Abstract

We empirically test an integral model for healthcare and child support benefits take-up using a probability sample of the Dutch population (N = 905). To examine how different psychological factors, in conjunction, explain take-up, we apply model averaging with Akaike’s Information Criterion (AICC). For both types of benefits, people’s perceptions of eligibility best explain take-up. For healthcare benefits, take-up also relates to perceptions of need. Exploratory analyses suggest that for healthcare benefits but not for child support benefits, executive functions, self-efficacy, fear of reclaims, financial stress, and welfare stigma explain perceived eligibility. We find no support for knowledge, support, and administrative burden as explanatory factors in take-up. We discuss the results in relation to the Capability Opportunity Motivation Behaviour (COM-B) model for developing behavioural change interventions.

Introduction

Social welfare provides income security for financially vulnerable households and can counteract financial distress. Many eligible families, however, do not claim social welfare. Non-take-up rates vary between countries and programmes, but 30–40% rates are not exceptional (Dubois and Ludwinek, 2015; Hernanz et al., 2004; Plueger, 2009). From a policy perspective, this implies that social welfare systems are not fully achieving their goals, which may undermine their legitimacy (Roosma et al., 2016). For eligible households, not claiming social welfare negatively affects their current wellbeing. Moreover, it affects their future wellbeing, as the non-take-up of welfare hampers saving for rainy days and investing in the future. Thus, the non-take-up of social welfare may exacerbate financial distress and contribute to poverty traps (Banerjee and Duflo, 2011).

To develop effective interventions to increase take-up, it is essential first to identify which factors contribute most strongly to the observed non-take-up. The study of welfare participation started almost a century ago. Yet, until this day, empirical evidence is fragmented, and most studies examine a limited set of potential inhibitors. Scholars in the domains of social policy and public administration initially studied welfare participation. Early social policy literature on the take-up of welfare assigned a prominent role to welfare stigma (Feagin, 1972; Odum, 1923). Later studies provided a more integrative view of welfare participation. They included the influence on benefits take-up of perceived eligibility, perceived need, knowledge, attitudes towards and expectations of the application procedure, and perceived stability (Craig, 1991; Kerr, 1982a, 1982b; Van Oorschot, 1994). Standard economic models predict that households participate in welfare programmes if the benefits outweigh the costs (Anderson and Meyer, 1997; Currie, 2004; Moffitt, 1983; Mood, 2006).

In the last two decades, behavioural insights have contributed significantly to the welfare participation literature. In public administration, scholars have realized that administrative burden, defined as ‘an individual’s experience of policy implementation as onerous’, looms larger for citizens with lower levels of human capital (Herd et al., 2013; Moynihan et al., 2015, 2016). Also, they have pointed out the executive functions’ potential role in inhibiting take-up (Baicker et al., 2012; Christensen et al., 2020). Behavioural economists have developed interventions to increase welfare participation, thereby deepening the understanding of welfare participation’s psychological inhibitors and promotors (Bhargava and Manoli, 2015; Deshpande and Li, 2019; Domurat et al., 2021; Dynarski et al., 2021; Finkelstein and Notowidigdo, 2019; Sunstein, 2019; Thaler, 2018). Important findings are that increasing the salience of households’ eligibility for welfare and simplifying application processes can increase take-up. Studies like these have added significantly to the understanding of non-take-up by adding behavioural insights, but they only included a limited number of potential promotors and inhibitors of welfare participation.

The current study integrates theoretical and empirical economics, public administration, and psychology findings into one model. It tests how different psychological factors, in conjunction, explain welfare take-up for two national Dutch benefits programmes: healthcare and child support benefits. It adds to the existing literature by identifying the relative strengths of different promotors and inhibitors of welfare participation, which may help design possible interventions. The remainder of this article is organized as follows. We first give an overview of the explanatory factors for take-up in our model based on the literature (the second section). Next, we describe our methodological approach (the third section) and present the results (the fourth section). Finally, we conclude and provide suggestions for policy and future research (the fifth section).

