Abstract

Purpose:

The objectives of the study include examining the role of family financial socialization (FFS) in shaping young adults’ financial self-efficacy (FSE), understanding how FSE contributes to financial behavior (FB), and exploring the mediating role of FSE in the relationship between FFS and FB of young adults.

Design/Methodology:

Using a quantitative technique, data were collected from 395 university students in Punjab, India. The study utilized partial least squares structural equation modeling (PLS-SEM) to scrutinize and decipher the intricate interconnections among the variables.

Findings:

The results support the hypotheses, demonstrating the significant influence of FFS on FSE and FB, as well as the mediating role of FSE.

Practical/Social Implications:

Educational institutions and policymakers can integrate these findings into financial education programs to boost financial literacy and self-efficacy among young adults. Additionally, policymakers can encourage parents to actively engage in open financial discussions with their children.

Originality/Value:

This study broadens the scope of existing research by investigating FFS through multiple dimensions and focusing on university students in Punjab, a previously underexplored demographic. It also uniquely examines the mediating role of FSE in the relationship between FFS and FB.

Introduction

This research delves into the complex interactions within family financial socialization (FFS), examining its significant impact on two critical components of personal financial behavior (FB): financial self-efficacy (FSE) and FFS. The role of familial financial socialization is of paramount importance in shaping individuals’ attitudes, beliefs, and behaviors toward money management and financial decision-making. As individuals navigate the complex landscape of personal finance, their family environment serves as a primary source of early exposure, education, and social learning regarding financial matters (Danes & Haberman, 2007). This process significantly impacts the expansion of financial skills, values, and behaviors that can persist throughout their lives. The interaction among FFS, financial self-confidence, and subsequent FB is an increasingly intriguing topic within the realms of financial psychology and consumer behavior. FSE, which refers to an individual’s belief in their capability to effectively control financial tasks and challenges, emerges as a crucial predictor of financial decisions and actions (Lusardi & Mitchell, 2011). The family’s role in fostering or hindering this sense of self-efficacy can shape individuals’ financial choices, from budgeting and saving to investing and debt management.

In an era characterized by increasing financial complexity and uncertainty, the ability to make sound financial decisions has become an essential life skill. Young adults, as they transition from adolescence to adulthood, face a myriad of financial challenges ranging from managing personal budgets to making investment decisions. The interplay of individual FB and the sociocultural context within which they are shaped presents a dynamic field of study.

The primary aim of this research paper is to investigate the complex interconnections among FFS, FSE, and FB within the young adult population residing in Punjab, shedding light on the mechanisms that influence their financial decisions. The financial landscape has transformed significantly over the years, placing a premium on individuals’ capacity to navigate complex financial choices. Concurrently, research on personal finance has unveiled a multifaceted web of factors that influence financial decisions. At the core of these determinants lies the family, often the primary source of financial socialization during formative years. FFS encompasses the transmission of attitudes, beliefs, and practices related to money management, and it is through this process that young adults develop the foundation for their FB (Shim et al., 2009).

The family serves as a powerful agent of socialization, introducing young individuals to financial concepts, values, and practices that can shape their FB throughout adulthood. Early exposure to discussions about budgeting, saving, investing, and debt management within the family can significantly influence financial attitudes and behaviors (Loibl & Hira, 2005). FFS has been found to impact financial literacy, decision-making, and future financial success (Shim & Serido, 2011). Thus, understanding how family dynamics interact with financial socialization to mold the FB of young adults is of paramount importance.

The confidence an individual has in their capacity to handle financial matters, known as FSE, emerges as a key psychological factor influencing FB (Lusardi & Mitchell, 2011). Elevated levels of financial self-confidence enable individuals to address financial challenges with assurance, leading to improved financial decision-making and behaviors (Dare et al., 2022). Considering the probable link between FFS and the formation of self-efficacy beliefs, exploring the mediating role of FSE in the connection between family influence and FB provides a more comprehensive insight into this multifaceted relationship.

While previous research highlights the significance of FFS and FSE in influencing FB, the available literature is notably deficient in terms of the number of studies conducted on this subject matter, that investigate these connections within the cultural and societal context of Punjab, India. The primary goal of this research is to bridge this gap by investigating the extent to which FFS influences the FSE and subsequent FB of young adults in Punjab. Additionally, the study seeks to explore the mediating role of FSE in this relationship. Moreover, this research endeavors to examine the intermediary function of FSE within this relationship.

