Abstract

Modern welfare states compete with private providers of welfare in offering economic security. This is most evident in the case of pensions competing with life insurance and private pensions as well as of public health insurance competing with private insurance providers. The common view of this public–private relationship is one of a trade-off: longitudinally, political scientists describe how retrenchment was pushed by privatized welfare, whereas economists trace the crowding-out of private to public welfare provisions. Cross-sectionally, they claim that countries have lower public spending levels because they have a large private sector. We suggest a more nuanced view. Drawing on a new long-run panel data of public pension and private life insurance expenditures and contributions in 20 OECD countries since Bismarck to the current day, we show that in the postwar years a cross-sectional trade-off emerged, which then faded. Longitudinally, complementary relationships of public and private provision growth have become the norm. We argue theoretically and show empirically that trade-offs only occur if governments still hold (waning) anti-interventionist and pro-market views.

Introduction

The past 130 years have seen a global diffusion of social security systems (Hu and Manning, 2010; Schmitt et al., 2015), yet the pre-existence and parallel growth of private alternatives such as insurance institutions have largely gone unnoticed with a few exceptions (Andersson and Eriksson, 2015; Horn and Kevins, 2018; Pearson, 2020; Röper, 2021). This also holds true for comparative welfare state research in which – post-Pierson’s seminal work on retrenchment – privatization is often conceived of in terms of state retreat or insufficient public spending (Jensen et al., 2019; Starke, 2006). In 2015, OECD countries spent on average 9.7% of their GDP on basic public pension, leaving the remaining 2.3% to private–public arrangements. In the same year, life insurers – one dominant provider of private pension products – collected almost 5% of GDP in annual premium income, whereas total non-life premiums reached 4% (OECD Insurance Database). Life insurance penetrates entire populations, much as pension systems. In the same year, public health insurance, in turn, spent 5.8% of GDP, whereas private health expenditures (private insurance or out of pocket) amounted to 2.4% (OECD SOCX). In short, in the shadow of well-researched public security systems, private welfare institutions have been left under-researched, even though life insurance spending surpassed that of public pension before the Second World War and in recent decades has been reaching a considerable size.

Modern welfare states complement, but also compete with the private insurance and private pension sector in providing economic security. The competition is most evident in the case of pensions competing with private life insurance and of public health insurance competing with private insurance providers, but depending on the country, it extends to other domains of economic security such as flood, accident or reinsurance. The common view of this public–private relationship is one of a trade-off or zero-sum game: longitudinally, political scientists often describe how welfare retrenchment was pushed by new forms of privatized welfare (Gingrich, 2011; Orenstein, 2008), whereas economists rather trace the crowding-out of private to public welfare provision (Andersson and Eriksson, 2015; Kangas and Palme, 1996; Kantor and Fishback 1996). Both views implicitly hold a trade-off view, but argue for different underlying mechanisms. Cross-sectionally, countries like the United States are seen to have lower public spending levels than Scandinavian countries because they have a large private sector. In this article, we suggest a more nuanced view: drawing on a unique collection of life insurance premiums and benefits as well as first-pillar public pension expenditure and contributions in 20 old-industrial countries 1 starting with the beginnings of public and private insurance in the late nineteenth century up to the current day, we show that in the postwar years a cross-sectional trade-off emerged for old age and health, which then faded in more recent decades. Longitudinally, complementary relationships of public and private provision growth have been the norm.

Rather than explaining outcomes in terms of insurance lobbying or micro preferences, we make a case for party ideology as an important factor to consider: we find that the fading of the post-war trade-off must be understood in light of ideological moderation and the changing ideological composition of cabinets. Since the 1980s, when beliefs in neoclassical economics and free market allocation peaked among OECD governments, centre-right parties have become more susceptible to welfare state intervention and less orthodox about market allocation. In addition, on the other side of the political spectrum, the old left that favoured ‘politics against markets’ (Esping-Andersen, 1985; Hamilton, 1989) to crowd out the market has been replaced by a pragmatic ‘Third Way’ Left that embraces market incentives (Green-Pedersen and Van Kersbergen, 2002) and ties social rights to a ‘rhetoric of responsibility’ (Sandel, 2020). While these two developments do not mark an end to ideology, they indicate that beliefs in a sharp private–public dualism, though still relevant for some parties, have lost some of their appeal. We argue that the public–private link is no longer significantly negative where pragmatism prevailed over a strong belief in market ideology.

The article is organized as follows: in the literature section, we report on the different claims made about the relationship of the public and private insurance position and on the mechanisms supposedly driving trade-off relationships. We then introduce our new dataset on long-run private and public old age and health expenditure and describe the overall long-run cross-sectional and longitudinal relationships. Our descriptive findings challenge easy zero-sum game or trade-off interpretations regarding the linkages between public and private welfare provision. In an attempt to shed light on the developments that contribute to less pronounced and less uniform trade-offs, we then highlight the role of changing cabinet ideologies (controlling for the size of public programmes and demographic and economic drivers of demand for welfare provision). We conclude by arguing that ‘politics matter’ studies (for an overview see Horn, 2017; Bandau and Ahrens, 2020) in comparative welfare research, with their focus on public programmes, should be complemented with analyses of the links between private welfare and public programmes and their ideological underpinnings. As long as ‘private welfare is a relatively under-researched topic’ (Gugushwvili and Laenen, 2021: 120), it is all the more vital to acknowledge that private insurance and risk privatization is much more than the absence of public provision or a near-synonym for state retreat.

Public–private welfare trade-off: An overview

Existing literature on the public–private trade-off can be grouped into two strands. The first is about why one would or would not expect the existence of a trade-off between public and private modes of welfare provision. The second is about potential mechanisms explaining how the one influences the other. The potential trade-off presupposes that private and public services exist in a similar domain and the perhaps most prominent domains are health, pensions, but also industries with market concentration (gas, water, electricity). We focus on welfare provision regarding health and pensions which are the most costly welfare pillars making up about 2/3 of government social expenditure, excluding education (Hacker, 2002: 62).

