Abstract

Lower-skilled workers face increasing pressures. Their bargaining position is declining under the twin pressures of globalisation and technological change; and they risk losing access to better positions as firms’ pay and conditions arrangements increasingly drift apart. Rising between-firm differences partly come about through increasing separation of lower-skilled workers into lower-paying firms with worse conditions, thereby reducing their opportunities further. Such polarisation is partly driven by (domestic) outsourcing where main firms take certain tasks that are seen as non-core out of their payroll, instead purchasing those same tasks from another official employer or temporary employment agency while retaining control. Outsourcing generally brings worse conditions and lower pay. This paper uses cross-national European data from the Labour Force Survey (LFS) along with contextual data to study how outsourcing – proxied by moves to business services providers or temporary employment agencies – contributes to a worse labour market position of lower-educated workers over time. I find that (1) domestic outsourcing is increasing over time across Europe; (2) outsourced workers are working under generally worse conditions than their counterparts; and (3) this process is not universal: it hits harder in sectors with greater technological innovation and can be alleviated by union density and worker representation.

Introduction

People’s working lives are increasingly fragmented, with the variation in employment relations and labour market outcomes growing (see e.g. Rubery, 2015; Weil, 2014). This fragmentation is linked to greater polarisation between workers on different dimensions of vulnerability. It drives inequality as it divides workers who are in better-paying and more protected positions from those more on the periphery (Flecker, 2010).

This greater divide between workers is shown clearly in recent work highlighting that workplaces become increasingly homogenous. While several studies have shown greater differences in pay between firms and a rising homogeneity across countries (Criscuolo et al., 2020; Tomaskovic-Devey et al., 2020; Wilmers and Aeppli, 2021; Zwysen, 2022a), less attention has gone to the mechanisms behind this rising homogeneity, which entails exclusion of workers that are seen as not core (Weil, 2014).

This paper focuses on one key mechanism through which workplaces circumscribe which workers are retained internally as core workers, and share in benefits, while others are moved to an outside firm or contractor: domestic outsourcing (OECD 2021; Weil 2014). While there is indication that domestic outsourcing events are increasing and are associated with worse labour market outcomes (see e.g. Bergeaud et al., 2021; Goldschmidt and Schmieder, 2017; OECD, 2021), this study goes beyond the existing literature by considering trends herein and how they are linked to macroeconomic and institutional factors making domestic outsourcing more likely. This is done by using representative cross-national data across the European Union countries from the Labour Force Survey [LFS] from 2001 to 2020. Fragmentation and outsourcing is proxied by (1) workers moving to the business service provider sector and (2) workers working for a temporary employment agency.

Conceptual framework

Labour markets are increasingly fragmented (see e.g. Rubery, 2015; Weil, 2014). Over time, the variation in employment relations and contract types is growing, with a greater divide in conditions between those workers carrying out what are considered core activities and those more on the periphery (Flecker, 2010). These phenomena of fragmentation and polarisation have been well studied in employment and industrial relations studies, where the growing complexity of employment relations, including the case where workers’ conditions and employment relations are shaped by more than one employer as in the case of outsourced work done at a site of another company, are described (Flecker, 2010; Grimshaw et al., 2004; Marchington et al., 2011).

The labour market position is particularly under pressure for the lower-educated. Their bargaining position is declining under the twin pressures of globalisation and technological change which reduces demand for lower-skilled, often routine, labour while increasing the demand for higher-skilled workers (Autor et al., 2003; Kalleberg, 2011; Michaels et al., 2013).

One important instance of this wider fragmentation of work is the outsourcing of tasks by separating the company where a task is performed from the official employer (Grimshaw et al., 2023). The degree of subordination to the outsourcing firm means workers are increasingly dependent on multiple and complex networks of employment relations. Generally, through competitive pressures, conditions of work are worse the further employees are from the core or main employer, as can be seen for instance in global value chains or chains of subcontractors (Flecker, 2010; Weil, 2014).

Such fragmentation is not random, and the decision of which workers are core is deeply embedded in systems of power relations within the organisation (Grimshaw et al., 2004; Tomaskovic-Devey and Avent-Holt, 2019). At the same time, structural economic and institutional trends have made these processes more likely and create incentives to circumscribe which workers to retain within the main firm (Flecker, 2010; Rubery, 2015; Weil, 2014).

A related and growing literature documents rising importance of where people work for their wages (Criscuolo et al., 2020; Tomaskovic-Devey et al., 2020; Zwysen 2022a, 2022b). This rising inequality between firms partly reflects a greater segregation and sorting of lower-paid workers with other lower-paid workers in lower-paying firms (Abowd et al., 1999; Song et al., 2019), as well as widening differences in what firms pay otherwise similar workers, through processes of rent sharing or through frictions in job search (Barth et al., 2016; Card et al., 2017; Mortensen, 2003).

One consequence of these pay differences between firms is precisely a division into core and peripheral workers whereby the firm seeks to restrict the better conditions to the workers seen as most necessary and seeks to exclude the others. Indeed, over time, firms’ workforces have become more homogenous (Godechot et al., 2020; Handwerker, 2023; Wilmers and Aeppli, 2021). Particularly, lower qualified workers are increasingly kept out of the better positions which, along with higher pay, also offer superior and more stable conditions (Kristal and Cohen, 2017; Wilmers and Aeppli 2021).

Domestic outsourcing – the situation where a worker is legally employed by one firm but, in practice, working for another (the lead firm) – is one process through which such exclusion of workers not seen as core happens. The lead firm has a continuing need for these workers, and exerts significant supervision or control, but is not the legal employer (OECD 2021). This is one route to wage discrimination at firm level (Goldschmidt and Schmieder 2017). This situation falls within what Weil (2014) named the fissured workplace – where firms increasingly focus on their own core tasks and use different set-ups to outsource tasks to flexible contractors, or franchisees, who have to follow strict standards set by the lead firm but are not legally employed by that firm. Temporary employment agency work can be seen as one instance of such domestic outsourcing and fits within the wider aspect of non-standard employment (Drenik et al., 2023), although it is somewhat more regulated generally. Temporary agency work is generally rather insecure and precarious and is part of this ongoing fragmentation of employment types and rising use of non-standard employment or alternative work relations (Mas and Pallais, 2020; Retkowsky et al., 2023; Yang et al., 2023).

Of course, outsourcing can also happen across borders (referred to as offshoring), but the focus here is on the process where the job itself does not leave the country, but is taken out of the company. This is done as the focus lies on the labour market inequalities within one country.

Such alternative work arrangements – through outsourcing and engaging employment temporary agency workers – are attractive to employers as it can provide flexibility, allowing employers to make use of specialised labour which they not have to keep as staff when it is not being used. Second, outsourcing can be a way to cut costs, even though the cost of outsourced labour includes both personnel costs and the company overhead. Costs are cut because workers that are deemed less competitive are excluded from common wage policies (Weil 2014). In pay setting, workers perceive that the differences between and among roles should be fair, but such considerations no longer hold when purchasing a service. By changing the logic of pay setting to one of paying for a service, these workers are generally excluded from any form of premia, also called rent sharing, through which workers participate in their firms’ profitability or productivity.

