Abstract

Purpose:

This article aims to examine the impact of different corporate social responsibility (CSR) expenditures on the reputation of a company.

Design/methodology/approach:

The article develops four hypotheses that are tested empirically through the Panel Corrected Standard Error model (PCSE). The study constitutes a sample of 100 Indian BSE-listed companies between 2015 and 2020.

Findings:

The findings provide an interesting observation about the relationship shared between CSR expenditure and its impact on the reputation of a company. Also, from the context of the triple bottom line (TBL), when CSR expenditure was segregated into economic, social, and environmental expenses it was found that only social expenditure impacts reputation significantly.

Managerial implications:

The companies’ priority should be to practice CSR with the motive of benefiting society. Parallel to this, the company may find the right balance of resource allocation for spending in CSR activities that might help the company achieve a higher reputational position.

Originality/value:

As per the authors’ knowledge, there is scarce literature exploring the relationship between CSR expenditure and corporate reputation in emerging markets like India. This research is integral as it would encourage companies to integrate CSR expenditures into their business strategy in such a way that it may give a boost to their current reputation status and bring along with itself many benefits to the company as discussed in the literature. This article is incremental to the existing literature by examining these topics in an emerging country. This exploration provides a glance into the present scenario of an emerging economy.

Keywords

Introduction

Corporate social responsibility (CSR) is a global practice which instils a sense of sustainable living in companies. Demands of the stakeholders are not restricted to just the products or services of a company but have gone beyond that toward social behavior and performance. The social performances of companies are judged by the information disclosed in the social reports. In India, CSR is mandatory (under Section 135 of the Indian Companies Act, 2013) for companies with a net worth of ₹500 crore or more, or a turnover of ₹100 crore or more, or a net profit of ₹5 crore or more during the immediately preceding financial year. These companies are required to spend 2% of their profits on CSR expenses. This information is disclosed by the companies in the form of social reports.

In recent years, companies are using their CSR practices as a strategy to meet stakeholders’ demands. CSR practices help companies in increasing their financial performance (FP), employee commitment (Harvey & Schaefer, 2001), and competitive advantage (Melo & Garrido-Morgado, 2012). CSR leads to customer satisfaction (Maden et al., 2012), increases purchase intentions of customers (Creyer, 1997), enhances brand loyalty of customers (Maignan et al., 1997), and creates more sympathy and lowers anger toward the company (Assiouras, 2011). CSR acts as an insurance agent helping in warding off negative effects against the company (Godfrey et al., 2009), generating higher company goodwill (Orlitzky et al., 2003) and increases the chances of companies’ being better identified among their stakeholders leading to reputation building.

Reputation can be understood as a continuous cumulative assessment of outsiders’ views of the company. It is the view that reflects how well the company executes its commitments and fulfills its stakeholder’s expectations along with maintaining its performance according to the social-political environment (Siltaoja, 2006). Reputation is an invisible asset of the company that possesses many benefits like increased profitability, allows companies to charge premium prices for their offerings, has the ability to attract and retain customers and investors and provides enhanced access to the global markets (Fombrun & Shanley, 1990; Roberts & Dowling, 2002). It is due to all these beneficial features of reputation, it is often considered one of the most integral intangible assets of the company which the company needs to nurture and maintain carefully.