Factors promoting and inhibiting take-up

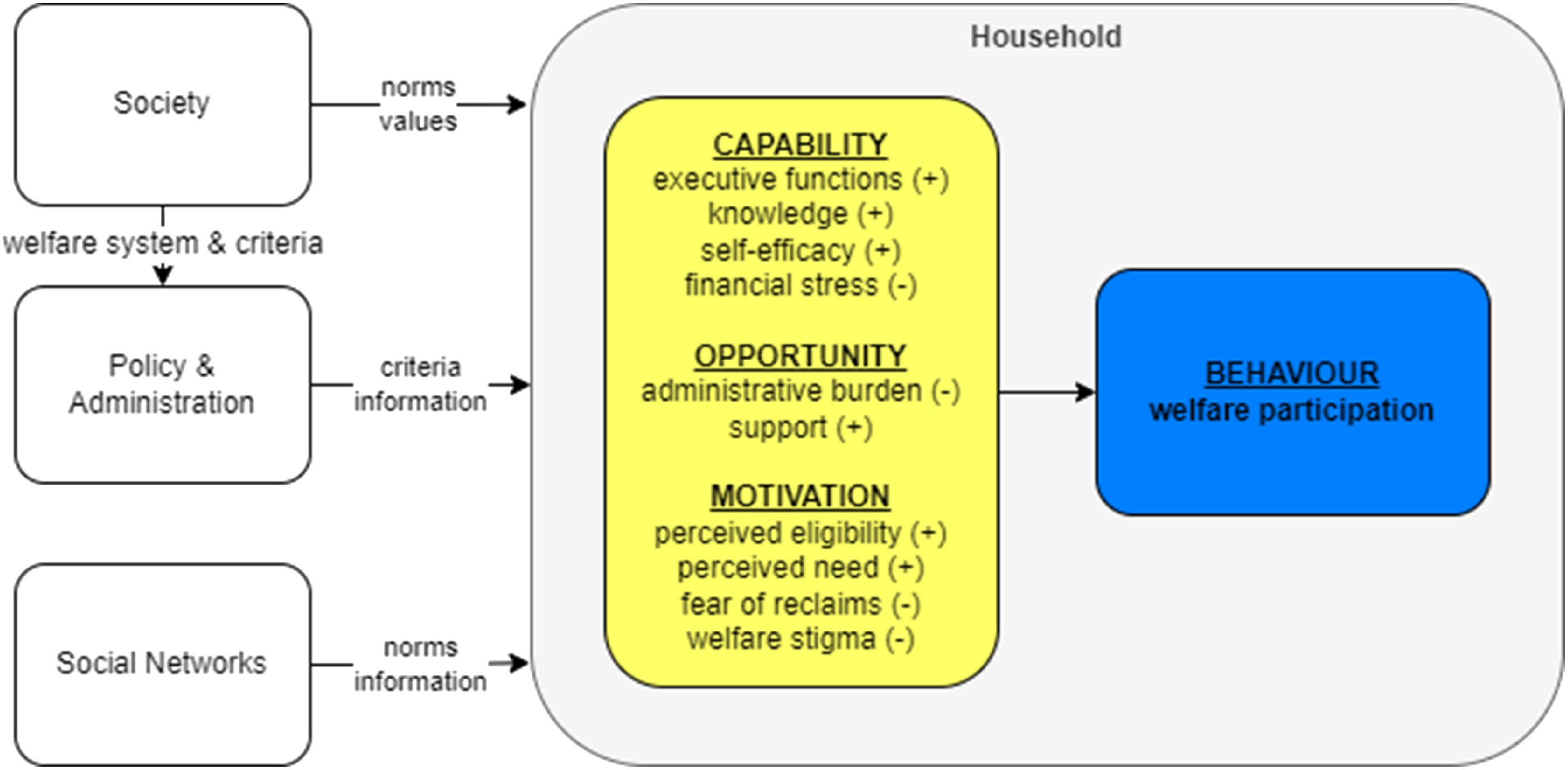

We use the COM-B framework designed by Michie et al. (2011) as a conceptual framework to organize promoting and inhibiting factors from the literature on welfare participation. This model is explicitly designed to understand behaviour and identify possible routes to promote behaviour change and interventions. The COM-B model identifies three groups of factors that need to be present for any behaviour to occur: capability, opportunity and motivation (see Figure 1). In the following, we apply this framework to organize the driving factors contributing to household welfare take-up behaviour. Combining potential promotors and inhibitors into one model allows us to test these factors’ relative strengths empirically. Conceptual model: factors promoting (+) and inhibiting (−) welfare participation.

In line with the COM-B model, our framework is dynamic and recursive. Households eligible for welfare go through an application process that consumes time. We propose that households are passively eligible (i) until the occurrence of some trigger. Van Oorschot (1994) describes triggers as ‘Sudden events which have the power of inducing claims quickly’ (p. 78). Examples include substantial income drops and direct advice and encouragement given to eligible people in personal contact. After a trigger, households go through an orientation (ii) and an application stage (iii). When the administration refuses the application, households may go through an appeal stage (iv). Finally, households must provide updates on their circumstances that affect their eligibility to the welfare administration (v). Households can thus move back and forth between these five stages. At each stage, different factors may promote and inhibit proceeding to the next stage.

The current study focuses on the behaviour of individual households. This behaviour, however, crucially depends on the context in which they operate. Society, welfare policy and administration, social networks, and individual households collectively determine the outcomes of the welfare system. Society influences welfare behaviour by establishing eligibility rules that may, in turn, affect welfare participation (Arts and Gelissen, 2002; Van Oorschot, 1994; Vrooman, 2009). A second way society influences welfare participation is through values and norms. In societies that regard welfare negatively, eligible households may experience more welfare stigma and feel less deserving than those with a more positive view of welfare (Hümbelin, 2019). Welfare policy may also affect the behaviours of street-level administrators who promote or inhibit take-up by eligible households (Berkel, 2020; Peeters and Campos, 2021). Social networks may influence the norms surrounding welfare participation and thereby affect stigma. Also, social networks can provide information on programmes and assistance in the application procedure (Bertrand et al., 2000; Markussen and Roed, 2015; Rege et al., 2012).

Capability factors

Michie et al. (2011) define capability as ‘the physical and psychological capacity to engage in the behaviour’ (p. 4). Based on the take-up literature, we propose that capability includes executive functions, knowledge, self-efficacy and financial stress.

Executive functions

‘Executive functions’ refer to a family of top-down mental processes needed when you have to concentrate and pay attention, when relying on automatic tendencies or intuition would be ill-advised, insufficient or impossible (Diamond, 2013). Executive functions consist of working memory, inhibitory control and cognitive flexibility. Research on the potential role of executive functions in welfare participation is relatively new and results from the application of psychology to public administration research. Christensen et al. (2020) proposed that executive functions play an essential role in non-take-up. They argued that those needing assistance might lack ‘cognitive resources required to negotiate the burdens they encounter while seeking such assistance’. This theoretical notion still lacks empirical support.

Knowledge

Early public administration frameworks included knowledge of a welfare programme as a threshold which eligible households had to pass before deciding to claim (Kerr, 1982a, 1982b; Van Oorschot, 1994). The rationale is that, to participate, eligible households need to know that a programme exists and understand its main characteristics. Recent empirical evidence indicates that pointing households to their eligibility for welfare may increase take-up, although the evidence is mixed. For example, Finkelstein and Notowidigdo (2019) demonstrated in a large-scale American food stamp programme (SNAP) experiment that sending eligible, non-claiming households a letter informing them of their eligibility and a reminder postcard increased take-up. In another experiment, Bhargava and Manoli (2015) sent reminders to people who had been asked to request earned income tax credit (EITC) but had not done so. The letters resulted in a 22% increase in applications. However, Linos et al. (2022) found that behaviourally informed messages to non-claimants of EITC did not increase take-up.

Self-efficacy

‘Self-efficacy’ refers to an individual’s belief in one’s capacity to execute behaviours necessary to produce specific performance attainments (Bandura, 1977, 1997). Self-efficacy influences various financial behaviours, such as saving, investing and borrowing (for example, Farrell et al., 2016; Lapp, 2010; Madern, 2015). Self-efficacy may also affect welfare participation. To our knowledge, no studies have examined this relationship.

Financial stress

Financial stress is the subjective feeling of having too few financial resources. The experience of financial stress occurs when pressing financial concerns are appraised as exceeding available resources that, in turn, evoke worry, rumination and a short-term focus (Van Dijk et al., 2022). Financial stress is associated with different aspects of one’s objective economic situation, such as having a low income, debts and the absence of savings (Drentea and Reynolds, 2015; Johar et al., 2015; Ruberton et al., 2016). Mullainathan and Shafir (2013) proposed that financial stress causes tunnel vision; it draws attention towards the instant issue of making ends meet and away from other issues. This tunnel vision impairs different aspects of executive functions (Adamkovic and Martončik, 2017; De Bruijn and Antonides, 2020; Huijsmans et al., 2019; Mani et al., 2013). Also, financial stress is associated with avoiding financial information (Hilbert et al., 2022). It seems plausible that financial stress inhibits welfare take-up because this involves processing complex information, problem-solving and perseverance.

On the other hand, a high level of financial stress could be associated with a higher degree of need for welfare and a higher degree of perceived eligibility and therefore be associated with a higher probability of benefits take-up. We are unaware of studies that empirically attempted to establish the role of financial stress in welfare participation. This line of investigation, therefore, deserves further attention.

Opportunity factors

Opportunity entails ‘all the factors that lie outside the individual that make the behaviour possible or prompt it’ (Michie et al., 2011: 4). We propose that households’ opportunity to take up benefits depends negatively on administrative burden and positively on support.

Administrative burden

‘Administrative burden’ refers to ‘an individual’s experience of policy implementation as onerous’ (Herd et al., 2013). There is ample evidence that administrative burden affects vulnerable groups more than others (Moynihan et al., 2015, 2016; Reijnders, 2020). Experimental evidence confirms that decreasing administrative burden can increase take-up. For example, Fox et al. (2020) found that reducing administrative burden increased the take-up of Medicaid. Bhargava and Manoli (2015) found that simplifying the reminder letters had a large effect on take-up (23%, compared to 14% in the control group).

