Abstract

This study examines human capital disclosure (HCD) practices among NIFTY 100 environmental, social, and governance (ESG) index companies in India, with a focus on sustainability reports. Using the GRI-G4 framework and prior academic models, a multidimensional HCD index was developed to measure disclosure across employment, health and safety, training, diversity, and human rights. Content analysis and panel regression reveal that while companies extensively report on health, safety, and training, disclosures regarding diversity, equity, and inclusion (DEI) and human rights remain limited and inconsistent. These findings underscore selective disclosure practices, with firms prioritizing reputationally safer domains while underreporting sensitive issues. The study contributes theoretically by extending stakeholder, signaling, and information disclosure perspectives to the Indian ESG context and methodologically by offering a replicable coding scheme that captures disclosure depth. Practical implications underscore the need for managers to enhance DEI reporting. At the same time, regulators, such as SEBI, must enforce standardized and transparent disclosures to align with global ESG standards and the Sustainable Development Goals.

Keywords

Introduction

In today’s knowledge-driven economy, human capital, encompassing the knowledge, skills, creativity, and well-being of employees, has emerged as a strategic driver of organizational success (Ganda, 2022; Ghlichlee & Goodarzi, 2022; Jaiswal & Medhavi, 2018; Jotabá et al., 2022). Recognizing employees as intangible assets, organizations increasingly adopt socially responsible human resource practices that promote equality, participation and engagement (De Araujo & Tejedo, 2016; Yaacoub & Frangieh, 2019). These efforts foster workplace harmony and motivation, enhancing long-term sustainability and financial performance (Pedrini, 2007). Despite this growing awareness, it is critical to ensure that organizations systematically disclose their human capital practices, particularly through sustainability reports. Human capital disclosure (HCD) is a key element of environmental, social, and governance (ESG) reporting, providing transparency on how companies treat their workforce across various areas, including employment, health and safety, diversity, and development (Jaiswal et al., 2024, 2025). While stakeholders, especially investors, are demanding greater visibility into how companies manage human capital (Jaiswal & Medhavi, 2018; Lev & Zambon, 2003), most prior research has focused on annual reports, which often lack the structure, depth, and comparability needed for meaningful HCD (Huang et al., 2013; Petty et al., 2008). A growing body of literature acknowledges the superiority of sustainability reports in presenting nuanced insights into human capital. Scholars have argued that sustainability disclosures are richer in detail and better suited for communicating employee-related aspects such as training, well-being, health, and diversity (Mahoney, 2013; Oliveira et al., 2010; Pedrini, 2007). However, empirical studies assessing HCD in sustainability reports, particularly in lower-middle income countries like India, remain limited (Aggarwal & Singh, 2019; Dissanayake et al., 2019; Kumar et al., 2023). Given India’s evolving ESG landscape, diverse socioeconomic fabric, and increasing regulatory momentum, there is a pressing need to examine how leading Indian companies disclose information on human capital.

This study focuses on companies listed in the NIFTY 100 ESG Index, a group recognized for integrating ESG factors into business strategy and disclosure. These companies serve as role models for ESG integration in India, offering valuable insights into the current state of sustainability reporting. The study explicitly investigates the human capital indicators that these firms reported from 2016 to 2021, using the Global Reporting Initiative (GRI-G4) framework. The rationale for this focus stems from the availability of structured, comparable, and comprehensive data in these reports, as well as the influential role of GRI standards in shaping global reporting practices (Brown et al., 2009; Etzion & Ferraro, 2010; Leeson & Kuszewski, 2023). This study builds upon several key strands. First, prior studies on employment disclosures have highlighted the importance of transparent reporting on recruitment, turnover, and workforce policies in contributing to employer branding and employee trust (Hegewisch & Gornick, 2011; Kumar, 2022). Second, disclosures related to health and safety have gained traction due to their implications for workplace well-being, stakeholder relations, and regulatory compliance (Coetzee & van Staden, 2011; Habisch et al., 2011). Third, training and education metrics signal the company’s commitment to employee development and innovation capacity (Grund & Titz, 2022). Fourth, diversity and inclusion are increasingly recognized as essential elements of ethical governance and sustainable performance, particularly in the post-pandemic world characterized by social movements and equity demands (Bananuka et al., 2022; Kalev et al., 2006; Klemesh et al., 2019). However, disclosure in this domain remains weak, often due to the absence of regulatory mandates, data limitations, or perceived reputational risk.

Despite the growing emphasis on ESG reporting in India, several gaps remain in the literature on HCD. First, disclosures on diversity, equity, and inclusion (DEI) remain limited in depth, highly inconsistent, and often non-comparable across firms. Recent reviews of business responsibility and sustainability reports (BRSRs) confirm that social performance transparency remains a weakness in Indian reporting, and SEBI’s ongoing review of ESG disclosure norms highlights this persistent shortcoming (Reuters, 2025; Upadhyay & Dugal, 2025). Second, although SEBI has mandated phased third-party assurance for BRSR Core indicators beginning with the top 500 firms in FY2025–2026, there is little empirical research on whether such assurance mechanisms enhance the credibility, completeness, or accuracy of HCD (SEBI, 2025). Third, disclosures on value-chain workforce metrics are underreported, as requirements for supply-chain reporting have been relaxed due to operational challenges. Nevertheless, there are no systematic studies assessing how human capital items are tracked or disclosed across value chains in the Indian context (SEBI, 2025; Upadhyay & Dugal, 2025). A fourth gap lies in methodology: while recent advances in natural language processing and machine learning have developed robust lexicons for analyzing HCD across categories such as DEI, health and safety, and labor relations (Demers et al., 2025), Indian studies have yet to adopt these tools, relying instead on more traditional content analysis. Fifth, issues of comparability persist across reporting frameworks, as although BRSR aligns with GRI and other international standards, structural differences in definitions, units of measurement, and levels of disaggregation reduce the scope for benchmarking (Garg et al., 2025). Sixth, most Indian studies provide only correlational evidence on HCD, with little causal analysis of whether stronger human capital reporting leads to better ESG or financial performance. In contrast, international evidence shows positive associations between HCD practices and sustainability outcomes (Cai et al., 2024; Ni, 2025), indicating the need for more rigorous causal designs in India. Governance also emerges as an underexplored dimension. While global studies suggest that board gender diversity influences the quality and extent of social and ESG disclosures (Alodat et al., 2023a; Bananuka et al., 2022), its impact on detailed HCD practices in India has not been systematically tested. In addition, concerns about data quality and granularity in BRSR “S” metrics persist, as there is limited validation of consistency, disaggregation, and time-series comparability across industries and reporting years (Garg et al., 2025). Furthermore, regulators have recently distinguished between “assessment” and “assurance” in ESG reporting, but no empirical research has examined how these different approaches affect investor confidence in HCD. Further, while human rights assessments are increasingly included in sustainability reports, studies rarely evaluate the substantive quality of these disclosures, raising questions about whether they are symbolic or genuinely reflective of corporate practices (Garg et al., 2025). Together, these gaps underscore the need for more in-depth, methodologically advanced, and context-specific studies of HCD in India, particularly those focusing on DEI and the role of governance in shaping disclosure practices.

