Abstract

The present study examines the bidirectional relationship between earnings management (EM) and the three dimensions of the ESG (environmental, social and governance) framework. The modified Jones model and Roychowdhury model were used for estimating the EM proxies. The study covers 82 companies (492 firm-year observations) during the period FY 2018–2019 to FY 2023–2024. The study reveals that among the three pillars of ESG, the governance (G) pillar is more effective than the environmental (E) and social (S) pillars in regulating managerial discretion. Even though the total EM was lower during the pandemic period, firms used current accruals as a tool to signal their performance. Findings of the study can aid policymakers and managers in enhancing the disclosure of environmental and social initiatives in India. Also, SEBI should consider the compilation of an integrated ESG rating mechanism to ensure standardization and consistency in reporting E, S and G engagements of the entity, as it can promote long-term prospects of the investors.

Introduction

The subprime lending that led to the Global Financial Crisis in 2008 redefined the concept of financial reporting (Earle, 2009). One of the major reasons for this crisis was managers’ discretion in lending high-interest loans to borrowers with higher risk and lower credit ratings (Feldkircher, 2014; Velde et al., 2008). Even the market analysts and external scrutinizers failed to forecast this market failure due to the purposive intervention by the insiders in reporting the financial figures (Head, 2010). The failure of major business giants such as Xerox, Enron and WorldCom has questioned the credibility of the figures reported in the financial statements (Hope, 2010). At that time, the credibility and prospects of the borrower were analysed based on their credit ratings assigned by the credit-rating agencies (CRAs) (Abraham & Kumar, 2023). The CRAs assign credit-rating scores after making an independent and unbiased assessment of the quality of firm fundamentals (Chen et al., 2015). However, the issuer-pay model, where the firm (issuer) pays CRAs for rating their public issue, has adversely affected the credibility of the credit-rating mechanism (Wangrow & Schepker, 2015). The issuer-pay model has been widely criticized due to the undue influence of insiders on CRAs, where the CRAs were highly rewarded for assigning favourable ratings to the entity. Evidence for such insider interventions is quite evident during various scenarios such as better proceeds during the public issues (DuCharme & Malatesta, 2001), avoiding debt covenant violations (Nalarreason et al., 2019), meeting analyst expectations (Zhang et al., 2018) and favourable valuations in corporate acquisitions (Louis, 2004). Even though these interventions benefit the insiders in the short run, they adversely affect the wealth of investors as well as the valuation of the entity in the long run (Brennan, 2021).

Due to the drainage of wealth, investors realized that reported figures disclosed in the financial statements cannot solely be depended on for making investment decisions. Thus, the concept of non-financial reporting, such as ethical reporting, sustainability reporting and green reporting, became popular following the compilation of Sustainable Development Goals by the United Nations. Thus, the integration of ESG aspects in financial reporting balances the financial benefits with ethical considerations (Paulsy, 2024). A firm that aligns with ESG standards is supposed to address environmental, social and governance issues effectively (Clementino & Perkins, 2021). At the global level, Bloomberg is one of the most prominent agencies that analyses the ESG performance of entities and publishes reports on ESG compliance (Pyles, 2020). So, a firm with higher ESG scores is considered to be more ethical and responsible towards its stakeholders (Gerard, 2019). Therefore, an increase in the interest of investors towards ESG metrics induced the managers to use higher ESG performance scores as a tool to manage their earnings (Kotsantonis et al., 2016). A firm that complies with higher ESG standards is subjected to minimal external scrutiny in the capital market (La Rosa & Bernini, 2022). So, the ESG framework has become a double-edged sword as it has its ethical compliance on one side and the enhanced ESG disclosure on the other side, being used as a tool to manage their earnings, which has made ESG metrics a controversy among the research community and regulators as well (Dasgupta, 2022). Thus, the integrity of ESG reporting demands an in-depth analysis in emerging markets, especially in India, where the sustainability reporting is at its initial phase due to the constraints in technology, availability of non-financial data, underdeveloped frameworks and so on (Tarczynska-Luniewska et al., 2024). So, the present study raises the following research question:

RQ: Are the environmental, social and governance pillars of the ESG framework effective in regulating insider discretionary behaviour in an emerging market like India?

Empirical evidence argues that the ESG framework in India serves as an important supplementary governance tool rather than a standalone solution for addressing earnings management (EM) practices (Dasgupta, 2022). Evidence documents that higher ESG disclosure quality is associated with reduced information asymmetry between managers and investors (Samarakoon et al., 2024). However, Mendiratta et al. (2023) also argue that an increase in media coverage on ESG controversies will reduce the firm value, and it will discourage managers from engaging in ESG-related misconduct, as it could trigger external scrutiny and investigation on insider interventions. The concept of sustainability investing became popular among Indian investors following the compilation of the Nifty ESG 100 Index in 2018, the first ESG-based index in India. The introduction of the corporate governance code (CGC) in the Companies Act 2013 and Clause 49 in the listing agreement contributed to the effective implementation of the ESG framework in India (Sharma et al., 2023). Due to the urge for sustainability reporting in the investing community, SEBI has mandated the large-cap companies to file business responsibility and sustainability reporting (BRSR). However, Devi and Firoz (2025) argue that early adoption of the ESG framework among Indian firms is motivated by the incentives for regulatory compliance that will lead to greenwashing (exaggeration of ESG engagements) of transactions.

A few studies have explored the linkage between EM and ESG compliance in the Indian context (Sabirali et al., 2025; Samarakoon et al., 2024), in which they focused on the composite impact of ESG compliance on EM. However, literature remains silent about the individual contribution of environmental (E), social (S) and governance (G) pillars in regulating managerial discretionary practices in India. Also, to the best of the authors’ knowledge, this is the first study that addresses both accrual-based and real EM practices in Nifty ESG 100, the first index in India based on sustainability compliance that represents nearly 72% of the floated market capitalization. Using 82 non-financial companies listed in the Nifty ESG 100 Index from 2018–2019 to 2023–2024 (492 firm-year observations), we found that the compilation of the ESG framework is effective in reducing EM practices. The present study also reveals that among the three pillars of ESG, the governance (G) pillar is more effective than the environmental (E) and social (S) pillars in regulating managerial discretion. The study also found that, even though the total earnings management (TEM) was lower during the pandemic period, firms used accounting accruals as a tool to manage their earnings.

