing in CSR. If they perceive the benefits of the investment, they will carry it out. Otherwise, they ignore investment if their financial conditions are conducive to it (Clarkson et al., 2011; Cormier & Magnan, 1999). For instance, Reverte (2009) examined how profitable companies have sufficient finances for CSR and environmental activities. They prefer investment in CSR initiatives, and perceive high profitability in it. Favouring this notion, Artiach et al. (2010) also acknowledged that firms with sufficient financial resources allow investment in CSR while postponing their immediate economic goals because they believe in the long-term benefits on their investment.

As discussed earlier, the failure ratio of newly born ventures is very high worldwide (Antretter et al., 2019; Anwar & Ali Shah, 2020). In response to this, many countries have initiated special financial schemes to facilitate new ventures (Anwar, Tajeddini, et al., 2020; Klingler-Vidra & Pacheco Pardo, 2020; Zhang et al., 2017). The alternative goal of this support is to achieve sustainable development and economic growth (Khattak, 2020). It can also be stated that if ventures receive adequate financial resources from government and financial institutions, they will prefer investment in CSR and sustainable activities.

Hasan and Habib (2017) claimed that a lack of resources and financial availability lead to high investment in CSR that results in strong profitability and performance. Winton and Yerramilli (2008) described how new ventures need careful scanning and monitoring of the environment in which they operate. Venture capital and financial support by banks are required for this process. Moura et al. (2019) state that firms seek public support and government financial incentives to configure their administrative processes and activities and boost their innovation. Zhang et al. (2017) claimed that the Chinese Government has formulated new policies (including providing financial support) for SMEs to configure technological, product and research innovation in SMEs. Spanos (2018) states that crowdfunding is one of the significant sources of finance in business ventures that generates a variety of benefits such as investment in CSR, exploiting new opportunities, initiating new projects and general business transformation.

H4: Entrepreneurial finance indirectly contributes to environmental performance through CSR in newly established ventures.

H5: Entrepreneurial finance indirectly contributes to financial performance through CSR in newly established ventures.

H6: Entrepreneurial finance indirectly contributes to innovative performance through CSR in newly established ventures.

Entrepreneurial Finance and CSR

Firms need financial capital to engage in CSR activity. CSR activities and early green adoption in newly established enterprises can be promoted through government financial incentives and monetary support (Diefendorf, 2000; Owen et al., 2018; Spanos, 2018). Firms with sufficient financial capital can better contribute to international development and achieve their social goals (Marti & Scherer, 2016).

Compared to MNCs, small firms face a lack of finances, which hinders their participation in CSR. Large firms on the other hand have sufficient finances, and can fully invest more in social activities and environmental initiatives (Marti & Scherer, 2016). Supporting this notion, several studies have claimed that the availability of financial resources is significantly aligned with the capacity of CSR investment and environmental initiatives (Strike et al., 2006; Surroca et al., 2010; Waddock & Graves, 1997). Spanos (2018) demonstrates that crowdfunding (a part of entrepreneurial finance) is one of the most prominent sources of finance in business ventures used for initiating new projects, CSR, new opportunities, transformation and social support. Financial resources promote environmental activities among firms (Bowen, 2002) and spur them towards charity and donations (Brammer & Millington, 2008).

H7: Entrepreneurial finance significantly and positively contributes to CSR in newly established ventures.

The hypothesised model is shown in Figure 1.

