Abstract

This commentary documents the spatiotemporal distribution of financial and business services (FABS) production in Poland, by using location quotients for employment and gross value added. Considering the growing prominence of Warsaw in the central European and international network of financial centres, one could expect increasing spatial concentration of FABS in the country. Our findings confirm the undisputed primacy of Warsaw, but also show a dynamic development of FABS in Wrocław, Poznań, and Kraków, suggesting a growing division of labour. Overall, there is little evidence to suggest consolidation of FABS in Poland.

Introduction

‘JPMorgan picks Warsaw for new operations center’ (Reuters, 22 September 2017), ‘Warsaw’s Wola district lures big U.S. companies’ (WSJ, 5 June 2018). 1 These headlines from major news outlets depict Warsaw as a regional (i.e. central European) financial and business services (FABS) centre. Alongside a vibrant initial public offerings market, Warsaw hosts an equity market larger (in terms of total market capitalisation) than Vienna 2 and became the first post-socialist market to be classified as ‘developed’ by FTSE Russell. Geographically, London, Paris, Frankfurt, and many other financial centres in Europe are all within the 2.5-hour radius by air from Warsaw. Local private equity and investment firms, such as Wood, Abris, MCI, and Enterprise, utilise the frequent flights from Warsaw to these cities, making the city a convenient hub for regional FABS trade.

Based on the office connectivity of major FABS firms, the Globalisation and World Cities network has categorised Warsaw as an ‘alpha’ city since 2016. Wrocław, Kraków, Poznań, Katowice, and Łódź are listed as the cities with ‘(high) sufficiency’ below the ‘gamma’ cities. The Association of Business Services Leaders (ABSL, 2018) reports that more than 1200 business process outsourcing/shared services centres (BPO/SSC) and other services centres were operating in Poland. Warsaw hosts more of such centres, while it is Kraków which takes the largest share in terms of labour force in this sector (23%). According to the Oxford Economics database, which defines FABS much more broadly, Warsaw employs in FABS nearly five times more people than Kraków or Wrocław. Thus, depending on the analytical focus, whether it is employment or office locations, or FABS in a narrower or broader sense, the degree of concentration in Warsaw would be acknowledged differently. In contrast to Warsaw, Wrocław and Poznań are known for German-speaking BPO/SSCs, and an increasing concentration of FABS in Warsaw would signal a rise of a central European regional hub, less dependent on the German financial flows. Thus, this case study on Poland shall be placed within a wider framing of relational European geographies.

Alongside these themes, this commentary illustrates how the changes in FABS at the national level are reflected across major Polish cities. In particular, it investigates if the primacy of the regional financial centre (i.e. Warsaw) has been strengthened over time, in a form of spatial concentration in FABS production.

Theoretical and methodological framework

Financial centre formation can be understood as the outcome of ‘an interplay between centripetal and centrifugal forces’ (Contel and Wójcik, 2019). On one hand, various economies of scale (McCann, 2001) accelerate the spatial concentration of FABS in the primate national financial centre, which also functions as a gateway into the national urban system (Taylor and Derudder, 2016). On the other hand, a survey by Deloitte (2019) highlights a recent trend that ‘strategic and interaction-heavy’ functions are increasingly outsourced (see also Feeny et al., 2005) in addition to orthodox cost-cutting outsourcing or operation optimisation (Zehnder et al., 2007). The aforementioned ABSL report (2018) depicts a decentralising trend from international financial centres abroad to the secondary (or local) financial centres in Poland. Such BPO/SSCs generally deals with services beyond high finance (e.g. equity underwriting, loan syndication, merger advisory), and, thus, this study defines FABS more broadly.

While Dicken (2007) lists financial services and advanced business services in parallel, Coe et al. (2014) rebrand these services as FABS with an emphasis on their hierarchical relationship among different types of services, placing investment banking on the top. Here, not only the number of employees but also the transaction value (or gross value added (GVA)) becomes a key to understand the interurban hierarchy.

Therefore, this study analyses the FABS data (NACE Rev. 2, sections K, L, M, and N of eight major metropolitan areas in Poland (i.e. Warsaw, Katowice, Wrocław, Kraków, Gdańsk, Łódź, Poznań, and Szczecin) from 2000 to 2015, 3 retrieved from Oxford Economics. In order to facilitate the illustration of (de)centralisation, ‘location quotients’ (LQs) are defined as:

where i notates a metropolitan area, x is the share of the metropolitan area in the national FABS employment or nationally aggregated FABS GVA, and s is the share of the metropolitan area in the national total employment or national gross domestic product (GDP), respectively. An increasing LQ means a shift towards FABS and/or consolidation of FABS in a given city.