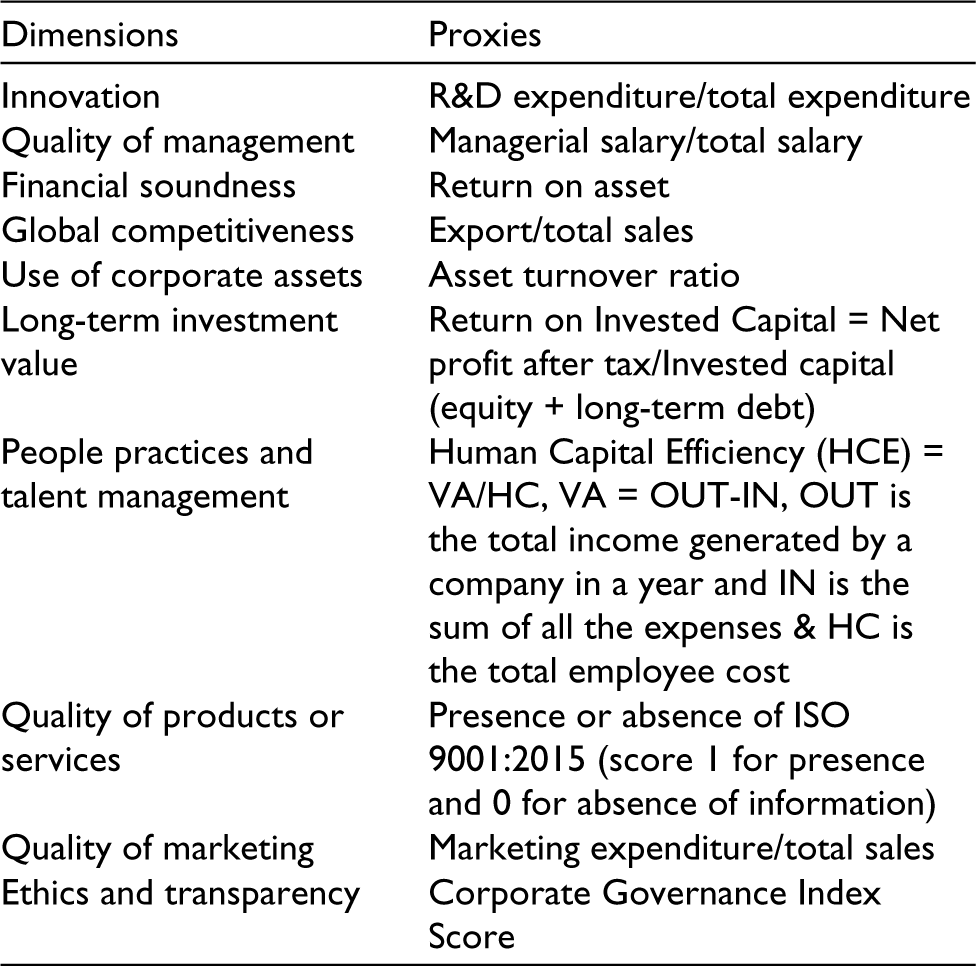

In our analysis, we use total CSR expenditure along with the various components of CSR expenditure made by a company to investigate the impact on reputation. CSR expenses of the companies are segregated into three categories (Hidayati, 2011; Trihermanto & Nainggolan, 2019) which is based on the triple bottom line (TBL) approach whereas reputation on is scored from 10 different dimensions namely innovation, use of corporate assets, long-term investment value, financial soundness, quality of management, quality of product and services, ethics and transparency, use of corporate assets, global competitiveness, and people practices and talent management. This methodology is adopted from Baruah and Panda (2020)which is not only captures the perception of all the stakeholders reputation comprehensively but also in a more objective in manner.

This article aims to investigate the least explored topics of CSR expenditure and reputation. Although there has been some research on CSR and reputation (Johnson et al., 2018; Melo & Garrido-Morgado, 2012; Odriozola & Baraibar-diez, 2017; Zhu et al., 2014), there is sparse literature on the relationship between CSR expenditure and reputation, especially in the Indian context. Therefore, this study will enhance the existing literature on CSR and reputation in the context of emerging markets, especially from the angle of the relationship between CSR expenditure and reputation. Additionally, previous research on the topic was conducted in a developed setting (Melo & Garrido-Morgado, 2012; Odriozola & Baraibar-diez, 2017) which makes it imperative to explore these issues in an emerging country context. The background that India has recently mandatorily implemented CSR enriches the contribution of this study in understanding how Indian firms implement and spend on CSR activities and their impact on their reputation.

The first section of this article discusses the theoretical background along with the understanding previous literature in the field. Followed by this second section encapsulates the description of our main variables along with the control variables, sample selection process followed by the methodology adopted. Finally, empirical findings are presented along with a discussion of the findings and limitations. The future scope of research in the area is presented at the last.

Literature Review

The nexus between CSR and reputation can be understood from a number of theories. Agency theory discusses about information asymmetry between a company and its various stakeholders (Clarkson et al., 2008; Martínez-Ferrero et al., 2016). CSR practices of the company, when disclosed by the company, act as asymmetries reducing agents and in turn, enhance the reputation of the company. Legitimacy theory opinionates that the CSR activities of the company serves as evidence to the legitimacy of a company as a good corporate citizen. The amalgamation of agency theory and legitimacy theory leads to another theory, that is, Stakeholder theory (Odriozola & Baraibar-diez, 2017). This theory propounds the need for extending the vision of the management of a company from being limited to only profit maximization to working for the interest of the various stakeholders of the company. Therefore, CSR is an instrument of a company that deals with the expectations of the stakeholders and society as a whole. Corporate reputation on the other hand may be thought of as a result of the perceptual evaluation of the stakeholders that arise from their evaluation of the CSR activities of the company (Smaiziene & Jucevicius, 2009). Social responsibility is a multifaceted concept that possesses multiple criteria (Harrison & Freeman, 1999) and changes over time (Mitchell et al., 1997). The extent social responsibilities are framed within the context of organizations’ relationship with their respective stakeholders thus is a crucial factor in determining their reputation value (Neville et al., 2005). Further support may be drawn from the Signaling theory where CSR activities act as signals sent out by a company in the form of information to its stakeholders by which a company can avoid information asymmetry.