Support

Several studies have demonstrated that professional or social network assistance and support may promote welfare participation. In a small-scale field experiment, interviewers answered questions of households eligible for food stamps. This intervention increased participation rates compared to the control group (Daponte et al., 1999). Finkelstein and Notowidigdo (2019) found that providing assistance and sending reminders increased take-up from 11% to 19%. Other studies have found that support from social networks may also increase take-up (Bertrand et al., 2000; Janssens and Van Mechelen, 2022; Rege et al., 2012).

Motivational factors

Motivation involves ‘all those brain processes that energize and direct behaviour… It includes habitual processes, emotional responding, as well as analytical decision-making’ (Michie et al., 2011: 4). We propose that households’ motivation to participate in welfare programmes relates positively to perceived eligibility and perceived need and negatively to fear of reclaims, financial stress and welfare stigma.

Perceived eligibility

Public administration literature often mentions perceived eligibility as a threshold for welfare participation (Kerr, 1982a, 1982b). According to Ritchie and Matthews (1982), perceived eligibility includes ‘ethical, factual and emotional notions about who could and should receive the benefit’ (cited in Craig, 1991: 548). From the finding that a relatively large proportion of non-claimants thought that they were ineligible, Van Oorschot (1994) concluded that perceived eligibility was a threshold for claiming.

Perceived need

Public administration and economic studies of welfare participation have consistently included perceived need or utility as a relevant factor. For example, Ritchie and Matthews (1982) proposed that income adequacy – the ability to make ends meet – serves as a threshold for welfare participation. Many economic studies have found a positive correlation between the potential amount and duration of welfare and take-up. For example, Anderson and Meyer (1997) found that welfare becoming subject to income tax almost entirely explained the decrease in the take-up of unemployment insurance in the US in the 1980s. Dahan and Nisan (2010) found that the welfare amount played a crucial role in shaping take-up rates. These findings confirm that eligible households are more likely to take up benefits as they derive more utility from doing so. In the current study, we conceptualized perceived need as the subjective assessment of a household’s need to receive benefits, thereby distinguishing it from objective factors such as income and benefits amount.

Fear of reclaims

The public administration and behavioural economics literature mention the fear of reclaims or sanctions as a potential inhibitor of welfare participation. There is some evidence that benefits recipients may fear sanctions due to unjustly received benefits (Reeves and Loopstra, 2017; Wright et al., 2020). In a qualitative study among low-income households in the Netherlands, Simonse et al. (2022) found that the fear of reclaims was the main reason respondents refrained from welfare participation. Bhargava and Manoli (2015) found that attempts to reduce fear of audits had little effect. So, although there are theoretical reasons for fear of reclaims inhibiting take-up, empirical evidence is scarce, and results are ambiguous.

Welfare stigma

There is a rich literature indicating that stigma is associated with welfare participation, depending on the cultural context (for example, the attitude towards welfare), the type of programme (for example, the generosity), and characteristics of the participants (for example, blame, identification) (Feagin, 1972; Horan and Austin, 1974). Moffitt (1983) was the first to quantify the role of stigma in inhibiting welfare participation. His economic model of welfare stigma demonstrated a negative appetite for participating in welfare programmes. Currie and Grogger (2001) observed that electronic benefits transfer increased the take-up of food stamps in the US and argued that this confirmed the role of stigma in take-up. Mood (2006) posited that welfare stigma in Australia was low because take-up was high. Bhargava and Manoli tested several interventions to increase take-up of earned income tax credit (EITC) in the US and concluded that stigma played an insignificant role in EITC take-up. Wildeboer Schut and Hoff (2009) concluded that stigma was relatively high but unrelated to non-take-up. In a cleverly designed lab experiment, Friedrichsen et al. (2018) provided causal evidence that social stigma inhibits take-up: participants were more reluctant to take up a redistributive transfer when claiming was publicly observable. Overall, the literature suggests that stigma may play a role in the non-take-up of social welfare. However, the difference in operationalizations makes it difficult to judge the extent to which welfare stigma explains non-take-up in different contexts.

Many potential promotors and inhibitors of welfare participation have emerged from the literature. There is empirical evidence for some of these factors, whereas the evidence is mixed, unclear, or lacking for other factors. Also, most empirical studies have focused on one or a few potential promotors or inhibitors. To our knowledge, no integral empirical studies examine these factors in conjunction and within one theoretical framework. We, therefore, examine the relative contributions of different factors using the COM-B framework.

Methodological approach

In this cross-sectional study, we surveyed participants of the LISS panel administered by Centerdata. We administered the survey in July 2020. The panel is based on a probability sample of households drawn from the population register by Statistics Netherlands (Scherpenzeel and Das, 2010). If needed, Centerdata provides households with a computer or internet connection so that vulnerable households can participate. Respondents fill in monthly questionnaires on various topics, including their economic situation. This enabled us to link eligibility for healthcare and child support benefits with our survey results. We selected respondents based on eligibility for either of the two benefits.

Dependent variables and respondent selection

We asked respondents to indicate which of the two benefits they had used in 2020 (only child support benefits, only healthcare benefits, neither, or both). Based on their responses, we could determine take-up, the dependent variable in our models.

Table 1 contains a short description of the two benefits that are the subjects of the current study; Appendix I includes the detailed eligibility criteria for the two benefits. For healthcare benefits, we selected respondents aged 18 years and older with (household) incomes and assets below the eligibility thresholds. We calculated gross household income as the sum of monthly household incomes in 2020. Since healthcare insurance is mandatory in the Netherlands, we assumed all respondents had insurance and paid their premiums. The last criterion is an approximation, but the number of people not paying their health insurance premium is low (around 2%). We disregarded the special situations described in Appendix I for the same reason.

For child support benefits, we selected households with assets below the asset thresholds and for whom their children’s birth years were known. Next, we calculated the eligible amounts based on income and children’s ages. 1 We asked respondents whether they or their partners received a general child allowance as a final check. For respondents who indicated having a partner, we assumed that their partner was also their benefits partner. This assumption holds for almost all households.

Independent variables

The survey included three multiple-choice questions to measure knowledge and Likert items (1 = fully disagree… 7 = fully agree) to measure the other independent variables. Appendix II contains the complete questionnaire.

Capability

We measured executive functions with the 12-item Amsterdam Executive Function Index (AEFI) (Van der Elst et al., 2012). Items included ‘I am easily distracted’ and ‘I often react too fast. I’ve done or said something before it was my turn.’ The internal consistency is high (Cronbach’s α = 0.84). Three multiple-choice questions measured knowledge: one on healthcare benefits, one on child support benefits, and one on benefits in general. We created two separate knowledge variables from these questions: one for healthcare benefits and one for child support benefits. Each variable included a specific question and the general question. We captured self-efficacy with three items, including ‘If I want, I can easily apply for benefits’ and ‘Even if I would try hard, I don’t think I would succeed in applying for benefits’ (α = 0.80). We captured financial stress with the five-item version of the Psychological Inventory of Financial Scarcity (PIFS) (see Hilbert et al., 2022). Items included ‘I often don’t have enough money’ and ‘I feel that I have little control over my financial situation’ (α = 0.93).

Opportunity

We measured administrative burden with a three-item scale. One example of an item was ‘Applying for benefits involves much hassle’ (α = 0.91). Our support scale consisted of three items, including ‘If I don’t succeed in applying for benefits, I know whom to turn to for help’ (α = 0.87).

