Abstract

The aim of this study is to explore the impact of overall and individual environmental, social and governance (ESG) disclosure scores on firm performance of the financial and non-financial companies. The study has used the data of 95 companies for the period of 2020 to 2023. The data has been calculated from Thomson Reuters Framework. The sample companies’ ESG disclosure score is calculated by content analysis, and the effect of the ESG score on firm performance is examined using panel data regression analysis. The environmental (ENV) and social (SOC) disclosure scores separately as well as the overall ESG score have an insignificant impact on return on asset (ROA). The ROA results have also additionally showed that the operational performance of the governance disclosure score is negatively impacted, but not significantly. According to return on equity (ROE) results, the individual (SOC) disclosure scores significant positive impact on ROE (financial performance). However, individual ENV and governance disclosure scores insignificant negative impact on ROE. Simultaneously, the analysis of overall ESG disclosure score is insignificant positive impact on ROE. Based on market-based performance (Tobin’s Q), results show that individual ENV disclosure score has a significant positive impact. In contrast, individual SOC and governance disclosure scores have an insignificant positive impact on Tobin’s Q. Simultaneously, the analysis of overall ESG disclosure score shows significant and positive impact on Tobin’s Q. Thus, ROA, ROE and Tobin’s Q show significant impact of firm size on form performance.

Introduction

Many concepts relating to environmental (ENV), social (SOC) and economic problems have evolved in response to corporate practices in recent decades as a result of the disclosure landscape’s expansion and the well-established global interest in non-financial information. As a result, several stakeholders took the initiative to adopt a corporate responsibility strategy for their position and the level of their contribution to reaching their ambitions (Abu Qa’dan & Suwaidan 2019). Governments need to offer a range of financial incentives to promote the adoption of environmental, social and governance (ESG) in order for businesses to engage in ESG disclosures that are advantageous to both their shareholders and their business value chain (Jallai, 2020). ESG disclosure is becoming common among communities and enterprises that prioritise SOC responsibility (Shaikh, 2021).

The ESG assessment is now an essential part of the investment process because of the increased focus on enhancing a company’s sustainability and SOC effects (Caporale et al., 2022). For ethical lenders and shareholders, a lack of clarity in the disclosure of ESG activities may lead to insufficient information during the decision-making process (Rabaya & Saleh 2021). Actually, the purpose of an ESG disclosure score consists of clearly and objectively examine ESG performance, taking into consideration all aspects of corporate social responsibility (CSR’s) ENV and SOC initiatives, as well as its corporate governance (GOV) efforts (Paolone et al., 2022). The aim of the ESG indicator is to demonstrate that these actions improve business success in beyond addressing ethical issues (Serban et al., 2022). ESG disclosures provide stakeholders, such as investors, communities, employees and regulators, with information about a company’s overall activities (Atif et al., 2022). Stakeholder expectations for SOC responsibility, accountability and transparency have led to an increase in the significance of ESG elements in the corporate world (Dathe et al., 2023).

Companies that perform well on ESG metrics often have greater accessibility to commercial credit (Luo et al., 2023) and demonstrate superior property as a safe investment vehicle amid the coronavirus disease 2019 (COVID-19)-related world health epidemic (Rubbaniy et al., 2022). Sustainability initiatives may be seen as a way for companies to show users that they are sincerely concerned about their requirements and concerns (Kalia & Aggarwal, 2023). Historically, companies have made choices that have had a major negative impact on GOV, society and the environment in order to boost their short-term financial performance (Khandelwal et al., 2023).

The majority of developed nations have reached a mature stage of development because of the attention that various borrowers, lawmakers, investors and journalists have paid to CSR information. In contrast, emerging nations are still in the early stages of economic development because they frequently overlook ESG practices in favour of concentrating solely on revenue growth, monetary benefits and manufacturing scale (Ali et al., 2017). However, there is a lot of potential for ESG work to be done in a developing nation like India. The Securities and Exchange Board of India (SEBI) business responsibility reporting standards and the Companies Act 2013’s corporate SOC responsibility provision provide a complete statutory foundation for sustainability law in India (Tewari et al., 2021). The SEBI required the top 1,000 listed companies to submit business responsibility and sustainability report (BRS) report that focus on ESG disclosure beginning in fiscal year 2021–2022, even though Section 135 of the Company Law of 2013 required CSR to be 2% of the mean net profit of the preceding three financial years.

Sustainable development law is the expanding body of legal articles, treaties and standards that connect the three primary domains of global economic law, ENV law and SOC legislation. As acknowledged in M. C. Mehta V. Union of India (Taj Trapezium Case, 1996), the Principles of Sustainable Development promote ENV preservation and developmental objectives that will benefit future generations. Although there is still work to be done, India has been one of seven developing countries recognised globally for having sustainability index linked to their securities markets (Vives & Wadhwa, 2012).

The second section of the article reviews the existing literature for in-depth understanding and theoretical background, third section research gaps, fourth section research objectives, fifth section research methodology, sixth section research hypotheses, seventh section showcases descriptive statistics, correlation and regression analysis and the diagnostic tests, eighth section the study’s conclusions and implication and ninth section study limitations.

Literature Review and Hypotheses Development

ESG Disclosure and Firm Performance

The ESG and company performance have been shown to correlate in a number of studies (Brooks & Oikonomou, 2018). According to a recent Indian study, financial performance and ESG are significantly and directly correlated, suggesting that businesses with more effective environment and GOV can achieve higher profitability (Maji & Lohia 2023).

Environment, Social and Governance Disclosure and Operating Performance (ROA)

ENV disclosure scores include sustainability strategies that emphasise raising awareness about the creation and use of sustainable goods and services (Bektur & Arzova, 2022; Russo & Fouts 1997). Return of asset (ROA) and ENV performance are positively correlated. Additionally, King and Lenox (2002) came to the conclusion that ROA and ENV dimension are directly correlated. Crook et al. (2008) show that the SOC dimension of ESG significantly impact on operating performance (ROA). Likewise, Rodriguez-Fernandez (2016) showed a positive correlation between SOC policies and operating performance by recognising the positive experience between firm profitability and firm SOC practices. Garcia and Orsato (2020) indicate a negative link between firm performance and ESG rankings in developing countries. Based on this information, we propose the following hypotheses:

ESG Disclosure and Operating Performance (ROA)

The ESG disclosure score is used globally to identify ENV activities, SOC obligations and corporate GOV practices of corporations (Alareeni & Hamdan, 2020). Naeem et al. (2021) examine how firm performance is impacted by ESG performance and find a positive and significant relationship between firm value and profitability (ROA) in both individually and composite ESG score (Giannopoulos et al. 2022). A study using Norwegian firms shows that firm performance as determined by return on assets is negatively impacted by ESG metrics. Chung et al. (2023) studied how a company’s performance is affected by ESG disclosure under Hong Kong’s required disclosure framework. The study reveals a positive and significant relationship between the overall level of ESG disclosure and the firm operational performance. The following hypothesis is based on the discussion above:

