Abstract

Purpose:

This research attempted to reveal the impact of financial distress (FD) on the efficiency level of firms working in India. The objectives are as follows: (a) Obtaining the amount of consequence FD has on the efficiency of firms; (b) Assessing the effect of FD on the firms’ efficiency under the influence of technical efficiency.

Design/Methodology/Approach:

This article used the panel data method to analyse the data ranging from 2010 to 2019.

Findings:

The study’s results show a strong and positive relationship between FD and the operational efficiency of businesses operating in India. Additionally, in Shareholder Activism (SHA) most analytical models continually show a consistently positive and statistically significant. However, the Profit Before Interest and Tax (PBIT) impact remains statistically insignificant in all cases. Practical Implications: The implications of this research highlight an essential insight for potential investors, emphasizing the knowledge that FD have the potential to negatively impact a company’s market standing when they culminate in unfavorable circumstances, potentially leading to financial losses for invested capital.

Originality/Value:

As of now, there are no studies in the body of literature that support the moderating effects of two different variables—PBIT and SHA—on the relationship between FD and a firm’s operational efficiency.

Introduction

A companyʼs efficiency level does not depend on how much contribution is made by a few people working in that company; it depends upon how passionately each individual contributes to the firmʼs success. Maintaining adequate effectiveness and efficiency among different tasks performed in a company is one of the main aims of companyʼs management. A company can only survive for a more extended period if there is a watch on the efficiency level of employees. Many different events keep happening in the day-to-day routine of various firms that can either minutely or severely affect efficiency. The main factors that can critically affect a companyʼs functions are always present in the surrounding environment of businesses and corporations. Out of all the business environment factors, the study intends to observe the influence of FD on the firmʼs efficiency level in the current study.

Investors prefer to consider some factors according to their risk-bearing capacity before investing their hard-earned money in a company. Investors consider several factors before making an investment decision, and performance efficiency is among them (Rawal et al., 2022a). Potential investors do not generally prefer a firm that cannot handle its activities effectively. An inefficient company has built a bad reputation, resulting in low market value and low returns to investors.

FD refers to the difficulty a corporation faces regarding its economic position and inability to pay its obligation on time, leading to the consequences of winding up the firm (Kanoujiya et al., 2022; Outecheva, 2007). A firm is known to be distressed when it cannot clear its dues, does not meet day-to-day financial obligations, and breaches creditors’ trust (Foster, 1986; Rastogi & Kanoujiya, 2022). According to Beaver (1966) and Betker (1997), through its cost implications, such as increased cost of debt services and supplies (i.e., indirect financial distress [FD] costs) and increase in legal and administrative expenses related to the bankruptcy process (i.e., direct FD costs), the FD has a significant effect on the company profitability and operations. When the renowned company declares it is in a problematic condition, the real impact of FD has been seen in the market since the resulting stressful environment decreases all other companies for a while (Rawal et al., 2022b).

Few studies have been conducted that involve exploring the field of FD by applying it as a primary or secondary variable; however, many deep-level new topics still need to be present in distress. Thus, researchers worldwide keep disclosing new and novel findings. However, in companies facing distressing situations in the practical world, distressed corporations and firms have always been a global concern in economies (Rawal et al., 2022a). Nowadays, the count of financially disturbed firms is increasing at a more excellent pace, making it difficult for potential investors to decide their targets for effective capital allocation. However, no such study has been conducted as of now that has considered exploring the FD area by observing the direct and indirect effects of three different variables (Profit Before Interest and Tax [PBIT], shareholder activism [SHA] and efficiency). Thus, FD is a deep ocean of unexplored topics that must be focused upon.

This study investigates the effect of “Financial Distress” on the efficiency level of the firms operating in India. FD is considered an independent variable, whereas the article takes efficiency level as a dependent variable. Along with these two variables, PBIT and SHA are also included in the study as moderating variables to observe their moderating impact on the association between FD and efficiency. The firms’ data has been collected for ten years, from 2010 to 2019. The articleʼs objectives are listed as follows: (a) Obtaining the amount of consequence FD has on the efficiency of firms; (b) Assessing the effect of FD has on the firms’ efficiency under the influence of technical efficiency.

Every researcher starts working on a topic only when motivation or proper gaps are present in that field. As far as this topic is concerned, some of the motivating factors for the conduction of this study are as follows. One of the worldʼs leading, fastest-growing economies is India. Thus, it is high time to focus on all the unattended fields that can affect the proper development of the economy. Second, no such article has come to our knowledge that has attempted to study the impact of FD on the efficiency of firms. Hence, the current report has tried a comprehensive investigation of distress conditions.

This article also accounts for some contributions in the field of FD. First, this is the first study that involves exploring the direct impact of variables on each other and includes the concept of moderation. Second, future researchers can consider this study as a base while aiming to conduct their respective studies on the same topic. Last, the study helps the managerial division of companies understand how important it is to concentrate on maintaining the efficiency level of employees while working, or else critical consequences are faced by the whole firm for negligence in maintaining the adequate level.

