Abstract

The long-run U-shaped patterns of economic inequality are standardly explained by basic economic trends (Piketty’s r > g), taxation policies or ‘great levellers’ such as catastrophes. This article argues that housing policy, and particularly rent control, is a neglected explanatory factor in understanding macro inequality. We hypothesize that rent control could decrease overall housing wealth, lower incomes of generally richer landlords and increase disposable incomes of generally poorer tenants. Using original long-run data for up to 16 countries (1900–2016), we show that rent controls lowered wealth-to-income ratios, top income shares, Gini coefficients, rents and rental expenditure. Overall, rent controls need to be strict in order to have tangible effects, and only the stricter historical rent controls did significantly reduce inequalities. The study argues that housing policies should generally receive more attention in understanding economic inequalities.

Introduction

With the publication of Thomas Piketty’s Capital in the Twenty-First Century, the U-shaped curve of inequality became one of the most discussed facts of our times (Piketty and Gabriel, 2013). The wealth-to-income ratio and income shares of the top 1% or the top 10% fell after the First World War from the heights of the prewar Belle Époque to a trough in the Trente Glorieuses after the Second World War, only to rise again after the 1970s, particularly in Anglophone countries. After 1990, post-socialist countries joined this general trend. But what explains it?

Piketty’s most recent book (Piketty, 2020) adds many more explanatory elements to this descriptive picture. Prompted by the moments of solidarity during the world wars, governments enacted progressive income and wealth taxation to expand redistributive welfare states and democratized education. With the ‘ownership ideology’ returning in the 1970s, however, the progressivity of these taxes was cut back (Scheve and Stasavage, 2016) and the democratization of tertiary education halted (Piketty, 2020). In countries like the US, where the cutback was particularly pronounced, inequality rose strongly, reaching the Golden Age levels of more than a century ago and ending the ‘great levelling’ that usually follows wars (Scheidel, 2018). Increasing globalization, declining union power, a technological skills gap, and wage setting by superstar firms have all figured prominently in existing explanations (Neckerman and Torche, 2007). A rich literature on financialization (Godechot, 2020) shows how the wages of the bottom 50% could stagnate while capital income at the top increased persistently.