Environment, Social and Governance Disclosure and Financial Performance (ROE)

There is a negative relationship between Turkish-listed companies’ financial performance and ENV disclosure (Saygili et al., 2022). However, a number of earlier research have shown that ENV variables have a negative correlation with profitability (Abdi et al., 2022; Ahmad et al., 2021; Alareeni & Hamdan, 2020; Duque-Grisales & Aguilera-Caracuel, 2021). The return on equity can be significantly decreased by GOV disclosure. On the other hand, according to a study done in the aviation industry, SOC disclosure has a beneficial impact on financial performance since it is closely linked to the operating and growth of the company (Abdi et al., 2022). Based on these considerations, we develop the following hypotheses:

ESG Disclosure and Financial Performance (ROE)

The results of empirical studies examining into the association between ESG disclosure and company performance are frequently contradictory and can be both positive and negative. Dalal and Thaker (2019) examined that ESG score had a positive impact on financial performance in 65 firms from 2015 to 2017. Landi and Sciarelli (2019) analysed 54 listed Italian companies from 2007 to 2015 and found a negative correlation between ESG scores and financial performance. Ahmad et al. (2021) showed a positive relationship between corporate financial performance (return of equity (ROE)) and ESG disclosure. De Lucia et al. (2020) examine a sample of 1038 public businesses from 22 European countries from 2018 to 2019, and found a positive correlation between ESG factors and financial performance (ROE). The following hypothesis is based on the information above:

Environment, Social and Governance Disclosure and Market-Based Performance (Tobin’s Q)

Several studies have revealed a correlation between particular ESG components and firm value. Lucas and Noordewier (2016) showed in their study that a company’s ENV efforts improve its firm performance by introducing the concept of “dirty industries.” Bhaskaran et al. (2020) investigated how ESG affected 4887 companies’ financial results between 2014 and 2018 and evaluated operational outcomes (ROE and ROA) and company value (Tobin’s Q) as dependent variables. Duque-Grisales and Aguilera-Caracue (2021) study results show an adverse relationship between firm performance and their ESG scores. The hypothesis presented below will be tested.

ESG Disclosure and Market-Based Performance (Tobin’s Q)

It’s interesting that the analysis shows a positive correlation between Tobin’s Q and ESG efforts. (Abdi et al., 2022) a global study covering the airline sector found a positive and significant association between ENV and SOC activities and the financial success as evaluated by Tobin’s Q. (Wong et al., 2020) examined at the relationship between ESG and firm value in developing nations and discovered that increasing ESG will decrease capital costs, which will raise a firm’s value (Tobin’s Q). Additionally, only the SOC component of ESG display a positive correlation with Tobin’s Q (Dumitrescu et al., 2020; Velte, 2017) discovered that ESG has a beneficial effect on German companies’ profitability (ROA) and firm value (Tobin’s Q). The following hypotheses will be examined:

Theoretical Background

There are several theories that can be used to examine how ESG disclosure affects corporate performance. Stakeholder theory, for instance, considers the various groups that businesses impact, including clients, vendors, local communities and creditors, and are applicable to organisational management and ethical business practices (Lin, 2018). Stakeholder theory is consistent with this ESG research because a company’s ESG practices will improve its management, satisfy different stakeholders and boost its bottom line (Freeman, 1994). The agency theory, which Jensen & Meckling (1976) established, is contradicts by the stakeholder theory, which claims that investing in ESG has no financial advantage as the corporation spends money on unproductive activities. Two fundamental pillars of the agency theory are (i) the link between principals and agents (ii) separation of ownership and management. Khan et al. (2013), on the one hand, showed the agent is more concerned with capturing chances in the short term. Transparency, therefore, increases with the amount of non-financial information disclosed. Because of this, there are contradictions of interest between the principles and the agent when two parties have very distinct needs.

ESG Disclosure Scores in Emerging Economies

International investors are interested in emerging economies due to their potential for rapid growth. But because of the extreme unpredictability of government policymaking, businesses functioning in this environment confront a wide range of difficulties on the fronts of the economy, politics, society and environment (Pollard et al., 2018). Companies are required to publish an ESG disclosure score that summarises their substantial ESG opportunities and threats. Proper reporting and scoring of ESG practices create trust and confidence among financial institutions, workers and investors. The meaning of the ESG disclosure score is becoming more uniform and easily comprehensible over time, which aids in assessing business risks and possibilities and risks and has a significant impact on their profitability. The ESG disclosure score is helpful in measuring productivity and profitability. The ESG disclosure score serves as a key factor in helping investors make the best decisions. Asset managers and investors need ESG disclosure scores to make investment decisions. ESG disclosure is crucial because stakeholders want to see vital ESG data from companies as transparent as their financial data. ESG disclosure scores help companies describe their management framework, policies and procedures relating to sustainability (Baudot et al., 2021). There is a strong need for ESG disclosure from companies since extractive and exploration activities in emerging economies are linked to unethical conduct, SOC unrest, unsafe working environments and corruption. Haji et al. (2022) observed that ESG policies and outcomes in emerging economies were more focused on welfare issues such as poverty reduction and human rights violations.

Research Gaps

It was found after review of literature that there are many conflicting findings in the literature and that it is still unclear how ESG and firm performance are related. A comprehensive picture has not yet emerged because most research focusses on the connection between disclosure and market value and financial performance, and some studies look at how ESG performance affects creditworthiness and the cost of capital. In contrast, studies that analyse the individual ESG pillars or concentrate on firm performance are few and highly confined to one or two areas. Prior research has mainly focused on the overall ESG performance, whereas not all aspects of ESG have been examined. However, some research has focused on the effects of all three ESG components on firm performance. But no research has shown how ESG disclosure impacts a firm operational, financial and market-based performance. The majority of research has been carried out primarily in Western economies, with relatively few studies being carried out in emerging economies such as India. As a result, in the majority of developing countries, researchers devote little or no effort to examining how ESG disclosure impacts corporate performance. This study examines the impact of ESG disclosure on firms’ market-based, operational and financial performance, as well as the relationships between them.

Research Objectives

This study aims to investigate how ESG disclosure scores impact a firm’s performance. The market-based, operational and financial performance have been measured using Tobin’s Q, ROA and ROE ratios respectively. The separate E, S and G disclosure scores have been computed and combined to provide the composite disclosure score.