Following that, the articleʼs structure develops as follows: A thorough literature review that clarifies the background is included in the following section. Then, in addition to a tabular display of the results, an explanation of the data, methodology, and models used follows. After the data have been presented, a thorough examination of the results is given. The latter sections of the study include a review of the inherent constraints and a summary summarizing the results.

Literature Review and Hypotheses Development

FD and Efficiency

Efficient corporations and firms are not required to promote their potential and capabilities to look attractive to the people. The efficiency level of the firms can be seen by the increase in market value and demand for the firmʼs share in the market by the investors. The organization has to plan appropriately and coordinate to become a fully efficient company. In actuality, the company cannot obtain efficiency after only working on some parts of the company as people think. In some cases, the impact of various external factors such as inflation, FD, or many other factors unfavorably affects the companyʼs performance even after the company works with proper coordination. In such a situation, no one can prevent it from being struck.

This study has gone through some essential articles in this area to analyse the severe impact of external factors such as FD on the efficiency level of the firm. Beginning with the oldest study to examine the relationship, Wruckʼs (1990) research stated a negative association between organizational efficiency and FD. Shahwan and Habib (2020) conducted a study on the market in Egypt and identified that their efficiency score negatively affects the probability of FD. Many other studies, such as Wu et al. (2021), Wanke et al. (2015) and Shagerdi et al. (2020), got the same kind of result after being conducted at different times and in other countries.

Various studies have been carried out so far to detect the significant impact on the efficiency of the firms. Despite that, none of them aimed to explore the association between FD and efficiency in the firms operating in the Indian market till now. This gap is quite enough to support its involvement in this research. FDʼs impact on firms’ efficiency levels is empirically tested to frame the hypothesis for this study.

H1: A significant impact of a firmʼs financial distress on the firmʼs efficiency.

Interaction of SHA on the Association of FD with Efficiency

SHA has been regarded as a reliable source of monitoring. As per Pound (1992), a study analyses that investors look for other options to monitor the companyʼs management and performance, and SHA is the inevitable result of a restrictive external market for corporate control. In recent years, SHA brought the resolutions submitted to management by individual investors and significant social investors, pension funds, institutional investors, and labor unions (e.g., Schwab & Thomas, 1998; Smith, 1996). Regarding the association between FD and SHA, some published work can be uncovered (Barros et al., 2021; He et al., 2017; Jory et al., 2017; and others). However, none of the studies have explored the relationship between SHA and efficiency.

A wide range of literature discusses FD, SHA, and efficiency separately or combines any of the two variables. However, work that finds the moderating effect of SHA on the association between FD and the efficiency level of corporations has not been conducted before. This gap in the field of FD motivated us to pursue our research. Therefore, hypotheses have been framed to examine this understudied problem and induce some discoveries.

H2: Shareholder activism moderates FDʼs association with firms’ efficiency level.

Interaction of PBIT on the Association of FD with Efficiency

PBIT is considered one of the most important ratios to be focused upon while measuring a firmʼs performance. PBIT is calculated as a companyʼs sales minus its interest expenses but not subtracting its tax liability and interest paid (Brush et al., 2002). Many studies are accounted for in PBIT by involving different variables. However, no such research has come to our notice that focuses on the interacting effect of PBIT on the association between distress and efficiency of firms. Thus, to meet this significant research gap in this field, empirical hypotheses have been constructed to investigate this unexplored area and generate some novel results:

H3: PBIT moderates FDʼs association with firms’ efficiency level.