The pattern of change across major metropolitan areas in Poland

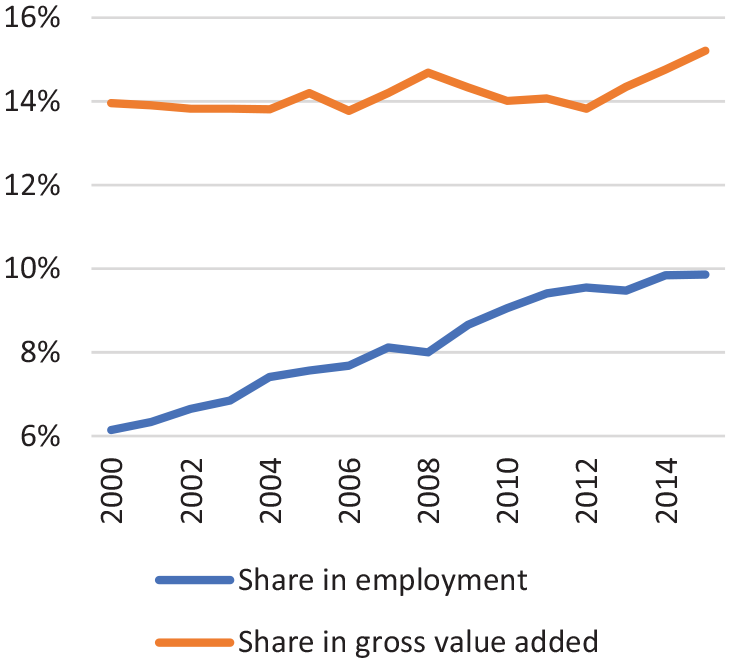

Generally speaking, despite large unit increases in total employment and GDP since 2003, FABS employment and GVA grew faster than total employment and GDP in Poland (Figure 1). In contrast to employment, the GVA share has not grown significantly. FABS are generally labour-intensive, and, unlike in manufacturing, it is difficult to obtain major increases in productivity in the sector. Given the pre-eminence of branch banking in Poland, a larger FABS employment is expected in a city with a larger population (retail customer base), but this was not the case (e.g. Warsaw vs Katowice, Gdańsk vs Poznań, Wrocław vs Kraków). Thus, this study focuses more on the share of FABS in total metropolitan employment (Figure 2) rather than in total metropolitan population.

Share of FABS in employment and GVA.

