Abstract

Using the case study of Slovakia, this article considers the role of the state in the rapid growth of the automotive industry in integrated peripheral markets of the global automotive industry. Although this growth has been mainly driven by the investment strategies of automotive lead firms, the state has played an important role by accommodating the strategic needs of foreign capital through neoliberal economic policies. In addition to secondary sources, the empirical research is based on a 2010 survey of 299 Slovak-based automotive firms with a response rate of 44% and on 38 on-site firm-level interviews conducted between 2011 and 2013 and one in 2005. The analysis draws upon approaches in economic geography, international political economy and upon global value chains and global production networks perspectives to argue that the successful development of the automotive industry in Slovakia has been achieved at the expense of its overwhelming dependence on foreign capital and corporate capture. The article considers the potential consequences of dependent industrial development for the domestic automotive industry and its position in the international division of labor.

Introduction

The state has played a key role in the industrialization of less developed countries (Kohli, 2004), including the development of the automotive industry (Dicken, 2011; Humphrey and Oeter, 2000). Its crucial importance for the automotive industry was most recently demonstrated in both developed and developing countries during the 2008–2009 economic crisis (Klier and Rubenstein, 2010; Stanford, 2010; Sturgeon and Van Biesebroeck, 2009; Van Biesebroeck and Sturgeon, 2010). Along with investment strategies of global automotive lead firms, state policies have played an important role in the rapid development of the automotive industry in less developed ‘emerging’ economies since the early 1990s (Carrillo et al., 2004; Humphrey et al., 2000; Humphrey and Oeter, 2000; Sturgeon et al., 2008). The fastest growth took place in countries with rapidly growing new demand and potentially very large domestic markets, such as China, India and Brazil (Liu and Dicken, 2006; Liu and Yeung, 2008; Van Biesebroeck and Sturgeon, 2010), and in ‘integrated peripheral markets’ – that is, less developed countries located in peripheral areas surrounding traditional core regions of automotive production, such as Mexico and East-Central Europe (ECE) (Layan, 2000; Pavlínek, 2002; Sturgeon et al., 2010). Integrated peripheral markets have been typified by ‘hands off’ industrial policies, dependence on foreign direct investment (FDI) and by integration into core-based production networks (Humphrey and Oeter, 2000). Core-based lead firms invested heavily in these peripheral regions in assembly operations because of low production costs and geographic proximity to large affluent core markets and also because of their inclusion in large regional economic blocs, such as the European Union (EU) and the North American Free Trade Agreement. While the role of lead firms in these processes has been emphasized and analyzed, much less attention has been given to the role of state strategies beyond the provision of investment incentives, although exceptions exist (e.g. Drahokoupil, 2008, 2009a; Humphrey and Oeter, 2000; Liu and Dicken, 2006; Liu and Yeung, 2008).

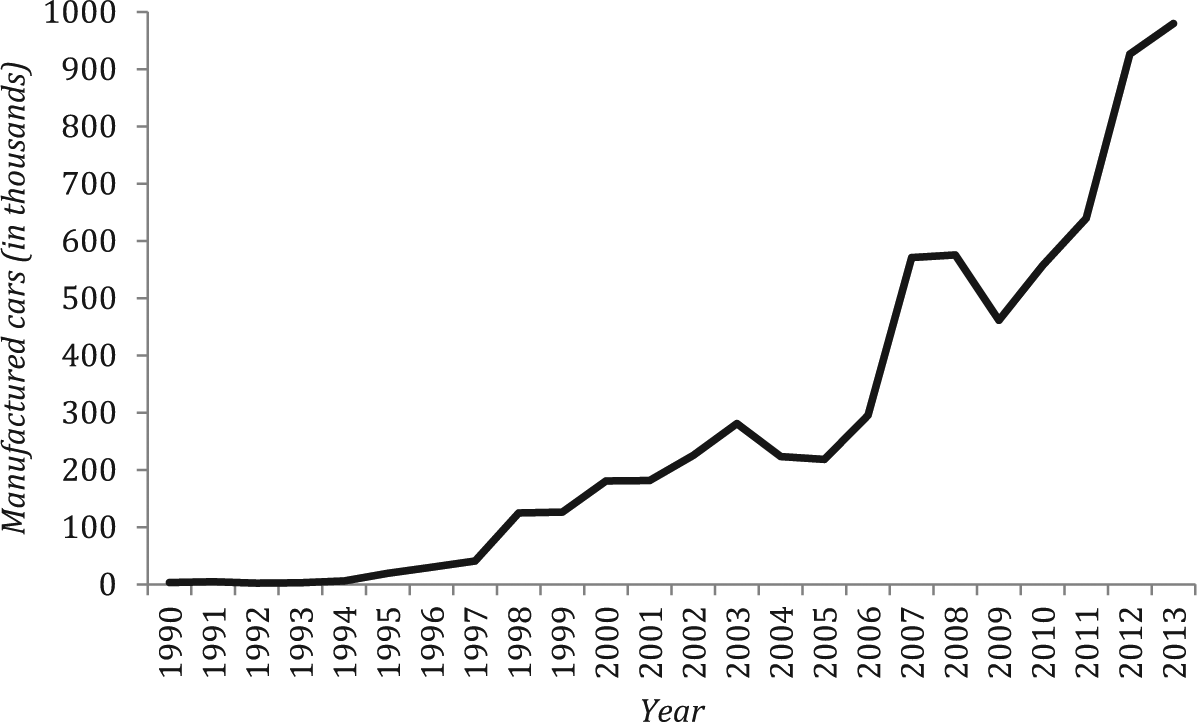

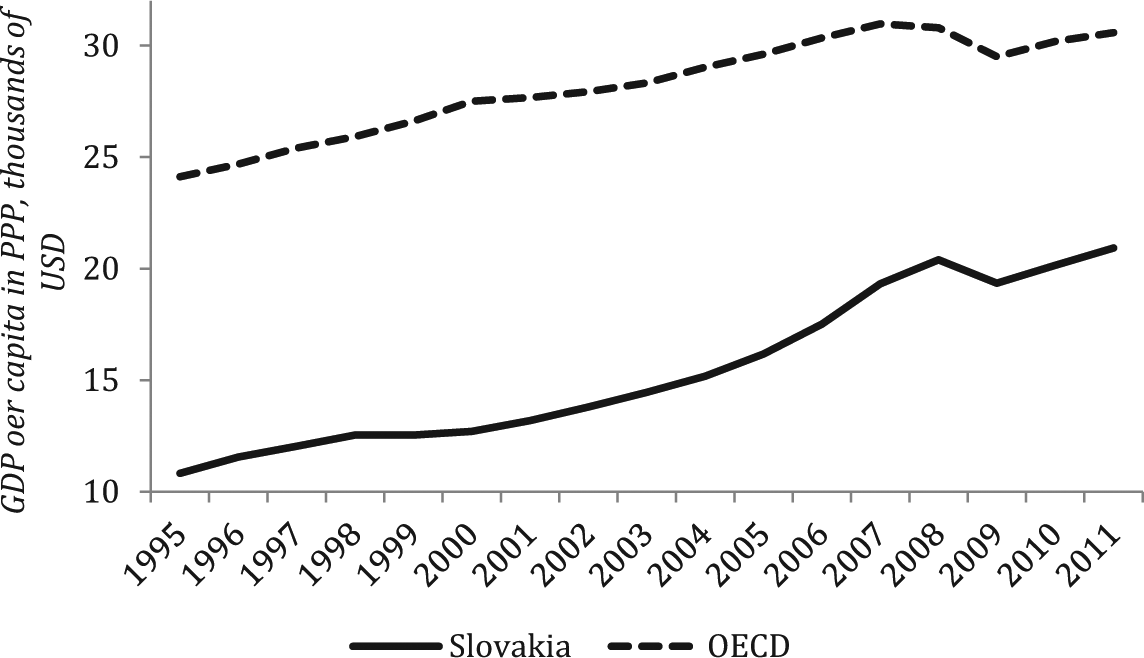

The aim of this article is to analyze the role of the state in the development of the automotive industry in Slovakia, which represents an excellent example of a peripheral country that has been integrated into European automotive production networks since the early 1990s. Driven by FDI inflows of €2.4bn in the automotive industry between 1990 and 2012 NBS, 2013), the annual assembly of passenger cars increased from less than 3000 units in 1993 to 980,000 units in 2013 (Figure 1). Slovakia became the 19th largest producer of automobiles in the world in 2012 and the largest producer of passenger cars per capita (181 units per 1000 people in 2012) ( SARIO, 2013). FDI-driven export-oriented expansion of the automotive industry contributed to rapid economic growth, especially between 2000 and 2007 (OECD, 2012). Slovakia recorded the fastest GDP growth per capita among the OECD members during 2001–2011 and it significantly narrowed the income gap relative to the more developed half of the OECD countries from more than 60% to almost 40% (Figure 2).

Passenger car production in Slovakia, 1990-2013.

GDP per capita in USD in purchasing power parity in OECD countries and Slovakia, 1995-2011.