Motivation

We asked respondents, ‘I think I am eligible for… benefits’, to measure perceived eligibility. For perceived need, we asked, ‘Without… benefits, it is difficult for me to make ends meet’ and ‘…benefits are worthwhile for me’. The correlations between the items for perceived need are moderate (rs = 0.64 for healthcare benefits and 0.61 for child support benefits). We assessed fear of reclaims with three questions, including ‘I am worried that I have to repay benefits because of a mistake’ (α = 0.91). We assessed welfare stigma with a tailored three-item Consciousness Scale (Pinel, 1999; Pinel et al., 2005). One question was, ‘There are negative prejudices about people who use child support or healthcare benefits.’ The internal consistency of the welfare stigma scale is moderate (α = 0.74). We used the full scale in our analyses. 2

Control variables

There is substantive evidence that income, benefits amount, age, household composition, and gender may relate to the take-up of welfare (for example, Berkhout et al., 2019). We, therefore, included these variables as control variables in our analyses to eliminate alternative explanations and demonstrate the unique relationship between psychological predictors and welfare participation. Centerdata takes several measures to increase the quality of self-reported income data. Households are asked to provide their income shortly after the due date for the tax declaration. Centerdata informs households which figures from their tax declaration they should use for gross and net income. Finally, if gross income is missing, Centerdata calculates it based on net income and vice versa.

Analytical model

Because take-up for the two benefits ranged between 56% and 69%, we used a linear probability model, which is easier to interpret than a binomial model (Hellevik, 2009). The following formula mathematically represents our model

Multimodel inference

We applied multimodel inference based on an information–theoretical framework using a corrected version of Akaike’s Information Criterion (AICC) (Akaike, 1973; Brewer et al., 2016). Akaike’s framework is well suited for model selection, especially if the purpose is to explain (rather than predict) the phenomenon under investigation (Bozdogan, 2000; Burnham and Anderson, 2004). Also, the framework guards against overfitting (Hawkins, 2004). Overfitting increases the probability of finding spurious effects (Anderson, 2008) and decreases generalizability (Myung, 2003). The traditional approach to overfitting, stepwise regression, leads to incorrect standard errors of the parameter estimates. As a result, relevant variables may not be selected for the model, and nuisance variables may be included, which leads to incorrect inferences (Smith, 2018). Regularization (or shrinkage) mechanisms such as Ridge regression, LASSO, and Elastic Net are alternatives for stepwise regression (Hoerl and Kennard, 1970; Tibshirani, 1996; Zou and Hastie, 2005). A flaw of regularization mechanisms is that they base inference on a ‘best’ model and disregard model uncertainty, which leads to underestimation of the residual variance (Zucchini, 2000) and over-confident inferences (Hoeting et al., 1999). Model averaging based on Akaike weights overcomes this problem (Anderson, 2008; Lukacs et al., 2010; Maes et al., 2021).

Results

Data inspection

Healthcare benefits and child support benefits in the Netherlands.

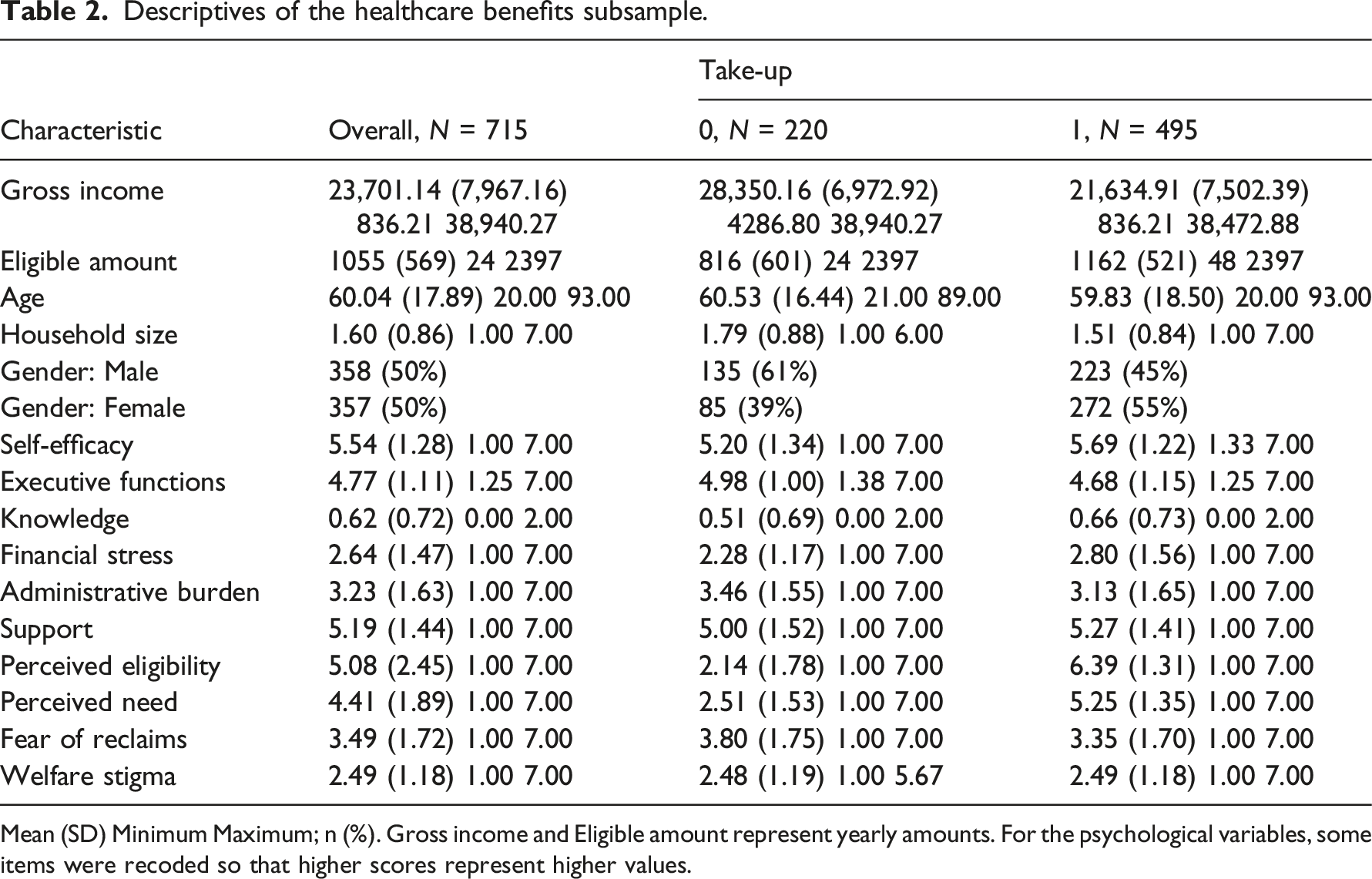

Descriptives of the healthcare benefits subsample.

Mean (SD) Minimum Maximum; n (%). Gross income and Eligible amount represent yearly amounts. For the psychological variables, some items were recoded so that higher scores represent higher values.