Public and private modes of (welfare) provision can either positively or negatively influence each other or be unrelated. The most widespread view is one of a public–private negative trade-off whose causal arrow can run in both directions. Economists tend to describe it as a crowding out of private by public welfare (Andersson and Eriksson, 2015), whereas political scientists tend to describe the reverse process as one of privatizing or liberalizing public services by means of private alternatives (Ebbinghaus and Gronwald, 2011; Orenstein, 2008). This latter description has gained momentum ever since the start of welfare state retrenchment in the 1970s and has been complemented more recently by the ‘financialization’ view which sees financial services as new providers of welfare (Gerba and Schelkle, 2013). The influence can generally be contemporaneous or with a time-lag, as when the prior existence of one pre-empts the rise or growth of the other (De Swaan, 1988). The bottom-line of these trade-off views is that private and public services compete for the same demand. Given a fixed demand, a zero-sum logic forces one to exist at the cost of the other.

This general view is opposed by the null-hypothesis that posits that there is no relationship between public and private provision in a given domain. Particularly the works emphasizing the complex worlds of ‘social welfare mixes’ (Sachße, 1996) highlight the division of labour and the complicated web of private–public services making up welfare provision which prevent the emergence of any systematic relationship. The zero-sum logic is suspended by a segmentation of welfare services or a layering of welfare addressees, where each segment or layer follows its own logic. Bismarck’s early old-age insurance served the uninsurable workers and life insurers catered to the demand of the (upper) middle classes. Public and private, in this view often invoked by historians (Pearson, 2020), are independent of each other.

The third possible view on the trade-off posits a positive association, that is, a complementarity or an embarrassment of riches. In this view, the zero-sum logic is not just disarmed, the one even contributes to the other’s growth and perhaps even mutually so, as found in the case of US pension politics (Dobbin and Boychuk, 1996). The history of insurance offers two potential arguments for this view. First, social security has historically created a general awareness of insurance and thus raised the expectations of what to expect in case of accidents (Eggenkämper et al., 2015: 15). Through this free marketing for the insurance idea and an inflation of expectations, it increased overall insurance demand and thus suspended the zero-sum logic. A second argument is about layering: welfare institutions, particularly in the Beveridge model, were restricted to a minimum provision, even with below-average growth rates, leaving a potentially growing segment of supplementary provision to the private sector (Klein, 2010).

The second strand of literature concerns political mechanisms that explain how changes in private provision end up changing public provisions. One such mechanism consists in the lobbying of the powerful private insurance sector. There is ample historical evidence, particularly from the United States (Hacker, 2002; Klein, 2010), Canada (Bryden, 1974), Switzerland (Leimgruber, 2008) or the UK (Gilbert, 1965), which suggests that private life and health insurers were more or less successful in restricting public provision to more basic levels, so as to allow a supplementary private provision or to leave upper-income groups as a private market segment. More recent studies have made use of the different insurance regulations across US states and found that a professional insurance background of policymakers is likely to lead to a political agenda more favourable for insurance schemes (Hansen et al., 2018). More generally, a higher economic share of an industry in US states, including the finance and insurance industry, has been shown to lead to a higher connection to legislators (Battista, 2013), who usually have active careers outside of legislative bodies and their occupation in turn helps to predict their appointment to the respective legislative committees (Battista, 2012). Finally, the post-1970 privatization of welfare institutions has been attributed to the rise of the financial service industry which actively lobbied for push-backs of public welfare provision (Naczyk and Palier, 2014; Kemmerling and Neugart, 2009; Röper, 2020). However, there are major data limitations for studying these mechanisms outside of the special subnational context of the US states.

A second mechanism concerns the potential embourgeoisement effects of holding a private insurance on voting for parties which in turn support public-insurance cut-backs. This mechanism has mainly been studied in the larger literature investigating policy-feedback effects of privatization policies (Zhu and Lipsmeyer, 2015) and has produced rather mixed results. This effect has been found to be strongest for the middle and upper classes’ support for a comprehensive welfare system (Busemeyer and Iversen, 2020). A major limitation of all of these micro studies cited is their cross-sectional nature which cannot rule out the crucial selection bias (Bendz, 2017). A recent panel study using lead-lag and fixed-effects models, however, suggests that contracting life insurance in one’s biography, while not an immediate game-changer, produces attitudes in favour of private welfare and conservative parties (Hadziabdic and Kohl, 2022).

In this article, we want to test a third potential mechanism which draws on variations in government partisanship (e.g., Wolf et al., 2014) and party ideologies: the public–private welfare (provision) trade-off could be driven by an active strategy of rather market-liberal political parties and ideologies to complement or even replace public provision by a private one. Vice versa, the disappearance or even reversal of a trade-off after the 1980s could be driven by the decline in the prominence of market ideology among OECD governments since neoliberal views peaked in the 1980s. The changing ideological complexion of governments is the result of two intertwined developments: ideological changes of parties and the changing electoral fortunes of parties. Both aspects are intertwined because parties who find themselves locked out of government for a sustained time tend to moderate their views and reassess their winning formula.

Since its high point in the 1980s (marked by Thatcherism and Reaganomics), neoliberalism has lost its edge among some centre and centre-right parties, which had to moderate their sceptical views on the welfare state in order to become electable again. Or as Arndt (2014) puts it, to create issue convergence around the welfare state issue (examples of moderation regarding the state–market nexus on the centre-right include Reinfeldt in Sweden, 2006, Rasmussen in Denmark, 2001, or Kohl in Germany in the 1990s). This became necessary after centre-right parties, in the 1990s, lost office to modernized centre-left parties that, in turn, distanced themselves from the old ‘tax-and-spend’ image deemed increasingly electorally harmful (Horn, 2020; Ross, 2000). Under the umbrella term of the ‘Third Way’, spearheaded by intellectuals such as Giddens and Bobbio, left parties shifted their emphasis from government intervention to market allocation. While this shift from rights to obligations of Third Way social democrats is often associated with labour market and (more specifically) workfare reforms, it also had ramifications for private and public institutions and services that cover life-course risks such as old age and sickness. As a result of both transformations, a) economic worldviews have become less polarized over the state-versus-market issue and b) historic party labels (e.g., left) have lost much of their heuristic and explanatory power.

Given the data-limitations for studying the lobbying and micro-preference mechanisms in a cross-country setting, we will probe to what extent the ideology mechanisms can help in understanding the historical variation of the trade-off which the next section introduces descriptively.

Has the trade-off lost its bite? The historical evolution of public–private linkages

To operationalize the size of the public and private health and life/pension sector we first start from readily available sources. Health expenditures and their composition into public and private parts has been collected by the OECD since 1960. We draw on the OECD database on health expenditure and use the ‘public’ expenditure with the remainder being private (including private insurance and out-of-pocket expenses post 1970). We combine these 1970 data with the pre-1970 data as available in the Comparative Welfare Dataset (version 2020). While there were many private sources for health expenditure before the Second World War – out of pockets, friendly societies, occupational, corporate or mutual associations – actuarial insurance companies working on a for-profit basis did not emerge to a significant extent until the post-Second World War era, when health risk calculation improved (Reidegeld, 2007).