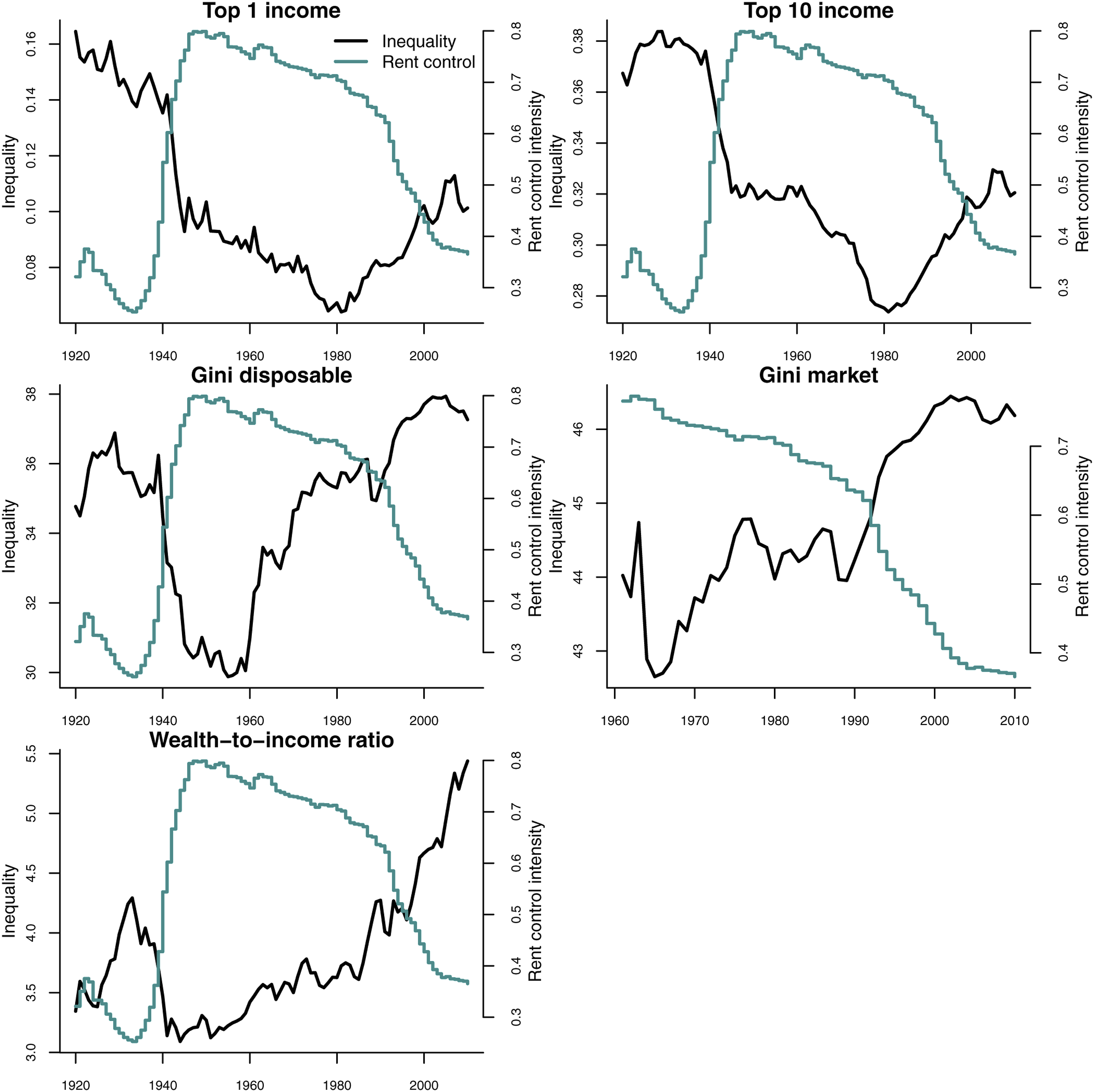

This article introduces a new, somewhat hidden, explanatory factor to the debate, linking inequality to recent housing debates: rent control, mentioned by Piketty only en passant (Piketty, 2020: 436). This ‘minimum wage’ of the housing market limits the incomes and real estate values of generally richer landlords while simultaneously increasing the disposable incomes of generally poorer tenant households. The regressive incidence of rental expenditure and the progressive incidence of rental revenues makes rent controls a highly progressive policy measure. Prima facie, the history of rent regulation fits the stylized inequality facts very well (see Figure 1). First introduced during a time of high inequality during the two world wars and prolonged in the aftermath, it was part of the solidarity package of high taxes on income and wealth that reduced inequality throughout the Trente Glorieuses (Voldman, 2013). It was lifted and deregulated at about the same time as inequality started to rise again after the 1970s, but persisted as softer control in more equal societies while quickly being abolished in the high-inequality Anglophone countries. It was highest in the most equal socialist countries. The U-shaped curve of inequality over time is hence mirrored by an inverted U of rent regulation (see Figure 2, and Figure A1 in the Appendix). Long-run evolution of inequality measures and rent control indices. Long-run revolution of rents, rental expenditure and rent control indices.

To determine whether this prima facie evidence holds up, the article conducts a broad empirical analysis using a unique panel of up to 16 countries 1 in a time series between 1900 and 2016, based on an original combination of new long-run data. It finds that rent control is negatively associated with rent increases, rental expenditure, the top 10% income share, the Gini coefficient, and Piketty’s wealth-to-income ratio, conditioned on a range of standard control variables. Impulse–response functions show that a one-time rent control shock has effects over several years.

The study makes a broader case for including housing more systematically in the study of social policies and inequality with its focus on the welfare state and income inequality (Hannah et al., 2019; Iosifidi and Mylonidis, 2017). Housing has become the largest item in households’ wealth portfolio and monthly expenses. Moreover, the unprecedented house price increases since 1990 are contributing to the increasing unaffordability of superstar cities, decoupling them economically and politically from stagnating hinterlands in many countries (Adler and Ansell, 2019; Le Galès and Pierson, 2019). Linked with family formation, neighbourhood segregation, educational access and political participation, housing inequalities, moreover, tend to spill over into other social domains.

In the next section, we introduce the general inequality literature with some of its main explanations before zooming in on the smaller housing and inequality literature to generate three guiding hypotheses. We then present the empirical data used. In the results section, we describe overall patterns in the data and run dynamic panel regressions. After robustness tests, we discuss the potential implications and limitations of our findings for further research.

Literature: inequality and housing

The starting point for the more recent inequality literature is the observation of a growing trend in economic inequality, which occurred in many countries in the Global North, but also beyond, following a longer decline in the earlier 20th century (Piketty, 2014). Rising inequality within countries is matched by falling inequality between countries (Milanovic, 2011). Economic inequality is usually viewed through inequality of wealth and inequality of incomes, that is, labour and capital income, with the fall and rise observable for both. The study of wealth inequality, due to data limitations, is much less developed than that of income inequality, and there is limited cross-country correlation between income and wealth inequality (Pfeffer and Waitkus, 2021).

Various factors have been proposed to understand inequality dynamics. For Piketty, the relationship between economic growth and interest rates (r > g) is central (Góes, 2016). Others hold that extraordinary events, such as catastrophes, revolutions and wars, are historically ‘great levellers’ of wealth and income (Scheidel, 2018). For the last century, some highlight the redistributive effects of high income and wealth taxation (Scheve and Stasavage, 2016), while others point to the spillover of wartime welfare into the growth of redistributive welfare states (Obinger et al., 2018) or the surge in collective postwar investments (Haffert, 2019). With war solidarity fading, political measures ran out, thus allowing a new rise in inequality, which some accounts see as additionally driven by rising globalization, technological divides and declining unionism (Neckerman and Torche, 2007).

Generally, housing is not yet a core theme in the inequality literature, even though it can affect income and wealth inequality through at least two channels. First, housing can act as an income stream by generating rental income and capital gains. It is also the largest component in most households’ wealth portfolios, and house price changes can substantially alter its size (Christelis et al., 2013; Fuller et al., 2020; Kolb et al., 2013). Second, as it became the largest household expenditure item during the 20th century, moving ahead of food (Reckendrees, 2007), housing also affects disposable income.

Shortly after Piketty’s English publication, Rognlie (Rognlie 2014: 3) pointed out that nearly 100% of the long-term increase in the capital/income ratio, and more than 100% of the long-term increase in the net capital share of income were due to housing wealth alone. The result is similar when replacing the potentially inflated house prices with the more fundamental rents as a measure of national housing wealth (Bonnet et al., 2014). How housing wealth is distributed is a crucial component of total wealth inequality: a study of Germany (2002–2017) finds that primary residences contribute up to 16% to overall wealth inequality, while secondary real estate contributes up to 30% of wealth inequality (Bartels and Schroeder, 2020).

The relationship between rent regulation and housing wealth receives little attention, even though rent regulation is probably one of the most important factors determining the rate of return on housing investment. Research on strict rent controls in interwar France suggests that they substantially reduced overall housing values (Bonneval and Robert, 2013). Rent controls can act as a disciplining device for house prices. From this, we deduce a first hypothesis about the relationship of rent price controls and housing capital:

Housing–capital hypothesis: Rent controls decrease the size of total housing wealth and, hence, the overall wealth-to-income ratio.