Review of Literature and Hypothesis Development

EM is considered one of the prominent challenges in ensuring the integrity of financial reporting in the modern era. When the managers or insiders of the entity prioritize their personal gains over organizational benefits, a conflict of interest arises between the agents (managers) and principals (owners) of the company. Even though numerous theories in the literature explain the EM behaviour, agency theory is considered to be the prominent one that explains the asymmetry of information between the owners and insiders of the entity, which creates the scope for managerial discretionary practices. Jones (1991) found the primary evidence for such managerial discretion, where US firms managed their earnings to increase the availability of relief grants on their imports. Later, Teoh et al. (1998) revealed that the managers used their discretion in managing their accruals to get better proceeds during the IPOs. Likewise, Chen et al. (2015) found that firms employ both accounting accruals and cash transactions to enhance their credit ratings. Similarly, firms with financial requirements will use current accruals to avoid the violation and restructuring of their debt contracts (Jaggi & Lee, 2002). Managers also use their discretion to meet or beat analyst forecasts and benchmark in the capital market (Dutta & Gigler, 2002). Even though the management of earnings enhances the value of the firm in the short run, it will adversely affect the wealth of shareholders due to the reversal of accounting accruals in the future (Dang et al., 2018). Thus, the aggressive EM has enhanced the credit ratings of the entity but deterred the quality of financial statements and resulted in the drainage of shareholders’ wealth (Yahanpath & Joseph, 2017). The presence of aggressive EM in financial statements magnified the need to incorporate ethical and responsible aspects into financial reporting (Abraham, 2024), because an entity is responsible not only towards its owners but also towards the environment and society in which it operates (Nalarreason et al., 2019). A responsible and ethical approach in business conduct can be facilitated through a proper governance mechanism (Velayutam, 2018). However, due to aggressive EM, concerns about ethical aspects have risen. So, apart from considering the financial aspects alone, investors have started to analyse the risk propensity of an entity in terms of its ESG aspects of their investments (Ehsan et al., 2020).

As far as the protection of investors is concerned, the passage of the Sarbanes–Oxley (SOX) Act in 2002 is supposed to be the pioneering step towards securing the financial interest, while the non-financial interest at the global level was addressed for the first time through the global reporting initiative that standardized the reporting of CSR and sustainability engagements (Halkos & Nomikos, 2021). The rapid surge in sustainable investments at the global level has redefined the concept of traditional investments based on financial metrics, as the former has a significant impact on the long-term prospects of the entity. Thus, the integration of sustainability aspects in financial reporting has led to the concept of impact reporting (Tschopp & Huefner, 2015). One of the vital elements in impact reporting is engagement in CSR activities, where the investors presume that higher CSR engagement mitigates managerial discretionary practices (Dhaliwal et al., 2011), because higher CSR compliance signals that the conduct of business practices is in line with social norms and ethical standards, and is legitimate to the accepted rules and regulations (Abraham, 2024; Bian et al., 2021). However, the growing concern about climate change and corporate governance aspects at the regional as well as international level led to the inception of the ESG framework by incorporating environmental aspects along with social and governance aspects by redefining the prevailing CSR mechanism (Bose, 2020).

As far as the pillars of the ESG framework are concerned, the environmental pillar discloses the initiatives taken by the entity to preserve natural resources and reduce the emission of pollutants (Singhania & Saini, 2023). Empirical evidence suggests that environmentally committed firms invest more in green initiatives, which reduces their political costs and enables them to procure funds at lower costs (Chakroun et al., 2022). Empirical evidence also reveals that family firms are more concerned with investing in green initiatives and disclose the same to maintain their long-term ethical orientation and reputation in the capital market (Campopiano & De Massis, 2015). However, the social pillar of the ESG framework reveals the extent to which business practices are ethical and beneficial to society by ensuring quality and integrity in delivering goods and services for their well-being (Sanches et al., 2018). Firms with high societal engagements can enhance their corporate image (Lodhia et al., 2020) and create a sense of legitimacy that eventually mitigates managerial discretionary practices (Abraham & Kumar, 2023; Lopez-Gonzalez et al., 2019). As far as the governance aspect of the ESG framework is concerned, it analyses the processes and systems that ultimately protect the interests of shareholders and stakeholders of an entity (Sassen et al., 2016), because investors presume that firms with high governance disclosure scores are less prone to manage their earnings due to the effectiveness of their internal control system (Goyal & Gulati, 2024).

However, the integrity of the ESG framework became controversial when managers employed greenwashing (exaggerating environmental initiatives) and brownwashing (understating environmental initiatives) approaches in managing their earnings (Kim & Yoon, 2023). Empirical evidence from the high-income economies argues that firms with higher ESG compliance are less prone to EM using accounting accruals; instead, they tend to smooth their earnings using real transactions (Velte, 2021). Similarly, firms with unstandardized and inconsistent reporting policies use CSR disclosures as a tool to smooth their earnings and to reduce their borrowing cost (Miroshnychenko & De Massis, 2022).

However, the evidence from recent studies highlights a negative association between EM and ESG disclosure in emerging markets (Almubarak et al., 2023; Liu et al., 2023; Nuhu & Alam, 2024). Mandatory ESG disclosure has significantly reduced managerial discretionary practices in Chinese firms (Cui et al., 2024). Similarly, empirical evidence from emerging markets reports that higher ESG performance has enhanced the quality of earnings (Vatis et al., 2025). Recently, in a study among six emerging economies, Mohapatra et al. (2025) report that ESG disclosure mitigates managerial discretion using current accruals. Litt et al. (2013) argue that engagement in environmental initiatives reduces EM using accounting accruals. Likely, Gaio et al. (2022) report that involvement in social initiatives reduces managerial discretionary practices in the emerging market. Similarly, Ghaleb et al. (2022) reveal that firms with higher corporate governance compliance are less likely to manage their earnings. Recent studies also found that ESG reporting or sustainability reporting in emerging markets has enhanced the transparency and integrity of reported figures (Masmoudi & Ben Salem, 2024). As far as India is concerned, mandatory CSR compliance in the Companies Act 2013, inclusion of Clause 49 in the listing agreement and compilation of the BRSR framework make India one of the few emerging economies with standardized ESG disclosures. Although a growing body of literature suggests a negative association between ESG performance and EM, this relationship remains inadequately explored within the unique institutional framework of India. Also, the existing studies in India have primarily focused on corporate governance in isolation or on aggregate ESG scores and their linkage in regulating EM practices (Maji & Lohia, 2023). Unfortunately, the recent evidence of greenwashing and brownwashing transactions in India undermines the effectiveness of the ESG framework in India (Mulchandani & Vishnani, 2025). Integration of financial elements with the sustainable aspects under the ESG framework reduces EM using accounting accruals (AEM) but fails to address cash-based EM (REM). As per the MSCI 2024 report, among the emerging economies, India holds the third position in terms of growth in sustainable investments. Therefore, it warrants further investigation to assess how each pillar in the ESG framework independently influences accruals as well as cash-based EM behaviour among companies listed in the Nifty ESG 100 Index, the first ESG-based index in India, which was compiled in 2018. So, we hypothesize the following to address the role of the ESG framework and its pillars on managerial discretionary practices in India.