Research Methodology

For the study, the following methodologies has been adopted:

Sample and Data Collection

The study’s sample consists of companies listed on the National Stock Exchange (NSE) of India. The sample size is selected by the judgemental sampling method. As a sample, the top hundred companies have been selected on the basis of market capitalisation. Five financial companies have been removed from the study’s purview due to the reason that not all of the ESG disclosures relate to these companies. After their removal, the sample consists of 95 companies. The sample companies’ annual reports, sustainability reports or ESG reports for the years 2020–2023 are used in this study. The COVID-19 pandemic and geopolitical caused significant market volatility throughout the study period of 2020–2023. The Ministry of Corporate Affairs issued national guidelines on responsible business conduct (NGRBC) Guidelines 2019 and with this SEBI increased the requirement for filing business responsibility report (BRR) report along with the annual report from 500 companies to 1000 companies. SEBI issued a statement in May 2021 making it mandatory for the top 1000 companies (based on market capitalisation) to submit the BRS report along with the annual report. We included this time period in our analysis to figure out the impact of all of this information on company performance. Content analysis has been utilised to gather data from their sustainability reports, ESG reports and annual reports. Companies’ financial information for the same time period have been extracted from the Prowess IQ database.

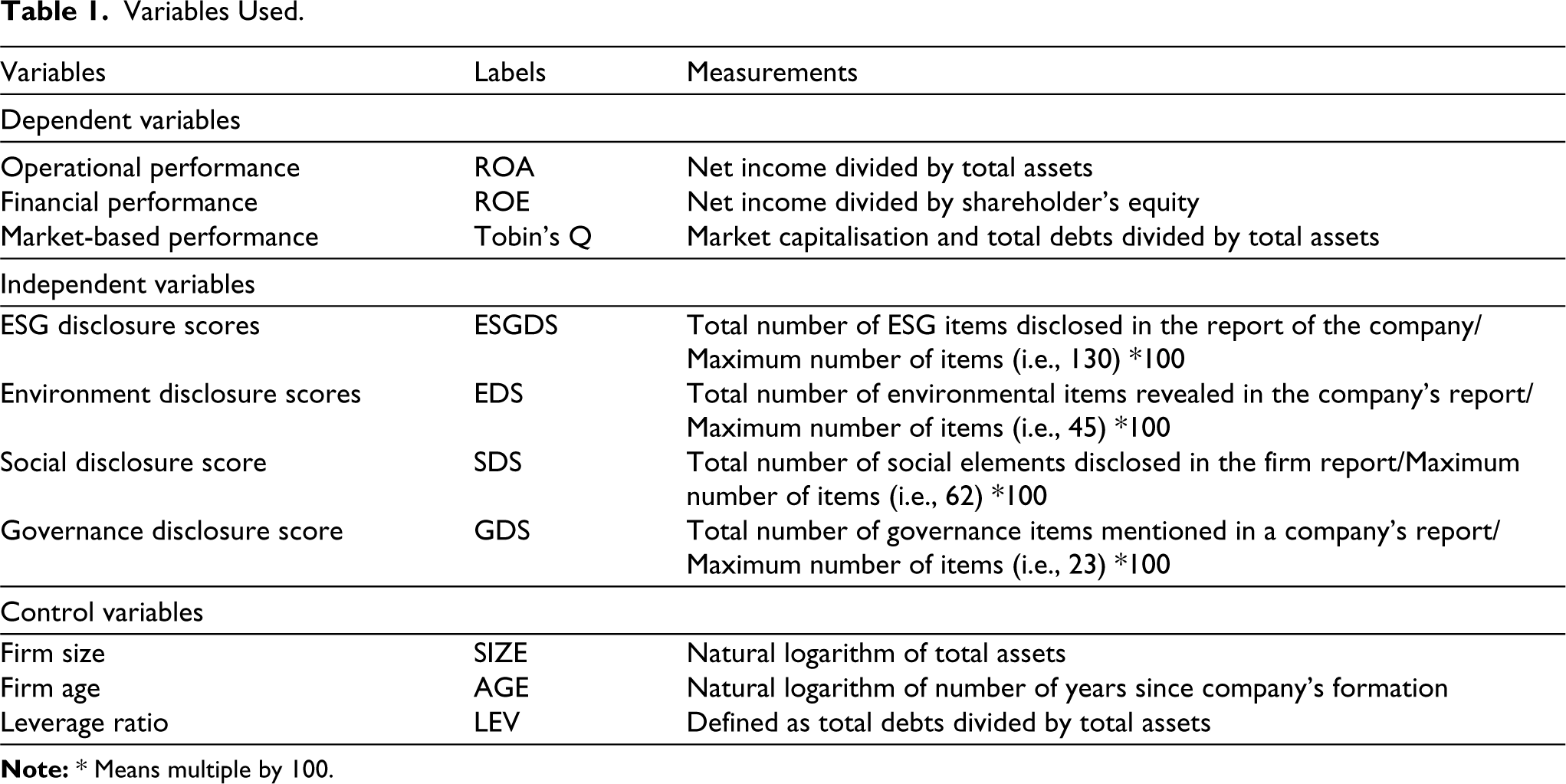

Variables

This study aims to create a model for multivariate regression. As dependent variables for market-based, operational and financial performance respectively Tobin’s Q, ROA and ROE ratios have been defined and ESG disclosure scores will be considered as independent variables.

Dependent Variables (Firm Performance)

Firm performance is assessed using the followings criteria—market-based, operational and financial performance. Tobin’s Q has been used to measure the market valuation of firm (Abdi et al., 2022; Alareeni & Hamdan, 2020; Chouaibi et al., 2022). ROA has been utilised to evaluate the company’s operational performance (AlDhaen, 2018; Buallay et al., 2017; Buallay & Al-Ajmi 2019) and the firm’s financial performance has been evaluated using ROE (Alareeni & Hamdan, 2020; Al-Faryan, 2021). ROA indicates how well the firm uses its assets to make profit, ROE represents how effectively the corporation uses the funds of its shareholders to make earnings and Tobin’s Q reveals how strongly the company uses all of its assets to create market value.

Independent Variables (ESG Disclosure Score)

The ESG disclosure score reflects firms’ fulfilment of ESG aspects. The data was based on 130 company-level ESG measures that were categorised into 10 parameters. The category scores were combined into three pillar scores, namely ESG. Aggarwal (2013), Aggarwal & Mehta (2013), Mir & Shah (2018), Dalal & Thaker (2019), Singhania & Saini (2022), Parikh et al., (2023) and Maji & Lahia (2023) were referred for use of such scores in their respective studies.

Control Variables

Our regression models additionally included size, age and leverage as control factors. A proxy for firm size is the natural logarithm of a company’s total assets (Abeyrathna et al., 2019; Hummel et al., 2016). The natural logarithm of the number of years since the company’s founding is used to calculate the firm age (Aboud & Diab; 2018; Abdi et al, 2022). Total debt divided by total assets yields leverage (LEV). This variable, which evaluates the possibility that a business will employ debt in its capital structure using tangible assets, is used to control the capital structure of enterprises (Opler & Titman, 1994; Surroca et al., 2010).