Rent controls may not only affect housing values but also and more directly the income flows from residential real estate. Households can own real estate directly, or indirectly through investment funds. While there are self-employed, below median-income and even poor households for which rental income makes up a substantial income share, perhaps compensating for precarious welfare provision (Wind et al., 2020), rental-income households are generally small homeowners themselves, older, high-income, highly educated and very wealthy (Ziegelmeyer, 2015). The socio-demographics and numbers are somewhat reminiscent of Paris rentiers of the Belle Époque (Daumard and Codaccioni, 1973) and, perhaps not surprisingly, the term ‘rentier’ is being revived (Christophers, 2020). In Germany, rental income, although making up only about 3% of total pre- or post-government income in 2017, is crucial for total inequality because it is very unevenly earned (Bartels and Schroeder, 2020): up to €12,000 in 2017 for the average landlord compared to about €26,000 in the average household’s disposable income. A decomposition of rental expenditure of private tenants and rental income by household-income deciles shows that this pattern holds across European countries reporting in the EU-SILC 2019 (see Appendix Table A1). The standard economic textbook assumption is that rent controls, as price caps, obviously limit the rental income flows and hence returns, even though anticipation of controls could simultaneously lower housing values. Landlords might switch to alternative safe assets or convert rental real estate into owner-occupied properties (Fetter, 2016). To the extent that rental income is very unevenly distributed in societies, we would expect that:

Rental–income hypothesis: Rent controls decrease income flows from rental housing for landlords and, hence, reduce overall income inequality.

The flipside of this zero-sum game of rent regulation is that tenant households have more disposable income after housing costs. Inequality is usually measured by market or disposable income, that is, before and after state redistribution. These concepts, however, ignore potential inequalities on the consumption side of household budgets, which would be inexistent if households spent equal shares of their incomes on all goods, such that inflation and deflation affected all households similarly. Yet, already in the 1860s, statisticians noted an inverse relationship between household income and the budget share devoted to basic necessary (or inferior) goods, also known as Engel’s law for food expenses and Schwabe’s law for housing expenses (Schwabe, 1868). This can make the typical household budget dependent on people’s income. These income-specific inflation rates and their effects on inequality are the subject of contemporary research. One comprehensive study, for instance, looks at household income-specific inflation rates in the European Union (Gürer and Weichenrieder, 2020): across 25 EU countries, the lowest income decile had an 11.2% higher inflation rate between 2001 and 2015 (or yearly 0.76 percentage points higher) than the top decile, which translates into an underestimation of the Gini of 0.04 points. A recent study of German housing expenditures finds that ‘the 50/10 ratio of net household income increases from 1.75 to 1.97 (by 22 percentage points, henceforth pp) between 1993 and 2013, while the same ratio net of housing expenditures increases from 1.97 to 2.59 (by 62 pp)’ (Dustmann et al., 2022: 1). In short, the ‘Schwabian’ distribution of rent loads makes rents a channel for inequality on the consumption side of household budgets. From this research, we deduce the third hypothesis:

Rental–expenditure hypothesis: Rent controls decrease rental expenditure and, hence, post-housing expenditure inequality.

Housing is obviously associated with many more dimensions of socio-economic inequality beyond the capital and income hypothesized about in this article. It is a crucial reflection of residential segregation and unequal access to a range of local services, from education to all kinds of amenities, and higher exposure to crime or other negative neighbourhood effects (see Zavisca and Gerber, 2016). The quality and size of and access to housing are other important sources of housing inequality (Dewilde and Lancee, 2013). For this study, however, we zoom in on income-related inequalities to enrich the existing inequality literature on this topic with the housing dimension.

Empirical operationalization

We use the following dependent variables to approximate our three hypotheses: wealth-to-income ratios from the World Inequality Database (WID) are the crucial measure for the ‘capital is back’ claim, and its wealth component contains housing as a crucial asset in national wealth portfolios. As for rental income, the Gini coefficient, the top 1% and top 10% income shares contain rental income flows as part of households’ capital income. We use a combination of the standardized income inequality database (Solt, 2016) and WID, accessed through the merged dataset from Madsen et al. (2018). We prefer the Gini of disposable income for data coverage reasons but also show the Gini of market incomes. Rental expenditure, in turn, has figured historically as part of the expenditure items in national accounts (Knoll et al., 2015). These macro variables are not all perfect measures, because they contain housing and rents as only one, albeit an important – if not the most important – component. Yet, on the macro level and particularly for this long-run analysis, we cannot isolate the particular components, but can only use control variables.

The main explanatory variable is rent control, which we approximate by relying on the coding of historical rent laws into regulation indices for more than 130 countries and states since rent control began around 1914. 2 The rent control index measures the intensity restrictions imposed on the level of rent and its rate of increase as well as possible exceptions from the general rule. This index is computed as a simple average of six binary indices reflecting the following policies: real rent freeze; nominal rent freeze; rent level control; intertenancy decontrol; other specific rent decontrol; and specific rent recontrol. Each of the binary variables takes only two values: 1, if the corresponding restriction (for example, nominal rent freeze) is imposed, and 0, otherwise. Thus, the rent control index ranges between 0 (no rent control) and 1 (very strict rent control) and is higher the stricter and more encompassing rent controls have been. The information on each of the six policies was in most cases extracted directly from the original legal acts. In cases where the texts of legal acts could not be found, the analysis relied upon secondary literature considering the country-specific regulations.

The two major limitations of this approach are as follows: 1) it considers the written laws and does not take into account how they are enforced; 2) it approximates the sphere of application of these laws rather roughly using the last two binary variables representing exceptions from the general rule. In both cases, a more precise assessment is precluded by a lack of data. It would be possible to measure the enforceability for the last few years; however, no consistent information about the enforceability of rental laws covering all countries can be found for the earlier periods. The exact extent of exceptions cannot be evaluated either, since these exceptions often refer to very different specific geographic areas, population groups, or dwelling types. Thus, finding statistical data on the rental sector subject to controls is not feasible. A final issue is that in some countries rent control regulations are adopted not only at the national, but also at the regional (state or province) level. This is accounted for, for some countries, for example, Australia and Canada. For bigger countries, like the USA with its 50 states, it is a very complex task, especially given that historical legal acts for most states are not publicly available. Therefore, in the case of the USA, the rent control index is constructed at the national level, modelling some state-level regulations (in DC and New York) as the binary variable ‘specific rent recontrol’. Nevertheless, the indices are the only available and best data option to operationalize rent control in the long-run and they correlate quite well with alternative indicators constructed using different methods and data.