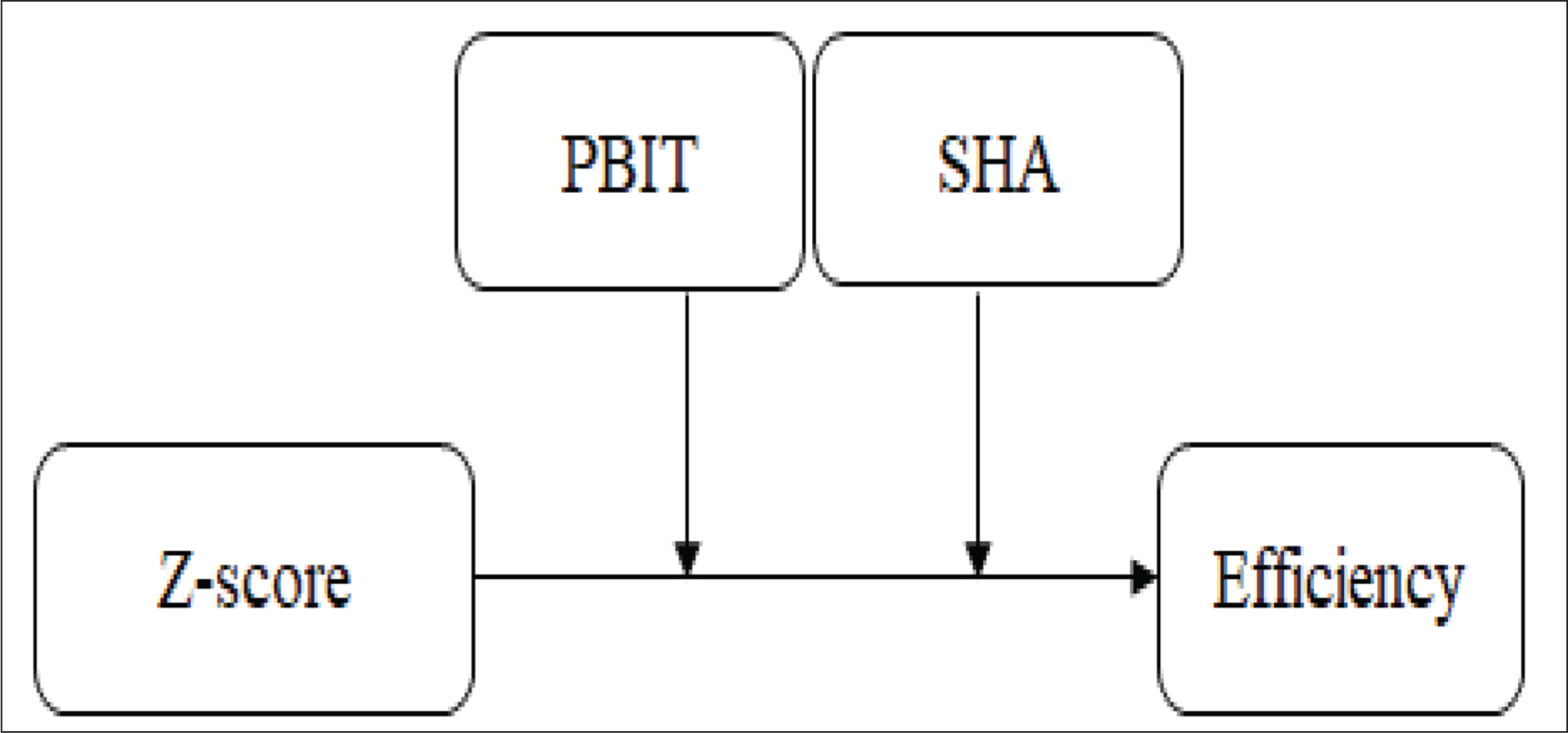

In order to understand the topic of this articleʼs focal point, a hypothesis has been developed after a thorough assessment of the relevant literature. The current study intends to develop a conceptual framework that outlines the relationship between FD and organizations’ levels of efficiency, with the moderating influences of PBIT and SHA. This conceptual framework, which is illustrated in Figure 1, visualizes the theoretical framework supporting the research endeavor.