H1a: Environmental initiatives mitigate AEM.

H1b: Environmental initiatives mitigate REM.

H1c: Environmental initiatives mitigate TEM.

H2a: Social initiatives mitigate AEM.

H2b: Social initiatives mitigate REM.

H2c: Social initiatives mitigate TEM.

H3a: Governance initiatives mitigate AEM.

H3b: Governance initiatives mitigate REM.

H3c: Governance initiatives mitigate TEM.

H4a: Compliance with the ESG framework reduces AEM.

H4b: Compliance with the ESG framework reduces REM.

H4c: Compliance with the ESG framework reduces TEM.

Data and Methodology

Sample Selection

The present study analyses the role of E, S and G pillars of the ESG framework in regulating EM practices in India. The final sample of the study, after eliminating financial companies and companies with missing data, stands at 82 companies (492 firm-years) in the Nifty ESG 100 Index, the first sustainability index in India compiled in 2018. The study covers the period FY 2018–2019 to FY 2023–2024. Financial data were extracted from the CMIE Prowess IQ database and annual reports of the companies. The ESG-related data were collected from the Refinitiv Eikon database. EViews 10 and Stata 15 software were used for analysing the collected data.

Estimation of EM Proxies

Managerial discretionary practices are done through both accrual-based and real transactions. One of the major challenges in EM research is the difficulty in detecting managerial discretion from the reported figures.

Accrual Earnings Management

Accrual earnings management (AEM) is estimated as the proxy called discretionary accruals (DA) as a difference between non-discretionary accruals (NDA) and total accruals (TA). Here, we applied the modified Jones model (Dechow et al., 1995) to estimate DA, as it gives the best approximation for AEM (Costa & Soares, 2021).

The value of TA is estimated using the following equations:

ΔCA indicates the change in the value of short-term assets of firm j in the year n, ΔCash suggests the change in the cash balance of firm j in the year n, ΔCL indicates the change in the value of short-term liabilities of firm j in the year n, ΔSTD indicates the change in the value of short-term debt of firm j in the year n and Dep indicates expenses on depreciation and amortization for the firm j in the year n.

The magnitude of NDA is estimated using the following equation:

Thus, the proxy for AEM, DA is estimated as the difference between TA and NDA:

In the year t, firm-specific parameters are denoted as α0, α1 and α2; the change in revenue scaled by the total assets is indicated as ΔREV; the change in receivables scaled by the total assets is denoted as ΔREC; and the gross value of the plant-property equipment of the firm j in the year n is denoted as PPE. Here, A indicates the value of total assets of entity j in the year n.

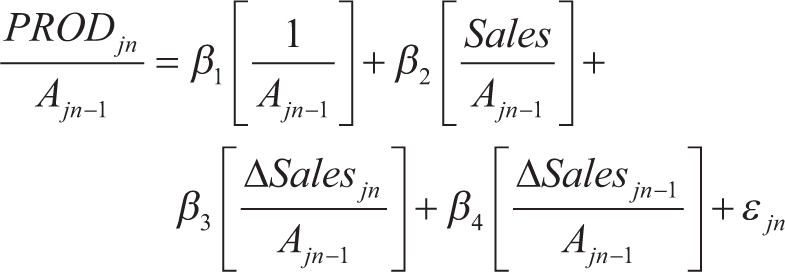

Real Earnings Management

Due to the difficulty in the estimation, real earnings management (REM) is estimated as the sum of various proxies such as AbnProd (abnormal production cost), AbnCash (abnormal cash flow from operations) and AbnDis (abnormal discretionary expenses). We employed Roychowdhury’s (2006) model, which gives the best approximation in the estimation of REM proxies (Joosten, 2012).

AbnProd is estimated using Equation (5), where the entity tries to reduce the per unit cost of production by increasing the volume of production (Dakhlallh et al., 2020). Here, PROD = Cost of goods sold + Change in inventory. The error term of Equation (5) gives the abnormal production cost.

AbnCash (abnormal CFO) is estimated using Equation (6), where CFO indicates cash flow from operations, and Sales and ΔSales indicate operational revenue and change in the operational revenue, respectively. The error term of Equation (6) indicates the abnormal CFO of the entity.

Managers use their discretionary powers in various expenses such as research and development, advertising and marketing, and selling, general and administration to manage their earnings.

AbnDis (abnormal discretionary expenses) is estimated using Equation (7).

TEM is taken as the sum of AEM and REM proxies, assuming that firms can manage their earnings using accounting accruals as well as cash transactions (Cohen et al., 2008). That is,

Several control variables such as the size of the firm (SIZE), age of the firm (AGE), Tobins Q (TQ), Leverage (LEV), firm growth (GROW), cash flow (CFO) and return on assets (ROA) are introduced in the regression models to reduce the effect on the response variables (Dokas, 2023, Zamri et al., 2013).

Table 1 illustrates the variables used in the regression analysis along with their corresponding descriptions.

Variables and Their Description.

The following regression models were used in the study:

The results of Breusch–Pagan Lagrange Multiplier (BP-LM) suggest the application of random effects over the pooled OLS regression. Hausman test (HT) was applied to choose the appropriate regression model, and the HT statistics confirm the application of the fixed-effects model over the random-effects model (Amini et al., 2012). The test statistics of the Durbin–Watson test (1.981) and the values of VIF (Table 3) suggest that there are no serious issues of autocorrelation and multicollinearity (Williams & Grajales, 2019). The augmented Dickey–Fuller (ADF) test was used to analyse the stationarity of the data. We failed to reject the null hypothesis due to the presence of unit root at level. However, at first difference, the p values of ADF test statistics are less than .05, suggesting that variables are stationary. The p values of Jarque–Bera are above .05, confirming the normality of variables.

The outbreak of COVID-19 witnessed severe economic impacts such as shrinkage in cash flow, volatility in the stock market, shift in investor risk perception, moratorium and waiving of interest (Habib & Anik, 2021). So, the structural break in the data during the COVID-19 (FY 2020–2021) period was analysed using the Chow test. The dummy variable COV19 was introduced to incorporate the impact of structural break by assigning a value of 1 to FY 2020–2021 and 0 to the other periods (Usheva & Vagner, 2021; Zhang & Zheng, 2022).