As control variables we use the GDP and population from the Macrohistory database (Jordà et al., 2017) as well as annual marriage rates and the old-age dependency ratio as interpolated series from Mitchell and the World Bank for more recent periods (Mitchell, 2005). We use the national marginal tax rates of top earners as a proxy for the extent of progressive taxation, taken from Scheve and Stasavage (2016) and extended with OECD tax data after 2010. In Piketty’s work, the difference between the real interest rate and economic growth is the central predictor for the fall and rise of income inequality (Piketty, 2014), and we follow Góes (2016) in using the difference of real 10-year government returns and real economic growth rates. We also control for average years of schooling as an indicator for social mobility chances through education as well as for trade openness as a proxy for globalization (Scheve and Stasavage, 2009). In addition, we include mortgage indebtedness as a measure of financialization which may influence inequality in two ways: 1) higher-income households have better access to borrowing that allows them to acquire more properties, and 2) credit overburdened lower-income households can more easily go bankrupt and lose their real estate assets. We also use social expenditure per GDP as a proxy for governmental transfers to lower-income households, including housing allowances. We collected housing-unit counts at census dates to compute the interpolated ratio of population-to-housing as a measure for (war-related) housing shortages. Finally, one could argue that the expansion of homeownership and social housing over the 20th century reduced the importance of rent transfers from poor tenants to rich landlords and we therefore run separate regressions including these tenure variables. As their coverage is lower (Kholodilin and Kohl, 2021), we alternatively make use of the binary variable ‘institutionalization of flat-ownership’ (for example, condominiums in Anglo countries) as a homeownership proxy in the Appendix Tables A4–5 regressions, because it correlates (0.43) with homeownership rates.

Methodologically, we estimate dynamic panel regression models. Our data have several specific features that need to be addressed. First, we deal with longitudinal data, which suggests the use of a panel data model. Second, most dependent variables persist over time. Therefore, we need dynamic models to capture the temporal autocorrelation, which is high for many slow-moving variables measured as ratios. Alongside a model with yearly data, we therefore also do a robustness check with quinquennial data. Third, there could be endogeneity issues: more equal societies could vote for more rent control-friendly governments, or higher inequality could give the top 10% more power to obstruct rent control legislation. Typically, in such cases, the dynamic panel models are estimated using the GMM (generalized methods of moments) of Arellano and Bond (1991) because the lagged dependent variable can be correlated with the error term (Anderson and Hsiao, 1981). However, given the long-term and multi-country nature of our data, it is extremely difficult to find appropriate instrumental variables. Moreover, in our dataset, the time dimension, T, is much larger than the number of countries, N, while the Arellano–Bond approach is more appropriate in the opposite situation (small T and large N).

Therefore, we account for these three features using the panel vector autoregressive (VAR) model with country fixed effects:

Rent control and inequality in the historical long run

Rent controls are almost a mirror image of income inequality trends across the last century (see Figure 2). Before the First World War, inequality levels – measured by top income shares, the Gini of market and disposable income or the wealth-to-income ratio – were very high, while rent controls were non-existent, with the exception of hardly enforced usury laws. In the First World War, the modern tax state evolved towards progressive income taxation in parallel with the apparatus of strict rent control, eviction protection and housing rationing regulations, and inequality levels started to decrease. Rent controls were only partly removed in interwar Europe and partly moved into regular civil law (Voldman, 2013). In the Second World War, countries witnessed a re-introduction of strict controls, which were maintained into the postwar years (Führer, 1995). They were lifted earlier in Anglophone countries than in continental Europe, which transitioned to a regime of softer so-called second-generation rent controls that constrained rent increases but not initial rent levels from the early 1970s. Inequality started to rise again following the 1970s, when postwar rent controls were abolished or liberalized into second-generation controls. Both the rise in inequality and the deregulation of rental markets were more pronounced in Anglo-Saxon countries. For example, rent controls and the top 10% income share have a bivariate correlation of about −0.3. The Appendix confirms this correlation in a country-by-country Figure (A1). Prima facie, then, both the housing-capital and the rental-income hypothesis find some bivariate evidence.

Rent controls have been neglected in the study of social policies, perhaps because they acted through consumer rather than labour markets and, contrary to direct transfers, were a budget-neutral regulatory measure. Yet, their interference in free market rents can also be seen as a form of decommodification of housing. Initially, they were used in the form of rent freezes, when the rental prices were fixed at a constant level, for example, at the price paid on a specific date or as a specific amount. Various institutions were responsible for fixing rents: courts, rent arbitration councils composed of tenant and landlord representatives, or state-appointed rental administrators. No rent increases were allowed without permission from such entities. In some cases, the government even forced landlords to reduce rent. From the early 1970s, a softer form or second generation of rent control, such as rent stabilization, emerged. This softer form implies that the initial rent, at least theoretically, is set at the market level in a free negotiation between landlord and tenant. However, during the contract period, rent increases are limited by cost-of-living measures. While we focus our analysis on a global index of rent control in countries, Appendix A4 also shows separate results for the hard first-generation versus softer second-generation controls (Arnott, 1995).