This study aims to explore the underreporting of diversity and inclusion (D&I) in Indian companies, despite its relevance to investor decision-making, global benchmarking, and corporate legitimacy. As #MeToo and Black Lives Matter reshape global expectations, the Indian corporate sector must demonstrate its commitment to inclusive workplaces through clear and structured reporting. To this end, the study seeks to address three key research questions. First, it investigates the extent to which companies listed in the NIFTY 100 ESG Index disclose human capital information within their sustainability reports (RQ1). Second, it examines which human capital items are most frequently reported and which remain least emphasized, thereby highlighting disclosure imbalances across different dimensions (RQ2). Third, the study examines which specific sub-dimensions of human capital contribute most significantly to the overall HCD index, providing insights into the strategic priorities of firms in shaping their reporting practices (RQ3). Using a mixed-methods approach that combines content analysis and panel data regression, the study makes several contributions to the literature. First, it offers one of the few empirical analyses of HCD in Indian sustainability reports. Second, it introduces a structured HCD index based on the GRI framework to assess the comprehensiveness of disclosure. Third, it bridges theoretical perspectives from stakeholder, signaling, and information disclosure theories to explain firms’ motivations and strategies for workforce-related disclosures. Furthermore, this study advances the discourse on transparent and inclusive reporting in lower-middle income economies, informing policymakers, investors, and companies that strive to align with global sustainability goals, particularly SDG 5 (gender equality), SDG 8 (decent work), and SDG 10 (reduced inequalities).

Theoretical Background

Stakeholder Cardinality, Signaling Afflux and Quest for Information Disclosure

Understanding why firms disclose human capital information in sustainability reports requires a multi-theoretical lens. Hahn et al. (2015) emphasize that a combination of institutional, strategic, and ethical motivations shapes sustainability reporting. This study draws on three key theoretical perspectives—information disclosure theory (IDT), stakeholder theory, and signaling theory—to examine the breadth and depth of HCD practices among Indian firms. Each theory offers a distinct rationale for why companies disclose specific employee-related information, helping to explain the patterns observed in this study.

Information Disclosure Theory

IDT posits that organizations voluntarily share information to meet regulatory expectations, respond to stakeholder pressure and gain strategic advantages (Alodat et al., 2023c). In the context of HCD, IDT helps explain why some Indian firms are more forthcoming in reporting on areas such as training and development, or health and safety, while others remain reticent, particularly around D&I. For example, companies may highlight their investments in employee training to project an image of innovation-readiness and competitiveness. Disclosing health and safety initiatives in the post-COVID period aligns with regulatory expectations and reflects employee welfare concerns. However, the limited disclosure of diversity-related metrics, as observed in this study, may reflect either a lack of formal policies or a strategic choice to avoid scrutiny in sensitive areas. According to IDT, companies operating in environments where societal norms emphasize inclusivity and ethical treatment of workers are more likely to disclose such practices voluntarily (Chen & Roberts, 2010; Ehnert et al., 2016). The theory also highlights that perceptions of legitimacy often shape reporting firms’ disclosure of what they believe their stakeholders expect to see. Thus, HCD becomes a tool for compliance and strategic alignment with societal expectations (Soobaroyen & Ntim, 2013).

Stakeholder Theory

Stakeholder theory emphasizes that organizations are accountable to a broad spectrum of stakeholders, including shareholders, employees, investors, regulators, and society (Donaldson & Preston, 1995; Guthrie et al., 2004). This theory is particularly relevant for understanding why firms disclose certain types of human capital information over others. For instance, reporting on employment practices, occupational safety, or employee well-being addresses the concerns of internal stakeholders such as employees and labor unions. Meanwhile, external stakeholders, including socially responsible investors and civil society, expect diversity, inclusion, and transparency in human rights assessment. When companies fail to meet these expectations, it can lead to reputational damage or loss of stakeholder trust (Jan et al., 2022; Shah & Guild, 2022). Stakeholder theory also offers a framework for assessing the alignment between what is reported and what stakeholders prioritize. For example, this study finds that although employee training and health initiatives are often reported, diversity disclosures remain weak, indicating a possible mismatch between stakeholder expectations and firm behavior. Moreover, the theory underlines the importance of stakeholder engagement in shaping disclosures. Companies that actively involve stakeholders in sustainability planning are more likely to report comprehensively across all key HCD dimensions (Alodat et al., 2023a, 2023b).

Signaling Theory

Signaling theory (Healy & Palepu, 2001; Spence, 1973) offers a valuable lens for understanding how companies utilize HCD to mitigate information asymmetry and convey deliberate signals to the market. By disclosing data on their workforce policies, companies seek to signal their ethical orientation, internal strength, and long-term viability. It is particularly relevant for investors, who may interpret detailed human capital metrics as indicators of organizational health and risk mitigation. For instance, by reporting on employee safety, mental health initiatives, or professional development programs, firms signal a culture of care and resilience traits increasingly valued in ESG investing. Meanwhile, firms that disclose gender diversity statistics or anti-discrimination policies demonstrate a commitment to inclusion, aligning themselves with global standards and investor expectations. Crucially, signaling through HCD also enhances legitimacy and reputation, especially in competitive or highly regulated sectors. Transparency in sustainability reports can differentiate firms as socially responsible leaders, attracting talent, investment, and public goodwill (Curado et al., 2011). It explains why, in our findings, companies reporting extensively on employment, health and safety, and training often rank higher in ESG assessments. However, the theory also helps explain that strategic omission firms may avoid reporting in areas where performance is weak or data are lacking, such as diversity metrics. It underscores the importance of critically assessing the presence and absence of disclosures in signaling practices. In this study, human capital information is treated as a “signal” quantified in terms of both type and extent, and analyzed for its impact on perceptions of corporate responsibility and trustworthiness.

Hypothesis Development

Human Capital Disclosure

Human capital has long been recognized as a key intangible asset influencing organizational performance and competitive advantage (Salvi et al., 2022; Stewart, 1997; Sveiby, 1997). Effective human capital management requires systematic monitoring and transparent disclosure of various dimensions, including recruitment, retention, well-being, training, and equity (Cai et al., 2024; Flamholtz et al., 2002; Margherita, 2022; Roslender, 2011; Zafiryadis, 2025). HCD in sustainability reporting enables firms to demonstrate their alignment with social values and governance principles. From the IDT lens, firms voluntarily disclose such information to signal legitimacy and meet stakeholder expectations (Alodat et al., 2023c; Chen & Roberts, 2010). Stakeholder theory emphasizes transparency to internal and external groups concerned with fair treatment and equity (Guthrie et al., 2004), while signaling theory views disclosure as a strategic tool to manage corporate image, reduce information asymmetry, and attract responsible investment (Spence, 1973). Over the last decade, global attention toward social dimensions of ESG—particularly DEI—has increased. In this context, analyzing the evolution of HCD content over time and across specific dimensions is essential for assessing firms’ alignment with these expectations. Accordingly, this study proposes the following hypothesis:

H1: Between 2016 and 2021, the level of HCD in sustainability reports has become significantly more comprehensive and inclusive, with increased emphasis on employment equity, workforce well-being, and diversity-related initiatives.

Employment

Employment is a foundational component of human capital, serving as a proxy for an organization’s workforce policies, including recruitment practices, employment contracts, turnover management, and benefits. Transparent employment-related disclosures are essential for signaling responsible labor practices and equity in hiring (Kumar, 2022; Soobaroyen & Ntim, 2013). From a stakeholder theory perspective, firms are accountable to employees and regulators for equitable and fair labor practices. As signaling theory suggests, firms that disclose details on workforce size, contract types, and hiring policies indicate stability, ethical practices, and inclusivity. Employment disclosure indirectly signals diversity when firms break down data by gender, age, or minority representation.

H2: Human capital disclosure in sustainability reports is positively associated with the extent and transparency of employment-related information, particularly when firms emphasize fair hiring practices, retention, and workforce structure.

Health and Safety

Health and safety disclosures reflect an organization’s commitment to employee well-being, a key tenet of the “social” pillar of ESG. In post-pandemic contexts, firms utilize these disclosures to signal their resilience, employee care, and compliance with labor safety regulations (Coetzee & van Staden, 2011; Habisch et al., 2011). From an IDT lens, reporting workplace injuries, mental health initiatives, and safety training builds legitimacy and reduces reputational risks. Under the stakeholder theory, employees and unions expect firms to ensure a safe work environment. Furthermore, signaling theory highlights that firms emphasizing health and safety demonstrate long-term sustainability and organizational maturity.