Data and Research Methodology

Data

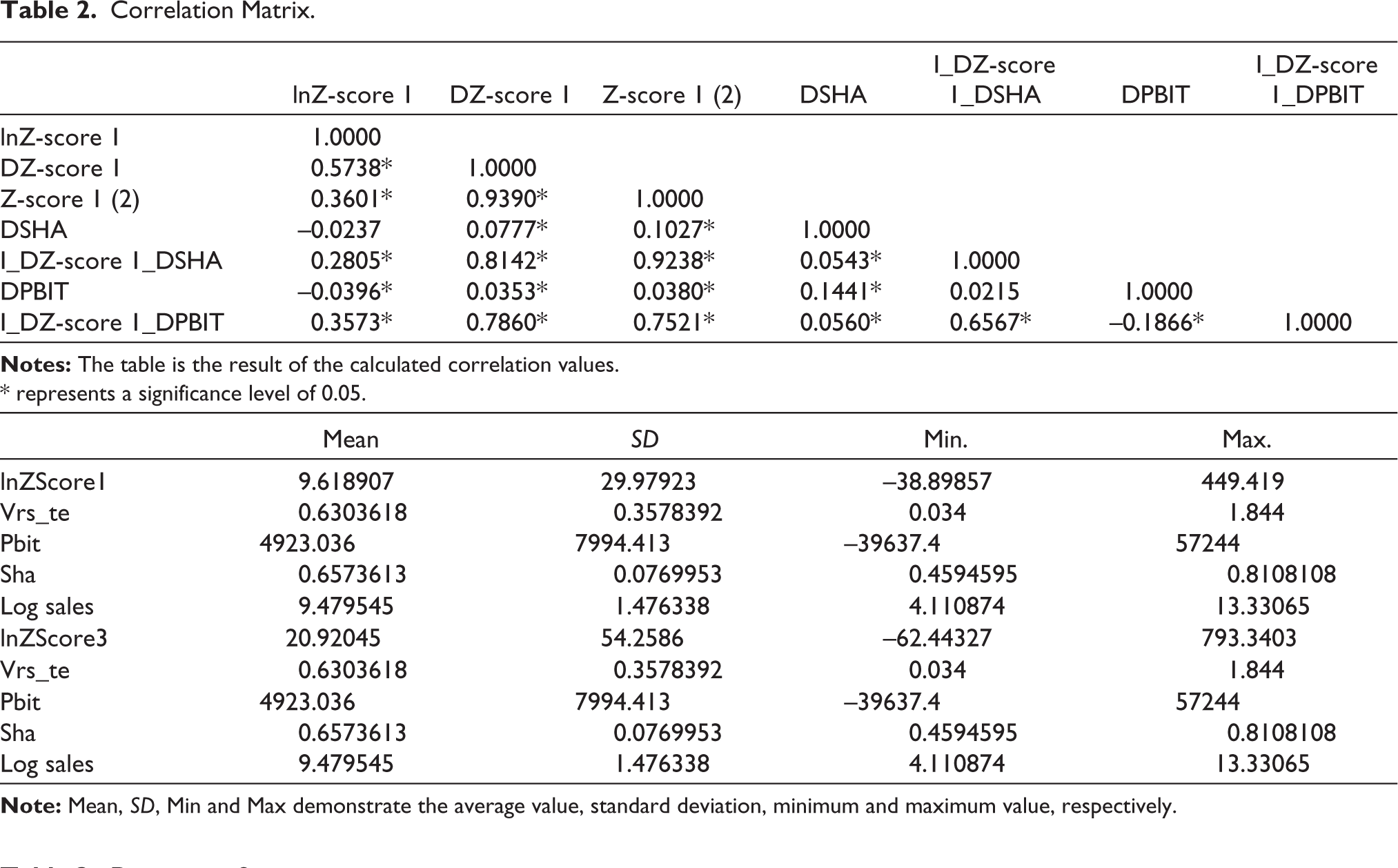

The current study involves data from 76 firms working in the Indian economy. The collected data of each company is secondary as it is retrieved from CMIE Prowess as well as the companyʼs yearly reports of the selected companies. The analysis has been performed by considering the data for ten years, from 2010 to 2019. The primary reason behind involving 76 firms working in different sectors is to obtain reliable results. The bigger the sample size, the higher the probability of getting better and more robust outcomes. A variety of variables are used in the article. A brief description of each variable is given below in Table 1.

List of Variables.

*indicates a moderating variable. CV represents the control variable.

Research Methodology

The analysis performed for the retrieved data has been done with the help of a panel data model (PDM). As per some academicians such as Hsiao (1985) and Baltagi and Baltagi (2008), the PDM contains features of both the cross-sectional and time series analyses. Thus, it is better to use panel data analysis to perform the analysis and obtain many robust results afterwards. In the current study, a total of 16 models have been developed. The independent variable, FD, is divided into two factors, Z-score 1 and Z-score 3. In addition, the dependent variable, efficiency, is also segregated into parts- crs_te and vrs_te. Therefore, the first eight models are related to Z-score 1 with vrs_te and Z- Z-score 1 with crs_te, respectively, whereas the other eight models are developed with the help of Z-score 3 with vrs_te and Z-score 3 with crs_te. The models are in the following order- examining the base association (Baltagi, 2015; Baltagi & Li, 2002), then the other model examines the quadratic association (Arellano & Bonhomme, 2009; Baltagi, 2015), and finally, model investigating the interaction effect (Baltagi, 2015; Cheng, 2007) of the moderating variable (PBIT and SHA) on the independent and dependent variables. The same type of model has been developed using the other independent variable (z-score3). The model specifications are as follows:

Where first four equations are related to the Z-score 1 term of fd, whereas the other four equations are used to show the z-score 3 terms of fd. Therefore, the yit represents the studyʼs dependent variable, the efficiency of the companies I, at the time of t. Z-score 1 and Z-score 3 are included as explanatory variables. Furthermore, the moderating variable used in the study is included in Equations (4) and (8), which is PBIT and SHA, respectively. Log of sales is also included in the study for a better fit as a control variable. Lastly, the α is the constant term and α is the error term in the models.

The same kind of base, quadratic, and interaction equations are performed for the other 9 to 16 models. The only difference is that the Z-score 3 term of FD is used in the models.