In this article, I seek to move beyond the uncritical praise by the state, media, supranational organizations and consulting firms of FDI-driven development of the Slovak automotive industry (e.g. Ernst & Young, 2010; Jakubiak et al., 2008; SARIO, 2013) and provide a more critical reading of the role of the state in these processes. I show that the state’s role was instrumental in the growth of the Slovak automotive industry. Although its post-1990 development has been driven by FDI, I argue that the state played an important role in making it possible by creating highly favorable conditions for foreign capital in Slovakia. In the process, the dependence of Slovakia on the externally controlled automotive industry has increased sharply. By 2004, foreign capital controlled 97.3% of the automotive industry, measured by a percentage of turnover (Vliegenthart, 2010). As of 2012, 80% of automotive suppliers were foreign-owned and 93.5% of technologies were imported (Luptáčik et al., 2013; ZAP, 2013). In 2012, the automotive industry accounted for 26% of Slovak exports and 20% of its imports (ZAP, 2013).

Theoretically and conceptually, this article draws upon analyses of ECE in international political economy (e.g. Drahokoupil, 2009a; Shields, 2008), studies of external dependency and truncation in economic geography (e.g. Britton, 1980; Dicken, 1976), and on global value chains (GVC) and global production networks (GPN) perspectives (e.g. Gereffi et al., 2005; Henderson et al., 2002). Empirically, in addition to secondary sources, the article uses data from a 2010 survey of 299 Slovak-based automotive firms with 20 or more employees which yielded a response rate of 44%, and from 38 on-site interviews conducted with Slovak-based automotive firms between 2011 and 2013, plus from a 2005 interview at Volkswagen (VW) Slovakia.

The article begins with a discussion of the state and the development of the automotive industry in ECE. The changing role of the state in the automotive industry during the post-1993 independence period is then analyzed, followed by case studies of the role of the state in attracting and accommodating three foreign assembly firms: VW, PSA Peugeot-Citroën (PSA) and Kia. Based on firm-level interviews, an evaluation of state policies towards the automotive industry by foreign and domestic firms is then presented. The limits of the state–foreign capital nexus for successful economic development in Slovakia are considered; and, finally, the main results are summarized.

The state and the development of the automotive industry in East-Central Europe

Since the early-1990s, neoliberal export-oriented strategies of economic development have become the new orthodoxy in less developed economies, including the former state socialist countries of ECE (Bohle, 2006; Gereffi, 2013; Gowan, 1995; Harvey, 2005). The automotive industry is a prime example of the implementation of such strategies that are based upon attracting large inflows of FDI to finance and restructure existing industries, build new industrial capacity and promote domestic automotive production. Despite questions about the appropriateness of automotive industry-centered strategies in contemporary economic development (Humphrey, 2000), countries around the world continue to lure automotive transnational corporations (TNCs) to set up new production within their territories (Liu and Dicken, 2006). In this intensifying competition, ECE countries have capitalized on the needs of core-based TNCs to expand geographically into ECE markets and increase their global competitiveness by offshoring labor-intensive production to lower-cost peripheral locations. In addition to its market potential and low production costs, ECE is attractive because of its proximity to affluent Western European markets, its inclusion in the EU, flexible labor policies, low labor militancy, and weak labor unions. In other words, ECE has become one of the latest ‘spatial fixes’ sought by TNCs for the absorption of surplus capital (Harvey, 2006, 2010).

The state has played an important role in making this spatial fix possible during ECE’s transition from ‘state socialism to neoliberalism’ (Shields, 2008: 447). In the absence of sufficient domestic capital and after the failure of national-oriented strategies of the early 1990s (Drahokoupil, 2008), neoliberal strategies of industrial development have prevailed in ECE. Restructuring of the state through the processes of transnationalization (Shields, 2004, 2008; Vliegenthart, 2009) opened up national economies for penetration by foreign capital. Some of the domestic political elites, variously labeled as ‘comprador administration’ (Baran, 1957), ‘comprador fraction of the bourgeoisie’ (Poulantzas, 1973), ‘comprador intelligentsia’ (Eyal et al., 1997), ‘comprador class’ (Vliegenthart, 2010) or ‘comprador service sector’ (Drahokoupil, 2009b), aligned their interests with those of foreign capital and gained political influence, which they used to promote successfull FDI-friendly policies across ECE. In other words, they ‘helped to translate the structural power of transnational capital into tactical forms of power that enabled agential power to work in sync with the interests of the multinationals’ (Drahokoupil, 2009a: 3). By the late 1990s, ECE states had become competition states (Cerny, 1997), which are typified by state strategies that rely on foreign capital as a primary vehicle for increasing national economic competitiveness and by adopting FDI-driven industrialization and restructuring strategies (Drahokoupil, 2008, 2009a, 2009b). ECE competition states have competed for mobile FDI by creating favorable conditions for the entry and operation of TNCs in their national economies, including offering various investment incentives, tax provisions, education policies, and industrial relations. These competition states are typified by ‘inward investment regimes’ (Phelps and Wood, 2006) or ‘investment promotion machines’ (Drahokoupil, 2008) that are subnational territorial coalitions which ad hoc mobilize social actors at local, regional and national scales, with the aim of attracting selected foreign investors and promoting their interests in a particular locality, region and country (see also Phelps, 2000, 2008). Thus, FDI and industrial policies in ECE have been driven primarily by the imperative to accommodate the needs of foreign capital and, in particular, the needs of large ‘strategic’ (or flagship) investors, whose interests are represented by the comprador sector in domestic politics. The goal of these policies has been to improve or maintain a country’s competitive position in transnational flows of FDI, important not only for attracting new investments but also for stabilizing existing ones. Although individual countries might be attempting actively to shape their industrial structure by attracting FDI into particular sectors of the economy, they will only succeed if these sectors are attractive to foreign TNCs and in line with their transnational investment strategies.

The bargaining powers of states have declined, especially in less developed countries, because of the liberalization of FDI policies and certain controls over their national economies being relinquished to supranational organizations (Phelps, 2008; Phelps and Raines, 2003). The bargaining powers of ECE states with vis a vis foreign TNCs with regard to FDI terms have been further undermined by their small domestic markets and intense competition from neighboring countries with similar factor endowments (see Liu and Dicken, 2006). Automotive TNCs exploited this relative weakness of ECE countries by engaging in regulatory arbitrage, playing countries off against one another with the aim of securing the best possible terms for their investment (Kolesár, 2006, 2007). Consequently, automotive TNCs were able to ‘secure exceptionally favorable terms of entry into the region’ (Bartlett and Seleny, 1998: 320). Regulatory arbitrage may lie behind the reduced economic benefits of FDI for host economies because it can lead to ‘corporate capture’ of national and local institutions and resources, in which the state and regional governments act in the context of an asymmetrical power relationship with respect to foreign capital and, consequently, end up serving the interests and needs of foreign TNCs at the expense of domestic firms and populations (Phelps, 2000, 2008). In this situation, the state provides resources to reduce the investment costs of incoming flagship investors and tailors investment incentives to investors’ specific needs. Typically, the state agrees to finance and build customized infrastructure, such as highway links, railway terminals or supplier parks; secures customized assembly and provision of land for greenfield production complexes; and finances workforce training. Additional signs of corporate capture include: state agencies, regional and local politicians placing the interests of flagship investors above those of domestic firms and local residents; flagship investors exerting disproportionate influence over state economic, education and training policy-making, to serve investors’ specific needs; the state agreeing not to allow other investors to locate in the proximity of a flagship investor, in order to reduce competition for labor in the local labor market; and few positive regional development effects of FDI, beyond that of newly created jobs (Phelps, 2000, 2008). In the words of the UNCTAD (1998: 103): ‘When governments compete to attract FDI, there will be a tendency to overbid… The effects can be both distorting and inequitable since the costs are ultimately borne by the public and hence represent transfers from the local community to the ultimate owners of the foreign investment’.

At the same time, however, the EU local content regulations, combined with co-location imperatives of assembly plants and suppliers in contemporary modular assembly processes (Sturgeon and Lester, 2004), forced automotive lead firms to develop supplier networks in ECE. Lead firms put pressure on established foreign suppliers to follow them into ECE and also forced the most capable domestic suppliers to upgrade in order either to meet the lead firms’ quality and timing requirements or be excluded from supplier networks (e.g. Pavlínek, 2003; Pavlínek et al., 2009). Territorial embeddedness of foreign investors in host economies through the development of supplier networks generates potentially significant economic benefits, by (i) increasing the value from production in host economies and (ii) by generating spillovers that might increase the competitiveness of domestic firms (Pavlínek and Žížalová, 2016). For example, Slovakia attracted 121 investments in new automotive supplier plants between 1997 and 2009 and Central and Eastern Europe as a whole attracted 1,258 (Ernst & Young, 2010). 1 These potentially large economic benefits of territorial embeddedness make foreign-owned automotive assembly plants extremely desirable in the eyes of national governments and increase their willingness to engage in competitive bidding with other countries in order to attract them.