Reputation is the stakeholders’ evaluation of the credibility of a firm’s projection (Neville et al., 2005) and CSR activities have an influence on these evaluations through marketing efforts such as corporate communications, reputation building, and branding. CSR influences the perceptions of the stakeholders through the information conveyed through mass media and interpersonal communication. Various empirical research has supported this relationship by stating that CSR activities contribute to stakeholders’ willingness to associate with the company actively participating in these activities along with companies enjoying a strong customer loyalty base leading to favorable assessment of the company (Axjonow et al., 2016). CSR is considered an important component of reputation-building (Johnson et al., 2018). CSR is believed to bring with it many benefits to the company like increased FP (Garg & Gupta, 2020), employee commitment (Johnson et al., 2018), and competitive advantage (Melo & Garrido-Morgado, 2012). CSR increases customer satisfaction (Maden et al., 2012), purchase intentions (Creyer et al., 1997) and brand loyalty (Maignan et al., 1997). CSR activities lead to customers sympathizing with the company and minimize anger in the minds of the stakeholders (Assiouras, 2011). CSR also acts as an insurance agent shielding a company against negative attention (Godfrey et al., 2009) along with creating higher goodwill for the company (Orlitzky et al., 2003). CSR activities influence the firm’s marketing efforts such as corporate communication, branding, and reputation-building (Pradhan, 2016). Therefore, reputation is the justification for the various CSR practices of the company with the belief that CSR improves a firm’s image and strengthens the brand (Porter & Kramer, 2006). A good reputation acts as a competitive advantage giving firms the ability to attract investors easily, gain access to capital markets, charge premium prices, and have improved credit ratings (Fombrun, 1996).

This study is an attempt to delve deeper into this notion of CSR expenditure impacting reputation. To explore further the relationship is investigated and analyzed empirically and a suitable conclusion is attained at the end. Based on the underlying theories and the empirical studies in the field we move with the assumption that different expenditure of CSR significantly impacts the reputation of the company differently.

H1: CSR expenses of Indian companies significantly impact their reputation.

Further, we segregate CSR expenditure into three broad groups, that is, economic, social, and environmental expenses (following the TBL approach). The Global Reporting Initiative (2001) pointed out the main dimensions of CSR or the TBL. The first dimension is the economy. Under this dimension, CSR activities should indulge more in new measurements of wealth (HRD, R&D, and intellectual capital developed by the company) than just traditional financial accountancy. This can also be done by reducing business costs through an appropriate business integrity policy, increasing employees’ productivity by conducting pieces of training and various other approaches under HRD.

The second dimension is the environment. This means that CSR should be based on a thorough study of the implications of resource and energy usage, and the company’s effect on the integrity of the environment. This can be achieved through proper environmental policy and audit, and environmental responsibility management programs.

The third dimension is social. In this dimension, CSR should aim toward maximizing the positive influence of the company’s existence on a wider community. Concentration should be on topics like community health problems, social justice, and inter- and intra-organizational justice (Hidayati, 2011).

The economic, social, and environmental responsibilities which are also known as the “Triple Bottom Line” altogether, are considered a systematic approach to managing a company’s responsibility. In simpler terms, it is a measuring frame and company’s report on its economic, social, and environmental performance whereas, in a wider sense, the term is applied to hold the process done by the company to maximize the positive influence of its activities and generate additional economic, social and environmental values (Hidayati, 2011).

Therefore, companies have started to realize that greater social and environmental responsibilities can lead to higher firm performance. Social and environmental responsibilities like contributing to communities, charitable giving, improving workplace conditions, eliminating waste, and using efficient resources (Trihermanto & Nainggolan, 2019).

Therefore, based on the above notions we formulated the following hypotheses:

H2: CSR economic expenses of Indian companies significantly impact their reputation. H3: CSR social expenses of Indian companies significantly impact their reputation. H4: CSR environmental expenses of Indian companies significantly impact their reputation.

Therefore, a humble attempt has been made to investigate the impact of different components of CSR expenditure on reputation empirically. It was found in the literature review that earlier literature viewed CSR from a wider angle and considered companies as social institutions. Over time due to the advent of sustainability and the TBL CSR as a broad concept got narrowed down to fewer aspects. In the context of India, the new Companies Act, 2013 has clearly defined CSR, especially in terms of the mandatory amount of spending and the possible areas of spending in the name of CSR activities of the company. Whereas on the other hand, reputation is an extensive concept concerning various perceptions of all stakeholders. Deriving reputation by focusing on only one group of stakeholders or measuring the multifaceted concept of reputation from only one dimension of reputation disregards the other stakeholders and other dimensions of reputation. Disregarding these aspects may not represent reputation in its true nature (Fombrun & Shanley, 1990; Moser & Martin, 2012). Therefore, we have tried to capture reputation in a concrete and objective form representing the perspectives of all possible stakeholders of a company while conducting the study of the impact of different CSR expenditures on the reputation of a company.