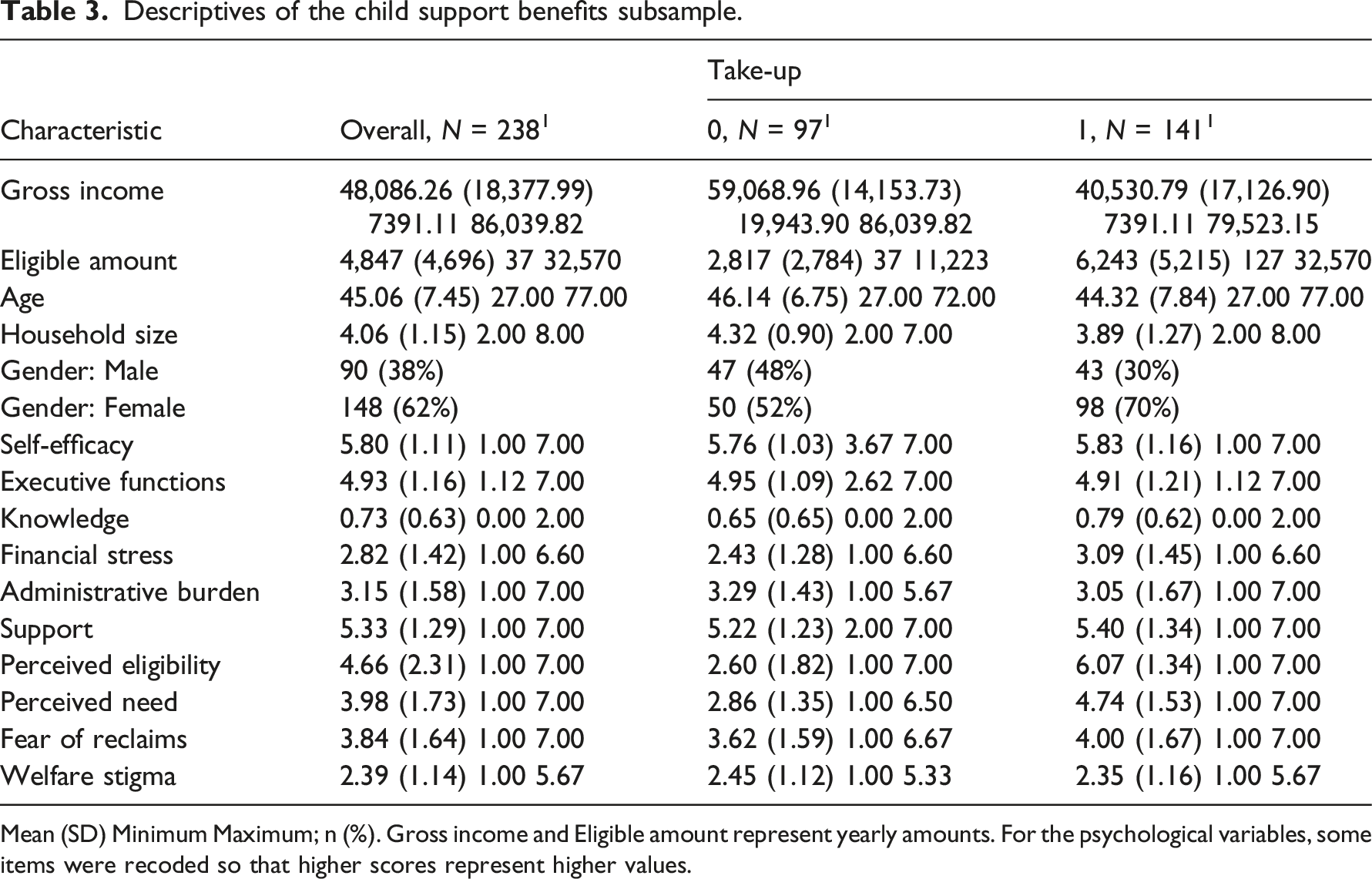

Descriptives of the child support benefits subsample.

Mean (SD) Minimum Maximum; n (%). Gross income and Eligible amount represent yearly amounts. For the psychological variables, some items were recoded so that higher scores represent higher values.

Descriptive statistics

The mean household income for the sample is €30,076 (Mdn = €26,400, SD = 15,860), which is lower than the mean for the Dutch population (M = €32,400, Mdn = €28,600) (Statistics Netherlands, 2021). The sample comprises 52% females, and the respondents are between 20 and 93 years old (M = 57.00, SD = 17.21). The mean household size is 2.14 (SD = 1.39), which corresponds well with that of the wider population (2.17). We created two samples from the total sample: one for healthcare benefits (N = 715) and one for child support benefits (N = 238).

Healthcare benefits

The mean income of respondents eligible for healthcare benefits (M = €23,701, SD = 7967) is below the population mean (Table 2). This is likely due to healthcare benefits aiming at low-income households. The mean eligible amount is €1055 (SD = 569). Respondents in the healthcare benefits subsample are somewhat older and belong to smaller households than the full sample (M = 60.04, SD = 17.89). Of the respondents, 20% fully disagree with the statement ‘I think I am eligible for healthcare benefits’, whereas 54% fully agree. The remaining 26% are not (entirely) certain about their eligibility. Self-efficacy, knowledge, financial stress, support, perceived eligibility and perceived need were higher in the take-up group. In contrast, executive functions, administrative burden and fear of reclaims were higher in the non-take-up group. Welfare stigma did not differ between the two groups. Spearman’s correlations of take-up with most of the variables of interest are weak, with some exceptions (Appendix III, Table A1). Take-up of healthcare benefits correlates strongly with perceived eligibility (rS = 0.76) and moderately with income (rS = −0.40) and perceived need (rS = 0.64).

Child support benefits

For respondents eligible for child support benefits, the mean income is above the population mean (M = €48,061, SD = 18,343) (Table 3). In contrast to healthcare benefits, child support benefits do not target low-income households; income thresholds are higher. Child support benefits target families with children, many of which are two-income households. The mean eligible amount is €4847 (SD = 4696). The mean household size (M = 4.06, SD = 1.15) is higher, and the mean age (M = 45.06, SD = 7.45) is lower than the healthcare benefits sample. These findings are in line with child support benefits targeting families with children. Notably, 62% of the respondents in this group are female. For child support benefits, 16% of eligible households fully disagree with the statement ‘I think I am eligible for child support benefits’, whereas 36% fully agree. The remaining 48% are not (entirely) certain about their eligibility. Results show that self-efficacy, knowledge, financial stress, support, perceived eligibility, perceived need, and fear of reclaims were higher in the take-up group. Administrative burden and stigma were higher in the non-take-up group. There was no difference in executive functions between the two groups. This pattern differs somewhat from the pattern observed for healthcare benefits. The most notable difference occurs for fear of reclaims: for healthcare benefits, the fear of reclaims is higher in the non-take-up group, whereas for child support benefits, the fear of reclaims is higher in the take-up group. We observed no difference in child support benefits between the two groups, whereas the non-take-up group scored higher on executive functions for healthcare benefits. For welfare stigma, we observed no difference between the two groups for healthcare benefits, whereas the non-take-up group scored higher on welfare stigma for child support benefits. For child support benefits, take-up correlates strongly with perceived eligibility (rS = 0.72) and moderately with income (rS = −0.50), eligible amount (rS = 0.43), and perceived need (rS = 0.53) (Appendix III, Table A2).