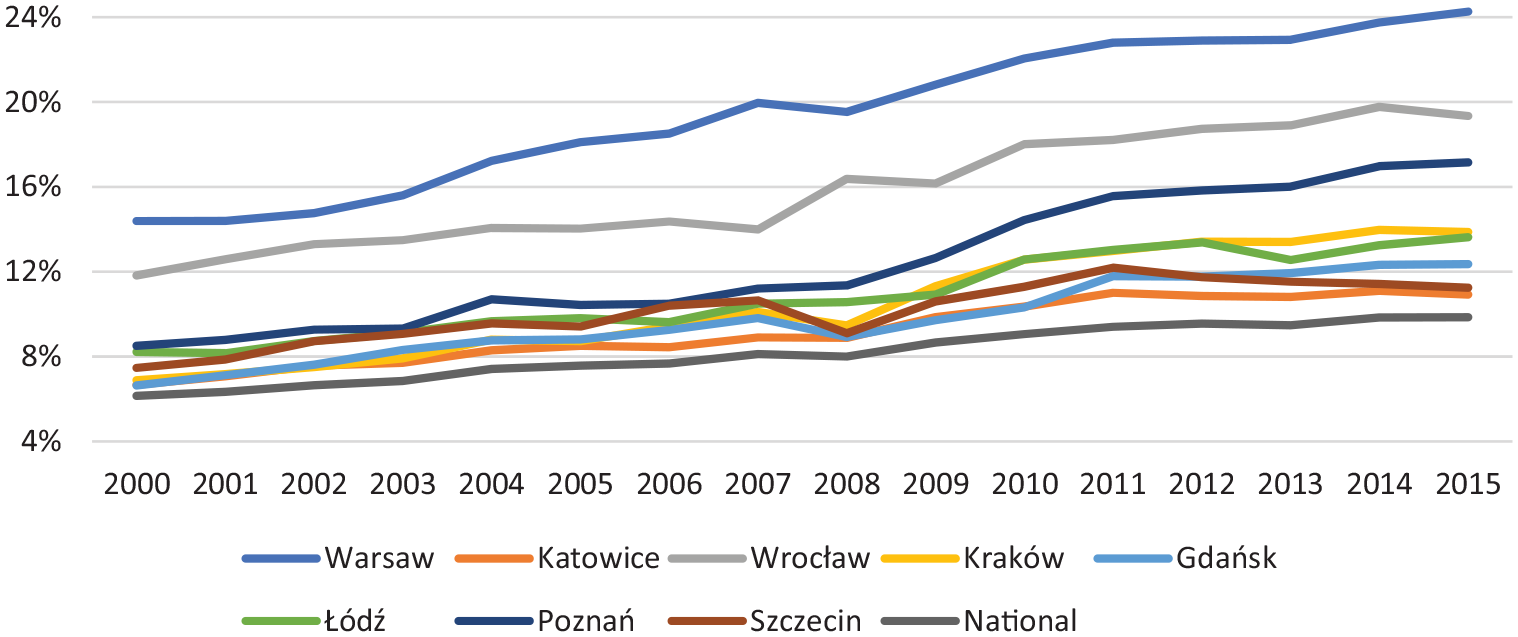

Share of FABS in total employment (metropolitan and national).

On the national level, the share of FABS in total employment increased from 6.1% in 2000 to 9.9% in 2015. All eight major metropolitan areas exceeded the national average every single year, highlighting the concentrated presence of FABS in the metropolitan areas. Warsaw has increased the share of FABS in total metropolitan employment, indicating a high rate of increase above the national average. Wrocław, the third largest city in terms of FABS employment, maintained the second highest share, also increasing faster than the national average. Katowice, the second largest city in terms of FABS employment as well as total population, has the lowest share among major metropolitan areas, suggesting the city’s reduced financial centre functions. After 2008, Poznań accelerated its increase in the share, establishing itself as the third highest city in terms of the share of FABS in total metropolitan employment. In this regard, Wrocław and Poznań stand out as local financial centres, despite their relatively small size in terms of FABS employment.

Wrocław and Poznań share the legacy of Bank Zachodni WBK (today’s Santander Bank Polska), which was formed by the 2001 merger of Bank Zachodni in Wrocław and Wielkopolski Bank Kredytowy in Poznań. Wrocław is home to many SSCs of global FABS firms, such as BNY Mellon, Credit Suisse, McKinsey, Société Générale, and UBS. Located in western Poland, the city is known for easy access to the German-speaking labour market, with German being the third most spoken language in the Polish BPO/SSC sector after English and Polish (ABSL, 2018). Poznań is conveniently located between Warsaw and Berlin, also with easy access to the German-speaking labour market. Its steady flow of university students and graduates makes the city highly attractive for BPO/SSC (Pro Progressio, 2019). Although Poznań hosts more and more BPO offices and SSCs, a majority of them deal with FABS for global non-FABS firms (e.g. Carlsberg, GSK, Volkswagen). It thus suggests a certain division of labour between Wrocław and Poznań, the former focusing on BPO/SSC for global FABS firms, and the latter focusing on BPO/SSC for global non-FABS firms.