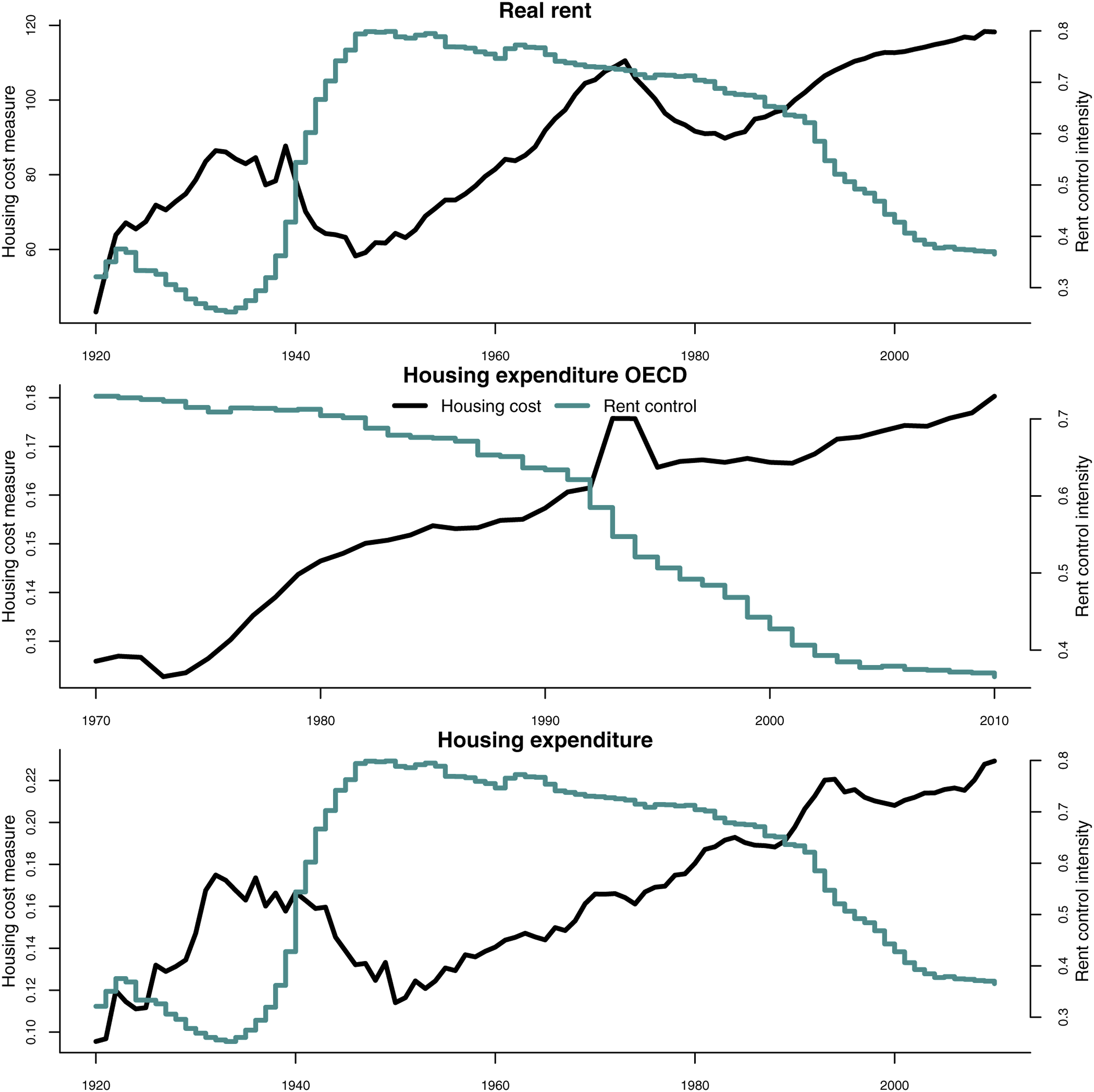

Rent controls also correlate with households’ housing expenditure and rent levels over time (see Figure 1). Historically, rent is a major component of household budgets and, with the decline of real food and textile prices, has even become the dominant expenditure in most countries. Housing costs (actual and imputed rents), sometimes including utilities, appear in most national accounts’ consumption statistics, even though they are not computed or surveyed in a standardized way and are harmonized within rather than across countries for long time spans. For the shorter time span, the OECD offers a specific time series of housing expenditure. Several individual country studies show, for the post-1970 period, that the increases are (entirely) due to increasing tenant expenditures (Albouy et al., 2014; Dustmann et al., 2022) and that tenants have higher expenditure shares. With these given caveats, housing expenditure follows a common trend in most countries: it starts falling around 1900, reaches a minimum in the post-First World War era, with rent controls only slowly fading out, and then recovers only to fall again below mostly 15% budget share until the 1960s. Ever since, with rent controls either removed completely (Anglophone countries) or softened into a second generation (Europe), housing costs have risen persistently. Thus, on a bivariate level, the rental-expenditure hypothesis also has certain prima facie evidence.