While parts of the literature identify key economic reasons having to do with the evaluation of the company’s performance and the pressure of financialisation there is also a power dynamic at play. Within companies the calculation of which jobs or workers are seen as key will likely differ reflecting societal evaluations and generally be to the detriment of more vulnerable workers. Given these power dynamics and the structural changes moving to more specialised firms, which is rewarded by the financial markets, these more vulnerable workers are at risk of exclusion (Dünhaupt, 2017; Flecker, 2010; Rubery, 2015; Weil, 2014).

Indeed, several studies that identify the impact of outsourcing on outsourced workers’ pay and conditions find that their wages tend to decline relative to those not outsourced. This penalty is estimated at between 4% (Bergeaud et al., 2021) and 12% (Bilal & L’Huillier 2021) in France, 8–19% for temporary agency workers in Argentina (Drenik et al., 2023), 4–7 per cent, or 8-24% for specific profiles, in the United States (Dube and Kaplan, 2010), and around 10% in Germany (Goldschmidt and Schmieder 2017). Where it is possible to measure this, these pay losses are almost completely due to outsourced workers losing out on firm or industry premia and rents (Drenik et al., 2023; Dube and Kaplan, 2010; Goldschmidt and Schmieder 2017). While most studies focused on wages, one study found the risk of job separation also increases, which may further indicate other work conditions are affected as well (Goldschmidt and Schmieder 2017).

Crucially, such processes of fragmentation, of which outsourcing is a type, differ by the institutional and macroeconomic context (e.g. Flecker, 2010; Grimshaw et al., 2004; Rubery and Grimshaw, 2003). One key difference is the extent to which the outsourced workers have representation and voice, and thereby the extent to which their bargaining power is diminished. Institutions however also determine the extent to which these complex relations are managed and power imbalances are exploited (Grimshaw et al., 2023). These processes are also guided partly by common global trends in the labour market that threaten the position of lower-educated workers specifically.

While there is a general increase in the use of domestic outsourcing, it is not always as likely or has the same effects, as its use and implementation are affected by contextual factors. It is then important to consider variation over countries and industries in the likelihood of such outsourcing, and in its effects on workers. This paper considers three key factors. While these are not exhaustive, as there is further difference based on the company culture or, in the case of the public sector for instance, external demands for cost-cutting, these factors aim to capture cross-national and cross-sectional variation through differences in (1) the incentive to exclude workers from the main workforce by increasing rents to be shared; (2) the relative differences in demand for higher- and lower-skilled workers which increases the vulnerability for lower-educated workers and their risk of outsourcing through lower bargaining power; and (3) the collective support of workers which can affect the propensity to outsource and its impact on outcomes.

First, new technologies are increasing the demand for high-skilled workers and can contribute to wage polarisation (Autor et al., 2003; Goos et al., 2014). As firms differ in their ability to take up new technologies, productivity differences also grow, in turn raising divergence in firm premia and increasing inequality overall (Berlingieri et al., 2017; Faggio et al., 2010). New technologies may also make it easier to monitor employees and maintain standards while outsourcing (Bergeaud et al., 2021; Fort, 2017).

Second, globalisation and trade affect wage differences by skill as some, often lower-skilled, tasks can more easily be offshored and replaced by the import of intermediate products from countries where labour costs are lower (Autor et al., 2016; Kramarz 2017; Michaels et al., 2013). Further, international trade provides opportunities for exporting firms which increases their incentives to offer higher pay for high-skilled workers, increasing the firm premia overall. Of course, globalisation may also weaken the position of more vulnerable workers by offering the opportunity of offshoring, or international outsourcing. In this paper, however, I focus specifically on how variation due to the on average increased rents and weakened position of lower-educated workers put them more at risk of exclusion also in the domestic labour market (Davidson et al., 2014).

Third, institutions that should protect workers and compress the differences between workers and firms, such as collective agreements and trade unions, have declined over time (Tomaskovic-Devey et al., 2020; Zwysen 2022b; Zwysen and Drahokoupil 2022). The impact of trade unions and collective agreements is however not so straightforward as empirically, it is not clear that they always protect all workers as they may benefit insiders. However, previous research does show that unions generally oppose domestic outsourcing (Bernhardt et al., 2016; Perry, 1997). Trade union weakening is also explicitly linked to a greater use of outsourcing specific tasks (Goldschmidt and Schmieder, 2017). I then expect that stronger worker representation is associated with less outsourcing in general and less inequality between workers in this risk as it supports their bargaining power. However, stronger trade unions may, at the firm level, be associated with greater rent sharing and thereby indirectly increase employers’ incentives to circumscribe their workforce (Kramarz, 2017). Regarding the link with job quality, in the European system the extent to which outsourced workers would still fall under the same collective agreements would strongly affect the extent to which conditions can change. It is therefore important to consider the impact of outsourcing and subcontracting under different types of agreements, where possible.