This is different for the mortality and longevity risks at the heart of the life insurance industry, where the first actuarily calculating company had already emerged in 1760s’ Britain. From the very beginning, life insurance was contracted to provide a pension to survivors or to create an endowment for oneself, and while competing with other savings products, the aspect of insurance against individually unpredictable mortality risks and the risk of outliving one’s assets made insurers the most important provider of private pensions until the later twentieth century, when pensions or mutual funds entered the competition in some countries. In a first instance, to cover the long-run perspective, we therefore resort to measuring the size of the life insurance sector in the respective countries through the annual flow of premium and benefit payments. Life insurance premiums and, if available, claims paid were collected from national statistics which are based on the reports of supervision authorities or industry associations starting as early as the early nineteenth century for some countries like the US and as late as the interwar years (Belgium). We primarily draw on these national sources for more detailed and harmonized coverage starting in the nineteenth century and only resorted to the OECD Insurance Database or the Swiss Re Sigma database for the more recent period, if national sources were not available. We detail the country-specific sources used in a separate data appendix (A01). In almost all countries and periods, the more readily available life gross premiums were collected as the total domestic business of all types of life insurers in place. In the case of life expenditures we attempted to cover all payments going to policyholders from life insurers, that is, predominantly from claims, but also surrender values, bonuses or dividends for policyholders. Insurers have other types of income (mainly investment income) and other types of expenses (management, shareholder dividends and so on), but premiums and benefits have long made up the core business and their respective shares to GDP correlate at 0.90 in the pooled cross-section.

In the later twentieth century, life insurers were obviously no longer the only provider of private pensions which is why we additionally make use of other measures1, 2 primarily, the OECD private pension expenditure as provided in the Social Expenditure Database since 1980 (we also consulted the total life and pension assets by GDP, provided by the World Inequality Database by Alvaredo et al., 2016 – which, however, is only available for a too small subset of the country-years we cover).

The public side of the pension system in turn is represented by the first pillar of the pension (or invalidity) insurance starting with Bismarck’s laws in Germany in 1889 diffusing globally in the old industrial countries until 1946, when Switzerland passed its first federal pension law (Abbott and DeViney, 1992). Despite the enormous welfare state research, there is still no annual dataset starting with the introduction of the first pillar and documenting its expenditure and contributions up to the current day. We therefore resorted to a different set of national sources to document the long-run development of public pensions in the 20 countries. The appendix Table A0 details the changing definitions and names of first-pillar pension programmes as well as the country-specific sources used to collect pension expenditure and contributions. Both variables are set to zero before the starting year of the first programme, when values jump to the first positive value. Expenditures are consistently available throughout the period, whereas contributions are only available where programmes are not tax-based, that is, where general tax income covers the necessary expenditure. The expenditure, and, where available, contributions show a co-movement and their GDP shares correlate at 0.95.

Additionally, we also draw on a combination of existing long-run welfare development sources, not least to include the second pillar of occupational pensions in the post-Second World War period and the transition to the third pillar of supplementary private pension provision, using a combination of data from Flora et al. (1983), Lindert (2004), and post 1960, the OECD (1985). After 1980, the OECD social expenditure data allows us to distinguish the public first from other private pillars.