Research Design

Measure for Corporate Reputation

Many empirical studies have tried to capture reputation. Different studies have used different methods and measures techniques of reputation (Brammer & Millington, 2004; Chun, 2005; Fombrun & Shanley, 1990; Kanto et al., 2016; Melo & Garrido-Morgado, 2012; Sánchez & Sotorrío, 2007; Zhang & Schwaiger, 2009); we use reputation which is computed by following the works of Baruah and Panda (2020). The score is computed using appropriate proxies for different dimensions. These dimensions are adopted from the most widely used technique of most admired companies survey by Fortune magazine with some additional items from other ranking measures making it a more comprehensive and robust measure. All these dimensions along with their appropriate proxies are explained below.

The values obtained on these 10 different dimensions are converted into a single composite score as indicated below by creating an equally weighted average which provides us the measure of the corporate reputation of a particular company.

Where CRS = corporate reputation score and V1, V2, V3……Vn are the parameters used in the model and n is the number of parameters.

Measure for CSR

Under Section 135 of the Companies Act, 2013, reporting CSR activities was made mandatory. Schedule VII of the section mentions the activities where the company may spend as CSR expenditure. In our analysis, we use the total CSR expenditure made by a company along with various CSR expenditures made by the company to investigate the impact of different components of CSR expenditure on reputation. For the purpose of the study, we have focused on the TBL, the accounting framework that consists of three major parts. They are social, environmental and economic. Based on TBL we have classified the CSR expenses of the companies into social expense, environmental expense and economic expense. For measuring CSR expenses in quantitative terms we have followed the works of (Hidayati, 2011; Trihermanto & Nainggolan, 2019). Based on this literature, part of CSR expenditure is considered CSR economic expenses if the company states its CSR spending on business partnerships, community development, and infrastructural projects. CSR is CSR social expense when a company makes CSR spending on activities like education, charitable philanthropy, and social contributions. Finally, CSR is taken as CSR environmental expenses if the company spends on the conservation of nature and environmental protection activities.

Control Variables

The relationship between CSR and CR can be affected by other factors. It was found in the literature that previous studies have used certain control variables. This can be traced back to the seminal work of Fombrun and Shanley (1990). For the selection of control variables, we have followed the approach of studies that are conducted in an emerging country setting (Mishra & Suar, 2010; Muller & Kolk, 2009; Wang et al., 2011; Zhu et al., 2014). Hence, in this study four control variables are employed namely; firm size (FS), FP, firm age, and market risk (MR). FS is captured as the natural log of market capitalization (Dang et al., 2018). This measure will aptly represent FS as large funds have a larger market share thereby having more visibility than small firms. This tends to stakeholders remember a large company more easily than a smaller one (Brammer & Pavelin, 2006; Fombrun & Shanley, 1990). FP is measured as the ratio of market to book value (Brammer & Pavelin, 2006; Fombrun & Shanley, 1990; Roberts & Dowling, 2002). This ratio captures the beneficial effects of high-performing firms more easily. Stakeholders show a favorable attitude toward financially successful firms. Reputation can be considered as an accumulation of stakeholders’ perspectives over the years (Baruah & Panda, 2020). The older a company gets the higher might be the reputational status. On the other hand, the opposite might be the scenario where reputation over the years may be positive, negative, or a combination of both. The firm’s age as a control variable is calculated by the number of years between the date of incorporation of the firm and the date of the study (Zhu et al., 2014). Lastly, MR, another control variable is measured through the company’s beta coefficient (Fombrun & Shanley, 1990). A common notion is that all stakeholders are risk-averse, and prefer companies that offer less risk. Less risky firms therefore may show better signs of reputation. Opposite to this, some stakeholders may prefer to invest in high-risk companies expecting high returns on their investment. The control variables related data were collected from the corporate database “Capitaline Plus,” “ProwessIQ,” and the Indian financial portal “

Sample and Period of the Study

The sample for the study consists top 100 listed companies that are selected from the BSE 500 (Bombay Stock Exchange) which is based on the market capitalization list of 2015. 2015 has been chosen as the base year as this was the year when the reporting of CSR activities was made mandatory under Section 135 of the Indian Companies Act, 2013. The reason for selecting these top 100 companies is that they capture around 62% of the whole market share. Therefore, investigating them will aptly represent the scenario.

The period of the study extends from 2015 to 2020. CSR expenditure data is collected from the CSR reports of the sample companies from the year 2015 onwards and CR data is extracted according to the methodology adopted from 2016 onwards. We have taken into consideration the long-term effect of CSR and control variables on the reputation and therefore reputation data is collected following a lag of a year.

