Abstract

This research looks into the factors affecting Central Bank Digital Currency (CBDC) adoption intentions among households in India. Extending the Unified Theory of Acceptance and Use of Technology (UTAUT) model, this study integrates perceived trust and perceived security as mediators and attitude as a moderator. After collecting data from 386 respondents, the proposed model is validated through Partial Least Squares Structural Equation Modeling (PLS-SEM) and Importance-performance Map Analysis (IPMA). The results indicate that the intention to use CBDC is most affected by performance expectancy and facilitating conditions. Moreover, perceived trust substantially affects the association between perceived security and behavioral intention. Also, it is found that attitude significantly moderates the path from performance expectancy to behavioral intentions, whereas it exerts an insignificant moderating effect on the relationships involving effort expectancy, social influence, perceived security, and behavioral intentions. Finally, this study contributes uniquely to the existing body of literature on CBDC by focusing on households’ perspective, providing an insightful information on customer-specific adoption factors and other such information for policymakers and practitioners.

Introduction

Money has a fascinating history that spans several millennia. From the earliest days of bartering to the introduction of metal coins and eventually paper currency, money has always had a significant impact on the way our society functions (Banerjee & Sinha, 2023). Over time, the evolution of money has closely mirrored broader changes in financial systems and monetary history. In the modern era, this evolution has taken a significant turn, with many economies worldwide shifting from physical currency to digital forms of money (Bai et al., 2025; Ozili, 2023a). Especially in India, the monetary system has undergone profound alterations after demonetization. People have transitioned to digital platforms for conducting financial transactions (Sandhu et al., 2023). One of the major and popular digital platforms that is used by people is the Unified Payments Interface (UPIs). The Reserve Bank of India’s “Payment System Report” indicated that by the end of 2024, UPI accounted for 83% of total digital payment transactions in India, a significant rise from 34% in 2019 (Economic Times, 2025). By merging various banking functions, smooth money transfers, and merchant payments, UPI combines several bank accounts into one mobile application (of any participating bank) (Gohil et al., 2023). And the advent of advanced technological innovations has marked the next phase in the evolution of money: its complete digitalization. CBDC is a relatively new form of currency made feasible by technological advancements (Ogunmola & Das, 2024). CBDC is considered legal money by the RBI, which is a central bank’s liability in digital form that is denominated in sovereign currency and shows up on the central bank balance sheet (Ogunmola & Das, 2024; Priyadarshini & Kar, 2021). Actually, the country’s central bank issues CBDC, a digital version of fiat money that is regarded as legal tender (Griffoli et al., 2018; Ozili, 2023b; Söilen & Benhayoun, 2022).

UPI and CBDC are two distinct concepts in terms of financial system digitalization. Even though they both use digital payments, they have different goals and function at different financial system levels. UPI is a payment system created by the National Payments Corporation of India (NPCI) that allows users to transfer money, pay bills, and make payments without using actual currency by allowing immediate transfers of monies between bank accounts using mobile devices. In contrast, CBDC is expected to work similarly like fiat money in order to be accepted as payment for goods and services (Kim et al., 2024). While UPI is a money-using interface, CBDC is a type of currency (Gupta et al., 2023).

In India, the goal of implementing CBDC in conjunction with the UPI payment system is to improve monetary policy, lower transaction costs, increase financial inclusion, and establish a safe payment system (Gupta et al., 2023). It is speculated that monetary policy instruments, such as interest rate setting and liquidity management within the financial system, can be implemented and adjusted effectively by central banks through the use of CBDC (Priyadarshini & Kar, 2021). Moreover, CBDC is also expected to enhance the efficiency of cross-border transactions (Eichengreen et al., 2022). On the retail front, digital currency has the potential to streamline payment processing across various channels, including point-of-sale (POS) systems, online transactions, and peer-to-peer (P2P) payments. Wholesale and interbank payments may also benefit from the implementation of CBDC, as it can facilitate greater flexibility and accelerate settlement processes.

While there are numerous studies on CBDC design and legal aspects of it, the existing literature underpins a dearth of research on the household acceptance. There is a conspicuous lack of efforts in soliciting public opinion on CBDC adoption (Griffoli et al., 2018; Kala & Chaubey, 2023; Wang et al., 2023), even though the primary focus in the development of CBDCs should be on identifying and addressing the real-world challenges faced by everyday people. The prior study largely focused on the design and technological aspects of CBDCs, with insufficient consideration given to the demands and preferences of end users, including individuals and enterprises (Auer & Böhme, 2020). This oversight not only highlights a big gap in the CBDC research but also points out that the approach to developing these digital currencies might be backward. Thus, this work seeks to examine the following research objective:

To develop and empirically test a predictive model based on the primary factors influencing households’ behavioral intentions toward the adoption of CBDC.

To accomplish this objective, this study incorporates the Unified Theory of Acceptance and Use of Technology (UTAUT) with other factors such as attitude, perceived security, and perceived trust. This study contributes theoretically and practically in several ways. Theoretically, this research makes a major contribution to the existing knowledge on CBDC adoption by integrating multiple constructs such as trust, attitude, and perceived security, within a well-established technology adoption model. By doing so, it extends the theoretical understanding of consumer behavior toward digital financial innovations, particularly in emerging economies like India. From a literature standpoint, this study fills the research gap concerning household intentions and perceptions regarding CBDC adoption, an area that remains underexplored in the Indian context. Practically, this study can guide policymakers, regulatory bodies and financial institutions to develop strategic initiatives that enhance acceptability and adoption of CBDC among Indian households. Additionally, this study provides valuable insights to fintech firms and financial service providers on addressing consumer concerns related to security, trust, and usability, for smoother transition to digital stakeholders to design targeted awareness campaigns, improve digital financial literacy, and develop robust regulatory frameworks that align with consumer expectations and technological advancements.

This article’s remaining sections are organized as follows: the second section discusses the theoretical foundation and hypotheses development. The third section covers the research approach. The fourth section provides the outcomes of the study. The fifth section includes a full discussion of the findings, followed by the conclusion in the sixth section. The implications of the study are examined in the seventh section, while the eighth section underlines the limitations and proposes possibilities for future research.

Theoretical Foundation and Hypotheses Building

Theoretical Framework

UTAUT stands for unified theory of acceptance and use of technology that explains a user’s intention to engage with a technology and ensuing usage behavior (Venkatesh et al., 2003). This theory is the result of consolidating the constructs from eight different theories concerning technology acceptance, namely, theory of reasoned action (TRA), technology acceptance model (TAM), motivation model (MM), theory of planned behavior (TPB), combined TAM and TPB (C-TAM-TPB), model of PC utilization (MPCU), innovation diffusion theory (IDT), and social cognitive theory (SCT). It consists of four different factors, including performance expectancy, effort expectancy, social influence, and facilitating conditions that affect behavioral intentions to use a technology (Venkatesh et al., 2003). Our study takes all four antecedents as the predictors of behavioral intentions to adopt CBDC among households.