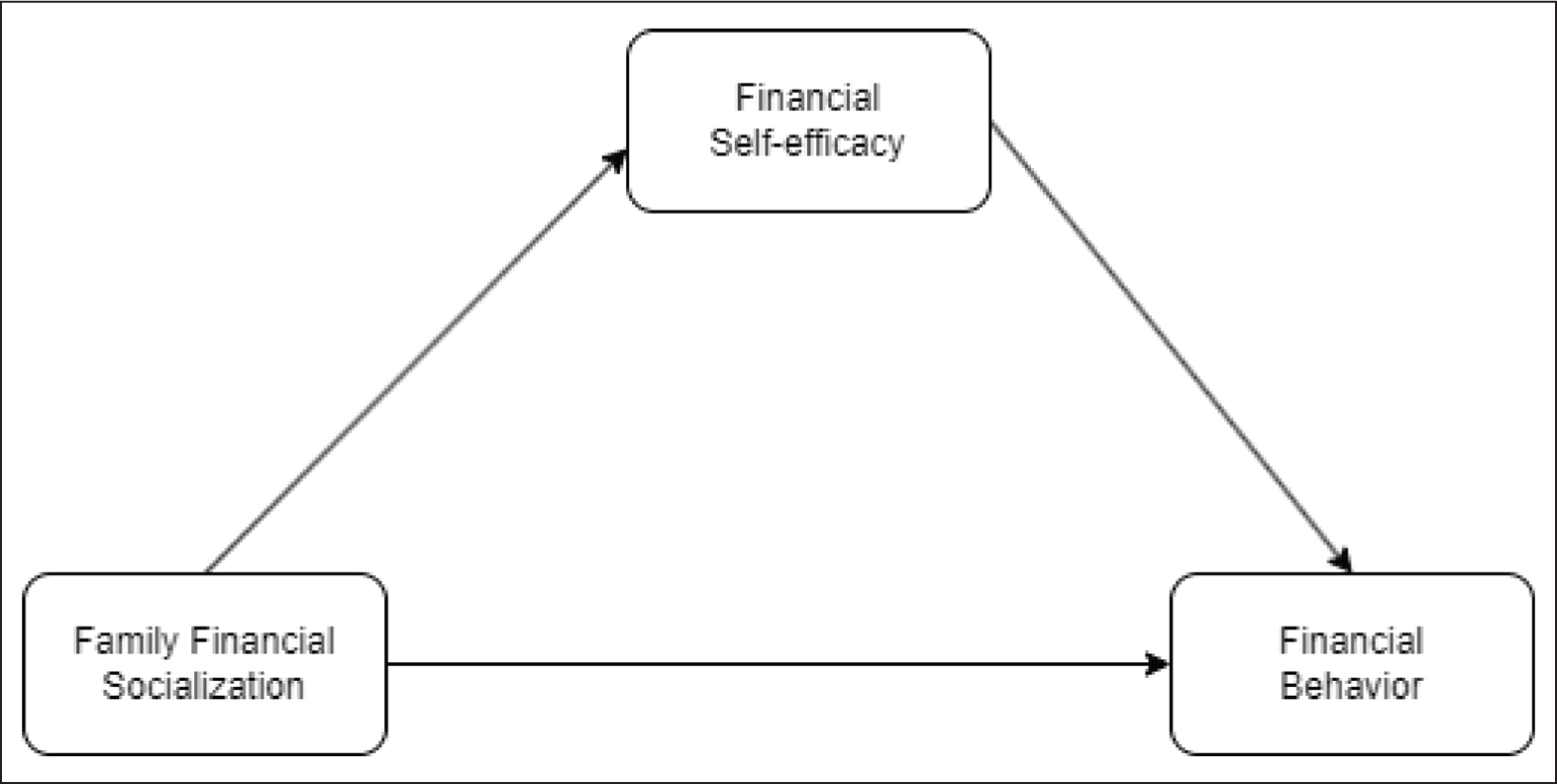

This paper significantly contributes to the existing body of literature by addressing gaps in prior research, which predominantly focused on the impact of FFS through financial discussions or role modeling. This study broadens the scope by investigating FFS through the dimensions of parental communication, parental financial role modeling, financial interactions with parents, and parental financial norms. Additionally, it provides a valuable contribution by focusing on university students in Punjab, a demographic that has not been extensively studied before. Furthermore, the research explores the mediating role of FSE in the relationship between FFS and FB, and constructs a conceptual framework grounded in previous studies (Figure 1).

Conceptual Framework.

By gathering data from university students in Punjab, this research aims to offer insights into the following research questions:

RQ1: What is the role of FFS in shaping young adults’ FSE? RQ2: How does FSE contribute in building young adults’ FB? RQ3: Does FSE mediate the relationship between FFS and FB of young adults?

The subsequent sections of this paper are organized as follows: initially, study introduces the theoretical framework and elaborates on the formulation of hypotheses. Subsequently, outline the research methodology, analyze the collected data, and present the findings. Finally, the study concludes with a thorough discussion of the results, their potential implications, and any limitations.

Literature Review and Hypothesis Formulation

Family Financial Socialization Theory

Characteristics of individuals and families that impact interactions and relationships within the family, as well as purposeful financial socialization, are included in the FFS theory. The outcome of this theory is a financial attitude, knowledge, and skills that affect FB and financial well-being. Financial attitude, knowledge, and capability play a mediating role between the financial process and socialization outcome (Kim & Torquati, 2020). The focus of this theory is more on the parent–child relationship (Gudmunson & Danes, 2011). Also, family members play an essential role in the socialization process, and adults learn habitual patterns from their parents (Shim et al., 2015; Zhu, 2019). This theory focuses both on the interaction among family members and family roles (Rea et al., 2019). According to the FFS model, children are taught to get used to money from their families, and it is the family that provides socially appropriate knowledge to children through their acts and behavior in noticeable social circumstances (Jurgenson, 2019). Before reaching the university level, the observation of parental behavior serves as a form of implicit learning for students, while direct teaching by parents represents explicit learning (Sirsch et al., 2020).

Relationship Between Family Financial Socialization and Financial Self-efficacy

“Self-efficacy is an individual’s sense of confidence in their ability to perform a certain skill or task to obtain specific outcomes” (Bandura, 2010). Individuals’ attitudes, beliefs, and self-reliance in creating financial decisions are referred to as FSE (Rothwell et al., 2016). Danes and Haberman (2007) undertook a comprehensive study to investigate the intricate nexus among self-efficacy, financial knowledge, and behavior within a substantial cohort of 5,329 secondary school students. The research delved into the realms of FSE and financial knowledge. It revealed that females were more inclined than males to assert that their financial decision-making capabilities were influenced by managing money. Conversely, males exhibited a greater sense of confidence when making financial judgments. Self-efficacy constitutes a widely embraced cornerstone within the framework of social cognition theory, although with pertinent implications (Leon, 2020).

A study on women only has been conducted by Farrell et al. (2016) to determine the relationship between FSE and FB of women, which revealed that women retain saving products as compared to debt-related products due to their high FSE. A recent study by LeBaron-Black et al. (2022) explores how three family FFS methods impact financial well-being in U.S. emerging adults, using data from 4,182 participants. It finds that parent financial modeling and experiential learning are crucial, with modeling influencing FB and satisfaction, and experiential learning enhancing FSE. These insights suggest that parents should emphasize modeling and experiential learning to foster better financial outcomes in their children, and educators should support these methods to enhance financial well-being. Hence, grounded on the previous studies, the following hypothesis is framed:

H1: FFS positively influences FSE.

Relationship Between Financial Self-efficacy and Financial Behavior

The study of FB encompasses a multidisciplinary approach, drawing insights from economics, psychology, sociology, and other fields. Lusardi and Mitchell (2014) defined FB as an important dimension of FFS. FB is also one of the prominent outcomes in the field of FFS. According to various previous studies, there has been a vast increase in the publication of FB. Hence this increase provided many factors affecting FB.