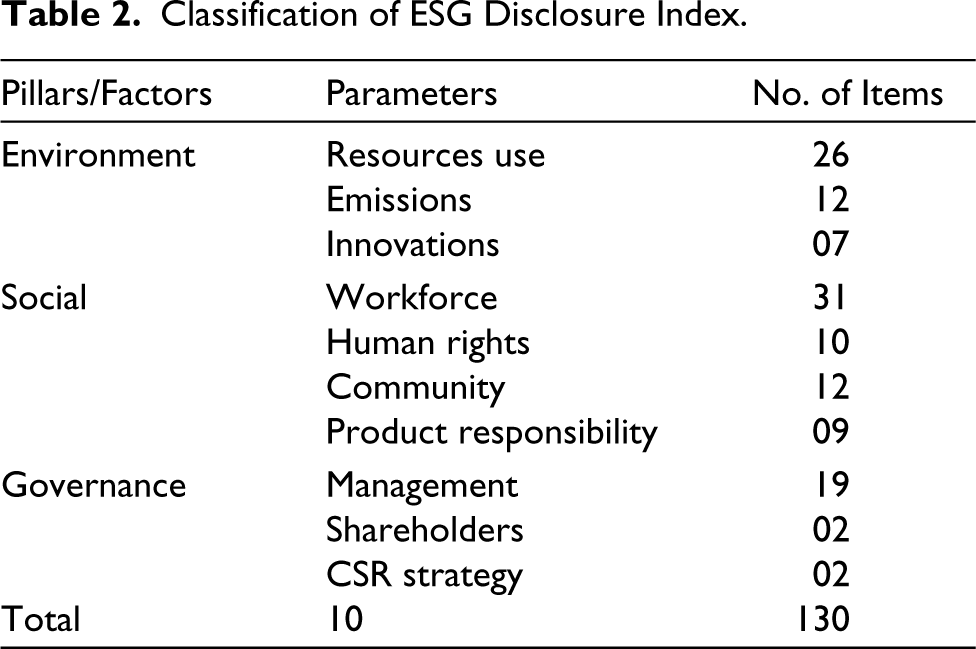

Construction of ESG Disclosure Index

The ESG parameters measured in this study are based on Thomson Reuters. Many authors have used the Thomson Reuters ESG Index such as Naeem et al. (2021); Nirino et al., (2019); Rajesh (2019); Garcia et al (2017) and Breuer and Nau (2014). Hence, this ESG disclosure index has been used in our study. Thomson Reuters provides index for the evaluation of ESG performances of firms based on 10 major parameters. ESG scores and distinct metrics for every component are examples of sustainability metrics found in Thomson Reuters Eikon. The annual reports of the company were analysed to explore the items with the help of content analysis. Content analysis is widely used by previous studies such as Montabon et al. (2007), Smith et al. (2007), Branco and Rodrigues (2008), Fauzi (2009), Rouf and Abdur (2011), Uwuigbe (2011), Clarkson et al., (2013), Kansal et al. (2014) and Nurhayati et al. (2015). Through content analysis parameters under various pillars, as shown in Table 2, were captured for their presence or absence.

Variables Used.

Classification of ESG Disclosure Index.

This study used the unweighted disclosure index in which the disclosure item is scored 1 (1) if this particular item is disclosed in the report of company and zero (0) if this item is not disclosed (Kansal & Singh, 2012). Once the disclosure index scores have been assigned, the total number of companies that disclosed the item has been determined and transformed into percentage terms.

Panel Regression Model

This study relies on the panel data regression analysis to estimate the impact of ESG disclosure score on firm performance. Three models are used to test the hypotheses of the study which have been shown below:

i = Number of companies (i.e., 95) ε = Error term, t = Time period (i.e., 2020 to 2023).

Results and Discussions

In this study, the secondary data of 95 companies have been used for the period of four years from 2020 to 2023. This section presents the specific findings from the regression analysis, model specification tests, correlation matrix and descriptive statistics.

Descriptive Statistics

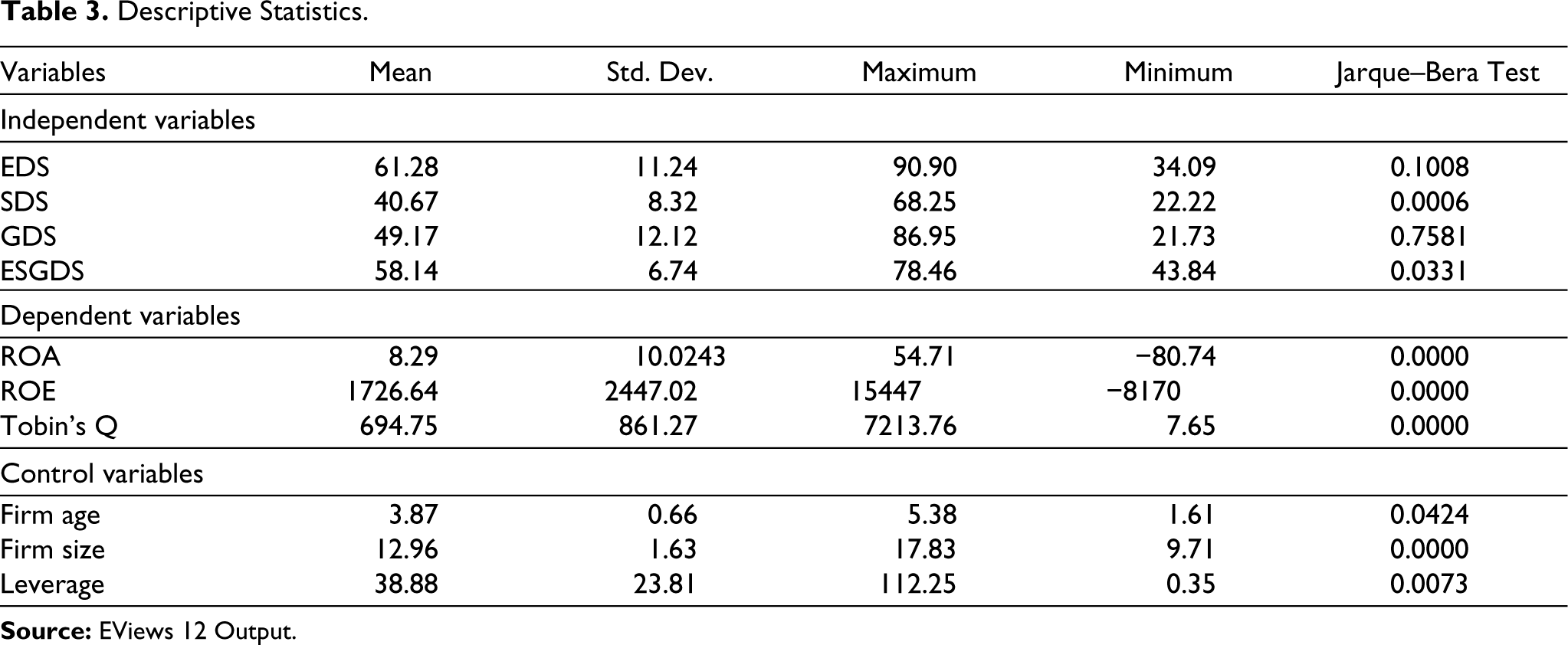

The statistical results for every variable are shown in Table 3.