Results and Discussion

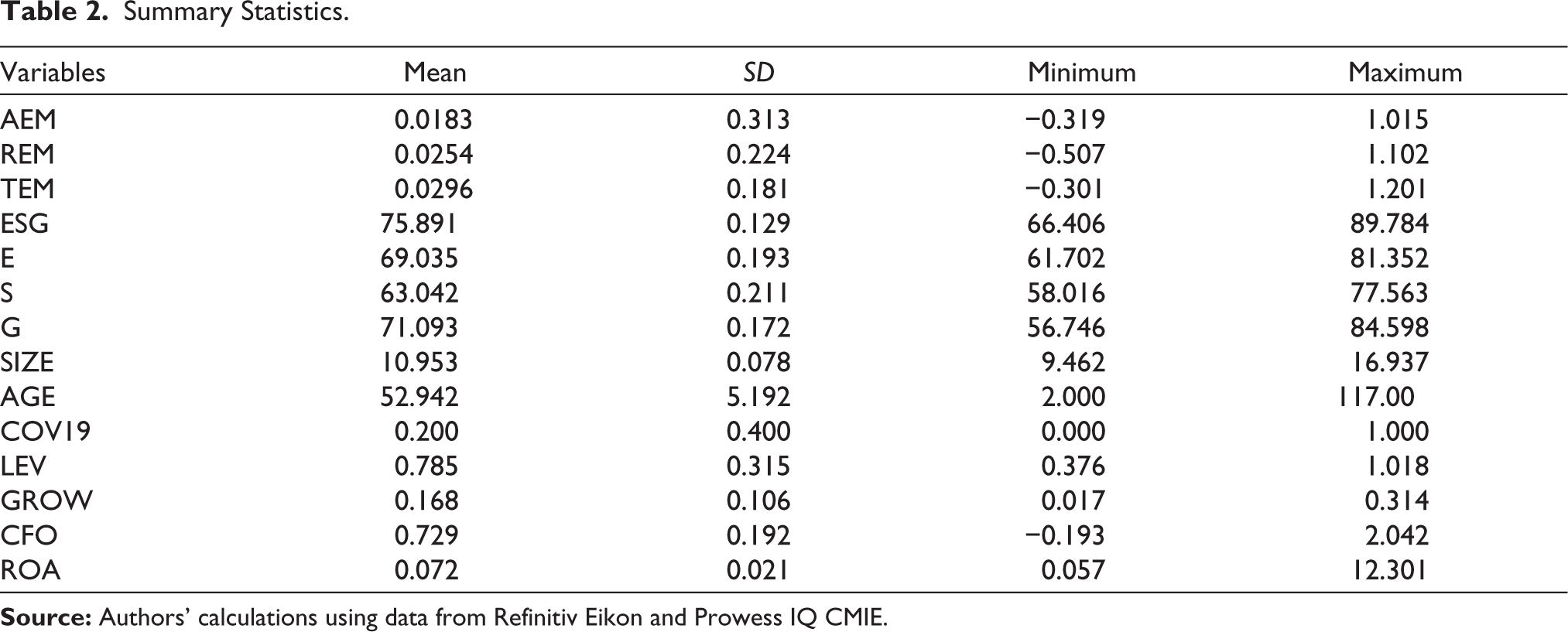

The summary statistics reported in Table 2 describe the nature of the variables used in the study. The descriptive statistics observe that the average value of REM is slightly higher than the mean value of AEM, which indicates that firms are more prone to manage their earnings using real transactions, as it is difficult to detect. Also, the mean value of TEM (0.029) indicates that sample firms in the study are managing their earnings as nearly 3% of their total assets.

Summary Statistics.