Empirical Results

Descriptive Analysis and Correlation

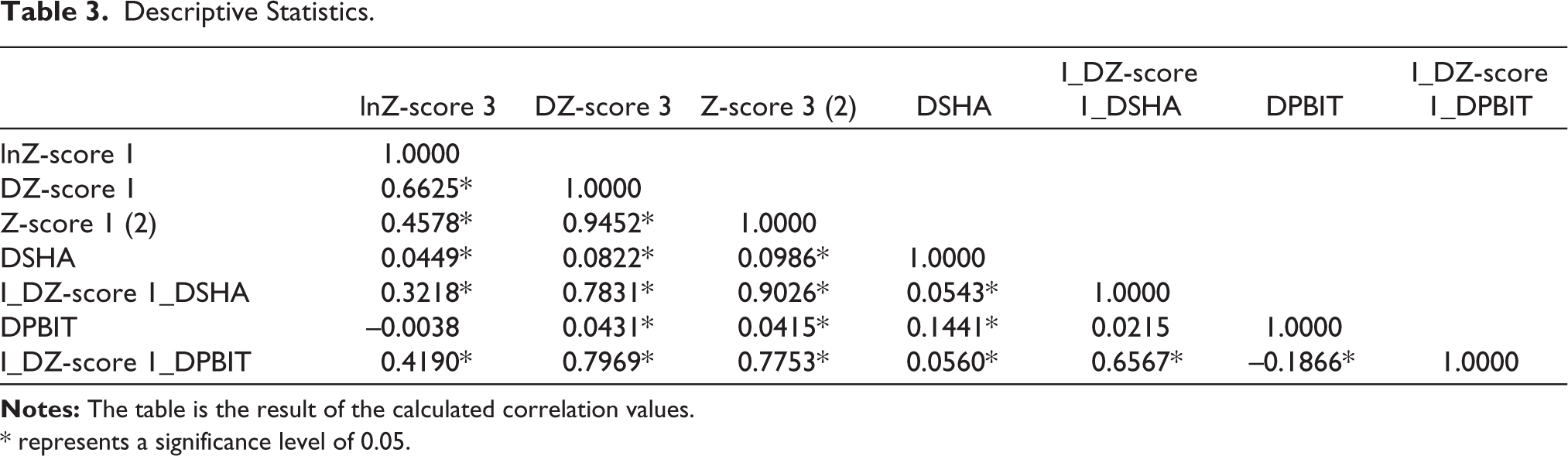

Tables 2 and 3 represent correlational values among the variables and the description of the statistics, respectively. As per the correlation matrix, the explanatory variable, Z-score 1 and Z-score 3, positively correlate with other variables except for the dmean of SHA and dmean of PBIT. Many factors are present in both tables that have significant correlations with a value of more than 0.80. Hence, the multicollinearity problem is not retrained in all cases (Baltagi & Baltagi, 2008).

Correlation Matrix.

Descriptive Statistics.

* represents a significance level of 0.05.

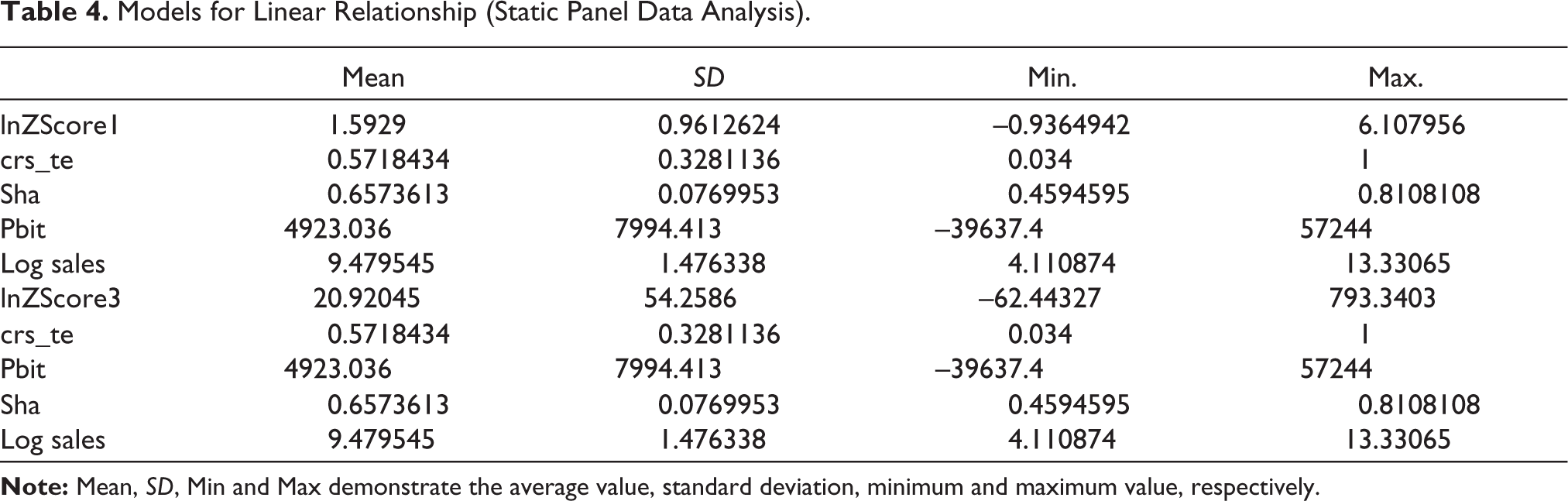

Table 3 demonstrates the statistical value of the variables. As per the first part of the table, the average value of a dependent variable, vrs_te, with a Z-score of 1, is 0.630, indicating a low quality of efficiency among the working employees or performance of other functions in the firm. The mean value of Z-score 1 is a moderate to high range of 9.61. In contrast, the mean value of Z-score 3 is approximately 20.92, which means a high probability of the occurrence of distressing conditions is possible in the firms. Of all the variables, PBIT has the highest mean value in the table, that is, 4923.06.

The other part of the table, which depicts the statistical values related to crs_te (another part of efficiency), is discussed in this part of the description as the average value of crs_te is low, that is, 0.571, which shows that a low quality of efficiency is present in the sample companies. The mean value of Z-score 1 is in the moderate range, 1.59. In contrast, the mean value of Z-score 3 is approximately 20.92, which means a high probability of the occurrence of distressing conditions is possible in the firms. In addition, the highest average value in this table is also PBIT.