H3: The extent of health and safety disclosures in sustainability reports is positively associated with the firm’s efforts to signal employee welfare, regulatory compliance, and social responsibility.

Training and Education

Training and education disclosures convey how firms invest in workforce development, skill-building, and leadership potential. These initiatives enhance productivity (Grund & Titz, 2022; Huselid, 1995) and promote inclusion by offering equitable access to growth opportunities. Stakeholder theory emphasizes that inclusive training policies align with employee expectations for career advancement. From a signaling perspective, firms use these disclosures to attract skilled talent and establish reputational advantages. Furthermore, under IDT, firms may disclose training programs to demonstrate proactive investment in human capital.

H4: Human capital disclosures emphasizing training and education are positively associated with a firm’s strategic positioning as an equitable and development-oriented employer.

Diversity and Equal Opportunity

Diversity and equal opportunity (DEO) are core indicators of ethical business conduct and ESG maturity. Public movements such as #MeToo and Black Lives Matter have amplified expectations around workplace equity and inclusion (Bananuka et al., 2022; Klemesh et al., 2019). Disclosures in this area cover gender equality, non-discrimination policies, equal pay, and representation of underrepresented groups. Under signaling theory, DEO reporting sends strong cues to investors and stakeholders about a firm’s ethical stance, cultural openness, and compliance with global standards. From a stakeholder theory perspective, such transparency reflects a commitment to fairness and inclusivity. However, despite these pressures, our content analysis shows limited DEO disclosures, highlighting an important gap.

H5: Firms with higher human capital disclosure scores are likelier to report on diversity and equal opportunity initiatives, signaling alignment with global inclusivity standards and stakeholder expectations.

Human Rights Assessment

Human rights in the workplace include fair treatment, freedom from discrimination, and protection from exploitation. Reporting on human rights assessments communicates a company’s ethical posture and accountability to global standards (Ferracioli & Parkhomenko, 2021; McPhail & Ferguson, 2016). From an IDT standpoint, disclosing human rights practices enhances institutional legitimacy. Stakeholder theory views such disclosures as essential to meeting the expectations of both civil society and investors. Signaling theory suggests that firms use human rights disclosures to enhance reputation, manage risk, and attract socially responsible investors.

H6: Human capital disclosure is positively associated with the extent of human rights assessments disclosed in sustainability reports, reflecting firms’ commitment to ethical conduct and social accountability.

Materials and Methods

Sample Selection and Dataset

To examine the trends and patterns of HCD in sustainability reporting within the Indian context, this study focuses on companies listed under the NIFTY 100 ESG Index, which was launched on March 27, 2018. This index integrates ESG factors into the traditional financial framework of the NIFTY 100 index. Specifically, it excludes companies engaged in tobacco, alcohol, gambling, and controversial weapons, aligning more closely with the values and ethical preferences of socially responsible investors. At the time of the study, the NIFTY 100 ESG Index comprised 88 actively listed companies.

The sampling process for this study followed a multi-stage procedure to ensure rigor and representativeness. The study began with an initial screening of all 88 companies in the NIFTY 100 ESG Index by reviewing their official websites to identify the availability of sustainability reports for the period 2016–2021. This step revealed that 47 companies had publicly available sustainability reports conforming to the global reporting initiative (GRI) G4 framework, which is widely adopted for ESG reporting. For the remaining 41 companies without accessible sustainability reports online, the authors contacted investor relations and ESG departments directly via official e-mails, requesting access to historical reports. From these requests, 10 companies responded positively; however, only four were able to provide complete sustainability reports covering the whole 6-year analysis period, while six were excluded due to incomplete or inconsistent data. As a result, the final pool of eligible firms consisted of 51 companies (47 with accessible reports plus 4 obtained through direct requests) that consistently published GRI-G4-aligned sustainability reports during the study period. To further strengthen the analysis, the study then focused on the top 10 constituents of the NIFTY 100 ESG Index, which together account for over 55% of the index’s total weightage. Among these, seven companies—Infosys, Reliance Industries, HDFC Bank, Tata Consultancy Services (TCS), Hindustan Unilever, Axis Bank, and Larsen & Toubro Ltd.—had complete sustainability reports across 2016–2021 and were therefore retained for panel data regression. The other three firms, namely ICICI Bank, HDFC Ltd., and Kotak Mahindra Bank, were excluded at this stage due to the absence of GRI-G4-based reports. This resulted in a balanced panel comprising 42 firm-year observations (7 companies × 6 years), which was used for hypothesis testing and subsequent content analysis. This sampling approach ensured that the selected companies were not only aligned with ESG priorities but also represented industry leaders with the potential to influence reporting practices across the Indian corporate landscape. The emphasis on high-weightage firms further enhanced the study’s relevance and generalizability for policymakers, investors, and ESG-focused stakeholders.

Content Analysis of HCD

To assess the trend and depth of HCD in the sustainability reports of NIFTY 100 ESG companies, we employed a structured content analysis approach, which systematically identifies the presence, frequency, and contextual relevance of predefined themes and indicators (Guthrie et al., 2004). Content analysis is particularly suited for examining qualitative disclosures in corporate reports and has been widely applied in intellectual and human capital studies (Beattie & Thomson, 2007; Silva et al., 2014).

The data collection spans 6 years, from 2016 to 2021, for two key reasons. First, the introduction of the NIFTY 100 ESG Index in 2018 served as a significant policy and market signal for ESG alignment among Indian companies. This development enabled a meaningful comparison of HCD practices before and after the index launch, thereby providing a quasi-experimental design for longitudinal analysis. Second, this timeframe coincides with a growing emphasis on ESG disclosures in India, driven by evolving corporate governance norms and the broader adoption of GRI reporting frameworks. Together, these factors make the selected period strategically and contextually relevant for assessing shifts in non-financial reporting behavior.

Content Analysis Framework

This study employed Weber’s (1990) seven-step content analysis procedure, which involves defining categories, establishing coding rules, selecting a sample, training coders, coding data, assessing reliability, and interpreting results. The analytical process was informed by prior HCD studies (Abeysekera, 2008; Abeysekera & Guthrie, 2005; Ax & Marton, 2008; Huang et al., 2013).