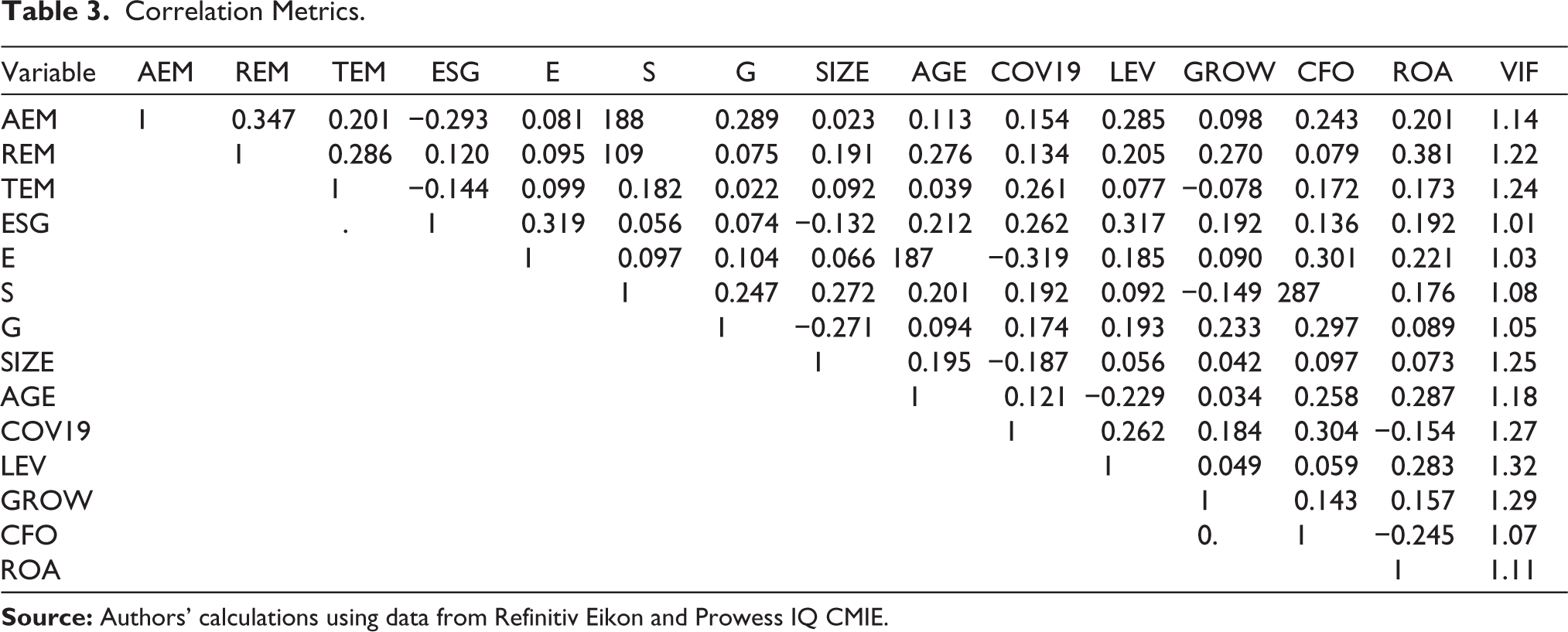

The mean value of the ESG score (75.9) indicates that firms in the study have higher ESG compliance. Among the three pillars of ESG, Pillar G possesses the highest mean value (71.09) and Pillar S has the lowest mean value (63.04). Pearson’s correlation matrix between all the variables used in the study is reported in Table 3. The highest value in the correlation matrix stood at 0.347, and all the remaining correlation coefficients between the variables are within the recommended level (0.8) (Gujarati, 2009). As far as the VIF values are concerned, LEV has the highest VIF statistics (1.32), and E has the lowest VIF statistics. So, all values of VIF are less than 2, suggesting that there is no serious issue of multicollinearity (Groß, 2003).

Correlation Metrics.

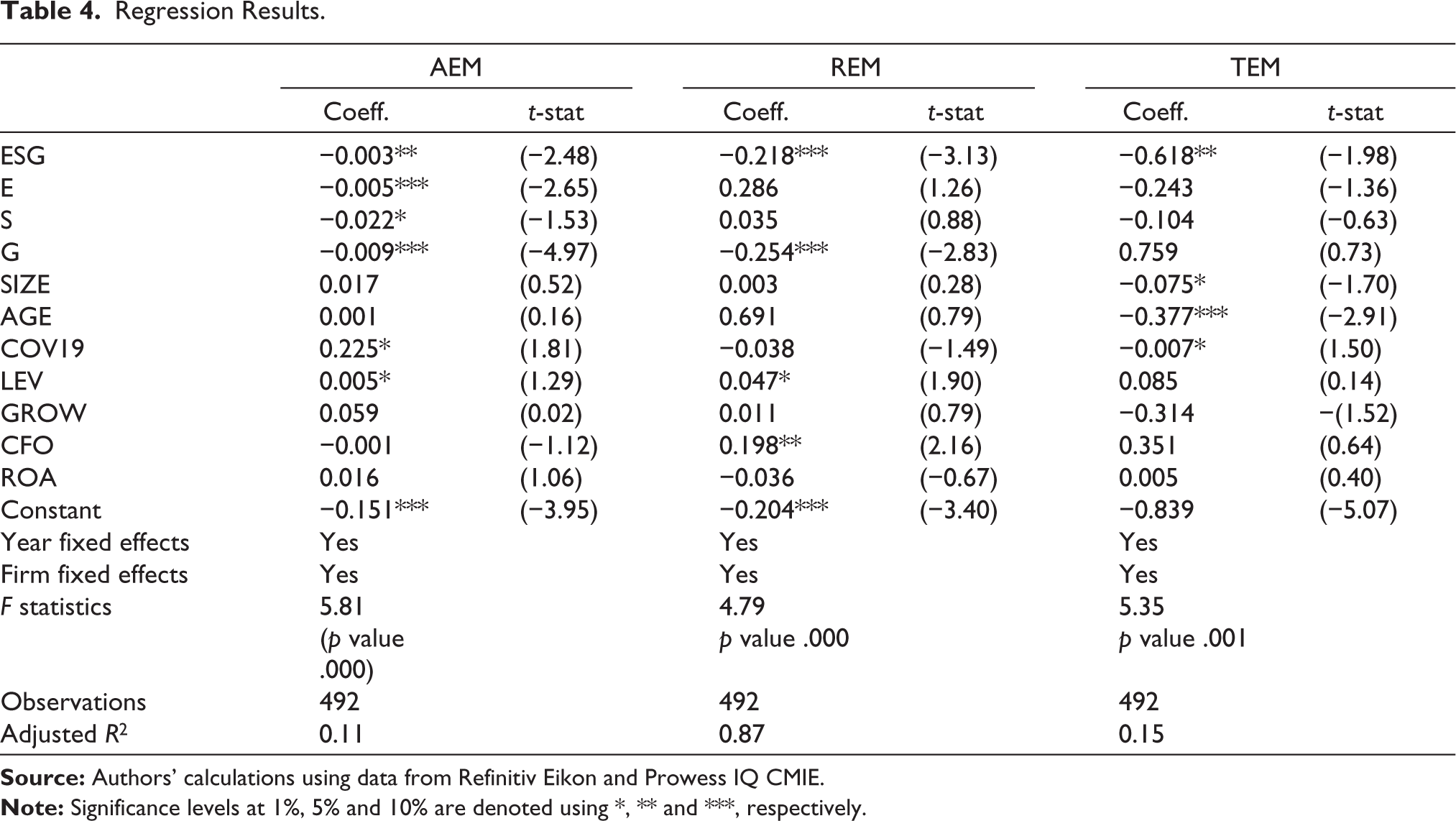

The results of fixed-effect multivariate regression analysis to assess the role of ESG and its three (E, S and G) pillars on the proxies of EM (AEM, REM and TEM) are illustrated in Table 4. The regression coefficient of the composite ESG score reports that it is negatively associated with all three proxies of EM (supports H4a, H4b and H4c). It is in line with Abraham & Kumar (2025), who also found the evidence for inverse association.

Regression Results.

On the other hand, the coefficients of E and S are inversely associated with managerial discretion using accounting accruals (supports H1a and H2a). It reaffirms the evidence of Litt et al. (2013), Ghaleb et al. (2022) and Abraham and Kumar (2025), who reported that environmental and social engagements reduce EM using current accruals. However, it is not surprising that the regression estimate of G is negatively significant to both accrual-based and real EM (supports H3a and H3b). It is in line with the findings of Al-Haddad and Whittington (2019), who revealed the role of effective corporate governance mechanisms in reducing AEM and REM. It is also evident from the results that COV19 is positively significant to AEM and negatively significant to REM and TEM. It is similar to the findings of Ricapito (2024), who posits that, during the pandemic, firms use current accruals to signal their performance to the stakeholders and potential investors. However, findings of the study are contrary to Buertey et al. (2024), ElHawary and Elbolok (2024) and Kuo et al. (2024), who argue that managerial discretion and involvement in ESG initiatives are positively associated, because insiders of managers use their discretion in disconnecting the disclosure of sustainability initiatives and performance aspects for their benefit (García-Sánchez & García-Sánchez, 2020).