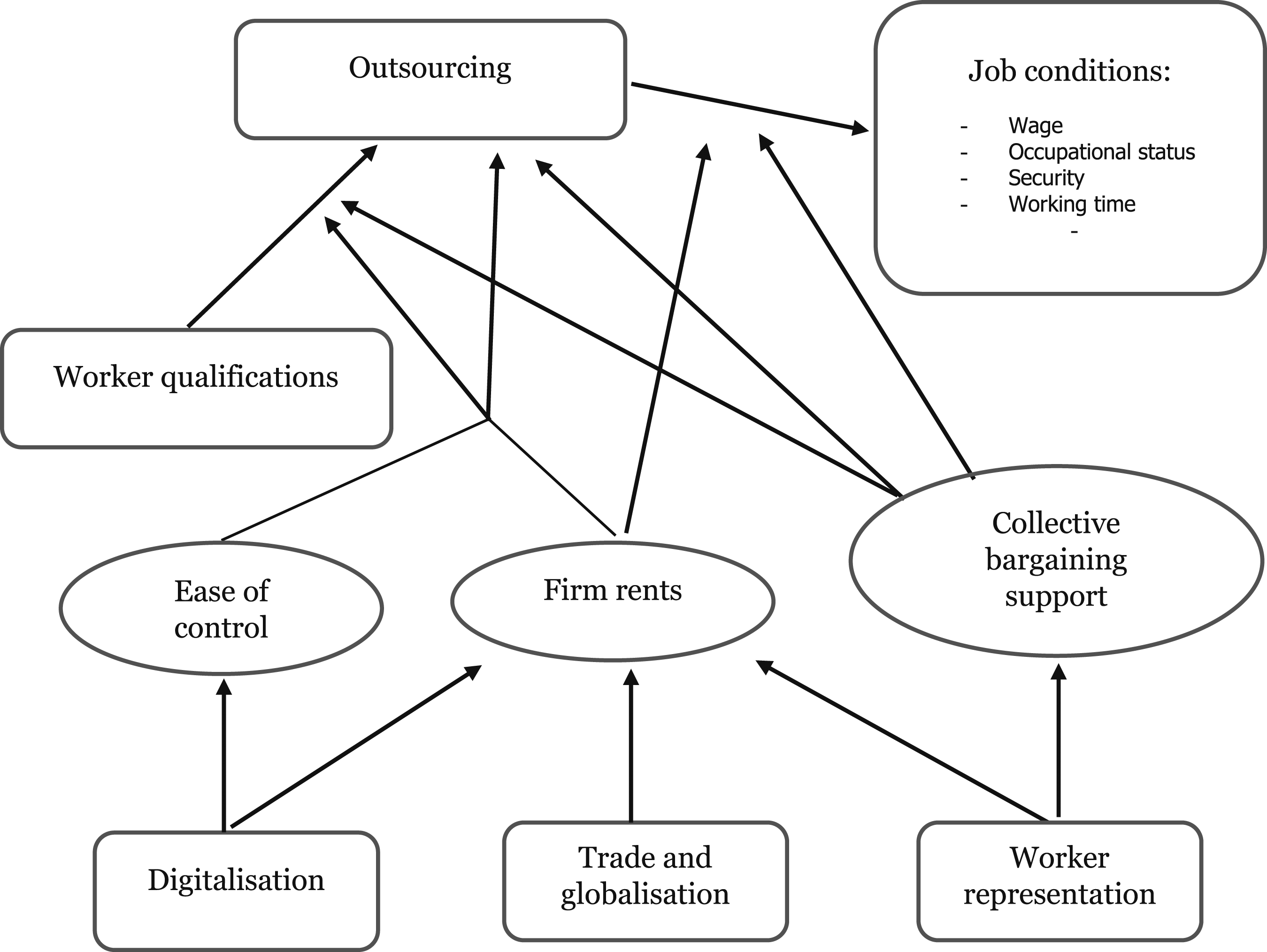

Figure 1 highlights the conceptual framework. The risk of being outsourced is expected to be increased by digitalisation – increasing firm rents and the ease of controlling outsourced workers – and greater trade and globalisation within a sector or country – affecting firm rents – while worker representation and stronger unions are expected to decrease the risk of outsourcing and its’ impact through supporting workers, especially the more vulnerable, through collective bargaining. As outsourcing is expected to impact lower-educated workers more, they would also be expected to be more affected by these conditional factors. Conceptual framework.

I assume that outsourcing work affects the conditions of work negatively – lower income and worse quality of jobs. I further expect that the negative association between being outsourced and job quality is stronger when the firm premia are generally expected to be larger in the sector, as when there are is more technological investment and greater trade and globalisation, while under stronger worker representation I expect the conditions of work to be more protected.

First, as the act of outsourcing entails decisions on which workers to retain in the firm and which are core, power relations and the bargaining position of different groups play an important role. Education is expected to be an especially important dimension as it relates to specific tasks performed and the impact of structural and economic factors, such as digitalisation and trade, differ by skills and education levels (Goos et al., 2014). I expect then that lower qualified workers are more at risk of being outsourced (H1).

Second, I expect that the risk of outsourcing, particularly for lower-educated workers, differs to some extent systematically with economic trends and institutional factors (H2). Specifically, I expect to see more domestic outsourcing in countries and sectors characterised by greater digitalisation – measured by investment in new technologies – and more open to global trade; while I expect less domestic outsourcing in countries and sectors characterised by more worker representation in the form of stronger collective bargaining and higher trade union density.

Third, I also expect variation in the impact of outsourcing on the quality of jobs – measured as wages, but also the risk of working on temporary contracts and on working on non-standard working times (H3). Specifically I would expect that (1) in countries and sectors where I expect greater rents to be shared as approximated by their digitalisation and globalisation the difference between those workers who are outsourced or work for a temporary employment agency compared to their peers is larger; and (2) that stronger collective bargaining and union density minimise the negative impact of outsourcing as better conditions are negotiated.

The key expectations are then that (1) outsourcing is particularly likely for more vulnerable workers in terms of education as they are more at risk of being excluded from better-paying firms, (2) such outsourcing is associated with generally lower job quality, and (3) this process is more likely for workers in cases where their bargaining power is relatively lower, where firm premia are relatively higher, and where it is easier to control workers, meaning the incentive to exclude workers from them is higher.

Data and methods

This paper makes use of cross-national data of European countries to describe trends in domestic outsourcing. The EU Labour Force Survey (LFS) holds representative yearly data and allows for an operationalisation of domestic outsourcing. Descriptive statistics of all key variables are shown in Table A1.

Contextual factors

The data is enriched with external data at country-industry-year level to capture macroeconomic and institutional factors. Industry is measured in 12 large sectors in the LFS. Trade and globalisation are expected to affect the risk of outsourcing by increasing firms’ rents and the incentive to limit rent sharing. The importance of trade in an industry is captured through trade openness – measured as imports plus exports over value added in an industry per country and year (Michaels et al., 2013). The data is available up to 2018.

Digitalisation is expected to affect the ease of outsourcing by making it easier to control workers, as well as increasing rents and increasing the incentive to limit the workforce. It is captured through the industry-specific investment in ICT equipment including software and databases, expressed as a share of non-residential gross fixed capital formation (Calvino et al., 2018; Kristal and Cohen 2017; Michaels et al., 2013). This measures the investment in new technologies which can then be used for production. Where possible, the data is obtained from national accounts data provided through the OECD but, where this is not available, data was obtained through the 2018 update of the 2017 EUKLEMS data. This data is generally available until 2017.

Worker representation is expected to provide support to workers and thereby limit their risk of outsourcing as well as limit the negative impact on wages. Union density is taken from the Database on Institutional Characteristics of Trade Unions, Wage Setting, State Intervention and Social Pacts (ICTWSS version 6.1) by country, sector (12 large groups), and year (Visser, 2019), available up to 2018. Collective bargaining coverage is obtained at the same sectoral groups from the Structure of Earnings Survey from 2002 to 2018, intrapolating trends between those years and extrapolating to additional years. Within the European context where agreements are often extended beyond the individual firms or union members the coverage rate is an important indicator of the strength of these agreements (Zwysen and Drahokoupil, 2022).

Outsourcing and job quality

The EU Labour Force Survey (LFS) is a European micro-dataset carried out quarterly with information on the labour market situation of a representative sample of the EU population. This paper uses data from 2001 to 2020 to study the trends in proxies for outsourcing and their impact on job quality for EU Member States plus Norway and the UK. 1

Ideally, outsourcing events are measured using longitudinal linked employer–employee data as this allows the registration of when a large group of employees is shifted from one legal employer to another while remaining at work on the premises of the original employer (Bertheau et al., 2020; Goldschmidt and Schmieder 2017). Unfortunately, such data is not available cross-nationally. I proxy the rise in domestic outsourcing through the share of workers who are employed in the sector providing business services (K in NACEr1 and N in NACEr2). This captures an indication of the importance of business services being outsourced to other businesses, but it is a crude measure as I use large sectors here, and will capture workers who are not outsourced as well as miss some outsourced workers. It is in line with earlier work by the OECD (2021) using more detailed sectors. To minimise the issue of misclassification I make use of the moves from another sector to the business services sector, rather than simply comparing people in the business services sector to others. As a second approximation of outsourcing (Drenik et al., 2023), I make use of the share of workers who are employed through a temporary employment office, which is a measure available from 2006 onwards. Temporary employment agencies are interesting as they also constitute a rather heavily regulated set of workers across many of the countries studied here (OECD 2021). Both measures capture the risk of outsourcing for workers and are introduced separately. While this paper does not capture outsourcing events directly, it aims to capture the extent to which workplaces rely on other businesses to carry out work rather than doing it internally.