Psychological factors, including financial attitudes, beliefs, and self-efficacy, have been identified as substantial determinants of FB. A favorable association between FSE and FB has been conclusively established (Lusardi & Mitchell, 2011), indicating that individuals who have confidence in their financial abilities are more likely to engage in reliable financial practices. Moreover, financial attitudes, plus risk tolerance and money management attitudes, can shape investment choices and savings behaviors. A quantitative study on 411 United kingdom adults by Dare et al. (2022) revealed that FSE had a strong positive relationship with financial well-being through the adoption of positive FB.

Recent studies highlight the significant role of FSE in shaping FB. Individuals with strong FSE tend to exhibit greater perseverance in financial goal pursuit, leading to improved financial outcomes over time (Lusardi & Mitchell, 2011). A recent study by Lone and Bhat (2024) investigates the impact of financial literacy on financial well-being among business school faculty in Jammu and Kashmir, revealing a significant positive relationship mediated by FSE. The findings suggest that enhancing financial literacy and self-efficacy can improve financial well-being, emphasizing the need for targeted educational programs to address long-term financial planning in regions with limited access to financial literacy resources. Furthermore, FSE has been linked to heightened engagement in retirement planning, investment endeavors, and various other long-term financial decision-making processes (Agnew et al., 2008). Therefore, drawing upon prior research, the study offers the following hypothesis:

H2: FSE positively influences FB.

Relationship Between Family Financial Socialization and Financial Behavior

FFS encompasses the process through which individuals acquire financial knowledge, cultivate attitudes, and develop behaviors from their familial contexts. It serves as the cornerstone upon which individuals build their FB, laying the groundwork for their financial decision-making patterns (Lown, 2011). Early exposure to financial discussions, role modeling, and parental financial management practices can significantly influence an individual’s FB in adulthood. Various authors explored many components of FFS, like communication (Li et al., 2021), role modeling (Zhu, 2019) norms, and behavioral controls (Shim et al., 2010).

Communication within the family serves as a crucial channel for financial socialization. Studies in the field have provided empirical evidence indicating that the nature and regularity of financial dialogues occurring between parents and their offspring can play a pivotal role in molding financial attitudes and behaviors. Adolescents who are involved in regular conversations about money matters with their parents tend to develop higher levels of financial responsibility and exhibit better FB in adulthood (Kim & Torquati, 2019).

Research suggests that FB are often handed down from one generation to the next. Young adults who observe positive FB within their families, such as prudent budgeting and responsible credit management, are more likely to emulate similar behaviors in their own financial lives (Gudmunson & Danes, 2011). Conversely, negative FB, like overspending or financial procrastination, can also be perpetuated across generations (Roberts & Jones, 2001). Utilizing previous research as a foundation, this study puts forward the following hypothesis:

H3: Financial FFS positively influences FB.

Mediating Role of Financial Self-efficacy

An increasing volume of academic literature has examined the function of FSE as a mediating factor in the relationship between FFS and FB. Contemporary research findings put forth the notion that family financial instruction exerts an influence not only through its direct impact on FB but also indirectly, mediated by its effect on an individual’s FSE (Riaz et al., 2022). Positive messages about money management within the family environment can contribute to the development of a stronger sense of FSE, subsequently, leading to the adoption of responsible financial actions.

Recent research highlights the practical implications of the mediating role of FSE. It suggests that interventions targeting FFS can play a pivotal role in fostering elevated levels of FSE among individuals. Parents and caregivers can empower young adults by offering positive financial guidance, bolstering their belief in their ability to navigate financial challenges effectively (Rudi et al., 2020).

Shim et al. (2015) in their longitudinal report measured the influence of financial socialization agents (parental modeling, parent communication, parent expectations, friend’s behaviors, class learning, and self-learning) on mental outcomes (financial attitude, financial controllability, and financial efficacy) on behavioral outcomes (healthy FB). The results show that there FB of students depends more on FSE and financial controllability. But this study didn’t measure the mediate effect of FSE. According to a relatively small body of research, FSE may moderate certain relationships between financial socialization and financial outcomes (Rea et al., 2019). Rothwell et al. (2016) aimed to ascertain the mediating influence of FSE within the context of the relationship between objective financial knowledge and the accumulation of savings for postsecondary education. Thus, building upon prior research, this study presents the following hypothesis:

H4: FSE mediates the relationship between FFS and FB.

Research Methodology

Data

The data collection procedure entailed the utilization of a self-administered questionnaire, through which data were gathered from a sample of 395 full-time university students hailing from Punjab. Punjab, being the 16th most populous state in India, boasts a diverse population encompassing various religions and communities (Census, 2011). Additionally, the high level of financial literacy and varied financial habits in Punjab, ranging from traditional saving practices to modern investment strategies, offers a comprehensive backdrop to examine the nuances of financial socialization among young adults (National Centre for Financial Education, 2019). According to the Ministry of Youth Affairs and Sports (2003), a young adult is between the age of 15 to 19 years. But later Ministry of Youth Affairs and Sports (2014) improved it and defined the youth between the age group of 15–29 years. Moreover, according to Mhavan et al. (2022), an 18+ year student "has critical thinking ability and enters in higher secondary education. Therefore, employing a convenient sampling technique, the questionnaire was distributed to students enrolled full-time in UGC-approved universities located in Punjab, including Chandigarh. These students were enrolled in programs related to commerce, economics, business, and management, and they belonged to the age group of 19 to 24 years.

The sample size exceeded the calculated minimum requirement utilizing G*Power software v. 3.1.9.6, developed by Faul et al. (2007). According to the criteria established by Cohen (1998) to compute the sample size, the study utilized an a priori sample size calculator, using a medium effect size of 0.2, a significance level (α) of 0.05, and a desired statistical power of 0.80, the analysis revealed a recommended minimum sample size of 191 participants. Therefore, the questionnaire was distributed to 450 students and received 413 completed responses, leading to an achieved response rate of 91.77%. Following a thorough review, a total of 395 responses were selected and considered for the purpose of data analysis in accordance with the study’s specific criteria.

