Abstract

Micro, small and medium enterprises (MSMEs), which are business activity units that run businesses in several fields, are vital for the economies of several countries. Credit access (CA) is regarded as an important matter for MSMEs’ growth in the development and sustainable growth of MSMEs. In the financial sectors, the government’s role via policies like augmenting MSMEs’ credit becomes completely significant. For evaluating CA towards MSMEs in Kerala, this study was developed. Analysing the challenges in accessing credit in MSMEs is the aim. For evaluating the outcomes, a simple random sampling methodology was deployed. In Kerala, the impact of credit knowledge was significant on MSMEs’ CA. As per the outcomes, a greater probability of augmenting loan access is engendered by the factor of challenges in attaining private equity funding and high lending interest rate.

Introduction

MSMEs, which have a huge contribution towards realising national economic enhancements targets like economic growth, employment opportunities and regional economic development, are significant sectors (Sisharini et al., 2019; Valeriani & Putri, 2020). For emerging economies as of the viewpoint of employment and innovation, MSMEs are frequently regarded as the ‘engine of growth’ (Madan, 2020). The initial individual comprehensive legislation covering every segment is the MSME Development (MSMED) Act, 2006 in India. MSMEs, which are accepted globally to promote equitable growth in the company, are a significant segment of the Indian industrial setup (Padmanabhan, 2021). Due to MSME’s limited access to alternative sources of finance, credit is a significant input to promote its development as per the 12th 5-year Plan in India. In emerging markets globally, close to 45%–55% of the formal MSMEs of 11–17 million do not have access to formal institutional finance as per the International Finance Corporation (IFC) (Choudhury & Goswami, 2019; IFC, 2013). The MSME sector had emerged to depict the Indian entrepreneur’s capability for innovating along with creating solutions regardless of the challenges with a continuous growth rate of over 10% recently. The inter together with the economic power of huge enterprises are encouraged by the enhancement of an MSME (Ottoman, 2018; Suidarma et al., 2018).