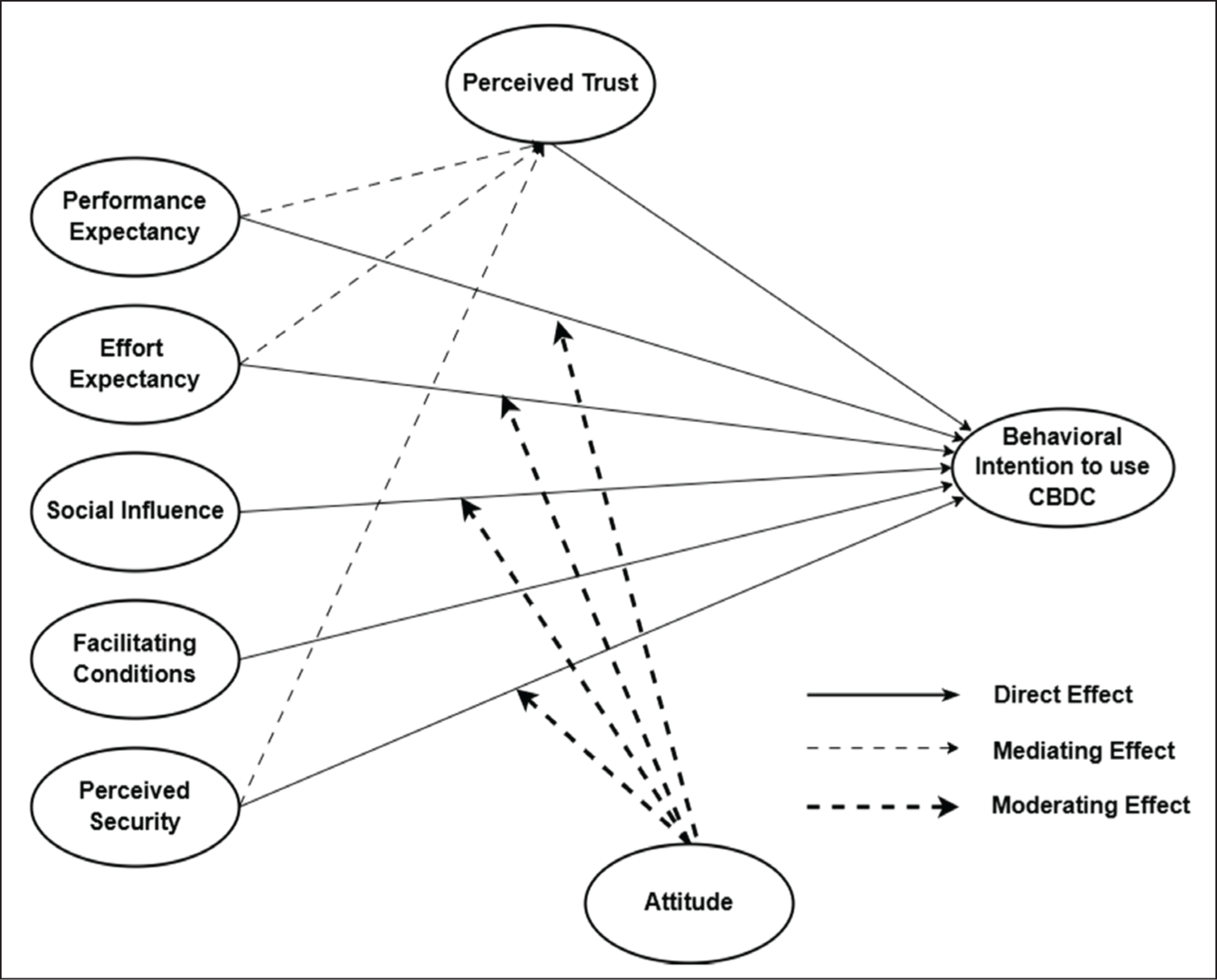

Besides, it is crucial to develop sufficiently secure technology so that users feel protected while using it and their data is not compromised. If consumers believe the system lacks sufficient security, they will not intend to use it and, thus, lose trust as well. Therefore, perceived security, being a crucial factor, is integrated with other four predictors of the UTAUT model that influence users’ behavioral intentions toward CBDC, while perceived trust has been incorporated as a mediator in the study. Moreover, it is important to know the effect of positive or negative attitude toward digital currencies on the intentions to use CBDCs. Thus, attitude is considered as a moderator for this study. The conceptual model of this study is presented in Figure 1.

Conceptual Model.

Hypotheses Development

Performance Expectancy and the Behavioral Intention to Use CBDC

According to Venkatesh et al. (2003), performance expectancy is the “degree to which an individual believes that using the system will help him/her to attain gains in job performance.” This research employs the concept of performance expectancy, which captures an individual’s belief that using a CBDC will improve their efficiency or productivity. The construct of performance expectancy aligns closely with the idea of perceived usefulness as introduced in the Technology Acceptance Model (TAM) by Davis (1989) and Davis et al. (1989), and this equivalence has been supported in prior studies (Kaur & Arora, 2021). Previous literature consistently indicates a significant association between performance expectancy and behavioral intention (Molina et al., 2019; Sivathanu, 2019; Söilen & Benhayoun, 2022). For instance, Kaur and Arora (2021) highlighted a positive impact of performance expectancy on users’ intention to engage with internet banking. Similarly, several researchers have found that users are more likely to adopt digital payment systems when they perceive them as performance enhancing (Aljawder & Abdulrazzaq, 2019; Seesuk, 2020; Sivathanu, 2019). This connection has also been confirmed in the domain of mobile investment applications (Hanif et al., 2024). Furthermore, recent studies on chatbot adoption (Paraskevi et al., 2023; Tian et al., 2024) reinforce this relationship. In light of this evidence, the current study formulates the following hypothesis:

H1: Performance expectancy has a positive effect on the behavioral intention to use CBDC.

Effort Expectancy and the Behavioral Intention to Use CBDC

Effort expectancy refers to how easy an individual perceives a technology to be when it comes to its usage (Venkatesh et al., 2003). In this study, it reflects a person’s belief about the simplicity and ease of interacting with CBDC. This concept closely aligns with the perceived ease of use described in TAM, developed by Davis (1989) and Davis et al. (1989), a similarity also acknowledged by Kaur and Arora (2021). Prior studies suggest that when users, particularly students, find mobile banking applications easy to navigate, their intention to use them tends to rise (Mustika & Puspita, 2021). This link was further supported in recent digital banking research by Meiranto et al. (2024). The adoption likelihood for fintech solutions increases when users believe the solutions have easy-to-use interfaces (Mangini et al., 2021). The findings of Mustika and Puspita (2021) demonstrate how usability enhances users’ intentions to utilize mobile banking applications. Hence, our study proposes the following hypothesis:

H2: Effort expectancy has a positive effect on the behavioral intention to use CBDC.

Social Influence and the Behavioral Intention to Use CBDC

According to Venkatesh et al. (2003), social influence describes the level at which individuals believe important people in their circle think they should adopt a specified system. The acceptance of CBDC by individuals depends on the views and anticipated behavior of the people in their social networks according to the context of this study. Venkatesh et al. (2003) linked social influence to three core elements, including subjective norms (Ajzen, 1991; Davis et al., 1989; Mathieson, 1991; Taylor & Todd, 1995a, 1995b), social factors (Thompson et al., 1991), and image (Moore & Benbasat, 1991). Research shows social power significantly influences how people form their intentions to behave especially when adopting mobile banking services (Safira, 2018). Also, there is a positive influence of social influence on the behavioral intention to use cryptocurrency (Kumari et al., 2023). The same relationship was found even in the context of digital payment system (Sivathanu, 2019). Hence, the study proposes the following hypothesis:

H3: Social influence has a positive effect on the behavioral intention to use CBDC.

Facilitating Conditions and the Behavioral Intention to Use CBDC

Facilitating conditions is “the degree to which an individual believes that an organisational and technical infrastructure exists to support use of the technology” (Venkatesh et al., 2003). In this research, facilitating conditions is defined as the extent to which an individual believes in the existence of organizational and technical infrastructure provided by RBI while using the CBDC. Research by Nur and Panggabean (2021) as well as Seesuk (2020) has highlighted a meaningful link between facilitating conditions and individuals’ intention to adopt mobile banking services. Similarly, a study by Paraskevi et al. (2023) emphasized the positive role of facilitating conditions in shaping users’ intention to engage with chatbots. This association has also been affirmed in the broader context of fintech adoption (Rahim et al., 2022). Supporting this, Sivathanu (2019) concluded that conducive technological and infrastructural support significantly affects users’ willingness to adopt digital payment systems. In light of these findings, the present study puts forward the following hypothesis:

H4: Facilitating conditions have a positive effect on the behavioral intention to use CBDC.

Perceived Security and the Behavioral Intention to Use CBDC

According to Kalakota and Whinston (1997), security is “a threat which creates circumstances, condition, or event with the potential to cause economic hardship to data or network resources in the form of destruction, disclosure, modification of data, denial of service and/or, fraud, waste, and abuse.” Users, regardless of whether they have internet access, have a widespread notion that conducting financial transactions online is not safe, which is why they do not engage in such activities (Singh et al., 2020). Service quality and security enhance user experience, ultimately fostering adoption and continuance intentions (Jain & Jain, 2025). When performing any kind of transaction by using the CBDC, a user’s perception of security is measured by the extent to which they feel secure doing so. There is a direct association between perceived security and the intention to use e-wallet (Nisa & Solekah, 2022). Therefore, while using the mobile banking, perceived security plays an important role (Singh & Srivastava, 2018). Sasiang et al. (2024) also validated this association in their study focusing on the adoption of DANA, an electronic money application. Hence, the study proposes the following hypothesis:

H5: Perceived security has a positive effect on the behavioral intention to use CBDC.