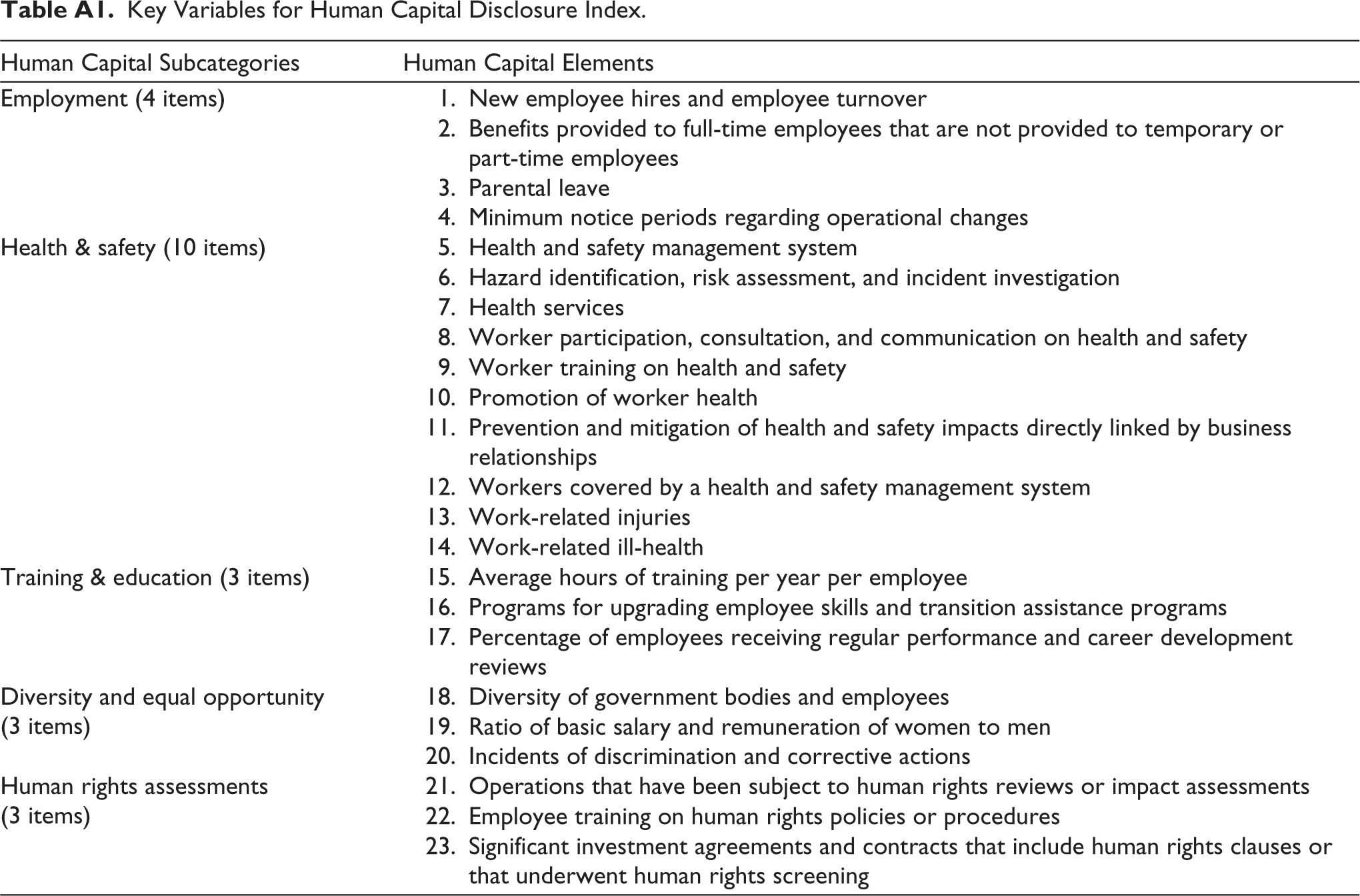

The development of the coding scheme and HCD indicators was grounded in established reporting standards and prior research. Specifically, the initial coding framework drew upon the GRI-G4 guidelines, with a focus on indicators outlined under GRI 401–GRI 412. These included employment-related metrics such as new hires and turnover (GRI 401), occupational health and safety practices (GRI 403), training and education initiatives (GRI 404), DEO disclosures (GRI 405), and human rights assessments (GRI 412). In addition to the GRI framework, the coding scheme was further informed by prior academic models of HCD, particularly the work of Abeysekera (2008) and Vithana et al. (2021), which provided conceptual clarity and methodological guidance for capturing and categorizing disclosure practices. A pilot analysis of 12 sustainability reports (from 2016 and 2017) was conducted to refine and validate the indicator set. Based on its findings, the original list of 32 items was condensed to 23 final HCD indicators, listed in Table A1. These indicators served as the primary coding categories.

Coding and Scoring Process

The coding process was carried out in two systematic steps. In the first step, disclosure identification, each sustainability report was reviewed to confirm the presence or absence of the 23 predefined indicators. In the second step, disclosure depth was measured using a quantitative word count method for each indicator, which was then converted into a 5-point Likert scale. Specifically, a score of 0 was assigned for no disclosure, 1 for a minimal mention of up to 25 words, 2 for a basic description ranging from 26 to 50 words, 3 for moderate elaboration between 51 and 100 words, 4 for a detailed explanation of 101–200 words, and 5 for comprehensive reporting exceeding 200 words. In addition to this quantitative assessment, a qualitative classification of disclosure content was undertaken across five thematic dimensions—objectives, measurements, targets, initiatives, and accomplishments—adapted from Vithana et al. (2021). This combined approach ensured a more holistic evaluation of the completeness and credibility of the disclosures.

Intercoder Reliability and Validity Checks

Two trained researchers independently coded the full sample of sustainability reports to ensure objectivity and consistency. The process was conducted blind to the study’s hypotheses. Discrepancies in coding were discussed and resolved through consensus. Krippendorff’s α was calculated to test intercoder reliability. A score of 0.923 was achieved, indicating excellent reliability (Hayes & Krippendorff, 2007). Additionally, consistent coding rules, with no weightage given to formatting (e.g., sentence length or font), and structured scoring enhanced validity.

Research Model and Measures

The first two research objectives are investigated using trend analysis. In contrast, the final objective involves evaluating the importance of the HCD index and human capital item using panel data regression analysis. The disclosure index (human capital index) and five disclosure sub-indices were developed to focus on a comparative study on reporting of various human capital metrics across different sectors based on employment, health and safety, training and education, diversity, equal opportunity, human rights, etc., representing a different aspect of voluntary human capital reporting. Therefore, this study considers these key measures as variables/constructs for HCDs reported in sustainability reports. Furthermore, regression models for panel data were developed using the human capital index as the dependent variable and the other five as independent variables.

Research Model

This study employs a panel data regression model to empirically test the research hypotheses and analyze the variation in HCD across firms and over time. The panel comprises data from seven top-weighted companies in the NIFTY 100 ESG Index over a 6-year period (2016–2021), resulting in a balanced panel of 42 firm-year observations. The panel data regression is selected because it captures both cross-sectional and time-series variations. Panel data enable the study to analyze differences in HCD practices between firms and how these practices evolve, both before and after the introduction of the NIFTY 100 ESG Index 2018. It also controls for unobserved heterogeneity. By accounting for firm-specific effects (e.g., industry characteristics, firm culture), panel regression minimizes omitted variable bias and improves the precision of estimated relationships. Furthermore, compared to pure cross-sectional or time-series analysis, panel data increases the number of observations, thereby enhancing the statistical power and robustness of the results. This approach aligns well with the study’s objective of identifying the effect of specific human capital dimensions (employment, health and safety, training, diversity, human rights) on the overall extent of HCD and changes across time.

Variables and Measurement

The study employed a structured set of variables and measurements to analyze HCD. The dependent variable, the HCD_Index, represents a composite disclosure score for each firm-year, calculated as the sum of scores (ranging from 0 to 5) across 23 disclosure items. This index was derived through content analysis of sustainability reports, using word count thresholds and qualitative depth criteria as outlined earlier. The independent variables included five key dimensions of HCD: employment disclosure, health and safety disclosure, training and education disclosure, diversity disclosure, and human rights disclosure. Each of these variables was coded on a 5-point scale, from 0 to 5, consistent with the method applied to the dependent variable. In addition, a time dummy variable, Post_ESG_Index, was incorporated to distinguish whether the reporting year occurred before (0) or after (1) the launch of the NIFTY 100 ESG Index in March 2018. This enabled the study to isolate the potential influence of index inclusion on firms’ HCD practices. Where applicable in extended models, control variables such as firm size, industry type, and ESG score were also considered to account for contextual differences across companies. The panel data model is specified as follows:

Where,

HCDI = Human capital disclosure index

EMPit = Employment

HSit = Health and safety

TEit = Training and education

DEOit = Diversity and equal opportunity

HRAit = Human rights assessments

µit = Residual value; β0 = Constant; β1, β2, β3, β4, and β5 = Regression coefficients