Analysis

To address the research questions, we use the Panel Corrected Standard Error (PCSE) model using STATA 16 while estimating the following equations:

A series of tests was conducted to evaluate the assumptions for regression analysis and its fit. To test the normality of the data JarqueBera test was conducted and all the results (1.1, 2.7, 3.2, and 7.9 in respective order of equations) being greater than 0.05 indicate that our data is normal. Multicollinearity among variables was measured by using the variance inflation factor (VIF). The test revealed the mean VIF as 1.09, 1.08, 1.07, and 1.08 in the respective order of the equations. All values being <10 indicate that multicollinearity is not present (Johnson et al., 2018). The heteroscedasticity assumption was tested using the Breusch-Pagan/Cook-Weisberg test for heteroskedasticity. The p values (.0084, .0039, .0182, and .0154 in respective order of equations) obtained from the test show that the variables of the study suffer from heteroscedasticity. Test for autocorrelation (using Wooldridge test of autocorrelation) revealed the existence of 1st-order autocorrelation. To address these problems, we employed PCSE model. SE estimates of the PCSE model are robust to disturbances that are heteroscedastic, contemporaneously cross-sectionally correlated and autocorrelated to type AR (1). In the analysis, the reputation of the current year is regressed with the CSR expenditures and control variables of the precedent year. This was done to evade the potential endogeneity issue (Melo & Garrido-Morgado, 2012) and isolate this study from the theories supporting the two-fold proposition (Hillman & Keim, 2001).

Results

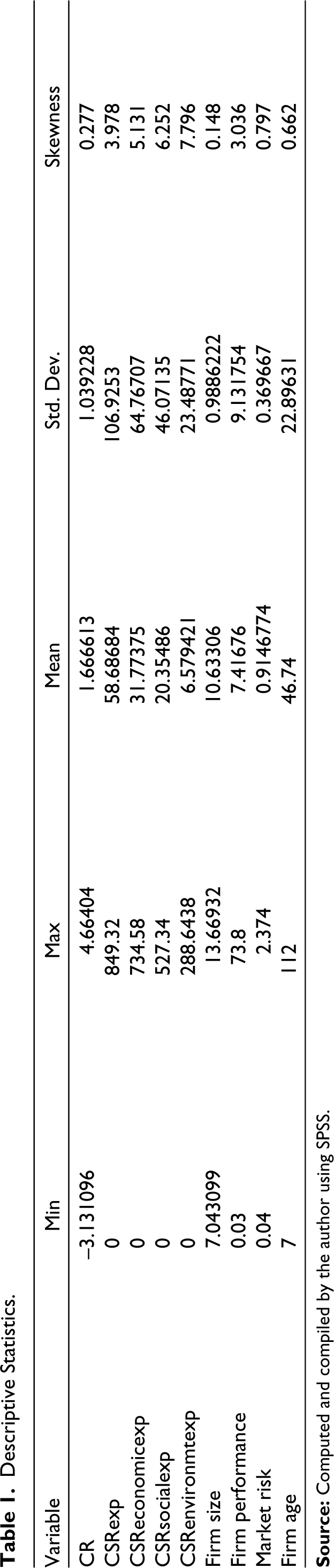

Table 1 presents the descriptive statistics for all the variables used in this study. The mean value of reputation is recorded at 1.67 and skewness at 0.28 demonstrating that the distribution is not far from symmetry. The observation is the same in the case of FS. The mean CSR_expenditure (₹in crores) of the sample companies (n = 100) during the study period is computed at 58.68 and when decomposed into its components the mean values (₹in crs) are observed at 31.77, 20.35 and 6.58 for economic, social, and environmental components in their respective order. This indicates that while the Indian companies on average have spent ₹58.68 cr on CSR expenditure their average expenditure on the economic component is ₹31.7 cr and on the social component is ₹20.3 cr, and surprisingly on environmental activities is only ₹6.58 cr. The sample companies have a mean market capitalization of ₹10.633 Crs (for FS), mean performance of 7.42, mean risk of 0.915, and the firm’s age ranges from 7 to 112 years.

Descriptive Statistics.