Perceived Trust as a Mediator

According to McKnight et al. (2011), trust is understood as the belief that a particular technology possesses the qualities required to function reliably in a specific context. When applied to CBDCs, perceived trust reflects the level of confidence users place in the system while interacting with it. In their study, Mustika and Puspita (2021) examined how perceived trust acts as a mediating factor between the perceived ease of use and the behavioral intention to use mobile banking. Al-Sharafi et al. (2018) and Ramos et al. (2018) in their study found the significant impact of perceived ease of use and perceived usefulness on perceived trust. The research by Kaur et al. (2024) showed that perceived security produces specific effects that enable perceived trust development. Bhatt et al. (2022) established through research that perceived security along with trust levels affects how much people adopt mobile banking technology. The relationship between users’ behavioral intentions toward AI-driven teacher bots demonstrates a significant connection with the perception of trust (Pillai et al., 2024). Kumari et al. (2023) identified a direct relationship between perceived trust and the adoption intent for cryptocurrency. The research by Nisa and Solekah (2022) established that perceived trust acts as a mediator that links perceived security to behavioral intention when analyzing e-wallet adoption. Additionally, a significant relationship between perceived trust and behavioral intention toward fintech was discovered by Ali et al. (2021). Hence, the study proposes the following hypothesis:

H6a: The relationship between performance expectancy and the behavioral intention to use CBDC is mediated by perceived trust. H6b: The relationship between effort expectancy and the behavioral intention to use CBDC is mediated by perceived trust. H6c: The relationship between perceived security and the behavioral intention to use CBDC is mediated by perceived trust.

Attitude as a Moderator

With regard to CBDC, one’s attitude can be described as “their beliefs, which can be either good or negative.” Schierz et al. (2010), in their research, found that factors such as perceived usefulness, ease of use, subjective norms, and perceived security positively and significantly shape users’ attitudes, which in turn influence their intention to use mobile payment services. This relationship was supported by Kaur et al. (2024) and Alswaigh and Aloud (2021) as well in the context of mobile wallets. It was also found that attitude is positively influenced by perceived usefulness and perceived ease of use, and further, it impacts the behavioral intention to use mobile financial services (Himel et al., 2021). Moreover, Rahman et al. (2022) found that attitude is dependent on perceived usefulness. Polyportis and Pahos (2025) examined how performance expectancy and effort expectancy are positively associated with users’ attitudes. Research by Durak and Onan (2024) demonstrated attitude has a major influence on determining how people form behavioral intentions regarding AI-driven system adoption. Hence, the study proposes the following hypothesis:

H7a: Attitude moderates the relationship between performance expectancy and the behavioral intention to use CBDC. H7b: Attitude moderates the relationship between effort expectancy and the behavioral intention to use CBDC. H7c: Attitude moderates the relationship between social influence and the behavioral intention to use CBDC. H7d: Attitude moderates the relationship between perceived security and the behavioral intention to use CBDC.

Research Methodology

Research Design

This research adopts a descriptive approach. This article uses a multi-indicator model with several reflective constructs to evaluate the influence of different latent variables under study. The data collected is cross-sectional in nature. The cross-sectional designs are particularly useful when examining the prevalence of certain attitudes and levels of awareness, especially for the purpose of evaluating the reliability and validity of a given concept (Kesmodel, 2018).

Instrumentation and Measurement Items

To gather primary data, a carefully designed close-ended questionnaire incorporating a Likert scale was utilized. The questionnaire so formulated comprised two sections. Section I consisted of demographics of the respondents, and Section II collected their responses on various scale items. All the scales used in this study were standardized; however, they were modified as per the suitability of the research objective of the present study. The items for different scales used in the study such as performance expectancy (Venkatesh et al., 2003, 2012; Zhou et al., 2010), effort expectancy (Chan et al., 2022; Venkatesh et al., 2003, 2012; Zhou et al., 2010), social influence (Chan et al., 2022; Zhou et al., 2010; Sivathanu, 2019), facilitating conditions (Gan et al., 2021; Venkatesh et al., 2003, 2012; Zhou et al., 2010), perceived security (Liu et al., 2022; Nadeem et al., 2021), perceived trust (Akinwale & Kyari, 2022; Chan et al., 2022), attitude (Bashir & Madhavaiah, 2015; Grabner-Kräuter & Faullant, 2008), and behavioral intention (Venkatesh et al., 2003, 2012), were measured on a five-point Likert scale ranging from 1 (strongly disagree) to 5 (strongly agree).

Sampling and Data Collection

Primary data for the study were collected using an online survey distributed among individuals within the researchers’ social circles. Participation was entirely voluntary, and those who agreed to take part were also encouraged to forward the questionnaire within their own networks. This snowball sampling technique has been successfully adopted in previous studies to access specific respondent groups (Eren, 2021; Zainudin et al., 2019). To ensure the relevance of the sample, an initial screening question assessed participants’ awareness of CBDC. A total of 500 survey links were distributed to households based in northern India. Of these, 398 valid responses were received. During the data screening process, 12 responses were removed due to incompleteness, resulting in a final data set comprising 386 usable responses. To validate the adequacy of this sample size, a G*Power analysis was conducted, following the guidance provided by Hair et al. (2014). The results showed that a minimum of 210 responses is sufficient to achieve a statistical power of 95%, while 172 responses are adequate for a 90% power level. Therefore, the final sample size of 386 is considered more than sufficient for robust analysis.

Non-response Bias and Common Method Bias

In order to analyze if non-response bias was not an issue in our research, we compared early respondents with late respondents with 50 respondents in each group (Armstrong & Overton, 1977). According to the continuum of resistance model, late respondents can be used as a proxy for non-respondents in calculating the non-response bias (Lin & Schaeffer, 1995; Voogt et al., 1998). Then, the comparison of early respondents and late respondents was done using paired samples t-test in SPSS 25. The results of the t-test showed no significant differences between early respondents and late respondents, indicating that non-response bias is not an issue in our study. Hence, the sample of 386 for data analysis was fit enough in all respects. Further, the common method bias was investigated using full-collinearity variance inflation factors (VIFs) of the inner model. If all the values in the inner model resulting from a full collinearity test are equal to or lower than 3.3, the model can be considered free of common method bias (Kock, 2015). In the present study, the VIF of all the constructs (performance expectancy = 1.96, effort expectancy = 2.060, social influence = 1.383, facilitating conditions = 1.654, perceived security = 1.748, perceived trust = 2.257, attitude = 2.239) is lower than the threshold limit; hence, there is no common method bias in our inner model.

Analytic Approach

PLS-SEM is generally recommended when the primary aim of the research is to contribute to or expand upon existing theoretical frameworks (Hair et al., 2011). This method offers flexibility in modeling complex constructs, making it suitable for exploratory studies (Henseler, 2010). Considering the nature of our conceptual framework and the characteristics of the data set, we employed SmartPLS version 4.1.0.9 (Ringle et al., 2014) to evaluate the constructs in terms of validity and reliability, as well as to test the proposed hypotheses. Additionally, SPSS version 25 was utilized for analyzing demographic data, specifically to calculate frequencies and percentages, due to its user-friendly interface and efficient data handling capabilities.