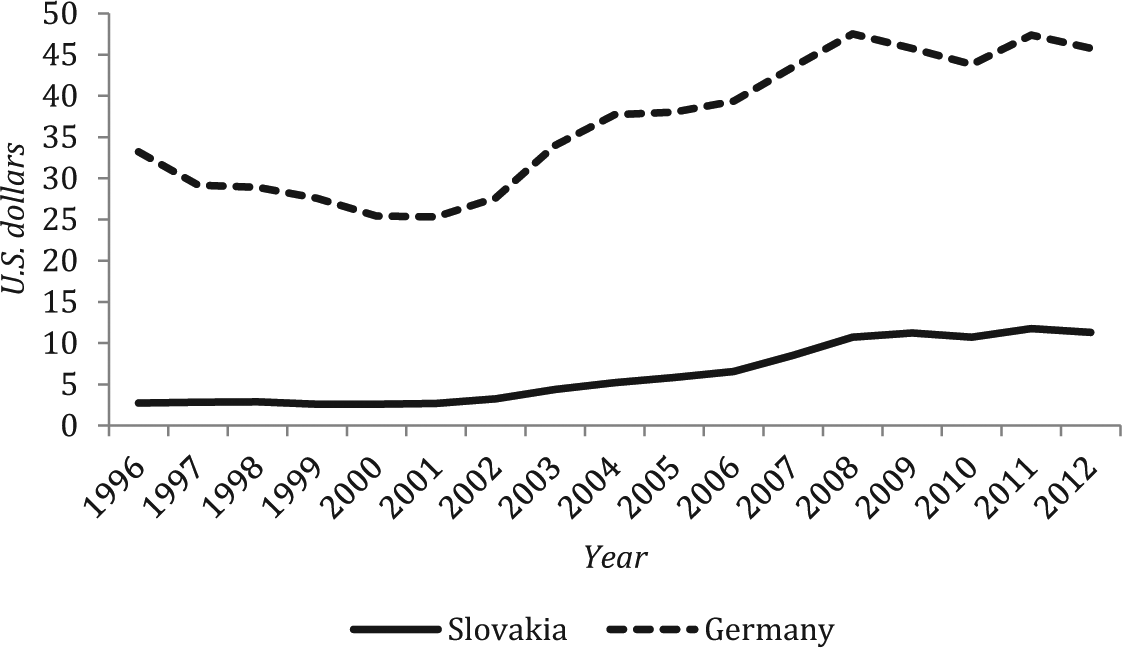

However, the state-based competition over FDI in ECE has been mostly of the ‘low-road’ variety ‘on the basis of low wages, docile labour and low taxes, which perpetuate an inability to upgrade to an economic base of higher skill and higher wages’ (Malecki, 2004: 1104). In 1997, Ellingstad (1997) warned that a ‘maquiladora syndrome’ might be developing in ECE. According to Ellingstad (1997), the maquiladora economy is typified by export-oriented manufacturing, low wages that do not match increases in productivity, and by worker productivity and skills that are lower than in the home countries of foreign investors. Export-oriented foreign-owned factories often assemble high-tech, high quality goods with a relatively high value-added from components that are either imported or produced locally by other foreign firms. Export-oriented manufacturing is usually highly regionally concentrated and it thus contributes to large regional development disparities in maquiladora economies. Overall, the maquiladora strategy promotes the development of ‘low-wage, low or medium-skill, low value-added manufacturing’ with limited chances of upgrading in the foreseeable future (Ellingstad, 1997: 9). Although Bernaciak and Šćepanović (2010: 141) argued that “by the late 1990s, regional industry had largely recovered from the “maquiladora syndrome”, a number of indicators suggest otherwise, including low real wages despite substantially increased productivity, weak unions, high unemployment (14% in Slovakia in 2013), a persistent wage gap between ECE and Western Europe (Figure 3), imports of high value-added components or their production by foreign-owned suppliers rather than domestic firms, the weak development of higher value-added non-production functions (Table 1), and the intensification of uneven development because of FDI (Pavlínek, 2004). 2 Nölke and Vliegenthart (2009) argued that FDI-driven industrial development strategies have increased ECE’s external dependence on foreign capital to such an extent that it has led to the emergence of a ‘dependent market economy’ as a distinct variety of capitalism in ECE.

Hourly compensation costs in manufacturing in Slovakia and Germany, 1996-2012.

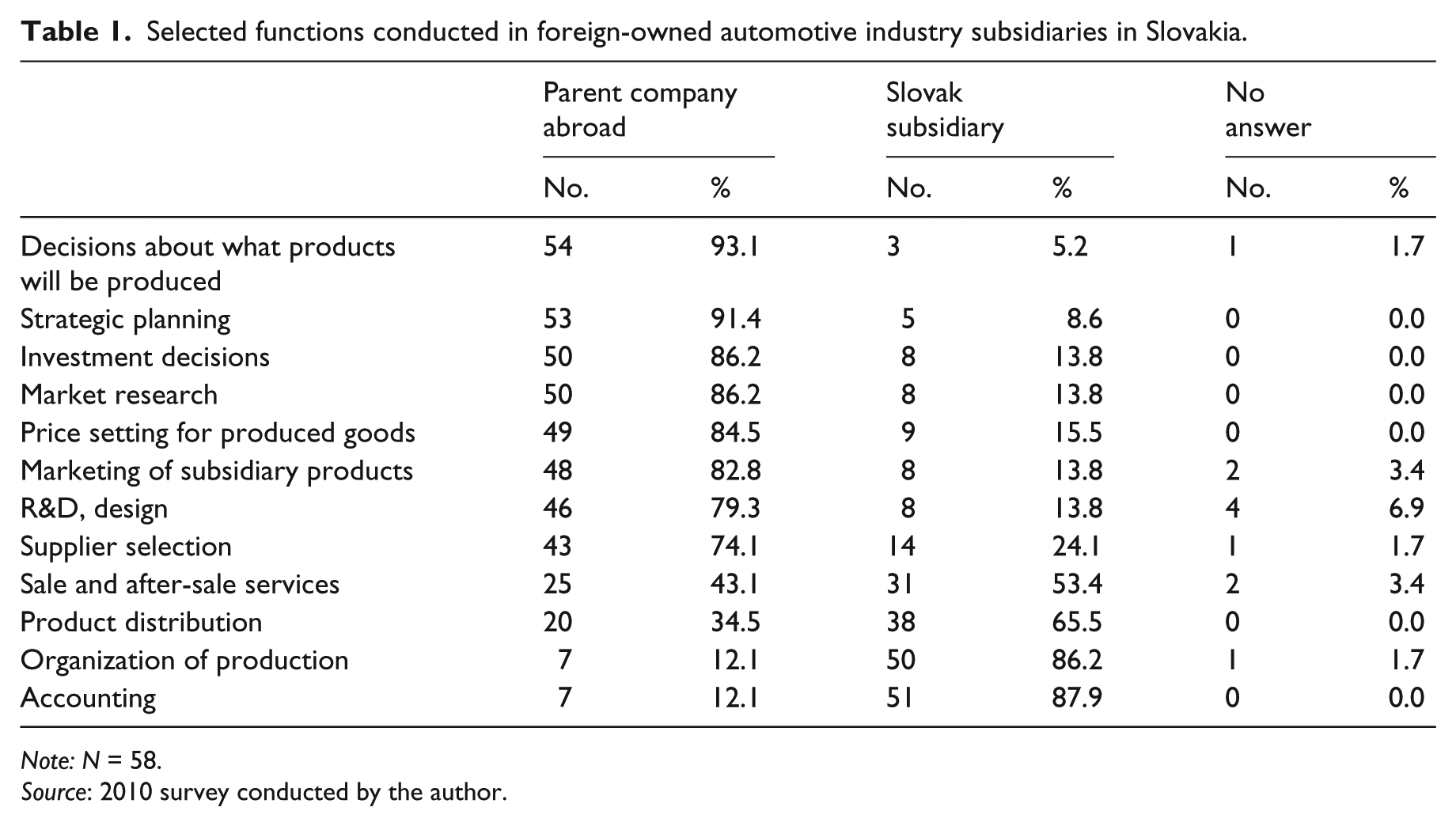

Selected functions conducted in foreign-owned automotive industry subsidiaries in Slovakia.

Note: N = 58.

Source: 2010 survey conducted by the author.

Economic geographers have analyzed the effects of FDI on national and regional economies since the 1970s (e.g. Britton, 1980; Dicken, 1976; Firn, 1975; Hayter, 1982). The early studies concluded that in addition to external dependency FDI-driven industrial development has long-term structural costs for less developed regions and countries in the form of truncated development. Truncated firms are defined as ‘subsidiaries and branch plants, which rely on their foreign based parent companies for various services and functions and whose autonomy is circumscribed by head-office dictates’ (Hayter, 1982: 277). Instead of upgrading and catching up with more developed economies, truncation tends to exacerbate the industrial and technological underdevelopment of host economies by developing routine capital-intensive and low-skill industrial activities, while high-skill and control functions remain concentrated in core regions/countries (Britton, 1980; Hayter, 1982). However, with the introduction of post-Fordist production methods since the late 1970s, there has been significant geographical reorganization of industrial activities by TNCs (Dicken, 2011), including changes in the relationship between TNCs and local areas (Dicken et al., 1994). We need, therefore, to consider the possibility that the conclusions of the truncation literature may no longer be as relevant in the early 21st century as they were in the 1970s and 1980s.