Methodology

Sample and Data

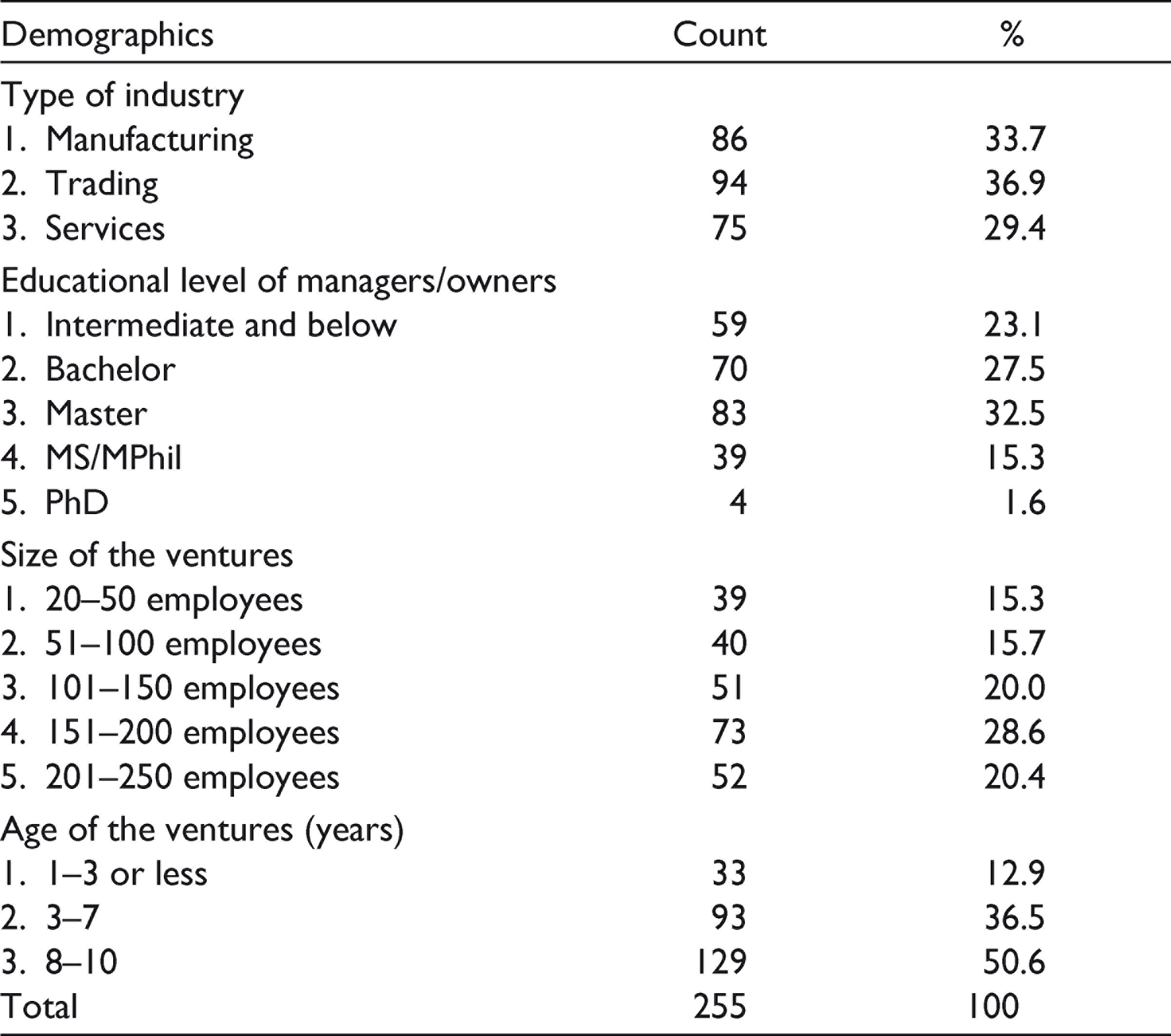

This research targeted manufacturing, trading and service SMEs in Pakistan that started their operation within the last 10 years (e.g., new ventures). We applied hard copy and online data collection. The questionnaire was categorised into two sections: (1) demographic factors such as the nature of the business (manufacturing, services or trading), size of the venture, age of the venture and educational background of the top managers/owners; and (2) main variables (entrepreneurial finance, CSR, environmental, financial and innovative performances). In addition, to gain maximum responses and avoid social desirability bias, we included a cover letter in the survey informing the participants that their data would be kept private. We also requested top managers and owners fill out the survey because they are the active members of the firms who design strategies and best know their firms’ related activities (Anwar, 2018). We obtained registered firm lists from the Islamabad, Rawalpindi and Khyber Pakhtunkhwa chambers of commerce, and randomly sent 1,000 e-mails to registered SMEs in the three different cities. In parallel, we distributed 600 hard copy questionnaires (200 in each city). We received 181 useable returns from these, corresponding to a response rate of 30.17%. The online survey returned only 74 useable responses, corresponding to a response rate of 7.40%. This amounted to a total of 255 useable responses, of which 86 were manufacturing, 94 trading and 75 service firms. Our survey showed that 59 managers/owners have an intermediate or a lower level of education, 70 managers/owners hold a bachelor’s degree, 83 managers/owners hold a master’s degree, 39 have a MPhil degree, while only 4 managers/owners have a doctoral qualification. In all, 39 firms have 20–50 employees, 40 firms have 51–100 workers, 51 firms have 101–150 employees, 73 firms have 151–200 workers and 52 firms have 201–250 employees. In all, 33 ventures started their operational activities within the last three years, 83 ventures within the last three to seven years, while 129 firms have been in operation for the last 10 years. Table 1 displays the demographic information of the ventures participating in the survey.

Demographic Information

Measures

Variable Measures and Scales

We used 5-point Likert scales displaying strongly disagree 1, disagree 2, neutral 3, agree 4 and strongly agree 5. For financial performance, we used the scales showing extremely declined 1, declined 2, average 3, improved 4 and extremely improved 5. All the items are provided in the appendix.

Entrepreneurial Finance