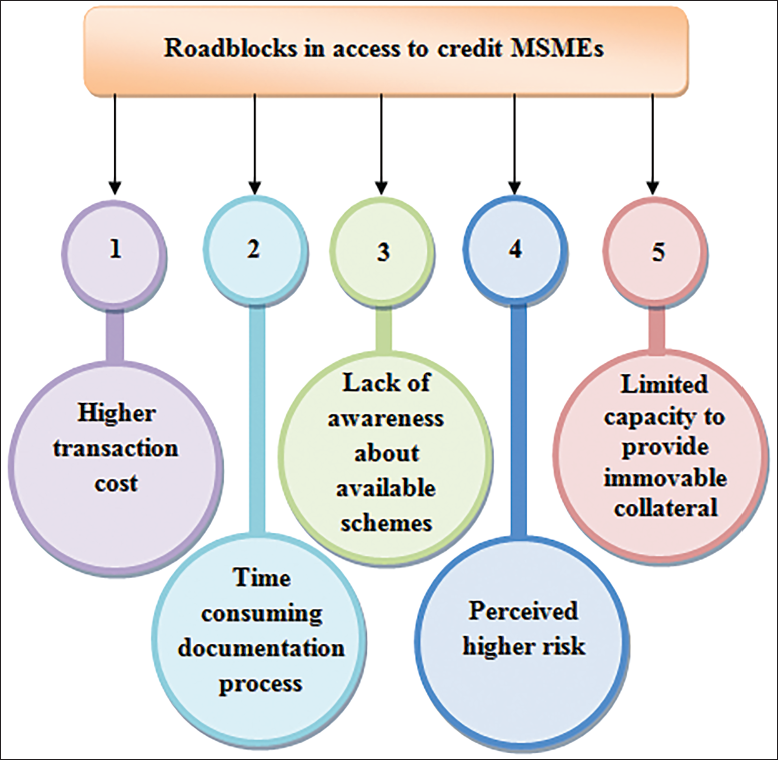

One among the key means to address and challenge the insufficient function, which is present in the small and medium enterprises (SMEs) sector with the fact that MSMEs are the hidden agenda of industrial development and growth in many lower-middle income countries, is termed bank credit. Micro and small enterprises (MSEs) are encompassed in the Reserve Bank of India in the priority sector list for lending as banks are the principal sources of finance in India. In credit to MSE, banks have to attain 20% year-on-year growth; in addition, in microenterprise accounts, it has to attain annual growth of 10%. For supporting this sector, novel policies are made by the Government of India, especially for the smooth flow of credit to this sector (Mund, 2020; Ssempala & James, 2018). The credit access (CA) was evaluated towards MSMEs. Analysing the challenges in access to credit (ATC) in MSMEs from the banker’s perspective is the aim. For analysing CA towards MSMEs, a well-structured questionnaire was done. In Figure 1, the diagrammatic representation of unblocking CA to MSMEs is depicted.

Credit Access to Micro, Small and Medium Enterprises (MSMEs).

The remaining part is arranged as: The related work is depicted in the next section, followed by elucidation of research methodology; the results are expounded in the subsequent section; the article is concluded in the final section.

Related Works

This section presents the survey of recently conducted research studies to identify the CA towards MSMEs and challenges in ATC in MSMEs.

Choudhury and Kashyap (2020) evaluated the influential factors that detect the challenges in MSMEs by banks. In Assam, from 172 banks with the highest concentration of MSMEs, data were gathered. For analysing whether the average individual difficulty scores were similar across several banks, the Kruskal–Wallis test was done. The study indicated that the factors which were detected to deter banks from lending to the sector were the difficulty in recovery and scarcity of trained manpower, high average cost on loans, information asymmetry and hassles with repayment. Maumita (2018) analysed the characteristics of MSMEs operating in the rural villages in Assam. Whether the MSMEs were registered with District Industries Centres (DIC) was evaluated. From the 100 sample units registered and not registered under DIC, a sample of data was collected. For choosing the samples from the registered MSME units, a random sampling (RS) method was wielded. The result showed that the borrowers’ satisfaction with the source of finance, satisfaction with the amount sanctioned, along with the average challenge in acquiring loans as of the bank were not influenced by the registration. Kavitha and Gopinath (2020) explored the initial challenges that small businesses regard while implementing a bank loan. From 280 small-scale businesses in Tamil Nadu, data were collected. A judgement sampling was done for evaluating the gathered data. Structural equation modelling (SEM) was wielded for scrutinising the linkages betwixt the construct in the conceptual model. Finally, it concluded that the ‘nine’ aspects small businesses perceive to be important when implementing a loan were depicted. Further, it showed that for attaining working and fixed capital needs, sufficient funds were required. Ratnawati (2020) examined the influence of financial inclusion on MSMEs’ performance; in addition, appraised the mediation role of financial intermediation (FI) along with ATC. From the 100 MSME actors in Malang, data were gathered. For appraising the engendered hypotheses, partial least squares (PLS) was deployed. It revealed that the MSMEs’ performance was influenced directly along with indirectly by financial inclusion via mediation as of FI together with ATC. Kustina et al. (2018) evaluated the MSMEs’ credit variable to non-performing loan (NPL) variable and the MSMEs’ credit variable distributed to profit variables. In banking companies, for the profiting variable via NPL, the effect was detected indirectly in MSMEs’ credit variable. From MSMEs’ 15 largest credit banks in Indonesia, secondary data were gathered. Then, the hypothesis was engendered along with tested. The analysis of the study showed that there was a considerable positive effect on the banking company’s profit by the amount of MSMEs credit. Athaide and Pradhan (2019) examined credit limitations by employing a standard system in the huge constrained MSMEs sector in India. For the financial years 2004–2010, from the Centre for Monitoring Indian Economy (CMIE) prowess, the data were grouped. The study demonstrated that the enhanced probability of being credit constrained was included in the firms with minimised working capital cash flows, minimised gross fixed asset formation, along with a lower ability to leverage. Nair and Gopal (2021) evaluated the MSME sectors’ financial access concerning the food processing unit in Kerala. By employing the collected MSME owners’ responses, financial access was explored. From the 879 owners of food processing MSME sectors, questionnaire data were collected. Thus, the denial of loans by the banks and financial institutions grounded on low capital, sales turnover and inexperience were analysed. As per the outcomes, the MSME sector’s financial access was sturdy. Experience and turnover maintenance were the key factors to access finance from the bank in addition to other financial institutions. Raheem and Meera (2018) analysed the MSME access to funding and working capital financing issues in Malaysia. From the population of MSMEs in Klang Valley, a sample of data had been collected. For the analysis of the data, stratified sampling was used. The study revealed that the access to financing, heavy competition from peers and production and labour costs were the main issues for MSMEs in the Klang valley. Schmidt and Hoffmann (2019) examined the guarantees deployed in innovation’s refundable financing in MSME enterprises. A semi-structured interview was done. From the players’ perceptions of Santa Catarina’s innovation ecosystem, the data were grouped. The Regional Bank for the Development of the Extreme South (BRDE) was aided to consolidate itself as innovation’s key financing agent in MSMEs. The study of the result showed that the innovative MSMEs accessing credit and the prevailing guarantee play a considerable role in MSMEs sector. Mbowe et al. (2020) assessed the level to which financial modernisms contributed to enhance MSMEs’ ATC in Tanzania. From 318 respondents, questionnaire data were gathered. For the factor’s robustness check, which influences the MSMEs’ borrowing behaviour, the probit estimates were wielded. The result indicated that the requirement of attaining business start-up, operational, along with development costs and influencing the MSMEs to borrow the money was included. Furthermore, for enhancing access to financial services, and loan access by folks or else businesses via pioneering platforms, the progress was less.