Results

Demographic Profile

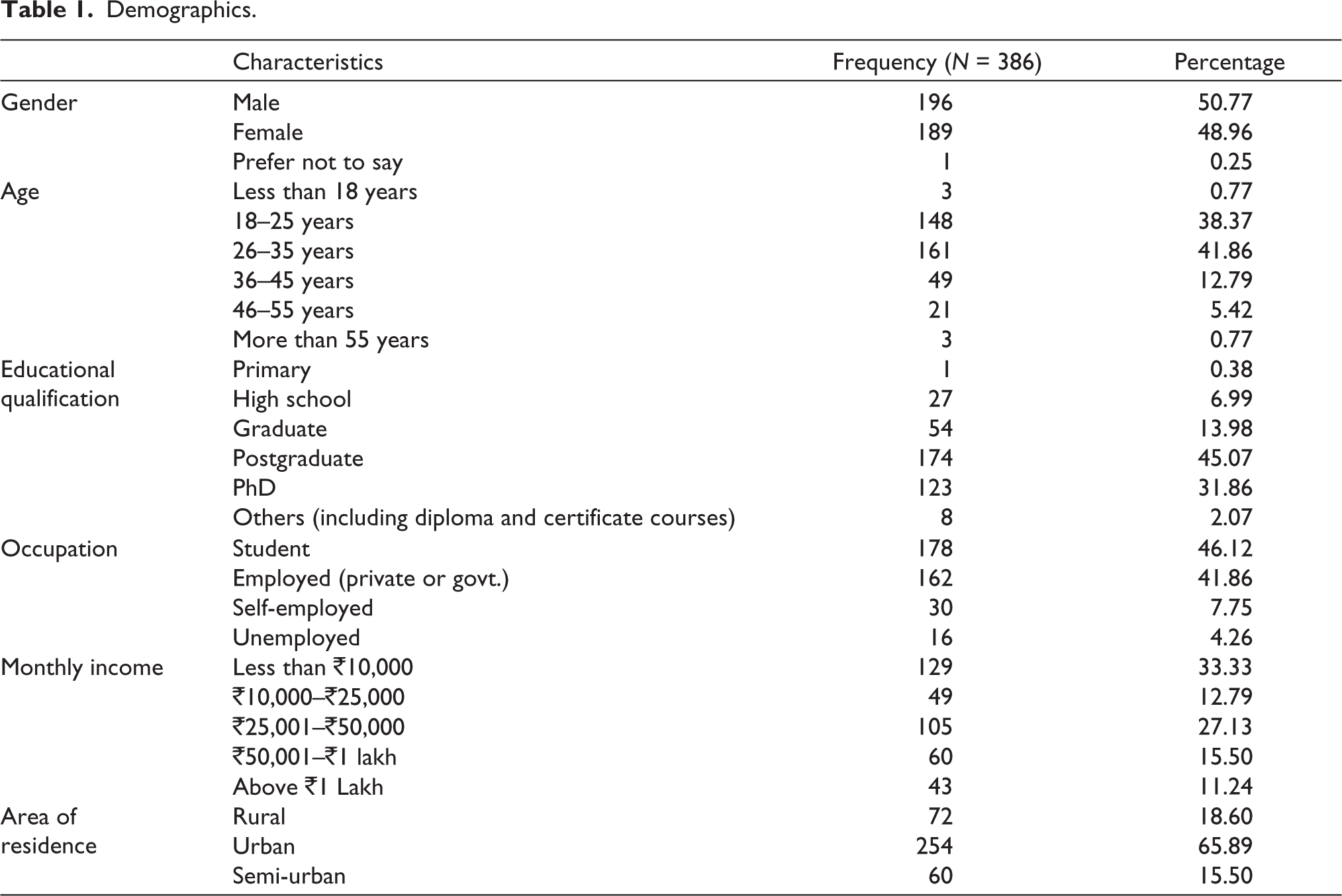

Out of 386 surveyed participants, 50.77% were males and 48.96% were females. A significant portion of the participants (80.23%) fell within the age group of 18– 35 years. Educational qualifications were predominantly postgraduate (45.07%) and PhD holders (31.86%). In terms of occupation, 46.12% were students, followed by 41.86% employed individuals. Monthly income varied, with 33.33% earning below ₹10,000 and 27.13% between ₹25,001 and ₹50,000. Most respondents resided in urban areas (65.89%), while 18.60% were from rural and 15.50% from semi-urban regions. The detailed demographics of the sample are depicted in Table 1.

Demographics.

Assessment of Multivariate Normality

For the purpose of evaluating multivariate normality, the authors investigated “multivariate skewness and kurtosis” using a statistical tool from a website named Web Power (