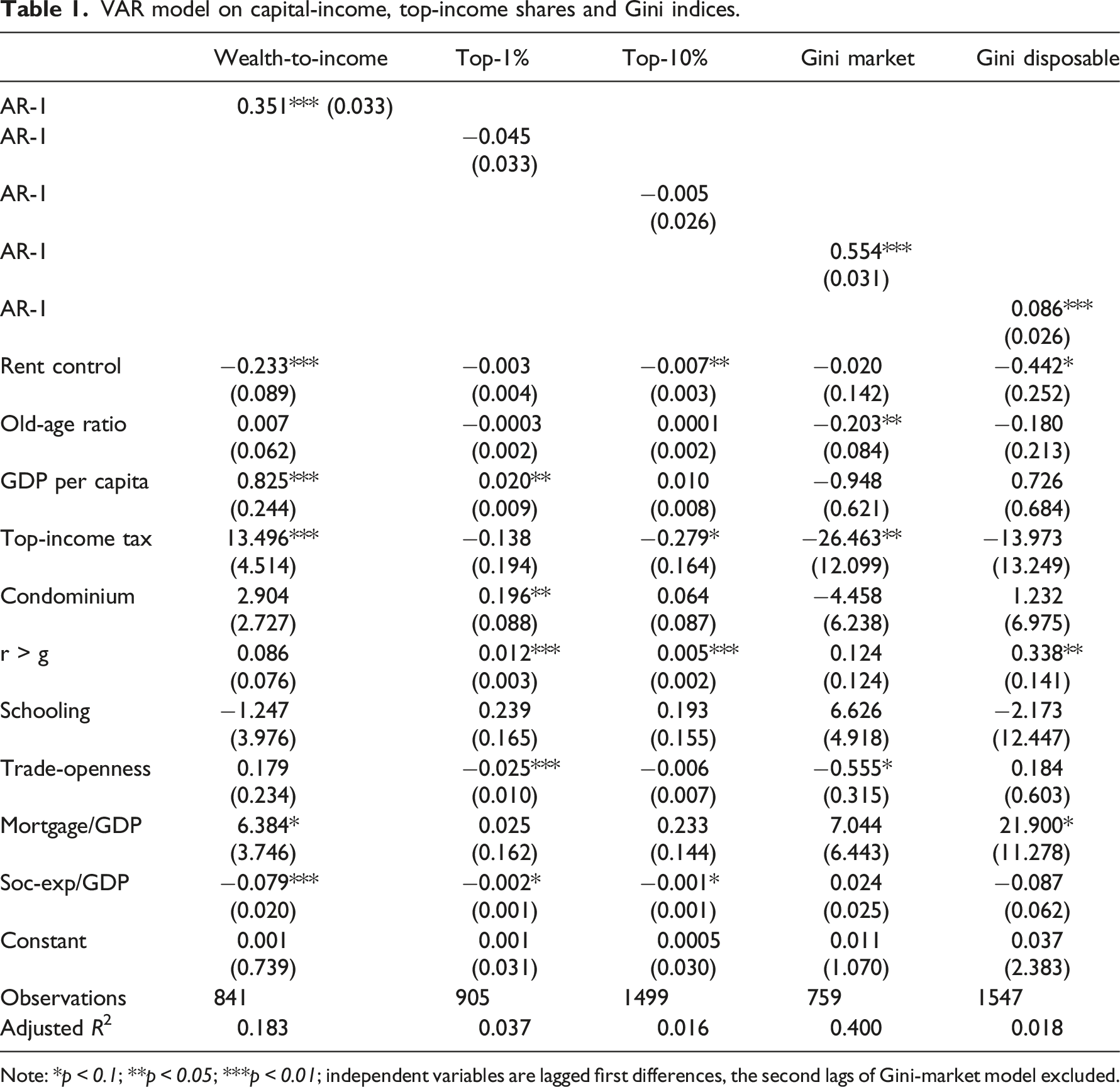

VAR model on capital-income, top-income shares and Gini indices.

Note: *p < 0.1; **p < 0.05; ***p < 0.01; independent variables are lagged first differences, the second lags of Gini-market model excluded.

The estimates show a significant negative average effect of rent price controls on subsequent wealth-to-income ratios, top 10% income shares, and the Gini coefficient of disposable incomes. It is negative also for the top 1% incomes and the Gini of market incomes, but not significant, which could point to rental incomes not being important at the very top. There are also the two shorter series, often excluding the pre-1950 years, which could point to historical effects being more important. A one-point increase in the rent control index is followed by a 0.226 decrease in the wealth-to-income ratio. The effect is stable when including typical control variables: the top income tax rates have the most persistent expected negative effect, while the old-age ratio and spread of condo-ownership institutions rather increase inequality. Disconfirming previous shorter-term analyses, our long-run analysis proves Piketty econometrically right: economic times when r > g have a statistically significant positive effect on inequality. Mortgage debt relative to GDP (or housing financialization) is positively associated with inequality, whereas social expenditure per GDP (which includes housing allowances) and trade-openness are associated negatively.