As far as the control variables are concerned, AGE and SIZE are negatively significant to TEM. This implies that firms with larger sizes and ages tend to manage their earnings less due to their reputation and long-term prospects (Wijaya et al., 2020). The positive association of LEV with AEM and REM is similar to the findings of Dyreng et al. (2022) that firms use both accrual and real transactions to avoid debt covenant violations. Likely, the coefficients of CFO are positively associated with REM, which implies that an increase in the cash flows enables firms to manage their earnings using real transactions (Boujelben et al., 2020).

Findings of the study highlight the fact that the long-term prospects of an entity depend on its commitment and continued involvement in sustainable business practices. Also, the agency theory states that managers substitute their short-term personal benefits for the long-term shareholder benefits, whereas the stakeholder theory mitigates managerial opportunism in disclosing financial and non-financial information. Stakeholders always expect transparency and reliability in the reported figures for making efficient financial decisions on time (Ehsan et al., 2020). So, in the modern scenario, managers perceive sustainable business practices as the mantra to long-term stakeholder relationships by reducing principal–agent conflicts and managerial discretionary practices. Managers believe that sustainable business practices can enhance their managerial reputation, survival and growth in the long run (Mukherjee & Sen, 2022).

So, it is evident from the study that compilation of the ESG framework is effective in curtailing both accrual, cash-based and total EM among the companies listed in the Nifty ESG 100 Index. Mandating the CSR regulations in the Companies Act, Clause 49 in the listing agreement and the BRSR framework by SEBI has resulted in the holistic adoption of ESG principles by integrating the financial objectives with the non-financial prospects of the entities. Composite ESG score captures the synergistic effect; when governance controls are combined with environmental and social visibility, managers face multiple channels of scrutiny from NGOs, stakeholders and regulators such the Green Tribunal and Labour Commission. While considering the role of the governance (G) pillar in deterring both accruals and cash-based EM, SEBI’s focus on board independence and audit quality reinforces this deterrent effect. In India, compared to the environmental and social engagements, governance activities are highly visible to the stakeholders due to the provisions embedded in the CGC. So, both E and S pillars individually contribute to regulating accrual-based EM but not real EM. The absence of a strong internal control mechanism in environmental and social reporting in India makes it less standardized and inconsistent. So, inconsistency in E/S reporting results in greenwashing transactions.

Analysis of the Bidirectional Relationship of ESG and Its Pillars with EM Proxies

It is evident from the literature that nowadays ESG metrics are widely criticized as managers use them as a tool to manage earnings using numerous techniques such as greenwashing (Nguyen et al., 2022) and brownwashing (Kim & Lyon, 2015). Thus, the inverse association between ESG and EM is addressed through empirical models, in which we consider composite ESG score and E, S and G pillar scores as dependent variables and AEM, REM and TEM as independent variables.

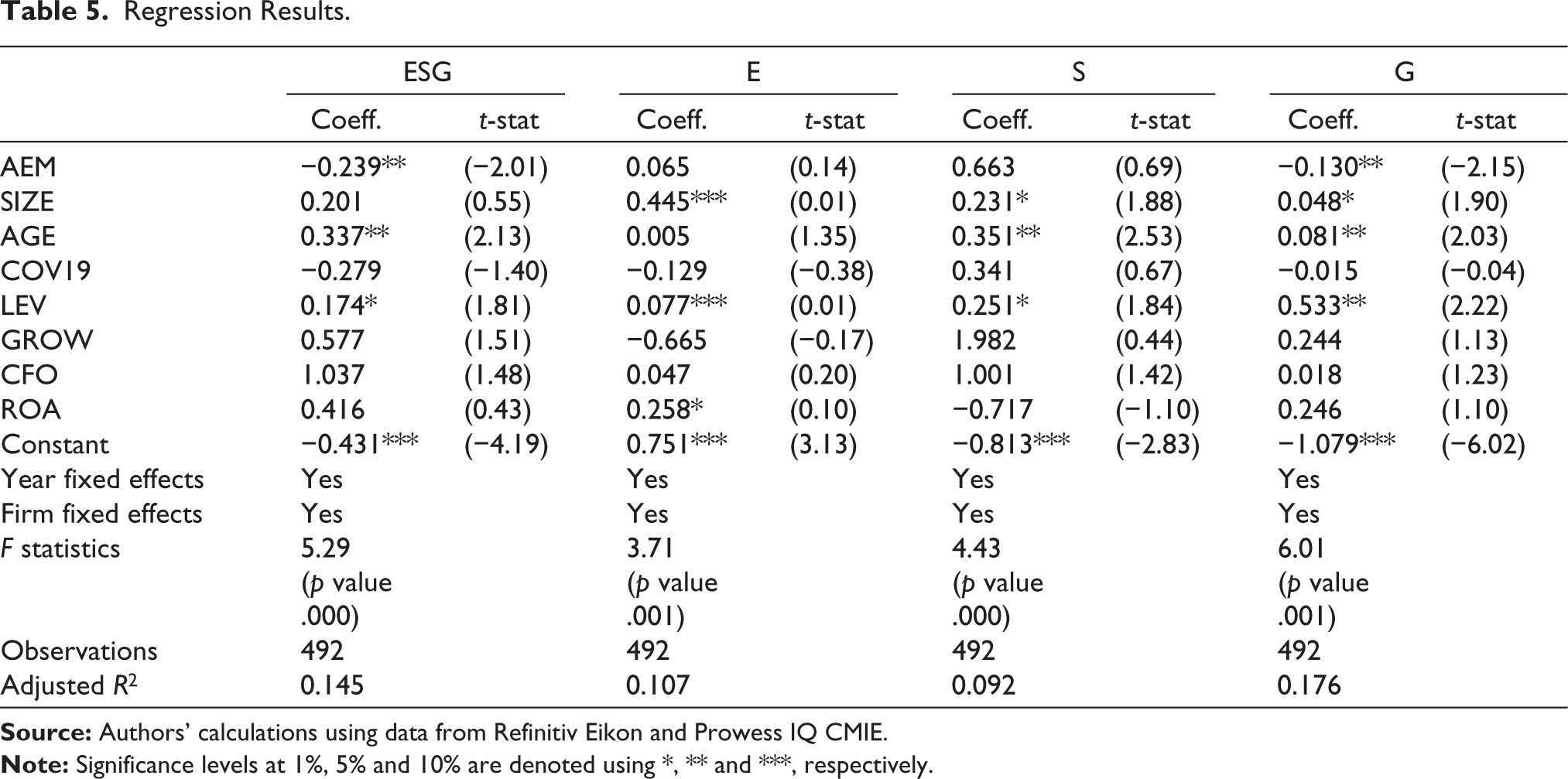

Table 5 illustrates the results of regression analysis with ESG, E, S and G scores as dependent variables and AEM as an independent variable. The coefficients of combined ESG and governance (G) scores are negatively significant to AEM. This confirms the previous findings of Bekiris and Doukakis (2011) and Ghaleb et al. (2022), who argue that firms with higher corporate governance compliance tend to manage their earnings less using accrual transactions due to their ethical obligations to stakeholders.