Entrepreneurial finance is a broad topic. It answers the main questions of ‘How do new ventures or entrepreneurs who start a business get finance for their operational process?’ and ‘How do angels and venture funds play a role here?’ (Kerr et al., 2014). Cumming and Johan (2017) state ‘entrepreneurial finance encompasses venture capital, private equity, private debt, trade credit, IPOs, angel finance, and crowdfunding, among other forms of finance’. It demonstrates the financial resources provided by financial institutions, banks and public authorities to boost the operational activities of newly born ventures (Anwar, Tajeddini, et al., 2020). To measure entrepreneurial finance, we asked managers/owners six questions adopted from a recently published study by Anwar, Tajeddini, et al. (2020); similar items were used in previous studies (Anwar & Li, 2021; Khattak, 2020). A sample item includes ‘We receive sufficient finance from banks when we need it for new projects’.

Csr

There is no single definition of CSR. However, most studies discuss three major dimensions of it: CSR towards employees, CSR towards the environment and CSR towards community (Khan et al., 2019). To extract comprehensive insights, we also relied on three dimensions of CSR that are widely used in the literature of SMEs (Bai & Chang, 2015; Khan et al., 2019). One sample item is ‘Emphasizing the importance of its social responsibilities to society’.

Environmental Performance

This indicates the contributions of firms to the environment in terms of recycling products, environmental safety and resources saved. We used five items to measure environmental performance that are validated and used by Martinez-Conesa et al. (2017) and Memon et al. (2020) in the context of SMEs. One item includes ‘Implements programs to reduce water consumption’.

Financial Performance

Measuring financial performance in SMEs is not an easy task when financial data and information are unavailable (Anwar, 2018; Ilyas et al., 2020; Khan et al., 2019). In this instance, the self-reported approach is used to measure the financial performance of SMEs where managers/owners are asked about their performance with respect to return on assets, equity and investment compared to their major competitors and industry rivals (Anwar & Li, 2021; Khan et al., 2019). We also relied on the same approach, using six items (taken from Anwar, 2018; Memon et al., 2020) to measure the financial performance of SMEs.

Innovative Performance

This indicates the ability of firms with respect to new product development, methods and processes. We used five items to measure innovative performance that are widely used in the SME literature (Martinez-Conesa et al., 2017; Memon et al., 2020). A sample item is ‘Changes introduced in our products during the last five years are improved’.