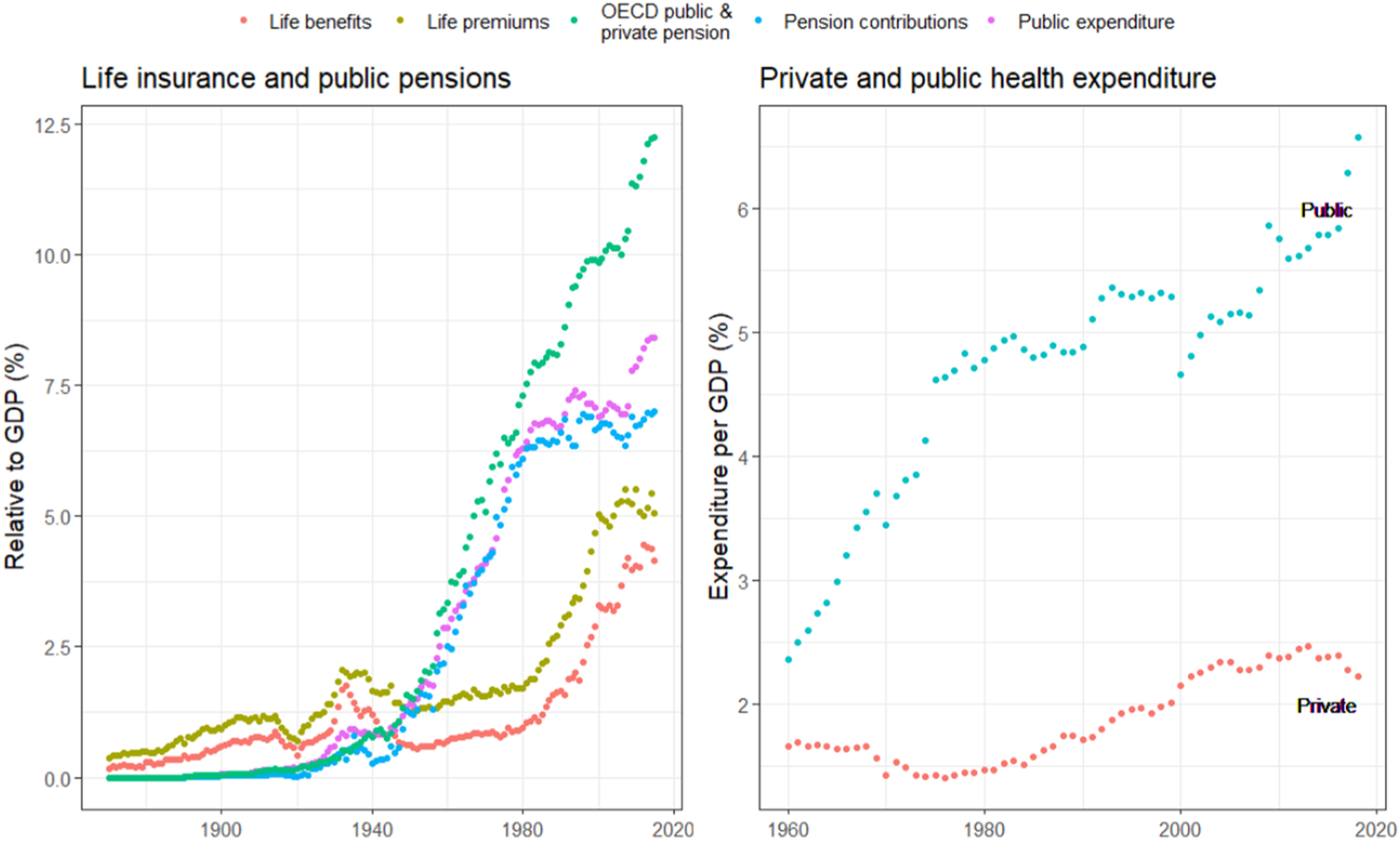

Figure 1 displays the rising trends in provision in the pension and health domain as average across the 20 countries. On the left-hand panel, we see the co-movement of private life insurance premiums and benefits and the co-movement of public first-pillar pension expenditure and contributions, with the combination of public and private pension provisions in the OECD definition on the very top. The Second World War is about the time when the predominant life insurance provision in relation to GDP was first surpassed by the public pension programmes which saw the highest growth rates in the post-Second World War period, reaching a plateau around 1980, from then on the private life insurers showed much higher growth rates, closing the private–public gap and driving the total pension expenditure up. Only in recent years have private life insurers also found a plateau at historically high levels. On the right-hand panel, health expenditures have equally risen in both the private and public sector, with a clear predominance of public health expenditure (with the US and Switzerland excepted). Health expenditures also show a rising trend over time throughout all countries, but at a lower absolute level when compared to pensions. Private–public expenditure per GDP in old age and health.