Regression Results.

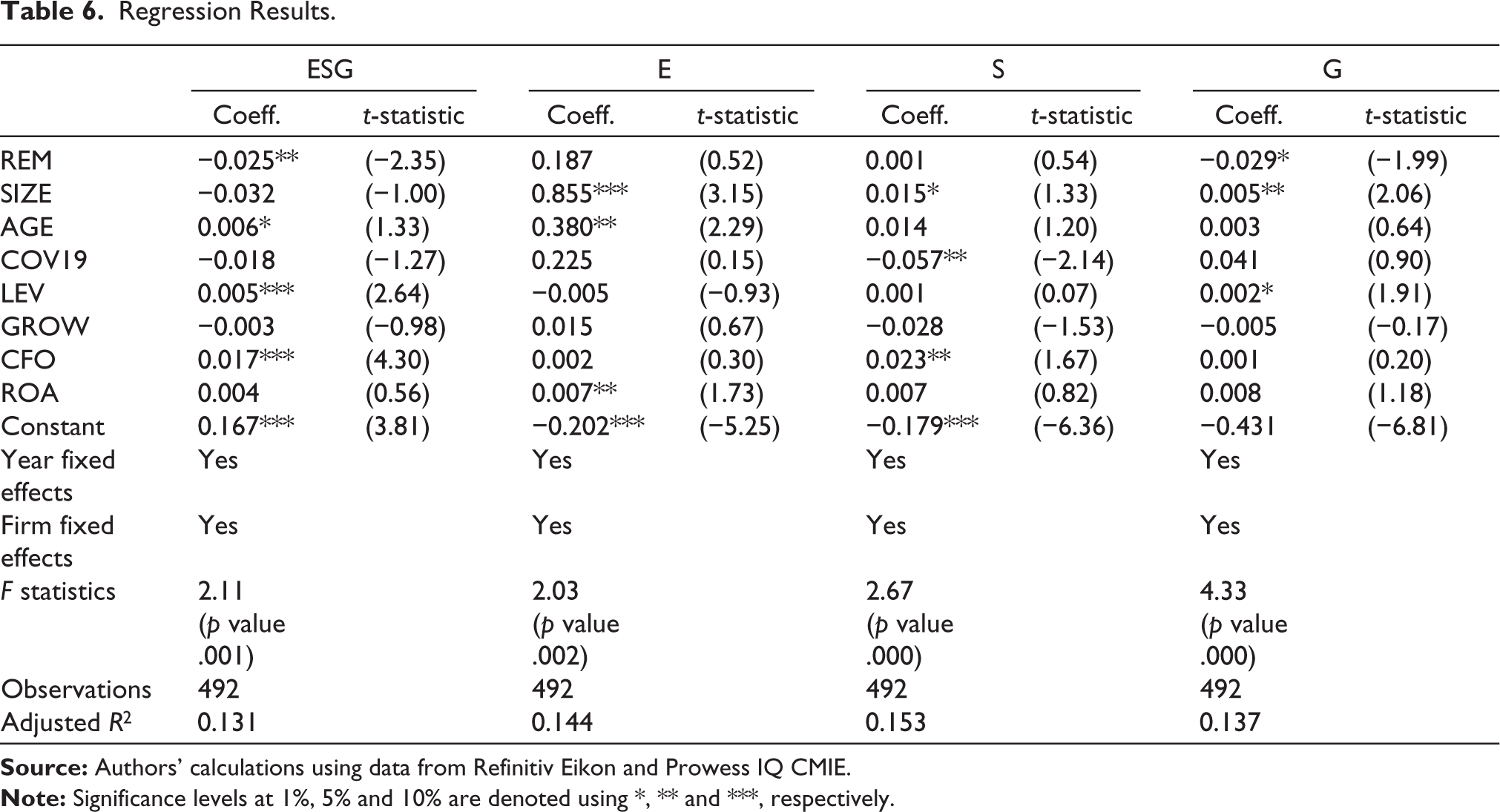

The results of multivariate regression analysis with combined ESG, E, S and G scores as dependent variables and REM as the independent variable are depicted in Table 6. A negative association of REM with ESG and G pillar indicates that compliance with sustainability aspects and governance mechanisms is effective in mitigating EM using real transactions. As our sample constitutes large-cap firms, findings are similar to Maji and Lohia (2023) and Drempetic et al. (2020), who report that larger firms tend to invest more in ESG initiatives. Also, the SEBI DRG study reveals that the magnitude of EM in large-cap companies is low as compared to the mid-cap and small-cap firms in India (Ajit et al., 2013). The negative coefficient of COV19 to social (S) score reveals the shrinkage of social investments during the pandemic period, and it reaffirms Rubbaniy et al. (2022), who revealed the decline in social initiatives during the pandemic period due to the contraction in business activities.

Regression Results.