FDI-driven dependent development often results in rapid industrialization and fast economic growth. Certain ECE economies, such as those of Slovakia and Poland, have recorded some of the fastest rates of economic growth in Europe since 2000 (OECD, 2013), which could be largely attributed to FDI-driven extensive industrial development. In this type of economic development, ECE became specialized in labor intensive manufacturing, while control, R&D and other higher value-added functions, such as marketing and branding, remained concentrated in the global economic core. None of the three large foreign-owned automotive assembly plants in Slovakia have any R&D functions and their other higher value-added functions are extremely limited. Strategic planning, marketing, investment decisions, supplier selection, product pricing and distribution, sale and after-sale services are all located abroad in the home countries of their foreign owners (2011–2013 interviews). The 2010 survey of 299 Slovak-based automotive firms, conducted by the author and which yielded a response from 133 firms, showed that a similar situation exists among foreign-owned component suppliers in Slovakia. Subsidiary functions and competencies were reported by 58 foreign firms. The results, which are summarized in Table 1, confirm that the vast majority of foreign subsidiaries have limited non-production functions and that most strategic functions, such as strategic planning, investment decisions, product decisions, marketing and R&D are overwhelmingly concentrated abroad. In other words, the majority of foreign firms in the Slovak automotive industry do not engage in high value-added activities that remain concentrated abroad and, as such, they fit the notion of truncated branch plants. The survey results thus suggest that external ownership makes it less likely that higher value-added activities will be developed in Slovak-based foreign automotive firms, and are in line with the conclusions of the truncation literature on FDI effects in peripheral regions of developed countries (Britton, 1980; Dicken, 1976; Firn, 1975; Hayter, 1982). Although high value-added functions and competencies might gradually develop in some subsidiaries over time (Amin et al., 1994; Dicken, 2011), the evidence from both Western Europe and ECE suggests that to date functional upgrading in foreign-owned branch plants has typically been very limited and uneven (Amin et al., 1994; Pavlínek and Ženka, 2011; Phelps, 1993). Furthermore, truncation is also unfavorable for the development of a strong domestic automotive sector because it ‘necessarily implies that foreign investment replaces or preempts economically viable indigenous development’ (Hayter, 1982: 277).

In this mode of dependent development, value enhancement and value capture tend to be low (Smith et al., 2002). In the case of Slovakia, labor costs account for only 7% of the total cost of automotive assembly (Bella, 2013) and tax holidays reduce further the potential for value capture. In this respect at least the situation in ECE is reminiscent of peripheral regions in developed countries that were analyzed and reported in the literature on truncation. It is not surprising that the truncation effects of FDI in ECE were documented in the 1990s and 2000s (Grabher, 1994, 1997; Pavlínek, 2004, 2012). Consequently, the ‘catching-up’ process of ECE with the economic core and upgrading to a better position in the European automotive industry division of labor are likely to be limited, despite the rapid FDI-driven industrialization of the 2000s.

GPN and GVC approaches in particular have argued that successful regional and national economic development can be achieved through the active insertion of regions and countries into externally organized production networks and value chains (Coe et al., 2004; Gereffi, 1999; Gereffi et al., 2005; Henderson et al., 2002). For example, it has been argued that automotive branch plants located in peripheral regions are being transformed into ‘performance/networked branch plants’ that are embedded in local economies, have greater operating and even strategic autonomy and, as such, can gradually upgrade their functions and position in GPNs (Dawley, 2011; Pike, 1998). GVC and GPN perspectives have emphasized the possibilities for upgrading in peripheral regions through the coupling of local, regional and national assets with the strategic needs of TNCs (Coe et al., 2004; MacKinnon, 2012). The state plays an important role in building and maintaining regional and national assets in the form of particular labor skills, knowledge, regional institutions and FDI policies that attract foreign capital. There is evidence from East and Southeast Asia supporting these arguments (Yeung, 2009, 2013). Nevertheless, Dicken et al. (1994: 40–41) remind us that ‘the prospects for greater local embeddedness of TNCs created by the new organizational forms appear to be limited to a minority of favoured places’. Even performance plants located in peripheral regions have been susceptible to closure and corporate rationalization (Dawley, 2007), which suggests the continuing validity of the truncation argument. In the context of the automotive industry generally and of the ECE automotive industry specifically, the GVC/GPN perspectives seem to be unduly optimistic because firm-level upgrading, especially among domestic firms, has mostly been limited to process upgrading (Pavlínek, 2012; Pavlínek et al., 2009; Pavlínek and Ženka, 2011). Empirical evidence from ECE and other less developed countries also points to the decreasing role of domestic firms in automotive value chains, which are increasingly dominated by foreign firms (Barnes and Kaplinsky, 2000; Humphrey, 2000, 2003). Examples of successful strategic couplings in the ECE automotive industry are an exception rather than a rule (Pavlínek, 2012), while the newly developed dependence on foreign capital and truncation effects are widespread (Table 1).

A review of existing research thus suggests that state industrialization strategies based on large inflows of FDI are problematic because FDI represents a double-edged sword. It can lead to rapid industrialization and economic growth in host economies but at the expense of truncation, foreign control and dependent development. An empirical analysis of the role of the state in the development of the Slovak automotive industry follows, which supports my argument about the crucial role of ECE competition states in making the FDI-driven development of the automotive industry possible, despite their relatively weak bargaining position with foreign automotive TNCs.

The state and the automotive industry in Slovakia after 1990

Development of the automotive industry in Slovakia was limited before 1990. Final assembly was concentrated in Czechia, despite the construction of the Bratislava Automotive Works (Bratislavské automobilové závody – BAZ), which started in the early 1970s (Pavlínek, 2008; Studeničová and Uhrík, 2009). Throughout the early and mid-1990s, Slovakia was not perceived as a favorable destination for foreign investors because of the perceived uncertainty related to the establishment of the new independent country, weak investment incentives and shifting privatization and FDI policies mired in low transparency and corruption (Jakubiak et al., 2008; Javorcik and Kaminski, 2004; Smith and Ferenčíková, 1998). During this period, the Slovak government pursued an inward-oriented strategy of economic development that supported large domestic firms and was hostile to FDI (Drahokoupil, 2009a; Pavlínek and Smith, 1998). The failure of this policy to generate sustainable economic growth, combined with domestic pressure from the emerging comprador sector and external pressure from the EU, the International Monetary Fund (IMF) and the World Bank to open up to FDI (Medve-Bálint, 2014), paved the way for an alternative approach based on attracting large FDI inflows (Drahokoupil, 2008).

3

In its various reports the IMF, for example, repeatedly urged the Slovak government to speed up privatization and open up to FDI in the late 1990s: ‘Accelerated privatization of telecommunications and of other companies held by the State would convey an important message about the new government’s open attitude to foreign investors…’ (IMF, 1998 cited in Marcinčin, 2000b: 309). In its report, prepared for consultations with the Slovak government, the IMF (1999) considered macroeconomic instability, high rate of corporate income tax, the lack of tax incentives compared to neighboring countries, and the government’s privatization policy that discriminated against foreign investors in favor of domestic managerial groups, as the principal reasons for low FDI in Slovakia. In 1999 the IMF stated further that:

For the revitalization of the banking and corporate sectors it is most important to accelerate their restructuring and privatization. Delayed addressing of these serious economic issues would undoubtedly threaten the economic stability of Slovakia and reduce its chances for an early integration into Western Europe (IMF, 1999; cited in Marcinčin, 2000a: 335).

A shift away from the inward-oriented development strategies promoting national capitalism and the changing attitude to FDI was reflected in the ‘Program for the Development of the Automotive Industry in Slovakia’ approved by the nationalist government in July 1998 (Vestník, 1998) just before the administration was replaced by a ‘reformist’ (neo-liberal) government in October 1998, following the September 1998 elections. The Program defined the vision, strategy and goals of the development of the automotive industry up to 2010. It set three basic goals: (1) securing the supply of vehicles necessary for the development of the Slovak economy, while achieving a positive trade balance with automotive products; (2) increasing automotive output and restructuring related industries, especially the manufacturing, electronic, iron and steel, rubber and plastic industries; and (3) increasing the integration of Slovakia in the global economy through the automotive industry. Each of these basic goals had specific targets attached. For example, the automotive industry output was supposed to grow by 20% annually until 2000, by 15% between 2001 and 2005 and by 12% between 2006 and 2010. The government required the automotive industry to create 15,000 new jobs and invest 60–80bn Slovak crowns (US$1.7b–2.3b), mainly through FDI (US$1.4b–1.8b) by 2010. 4 The Program included detailed production goals for individual producers, such as trebling the output of VW Slovakia by 2010 and attracting at least one additional passenger car assembly plant of a global lead firm that would assemble 100–150 thousand units annually in Slovakia. There were also annual production goals for the assembly of trucks (2,000–3,000 units), buses (500–800 units), light commercial vehicles (2,000 units) and the components industry, the output of which was to quadruple by 2010. Domestic technological investment was intended to account for 15–20% of the total technological investment in the automotive industry, with the rest to be secured through FDI. Slovakia was to start exporting automotive technologies mainly to other ECE countries as well as developing and starting export business services for the automotive industry (Vestník, 1998).