Control Variables

In addition to the main variables in the hypothesised model, we controlled for the educational level of managers/owners and the age and size of their enterprises. Studies have recommended these factors to be controlled while assessing the outputs and performance of SMEs (Anwar & Li, 2021; Ilyas et al., 2020; Khan et al., 2019). We therefore controlled for these factors in all the models. The results are discussed in the regression analysis.

Data Analysis and Results

Before testing the hypotheses, the data were tested for normality, non-response bias, common method bias and reliability.

Non-response Bias and Common Method Bias

We executed a t-test and compared the results to check the variation between early responses and late responses as well as between the hard copy and online survey data (Armstrong & Overton, 1977). The t-test results did not display any significant difference between the groups, confirming the absence of non-response bias as a result.

There are several common method variance approaches, such as conducting the survey anonymously, time-lagged data, different responses, different scales for the items and the iterative approach (Podsakoff et al., 2003). There are two recommended approaches for extracting common method variance: Harman’s single factor test and common latent factor. The first approach is executed in SPSS using exploratory factor analysis where all the items are included to know whether they overlap or have cross-loading. The second approach (common latent factor) is normally performed in AMOS where the influence of the common latent factor is checked on the measurement model, and compares the results of the main model with the common latent factor model. Since we analysed our sample data via SPSS, we applied Harman’s single-factor analysis to check the common method bias. The results indicated five factors having an eigenvalue above 1. The first factor displayed only a 24.87% variance, that is, below 50%. This approach as a result supports the absence of common method variance in the sample.

Reliability

To assess the internal consistency of the items towards their respective constructs, we executed Cronbach’s alpha in SPSS. According to Tavakol and Dennick (2011), a value equal to or greater than 0.70 acknowledges desirable consistency and reliability among items towards a specified construct. Our research arrived at Cronbach’s alpha values of: entrepreneurial finance (0.90), CSR (0.90), environmental performance (0.90), financial performance (0.92) and innovative performance (0.89). The results met the threshold requirement of reliability.

Descriptive Statistics and Correlation

Table 2 illustrates that the highest mean was of financial performance, while the lowest mean was of CSR. Innovative performance had the highest standard deviation, while entrepreneurial finance had the lowest. Our data were normally distributed as skewness and kurtosis values, and were in the recommended range (+2) as per the suggestions of George (2011).

Descriptive Statistics and Correlation

The correlations among most of the constructs were significant, thus providing support for the proposed hypotheses. For instance, entrepreneurial finance was significantly positively related to CSR (r = 0.196, p < .01), to environmental performance (r = 0.130, p < .05), to financial performance (r = 0.443, p < .01) and to innovative performance (r = 0.217, p < .01). Similarly, CSR was significantly positively related to environmental performance (r = 0.252, p < .01), to financial performance (r = 0.232, p < .01) and to innovative performance (r = 0.267, p < .01).