Regression Estimation

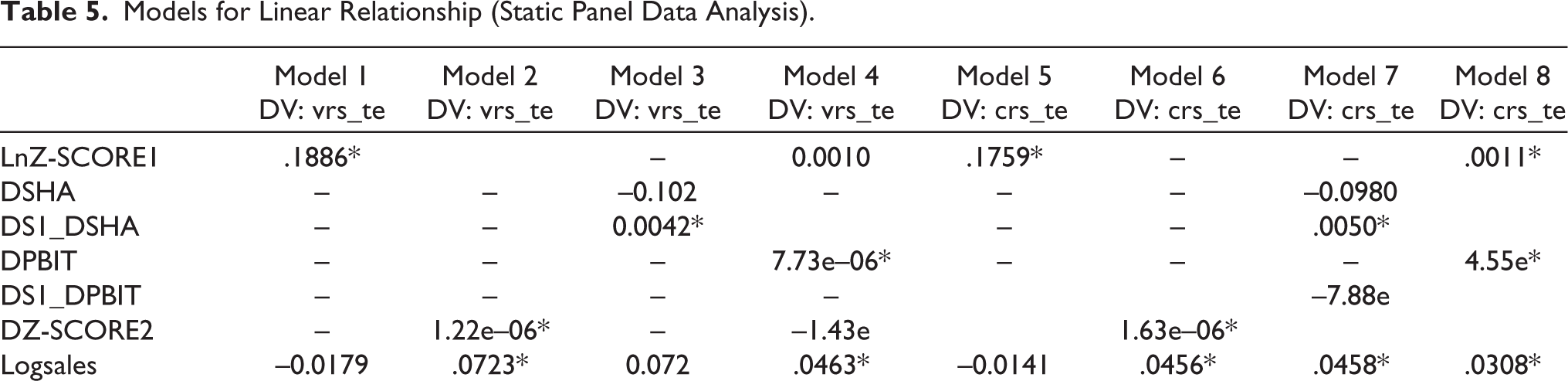

Table 4 represents the results for Models 1 to 8 to examine the relationship between the two groups. The first group (models 1 to 4) is Z-score 1 with vrs_te. The second group (models 5 to 8) is of Z-score 1 with crs_te. This study shows that the first four models are related to the first component of FD, Z-score 1. The F- and BP tests have been applied for fixed and random effects. Both of them are significant as p value (<.05), resulting in the application of the Hausman test. Models 1 and 5 are compatible with FE, whereas models 2, 3 and 4 show. Furthermore, as per the analysis, all the models except model 4 and 8, which belongs to the interaction variable, PBIT, are significant. Therefore, there is a significant and positive relationship between Z-score 1 and vrs_te and crs_te in all the other models, excluding 4 and 8.

Models for Linear Relationship (Static Panel Data Analysis).

As per the quadratic and interaction models, the coefficient value of the square form of score 1 is 1.22e and 1.63e, respectively, for both vrs_te and crs_te. However, with a p value <.05. Thus, as in models 2 and 6, there is a significant relationship between Z-score1 and vrs_te and crs_te. In models 3, 4 and 7, 8, this study tried to analyse the association between dependent and independent variables under the moderating impact of SHA and PBIT. As per the model, the interaction is significant with the p value of .000 but only SHA. Thus, this study also considers the nature of the effect of SHA as a moderating variable, which is significant.