Although the Program relied mainly on foreign capital for its financing, it called for state financial support of the automotive industry exports, employment, restructuring and regional development. It stressed the importance of state incentives for foreign investors, including lower taxes and the removal of trade barriers. It also declared state support for automotive R&D in Slovakia, labor force training and educational programs to train the labor force for the automotive industry, active seeking and attracting foreign investors, and the development of infrastructure and integrated information systems (Vestník, 1998). The Slovak Ministry of Economy became responsible for the entire Program, which was coordinated by the government’s plenipotentiary for the development of the automotive industry and further advised by the Council for the Development of the Slovak Automotive Industry. During its annual evaluation of the Program, the Slovak government specified tasks to be completed by individual ministries in a given time period in support of the Program. In other words, the state put in place a battery of policies designed to develop the automotive industry through FDI by global assemblers and component suppliers.

The goals set in the Program for the development of the automotive industry could only be achieved through large inflows of FDI, which required a radical opening of the domestic economy to foreign capital. In 1999, the government approved a ‘Strategy of the support of FDI entry’ (Medžová, 1999), which was a reaction to and emulation of the generous system of investment incentives introduced in Czechia in 1998 (Drahokoupil, 2009a). Investors investing at least €5m (€2.5m in regions with high unemployment rates) in setting up new manufacturing operations in Slovakia with at least 75% of foreign ownership were offered five years of tax holidays. They were required to export at least 60% of their output and could qualify for 50% lower taxes on their profits for an additional 5 years provided they invested an additional €5m (€2.5m in regions with high unemployment rates) (Medžová, 1999). The corporate tax rate was reduced from 40% to 29% and in 2003 the government introduced a 19% flat-rate tax and an employer-friendly, flexible labor code (Bohle and Greskovits, 2006; Duman and Kureková, 2012; Fisher et al., 2007). This radical shift in the treatment of foreign TNCs by the state was strongly influenced by the lobbying efforts of various organizations on behalf of foreign capital included in the comprador sector, such as the American Chamber of Commerce in Slovakia, by bilateral negotiations with foreign TNCs, and by the introduction of a ‘race to the bottom’ in tax regimes, labor protection and investment incentives for foreign capital in ECE (Bohle, 2006).

Although the Program seemed to be very ambitious when it was introduced in 1998, many of its goals – such as the employment, investment and total output targets of passenger cars – were achieved much quicker than the government had anticipated. This was the outcome of the extensive growth of the automotive industry after 2000 that was driven by large inflows of FDI that were strongly supported by investment incentives (Figure 1). At the same time, state support for the development of the indigenous automotive industry was virtually non-existent. While the pre-1998 state support targeted large domestic enterprises in basic industries, such as petrochemicals, chemicals, metals and the energy sector, and ignored the needs of small and medium enterprises (SMEs) (Beblavý, 2000), the post-1998 governments also failed to introduce any policy supporting the development of domestic SMEs (Duman and Kureková, 2012).

In order to illustrate further the role of the state in the development of the Slovak automotive industry, the next section provides short case studies of the role of the state in attracting three passenger car assembly plants to Slovakia after 1990: Volkswagen (VW), PSA and Kia.

The competition state and flagship investments by foreign assemblers

VW Slovakia

Throughout the 1990s the development of the Slovak automotive industry was closely linked to VW investment at BAZ. In 1991, VW proposed to assemble 30,000 automobiles annually at BAZ, produce gearboxes and reorganize the automotive supplier network in Slovakia. The joint venture (JV) agreement was signed in May 1991 and VW became the sole owner of VW Bratislava in 1994, renamed as VW Slovakia in 1999 (Studeničová and Uhrík, 2009; interview at VW Slovakia, 14 June 2011). One of the most important reasons why VW bought BAZ was the potential to increase its cost competitiveness by developing low-cost export-oriented production in Slovakia based on large labor cost differences between Germany and Slovakia (Pavlínek and Smith, 1998). In the early and mid-1990s, Slovak labor costs were at less than 10% of German labor costs. In 2011, the average hourly compensation costs in the automotive industry were still 79.4% lower in Slovakia than in Germany (USBLS, 2013) (Figure 3). Despite the claims that ‘the advantage of cheap labor no longer exists in the automotive industry’ (Bella, 2013), wage differences between the core and periphery are the ‘key to North-to-South offshoring’ (Baldwin, 2013: 31) and automotive firms try to minimize increases in wages and keep them as low as possible (Freyssenet and Lung, 2000). VW Slovakia is no exception and low wages continue to be extremely important with regard to its competitiveness.

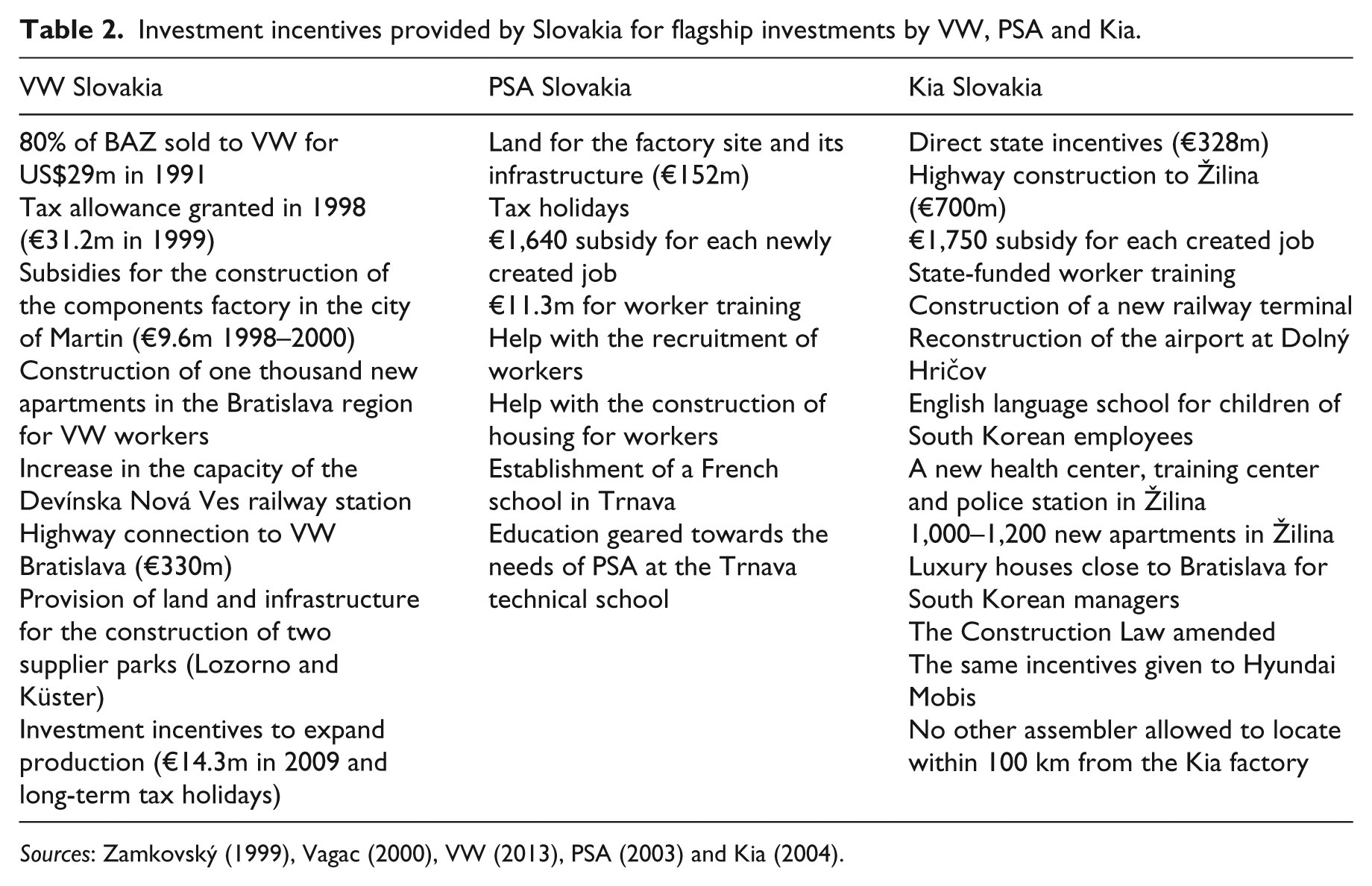

However, despite low production costs, the output of VW Slovakia increased slowly to 41,000 cars in 1997. VW demanded lower taxes as a precondition for increased production (Studeničová and Uhrík, 2009). After taxes were reduced in the middle of 1998, VW relocated the assembly of the Golf Synchro from Germany to Slovakia. As the most sophisticated Golf model, the Synchro required a higher level of labor input than more standardized Golf models and therefore benefited from the low labor costs in Slovakia. The output of VW Slovakia tripled in 1998 compared to the level in 1997. The successful assembly of the Synchro led to further production increases and by 2003 VW was assembling 281,000 passenger cars in Slovakia (interview at VW Slovakia, 14 June 2011). The state strongly supported this growth by approving investment incentives for VW and by subsidizing the location of foreign suppliers in Slovakia, in particular through the construction of supplier parks (Table 2). In 1997, VW had only four direct and nine indirect suppliers located in Slovakia (Javorcik and Kaminski, 2004) and the vast majority of components were supplied from abroad (Pavlínek and Smith, 1998). By 2004, 17 VW principal suppliers were located in two newly built supplier parks (interview at VW Slovakia, 21 July 2005). In 2009 the state subsidized the expansion of production, which increased the production capacity to 400,000 units and added 1,500 jobs. With strong support from the state, VW Slovakia thus successfully developed as a low-cost assembler within the VW corporate production network.