Table A1 in the appendix shows, across our sample, the average characteristics in terms of work and background of workers who work in the business services sector or who work for temporary employment agencies compared to the average. They have generally lower earnings, lower occupational status, and are more likely to work on involuntary temporary contracts. In the temporary employment agencies they also work more on unsociable hours. Those in the business services sector work somewhat fewer hours, but work in similarly sized firms. They are lower qualified on average and the group has more women on average as well as being of a similar age. Workers for temporary employment agencies generally work in larger companies, are lower qualified, and more likely to be young and male. Table A2 in the appendix also shows the risks of moving to the business services sector and working on temporary employment agency work by industry. This shows temporary employment agency work is used most in manufacturing, real estate and business, and construction. The risk of moving from one sector to the business services sector is highest in other services, accommodation and food, finance, and insurance.

I test whether contextual drivers – globalisation, digitalisation and worker representation – are shaping this process. Using the LFS I merge contextual data by year, 1-digit industry and country, and analyse the probability of moving to the business services sector from t−1 to t, or of working in a temporary employment agency (outsourced), controlling for other socio-demographic characteristics X (gender, age, gender by age, cohabiting status, whether a dependent child lives in the household, and level of qualifications) to isolate the contribution of one’s own qualifications as opposed to other factors on which people may sort, and to account for family constraints. I also include controls for the hours worked at time t as a relevant control in terms of intensity of work and for the quality of jobs. When comparing the issue of job quality and the probability of working on a temporary employment agency, I further include a control for firm size (<10, 10–50, 50+). I do not include firm size in the models on the propensity to move to the business sector as it could be an outcome of the outsourcing process. I further include fixed effects for country (

Besides describing the risk of outsourcing, this paper also addresses the association between outsourcing and job quality. Job quality is a complex and multi-dimensional concept which captures dimensions going beyond remuneration, including job security, work-life balance, the conditions of work, development opportunities, and interest representation (Piasna, 2023). This paper does not address all aspects, but aims to, besides income and status of the job, also capture the issue of contractual security and the timing of work to capture aspects of work-life balance. Income is captured through deciles (available from 2009) and occupational status (ISEI), recoded from 3-digit ISCO codes (Ganzeboom and Treiman 1996). I capture the security of the contract through a dummy variable for being on a temporary contract because no indefinite contract was available; while work-life balance is addressed through a dummy variable indicating having at least two types of non-standard work in the regular job (working evenings, nights, Saturdays or Sundays, or working in shifts). The income and status are important as these are expected to decline directly in response to exclusion from the better-paying company. Similarly, the more competitive environment of workers that are outsourced or work as contract agents would be expected to lead to less secure contractual arrangements. Working on non-standard times then captures one dimension in which the outsourced worker may be excluded from protections regarding working time.

Each job quality outcome is linearly regressed on indicators of qualifications, a dummy variable proxying outsourcing, and the interaction between qualifications and outsourcing for individuals i in occupation o, industry j, country c at time t, controlling for individual characteristics X (gender, age, gender by age, cohabiting status, whether a dependent child lives in the household in order to capture family constraints, and hours worked an firm size in groups), and country by year fixed effects. The job quality of workers who move from any sector into business services is analysed first. By including fixed effects for the combination of country, occupation, and industry at t−1, I compare those who had moved to a sector providing services to other businesses with those who had stayed in the same sector.

Second, the job quality of workers who work for a temporary employment agency is compared to that of those who do not but who work in the same industry, occupation, and country at time t.

To address the third hypothesis, I include interactions between outsourcing and contextual factors in equations (2) and (3) analysing the impact of outsourcing above. These analyses indicate whether union density and collective bargaining coverage affect the impact of outsourcing. This is done through a separate analysis per contextual factor.

Findings

Outsourcing on the rise

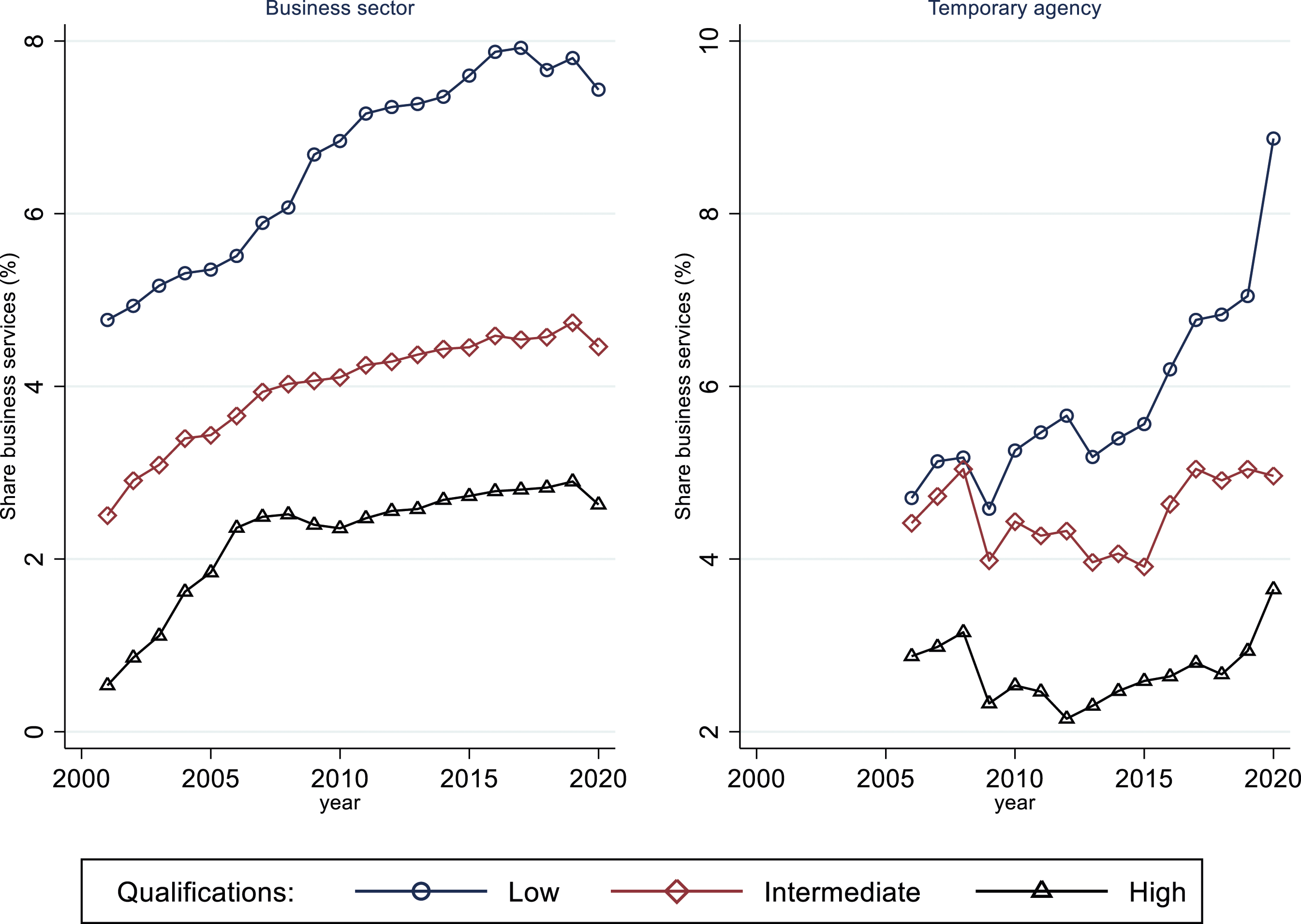

Figure 2 shows that across the EU there has been a clear upward trend in the share of workers working in the business services sector (left panel), as well as an upward trajectory in the share of workers on temporary employment agency work. While the rates of working in the business services sector are highest for lower qualified workers, with around 4.5% working in the business services sector compared to 2.5% of those with tertiary qualifications, for both groups there has been a sizeable rise over time. Second, the share of workers in temporary employment agency jobs has increased over time particularly for the lower qualified. Temporary employment agency jobs increased overall until 2008, although they did decline sharply from 2008 to 2009. Since then, their use more or less stagnated up to 2015, particularly for intermediate and higher qualified workers. Between 2010 and 2017, however, there was a sharp increase among those with lower and intermediate levels of qualification and then a rapid increase by 2020 for the lower qualified of up to 9% and for the higher qualified to close to 4%. Trends in outsourcing as proxied through business services sector workers and temporary agency staff. Source: LFS 2001–2020, EU27 + NO, UK. Note: Estimated average from EU LFS for EU countries, weighted. Series adjusted for break in 2007 with industry switch from NACE1 to NACE2.