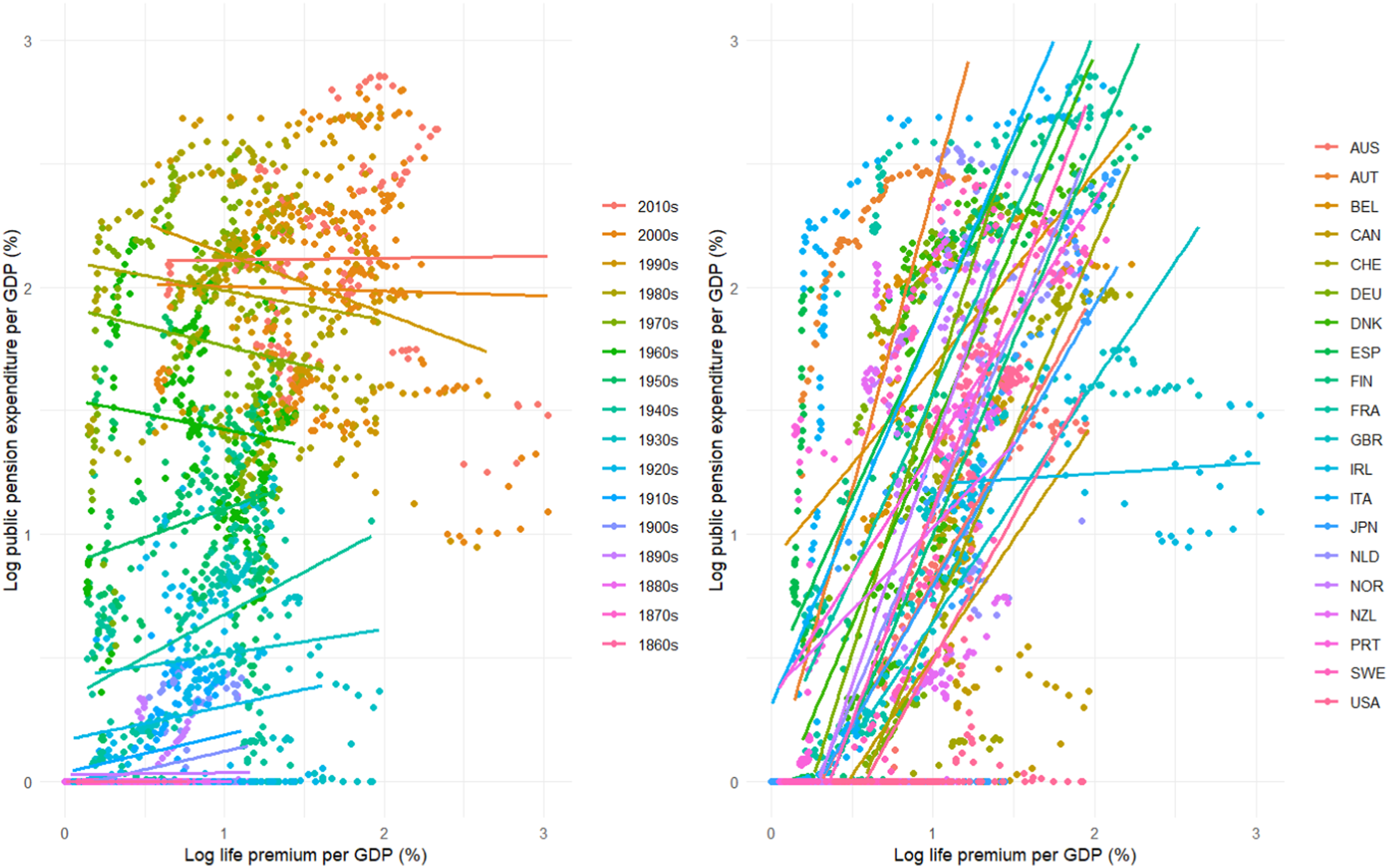

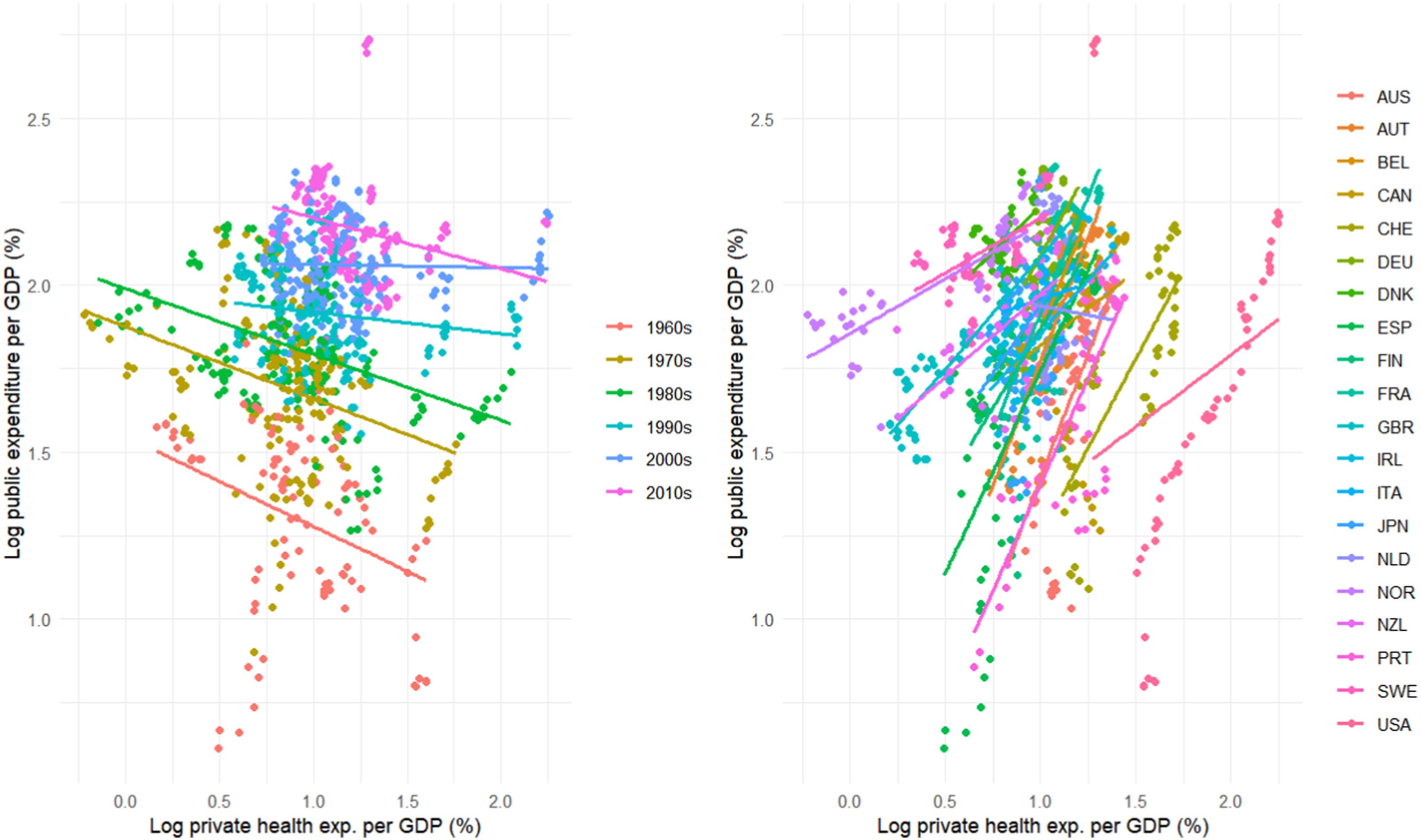

The historical evolution is thus one of parallel rising trends and does not reflect a trade-off at first sight. To investigate the cross-sectional relationship, we display scatterplots of the public–private provision in pension and health including linear regression lines by decades in the left-hand panel and by countries in the right-hand panel of Figures 2 and 3, respectively. Overall, in Figure 2 we see that for pensions there is no discernable relationship in the very early years of life insurance, when there was no public pension system in place. In the earlier twentieth century, the relationship turns moderately positive until about the post-Second World War period, from when on the relationship becomes clearly negative only to turn insignificant after 2000. In health, shown in Figure 3, the cross-sectional relationship also starts out negative after 1960 and becomes insignificant in the 2000s. The cross-sectional correlation of growth rates, instead of levels, also reveals a similar, though blurrier picture (cf. Appendix). Cross-sectional and longitudinal correlation between public and private old-age provision over time. Cross-sectional and longitudinal correlation between public and private health provision.

While this cross-sectional picture generally reveals the turn from a trade-off to a null relationship, the longitudinal association is generally one of joint growth for old age provisions often even taking an S-curved shape (except for NZL and the US and Canadian interwar years). As both measures tend to grow over time, both axes contain an implicit chronology. In most countries, the public pensions grew at rather low levels of life insurance provision. In a second, mostly post-war phase, both grew considerably and started to plateau towards the end of the twentieth century, when the rapid expansion of life insurance payments occurred at stagnating levels of public pension expenditure. The longitudinal trade-off picture for health provision is also rather one of complementarity and joint growth. The Netherlands and the United States are exceptions to this rule in the more recent period.

Can variation in anti-interventionist views account for variations in public–private links?

Overall, the descriptive evidence from our historical data collection shows that there is no simple trade-off between public and private health or old-age provision, but that time and country contexts matter. Cross-sectionally, a trade-off in both sectors existed in the post-Second World War period, but faded since the 1980s, whereas in longitudinal perspective, it is much more a story of parallel growth.

To make sense of variations in the trade-off relationship in more recent decades, we turn to multivariate analysis and probe the ideology mechanism spelt out in the literature, that is, the idea that governments’ beliefs about the role of market allocation vis-à-vis government intervention can be crucial in understanding how linkages between public and private welfare provision play out. Existing studies (Wolf et al., 2014) usually discuss the extent to which certain beliefs characterize party families, but do not measure them directly. To test our ideas, we draw on multivariate regressions and interaction analyses to quantify the impact that private health and life insurance have on social security. We account for the public–private trade-off by regressing public on private insurance spending. To the extent that we find, ceteris paribus, a significant negative effect of public schemes, we speak of a trade-off. Our aim here is to assess how this link is affected by cabinets’ market ideology despite different path dependencies and mounting problem pressure (the two most important factors here are low growth and demographic ageing).

The underlying rationale is simple: governments sceptical of state intervention and the welfare state and with particularly favourable views of market allocation will not only more readily accept or pursue a hollowing-out – or at least weakening – of public programmes (via drift, non-adjustment to inflation, or outright cutbacks), but actively support and/or subsidize new private options (what Jensen (2014) has called marketization via layering) – and hence drive the trade-off from both sides.