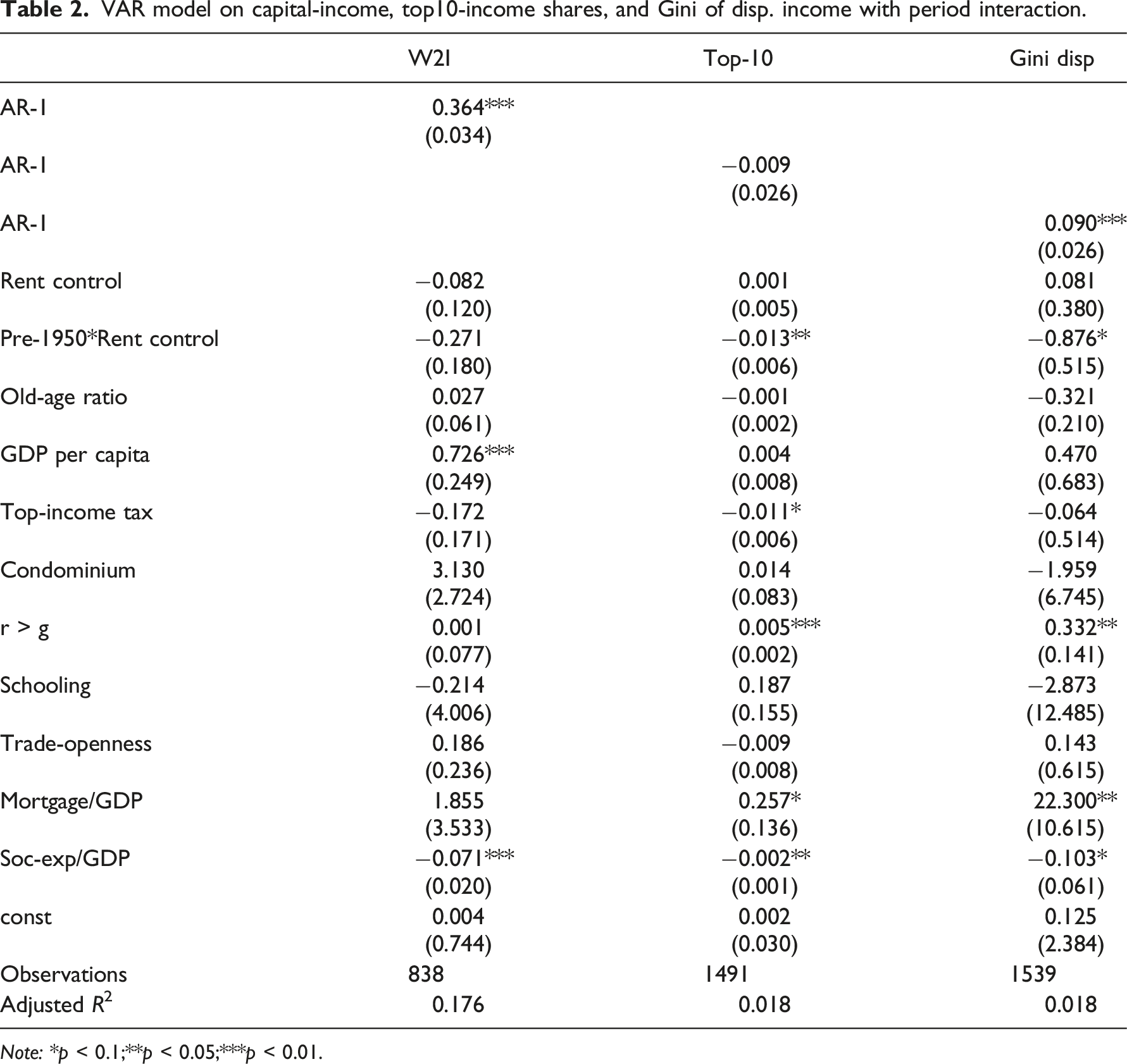

VAR model on capital-income, top10-income shares, and Gini of disp. income with period interaction.

Note: *p < 0.1;**p < 0.05;***p < 0.01.

Rent controls were not independent of three important changes in countries’ housing stock: housing shortages and trends of the competing tenures, homeownership and social housing. Rent controls may have just been a function of war-related shortages and may have become less important as homeownership and social housing became serious alternatives over time. These variables are sometimes only available for shorter time periods, such that we estimated the main model including these additional independent variables separately (see Appendix A3). The results suggest that all three housing stock trends eat into the influence of rent controls without making their significance and magnitude completely obsolete.

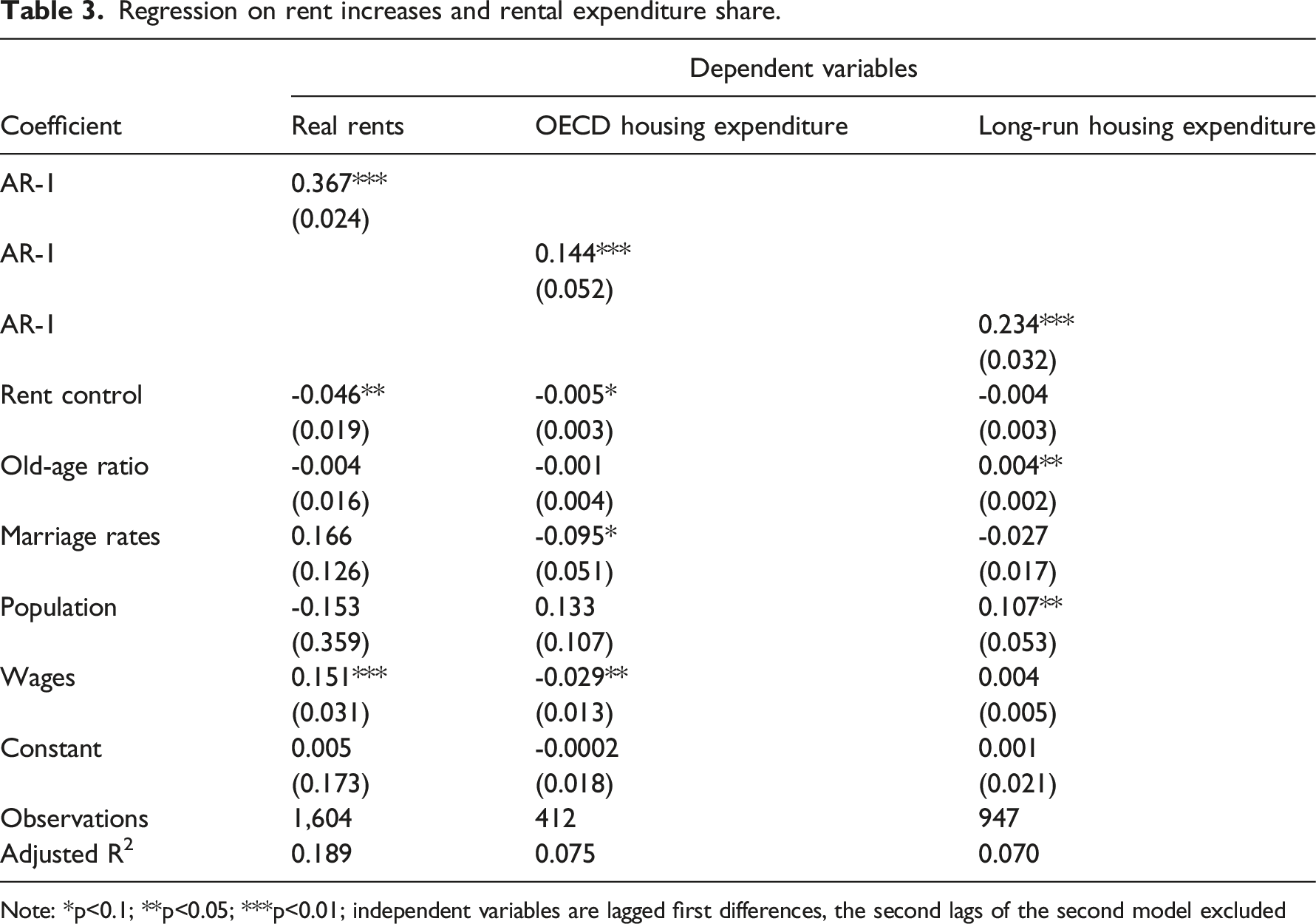

Regression on rent increases and rental expenditure share.