Descriptive Statistics.

The mean value of ESG disclosure was 58%, with a minimum disclosure of 44% and a maximum of 78%. Additionally, the mean of environment disclosure was 61%, with a minimum disclosure of 34% and a maximum of 91%. On the other hand, the mean of SOC and GOV disclosure was 41 and 49% with a minimum disclosure of 22% each and a maximum of 68 and 86% respectively. This shows that there is wide variation in disclosure score of environment and GOV. Further, disclosure on SOC aspect is less as compared to other parameters of ESG. The data’s normality is assessed using the Jarque–Bera test. Since the P value is less than .05, it can be concluded that the almost variables are not distributed normally.

Correlation Matrix

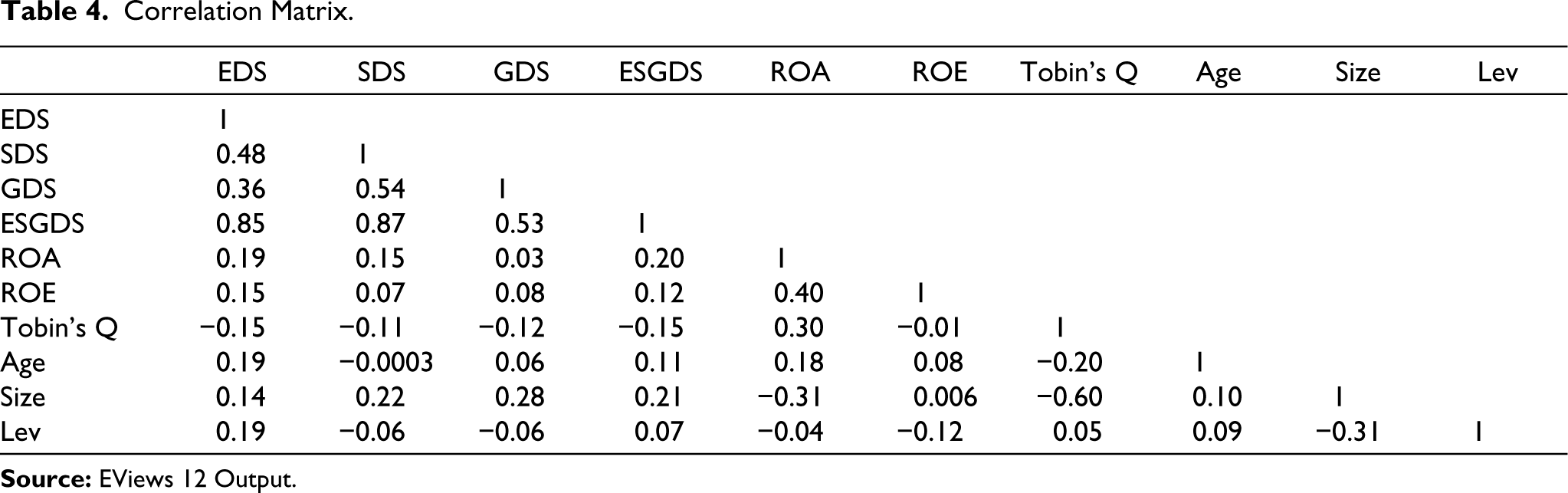

The results of correlation have been shown in Table 4. It is useful to show the correlation between all of the independent, dependent and controlling variables.

Correlation Matrix.

All independent variables, in general, have a positive correlation with all dependent variables except Tobin’s Q. Multicollinearity is demonstrated by the variables with correlation values more than 90%. Therefore, regression analysis shouldn’t use these variables to avoid the multicollinearity problem (Shah & Afridi, 2015). According to the findings, the firm age and ROE have the lowest correlation (0.0003) and the ESGDS and SOCDS have the highest correlation (0.85) and (0.87). Additionally, the results showed that there is no multicollinearity because all of the variables have correlation values less than 90%.

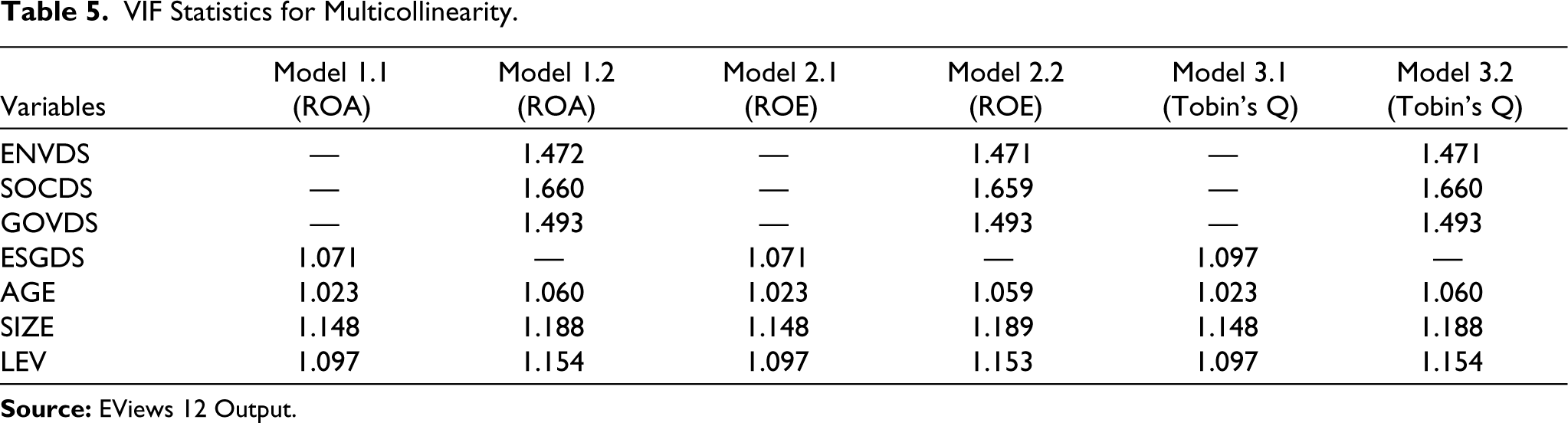

Tests for Multicollinearity

The multicollinearity is verified using the correlation matrix and the variance inflation factor (VIF). Table 5 provides the VIF findings for each model. According to Gujrati (2005), there may be a multicollinearity issue if the VIF value is greater than 5. According to the results, there was no multicollinearity among the variables since the values of every variable in the different models were less than 5.