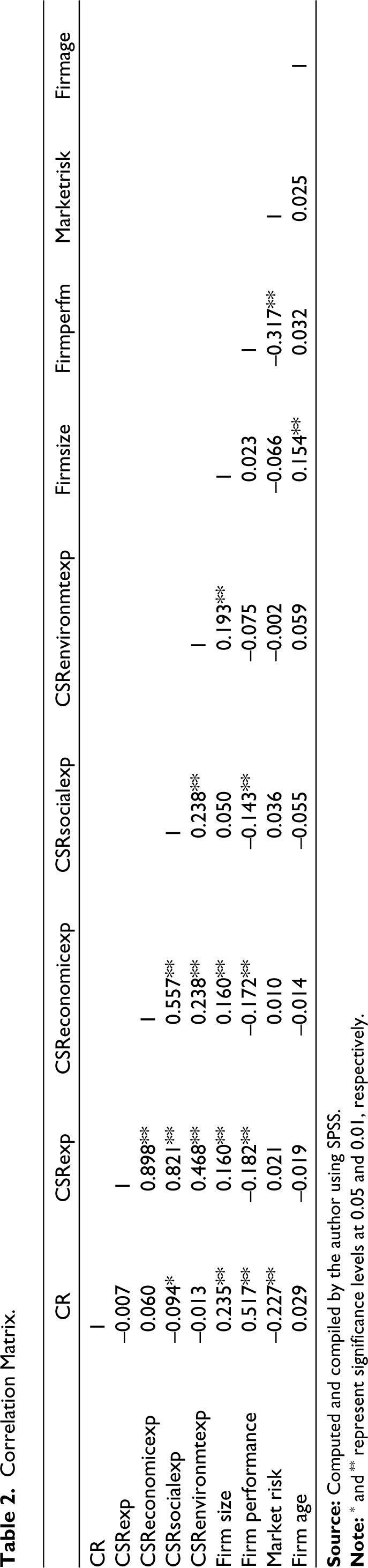

Table 2 presents the correlation among variables included in the regression models. No significant correlation is obtained between corporate reputation and CSR expenditure, CSR_economic expenses and CSR_environmental expenses. A negative correlation is obtained between corporate reputation and CSR_social expenses (r = –0.094) significant at 5%. Regarding our control variables, we find a significant correlation of corporate reputation with FS (r = 0.235) and firm performance (r = 0.517) both significant at 1%. However, MR (r = –0.227 at 1% level of significance) is negatively correlated with reputation. However firm age; is statistically not significant.

Correlation Matrix.

