Abstract

Purpose:

Bitcoin, the most popular form of virtual currency, currently holds the highest market capitalization among cryptocurrencies and serves as a benchmark for the typical cryptocurrency. The main goal of this research is to evaluate Bitcoin’s potential as a distinct asset class. This will be achieved by building upon previous studies and investigating its utility as both a hedging instrument and a tool for portfolio diversification.

Methodology:

In this study, Bitcoin is compared with other asset classes, such as key stock indices of India’s Nifty-50 and Sensex, and key currency pairs with the Indian Rupee, including the US dollar ($), Euro (€), Pound sterling (£), and Japanese Yen (¥). Gold, as one of the most precise commodities, is analyzed using descriptive statistics to verify and confirm its properties as a distinct asset class. Additionally, the study employs the DCC-GARCH model to ascertain whether Bitcoin qualifies as both a hedging instrument and a tool for portfolio diversification.

Findings:

The findings of this study indicate that Bitcoins constitute a unique and separate category within alternative assets and investment classes. Various descriptive statistics confirm that Bitcoins exhibit characteristics of an asset class. Additionally, the study reveals and verifies the hedging and portfolio diversification capabilities of Bitcoin based on the results of the DCC-GARCH model.

Practical Implications:

The findings of this study will prove useful for investors considering cryptocurrency (Bitcoin) as an alternative asset class for diversifying their portfolios and hedging against volatility.

Originality/Value:

This study contributes to the research paradigm of Bitcoin finance by providing a perspective from a developing nation on Bitcoin as an asset class, which differs from other asset classes such as Nifty-50, Sensex, USD–INR, EUR–INR, GBP–INR, JPY–INR, and gold. While previous research has predominantly focused on developed nation contexts, this study underscores the importance of examining Bitcoin’s role in portfolio diversification and hedging strategies. To enhance our understanding, this research presents daily observations of recent economic data spanning from 2011 to 2021. Assessing whether Bitcoin qualifies as an alternative investment and a distinct asset class is crucial, as it could significantly influence investment decisions and serve as a valuable tool for risk management and diversification purposes for investors.

Introduction

Bitcoin is a type of digital currency. It has gained vast popularity in recent years. Like any other currency, Bitcoins can be used for the purpose of storage, exchange, and investment. On the other hand, it is different from other major currencies such as dollar, Euro, Pound, and Rupee as it has a distinct decentralized structure and is an opt-in currency that moves as per the wish of its users. Bitcoin has some unique properties such as decentralized structure, limited supply, easy divisibility, and durability, which make it very useful and popular among its users. Along with these, it has a few more features such as easy transfer from one place to another and easiness of verification of authenticity.

Many experts believe that Bitcoin has all the essential features of an emerging asset class, making it more desirable and popular among its users. The properties incorporate holding value across existence for quite a long time and some genuine use cases (Baek & Elbeck, 2015). Use instances of cryptographic forms of money could be considerably more significant than the internet, which will come into the image in the further phases of the computerized upheaval. One more important characteristic of this asset class is unpredictability, which is an indistinguishable attribute of any developing asset class, as has been the case with oil. The instability of virtual assets such as Bitcoins would descend as it gets more immovably settled (Ram, 2019). The fear of missing out has additionally slid down from previously and will proceed as the crypto users gain maturity.

If we compare Bitcoin with one of the oldest and most popular asset classes, gold, then gold is a long-term value-creation asset and one of the most potent tools for hedging in adverse market situations. Although Bitcoin is relatively new and unproven compared to gold, its users repeatedly use it for speculation, storing value, and hedging against corrections and recessions. Even during the COVID pandemic and post-pandemic period, it has shown beneficial results as a hedging and diversification tool. Comparability and competition of Bitcoin with gold depend on risk-taking ability, investment goal, amount of investment, and strategy employed by the individual investor (Henriques & Sadorsky, 2018). We can differentiate between these asset classes based on their regulation, utility, liquidity, long ability, and volatility.