VIF Statistics for Multicollinearity.

Model Specification

Three panel approaches—poised ordinary least squares (OLS), fixed-effect (FEM) and random-effect models (REMs)—are used in the study’s panel data regression to forecast the factors influencing ESG disclosure scores. After applying pooled OLS, breusch-pagan lagrange multiplier (BPLM) test is applied to choose between pooled OLS or FEM/REM. If the P value of the BPLM is less than .05, pooled OLS will not be used. The P value of BPLM test in all models is .00, hence Finally, it is determined that pooled OLS test is not appropriate for panel data regression. The Hausman test is used to decide between the FEM and the REM (Greene, 2008). When P values are significant, FEMs are applied; otherwise, a REM ought to be used (Klarner, 2010). The FEM was adopted since the Hausman test resulted in a P value less than .05. The results showed that all of the models had significant P values for operating performance (ROA), financial performance (ROE) and market-based performance (Tobin’s Q), confirming that the FEM is the best fit for panel data regression analysis.

Regression Results of ESG and Firm Performance

Impact of Individual Environment, Social, Governance and Overall ESG Disclosure Score on Operational Performance (ROA)

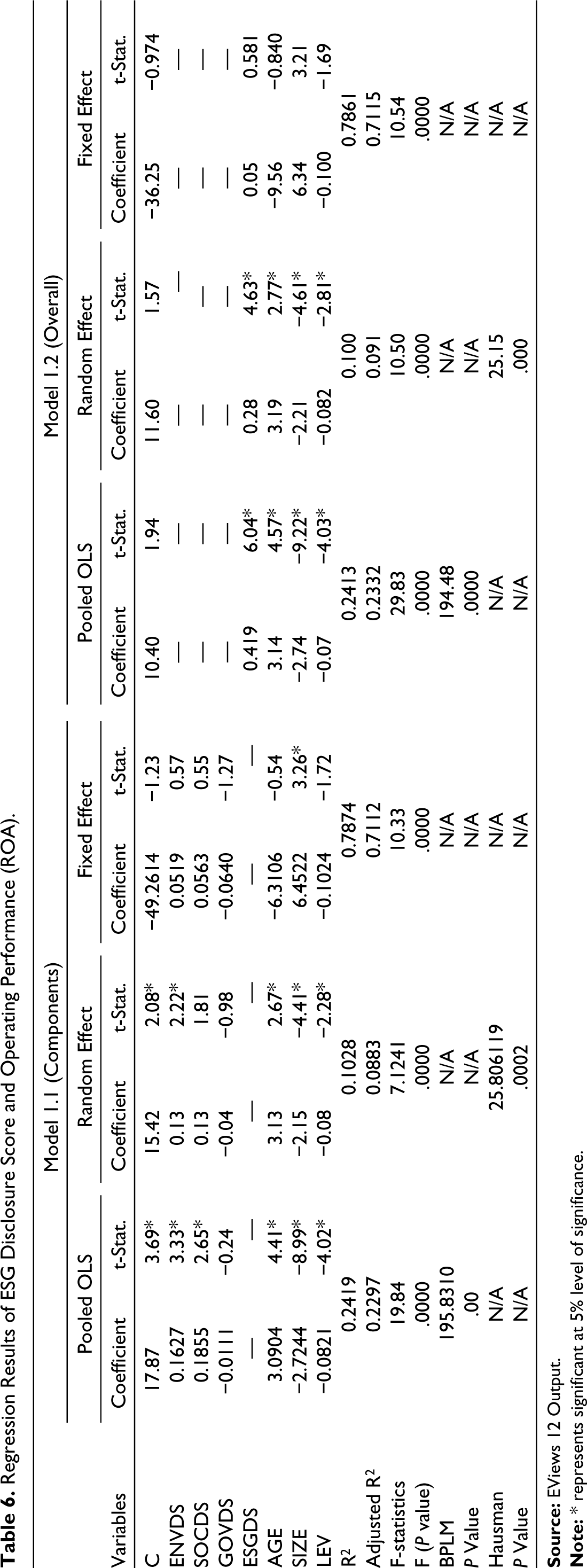

Tables 6 shows the results of the pooled OLS, REM and FEM, which used ROA as a proxy for operating performance.

It is found for Model 1.1 and 1.2 from pooled OLS that model is significant (significant F value) but poor explanatory power (low adjusted R2 value). Significant BPLM test value led to the estimation of REM which resulted into a significant model but even lower explanatory power. Significant Hausman test results led to the estimation of FEM. Hence, results of FEM are discussed in detail.

Application of FEM 1.1 for components of ESG disclosure found that the F-statistic is 10.33 with a P value of .00 and adjusted R2 value is 0.7112. Thus, the model is a good fit at 5% level of significance and is able to explain 71.12% variations is ROA. The individual ENV and SOC disclosure scores have insignificant positive impact on ROA, whereas the impact of individual GOV disclosure scores on ROA is insignificantly negative. Furthermore, results verified that operating performance is insignificantly and negatively impacted by control variables like firm age and leverage and significantly positively impacted by firm size.

Regression Results of ESG Disclosure Score and Operating Performance (ROA).

Application of FEM 1.2 using overall ESG disclosure score found that the F-statistic is 10.54 with a P value of .00 and adjusted R2 value is 0.7115 respectively. Therefore, at the 5% level of significance, the model fits well and is responsible for 71.15% of the changes in ROA. The overall ESG score has a significant positive impact on ROA. Furthermore, results verified that operating performance is significantly impacted negatively by control variables like firm size and leverage and insignificantly positively impacted by firm size.

Impact of Individual Environment, Social, Governance and Overall ESG Disclosure Score on Financial Performance (ROE)