This rise in the incidence of workers – particularly lower-educated – performing services for other businesses can be one possible reason for rising homogeneity at the workplace (Handwerker, 2023). Employment agencies and business service providers likely operate in a more competitive environment and contend with each other on conditions and price, resulting in relatively worse working conditions for the outsourced workers (Goldschmidt and Schmieder 2017; OECD 2021). It also indicates that firms increasingly guard off certain tasks from being done by their own employees and rather buy these services.

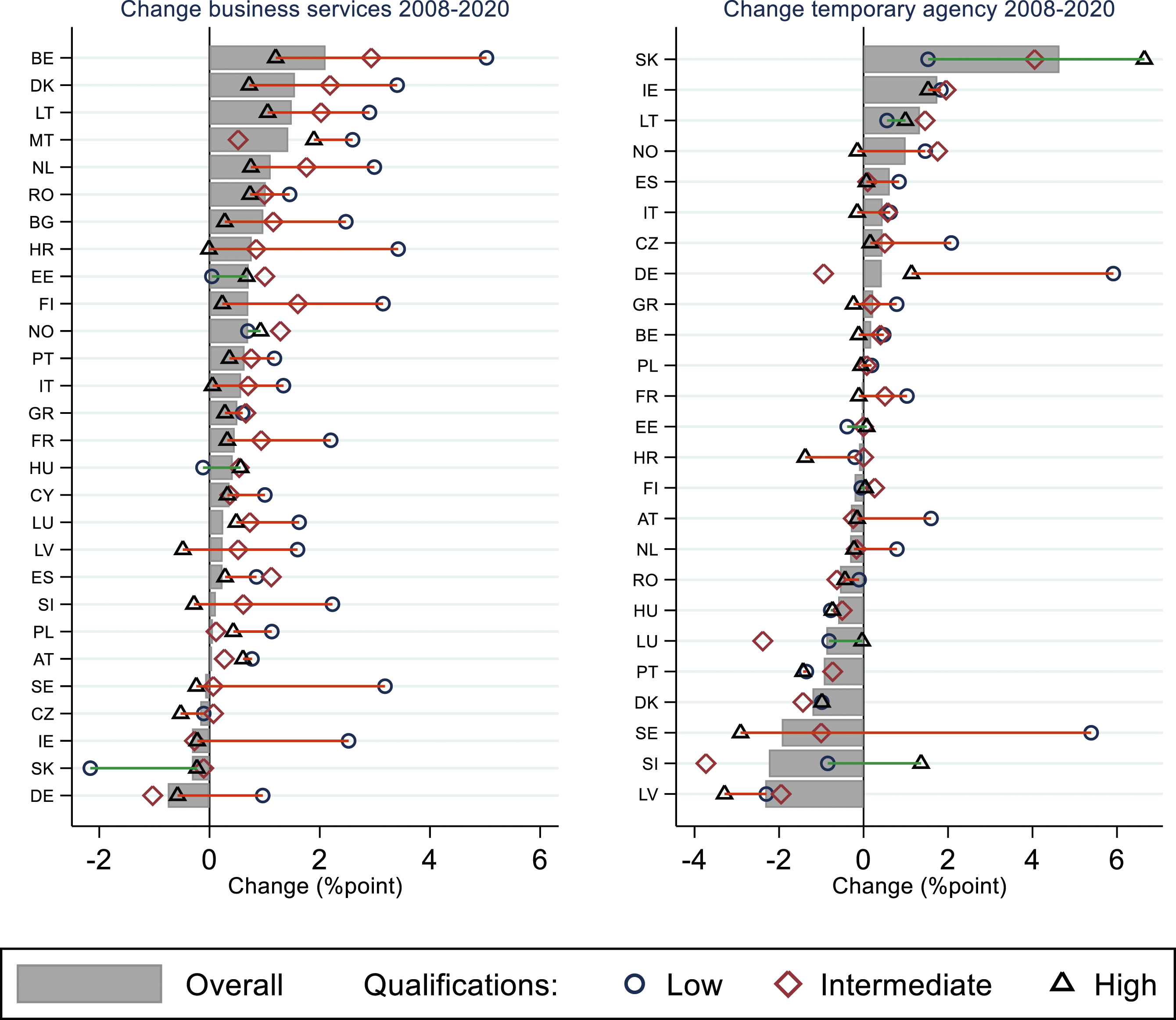

Figure 3 breaks the change from 2008 to 2020 – where consistent industry codes are used – in the risk of outsourcing down per country. This shows first of all that the risk of moving to the business services sector increased all countries barring Sweden, Czechia, Ireland, Slovakia, and Germany. In all but three countries (Hungary, Estonia, and Slovakia), the change was higher for lower-educated workers than for the other groups. For temporary agency employment, there is more variety in the trends, although again it is generally increasing more or decreasing less for the lower-educated. Change in business services and temporary agency work from 2008 to 2020. Note: estimated change from 2008 to 2020 by country, from 2008 to 2020, source LFS.

What is driving segregation and outsourcing?

What then is driving these patterns of segregation and possible domestic outsourcing; and is this a pervasive and common trend?