Measurement Model Results

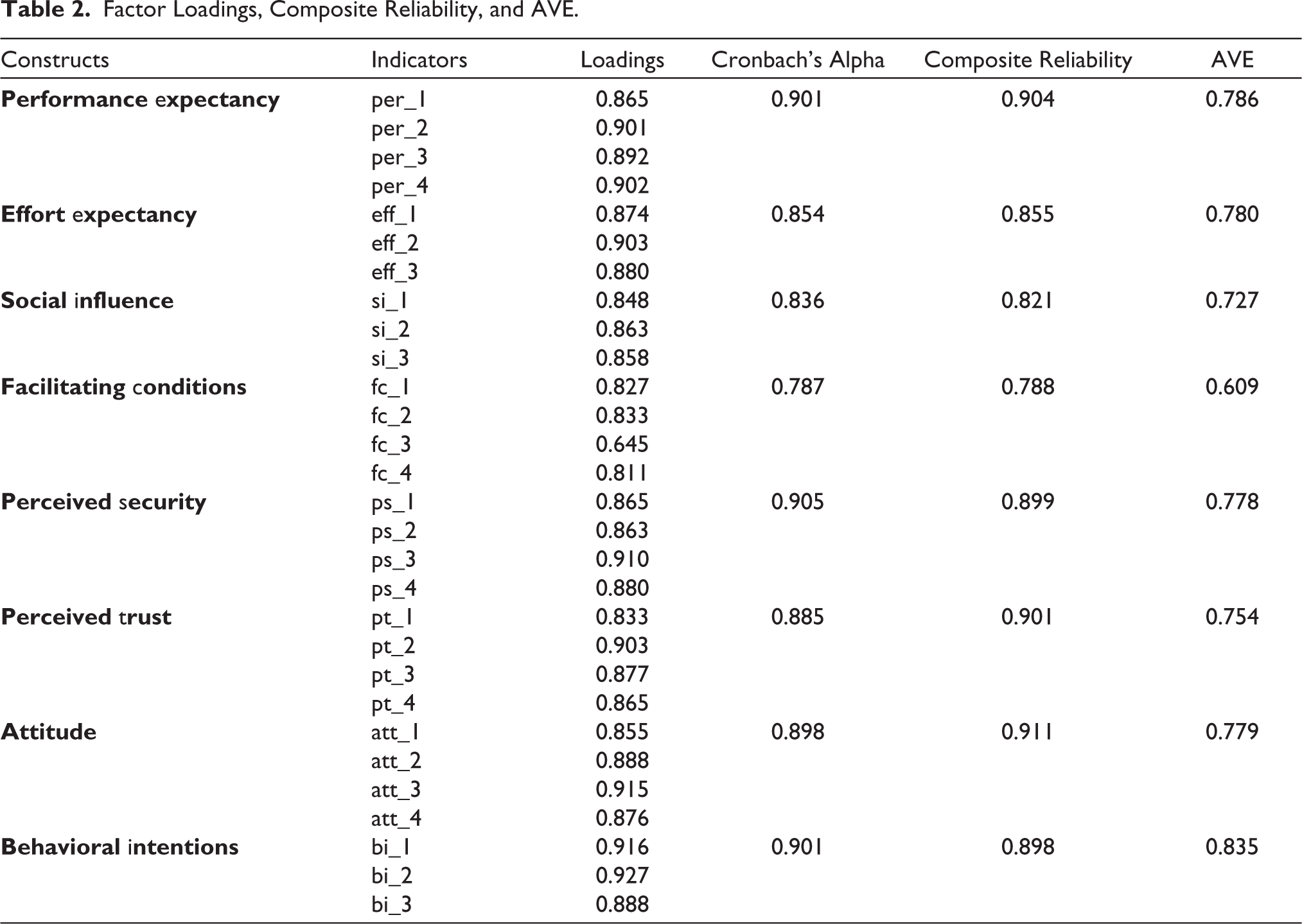

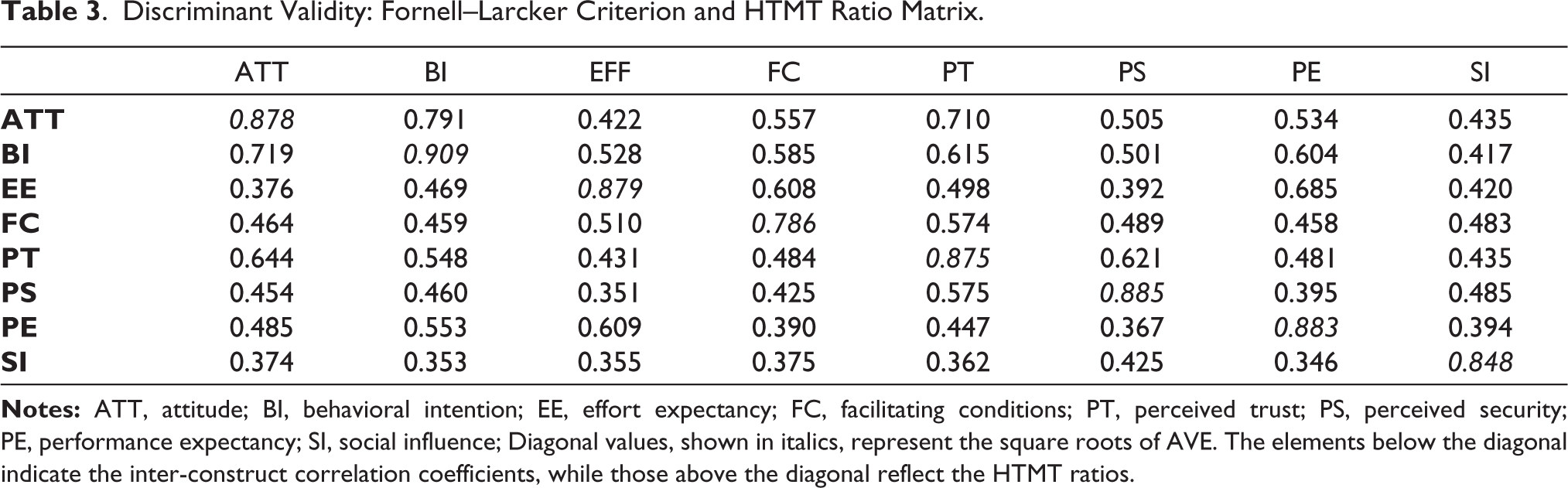

The results of empirical model are generally measured in two parts, namely, measurement model results and structural model results. The research evaluated its measurement model to verify both construct validity and reliability using indicator reliability, internal consistency, discriminant validity, and convergent validity measures (Kaur & Singh, 2024). Table 2 demonstrates the factor loadings of the items of constructs used in this research. Henseler and Guerreiro (2020) recommend that factor loadings should surpass 0.708 to ensure indicator reliability in a measurement model. The majority of items achieved the acceptable loading threshold though the third item from the construct facilitating conditions (Fc_3) failed to reach it. However, items with loadings slightly below 0.708 can still be retained if the average variance extracted (AVE) for the construct remains above the acceptable level, as supported by Hair et al. (2014) and Mago et al. (2024). In this case, AVE was not compromised, thus validating the inclusion of the item. The assessment of convergent validity depended on the examination of AVE values according to the minimum parameter of 0.50 (Henseler & Schuberth, 2020). The reported AVE values indicate convergent validity in this study because all constructs exceeded the 0.50 benchmark (Hair et al., 2020). Composite reliability and Cronbach’s alpha values (refer to Table 2) served to validate the internal consistency and reliability of the study. Benitez et al. (2020) indicate that a minimum composite reliability of 0.70 validates the measurement quality. The internal consistency of all constructs showed high strength through both composite reliability and Cronbach’s alpha measurements, which exceeded 0.80 (Henseler et al., 2009). The assessment of discriminant validity employed two approaches, which consisted of Fornell–Larcker criterion and heterotrait–monotrait (HTMT) ratio. The results in Table 3 support construct discriminant validity via the Fornell–Larcker criterion because all construct AVE square roots exceeded their correlation values with other constructs (Fornell & Larcker, 1981). The HTMT ratio revealed results that stayed under a conservative threshold of 0.85 for every construct pair, which supported discriminatory validity (Henseler et al., 2015).

Factor Loadings, Composite Reliability, and AVE.

Discriminant Validity: Fornell–Larcker Criterion and HTMT Ratio Matrix.

Structural Model Results

The structural model was used to understand how well our model could predict and explain certain outcomes (Sarstedt et al., 2022). In this model, the path coefficients (β) were analyzed, which demonstrate the strength and significance of the relationship between different variables (Ghasemy et al., 2020; Saari et al., 2021). We employed bootstrapping with 10,000 subsamples to ascertain the statistical significance of the path coefficients.

Analysis of Direct Effects

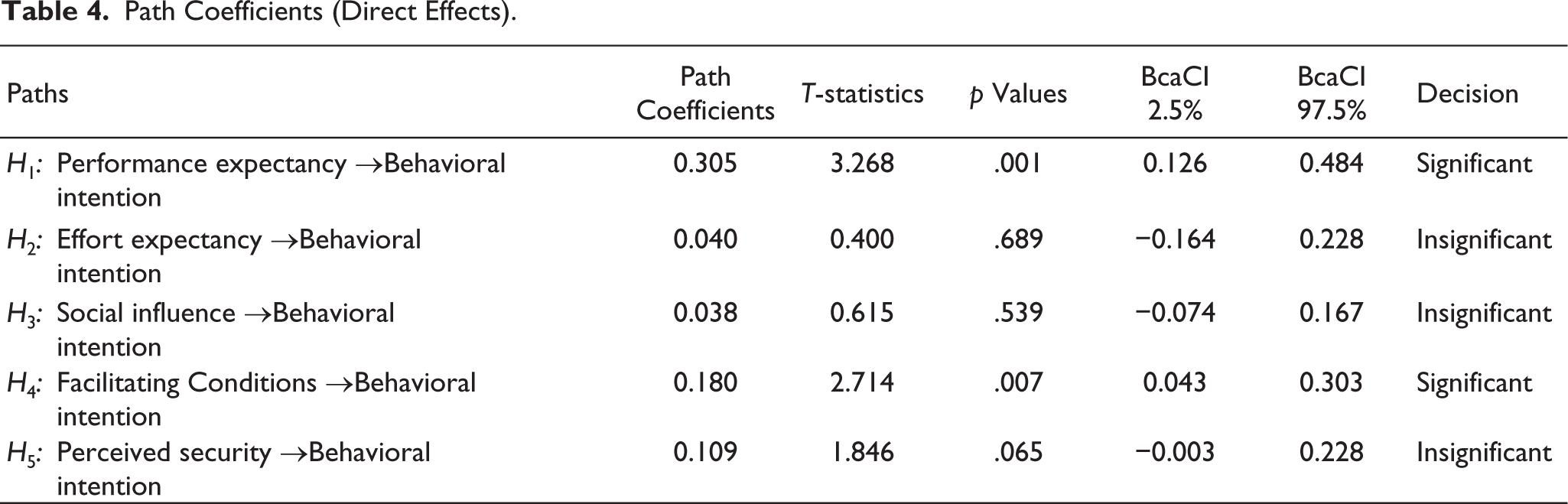

Table 4 exhibits the results of direct effects of different variables. The outcomes from the data analysis reveal that paths from performance expectancy and behavioral intention (β = 0.305, t-statistics = 3.268, p value < .05), facilitating conditions to behavioral intention (β = 0.18, t-statistics = 2.714, p value < .05), were statistically significant as their p values were at less than .05 significance level. Hence, the results from the data analysis support the hypotheses H1 and H4; however, H2, H3, and H5 were rejected.

Path Coefficients (Direct Effects).