Sample Description

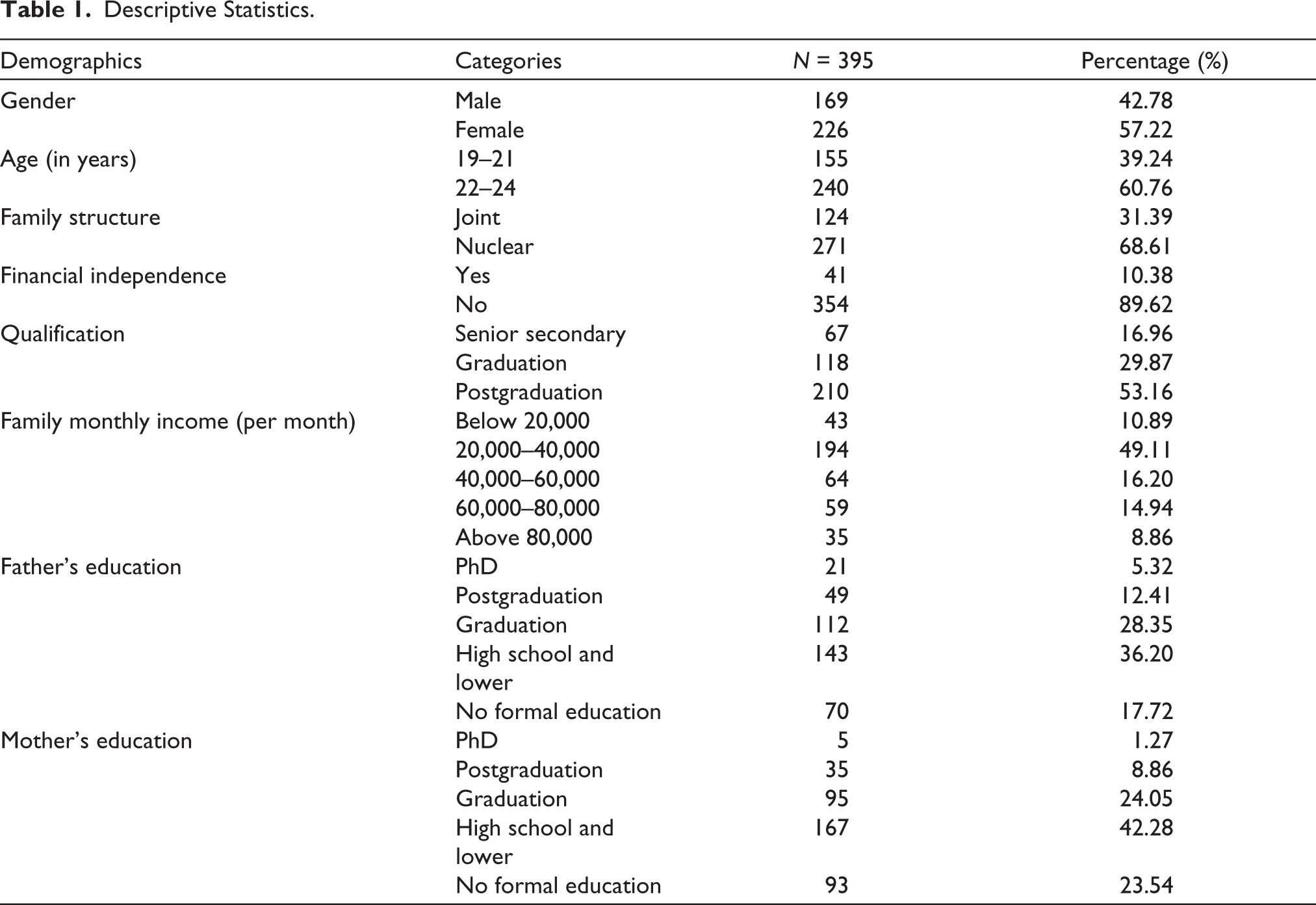

Table 1 provides a comprehensive depiction of the demographic composition pertaining to the 395 study participants. In terms of gender, there is a fairly balanced representation, with 42.78% being male and 57.22% female. The age distribution shows that a significant portion of the participants falls within the 22–24 age range, comprising 60.76% of the sample, while 39.24% fall into the 19–21 age category. Family structure data reveal that 68.61% of the participants come from nuclear families, while 31.39% have joint family structures.

Descriptive Statistics.

Regarding financial independence, only 10.38% of participants reported being financially independent, while the majority, 89.62%, indicated financial dependence. The majority of participants in the study have postgraduate qualifications (53.16%), followed by those with undergraduate degrees (29.87%), and a smaller proportion have completed only senior secondary education (16.96%). Family monthly income varies, with 49.11% falling within the ₹20,000–40,000 range, followed by 16.20% in the 40,000–60,000 range. The distribution of father’s education levels shows that a significant portion has completed high school and lower education (36.20%), followed by graduation (28.35%). Mother’s education follows a similar trend, with the highest percentage having high school and lower education (42.28%), and 24.05% having completed graduation. These demographic insights provide valuable context for understanding the characteristics of the study’s participants, which may be essential for interpreting the research findings.

Measures

The study tested the model using a standard scale found in previous research. All the aspects were rated on a scale of 1 to 5, where 1 meant strongly disagree and 5 meant strongly agree.

Family Financial Socialization (FFS)

The questionnaire encompassed a total of 32 items adopted from Allen et al. (2007) and Shim et al. (2015). Items were allied to parental financial communication, parental financial role modeling, parental financial norms and financial relationship with parents. The scale included statements such as “My parents discuss family financial matters with me, I make financial decisions based on what my parent(s) have done in similar situations, My parents track monthly expenses, My relationship with parents is good because of money issues” were asked.

Financial Self-efficacy (FSE)

The measurement of young adults’ FSE employed a six-item scale established by Lown (2011). The items like “It is easy to stick to my spending plan when unexpected expenses arise” were asked.

Financial Behavior (FB)

Dew and Xiao (2011) scale comprising 12 distinct items to evaluate the FB of young adults. The items were asked for such as “paid all your bills on time, kept a written or electronic record of your monthly expenses.”