We know that political choices regarding welfare programmes and risk privatization are closely linked to the beliefs of cabinets regarding the role of the state and the market (Horn, 2017). Yet, our more specific point of departure is that the variation of the public–private link and the fading of the trade-off must be understood in light of ideological changes that render old left–right party labels useless. First, the proponents of a pronounced market ideology, which (as we show below) peaked in the 1980s, have become less successful electorally and gave way to pragmatic third-way centrists. These new left parties, in turn, were less focused on decommodification and less susceptible to politics against markets than before. As the ideological trajectories in the US (after Reagan) and the UK (after Thatcher) show, ideological variation is not simply driven by changes in government. Rather, even once vocal centre-right critics of welfare state interventions (e.g., Anders Fogh Rasmussen in Denmark or Helmut Kohl in Germany in the 1980s) have moderated and toned down ideas of a minimal state and criticisms of the allegedly paternalist aspects of modern welfare states. 3 , 4

To test this claim that variations in the public–private linkage can partially be explained with a less antagonistic view of state interventions and market allocation, and to avoid opportunistic data choices, we draw on an existing measure of market ideology developed in previous studies (Horn, 2017; Horn and Jensen, 2017). 5 This measure, based on coding and content analyses of the widely used Comparative Manifesto Project (now MARPOR), quantifies the extent to which the government parties (weighted by share of ministers in cabinet) use party manifestos to express views that MARPOR coders have classified as anti-interventionist, laissez-faire (neoclassic economic orthodoxy), entrepreneur-friendly and welfare-state sceptical (items 505, 702, 704, 401, and 414). As a measure of relative emphasis (relative to the rest of the manifesto), the sum of these items captures the ideological trajectories in government ideology with high face validity for well-known cases such as Thatcherism and more short-lived, less well-known conservative revolutions (e.g., the generally moderate Danish market ideology scores spike when the only conservative Statsminister after the Second World War, Poul Schlüter, came to office to fight against welfare expansion).

Using this dynamic measure of market ideology, pairwise comparisons of cabinet ideology averaged by decade (e.g., 1980 vs 1990) confirm that OECD countries have – when we look at government parties – witnessed a substantial, statistically significant, moderation of market ideology since the 1980s. The comparison of 1990 versus 1980 yields a decline of −1.82 (the 95% confidence interval goes from −2.65 to −0.99), 2000 versus 1980 yields a decline of −2.86 (CI ranges from −3.67 to −2.05), and the gap between 2010 versus the 1980s is 2.58 (CI ranges from −3.56 to −1.60).

If market ideology plays a vital part in how the public–private link plays out, we should find that this link is conditional on the emphasis on market ideology. We should find that the interaction term (private welfare provision x market ideology) is significant and that the private–public link is only negative when market ideology is pronounced (this is the weak version of the hypothesis) or positive for low values of market ideology, non-existent for medium levels, and negative for high values of market ideology (strong version). To do justice to the different substantive implications of different econometric strategies, we use a (repeated) cross-sectional and a longitudinal approach.

First, the public–private tradeoff hypothesis can be conceived of as a cross-sectional equilibrium hypothesis. While some countries (e.g. the US) have persistently low public spending and high private spending, others (e.g. France) have persistently higher public and lower private spending. Such a hypothesis should be tested in a cross-sectional manner. Thus, similar to the descriptive approach in the first part, we first run cross-sectional models without country dummies, but with year dummies and with and without a variable that captures a country’s ‘initial’ or previous levels of public provision (to account for catch-up effects and potential path dependency, as in Brady et al. (2016)). The rationale for including these initial levels of public provision is that countries with historically less generous welfare schemes have more potential for complementary public–private growth. 6

Second, we use fixed effects models to capture the within-country dynamics, in particular the effect of ideology on the public–private trade-off. Using country dummies also helps to ensure that estimation results are not driven by stable (yet) unobserved country characteristics (often referred to as unit heterogeneity). There are two other problems in the analysis of time-series cross-sectional data that could violate the assumptions underlying ordinary least squares regressions: autoregressiveness and heteroscedasticity. Operating in a framework in which number of temporal units (years) is much greater than the number of spatial units (countries) (following Wilkins’ 2018 defence of the LDV/lagged dependent variable vis-à-vis Achen, 2000 for robust estimation strategies), we include the time-lagged dependent variable as regressor to address serial correlations (that is, autoregressiveness) and panel corrected standard errors to address panel heteroscedasticity. In addition to this specification (Plümper et al., 2005), we also ran Prais-Winsten regressions (with AR1 autocorrelation structure) to address autoregression and heteroscedasticity. Both yield substantively identical (non-)results.

While we have already emphasized that our dynamic ideology measure allows us to capture the heterogeneity underlying historically grounded labels such as left and right, it is also necessary to reflect on the differences between age and health-related risks (and insurance schemes). Both are approximations of what Jensen (2014) called life-course risks; as opposed to labour market risks, which are more socially stratified and can more easily be mapped on the classic left–right cleavage. Regarding the role of market ideology, there are three key differences that render ideological effects more likely regarding health care insurance. The time horizon of pension policy changes and reforms is longer (Jacobs, 2011), the visibility and degree of political contention is lower (Jensen et al., 2018), and the idea that performance problems may be improved with market incentives (such as co-payments or the possibility to switch from public to private insurance if waiting times reach a threshold) has less direct appeal for parties faced with mounting problem pressure (performance and cost control) who are always on the lookout for measures which yield budgetary reliefs.

The selection of the control variables is based on extant research on the determinants of welfare policy – though rarely studied explicitly as a trade-off. More specifically, we draw on three bodies of research. First, we must consider the impact of structural pressures; such as the share of the elderly – which affects the demand for welfare provision – economic growth, and the fiscal balance (Pierson, 1996; Wilensky, 1975). Both economic growth and the fiscal balance affect the potential to provide and afford public and private welfare and should thus be controlled for in our analysis. Second, we need to capture the role of political institutions that constrain the power of the executive to change policies (Immergut, 1992). Lastly, a large literature points to the necessity to control the impact of societal and political power resources held by groups and/or classes (Korpi, 1983). Thus, we do not only control for cabinet parties, but also the strength of labour unions. We account for these factors via the Comparative Political Dataset/CPDS (Armingeon et al., 2018). 7

While we continue to use the OECD measures of private and public health insurance as independent and dependent variables here, the pension variables need to be adapted to the most recent period: for the long-run analysis above, we used the life insurance sector as it had already emerged in the nineteenth century in all countries and, over time, became a major provider of private pensions. In the later twentieth century, however, life insurers were no longer the only provider of private pensions, but received competition from investment and private pension funds, particularly in Anglophone and some Scandinavian countries, and the Low Countries. For this reason, rather than using life insurance only for the recent period, we also rely on the post-1980 OECD items of voluntary and mandatory private pensions which we oppose to the public statutory one. In any case, the effects on public spending ratios we present do not depend on the measure we use for the private insurance.