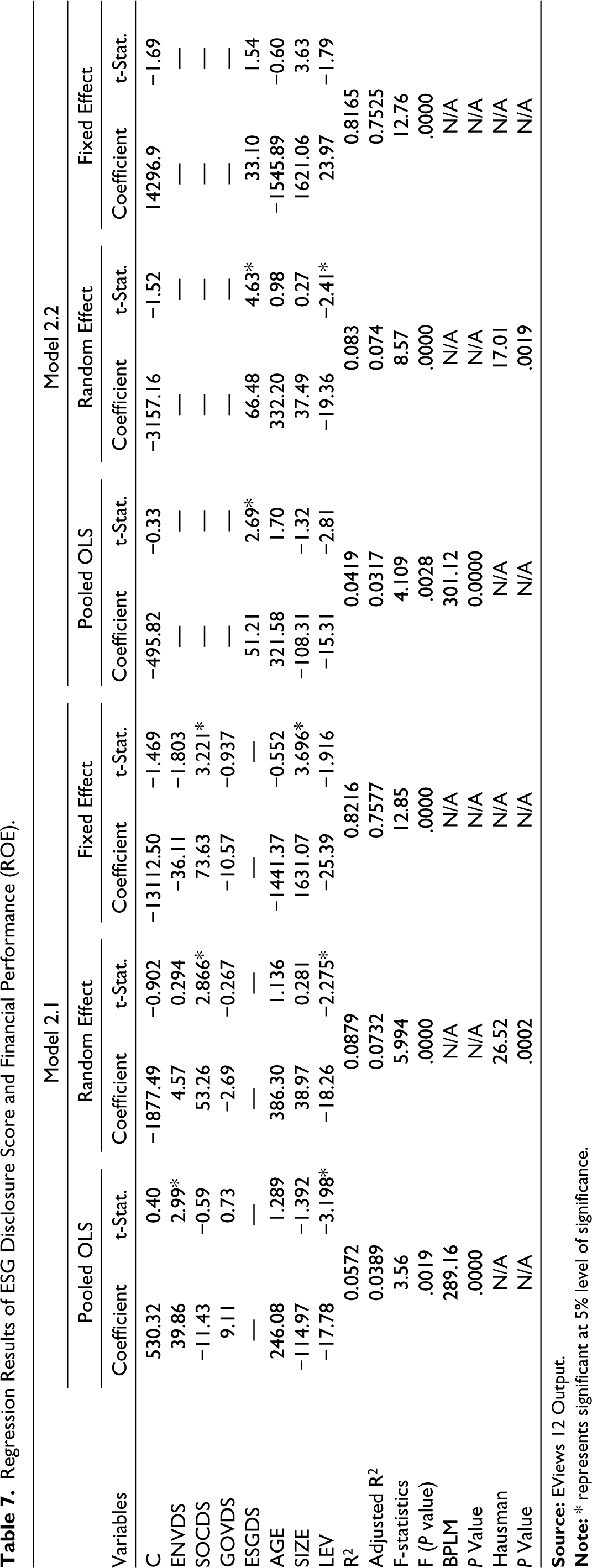

Tables 7 displays the results of the pooled OLS, REM and FEM, which used ROE as a proxy for financial performance.

It is found for Model 2.1 and 2.2 from pooled OLS that model is significant (significant F value) but poor explanatory power (low adjusted R2 value). Significant BPLM test value led to the estimation of REM which resulted into a significant model but even lower explanatory power. Significant Hausman test results led to the estimation of FEM. Hence, results of FEM are discussed in detail.

Application of FEM 2.1 for components of ESG disclosure found that the F-statistic is 12.85 with a P value of .00 and adjusted R2 value is 0.7557. Thus, the model can explain 75.57% of the changes in ROE and correlates good at the 5% level of significance. The individual ENV and GOV disclosure scores have insignificant negative impact on ROE (financial performance), whereas the impact of individual SOC disclosure score on ROE is insignificantly positive. Furthermore, results verified that operating performance is insignificantly and negatively impacted by control variables like firm age and leverage. On the other hand, the only control variable that significantly impacts ROE is firm size.

Application of FEM 2.2 using overall ESG disclosure score found that the F-statistic is 12.76 with a P value of .00 and adjusted R2 value is 0.7525 respectively. As a result, the model can account for 75.25% of fluctuations in ROE and fits well at the 5% level of significance. ROE is significantly positively impacted by the overall ESG score. The findings additionally showed that operating performance is negatively impacted by control variables like firm size and leverage. However, firm age is a single control variable with a significant impact on ROE.

Impact of Individual Environment, Social, Governance and Overall ESG Disclosure Score on Market-Based Performance Tobin’s Q)

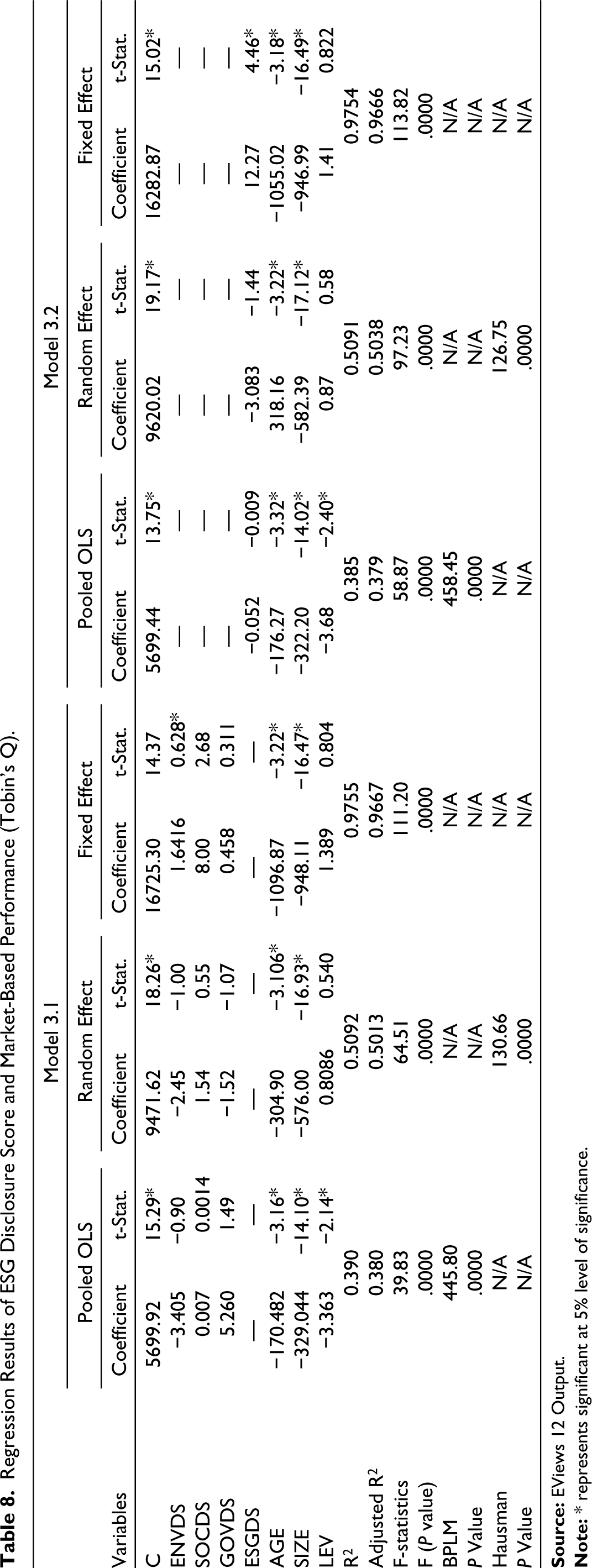

The outcomes of the FEM, REMs and pooled OLS models are displayed in Table 8. The outcomes of the FEMs, REM and pooled OLS models are displayed in Table 8. These models use the Hausman test and BPLM for regression analysis, and Tobin’s Q as a proxy for market-based performance.