Investment incentives provided by Slovakia for flagship investments by VW, PSA and Kia.

Sources: Zamkovský (1999), Vagac (2000), VW (2013), PSA (2003) and Kia (2004).

State policies towards VW Slovakia contributed to the development of the competition state. By the early 2000s, Slovakia was able to compete with other ECE countries in attracting large FDI projects, as demonstrated by the decisions of PSA and Kia to build their assembly plants in Slovakia. Both investments illustrate the active role of the Slovak state in the development of the automotive industry and its willingness to engage aggressively in the ‘race to the bottom’ with its Central European neighbors over flagship automotive investment projects.

PSA Peugeot-Citroën Slovakia

The November 2002 announcement by PSA that it would build a €700m assembly plant in ECE, mainly because of 75% lower labor costs compared to France (Schönwiesner, 2002), started a bidding war among Czechia, Hungary, Poland and Slovakia. Eventually, Hungary and Poland lost because of high labor costs compared with Slovakia and also because of the poor quality of the infrastructure at the proposed site at Radomsko in Poland (Trend, 2003). Czechia was disqualified because PSA was already building a JV factory with Toyota (TPCA) at Kolín and also because of the poor quality of infrastructure and unresolved previous environmental liabilities at the proposed factory site close to the city of Žatec (iDNES, 2003). PSA chose the Slovak offer and its proposed Trnava site. The total value of investment incentives was limited by EU regulations to 15% of the original investment. Slovakia offered €152m in the form of the land for the factory site and its infrastructure, tax holidays, a €1,640 subsidy for each newly created job and €11.3m for worker training. The state also promised to help with worker recruitment, education geared towards the needs of PSA at the Trnava technical school, the construction of housing for workers and the establishment of a French school in Trnava (PSA, 2003). The combination of investment incentives, low labor costs and high unemployment rate in the Trnava region (around 13%) were the most important factors favoring Slovakia, in addition to Trnava’s automotive tradition, well developed infrastructure and its proximity to the capital Bratislava (Table 2). At the time of negotiations, the government did ‘the maximum to accommodate the wishes and needs of PSA’ (interview at PSA Slovakia, 17 June 2011).

Kia Slovakia

The Slovak competition state was the most aggressive in attracting an investment by Kia of US$1.5bn. In November 2002 Hyundai top management began to negotiate with politicians of Czechia, Hungary, Poland and Slovakia but kept them guessing about its selection process. In August 2003 it was reported that the decision about the factory location would be made, the choice being either Hungary or Czechia, with Czechia being the frontrunner (Kremský, 2003). At that point, the Slovak minister of Economy traveled to South Korea to present in person a new package of investment incentives to the management of Kia, ‘an offer which was impossible to refuse’ according to a highly ranked former official at the Slovak Ministry of Economy (Kolesár, 2007: 59). Kia obviously used the late Slovak offer to attempt to obtain bigger incentives from Hungary and Czechia. Both countries complained that the size of incentives sought by Kia violated EU and national regulations and exceeded the expected benefits of the investment (Kolesár, 2007; Pavlínek, 2008). This suggests that Slovakia was overbidding and ended up paying too much for the investment. 5 Kia eventually selected Slovakia on 2 March 2004. The size of the investment incentives was the decisive factor, in combination with low labor costs and low labor militancy (Table 2). Slovakia simply provided everything Kia asked for (Kolesár, 2006, 2007), including promises that the state would not change laws for the duration of the investment in such a way ‘that would endanger economic benefits of the state support for Kia’, would not change its tariff policy and defend the investment incentives for Kia with the European Commission and defend Kia’s interests in any potential dispute (Kia, 2004). At the same time, Kia was to receive all of the incentives, even if it did not complete all of the investments listed in the contract, and Slovakia had no right to demand any additional investment or return of any investment incentives (Kia, 2004). The contract was thus extremely one-sided, suggesting a very asymmetrical power relationship between Kia and the state, and it represents an example of corporate capture (Phelps, 2000, 2008).

In 2005, Slovakia won another regulatory arbitrage over the €500m investment by South Korean Hankook Tire by offering €105m or 21% of the total value of the investment. In this case, however, the government did not approve the investment agreement after strong criticism from Slovak entrepreneurs and politicians that the country would be paying too much (€90,000) for each newly created job. Slovakia then offered lower incentives (€25,000 per job or 6% of the total value of the investment), which Hankook refused and, instead, built the factory in Hungary, which offered €56m in direct incentives (12% of the value of the investment) (Kolesár, 2006). The case of Hankook Tire suggests three important conclusions. First, investment incentives do matter, despite the fact that TNCs and competition states tend to downplay their importance, compared to other factors, in location decisions. The size of investment incentives was obviously the most important factor in the final choice made by Hankook Tire between Slovakia and Hungary. Second, the Slovak competition state had reached its limit with the Kia investment and the state recognized that attracting FDI at any cost might be counterproductive. Third, states can ultimately limit the power of TNCs and the comprador sector on their territories but often at the expense of foreign capital exit.

Beyond assemblers: state policies from the perspective of component suppliers

As can be seen, VW, PSA and Kia benefitted significantly from investment incentives and therefore it is not surprising that they evaluated the state automotive industry policy positively during 2011–2013 interviews. In addition to investment incentives, they stressed the importance of the flat tax and the adoption of the Euro. The assembly companies, together with the OECD (2012), would like to see the creation of ‘as flexible labor markets as possible’ and the restructuring of the education system so that it would reflect better the ‘market demand for labor’ (interviews at VW Slovakia, Kia Slovakia and PSA Slovakia on 14, 16 and 20 June 2011). However, it has been argued that the state offered large investment incentives to foreign TNCs at the expense of tax payers and SMEs (Bohle and Greskovits, 2006; Zamkovský, 2001). Indeed, after 1998, when Slovakia began to vigorously compete for automotive FDI, the state withdrew from the welfare system and from supporting domestic firms (Duman and Kureková, 2012), spending on education in Slovakia has been one of the lowest among the OECD countries (OECD, 2013), and state support for domestic research has been erratic. 6