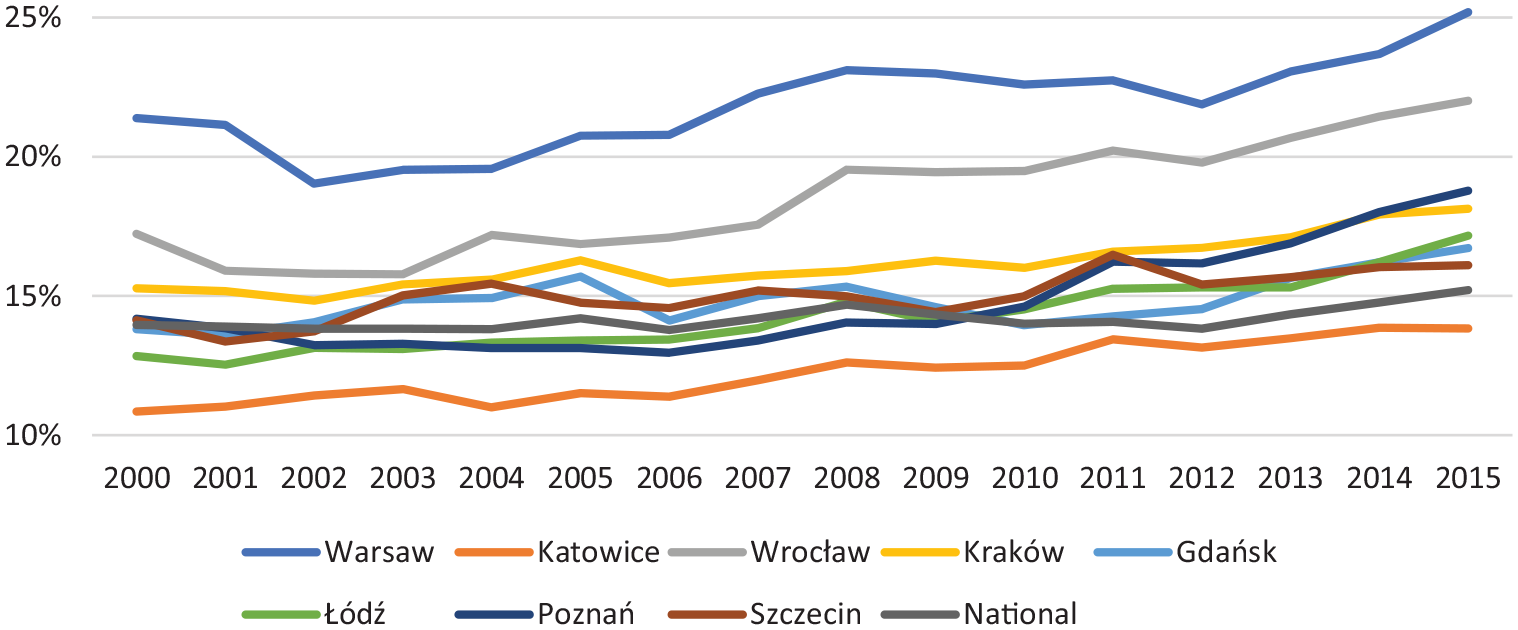

Figure 3 focuses on GVA. The share of FABS in metropolitan GDP for Katowice is below the national average throughout the studied period. The share of FABS in Poznań reached the national average in 2010 and has increased since. Unlike the share of FABS in total metropolitan employment, the share of FABS GVA in metropolitan GDP tends to fluctuate. Still, Warsaw dominates throughout the studied period, followed by Wrocław and Kraków, suggesting a high degree of business-value-driven FABS produced in these cities. After the financial crisis, the share of FABS GVA declined in Warsaw until 2012, but both Wrocław and Kraków maintained their share. It follows that the latter cities have a certain degree of independence from Warsaw in FABS production (i.e. decentralised), with its values not necessarily influenced by Warsaw. The relationship between Warsaw and Wrocław/Kraków is not based on command and control, despite the fact that Warsaw hosts many headquarters in the sector. Otherwise, the performance of Warsaw in terms of FABS GVA would have been reflected in those of other cities. Furthermore, the dominance of Warsaw in FABS has not been maintained at a cost to other cities, as the increase of FABS GVA in Warsaw does not coincide with the decline of it in another city.

Share of FABS in GDP (metropolitan and national).