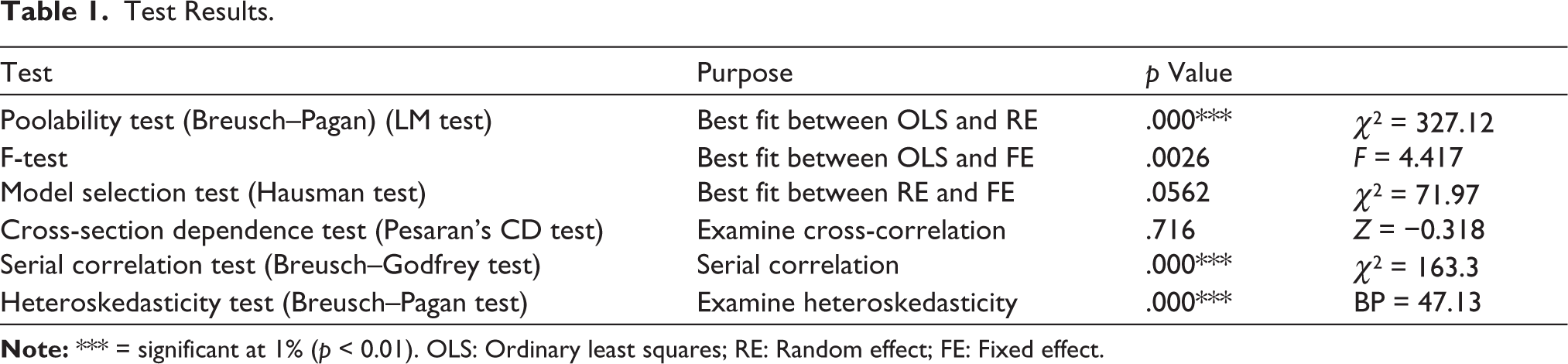

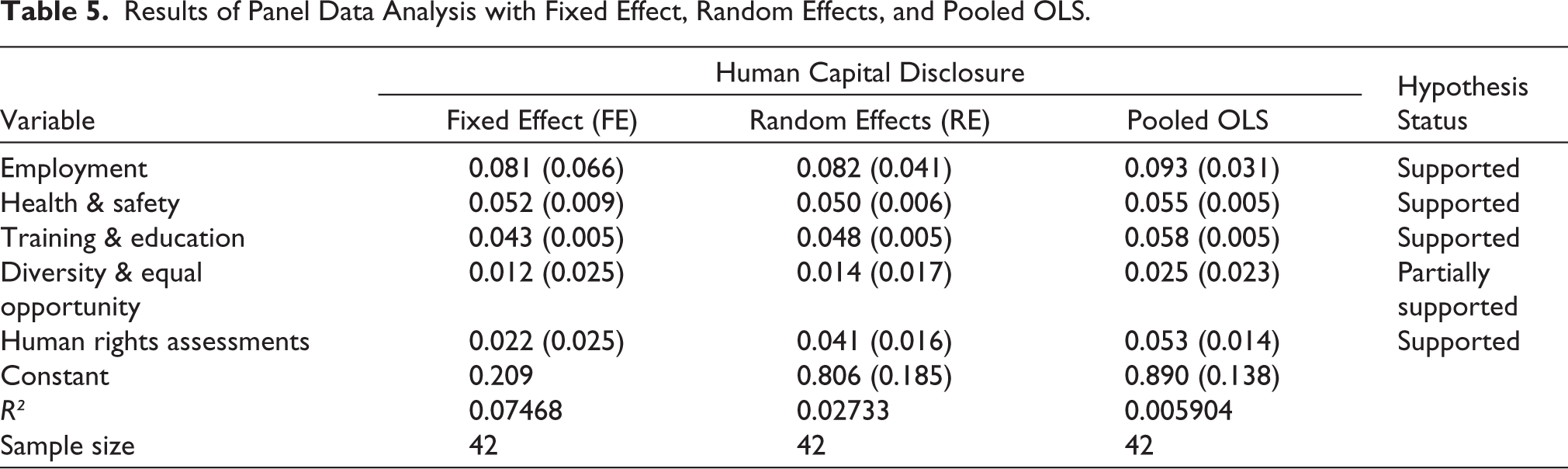

This model allows the study to estimate how changes in disclosure across individual HCD dimensions influence the overall comprehensiveness of human capital reporting. Data are highly heterogeneous after the Breusch–Pagan (LM) test, as the resulting p value is .000. Hence, the OLS test is no longer administered. The best fit between OLS and FE is then determined using the F-test. FE supports the outcome. Therefore, OLS will no longer be included in this test. Furthermore, the Hausman test was used to decide between FE and RE, with the proviso that RE would be taken into consideration only if the p value was more significant than >.05. Since the p value in this study is more significant than .05, the RE model is chosen for the analysis. Table 1 displays the outcome.

Test Results.