Most of the above studies focussed on accessing credit to MSMEs from different aspects. However, the study does not focus on the Indian context. Nevertheless, trade credit behaviour was a major challenge, especially in semi-urban and rural areas. Despite the increase in CA to MSMEs, the challenge of accessing MSMEs from bankers’ perspectives has received little attention and remains largely unexplored. Henceforth, this study was done considering the bankers’ perspectives in Kerala for accessing credit to MSMEs. Today, India’s MSME sector is made up of millions of enterprises. More than 80% of MSMEs were not receiving any formal financing due to a lack of formal accounting systems or even collateral securities. Thus, the present piece of work will focus on CA in MSMEs and the challenges in accessing credit in MSMEs of Kerala.

Research Methodology

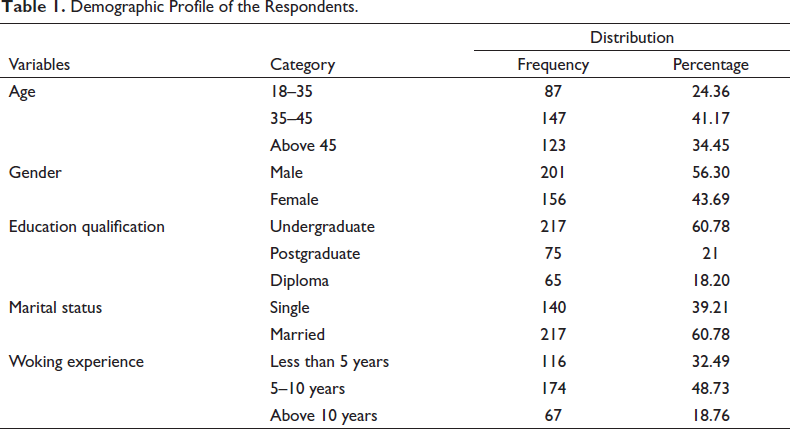

This study is done to evaluate the CA to the MSMEs from the banker’s perspective. The deployed methodology is grounded on a well-structured questionnaire and quantitative research. This research is centred on primary and secondary data. From several banks in the state of Kerala, the primary data were collected. This data was collected by distributing questionnaires to several selected banks and through personal interviews. From papers, journals, books and reviews and websites, secondary data were collected. The questionnaires, which were prepared by the five-point Likert scale, were distributed to 400 respondents. By assigning scores from 1 to 5, the bankers were asked to respond to the statements as per their relevance. Out of 400 respondents, 357 respondents completed the survey, and the remaining 43 respondents did not properly reply to the structured questions. In Table 1, the surveyed participants’ demographic characteristics were depicted.