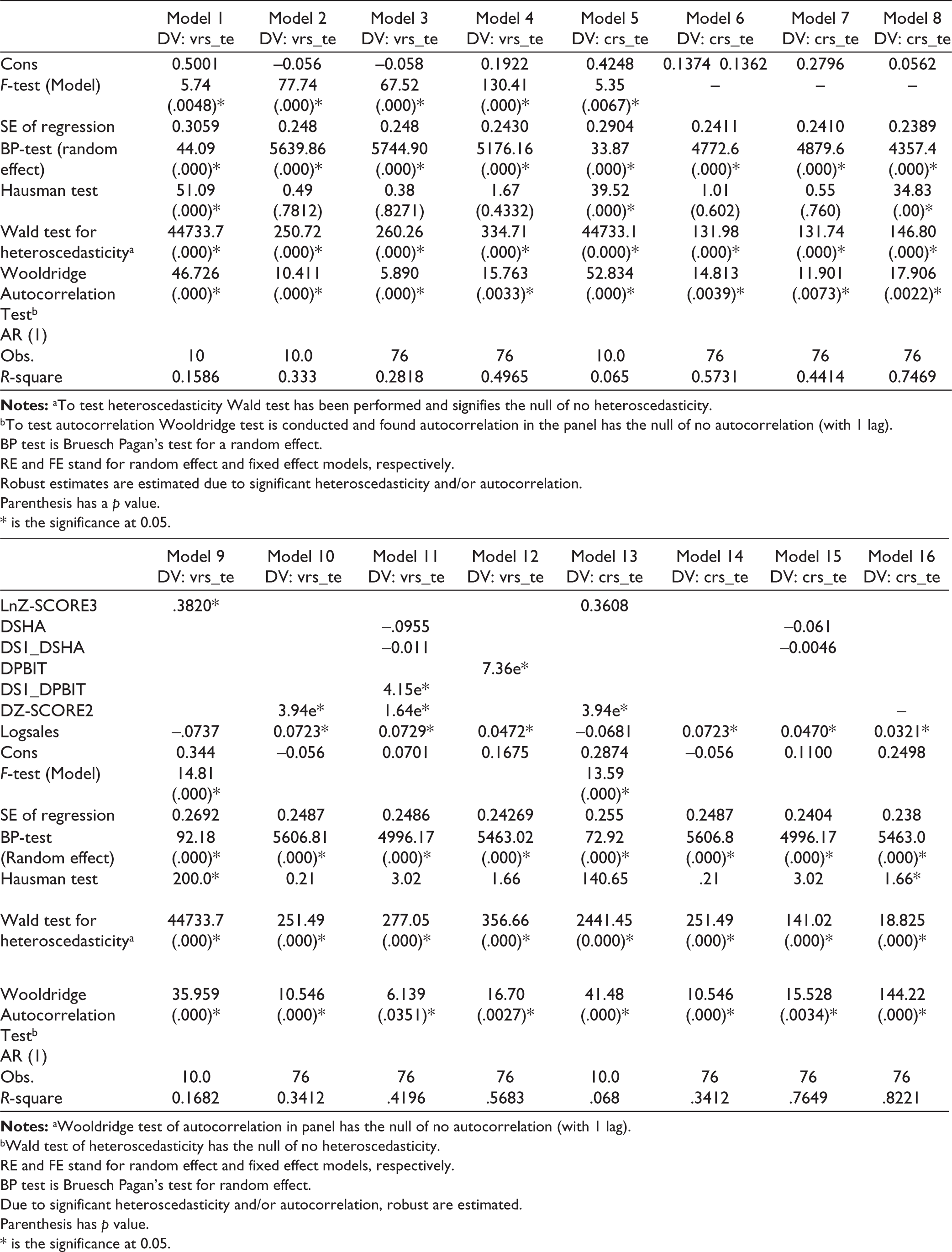

In models 9 to 16, the same kind of results have been obtained from the analysis. The F-test and BP test have been applied to determine the type of effect, respectively. Both of them are significant as p value (<.05), resulting in the application of the Hausman test. Thus, the 9 and 13 model shows compatibility with FE. Similarly, the base model with coefficient values .3820 and .3608 represents the significantly positive association between Z-score 3 with both crs_te and vrs_te.

Further, the importance of square or quadratic models also represents significant associations between the independent and dependent variables. Lastly, the interaction model shows an insignificant interacting effect of SHA on the association between Z-score 3 and efficiency factors (crs_te and vrs_te). Regarding PBIT, it is always insignificant in all the models mentioned above, but it is marginally significant in case 12. In contrast, it is fully significant in nature in model 16 where the factors involved are Z-score 3 and crs_te.