Regression Analysis

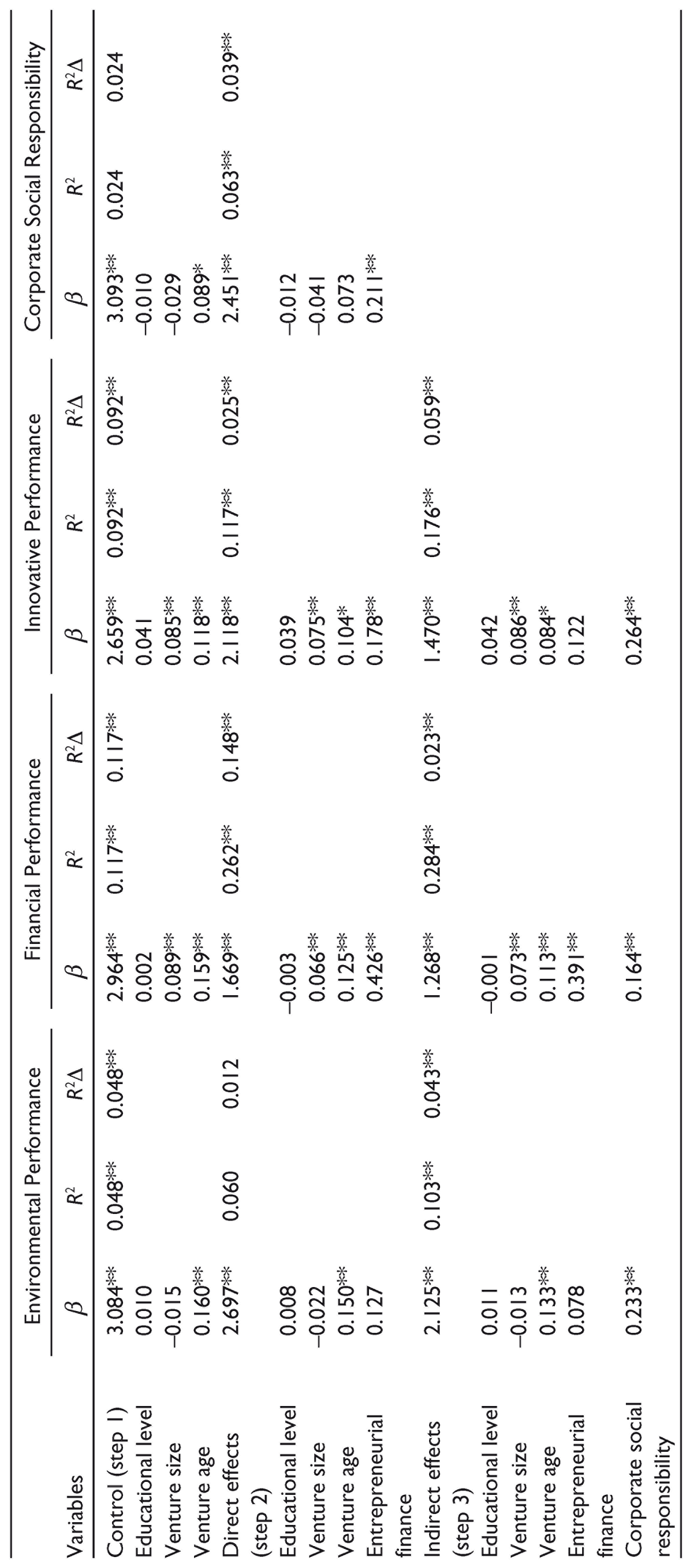

The hypotheses of the model were tested in SPSS using regression analysis (Table 3). We performed four models where the influence of entrepreneurial finance via a mediator on (a) environmental performance, (b) financial performance and (c) innovative performance was executed in the presence of control variables. The impact of entrepreneurial finance on CSR was checked in the final model (d).

Regression Analysis

We entered the control variables in the first step of each model: the educational level of managers/owners and the size and age of the enterprises. In the second step, we included entrepreneurial finance. In the third step, we entered CSR (e.g., mediator).

The results of the first model showed only the age of the venture as a significant predictor, while the educational level of managers/owners and the size of the firms did not show a significant role in the model. Entrepreneurial finance was extracted as a non-significant predictor of environmental performance in the direct effect (β = 0.127, p > .05); it did not support H1.

With the second model, we found that only the educational level of managers/owners did not have a significant influence, while the size and age of the enterprise had a significant influence on financial performance. Entrepreneurial finance had a significant influence on financial performance (β = 0.125, p < .05), supporting H2.

The third model also displayed only the educational level as a non-significant predictor of innovative performance, and entrepreneurial finance had a significant influence on innovative performance (β = 0.178, p < .05), supporting H3.

With mediation, after including CSR in Model 1, the influence of entrepreneurial finance on environmental performance became non-significant (β = 0.078, p > .05), while the impact of CSR on environmental performance maintained significance (β = 0.233, p < .05). Therefore, CSR fully mediates the relationship between entrepreneurial finance and environmental performance, resulting in full support of H4.