Analysis of Mediating Effects

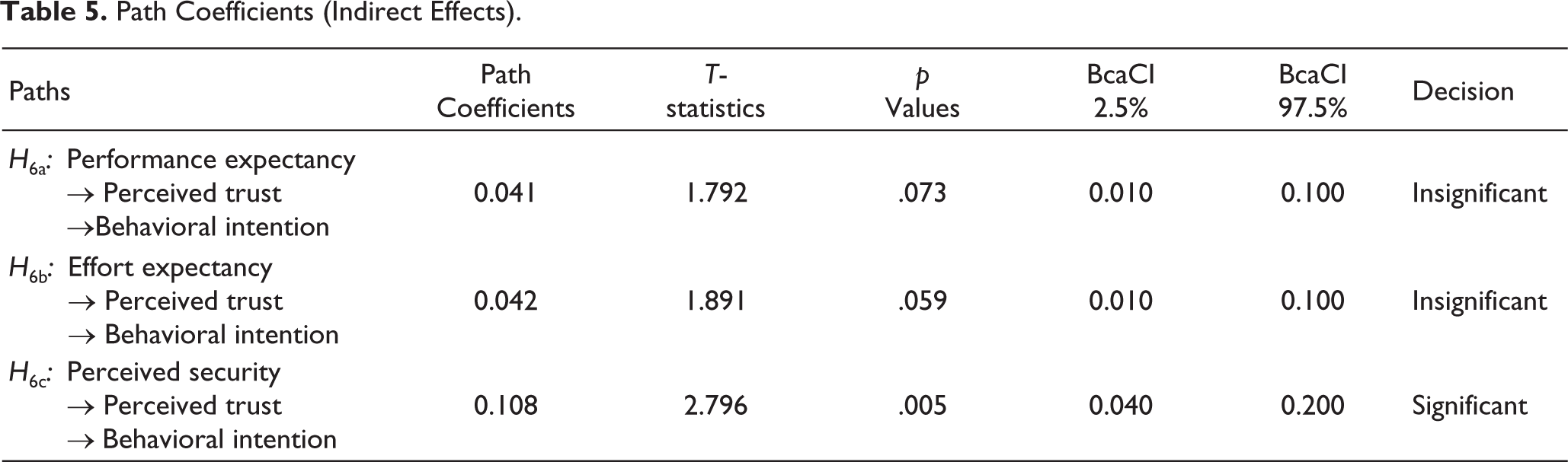

The results in Table 5 reveal that the indirect effect of perceived security on behavioral intention through perceived trust (β = 0.108, t-statistics = 2.796, p value < .05) was statistically significant, pointing to the fact that perceived trust had significant mediation effect on the relationship between perceived security and behavioral intention. Hence, H6c was supported. However, the indirect effect of performance expectancy on behavioral intention through perceived trust (β = 0.041, t-statistics = 1.792, p value = .073) and effort expectancy on behavioral intention through perceived trust (β = 0.042, t-statistics = 1.891, p value = .059) was statistically insignificant as per the results from the data set. Hence, H6a and H6b were rejected.

Path Coefficients (Indirect Effects).

Moderating Effects

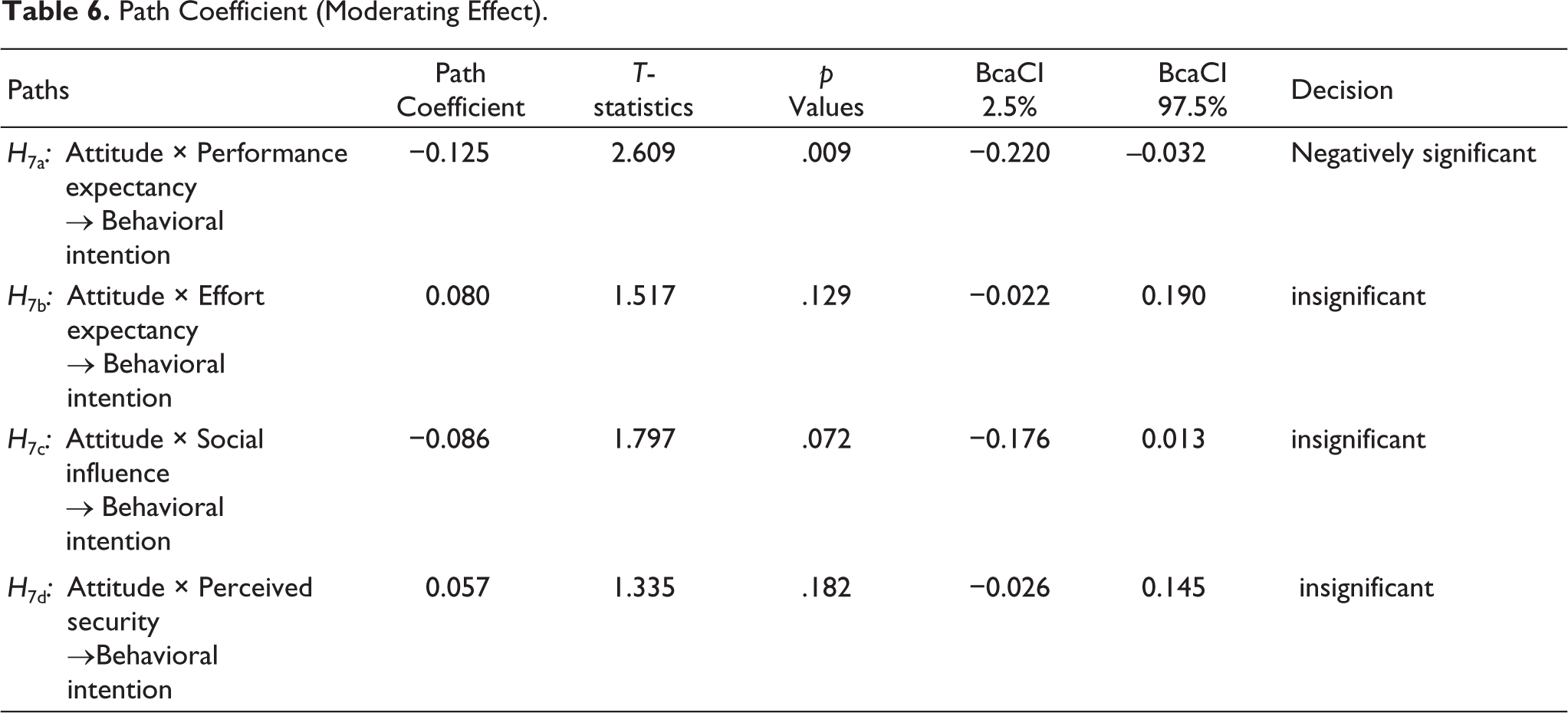

Hypotheses H7b, H7c, and H7d were not supported, as the analysis did not reveal any significant moderating role of consumers’ attitudes toward CBDC in the relationships between effort expectancy and behavioral intention (β = 0.080, t = 1.517, p > .05), social influence and behavioral intention (β = −0.086, t = 1.797, p >.05), and perceived security and behavioral intention (β = 0.057, t = 1.335, p > .05). However, the results did indicate a significant negative moderating effect of attitude on the link between performance expectancy and behavioral intention (β = −0.125, t = 2.609, p < .05), thus validating hypothesis H7a (see Table 6). This suggests that when individuals hold a less favorable attitude toward CBDC, the positive impact of performance expectancy on their intention to adopt it diminishes. In simpler terms, those skeptical or uncertain about CBDC may be less likely to believe in its functional benefits compared to other existing digital payment alternatives.

Path Coefficient (Moderating Effect).

Coefficient of Determination (R-squared)

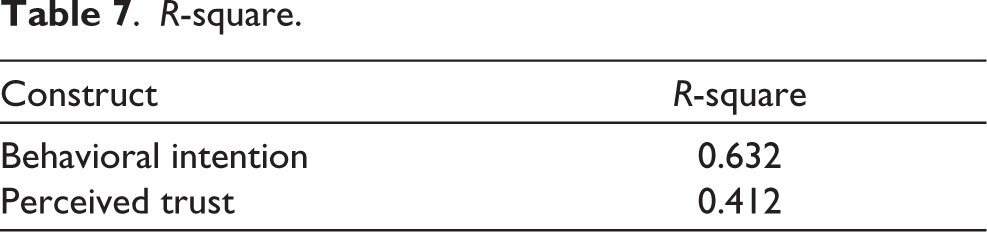

The empirical model explains an overall 63.2% behavioral intention to adopt CBDC based on the six latent constructs of performance expectancy, effort expectancy, social influence, facilitating conditions, perceived security, and perceived trust (Table 7). The R-square value of 0.632 for behavioral intention supports model reliability and statistical potency based on Falk and Miller (1992) standards while meeting the criteria established by Cohen (2013). Additionally, the value of R-square for perceived trust was 0.412, which signifies that 41.2% variance of perceived trust is explained by the three independent variables of our empirical model, that is, performance expectancy, effort expectancy, and perceived security.