Demographic Profile of the Respondents.

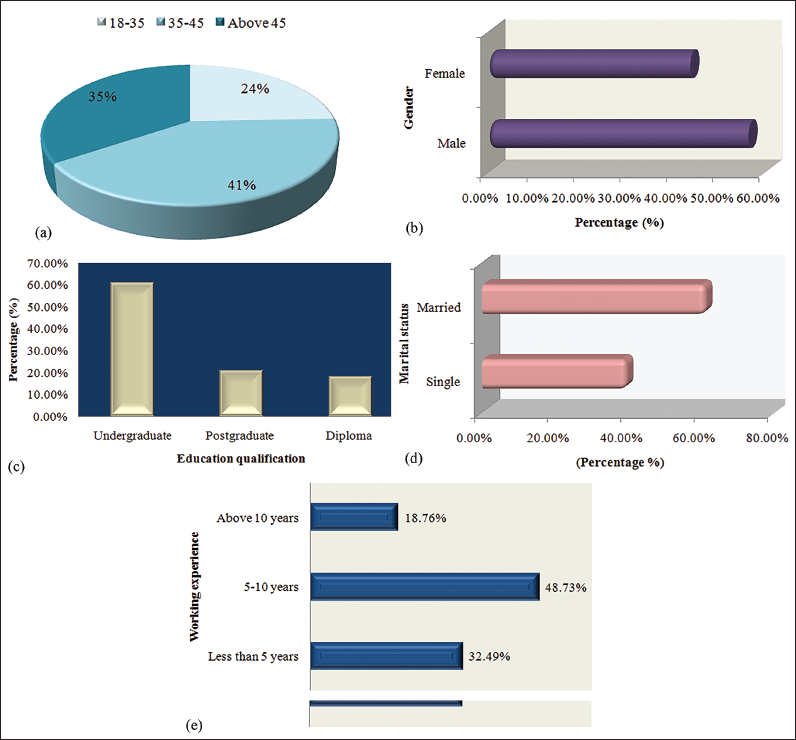

The demographic characteristics of respondents who took part in this research study are depicted in Table 1. A total of 24.36% respondents were between 18 and 25 years, 41.17% were between 35 and 45 years, and those above 45 years represented 34.45% regarding age. The respondents’ gender, which is categorised into male and female, is depicted. The percentage of male and female respondents is 56.30% and 43.69%. The majority of the respondents were qualified undergraduates (60.78%), then 21% had postgraduate, and 18.20% of respondents had diplomas on the side of educational qualification. A total of 60.78% were married, while 39.21% were single—marital status. A total of 48.73% surveyed respondents had working experience of between 5 and 10 years on average. The respondents’ working experience of fewer than 5 years and above 10 years is 32.49% and 18.76%. The working experience between 5 and 10 years achieved the highest percentage when evaluating the categories of working experiences of the respondents. In Figure 2, the graphical representation of the respondents’ demographic profile is depicted.

Graphical Representation of (a) Age, (b) Gender, (c) Education Qualification, (d) Marital Status and (e) Working Experience.