After introducing the mediator into Model 2, the influence of entrepreneurial finance on financial performance remained significant (β = 0.391, p < .05), and CSR also maintained its significant influence on financial performance (β = 0.164, p < .05), indicating partial mediation of CSR between entrepreneurial finance and financial performance, resulting in partial support of H5.

In the presence of the mediator in Model 3, the impact of entrepreneurial finance on innovative performance turned non-significant (β = 0.122, p > .05), although CSR remained significant (β = 0.264, p < .05), confirming the fully mediating role of CSR between entrepreneurial finance and innovative performance, and fully supporting H6.

Model 4 indicates that entrepreneurial finance has a significant influence on CSR (β = 0.211, p < .05), supporting H7.

Discussion and Conclusion

This research aimed to bridge the gap identified in the literature between entrepreneurial finance, CSR and the environmental, financial and innovative performances of newly established ventures. The nonexistence of previous empirical studies analysing the importance of entrepreneurial finance in newly recognised SMEs in emerging markets towards integration of CSR practices and performance confirmed the importance of this research, adding value to the body of knowledge. Our research endorses the RBV theory (Barney, 1991) that has recently considered CSR and environmental activities as a part of organisational activities. Using the empirical evidence of new ventures from an emerging market, our research reveals that entrepreneurial finance is essential for CSR and performance in new emerging ventures. This research enriches the RBV literature by shedding light on the importance of entrepreneurial finance boosting CSR to enhance the performance of newly born ventures. In particular, our research tests the importance of entrepreneurial finance in environmental, financial and innovative performances by using CSR as a mediator. Our findings add new evidence to the theory of RBV and acknowledge that entrepreneurial finance as a tangible resource is a key factor of both CSR and the aforementioned types of performance.

Our research arrived at a non-significant relationship with the aspects of entrepreneurial finance in environmental performance. It does not support the findings of Wang and Bansal (2012) and Anwar and Li (2021) who revealed a significant positive association between financial resources and environmental practices. However, these results are not surprising because entrepreneurial finance indirectly contributes to environmental performance through CSR. Our results endorse Fiandrino et al. (2019) who claimed that firms with sufficient financial resources are more likely to invest in CSR, resulting in satisfactory environmental performance. Similarly, Memon et al. (2020) also found that financial availability does not directly configure environmental performance; SMEs instead need to recognise and exploit fruitful opportunities by using their finances to participate in environmental initiatives. One explanation from the results is that newly born ventures first attempt to invest in CSR, which in turn can result in increased environmental performance.

Our research reveals that entrepreneurial finance significantly influences financial performance, supporting the findings of Anwar, Tajeddini, et al. (2020). The results also related to Fatoki (2011) and Wasiuzzaman et al. (2020) who asserted that ventures with sufficient financing have better profitability than their counterparts, and most of the enterprises use finance as a shield against unexpected challenges and loss (Cooper et al., 1997). Moreover, financial capital spurs their sustainable competitive advantage (Khan et al., 2019). Our results show that CSR partially mediates the relationship between entrepreneurial finance and financial performance, consistent with Gregory-Smith et al. (2017) who claimed that customers are willing to pay more for environmentally friendly products that contribute to the sales growth of firms. It can be derived from the results that new ventures need to pay equal attention to both CSR activities as well as profitability.