Robustness and Endogeneity of the Results

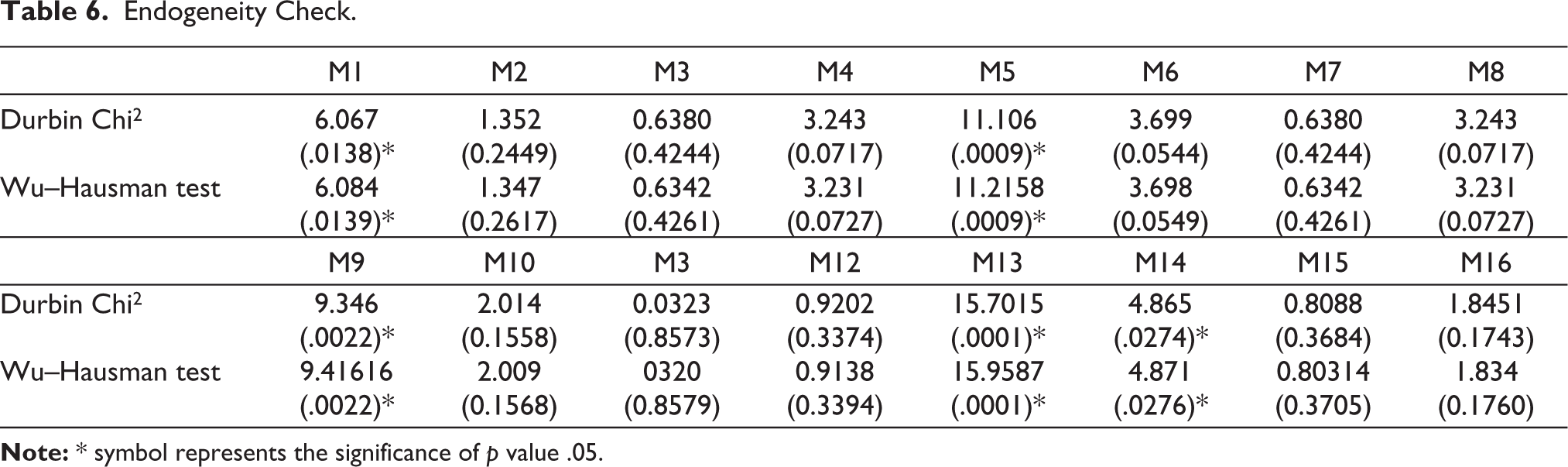

As per Table 5, the Durbin Ch-square and Wu Hausman test having significant p values confirm that there is an endogeneity issue among all the models except some models in the study. The results show that all the models resulted in insignificant p values (except models 1, 5, 9, 13, 14). See Table 6. Hence, the tests proved that the null of no endogeneity is rejected in almost all the cases, and the robustness results are guaranteed (Kanoujiya & Rastogi, 2022).

Models for Linear Relationship (Static Panel Data Analysis).

bWald test of heteroscedasticity has the null of no heteroscedasticity.

RE and FE stand for random effect and fixed effect models, respectively.

BP test is Bruesch Pagan’s test for random effect.

Due to significant heteroscedasticity and/or autocorrelation, robust are estimated.

Parenthesis has p value.

* is the significance at 0.05.

Endogeneity Check.

Discussion

Hypotheses Testing

The significance of two of the three hypotheses included in this research cannot be dismissed in accordance with the methodological framework used in the present study. According to the results of our investigation, FD, notably vrs_te and crs_te, exhibit a linear relationship with FD (with z-scores of 1 and 3). This outcome means a significantly positive relationship exists between FD and efficiency (H1). Second, SHA significantly moderates the association between FD and the efficiency level of firms (H2) in almost all the models except in model 11 and model 15. Lastly, PBIT insignificantly moderates the association between FD and efficiency, except in model 16. Thus, H3 has been rejected in almost all the cases as per our analysis.

Comparison with the Earlier Work

FD is one of the well-versed areas, and several research has been carried out till now. However, quite a few researchers have concentrated on observing the immediate effect of the distressing situation on the efficiency level of companies. Shahwan and Habib (2020) researched the firms operating in the Egyptian market and confirmed that FD is likely to affect efficiency scores among the firms negatively. Similarly, in their study, Wruck (1990) claimed a negative association between FD and organizational efficiency. In contrast, another study by Vosoughi et al. (2016) performed a survey on the firms dealt in on the Tehran stock exchange, examined the relationship between investment efficiency and FD, and found a correlation of a positive nature between investment efficiency and FD. Various research has been conducted on multiple nations across the globe. But when it comes to one of the fastest-growing economies in the world, India, no such correlation between FD and efficiency has yet to be researched. In addition to the effort to clarify potential relationships between FD and efficiency, our work has broadened its focus to examine a different aspect: the moderating impact of PBIT and SHA on the relationship between FD and efficiency. In terms of the current study, this novel aspect of association has not yet been investigated.

Contribution

Despite various results established by researchers in their respective studies, the current studyʼs findings are new and novel. First, this study provides evidence of the natural interaction effect of PBIT as a moderating variable on the association between the two major variables included in the study, that is, FD and efficiency. This addition of a new aim, along with finding the direct impact of dependent and independent variables, has not been seen in other studies until now. Therefore, the concepts used in the present research have given new and interesting evidence in the area of FD.

Implication

The current report has some research implications along with the novelty and new findings. First, after going through this article, companies working in a developing country like India can understand how devastating consequences can occur for an extended period if they do not focus on maintaining a proper level of efficiency in the company. The more the company becomes careless about being efficient, the more chances that the company can become bait for a distressing situation or other critical business environment factors. Second, potential investors also learn about FD from their point of view on how a distressing situation can destroy a companyʼs whole system and image in the market, thus leading to the loss of money they have invested. Hence, an investor should choose to invest somewhere only after thoroughly reviewing each piece of information by the company.

Conclusion, Limitations, and Future Scope

The main aim of this study is to supplement new novel findings in the field of FD. While analyzing the data of companies operating in the Indian market. As per the studyʼs first aim, a positively significant relationship exists between FD and the efficiency of Indian firms. Second, the moderating impact of SHA on the association between FD and efficiency is also positively substantial in every model except for models 11 and 15. Furthermore, the conclusive aim of this research is to examine the moderating impact of PBIT on the association between FD and efficiency. The result was that the effect was insignificant in all cases except in the 16th model. Hence, the results discussed above also provide insights to the companyʼs management, stakeholders, and potential shareholders while making decisions about investing in the future and capital allocation.

The present study cannot be summarized worldwide as the association between variables has been observed only in the firms working in the Indian market. Additionally, the small size of companies is another limitation. Therefore, future researchers can consider investigating this kind of association between FD and efficiency in different kinds of firms established in multiple countries. As the issue of distress is quite devastating for the image of a company, thus, more investigation should be made into this area in future studies.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.