Many experts believe that Bitcoins are correlated with major stock markets around the globe, which makes them very useful for risk diversification, hedging, and portfolio management. Before the pandemic, there was only a weak relationship between the world’s most major stock indices and cryptocurrencies such as Bitcoin and Ether. This was the case even though Bitcoin and Ether are both digital currencies. They were recalled as helping distinguish risk and act as a buffer against the movement in other asset types. However, this changed after the alternative banking and currency crisis of mid-2020; the practices of involving Bitcoins and US stocks both mirrored simple worldwide monetary circumstances and more prominent investors’ risk appetite. The strong relationship between Bitcoins and equity indices is evident in developing economies such as India, a few of which have driven the way in Bitcoins reception. Increased Bitcoin-stock connections increase the possibility of financial backer opinion spillovers between those resource classes. The prolonged and considerable co-development and overflow between Bitcoin and value markets demonstrate the rising connectivity between the two investment vehicles, which facilitates the transfer of shocks that might harm financial systems.

In developed economies, many studies are conducted to check the hedging and safe investment properties of Bitcoins. Since its inception, Bitcoin has shown fundamental diversification properties concerning major stock indices worldwide. In the extreme market situation and in times of crisis, investors have shown strong faith in Bitcoin and other vital cryptocurrencies (Chen & Pandey, 2014). Let us look at the existing literature from emerging economies; very few studies have been conducted on the comparison and correlation of Bitcoin with major stock indices, commodity indices, and Fiat currencies of major global economies in the world.

Yermack (2015) and Dyhrberg (2016) explored Bitcoin as a tool for hedging portfolio risk and the possible use of Bitcoin for portfolio diversification and came up with opposite findings. Yermack (2015), in his results, suggested that Bitcoin does not appear to correlate with the vast majority of the world’s currencies, for example, the US dollar, Euro, and Pounds, and shows a very high degree of volatility. Therefore, it cannot be used for the purpose. Krueckeberg et al. (2018) explored cryptocurrency as a possible asset class. They concluded that cryptocurrencies such as Bitcoin show distinct characteristics of an asset class as they show internal cross-sectional correlation, absence of correlation with other asset classes, and required market liquidity. They also suggested that investors can manage portfolio risk by adding cryptocurrency to their investment portfolio. Liu and Tsyvinski (2021) conducted their study on three significant cryptocurrencies. They tried to analyze market capitalization, return, investor attitude toward these cryptocurrencies, momentum, and investor attention. They tried to establish that returns of these major cryptocurrencies are driven mainly by factors related to the cryptocurrency market specific to this distinguished market. In their study, they concluded that the return of cryptocurrency is caused by network factors, not by the production factors of these cryptocurrencies. They also concluded that the return of cryptocurrency is very minutely exposed and driven by other asset classes such as currencies, commodities, macroeconomic factors, and stocks. Their study found that cryptocurrencies such as Bitcoin show a very minimal correlation with many macroeconomic factors related to consumer and industrial economic growth.

Baur et al. (2018) concluded that Bitcoin is more speculative and shows a risky nature in volatile market situations. Therefore, it can be used as a tool for making a profit by risk seekers but cannot be used for hedging. Therefore, it is recommended that it is not helpful for risk-averse and retail investors. As far as a store of value nature is concerned, Bitcoin has minimal use in this direction (Yermack, 2015).

Walid et al. (2021) studied the role of various cryptocurrencies in portfolio management. They found the importance of cryptocurrency in achieving risk and return targets related to an investment portfolio. They specifically suggested that Bitcoin is the most valuable cryptocurrency as far as portfolio management is concerned. In addition, Ma et al. (2020) argued that portfolio construction should be done by including multiple cryptocurrencies. They presented the multilayer benefits of cryptocurrencies which can enhance the performance and manage the risk of an investment portfolio. While comparing different cryptocurrencies, they concluded that Bitcoin is not as helpful as Ethereum for achieving portfolio diversification. Similarly, Conrad et al. (2018) compared Bitcoin’s volatility with another financial asset. They suggested that Bitcoin negatively correlated with different financial assets, making it the perfect instrument for portfolio diversification. They also showed that during difficult market conditions and the downward market movement of the US stock market, Bitcoin showed less volatility.

Further, they suggested that Bitcoin is useful for portfolio diversification, hedging, and safe-haven investment during adverse market conditions. Wątorek et al. (2021) checked the volatility, liquidity, and diversification ability of various cryptocurrencies. They found that Bitcoin is one of the most liquid cryptocurrencies. They also found that it is not correlated with many traditional financial assets such as gold, equity, bonds, and commodities, making it the perfect choice for portfolio diversification and risk management. Ozturk (2020) analyzed the volatility and fluctuation of Bitcoin on a short-term, medium-term, and long-term basis. He found that as far as the short-term and medium-term volatility of Bitcoin is concerned, it is not helpful for diversification due to its highly volatile nature. On the other hand, in the long run, Bitcoin shows very minimal volatility and significantly less correlation with financial assets such as gold, crude oil, and bonds, which makes it perfect for achieving long-term diversification in the investment portfolio.