Main analyses

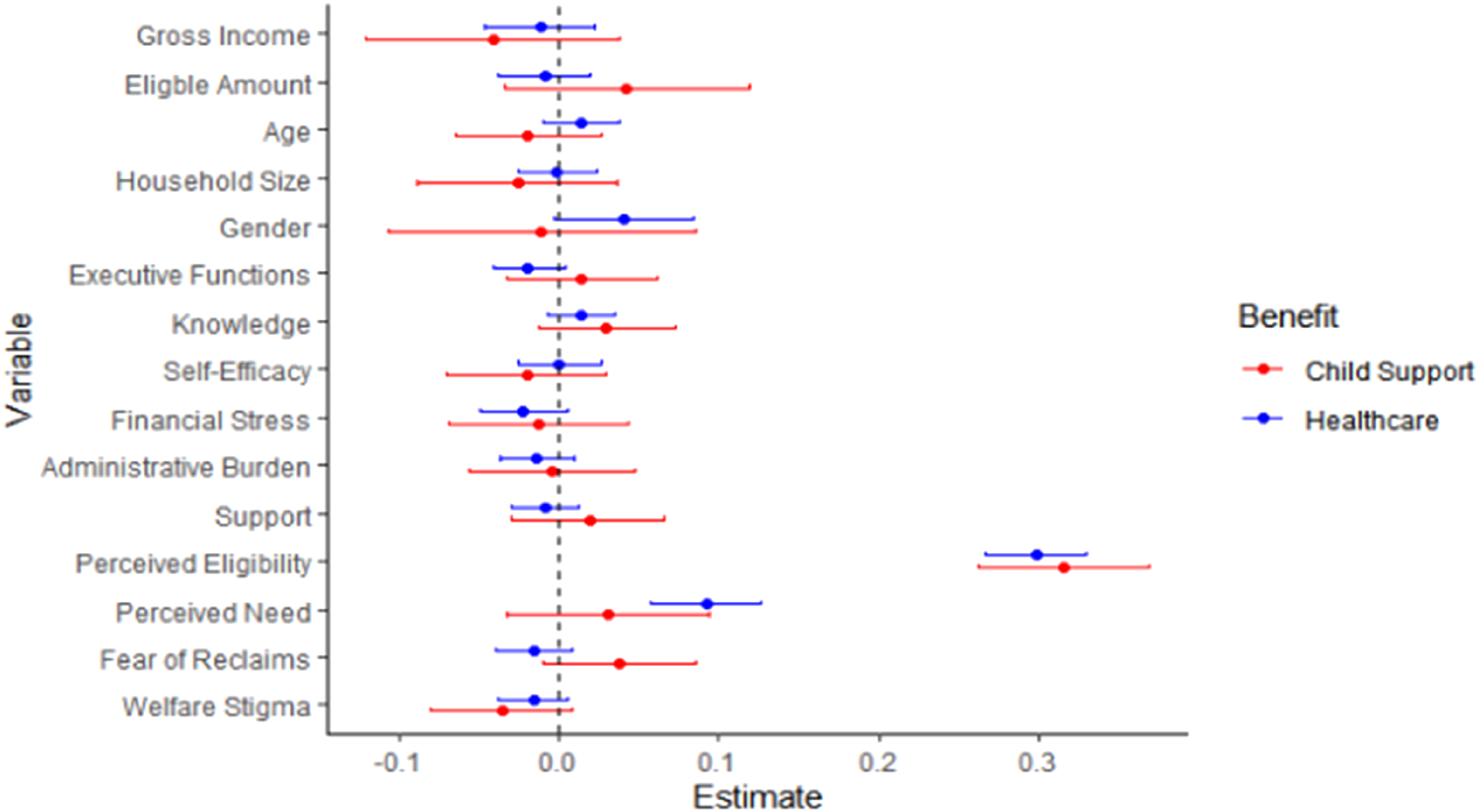

We applied maximum likelihood regression on the linear probability models represented by formula (1) and used robust standard errors (King and Roberts, 2015). We compared the base model – containing only the control variables – with the primary model – including independent and control variables. We standardized the numeric independent variables before conducting regression analyses to ease interpretation. We constructed Wald 95% confidence intervals for the regression coefficients to determine which variables contribute to predicting welfare take-up. Figure 2 graphically summarizes the results. Results of model averaging for healthcare and child support benefits. Dots represent the parameter estimates; lines represent the 95% confidence intervals.