Results

Data Preparation

In this research, Mardia’s test was utilized to evaluate multivariate normality, and this analysis was conducted through the Web Power online tool (

Evaluation of the Measurement Model

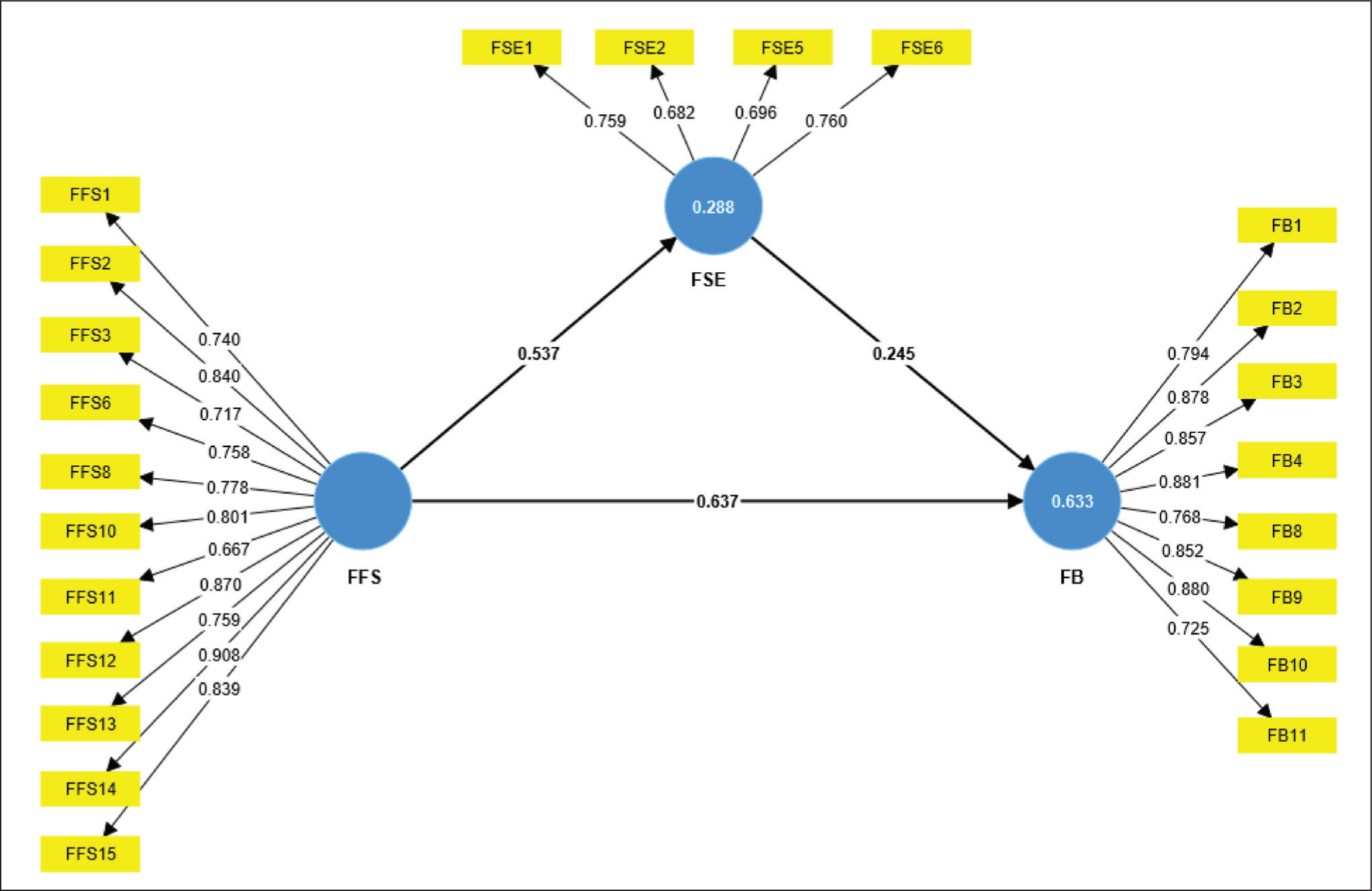

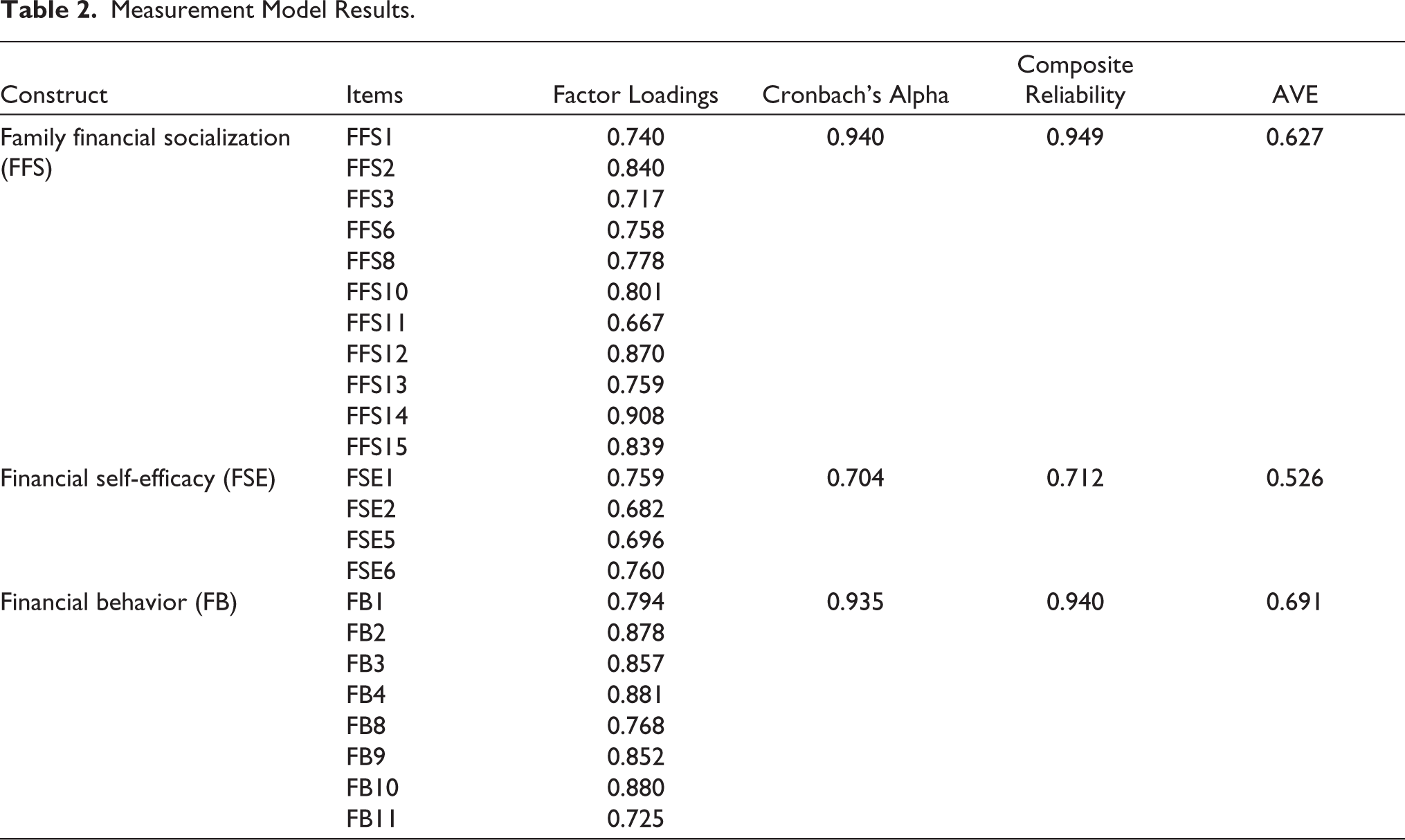

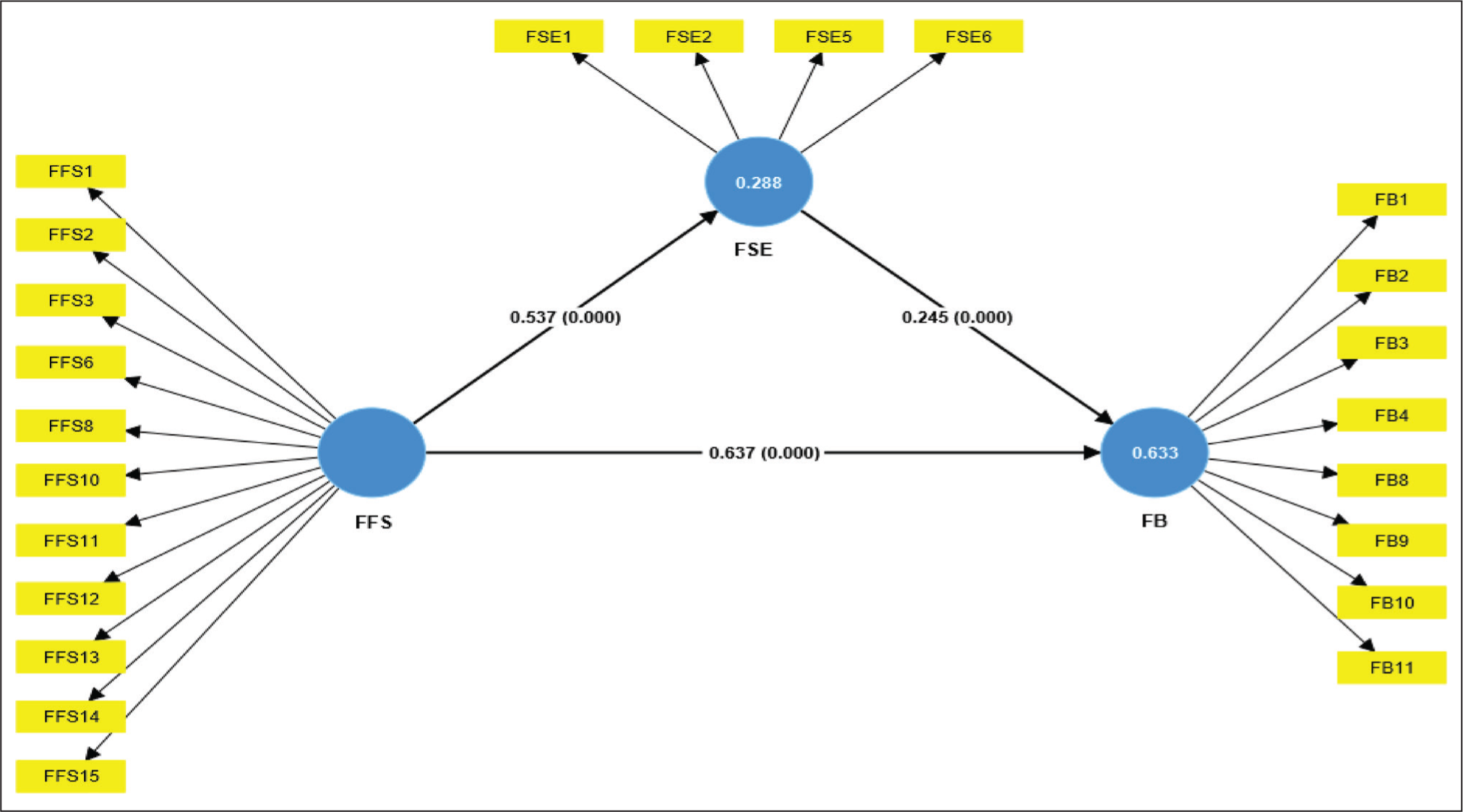

To ascertain the integrity of the measurement model, researchers conducted a comprehensive evaluation encompassing, internal consistency reliability indicator loadings, convergent validity, and discriminant validity (Hair et al., 2020). Loadings above 0.70 and 0.50 were retained (Figure 2). In accordance Hair et al. (2017) indicators exhibiting loadings equivalent to or surpassing 0.5 should be retained, provided that they meet the criteria for composite reliability (CR) and average variance extracted (AVE). Yet, low loadings (<0.50) were removed (FFS4, FFS5, FFS7, FFS9, FSE3, FSE4, FB5, FB6, FB7, FB12) as insignificant. In Table 2, all constructs exceeded 0.70 but remained below 0.95 for CR. Convergent validity was met, with AVE values surpassing 0.5 and each construct’s AVE being lower than its CR as exposed in Table 2.

Measurement Model.

Measurement Model Results.