R-square.

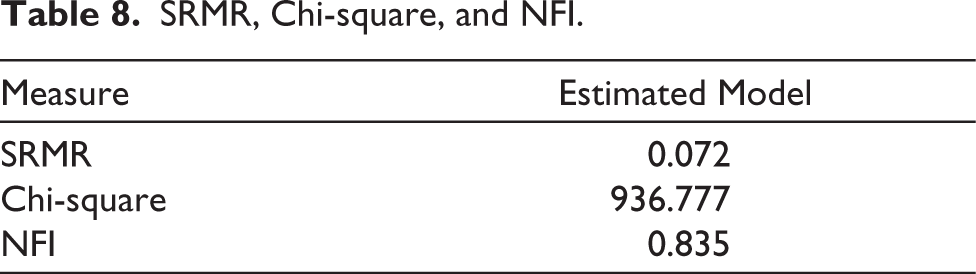

Model Fit Criteria

The measures utilized to evaluate the model fit of our empirical model include standardized root mean square residual (SRMR), chi-square, and Normed Fit Index (NFI), also known as the Bentler and Bonett Index. SRMR value less than 0.08 is considered a good fit (Hu & Bentler, 1999). In our case, the value of SRMR is 0.072 (refer to Table 8), which is well below the threshold value. Hence, our model is a good fit. Besides, chi-square and NFI have been calculated. The NFI is calculated by subtracting the ratio of the chi-square value of the proposed model to that of the null model from 1. The closer the NFI to 1, the better the fit. In our case, the value of chi-square is 936.777 (Table 8), while the value of NFI is 0.835 (Table 8), which represents a satisfactory fit of the proposed model.

SRMR, Chi-square, and NFI.

Predictive Relevance (Q-square)

The predictive relevance of the model was analyzed with the help of blindfolding, in which Stone–Geyser’s Q-square and root mean square error (RMSE) of the endogenous construct were calculated, and it was found that the value of Q-square for the model was 0.584, which points to the fact that the model has quite high predictive relevance (Hair et al., 2011), while the RMSE value for the same is found to be 0.652 (Table 9). For RMSE, it is generally believed that the closer the value of RMSE to 0, the better it is (Armstrong & Collopy, 1992).

Predictive Relevance.

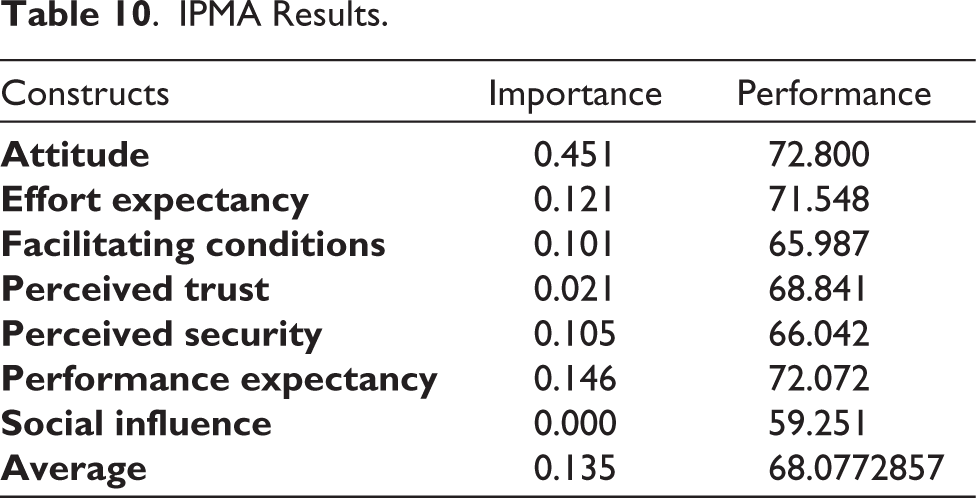

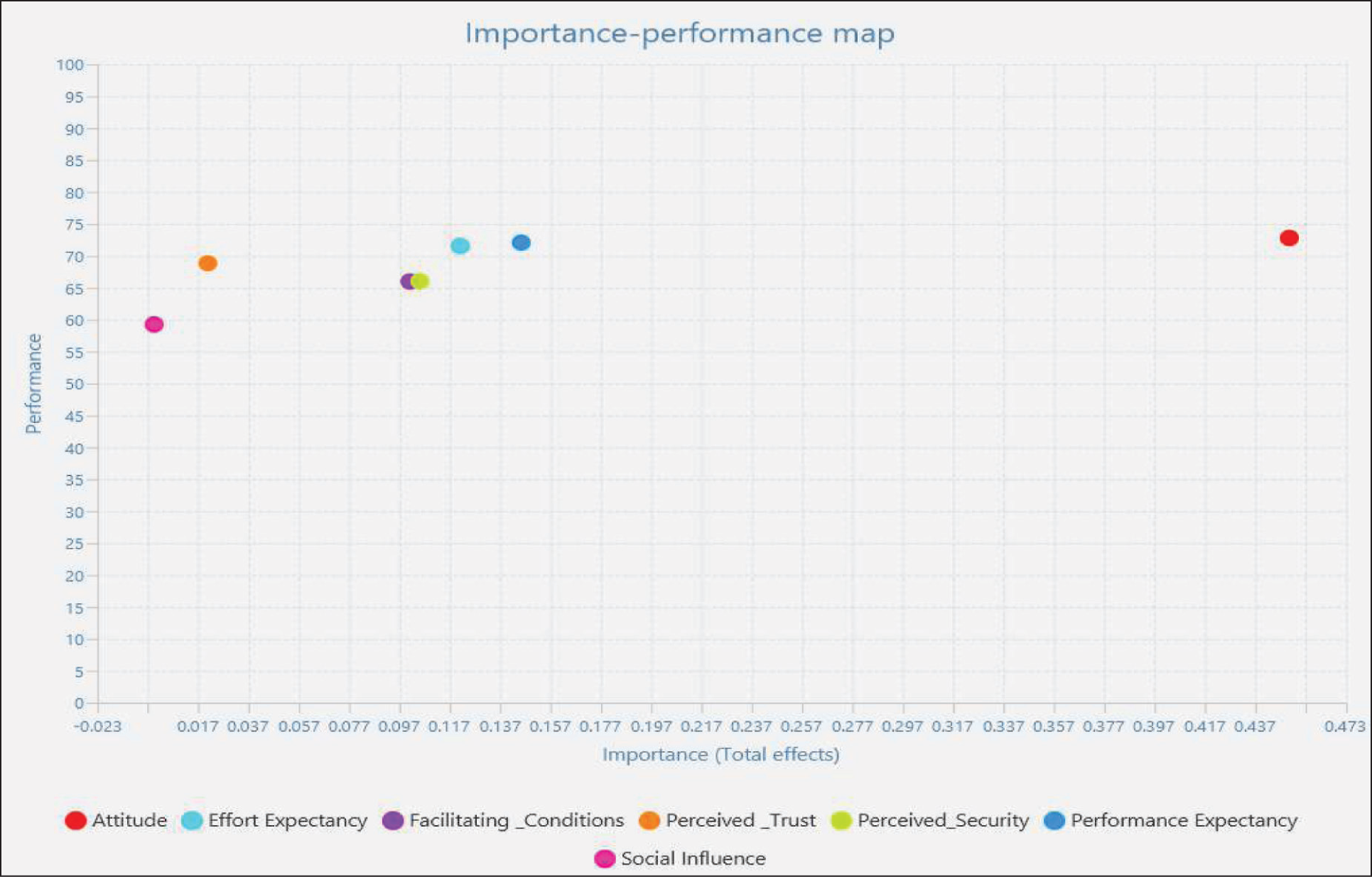

IPMA Results

Table 10 and Figure 2 present the results of IPMA by keeping an utmost focus on the endogenous variable of our study, that is, behavioral intention toward the usage of CBDC. Notably, performance expectancy has both high performance and high importance in the proposed and tested empirical model of our study. This is suggestive of the fact that households are completely aware about the performance aspect in any online payment system and place relatively significant amount of importance on this particular aspect before adopting any online based currency system such as CBDC. Similarly, our results reveal that effort expectancy has second highest performance while it also has quite high importance, which means that the central government ought to make serious efforts toward providing a robust customer support to the consumers so that they develop confidence that they can rely on the system in the case of need. Next, facilitating conditions and perceived security were found to have moderate importance and performance. This means that the central government must ensure that the consumers are fully aware so as to prevent cyber frauds. Further, we observe that perceived trust, the mediator used in the study, has relatively high performance; however, its importance index is significantly low compared with other constructs. Regarding this construct, the central banks must create an awareness among the consumers to place utmost faith in the central system of launching CBDC. Finally, regarding social influence construct, the values of both performance and importance are the lowest among all the other constructs, which means that the consumers are generally least affected by the opinion of their peer groups for the adoption of CBDC. In this regard, the central government must make efforts to disseminate widespread knowledge about CBDC among the people of the country, and it must induce the people to carry out the transactions with their acquaintances through CBDC in future. Besides, the moderating variable, attitude, has the highest performance and importance. This implies that the central government must ensure widespread efforts to develop a positive attitude among the public regarding CBDC and to encourage Indian households to embrace the use of CBDC.