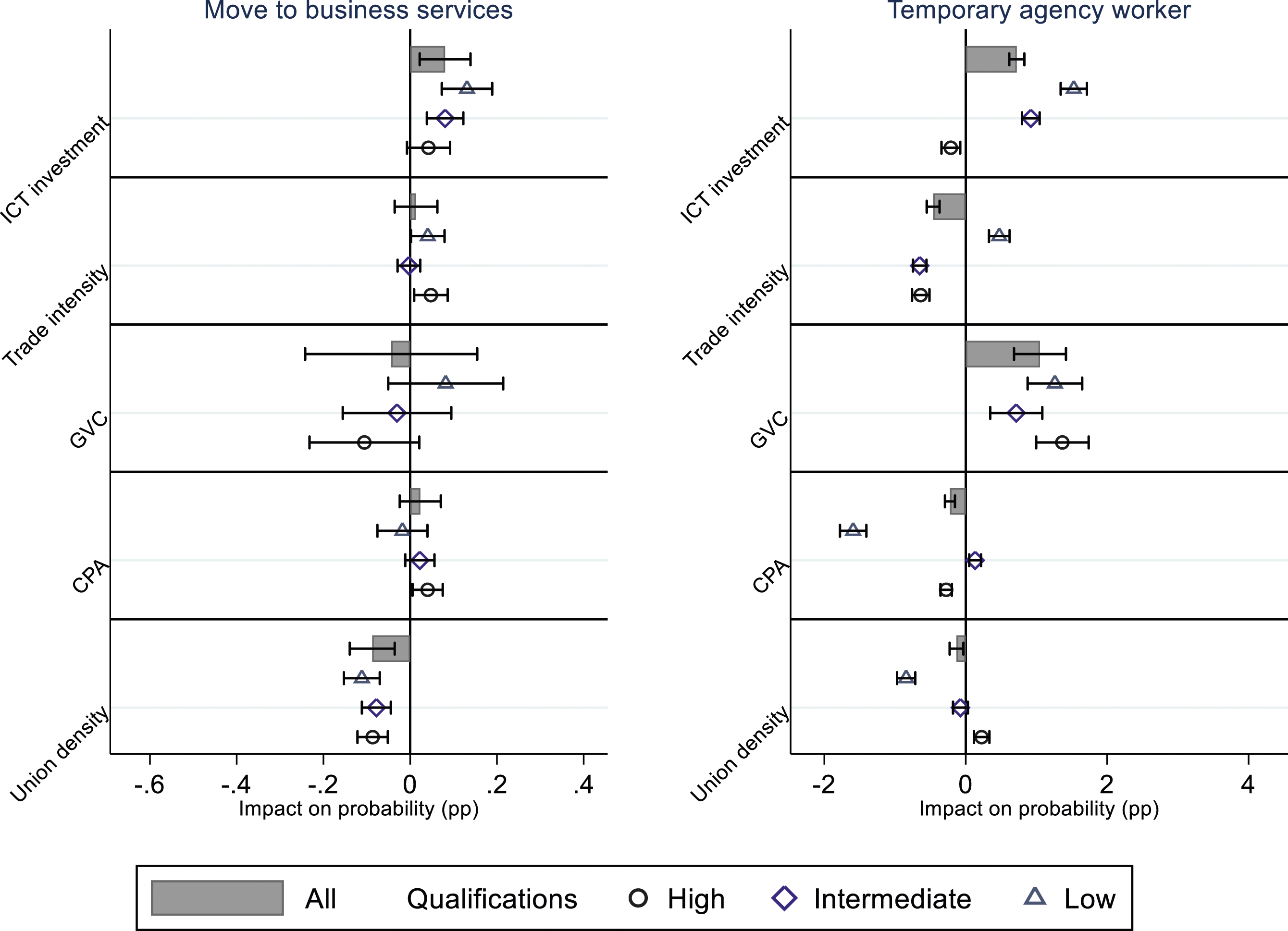

Figure 4 shows the relationship between the contextual factors and the probability of moving from a different sector to business services – as a proxy for outsourcing – or the probability of being a temporary agency worker. Coefficients of the main model estimating the probability of outsourcing are shown in Table A3 in the appendix. In sectors with greater ICT capital investment, the probability of lower-skilled and intermediate workers being employed on a temporary agency contract, or of them moving to the business services sector, is higher. The impact of globalisation is somewhat more mixed, but it actually does provide some support for an increase in the risk of outsourcing, particularly for lower-educated workers. On the one hand, a greater involvement in international trade is associated with greater risks of moving to the business services sector for low and high educated workers – which can of course also be an indication of outsourcing – while also being associated with a greater risk of working for a temporary employment agency for lower-educated workers. A higher involvement in global value chains is also associated with much more temporary employment agency work. On the other hand, global value chains have limited impact on the probability of moving to business services sector, and trade intensity actually reduces the risk of temporary employment agency work overall. Macroeconomic and institutional factors driving possible outsourcing, with 95% CI. Source: LFS 2001–2020. Note: Estimated average from EU LFS, weighted, showing the estimated change in contextual factors (10th to 90th percentile) on the share of workers moving from a sector [t−1] to the business services sector, or being employed in temporary agency work, with a 95% CI. Estimated from a regression of the contextual factors, controlling for gender, age, qualification, part-time and temporary contract work, with fixed effects for country, sector, year and occupation, and standard errors clustered at country-sector-year.

While these macroeconomic trends seem to be driving a greater risk of outsourcing, there is some indication of support offered by collective bargaining and stronger trade unions, which can support workers’ limited bargaining power. First, in countries and sectors with a higher share of workers covered by collective pay agreements, the use of temporary employment agency work is substantially lower, as is that of university-qualified workers but to a lesser extent. It does not have the same protective effect on the risk of moving to the business services sector however. Second, in countries and sectors with stronger trade unions, the risk of being outsourced – measured as moving to the business services sector or working for temporary employment agencies – is statistically significantly (p < .05) lower, which seems more driven by lower rather than higher qualified workers.

These results indicate quite starkly that the risk of outsourcing is more widespread in more digitalising or more globalised countries and sectors, while worker representation is associated with less of such outsourcing of services to other businesses. Through using country-industry specific fixed effects, any time-invariant factors that would affect this relation within a country-industry are modelled out. Of course, factors that are unobserved but do change over time, such as management practices, for instance, can still bias the association. Importantly then, these trends towards greater segregation and domestic outsourcing do not seem to be universal. It is entirely in line with earlier findings that greater inequality between firms – helped along by segregation and the sorting of higher-paid workers into high-paying firms – is shaped by institutional differences; and that declining worker representation is one particular driver allowing for greater differentiation between firms (Tomaskovic-Devey et al., 2020; Zwysen 2022b).

Relationship between outsourcing and job quality

Then, the question is whether such possible outsourcing is affecting the labour market outcomes of workers as well. Segregation itself would not necessarily be a problem, although there is value in meeting people with different skills and characteristics at work, but if this is also associated with worse labour conditions, it can point to widening inequalities over time.