Therefore, this research aims to investigate whether Bitcoin is beneficial in the Indian context as a separate asset class, instrument for hedging, and diversifier. This study implicitly focuses on comparing Bitcoins with two major stock indices of India, the Nifty-50 and Sensex. Along with this, Bitcoins are also compared with major tradable currency pairs in India such as USD–INR, EUR–INR, GBP–INR, JPY–INR, and one of the most valuable commodities in India “Gold” through Gold-ETF.

The primary purpose of this research work is to check the eligibility of Bitcoin as an asset class, whether it can be used to hedge financial risk or not, and whether it can be used as a tool of portfolio diversification by investors or not. Various key descriptive statistics—measures of frequency, central tendency, and dispersion or variation—are used to compare Bitcoin with other key identified asset classes. The dynamic conditional correlation (DCC)-GARCH model is utilized in order to investigate the hedging, portfolio diversification, and safe investment properties of Bitcoins.

Methodology

As a result of the literature study, we were able to identify some research gaps, and based on those gaps, we developed two objectives for our research:

To investigate the possibilities of Bitcoin as a unique asset class and To analyze the hedging and safe-haven (diversification) properties of Bitcoin in the Indian scenario.

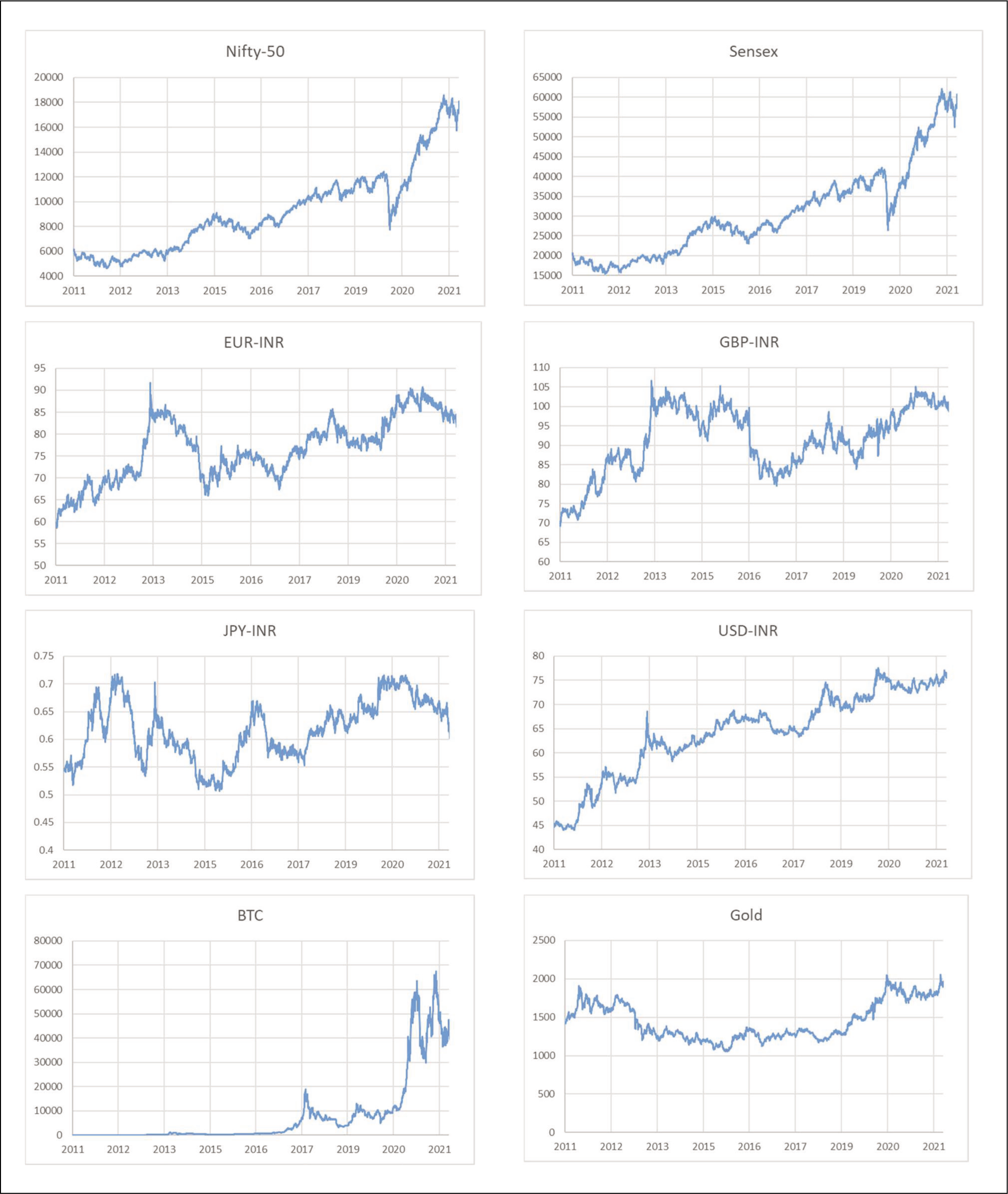

To achieve the above objectives, we have collected the daily closing price of Bitcoin, Nifty-50, Sensex, USD–INR, EUR–INR, GBP–INR, JPY–INR, and gold from January 2011 to April 2022 from Yahoo Finance (

Quotations of Selected Investment Instruments for the Period (January 2011–April 2022).