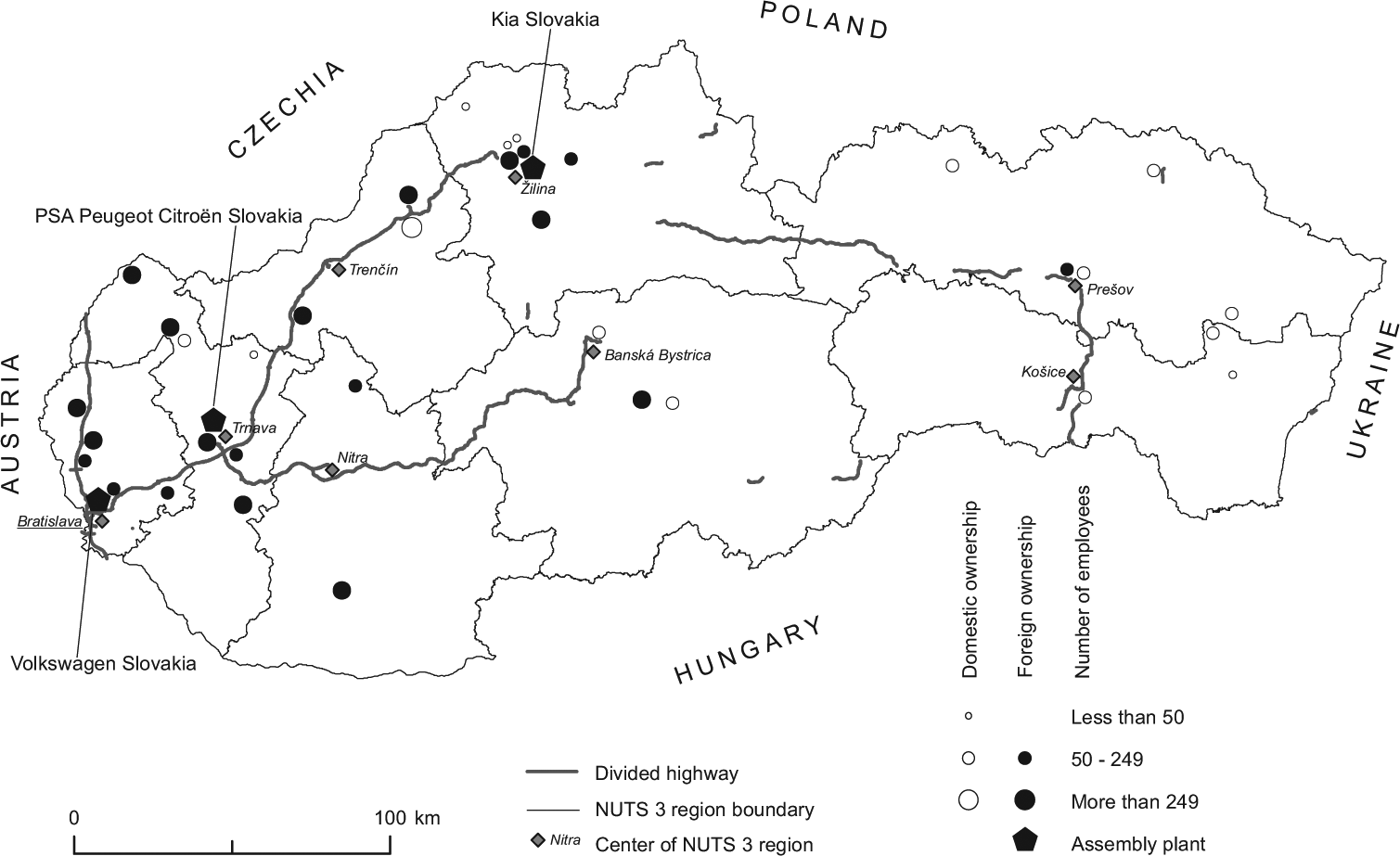

Therefore, this article looks next beyond large TNC assembly companies in order to gain a broader perspective on how the Slovak-based automotive firms evaluate state policies concerning the automotive industry. It draws on 38 on-site interviews with automotive firms conducted in Slovakia between 2011 and 2013 with 15 domestic-owned (henceforth domestic) firms and 23 foreign-owned (henceforth foreign) firms, including VW, PSA and Kia (Figure 4). The firms interviewed comprise a representative sample selected from the database of 299 Slovak-based automotive firms in terms of size, ownership and position in the supplier hierarchy. The interviews were conducted with directors or top managers and included various questions about the operation and development of automotive firms in Slovakia. Foreign firms were asked whether the state economic and industrial policies helped them develop, or at least maintain, the strategic asset which led them to invest in Slovakia. Domestic firms were asked a similar question: whether the state economic and industrial policies helped them improve or at least maintain their competitive advantages. The results are summarized in Table 3.

The location of interviewed automotive firms in Slovakia.

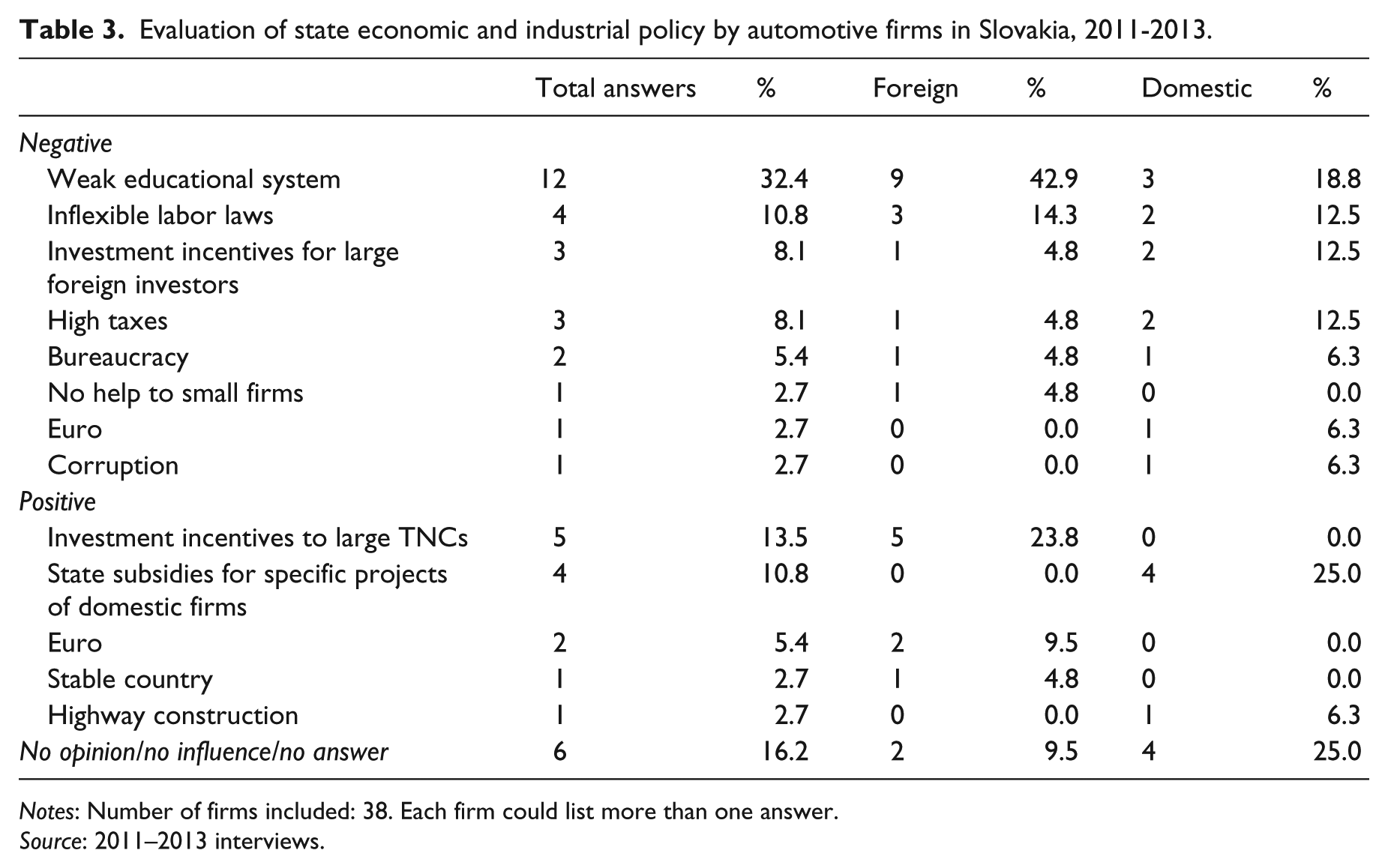

Evaluation of state economic and industrial policy by automotive firms in Slovakia, 2011-2013.

Notes: Number of firms included: 38. Each firm could list more than one answer.

Source: 2011–2013 interviews.

Of the 33 answers, eight respondents (24%) evaluated the state policy towards the automotive industry positively, 20 (61%) negatively, and five evaluations (15%) were neutral, highlighting both positive and negative perceptions of the state policy. Of the 12 domestic firms who replied to the question, three (25%) viewed the effects of state economic policies positively and nine (75%) negatively. Among foreign firms, five of 21 responses (24%) were positive, 11 (52%) were negative and five (24%) were neutral. A less critical view of state policies by foreign compared to domestic firms could be attributed to the fact that many foreign firms strongly benefited from investment incentives, which some firms appreciated, while criticizing other aspects of state policies. In many cases, however, foreign firms failed to mention incentives and emphasized negative aspects of state policies.

Table 3 highlights the positive and negative views on state economic and industrial policies expressed by those interviewed in addition to different views expressed by foreign and domestic firms. Automotive firms were concerned most about the quality of the Slovak labor force and the failure of the state to educate the workforce adequately in order to satisfy the needs of automotive firms. The weak education system was highlighted by 43% of foreign firms and 19% of domestic firms, suggesting that the quality of the workforce was a bigger problem for foreign than for domestic firms. Domestic firms might be better accustomed to the existing quality of the local labor force and, therefore, do not perceive it to be a major problem. Respondents complained about difficulties encountered in finding skilled workers on the labor market and the lack of practical skills possessed by graduates from state schools at all levels. Quotes from four different interviews highlight the problems felt by foreign firms:

We need a high share of skilled workers for our operations, and I am not talking about operators, but technicians and engineers. Here, I need more brains, more people thinking how they can better perform, improve processes and machines. And I am struggling with that. And that are the two factors my parent company needs to be successful in Slovakia. Definitely it would be preferable to get it locally, to start with the base where people are trained, where they have the automotive industry spirit. But this is not the case (interview with CEO of foreign firm, 23 June 2011). The problem is the support from the government. It is very formal and difficult to follow. The government is not providing the conditions we need. We have problems to find enough employees, the unemployment rate is very low, especially in this area, in Bratislava and it is the same for Košice. More importantly, in my opinion, the labor force training is not good in Slovakia, the training after school, so that they [young workers] would have the training in factories and not [just] the theoretical training. I would pay for that. And that is missing here (interview with CEO of foreign firm, 22 June 2011). A long-term problem of the Slovak education system is that it does not reflect labor market demand. What is missing here are technically-oriented workers with university degrees, and, of course, workers with the vocational and high school technical training. The existing demand is not absolutely covered… Certainly, we feel that the education system is not adequately supported by the government (interview at a vehicle assembly firm, 22 June 2011). The government should be really investing in the qualification of students, qualification of workers, or it will be a mess. The problem is really, what is the benefit of purchasing from Slovak companies today? I can buy cheap products somewhere else but I can’t find good products here (interview with CEO of foreign firm, 23 June 2011).

Increasing labor shortages in the rapidly growing automotive industry forced the government to restructure the state run system of vocational training and initiate changes in the structure of educational programs in state universities in the mid-2000s. The government argued that universities ‘must permanently adjust their curricula to the needs of the automotive industry and closely cooperate with the industry’ (SEM, 2005). This quotation implies corporate capture in the area of education and training policy-making, but no positive outcomes of these state efforts were acknowledged by automotive firms during the 2011–2013 interviews. Thus, despite corporate capture, the Slovak state has so far been unable to satisfy the needs of foreign TNCs in the area of educational policy and labor force training that are essential for their continuing success in Slovakia and for the potential upgrading of the Slovak automotive industry.