Healthcare benefits

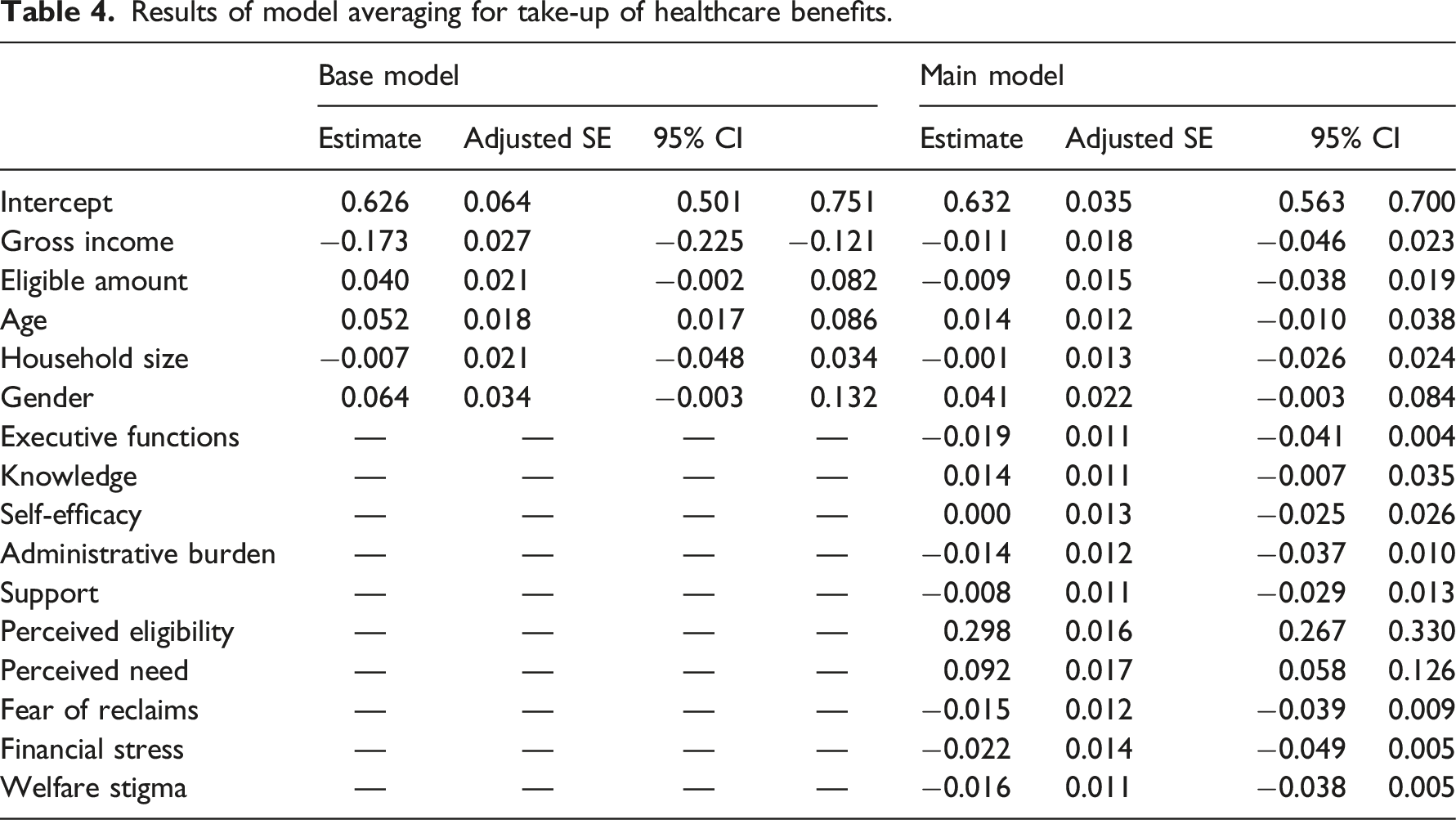

Results of model averaging for take-up of healthcare benefits.

We averaged the regression results over all models with income, eligible amount, age, household size and gender as control variables (Table 4, right). Results reveal that the take-up of healthcare benefits is significantly explained by perceived eligibility and perceived need after controlling for demographics. The model fit increase compared to the base model is high (

The association between take-up and perceived eligibility is the strongest: one standard deviation (SD) increase in perceived eligibility is associated with a 0.30 increase in take-up probability. One SD increase in perceived need is associated with a 0.09 increase in take-up. Contrary to our theoretical model, executive functions, knowledge, self-efficacy, administrative burden, support, fear of reclaims, financial stress, and welfare stigma do not significantly explain the take-up of healthcare benefits.

Child support benefits

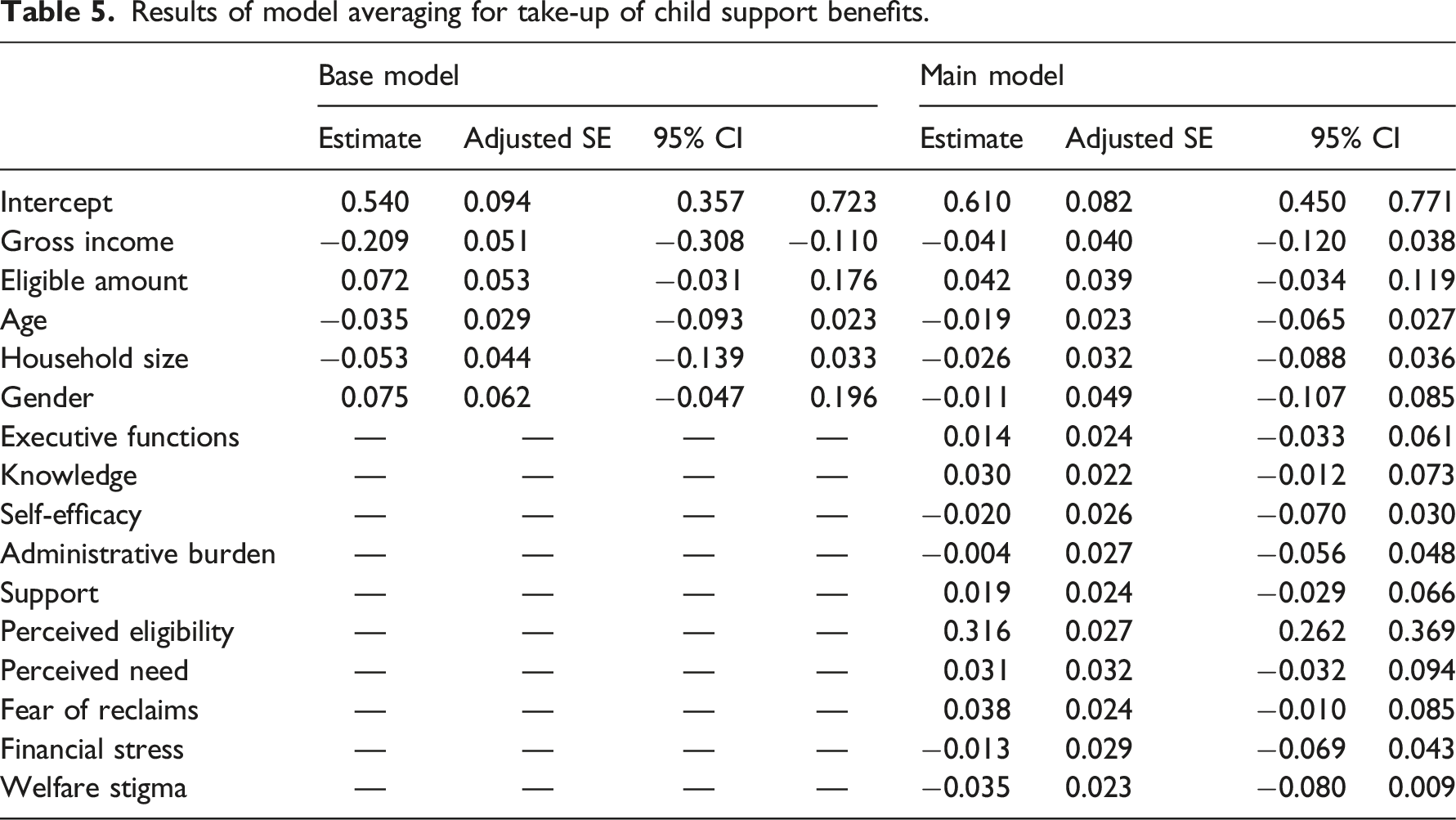

Results of model averaging for take-up of child support benefits.

Results from model averaging over all variants of the primary model indicate that perceived eligibility significantly explains take-up for child support benefits after controlling for demographics (

Exploratory analyses

In addition to the confirmatory analysis in the previous section, we performed exploratory analyses to check the robustness of our findings to different modelling choices and to examine the interaction effects. The corresponding tables are in Appendix IV. Since these analyses are exploratory, we are cautious about drawing conclusions (Anderson, 2008). Confirmatory studies should verify these findings.

When probabilities for the dependent variable are small, it is better to use a binomial model instead of a linear probability model. In our case, take-up probabilities were 0.31 and 0.41, respectively. Indeed, using a binomial model does not change the results (Appendix IV, Table A3). A combined model for the two benefits confirmed that perceived eligibility and perceived need explain take-up (Appendix IV, Table A4).

To test whether the relative contributions of promoting and inhibiting factors differ between low- and high-income households, we explored models including interactions between the independent variables and income (Appendix III, Tables A5 and A6). Similarly, we explored interactions between the independent variables and knowledge (Appendix III, Tables A7 and A8). We found that interactions do not aid in explaining take-up.