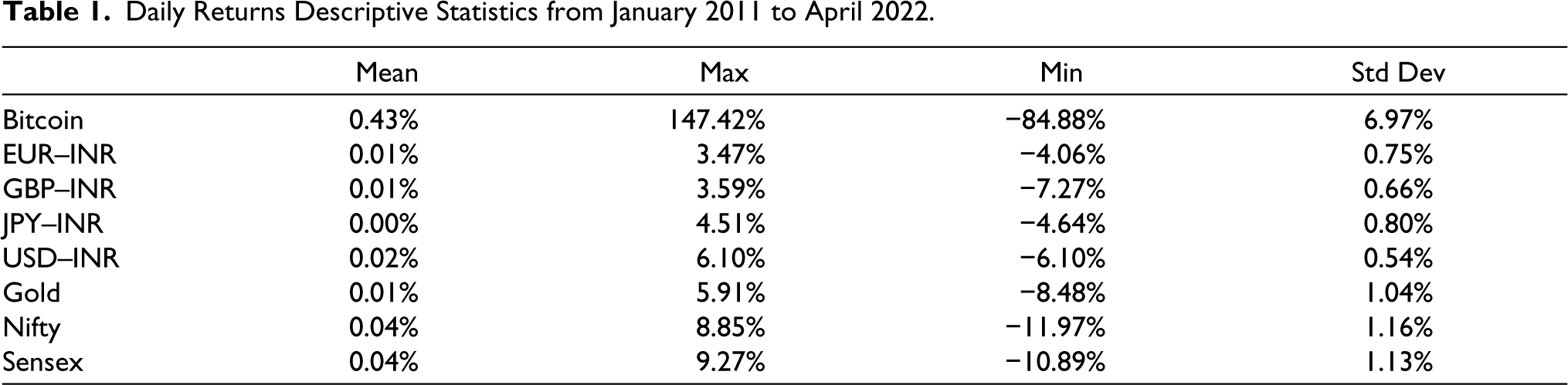

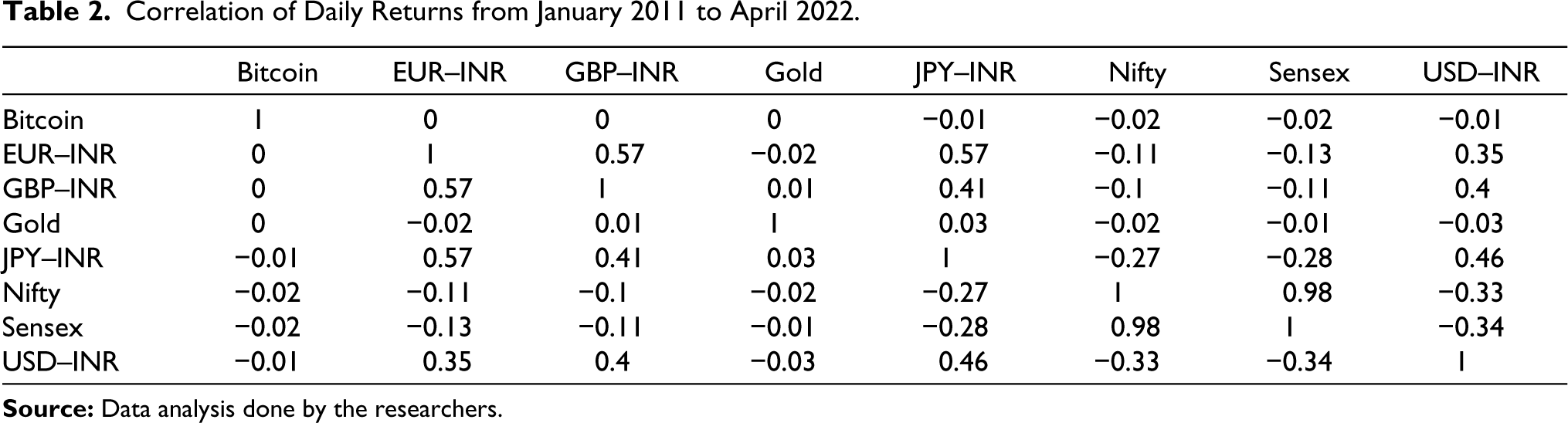

To investigate the possibilities of Bitcoin as a unique asset class, we have compared the descriptive statistics of Bitcoin with another asset (Table 1) and performed a correlation analysis (Table 2). The DCC-GARCH model was utilized to investigate the hedging and safe-haven qualities possessed by Bitcoin in the Indian context.

Daily Returns Descriptive Statistics from January 2011 to April 2022.

Correlation of Daily Returns from January 2011 to April 2022.

DCC-GARCH Model

The safe-haven and hedge literature for gold extensively uses DCC-GARCH. Over time, the returns on financial assets are known to be influenced by historical volatility and shocks to returns (Bollerslev, 1990). For many financial assets, the supposition that the correlation will remain constant over time is disputed, even if a poor correlation between investment results is essential for lowering portfolio risk (Bera & Kim, 2002). Some researchers use the ‘rolling regression’ or ‘exponential smoothing’ approach to account for temporal variant relationships. Although useful in some situations, both methods have flaws. Rolling regression overlooks the importance of earlier prior findings that are no longer within the rolling window and depends on similar weights for all observations inside the sample window. Rolling regression is inefficient in tracking sudden changes in volatility and necessitates an ad hoc method for choosing the breadth of the rolling window.

Additionally, due to the parameters’ fixed weights, exponentially weighted moving average (EWMA) models’ volatility estimations are insufficient. Although EWMA favors recent volatility estimates over older ones, the research has shown that the characteristics of Bitcoin can vary over time; thus, using relative weightings across various periods may not be acceptable in this scenario (Bouri et al., 2017a, 2017b).