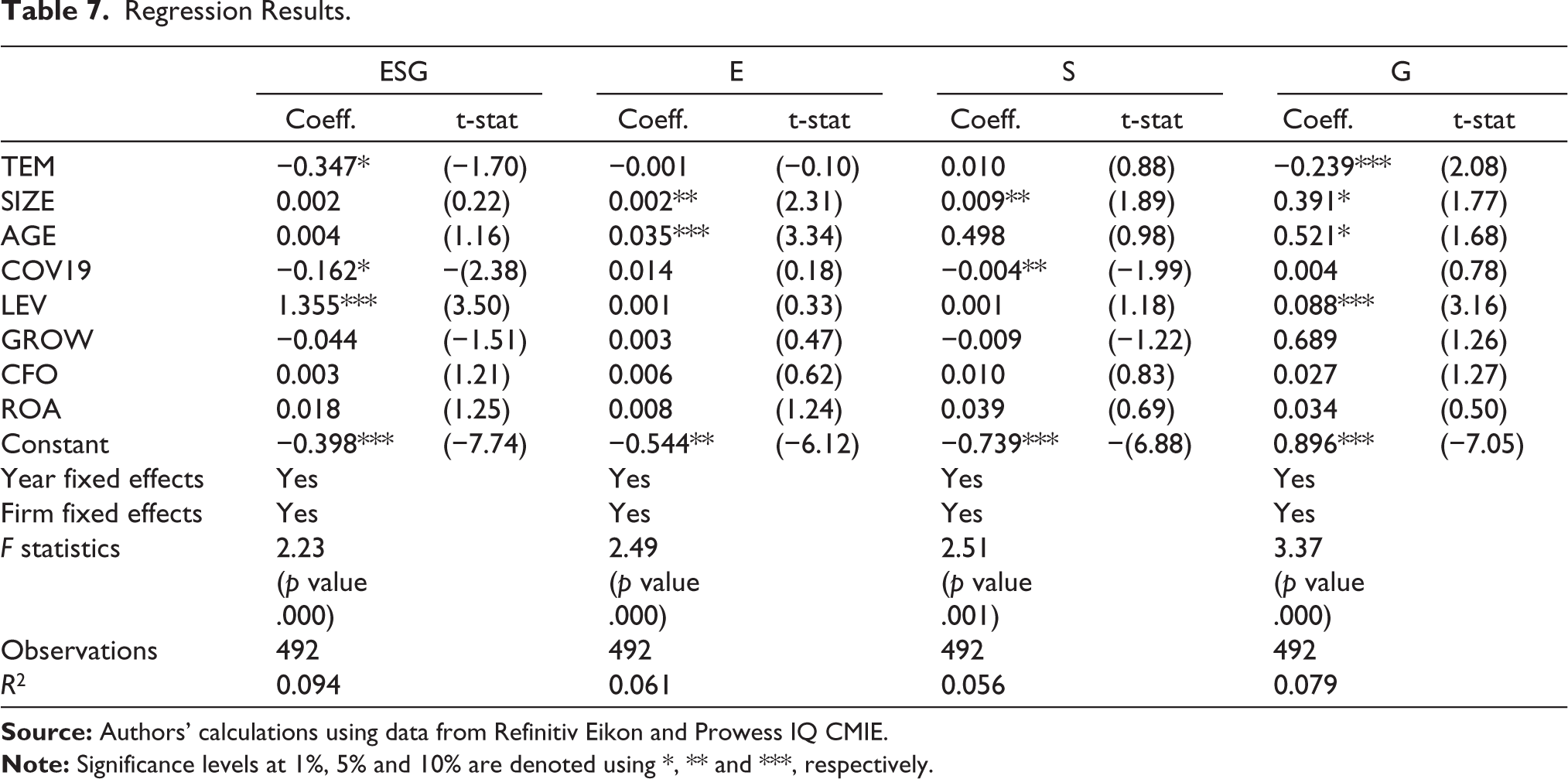

Table 7 illustrates the results of multivariate regression analysis with ESG, E, S and G as dependent variables and TEM as an independent variable. Regarding TEM, the coefficients are negatively significant with the ESG and G aspects of the entities. It supports Sun et al. (2024), who posit that higher compliance with the ESG framework and corporate governance mechanisms mitigates managerial discretionary practices.

Regression Results.

As far as our samples are concerned, large-cap firms are reputable firms with long-term prospects, and hence, they are more active towards sustainable business practices due to their ecological and ethical considerations (Akhtar et al., 2023). It is also evident from the results that the regression coefficient of COV19 is negatively significant to ESG and S scores, which infers the adverse impact of the pandemic on sustainable initiatives due to the contraction in cash inflows and business activities (Demers et al., 2020).

Conclusion, Implications, Limitations and Future Research

The present study analysed the composite role of the ESG framework and the individual contribution of ESG initiatives in regulating EM practices in India. We used 82 non-financial firms (492 firm-year observations) listed in the Nifty ESG 100 Index during the period 2018–2019 to 2023–2024. Results reveal that the composite ESG framework is effective in regulating the TEM by reducing EM based on accruals (AEM) and real transactions (REM). As far as the three pillars of ESG are concerned, the governance (G) pillar seems to be more effective than the environmental (E) and social (S) pillars. The effectiveness of the implementation of the CGC in the Companies Act 2013 has significantly contributed to the regulation of EM in India (Goyal & Aggarwal, 2014; Maji & Lohia, 2023). Clause 49 in the listing agreement has also contributed to the mitigation of managerial discretionary practices in India. Recently, SEBI has mandated the top 100 companies to file BRSR to ensure the responsible and sustainable conduct of business activities. Now, the purview of the BRSR has been extended to the top 1,000 capitalized companies in India to ensure wider compliance with the ESG framework. The study also found that during the pandemic period (COVID-19), the magnitude of TEM was lower while the firms were using current accruals (AEM) as a tool to signal their performance to stakeholders to cover up the shrinkage in cash inflows and business activities during the period.

Findings of the study can aid policymakers and managers in enhancing the environmental and social initiatives of Indian corporates, because as per the MSCI report 2024, Indian firms have a better governance score among firms in other emerging economies, but lag in social and environmental engagements. As far as the ESG ratings in India are concerned, different agencies produce different scores for the same entity, which affects the reliability and comparability of ethical funds (sustainable investments) among investors. SEBI should consider developing an integrated ESG rating system to ensure the quality of sustainable investments to protect the interest of the investors in the long run. The study contributes to the existing literature by providing insights into the role of ESG initiatives in regulating EM in an emerging economy like India. Like any other emerging country in the Asian region, India is also characterized by concentrated ownership and weaker concerns on environmental and social aspects may lead to managerial discretionary practices (Afifa et al., 2021). As one of the largest emitters of CO2 in the world (Tran et al., 2024), the outcome of the study contributes to the relevance of involvement in environmental initiatives to ensure the long-term corporate sustainability in India.

The present study is limited to the large-cap non-financial companies listed in the Nifty ESG 100 Index. So, the studies in the future can explore corporate sustainability among the small-cap and mid-cap companies in India. Future research can address the sector-wise analysis of ESG engagement in the Indian capital market. Also, the individual role of E, S and G pillars in each sector in addressing managerial discretionary practices needs further investigation to analyse the effectiveness of implementing the BRSR framework in India. Comparative analysis of E, S and G pillars in regulating EM practices with other emerging economies can also provide more insights into the quality of sustainable finance in lower-middle income economies.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.