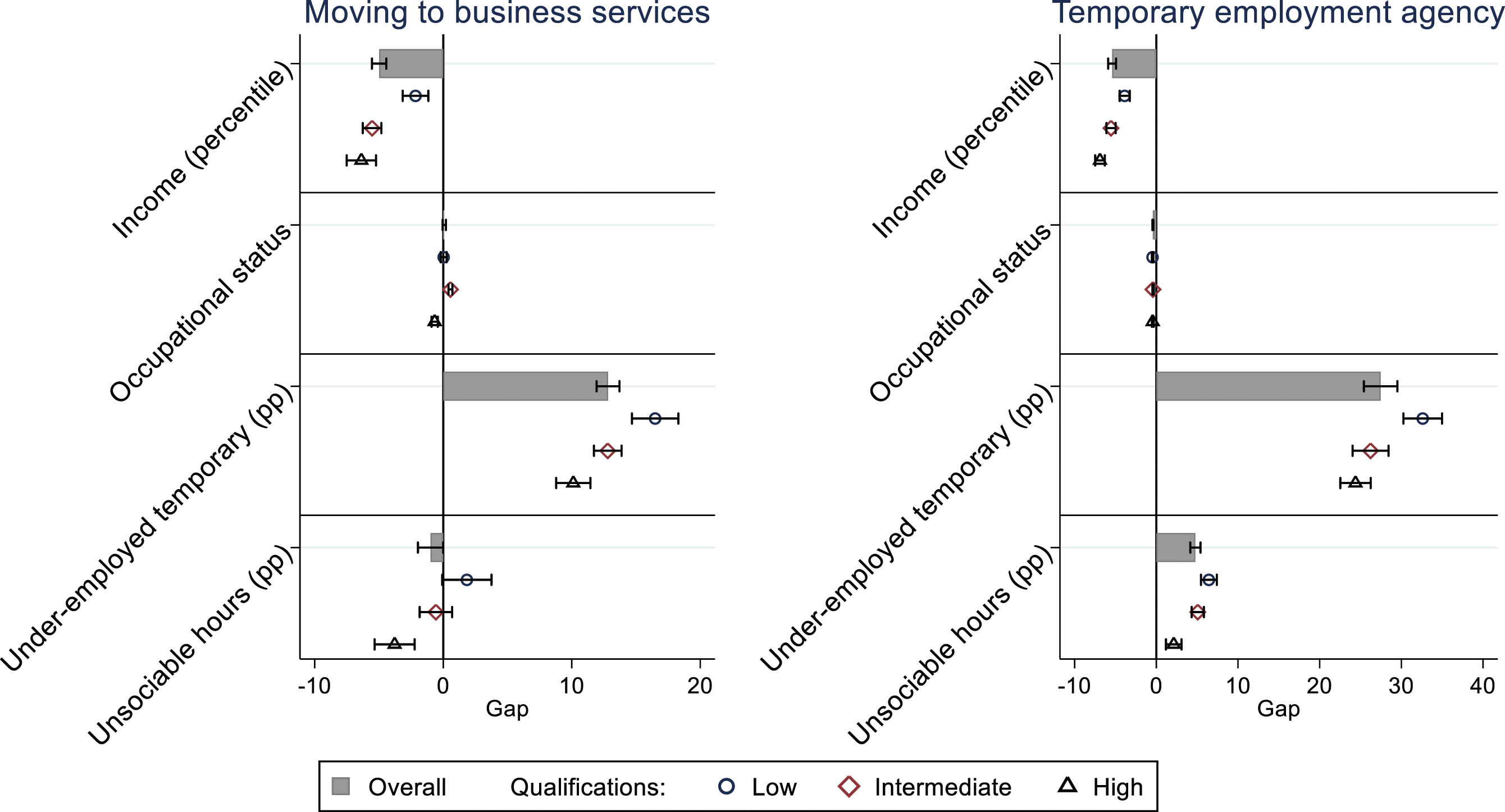

The left panel of Figure 5 compares workers who have recently moved from somewhere else to the business services sector with comparable workers who worked in the same sector the year before but had not moved to business services. Moving to the business services sector – which carries a risk of having been outsourced – is associated with having earnings around half a decile less than those who worked in the same sector last year with similar characteristics, but who had not moved. The gap is somewhat higher for the more highly qualified, which is likely to reflect the greater variation in pay scales for those groups. While moving to the business service is associated with a slight increase in occupational status, the effect is very small – given I control for large occupational groups. Moving to the business services sector is associated with a 10% point higher risk of working on an involuntary temporary contract, especially for lower-educated workers. There is little difference in whether workers work on standard hours, but the lower-educated who move to the business services sector do see this risk increase slightly, while higher-qualified workers are less likely to work on these non-standard times. Overall then, workers who recently moved to the business services sector work for lower pay and are more likely to be under-employed than their colleagues who worked similar jobs but did not move. This is generally in line with higher insecurity and lower incomes resulting from outsourcing. There is also an indication that in terms of contractual arrangements at least the lower qualified workers are most at risk. Estimated impact of moving to the business services sector, or working in a temporary employment agency, 95% CI. Note: Coefficients with 95% C.I. estimated from regression controlling for country*year and country*industry*occupation fixed effects as well controls for gender, age, gender by age, dependent child, cohabiting, hours worked per week, and firm size. Source: LFS 2001–2020.

The right panel proxies outsourcing by working for a temporary employment agency. Findings are generally comparable, in that incomes are lower for temporary employment agency workers compared to their peers in similar jobs in the same occupational group and industry who work in a more standard arrangement, and the income effects are larger for the highly qualified. There is also a much higher association with the risk of working on an involuntary temporary contract, especially for lower qualified workers. Workers for a temporary employment agency also have a higher risk of working on non-standard working times making it more difficult to combine work with personal life.

These analyses clearly show that workers who are at risk of being outsourced work under worse conditions than those who work under more traditional conditions. This is in line with the literature showing negative impacts of outsourcing on wages. Crucially as well, such outsourcing exacerbates the weak labour market position of lower-educated workers. As this risk increases over time, it can contribute to worse labour market positions for the lower-educated and to greater inequality and polarisation overall. Coefficients of these models are shown in Tables A4 and A5 in the online appendix.

How does the impact differ?