Effectiveness of ATC on the Development of MSMEs

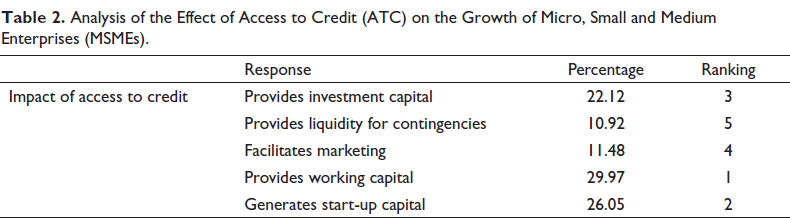

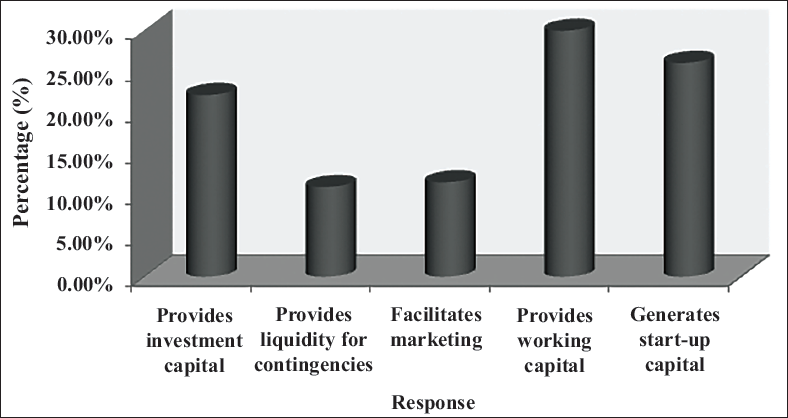

The impact of ATC on the growth of the MSMEs sector is evaluated in Table 2. For the analysis, the responses of providing investment capital, providing liquidity for contingencies, facilitating marketing, providing working capital and generating start-up capital were considered (Ssempala & James, 2018). The percentage for the responses is calculated, and each response is ranked on the table. There was a positive relation between MSMEs’ ATC together with their growth. Signs of rapid transformation were depicted by most small businesses that have access to financing from banks along with other financial institutions regarding ATC. With a percentage of 29.97%, the responses of providing working capital achieved the highest percentage and ranked in 1st place. With 26.05%, the responses of generates start-up capital ranks second place followed by the responses of provides investment capital (22.12%), facilitates marketing (11.48%), and provides liquidity for contingencies (10.92%). In Figure 3, the graphical representation of the impact of ATC was depicted.

Analysis of the Effect of Access to Credit (ATC) on the Growth of Micro, Small and Medium Enterprises (MSMEs).

Impact of Access to Credit (ATC).

Difficulties in Accessing Credit and Areas of Improvement to Increase ATC

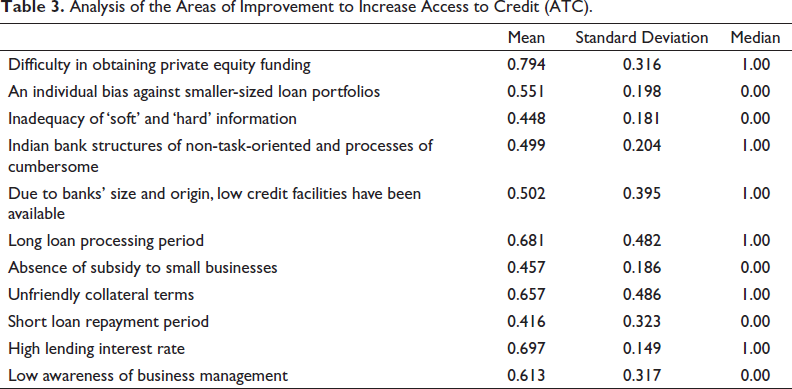

The difficulties in accessing credit and areas of improvement to increase ATC are evaluated in Table 3 (Faircent, 2019; Mbowe et al., 2020). For the analysis, the mean, standard deviation, along with median of the values were calculated. The variable of Difficulty in obtaining private equity funding achieved the highest mean value, which is 0.794 and its standard deviation value is 0.316. The variable of High lending interest rate achieved the second highest mean value (0.697) followed by Long loan processing period (0.681), Unfriendly collateral terms (0.657), Low awareness of business management (0.613), A specific bias against small-sized loan portfolios (0.551), Availability of low credit facilities due to the origin along with size of banks (0.502). The mean value 0.416 is attained by the Short loan repayment period, which is low and it obtained a 0.323 standard deviation value.

Analysis of the Areas of Improvement to Increase Access to Credit (ATC).

Results and Discussion

Here, the data of the collected respondents were analysed and discussed. The analysis of correlation coefficients between the effects of credit knowledge on MSMEs’ CA and determinants of growth of MSMEs was done.