Our findings show that entrepreneurial finance significantly contributes to innovative performance. The findings are aligned with several studies ascertaining a significant positive association between the financial resources and innovative performance of SMEs (Pellegrino & Savona, 2017; Xiang & Worthington, 2017). Our results specifically lean towards Park and Tzabbar (2016) who revealed that early stage ventures use venture capital to configure their innovation in the market. Our results also confirmed that CSR fully mediates the path between entrepreneurial finance and the innovative performance of newly established enterprises. These findings are aligned with Franco-Leal and Diaz-Carrion (2021) who recommended policymakers provide sufficient finances to social entrepreneurs, allowing them to effectively perform their social and environmental activities, leading in turn to environmental and social innovation. Similarly, Ekins and Medhurst (2006) described that, in an effort to obtain innovative outcomes, social entrepreneurs focus on their financial resources when they aim to participate in social activities. Also, O’Leary et al. (2018) mentioned in their study that Germany, Italy, Finland, Greece and Spain have special programs to financially support entrepreneurs as they engage in social activities and innovation. We learn from these findings that ventures with sufficient entrepreneurial finance participate in CSR, boosting their innovative performance.

To summarise, our findings endorse the notion that financial resources are crucial for CSR and environmental initiatives (Anwar & Li, 2021; Diefendorf, 2000; Owen et al., 2018; Spanos, 2018). As a result, CSR significantly improves environmental, financial and innovative performances (Bernal-Conesa et al., 2017; Martinez-Conesa et al., 2017; Ruggiero & Cupertino, 2018).

Implications for Practice

The findings from this research have practical implications for top managers and owners of newly established ventures as well as for policymakers. Environmental, financial and innovative performances are essential for new ventures. Hence, managers/owners of new enterprises need to pay sufficient attention to performance determinants. Our results indicate that entrepreneurial finance is one of the best strategies that can either directly or indirectly boost the performance of enterprises. This notion is supported in several studies (Cumming & Vismara, 2016; Park & Tzabbar, 2016; Shi & Xu, 2018), especially Anwar, Tajeddini, et al. (2020), who showed that entrepreneurial finance is a significant predictor of new venture success in emerging economies.

Our results display an indirect role of entrepreneurial finance in innovative and environmental performance where the relationship is mediated by CSR. Entrepreneurial finance is considered a stimulant for CSR in business ventures regardless of their size and nature of business. Therefore, owners and managers of new ventures should strive to establish favourable ties and relationships with banks, financial institutions and political bodies to access entrepreneurial finance. This financing can be in turn used for CSR, resulting in desirable environmental and innovative performance. Customers favourably endorse products if they think they are environmentally friendly (Gregory-Smith et al., 2017), contributing to sales growth and profitability. Financial resources therefore not only configure CSR, environmental activities and profitability, but also boost the innovative performance of ventures.

It is a well-known phenomenon that SMEs face a shortage of resources, hindering their participation in social and environmental activities (Khattak, 2020; Memon et al., 2020). Financial capital shortages will be the greatest challenge of newly established ventures due to their smallness and lack of internal resources. Hence, new ventures should utilise finance in a way to cope with external challenges and competition by producing new and unique products. New ventures should pay close attention to entrepreneurial finance, as it can either directly influence performance (e.g., financial performance) or indirectly contribute to environmental and innovative performance through CSR.

Limitations and Future Research

The first limitation of this research is seen with its sample size. We encourage future research to survey the maximum number of newly established SMEs from different cities in Pakistan for better results in a better, deeper manner. The second limitation is this study’s use of cross-sectional data, with higher probabilities of common method variance and social desirability bias. Longitudinal studies and in-depth interviews can be considered for future work in an effort to avoid this. Third, the survey was conducted in Pakistani SMEs, which may not be suitable representatives of other emerging markets. Evidence from other countries can help deepen the generalisability of the insights and implications found here. Fifth, our hypothesised model is limited to newly established SMEs. Both mature as well as large firms have adequate resources, thereby investing more in environmental and innovative activities (Marti & Scherer, 2016). A comparative study between new and mature ventures will provide useful insights concerning their financial and environmental activities.

Our research confirms entrepreneurial finance as a significant direct predictor of financial performance, and an indirect predictor of environmental and innovative performance. Moreover, our research reveals that CSR partially mediates the relationship between entrepreneurial finance and financial performance, while it fully mediates the association between entrepreneurial finance and environmental as well as innovative performance.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.