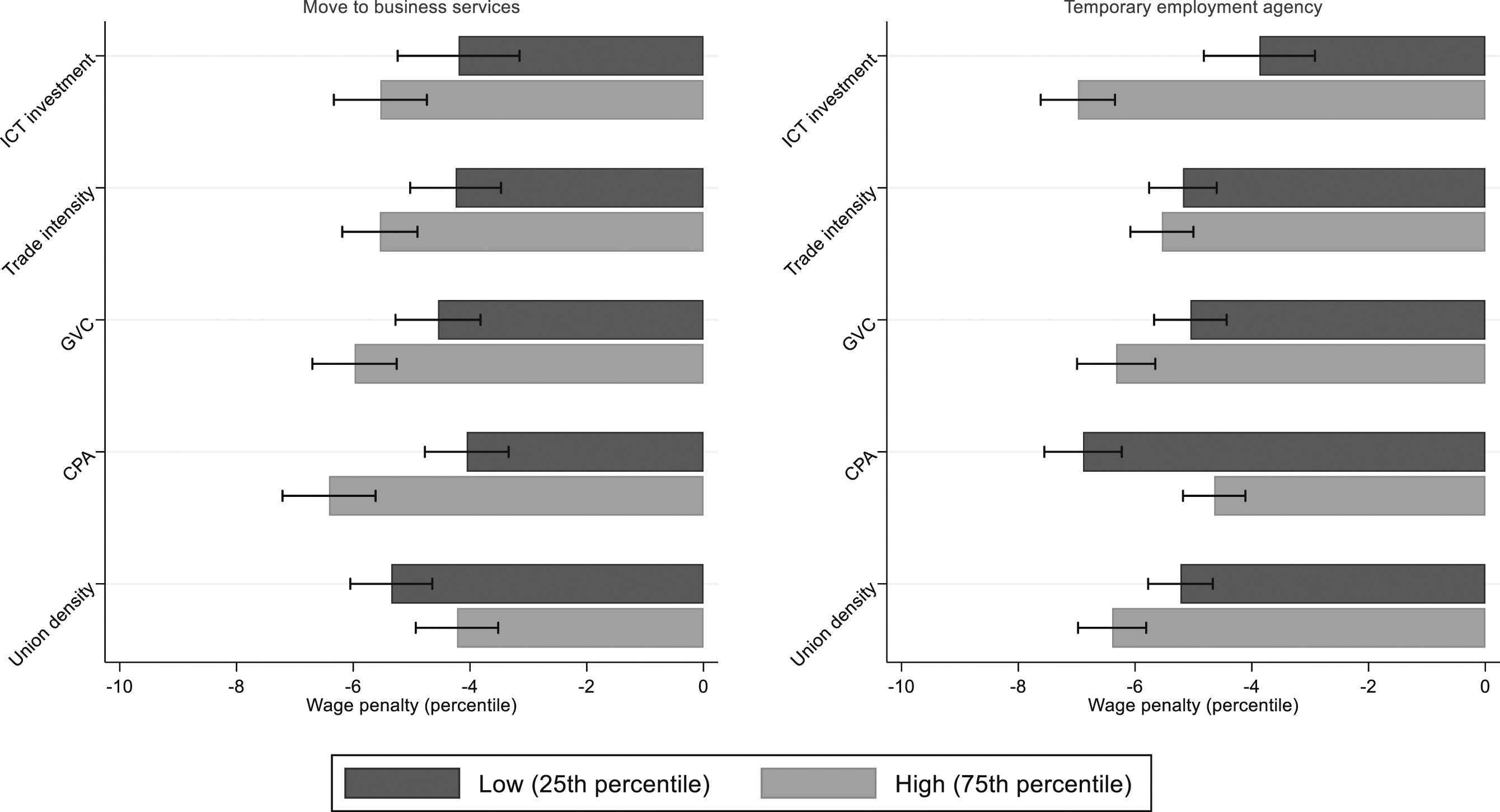

Finally, I consider the extent to which penalties for being outsourced differ by the characteristics of the country and sector. For ease of presentation, I only show results for earnings in Figure 6. Coefficients are shown in Table A6 in the appendix. Overall, I find that the average earnings penalty for moving to the business services sector or working for a temporary employment agency are substantially worse when working (originally) in a sector with a higher share of ICT investment or more involved in global trade. This could indicate that domestic outsourcing is especially problematic in those countries and sectors where profit margins are higher as workers lose out from rent sharing, which is in line with the loss of firm rents as a major cost. I also find that the penalties are somewhat smaller, although the effect is limited, for workers moving to the business services sector in those sectors with higher trade union density which could indicate that a stronger trade union limits the extent to which outsourced or interim workers can work under worse conditions. On the other hand, there is a limited worse outcome for temporary employment agency workers in sectors with higher union density, which can indicate a stronger insider-outsider divide in those sectors. Collective pay agreement coverage has the reverse association, in that workers in a sector with higher coverage by collective agreements actually lose out more when moving to the business services sector. This could indicate precisely that those workers lose out from the benefits obtained through the collective agreement, which is generally also associated with higher wages (Zwysen and Drahokoupil, 2022). For workers in a temporary employment agency, there is a very clear benefit to working in a sector where more workers are covered by collective agreements as the wage gap with their colleagues on more standard arrangements is much lower. This section then finds some support for the hypotheses in that the cost of outsourcing is not equal across contexts, and it is generally worse in countries and sectors more involved in global trade relations and with higher digitalisation, while collective representation has a more mixed relation, but can help reduce the disadvantage. Wage penalty for domestic outsourcing by context. Source: LFS 2009–2020. Note: The figure shows the estimated impact and 95% CI. of moving to business services (left) or working for a temporary agency (right) when the contextual factor changes from the 25th to the 75th percentile, controlling for education, couple, dependent child, age by gender, working hours and firm size group, and fixed effects for country by year, and country by occupation (1 digit) by industry (previous – business sector; or current – temporary).

Discussion and conclusion

This paper describes how workers – especially with lower or middling qualifications – are increasingly at risk of not working directly for a company, but rather of providing services through another company or a temporary employment agency. This means they are providing services and working on the premises of an employer that is not their own.

This matters as such domestic outsourcing is associated with relatively lower wages and worse working conditions – less secure contracts and more non-standard working times. Such findings are in line with a loss of firm premia from being excluded from the better-paying positions, but demonstrate that other job quality aspects are also negatively affected (Card et al., 2017; Goldschmidt and Schmieder, 2017; OECD, 2021). The overall effect would then be a greater inequality between workers who are excluded from internal markets of better-paying firms and the vulnerable, outsourced, or temporary workforce (Bilal & L’Huillier, 2021; Drenik et al., 2023; Goldschmidt and Schmieder, 2017; Handwerker, 2023).

Crucially, this paper uses the variation between countries, sectors and over time to show that this process is not universal. Such outsourcing and segregation by qualification level is more present in sectors that use more digital technologies and that are more open and involved in global value chains. These wider trends that all countries face help firms on the one hand to outsource tasks more easily while still using digital technologies to control workers and, on the other, to increase the incentives to do so and to focus on their core tasks. However, more outsourcing and polarisation is not a foregone conclusion; this occurs less in countries and sectors characterised by stronger trade unions.

Importantly, the cost of this outsourcing in terms of wage loss also depends on the context shaping these decisions. Where outsourcing seems more likely, the cost for those workers also tends to be higher. This finding is in line with outsourcing being more beneficial for employers who have higher rents from which they want to exclude non-core workers, and who have better opportunities for controlling the outsourced workforce. When being outsourced, workers then miss out on these higher rents (Goldschmidt and Schmieder, 2017; OECD, 2021). Stronger unions however do have an impact on limiting outsourcing, indicating they may make it more costly to outsource and protect workers more generally. While results are more mixed, there also seems to be a moderating effect of stronger unions on the wage loss related to outsourcing while collective agreements help support temporary employment agency workers, which could indicate better conditions and are obtained when workers’ bargaining power is supported by collective actors. As technological innovation and globalisation increase over time and union density is generally declining, this is possibly related to the overall growth in outsourcing.

While suggestive, there are certain limitations to this study. First, this paper does not identify outsourcing events directly and rather approximates it by studying the use of temporary employment agencies and the growth of the industrial sector providing services to other businesses. This will miss certain types of outsourced labour, and importantly also include some workers that are not outsourced. Second, through design, this paper does not consider the issue of international outsourcing or offshoring. This is because this paper focuses on how the division of tasks within firms within a country or sector affects the workers and inequality within that country. Third, this paper lacks a firm perspective, as the analyses do indicate that for instance technological innovation at the sectoral level affects the use of business services or temporary employment agencies, but this is only considered in the aggregate and not at the level of the individual firm which may or may not outsource when investing in new technologies. For this reason, more research using detailed firm level data is needed. Fourth, the end period of this paper coincides with the start of the COVID-19 pandemic in 2020 which obviously had a dramatic impact on work, with a large increase in remote working (Zwysen, 2023).

Differences between firms in their pay setting arrangements and who they hire are the driving force behind much of the growth in inequality in wealthy countries (Criscuolo et al., 2020; Lazear and Shaw 2009; Tomaskovic-Devey and Avent-Holt 2019; Zwysen 2022b). This means that it is all the more important to study these differences in the workforce overtime and the processes behind segregation and growing inequality. Across Europe, there has been a rise in outsourcing, as one pathway restricting more vulnerable workers from the better positions. This is not inevitable though as the variation between sectors and countries over time shows.

In conclusion then, strengthening the institutional factors protecting workers across Europe can also serve to limit the greater precariousness and the race to the bottom that greater outsourcing and segregation implies for lower qualified workers – already vulnerable and facing worse conditions – when pushed away from the better and more protected firms.

Supplemental Material

Supplemental Material - Working apart: Domestic outsourcing in Europe

Supplemental Material for Working apart: Domestic outsourcing in Europe by Wouter Zwysen in European Journal of Industrial Relations

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Note

Author biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.