Several other multivariate GARCH models, such as Baba-Engle-Kraft-Kroner parameterization of multivariate GARCH models and the constant conditional correlation (CCC), have been used to analyze the hedging and safe investing capabilities of a wide range of assets. These models are multivariate GARCH models. According to Bouri et al. (2017a), these models might have trouble converging, and they might also have unreasonable parameter estimates. The DCC approach, unlike the constant correlation model, permits correlations to be zero, positive, or negative. According to Lee (2006), DCC offers an accurate method for assessing changes in the co-movement of financial instruments, which may be utilized in time-series analysis.

The DCC-GARCH is an extended development of Bollerslev’s (1990) CCC model. This measures correlation and better captures the interactions between assets by allowing the correlation to fluctuate over time. Additionally, the coefficients of correlation of the standardized residuals are computed by the model, and the heteroscedasticity of the data is taken into explicit consideration (Chiang et al., 2007). We separately estimate the return-series pairs as mentioned by Bouri et al. (2017a, 2017b).

The DCC-GARCH model emerges as the most suitable choice amidst available alternatives for analyzing safe-haven and hedging properties of time series data. Traditional methods often assume constant correlations over time, a premise contested by empirical evidence. Rolling regression and exponential smoothing, while utilized, suffer from shortcomings such as inefficiency in tracking sudden volatility changes or inadequate volatility estimations due to fixed parameter weights. Likewise, other multivariate GARCH models such as Baba-Engle-Kraft-Kroner parameterization of multivariate GARCH models and CCC face challenges such as convergence issues and unrealistic parameter estimates.