It is found for Model 3.1 and 3.2 from pooled OLS that model is significant (significant F value) but poor explanatory power (low adjusted R2 value). Significant BPLM test value led to the estimation of REM which resulted into a significant model but even lower explanatory power. Significant Hausman test results led to the estimation of FEM. Hence, results of FEM are discussed in detail.

Application of FEM 1.1 for components of ESG disclosure found that the F-statistic is 111.20 with a P value of .00 and adjusted R2 value is 0.96.67. Thus, the model is a good fit at 5% level of significance and is able to explain 96.67% variations is Tobin’s Q. The individual ENV disclosure score has significant negative impact on Tobin’s Q, whereas the impact of individual SOC and GOV disclosure scores on Tobin’s Q is insignificantly positive. Furthermore, results verified that operating performance is significantly and negatively impacted by control variables like firm age and size. On the other hand, the control variable that insignificantly and positively impacts Tobin’s Q is firm leverage.

Application of FEM 1.2 using overall ESG disclosure score found that the F-statistic is 113.82 with a P value of .00 and adjusted R2 value is 0.9667 respectively. As an outcome, the model can explain 96.67% of swings in Tobin’s Q and fit good at the 5% level of significance. Tobin’s Q is significantly positively influenced by the overall ESG score (market-based performance). Furthermore, results verified that operating performance is significantly impacted negatively by control variables like firm size and age. On the other hand, the control variable that insignificantly and positively impacts Tobin’s Q is leverage.

Conclusion and Implication

The objective of this study is to ascertain how the company’s performance is affected by both the overall and individual ESG disclosure scores. The study is quantitative in nature and is based on 380 observations from panel data analysis of 95 firms listed on the NSE during a period of four years from 2020 to 2023. The firm’s performance was measured by the study using three proxies: operating performance (ROA), financial performance (ROE) and market-based performance (Tobin’s Q). Additionally, the study calculated the individual ESG scores as well as the overall ESG scores to evaluate the performance of the firm. These scores were calculated using content analysis of annual reports of the sample firms.

Regression Results of ESG Disclosure Score and Financial Performance (ROE).

Regression Results of ESG Disclosure Score and Market-Based Performance (Tobin’s Q).

The outcomes of the FEM revealed that, in accordance with the first proxy’s results, or ROA, pillar-wise ENV, SOC disclosure and aggregate ESG scores were positively associated with ROA but not statistically significant. On the other hand, there was a negative but statistically insignificant correlation between ROA and GOV disclosure scores. Similarly, research by Bătae et al., (2021), Menicucci & Paolucci (2022), Duque-Grisales & Aguilera-Caracuel (2021) and Bahadori et al. (2021) also showed the negative impact of GOV disclosure on ROA.

The results of the second proxy showed that SOC disclosure score had a positive and statistically significant impact with ROE in the FEM. Furthermore, there was a negative correlation between ROE and the scores for ENV and GOV, although this relationship was not statistically significant. These researchers presented opposite results in their studies (Ahmed et al., 2021; Maji & Lohia, 2022; Mardini, 2022; Saygili et al., 2022). Conversely, ROE and the overall ESG disclosure score had an insignificant but positive relationship. Similarly, studies by Bahadori et al. (2021) and Grisales & Aguilera-Caracuel (2021) revealed the positive impact on ROE.

The results of the third proxy showed that ENV disclosure score had a positive and statistically significant relationship with Tobin’s Q in the FEM. Those findings are consistent with previous research (Bahadori et al., 2021; Bătae et al., 2021; Buallay, 2020; Maji & Lohia, 2022; Mardini, 2022). Additionally, Tobin’s Q and the SOC and GOV score were positively correlated; however, this correlation was not statistically significant. This result is contrary of these researchers (Ahmed et al., 2021; Alareni & Hamdan, 2020). However, the results from the point of view of GOV disclosure are supported by previous studies (Ahmed et al., 2021; Maji & Lohia, 2022; Mardini, 2022; Saigili et al., 2022). In contrast, Tobin’s Q and the total ESG disclosure score showed a strong and positive association. These findings adverse with previous studies (Aureli et al., 2020; Bin Khidmat et al., 2020; El Khoury et al., 2021; Jibril et al., 2022; Manita et al., 2018).

Additionally, the results of the FEM demonstrated that the control variables, firm age and leverage, are negatively and marginally impacted by ROA and ROE. On the other hand, the single factor that significantly impacts ROA and ROE is firm size. Tobin’s Q is significantly and negatively impacted on the control variable (firm size and firm age). However, Tobin’s Q is an insignificantly and positively impacted on the leverage.

Theoretical and Practical Implications

The findings provide theoretical and practical implications. At first, the results of this study can be used by regulators and policymakers to develop appropriate policies and regulations that will promote ESG practices and reporting among Indian companies. With most data indicating a negative relationship between ESG disclosure and business performance, changes to the relevant laws and regulations as well as the ESG implementation guidelines are required. Similarly, this study can be useful to regulators and policymakers in other developing nations, especially those that have not yet required their firms to report and discharge ESG activities. It can help them develop criteria for their companies to follow. The study’s conclusions can also be used by domestic and foreign investors to help them make prudent financial decisions that will increase their wealth. Managers need to consider ESG as an investment rather than an expense. Investors, as well as other stakeholder groups like regulators, legislators and SOC stakeholders like community organisations, would profit from favourable value advantages of ESG operations in this unstable corporate climate.

Managerial and Social Implications

These findings can be used by managers to assess the relationship between ESG disclosure scores and company performance, enabling them to decide whether to give preference to individual or combined ESG scores. When building their portfolios, fund managers can include these results into their investment decisions when it comes to ESG-focused funds. The positive impact of ESG suggests that it is possible to incorporate ESG practices into a company’s business planning. Firms will have a higher SOC standing if they reveal their ESG practices since different stakeholder groups will find their goods and services appealing and advantageous. For company managers who are interested in ESG strategies, our findings offer insightful information. Policy authorities may find the study’s findings helpful in developing guidelines or rules and in further refining the ESG framework.

Limitations

There are a number of limitations to this study. The first constraints related to secondary data. Future researchers could conduct a qualitative investigation involving interviews with businesses that have made their ESG disclosures. Second, we limited our analysis and examination to 95 listed Indian firms whose ESG disclosure scores are determined by the self. Therefore, future research may consider larger sample sizes as data. Other industries like financial or non-financial businesses listed in NSE may be the subject of future research. Also, comparative study of different areas can be done. Third, the research used a sample of only Indian listed companies. Therefore, the study can be expanded to cover more countries, especially developing countries. The fourth limitation is that the focus is on firm performance-related variables that are affected by ESG disclosures, including financial (ROE), operating (ROA) and market-based (Tobin’s Q). Additional variables like profitability, performance, company value and corporate SOC responsibility may be used in future studies.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.