Results and Discussion

Results

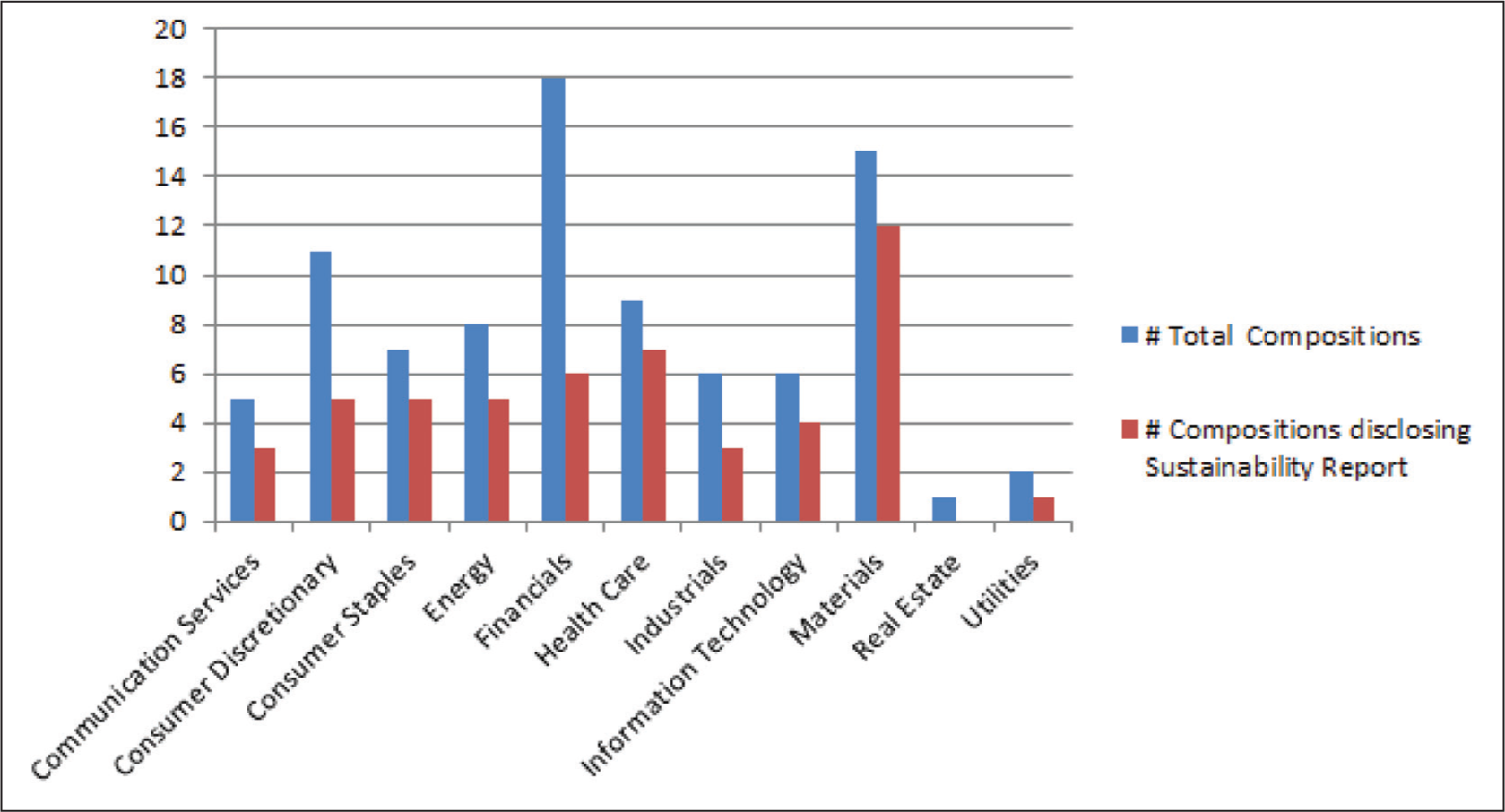

The findings of the content analysis show that human capital information is disclosed in sustainability reports. The author found that 51 companies from the Nifty100 ESG index have sustainability reports, with 80% of companies from the materials sector producing sustainability reports voluntarily. Sixty percent of companies in 6 out of 11 sectors are producing their sustainability reports (see Figure 1). However, the other 37 companies might be sharing business responsibility report, BRSR, integrated report, or putting some part of the ESG information in their annual report as per guidelines provided by the Securities and Exchange Board of India (SEBI).

Summary of NIFTY 100 ESG Constituents Voluntarily Producing Separate Sustainability Reports According to Sector.

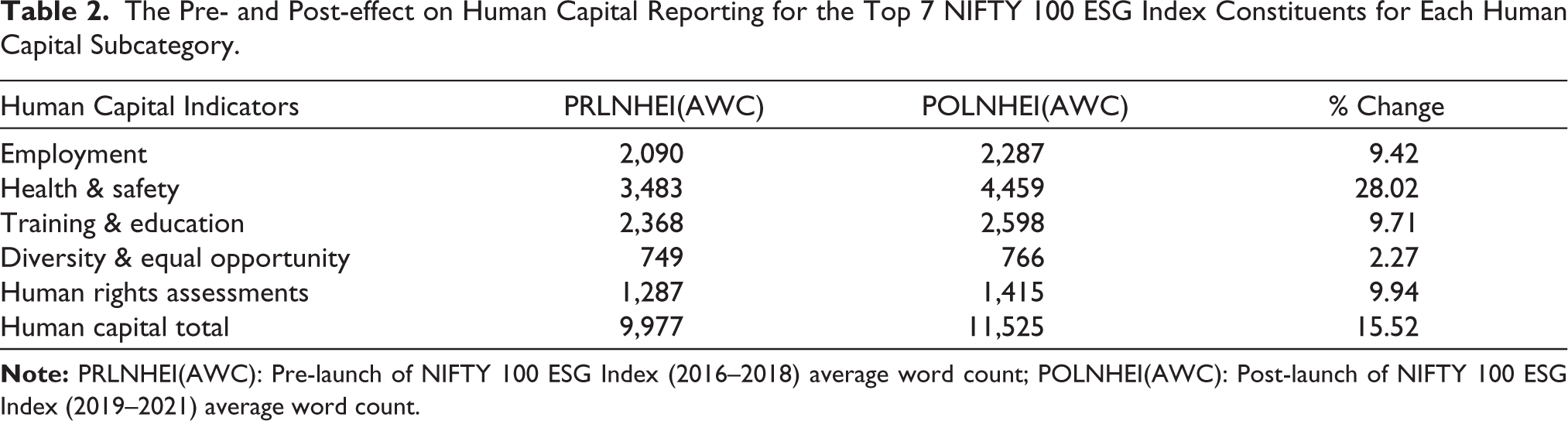

In Table 2, the author found that there has been a 15.52% change in human capital reporting for the top 7 compositions of the Nifty 100 ESG Index. Interestingly, health and safety (+28.02%) of the workforce has been a focus area where they have increased reporting, followed by human rights assessments (+9.94%), training and education (+9.71%), and employment(+9.42%), with a minuscule increase in DEO (+2.27%). Moreover, the trend indicates that sustainability reports are allocating more space to human capital items during this period. Therefore, H1 is supported. The most frequently reported item is “health and safety,” followed by “training and education,” and the least is “diversity and equal opportunity.” Content analysis of sustainability reports also indicates that corporations use sustainability reports to communicate human capital information effectively. Several factors, such as legitimacy (Coetzee & van Staden, 2011), stakeholder relations (Habisch et al., 2011), compliance, and institutional pressure, may account for the increase in reporting by NIFTY100 constituent companies after the launch of the ESG index. On the other hand, it may be due to COVID-19, a virus that has disrupted human life globally, and the widespread belief that healthy employees are happier and more productive.

The Pre- and Post-effect on Human Capital Reporting for the Top 7 NIFTY 100 ESG Index Constituents for Each Human Capital Subcategory.

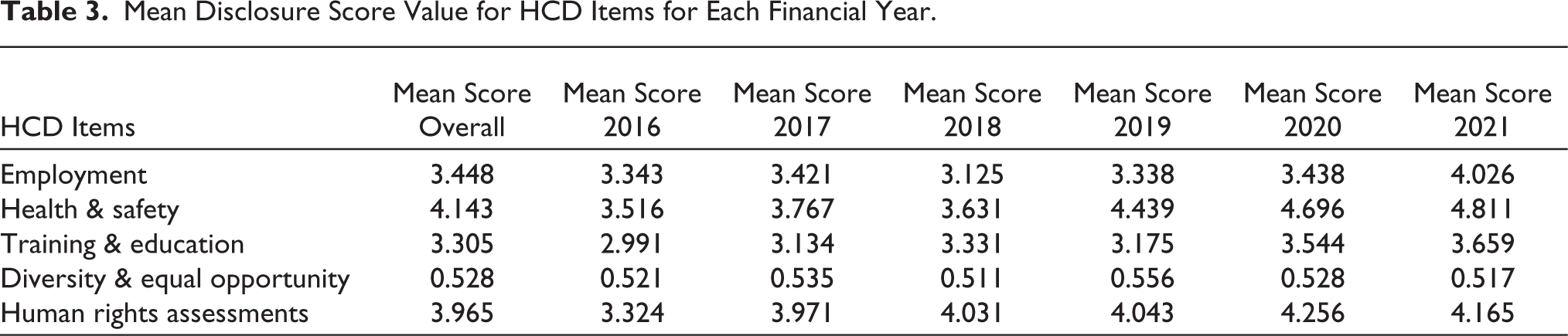

The mean disclosure score for human capital information for each financial year, along with the mean overall score, is represented in Table 3. The mean HCD scores have increased over the period. To address the second objective, this study found that the most frequently disclosed items related to sustainable healthcare disclosure are health and safety, with an overall mean score of 4.143. In contrast, the least disclosed items are diversity and equal opportunities, with an overall mean score of 0.528.

Mean Disclosure Score Value for HCD Items for Each Financial Year.