Note: *p<0.1; **p<0.05; ***p<0.01; independent variables are lagged first differences, the second lags of the second model excluded

The above analysis already uses a number of different measures and finds mostly significantly negative effects of rent control on inequality through the three hypothesized channels. We conducted a number of robustness checks to further verify the results (see Appendix). We split our sample in two: first, 1949 or earlier (‘historical’) and, second, 1950 or later (‘more recent’). While the overall rent control effects remain negative throughout, the more recent the period (and hence also number of observations), the less significance we have. This suggests that the rent control effect is more pronounced in the historical periods which also include the stricter controls and (post)war periods. In the earlier period, housing wealth and rental income were also likely to be much more important than financial wealth or income from it. Before the post-Second World War introduction of flat ownership, landlords were more likely to own entire apartment buildings with even more concentrated rental incomes. Therefore, we conduct another robustness check differentiating first-generation rent controls (rent freezes) from second-generation rent controls (rent stabilizations). Here, the significant negative effect is mostly attributable to the former controls, which coincide with the earlier periods. This is also confirmed by the five alternative panel model estimates with fixed effects. In addition, they show that there are no significant quadratic effects of rent control. To explore whether rent control is reducible to the wars and their effects, we included war casualties as a wartime proxy in another robustness check. The model still shows a significantly negative effect of rent control, distinct from wars.

Overall, we believe that this analysis shows that rent controls, mostly of the stricter kind as applied in the more historical period, have had a significantly negative effect on inequality, in both the capital and income dimension. The results also hold when using 5 year average instead of annual values or when moving from VAR to panel models (see Appendix Tables A7–11). Finally, the VAR model also permits the assessment of short- and long-term effects through impulse–response functions which Appendix Figure A2 displays: a one-time 1-year rent control shock reduces inequality in the first 3 to 5 years following the shock. These effects are especially long-lived for the top 10% and Gini index. The impact is especially strong in the second year after the shock.

Discussion and conclusion

Although ignored by much inequality research, housing clearly is a crucial vector of economic inequalities whose divides might even supplant the classic labour–capital divide (Adkins et al., 2019), re-structuring electoral politics as already witnessed in the surge of populism (Adler and Ansell, 2019). The increasing unaffordability problems in superstar cities are reanimating a policy idea that some consider to be just an exceptional wartime measure of days gone by: rent controls. Rather than seeing them as a relic of the past, most European countries are actively using deregulated, softer, versions of the exceptional wartime measures which produced tenancy regulation. Stricter rent controls have recently and controversially been introduced at the regional level in Berlin and Catalonia. The outbreak of the global COVID-19 pandemic is also leading to the re-introduction of strict rent controls. In many countries, rents were frozen for the duration of the health emergency. In some countries, rent controls are likely to remain even after the crisis. Much criticized by economists for their supply-distorting effects, rent controls are primarily intended to protect tenants from price increases deemed too excessive compared with income levels.

This study investigates the potential secondary effect this may have on overall inequality levels: the main takeaway from the historical long-run perspective, which follows a century of national rent controls from their inception to the present day, is that, in particular, the hard rent controls during and following the world wars, part of the historical period, had inequality-decreasing effects much like progressive income taxation or Piketty’s r > g. The inequality decline runs through three mechanisms: rent controls keep capital–wealth ratios lower, reduce landlords’ incomes, and increase tenants’ post-housing disposable income. This is mainly because landlords are rich and tenants are poor, such that rent control acts as a channel for redistribution. This effect also holds despite private tenancy becoming less important over the historic long run. Very soft rent control effects on inequality are of rather low magnitude, and the macro effects of softer rent regulation and those outside of war contexts are mostly not significant.

One layer of complexity the article does not touch upon is the various institutional forms of real estate ownership, that is, rich individuals holding residential real estate not only directly but also indirectly through a variety of institutional ownership forms, shares in traded real estate companies, REITs (Real Estate Investment Trusts), etc. Funded privatized pensions have increasingly found residential real estate a promising investment in times of decreasing yields on government bonds and other safe assets (Gabor and Kohl, 2022). In extreme cases, such as Switzerland with its more than 60% tenancy rate in the population and one of the most privatized pension systems, tenants essentially provide a private pension to the nation’s retirees by paying large shares of their income in rent. Both private pensions and financial shares in real estate are obviously skewed towards the upper-income parts of the population. To the extent that rent controls also affect the profitability of real estate holdings beyond individual households, our results rather underestimate the total effect rent controls can have on economic inequality.

Housing can affect inequalities in a multitude of ways, and rent controls could have more longer-term effects than those investigated here (Turner and Malpezzi, 2003). Rent controls are often associated with reduced residential mobility (Diamond et al., 2019), which could create inequalities between existing tenants and more mobile parts of the population. This could not only freeze existing segregation but also prevent gentrification (Sims, 2011). Reduced mobility could create mismatches in the labour market. Rent controls are also associated with underinvestment in both the housing stock and new supply, as well as with a flight into homeownership (Downs, 1988). To the extent that upper-income households are more likely to buy themselves out, rent controls could increase the quality divide between rental and owner-occupied units in the housing stock while also limiting the supply for new families and other mobile households, thus affecting intergenerational inequalities. Finally, rent regulation could be implemented in different ways, with richer households being better able to evade it.

Our analysis could imply that politicians interested in decreasing inequality through a cap on ‘rental capitalism’ would have to use a ‘rent-freeze bazooka’ rather than the fine-grained comparative rent measures of soft control. While rent controls may then have sizeable effects and target specific housing inequalities at the consumer end, our analysis also shows that the classical income tax or welfare measures have a strong inequality-decreasing effect. While income taxes may target income inequality directly at its source, housing allowances and other housing transfers may target housing inequalities more directly, as they focus on households and not broadly on housing units as rent controls do. In the short term, however, rent controls may be an effective tool to counter rent price frenzies in speculative moments on the housing market.

Supplemental Material

Supplemental Material - Rent price control – yet another great equalizer of economic inequalities? Evidence from a century of historical data

Supplemental Material for Rent price control – yet another great equalizer of economic inequalities? Evidence from a century of historical data by Konstantin A Kholodilin and Sebastian Kohl in Journal of European Social Policy

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental Material for this article is available online

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.