In contrast, the DCC-GARCH model, an advancement of Bollerslev’s CCC model, addresses these limitations effectively. By allowing correlation to fluctuate over time, it better captures the dynamic interactions between assets. Moreover, it computes correlation coefficients of standardized residuals while explicitly considering data heteroscedasticity. This flexibility and accuracy make it a preferred choice for assessing changes in asset co-movements, especially in analyzing time-series data.

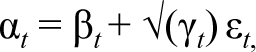

The calculation of the univariate GARCH model’s estimation (1,1) model and figuring out how to measure conditional correlations that change over time using the normalized residuals from step I are the first two steps in the process of estimating the DCC model, which directly defines the conditional correlations. Both of these steps are performed in order to directly define the conditional correlations.

As for the model, it is

A vector of prior observations is represented by the expression αt = (α1t, α2t, α3t, …,αNt, the multivariate conditional variance is denoted by γ t ; the vector of conditional returns for time t is given by β t = (β1t, β2t,…, β Nt ); the vector of the standardized residuals is εt = (ε1t, ε2t,…, εNt); the conditional correlations are included in a correlation matrix ρ t and Mt is a diagonal matrix that contains conditional time-varying standardized residuals (t). It is produced by applying the univariate GARCH (1,1) model with √(γ it ) positioned at the ith diagonal, where i = 1, 2, 3,…,N.

Further, the DCC is described as

where ρ t is the standardized residuals’(σ it = (ε t /√(γ it ) time-varying N × N covariance matrix and θ and λ are non-negative scalar parameters that meet the requirement that θ + λ < 1, and ρ’ is the unconditional correlation of σ it and σ jt .

We use the methodologies proposed by Ratner and Chiu (2013) and Bouri et al. (2017a) to investigate Bitcoin’s prospects as a diversifier, hedge, and safe investment against stock market volatility, regional indices, and commodities. This allows us to evaluate Bitcoin’s prospects as a safe investment against the volatility in stock markets, regional indices, and commodities. The DCCs between each asset and Bitcoin are extracted into a separate time series after DCC-GARCH estimation. Regression of DCC t on a dummy variable (V).

where V represents an extreme move, equal to 1, when the asset’s bottom 1st, 5th, and 10th percentiles of the return distribution indicate that the return has exceeded a predetermined threshold when Φ0 is considered positive, Bitcoin acts as a diversifier for other assets, when Φ0 is zero, it acts as a weak hedge for other assets, when Φ0 is significantly negative, it acts as a strong hedge, and when Φ1, Φ2, or Φ3 are marginally non-zero or significantly negative, it acts as a strong safe investment.

Results and Discussion

To investigate the possibilities of Bitcoin as a unique asset class, descriptive statistics have been applied to the daily return of all 8 variables; the result is mentioned in Table 1.

According to Table 1, Bitcoin has the most significant daily average return (mean) and most enormous volatility (standard deviation) compared to other asset indices. It also has the highest maximum and lowest minimum values compared to other indices.

The foundation of index trading is volatility. Volatility data are frequently used in the majority of index trades. Table 1 shows certain features of Bitcoin as an alternative asset class. According to an examination of its statistical features, Bitcoin might potentially be used as a tool for both hedging and speculating.

The variation in the volatility of these asset classes gives chances for portfolio diversification to reduce this volatility. We have conducted a correlation analysis among these indices to check the chances of portfolio diversification.

The correlation analysis among all eight assets has been performed and found that Bitcoin has a weak correlation with others. From the analysis of descriptive statistics (Table 1) and correlation (Table 2), it is implicit that Bitcoin is potentially a distinct asset class. This suggests that investors may use Bitcoin as a tool to diversify their portfolios or to reduce investment risk.

We investigated the hedging and safe-haven qualities of Bitcoin in the context of the Indian scenario using the DCC-GARCH estimate. Equation (3) was used to extract the paired DCC among each asset and Bitcoin, and then these correlations were translated into their own unique time series. Equation (4) regresses DCC t on a dummy variable (V).

The DCC (1,1)-GARCH (1,1) model measured with the t distribution provides the most athletic fit for the sample and best illustrates the fat-tailed nature of the return distribution obtained from the data, as determined by the Akaike information criterion and Bayesian information criterion. This model was estimated with the t distribution. The outcomes of the regression analysis using Equation (4) are shown in Table 3.