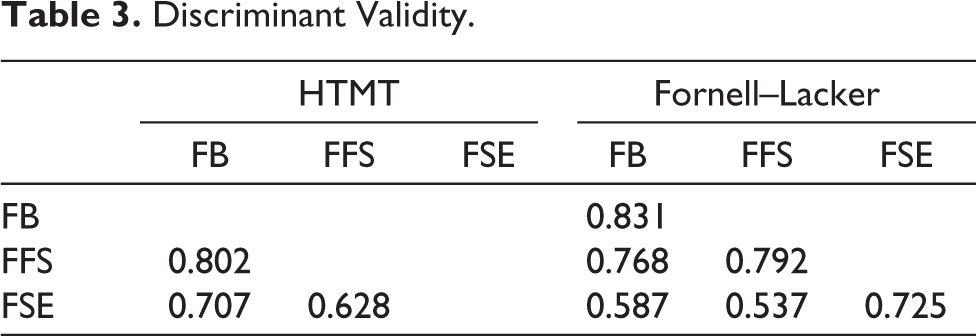

The researchers used the heterotrait-monotrait ratio (HTMT) to assess discriminant validity, all HTMT ratios below the 0.90 threshold (Henseler et al., 2015), and the Fornell–Lacker criterion confirmed. Both two criteria collectively confirmed sufficient discriminant validity (Ab Hamid et al., 2017; Fornell & Larcker, 1981; Sarstedt et al., 2019), as shown in Table 3.

Discriminant Validity.

Evaluation of Structural Model

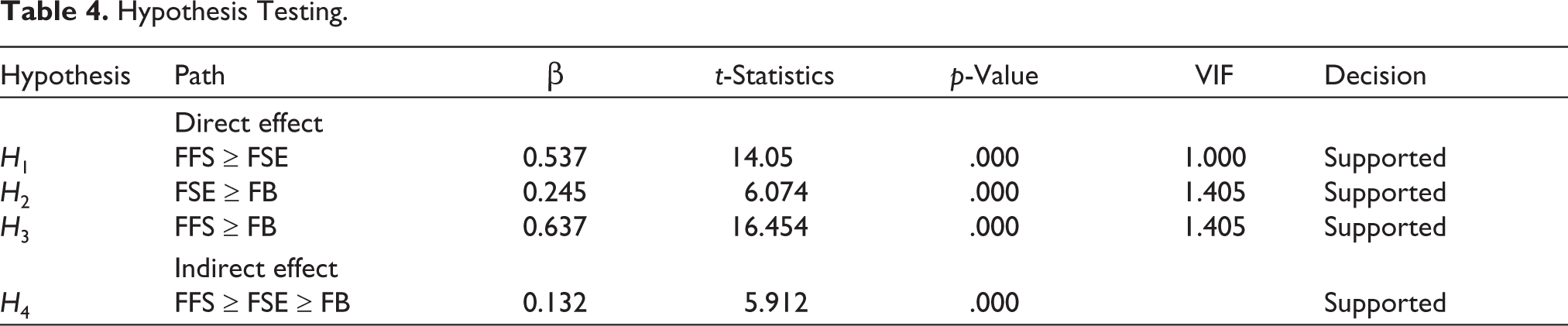

To assess the hypothesized model, the study conducted the bootstrapping technique with 5000 samples (Hair et al., 2020; Preacher & Hayes, 2008; Shrout & Bolger, 2002). In Table 4 and Figure 3, the study’s findings reveal a positive association between FFS and FSE (β = 0.537, t-value = 14.050, p < .001). Moreover, a positive relationship as hypothesized was also found among FSE and FB (β = 0.245, t-value = 6.074, p < .001), also FFS exhibits a positive relationship with FB (β = 0.637, t-value = 16.454, p < .001). Thus, H1, H2, and H3 were supported based on empirical results.

Hypothesis Testing.

Structural Model.

The significance of indirect relationships was examined by the method given by Preacher and Hayes (2008). The information in Table 4 demonstrates that the mediation of FSE is evident in the connection between FFS and FB (β = 0.132, t-value = 5.912, p < .001). Consequently, there is support for Hypothesis H4.

Role of Demographic Factors on Financial Behavior

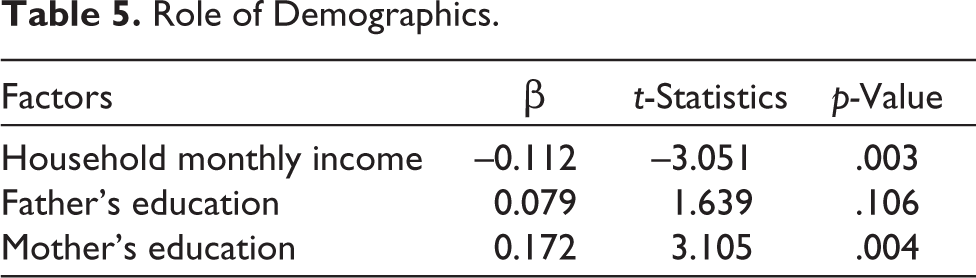

Table 5 examines the role of household monthly income and parental education on the FB of university students. The regression analysis results reveal significant findings for household income and mother’s education, but not for father’s education. Specifically, the negative regression coefficient for household monthly income (β = –0.112, p = .003) suggests an inverse relationship, indicating that higher household incomes are associated with less prudent FB among students due to greater financial security, lack of financial education, which reduces the perceived need for careful money management. Similarly, the positive coefficient for mother’s education (β = 0.172, p = .004) implies that higher levels of maternal education correspond to higher FB in students. These relationships are statistically significant, as indicated by their respective p-values being below the 0.05 threshold. In the Indian context, educated mothers are more likely to emphasize the importance of budgeting, saving, and prudent spending, significantly influencing their children’s financial habits. Studies have shown that parental education, particularly mothers’, leads to better academic and financial outcomes for children by improving the home learning environment and parental involvement in education (Banerji et al., 2017).

Role of Demographics.

In contrast, father’s education shows a positive but nonsignificant effect (β = 0.079, p = .106) on FB, suggesting no strong evidence of influence, this could be due to traditional family roles where fathers may focus more on external responsibilities, leaving a less direct influence on daily FB of their children. Additionally, the impact of paternal education might be diluted by other prevailing socio-economic and cultural factors within the family environment (Böhm et al., 2023).