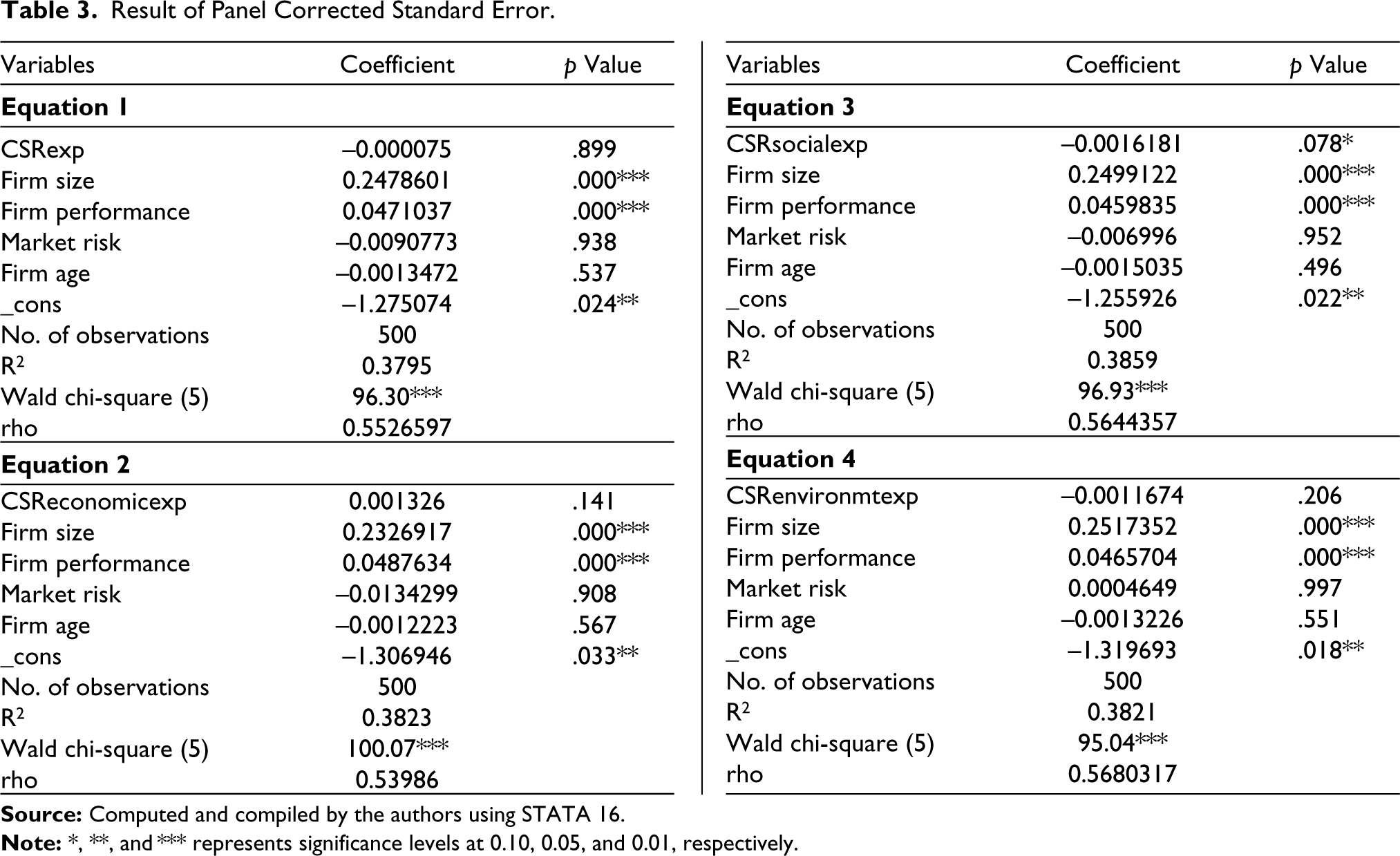

Table 3 presents the result of estimating the equations using PCSE model. The estimated coefficient of CSR expense for Equation (1) is insignificant. Therefore, there exists no significant relationship between corporate reputation and expenses. For Equation (2) the estimated coefficient of CSR_economic expenses is statistically insignificant. Thus, we find that there exists no significant relationship between corporate reputation and CSR_economic expenses. The result of estimating Equation (3) revealed coefficients of CSR_social expenses are statistically significant at a 10% level of significance indicating that a negative significant relationship exists between corporate reputation and CSR_social expenses. Estimating Equation (4) revealed coefficient of CSR_environmental expenses is statistically insignificant. Thus, we can say that there exists no significant relationship between corporate reputation and CSR_environmental expenses.

Result of Panel Corrected Standard Error.

Regarding the control variables, a significant relationship was found between corporate reputation with FS and firm performance (for all the equations). However, MR and firm age, other explanatory variables, are not statistically significant (for all the equations). The R2 for all the equations in respective order are 38.23%, 38.59%, and 38.21%. Estimates of Rho for all the equations are in the range –1 to 1.

The result of the study suggests that the different CSR expenditure of an Indian company have no impact on its reputation. However, a differential effect of components of CSR expenditure is observed on reputation. The outcomes of our empirical investigation suggest that it is the CSR expenditure on social concerns that significantly impact reputation rather than the CSR expenditures made on economic or environmental concerns. However, the impact is found to be a negative one.

Discussion

This article is an attempt to investigate if different CSR expenditures may have a differential impact on the reputation of a company. The findings of our analysis show that different components of CSR expenditure have a differential impact on reputation. The result of the study substantiates that social-related spending by Indian companies has a significant negative impact on the reputation of the company (Baruah & Panda, 2021). However, the other forms of expenditure like economic and environmental expenses render no significant impact. This finding draws support from the empirical evidence demonstrating that CSR investment can be destructive to firm performance when it passes a certain level (Wang et al., 2008). The push factor arising out of positive evaluation by some stakeholders might have been offset by the pull factor arising out of negative evaluation of those activities by some other stakeholders (in this case the shareholders when the FP is adversely affected). The shareholders might perceive that the managers allocate significant resources for CSR leaving meager funds for dividends or future investment for their hidden personal reputational benefits (DesJardine et al., 2023). The Ministry of Corporate Affairs (MCA) has also highlighted the limited impact of CSR initiatives in India, despite a significant increase in spending. According to the MCA, CSR spending stood at ₹26,210 crore in FY21, a growth of 80% since FY16. However, the impact of these funds is not widely felt, and there is a need to enhance their visibility and effectiveness (Pattanayak, 2023). The negative relationship between the social component of CSR expenditure and CR, though contradicts the findings of the earlier literature is very much in consonance with the opinion of the officials in the concerned ministry of the Government. The CSR spending in social activities is more concentrated in the areas where the companies operate to gain the goodwill of the local community given that the support of the local community is just as important for the running of their business smoothly. In contrast, the northeastern states of Assam, Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, and Tripura receive a mere amount (to substantiate factually - only 0.91% of the funds in FY 2020–21 against 13.21% only for Maharastra). Whatever the reasons, this type of spending might be negatively perceived by the other stakeholders, particularly the wider society as the smaller regions are ignored in the spending prioritization despite their status as the most socio-economically and culturally diverse in the country and have a high incidence of poverty and underdevelopment (Pattanayak, 2023) Another pertinent explanation for this finding could be poor communication.

As in the case of company-specific characteristics like FS and firm performance significantly impacts reputation (Brammer & Pavelin, 2006; Fombrun & Shanley, 1990). This proves that the bigger the firm higher the reputation a company might enjoy. In the case of performance, the better the company’s FP the stakeholders perceive the company from a positive perspective. Further, the independent variables MR and the age of the firm have no impact on reputation. The amount of risk a company takes has no impact on the reputation of the business. The result obtained for firm age is in resemblance with the assumption that as a company age passes by it may enjoy a positive or negative reputation or a combination of both ultimately leading to a constant reputation throughout its lifetime. This is in contrast to our belief that the older the company is the better it may be in attaining the optimal way of allocation of the CSR resources for facilitating reputation growth.