The second most cited criticism of state policies in Slovakia was the perceived inflexible labor law, especially in terms of hiring and firing workers according to the momentary needs of firms, and the inability of firms to use short-term employment contracts. Additional negative views included the support for foreign investors at the expense of domestic firms, the strong Euro, which was undermining the competitiveness of domestic products in foreign markets, high and rising taxes, and corruption. Among the positive aspects of state economic and industrial policies, foreign firms appreciated investment incentives most, while several domestic firms highlighted the importance of state subsidies for their specific projects. Two respondents emphasized the importance of the Euro for their firms (Table 3).

Limits of the state-foreign capital nexus

The long-term goal of the state is to improve Slovakia’s position in automotive GPNs through industrial upgrading. It should be achieved through the development of automotive R&D (SEM, 2005), which seems to be a typical approach towards the automotive industry in less developed economies. As Humphrey and Oeter (2000: 55) argued ‘governments expect to generate investment and employment in labour-intensive activities in the short term, and hope that eventually higher-skilled jobs will also be created’.

Firm-level interviews confirmed that Slovakia is attractive for the FDI-driven development of R&D activities because of its low R&D labor costs (2011–2013 interviews). However, the limited supply of an R&D labor force is viewed as a major constraint. A director of the foreign-owned supplier of plastic parts in Slovakia argued during an interview on 23 June 2011, ‘we [foreign investors] are all struggling with [low] technical competencies and knowledge of university graduates’. More importantly, given the overwhelming dependence of the Slovak automotive industry on foreign capital, the state effort to develop strategic automotive R&D in Slovakia is likely to succeed only if it is in line with the strategic need of automotive TNCs. To date, automotive lead firms have engaged in very limited internationalization of their R&D into ECE (Pavlínek, 2012). Given these constraints, the development of larger-scale and strategic automotive R&D, beyond more routine R&D, is likely to be difficult to achieve in Slovakia. Industry-financed expenditures on R&D decreased in Slovakia from 0.65% of GDP in 1995 to 0.2% of GDP in 2010 (OECD, 2013) and Slovakia fell further behind many advanced and emerging countries because its industrial R&D investment did not keep up with the extensive growth of automotive production during the 2000s.

The dependence of the development of the automotive industry in Slovakia on the strategic needs of foreign TNCs is obvious from the fact that the annual production targets specified by the government in 1998 (Vestník, 1998) for the assembly of trucks, buses and light commercial vehicles have not been achieved. This illustrates that the state policy has only been successful to the extent that it has met the strategic needs and goals of large automotive TNCs. High volume production of passenger cars and labor intensive assembly of special models in particular could benefit from the combination of a cheap labor force and investment incentives to develop low-cost production in integrated peripheral markets. To date, automotive TNCs have not shown any interest in the assembly of trucks, buses and light commercial vehicles in Slovakia.

Superficially, state policies for the development of the automotive industry in Slovakia appear to be extremely successful. FDI in the automotive industry has contributed strongly to capital formation, exports, the balance of payments and employment. For example, in 2012 the narrowly defined automotive industry (NACE 29) directly employed 60,828 workers (compared to 6,000 in 1993) and it generated an additional 140,000 jobs indirectly (Luptáčik et al., 2013). However, despite the FDI-driven economic growth, the unemployment rate has remained one of the highest among OECD countries, and the concentration of automotive FDI in western Slovakia, where 74% of all automotive firms are located, has contributed to uneven development. As of 2011, Slovakia recorded the highest regional inequalities at the TL2 level among OECD countries (OECD, 2012). It is also questionable to what extent large investment incentives contribute to self-sustaining growth (Amin et al., 1994). More importantly, this growth has been achieved at the expense of subordinating state policies and decision-making to those of foreign capital. Bella (2013) has argued: ‘Volkswagen and Kia do not care about the enforceability of law or the administrative maze [in Slovakia] because any government minister is as far away from them as the nearest phone and they manage to negotiate a service from the state they need’. State industrial policies have been driven by the needs of foreign capital, resulting in foreign-capital dependent development (Nölke and Vliegenthart, 2009) and corporate capture (Phelps, 2000), in which automotive lead firms achieved disproportionate influence over government decision making and its economic policies.

Conclusion

There is no doubt that Slovakia has experienced extremely successful growth in the automotive industry when measured by its rapidly increased output and exports. This article has demonstrated that the state and its policies concerning foreign capital have played an important role in this growth, by opening the domestic economy to FDI and by competing successfully for large FDI projects with generous investment incentives and low taxes. It has also illustrated the power of automotive lead firms to achieve the best possible investment terms from the states through regulatory arbitrage among countries with similar factor endowments.

The development of extensive spillovers from foreign to domestic firms, which would drive the upgrading and development of a strong domestic automotive sector, might justify FDI-driven industrialization policies and large state expenditures spent on attracting foreign lead firms. At present, the lack of available data makes it impossible to evaluate the extent of spillovers in the Slovak automotive industry but ‘the spillover effect on domestic companies in the [automotive] sector is likely to be very limited’ (Šipikal and Buček, 2013: 479). Experience from other integrated peripheral markets, such as Mexico, suggests that the development of capabilities of local suppliers is a long-term process that takes decades to come to fruition (Sturgeon et al., 2010). Furthermore, the current configuration of the global automotive industry has not been favorable with regard to the extensive development and upgrading of domestic firms beyond process upgrading (Barnes and Kaplinsky, 2000; Humphrey, 2000, 2003). In other words, a strong development of the domestic automotive industry that would justify high levels of state expenditure on attracting foreign firms, reduce the dependence of the Slovak automotive industry on foreign capital, and stabilize the supplier network in Slovakia, will be difficult to achieve. The future success of the automotive industry in integrated peripheral markets, such as Slovakia, will continue to depend on FDI and the transfer of foreign technology. However, the wage-competitiveness of Slovakia, its distinct advantage in the 1990s and early 2000s, has been eroded as Central European currencies devalued during and after the 2008–2009 economic crisis (OECD, 2012) and Slovakia has increasingly been threatened by relocation of the most cost-sensitive labor intensive activities to lower-cost countries (Pavlínek, 2015). 7

Firm-level interviews suggested that long-term state investment in higher education and vocational training is important for maintaining and improving the competitiveness of Slovak-based automotive firms and it is crucial for the development of higher value-added functions in both foreign subsidiaries and domestic firms. Because local value creation is based on high knowledge activities stemming from both domestic and foreign firms, the development of these competencies would help Slovakia upgrade its position in automotive GPNs from being a predominantly automotive industry subcontractor based on cheap labor to a knowledge-based automotive producer with innovative globally-oriented foreign and domestic firms. As can be seen, however, while the state has been willing to offer generous incentives to foreign firms to invest in Slovakia, its investment in vocational training and higher education has been inadequate to meet the labor needs of automotive firms. The state support of R&D and of the development of innovative domestic firms has also been inadequate. To date, the state has mainly pursued quick, FDI-based policy solutions rather than a long-term policy focusing on the development of strategic assets that could attract FDI in higher value-added functions.

External control and dependence on foreign capital and technology represent the greatest weaknesses of the FDI-driven industrialization. Overwhelming foreign ownership means that ultimate decisions about the industry are made abroad by TNC headquarters in the context of their global operations. Sturgeon et al. (2010: 232) have recently argued with respect to Mexico: ‘Clearly, the fate of an [automotive] industry in a small, regionally embedded country like Mexico is tied to factors that lie largely outside the control of the state or of local firms’. To a large extent state industrial policies in Slovakia have been subordinated to the needs of foreign capital, leading to corporate capture, which may limit the abilities of the state to pursue independent industrial development policies. Large investment incentives and low corporate taxes undermined the ability of the state to finance adequately domestic research, education and the support of domestic firms. Ultimately, therefore, the rapid development of the automotive industry in Slovakia, ECE as a whole, as well as other integrated peripheral markets, is to be attributed to a successful spatial fix by global automotive lead firms. The rapidly increased automotive output and exports tell us more about the successful offshoring of automotive technologies and production models by German, French, South Korean and other foreign firms to Slovakia than they do about the capabilities of the domestic automotive industry (Baldwin, 2011). Based on the experience of other peripheral regions, it is unlikely that foreign lead firms will develop higher value-added functions to a significant extent in Slovakia. In the long term, it is likely that value transfer in the form of profit repatriation by foreign firms will exceed the value of invested foreign capital, and the profit-seeking behavior of foreign firms will not necessarily be aligned with long-term state development goals. For example, because foreign automotive firms have been most interested in low-cost production in Slovakia, they will be interested in maintaining the wage gap between Slovakia and Western Europe; while the state should strive to close this gap in order to increase the standard of living of its population. In such a situation, it will be difficult for Slovakia and other ECE countries to improve substantially their peripheral position with regard to the division of labour in the European and global automotive industry and join the core areas of the automotive industry in order to benefit fully from the rapid FDI-driven development that has taken place since the early 1990s.

Footnotes

Acknowledgements

The author wishes to thank the editor and two anonymous referees for their comments on an earlier version of this article. I am grateful to Pavol Hurbánek and Jan Ženka for help with organizing and conducting company interviews in Slovakia. I acknowledge the help of Jan Ženka with the administration of the company survey. I also want to thank Karel Hostomský for preparing the map.

Funding

This work was supported by the Czech Science Foundation [Grant Number 13-16698S].