Effect of Credit Knowledge on MSMEs’ CA

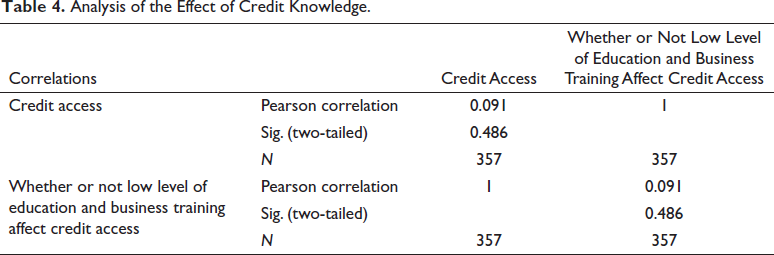

The role of credit knowledge in MSMEs’ CA and the correlation between the two variables are depicted in Table 4 (Ottoman, 2018). The estimation of the relation betwixt CA and whether or else not a lower level education along with business training effect CA of Pearson correlation was done. Moreover, a considerable two-tailed was estimated. The probability value attained 0.473; while, the significance level attained α = 0.05 for the two-tailed test. The MSMEs’ CA was affected in Kerala by the level of credit knowledge. Grounded on financial mediators, the state of Kerala resorted to financing its operations as of its savings, support as of members and short-term credit offered by supplies. For helping in the generation of business groups for MSMEs, simplifications of loan conditions were not present.

Analysis of the Effect of Credit Knowledge.

Determinants of MSMEs Growth

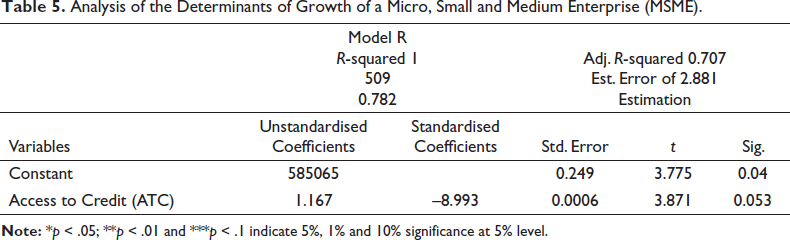

The determinants of MSMEs’ growth towards the impact of credit to access are evaluated in Table 5 (Ssempala & James, 2018). For evaluating the effect of ATC, a linear regression system was deployed. The gauging of the (a) unstandardised coefficients, (b) standardised coefficients, (c) standard error, (d) t-value and (e) significance level of variables was done. An unstandardised coefficient of 585,065 was attained by the variable of constant and its significance value is 0.04. The unstandardised coefficients of 1.167 were acquired by the variable of ATC and it obtained negative standardised coefficients (–8.993) and its standard error and significance values are 0.0006 and 0.053. The Adj R-squared a stand at (0.782), which implies that 78.2% of the total variations in the SMEs’ growth were experienced by ATC. The random component elucidated the remaining 21.8%. Thus, in determining the growth of SMEs, the explanatory variables are important factors.

Analysis of the Determinants of Growth of a Micro, Small and Medium Enterprise (MSME).

Conclusion

Since MSMEs play a catalytic role in the enhancement process of most economies, their popularity has grown globally. MSMEs, which have become an engine of economic growth in India, are the Indian economy’s backbone. For evaluating the ATC in MSMEs, this study was developed; in addition, the challenges in accessing credit were scrutinised. From 357 respondents of bankers in Kerala, the data were collected. A simple RS methodology was wielded for evaluating the outcomes. As per the result, credit knowledge had a considerable effect on MSMEs’ CA. The highest mean value of 0.794 and 0.697 was attained by the factor of challenges in obtaining private equity funding and lending rate, which possess the probability of augmenting loan access. The study’s outcome was constrained to a particular geographical region. By considering more populations and extending geographically, the study can be extended in the future for including other states in India. To ease the financing of MSMEs’ credit, several systems presented by the government were analysed to access another area, which can be scrutinised.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.