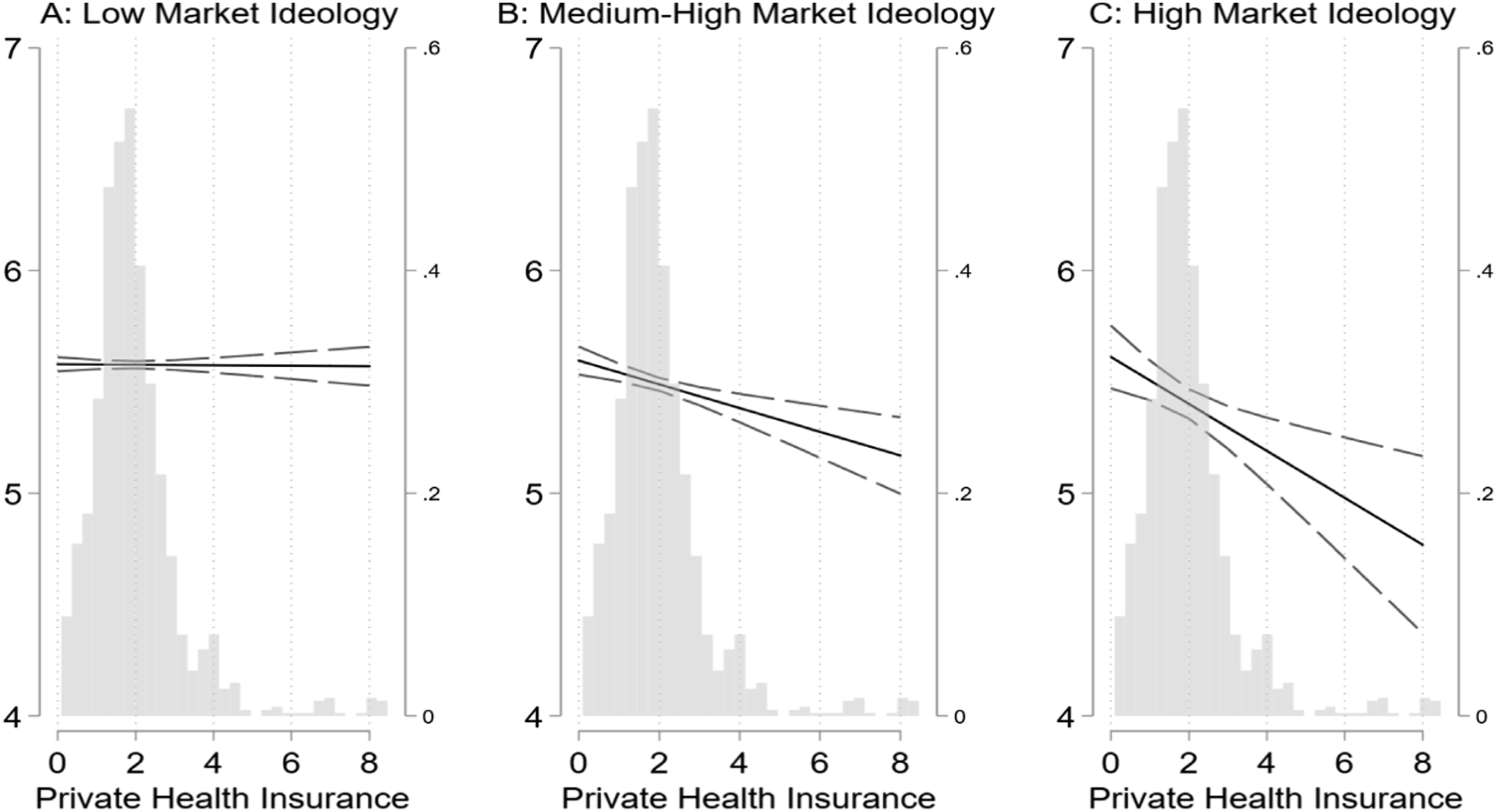

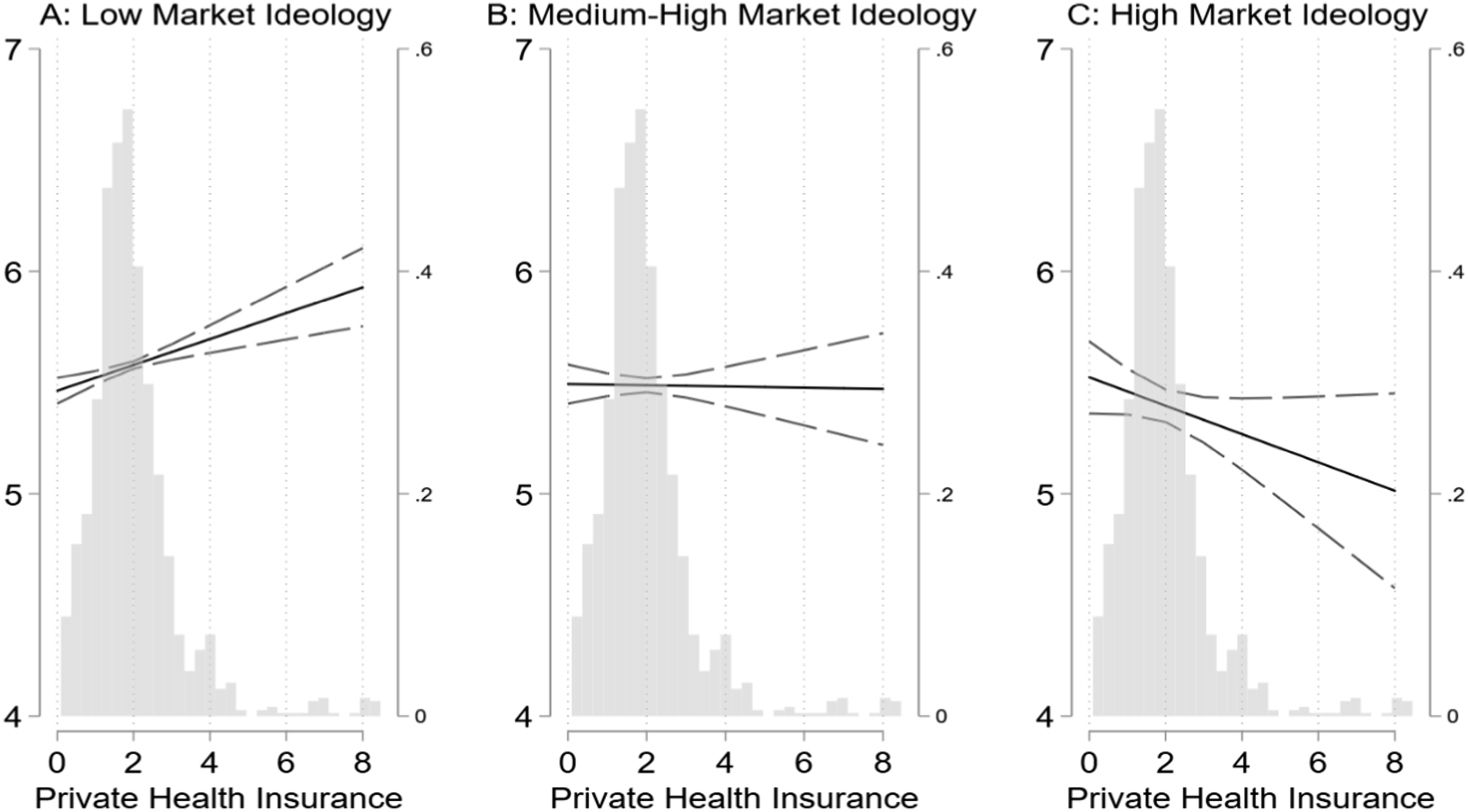

Starting with the health trade-off, appendix tables A1 and A2 show the results for the between-country (using year dummies) and the within-country regressions (using country dummies). Based on the modes in both tables, respectively, the predicted values plotted in Figures 4 and 5 show how the effect of private health insurance spending on public spending depends on governments’ market ideology. A negative slope indicates a trade-off. Both for the between-country and the within-country results, the slope is only negative if market ideology is pronounced (panel C). By contrast, Panel A and B in both figures show that this is not true if cabinet’s market ideology is weak. Rather, either no link (horizontal slope, see Panel A in Figure 4 for the between-country pattern) or a positive slope (Panel A in Figure 5, Fixed Effects) indicates that the public–private link is complementary. These results prove robust if we control for the size of the initial public health insurance sector. Effect of private on public health provision depending on market ideology. Note: based on Table A1 (appendix), M5. FE of private on public health provision depending on market ideology. Note: based on Table A2 (appendix), M5.

Turning to the old age trade-off, we find no general trade-off pattern and, in contrast to the results for health, we find that the public–private association is substantively independent of the ideological composition of the government. This is best understood when we compare the effect plots with Figures 4 and 5 (the underlying regression tables A3 and A4 are in the appendix). Figure A3 in the appendix shows that the slopes which indicate the public–private link are horizontal for high and low market ideology. The between-country results (panels A and B for low vs high market ideology) and fixed effects models (panels C and D) yield similar near-horizontal ‘slopes’. 8

Our reading of these non-results is that the horizontal slopes confirm that the long time horizons, low visibility, and/or looser links to incentives make it unlikely to find immediate partisanship effects. The above results (or for old age, non-results) are similar if we run Prais Winsten regressions instead and do not depend on individual observations.

Conclusion

Public and private provision should be studied together, despite the enormous complexities (and necessary simplifications) it entails. As we show, notions according to which private provision crowds out the state or governments crowd out markets do not necessarily reflect the heterogeneous public–private linkages documented here (and that qualification applies to both between-country and within-country perspectives over time). Our descriptive analysis based on new long-run historical data showed that public and private pension and health provision did not stand in a clear trade-off relationship for a long time: the cross-sectional trade-off started with the expansion of post-Second World War welfare states and it broke down again in more recent decades, while longitudinally, parallel growth was the predominant relationship in both policy domains. Parallel growth doesn’t have to be incompatible with retrenchment views on public welfare, as growth rates of public social expenditure can still be lower compared to private growth rates.