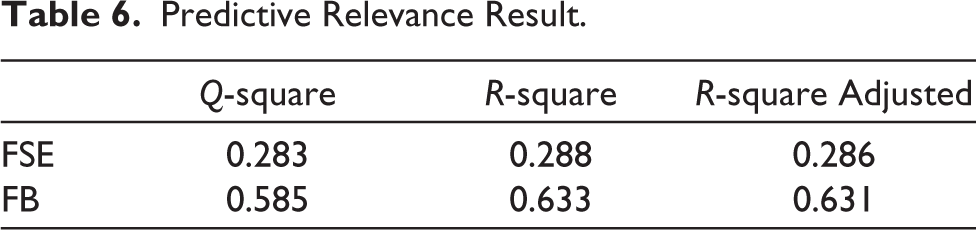

Predictive Relevance

Table 6 presents evaluation metrics for FSE and FB. The Q2 values assess their predictive ability, with FB having a higher value (0.585) than FB (0.283). According to the recommendations put forth by J. Cohen (1988), R2 values pertaining to endogenous latent variables may be assessed at 0.02, signifying a relationship of weak magnitude; 0.13, indicative of a relationship of moderate magnitude; and 0.26, denoting a relationship of substantial magnitude. The R2 values measure the proportion of variance explained by the models, with FB (0.633) outperforming FSE (0.288). Therefore, the findings indicate that all the endogenous constructs surpass a value of 0.26, demonstrating that the model possesses substantial explanatory power. Additionally, the adjusted R-square values, which consider model complexity, show similar trends, with FB (0.631) having a higher value compared to FSE (0.286). Overall, these metrics suggest that FB exhibits better predictive ability and explains more variance in the data compared to FSE.

Predictive Relevance Result.

Discussion

The present study aimed to investigate the relationships between FFS, FSE, and FB. Through the utilization of a bootstrapping technique with 5,000 samples, the study was able to robustly evaluate the hypothesized model and provide insights into the underlying dynamics of these relationships. The findings, as elucidated in Table 4, unveil multiple significant and pivotal relationships that enhance our understanding of financial attitudes and behaviors.

Positive Relationship Between Family Financial Socialization and Financial Self-efficacy

The findings derived from the study suggest a substantial and favorable link between FFS and FSE. This finding aligns with the hypothesis (H1) and supports prior research that underscores. The crucial role of the family in molding an individual’s financial beliefs and self-confidence (Shim et al., 2009). The robust positive association (β = 0.537) observed between FFS and FSE demonstrates that individuals who experience greater exposure to positive financial discussions and role modeling within their families tend to foster increased levels of confidence in their capability to accomplish financial concerns. The findings support the study by Vijaykumar (2022), which demonstrates the positive relationship between both factors leads to the attachment relationship between parents and children.

Positive Relationships Between Financial Self-efficacy, Family Financial Socialization, and Financial Behavior

The outcome of the study further reinforces the hypothesized connections between FSE and FB (H2), as well as among FFS and FB (H3). The positive relationships established in these aspects (β = 0.245 and β = 0.637 respectively) highlight the significance of both individual beliefs in financial abilities and the influence of familial financial discussions on actual FB. This echoes the notion that an individual’s assurance in their financial capabilities can translate into tangible financial decisions and actions, supported by a foundation of early family teachings.

Mediating Role of Financial Self-efficacy

Previous studies validate that FSE mediates the association among various factors of FFS and its outcome, that is, FB (Gudmunson & Danes, 2011). Similarly, the present study also provided notable contributions in its examination of the mediating role of FSE (H4). The results, as affirmed by the bootstrapping method, indicated a substantial indirect impact (β = 0.132) on FSE indicates that individuals who receive positive financial guidance within their families tend to develop higher FSE, leading to responsible FB. This suggests that interventions aimed at enhancing FB should consider targeting individuals’ self-confidence in their financial capabilities.

Implications and Future Directions

The implications of this research paper carry significant weight across various domains. First and foremost, the study underscores the need for educational initiatives that acknowledge the influential role of FFS. Educational institutions and policymakers can integrate these findings into programs focused on financial education, emphasizing the significance of fostering positive family financial discussions and role modeling. By doing so, they can bolster financial literacy and self-efficacy among young adults, equipping them with essential life skills. Additionally, these insights have policy implications, as policymakers can use them to design interventions that promote responsible FB within families, Encouraging parents to actively participate in open financial discussions with their children.

On an individual level, the research highlights the enduring impact of early financial socialization experiences, empowering individuals to reflect on their upbringing and make informed decisions to improve their financial well-being. Furthermore, these findings underscore the worth of cultural sensitivity in addressing FB. The study’s focus on Punjab, India, underscores the need to consider diverse cultural and societal contexts when implementing financial education programs and interventions to ensure their effectiveness within different communities.

However, certain shortcomings should be acknowledged. The study’s cross-sectional design limits the proficiency to make causal inferences. Longitudinal research designs could stipulate a more in-depth construction of the progressive relationships between the variables. Furthermore, utilizing self-report measures could potentially lead to the introduction of common method bias, suggesting the value of incorporating more objective indicators of FB. A shortcoming of this study is the exclusive collection of student data. To adequately measure parental influence, data from both parents and children are necessary. Lastly, this research paper opens the door to further investigation in the field. Future research can build upon these findings by exploring FFS and its impact in various cultural contexts and age groups. It offers a valuable foundation for studying Assessing the efficacy of specialized interventions tailored to augment FSE and behavioral outcomes within familial contexts, ultimately contributing to the ongoing advancement of financial education and well-being initiatives.

Footnotes

Authors’ Contributions

Rajwinder Kaur and Dr. Manjit Singh contributed to the design and implementation of the research, to the analysis of the results and to the writing of the manuscript.

Data Availability Statement

The data that validate the findings of this study are available from the corresponding author, upon reasonable request.

Declaration of Conflicting Interests

The authors declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: The authors have no conflicts of interest to declare. All authors have seen and agree with the contents of the manuscript. We certify that the submission is original work and is not under review at any other publication.

This article does not contain any studies involving human participants and/or animals performed by any of the author. Informed consent was not required as the study was on young adults.

Ethics Approval

The manuscript is not submitted to more than one journal. The submitted work is original and is not published elsewhere in any form or language. The paper reflects the authors’ own research and analysis in a truthful and complete manner. The results are appropriately placed in the context of prior and existing research.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.