We explored which variables in our model explained perceived eligibility. For healthcare benefits, perceived eligibility was explained by executive functions, self-efficacy, perceived need, fear of reclaims, financial stress and welfare stigma (see Appendix III, Table A9 and Figure A1). Perceived eligibility negatively relates to executive functions, financial stress and welfare stigma. For self-efficacy, fear of reclaims, financial stress and welfare stigma, the negative association is as expected. The same goes for the positive associations between self-efficacy and perceived need on the one hand, and perceived eligibility on the other. The negative association between perceived eligibility and executive functions is counterintuitive and warrants further research. Perhaps higher executive functions are indicative of being more self-sufficient. Households may perceive themselves to be ineligible because they think that benefits are meant for households that are not self-sufficient. The association estimates’ confidence intervals for child support benefits included zero. We find no support for an association between perceived eligibility and the other independent variables for child support benefits. Figure A1 demonstrates that the confidence intervals are much wider for child support than for healthcare benefits. That may be due to the sample of eligible households for child support benefits being too small to detect differences.

Discussion

The current study empirically tested an integrative model for take-up by households that includes the most relevant factors found in the literature on welfare participation across different research domains. Using Michie et al.’s (2011) COM-B Model as a theoretical framework, we identify the relative contribution of various factors (related to capability, opportunity, and motivation) in promoting and inhibiting welfare take-up. We add to the existing take-up literature by testing these factors in conjunction.

We used a survey in a probability sample of the Dutch population to measure potential inhibitors of welfare participation in the Netherlands. We linked the outcomes to (self-reported) economic data of the respondents. We controlled for demographic variables (income, eligible amount, age, household size and gender).

For both benefits types, many eligible households perceive themselves as ineligible or uncertain about their eligibility: one in four households for healthcare benefits and almost half for child support benefits. In line with our theoretical model, we find a strong role for perceived eligibility in explaining take-up. When households perceive eligibility as higher, they are more likely to take up benefits. Put differently, when households incorrectly think that they are ineligible or uncertain about their eligibility, they are less likely to take up benefits. The strong association between take-up and perceived eligibility remains after correcting for income and eligible amount. This makes it extra noteworthy because it implies that high-income and low-income households may forgo benefits because they incorrectly perceive themselves to be ineligible.

For healthcare benefits, perceived need is an additional strong predictor of take-up. Households who need healthcare benefits to make ends meet or for whom healthcare benefits are more worthwhile are more likely to take up healthcare benefits. We do not find perceived need to be relevant in explaining take-up for child support benefits.

Exploratory analyses indicated that executive functions, perceived need, fear of reclaims, financial stress, and welfare stigma predict perceived eligibility for healthcare benefits. For all but executive functions, the estimates had the expected signs. We found no support for other variables in our model predicting perceived eligibility for child support benefits.

Our findings suggest that motivational factors have the largest direct associations with take-up. Motivations can often be understood in a cost–benefits frame (see, for example, Fuchs et al., 2020), such that motivations can be assumed to be stronger when the costs of certain behaviours are lower, or benefits are higher. Some elements of the factors we included can be conceived as being more related to the costs of claiming (for example, stigma), while others are more related to the benefits of claiming (for example, perceived need). But there may also be other costs and benefits that one could consider. For future research, it may be helpful to supplement our framework to include and specify information costs (time, effort and money needed to find information about eligibility, benefits and so on) or supplement the benefits with the expected duration of the welfare.

Our findings contribute to identifying the main inhibitors of welfare participation and their relative contribution to non-take-up. To our knowledge, our study is the first to empirically examine the interplay of a comprehensive set of psychological factors in explaining welfare participation. Our findings suggest that motivational factors have the largest direct association with take-up.

The results of this study can aid policymakers in identifying which factors might best be targeted when designing interventions aimed at increasing take-up. Results suggest that targeting perceived eligibility may be the most promising avenue for increasing take-up. Households who incorrectly perceive themselves as ineligible or are uncertain about their eligibility are less likely to take up benefits. Because we found no support for general knowledge about benefits programmes in explaining take-up, we propose a personalized approach to informing or reassuring households about their eligibility. The effectiveness of such interventions could be increased by combining them with interventions considering self-efficacy, fear of reclaims, and welfare stigma. Self-efficacy may be increased by training eligible households in the application process and providing clear and understandable instructions. The fear of reclaims is often realistic; when households do not provide updates to the Tax Office when their circumstances change, this may result in a reclaim. Making the update process as easy as possible and reminding households to provide updates when their circumstances change may decrease the risk and fear of reclaims. It may be possible to reduce welfare stigma by pointing out to eligible households that many others in a similar situation claim benefits.

At the same time, we caution against overstating the immediate policy implications of our current findings. Indeed, it would be good to replicate our study findings with confirmatory analyses in searching for and developing effective interventions. In addition, we advise policymakers and scholars to set up experiments to test interventions’ effectiveness jointly. Also, experiments may provide a viable route to establish causal relationships between the variables of interest. Our correlational cross-sectional study allowed us to examine relationships as they exist in the real world but do not provide a solid basis for causal inferences.

A particular strength of the current study is that it incorporated several potential promotors and inhibitors of take-up. This enabled us to determine the relative strength of these factors. Also, our approach reduced the risk of finding spurious associations compared to previous studies. Our study also has some limitations. First, it used self-reported data. Previous studies have indicated that self-reported take-up may contain errors (Bruckmeier et al., 2018; Krafft et al., 2015). Future studies could link potential thresholds for take-up with administrative records. Second, our study focused on thresholds and inhibitors of welfare participation at the household level. Future studies could examine how factors at the level of society, administration and social networks interact with factors operating at the level of individual households. Third, our study did not consider the different stages of welfare participation. Future studies could examine the association between promotors and inhibitors of take-up in various stages of the welfare participation process (orientation, application, appeal and update) (Van Oorschot, 1994).

Our study revealed the relative contribution of different factors to explaining take-up for the broad population of eligible households. Future studies could examine the lived experiences of financially vulnerable households with welfare participation. Such studies could deepen our understanding of promoting and inhibiting factors in take-up for groups that welfare programmes aim to address par excellence. Also, such studies could reveal whether the relative contribution of factors affecting take-up differs for financially vulnerable households. Moreover, such studies could reveal aspects that have not been studied thus far.

We focused on healthcare and child support benefits in the Dutch context. It would be worthwhile to test our model in other contexts, that is, for additional benefits types and different jurisdictions.

In sum, our results show that elements of motivation, in particular perceived eligibility and need, explain participation in two Dutch national benefits programmes. Exploratory results suggest that aspects of capability and motivation may explain perceived eligibility. Promotors and inhibitors of take-up may differ between welfare programmes. Our findings imply that a personalized approach to informing households about their eligibility is a promising avenue for increasing take-up. Also, providing training and instruction, and reducing welfare stigma, may improve income security and reduce financial distress.

Supplemental Material

Supplemental Material - Psychological barriers to take-up of healthcare and child support benefits in the Netherlands

Supplemental Material for Psychological barriers to take-up of healthcare and child support benefits in the Netherlands by Olaf Simonse, Marike Knoef, Lotte F van Dillen, Wilco W van Dijk and Eric van Dijk in Journal of European Social Policy

Footnotes

Acknowledgements

The authors thank ODISSEI and Centerdata for enabling data collection for this study, and particularly Suzan Elshout for her support in collecting the data.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Open Data Infrastructure for Social Science and Economic Innovations (ODISSEI).

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.