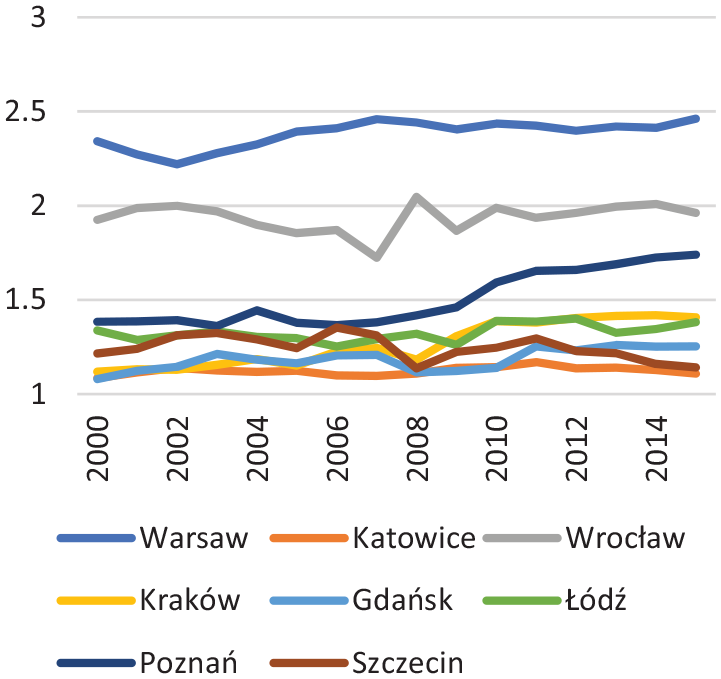

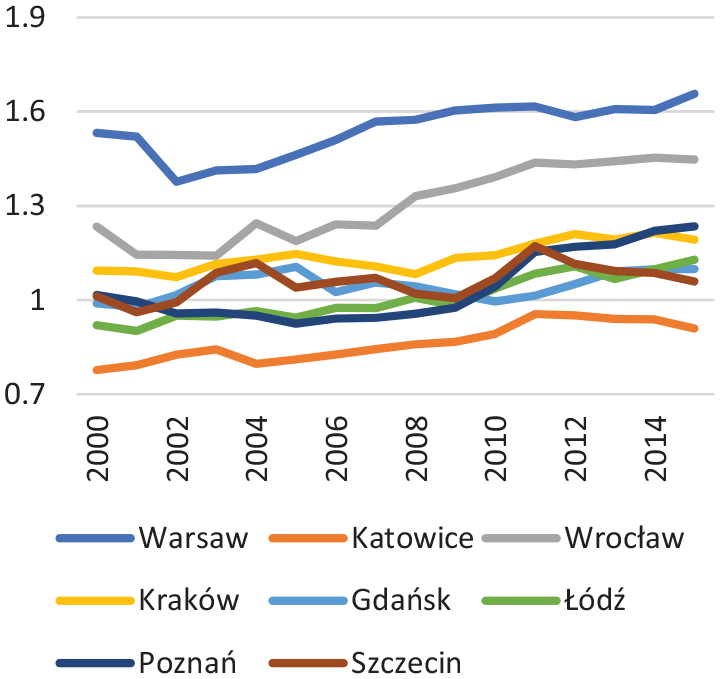

As far as the dominance of Warsaw is concerned, roughly a quarter of national FABS employment is concentrated in the city. FABS GVA also shows a similar magnitude of concentration in Warsaw, though it declined to 20% in the years 2002–2004. Otherwise, the concentration of FABS employment and the concentration of FABS GVA are similar, with no significant changes observed in the order of metropolitan areas. LQs, however, provide a more nuanced picture (Figures 4 and 5). The LQs for FABS employment exceeded 1.0 (i.e. FABS employment being concentrated out of proportion to the concentration of total employment in the given metropolitan area) for all eight metropolitan areas during the studied period. The LQ for FABS employment remained just below 2.5 in Warsaw, followed by Wrocław and Poznań. These LQs confirm that the labour markets in Warsaw, Wrocław, and Poznań are heavily oriented towards FABS.

LQ for FABS employment.

LQ for FABS GVA.

The LQs for FABS GVA also illustrate a concentration of FABS in Warsaw followed by Wrocław, but unlike the LQs for FABS employment, Kraków has maintained third position until 2014. The LQ for FABS GVA has been below 1.0 in Katowice, and only in Warsaw, Wrocław, and Kraków exceeded 1.0 throughout the whole period under consideration. Like the LQ for FABS employment, Poznań has shown its dynamism in the LQ for FABS GVA since 2010. These LQs indicate that Warsaw, Wrocław, and Poznań have strengthened their financial centre characteristics, and, alongside Kraków, these financial centres seem to attract more business-value-driven services, increasing the LQ for FABS GVA.

According to the Dealogic database, the FABS firms headquartered in Poland conducted 1050 merger and acquisition (M&A) deals between 2000 and 2017, amounting to US$38.1b in total deal value. Warsaw-headquartered acquirers dominated the scene with 651 deals (US$28.6b), but the largest portion (US$12.6b) took place within Warsaw (i.e. both the acquirer and target located in Warsaw), followed by US$5.1b targeting firms located in the Gdańsk metropolitan area (i.e. Tri-City). The latter was shaped by Pekao in Warsaw, purchasing the operational assets of BPH in Gdańsk (US$3.0b) in 2006, in relation to the merger of their parent banks (UniCredit and HVB, respectively). Otherwise, no significant interurban consolidation was observed.