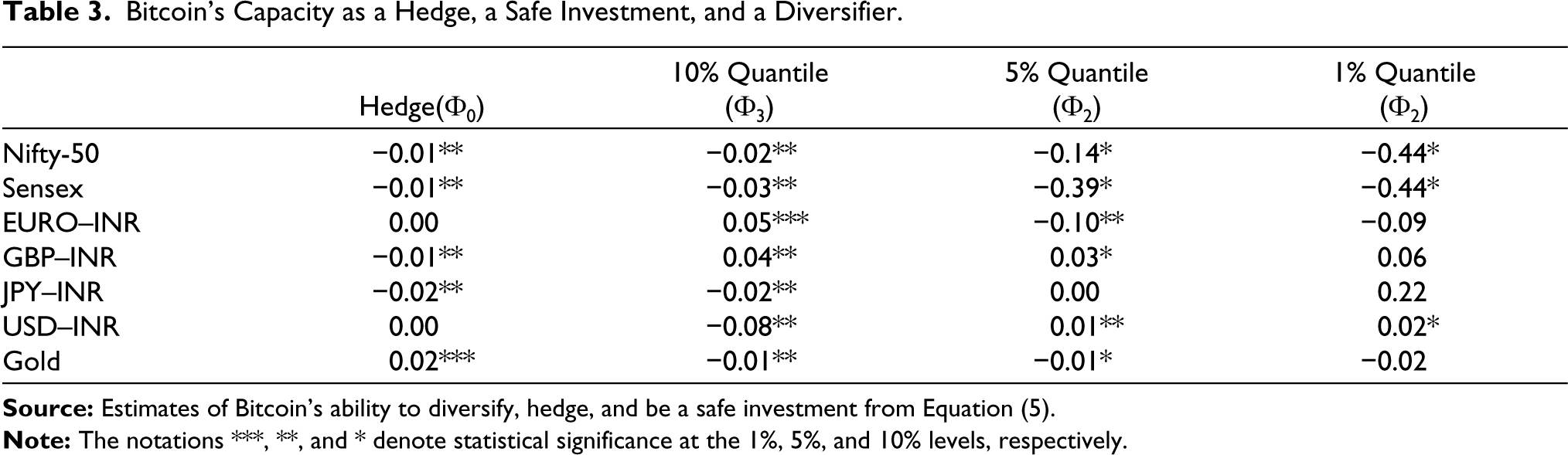

Bitcoin’s Capacity as a Hedge, a Safe Investment, and a Diversifier.

According to Table 3, Bitcoin has the potential to be an effective hedge for the Nifty-50, Sensex, GBP_INR, and JPY-INR as their coefficients (Φ0) are negative and significant and can act as a diversifier for gold as Φ0 is positive and significant and can act as a weak hedge for EURO–INR and USD–INR as Φ0 is zero.

As for safe-haven capability, Bitcoin shows strong, safe-haven properties for Nifty-50, Sensex, and gold at 10%, 5%, and 1% quantile as the value of coefficients (Φ1, Φ2, Φ3) is significantly negative; EURO–INR shows strong, safe-haven properties in case of 5% and 1% quantile, and JPY–INR and USD–INR show strong, safe-haven properties only in case of 10% quantile. Bitcoin shows weak safe-haven properties for GBP–INR, and the value of coefficients (Φ1, Φ2, Φ3) is significantly different from zero.

Conclusion

Based on the results of this analysis, Bitcoin demonstrates potential as an effective hedge for investments in Nifty-50, Sensex, GBP–INR, and JPY–INR, serving as a diversifier for gold, and offering a weak hedge for EURO–INR and USD–INR. Furthermore, this study explores the safe investment properties of Bitcoin, revealing its robustness as a safe investment option for Nifty-50, Sensex, EURO–INR, JPY–INR, USD–INR, and gold, although exhibiting weak safe-haven characteristics for GBP–INR.

This research suggests that investors seeking to hedge against market volatility in equities and commodities can consider incorporating Bitcoin into their strategies. The insights provided in this research could prove beneficial for central authorities and regulators in formulating appropriate regulatory frameworks and guidelines for cryptocurrency trading in the Indian market. Nonetheless, Bitcoin should not be perceived as a secure investment due to its limited liquidity and high volatility. The transfer of funds between Bitcoin and traditional financial instruments poses challenges owing to insufficient liquidity in the latter, such as stocks and commodities.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.