From the Indian context although the Companies Act, 2013 mentions the activities where CSR expenditures are to be done, spending on social activities has only proved that it impacts reputation. The impact is found to be a negative one. The implementation of CSR activities by companies was so improper that companies could evade any sanctions on them by merely giving a statement explaining their failure to perform CSR activities. It is only after 2019 that the Act became strict in these regards and the mandate is followed in the strict sense. Additionally, stakeholders always perceive CSR as a philanthropical activity but when CSR became a mandate put on companies under that Act it lost its true meaning and now stands just as a namesake to comply with the existing law. Therefore, the real impact of CSR on reputation is lost somewhere. Another reason is that Indian companies are not practicing a proper decision-making mechanism of optimal CSR resource allocation which induces reputation building. This might be a reason for the attainment of such a finding that contradicts the literature (Brammer & Millington, 2004; Cho et al., 2012; Fombrun & Shanley, 1990; Pérez, 2015; Toms, 2002).

According to an article (Jafri, 2021; Rai, 2020), CSR has been reduced to the mere accumulation of projects without creating any social impact. Hindrance in the effective implementation of CSR in India is due to the lack of proper enforcement agencies and finding credible projects that the corporate can support. They stated that bigger charities get flooded with money while the smaller ones have to seek their way to finding funds due to lack of resources and capacity to cope up with the company’s bureaucratic and operational demands. KPMG report has pointed to geographical bias as another problem, where companies lean to fund only those projects that are close to the location they operate resulting in only those industrialized areas getting preference over the poorer and underdeveloped areas that truly require the development and aid. An Economic Times investigation allegedly found the companies cheating by giving charitable foundations donations which they return to the company after deducting a certain commission amount. The spending in the name of CSR has mostly gone to the set priorities of the company rather than the democratically determined priorities by the Act. Various analysis of CSR shows that the law in its present form is failing to promote a healthy CSR initiative due to ambiguous obligations. The legal provisions are presented in vague language which leaves room for a high degree of self-interpretation of the Act. The Act does not penalize a defaulter and allows evading with an explanation regarding their non-compliance with CSR rules. This led to high corruption, slow development, and low levels of public confidence which is reflected in the reputation of the business.

In our analysis, we have incorporated a lag period of 1 year. This was done because CSR of a particular year will not impact the reputation of the company in the same year. The CSR efforts of the company will take time to reach its stakeholders to create a positive picture of the company in the minds of the stakeholders. Therefore, if the lag is extended by one or more years then we might achieve results consistent with the literature.

Therefore, CSR when broken into economic, social, and environmental expenditure impacts reputation differently. The result obtained neither accepts nor contrasts literature fully but brings forward a mixed picture where a part of total CSR expenditure is expected to affect the company’s reputation. This study contributes a new dimension of thinking into the research and new insight into this particular topic. Also, it is an addition to the current body of literature which to our knowledge is very sparse.

Conclusion, Limitation and Future Research

CSR expenditure of the company not only benefits its stakeholders but also benefits the company in creating and enhancing its reputation. However, we found a mixed result where CSR expenditure when segregated into economic, social, and environmental expenses (based on TBL) impacts a company’s reputation differently. Results were obtained after estimating the data using PCSE model after meeting all necessary assumptions. It has been observed in our study that different components of CSR expenditure do impact reputation differently, accepting one hypothesis and making the other two hypotheses unacceptable. This study is a new addition to the literature as the result obtained is a combination of both the notion of CSR significantly impacting reputation and CSR not impacting reputation. This empirical analysis contributes to the existing literature by adding a new dimension of thinking into the research and new insight into this particular topic. An explanation for attaining such an amalgamation is that CSR is often criticized as a double-edged sword. CSR practice should have no other purpose other than benefiting the stakeholders and the society at large along with finding an optimal way of allocating a firm’s resources to make a profit and ultimately achieve a higher reputational status (According to the Theory of the firm; Friedman, 1970). Therefore, CSR practices of a company should be philanthropic acts along with profit maximization, reputation boosting and conformity to provisions imposed by the law.

The result of the study leads to the certain managerial implications that the management can take into concentration. To begin with, company’s priority should be to practice CSR with a motive of benefiting society; parallel to this the company may find the right balance of CSR resource allocation for spending in the CSR activities as when a firm aligns its CSR activities with its organizational strategy, it tends to improve reputation (Pradhan, 2016).

The main limitation of this study is the sample size. Future research may increase the sample beyond 100 companies with a bigger time span. A lag of 1 year was taken. A longer lag period may be taken of two or more years to capture the long-term impact of CSR on reputation. Finally, the sample companies are limited to India, it would be an interesting line of study to analyse other emerging economies in the same line and counter-check the findings for similarity or dissimilarity.

To sum up we believe that this investigation portrays and increments current literature on how different CSR expenditures may impact the reputation differently in an emerging economy setting like India and contribute to the existing literature as an important enrichment in the field.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.