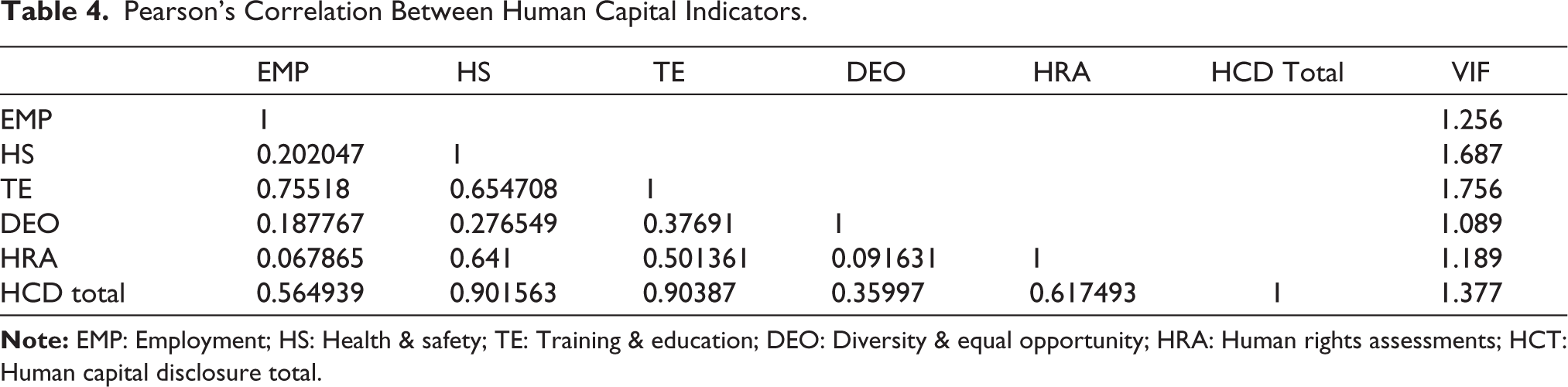

This study found a positive relationship between the human capital sub-indicators and overall human capital total based on Pearson correlation coefficients (see Table 4). In addition, multicollinearity was assessed using VIF analysis. Multicollinearity problems arise in regression analysis when the VIF exceeds 10 (Chatterjee et al., 2000; Gujarati, 2003). Table 4 shows that none of the reported VIF values for any variables exceed the threshold value of 10, eliminating the possibility of multicollinearity in the estimated model. Further, this study employed the Durbin–Wu–Hausman test to investigate potential endogeneity issues in the model (Ullah et al., 2018). Endogeneity did not influence the research outcomes, as indicated by a non-significant test and static, non-significant coefficients.

Pearson’s Correlation Between Human Capital Indicators.

Based on the Hausman test (Table 1), the author found that the random effect model is best suited for predicting the top human capital indicators, which have more weightage in overall human capital indicator disclosure reported in the sustainability report (Table 5). When relying on the random effects model reported in Table 5, a strong positive association is observed between the extent of “employment” and the level of the HRD index, as indicated by the reported coefficient. Therefore, H2 is supported. This implies that companies are stressing employee retention and the associated policies (Hegewisch & Gornick, 2011; Kumar, 2022). H3 predicted that human capital reporting in corporate sustainability reports correlates positively and significantly with health and safety. It suggests that a company culture that values its employees’ health has led to higher rates of job satisfaction, lower rates of absenteeism, and a more balanced and fairer workplace that is also in line with prior studies (Coetzee & van Staden, 2011; Habisch et al., 2011). H4, the empirical finding, suggested that human capital reporting in corporate sustainability reports correlates positively and significantly with training and education. It means that when a company discloses its HC, it describes its workforce’s training, expertise, drive and innovation levels, influencing the investor minds for the company’s prospects (Grund & Titz, 2022).

Results of Panel Data Analysis with Fixed Effect, Random Effects, and Pooled OLS.

In contrast, DEO has the slightest extent in the overall HRD index, which is concerning, as modern society is a product of globalization and technological advancement and is intricate and interdependent. Henceforth, H5 is partially supported. Unsurprisingly, our personal lives’ social and cultural dynamics also manifest in our professional environments. It benefits everyone involved when a workplace is diverse, as it is more likely to inspire originality, creativity, and empathy than a more homogenous setting. Nevertheless, careful cultivation and deliberate orchestration are essential to tap into this invaluable resource fully. H6 predicts that human capital reporting in corporate sustainability reports correlates positively and significantly with human rights assessment. The reported coefficient supports acceptance of H6. Evidence shows that investors pay attention to how companies focus on human rights assessment in practice and their reporting (Ferracioli & Parkhomenko, 2021; McPhail & Ferguson, 2016).

Theoretical Implications

This study advances theory in several ways. It addresses the gap in DEI disclosure by empirically confirming that such reporting remains superficial, thereby extending stakeholder theory by demonstrating how selective disclosure reflects asymmetrical stakeholder engagement. Second, it contributes to IDT by demonstrating that firms disclose more extensively in “safe” domains, such as health and safety, while underreporting sensitive areas such as diversity and human rights, reflecting strategic choices shaped by legitimacy concerns. Third, by integrating signaling theory, the study highlights that Indian firms use HCD as a reputational tool, with disclosure depth varying by category, thus extending the application of signaling mechanisms to emerging markets. The customized HCD index, which incorporates both word count thresholds and qualitative dimensions, contributes methodologically by moving beyond binary presence/absence measures and offering a replicable, multidimensional approach to capturing the substance of disclosure. It reinforces that HCD functions as a strategic signaling mechanism, conveying essential information to investors, employees, and other stakeholders about a firm’s values, governance practices, and workforce priorities. The findings indicate that while the frequency and volume of disclosure, particularly on themes such as health and safety, training, and development, have increased over time, the comprehensiveness and consistency of these disclosures remain uneven across firms and categories. This nuance advances existing literature that often treats disclosure as a binary presence/absence measure, and instead emphasizes the importance of depth, substance, and standardization in non-financial reporting. By analyzing human capital separately from other forms of intellectual capital (as suggested by Abeysekera, 2008), the study provides a domain-specific understanding of HCD, grounded in a multi-theoretical framework that integrates IDT, stakeholder theory, and signaling theory. It builds upon and extends prior work by proposing that external stakeholder salience and internal strategic intent shape the quality of HCD. The study empirically validates that increased HCD, particularly in areas that align with compliance and stakeholder pressure (e.g., health and safety), reflects organizations’ attempts to maintain legitimacy and trust. However, the persistent underreporting in sensitive areas such as diversity, inclusion, and human rights points to the limitations of instrumental stakeholder engagement and reveals that signaling often remains selective and reputational rather than value-driven. Methodologically, the study departs from traditional dichotomous scoring approaches by developing a customized disclosure index that captures the breadth and depth of HCD practices. This contribution extends the broader literature by providing a more nuanced and replicable method for evaluating narrative disclosures in sustainability reports. The index also evaluates whether firms provide meaningful insights across five dimensions: objectives, measurements, targets, initiatives, and accomplishments (following Vithana et al., 2021).

The study also illuminates the disconnect between corporate signaling and actual stakeholder alignment. While firms increasingly adopt advanced HCD frameworks, the results suggest that this evolution is asymmetric, influenced more by risk mitigation and competitive positioning than by inclusive engagement or ethical imperatives. This supports the view that disclosure practices in India remain largely reactive, particularly in domains such as gender equity, workplace inclusion, and the ethical treatment of labor. Comparisons with global financial institutions such as Morgan Stanley, J.P. Morgan, and MSCI further illustrate the evolving role of human capital, especially diversity, as central to long-term competitiveness, innovation, and legitimacy. These examples highlight the maturity of institutionalized D&I practices in advanced markets and underscore the potential for cross-contextual theory development, particularly in adapting stakeholder and legitimacy theory to culturally and institutionally diverse settings. The study affirms that HCD is no longer a purely internal HR function, but a key dimension of organizational identity, accountability, and ESG performance. It provides a conceptual and empirical framework for evaluating the alignment between employee-related disclosures and stakeholder expectations. This strengthens the application of signaling theory, offering insights into how sustainability reports signal a company’s ethical posture, responsiveness, and long-term commitment to employee welfare and development.