To better understand the trade-off dynamics of recent decades, we then looked at the role of ideology. We found that governments’ beliefs about market-versus-state intervention are a crucial driver of the trade-off in health provision: in between-country and in particular in within-country perspectives, classic trade-offs prevail only under governments with pronounced market ideology. Here it is the pronounced party–ideology cleavages that drive part of the trade-off. By contrast, regarding old age, the lack of a strong link between public and private provision does not depend on the extent to which governments favour market allocation over state intervention.

As outlined above, these differences in the public–private linkages across pension and health care politics are in line with the distinct logics of both fields/domains. They can be understood in light of three (well researched and related) factors that distinguish both life-course risks from each other despite being the subject of similar demographic and fiscal constraints and pressures: for pensions, the implementation and phasing-in period is longer (Jacobs, 2011), reform visibility is – partly due to the long implementation period – lower (Jensen et al., 2018), and new incentives and measures are less likely to yield (behavioral-, performance- or cost-cutting effects) within one cabinet period.

A related factor is that, with all OECD-societies ageing rapidly, old-age costs explode in both the private and public systems and all countries have had to introduce third-pillar systems, some earlier, some later (Brooks, 2005; Röper, 2021). Even though pension politics has traditionally followed a left–right logic and even though both health and pension costs are driven by demographic ageing (a factor that we have controlled for in all regression models), cabinets of different orientations have seemingly come to embrace the idea that private pillars in pension systems are needed.

Old age and health are just two domains in which modes of public and private welfare provision potentially compete. From a public-expenditure perspective, they are among the most expensive domains. Yet, there are a number of other policy domains in which a similar long-run analysis of trade-offs could be implemented, most notably perhaps in the domains of education (Garritzmann, 2016), but also in the domain of housing (Van Gunten and Kohl, 2020) and public/private indebtedness (Wiedemann, 2022), where new forms of private provision have increasingly come to challenge traditional state functions.

Supplemental Material

Supplemental Material - Beyond trade-offs: Exploring the changing interplay of public and private welfare provision in old age and health in the historical long-run

Supplemental Material for Beyond trade-offs: Exploring the changing interplay of public and private welfare provision in old age and health in the historical long-run by Alexander Horn and Sebastian Kohl in Journal of European Social Policy

Footnotes

Acknowledgements

We are grateful to Nils Röper, Marius Busemeyer, Julian Garritzmann, Carsten Jensen, Nadja Wehl, Gianna Maria Eick, many panellists at CES and ECPR events and the reviewers for very instructive comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.