Out of US$28.6b of deals involving Warsaw-headquartered acquirers, US$19.4b came from the finance sector, followed by US$6.7b from insurance. However, the latter was dominated by the 2016 purchase of Pekao from UniCredit by the state-owned insurance giant PZU (accompanied by the also state-owned national development fund PFR, valued at US$5.1b). PZU has been active in banking sector consolidation: the insurance firm is heavily exposed to the sector as the largest corporate and government debt holder, and the KNF (financial supervisory authority) objected to private equity firms owning retail banks. Non-PZU/PFR acquisition in the insurance subsector amounted to only US$300m. Thus, US$25.8b out of US$28.6b of deals originated in Warsaw were linked to the financial (i.e. narrower than FABS) sector consolidation.

Warsaw is ‘the only game in town’ when it comes to FABS M&As, but this trend is largely characterised by narrower banking sector consolidation rather than a broader FABS sector consolidation. In fact, when the M&A data are limited to those with a deal value greater than US$1m, Warsaw conducted 107 out of 155 deals, followed by Wrocław (15 deals) – no other city has more than a few deals. Even though the analysis on FABS employment and GVA noted some evidence of dynamism observed in Wrocław, Poznań, and Kraków, these cities are largely absent when it comes to M&As.

Conclusion

Poland has experienced a spectacular growth in FABS. As the LQs for FABS employment illustrate, the sector is concentrated in the largest metropolitan areas. While the share of FABS in GDP is significantly higher than that in employment, the growth of the former is slow, illustrating difficulties to obtain major productivity increases in FABS as a whole. Nevertheless, the share of FABS in GDP has been increasing since 2012, corresponding to the opening of several SSCs for global FABS firms in Poland. As is illustrated by the Deloitte survey (2019), the findings suggest that more business-value-driven services are produced in/outsourced to Poland. In light of Coe et al. (2014), the Polish metropolitan areas (i.e. Warsaw, Wrocław, Poznań, and Kraków) are well integrated into the global financial network as FABS centres.

Warsaw is clearly dominating the sector, having the highest share of FABS in both metropolitan employment and GDP. The rate of increase in the share is faster than the national average, signifying its financial centre characteristics. While Wrocław is known for SSCs for global FABS firms, Poznań hosts many SSCs for non-FABS firms, suggesting a certain division of labour among FABS centres. Despite the recent rise of Poznań, Kraków has maintained a large share of FABS in metropolitan GDP, suggesting a high degree of business-value-driven FABS produced in Kraków. The evidence thus illustrates the interplay between centripetal and centrifugal forces in FABS development.

Given the location of these cities, the findings suggest that the Polish urban system is relatively decentralised as far as FABS are concerned, in analogy to the German urban system (cf. Wójcik and MacDonald-Korth, 2015). While Warsaw dominates the M&As in FABS, they are infrequent and characterised by the narrower finance/banking sector consolidation. Hence, there is little evidence to suggest interurban consolidation in FABS, depicting a stable hierarchy of financial centres: the national financial centre Warsaw, followed by a regional FABS centre Wrocław, an emerging FABS centre Poznań, and a relatively established business-value-driven FABS centre Kraków. Warsaw did not increase its dominance in FABS at the expense of other FABS centres, further strengthening the observation regarding the spatial division of labour in FABS production.

Wrocław and Poznań are known for German-speaking BPO/SSCs, while the presence of Goldman Sachs or JP Morgan in Warsaw suggests direct office connectivity between Warsaw and London/New York. In a context of a wider pan-European geography of financial centres, the Polish case highlights a complex hierarchy of national and regional FABS centres. The spatial division of labour among the Polish FABS centres reflects the relational geographies of a wider Europe, where the centripetal trends towards national and regional centres are accompanied by the centrifugal trends of outsourcing and the international/global division of labour.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement number 681337). The article reflects only the authors’ views and the ERC is not responsible for any use that may be made of the information it contains.

1.

In this commentary, news articles are treated as data sources and are cited in the endnotes. Available at: https://www.reuters.com/article/us-jpmorgan-poland/jpmorgan-picks-warsaw-for-new-operations-center-polish-deputy-pm-idUSKCN1BX1HC and ![]() .

.

2.

Amounting to €135b and €119b, respectively, according to the Federation of European Securities Exchanges (as of December 2019, prior to the coronavirus outbreak in Europe).

3.

The 2016 data contain estimates and are thus omitted from this study.