Managerial Implications

The findings of this study offer several valuable managerial implications for corporate leaders, ESG strategists, and HR practitioners. Managers can use the insights to strategically align their sustainability initiatives with employee-centered priorities, ensuring that disclosures reflect substantive organizational practices rather than superficial compliance. The analysis reveals that while companies tend to report extensively on health and safety, as well as training and development, critical areas such as diversity, inclusion, and human rights are still underreported. This underscores the need for managers to take a more balanced approach by strengthening internal policies and external reporting mechanisms related to DEI and ethical labor practices. Additionally, the study encourages managers to implement robust systems to monitor the effectiveness of employee-related initiatives. By identifying underperforming dimensions through disclosure trends, managers can better allocate resources and design targeted interventions that address internal workforce development and stakeholder expectations. Furthermore, improved human capital reporting can enhance stakeholder trust, attract socially conscious investors, and bolster employer branding, particularly in a competitive talent landscape. Sharing credible information about workforce engagement, equal opportunities, and career advancement demonstrates a company’s long-term commitment to employee well-being and institutional accountability. The study also highlights the need for technological and structural improvements in disclosure systems. Managers are encouraged to adopt integrated reporting tools and cost-effective digital solutions that capture, structure, and communicate comprehensive human capital data, encompassing aspects such as board diversity, inclusive hiring practices, employee satisfaction, and retention rates. Benchmarking these practices against those of top ESG performers can help organizations adopt industry best practices and maintain their reputational credibility. These implications empower managers to lead with transparency, responsiveness, and innovation, fostering an inclusive and sustainable organizational culture.

Policy and Regulatory Implications

From a policy perspective, this study underscores the urgent need for standardized and enforceable guidelines regarding human capital disclosures, particularly in the areas of diversity, inclusion, and human rights. While voluntary disclosures have improved, the lack of uniformity and comprehensiveness in reporting undermines the comparability and credibility of sustainability communication across Indian firms. Regulatory bodies such as SEBI and developers of the BRSR framework are encouraged to mandate minimum disclosure requirements for DEI indicators, disaggregated employment data, and board-level diversity metrics. Furthermore, the study advocates for the integration of ESG policies into investment frameworks. With the rise of ESG-based investing, accurate and transparent HCD will be crucial in guiding investment decisions and minimizing risks associated with poor labor practices or social exclusion. The insights also support the potential development of a D&I sub-index within NIFTY ESG, encouraging companies to enhance performance on social dimensions. Institutional frameworks that reward companies for strong social disclosures, offer capacity-building support, and enable third-party assurance mechanisms can accelerate the maturation of sustainability reporting in India. Policy interventions in these areas will promote accountability, protect worker rights, and support the broader ESG reform agenda in emerging economies.

Contribution Towards SDG Goals

This study directly supports the advancement of multiple United Nations Sustainable Development Goals (SDGs) by assessing employee-related disclosures in sustainability reporting. By evaluating corporate reporting on workforce well-being, diversity, and human rights, the study contributes to SDG 8 (decent work and economic growth) by highlighting how companies promote productive employment, fair labor practices, and safe workplaces. The emphasis on training and education initiatives links the findings to SDG 4 (quality education), as organizations increasingly invest in skill development and lifelong learning programs. Furthermore, the study addresses SDG 3 (good health and well-being) by analyzing occupational health and safety disclosures. It supports SDG 5 (gender equality) and SDG 10 (reduced inequalities) by revealing the gaps and opportunities in reporting on D&I. It encourages organizations to promote equal opportunity across gender, socioeconomic background, and other identity categories. Lastly, the call for stronger human rights disclosures aligns with SDG 16 (peace, justice, and strong institutions), advocating for ethical governance, transparency, and organizational accountability. By encouraging responsible disclosure practices, the study enables businesses to contribute more effectively to global sustainability and equity objectives.

Limitations

Due to the availability of GRI-G4-based sustainability reports, the panel was limited to seven firms. Although these represent the top-weighted NIFTY ESG constituents, the findings may not generalize to mid-cap or unlisted firms. Future research could explore disclosures aligned with the updated GRI Standards (2021), integrated reporting, or the SASB frameworks for a broader comparison. Although high intercoder reliability was achieved (Krippendorff’s α = 0.923), content analysis inherently involves interpretation. Triangulating this with interviews or surveys with corporate reporters could enrich the findings. This study is observational. Future work may use quasi-experimental designs or event studies to assess the causal impact of ESG regulations or social movements (e.g., #MeToo, Black Lives Matter) on HCD practices.

Future Research Avenues

Future research avenues for exploring how well sustainability reports demonstrate the priorities of Indian businesses when it comes to their employees are shown in Table 6.

Future Research Avenues.

This knowledge can inform businesses, policymakers, and other stakeholders in promoting employee-centric practices and driving meaningful change in the Indian corporate landscape.

Conclusion

This study provides one of the first systematic examinations of HCD practices among NIFTY 100 ESG Index companies in India, using sustainability reports as the primary data source. By developing a comprehensive HCD index based on GRI-G4 guidelines and prior academic frameworks, the research captures both the breadth and depth of disclosure across employment, health and safety, training, diversity, and human rights. Findings reveal that 58% of companies produced standalone sustainability reports, with health and safety (a 28% increase following the launch of the ESG index) and training and education (a 9.7% increase) receiving the most disclosure. In contrast, DEO disclosures remain minimal, increasing by only 2.3%. This imbalance highlights how companies prioritize “safe” domains while underreporting sensitive areas, reflecting both reputational concerns and regulatory gaps. This study contributes theoretically by extending stakeholder, signaling, and information disclosure perspectives to the Indian ESG context and methodologically by offering a multidimensional index that moves beyond binary disclosure measures. Empirically, it provides robust longitudinal evidence through a balanced panel dataset of high-weighted firms, underscoring which HCD dimensions most influence overall disclosure. From a practical standpoint, the research urges managers to enhance their DEI and human rights reporting to meet the expectations of global investors. At the same time, policymakers, particularly SEBI, should enforce more standardized and assured disclosures. At a societal level, greater transparency in human capital practices is critical to advancing the SDGs related to decent work, equality, and inclusive growth. This study underscores the need for Indian corporates to transition from symbolic to substantive human capital reporting, thereby aligning business strategies with both stakeholder trust and sustainable development imperatives.

Footnotes

Authors’ Contribution

Rachana Jaiswal: Conceptualization, supervision, methodology, software, writing—Reviewing and editing, formal analysis, writing—Original draft preparation.

Shashank Gupta: Data curation, writing—Original draft preparation, methodology, visualization, investigation.

Data Availability Statement

The datasets analyzed during the current study are available upon reasonable request from the corresponding author.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Appendix

Key Variables for Human Capital Disclosure Index.

| Human Capital Subcategories | Human Capital Elements |

| Employment (4 items) | 1. New employee hires and employee turnover |

| 2. Benefits provided to full-time employees that are not provided to temporary or part-time employees | |

| 3. Parental leave 4. Minimum notice periods regarding operational changes |

|

| Health & safety (10 items) | 5. Health and safety management system |

| 6. Hazard identification, risk assessment, and incident investigation | |

| 7. Health services | |

| 8. Worker participation, consultation, and communication on health and safety | |

| 9. Worker training on health and safety | |

| 10. Promotion of worker health | |

| 11. Prevention and mitigation of health and safety impacts directly linked by business relationships | |

| 12. Workers covered by a health and safety management system | |

| 13. Work-related injuries | |

| 14. Work-related ill-health | |

| Training & education (3 items) | 15. Average hours of training per year per employee |

| 16. Programs for upgrading employee skills and transition assistance programs | |

| 17. Percentage of employees receiving regular performance and career development reviews | |

| Diversity and equal opportunity (3 items) | 18. Diversity of government bodies and employees |

| 19. Ratio of basic salary and remuneration of women to men 20. Incidents of discrimination and corrective actions |

|

| Human rights assessments (3 items) | 21. Operations that have been subject to human rights reviews or impact assessments |

| 22. Employee training on human rights policies or procedures | |

| 23. Significant investment agreements and contracts that include human rights clauses or that underwent human rights screening |