IPMA Results.

IPMA Chart.

Discussion

On the basis of the results obtained through the analysis, it is found that performance expectancy and facilitating conditions have a significant influence on the behavioral intention to use CBDC. Additionally, perceived trust establishes itself as a key mediator that connects perceived security with CBDC adoption intent.

In detail, the findings suggest that the users are more likely to use CBDC in future if they are convinced with its performance features, signifying a positive relationship between performance expectancy and behavioral intention (H1), in line with the findings of Molina et al. (2019), Sivathanu (2019), Söilen & Benhayoun (2022), Paraskevi et al. (2023) and Tian et al. (2024), who explored a similar relationship between performance expectancy and behavioral intention. However, hypothesis H6a) stating the indirect effect of perceived trust on the relationship between performance expectancy and behavioral intention was rejected, meaning that there is no mediating role played by perceived trust between performance expectancy and behavioral intention. Further, similar to the findings of Nur & Panggabean (2021), Safira (2018), Seesuk (2020) and Rahim et al. (2022), the relationship between facilitating conditions and behavioral intentions (H4) was found to be positive in our study, signifying the fact that institutional support enabled by RBI in case of need would have a profound effect on adoption of CBDC. Again, the positive relationship between perceived security and behavioral intention as proved by Ramos et al. (2018), Nisa and Solekah (2022), Singh and Srivastava (2018) and Sasiang et al. (2024) in their respective studies has been reconfirmed through our findings as the users tend to show greater likelihood toward the usage of CBDC if they feel that their financial transactions are safe and secure (Singh et al., 2020) but through the mediation of perceived trust. Clearly, it has been revealed by the study that perceived trust has an indirect effect on the relationship between perceived security and behavioral intention (H6c). Contrarily, in our proposed conceptual model, the relationship between effort expectancy and behavioral intention (H2) and perceived security and behavioral intention (H5) has been found to be insignificant in contrast to the previous studies (Mangini et al., 2021; Meiranto et al., 2024; Mustika & Puspita, 2021), pointing to the fact that the users will not associate the effort expectancy (or perceived ease of use) and perceived security directly with the intent to use CBDC in future. Additionally, the role of perceived trust as a mediator between effort expectancy and behavioral intention has also been found to be insignificant. So, hypothesis H6b was rejected in contradiction to the findings of Mustika and Puspita (2021). Besides, the effect of social influence (H3) is also insignificant in the intention to adopt CBDC, as the users might feel the decision to use CBDC to be their personal decision irrespective of the influence of any social group including peers, friends and family (Molina et al., 2019; Singh et al., 2020; Singh & Srivastava, 2018; Tang et al., 2021). In this research, the construct of attitude is examined to understand its moderating role in the relationships between performance expectancy, effort expectancy, social influence, perceived security, and the intention to use CBDC. The findings indicate that attitude shows a minimal moderating influence on the connections between effort expectancy, social influence, perceived security, and behavioral intention (H7b–H7d). However, a noteworthy negative moderation effect was observed between performance expectancy and behavioral intention (H7a). This suggests that when individuals hold a negative attitude toward CBDC, it may diminish the influence of performance expectancy on their intention to adopt it. In simpler terms, individuals who are skeptical or have unfavorable views of CBDC may not expect it to perform well or may question its efficiency compared to other digital payment alternatives (Himel et al., 2021).

Conclusion

Although many countries have successfully implemented it, the development of CBDC in India is still in its nascent stage. A smooth migration to digital currency needs a comprehensive analysis of factors that both promote its adoption and optimize its practical implementation. A variety of parameters such as gender, age, education, profession, and income have to be thoroughly examined through nationwide research to better comprehend their effects. Furthermore, since digital currency will be used as an alternative to traditional currency, understanding what makes users decide which system to use requires investigation. Our study actually charts out the motivations useful for the adoption of CBDC among the households in India. Particularly, our findings suggest that there is a dire need to diffuse the awareness about CBDC among the locals of the country and develop their attitude toward it so as to induce them to use CBDC for conducting smooth transactions in the future. Moreover, the study contributes to the existing literature by supporting the global community in creating a common base to make inter-country currency exchange possible through distributed ledger transactions (DLT), providing impetus to the countries running CBDC testing programs.

Implications of the Research

The study based on the application of UTAUT model extended with perceived security as an additional variable, perceived trust as a mediator and attitude as a moderator renders serious theoretical, practical and managerial implications for various stakeholders. First of all, the results of IPMA in the study suggests that the favourable attitude of the users toward CBDC is crucial for enhancing its popularity and usage, which is greatly influenced by the expected performance of the CBDC and the ease of using it. Also, the new constructs added to extend the UTAUT model demonstrated good predictive relevance and explanatory power, contributing greatly to the existing literature. Besides this, an important implication of our research is that the perception of trust for the system among the users can largely encourage the adoption of CBDC, and this will be one step forward in the direction of establishing control over the monetary policy by the government. Also, social influence has an insignificant effect on adoption intention toward CBDC, so in this case, the government should insist the users to exchange payments digitally so that the number of peer-to-peer digital payments can be fostered. Apart from this, the central bank should put collective efforts in the direction of reinforcing the trust of the general public in the facilitating conditions and perceived financial security of the system for establishing a favorable image toward a robust, safe, and secure CBDC system among the public.

One major observation from the study during data collection is that there is lack of awareness among the general public regarding the adoption of CBDC. Thus, this information can prove to be really helpful for policymakers as the policies and initiatives in the direction of promoting digital training and awareness among the potential users can be framed. In addition, the government should also promote financial literacy among the users so as to promote widespread adoption of CBDC. Also, it will serve as an impetus to the “Digital India” program, which aims at promoting seamless flow of transactions across international borders, making payments easy, convenient, and transparent.

Limitations and Suggestions for Future Work

The present study suffers from some limitations, which can be improved by the researchers who wish to undertake the study on this topic. First of all, the data used in this study is cross-sectional. In future, researchers can use the longitudinal approach for conducting the study on the subject of CBDC. In fact, in India, CBDC is still in its pilot testing stage; thus, future research studies can focus on a comparison between pre- and post-launch behavior toward CBDC once it is fully launched across the nation. Further, the literature suggests some variables that could significantly affect the intention behavior of the users toward CBDC such as perceived value, perceived credibility, system quality, etc. The present study mainly undertakes the UTAUT theory as a theoretical framework; instead of this, the extended versions of UTAUT theory such as UTAUT-2 and UTAUT-3 can be taken into account by the studies to be conducted in the future. Additionally, the current study studies only attitude as a moderator; apart from this, gender, age, qualification, and prior experience of the digital payment system can act as moderators in further studies. Furthermore, a majority of the respondents were students of higher educational institutions, which might affect the generalizability of our results. Hence, we recommend the future researchers to conduct studies on different segments of the population and also in other countries and continents to measure the difference in the results. Finally, the present study utilizes a limited number of constructs, which affect the adoption intention toward CBDC through PLS-SEM. Future research studies can test this conceptual model by incorporating additional constructs, which can affect the adoption intention of CBDC, and applying some other empirical tests such as confirmatory-tetrad analysis etc.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.